Generalised correlated batched bandits via the ARC algorithm with application to dynamic pricing

Abstract

The Asymptotic Randomised Control (ARC) algorithm provides a rigorous approximation to the optimal strategy for a wide class of Bayesian bandits, while retaining low computational complexity. In particular, the ARC approach provides nearly optimal choices even when the payoffs are correlated or more than the reward is observed. The algorithm is guaranteed to asymptotically optimise the expected discounted payoff, with error depending on the initial uncertainty of the bandit. In this paper, we extend the ARC framework to consider a batched bandit problem where observations arrive from a generalised linear model. In particular, we develop a large sample approximation to allow correlated and generally distributed observation. We apply this to a classic dynamic pricing problem based on a Bayesian hierarchical model and demonstrate that the ARC algorithm outperforms alternative approaches.

Keywords: multi-armed bandit, correlated bandit, parametric bandit, generalised linear model, Kalman filter, dynamic pricing

MSC2020: 62J12, 90B50, 91B38, 93C41

1 Introduction

In the multi-armed bandit problem, a decision maker needs to sequentially decide between acting to reveal data about a system and acting to generate profit. The central idea of the multi-armed bandit is that the agent has ‘options’ or ‘arms’, and must choose which arm to play at each time. Playing an arm results in a reward generated from a fixed but unknown distribution which must be inferred on-the-fly.

In the classic multi-armed bandit problem, the reward of each arm is assumed to be independent of the others (see [9, 1, 12]) and it is the only observation obtained by the agent at each step. In practice, we often observe signals in addition to the rewards and there is often correlation between the distributions of outcomes for different choices (i.e. playing one arm may give information about the other arms).

The differences between signals (observations) and rewards are important for designing learning algorithms, especially when the arms are correlated. In particular, it is possible that a single arm is informative but costly. Most algorithms for bandits will fail to choose this arm, since it never yields the best immediate reward (see [5] for discussion).

In [5], we develop the Asymptotic Randomised Control (ARC) approach to the learning problem with general observations by considering the dynamics of the posterior estimates together with a smooth asymptotic approximation. The ARC approach yields a natural interpretation of the value of each arm as a sum between the exploitation gain and the learning premium, as in the UCB principle [3, 2]. One of the main limitations of the original ARC approach is that it requires the model to have an explicit posterior update, which fundamentally requires the observations and prior to be a conjugate pair. This paper aims to extend this framework to study a more general class of learning problems, where the observations arrive from a Generalised Linear Model (GLM).

Some works have been developed to study bandits with correlation (see [8, 14, 16, 17]) and theoretical guarantees are often provided through regret analysis for specific examples. In particular, the reward is assumed to be the only observation and the structural correlation is assumed on the reward. Filippi et al. [8] considers the correlated bandit problem with GLM rewards (i.e. the reward of the th arm has mean , where is an unknown parameter, is a known feature of the th arm and is a known invertible link function. In contrast, we will model generic observations through a GLM, but allow increased flexibility in modelling rewards.

1.1 Dynamic Pricing Example

To illustrate an application where modelling observations (rather than rewards) is useful, we consider a simple dynamic pricing problem where our agent needs to learn customer demand while maximising revenue. We will refer to this setting later in this paper, to provide a concrete example of our problem setup and our solution. In fact, one can easily extend this framework to study a general class of learning problems.

Suppose that at the beginning of each day, our agent needs to choose a price from the set . At the end of day, with chosen price , our agent observes customers arriving at the store and a sequence of random variables , taking values in , indicating whether the product is bought by the th customer. Assuming independence between the number of customers arriving and their purchasing decisions, the expected revenue of the agent on that day can be given by

where is the probability that each customer will buy the product, given that the price is .

In September 2015, Dubé and Misra [6] ran an experiment, in collaboration with the business-to-business company ZipRecruiter.com, to choose an optimal price for an online subscription. Their experiment ran in two stages, as an offline learning problem: first collecting data using randomly assigned prices, and then testing their optimal price.

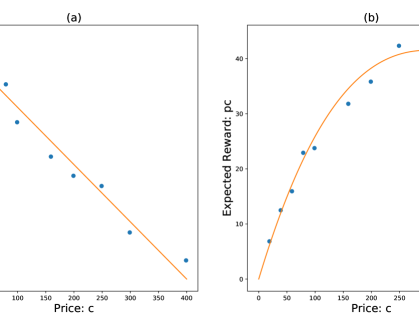

Figure 1(a) displays the relation between the logit of the acquisition rate (the proportion of the customers who subscribe), together with its best fit line. It is clear that the demands at different prices are related (i.e. demand decays with price), which agrees with economic intuition. These data can be found in Table 5 of [6]. We also observe that an approximately linear relation occurs between prices the logit function of the conversion rate, as seen in Figure 1(a), but not the expected reward as observed in Figure 1(b).

