Factor-augmented Smoothing Model for Functional Data

Abstract

We propose modeling raw functional data as a mixture of a smooth function and a high-dimensional factor component. The conventional approach to retrieving the smooth function from the raw data is through various smoothing techniques. However, the smoothing model is not adequate to recover the smooth curve or capture the data variation in some situations. These include cases where there is a large amount of measurement error, the smoothing basis functions are incorrectly identified, or the step jumps in the functional mean levels are neglected. To address these challenges, a factor-augmented smoothing model is proposed, and an iterative numerical estimation approach is implemented in practice. Including the factor model component in the proposed method solves the aforementioned problems since a few common factors often drive the variation that cannot be captured by the smoothing model. Asymptotic theorems are also established to demonstrate the effects of including factor structures on the smoothing results. Specifically, we show that the smoothing coefficients projected on the complement space of the factor loading matrix is asymptotically normal. As a byproduct of independent interest, an estimator for the population covariance matrix of the raw data is presented based on the proposed model. Extensive simulation studies illustrate that these factor adjustments are essential in improving estimation accuracy and avoiding the curse of dimensionality. The superiority of our model is also shown in modeling Canadian weather data and Australian temperature data.

Keywords: Basis function misspecification; Functional data smoothing; High-dimensional factor model; Measurement error; Statistical inference on covariance estimation

1 Introduction

With the increasing capability to store data, functional data analysis (FDA) has received growing attention over the last 20 years. Functional data are considered realizations of smooth random objects in graphical representations of curves, images, and shapes. The monographs of Ramsay & Silverman (2002, 2005) and Ramsay & Hooker (2017) provide a comprehensive account of the methodology and applications of the FDA; other relevant monographs include Ferraty & Vieu (2006) and Horváth & Kokoszka (2012). More recent advances in this field can be found in many survey papers (see, e.g., Cuevas, 2014; Febrero-Bande et al., 2017; Goia & Vieu, 2016; Reiss et al., 2017; Wang et al., 2016). One main challenge in the FDA lies in the fact that we cannot observe functional curves directly, but only discrete points, which are often contaminated by measurement errors. To model a mixture of functional data and high-dimensional measurement error, we introduce a factor-augmented smoothing model (FASM).

We denote a random sample of functional data as , and , where is a compact interval on the real line . In practice, the observed data are discrete points and are often contaminated by noise or measurement error. We use to represent the th observation on the th subject; the observed data can then be expressed as a “signal plus noise” model:

We use to denote the realization of the th discrete point on the curve , and is the noise or measurement error. We assume that measurement error only occurs where the measurements are taken; thus, the error is a multivariate term of dimension . Though in practice, the signal function component is of the same dimension, it differs from in nature. Although functions are potentially infinite-dimensional, we may impose smoothing assumptions on the functions, which usually implies functions possess one or more derivatives. This smoothness feature is used to separate the functions from measurement errors – a functional smoothing procedure.

When the variance of the noise level is a tiny fraction of the variance of the function, we say the signal-to-noise ratio is high. In this case, classic smoothing tools apply to functional data, including kernel methods (e.g. Wand & Jones, 1995), local polynomial smoothing (e.g. Fan & Gijbels, 1996), and spline smoothing (e.g. Wahba, 1990; Eubank, 1999; Green & Silverman, 1999). With pre-smoothed functions, estimates, such as mean and covariance functions, can be further obtained. More recent studies on functional smoothing approaches include Cai & Yuan (2011); Yao & Li (2013), and Zhang & Wang (2016). In this article, we apply basis smoothing to the functions ; that is, we represent as , where are the basis functions and are the smoothing coefficients. The smoothing model then becomes

When the signal-to-noise level is low, smoothing tools may not be adequate in removing the measurement error and may cause an inefficient estimation of the smoothing coefficients. Let us take a further look at the measurement error . In the FDA, the number of discrete points on each subject is often large compared with the sample size . Hence the term is a high-dimensional component. In this case, the observed data are, in fact, a mixture of functional data and high-dimensional data. The existence of the large measurement error raises the curse of dimensionality problem, which naturally calls for the application of dimension reduction models to . Many studies have been conducted on various dimension reduction techniques for high-dimensional data; among theses, factor models are widely used (e.g. Fan et al., 2008; Lam et al., 2011).

We propose using a factor model for the measurement error term. Without further information on the measurement error, factor model is appropriate since the estimation of latent factors does not require any observed variables. The high-dimensional measurement error is assumed to be driven by a small number of unobserved common factors.

where are the unobserved factors, are the unobserved factor loadings, is the number of latent factors, and are idiosyncratic errors with mean zero. Thus, the observed data can be written as the sum of two components:

This is a basis smoothing model with the factor-augmented form. This proposed model can be easily modified to adopt nonparametric smoothing methods. In Section 5, we illustrate the use of spline smoothing approaches. In Section 7.5, the nonparametric smoothing model is applied to simulated data.

In this paper, we motivate the FASM in three considerations, as listed below. In these three cases, using the proposed model remedies the defects of the traditional smoothing model. Examples of the following three motivations are provided in Section 2.

-

1.

In traditional smoothing models, the measurement error is assumed to be non-informative and independently and identically distributed (i.i.d.) in both directions. This is an unrealistic assumption when the measurement errors contain information. With the factor model applied, we assume that a small number of unobserved factors can capture the covariance in the measurement error. This is usually reasonable in practice because a few common factors often drive the occurrence of systematic measurement error.

-

2.

When the smoothing basis functions are incorrectly identified, the smoothing model will lead to an erroneous coefficient estimate and large residuals. The proposed model deals with this problem since the unexplained variation resulting from the basis’s misidentification can be modeled with a small number of unobserved common factors.

-

3.

When there are step jumps in the mean level of the functions, neglecting the mean shift in smoothing models will result in large residuals at the point where the jumps occur. The changes in the mean levels of the functions come from a universal source and can be modeled by common factors.

Since the latent factors are unobserved, we propose an iterative approach to estimate the smooth function and the factors simultaneously. Principal component analysis (PCA) is used as a tool in estimating the factor model, and penalized least squares estimation is applied to construct the estimator for the smoothing coefficient . We establish the asymptotic theories of the smoothing coefficient estimator, where the consistency of the estimator is proved. We also provide the asymptotic distribution of the projected estimator in the orthogonal complement of the space spanned by the factors . The interplay between the smooth component and the factor model component is manifested.

In the remainder of this article, we elaborate on the previously mentioned three motivations in detail, with examples given in Section 2. In Section 3, the model is formally stated, and the iterative estimation approach is provided. We discuss the asymptotic properties of the smoothing coefficients under various assumptions in Section 4. We extend the proposed model to a nonparametric smoothing approach in Section 5. In Section 6, we consider the statistical inference aspect of the model and propose a covariance matrix estimator for the raw data. In Section 7, we conduct Monte-Carlo simulations on the proposed model under different settings. A few real data examples are given in Section 8, and conclusions are drawn in Section 9. Last, we provide proofs of the relevant theorems and lemmas in the Appendix.

2 Motivation

We introduce three examples to motivate the proposed model. In these cases, the smoothing model is not adequate to capture the raw data’s signal information. In the first example, when large measurement error exists, the residuals after smoothing are large with some extreme values. In the second example, when the basis functions are selected incorrectly, part of the functions’ variation cannot be captured by the smoothing model. In the third example, when there are step jumps in the functional data, the residuals after smoothing contain gaps. These examples demonstrate that further modeling of the residuals is needed.

