Strength of Minibatch Noise in SGD

Abstract

The noise in stochastic gradient descent (SGD), caused by minibatch sampling, is poorly understood despite its practical importance in deep learning. This work presents the first systematic study of the SGD noise and fluctuations close to a local minimum. We first analyze the SGD noise in linear regression in detail and then derive a general formula for approximating SGD noise in different types of minima. For application, our results (1) provide insight into the stability of training a neural network, (2) suggest that a large learning rate can help generalization by introducing an implicit regularization, (3) explain why the linear learning rate-batchsize scaling law fails at a large learning rate or at a small batchsize and (4) can provide an understanding of how discrete-time nature of SGD affects the recently discovered power-law phenomenon of SGD.

1 Introduction

Stochastic gradient descent (SGD) is the simple and efficient optimization algorithm behind the success of deep learning (Allen-Zhu et al.,, 2019; Xing et al.,, 2018; Zhang et al.,, 2018; Wang et al.,, 2020; He and Tao,, 2020; Liu et al.,, 2021; Simsekli et al.,, 2019; Wu et al.,, 2020). Minibatch noise, also known as the SGD noise, is the primary type of noise in the learning dynamics of neural networks. Practically, minibatch noise is unavoidable because a modern computer’s memory is limited while the size of the datasets we use is large; this demands the dataset to be split into “minibatches" for training. At the same time, using minibatch is also a recommended practice because using a smaller batch size often leads to better generalization performance (Hoffer et al.,, 2017). Therefore, understanding minibatch noise in SGD has been one of the primary topics in deep learning theory. Dominantly many theoretical studies take two approximations: (1) the continuous-time approximation, which takes the infinitesimal step-size limit; (2) the Hessian approximation, which assumes that the covariance matrix of the SGD noise is equal to the Hessian . While these approximations have been shown to provide some qualitative understanding, the limitation of these approximations is not well understood. For example, it is still unsure when such approximations are valid, which hinders our capability to assess the correctness of the results obtained by approximations.

In this work, we fill this gap by deriving analytical formulae for discrete-time SGD with arbitrary learning rates and exact minibatch noise covariance. In summary, the main contributions are: (1) we derive the strength and the shape of the minibatch SGD noise in the cases where the noise for discrete-time SGD is analytically solvable; (2) we show that the SGD noise takes a different form in different kinds of minima and propose general and more accurate approximations. This work is organized as follows: Sec. 2 introduces the background. Sec. 3 discusses the related works. Sec. 4 outlines our theoretical results. Sec. 5 derives new approximation formulae for SGD noises. In Sec. 6, we show how our results can provide practical and theoretical insights to problems relevant to contemporary machine learning research. For reference, the relationship of this work to the previous works is shown in Table 1.

2 Background

In this section, we introduce the minibatch SGD algorithm. Let be a training set. We can define the gradient descent (GD) algorithm for a differentiable loss function as , where is the learning rate and is the weights of the model. We consider an additive loss function for applying the minibatch SGD.

Definition 1.

A loss function is additive if for some differentiable, non-negative function .

This definition is quite general. Most commonly studied and used loss functions are additive, e.g., the mean-square error (MSE) and cross-entropy loss. For an additive loss, the minibatch SGD with momentum algorithm can be defined.

Definition 2.

The minibatch SGD with momentum algorithm by sampling with replacement computes the update to the parameter with the following set of equations:

| (1) |

where is the momentum hyperparameter, is the minibatch size, and the set are i.i.d. random integers sampled uniformly from .

| Setting | Artificial Noise | Hessian Approximation Noise | Minibatch Noise |

| Continuous-time | Sato and Nakagawa, (2014); Welling and Teh, (2011) | Jastrzebski et al., (2018); Zhu et al., (2019) | Blanc et al., (2020); Mori et al., (2021) |

| Mandt et al., (2017); Meng et al., (2020) | Wu et al., (2020); Xie et al., (2021) | ||

| Discrete-time | Yaida, (2019); Gitman et al., (2019) | Liu et al., (2021) | This Work |

| Liu et al., (2021) |

One can decompose the gradient into a deterministic plus a stochastic term. Note that is equal to the gradient for the GD algorithm. We use to denote the expectation over batches, and use to denote the expectation over the stationary distribution of the model parameters. Therefore, we can write where is the noise term; the noise covariance is . Of central importance to us is the averaged asymptotic noise covariance . Also, we consider the asymptotic model fluctuation . gives the strength and shape of the fluctuation of around a local minimum and is another quantity of central importance to this work. Throughout this work, is called the “noise" and the “fluctuation".

3 Related Works

Noise and Fluctuation in SGD. Deep learning models are trained with SGD and its variants. To understand the parameter distribution in deep learning, one needs to understand the stationary distribution of SGD (Mandt et al.,, 2017). Sato and Nakagawa, (2014) describes the stationary distribution of stochastic gradient Langevin dynamics using discrete-time Fokker-Planck equation. Yaida, (2019) connects the covariance of parameter to that of the noise through the fluctuation-dissipation theorem. When is known, one may obtain by Laplace approximation the stationary distribution of the model parameter around a local minimum as . Therefore, knowing can be of great practical use. For example, it has been used to estimate the local minimum escape efficiency (Zhu et al.,, 2019; Liu et al.,, 2021) and argue that SGD prefers a flatter minimum; it can also be used to assess parameter uncertainty and prediction uncertainty when a Bayesian prior is specified (Mandt et al.,, 2017; Gal and Ghahramani,, 2016; Pearce et al.,, 2020). Empirically, both the fluctuation and the noise are known to crucially affect the generalization of a deep neural network. Wu et al., (2020) shows that the strength and shape of the due to the minibatch noise lead to better generalization of neural networks in comparison to an artificially constructed noise.

Hessian Approximation of the Minibatch Noise. However, it is not yet known what form and actually take for SGD in a realistic learning setting. Early attempts assume isotropic noise in the continuous-time limit (Sato and Nakagawa,, 2014; Mandt et al.,, 2017). In this setting, the noise is an isotropic Gaussian with , and is known to be proportional to the inverse Hessian . More recently, the importance of noise structure was realized (Hoffer et al.,, 2017; Jastrzebski et al.,, 2018; Zhu et al.,, 2019; HaoChen et al.,, 2020). “Hessian approximation", which assumes for some unknown constant , has often been adopted for understanding SGD (see Table 1); this assumption is often motivated by the fact that , where is the Fisher information matrix (FIM) (Zhu et al.,, 2019); the fluctuation can be solved to be isotropic: . However, it is not known under what conditions the Hessian approximation is valid, while previous works have argued that it can be very inaccurate (Martens,, 2014; Liu et al.,, 2021; Thomas et al.,, 2020; Kunstner et al.,, 2019). However, Martens, (2014) and Kunstner et al., (2019) only focuses on the natural gradient descent (NGD) setting; Thomas et al., (2020) is closest to ours, but it does not apply to the case with momentum, a matrix learning rate, or regularization.

Discrete-time SGD with a Large Learning Rate. Recently, it has been realized that networks trained at a large learning rate have a dramatically better performance than networks trained with a vanishing learning rate (lazy training) (Chizat and Bach,, 2018). Lewkowycz et al., (2020) shows that there is a qualitative difference between the lazy training regime and the large learning rate regime; the performance features two plateaus in testing accuracy in the two regimes, with the large learning rate regime performing much better. However, the theory regarding discrete-time SGD at a large learning rate is almost non-existent, and it is also not known what may be when the learning rate is non-vanishing. Our work also sheds light on the behavior of SGD at a large learning rate. Some other works also consider discrete-time SGD in a similar setting (Fontaine et al.,, 2021; Dieuleveut et al.,, 2020; Toulis et al.,, 2017), but the focus is not on deriving analytical formulae or does not deal with the stationary distribution.

4 SGD Noise and Fluctuation in Linear Regression

This section derives the shape and strength of SGD noise and fluctuation for linear regression; concurrent to our work, Kunin et al., (2021) also studies the same problem but with continuous-time approximation; our result is thus more general. To emphasize the message, we discuss the label noise case in more detail. The other situations also deserve detailed analysis; we delay such discussion to the appendix due to space constraints. Notation: denotes the minibatch size. is the model parameter viewed in a vectorized form; denotes a scalar learning rate; when the learning rate takes the form of a preconditioning matrix, we use . denotes the covariance matrix of the input data. When a matrix is positive semi-definite, we write ; throughout, we require . denotes the weight decay hyperparameter; when the weight decay hyperparameter is a matrix, we write . is the momentum hyperparameter in SGD. For two matrices , the commutator is defined as . Other notations are introduced in the context.111We use the word global minimum to refer to the global minimum of the loss function, i.e., where and a local minimum refers to a minimum that has a non-negative loss, i.e., . The results of this section are numerically verified in Appendix A.

