Adaptive Random Bandwidth for Inference in CAViaR Models

January 29, 2021)

Abstract

This paper investigates the size performance of Wald tests for CAViaR models (Engle and Manganelli,, 2004). We find that the usual estimation strategy on test statistics yields inaccuracies. Indeed, we show that existing density estimation methods cannot adapt to the time-variation in the conditional probability densities of CAViaR models. Consequently, we develop a method called adaptive random bandwidth which can approximate time-varying conditional probability densities robustly for inference testing on CAViaR models based on the asymptotic normality of the model parameter estimator. This proposed method also avoids the problem of choosing an optimal bandwidth in estimating probability densities, and can be extended to multivariate quantile regressions straightforward.

JEL Codes: C22

Keywords: covariance matrix estimation in quantile regressions, CAViaR models, bandwidth choice, stability conditions for CAViaR DGPs.

1 Introduction

Financial risk management is at the heart of banks’ and financial institutions’ activities to guide them in their investment plans, supervisory decisions, risk capital allocations and for external regulations. The use of quantitative risk measures has become essential in financial risk management. One of the most popular risk measures associated with financial portfolios is the value at risk (VaR hereafter). The VaR at probability of a portfolio is defined as the minimum potential loss that the portfolio may suffer in the worst portion of all possible outcomes over a given time horizon. VaR is very intuitive (Duffie and Pan,, 1997) and has for instance been incorporated into the 1996 Amendment to the Capital Accord for measuring the market risk in financial positions of each financial institution. Therefore, VaR is still a widely used risk measure even though many approaches to measuring market and credit risks have been proposed in the literature.

Generally, there are three ways to estimate VaR: (i) historical simulations, (ii) semi-parametric approaches and (iii) fully parametric frameworks. Within the class of semi-parametric approaches, it typically includes extreme value theory analyses and quantile regression techniques. In this paper, we focus on quantile regressions for the VaR estimation as quantile regressions are straightforward in studying one quantile of interest and numerically efficient without imposing parametric distributional assumptions.

Despite that the VaR is just a particular quantile of future portfolio losses conditional on present information, it is essentially a part of the underlying conditional distribution. VaR models are supposed to embrace features of the empirical conditional distributions of returns, such as time-variation and conditional heteroskedasticity. Drawing on (G)ARCH specifications which capture the presence of time-varying conditional heteroskedasticity in time series, Engle and Manganelli, (2004) have proposed to estimate conditional autoregressive value at risk by regression quantiles (CAViaR). It is appealing to consider CAViaR models for estimating VaR as CAViaR models associate the conditional quantile of interest with observable variables as well as the implicit information on lagged conditional quantiles.

This paper carefully investigates the size performance of Wald tests for CAViaR models. Having an accurate test statistic is important to obtain reliable models in financial applications. Several specifications are nested within a CAViaR specification, such as static quantile regressive models and quantile autoregressive models (see Koenker and Xiao,, 2006; Hecq and Sun,, 2020). Moreover, there exists several models nested within the general CAViaR specification that have been proposed in the literature. For instance, asymmetric slope CAViaR models (Engle and Manganelli,, 2004) that split the effect of positive and negative yesterday’s news shocks. Wald tests are used to test the null of a symmetric news impact. However, we find that the usual estimation strategy yields inaccuracies. Indeed, we show that existing density estimation methods cannot adapt to the time-variation in the conditional probability densities of CAViaR models. The method that we develop in this paper is able to adapt to time-varying conditional probability densities and produces much more reliable results than the existing ones for inference testing on CAViaR models based on the asymptotic normality of the model parameter estimator. This proposed method also avoids the haunting problem of choosing an optimal bandwidth in estimating probability densities, and can be extended to multivariate quantile regressions straightforward in theory.

The remainder of this paper is structured as follows. In Section 2, stability conditions for CAViaR data generating processes (DGPs) to be non-explosive are derived. In Section 3, we investigate the size performance of Wald tests for CAViaR models and find large size distortions by the usual estimation strategy. So we introduce a method called adaptive random bandwidth. An empirical study on stock returns is performed in Section 4. Finally Section 5 concludes this paper.

2 The CAViaR model

Let us consider a stationary time series process for instance the return of an asset or a portfolio, and denote a vector of observable variables at time and the information set up to time which is the -algebra generated by . The -th quantile () or the opposite of conditional on is denoted as (or simply when is taken in obviously). A generic CAViaR specification proposed by Engle and Manganelli, (2004) is

| (1) |

where collects the slope parameters, and is a function of a finite number of lagged observable variables, for instance the lagged returns entering potentially with different weights for positive and negative past lagged returns. As described in Engle and Manganelli, (2004) the autoregressive terms can ensure that the quantile changes smoothly over time. The quantile autoregressive model (QAR) of Koenker and Xiao (2006) is nested in the CAViaR specification by restricting in CAViaR. The role of is to account for the association of with observable variables in . CAViaR models as a generalization of QAR models are able to capture the time-variation in the conditional quantile in a way similar to GARCH models in explaining time-varying volatility and volatility clustering in financial time series in addition to ARCH models.