2.1 Functional data with measurement error

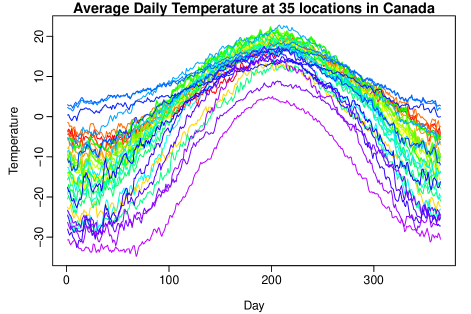

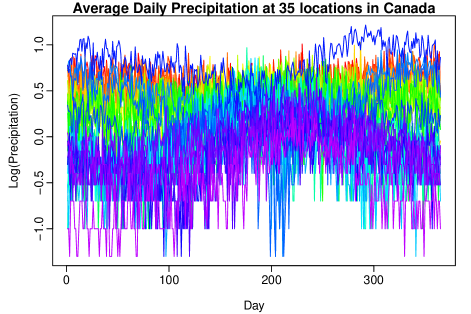

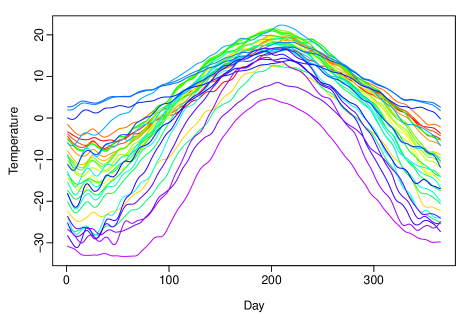

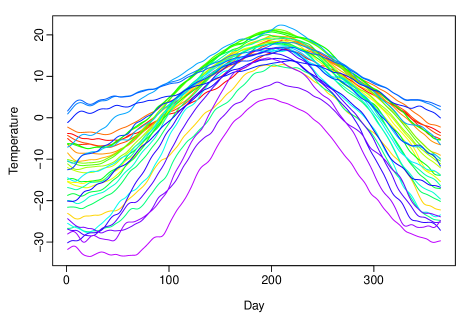

Figure 1 shows the rainbow plots of the average daily temperature and log precipitation at 35 locations in Canada. Due to the nature of the two kinds of data, it is reasonable to assume that temperature and log precipitation are functions over time. The two graphs, however, display distinct features. In the temperature plot, though there are some perturbations, it is relatively easy to discern each curve’s shape. In the precipitation plot, there is a tremendous amount of variability in the raw data, such that it is almost impossible to observe the underlying shape of the curves.

Smooth temperature data can be retrieved without much difficulty using basic smoothing techniques. The residuals are small, with constant variation. On the other hand, the residuals after smoothing exhibit a high level of variation for the precipitation data and even contain some extreme values. Our model endeavors to further explain the large residuals in similar cases to the precipitation data; we will show the fitting result in Section 8.

2.2 Misidentification of the basis function

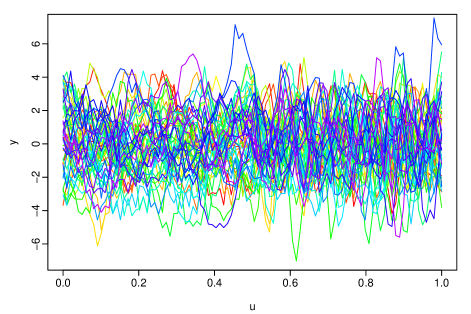

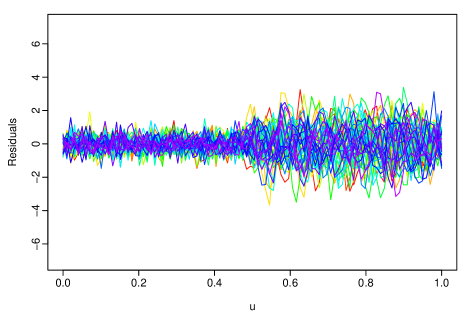

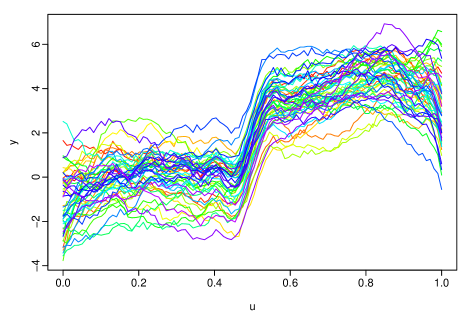

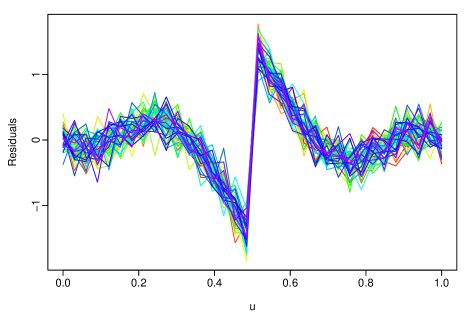

It is important to choose the appropriate basis functions in the smoothing method. In this example, we show the inadequacy of the smoothing model when the basis functions are misidentified. We generate functional data using basis functions with changing frequencies. The raw data are shown in Figure 2(a). Fourier basis functions are used. In the second half of the data, the frequency of the Fourier basis functions increases, so the data set exhibits more variation toward the right end. Suppose that we were not aware of the change in the frequencies in the basis functions, and still used the basis of the first half of the data for the whole curves. The consequence of misidentifying the basis functions when a smoothing model is applied can be observed in Figure 2(b). The residuals are large in the second half. The smoothing model fails to reduce the residuals; a factor model can be used to further model the signal hidden in the large residuals. The data generation process and further analysis can be found in Section 7.6.

2.3 Functional data with step jumps in the mean level

We provide another example of functional data with step jumps to motivate our proposed model. Suppose we observed a sample of the raw functional data, as shown in Figure 3(a). It can be seen that there is a jump at around . The jump applies to all the sample data, so this sudden shift is at the mean level. We will explain how the data are generated in Section 7.7. The residuals after smoothing are presented in Figure 3(b). The large residuals around the jump clarify that without measures to deal with the step jumps, smoothing itself is not enough to model these kinds of data. We show in Section 7.7 that the proposed model applied to the same data generates smaller residuals and has less flexibility. This is indeed one of the main goals because of model selection.

3 Model specification and estimation

In this section, we formally state the proposed model in Section 3.1 and provide the estimation method in Section 3.2. We first show how the smoothing coefficient and the latent factors are estimated separately and then introduce an iterative approach to simultaneously find these estimates.

3.1 Model statement

We consider a sample of functional data , which takes values in the space of real-valued square integrable functions on . The space is a Hilbert space, equipped with the inner product . The function norm is defined as The functional nature of allows us to represent it as a linear expansion of a set of smooth basis functions.

where is a set of common basis functions and is the th coefficient for the th curve. Therefore, we can express the full model as

where are the unobserved common factors, are the unobserved factor loadings and is the number of factors. We call this model the FASM. For the model to be identifiable, we require the following condition.

Identification Condition 1.

We require

-

(i)

is independent of for , and

-

(ii)

for some matrix , as ;

for some matrix , as .

The first part of the identification condition ensures the signal function component and the factor model component are independent. The second part ensures the existence of factors, each of which makes a non-trivial contribution to the variance of , which in turn guarantees the identifiability between the factors and the error term .

We treat the basis functions as known, and the number fixed. This is, of course, a simplification to accommodate for the theoretical proofs. In real data analysis, there are various choices for the basis functions, and the decision can be quite subjective. For example, Fourier bases are preferred for periodic data, while spline basis systems are most commonly used for non-periodic data. Other bases include wavelet, polynomial, and some ad-hoc basis functions.

3.2 Estimation

We can write the model for the th object as

| (1) |

where

Combining all the objects, we have in matrix form

| (2) |

where is and is a matrix containing all the smoothing coefficients. The matrix is and is Since is assumed to be known, we illustrate how the parameters and are estimated in the following.