4.1 Key Previous Results

When , the following proposition is well-known and gives the exact noise due to minibatch sampling. See Appendix E.1 for a derivation.

Proposition 1.

This gradient covariance matrix is crucial to understand the minibatch noise. The standard literature often assumes ; however, the following well-known proposition shows that this approximation can easily break down.

Proposition 2.

Let be the solution such that , then .

Proof. Because is non-negative for all , implies that . The differentiability in turn implies that each ; therefore, .

This proposition implies that there is no noise if our model can achieve zero training loss (which is achievable for an overparametrized model). This already suggests that the Hessian approximation is wrong since the Hessian is unlikely to vanish in any minimum. The fact that the noise strength vanishes at suggests that the SGD noise might at least be proportional to , which we will show to be true for many cases. The following theorem relates and of the discrete-time SGD algorithm with momentum for a matrix learning rate.

Theorem 1.

(Liu et al.,, 2021) Consider running SGD on a quadratic loss function with Hessian , learning rate matrix , momentum . Assuming ergodicity, then

| (3) |

Propostion 1 and Theorem 1 allow one to solve and . Equation (3) can be seen as a general form of the Lyapunov equation (Lyapunov,, 1992) and is hard to solve in general (Hammarling,, 1982; Ye et al.,, 1998; Simoncini,, 2016). Solving this analytical equation in settings of machine learning relevance is one of the main technical contributions of this work.

4.2 Random Noise in the Label

We first consider the case when the labels contain noise. The loss function takes the form

| (4) |

where are drawn from a zero-mean Gaussian distribution with feature covariance , and , for some fixed and is drawn from a distribution with zero mean and finite second momentum . We redefine and let with held fixed. The following lemma finds as a function of .

Lemma 1.

The model fluctuation can be obtained using this lemma.

Theorem 2.

Fluctuation of model parameters with random noise in the label Let the assumptions be the same as in Lemma 1 and . Then,

| (6) |

where with .

Remark.

This result is numerically validated in Appendix A. The subscript refers to momentum. To obtain results for vanilla SGD, one can set , which has the effect of reducing . From now on, we focus on the case when for notational simplicity, but we note that the results for momentum can be likewise studied. The assumption is not too strong because this condition holds for a scalar learning rate and common second-order methods such as Newton’s method.

If , then . This means that when there is no label noise, the model parameter has a vanishing stationary fluctuation, which corroborates Proposition 2. When a scalar learning rate and , we have

| (7) |

which is the result one would expect from the continuous-time theory with the Hessian approximation (Liu et al.,, 2021; Xie et al.,, 2021; Zhu et al.,, 2019), except for a correction factor of . Therefore, a Hessian approximation fails to account for the randomness in the data of strength . We provide a systematic and detailed comparison with the Hessian approximation in Table 2 of Appendix B.

Moreover, it is worth comparing the exact result in Theorem 2 with Eq. (7) in the regime of non-vanishing learning rate and small batch size. One notices two differences: (1) an anisotropic enhancement, appearing in the matrix and taking the form ; compared with the result in Liu et al., (2021), this term is due to the compound effect of using a large learning rate and a small batchsize; (2) an isotropic enhancement term , which causes the overall magnitude of fluctuations to increase; this term does not appear in the previous works that are based on the Hessian approximation and is due to the minibatch sampling process alone. As the numerical example in Appendix A shows, at large batch size, the discrete-time nature of SGD is the leading source of fluctuation; at small batch size, the isotropic enhancement becomes the dominant source of fluctuation. Therefore, the minibatch sampling process causes two different kinds of enhancement to the fluctuation, potentially increasing the exploration power of SGD at initialization but reducing the convergence speed.

Theorem 3.

The noise covariance matrix of minibatch SGD with random noise in the label is

| (8) |

By definition, is the FIM. The Hessian approximation, in sharp contrast, can only account for the term in orange. A significant modification containing both anisotropic and isotropic (up to Hessian) is required to fully understand SGD noise, even in this simple example. Additionally, comparing this result with the training loss (127), one can find that the noise covariance contains one term that is proportional to the training loss. In fact, we will derive in Sec. 5 that containing a term proportional to training loss is a general feature of the SGD noise. We also study the case when the input is contaminated with noise. Interestingly, the result is the same with the label noise case with replaced by a more complicated term of the form . We thus omit this part from the main text. A detailed discussion can be found in Appendix E.3.1. In the next section, we study the effect of regularization on SGD noise and fluctuation.

4.3 Learning with Regularization

Now, we show that regularization also causes a unique SGD noise. The loss function for regularized linear regression is

| (9) |

where is a symmetric matrix; conventionally, one set with a scalar . For conciseness, we assume that there is no noise in the label, namely with a constant vector . One important quantity in this case will be . The noise for this form of regularization can be calculated but takes a complicated form.

Proposition 3.

Notice that the last term in is unique to the regularization-based noise: it is rank-1 because is rank-1. This term is due to the mismatch between the regularization and the minimum of the original loss. Also, note that the term is proportional to the training loss. Define the test loss to be , we can prove the following theorem. We will show that one intriguing feature of discrete-time SGD is that the weight decay can be negative.

Theorem 4.

Test loss and model fluctuation for L2 regularization Let the assumptions be the same as in Proposition 3. Then

| (11) |

where , , with . Moreover, let , then

| (12) |

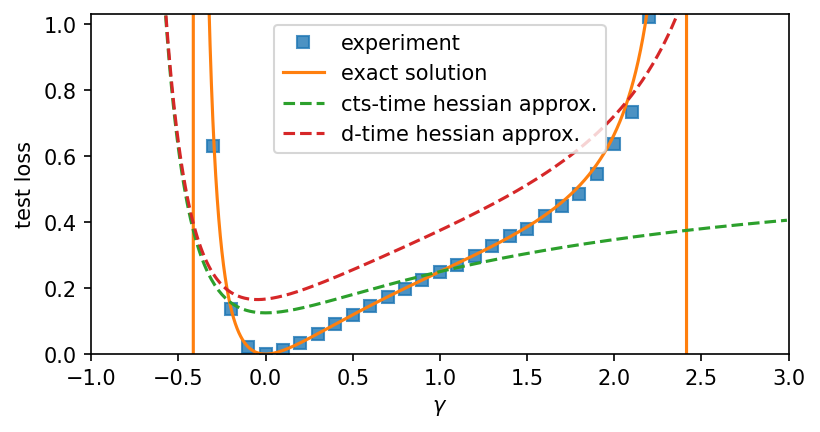

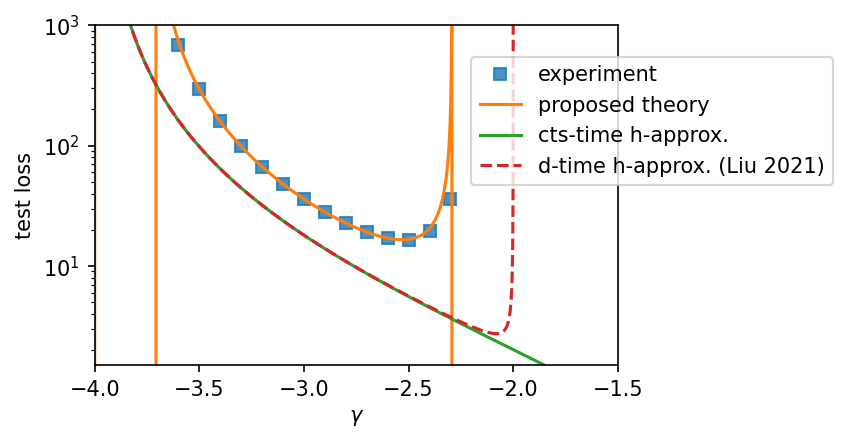

This result is numerically validated in Appendix A. The test loss (11) has an interesting consequence. One can show that there exist situations where the optimal is negative.222Some readers might argue that discussing test loss is meaningless when ; however, this criticism does not apply because the size of the training set is not the only factor that affects generalization. In fact, this section’s crucial message is that using a large learning rate affects the generalization by implicitly regularizing the model and, if one over-regularizes, one needs to offset this effect. When discussing the test loss, we make the convention that if diverges, then .

Corollary 1.

Let . There exist , and such that .