The CAViaR model (1) is nonlinear in parameters as long as there exists a nonzero which leads to not independent of .111In Appendix A, the gradient and the Hessian matrix of CAViaR models are illustrated to emphasize that the nonlinearity of model parameters makes CAViaR models different from other linear quantile regression models. The algorithm to estimate CAViaR models is given in Section 2.2.

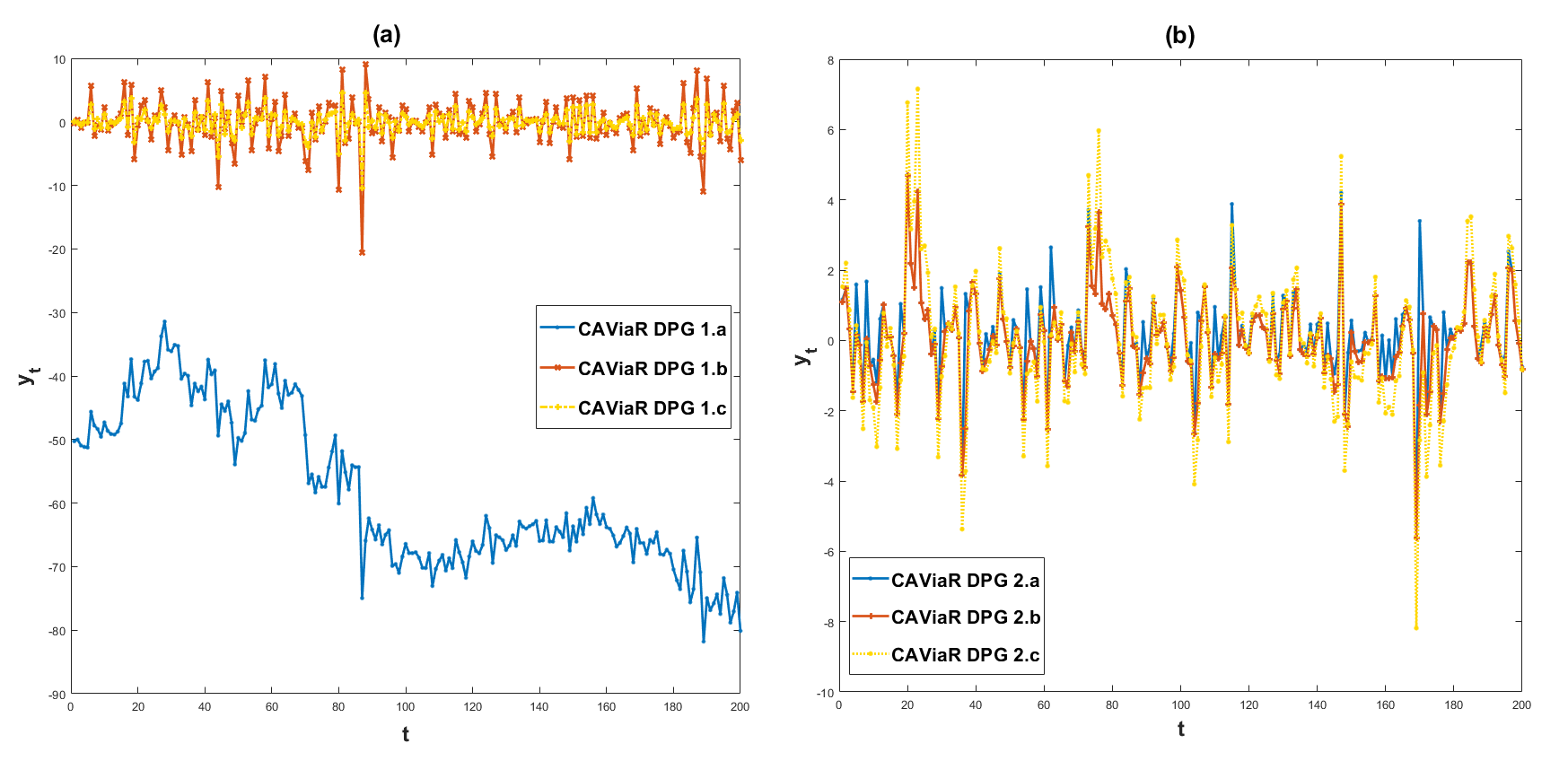

For illustration, we simulate samples from the following three CAViaR DGPs in (2) and plot Figure 1 (a). 222All the simulations of CAViaR DGPs in this paper follow the procedure given in Appendix B. In Figure 1 (a), we see a decreasing trend in CAViaR DGP 1.a mainly due to the negative term in compared with CAViaR DGP 1.b. Comparing CAViaR DGP 1.b with 1.c, we find that CAViaR DGP 1.b has a larger spread due to a higher slope of in . A similar finding further applies on Figure 1 (b) which plots simulated samples of CAViaR DGP 2.a, 2.b and 2.c in (3) respectively.

| (2) |

where is i.i.d. in the standard uniform distribution (denoted as ) and is the inverse function of Student’s t-distribution with degrees of freedom ( hereafter).

| (3) |

where , .