For the latent factor estimation, there is an identification problem such that for any invertible matrix . Thus we impose the normalization restriction on the matrices and

| (3) |

We propose to implement penalized least squares, where the objective function is defined as

where is a penalty term used for regularization, and is the tuning parameter controlling the degree of regularization. The same is used for all the functional observations . This is a simplified case, where we assume a similar degree of smoothness for all curves. The tuning parameter can be chosen by cross-validation or information criteria. We intend to penalize the “roughness” of the function term. To quantify the notion of “roughness” in a function, we use the square of the second derivative. Define the measure of roughness as

where denotes taking the second derivative of the function , the larger the tuning parameter , the smoother the estimated functions we obtain. Further, we denote

| (4) |

Then

We can re-express the roughness penalty in matrix form as the following:

where

| (5) |

Thee matrix is the same for all subjects and the penalty term differs for each subject only by the coefficient .

Remark 1.

The number of smoothing coefficient needed increases as the sample size increases. The inclusion of a penalty term not only penalizes the ”roughness” of the smoothed function but also mitigates the effect of increasing number of parameters to control the model flexibility.

Thus, the objective function can be written as

subject to the constraint .

We aim to estimate the smoothing coefficient of . We left multiply a matrix to each term in (1) to project the factor model term onto a zero matrix. Define the projection matrix

| (6) |

Then

So we estimate from the projected equation

The projected objective function becomes

| (7) |

By taking the derivative of with respective to each , we can solve for the estimator .

Setting the derivative to zero and rearranging the terms, we have

Using the fact that

we obtain the least squares estimator for given

Next, to estimate and , we focus on the factor model

and in matrix form

where . In high dimensions, the unknown factors and loadings are typically estimated by least squares (i.e., the principal component analysis; see, e.g., Fan et al. (2008); Onatski (2012). The least squares objective function is

| (8) |

Minimizing the objective function with respect to , we have using (3). Substituting in (8), we obtain the objective function

where the last equality uses (3) and that . Thus, minimizing the objective function is equivalent to maximizing . The estimator for is obtained by finding the first eigenvectors corresponding to the largest eigenvalues of the matrix in descending order, where

Therefore, knowing , we solve for using

| (9) |

where is a diagonal matrix containing the eigenvalues of the matrix in the square brackets in decreasing order. The coefficient is used for scaling.

Remark 2.

The number of factors is assumed to be known in this paper. In practice, is selected based on some criteria regarding the eigenvalues. There have been many studies on this topic. Examples include Bai & Ng (2002), where two model selection criteria functions were proposed; and Onatski (2010), where the number of factors was estimated using differenced eigenvalues; and Ahn & Horenstein (2013), where this number was selected based on the ratio of two adjacent eigenvalues.

It can be seen that is needed to find , and in turn is needed to find . The final estimator is the solution of the set of equations

| (10) |

Since there is no closed-form expression of and , we propose using numerical iterations to find the estimates. The details of these iterations are as follows:

-

1.

Denote the initial value as . Using (10), we obtain .

-

2.

With , we substitute into the second equation of (10), to obtain , where is the eigenvector of the matrix corresponding to its th largest eigenvalue.

-

3.

With , we obtain using (10)

-

4.

We then repeat steps 2 and 3 until , where is a small positive constant.

Remark 3.

In this paper, we use . This means we start by ignoring the factor model component so the initial value for the smoothing coefficient , which is simply the ridge estimator. The convergence of Newton’s numeric iteration requires the convergence of this estimator, which in turn requires the factor model component to have an expectation of zero. The stopping criterion only focuses on because we are interested in estimating as a whole.

Remark 4.

Common methods for selecting the shrinkage parameter include the Akaike’s Information Criterion (AIC Akaike, 1974), the Bayesian Information Criterion (BIC Schwarz, 1978), and cross-validation. In this paper, we use the mean generalized cross-validation (mGCV) method (Golub et al., 1979). We define, at step ,

| (11) |

where is the sum of squares residual for the th object at step and is the equivalent degrees of freedom measure, which can be calculated as

| (12) |

At each step of the iteration, the tuning parameter is chosen by minimizing the .

Remark 5.

Algorithm 1 is an iteration procedure in which ridge regression and PCA are iterated. The convergence of this iterative algorithm is studied in Jiang et al. (2020). For instance, Theorem 2 of Jiang et al. (2020) provides some sufficient conditions under which the recursive algorithm converges to the true value or some other values. In particular, when the regressors are independent of the common factors, or the factors involved in regressors are weaker than the common factors, this algorithm will converge to the true parameter.

After we obtain the estimates and , the estimated coefficient matrix is constructed as , and the estimated factor can be obtained by

Finally, the functional component can be estimated by , where is defined in (4).

Remark 6.

Although we have imposed the constraint in (3) and the identification condition 1, and are not uniquely determined, since the model (1) is unchanged if we replace and with and for any orthogonal matrix . However, the linear space spanned by the columns of is uniquely defined. Although we are not able to estimate , we can still estimate a rotation of , which spans the same space as does. The matrix defined in (6) is a projecting matrix onto the orthogonal complement of the linear space spanned by the columns of . It is shown in the next section that the estimator for is consistent.

4 Asymptotic theory

In this section, we study the asymptotic properties of the coefficient estimator with growing sample size and dimension. We state the assumptions in Section 4.1 and provide the asymptotic results of in Section 4.2.

4.1 Assumptions

We use to denote the true parameters. In this paper, the norm of a vector or matrix is defined as the Frobenius norm; that is, . We introduce the matrix

| (13) |

This matrix plays an important role in this article. It is used in the proof of the consistency of , as can be found in Appendix A. The identifying condition for is that is positive definite for all , which is stated in Assumption 3.

First, we state the assumptions.

Assumption 1.

The above assumption declares that the basis functions are bounded in the norm. This is quite natural as some of the most commonly used basis functions are bounded; for instance, the Fourier basis, B-spline basis, and wavelet basis functions (Ramsay & Silverman, 2005).

Assumption 2.

Above, we assume the smoothing coefficients are bounded uniformly for all . This assumption is introduced to ensure the uniform consistency of the estimated coefficients of .

Assumption 3.

Let . We assume

This assumption is the identification condition for . The usual assumption for the least-squares estimator only contains the first term on the right-hand side of (13). The second term on the right-hand side of (13) arises because of the unobservable matrices and .

Assumption 4.

For some constant , , and .

Assumption 5.

For some constant , the error terms are i.i.d. in both directions, with , , and .

Assumption 6.

is independent of , , and for all .

We require that the errors are independent in themselves and also of the functional term and factor model terms and . To not mask the main contribution of our method, we use a simplified setting on the error terms to exclude endogeneity. Nevertheless, with simple but tedious modifications, Assumption 5 can be relaxed, and our model can be extended to more complicated settings where correlations between the error term and the factor model term are allowed.

Assumption 7.

The tuning parameter satisfies .

This is conventionally assumed in ridge regression (see, e.g., Knight & Fu, 2000) and assures that the estimator’s asymptotic bias is zero.

Before stating the next assumption, we introduce some notations. Let denote the th column of the matrix , and let denote the th element of the matrix , where

| (14) |

Then, for any vector , we can write

| (15) |

In (15), for notation simplicity, we define as . The matrix is of interest because it is the main component that contributes to the asymptotic distribution of the estimators, as shall be seen in the next section.

Let

| (16) |

We make the following assumption.

Assumption 8.

This assumption is the multivariate Lindeberg condition, which is needed in constructing the central limit theorem in the next section. This is by no means a strong condition; for instance, when the factor model component is ignored, is simply , and . Since we assume in Assumption 1, the Lindeberg condition in (18) is met.

4.2 Asymptotic properties

As we have mentioned previously, the identification problem of the latent factor implies that we actually use the estimator to estimate a rotation of . Based on the objective function (7) in Section 3, we use a center-adjusted objective function, defined as below.

| (19) |

where is defined in (6), satisfying The second term on the right-hand side of (19) does not contain the unknown and , so the inclusion of this term does not affect the optimization result. This term is only used for center adjusting, so that the resulting objective function has an expectation zero. We estimate and by

| (20) |

In the following, we establish the asymptotic properties for the estimated coefficient matrix . In Theorem 1, the consistency of the matrix is proved. In Theorem 2, we show the rate of convergence of . Theorem 3 provides the asymptotic distribution of .