The proof shows that when the learning rate is sufficiently large, only negative weight decay is allowed. This agrees with the argument in Liu et al., (2021) that discrete-time SGD introduces an implicit regularization that favors small norm solutions. A too-large learning rate requires a negative weight decay because a large learning rate already over-regularizes the model and one needs to introduce an explicit negative weight decay to offset this over-regularization effect of SGD. This is a piece of direct evidence that using a large learning rate can help regularize the models. It has been hypothesized that the dynamics of SGD implicitly regularizes neural networks such that the training favors simpler solutions (Kalimeris et al.,, 2019). Our result suggests one new mechanism for such a regularization.

5 Noise Structure for Generic Settings

The results in the previous sections suggest that (1) the SGD noises differ for different kinds of situations, and (2) SGD noise contains a term proportional to the training loss in general. These two facts motivate us to derive the noise covariance differently for different kinds of minima. Let denote the output of the model for a given input . Here, we consider a more general case; may be any differentiable function, e.g., a non-linear deep neural network. The number of parameters in the model is denoted by , and hence . For a training dataset , the loss function with a regularization is given by

| (13) |

where is the loss function without regularization, and is the Hessian of . We focus on the MSE loss . Our result crucially relies on the following two assumptions, which relate to the conditions of different kinds of local minima.

Assumption 1.

(Fluctuation decays with batch size) is proportional to , i.e. .

This is justified by the results in all the related works (Liu et al.,, 2021; Xie et al.,, 2021; Meng et al.,, 2020; Mori et al.,, 2021), where is found to be .

Assumption 2.

(Weak homogeneity) is small; in particular, it is of order .

This assumption amounts to assuming that the current training loss reflects the actual level of approximation for each data point well. In fact, since , one can easily show that . Here, we require a slightly stronger condition for a more clean expression, when we can still get a similar expression but with some constant that hinders the clarity. Relaxing this condition can be an important and interesting future work. The above two conditions allow us to state our general theorem formally.

Theorem 5.

Let the training loss be and the models be optimized with SGD in the neighborhood of a local minimum . Then,

| (14) |

The noise takes different forms for different kinds of local minima.

Corollary 2.

Omitting the terms of order , when ,

| (15) |

When and ,

| (16) |

When and ,

| (17) |

Remark.

Assumption 2 can be replaced by a weaker but more technical assumption called the “decoupling assumption", which has been used in recent works to derive the continuous-time distribution of SGD (Mori et al.,, 2021; Wojtowytsch,, 2021). The Hessian approximation was invoked in most of the literature without considering the conditions of its applicability (Jastrzebski et al.,, 2018; Zhu et al.,, 2019; Liu et al.,, 2021; Wu et al.,, 2020; Xie et al.,, 2021). Our result does provide such conditions for applicability. As indicated by the two assumptions, this theorem is applicable when the batch size is not too small and when the local minimum has a loss close to . The reason for the failure of the Hessian approximation is that, while the FIM is equal to the expected Hessian , there is no reason to expect the expected Hessian to be close to the actual Hessian of the minimum.

The proof is given in Appendix C. Two crucial messages this corollary delivers are (1) the SGD noise is different in strength and shape in different kinds of local minima and that they need to be analyzed differently; (2) the SGD noise contains a term that is proportional to the training loss in general. Recently, it has been experimentally demonstrated that the SGD noise is indeed proportional to the training loss in realistic deep neural network settings, both when the loss function is MSE and cross-entropy (Mori et al.,, 2021); our result offers a theoretical justification. The previous works all treat all the minima as if the noise is similar (Jastrzebski et al.,, 2018; Zhu et al.,, 2019; Liu et al.,, 2021; Wu et al.,, 2020; Xie et al.,, 2021), which can lead to inaccurate or even incorrect understanding. For example, Theorem 3.2 in Xie et al., (2021) predicts a high escape probability from a sharp local or global minimum. However, this is incorrect because a model at a global minimum has zero probability of escaping due to a vanishing gradient. In contrast, the escape rate results derived in Mori et al., (2021) correctly differentiate the local and global minima. We also note that these general formulae are consistent with the exact solutions we obtained in the previous section than the Hessian approximation. For example, the dependence of the noise strength on the training loss in Theorem 2, and the rank- noise of regularization are all reflected in these formulae. In contrast, the simple Hessian approximation misses these crucial distinctions. Lastly, combining Theorem 5 with Theorem 1, one can also find the fluctuation.

Corollary 3.

Let the noise be as in Theorem 5, and omit the terms of order and . Then, when and when , and commute with each other, . When and , . When and , . Here the superscript is the Moore-Penrose pseudo inverse, is the projection operator with non-zero entries, is the rank of the Hessian , and is the rank of . For the null space , can be arbitrary.

6 Applications

One major advantage of analytical solutions is that they can be applied in a simple “plug-in" manner by the practitioners or theorists to analyze new problems they encounter. In this section, we briefly outline a few examples where the proposed theories can be relevant.

6.1 High-Dimensional Regression

We first apply our result to the high-dimensional regression problem and show how over-and-underparametrization might play a role in determining the minibatch noise. Here, we take with the ratio held fixed. The loss function is . As in the standard literature (Hastie et al.,, 2019), we assume the existence of label noise: , with . A key difference between our setting and the standard high-dimensional setting is that, in the standard setting (Hastie et al.,, 2019), one uses the GD algorithm with vanishing learning rate instead of the minibatch SGD algorithm with a non-vanishing learning rate. Tackling the high-dimensional regression problem with non-vanishing and a minibatch noise is another main technical contribution of this work. In this setting, we can obtain the following result on the noise covariance matrix.

We note that this proposition follows from Theorem 5, showing an important theoretical application of our general theory. An interesting observation is that one -independent term proportional to emerges in the underparametrized regime (). However, for the overparametrized regime, the noise is completely dependent on , which is a sign that the stationary solution has no fluctuation. This shows that the degree of underparametrization also plays a distinctive role in the fluctuation. In fact, one can prove the following theorem, which is verified in Appendix A.2.

Theorem 6.

When a stationary solution exists for , we have , where with .

6.2 Implication for Neural Network Training

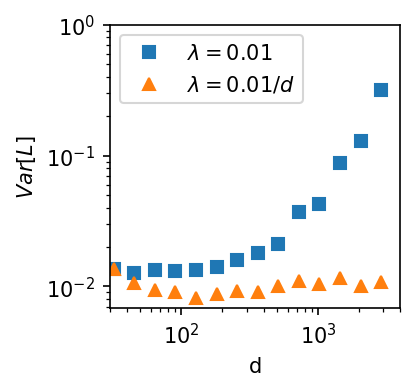

It is commonly believed that the high-dimensional linear regression problem can be a minimal model for deep learning. Taking this stance, Theorem 6 suggests a technique for training neural networks. For SGD to converge, a positive semi-definite must exist; however, if and only if . From , we have , where are the eigenvalues of . This means that each summand should have the order of . Thus the upper bound of should have the order of , where is the typical value of ’s. One implication of the dependence on the dimension is that the stability of a neural network trained with SGD may strongly depend on its width , and one may rescale the learning rate according to the width to stabilize neural network training. See Figure 1-Left and Middle. We train a two-layer tanh neural network on MNIST and plot the variance of its training loss in the first epoch with fixed . We see that, when , the training starts to destabilize, and the training loss begins to fluctuate dramatically. When rescaling the learning rate by , we see that the variance of the training loss is successfully kept roughly constant across all . This suggests a training technique worth being explored by practitioners in the field. In Figure 1-Middle, we also use Adam for training the same network and find a similar stabilizing trick to work for Adam.

6.3 A Natural Learning Example with Negative Weight Decay

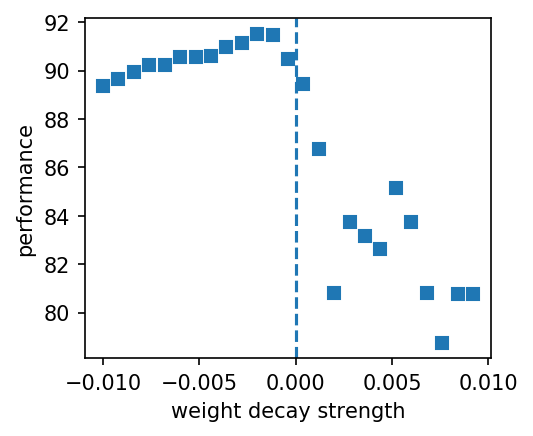

Sec. 4.3 shows that a too-large learning rate introduces an effective regularization that can be corrected by setting the weight decay to be negative. This effect can be observed in more realistic learning settings. We train a logistic regressor on the MNIST dataset with a large learning rate (of order ). Figure 1-Right confirms that, at a large learning rate, the optimal weight decay can indeed be negative. This agrees with our argument that using a large learning rate can effectively regularize the training.

