∎

22email: jiangjiecq@163.com 33institutetext: Xiaojun Chen 44institutetext: Department of Applied Mathematics, The Hong Kong Polytechnic University, Hong Kong

44email: maxjchen@polyu.edu.hk

Pure Characteristics Demand Models and Distributionally Robust Mathematical Programs with Stochastic Complementarity Constraints††thanks: This paper is dedicated to the memory of Olvi L. Mangasarian. His contributions to linear complementarity problems have impacted greatly on our research on distributionally robust mathematical programs with stochastic complementarity constraints.

Abstract

We formulate pure characteristics demand models under uncertainties of probability distributions as distributionally robust mathematical programs with stochastic complementarity constraints (DRMP-SCC). For any fixed first-stage variable and a random realization, the second-stage problem of DRMP-SCC is a monotone linear complementarity problem (LCP). To deal with uncertainties of probability distributions of the involved random variables in the stochastic LCP, we use the distributionally robust approach. Moreover, we propose an approximation problem with regularization and discretization to solve DRMP-SCC, which is a two-stage nonconvex-nonconcave minimax optimization problem. We prove the convergence of the approximation problem to DRMP-SCC regarding the optimal solution sets, optimal values and stationary points as the regularization parameter goes to zero and the sample size goes to infinity. Finally, preliminary numerical results for investigating distributional robustness of pure characteristics demand models are reported to illustrate the effectiveness and efficiency of our approaches.

Keywords:

distributionally robust stochastic equilibrium regularization discrete approximation pure characteristics demandMSC:

90C15 90C33 90C261 Introduction

Pure characteristics demand models are widely used in microeconometrics to estimate parameters in utility functions of agents for given prices and production decisions BP2007pure ; SJ2012constrained . Such models have advantages in inferring consumers’ preference and behavior, but face computational challenges to solve the optimization problem with set-valued stochastic equilibrium constraints as follows:

| (1) |

where is a compact and convex set, is a positive semidefinite matrix, , is a random vector defined on a probability space and supported on , , , , , is the number of markets, is a Aumann’s (set-valued) expectation for multifunction and for given ,

| (2) |

Here is the consumers’ utility function in market and is the vector with all elements being 1.

To efficiently solve problem (1), Pang, Su and Lee PSL2015constructive characterized consumers’ purchase decision in the constraints of problem (1) by linear complementarity problems and proposed the following quadratic program with stochastic complementarity constraints (QP-SCC):

| (3) |

where

and a.e. is the short for almost everywhere. The pioneered QP-SCC formulation opened a way to develop optimization algorithms for solving pure characteristics demand models. In CSW2015regularized , Chen, Sun and Wets proposed a penalty approach:

| (4) |

where is a penalty parameter.

In problems (1)-(4), the probability distribution is supposed to be known exactly. However, in practice the true probability distribution can hardly be acquired. This observation motivates us to consider a class of distributionally robust stochastic mathematical programs with complementarity constraints (DRMP-SCC) as follows:

| (P) |

where is a measurable mapping, , , , with denoting the collection of all probability distributions supported on , , and is positive semidefinite for a.e. . For fixed and , a feasible vector is a solution of the monotone LCP. The error bounds for the monotone LCP and exact penalty theory for mathematical programms with linear complementarity constraints established by Mangasarian et al. in M1990error ; M1992global ; MF1967fritz ; MP1997exact ; MR1994new ; MS1986error have inspired us to solve problem (P).

Throughout this paper, we assume that , and are continuously differentiable. Moreover, , , , and are Lipschitz continuous with Lipschitz moduli , , , and satisfying , respectively. We also assume that problem (P) satisfies the relatively complete recourse condition that is for every and a.e. , the solution set of the complementarity constraints in (P), denoted by is nonempty and is well-defined for all and . Moreover, we assume that the ambiguity set is defined by a general moment information as follows:

| (5) |

where is a continuous random mapping consisting of vectors and/or matrices with measurable random components, and is a closed convex cone in the Cartesian product of some finite dimensional vector and/or matrix spaces. The ambiguity set defined in (5) is a very general form and includes many commonly-used moment ambiguity sets, such as the moment ambiguity set in DY2010distributionally . For more examples, we refer to (LPX2019discrete, , Examples 3-5).