Let for a matrix .

We start by proving consistency for the vector . This consistency is uniform for all . Therefore, we could combine for all , and have the result for the coefficient matrix in . The matrix is of dimension , where is fixed and the sample size goes to infinity, so there is a scale in the result of . In the second part of the theorem, note that , where is the projection matrix onto the orthogonal complement of the linear space spanned by the columns of . Thus, and represent the spaces spanned by and , and we show that they are asymptotically the same in .

Next, we obtain the rate of convergence.

We study the case when the dimension and the sample size are comparable. We achieve rate convergence, considering on the whole. It is expected that the rate of convergence for smoothing models depends on the number of discrete points observed on each curve.

Remark 7.

The asymptotic result in Theorem 2 contains a projection matrix . This matrix projects onto the space orthogonal to the factor matrix . This theorem shows the interplay between and . When and are orthogonal, , and we obtain the rate of convergence of . When and are not orthogonal, the inference on will be affected by the existence of the factor model component.

We further begin to establish the limiting distribution. It is shown in Appendix A that

The limiting distribution is constructed based on the first term on the right-hand side. Let denote the th column of the matrix . We then have the following lemma.

This lemma paves the way for the next theorem on asymptotic normality.

Theorem 3.

The vector comes from the same vector in Lemma 1. The asymptotic bias is zero since we assume no serial or cross-sectional correlation in the error terms. This is a simplified setting, which can be extended to allow for weak correlations in errors in both directions. In that case, the asymptotic distribution will include a non-zero bias term.

Remark 8.

Theorem 3 shows that the asymptotic distribution of the coefficient matrix relies on the unobserved factor loading matrix . Although we are unable to consistently estimate with , what we need is in fact the projected matrix , which can be estimated by . We are able to find estimators for and based on ,

where is the th column of the matrix and is the th element in the matrix .

5 Extending the model to nonparametric smoothing

In the FASM, we use basis smoothing where we assume the basis functions are known, and we show the asymptotic properties in the previous section. However, in practice, the basis functions are usually unknown, and nonparametric smoothing techniques are frequently used. In this section, we extend the proposed model to a smoothing spline.

In spline smoothing, a spline basis is used to model functions. We consider smoothing splines, where regularized regression is performed, and the knots are placed on all the observed discrete points. The most commonly considered basis is the cubic smoothing splines, where the order is 4. The number of basis functions equals the number of interior knots plus the order. Thus, we use spline basis functions. Denote the th basis function as , . Let the matrix denote the basis matrix, where the th element is . The objective function can be written as

where is the vector of smoothing coefficient and the matrix is similarly defined as the matrix in (5). The estimators are the solution of the equation system

which can be solved by iteration approach in Section 3.2. The function estimator is , where is a vector containing all the basis functions .

It could be seen that the model is almost the same as the model proposed in Section 3. The difference lies in the dimensions of the matrices and . In the parametric model, we assume the basis functions are known, and the number of basis functions is fixed, so is a matrix. While in smoothing spline modeling, the matrix is of dimension . The number of basis functions goes to infinity. This does not render our model estimation infeasible, however, because we have included a penalty term.

6 Statistical inference on covariance matrix estimation

Having presented the model estimation approach and the estimators’ asymptotic properties, we now consider statistical inference with FASM. Our model serves as a dimension reduction technique and avoids the curse of dimensionality problem, rendering making inferences from the model convenient.

Covariance estimation is fundamental in both FDA and high-dimensional data analysis. In these areas, data are of high dimensions, which brings many challenges. In the FDA, the number of discrete points on each curve is often larger than the number of curves. Similarly, the dimension of high-dimensional data is typical of the same order or larger than the sample size . In this case, the traditional sample covariance estimator no longer works. Dimension reduction by imposing some structure on the data is one of the main ways to solve this problem (see, e.g., Wong et al., 2003; Bickel & Levina, 2008; Fan et al., 2008). By reducing the data dimension with a smoothing model and a factor model in FASM, we propose an alternative covariance matrix estimator.

We consider the covariance matrix of the observed high-dimensional data . Let

Based on the FASM where

we obtain

| (21) |

where and are covariance matrices of the vectors and respectively and denotes the error variance structure and is a diagonal matrix under Assumption 4. Based on the above equation, we have an estimator

| (22) |

where and can be calculated by

where s are vectors containing ones, the dimensions of which depend on the matrices multiplied before and after the vectors. The diagonal error covariance matrix is estimated by

where is the residual matrix calculated as .

Remark 9.

In functional data analysis where the functional signal is the focus, the estimation of the covariance function is of main interest. In this paper, we study the covariance structure of the mixture of functional data and high-dimensional data. This type of covariance estimator based on factor models has also been used in previous literature. For example, Fan et al. (2008) employed a multi-factor model where the factors are assumed observable, while Fan et al. (2011) considered an extension to approximate factor models where cross-sectional correlation is allowed in the error terms.

We compare the finite sample performance using mean squared error (MSE) of the proposed covariance estimator with the ordinary sample covariance estimator. When the factor structure is ignored, the sample covariance estimator is expected to have a larger variance than our estimator. The advantage of the proposed estimator is shown in Section 7.4.

7 Simulation studies

In this section, we use simulated data to illustrate the superiority of the proposed model. The FASM is compared with the smoothing model in Section 7.1 to 7.3. In Section 7.4, we compare the finite sample performance of the covariance matrix estimator introduced in Section 6 with the ordinary sample covariance estimator. In Section 7.6, we show how the FASM performs when applied to functional data with step jumps.

7.1 Data generation

We generate simulated data , where and from the following model:

where are chosen as B-spline basis functions of order 4 and the smoothing coefficients are generated from . The factors follow and the factor loadings , where is a 4 by 4 covariance matrix. We set the multivariate mean term and variance . We adjust the value of to control the signal-to-noise ratio. When is large, the signal-to-noise level is low, and when is small, the signal-to-noise level is high. The random error terms follow .

7.2 Estimation

The numeric iteration procedure for finding is introduced in Section 3. We compare the FASM with the smoothing model, where the factor model component is ignored. The smoothing model can be expressed as:

where the coefficient estimator is calculated as:

The tuning parameter is also chosen using mGCV defined in (11).

7.3 Results

We repeat the simulation setup 100 times and obtain the estimated smooth function . The averaged mean squared error (aMSE) for function estimation is calculated as

The results are reported in Table LABEL:tab:1. With the same sample size , increasing the number of points on the curve decreases the estimation error. However, with the same value for , increasing the sample size does not decrease the estimation error. This is consistent with the convergence rate stated in Section 4, where the estimator converges with the rate related to . When is large, such that the signal-to-noise ratio is high, the FASM performs better than the smoothing model.

| aMSE | |||

|---|---|---|---|

| Dimension | FASM | Smoothing model | |

7.4 Covariance matrix estimation

This section shows the finite sample performance of the covariance estimator defined in (22). We also calculate the regular sample covariance estimator using

where the matrix is the sample mean matrix whose th row elements are .

Both estimators are compared with the population covariance matrix, which is calculated using (21). We calculate the estimation errors under the Frobenius norm as

We show the MSE results in Table LABEL:tab:4. It can be seen that the FASM produces smaller MSE values in almost all cases.

| MSE | |||

|---|---|---|---|

| Dimension | FASM | Sample covariance | |

7.5 Nonparametric smoothing model

In this section, we apply the factor-augmented nonparametric smoothing model introduced in Section 5 to simulated data and compare the results with using nonparametric smoothing models without the factor component.

We generate simulated data , where and from the following model:

where are Fourier basis functions and the smoothing coefficients are generated from . The factors follow and the factor loadings , where is a 4 by 4 covariance matrix. The random error terms follow . We set the multivariate mean term and variance . We adjust the value of to control the signal-to-noise ratio. When is large, the signal-to-noise level is low, and when is small, the signal-to-noise level is high.

