Rolling Horizon Policies in Multistage Stochastic Programming

Abstract

Multistage Stochastic Programming (MSP) is a class of models for sequential decision-making under uncertainty. MSP problems are known for their computational intractability due to the sequential nature of the decision-making structure and the uncertainty in the problem data due to the so-called curse of dimensionality. A common approach to tackle MSP problems with a large number of stages is a rolling-horizon (RH) procedure, where one solves a sequence of MSP problems with a smaller number of stages. This leads to a delicate issue of how many stages to include in the smaller problems used in the RH procedure. This paper addresses this question for, both, finite and infinite horizon MSP problems. For the infinite horizon case with discounted costs, we derive a bound which can be used to prescribe an sufficient number of stages. For the finite horizon case, we propose a heuristic approach from the perspective of approximate dynamic programming to provide a sufficient number of stages for each roll in the RH procedure. Our numerical experiments on a hydrothermal power generation planning problem show the effectiveness of the proposed approaches.

Keywords Multistage stochastic programming Rolling-horizon Stochastic dual dynamic programming Approximate dynamic programming

1 Introduction

Multistage Stochastic Programming (MSP) is a class of decision-making models where the decision-maker (DM) may adapt and control the behavior of a probabilistic system sequentially over multiple stages. The goal of the DM is to choose a decision policy that leads to optimal system performance with respect to some performance criterion, e.g., maximizing the expected profit or minimizing the expected cost. MSP models have many real-life applications; these include (but not limited to) energy [1, 2, 3, 4, 5, 6], finance [7, 8, 9, 10], transportation [11, 12, 13] and sports [14], among others.

Two main challenges arise from solving MSP problems: (i) the uncertainty in the problem data; and (ii) the nested form in the sequential decision-making structure of the problem. A typical approach to tackle these challenges is to approximate the underlying stochastic process using scenario trees to address the former and make use of the dynamic programming principle via the so-called Bellman equations [15] to address the latter. This approach, however, could become quickly impractical – especially, with the increase in the dimensionality of the state variables () of the system, and the number of stages () in the planning horizon. This is known as the curse-of-dimensionality and it gives rise to an exponential growth in computational resources required to solve such large MSP problems under certain optimality guarantees. In this paper, we are concerned with the computational tractability of MSP problems with a large number of stages , including the special case when .

In practice, a typical workaround for the computational intractability of MSP problems with a large number of stages is to solve a sequence of MSP problems in an “online” fashion, each of which has a smaller number of stages. This approach is the so-called rolling horizon (RH) procedure, and the (smaller) number of stages used in each roll of the RH procedure is referred to as the forecast horizon [16, 17]. In this procedure, the DM fixes a forecast horizon with , solves the corresponding -stage problem, implements the decisions only for the current period, rolls forward one period, and repeats the process starting from a new initial state. Nevertheless, because the length of the forecast horizon employed by the RH procedure is typically smaller than the actual planning horizon of the original MSP problem, the resulting decision policy, which is referred to as the look-ahead policy, may not be optimal. It is conceivable that the degree of suboptimality in a look-ahead policy is tied to the choice for the number of stages used in the RH procedure. This leads to a very delicate issue of how to choose a small enough forecast horizon with a tolerable optimality gap, which we refer to as a sufficient forecast horizon (see Definition 1). The goal of this paper is to address the issue of finding in a RH procedure.

In the literature, there is a good deal of work on the RH procedure, aiming to achieve a balance between computational efficiency and the corresponding policy performance. In [18], for instance, instead of solving a sequence of MSPs with small forecast horizons, the authors use a deterministic approximation to the MSP in the RH procedure using the point forecasts of all the exogenous uncertain future information. The authors also provide bounds on the suboptimality of the corresponding solution and [19] extend these bounds to a stochastic RH approximation using what is known as the reference scenarios. [20] use a partial approximation approach which uses the point forecasts of exogenous future information only beyond a certain number of stages until the end of the horizon to truncate the number of stages considered in the MSPs. Another common approach is the so-called stage aggregation, where the DM aggregates all the decisions to be made in multiple stages into a single decision stage (see the discussion in [21]). This approach is used by [22], who introduced the partially adaptive MSP model where stage aggregations only occur after a certain period until the end of the horizon.

Unlike these prior works, we do not consider aggregating any of the future exogenous uncertain information nor the stages. Instead, we consider solving MSP problems with a smaller number of stages and provide a systematic way of detecting a sufficient forecast horizon . We focus on finite/infinite horizon MSP problems where the stochastic process characterizing the data uncertainty is stationary. In the infinite horizon discounted case, given a fixed forecast horizon , we show that the resulting optimality gap associated with the (static) look-ahead policy in terms of the total expected discounted reward/cost can be bounded by a function of the forecast horizon . This function can be used to derive a forecast horizon which achieves a prescribed optimality gap. In the finite horizon case (with no discount), we take an approximate dynamic programming (ADP) [23] perspective and develop a dynamic look-ahead policy where the forecast horizon to use in each roll is chosen dynamically according to the state of the system at that stage.

The rest of this paper is organized as follows. In Section 2, we describe in detail the key components of an MSP model, introduce the necessary mathematical notations, and discuss some basic assumptions and solution approaches. In Section 3 we provide a detailed description of the RH procedure and the main theoretical result for the infinite horizon discounted case. In Section 4 we present the ADP-based heuristic approach for constructing the dynamic look-ahead policy for the finite horizon case. An extensive numerical experiment analysis to the proposed approaches on a multi-period hydro-thermal power generation planning problem is presented in Section 5. Finally, in Section 6, we conclude with some final remarks.

2 Preliminaries on Multistage Stochastic Programming

This section is organized as follows. First, we introduce a generic nested formulation for a finite horizon MSP problem, its dynamic programming (DP) counterpart, and some basic assumptions. Second, we discuss solution methodology based on the DP formulation under these basic assumptions. Finally, we describe a stationary analog for the discounted infinite horizon MSP problems.

2.1 Generic MSP formulations and some basic assumptions

Consider a generic nested formulation for a finite horizon MSP problem as follows:

| (1) |

Here, the initial vector and initial data are assumed to be deterministic, and the exogenous random data is modeled by a stochastic process , where each random vector is associated with a known probability distribution supported on a set . Moreover, we denote the history of the stochastic process up to stage by . The decision variable is also referred to as the pre-decision state, and the state of the system in stage is fully resolved after the realization of the random vector is observed. Here, with .

In its present form, this formulation has two main challenges: (i) the nested optimization posed by the sequential nature in the decision-making structure; and (ii) the (conditional) expectation posed by the stochastic nature of the problem. The first challenge can be addressed by using a DP perspective via the Bellman equations and the computation simplifies dramatically under the following stage-wise independence assumption.

Assumption 1.

(Stage-wise independence) We assume that the stochastic process is stage-wise independent, i.e., is independent of the history of the stochastic process up to time , for , which is given by .

Under this assumption, problem (1) can be written as:

| (2) |

where for : is referred to as the expected cost-to-go function,

| (3) |

and . As for the second challenge, a typical approach is to proceed by means of discretization and/or approximate the (discretized) distribution of by a sample obtained using sampling techniques such as Monte Carlo methods. This is, for instance, the case in which (2) is a sample average approximation (SAA) where the expectation is approximated by a sample average. We refer the reader to [24] for a detailed discussion on this topic. Before we discuss the solution methodology based on the DP formulation (2), it is important to make the following additional assumptions.

Assumption 2.

(Relatively complete recourse) We assume that and .

Assumption 3.

(Boundedness) We assume that the immediate cost function at each stage is bounded, i.e., such that .

Assumption 4.

We consider multistage stochastic linear programs (MSLPs), i.e., in (1) is defined as:

| (4) |

and with for .

2.2 The stochastic dual dynamic programming (SDDP) algorithm

Under Assumption 4, a backward induction argument can be used to show that the expected cost-to-go function is piecewise linear and convex with respect to . Therefore, can be approximated from below by an outer cutting-plane approximation , which can be represented by the maximum of a collection of cutting planes (cuts):

| (5) |

A common approach for assembling these cuts is the SDDP algorithm [25]. Drawing influence from the backward recursion technique developed in DP, the SDDP algorithm alternates between two main steps: (i) a forward simulation (forward pass) which uses the current approximate expected cost-to-go functions to generate a sequence of decisions ; and (ii) a backward recursion (backward pass) to improve the approximation , for . After the forward step, a statistical upper bound for the optimal value of (2) can be computed; and after the backward step, an improved lower bound for the optimal value of (2) is obtained. We summarize the forward and backward steps of the algorithm next and the reader is referred to [25] for a detailed discussion on that topic.

Given the initial (pre-decision) state , the initial realization , and the current approximations of the expected cost-to-go functions , the SDDP algorithm proceeds as follows.

-

•

Forward pass.

-

1.

Initialize a list of candidate solutions , set , , .

-

2.

Solve with as shown in (3), to obtain and then set .

-

3.

If go to Backward pass. Otherwise, let , sample a new realization with probability , set , and go to step 2.

-

1.

-

•

Backward pass.

-

1.

Given , for do the following.

-

2.

For every , solve with as shown in (3). Add a cut weighted by the respective probability to (if violated by ).

-

3.

If the termination criterion is met, STOP and return the expected cost-to-go functions . Otherwise, go to Forward pass and repeat.

-

1.

While the SDDP algorithm has become a popular approach for solving MSP problems, using SDDP (and other similar decomposition schemes) can become impractical with the increase in the dimensionality of the problem. In the literature, there has been some recent advancement on how some of this impracticality can be mitigated by (static/dynamic) scenario reduction and aggregation techniques, see, e.g., [26] and the references therein. Nevertheless, even when using such enhancement techniques, the viability of these approaches could be easily undermined in MSP problems where the number of stages in the planning horizon is large.

2.3 Stationary discounted infinite horizon MSP problems

Consider an infinite horizon MSP problem of the form (1) introduced in [27], where and the stochastic process has a periodic behavior with periods. To simplify the presentation, we will only consider the risk-neutral and stationary case where the number of periods . To that end, we have the following stationarity assumption.

Assumption 5.

(Stationarity) The random vector has the same distribution with support , and functions are identical for all .

Unlike the finite horizon case, where the solvability of the DP formulation (3) is guaranteed by the finiteness of the terminal stage value function, infinite horizon MSP problems require an evaluation of an infinite sequence of costs for every state . As such, it is necessary to establish some notion of finiteness for the expected cost-to-go functions . One common approach for doing this is to introduce a discount factor and find a policy which minimizes the expected total discounted cost, that is,

| (6) |

Note that, since ’s are assumed to follow the same probability distribution for all , we can omit the stage subscript and obtain the following discounted infinite horizon stationary variant of the DP formulation (3):

| (7) |

where and random vector has the same distribution as ’s.

The popularity of these discounted models for infinite horizon MSPs stems from their numerical solvability and their wide range of direct applications in real-life economic problems where the DM accounts for the time value of future costs. This solvability, however, relies on the existence of a unique fixed point solution for function satisfying (7). Such existence can be asserted using the Banach fixed-point theorem. We summarize this result next, and readers are referred to [27] for a detailed discussion. To that end, consider the following:

-

•

: the Banach space of bounded functions , and is equipped with the sup-norm .

-

•

A mapping defined as where

(8)

Proposition 1.

(Contraction mapping) The mapping is a contraction mapping, that is, for every the following inequality holds:

| (9) |

Theorem 1.

[27] Under Assumptions 2, 3 and 5, the following results hold:

-

•

Uniqueness: there exists a unique function satisfying the DP formulation (7).

-

•

Convergence: for any the sequence of functions obtained iteratively by

(10) converges (in the norm ) to .

-

•

Convexity: if set is convex and function is convex in , then function , is also convex.

The uniqueness and convergence assertions of Theorem 1 imply that the unique solution obtained iteratively using (10) is the optimal solution to the DP formulation (7). Moreover, under the convexity assertion, [27] show that is piecewise linear and convex with respect to , and provide an SDDP-type cutting-plane algorithm which gives an optimal policy to the corresponding infinite horizon problem (6). We refer the reader to [27] for the proofs of Proposition 1 and Theorem 1, a detailed description of the SDDP-type algorithm, and further discussions on the topic.

3 An Error Bound for Rolling-horizon Policies in Multistage Stochastic Programming

The RH procedure is a well-known approach to construct online decision policies for sequential decision making. In this section, our goal is to provide an error bound to the suboptimality of the online policy corresponding to the RH procedure for solving the stationary discounted infinite horizon MSP model (7). To that end, let us first discuss the RH procedure and clarify what is meant by an online policy.

3.1 Rolling-horizon procedure: online vs. offline policies

To demonstrate what is meant by an online policy, it might be instructive to revisit and analyze the form of what is considered as an offline policy first. We consider the offline policy provided by the standard implementation of the SDDP algorithm as mentioned in Subsection 2.2. Recall that the final output of the SDDP algorithm is a collection of approximate expected cost-to-go functions . This collection of expected cost-to-go functions is what defines the offline policy provided by the SDDP algorithm. In other words, an offline policy is a policy induced by the approximate value functions obtained via an offline training procedure. The quality of this offline policy can be evaluated by using a set of (out-of-sample) scenarios , with , and .