6.4 Second-order Methods

Understanding stochastic second-order methods (including the adaptive gradient methods) is also important for deep learning (Agarwal et al.,, 2017; Zhang and Liu,, 2021; Martens,, 2014; Kunstner et al.,, 2019). In this section, we apply our theory to two standard second-order methods: damped Newton’s method (DNM) and natural gradient descent (NGD). We provide more accurate results than those derived in Liu et al., (2021). The derivations are given in Appendix D.2. For DNM, the preconditioning learning rate matrix is defined as . The model fluctuation is shown to be proportional to the inverse of the Hessian: , where . The main difference with the previous results is that the fluctuation now depends explicitly on the dimension , and implies a stability condition: , corroborating the stability condition we derived above. For NGD, the preconditioning matrix is defined by the inverse of the Fisher information that . We show that is one solution when , which also contains a correction related to compared to the result in Liu et al., (2021) which is . A consequence is that . The surprising fact is that the stability of both NGD and DNM now crucially depends on ; combining with the results in Sec. 6.1, this suggests that the dimension of the problem may crucially affect the stability and performance of the minibatch-based algorithms. This result also implies that some features we derived are shared across many algorithms that depend on minibatch noise and that our results may be relevant to a broad class of optimization algorithms other than SGD.

6.5 Failure of the scaling law

One well-known technique in deep learning training is that one can scale linearly as one increases the batch size to achieve high-efficiency training without hindering the generalization performance; however, it is known that this scaling law fails when the learning rate is too large, or the batch size is too small (Goyal et al.,, 2017). In Hoffer et al., (2017), this scaling law is established on the ground that . However, our result in Theorem 2 suggests the reason for the failure even for the simple setting of linear regression. Recall that the exact takes the form:

for a scalar . One notices that the leading term is indeed proportional to . However, the discrete-time SGD results in a second-order correction in , and the term proportional to does not contain a corresponding ; this explains the failure of the scaling law in small , where the second-order contribution of becomes significant. To understand the failure at large , we need to look at the term :

One notices that the second term contains a part that only depends on but not on . This part is negligible compared to the first term when is small; however, it becomes significant as the second term approaches the first term. Therefore, increasing changes this part of the fluctuation, and the scaling law no more holds if is large.

6.6 Power Law Tail in Discrete-time SGD

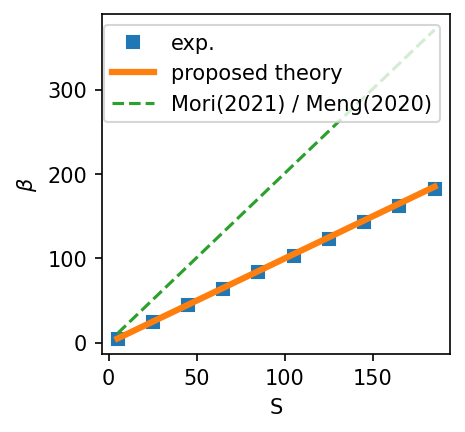

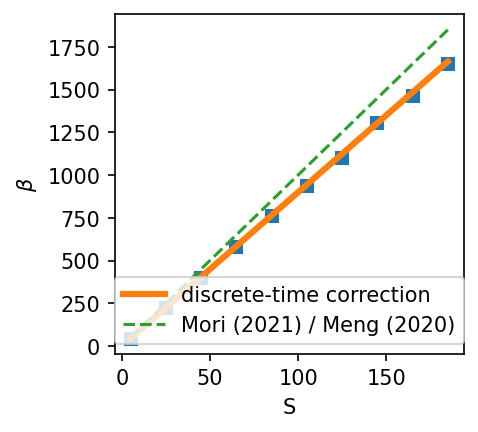

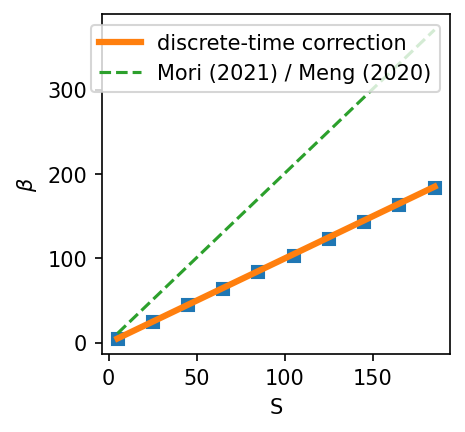

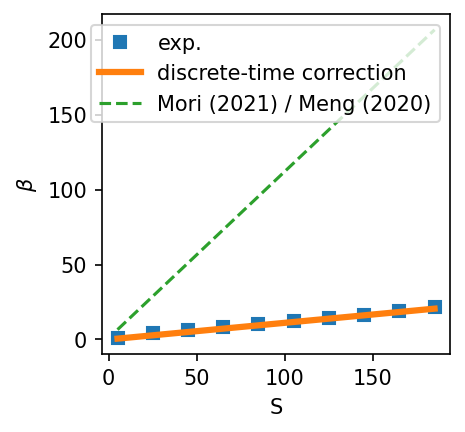

It has recently been discovered that the SGD noise causes a heavy-tail distribution (Simsekli et al.,, 2019; 2020), with a tail decaying like a power law with tail index (Hodgkinson and Mahoney,, 2020). In continuous-time, the stationary distribution has been found to obey a Student’s t-like distribution, (Meng et al.,, 2020; Mori et al.,, 2021; Wojtowytsch,, 2021). However, this result is only established for continuous-time approximations to SGD and one does not know what affects the exponent for discrete-time SGD. Our result in Theorem 2 can serve as a tool to find the discrete-time correction to the tail index of the stationary distribution. In Appendix D.3, we show that the tail index of discrete-time SGD in 1d can be estimated as . A clear discrete-time contribution is which depends only on the batch size, while is the tail index in the continuous-time limit (Mori et al.,, 2021). See Figure 2; the proposed formula agrees with the experiment. Knowing the tail index is important for understanding the SGD dynamics because is equal to the smallest moment of that diverges. For example, when , then the kurtosis of diverges, and one expects to see outliers of very often during training; when , then the second moment of diverges, and one does not expect to converge in the minimum under consideration. Our result suggests that the discrete-time dynamics always leads to a heavier tail than the continuous-time theory expects, and therefore is more unstable.

7 Outlook

In this work, we have presented a systematic analysis with a focus on exactly solvable results to promote our fundamental understanding of SGD. One major limitation is that we have only focused on studying the asymptotic behavior of SGD in local minimum. For example, Ziyin et al., (2022) showed that SGD can converge to a local maximum when the learning rate is large. One important future step is thus to understand the SGD noise beyond a strongly convex landscape.

Acknowledgement

Liu Ziyin thanks Jie Zhang, Junxia Wang, and Shoki Sugimoto. Ziyin is supported by the GSS Scholarship of The University of Tokyo. Kangqiao Liu was supported by the GSGC program of the University of Tokyo. This work was supported by KAKENHI Grant Numbers JP18H01145 and JP21H05185 from the Japan Society for the Promotion of Science.

References

- Agarwal et al., (2017) Agarwal, N., Bullins, B., and Hazan, E. (2017). Second-order stochastic optimization for machine learning in linear time. The Journal of Machine Learning Research, 18(1):4148–4187.

- Allen-Zhu et al., (2019) Allen-Zhu, Z., Li, Y., and Song, Z. (2019). A convergence theory for deep learning via over-parameterization. In International Conference on Machine Learning, pages 242–252. PMLR.

- Amari, (1998) Amari, S.-I. (1998). Natural gradient works efficiently in learning. Neural Comput., 10(2):251–276.

- Blanc et al., (2020) Blanc, G., Gupta, N., Valiant, G., and Valiant, P. (2020). Implicit regularization for deep neural networks driven by an ornstein-uhlenbeck like process. In Conference on learning theory, pages 483–513. PMLR.

- Chizat and Bach, (2018) Chizat, L. and Bach, F. (2018). A note on lazy training in supervised differentiable programming. arXiv preprint arXiv:1812.07956, 8.

- Clauset et al., (2009) Clauset, A., Shalizi, C. R., and Newman, M. E. (2009). Power-law distributions in empirical data. SIAM review, 51(4):661–703.

- Dieuleveut et al., (2020) Dieuleveut, A., Durmus, A., Bach, F., et al. (2020). Bridging the gap between constant step size stochastic gradient descent and markov chains. Annals of Statistics, 48(3):1348–1382.

- Fontaine et al., (2021) Fontaine, X., Bortoli, V. D., and Durmus, A. (2021). Convergence rates and approximation results for sgd and its continuous-time counterpart.