Guided by to Figure 1, it is reasonable to consider a logistic model (a case of the Generalised Linear Model (GLM)) for the probability of subscription; the reward, however, does not fit as naturally into a GLM framework. This means that this problem does not easily fit in the correlated bandit frameworks where a distributional assumption is directly made on the reward.

1.2 Contribution of this paper

The novelty of this work is to illustrate a method to study the correlated bandit problem, where observations and rewards are different, and to impose structural assumptions on the observations, rather than the rewards.

In this paper, we will extend the application of the ARC algorithm [5] to a wider class of learning problems, where the observations of each arm arrive from a parametric exponential family in batches, with shared parameter, following a GLM. We generalise the implementation of the ARC algorithm to tackle cases without exact prior-posterior conjugacy, by applying the Kalman filter with a large sample observation. We also provide a numerical simulation to illustrate the performance of our modification.

This paper proceeds as follows. In Section 2, we give an overview of the ARC approach proposed in [5]. We then describe the batched bandit problem, in Section 3, formulated through the generalised linear bandit model and describe how we can use large sample theory and Bayesian statistics to propagate our posterior. Finally, in Section 4, we describe how we can use offline data to construct a bandit environment, and use experimental data from [6] to simulate the pricing problem and compare our method with other approaches.

2 Frameworks for the ARC approach

To avoid unnecessary technical difficulty, we shall describe the setup of [5] without describing the full set of technical assumptions under which asymptotic optimality can be proven. The reader should consult the original paper for formal discussion.

2.1 Problem setup

Suppose that our bandit has arms. Let be an underlying (unknown) parameter taking values in with a (known) prior . The parameter describes the distribution of our bandit, i.e. when the th arm is chosen at time , we observe a random variable and obtain a reward .

The prior (and posterior) of is assumed to be described by a finite dimensional process taking values in a set . In particular, the posterior of at time is given by . Here, denotes the law of conditional on the historical observations . The process represents an estimate (i.e. posterior mean) of the unknown parameter , while represents statistical error (i.e. posterior variance) of our estimate. This parameterisation is shown to be useful in the analysis given in [5].

The transition of the posterior/prior when the th arm is chosen is assumed to be updated by

| (2.1) |

where , , and is a random variable obtained from rescaling , such that and . The random variable in the above update appears through the predictive distribution of the new observation.

2.2 Example: Linear Gaussian bandit

Suppose that our multi-armed bandit problem associates to the unknown parameter where describes the prior of where and .

Suppose that when the th arm is chosen, our observation has distribution where is a known vector in . Following classical Bayesian analysis, we can describe the posterior at time of by where follows

| (2.2) | ||||

for a process taking values in indicating the arm we choose at each time.

2.3 Problem objective and ARC solution

Assume the agent chooses the arm at time by sampling from the probability taking values in . Using the dynamics (2.1), [5] study the discounted reward over infinite horizon and rewrite the objective function in terms of a Markov decision process with underlying state and objective , where

| (2.4) |

with .

It was shown in [5] that an asymptotic solution (for small ) of the above problem is to sample using a distribution given by a feedback function (of the posterior parameter) , where:

is a chosen hyper-parameter.

is a function given by

| (2.5) |

is a function given by with and .

The function represents the (incremental) values of each arm obtained by the summation of the function describing the exploitation gain and the function describing the learning premium, which can be given explicitly in terms of the derivatives of by

| (2.6) |

with and given in (2.1) and , and satisfying

| (2.7) | ||||

with .

3 Batched ARC via Large Sample Theory

One of the main challenges in implementing the ARC approach is to ensure that the posterior distribution can be described by (2.1). In particular, examples in [5] only allow the observations under different arms to be correlated Gaussian or uncorrelated. Therefore, it is not clear how one can apply the ARC algorithm to a learning problem where the observations are not Gaussian and the arms are correlated, as in the pricing example discussed in Section 1.1.