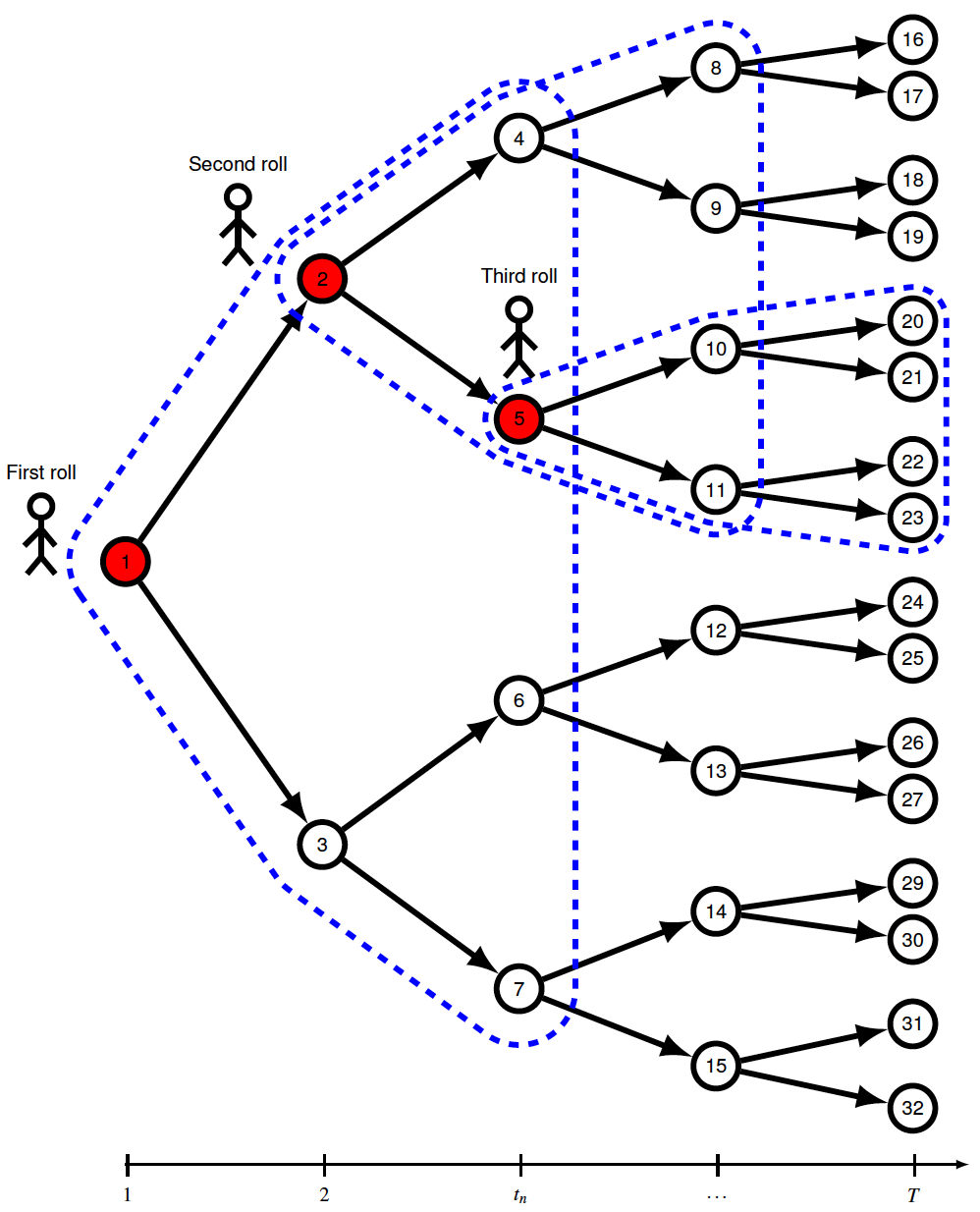

Alternatively, one might consider using an RH procedure where an online policy is given by solving an MSP problem on the fly for decision stage during an out-of-sample evaluation. To demonstrate how the RH procedure works, let us define a roll as the decision stage at which the DM implements their actions. For any trajectory of the stochastic process , at the beginning of every roll , based on the current (pre-decision) state and the observed realization , the DM defines a new MSP problem of the form (1) with being the number of look-ahead stages. The newly defined problem is then solved (e.g., using the SDDP algorithm) and only the first-stage decision is implemented. The DM then pays the immediate cost and moves forward to the next stage. At that stage (), a new problem is defined with state variable being the information carried over from the previous stage, being the observed realization of the stochastic process, and (possibly different from the one used in the previous stage) being the number of look-ahead stages. The online policy is then evaluated by collecting all the immediate costs incurred at every roll in a collection of (out-of-sample) scenarios . A symbolic representation of the RH procedure is depicted in Figure 1 (in the appendix) and an algorithmic description is provided in Algorithm 1.

-

•

Define an MSP problem of the form (3), with , as the initial value, and as the observed realization of the random variable.

-

•

Solve to obtain the optimal decision , and set .

-

•

Update

-

•

Set .

The MSP problem solved at the beginning of every roll, with being the length of the forecast horizon, can be defined in many different ways. We summarize them in the following three categories and the reader is referred to [21] for a detailed discussion. The reader is also referred to [16] for a classified bibliography of the literature on the RH procedure.

-

1.

Limiting the horizon: reduce the number of stages in every roll by assuming that .

-

2.

Stage aggregation: aggregate the stages from in the same spirit as the partially adaptive framework introduced in [22] such that

(11) -

3.

Outcome aggregation: use a point estimator for all the exogenous information from in the same spirit as the framework discussed in [20] such that

(12)

For simplicity, in this paper, we will only consider the first strategy (limiting the horizon). Nevertheless, we expect that similar results in this paper can be extended to the other strategies as well.

3.2 An error bound for RH online policies used for solving stationary infinite horizon discounted models

In this subsection, our goal is to construct an error bound to the suboptimality of the RH procedure when used to solve problem (7). The bound can then be used to derive a sufficient forecast horizon (see Definition 1). Our work is inspired by that of [28] where the authors provide similar ideas for discrete-time Markov control processes. an

To that end, let us first make clear the definition of a sufficient forecast horizon . Let be the sequence of optimal first-stage decisions obtained by an online RH procedure, where is the forecast horizon used in every roll , such that,

| (13) |

is the total expected discounted cost when evaluated using . Similarly, we have that is the minimizer of (6) where

| (14) |

Definition 1.

(-Sufficient forecast horizon ) For , we define a forecast horizon as -sufficient if for all .

Under the contraction mapping assertion of Proposition 1, we have the following lemma.

Lemma 1.

For any and , the value functions obtained iteratively using (10) satisfies .

Proof.

. ∎

Let us define , and suppose we solve (10) recursively for iterations. We claim that provides the same optimal first-stage action obtained by the RH policy . To see why this is the case, note that since , function is equivalent to the terminal stage value function obtained using the policy . Similarly, since is the minimizer of , we have that is equivalent to . We can then use the same argument by doing backward induction to show the equivalence between and for . This concludes that for a given initial state values and , function is equivalent to the optimal first stage solution of problem (2). Moreover, the minimizer given by

| (15) |

is also a minimizer of (2) for a given and .

Theorem 2.

Proof.

-

(a)

Since is the minimizer of (15), we have that

(16) Moreover, since , we have that

By letting , we get that

Therefore,

-

(b)

Let us define another (immediate) cost function . Since this newly defined function , the result follows from (a) (by redefining ).

∎

Theorem 2 provides a bound on the total expected discounted cost obtained by using the RH procedure as a function of the length of the forecast horizon . This bound can be used to obtain the following formula for an -sufficient forecast horizon

| (17) |

which guarantees that, for all , the suboptimality of the respective policy is within an optimality gap of . Note that, similar bounds can also be constructed for the situation where the number of periods . However, since the mapping is going to be defined for all the stages within a period , the bound will scale by a factor for every increment in the forecast horizon .

While Theorem 2 does provide a cue on how to choose the number of look-ahead stages in the RH policies to perform in MSP problems, the formula for an -sufficient forecast horizon provided in (17) indicates that could grow quickly as gets bigger and/or gets smaller. From a computational perspective, this is somewhat pathological and defeats the purpose of using an RH procedure – now that constructing a policy with a relatively small and large entails solving a sequence of MSP problems, each with a significantly large horizon . Another concern with this bound is that its dependency on the original MSP problem is only through the (constant valued) upper bound on the immediate cost function . This makes the choice of the employed -sufficient forecast horizon to be static, losing the opportunity to exploit the system state related information. In Section 4, we exactly address these concerns by constructing a dynamic policy which maps the state of the system to a sufficient forecast horizon . To that end, henceforth, we will introduce a subscript to distinguish between the static forecast horizon and the dynamic forecast horizon which is time dependant (via the state ).

4 An Approximate Dynamic Programming Approach for Dynamic Look-ahead Policies

In this section, we propose a solution approach for constructing a dynamic RH look-ahead policy from an ADP perspective. Although novel in stochastic programming, similar ideas to our proposed dynamic look-ahead policy have been discussed in the MDP literature. For instance, [29] construct a dynamic look-ahead policy for the infinite horizon discounted MDP as follows. First, the authors show the existence of a finite sufficient forecast horizon for any given system state. Second, they identify the optimal first-stage decision which corresponds to this . Finally, they propose an optimality criterion to this , and then use this result to provide a procedure for detecting the smallest such that .

The high-level idea of the procedure described in [29] for detecting is to go through every possible system state and increase the length of the forecast horizon one stage at a time until is identified. To do this, for each step, the algorithm loops over every feasible action, and solves a DP problem, where all actions which do not satisfy the (predetermined) optimality criterion for are eliminated. This process is repeated until the finite action space is reduced to a single element, in which case the corresponding forecast horizon is considered sufficient. Similar procedures have also been discussed in [17] for a more general class of MDPs.

Showing the existence of and finding the corresponding are somewhat readily accessible for the MDP setting because of the finiteness assumptions on the state/action space. While it seems challenging to extend this procedure in MSP problems with continuous state/action space, we expect that this idea and its featured theoretical results are extendable to MSP problems with pure discrete variables. However, even if such extensions are possible, since this procedure solves a DP for every state, action, and , the computation might scale poorly with the size of the state and action space. Instead, we propose a more practical approach next.

4.1 An approximate dynamic programming approach

Ultimately, our goal is to construct a function which maps every state at the beginning of every roll to the smallest sufficient forecast horizon . As previously noted, when using the RH procedure, at the beginning of every roll , the DM solves an MSP problem with a given forecast horizon, implements the first-stage only, and repeats this process at the next roll . As such, if the inclusion of additional stages in the forecast horizon (i.e., using stages instead of ) does not influence the first-stage decision (i.e., remains the same for all ) then can be viewed sufficient for this roll . The main idea of our proposed approach is to train the dependency of a “small and sufficient” forecast horizon on the state using an offline training procedure. Specifically, we consider a regression model by treating the system states as the independent variables and treating the corresponding smallest sufficient forecast horizon as the dependent variables in the regression. First, we generate a random sample of the system states . Then, for each sample , we solve an MSP problem using different forecast horizons , and we record the smallest forecast horizon for which the optimal first-stage solution “converges”, i.e., it remains the same for all . To practically determine whether or not will remain the same for all we use the following stability test: we increase the length of the forecast horizon one step at a time, and we keep track of the optimal first-stage solution for every . Then, whenever for some user-specified tolerance parameter and stability parameter , we conclude that . Once all the data points has been collected, we use a real-valued function to fit these points. To do this, we define a set of basis functions , and look for in the finite dimensional space spanned by these functions. In other words, we look for in the form of the following linear combination:

| (18) |

and fit a regression model to find the parameters . We note that to find a good design of the basis functions, one needs to take advantage of specific problem structures. Given and the form of the basis functions, one can obtain the forecast horizon to consider for each state encountered online during the RH procedure. This approach is summarized in Algorithm 2.

-

•

while true do

-

(a)

Given as an input, solve an MSP problem of the form (3) with to obtain the optimal (first-stage) action and append to .

-

(b)

If go to (c). Otherwise, go to (d).

-

(c)

If , set and stop. Else, go to (d).

-

(d)

If , let and go to (a). Else, set and stop.

-

(a)

Next, we illustrate the proposed approach on a class of hydrothermal energy planning problems, which are used as the benchmark instances in our numerical experiments shown in Section 5.

4.2 An illustrating example: the hydrothermal power operation planning problem

The hydrothermal power generation system is one of the main energy sources in many countries. For example, the Brazilian hydrothermal power system is a large scale network of facilities that can be used to produce and distribute energy by circulating H2O fluids (water). The power plants in the Brazilian network can be categorized into two types:

-

1.

A set of hydro plants , which has no production cost, but for each hydro plant there is an upper limit , which is the maximum allowed amount of turbined flow that can be used for power generation. These hydro plants can also be categorized further into two types:

-

(a)

Hydro plants with reservoirs , and for each there is an upper and lower limit on the level of water allowed in the reservoirs, denoted by and , respectively.

-

(b)

Hydro plants without reservoirs (run-of-river) , and thus no water storage is possible.

Moreover, for each hydro plant , a unit of released water will generate units of power, also known as efficiency rate. The set of immediate upper and lower stream plants for hydro plant in the network is given by and , respectively.

-

(a)

-

2.

A set of thermal plants , where for each thermal plant , the minimum and maximum amount of power generation allowed is and , respectively, . Additionally, each plant is associated with an operating cost of for each unit of thermal power generated. We denote the cost vector of generating thermal power at time by .

In the hydrothermal power operation planning problem (HPOP) problem, the goal of the DM is to find an operation strategy , in order to meet production targets (demands) for each decision stage , while minimizing the overall production cost. To do this, at each decision stage and given the state of the system (i.e., the water level at each hydro plant ), the DM has to decide on how much water to turbine by each hydro plant and how much thermal power to generate by each plant . In the event where the levels of energy production using hydro/thermal plants does not meet the levels of demand, the DM must pay a penalty of for each unit of unsatisfied demand. Such penalty can also be thought of as a cost of buying energy from the outside market, which typically has a higher cost compared to the cost of generating energy using internal resources (thermal plants), i.e., .

The HPOP problem can be modeled as an MSP problem because of the uncertainty in the problem data, such as future inflows (amount of rainfall) , demand , fuel costs and equipment availability [30]. We will use the notation whenever the parameter is deterministic (e.g., stage ) and whenever it is random. To introduce a mathematical programming formulation for the decision problem which the DM has to solve at every decision stage , for , consider the following decision variables:

-

•

: where is the amount of water stored at each hydro plant with a reservoir .

-

•

: where is the amount of water turbined by each hydro plant .

-

•

: where is the amount of thermal power generated by each thermal plant .

-

•

: where is the amount of spilled/pumped-back water (without generating power) in hydro plant

-

•

: the amount of unsatisfied demand at stage .