- Gal and Ghahramani, (2016) Gal, Y. and Ghahramani, Z. (2016). Dropout as a bayesian approximation: Representing model uncertainty in deep learning. In international conference on machine learning, pages 1050–1059. PMLR.

- Gitman et al., (2019) Gitman, I., Lang, H., Zhang, P., and Xiao, L. (2019). Understanding the role of momentum in stochastic gradient methods. In Advances in Neural Information Processing Systems, pages 9633–9643.

- Goyal et al., (2017) Goyal, P., Dollár, P., Girshick, R., Noordhuis, P., Wesolowski, L., Kyrola, A., Tulloch, A., Jia, Y., and He, K. (2017). Accurate, large minibatch sgd: Training imagenet in 1 hour. arXiv preprint arXiv:1706.02677.

- Hammarling, (1982) Hammarling, S. J. (1982). Numerical solution of the stable, non-negative definite lyapunov equation lyapunov equation. IMA Journal of Numerical Analysis, 2(3):303–323.

- HaoChen et al., (2020) HaoChen, J. Z., Wei, C., Lee, J. D., and Ma, T. (2020). Shape matters: Understanding the implicit bias of the noise covariance. arXiv preprint arXiv:2006.08680.

- Hastie et al., (2019) Hastie, T., Montanari, A., Rosset, S., and Tibshirani, R. J. (2019). Surprises in high-dimensional ridgeless least squares interpolation. arXiv preprint arXiv:1903.08560.

- He and Tao, (2020) He, F. and Tao, D. (2020). Recent advances in deep learning theory. arXiv preprint arXiv:2012.10931.

- Hodgkinson and Mahoney, (2020) Hodgkinson, L. and Mahoney, M. W. (2020). Multiplicative noise and heavy tails in stochastic optimization. arXiv preprint arXiv:2006.06293.

- Hoffer et al., (2017) Hoffer, E., Hubara, I., and Soudry, D. (2017). Train longer, generalize better: closing the generalization gap in large batch training of neural networks. In Advances in Neural Information Processing Systems, pages 1731–1741.

- Janssen and Stoica, (1988) Janssen, P. H. M. and Stoica, P. (1988). On the expectation of the product of four matrix-valued gaussian random variables. IEEE Transactions on Automatic Control, 33(9):867–870.

- Jastrzebski et al., (2018) Jastrzebski, S., Kenton, Z., Arpit, D., Ballas, N., Fischer, A., Storkey, A., and Bengio, Y. (2018). Three factors influencing minima in SGD.

- Kalimeris et al., (2019) Kalimeris, D., Kaplun, G., Nakkiran, P., Edelman, B., Yang, T., Barak, B., and Zhang, H. (2019). Sgd on neural networks learns functions of increasing complexity. Advances in Neural Information Processing Systems, 32:3496–3506.

- Kunin et al., (2021) Kunin, D., Sagastuy-Brena, J., Gillespie, L., Margalit, E., Tanaka, H., Ganguli, S., and Yamins, D. L. (2021). Rethinking the limiting dynamics of sgd: modified loss, phase space oscillations, and anomalous diffusion. arXiv preprint arXiv:2107.09133.

- Kunstner et al., (2019) Kunstner, F., Balles, L., and Hennig, P. (2019). Limitations of the empirical fisher approximation for natural gradient descent. arXiv preprint arXiv:1905.12558.

- Levy and Solomon, (1996) Levy, M. and Solomon, S. (1996). Power laws are logarithmic boltzmann laws. International Journal of Modern Physics C, 7(04):595–601.

- Lewkowycz et al., (2020) Lewkowycz, A., Bahri, Y., Dyer, E., Sohl-Dickstein, J., and Gur-Ari, G. (2020). The large learning rate phase of deep learning: the catapult mechanism. arXiv preprint arXiv:2003.02218.

- Liu et al., (2021) Liu, K., Ziyin, L., and Ueda, M. (2021). Noise and fluctuation of finite learning rate stochastic gradient descent. arXiv preprint arXiv:2012.03636.

- Lyapunov, (1992) Lyapunov, A. M. (1992). The general problem of the stability of motion. International journal of control, 55(3):531–534.

- Mandt et al., (2017) Mandt, S., Hoffman, M. D., and Blei, D. M. (2017). Stochastic gradient descent as approximate bayesian inference. J. Mach. Learn. Res., 18(1):4873–4907.

- Martens, (2014) Martens, J. (2014). New insights and perspectives on the natural gradient method. cite arxiv:1412.1193Comment: New title and abstract. Added multiple sections, including a proper introduction/outline and one on convergence speed. Many other revisions throughout.

- Meng et al., (2020) Meng, Q., Gong, S., Chen, W., Ma, Z.-M., and Liu, T.-Y. (2020). Dynamic of stochastic gradient descent with state-dependent noise. arXiv preprint arXiv:2006.13719.

- Mori et al., (2021) Mori, T., Ziyin, L., Liu, K., and Ueda, M. (2021). Logarithmic landscape and power-law escape rate of sgd. arXiv preprint arXiv:2105.09557.

- Pearce et al., (2020) Pearce, T., Leibfried, F., and Brintrup, A. (2020). Uncertainty in neural networks: Approximately bayesian ensembling. In International conference on artificial intelligence and statistics, pages 234–244. PMLR.

- Sato and Nakagawa, (2014) Sato, I. and Nakagawa, H. (2014). Approximation analysis of stochastic gradient langevin dynamics by using fokker-planck equation and ito process. In International Conference on Machine Learning, pages 982–990. PMLR.

- Simoncini, (2016) Simoncini, V. (2016). Computational methods for linear matrix equations. SIAM Review, 58(3):377–441.

- Simsekli et al., (2019) Simsekli, U., Sagun, L., and Gurbuzbalaban, M. (2019). A tail-index analysis of stochastic gradient noise in deep neural networks. In International Conference on Machine Learning, pages 5827–5837. PMLR.

- Simsekli et al., (2020) Simsekli, U., Sener, O., Deligiannidis, G., and Erdogdu, M. A. (2020). Hausdorff dimension, heavy tails, and generalization in neural networks. Advances in Neural Information Processing Systems, 33.

- Thomas et al., (2020) Thomas, V., Pedregosa, F., Merriënboer, B., Manzagol, P.-A., Bengio, Y., and Le Roux, N. (2020). On the interplay between noise and curvature and its effect on optimization and generalization. In International Conference on Artificial Intelligence and Statistics, pages 3503–3513. PMLR.

- Toulis et al., (2017) Toulis, P., Airoldi, E. M., et al. (2017). Asymptotic and finite-sample properties of estimators based on stochastic gradients. Annals of Statistics, 45(4):1694–1727.

- Wang et al., (2020) Wang, X., Zhao, Y., and Pourpanah, F. (2020). Recent advances in deep learning. International Journal of Machine Learning and Cybernetics, 11(4):747–750.

- Welling and Teh, (2011) Welling, M. and Teh, Y. W. (2011). Bayesian learning via stochastic gradient langevin dynamics. In Proceedings of the 28th international conference on machine learning (ICML-11), pages 681–688. Citeseer.

- Wojtowytsch, (2021) Wojtowytsch, S. (2021). Stochastic gradient descent with noise of machine learning type. part ii: Continuous time analysis. arXiv preprint arXiv:2106.02588.

- Wu et al., (2020) Wu, J., Hu, W., Xiong, H., Huan, J., Braverman, V., and Zhu, Z. (2020). On the noisy gradient descent that generalizes as sgd. In International Conference on Machine Learning, pages 10367–10376. PMLR.

- Xie et al., (2021) Xie, Z., Sato, I., and Sugiyama, M. (2021). A diffusion theory for deep learning dynamics: Stochastic gradient descent exponentially favors flat minima. In International Conference on Learning Representations.

- Xing et al., (2018) Xing, C., Arpit, D., Tsirigotis, C., and Bengio, Y. (2018). A walk with sgd. arXiv preprint arXiv:1802.08770.

- Yaida, (2019) Yaida, S. (2019). Fluctuation-dissipation relations for stochastic gradient descent. In International Conference on Learning Representations.

- Ye et al., (1998) Ye, H., Michel, A. N., and Hou, L. (1998). Stability theory for hybrid dynamical systems. IEEE transactions on automatic control, 43(4):461–474.

- Zhang et al., (2018) Zhang, C., Liao, Q., Rakhlin, A., Miranda, B., Golowich, N., and Poggio, T. (2018). Theory of deep learning iib: Optimization properties of sgd. arXiv preprint arXiv:1801.02254.

- Zhang and Liu, (2021) Zhang, Z. and Liu, Z. (2021). On the distributional properties of adaptive gradients. In Uncertainty in Artificial Intelligence, pages 419–429. PMLR.