Let be a set of samples of and define the discrete approximation of by

We consider the discrete approximation problem of (P) as follows:

| () |

where ,

Moreover, to develop numerical methods and convergence analysis, we consider the following regularized problems of (P) and (), respectively,

| () |

and

| () |

where is the regularization parameter and is the identity matrix with proper dimension.

Since is positive semidefinite for fixed , the complementarity problem LCP has a unique solution CPS1992linear , denoted by . Moreover, from the Lipschitz continuity of , is Lipschitz continuous CX2008perturbation . Analogously, LCP has also a unique solution, denoted by , which is also Lipschitz continuous with respect to (w.r.t.) .

Mathematical programming with equilibrium constraints (MPEC) has been extensively studied IS2008active ; LPR1996mathematical ; MP1997exact . Structural properties, discrete approximation based on sampling and numerical methods of stochastic MPEC with deterministic probability distribution have been investigated LCF2009solving ; LF2010stochastic ; LSS2016approximation ; SX2008stochastic ; XY2011approximating . To the best of our knowledge, there is little discussion on distributionally robust MPEC. Moreover, due to the complementarity constraints and the composite structure of the objective function, the minimax problems (P), () and () are generally nonconvex-nonconcave and their saddle points may not exist. We will focus on their minimax points, minimizers in -space and corresponding optimality conditions.

The main contributions of the paper are summarized as follows.

-

•

Inspired by the constructive reformulations of pure characteristics demand models in PSL2015constructive , we propose a DRMP-SCC model (P) under uncertainties of probability distributions. We give the definitions of global and local minimax points to capture the optima of the nonconvex-nonconcave minimax problem (P). Some sufficient conditions of existence of solutions are derived.

-

•

Under certain conditions, we prove the convergence of problem () to problem (P) regarding optimal solution sets and optimal values as the regularization parameter and the sample size .

- •

Notations. denotes the closed unit ball centered at original point in the corresponding space. denotes the set of nonnegative vectors in . denotes the Euclidean norm of vectors or the induced matrix norm. denotes the diameter of . and for and . denotes the interior of .

This paper is organized as follows. In Section 2, we give some preliminaries on the ambiguity set and its approximation . In Section 3, we give definitions of global and local minimax points of problems (P), () and (), and some existence results. After that, we prove the convergence of the solution set and optimal value of problem () to those of problem (P) as and . In Section 4, we first give definitions of stationary points of problems (P), () and () and then study convergence assertions on the stationary points of problem () to those of problem (P). In Section 5, we report numerical results on the pure characteristics demand model under uncertainties of probability distributions. In Section 6, we give concluding remarks.

2 Preliminaries

Note that for each , it uniquely determines a discrete probability distribution , where is the indicator function, namely, if ; otherwise. Thus, in what follows, we will not distinguish and the corresponding probability distribution. In other words, we can write

Based on the set , we have the corresponding Voronoi tessellation of ,

Obviously, and for any .

In this paper, we make a commonly employed Slater type assumption for ambiguity set (5) as follows (see e.g. DY2010distributionally ; LPX2019discrete ).

Assumption 1

There exist and such that

Proposition 1

Under Assumption 1, there exists such that is nonempty for any

The proof of Proposition 1 is given in Appendix.

To measure the distance between two probability distributions (and thus two ambiguity sets), we use the well-known Wasserstein metric.

Definition 1 (KR1958space )

Let . The Wasserstein metric between is defined as

Notice that Definition 1 gives the definition of Wasserstein metric by using the Kantorovich-Rubinstein theorem. Another definition of Wasserstein metric is based on the joint probability distributions with marginal distributions and , see e.g. V2003topics for more details.

The deviation distance between induced by Wasserstein metric is denoted by , namely,

Obviously, , which implies that the deviation distance between and is always zero, i.e. . To derive the estimation of , we assume in the rest of this section that is bounded and denote

| (6) |

where is defined in Assumption 1.

The following Hoffman’s type lemma is from (LPX2019discrete, , Theorem 2).

Lemma 1 (LPX2019discrete )

For a sample set and the resulting Voronoi tessellation , we call the following probability distribution

the Voronoi projection of . Denote by

| (7) |

the Hausdorff distance between and .