See Table 8 in the appendix for a summary of all the notations used in the HPOP problem. The local optimization problem at every decision stage , for is defined as follows:

| (19a) | ||||

| s.t. | (19b) | |||

| (19c) | ||||

| (19d) | ||||

| (19e) | ||||

| (19f) | ||||

| (19g) | ||||

| (19h) | ||||

Constraints (19b) describe the flow balance in the system, which gives the (post-decision) water level stored in a reservoir at the end of stage . Constraints (19c) describe the system dynamics in the run-of-river and it is similar to the first set except that the state variables representing the water level in the reservoirs are excluded. Constraint (19d) models the demand requirement. Constraints (19e) to constraints (19g) are the capacity constraints for the reservoirs, the amount of water that can be turbined, and the thermal power generation, respectively. Note that in this context, the system state is given by for a hydro plant with a reservoir and for each run-of-river hydro plant .

In our implementation, to construct the mapping from the system state to a sufficient forecast horizon for this HPOP problem, we consider a piecewise linear function where each piece is given by (18) with . The basis functions for each piece are defined as: (following the ADP literature for numerical stability, see, e.g., [31]) and . In other words, we define as the total amount of electricity that can be generated by all the hydro plants given their current levels of water in the reservoir. As such, performing the regression now reduces to estimating parameters and for each piece of the piecewise linear function through an offline training procedure.

5 Numerical Experiments

In this section, we present our computational results on the empirical performance of different RH policies. In Section 5.1 we provide an overview of the implementation details of the different RH policies used in our numerical experiments. We then describe the test instances in Section 5.2. Afterwards, we compare the performance of various approaches considered in the experiment in Section 5.3. Finally, we present some sensitivity analysis on some key parameters used in the proposed algorithms in Section 5.4.

5.1 Implementation details

We implemented two different policies for choosing the forecast horizon in the RH procedure: a static policy where the forecast horizon is kept the same in each roll, and a dynamic policy where the forecast horizon is dynamically chosen based on the system state according to the regression model trained offline as described in Algorithm 2. To train this function, we use a sample size of , a tolerance parameter , a stalling parameter , and a maximum forecast horizon (we chose as the maximum forecast horizon due to limited computational budget and the observation that the policy performance does not improve significantly beyond that). We refer to this procedure as the offline training step. We then evaluate both the static and the dynamic RH policies on a sample path with stages as the out-of-sample evaluation. We refer to this step as the online evaluation step. To measure the performance of each policy, we calculate the long-run average cost which is given by

| (20) |

It might seem computationally prohibitive to consider evaluating the out-of-sample performance on a sample path of stages for different policies to choose the number of look-ahead stages in each roll, static or dynamic. However, the situation simplifies dramatically under our stationarity assumption (see Assumption 5) where the expected cost-to-go functions for the MSPs defined in every roll are identical for any fixed length of the forecast horizon. In this case, one can then reuse the approximate value function obtained in previous rolls in the current roll as an initial approximate value function, instead of redefining a new MSP problem and training the value function starting from scratch. Since the problems solved in previous rolls were solved under initial states that may not be necessarily the same as the one observed in the current roll, the approximate value function inherited from previous rolls might not be a good enough approximation under the new initial state in the current roll, and therefore need to be evaluated and trained further if necessary. Note that an algorithmic procedure similar to that described in Algorithm 1 can be employed here. The only difference is that, as we move forward over time, we do not dispose of the cuts generated in previous rolls. Instead, we carry them over to the next roll and then resolve the problem under the new initial state (if needed). This idea of “reusing” the approximate value functions has appeared in the literature (see, e.g., [32]).

We care to remark the following subtle distinction between reusing the approximate value functions in the static policy vs. dynamic policy for choosing the number of look-ahead stages in the RH procedure. In the static policy, a single MSP problem is defined and the same approximate value functions in every stage are simply reused over the course of the entire procedure. Whereas in the dynamic policy, we keep track of multiple MSP problems (and the associated approximate value functions) one for each forecast horizon . If the forecast horizon given by at the beginning of every roll has been observed before, we reuse the corresponding (previously defined) MSP problem which has the same value. Otherwise, a new MSP problem is defined and is added to the list of MSP problems with the corresponding forecast horizon encountered so far.

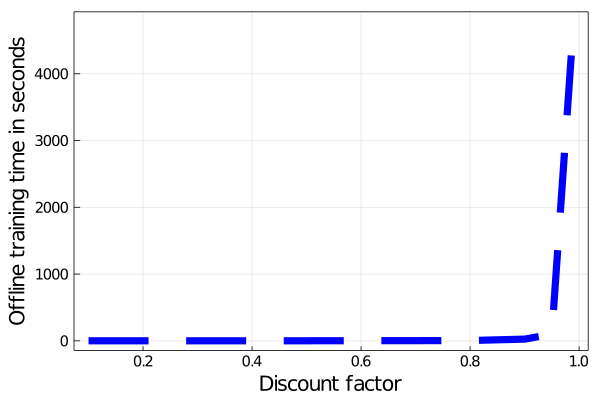

In addition, as previously noted, discount factors have many economical interpretations where the DM accounts for the time value of the costs. One such interpretation is that the future cost is considered less valuable than the current cost. Meaning that, the smaller the discount factor, the less the DM values future costs and vice versa. It is intuitively clear that for each discount factor, there exists a certain length of the look-ahead horizon, both of which represent how the DM values future costs. To show this analogy, we implemented the periodic variant of the SDDP algorithm described in [27] using different values for the discount factor and made a comparison with RH policies.

In summary, we compare the performance of the following policies:

-

1.

A static RH policy that reuses the cuts generated during the online evaluation steps with no discount factor.

-

2.

A dynamic RH policy that reuses the cuts generated during the online evaluation steps with no discount factor.

-

3.

A stationary policy trained with a given discount factor using the periodic variant of the SDDP algorithm described in [27].

In all of our experiments, we consider varying the number of sample paths used in each iteration of the SDDP algorithm for solving the MSP problems. However, we observe that using a single sample path per forward/backward step works the best, and thus we use it in all of our experiments. We use the following termination criteria for stopping the SDDP algorithm: (i) a maximum number of iterations is achieved; or (ii) a time limit of 10,800 seconds (three hours) is achieved; or (iii) the lower bound does not progress by more than (in the relative term) in consecutive iterations (i.e., ). We refer to as the “stalling parameter”, which is set to by default. When solving the MSP problems in an RH procedure during the out-of-sample evaluation, we gradually tune down the online training effort by decreasing this parameter to accelerate computation without sacrificing the solution quality by much. The rationale behind this dynamic parameter setting is that, as the online evaluation procedure proceeds, the state space is explored more extensively, implying that the quality of the approximate value functions keeps improving. Therefore, it does not worth the same effort to do online training in later rolls as initial rolls. Specifically, we gradually tune down the online training effort by doing the following:

-

1.

Starting from the second roll (), we set .

-

2.

Then, once all of the realizations of the random data process are encountered in the online evaluation procedure, we set .

-

3.

Finally, if the algorithm keeps getting terminated as soon as the stalling parameter is hit (i.e., right after iterations) for more than 50 consecutive rolls, we turn off the online training by setting .

We remark that all parameters above are chosen in a rather heuristic manner and can be tuned according to specific problem instances to improve the computational performance.

5.2 Test instances

All proposed approaches are tested using benchmark instances motivated by the Brazilian HPOP problem described in Section 4.1. To create a variety of instances, we consider different values for the demand parameter , number of hydro plants in the network , number of realizations and probability distribution of the random process as shown in Table 9 and Table 10 (in the appendix). In these instances, hydro plants that have reservoirs correspond to , and the run-of-river hydro plants are . The problem parameters used in formulation (19) are given in Table 11 (in the appendix). Note that in instances where , we chose the third hydro plant () and in instances where , we chose the second, third and fourth hydro plants. In addition to the hydro plants, we also consider a set of four thermal plants with maximum power generation capacity and cost for each thermal plant as shown in Table 12 (in the appendix). Finally, we use as the penalty parameter for each unit of unsatisfied demand and as the parameter for converting the amount of water flow into the water level in the reservoirs.

All algorithms were implemented in Julia 1.4.0, using JuMP 0.18.4 package [33], with commercial solver Gurobi, version 9.0.0. All of the tests were conducted on Clemson University’s primary high-performance computing cluster, the Palmetto cluster, where we use an R830 Dell Intel Xeon “big memory” compute node with 2.60GHz, 1.0 TB memory, and 24 cores.

5.3 Numerical Results

The first step in our implementation for the dynamic RH policy is the offline training step where we estimate parameters and in each piece (see (18)) of the piecewise linear function. The choice of using a piecewise linear function as the regression function is inspired by our preliminary observations that, in these instances, the relationship between and exhibit a piecewise linear structure with up to three pieces. The best fit results are shown in Table 1.

| Range | |||||||||

| 1 | 1000 | 5 | -6.69 | 66.36% | 88.61% | ||||

| -1.59 | 99.48% | ||||||||

| 5.00 | 0.00 | - | |||||||

| 12 | -14.61 | 80.06% | 93.19% | ||||||

| -1.95 | 99.49% | ||||||||

| 4.00 | 0.00 | - | |||||||

| 1500 | 5 | -10.61 | 63.08% | 85.57% | |||||

| -3.86 | 99.38% | ||||||||

| -0.81 | 94.24% | ||||||||

| 12 | -1.00 | 87.50% | 94.57% | ||||||

| -5.33 | 99.00% | ||||||||

| -0.74 | 97.22% | ||||||||

| 3 | 1750 | 5 | 5.08 | 24.95% | 56.35% | ||||

| -1.32 | 87.74% | ||||||||

| 12 | 0.70 | 77.27% | 84.27% | ||||||

| 1.07 | 91.27% | ||||||||

| 2250 | 5 | 0.49 | 84.52% | 84.52% | |||||

| 12 | 0.76 | 83.87% | 83.87% | ||||||

| 6 | 2000 | 5 | -0.55 | 73.96% | 91.17% | ||||

| -5.40 | 99.53% | ||||||||

| -7.21 | 83.20% | ||||||||

| 12 | 6.19 | 23.27% | 74.22% | ||||||

| -5.85 | 99.38% | ||||||||

| -8.03 | 60.84% | ||||||||

| 2500 | 5 | -6.72 | 90.78% | 90.55% | |||||

| -6.44 | 99.35% | ||||||||

| -13.48 | 81.53% | ||||||||

| 12 | -14.59 | 80.35% | 86.78% | ||||||

| -8.36 | 98.45% | ||||||||

| -5.61 | 81.54% | ||||||||

To measure the quality of the obtained regression functions, we use an aggregated coefficient of determination , which is given by a weighted summation of the values over all pieces representing the function. For example, in the test instance where and , the piecewise linear regression function contains three pieces with an average (the values are , and respectively for each piece), which is almost sixteen times higher than the value when we use a simple linear regression (i.e., with a single piece). Similar improvements in terms of the values can be observed for most instances, except two instances where and , where the coefficients of determinations given by the simple linear regression are already satisfactory.

To analyze the performance of different RH look-ahead policies and the stationary policy, we record the following performance metrics:

-

•

The training time (in seconds): which is recorded online in the case of the RH policies, and offline in the case of the stationary policy obtained by the periodic variant of the SDDP algorithm.

-

•

The long-run average cost: given by (20) which is denoted by in the case of an RH policy with look-ahead stages, and in the case of stationary policy with discount factor .

-

•

The relative gap which is given by in the case of RH policies and is given by . We treat as the “optimal” RH policy as the length of the look-ahead horizon is large enough in the sense that the policy performance does not improve significantly beyond that, according to our computational experiments. We treat as the “optimal” stationary policy as the discount factor of is close enough to .

All of the numerical results for instances where are shown in Table 2 to Table 5. Next, we summarize our main observations.

Time Gap Time Gap Time Gap 5 1 1000 3.65 13365.99 40.38% 1750 3.72 74337.5 110.71% 2000 14.22 47455.92 269.12% 2 5.43 11417.63 19.92% 7.69 52646.73 49.23% 17.06 21520.59 67.39% 4 18.29 10148.72 6.59% 60.51 41181.76 16.73% 131.58 16273.22 26.58% 8 114.5 9724.37 2.13% 509.18 38010.33 7.74% 1524.64 14342.81 11.56% 16 693.13 9546.52 0.27% 2020.42 36264.1 2.79% 6194.63 13385.28 4.11% 32 2305.26 9534.69 0.14% 5641.59 35415.53 0.38% 15972.43 12956.27 0.78% 64 6462.9 9521.29 - 13567.29 35279.98 - 34677.73 12856.51 - dynamic 333.99 9576.75 0.58% 661.78 37755.31 7.02% 2584.86 13199.63 2.67% 12 1 3.71 11613.72 42.33% 11.02 87358.81 96.39% 14.14 40188.54 235.38% 2 9.24 10167.24 24.60% 12.75 60440.18 35.88% 32.05 19429.49 62.14% 4 39.78 8958.41 9.79% 257.2 51222.79 15.16% 421.47 14799.7 23.51% 8 326.72 8440.7 3.44% 1891.9 47664.75 7.16% 3368.73 13268.63 10.73% 16 1816.15 8221.67 0.76% 5216.76 45670.92 2.67% 9991.14 12431.27 3.74% 32 5566.49 8165.87 0.08% 12876.73 44659.88 0.40% 24691.71 12068.17 0.71% 64 15372.1 8159.69 - 32105.21 44481.48 - 59671.12 11982.87 - dynamic 1809.69 8314.8 1.90% 715.67 48737.93 9.57% 4816.96 12387.48 3.38% 5 1 1500 3.64 65637.12 62.16% 2250 3.72 222334.09 19.82% 2250 14.93 93311.6 274.95% 2 5.52 51512.1 27.26% 7.22 194007.97 4.55% 19.1 44648.11 79.41% 4 24.36 44917.91 10.97% 40.67 187064.07 0.81% 140.71 32492.63 30.56% 8 164.29 42523.65 5.05% 278.58 185591.37 0.02% 1441.57 28113.77 12.97% 16 731.55 41178.16 1.73% 931.33 185404.47 -0.08% 5428.05 26128.32 4.99% 32 2413.37 40540.81 0.16% 2165.64 185404.47 -0.08% 14387.64 25113.81 0.91% 64 6947.46 40477.72 - 2752.87 185560.35 - 32775.48 24886.25 - dynamic 497.22 41195.23 1.77% 38.36 186375.7 0.44% 1928.97 27090.02 8.86% 12 1 3.75 58454.13 56.89% 3.7 246632.4 6.41% 14.16 83937.73 259.96% 2 9.43 45440.69 21.96% 12.32 231867.49 0.04% 31.81 40306.08 72.85% 4 58.07 40601.52 8.97% 64.43 231628.54 -0.06% 473.26 29854.98 28.03% 8 422.79 38515.49 3.37% 247.52 231628.54 -0.06% 3205 26178.52 12.27% 16 1891.91 37602.58 0.92% 418.06 231628.54 -0.06% 10452.26 24357.1 4.45% 32 5301.44 37267.23 0.02% 891.85 231764.99 0.00% 26822.58 23508.5 0.81% 64 13494.45 37259.01 - 1050.57 231764.99 - 65099.79 23318.46 0.00% dynamic 962.55 37716.6 1.23% 40.95 231628.54 -0.06% 4672.58 25418.94 9.01%