- Zhu et al., (2019) Zhu, Z., Wu, J., Yu, B., Wu, L., and Ma, J. (2019). The anisotropic noise in stochastic gradient descent: Its behavior of escaping from sharp minima and regularization effects. In International Conference on Machine Learning, pages 7654–7663. PMLR.

- Ziyin et al., (2022) Ziyin, L., Li, B., Simon, J. B., and Ueda, M. (2022). SGD can converge to local maxima. In International Conference on Learning Representations.

Appendix A Experiments

A.1 Label noise and regularization

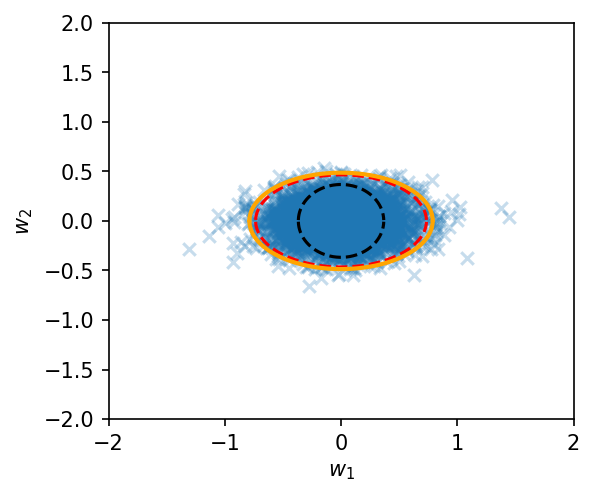

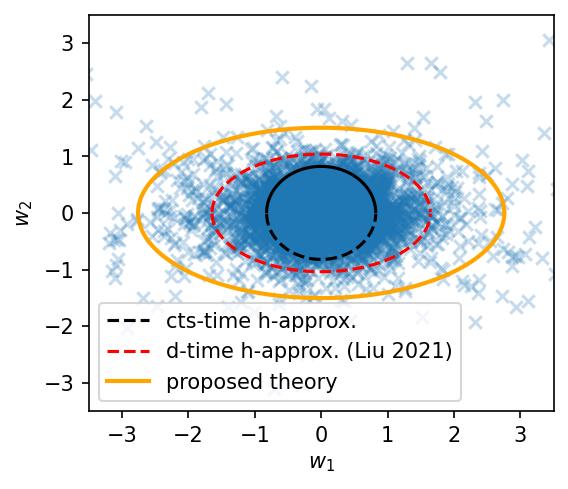

Theorem 2 can be verified empirically. We run 1d experiment in Figure 4(a) and high dimensional experiments in Figures 4(b)-(c), where we choose for visualization. We see that the continuous Hessian approximation fails badly for both large and small batch sizes. When the batch size is large, both the discrete-time Hessian approximation and our solution give a accurate estimate of the shape and the spread of the distribution. This suggests that when the batch size is large, discreteness is the determining factor of the fluctuation. When the batch size is small, the discrete Hessian approximation severely underestimates the strength of the noise. This reflects the fact that the isotropic noise enhancement is dominant at a small batch size.

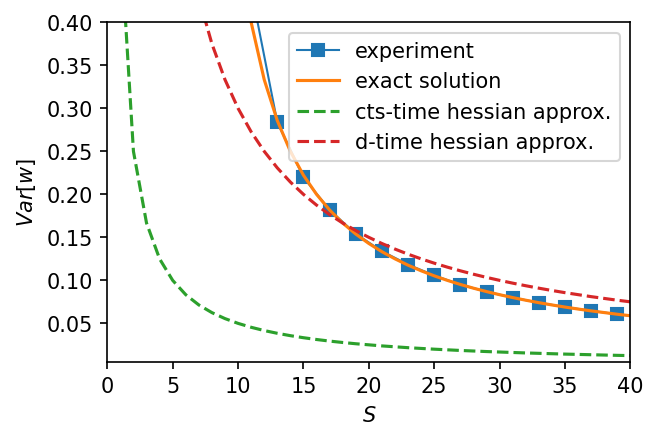

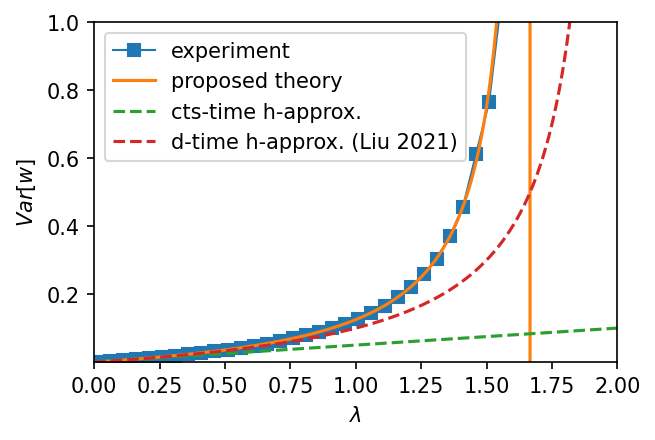

In Figure 3-Left, we run a 1d experiment with , and . Comparing the predicted , we see that the proposed theory agrees with the experiment across all ranges of . The continuous theory with the Hessian approximation fails almost everywhere, while the recently proposed discrete theory with the Hessian approximation underestimates the fluctuation when is small. In Figure 3-Right, we plot a standard case where the optimal regularization strength is vanishing.

Now, we validate the existence of the optimal negative weight decay as predicted by our formula. For illustration, we plot in Figure 5 the test loss (11) for a 1d example while varying either or . The orange vertical lines show the place where the theory predicts a divergence in the test loss. We also plot a standard case where the optimal is close to 0 in Appendix A. Also, we note that the proposed theory agrees better with the experiment.

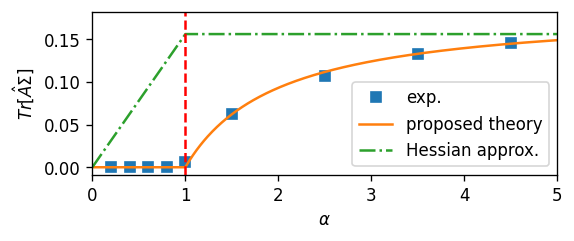

A.2 High-Dimensional Regression

See Figure 6-Left. We vary with held fixed. We set and . We see that the agreement between the theory and experiment is good, even for this modest dimension number . The vertical line shows where the over-to-underparametrization transition takes place. As expected, there is no fluctuation when , and the fluctuation gradually increases as . On the other hand, the Hessian approximation gives a wrong picture, predicting fluctuation to rise when there is no fluctuation and predicting a constant fluctuation just when the fluctuation starts to rise.

Appendix B Comparison with Conventional Hessian Approximation

We compare our results for the three cases with the results obtained with the conventional Hessian approximation of the noise covariance, i.e., , where is the Hessian of the loss function. We summarize the analytical results for a special case in Table 2.

B.1 Label Noise

We first consider discrete-time dynamics with the Hessian approximation. The matrix equation is

| (18) |

Compared with the exact result (3), it is a large- limit up to the constant . This constant factor is ignored during the approximation that , which is exact only when is a negative log likelihood function of . Solving the matrix equation yields

| (19) |

The training loss and the test loss are

| (20) | |||

| (21) |

On the other hand, by taking the large- limit directly from the exact equation (3), the factor is present:

| (22) |

For the continuous-time limit with the Hessian approximation, the matrix equation is

| (23) |

which is the small- limit up to the factor . The variance is

| (24) |

The training and the test error are

| (25) | |||

| (26) |

Again, taking the small- limit directly from the exact result (3) shows the presence of the factor on the right hand side of the matrix equation.

B.2 Input Noise

The case with the input noise is similar to the label noise. This can be understood if we replace by and by . The model parameter variance resulting from the discrete-time dynamics under the Hessian approximation is

| (27) |

The training and the test error are

| (28) | |||

| (29) |

The large- limit from the exact matrix equation (144) results in a prefactor in the fluctuation:

| (30) |

For the continuous-time limit, we take . The Hessian approximation gives

| (31) | |||

| (32) | |||

| (33) |

The large- limit again produces a prefactor .