2.1 The stability conditions for CAViaR models

The stationarity of CAViaR time series is required for the model estimation consistency (Engle and Manganelli,, 2004). After simulating a CAViaR DGP, we can view its behaviour such as explosiveness in the long run. We know that a time series is explosive if and only if at least one conditional quantile of the time series with nonzero probability density to occur is explosive. So we derive stability conditions for the conditional -th () quantile of a CAViaR DGP specified as follows:

| (4) |

where , and with . There is a monotonicity requirement on this model which is that is monotonically increasing in so that the -th quantile () of conditional on can be expressed as .

Assume the conditional -th quantile of follows the model (4) with nonzero probability density to occur at each time. Without loss of generality, there is a time such that

Now let us derive the value of . First we have the following equation from (4).

where the second line is obtained by substituting the specification (4) of into the first line, and is the lag operator. Further rewrite the above equation, and we have

We continue to rewrite the lagged terms of on the right-hand side of the above equation, and then organize the equation such that only the left-hand side contains terms of . Therefore, we obtain that

|

|

(5) |

Now we can get the first necessary condition for to be nonexplosive, which is

| (6) |

Under the condition (6), we can simplify the equation (5) when letting as follows:

Now we obtain the autoregressive polynomial of which is

| (7) |

So the second necessary condition for to be nonexplosive is that the roots of are outside the unit circle. When there exists at least one , this second condition is equivalent to require that the roots of and the common roots of and all are outside the unit circle. More examples of CAViaR DGPs are illustrated in Appendix D, among which we can find explosive DGPs which break the condition on the roots of but meet the condition on the common roots of and .

We can review Figure 1 with the above stability conditions. CAViaR DGP 1.b, 1.c, 2.b and 2.c meet the above conditions and we also see their nonexplosive behaviours in the plots. The nonexplosiveness of CAViaR DGP 2.a can also be ensured since it has a narrower spread in theory in comparison with CAViaR DGP 2.b. On the other hand, we know that CAViaR DGP 1.a has a downward trend due to the negative term and hence is explosive.

2.2 Estimation algorithm

The estimation for CAViaR models can be achieved by the differential evolutionary genetic algorithm (Storn and Price,, 1997) used by Engle and Manganelli, (2004). Suppose the model is specified as (1) for data . We want to obtain the parameter estimator by the following optimization:

| (8) |

where is the objective function in quantile regressions, and is called check function (Koenker,, 2005) with the indicator function .

Following the steps below, we can obtain in (8).

-

Step 1:

Generate (say ) trial vectors independently from a uniform distribution as parameter initial trials, where and are vectors roughly covering the lower and upper bounds of the true parameter vector of the underlying process in our belief. It is worth mentioning that the values of and acting as initial conditions are also input-demanded in order to calculate for any . For instance, as used by Engle and Manganelli, (2004) is given as the estimated -th quantle of and is fixed in the optimization.333 is known as the floor function (or the greatest integer function) and of a real number denotes the greatest integer less than or equal to .

-

Step 2:

Each parameter initial is used to kick off a minimization routine444 The Nelder Mead simplex algorithm is used in our minimization routine. on the objective function , and the returned value of from the routine and its objective function value are stored.

-

Step 3:

Select (say 10) returned vectors of which result in the lowest values among the stored objective function values.

-

Step 4:

Denote the selected vectors as and use them as initials to restart the minimization routine individually, and update with the newly returned vectors respectively.

-

Step 5:

Repeat Step 4 (say ) times.

-

Step 6:

Calculate . And set the solution to be .

We implement the above estimation algorithm throughout this paper for CAViaR model parameter estimations. There might be a concern if the artificial input of the initial values and affects the parameter estimator. In fact, the effect usually is small and can be neglected when the sample size is large enough because the fitted conditional quantiles are kept close to the true ones such that it can minimize the objective function despite some burn-in period.

3 Adaptive random bandwidth method for CAViaR covariance matrix estimation

Consistency and asymptotic normality of CAViaR model parameters have been proved by Engle and Manganelli, (2004). After regressing data onto a CAViaR model, we would like to implement an inference testing on whether the model is correctly specified. In this section we first investigate how we result in the asymptotic normality of CAViaR model parameter estimators. We focus on the elements of the asymptotic covariance matrix to highlight their roles in connecting sample elements with the corresponding limit behaviours. Next, we check whether existing estimation strategies can perform robustly and satisfactorily for Wald tests on CAViaR models. Finally, we propose a new method called adaptive random bandwidth for CAViaR models.