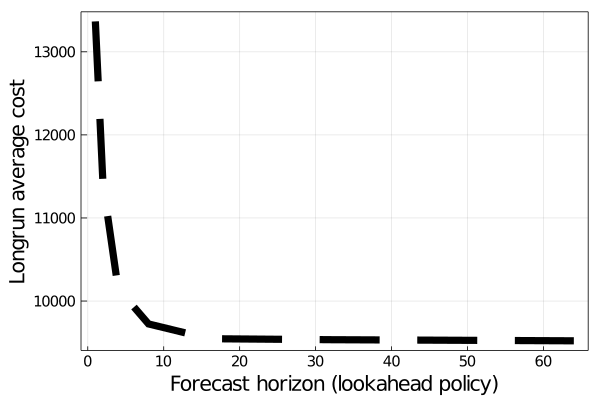

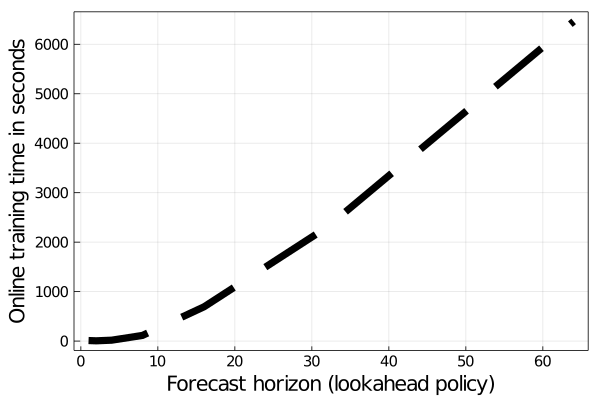

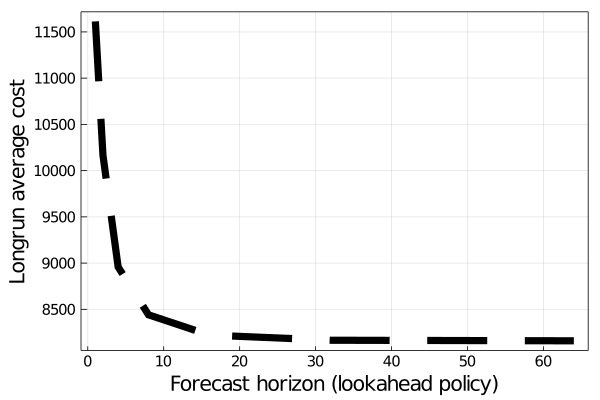

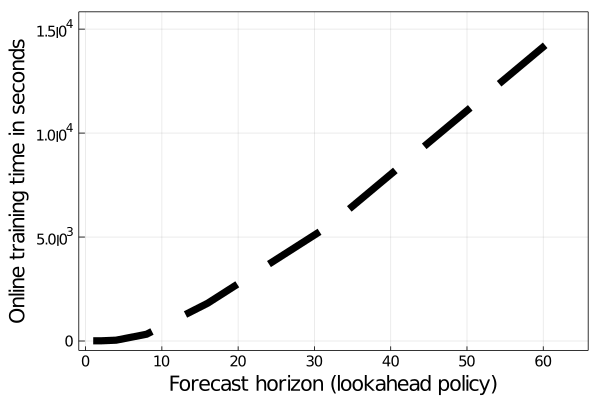

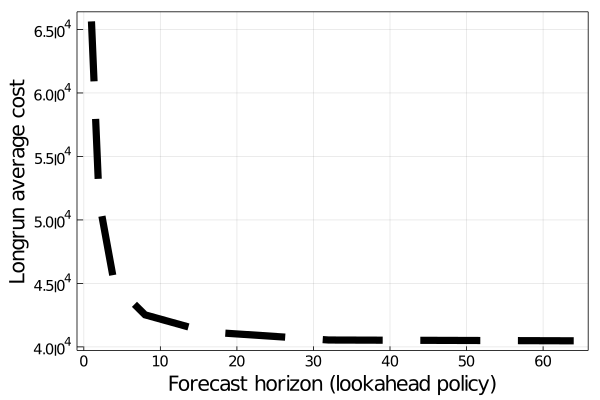

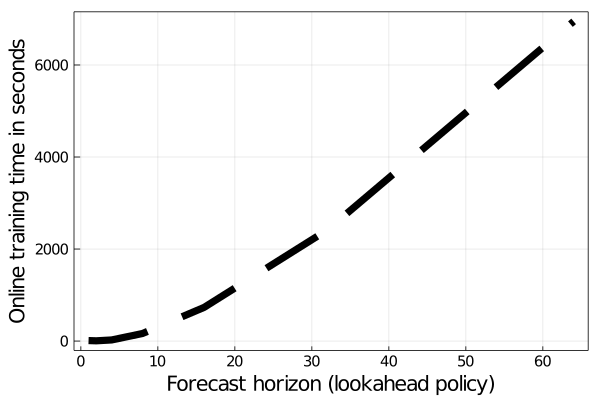

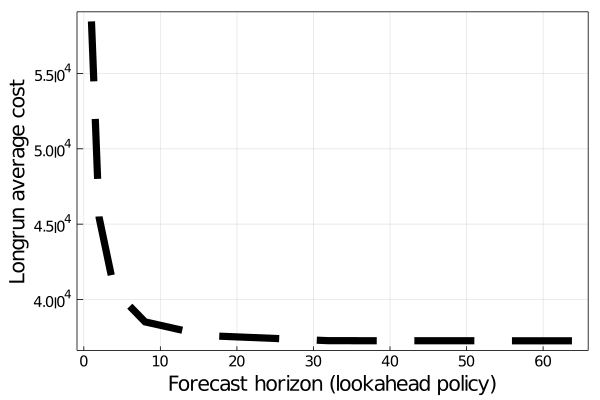

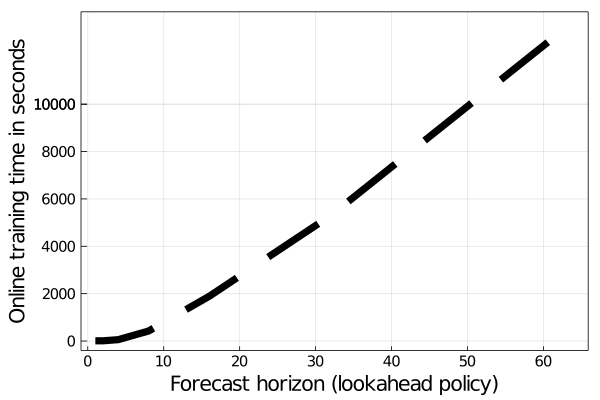

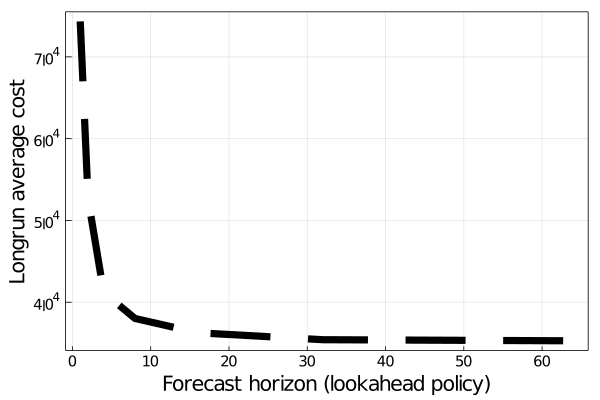

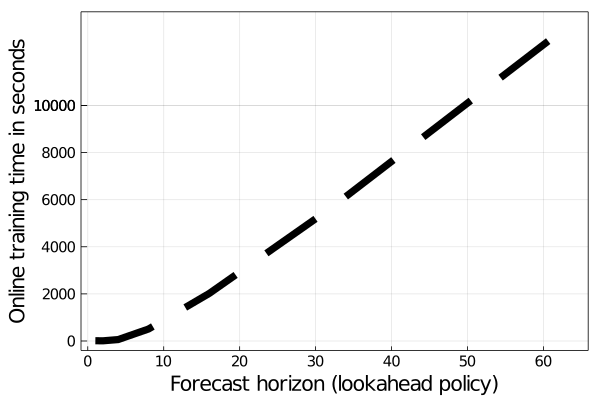

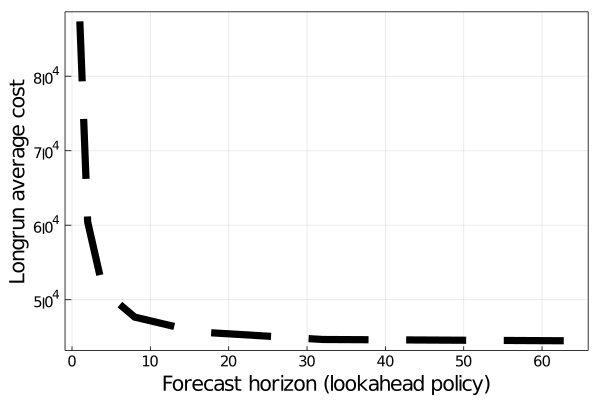

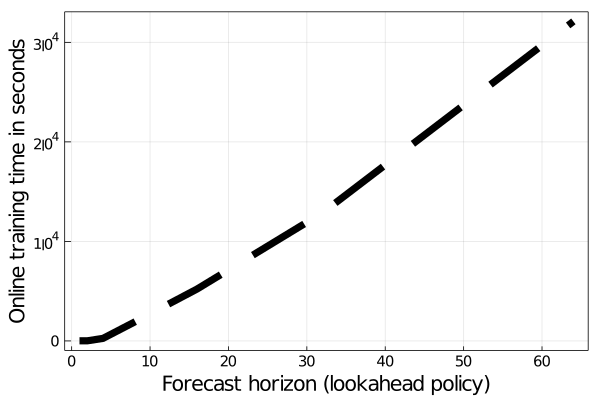

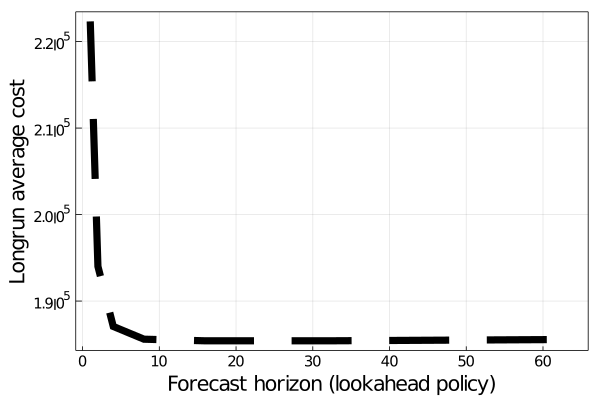

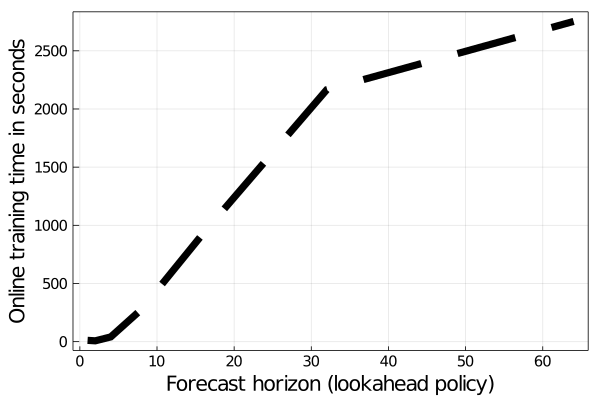

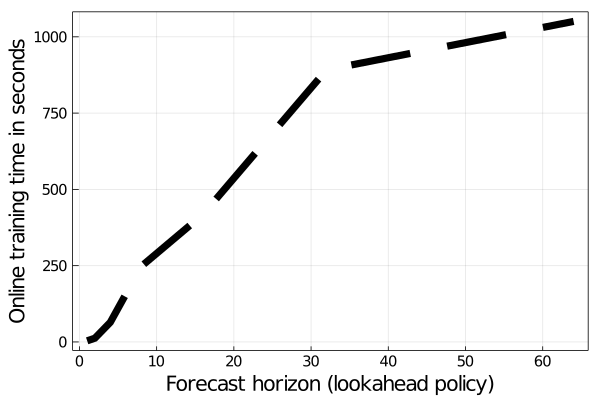

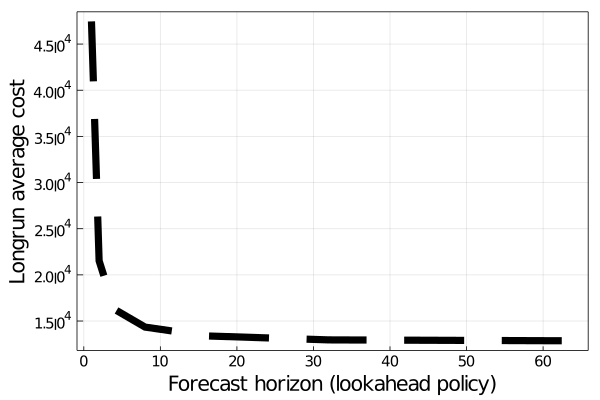

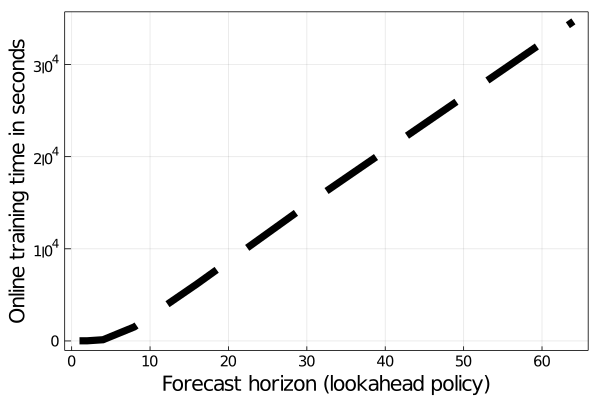

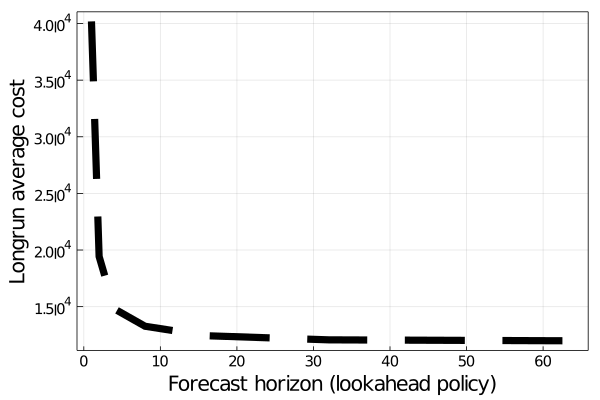

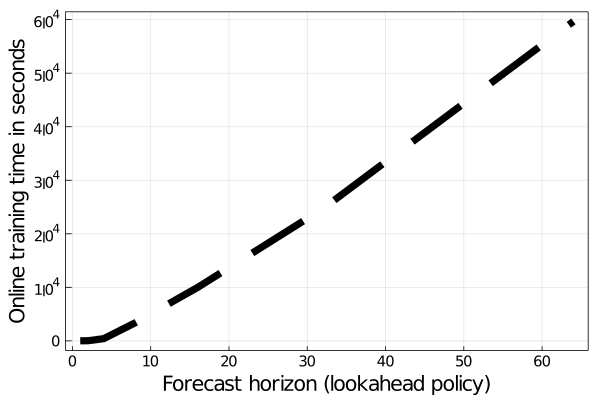

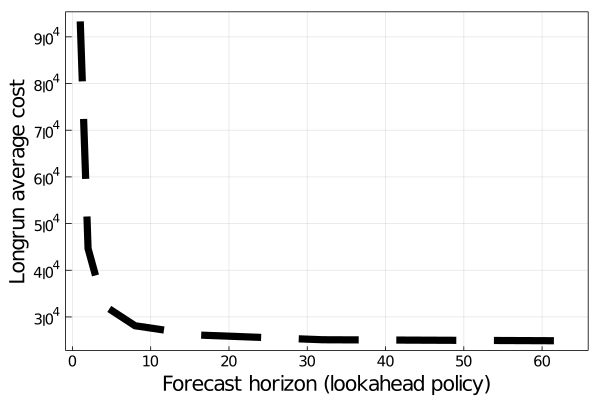

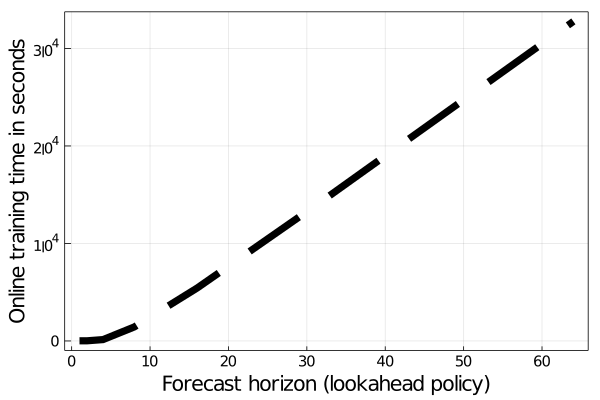

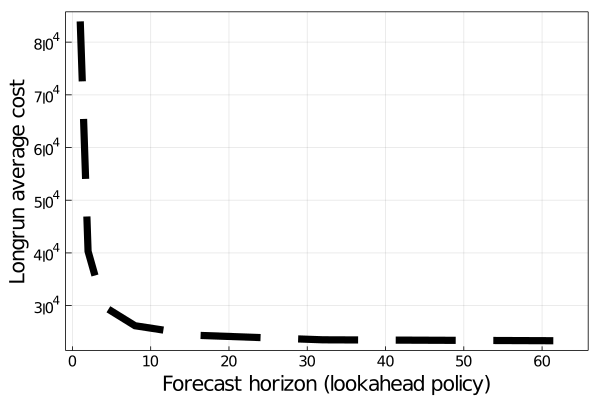

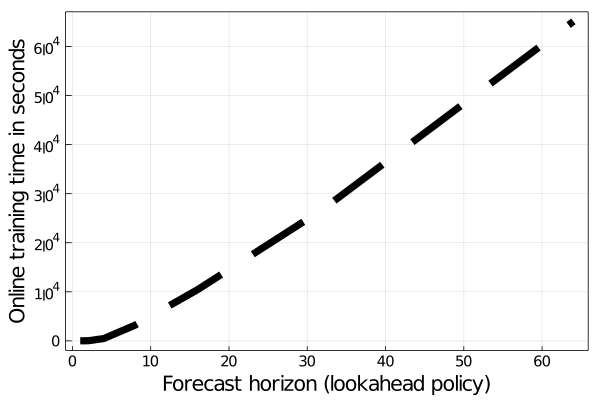

5.3.1 The plateauing effect and exponential growth in computational time.

The first observation is that in static RH policies, across different instances, the long-run average cost plateaus after a certain length of forecast horizon . In other words, the decrease in as increases becomes hardly noticeable after . This behavior can be observed in Figure 2 to Figure 4 in the appendix. Across all of the instances, this plateauing behavior seems to take place somewhere between where is around , , and larger than on average, for instances where , and , respectively. On the other hand, we can see that static RH policies with require, on average, a computational time of 770.13 seconds, 1439.22 seconds, and 8016.52 seconds for instances where , and , respectively. Comparing these to the static RH policy with , we can see that on average, it requires a computational time of 10569.23 seconds, 12368.98 seconds, and 42374.78 seconds for instances where , and , respectively. This means that for a , and reduction in the optimality gap, using a static RH policy with instead of would require a , and increase in the computational time, on average, for instances where , and , respectively.

5.3.2 Static vs. dynamic RH policies.

Overall, across all of the instances, the dynamic RH policy performs quite well compared to the benchmark static RH policy with . At its worst, the is larger than , which happens in the instance where (, ), followed by the instance where (, ) and (, ), where the corresponding is and larger than , respectively. It is interesting to see that these three instances also happen to be the ones with the least accurate regression fit according to the (aggregated) coefficient of determination as shown in Table 1. Nevertheless, apart from these three instances, on average, is only around larger than in the instances where , larger in the remaining instances where , and larger in the remaining instances where . Comparing these gaps to the computational time required to compute the static RH policy with , we can see from Table 2 that for a , , and reduction in the optimality gap, it would require , , and increase in the computational time, for the instances where , and , respectively.