Smoothing spline

We use order 4 B-spline basis with knots at every data point. With data of dimension , we use basis functions. The tuning parameter is selected by the mean generalized cross-validation (11) at each iteration step. The covariance estimate is calculated using (22). Table LABEL:tab:4 presents the results.

| aMSE | MSE | ||||

|---|---|---|---|---|---|

| Dimension | FASM | Smoothing | FASM | Sample covariance | |

7.6 Misidentification of the basis function

We elaborate on the example presented in Section 2.2. We generate data from

| (23) |

where are a set of Fourier basis functions. The first Fourier basis function is the constant function; the remainder are sine and cosine pairs with integer multiples of the base period. We generate the Fourier functions with doubled frequencies in the second half to simulate the change in the basis functions. In particular, when for and for , and when for and for . The coefficients are generated from the normal distribution with mean 0 and variance . The error terms are also drawn from the normal distribution with mean 0 and variance . The generated are shown in Figure 2(a). It can be seen that the data exhibit more variation in the second half of the interval.

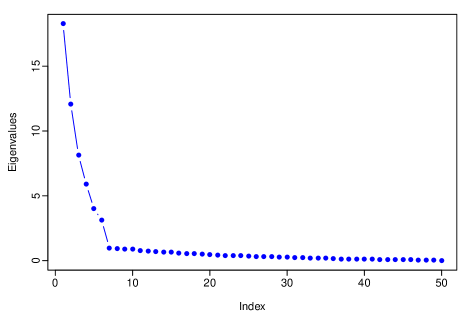

Suppose we were unaware of the change in the frequencies of the basis functions and used the bases in the first half to fit the data on the whole interval. The smoothing model residuals, shown in Figure 2(b), are large in the second half. When the frequency of the basis functions is misidentified, a smoothing model with the wrong set of bases is inadequate. We conduct principal component analysis on the smoothing residuals; the eigenvalues in descending order are shown in Figure 4(a). The residuals preserve a spiked structure, where six common factors can explain most of the variation.

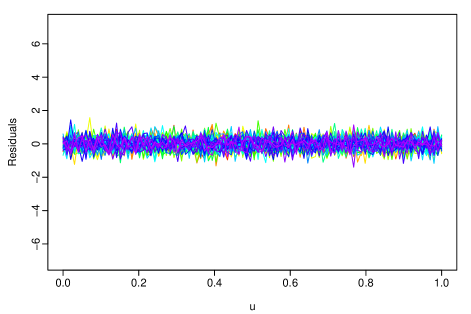

We also apply FASM to the same data with the wrong set of basis functions. According to the eigenvalue scree plot, we retain six factors in the model (). The resulting residuals are shown in Figure 4(b). The large residuals in the second part of Figure 2 (b) are removed. When the basis functions are misidentified, the FASM serves as a remedy.

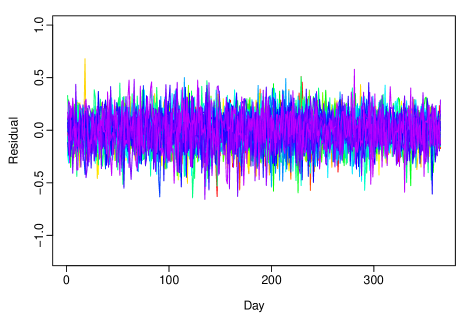

7.7 Functional data with step jumps

We study the case where the functional data exhibit a dramatic change in the mean level within a small window. We generate data from the following model

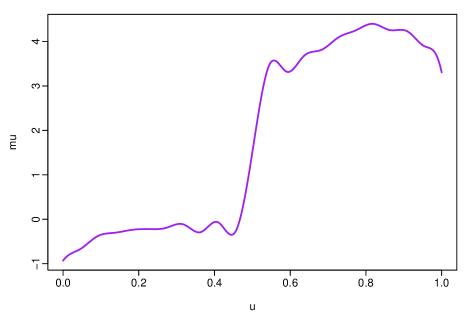

where the basis functions are order 4 B-spline bases. The coefficients come from and the error terms from . The mean function is generated by a linear combination of 25 B-spline basis functions. Figure 5 shows an example of the mean function- there is a sharp increase in the mean function at around .

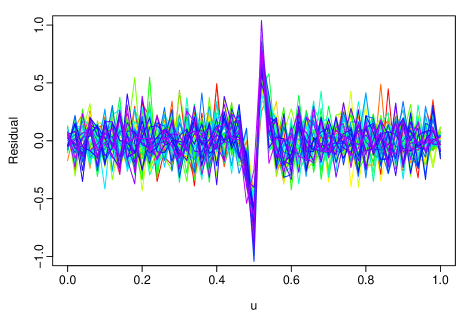

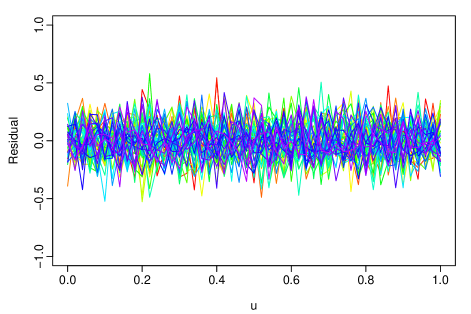

The change in the mean level happens at , and denotes the amount of change. Figure 3 is generated using . Figure 6 compares the residuals from the smoothing model and the FASM. With the smoothing model, the residuals around the jump are large. In contrast, our model explains the large residuals around the structural break very well. In the aspect of model selection, we consider the trade-off between model fit and model flexibility. We first define a notion of flexibility for a fitted model with the degrees of freedom. We use the same concept as in most textbooks that the degrees of freedom measure the number of parameters estimated from the data required to define the model. The degrees of freedom for the smoothing model are calculated by (12) of the last step of convergence. The degrees of freedom for the FASM is

where is the number of factors retained in the fitted model, the larger the degrees of freedom, the more flexible the fitted models are. To quantify the model fitting, we use

where . In Table 4, we show the simulation results by changing the value of the mean shift . The RMSE of the FASM is always smaller than the compared model. The degrees of freedom when are similar. When increases, the degrees of freedom is smaller for the proposed model. Therefore, we achieve better fit but less flexibility with the FASM.

| RMSE | DF | |||

|---|---|---|---|---|

| Smoothing | Proposed | Smoothing | Proposed | |

8 Application to climatology

In this section, we apply the FASM to two real data sets. In Section 8.1, we compare Canadian yearly temperature and precipitation data and demonstrate the advantages of the FASM when the measurement error is large. In Section 8.2, we analyze Australian daily temperature data and display the necessity of including the factor model because of the spike structure of the data.

8.1 Canadian weather data

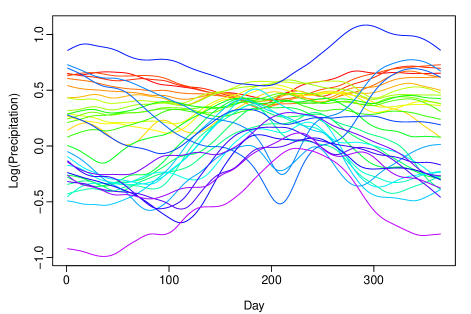

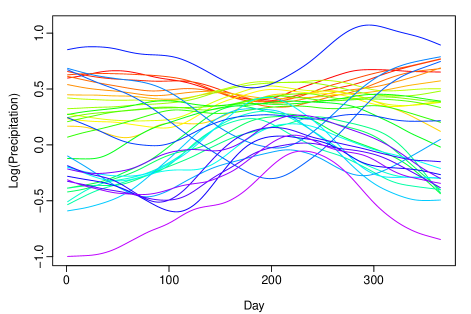

In Section 2.1, we introduced Canadian weather data. Raw observations of daily temperature and precipitation data are presented in Figure 1. Since the true basis functions are unknown, we apply the FASM with nonparametric smoothing splines introduced in Section 5 to these two datasets.