In this section, we will enhance the ARC algorithm to learning problems where observations arrive in batches from an exponential family, where the arms are correlated through an (unknown) parameter, in the same manner as in the generalised linear model. We assume that the observations take values in one dimension, for notational simplicity; the extension to multiple dimensions is straightforward.

3.1 Batched bandit problem

Let be a collection of features corresponding to choices , and let be a random variable taking values in representing an unknown parameter. After the agent chooses features at time , the agent observes where is independent of each and each is independent with GLM density

| (3.1) |

with for known. Here, , and are known functions. For simplicity, we will assume that the distribution of the number of observations does not depend on the unknown parameter .

3.2 Large sample theory of batched observations

In order to apply the ARC approach to a batched bandit problem, we need to understand the evolution of the process describing the posterior distribution. As our observations arrive in batches, we use a large sample approximation to update via a classical normal-normal conjugate model for Bayesian inference.

Suppose that the link function is invertible and differentiable. If our model is non-degenerate, must also be invertible. We define . It then follows from the Central Limit Theorem and the Delta method that

where .

Moreover, by Slutsky’s lemma,

| (3.3) |

where .

By large sample theory, the likelihood function for when observing is

where the constant does not depend on .

Standard Bayesian analysis shows that the posterior of , after observing , the prior can be approximately updated by

where

| (3.4) | ||||

By rearranging the algebra above, we see that

| (3.5) | ||||

where and which can be shown using (3.3) and the predictive distribution of as in (2.3).

It is worth pointing out that forms a sufficient statistic for given . Therefore, as is invertible, the information provided by is sufficient to update the posterior.

3.3 Overcome model degeneracy via Kalman filter

In some settings (e.g. logistic regression), it is possible that lies on the boundary (e.g. for logistic regression). However, the function is only defined on the interior (e.g. for logistic regression). To avoid this degeneracy, one may adopt the approach of [7] for Kalman filtering in the generalised linear framework to estimate using a linear expansion around . In particular, instead of taking , we may use an approximation

| (3.6) |

where .

3.4 ARC approach for the batched observation

Using the approximate posterior update (3.5) and (3.6), we can solve the batched bandit problem using the ARC approach. The posterior dynamic (2.1) can be computed using

| (3.7) |

where and for and corresponding to the exponential family in (3.1).

In addition to identifying the posterior dynamic through (2.1) and (3.7), we need to estimate the expected reward . Since the distribution of depends on only via , it is reasonable to assume that there exists a function such that, for an observation and reward , we have

| (3.8) |

Using a normal approximation, we write

| (3.9) |

where is the standard normal density function.

3.5 ARC algorithm for batched bandits

We can now describe the batched ARC algorithm.

As discussed in [5], an alternative policy to the ARC algorithm is to choose an arm which has the maximum value of .

4 Numerical Simulation

4.1 Generating environments from offline data

As the strategy followed determines the observations available, we cannot directly use historical data to test the algorithm. However, we can use the data to construct an environment in which to run tests. We take a Bayesian view and build a simple hierarchical model (with an improper uniform prior). Effectively, this assumes that our observations come from an exchangeable copy of the world we would deploy our bandits in, with the same (unknown) realised value of . Then we will use Laplace approximation, as in [16, Chapter 5] or [4], to obtain a posterior sample to simulate the markets.

Remark 4.1.

It is worth emphasising that, when implementing the algorithm in simulations, we do not assume that our algorithms know the distribution that we use to simulate the parameter . Instead simulations are initialised with an almost uninformative prior.

To construct a posterior for given historical data, we assume that we have a collection of observations , , …, from an exponential family modeled by (3.1). We denote the corresponding log-likelihood function of by .

Let be the maximum likelihood estimator. i.e. . Then we may approximate the log-likelihood function by

where the constant does not depend on . Therefore, under the uninformative (improper, uniform) prior, we can estimate the posterior of the parameter by

| (4.1) |

Moreover, if the parameter for the exponential family is given in its canonical form, i.e. when in (3.1) is the identity, then the second derivative of the log-likelihood (i.e. the observed Fisher information) is We can use (4.1) to simulate values of and use them as the (hidden) parameters to test our algorithms.

4.2 A selection of other multi-armed bandit algorithms

As a benchmark, we compare the ARC algorithm with other approaches to the multi-armed bandit problem. It is worth pointing out that the theoretical guarantees of these approaches are often provided given that the reward (not the observation) satisfies some distributional assumption, which is not the case for our setting. Nevertheless, the principles of these approaches can be extended to our setting.