The following lemma gives an estimation of Wasserstein distance between and its Voronoi projection.

Lemma 2 (Lemma 4.9, PP2014multistage )

Let and be the Voronoi projection of . Then .

Then, we have an estimation of from LPX2019discrete .

Proposition 2 (LPX2019discrete )

In the remaining paper, we tacitly assume that both and are nonempty.

3 Optimal values and solutions of problems (P) and ()

Note that the function is not convex for a fixed , and is not concave for a fixed tuple . This usually implies that

By the saddle point existence theorem Debreu , does not have a saddle point that satisfies

for any . Hence, we define global and local minimax points of problem (P) by using the idea in JNJ2020local .

Definition 2

We call a local minimax point of problem (P), if there exist a and a function satisfying as , such that

for any , satisfying and and satisfying .

Similarly, we can define global minimax points and local minimax points of problems (), () and (), respectively.

Using the notation , problem (P) regarding minimizers can be rewritten as

| (8) |

By substituting the unique solution of LCP (denoted by ) into the objective function, problem () can be rewritten as

| (9) |

Then its discrete approximation problem () can be rewritten as

| (10) |

where .

Denote by , , , and , , the sets of minimizers and optimal values of problems (8), (9) and (10), respectively. Let be the projection of onto -space. In this section, we provide conditions for the existence of minimizers of problems (P), () and (), and prove the convergence of optimal values and optimal solution sets of problem () to those of problem (P) as and . The convergence analysis is divided into two parts: the convergence of () to (P) as and the convergence of () to () as for a fixed .

3.1 Existence of solutions

In this subsection, we provide some sufficient conditions for the existence of global minimax points of problems (P), () and (), respectively.

Let be the Lipschitz modulus of and be the Lipschitz modulus of . For a fixed and , we have

for any . Therefore, is Lipschitz continuous over the compact and convex set , and it has a minimizer . Moreover, is closed and bounded due to the continuity of and is continuous w.r.t. . Hence, there is a maximizer such that is a global minimax point of problem ().

In what follows, we provide sufficient conditions for the existence of solutions to problems (P) and ().

Recall that a sequentially compact set means that any sequence contained in this set has a convergent subsequence. We say a sequence of probability distribution weakly converges to if as for any continuous and bounded function . A subset of is weakly compact if any sequence in this subset has a weak convergent subsequence with a weak limit point contained in this subset.

Assumption 2

-

(i)

There exists with such that

-

(ii)

There exists a tuple such that .

Theorem 3.1

Proof

By Assumption 2, we have

Hence for any , which means there is such that . To prove that problem (P) has a minimizer under Assumption 2, we only need to show that is lower semicontinuous (lsc) due to the sequential compactness of (RW2009variational, , Theorem 1.9).

First, we show that for a fixed , is lsc. By the Lipschitz continuity of and , we know that

if Hence is continuous for fixed and , which implies that is lsc.

Similarly, we can show that is lsc over . Since is a Lipchitz continuous function of , we derive that is lsc. ∎

Theorem 3.2

Proof

Since is a positive definite matrix for any , the solution set SOL has a unique vector for any and . Moreover, from Lipschitz continuity of and and boundness of and , there is a positive number such that

which implies , for . See error bounds for the LCP in CX2008perturbation ; CPS1992linear . Hence, Assumption 2 holds with and . Using a similar proof of Theorem 3.1, we can show that problem () has a minimizer .

3.2 Convergence analysis between problems (P) and ()

We use that LCP has a unique solution to introduce the following auxiliary problem with fixed and ,

| (11) |

Since is a measurable function for any and is bounded, is a measurable function for any . By assumptions of Theorems 3.1-3.2, problems (P), () and (11) have minimizers. Denote by the optimal value of problem (11). We make the following technical assumption.

Assumption 3

Remark 1

Assumption 3 is a standard assumption and used widely in the perturbation analysis for parametric programming, see also (CSW2015regularized, , Assumption 1) and (BS2013perturbation, , Chapter 4).