We use order 4 B-spline basis functions with knots at every data point. Thus, when the number of data points is 365, we use 367 basis functions. The number of factors is chosen with the scree plot showing the fraction of variation explained. For temperature data, we presumed the measurement error is small. The resulting smoothed curves are shown in Figure 7. Compared with using the smoothing model introduced in Section 7.2, the FASM generates similar results. This meets our expectation that our model should work the same as a simple smoothing model when measurement error does not exist.

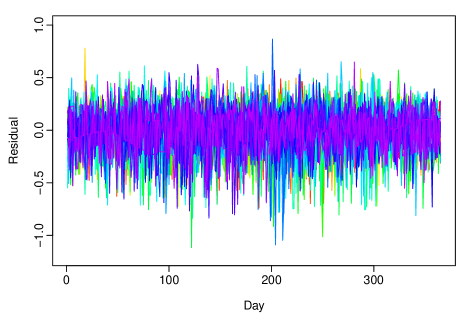

In Section 2.1, we suspect large measurement errors are contained in the raw log precipitation data. We apply the two models to the log precipitation data; the resulting smoothed curves are presented in Figure 8. The plot on the right shows smoother curves, especially at the drop in the blue curve (the ’Victoria’ Station) at around day 200. Looking at the residual plots in Figure 9, our model mainly explains some extreme residuals left out from solely applying the smoothing model. As in Section 6, we also compare the RMSE and degrees of freedom of the two fitted models; they are 0.1933 and 14.41 for the smoothing model and 0.1659 and 12.71 respectively for the proposed model. Thus, in terms of model selection, our model performs better across both model fit and model simplicity.

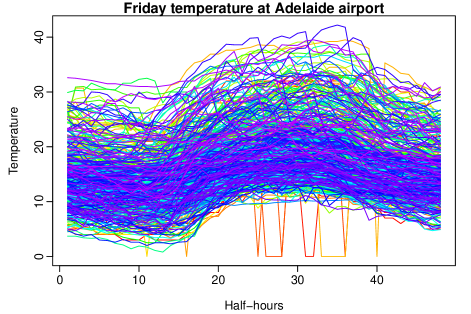

8.2 Australian temperature data

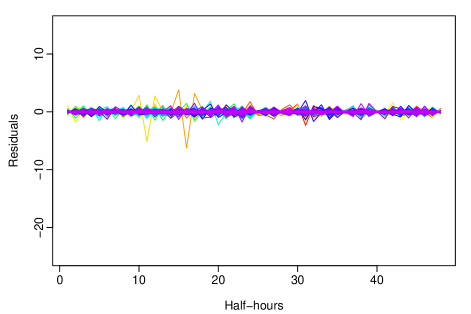

In this section, we consider Friday temperature data at Adelaide airport. We choose Adelaide because it tends to have the hottest temperature among Australia’s big cities. Data from other weekdays exhibit similar features and are not shown here. The data are measured every half an hour from the year 1997 to 2007. The sample size is 508, and the number of discrete data points from each curve is 48. The plot of the raw data can be found in Figure 10(a). It can be seen that the data are quite noisy, with extreme values in some of the curves due to large measurement errors.

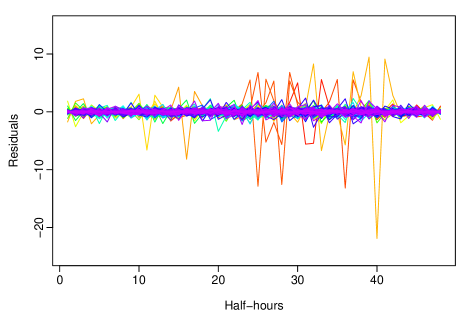

We use the B-spline basis functions of order 4 with knots at every data point. A penalized smoothing model is fitted to the data, with the tuning parameter selected to minimize the mGCV value. The residuals are shown in Figure 10(b). As can be seen, the smoothing model fails to capture the extreme values in the data.

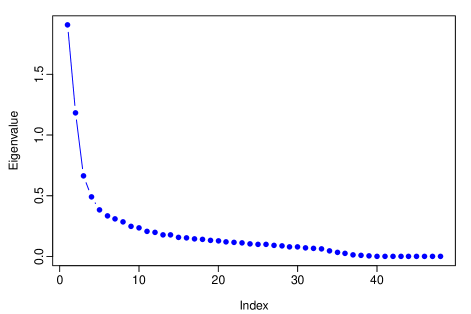

We check the residuals’ spikiness in Figure 10(b) by conducting a principal component analysis. The eigenvalues in descending order are shown in Figure 10(c). The first few eigenvalues are significantly larger than the rest. This means the residuals contain information captured by just a few factors, which calls for a further dimension reduction model on the residuals.

As a comparison, the FASM is also applied to the data. The tuning parameter for the smoothing part is selected based on mGCV at each step of the iteration. The number of factors retained in the factor model component is five. The residuals are shown in Figure 10(d). The extreme values are almost all removed from the remaining residuals.

9 Conclusion and future work

In this paper, we propose a factor-augmented smoothing model for functional data. We study raw functional data, which is a mixture of functional curves and high-dimensional errors. When measurement error is informative, a smoothing model alone is inadequate to capture data variation and recover the signal functional component. The proposed model incorporates a factor structure into the smoothing model to further explain the large residuals. We propose a numerical iteration approach to simultaneously obtain estimates in the smoothing model and the factor model. The asymptotic distribution of the estimators is given with proof. Our model also serves as a dimension reduction method on functional and high-dimensional mixture data, easing the path to making inferences. We provide an example of the construction of a covariance estimator for the raw data. Further, we show that the model can be applied in situations where there is misidentification in the data structure, two examples of which are the misspeficications of smoothing basis functions and the neglect of the step jumps in the mean level of the functions. The advantages of the proposed model are demonstrated in extensive simulation studies. We also show how our model performs via applications to Canadian weather data and Australian temperature data.

The proposed model is a good start point for modeling complex data structures. The data we deal with are a mixture of smooth functional curves and high-dimensional measurement error. The factor model component can be regarded as a ”boosting” component that improves model accuracy. Extending from this idea, the model can be applied to other data structures. One example is the data that contain change points. Change point is a popular problem in many statistics and econometric topics and has been extensively studies in the multivariate setting. Previous literature on change point in functional data include Berkes et al. (2009); Hörmann & Kokoszka (2010) and Hörmann et al. (2015). It is shown in simulation examples that our model can be used for modeling functional data with change point in the cross-sectional direction. The model can be modified to account for change point also in the sample direction. Further research can be conducted along this line.

References

- (1)

- Ahn & Horenstein (2013) Ahn, S. C. & Horenstein, A. R. (2013), ‘Eigenvalue ratio test for the number of factors’, Econometrica 81(3), 1203–1227.

- Akaike (1974) Akaike, H. (1974), ‘A new look at the statistical model identification’, IEEE Transactions on Automatic Control 19(6), 716–723.

- Bai & Ng (2002) Bai, J. & Ng, S. (2002), ‘Determining the number of factors in approximate factor models’, Econometrica 70(1), 191–221.

- Berkes et al. (2009) Berkes, I., Gabrys, R., Horváth, L. & Kokoszka, P. (2009), ‘Detecting changes in the mean of functional observations’, Journal of the Royal Statistical Society: Series B (Statistical Methodology) 71(5), 927–946.

- Bickel & Levina (2008) Bickel, P. J. & Levina, E. (2008), ‘Regularized estimation of large covariance matrices’, The Annals of Statistics 36(1), 199–227.

- Cai & Yuan (2011) Cai, T. T. & Yuan, M. (2011), ‘Optimal estimation of the mean function based on discretely sampled functional data: Phase transition’, The Annals of Statistics 39(5), 2330–2355.