B.3 Regularization

For learning with regularization, there is a more difference between the Hessian approximation and the limit taken directly from the exact theory. We first adopt the Hessian approximation for the discrete-time dynamics. The matrix equation is

| (34) |

which is similar to the previous subsection. However, it is different from the large- limit of the exact matrix equation (154):

| (35) |

This significant difference suggests that the conventional Fisher-to-Hessian approximation fails badly. The fluctuation, the training loss, and the test loss with the Hessian approximation are

| (36) | |||

| (37) | |||

| (38) |

while the large- limit of the exact theory yields

| (39) | |||

| (40) | |||

| (41) |

The continuous-time results are obtained by taking the small- limit on Eqs. (36)-(38) for the Hessian approximation and on Eqs. (39)-(41) for the limiting cases of the exact theory. Specifically, for the Hessian approximation, we have

| (42) | |||

| (43) | |||

| (44) |

The small- limit of the exact theory yields

| (45) | |||

| (46) | |||

| (47) |

Appendix C Proof of the General Formula

C.1 Proof of Theorem 5 and Corollary 2

We restate the theorem.

Theorem 7.

Let the training loss be and the models be optimized with SGD in the neighborhood of a local minimum . When , the noise covariance is given by

| (48) |

When and ,

| (49) |

When and ,

| (50) |

Proof.

We will use the following shorthand notations: , , . The Hessian of the loss function without regularization is given by

| (51) |

The last term of Eq. (51) can be ignored when , since

where stands for the Frobenius norm333In the linear regression problem, the last term of Eq. (51) does not exist since ., and we have defined the variable . Since for the mean-square error, we obtain

| (52) |

near a minimum. The Hessian with regularization is just given by .

On the other hand, the SGD noise covariance is given by Eq. (2). By assumption 2, the SGD noise covariance is directly related to the Hessian:

| (53) |

This finishes the proof.

Now we prove Corollary 2.

Proof. Near a minimum of the full loss , we have

| (54) |

within the approximation . Equations (14) and (54) give the SGD noise covariance near a minimum of .

Now it is worth discussing two different cases separately: (1) with regularization and (2) without regularization. We first discuss the case when regularization is present. In this case, the regularization is not small enough, and the SGD noise covariance is not proportional to the Hessian. Near a local or global minimum , the first term of the right-hand side of Eq. (54) is negligible, and hence we obtain

| (55) |

where we have used the fact that . The SGD noise does not vanish even at a global minimum of . Note that this also agrees with the exact result derived in Sec. 4.3: together with an anisotropic noise that is proportional to the Hessian, a rank- noise proportional to the strength of the regularization appears. This rank-1 noise is a signature of regularization.

On the other hand, as we will see below, the SGD noise covariance is proportional to the Hessian near a minimum when there is no regularization, i.e., . We have

| (56) |

For this case, we need to differentiate between a local minimum and a global minimum. When is not small enough (e.g. at a local but not global minimum),

| (57) |

and so, to leading order,

| (58) |

which is proportional to the Hessian but also proportional to the achievable approximation error.

On the other hand, when is vanishingly small (e.g. at a global minimum), we have , and thus obtain

| (59) |

i.e.,

| (60) |

This completes the proof. ∎

Remark.

It should be noted that the second term on the right-hand side of Eq. (59) would typically be much smaller than the first term for large . For example, when with , the first and the second terms are respectively given by and . The Frobenius norm of the former is given by , while that of the latter is given by , which indicates that in Eq. (59), the first term is dominant over the second term for large . Therefore the second term of Eq. (59) can be dropped for large , and Eq. (59) is simplified as

| (61) |

Again, the SGD noise covariance is proportional to the Hessian.

In conclusion, as long as the regularization is small enough, that the SGD noise covariance near a minimum is proportional to the Hessian is a good approximation. This implies that the noise is multiplicative, which is known to lead to a heavy tail distribution (Clauset et al.,, 2009; Levy and Solomon,, 1996). Thus, we have studied the nature of the minibatch SGD noise in three different situations. As an example, we have demonstrated the power of this general formulation by applying it to the high-dimensional linear regression problem in Sec. 6.1.

C.2 Proof of Corollary 3

Proof.

We prove the case where and as an example. Substituting Theorem 5 into Theorem 1yields

| (62) |

where we have assumed necessary commutation relations. Suppose that the Hessian is of rank- with . The singular-value decomposition and its Moore-Penrose pseudo inverse are given by and , respectively, where and are unitary, is a rank- diagonal matrix with elements being singular values of , and is obtained by inverting every non-zero entry of . Multiplying to both sides of the above equation, we have

| (63) |

where is the projection operator with non-zero entries. When the Hessian is full-rank, i.e., , the Moore-Penrose pseudo inverse is nothing but the usual inverse. The other cases can be calculated similarly. ∎

Appendix D Applications

D.1 Infinite-dimensional Limit of the Linear Regression Problem

Now we apply the general theory in Sec. 5 to linear regressions in the high-dimensional limit, namely with held fixed.

D.1.1 Proof of Proposition 4

The loss function

| (64) |

with can be written as

| (65) |

where is an empirical covariance for the training data and . The symbol denotes the Moore-Penrose pseudoinverse. We also introduce the the averaged traing loss:

The minimum of the loss function is given by

| (66) |

where is an arbitrary vector and is the projection onto the null space of . Since , is also expressed as

| (67) |

In an underparameterized regime , almost surely holds as long as the minimum eigenvalue of (not ) is positive (Hastie et al.,, 2019). In this case, and we obtain

| (68) |

On the other hand, in an overparameterized regime , and there are infinitely many global minima. In the ridgeless regression, we consider the global minimum that has the minimum norm , which corresponds to

| (69) |

In both cases, the loss function is expressed as

| (70) |

Asymptotically, converges to a stationary point with fluctuation obeying the following equation (Theorem 1:

| (71) |

The SGD noise covariance is given by Eq. (14). In the present case, the Hessian is given by and we also have

| (72) |

On the other hand, , and hence . Therefore we obtain

| (73) |

Now, we find . First, we define as , and as . Then .

With this notation, we have , and the loss function is expressed as

| (74) |

We therefore obtain

| (75) |

Here,

| (76) |

We can prove that the following identity is almost surely satisfied (Hastie et al.,, 2019) as long as the smallest eigenvalue of (not ) is positive:

| (77) |

We therefore obtain

| (78) |

D.1.2 Proof of Theorem 6

D.2 Second-order Methods

Proposition 5.

Suppose that we run DNM with with random noise in the label. The model fluctuation is

| (83) |

where .

Proof.

Proposition 6.

Suppose that we run NGD with with random noise in the label. The model fluctuation is

| (87) |

where .

Proof.

Similarly to the previous case, the matrix equation satisfied by is

| (88) |

Although it is not obvious how to directly solve this equation, it is possible to guess one solution according to the hope that be proportional to , in turn, (Amari,, 1998; Liu et al.,, 2021). We assume that and substitute it into the above equation to solve for . This yields one solution without claiming its uniqueness. By simple algebra, this is solved to be

| (89) |

Let . We obtain the result in Sec. 6.4. ∎

D.3 Estimation of Tail Index

In Mori et al., (2021); Meng et al., (2020), it is shown that the (1d) discrete-time SGD results in a distribution that is similar to a Student’s t-distribution:

| (90) |

where is the degree of noise in the label, and is the local curvature of the minimum. For large , this distribution is a power-law distribution with tail index:

| (91) |

and it is not hard to check that also equal to the smallest moment of that diverges: . Therefore, estimating can be of great use both empirically and theoretically.

In continuous-time, it is found that (Mori et al.,, 2021). For discrete-time SGD, we hypothesize that the discrete-time nature causes a change in the tail index , and we are interested in finding . We propose a “semi-continuous" approximation to give the formula to estimate the tail index. Notice that Theorem 2 gives the variance of the discrete-time SGD, while Eq. (90) can be integrated to give another value of the variance, and the two expressions must be equal for consistency. This gives us an equation that must satisfy:

| (92) |

this procedure gives the following formula:

| (93) |

and one immediately recognizes that is the discrete-time contribution to the tail index. See Figure 7 for additional experiments. We see that the proposed formula agrees with the experimentally measured value of the tail index for all ranges of the learning rate, while the result of Mori et al., (2021) is only correct when . Hodgkinson and Mahoney, (2020) also studies the tail exponent of discrete-time SGD; however, their conclusion is only that the “index decreases with the learning rate and increases with the batch size". In contrast, our result give the functional form of the tail index directly. In fact, this is the first work that gives any functional form for the tail index of discrete-time SGD fluctuation to the best of our knowledge.

The following proposition gives the intermediate steps in the calculation.

Proposition 7.

Tail index estimation for discrete-time SGD Let the parameter distribution be , and be given by Theorem 2. Then

| (94) |

Appendix E Proofs and Additional Theoretical Considerations

E.1 Proof of Proposition 1

The with-replacement sampling is defined in Definition 2. Let us here define the without-replacement sampling.

Definition 3.