Moreover, given the monotonicity of as increases, it might be instructive to explore where the dynamic policy ranks (in terms of its performance) compared to static RH policies with various lengths of forecast horizons. In nine out of the twelve instances that we have, the long-run average cost and the computational time by the dynamic policy are both placed between the static RH policies with and . Even in instances where this is not the case – namely, the instances (, ), (, ) and (, ) – the performance of the dynamic RH policy, in terms of and , places very closely to policies with in the case of the two instances with and very closely to policies with in the case of the instance with . This time interval is, as discussed earlier, the same interval at which the plateauing behavior starts to take place. This coincidence, however, is somewhat expected given the fact that our regression functions are constructed precisely so that the corresponding states are mapped to the smallest forecast horizon for which and hence , i.e. when plateaus. This provides a numerical evidence on the validity of our proposed approach.

Finally, another advantage to this dynamic policy over the static policy is its usability. To elaborate on this, it is important to note that when using a static policy, it is not clear how one can identify a sufficient forecast horizon a priori, for which plateaus for all . In our implementation, for instance, we do this by keeping track of and testing the static RH policy with every . In other words, if the DM chooses to use a static policy, then prior to solving the problem he/she does not know what is, and the only way to find out is to solve the actual problem for multiple values of . While the offline training step involved in the estimation of the dynamic policy regression parameter, in some sense, also follows this same enumeration process, it is less expensive from a computational perspective and allows for more flexibility. First, when enumerating the values , we do not have to solve the actual problem for every . Instead, we only need to do this for the first stage problem under different sampled initial states . Moreover, the accuracy of the regression fit can be adapted according to the sample size which depends on the available computational budget. Finally, the DM has the opportunity to study and analyze function prior to solving the actual problem, e.g., he/she has the freedom to construct the regression functions that fit the set of sample initial states and the corresponding responses the best.

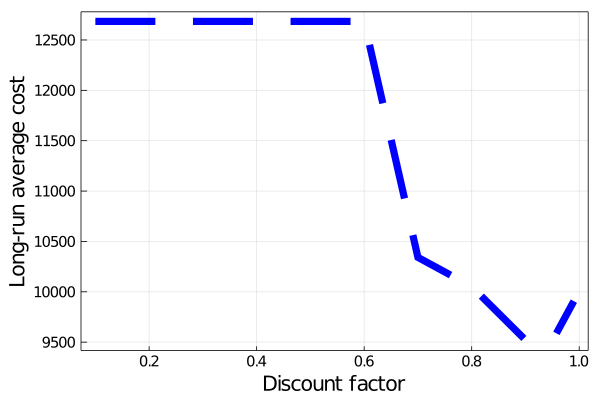

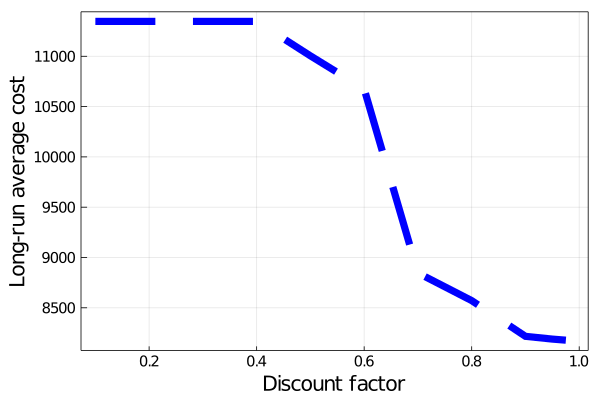

5.3.3 RH policies vs. stationary policy.

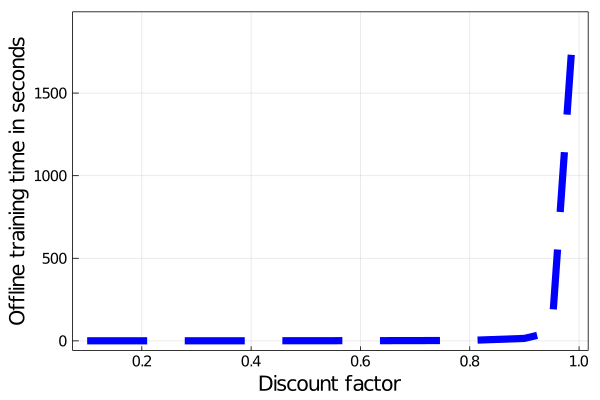

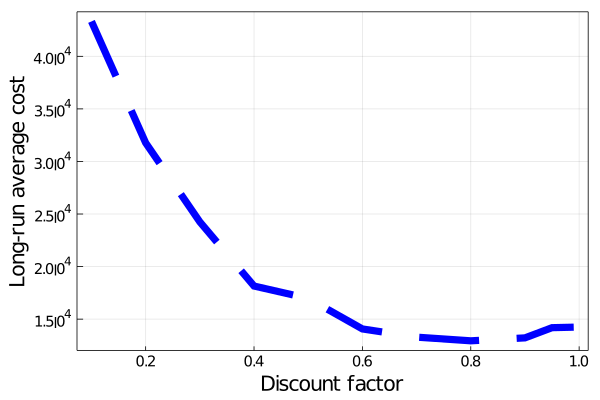

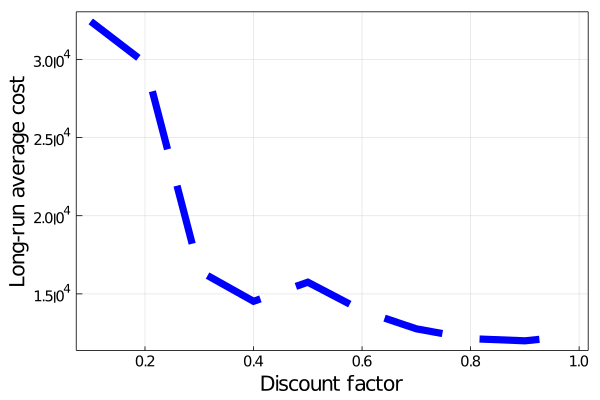

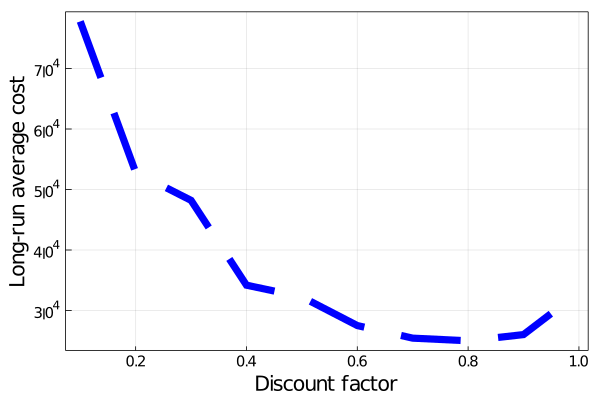

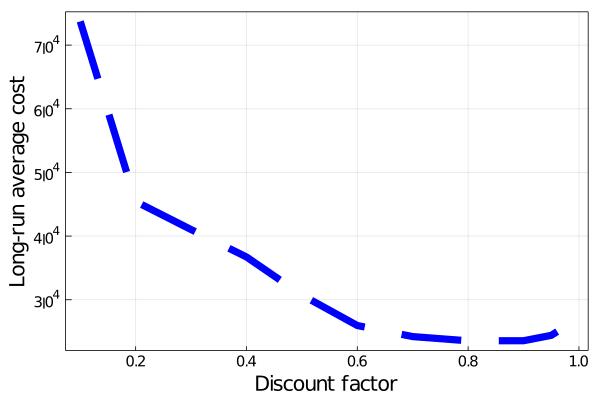

From Table 3 to Table 5, we can see that stationary policy trained with a given discount factor using the periodic variant of the SDDP algorithm performs quite well compared to the RH policies. Specifically, if we pick the policies corresponding to values in every instance and compare them to , we can see that is only around , and larger than on average, for instances where , and , respectively. More importantly, the computational time required in the stationary policy is , , and less, on average, than that of the static RH policies with , for instances where , and , respectively.