- Cuevas (2014) Cuevas, A. (2014), ‘A partial overview of the theory of statistics with functional data’, Journal of Statistical Planning and Inference 147, 1–23.

- Eubank (1999) Eubank, R. L. (1999), Nonparametric Regression and Spline Smoothing, 2nd edn, Marcel Dekker, New York.

- Fan et al. (2008) Fan, J., Fan, Y. & Lv, J. (2008), ‘High dimensional covariance matrix estimation using a factor model’, Journal of Econometrics 147(1), 186–197.

- Fan & Gijbels (1996) Fan, J. & Gijbels, I. (1996), Local Polynomial Modelling and Its Applications, Chapman & Hall, London.

- Fan et al. (2011) Fan, J., Liao, Y. & Mincheva, M. (2011), ‘High dimensional covariance matrix estimation in approximate factor models’, The Annals of Statistics 39(6), 3320.

- Febrero-Bande et al. (2017) Febrero-Bande, M., Galeano, P. & González-Manteiga, W. (2017), ‘Functional principal component regression and functional partial least-squares regression: An overview and a comparative study’, International Statistical Review 85(1), 61–83.

- Ferraty & Vieu (2006) Ferraty, F. & Vieu, P. (2006), Nonparametric Functional Data Analysis: Theory and Practice, Springer Science & Business Media, New York.

- Goia & Vieu (2016) Goia, A. & Vieu, P. (2016), ‘An introduction to recent advances in high/infinite dimensional statistics’, Journal of Multivariate Analysis 146, 1–6.

- Golub et al. (1979) Golub, G. H., Heath, M. & Wahba, G. (1979), ‘Generalized cross-validation as a method for choosing a good ridge parameter’, Technometrics 21(2), 215–223.

- Green & Silverman (1999) Green, P. J. & Silverman, B. W. (1999), Nonparametric Regression and Generalized Linear Models: A Roughness Penalty Approach, Chapman & Hall, London.

- Hörmann et al. (2015) Hörmann, S., Kidziński, L. & Hallin, M. (2015), ‘Dynamic functional principal components’, Journal of the Royal Statistical Society, Statistical Methodology, Series B 77(2), 319–348.

- Hörmann & Kokoszka (2010) Hörmann, S. & Kokoszka, P. (2010), ‘Weakly dependent functional data’, The Annals of Statistics 38(3), 1845–1884.

- Horváth & Kokoszka (2012) Horváth, L. & Kokoszka, P. (2012), Inference for functional data with applications, Vol. 200, Springer Science & Business Media, New York.

- Jiang et al. (2020) Jiang, B., Yang, Y., Gao, J. & Hsiao, C. (2020), ‘Recursive estimation in large panel data models: Theory and practice’, Journal of Econometrics .

- Knight & Fu (2000) Knight, K. & Fu, W. (2000), ‘Asymptotics for lasso-type estimators’, The Annals of Statistics 28(5), 1356–1378.

- Lam et al. (2011) Lam, C., Yao, Q. & Bathia, N. (2011), ‘Estimation of latent factors for high-dimensional time series’, Biometrika 98(4), 901–918.

- Onatski (2010) Onatski, A. (2010), ‘Determining the number of factors from empirical distribution of eigenvalues’, The Review of Economics and Statistics 92(4), 1004–1016.

- Onatski (2012) Onatski, A. (2012), ‘Asymptotics of the principal components estimator of large factor models with weakly influential factors’, Journal of Econometrics 168(2), 244–258.

- Ramsay & Hooker (2017) Ramsay, J. O. & Hooker, G. (2017), Dynamic Data Analysis: Modeling Data with Differential Equations, Springer, New York.

- Ramsay & Silverman (2002) Ramsay, J. O. & Silverman, B. W. (2002), Applied Functional Data Analysis, Springer, New York.

- Ramsay & Silverman (2005) Ramsay, J. O. & Silverman, B. W. (2005), Functional Data Analysis, Springer, New York.

- Reiss et al. (2017) Reiss, P. T., Goldsmith, J., Shang, H. L. & Ogden, R. T. (2017), ‘Methods for scalar-on-function regression’, International Statistical Review 85(2), 228–249.

- Schwarz (1978) Schwarz, G. (1978), ‘Estimating the dimension of a model’, The Annals of Statistics 6(2), 461–464.

- Wahba (1990) Wahba, G. (1990), Spline models for observational data, Vol. 59, SIAM.

- Wand & Jones (1995) Wand, M. P. & Jones, C. M. (1995), Kernel Smoothing, Chapman & Hall, Boca Raton, FL.

- Wang et al. (2016) Wang, J.-L., Chiou, J.-M. & Müller, H.-G. (2016), ‘Functional data analysis’, Annual Review of Statistics and Its Application 3, 257–295.

- Wong et al. (2003) Wong, F., Carter, C. K. & Kohn, R. (2003), ‘Efficient estimation of covariance selection models’, Biometrika 90(4), 809–830.

- Yao & Li (2013) Yao, W. & Li, R. (2013), ‘New local estimation procedure for a non-parametric regression function for longitudinal data’, Journal of the Royal Statistical Society: Series B (Statistical Methodology) 75(1), 123–138.

- Zhang & Wang (2016) Zhang, X. & Wang, J. L. (2016), ‘From sparse to dense functional data and beyond’, The Annals of Statistics 44(5), 2281–2321.

Supplement to “Factor-augmented Smoothing Model for Functional Data”

Yuan GaoPostal address: Research School of Finance, Actuarial Studies and Statistics, Level 4, Building 26C, Kingsley St, Australian National University, Canberra, ACT 2601, Australia; Email: yuan.gao@anu.edu.au

Research School of Finance, Actuarial Studies and Statistics

Australian National University

Han Lin Shang

Department of Actuarial Studies and Business Analytics

Macquarie University

Yanrong Yang

Research School of Finance, Actuarial Studies and Statistics

Australian National University

This section contains the proofs for the theorems in the main article. In Appendix A, we provide the proofs for the theorems in Section 4. In Appendix B, we include the results of a proposition and its proof. In Appendix C, the lemmas used for the proofs in Appendix A and B are stated as well as their proofs.

Appendix A

Theorem 2 is the main result of the asymptotic theories, and the proof of it is lengthy. Thus, we include in the following the outlines for the proof before we show the details.

Outlines for proof of Theorem 2

In Theorem 2, we find the order of convergence of the estimated coefficient matrix . The difference between and could be written into three terms:

| (24) |

The term is . The first term on the right-hand side of (19) comes from the penalty, and the order can be found easily from Assumption 6. The third term contains the random error matrix , and the order can be found using the result in Lemma 10. The second term is the most complicated one, and we show in the following proof that it could be further broken down into eight terms. We find the order of each of the eight terms using the lemmas in Appendix C. Most of the terms can be shown to be and thus can be omitted. Combining the remaining terms, we arrive at the result

| (25) |

where matrix and are

The first term on the right-hand side of (Outlines for proof of Theorem 2) is using the assumption on the tuning parameter . We also show the second term is using results from the lemmas. When and are of the same order, we are able to show the norm of projected on the matrix is .

Next begins the formal proofs.

Proof of Theorem 1

Proof.

The concentrated objective function defined in Section 4.2 is

Assume for simplicity without loss of generality. From , we have

Denote the first three terms in the above equation as

Then by Lemma 4,

It is easy to see that for any invertible , because and .

Here we define two matrix operations before further transformations on . For an matrix and a matrix , the vectorization of is defined as

and the Kronecker product is the block matrix defined as

where represents the element on the th row and th column of matrix .

Next we can further write as

If we denote

and , then we can write

In the last equation,

By Assumption 2 and 3, the matrices and are positive definite for each . Thus we have . In addition, if either or , then . Thus achieves its unique minimum at . Thus we have

Next, we show is consistent uniformly in .