Theorem 3.3

Under Assumption 3, if as , then we have

Proof

Using the Lipschitz continuity conditions on , we have

By Hölder inequality, we have that

as due to and as . Thus, we obtain . This together with Assumption 3 implies that as . ∎

Since is positive semidefinite and the solution set of LCP is nonempty for any and by the assumption of relatively complete recourse, the unique solution converges to the least norm solution of LCP as (CPS1992linear, , Theorem 5.6.2), which is defined by

Proposition 3

Suppose that uniformly as in and . Then

Proof

By assumptions and the boundness of , we have

as . Moreover, from the above inequalities, we find that converges to uniformly w.r.t. over as . By (SDR2014lectures, , Theorem 5.3), we derive the convergence of . ∎

3.3 Convergence analysis between problems () and ()

In this subsection, for a fixed , we consider the convergence between problems () and () as . Let the support set be bounded throughout this subsection.

By (CX2008perturbation, , Theorem 2.8), there exists an such that for any ,

where the existence of a constant employs the boundness of and and Lipschitz continuity of . Moreover, if is Lipschitz continuous, there exists an such that for any ,

| (12) |

We give the following quantitative stability results between problems (9) and (10) based on Wasserstein metric.

Theorem 3.4

Proof

4 Stationarity of problems (P) and ()

In this section, we consider the convergence of stationary points of problem () to these of problem (P) as and . We first consider the stationary points defined by the regular normal cone in RW2009variational .

The regular normal cone to a closed set at , denoted by , is

where means that as . The (limiting) normal cone to a closed set at , denoted by , is

is a closed and convex cone and is outer semicontinuous over . is a closed cone. Generally, we have . They are consistent when is convex, namely,

A necessary condition for to be a local minimizer of , where is a differentiable function over , is (see (RW2009variational, , Theorem 6.12))

In Section 4.1, we focus on the concepts of stationary points of problems (P), () and (). In Section 4.2, we give convergence results regarding the stationary points between problems () and (P) as and .

4.1 Concepts of stationarity

We first consider the concepts of stationary points of the discrete problems () and (). To simplify the notation, we denote

Then problems () and () can be rewritten, respectively, as

| (15) |

and

| (16) |

Note that the set is convex and bounded. We have the following optimality condition for a local minimax point.

Proposition 4 (optimality condition for a local minimax point)

If is a local minimax point of problem (15), then it satisfies

| (17) |

Proof

Let be a local minimax point. To simplify the notation, denote . According to the definition of local minimax points, there exist a and a function satisfying as , such that for any and satisfying and , we have

| (18) |

Obviously, the first inequality in (18) implies the second assertion in (17).

Next, we verify the first assertion in (17). For any , let be the tangent cone of at (see (RW2009variational, , Definition 6.1)) and

From the second inequality in (18), we have, for any with and , that

where the last equality follows from as , which implies

Thus, for any , which indicates (see (RW2009variational, , Proposition 6.5)) the first assertion in (17). ∎

It is noteworthy that the necessary condition for local minimax points in Proposition 4 is also a necessary condition for saddle points, see e.g. RHLNSH2020non ; PS2011nonconvex ; NSHLR2019solving . is a convex set because of the positive semidefiniteness of If we consider individually, it then leads to the concept of block coordinatewise stationarity (see e.g. XY2013block ) as follows:

| (19) |

Condition (19) is a weaker necessary condition than (17) for local optimality of problem (15) (see e.g. (XY2013block, , Remark 2.2)). The second assertion in (19) corresponds to a necessary condition for local optimality of the mathematical programming with linear complementarity constraint (MPLCC). Consider

| (20) |

To characterize optimality conditions of MPLCC, we define the following index sets:

Definition 3 (stationary points for MPLCC, CY2009class )

(i) We say that is a (weak stationary) W-stationary point of problem (20) if there exist multipliers such that

| (21) | ||||

(ii) We say that is a (Clarke stationary) C-stationary point of problem (20) if there exist satisfying (21) and

Obviously, we have the following observation:

For more details about the optimality conditions of the mathematical programming with equilibrium constraints (MPEC), we refer to monograph (LPR1996mathematical, , Chapter 3).

Combined (19) with Definition 3, we give the following concepts of block coordinatewise stationary points of problem ().