For convenience of the reader, we give a summary of the multi-armed bandit approaches considered; further discussion can be found in [5].

-

•

-Greedy (GD) [19]: For , we choose an arm based on its maximal expected reward with probability , and choose an arm uniformly at random and with probability .

- •

- •

-

•

Upper Confidence Bound (UCB) [10, 8, 3]: This is the optimistic strategy of choosing an arm based on an upper bound on the reward. In the classical UCB algorithm [3], the confidence bound is constructed by considering the reward of each arm independently. In particular, at time , the classical UCB chooses an arm with the maximum where is the average reward and is the number of attempt on the -th arm at time and is the horizon.

Since these classical methods do not incorporate correlated learning, we will also consider the Bayes-UCB algorithm [10] where the arm is chosen to maximise the upper quantiles at level where is a hyper-parameter chosen by the decision maker 333It is not clear how to extend the UCB method considered by [8] for the generalised linear model to our more general framework. This is because their confidence bound is constructed based on the assumption that the reward follows the generalised linear model..

-

•

Knowledge Gradient (KG) [17]: This is a Bayes one-step look ahead policy where we pretend that we will only update our posterior once, immediately after the current trial. The decision is made by optimising this objective.

- •

4.3 Dynamic Pricing Simulation

We now focus on the dynamic pricing problem discussed in Section 1.1.

In this model, at the beginning of day , we choose the price of a single product from the set . With chosen price , on day , we observe customers arriving at the store. Inspired by Figure 1, we model the probability that each customer buys the product using a logistic model, i.e. the relation between the demand (probability of buying) and the price is given by

where , (i.e. and for and in (3.1)).

At the end of day , we observe , where indicates whether the product (with price ) was bought by the th customer of the th day. The reward on day is our total revenue, given by . Using (3.2), we can explicitly express the function in (3.8) by by .

4.3.1 Market data and simulation environment

Dubé and Misra [6], in stage one of their experiment, randomly assigned one of ten experimental pricing cells to 7,867 different customers who reached ZipRecruiter’s paywall and estimated the price-dependence subscription rate. The exact numbers of customers that were assigned to each price are not reported. Hence, we assume that there are exactly customers for each price. We then use their reported subscription rate to estimate the number of customers who subscribed given each price.

Using this data, we apply (4.1) as in Section 4.1 to infer an approximate posterior distribution given this preexisting data:

| (4.2) |

In order to compare performance, we will consider each algorithm over a period of one year (365 days) and only allow the agent to change the price at the end of each day. We assume that a common price must be shown to all customers on each day. We also assume that the chosen price does not affect the number of customers reaching the paywall, i.e. we assume that .

We run independent simulations where for each simulation the underlying parameter is sampled from (4.2). We also independently sample to represent the number of visitors on each day. We apply the ARC approaches and other approaches with posterior parameter updating through (3.5) and (3.6) starting with a moderately uninformative prior and . We use Monte-Carlo simulation (as discussed in [5]) to compute relevant terms for KG and IDS. This incurs a noticeably higher computational cost than other approaches.

To assess the performance of each algorithm, we compare the cumulative pseudo-regret of each algorithm given the true parameter :

where , , and is the sequence of actions that the algorithm chooses.

4.3.2 Simulation results

Figure 2 shows the mean, median, 0.75 quantile and 0.90 quantile of cumulative pseudo-regret (against ) of the ARC and other approaches. We see that most algorithms outperform the classical UCB used in [13], which is unsurprising as this approach ignores correlation between demand at different prices. We also see that the ARC (and also ARC index) algorithm outperforms most algorithms both on average and in extreme cases (as shown by the quantile plots). The convergence of many well-known algorithms (e.g. Thompson, Bayes-UCB and IDS) is too slow, as the horizon () is relatively short. The performance of the ARC algorithms is a little better than the KG algorithm, but also requires lower computational cost as we do not need to use Monte-Carlo simulation to compute relevant terms. This demonstrates the benefit of studying the ARC algorithm to handle learning problems where the reward and observation are different.