| Time | ||||||

|---|---|---|---|---|---|---|

| 1000 | 5 | 0.10 | 0.19 | 12684.41 | 21.90% | 33.22% |

| 0.20 | 0.37 | 12684.41 | 21.90% | 33.22% | ||

| 0.30 | 0.53 | 12684.41 | 21.90% | 33.22% | ||

| 0.40 | 0.64 | 12684.41 | 21.90% | 33.22% | ||

| 0.50 | 0.80 | 12684.41 | 21.90% | 33.22% | ||

| 0.60 | 1.27 | 12684.41 | 21.90% | 33.22% | ||

| 0.70 | 1.62 | 10341.58 | 4.20% | 8.62% | ||

| 0.80 | 2.91 | 10051.84 | 1.44% | 5.57% | ||

| 0.90 | 14.94 | 9521.41 | -4.05% | - | ||

| 0.95 | 54.17 | 9513.41 | -4.14% | - | ||

| 0.99 | 1934.00 | 9906.97 | - | 4.05% | ||

| 12 | 0.10 | 0.21 | 11346.83 | 27.98% | 39.06% | |

| 0.20 | 0.41 | 11346.83 | 27.98% | 39.06% | ||

| 0.30 | 0.58 | 11346.83 | 27.98% | 39.06% | ||

| 0.40 | 0.77 | 11346.83 | 27.98% | 39.06% | ||

| 0.50 | 1.03 | 11004.30 | 25.74% | 34.86% | ||

| 0.60 | 1.72 | 10675.27 | 23.45% | 30.83% | ||

| 0.70 | 2.27 | 8845.99 | 7.62% | 8.41% | ||

| 0.80 | 3.63 | 8571.37 | 4.66% | 5.05% | ||

| 0.90 | 22.39 | 8216.27 | 0.54% | 0.69% | ||

| 0.95 | 97.13 | 8188.86 | - | - | ||

| 0.99 | 5391.60 | 8171.77 | - | - | ||

| 1500 | 5 | 0.10 | 0.23 | 65651.50 | 38.17% | 62.19% |

| 0.20 | 0.46 | 58755.27 | 30.91% | 45.15% | ||

| 0.30 | 0.54 | 58647.44 | 30.78% | 44.89% | ||

| 0.40 | 0.70 | 54744.80 | 25.85% | 35.25% | ||

| 0.50 | 0.69 | 46043.49 | 11.83% | 13.75% | ||

| 0.60 | 1.02 | 43352.34 | 6.36% | 7.10% | ||

| 0.70 | 1.48 | 42521.26 | 4.53% | 5.05% | ||

| 0.80 | 2.39 | 41663.21 | 2.56% | 2.93% | ||

| 0.90 | 12.14 | 40584.36 | - | - | ||

| 0.95 | 47.02 | 40617.51 | - | - | ||

| 0.99 | 2185.29 | 40594.81 | - | - | ||

| 12 | 0.10 | 0.26 | 58461.04 | 36.37% | 56.90% | |

| 0.20 | 0.52 | 58461.04 | 36.37% | 56.90% | ||

| 0.30 | 0.59 | 51964.42 | 28.42% | 39.47% | ||

| 0.40 | 0.86 | 47407.99 | 21.54% | 27.24% | ||

| 0.50 | 0.95 | 45398.62 | 18.07% | 21.85% | ||

| 0.60 | 1.57 | 40330.77 | 7.77% | 8.24% | ||

| 0.70 | 2.03 | 43005.42 | 13.51% | 15.42% | ||

| 0.80 | 2.95 | 37759.45 | 1.49% | 1.34% | ||

| 0.90 | 16.13 | 37305.85 | - | - | ||

| 0.95 | 72.57 | 37269.70 | - | - | ||

| 0.99 | 4651.74 | 37196.90 | - | - |

| Time | ||||||

|---|---|---|---|---|---|---|

| 1750 | 5 | 0.10 | 0.25 | 72329.48 | 48.80% | 105.02% |

| 0.20 | 0.50 | 61305.31 | 39.60% | 73.77% | ||

| 0.30 | 0.56 | 58958.97 | 37.19% | 67.12% | ||

| 0.40 | 0.78 | 45323.61 | 18.30% | 28.47% | ||

| 0.50 | 0.75 | 42397.72 | 12.66% | 20.18% | ||

| 0.60 | 1.15 | 37542.00 | 1.36% | 6.41% | ||

| 0.70 | 1.70 | 36528.44 | -1.37% | 3.54% | ||

| 0.80 | 2.55 | 35771.06 | -3.52% | 1.39% | ||

| 0.90 | 13.38 | 36459.97 | -1.56% | 3.34% | ||

| 0.95 | 43.60 | 37036.00 | - | 4.98% | ||

| 0.99 | 1938.69 | 37029.61 | - | 4.96% | ||

| 12 | 0.10 | 0.27 | 87359.15 | 48.74% | 96.39% | |

| 0.20 | 0.54 | 87359.15 | 48.74% | 96.39% | ||

| 0.30 | 0.67 | 75697.62 | 40.84% | 70.18% | ||

| 0.40 | 0.91 | 75597.00 | 40.76% | 69.95% | ||

| 0.50 | 1.03 | 55065.02 | 18.67% | 23.79% | ||

| 0.60 | 1.65 | 47649.75 | 6.01% | 7.12% | ||

| 0.70 | 2.67 | 47572.81 | 5.86% | 6.95% | ||

| 0.80 | 4.36 | 45281.33 | 1.10% | 1.80% | ||

| 0.90 | 19.38 | 44618.47 | - | - | ||

| 0.95 | 77.11 | 44853.49 | - | 0.84% | ||

| 0.99 | 5021.77 | 44783.72 | - | 0.68% | ||

| 2250 | 5 | 0.10 | 0.23 | 222307.24 | 16.62% | 19.80% |

| 0.20 | 0.47 | 222307.24 | 16.62% | 19.80% | ||

| 0.30 | 0.59 | 209145.23 | 11.38% | 12.71% | ||

| 0.40 | 0.79 | 208001.60 | 10.89% | 12.09% | ||

| 0.50 | 0.86 | 190872.27 | 2.89% | 2.86% | ||

| 0.60 | 1.41 | 187446.56 | 1.12% | 1.02% | ||

| 0.70 | 2.39 | 186434.33 | 0.58% | - | ||

| 0.80 | 3.58 | 185552.76 | - | - | ||

| 0.90 | 15.25 | 185434.50 | - | - | ||

| 0.95 | 55.98 | 185467.83 | - | - | ||

| 0.99 | 1985.85 | 185351.59 | - | - | ||

| 12 | 0.10 | 0.26 | 246633.48 | 6.09% | 6.42% | |

| 0.20 | 0.53 | 246633.48 | 6.09% | 6.42% | ||

| 0.30 | 0.67 | 244842.70 | 5.41% | 5.64% | ||

| 0.40 | 0.84 | 244842.70 | 5.41% | 5.64% | ||

| 0.50 | 1.06 | 231806.51 | - | - | ||

| 0.60 | 1.88 | 231710.85 | - | - | ||

| 0.70 | 3.25 | 231691.90 | - | - | ||

| 0.80 | 5.45 | 231691.90 | - | - | ||

| 0.90 | 26.18 | 231690.23 | - | - | ||

| 0.95 | 100.28 | 231691.90 | - | - | ||

| 0.99 | 4337.70 | 231602.68 | - | - |

| Time | ||||||

|---|---|---|---|---|---|---|

| 2000 | 5 | 0.10 | 0.34 | 43322.32 | 67.14% | 236.97% |

| 0.20 | 0.68 | 31772.28 | 55.19% | 147.13% | ||

| 0.30 | 0.77 | 24250.31 | 41.30% | 88.62% | ||

| 0.40 | 1.01 | 18149.80 | 21.56% | 41.17% | ||

| 0.50 | 0.98 | 16971.14 | 16.12% | 32.00% | ||

| 0.60 | 1.51 | 14068.05 | -1.19% | 9.42% | ||

| 0.70 | 1.97 | 13288.72 | -7.13% | 3.36% | ||

| 0.80 | 3.25 | 12938.78 | -10.02% | 0.64% | ||

| 0.90 | 16.13 | 13218.13 | -7.70% | 2.81% | ||

| 0.95 | 60.61 | 14188.20 | - | 10.36% | ||

| 0.99 | 2405.77 | 14235.84 | - | 10.73% | ||

| 12 | 0.10 | 0.37 | 32429.25 | 62.25% | 170.63% | |

| 0.20 | 0.74 | 29770.94 | 58.88% | 148.45% | ||

| 0.30 | 0.92 | 16466.87 | 25.65% | 37.42% | ||

| 0.40 | 1.12 | 14525.55 | 15.72% | 21.22% | ||

| 0.50 | 1.40 | 15746.90 | 22.25% | 31.41% | ||

| 0.60 | 2.15 | 13932.88 | 12.13% | 16.27% | ||

| 0.70 | 3.25 | 12764.11 | 4.09% | 6.52% | ||

| 0.80 | 4.96 | 12134.38 | -0.89% | 1.26% | ||

| 0.90 | 24.48 | 11997.69 | -2.04% | - | ||

| 0.95 | 97.90 | 12175.00 | -0.55% | 1.60% | ||

| 0.99 | 5250.73 | 12242.54 | - | 2.17% | ||

| 2250 | 5 | 0.10 | 0.40 | 77787.89 | 56.53% | 212.57% |

| 0.20 | 0.80 | 52850.73 | 36.02% | 112.37% | ||