Definition 4 (block coordinatewise -stationary points of ())

Let . We say it is a block coordinatewise -stationary point of problem (15) if it satisfies

where “” can be W, C, M and S.

Analogously, we give the block coordinatewise stationary point of regularized problem (). Since there is a unique solution of LCP for any , we use the following definition of block coordinatewise stationary points for problem ().

Definition 5 (block coordinatewise stationary points of ())

We call a block coordinatewise stationary point of problem (16), if it satisfies

| (22) |

The following lemma shows that a point satisfying (22) must be a block coordinatewise S-stationary point of problem ().

Lemma 3

For fixed and , is an S-stationary point of the MPLCC (20).

Proof

The feasible set of (20) with has a unique vector . From (GL2013notes, , Proposition 2.2, (ii) and (iii)), is an S-stationary point since both and are linear functions of . ∎

Remark 2

Note that and thus . Hence, if satisfies

| (23) |

then satisfies (22). The main considerations for (23) are that is not convex for given if is a nonlinear function, and is not Lipschitz continuous in the sense of Hausdorff distance, which can lead to failing the following convergence analysis (see e.g. XY2013block ). In view of these, we use in the sequel rather than .

MPEC is generally difficult to deal with because its constraints fail to satisfy the standard Mangasarian-Fromovitz constraint qualification (originated from MF1967fritz ) at any feasible point (YZZ1997exact, , Proposition 1.1). We recall the definition of MPEC linear independence constraint qualification (MPEC-LICQ).

Definition 6 (SS2000mathematical )

We say that MPEC-LICQ holds at for problem (20) if

is linearly independent, where is the th column of the identify matrix and is the th row of the matrix .

In what follows, we give the stationarity of problem (P). To this end, we assume that for arbitrary probability distribution/measure there exists a corresponding density function such that 111We can generally assume that for some nominal probability distribution . We know from Radon-Nikodym theorem (see e.g. (SDR2014lectures, , Theorem 7.32)) that there exists such a density function if and only if is absolutely continuous w.r.t. . Here we neglect to simplify the notation.. Denote by the collection of all density functions of .

To define the block coordinatewise stationarity of problem (P), we first give the definition of stationary points for stochastic MPEC (see Definition 3 for the discrete version).

For fixed , we consider the following stochastic MPEC problem

| (24) |

Define the following index sets:

| (25) | ||||

Denote by the collection of all measurable mappings from to .

Definition 7 (stationary points of problem (24))

(i) We say that is a W-stationary point of problem (24) if there exist multipliers such that for a.e. ,

| (26) | ||||

(ii) We say that is a C-stationary point of problem (24) if there exist satisfying (26) and for a.e. ,

4.2 Convergence analysis

In this subsection, we study the convergence of block coordinatewise stationary points of () defined by (23). We first consider the convergence of the block coordinatewise stationary points as for a fixed in the following theorem.

Theorem 4.1

Proof

Since is an accumulation point of as , there exists a sequence with as , such that as . Based on (23), we have

We know from Definitions 3 and 4 and Lemma 3 that

where and are two sequences of multipliers, and

Thus, for sufficiently large , we have

| (27) |

where

Next, we verify the boundedness of sequences and . Notice that if is bounded, from the boundedness of and continuous differentiability of , is bounded. Now we assume that is unbounded. Consider, by dividing , that

which can deduce, according to as , that

| (28) |

as . Since for and for , we rewrite (28) as

where

Then, by MPEC-LICQ at for problem (20) with and , we obtain

as , which contradicts for some . Therefore, both and are bounded. Without loss of generality, we assume that and as . Therefore, by letting , we have from (27) that

| (29) |

Moreover, for for , we have for . This together with (29) means that is a block coordinatewise C-stationary point of problem (). ∎

Let and its corresponding Voronoi tessellation be . For any feasible point of (), denoted by , we make the following notations. Define the following density function:

where is the th component of for . We denote

Denote by

where is the th block of for . Denote by

If, further, is a block coordinatewise C-stationary point of problem (), according to the definition of block coordinatewise C-stationary point, we have

| (30) |

where

Denote by

where is the th block of and is the th block of for .