3.1 Asymptotics of CAViaR

Consider a time series of random variables on a complete prbability space 555See the assumption C0 of Engle and Manganelli, (2004). We also apply this assumption throughout this paper. That is to say, all the random variables considered in this paper are assumed on a complete prbability space . . For applying a generic CAViaR model (1) on , the consistency and asymptotic normality of the estimator has been derived out by Engle and Manganelli, (2004):

Theorem 1 (Asymptotics given by Engle and Manganelli, (2004))

For a data generating process with its time conditional -th quantile following a generic CAViaR model as (1) parametrized by , it satisfies the regularity conditions (C0,…, C7, AN1,…, AN7) in the proof of Engle and Manganelli, (2004). Then

| (9) |

where

| (10) | ||||

and is denoted as the probability density of evaluated at conditional on the information set . is the identity matrix.

The above theorem is useful for quantile model (mis)specification tests. For instance, Wald tests can be used to check whether the current model is correctly specified by testing the validity of a more parsimonious nested model. To perform such a quantile model specification test, it often requires to estimate , and . When using traditional estimates , , of , and respectively, we found considerable size distortions in inference tests on CAViaR models in general. We will show that the reason lies in the inaccuracy of in the next subsection. In order to spot the discrepancy in approximating , we need a clear picture on how comes up into the asymptotic normality of the model parameter estimator. Doing so, we can see the role of and whether a sequence is capable to achieve the same role in practice. Let us review the proof of Engle and Manganelli, (2004) for Theorem 1 below.

The proof of Engle and Manganelli, (2004) is obtained by applying Theorem 3 of Huber et al., (1967) onto and the central limit theorem onto . Huber’s conditions are verified in the proof before applying Huber’s theorem. Denote

| (11) | ||||

gives value every time exceeds and otherwise. With the true underlying parameter , is a martingale difference sequence with respect to . It is easy to get that follows the central limit theorem because is a martingale difference sequence with the assumption AN1 of Engle and Manganelli, (2004) on its uniformly bounded second moment. So we get that

| (12) |

It has also been proved by Engle and Manganelli, (2004) that

| (13) |

Next, we are going to manifest in the proof in a way which makes the appearance of more intuitive. We rewrite as follows:

| (14) | ||||

Take expectation on the both sides of Equation (14) and get

| (15) | ||||

where is the supremum norm of vectors. And

| (16) | ||||

where is the probability density function of conditional on , and . Substituting (16) into (15) gives

| (17) | ||||

Success in applying Huber’s theorem gives

| (18) |

Therefore, the asymptotic normality of is obtained by substituting (12) and (17) into (18).

From the above derivation, it is clear that the role of is actually an approximation to in which is between and . This role comes to the surface of (16) using the fact that

| (19) |

by the Mean Value Theorem. This approximating role of sets a clear mission of any supposed to achieve, which can be used to examine an estimator for as well as to propose an improved estimation method. In next subsection, we are going to examine the performances of some existing methods for estimating and the role of will help to find out the intrinsic defects of those methods.

3.2 Existing methods for CAViaR covariance matrix estimation

Based on the literature on quantile regressions, in general there are two ways to estimate in with being potentially non-i.i.d.. One is referred to as the Hendricks Koenker Sandwich Approach (Hendricks and Koenker,, 1992; Koenker,, 2005) analogous to the finite difference idea resulting in the estimator for as follows:

| (20) |

where is subject to with as . The other one is referred to as the Powell Sandwich (Powell,, 1991; Koenker,, 2005) based on the kernel density estimation idea resulting in the estimator for as follows:

| (21) | ||||

where is a suitable kernel function with bandwidth and as . As we can see in (21), one kernel function is applied throughout with being the only distinguishable information for . Therefore, this kernel method does not capture sufficient information to distinguish time-varying conditional distributions of , and consequently cannot fully adapt to the time-variations. Additionally, the choice of the kernel function and the bandwidth parameter are still in a lot of nettlesome questions in practice. A similar issue in the Hendricks Koenker Sandwich Approach is on choosing and extra error resulted from estimating and .

The estimation method adopted by Engle and Manganelli, (2004) is a form of the Powell Sandwich as follows:

| (22) |

As suggested by Koenker, (2005) and Machado and Silva, (2013), the bandwidth generally adopted is defined as follows:

| (23) |

where is defined as

| (24) |

with and being the cumulative distribution and probability density functions of respectively. And is defined as the median absolute deviation of the conditional -th quantile regression residuals.

Wald tests are applied in this subsection to check the performances of the above estimation methods for CAViaR models.

First, we consider the following candidate model specifications for the conditional -th () quantile of a time series with denoted as the -th quantile of conditional on the information set .

The models (26) and (27) are nested within model (25). Now let us consider the Wald test on models (25) and (26) first. Simulate a time series with its DGP specified as the model (26) with the underlying parameter vector , where and is the inverse standard normal probability distribution function. The sample size of each simulated sample is . Conditional -th quantiles are estimated for each of total simulated samples in this DGP by regressing the sample onto the full model (25). The Wald test implemented here consists of the null hypothesis of the form , where , , and is the estimator of the full model parameter vector in (25). The Wald test statistic denoted by is formulated (Weiss,, 1991) as follows:

| (28) |

where and are estimates for and in (10) respectively. It is straightforward to obtain and by plugging in and , i.e.,

Notations on to distinguish different estimators used for are given by

| (29) |

| (30) |

where is determined as (23).