| 0.30 | 0.79 | 48205.23 | 29.86% | 93.70% | ||

| 0.40 | 0.96 | 34184.51 | 1.09% | 37.36% | ||

| 0.50 | 1.09 | 32246.83 | -4.86% | 29.58% | ||

| 0.60 | 1.50 | 27511.85 | -22.90% | 10.55% | ||

| 0.70 | 2.17 | 25430.95 | -32.96% | 2.19% | ||

| 0.80 | 3.27 | 24990.33 | -35.30% | - | ||

| 0.90 | 15.90 | 26020.24 | -29.95% | 4.56% | ||

| 0.95 | 56.71 | 29517.01 | -14.55% | 18.61% | ||

| 0.99 | 1558.71 | 33812.70 | - | 35.87% | ||

| 12 | 0.10 | 0.40 | 73726.60 | 63.92% | 216.17% | |

| 0.20 | 0.79 | 45434.47 | 41.45% | 94.84% | ||

| 0.30 | 0.91 | 41025.18 | 35.16% | 75.93% | ||

| 0.40 | 1.14 | 36716.93 | 27.55% | 57.46% | ||

| 0.50 | 1.34 | 30739.56 | 13.47% | 31.82% | ||

| 0.60 | 1.97 | 25950.83 | -2.50% | 11.29% | ||

| 0.70 | 3.15 | 24211.81 | -9.86% | 3.83% | ||

| 0.80 | 5.02 | 23548.44 | -12.96% | 0.99% | ||

| 0.90 | 25.96 | 23562.13 | -12.89% | 1.04% | ||

| 0.95 | 99.43 | 24407.57 | -8.98% | 4.67% | ||

| 0.99 | 4784.02 | 26599.80 | - | 14.07% |

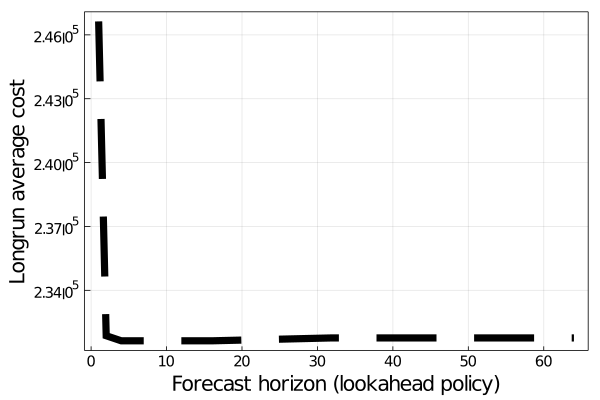

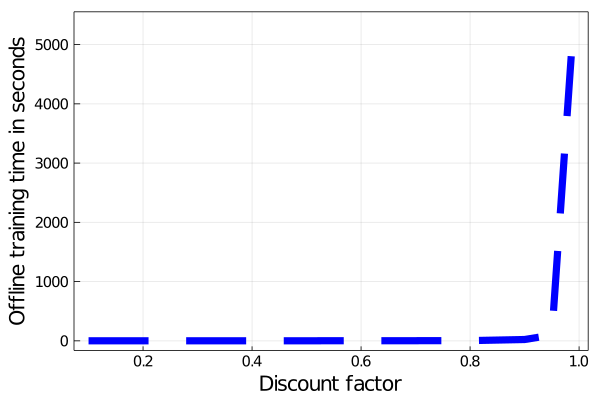

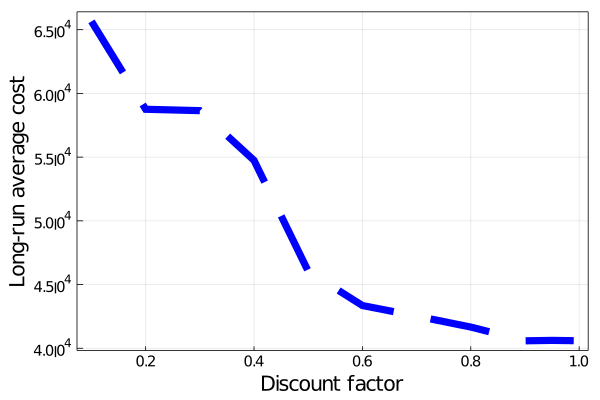

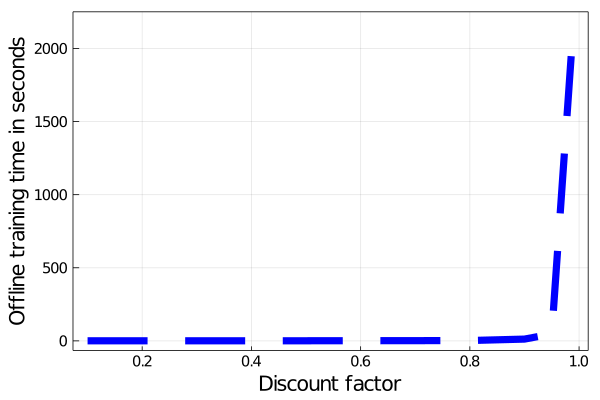

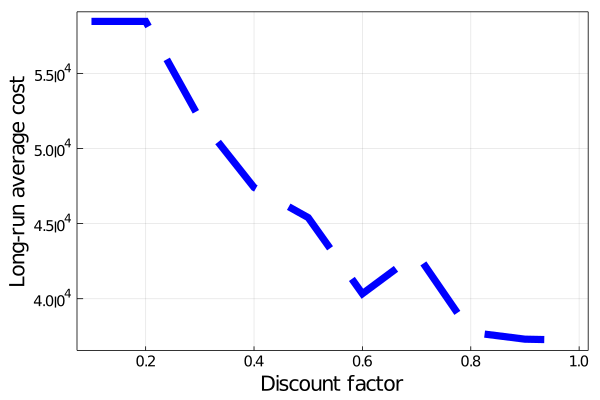

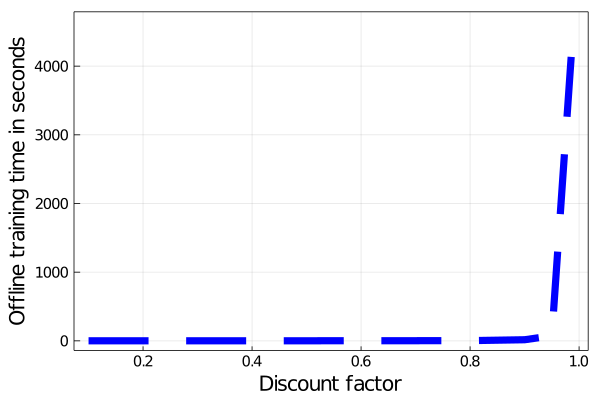

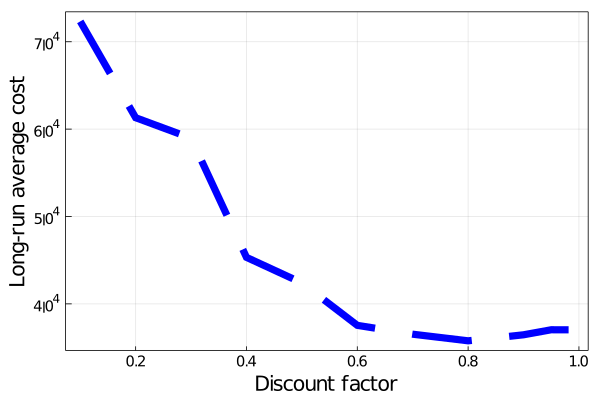

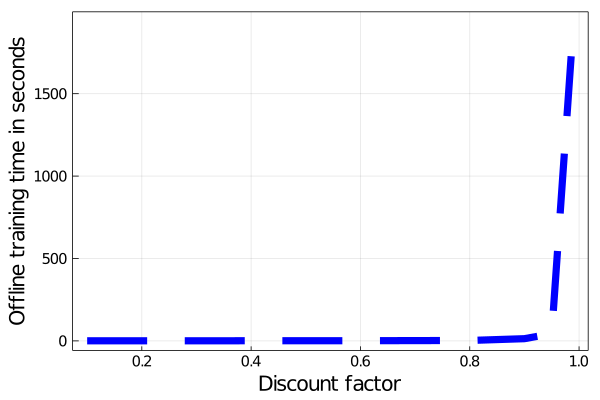

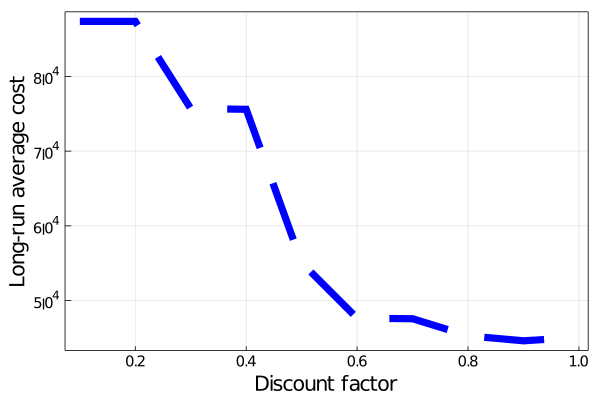

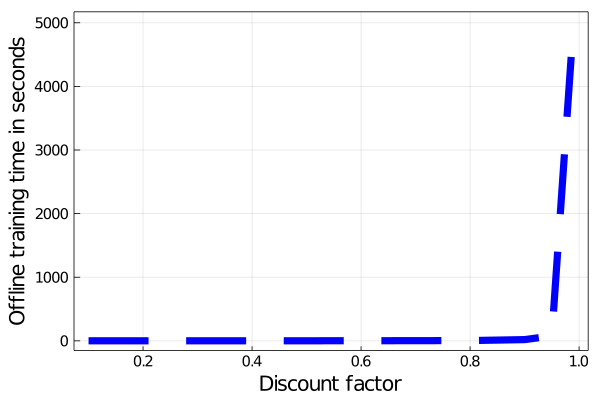

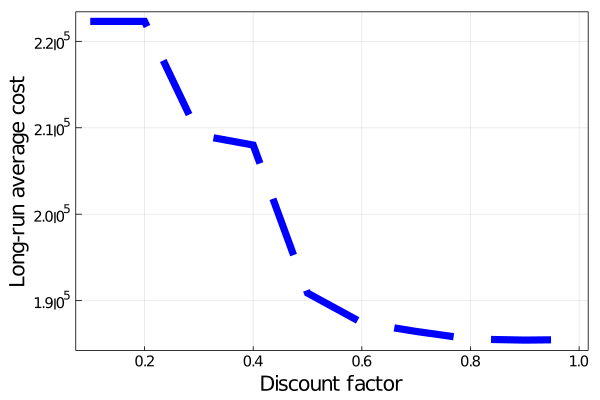

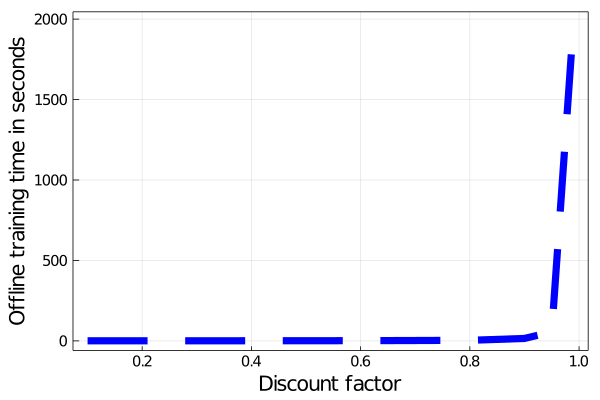

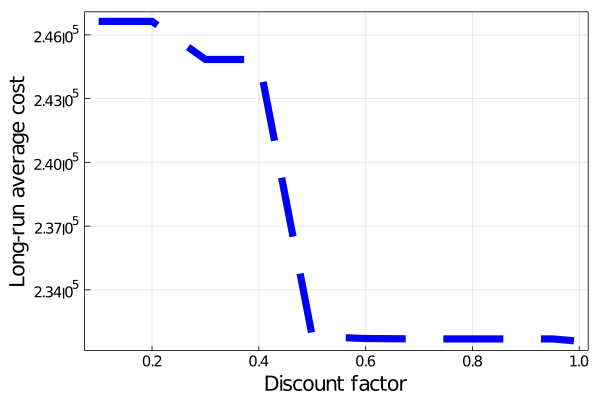

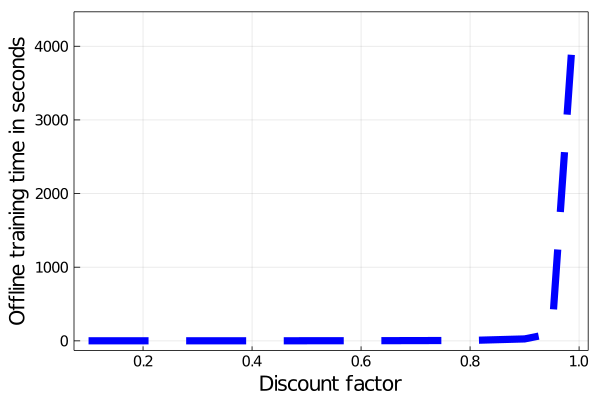

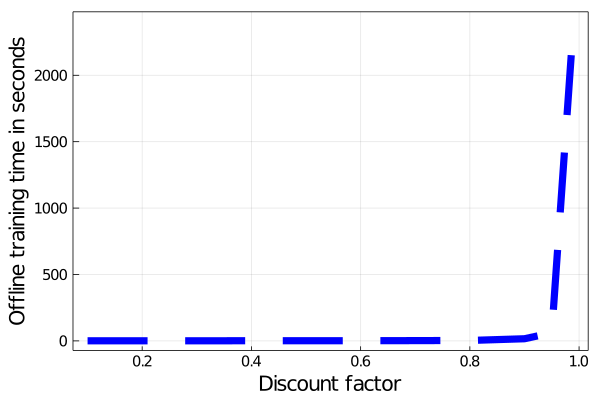

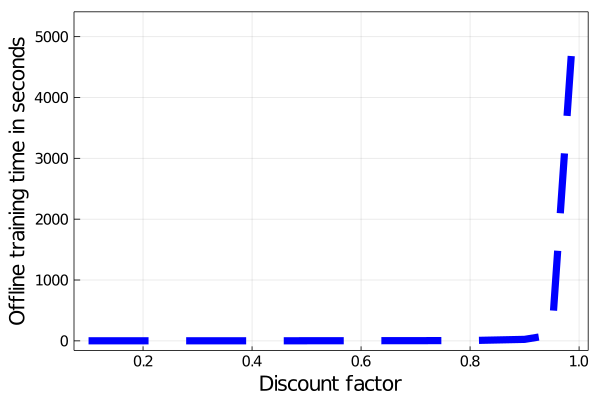

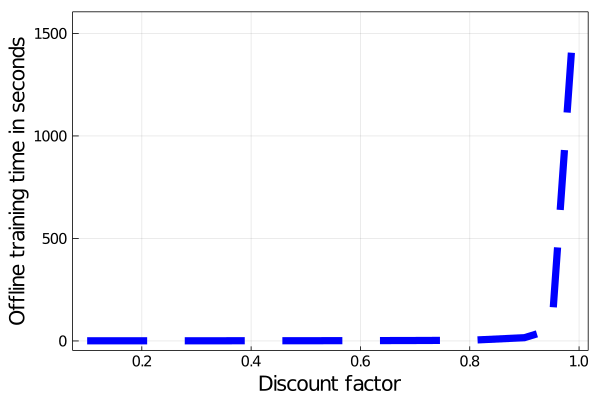

It is also interesting to see, as shown in Figure 5 to Figure 7 in the appendix, that the performance of the stationary policy exhibits a plateauing behavior (as increases) similar to that of the static RH policies (as increases). Although not with the same monotonicity rate, it is important to note that when implementing the periodic variant of the SDDP algorithm under the stationarity assumption (Assumption 5) with , the (infinite horizon) MSP reduces to a static problem. This leads to the delicate issue of how to choose the trial points during the forward pass of the SDDP algorithm, which should depend on the length of the horizon . Approximating using a finite horizon leads to an error which is a consequence of the so-called end-of-horizon effect. Moreover, when is close to 1, the convergence of the algorithm becomes slow since the needed can be large. To deal with this, in our implementation of the periodic variant of the SDDP algorithm, we treat as a random variable following a geometric distribution with a success probability . Then, at the beginning of every iteration , we sample a forecast horizon , a sample path and implement the forward/backward pass along . Note that the sampling error coming from sampling is what might be causing the non-monotonicity of as increases in our numerical results.

Finally, we investigate how the sufficient forecast horizon suggested by Theorem 2 (see also (17)) compared to the average length of forecast horizon used by the dynamic RH policy over the entire sample path in the out-of-sample test, as shown in Table 6. Note that the upper bound on the immediate cost function is calculated as the optimal objective value of problem (19) with state variables . From Table 6, we see that has an average value of around , and for instances when , and , respectively. These numbers are not only significantly smaller than those of the corresponding to the different discount factors computed via Theorem 2 and equation (17), but also consistent with the observations made in Subsection 5.3.2 regarding where the dynamic policy ranks (in terms of its performance) compared to static RH policies with various lengths of forecast horizons.

0.10 0.20 0.30 0.40 0.50 0.60 0.70 0.80 0.90 0.95 0.99 1 1000 8.93 53000 9.77 14.05 18.89 24.99 33.30 45.63 66.15 107.56 234.37 494.93 2686.09 1500 11.27 260500 10.46 15.04 20.22 26.73 35.60 48.74 70.62 114.69 249.49 525.98 2844.53 3 1750 8.42 385500 10.63 15.28 20.54 27.16 36.17 49.51 71.72 116.45 253.20 533.62 2883.52 2250 2.58 635500 10.85 15.59 20.96 27.71 36.89 50.49 73.12 118.69 257.95 543.36 2933.26 6 2000 12.26 412000 10.66 15.33 20.60 27.23 36.26 49.64 71.90 116.75 253.84 534.91 2890.14 2250 10.68 537000 10.78 15.49 20.82 27.52 36.64 50.16 72.65 117.93 256.35 540.08 2916.50

5.4 Sensitivity analysis

In this section, we present a sensitivity analysis to assess the robustness of the solution with respect to different values that we use for the stalling parameter . As previously noted, the stalling parameter is what we use to determine whether or not will remain the same for all , during the offline training step of our proposed approach for the dynamic RH policy (see also Step 3.3 in Algorithm 2). In Table 7, in addition to the results obtained by using the stalling parameter used in our original implementation, we also performed the same procedure using . As it is intuitive to consider as the stalling parameter with the most stable solution, we use it as the benchmark. Similarly to the analysis presented in Subsection 5.3, we also report (i) the training timew (in seconds) for ; (ii) the long-run average cost: given by (20) for ; and (iii) the relative gap in timew and for compared to time15 and .