Then, we have the reformulation of (30) as follows: for every ,

| (31) |

where is the probability distribution of density function and

For , define the inner product and its induced norm by

and

Based on -norm, we can define the convergence relationship, denoted by , and the deviation distance, denoted by .

The following theorem claims that: under certain conditions, a sequence of C-stationary points of problem () converges to block coordinatewise C-stationary points of problem (P) as .

Theorem 4.2

Proof

Note that

Since and , we have and for a.e. as . By the continuity of , we have

for a.e. as . Moreover,

By Lebesgue’s dominated convergence theorem, we have

as , and similarly

as . Therefore, as . Due to the continuous differentiability of , we obtain

| (32) |

Analogously, we have

as . We obtain

| (33) |

Since , are continuous and as , and as . By directly letting , we obtain from the second part of (31) that

for a.e. . Here is the limit of in the sense of -norm as . Its existence is due to the convergence of sequences , and as . Let , and be denoted in (25). Obviously, we have for a.e. that and for sufficiently large . Thus, we have

By a similar discussion as the proof of Theorem 4.1, we obtain . To sum up, we obtain

| (35) |

5 Pure characteristics demand models

In this section, we apply our results established in the previous sections to the pure characteristics demand model when the underlying probability distribution is uncertain. In particular, we consider the distributionally robust counterpart of problem (4):

where , and , which assumes that the mean of lies in a ball of size centered at the estimate (see e.g. (DY2010distributionally, , (1a))). By employing the Schur complement, we can reformulate as the form (5):

where the cone denotes the set of positive semidefinite matrices.

The regularization and discretization problem is

where , , for , and

We adopt the following settings, which follow from (CSW2015regularized, , Example 4.1). The utility function in market is given by

where , , , , . Let , and with , , , , .

To numerically present these convergence results in Section 3, we make the following specific settings. Set , , , , , , and , , . Consider

| (38) |

Here and .

It is easy to check that is an optimal solution of problem (38) and the corresponding optimal value is . To see this, we have

Therefore, . According to (2), we know that the solution set of is , where the least norm solution is for every . This implies that as . Thus, the conditions in Proposition 3 hold.

Under the above settings, and is the set of positive semidefinite matrices. Assumption 1 holds with being the uniform distribution over and being any positive scalar less than or equal to . Moreover, Assumption 2 holds with . Therefore, the convergence results in Section 3 hold.

We use the following alternating iterative algorithm to report some numerical results of problem (38).

Algorithm 1

Choose an initial point . Let and do the following two steps.

Step 1: Generate by solving

| (39) |

Step 2: Generate by solving

| (40) |

Let and go to Step 1.

Due to the special structure of matrix , we adopt the closed-form solution in CSW2015regularized to compute . The function is a quadratic convex function. We can use algorithm in Y1992affine to find a maximizer of in (40) on the bounded convex set . Since and are bounded, the sequence generated by Algorithm 1 has at least one accumulation point. We employ (23) as the stopping criterion. Actually, we only need to verify Due to the box structure of , the projection onto can be computed easily. Thus, we stop the iteration when

| (41) |

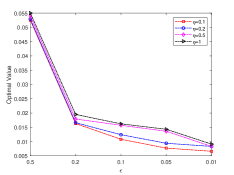

We chose an initial point with . First, for fixed and sample size , we compute optimal values of problem (38) w.r.t. . We present these results in Figure 1. It shows the tendency that the optimal value of problem (38) tends to zero as goes to zero. Meanwhile, for fixed each , we can observe from Figure 1 that the optimal value of problem (38) increases as increases, which shows that the distributionally robust model (38) works as expected.