We are going to examine each element in the estimation of . The analytic solution to can be obtained as follows:

| (31) | ||||

where . The last line is obtained by knowing . The analytic solution to is used to help identify inaccurate elements in by comparing the test performances of using , and the following

| (32) |

The test performances of using , and are shown in Table 1 and 2, which are compared together with the Wald test result using the true underlying parameter vector into

| (33) | ||||

where is the probability density function of .

The size performances of the Wald tests on the models (25) and (26) using different estimators are listed in Table 1 in which each estimated size is obtained by the percentage rejection rate among the 1000 samples of in the DGP (26). Analogously, we implement the Wald test on models (25) and (27) with the underlying DGP specified as the model (27) with the underlying parameter vector , where . The number of observations in each stimulated sample from this DGP is . Conditional -th quantiles are estimated for each of simulated samples by regressing the sample onto the full model (25). The Wald test implemented in this case consists of the null hypothesis of the form , where , , and is the estimator of the full model regression (25). In result, the size performances of the Wald tests on (25) and (27) are listed in Table 2.

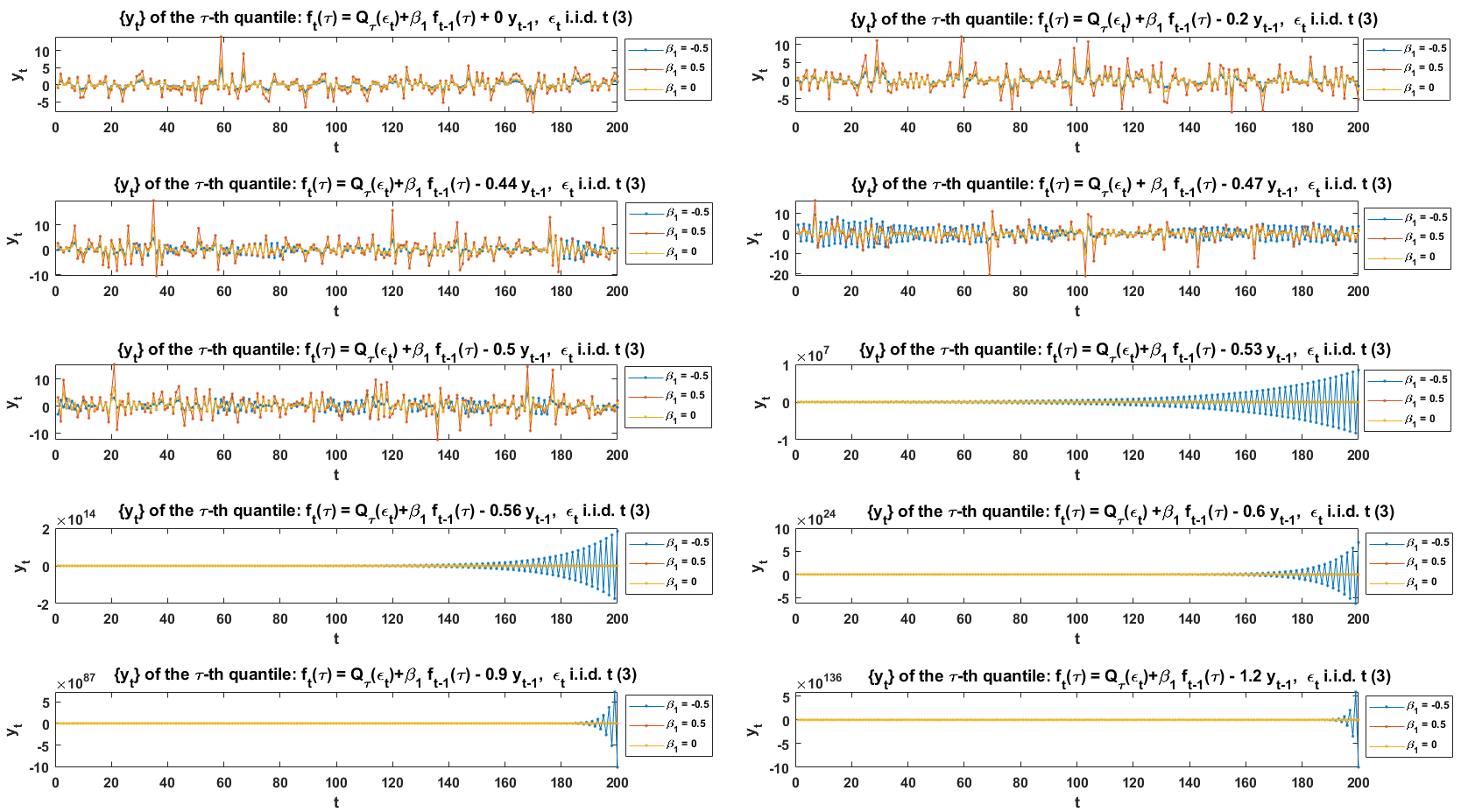