5.4.1 Sensitivity of the long-run average cost.

When comparing the performance in terms of and the obtained by using the supposedly most stable parameter , we can see from Table 7 that the difference is negligible. Specifically, compared to the obtained by the , has a relative gap of , , and when averaged across the instances where , and , respectively. Whereas, compared to the obtained by the used in our original implementation, has a relative gap of , , and when averaged across the instances where , and , respectively.

5.4.2 Sensitivity of the online training time.

Unlike the difference in the performance in terms of , the difference in the time it took each policy to perform the RH procedure seems to be significant. Specifically, compared to the Timew obtained for , Time15 has a relative gap of , , and when averaged across the instances where , and , respectively. Whereas, compared to the Timew obtained by the used in our original implementation, Time15 has a relative gap of , , and when averaged across the instances where , and , respectively.

As we can see, the dynamic RH policy constructed by using has much less computational time compared to the dynamic RH policy constructed by using . This is to be expected, however, since using is likely to prescribe smaller forecast horizons during the RH procedure and hence lead to less computational time overall. Similarly, apart from the instances where , we can see that the dynamic RH policy constructed by using has less computational time compared to the one with . Overall, using instead of will lead to an average of and decrease in the computational time for instances where , and , respectively. However, it will also lead to an average of , and increase in the optimality gap for these instances respectively.

| Timew | ||||||||

|---|---|---|---|---|---|---|---|---|

| 1 | 5 | 1000 | 10238.65 | 114.27 | -2.24% | -6.46% | -47.32% | 192.28% |

| 1500 | 42024.78 | 544.37 | 5.42% | -1.97% | -72.12% | -8.66% | ||

| 12 | 1000 | 8404.53 | 432.41 | 1.37% | -1.07% | -56.44% | 318.52% | |

| 1500 | 37770.62 | 1386.75 | 2.38% | -0.14% | -77.17% | -30.59% | ||

| 3 | 5 | 1750 | 43949.17 | 1010.73 | 14.41% | -14.09% | -85.15% | -34.53% |

| 2250 | 190165.57 | 42.50 | -0.44% | -1.99% | -11.90% | -9.74% | ||

| 12 | 1750 | 48421.16 | 891.34 | 0.46% | 0.65% | -17.39% | -19.71% | |

| 2250 | 232124.68 | 185.94 | -0.04% | -0.21% | -40.35% | -77.98% | ||

| 6 | 5 | 2000 | 13526.56 | 2383.90 | 1.46% | -2.42% | -51.27% | 8.43% |

| 2250 | 27025.64 | 2671.07 | 3.28% | 0.24% | -61.50% | -27.78% | ||

| 12 | 2000 | 12263.77 | 5337.97 | 5.86% | 1.01% | -64.81% | -9.76% | |

| 2250 | 24988.45 | 5774.15 | 3.26% | 1.72% | -69.92% | -19.08% | ||

6 Conclusion

In this paper, we have studied the question of how many stages to include in the forecast horizon when solving MSP problems using the RH procedure for both finite and infinite horizon MSP problems. In the infinite horizon discounted case, given a fixed forecast horizon , we have shown that the resulting optimality gap associated with the static look-ahead policy in terms of the total expected discounted cost can be bounded by a function of the chosen forecast horizon . This function could be used to provide an upper bound on forecast horizon where the corresponding static RH policy achieves a prescribed optimality gap. In the finite horizon case (with no discount), we have taken an ADP perspective and developed a dynamic RH policy where the forecast horizon to use in each roll of the RH procedure is chosen dynamically according to the state of the system at that stage via certain regression function that can be trained offline. This dynamic RH policy has shown to be capable of exploiting the system state related information encountered during the RH procedure. Our numerical results have illustrated the empirical behaviors of the proposed RH policies on a class of MSPs and highlighted the effectiveness of the proposed approaches. Specifically, when using a static RH policy where the length of the forecast horizon in every roll is fixed, we have shown that the optimality gap plateaued and ceased to respond to the increase in the length of the forecast horizon beyond a certain number of stages. On the other hand, we have shown that advantage of the dynamic RH policy against alternative approaches in the slight increase in the optimality gap compared to the significant reduction in the computational time.

We have identified several avenues for future research. First, we anticipate that the proposed approaches can be extended to various strategies to address the “end-of-horizon” effect during the RH procedure. Second, we expect that some assumptions made for the sake of simplicity in experiments and analysis can be relaxed, allowing the proposed approaches to be applied to a broader class of MSPs, including those defined on hidden Markov chains. Lastly, although we chose not to pursue in this paper, we expect that the proposed approaches can be more appealing for multi-stage stochastic integer programs with a finite action/control space.

References

- [1] Vikas Goel and Ignacio E Grossmann. A stochastic programming approach to planning of offshore gas field developments under uncertainty in reserves. Computers & Chemical Engineering, 28(8):1409–1429, 2004.

- [2] Vitor L de Matos, David P Morton, and Erlon C Finardi. Assessing policy quality in a multistage stochastic program for long-term hydrothermal scheduling. Annals of Operations Research, 253(2):713–731, 2017.

- [3] Tito Homem-de Mello, Vitor L De Matos, and Erlon C Finardi. Sampling strategies and stopping criteria for stochastic dual dynamic programming: a case study in long-term hydrothermal scheduling. Energy Systems, 2(1):1–31, 2011.

- [4] Mario Veiga Pereira, Sérgio Granville, Marcia HC Fampa, Rafael Dix, and Luiz Augusto Barroso. Strategic bidding under uncertainty: a binary expansion approach. IEEE Transactions on Power Systems, 20(1):180–188, 2005.

- [5] Steffen Rebennack. Combining sampling-based and scenario-based nested benders decomposition methods: application to stochastic dual dynamic programming. Mathematical Programming, 156(1-2):343–389, 2016.

- [6] Alexander Shapiro, Wajdi Tekaya, Joari Paulo da Costa, and Murilo Pereira Soares. Risk neutral and risk averse stochastic dual dynamic programming method. European Journal of Operational Research, 224(2):375–391, 2013.

- [7] Shabbir Ahmed, Alan J King, and Gyana Parija. A multi-stage stochastic integer programming approach for capacity expansion under uncertainty. Journal of Global Optimization, 26(1):3–24, 2003.

- [8] Pflug Georg Ch and Romisch Werner. Modeling, measuring and managing risk. World Scientific, 2007.

- [9] Jitka Dupačová. Portfolio Optimization and Risk Management via Stochastic Programming. Osaka University Press, 2009.

- [10] Jitka Dupačová and Jan Polívka. Asset-liability management for czech pension funds using stochastic programming. Annals of Operations Research, 165(1):5–28, 2009.

- [11] Antonio Alonso, Laureano F Escudero, and M Teresa Ortuno. A stochastic 0–1 program based approach for the air traffic flow management problem. European Journal of Operational Research, 120(1):47–62, 2000.

- [12] Boutheina Fhoula, Adnene Hajji, and Monia Rekik. Stochastic dual dynamic programming for transportation planning under demand uncertainty. In 2013 International Conference on Advanced Logistics and Transport, pages 550–555. IEEE, 2013.

- [13] Yale T Herer, Michal Tzur, and Enver Yücesan. The multilocation transshipment problem. IISE Transactions, 38(3):185–200, 2006.

- [14] Giovanni Pantuso. The football team composition problem: a stochastic programming approach. Journal of Quantitative Analysis in Sports, 13(3):113–129, 2017.

- [15] RICHARD Bellman. Dynamic programming. Princeton University Press, 1957.

- [16] Suresh Chand, Vernon Ning Hsu, and Suresh Sethi. Forecast, solution, and rolling horizons in operations management problems: A classified bibliography. Manufacturing & Service Operations Management, 4(1):25–43, 2002.

- [17] O Hernández-Lerma and JB Lasserre. A forecast horizon and a stopping rule for general markov decision processes. Journal of Mathematical Analysis and Applications, 132(2):388–400, 1988.

- [18] Francesca Maggioni, Elisabetta Allevi, and Marida Bertocchi. Bounds in multistage linear stochastic programming. Journal of Optimization Theory and Applications, 163(1):200–229, 2014.

- [19] Francesca Maggioni and Georg Ch Pflug. Bounds and approximations for multistage stochastic programs. SIAM Journal on Optimization, 26(1):831–855, 2016.

- [20] Giovanni Pantuso and Trine K Boomsma. On the number of stages in multistage stochastic programs. Annals of Operations Research, pages 1–23, 2019.

- [21] Warren B Powell. Clearing the jungle of stochastic optimization. In Bridging data and decisions, pages 109–137. INFORMS, 2014.

- [22] Jikai Zou, Shabbir Ahmed, and Xu Andy Sun. Partially adaptive stochastic optimization for electric power generation expansion planning. INFORMS Journal on Computing, 30(2):388–401, 2018.

- [23] W.B. Powell. Approximate Dynamic Programming: Solving the Curses of Dimensionality, volume 842. John Wiley & Sons, 2011.

- [24] Alexander Shapiro. Analysis of stochastic dual dynamic programming method. European Journal of Operational Research, 209(1):63–72, 2011.

- [25] Mario VF Pereira and Leontina MVG Pinto. Multi-stage stochastic optimization applied to energy planning. Mathematical Programming, 52(1-3):359–375, 1991.

- [26] Murwan Siddig and Yongjia Song. Adaptive partition-based sddp algorithms for multistage stochastic linear programming. arXiv preprint arXiv:1908.11346, 2019.

- [27] Alexander Shapiro and Lingquan Ding. Stationary multistage programs. Optimization Online, 2019.

- [28] O Hernández-Lerma and JB Lasserre. Error bounds for rolling horizon policies in discrete-time markov control processes. IEEE Transactions on Automatic Control, 35(10):1118–1124, 1990.

- [29] C Bes and JB Lasserre. An on-line procedure in discounted infinite-horizon stochastic optimal control. Journal of Optimization Theory and Applications, 50(1):61–67, 1986.

- [30] Alexander Shapiro, Wajdi Tekaya, Joari Paulo da Costa, and Murilo Pereira Soares. Report for technical cooperation between georgia institute of technology and ons-operador nacional do sistema elétrico, 2011.

- [31] Amir Ali Nasrollahzadeh, Amin Khademi, and Maria E Mayorga. Real-time ambulance dispatching and relocation. Manufacturing & Service Operations Management, 20(3):467–480, 2018.

- [32] Thuener Silva, Davi Valladao, and Tito Homem-de Mello. A data-driven approach for a class of stochastic dynamic optimization problems. Optimization Online, 2019.

- [33] Iain Dunning, Joey Huchette, and Miles Lubin. Jump: A modeling language for mathematical optimization. SIAM Review, 59(2):295–320, 2017.

Appendix A Tables

| Notation | Description |

|---|---|

| The set of hydro/thermal plants in the HPOP problem | |

| A hydro/thermal plant index in the set of hydro/thermal plants | |

| Cost and random cost vector of generating thermal power at time | |

| Unit penalty cost and random unit penalty cost for unsatisfied demand at time | |

| Amount of inflows and random inflows to hydro plant during stage | |

| Amount of power generated by releasing one unit of water flow in hydro plant | |

| Demand and random demand in stage | |

| Maximum allowed amount of turbined flow in hydro plant in stage | |

| , | Minimum/Maximum level of water allowed in hydro plant |

| , | Minimum/Maximum allowed amount of power generated by thermal plant in stage |

| , | Set of immediate upper/lower stream hydro plants of in the network |

| 245.50 | 125.20 | 1438.00 | 311.00 | 16.20 | 29.70 | 0.20 | |

| 201.70 | 103.90 | 1085.30 | 221.90 | 13.00 | 23.60 | 0.15 | |

| 158.00 | 82.60 | 732.50 | 132.70 | 9.90 | 17.50 | 0.30 | |

| 130.20 | 58.60 | 488.10 | 93.10 | 7.00 | 10.70 | 0.15 | |

| 102.40 | 34.60 | 243.60 | 53.40 | 4.20 | 3.90 | 0.20 |

| 245.50 | 125.20 | 1438.00 | 120.00 | 16.20 | 29.70 | 0.09 | |

| 232.50 | 117.00 | 1329.50 | 111.00 | 15.10 | 27.40 | 0.10 | |

| 219.40 | 108.70 | 1220.90 | 101.90 | 14.00 | 25.00 | 0.10 | |

| 206.40 | 100.50 | 1112.30 | 92.90 | 12.90 | 22.70 | 0.09 | |

| 193.40 | 92.30 | 1003.70 | 83.90 | 11.80 | 20.30 | 0.07 | |

| 180.40 | 84.00 | 895.10 | 74.80 | 10.70 | 18.00 | 0.06 | |

| 167.40 | 75.80 | 786.60 | 65.80 | 9.70 | 15.60 | 0.06 | |

| 154.40 | 67.50 | 678.00 | 56.70 | 8.60 | 13.30 | 0.07 | |

| 141.40 | 59.30 | 569.40 | 47.70 | 7.50 | 10.90 | 0.09 | |

| 128.40 | 51.10 | 460.80 | 38.70 | 6.40 | 8.60 | 0.10 | |

| 115.40 | 42.80 | 352.20 | 29.60 | 5.30 | 6.20 | 0.10 | |

| 102.40 | 34.60 | 243.60 | 20.60 | 4.20 | 3.90 | 0.09 |

| 0.18 | 0.35 | 0.75 | 0.32 | 0.56 | 0.15 | |

| 220.00 | 585.00 | 1688.00 | 5220.00 | 2028.00 | 1480.00 | |

| 672.00 | - | 17217.00 | 2500.00 | - | - | |

| 0.00 | - | 0.00 | 0.00 | - | - | |

| 336.00 | - | 10330.20 | 1250.00 | - | - | |

| 20.00 | 20.00 | 20.00 | 20.00 | |

| 20.00 | 40.00 | 80.00 | 160.00 |

Appendix B Figures