Furthermore, for fixed and , we compute optimal values of problem (38) with different sample sizes, see Figure 2. It shows that, for each fixed , the optimal values converge as sample size goes to infinity. Moreover, we present in Table 1 the distances between satisfying (41) and the true solution with different and for fixed . It shows the convergence of optimal solutions as sample size goes to infinity for fixed .

| 4 | 25 | 100 | 225 | 625 | 2500 | |

|---|---|---|---|---|---|---|

| 0.5 | 0.5688 | 0.5210 | 0.6791 | 0.6887 | 0.7091 | 0.7202 |

| 0.2 | 0.7851 | 0.4422 | 0.3195 | 0.2215 | 0.2119 | 0.2102 |

| 0.1 | 0.6649 | 0.1079 | 0.0851 | 0.0853 | 0.0867 | 0.0856 |

6 Concluding remarks

This paper considers a class of distributionally robust mathematical programs with stochastic complementarity constraints (DRMP-SCC) in the form of problem (P), which arise from pure characteristics demand models under uncertainties of probability distributions of the involved random variables. Since problem (P) is a nonconvex-nonconcave minimax problem, minimax is not equal to maximin and thus a saddle point does not exist in general. We define global and local optimality and stationary points of problem (P), and its discretization and/or regularization approximation problems (), () and (). We provide sufficient conditions for the convergence of optimal solutions and stationary points of problem () as goes to zero and goes to infinity. We show that all those conditions hold for pure characteristics demand models under uncertainties. Moreover, we use numerical results to show the effectiveness of our theoretical results.

Appendix

Proof (The proof of Proposition 1)

Denote for . We verify that for all sufficiently large in the following. Since is continuous, we know from mean value theorem of integrals that

for some , . Then

| (42) |

We first consider the case that is bounded. For , there exists such that if , then

Since is bounded, we can find a sequence such that the corresponding Voronoi tessellation satisfying

Hence there is such that for any .

Then, it knows from (42) that

This, together with Assumption 1, indicates that which implies the nonemptiness of .

Now we consider the case is unbounded. Let for . Denote a probability distribution supported on by

for any measurable , where is defined in Assumption 1. Note that

We have

Therefore, there exists such that, for any ,

From Assumption 1, we obtain

| (43) |

Due to the boundedness of and (43), by the same proof for the case that is bounded, there exists a such that is nonempty for . ∎

References

- (1) Berry, S., Pakes, A.: The pure characteristics demand model. Internat. Econom. Rev. 48, 1193–1225 (2007)

- (2) Bonnans, J.F., Shapiro, A.: Perturbation Analysis of Optimization Problems. Springer, New York (2013)

- (3) Chen, X., Jane, Y.: A class of quadratic programs with linear complementarity constraints. Set-Valued Var. Anal. 17, 113–133 (2009)

- (4) Chen, X., Sun, H., Wets, R.J.B.: Regularized mathematical programs with stochastic equilibrium constraints: Estimating structural demand models. SIAM J. Optim. 25, 53–75 (2015)

- (5) Chen, X., Xiang, S.: Perturbation bounds of P-matrix linear complementarity problems. SIAM J. Optim. 18, 1250–1265 (2008)

- (6) Cottle, R.W., Pang, J.S., Stone, R.E.: The Linear Complementarity Problem, vol. 60. SIAM, Philadelphia (1992)

- (7) Debreu, G.: Saddle point existence theorems. Cowles Commission Discussion Paper: Mathematicas No.412 (1952)

- (8) Delage, E., Ye, Y.: Distributionally robust optimization under moment uncertainty with application to data-driven problems. Oper. Res. 58, 595–612 (2010)

- (9) Guo, L., Lin, G.H.: Notes on some constraint qualifications for mathematical programs with equilibrium constraints. J. Optim. Theory Appl. 156, 600–616 (2013)

- (10) Izmailov, A.F., Solodov, M.V.: An active-set Newton method for mathematical programs with complementarity constraints. SIAM J. Optim. 19, 1003–1027 (2008)

- (11) Jin, C., Netrapalli, P., Jordan, M.: What is local optimality in nonconvex-nonconcave minimax optimization? In: International Conference on Machine Learning, pp. 4880–4889. PMLR (2020)

- (12) Kantorovich, L.V., Rubinshtein, S.: On a space of totally additive functions. Vestnik of the St. Petersburg University: Mathematics 13, 52–59 (1958)

- (13) Lin, G.H., Chen, X., Fukushima, M.: Solving stochastic mathematical programs with equilibrium constraints via approximation and smoothing implicit programming with penalization. Math. Program. 116, 343–368 (2009)

- (14) Lin, G.H., Fukushima, M.: Stochastic equilibrium problems and stochastic mathematical programs with equilibrium constraints: A survey. Pac. J. Optim. 6, 455–482 (2010)