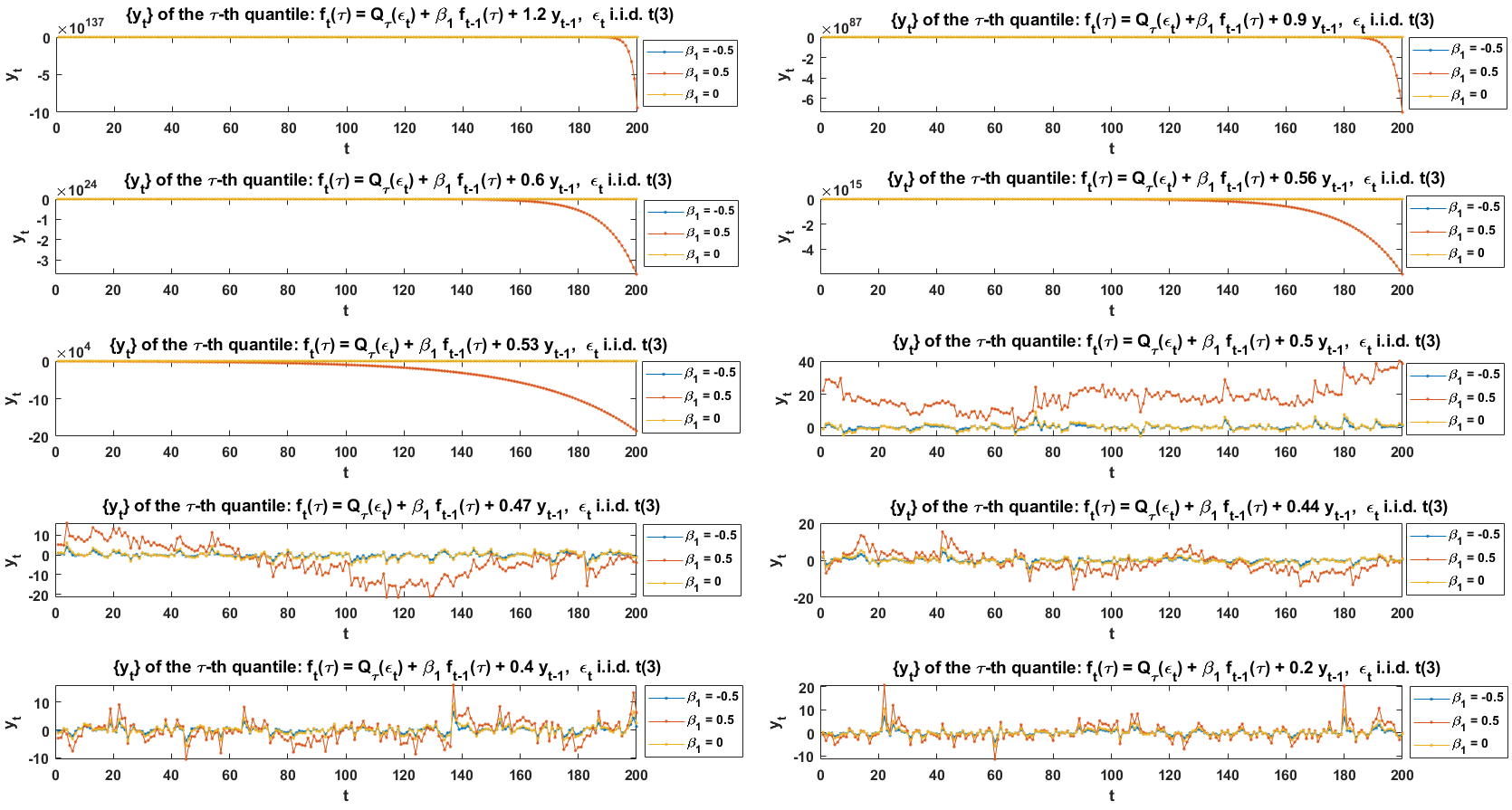

From Table 1 and 2, we can see large size distortions with , unlike , or that are performing in line with the nominal size. This comparison points out the crucial element estimation to the accuracy of which is . To check whether is capable to achieve the role of robustly for time-varying conditional probability densities, we consider the following DGP:

| (34) | ||||

| (35) |

where and the underlying parameters are given as . The analytic form of the corresponding conditional probability density of at its -th quantile given can be derived out as follows:

| (36) | ||||

where the first equation is obtained by iteratively rewriting at each and knowing . This analytic form of in (34) shows that indeed is time-varying and nonzero with probability one.

We simulate samples from the DGP (34) with , and estimate the conditional -th quantiles of each sample by regressing the sample onto the full model specification (35). The Wald test described as (28) with is performed on these samples and the size performance is presented in Table 3. We see a large size distortion with the kernel method in Table 3. More tests are conducted for different DGPs and together with the results are presented in Appendix E. Based on our test results, we see that the kernel method for estimating is not robust and cannot fully adapt to time-varying conditional probability densities.