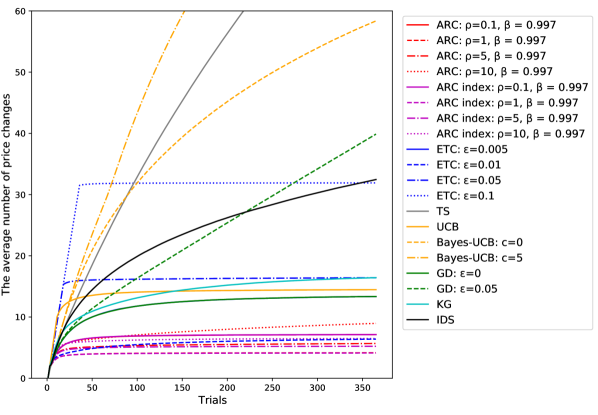

In addition to the regret criteria, when displaying the price, the agent may not want to change the price too frequently. Figure 3 shows that the ARC algorithm and KG algorithm typically require a small number of price changes, yet achieve a reasonably low regret (as shown in Figure 2), whereas Thompson sampling and UCB-type algorithms require a larger number of price changes.

Acknowledgements: Samuel Cohen also acknowledges the support of the Oxford-Man Institute for Quantitative Finance, and the UKRI Prosperity Partnership Scheme (FAIR) under the EPSRC Grant EP/V056883/1, and the Alan Turing Institute. Tanut Treetanthiploet thanks the University of Oxford for research support while completing this work, and acknowledges the support of the Development and Promotion of Science and Technology Talents Project (DPST) of the Government of Thailand and the Alan Turing Institute.

References

- [1] R. Agrawal, Sample mean based index policies by regret for the multi-armed bandit problem, Advances in Applied Probability, (1995), pp. 1054–1078.

- [2] P. Auer, Using Confidence Bounds for Exploitation-Exploration Trade-off, Journal of Machine Learning Research, (2002), pp. 397–422.

- [3] P. Auer, N. Cesa-Bianchi, and P. Fischer, Finite-time analysis of the multiarmed bandit problem, Machine Learning, (2002), p. 235–256.

- [4] O. Chapelle and L. Li., An empirical evaluation of thompson sampling, Advances in Neural Information Processing Systems 24, (2011), p. 2249–2257.

- [5] S. N. Cohen and T. Treetanthiploet, Asymptotic Randomised Control with applications to bandits. arXiv:2010.07252v2, 2022.

- [6] J.-P. Dubé and S. Misra, Scalable price targeting. NBER working paper No. w23775, National Bureau of Economic’ Research, 2017.

- [7] L. Fahrmeir, Posterior mode estimation by extended kalman filtering for multivariate dynamic generalized linear models, Journal of the American Statistical Association, (1992), pp. 501–509.

- [8] S. Filippi, O. Cappé, A. Garivier, and C. Szepesvári, Parametric bandits: the Generalized Linear case, in NIPS’10: Proceedings of the 23rd International Conference on Neural Information Processing Systems, 2010.

- [9] J. C. Gittins and D. M. Jones, A dynamic allocation index for the sequential design of experiments, in Progress in Statistics, J. Gani, ed., Amsterdam: North Holland, 1974, pp. 241–266.

- [10] E. Kaufmann, O. Cappé, and A. Garivier, On Bayesian Upper Confidence Bounds for Bandit problems, in Artificial intelligence and statistics, 2012, pp. 592–600.

- [11] J. Kirschner and A. Krause, Information directed sampling and bandits with heteroscedastic noise, Proceedings of Machine Learning Research, (2018), pp. 1–28.

- [12] T. Lattimore and C. Szepesvári, Bandit Algorithms, Cambridge University Press, 2019.

- [13] K. Misra, E. M. Schwartz, and J. Abernethy, Dynamic online pricing with incomplete information using multiarmed bandit experiments, Marketing Science, (2019), pp. 226–252.

- [14] P. Rusmevichientong and J. N. Tsitsiklis, Linearly parameterized bandits, Mathematics of Operations Research, (2009), pp. 395–411.

- [15] D. Russo and B. V. Roy, Learning to Optimize via Information-Directed Sampling, Operations Research, (2017), pp. 1–23.

- [16] D. Russo, B. V. Roy, A. Kazerouni, I. Osband, and Z. Wen, A tutorial on thompson sampling, Foundations and Trends in Machine Learning, 11 (2018), pp. 1–96.

- [17] I. O. Ryzhov, W. B. Powell, and P. I. Frazier, The knowledge gradient algorithm for a general class of online learning problems, Operations Research, (2012).

- [18] W. R. Thompson, on the likelihood that one unknown probability exceeds another in view of the evidence of two samples, Biometrika, (1933), pp. 285–294.

- [19] J. Vermorel and M. Mohri, Multi-armed bandit algorithms and empirical evaluation, in European Conference on Machine Learning., 2005.