- (15) Liu, Y., Pichler, A., Xu, H.: Discrete approximation and quantification in distributionally robust optimization. Math. Oper. Res. 44, 19–37 (2019)

- (16) Luna, J.P., Sagastizábal, C., Solodov, M.: An approximation scheme for a class of risk-averse stochastic equilibrium problems. Math. Program. 157, 451–481 (2016)

- (17) Luo, Z.Q., Pang, J.S., Ralph, D.: Mathematical Programs with Equilibrium Constraints. Cambridge University Press, Cambridge (1996)

- (18) Mangasarian, O.L.: Error bounds for nondegenerate monotone linear complementarity problems. Math. Program. 48, 437–445 (1990)

- (19) Mangasarian, O.L.: Global error bounds for monotone affine variational inequality problems. Linear Algebra Appl. 174, 153–163 (1992)

- (20) Mangasarian, O.L., Fromovitz, S.: The Fritz John necessary optimality conditions in the presence of equality and inequality constraints. J. Math. Anal. Appl. 17, 37–47 (1967)

- (21) Mangasarian, O.L., Pang, J.S.: Exact penalty for mathematical programs with linear complementarity constraints. Optimization 42, 1–8 (1997)

- (22) Mangasarian, O.L., Ren, J.: New improved error bounds for the linear complementarity problem. Math. Program. 66, 241–255 (1994)

- (23) Mangasarian, O.L., Shiau, T.H.: Error bounds for monotone linear complementarity problems. Math. Program. 36, 81–89 (1986)

- (24) Nouiehed, M., Sanjabi, M., Huang, T., Lee, J.D., Razaviyayn, M.: Solving a class of non-convex min-max games using iterative first order methods. In: Advances in Neural Information Processing Systems, pp. 14934–14942 (2019)

- (25) Pang, J.S., Scutari, G.: Nonconvex games with side constraints. SIAM J. Optim. 21, 1491–1522 (2011)

- (26) Pang, J.S., Su, C.L., Lee, Y.C.: A constructive approach to estimating pure characteristics demand models with pricing. Oper. Res. 63, 639–659 (2015)

- (27) Pflug, G.C., Pichler, A.: Multistage Stochastic Optimization. Springer, Cham (2014)

- (28) Razaviyayn, M., Huang, T., Lu, S., Nouiehed, M., Sanjabi, M., Hong, M.: Non-convex min-max optimization: Applications, challenges, and recent theoretical advances. To preprint on arXiv (2020)

- (29) Rockafellar, R.T., Wets, R.J.B.: Variational Analysis, vol. 317. Springer-Verlag, Berlin (2009)

- (30) Scheel, H., Scholtes, S.: Mathematical programs with complementarity constraints: Stationarity, optimality, and sensitivity. Math. Oper. Res. 25, 1–22 (2000)

- (31) Shapiro, A., Dentcheva, D., Ruszczyński, A.: Lectures on Stochastic Programming: Modeling and Theory. SIAM, Philadelphia (2014)

- (32) Shapiro, A., Xu, H.: Stochastic mathematical programs with equilibrium constraints, modelling and sample average approximation. Optimization 57, 395–418 (2008)

- (33) Su, C.L., Judd, K.L.: Constrained optimization approaches to estimation of structural models. Econometrica 80, 2213–2230 (2012)

- (34) Villani, C.: Topics in Optimal Transportation. American Mathematical Soc. (2003)

- (35) Xu, H., Jane, Y.: Approximating stationary points of stochastic mathematical programs with equilibrium constraints via sample averaging. Set-Valued Var. Anal. 19, 283–309 (2011)

- (36) Xu, Y., Yin, W.: A block coordinate descent method for regularized multiconvex optimization with applications to nonnegative tensor factorization and completion. SIAM J. Imaging Sci. 6, 1758–1789 (2013)

- (37) Ye, J., Zhu, D., Zhu, Q.J.: Exact penalization and necessary optimality conditions for generalized bilevel programming problems. SIAM J. Optim. 7, 481–507 (1997)

- (38) Ye, Y.: On affine scaling algorithms for nonconvex quadratic programming. Math. Program. 56, 285–300 (1992)