Estimating robustly has to be achieved in order to ensure the reliability of CAViaR analysis based on the asymptotic properties of CAViaR model parameter estimators. In seeking for improving the accuracy of , we bear in mind two guidances. One is the role of on how it links sample elements with the corresponding limit behaviours, see Section 3.1. The other guidance is the fundamental flaws of and in their accuracy. In terms of , needs to be determined properly and two more quantile regressions need to be preformed in order to obtain and . The effect of this extra estimation error is crucial to the performance of . Although does not need extra quantile regressions, it still requires a proper choice on the kernel function and the bandwidth . Remarkably, does not differentiate the observations within the bandwidth regardless of the number of the observations in the bandwidth while using the kernel function . Therefore, it is desirable to get rid of choosing bandwidth or and the kernel function in the estimation. In the next subsection, a robust estimation method for is developed up without the need in choosing a bandwidth or a kernel function.

3.3 Adaptive random bandwidth method

We have noticed that the accuracy of the estimation is crucial to the performance of inference tests based on the asymptotic normality of CAViaR model parameter estimators. It is also well known that suffers both from the error in estimating and and from choosing a proper . On the other hand, has some fundamental problems. First of all, cannot fully adapt to time-varying conditional distributions of time series due to the fact that the same kernel function and only timely information are used in estimating for all t. Second, finding a proper kernel function with a proper bandwidth still faces a lot nettlesome problems in practice. Neither of these two methods is practically robust. The goal in this subsection is to develop an estimation method for which can adapt to time-variation characteristics of CAViaR DGPs and is robust in practice without the need to determine a proper bandwidth. We name this estimation method as the adaptive random bandwidth (ARB) method which can reliably bridge asymptotic properties of CAViaR models in theory with CAViaR applications.

The idea of this method is inspired by viewing the role of on how it links sample elements with the corresponding limit behaviours, see Section 3.1. Reviewing equation (16), we can explicitly formulate as follows:

| (37) |

which actually is a conditional expectation taken with respect to random variables and . We use the subscript in to clarify the expectation is taken with respect to specific random variable(s) hereafter. Considering this role of as well as equation (19), we are enlightened to use random bandwidth with and . We can set to start with. After sufficient times Monte Carlo simulating from , an estimator of can be achieved as follows:

| (38) |

After achieving the above , we can estimate so as to update . Redo the simulation of with the updated . We can estimate and again. This estimation repetition can mitigate the influence of an arbitrary chosen in ARB.

Compared to the Powell Sandwich estimation (21) with , our proposed method uses random bandwidth and Monte Carlo simulations such that it can adapt to time-varying conditional distributions of CAViaR DGPs by approaching to the role of as in (19) and in (37). The adaptive random bandwidth method can remarkably outperform the Powell Sandwich method in the applications on DGPs of time-varying conditional distributions, as shown in Table 3. In theory, the adaptive random bandwidth method is valid as long as and have the same order of magnitude. We formally establish this adaptive random bandwidth method in Theorem 2.

Theorem 2 (Adaptive Random Bandwidth Method)

Assume the conditions and the asymptotic normality result in Theorem 1. Choose an arbitrary positive definite symmetric matrix . Under the condition that

| (39) |

and

the adaptive random bandwidth estimator for is formulated as follows:

|

|

(40) |

such that

as . 666 We regard the least absolute residuals in as zeros. In fact, iterations of a simplex-based direct search method like the Nelder–Mead method for optimizing parameters terminates at the vertices of a simplex in the parameter space (Lagarias et al.,, 1998). That is to say, the iterations in optimizing the -th quantile regression objective function terminate with elements of solved to be zeros. Therefore, we set at the least absolute residuals in in all the tests throughout this paper.

Proof. See Appendix C.

We separate the case of from others to maintain the convergence of the ARB estimator due to . Zero given to at also enables the ARB estimator to approximate from the left and from the right in half weights respectively in expectation, see the proof of Theorem 2. The convergence property of the partial sum in the sequence by ARB is given in Corollary 3.

Corollary 3

Under the conditions of Theorem 2, the adaptive random bandwidth estimator has the following property:

| (41) |

as .

Proof. See Appendix C.

It is clear that both and are taken into account by ARB to approximate . In order to identify how and jointly shape , we would like to formulate in Theorem 2 into an analytic expression in terms of and so as to manifest the relationship. The analytic form of by ARB described in Theorem 2 is presented in Corollary 4.

Corollary 4

Under the conditions of Theorem 2, we can get the analytic form of as follows:

| (42) |

where , , and is a special integral known as the exponential integral or the incomplete gamma function .

Proof. See Appendix C.