A minibatch SGD without replacement computes the update to the parameter with the following set of equations:

| (98) |

where is the minibatch size, and the set is an element uniformly-randomly drawn from the set of all -size subsets of .

From the definition of the update rule for sampling with or without replacement, the covariance matrix of the SGD noise can be exactly derived.

Proposition 8.

In the limit of or , two cases coincide. In the limit, both methods of sampling have the same noise covariance as stated in Proposition 1:

| (100) |

Remark.

We also note that a different way of defining minibatch noise exists in Hoffer et al., (2017). The difference is that our definition requires the size of each minibatch to be exactly , while Hoffer et al., (2017) treats the batch size also as a random variable and is only expected to be . In comparison, our definition agrees better with the common practice.

Now we prove Proposition 8.

Proof.

We derive the noise covariance matrices for sampling with and without replacement. We first derive the case with replacement. According to the definition, the stochastic gradient for sampling with replacement can be rewritten as

| (101) |

where and

| (102) |

The probability of assuming value is given by the multinomial distribution

| (103) |

Therefore, the expectation value of is given by

| (104) |

which gives

| (105) |

For the covariance, we first calculate the covariance between and . Due to the properties of the covariance of multinomial distribution, we have for

| (106) |

and for

| (107) |

Substituting these results into the definition of the noise covariance yields

| (108) |

Then, we derive the noise covariance for sampling without replacement. Similarly, according to the definition, the stochastic gradient for sampling without replacement can be rewritten as

| (109) |

where

| (110) |

The probability of that is sampled in from is given by

| (111) |

The expectation value of is then given by

| (112) |

which gives

| (113) |

For the covariance, we first calculate the covariance between and . By definition, we have for

| (114) |

and for

| (115) |

Substituting these results into the definition of the noise covariance yields

| (116) |

∎

E.2 Proofs in Sec. 4.2

E.2.1 Proof of Lemma 1

Proof.

From the definition of noise covariance (2), the covariance matrix for the noise in the label is

| (117) | ||||

| (118) |

where we have invoked the law of large numbers and the expectation value of the product of four Gaussian random variables in the third line is evaluated as follows.

Because is large, we invoke the law of large numbers to obtain the -th component of the matrix as

| (119) |

Because the average is taken with respect to and each is a Gaussian random variable, we apply the expression for the product of four Gaussian random variables (Janssen and Stoica,, 1988) to obtain

| (120) |

Writing , we obtain

| (121) |

∎

This method has been utilized repeatedly in this work.

E.2.2 Proof of Theorem 2

Proof.

We substitute Eq. (5) into Eq. (3) which is a general solution obtained in a recent work (Liu et al.,, 2021):

| (122) |

To solve it, we assume the commutation relation that . Therefore, the above equation can be alternatively rewritten as

| (123) |

To solve this equation, we first need to solve for . Multiplying Eq. (123) by and taking trace, we obtain

| (124) |

which solves to give

| (125) |

Therefore, is

| (126) |

∎

E.2.3 Training Error and Test Error for Label Noise

In the following theorem, we calculate the expected training and test loss for random noise in the label.

Theorem 8.

Approximation error and test loss for SGD noise in the label The expected approximation error, or the training loss, is defined as ; the expected test loss is defined as . For SGD with noise in the label given by Eq. (5), the expected approximation error and test loss are

| (127) | |||

| (128) |

Remark.

Notably, the training loss decomposes into two additive terms. The term that is proportional to is the bias, caused by insufficient model expressivity to perfectly fit all the data points, while the second term that is proportional to is the variance in the model parameter, induced by the randomness of minibatch noise.

Remark.

When the learning rate is vanishingly small, the expected test loss diminishes whereas the training error remains finite as long as label noise exists.

Proof.

We first calculate the approximation error. By definition,

| (129) |

The test loss is

| (130) |

∎

E.3 Minibatch Noise for Random Noise in the Input

E.3.1 Noise Structure

Similar to label noise, noise in the input data can also cause fluctuation. We assume that the training data points can be decomposed into a signal part and a random part. As before, we assume Gaussian distributions, and . The problem remains analytically solvable if we replace the Gaussian assumption by the weaker assumption that the fourth-order moment exists and takes some matrix form. For conciseness, we assume that there is no noise in the label, namely with a constant vector . One important quantity in this case will be . Notice that the trick no more works, and so we write the difference explicitly here. The loss function then takes the form

| (131) |

The gradient vanishes at , which is the minimum of the loss function and the expectation of the parameter at convergence. It can be seen that, even at the minimum , the loss function remains finite unless , which reflects the fact that in the presence of input noise, the network is not expressive enough to memorize all the information of the data. The SGD noise covariance for this type of noise is calculated in the following proposition.

Proposition 9.

Remark.

Defining the test loss as , Proposition 9 can then be used to calculate the test loss and the model fluctuation.

Theorem 9.

Training error, test loss and model fluctuation for noise in the input The expected training loss is defined as , and the expected test loss is defined as . For SGD with noise in the input given in Proposition (9), the expected approximation error and test loss are

| (133) | |||

| (134) |

where with , and . Moreover, let . Then the covariance matrix of model parameters is

| (135) |

Remark.

Note that is necessary only for an analytical expression of . It can be obtained by solving Eq. (144) even without invoking . In general, the condition that does not hold. Therefore, only the training and test error can be calculated exactly.

Remark.

The test loss is always smaller than or equal to the training loss because all matrices involved here are positive semidefinite.

E.3.2 Proof of Proposition 9

Proof.

We define . Then,

| (136) | |||

| (137) |

where we use the shorthand notations , and , . We remark that the covariance matrix here still satisfies the matrix equation (3) with the Hessian being .

The noise covariance is

| (138) |

In Eq. (138), there are four terms without trace and two terms with trace. We first calculate the traceless terms. For the latter two terms, we have

| (139) | |||

| (140) |

Because , after simple algebra the four traceless terms result in .

The two traceful terms add to . With the relation , what inside the trace is

| (141) |

Therefore, the asymptotic noise is

| (142) | ||||

| (143) |

∎

E.3.3 Proof of Theorem 9

Proof.

The matrix equation satisfied by is

| (144) |

By using a similar technique as in Appendix E.2.2, the trace can be calculated to give

| (145) |

where with .

With Eq. (145), the training error and the test error can be calculated. The approximation error is

| (146) |

The test loss takes the form of a bias-variance tradeoff:

| (147) |

Let . Then can be explicitly solved because it is a function of and . Specifically,

| (148) |

∎

E.4 Proofs in Sec. 4.3

E.4.1 Proof of Proposition 3

Proof.

The covariance matrix of the noise is

| (149) |

E.4.2 Proof of Theorem 4

Besides the test loss and the model fluctuation, we derive the approximation error here as well.

Theorem.

Training error, test loss and model fluctuation for learning with L2 regularization The expected training loss is defined as , and the expected test loss is defined as . For noise induced by L2 regularization given in Proposition 3, let . Then the expected approximation error and test loss are

| (151) | |||

| (152) |

where , , with . Moreover, if , and commute with each other, the model fluctuation is

| (153) |

Remark.

Because may not be positive semidefinite, the test loss can be larger than the training loss, which is different from the input noise case.

Proof.

The matrix equation obeyed by is

| (154) |

where we use the shorthand notation . Let . Using the trick in Appendix E.2.2, the trace term is calculated as

| (155) |

where , , and .

The training error is

| (156) |

The test loss is

| (157) |

Let , and commute with each other. Then,

| (158) |

∎

E.4.3 Proof of Corollary 1

For a 1d example, the training loss and the test loss have a simple form. We use lowercase letters for 1d cases.

Corollary 4.

For a 1d SGD with L2 regularization, the training loss and the test loss are

| (159) | |||

| (160) |

Proof.

The training error and the test loss for 1d cases can be easily obtained from Theorem Theorem. ∎

Now we prove Corollary 1.

Proof.

The condition for convergence is . Specifically,

| (161) |

For a given , the learning rate needs to satisfy

| (162) |

For a given , needs to satisfy

| (163) |

which indicates a constraint on :

| (164) |

If is allowed to be non-negative, the optimal value can only be due to the convergence condition. Therefore, a negative optimal requires an upper bound on it being negative, namely

| (165) |

Solving it, we have

| (166) |

By combining with Eq. (164), a necessary condition for the existence of a negative optimal is

| (167) |

Hence, a negative optimal exists, if and only if

| (168) |

∎

For higher dimension with , it is possible to calculate the optimal for minimizing the test loss (11) as well. Specifically, the condition is given by

| (169) |

where

| (170) | |||

| (171) |

Although it is impossible to solve the equation analytically, it can be solved numerically.