We can write

Using Taylor’s expansion at ,

where denotes the small order terms. Then we have

| (26) |

In the above equation, the right-hand side is uniformly in . This is because and and both consist of summations over . Furthermore, all other terms on the right-hand side are as proved in Lemma 4 and all contain summations over . On the left-hand side of (Proof.), is uniformly because as shown in Lemma 4 . Moreover, the term is also uniformly using Lemma 4 and that we assume are bounded uniformly in Assumption 2. This leads us to the result that

Combining the , we have

To prove part , note that the centred objective function satisfies and, by definition in (20), we have . Therefore,

Combined with , it must be true that

This implies that

Since , it must be true that

| (27) |

By Assumption 4, is invertible. Thus is also invertible. Next,

But (27) implies , which means . ∎

Proof of Theorem 2

Proof.

Writing the first equation in (10) in matrix notation, we have

| (28) |

Substitute into (28) and subtract the matrix on both sides, we get

or

| (29) |

We first look at the second term on the right-hand side of (29). Recall that . We have . Thus

where is defined in (43). Using (47), it follows that

| (30) | ||||

In the following, we calculate the order for each from to . Note that to are defined in (Proof.). Before we begin, for simplicity, denote

| (31) |

We prove in Lemma 5 that . We also use the fact that . Now

| (32) |

Since , using the result from Lemma 2 , the term is bounded in norm by . Thus it is also .

| (33) |

For the term , since it is not a small order term, we keep it as what it is.

Now consider

| (34) |

We take , where the order of each term can be found in Lemma 6 . Again using the result of Lemma 2 and , it can be shown that is .

It can also be proven that .

Then we consider

where the last equation comes from . Now

using Lemma 6. Thus,

| (36) |

where Proposition 1 is used in the first equation, and the second equation is a result of the calculation on the orders. Next

| (37) |

This term is not a small order term, so we keep it as what it is. And lastly, the proof of order for the term is too long, so we show in Lemma 11 that

| (38) |

Collecting terms from to , we can write (29) as

Combining the results we have found for and in Proof., Proof., Proof. and 38,

| (39) |

Substitute and from Proof. and Proof. into (Proof.), we have

| (40) |

We combine the two terms on the left-hand side of (Proof.) and also combine the second and third term on the right-hand side of (Proof.), then we get

Let , and . Left multiplying to both sides of the equation above, we have

where in the last equation, we substitute with using Lemma 8 and substitute with using Lemma 10. Note that in the result of Lemma 10 is dominated by . Next by multiplying a scale of ,

| (41) |

when and are of the same order, that is . ∎

Proof of Theorem 3

From (Proof.), we have when ,

Appendix B

In this section, we provide the proposition used in Appendix A, along with its proof.

Proposition 1.

Proof.

Write the second equation in (10) in a matrix form, we have

By (2), we also have

| (44) |

Plugging it in (44) and by expanding terms, we obtain

| (45) |

The above can be rewritten as

| (46) |

Right multiplying on each side, we obtain

| (47) |

Note that the matrix in the square brackets is , but the invertibility of hasn’t been proved yet. We can write

| (48) |

where is defined in (31) and is proved to be in Lemma 5. In the following, we find the order for each term on the right-hand side of (48). We repeatedly use results from Lemma 2, where the orders of the matrices and are given. The first term

For the second term

The terms to are all . The proofs are similar to the proof for since they are only a switch in the order of the matrices. For the sixth term

by Lemma 3 . Similarly, for the next term

For the last term

where Lemma 3 is used.

Putting all the above together, we have

| (49) |

To show , left multiply (46) by . Using , we have

where the last equality is using Lemma 2 and that from (Proof.). Thus,

We have shown in (27) that is invertible, thus is invertible. To obtain the limit of , left multiply (46) by to yield

or

| (50) |

because . Equation (50) shows that the columns of are the eigenvectors of the matrix , and that consists of the eigenvalues of the same matrix in the limit. Thus, , where the matrix is a diagonal matrix consisting of the eigenvalues of .

For , since is invertible, is also invertible we can write (Proof.) as

By right multiplying the matrix , we obtain .

∎

Appendix C

In this section, we state all the lemmas used for previous theorems and propositions, along with the proofs of the lemmas.

Proof.

For any vector ,

where is the th column in the matrix . Since we assume are i.i.d., the variance of the above quantity is given by

The Lindeberg condition is assumed to hold in Assumption 7. Thus we have a central limit theorem result

where is defined in (17).

∎

Proof.

In Assumption 1, we assume the basis functions are bounded. The basis matrix contains discrete evaluations on the basis functions so each element is , thus is of order . Similarly, using Assumption 3, we have results and . Using Assumption 4, we have result . Lastly, is directly from the restriction . ∎

Proof.

The proof of and is similar to ). For ,

where Assumption 4 is used. The proof of is the same. The orders of and are the same since

and

where the order of is assumed to be in Assumption 3.

∎

Proof.

We prove . First, we have

Since , we have

| (51) |

The first term on the right of (51) is since

where the third equation uses Assumption 5; the fourth equation uses the assumption that are independent in both directions.

The second term on the right-hand side of (51) is also since

where the third equality uses the independence in Assumption 5 and the last equality uses the results in Lemma 2, where and are both .

The proofs for and are similar. And is a direct result from Assumption 6. ∎

Proof.

The matrix is positive definite by Assumption 3. We have shown in the proof of Theorem 1 in (27) that the matrix is invertible, thus is also positive definite. Therefore, , and , where denotes the smallest eigenvalue of a matrix. So we have

∎

Lemma 6.

We have the following

-

(i)

-

(ii)

Proof.

For , from Proposition 1, we can write

To find the order for each term, the results from Lemma 2 are repeatedly used where the order of the matrices and are given.

where the order of is from Lemma 3 . The orders of , and can be found from Lemmas 2 and 5. Similarly,

where Lemma 3 is used.

where Lemma 3 is used.

where the order of is proved in Proposition 1 and the order of other matrix norms can be found in Lemma 3 and .

where Lemma 3 is used.

where the order of is proved in Proposition 1 and the order of other matrix norms can be found in Lemma 3 and .

Combining all the terms, we have

For , multiplying the matrix in the front does not change the order, using the fact that is of the same order as and that and are of the same order as , as proved in Lemma 3. ∎

Proof.

For , using (47)

| (52) |

It can be easily proved that the first five terms in (52) are using the results from Lemma 2 and 3. Recall that , and that from Lemma 5. For the sixth term,

using the results from Lemma 6. Next,

where the order of is found in Lemma 3 .

where Lemma 3 and Lemma 6 are used. Combining the terms, we have proved . The proof for is the same.

For , we can write

The order of the first term on the right can be found in Propostion 1. The order of the second term on the right is proved in . For , we have

where the orders of the two terms are proved in and . ∎

Proof.

Lemma 9.

Recall defined in Proposition 1, then

Proof.

Lemma 10.

Proof.

Using

we calculate

where we substitute with in the second equality. So the first term on the right-hand side of the first equality is broken down into four terms, one of which is combined with the second term in the right-hand side of the first equality.

For notation simplicity, we denote

| (55) |

which is used to represent the order in the result of Proposition 1.

We calculate each term:

where the order of is as proved in Proposition 1 and the order of can be found in Lemma 2 and 3 respectively. And when ,

where again Proposition 1 and Lemma 2 are used. And

where the second equality is using . In the third equality, we subtract from and then add it back.

For , when

where the order of , and are found in Lemma 2; the order of is found in Lemma 9; and the order of is found in Proposition 1. Now for , using the same lemmas and proposition,

which is when .

Thus combining the above terms, we have

when . ∎

Lemma 11.

Recall defined in (30), we have

Proof.

where we use . For ,

then

where the order of and are found in Lemma 3; the order of is from Proposition 1; and the orders of and are found in Lemma 2 and Lemma 5 respectively.

For ,

then

where the order of and are found in Lemma 3; the order of is from Proposition 1; and the orders of , and are found in Lemma 2 , and Lemma 5 respectively.

Combining and , we have

Since , the term is dominated by , thus

∎