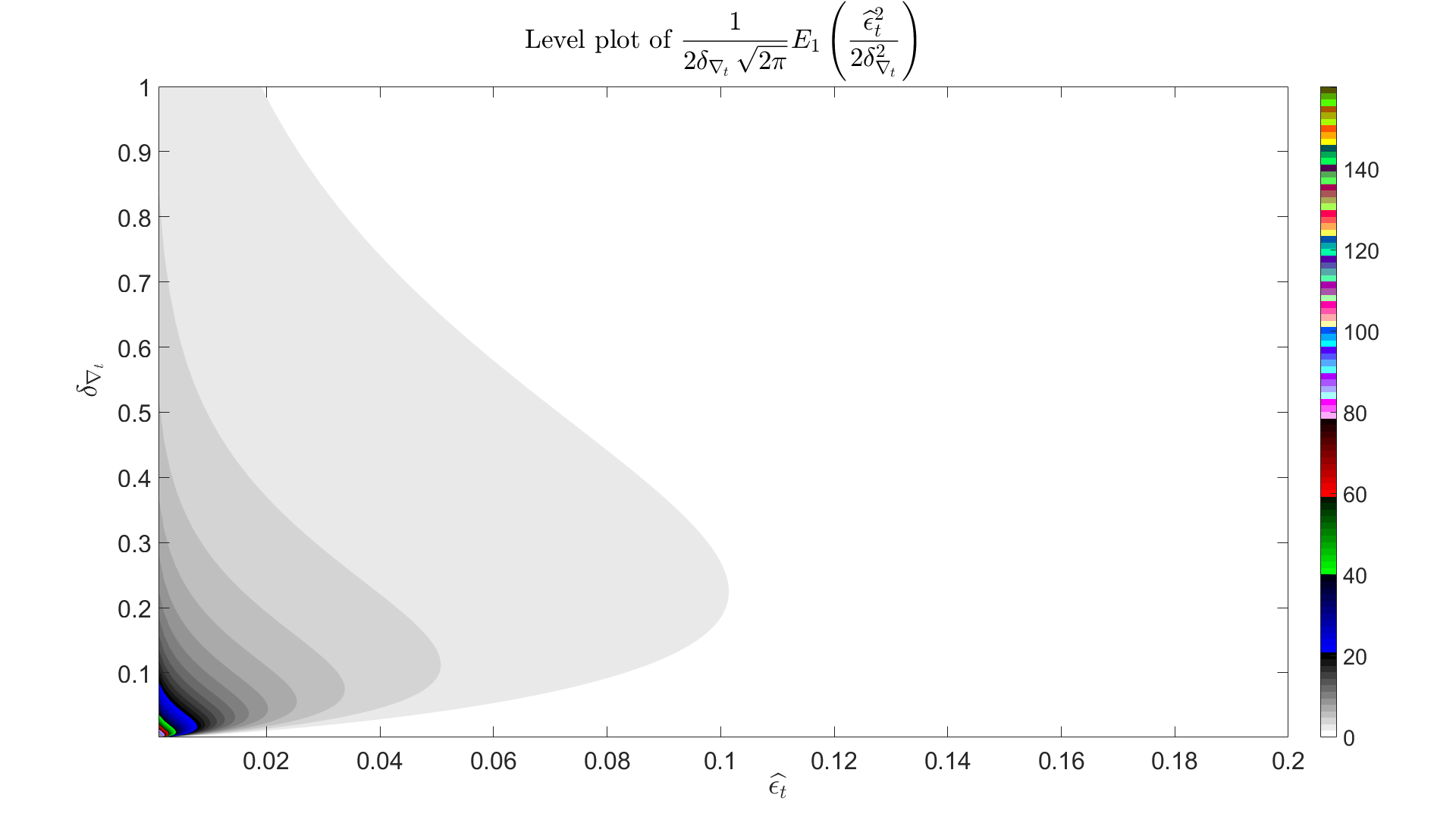

For visually checking the roles of and in the analytic in Corollary 4, we present a level plot of the analytic over and in Figure 2 which uses colors to differentiate different ranges of . It is straightforward to get that the analytic is decreasing in as also shown in Figure 2. However, , or say , can shift by reflecting on how rare an is observed given the information set and the model specification. That is how the information of in ARB shapes adaptively to time-varying conditional probability densities.

The ARB estimator via simulations in Theorem 2 performs as robustly as the analytic ARB estimator in Corollary 4, as shown in Table 1, 2 and 3. The analytic way is faster than the simulation one. However, the ARB estimator via simulations is more intuitive and more flexible to adapt to a very different distribution for simulating .

need to be estimated consistently for inference tests on CAViaR models based on the asymptotic normality of the model parameter estimator. by ARB facilitates our estimation on by just plugging in and . The resulted estimator has the consistency property presented in Theorem 5.

Theorem 5

Proof. See Appendix C.

The adaptive random bandwidth (ARB) method is intuitive, robust and simple in practice, which can adapt to time-varying conditional distributions without a specific bandwidth or kernel function. A comparison of size performances of Wald tests using ARB with other competing methods are presented in Tables 1, 2 and 3. We also find that updating improves the size performance with use of levels in the interquartile range around but not much for levels like . More test results are presented in Appendix E with changing sample size, quantile index and varying DGPs. The performance of ARB is robust. ARB can also be easily generalized to apply on multivariate quantile regressions, which is beyond the scope of this paper but in the interest of multivariate quantile regressions for future research. ARB also has the potential to achieve the second-order accuracy to Wald tests of nonlinear restrictions (Phillips and Park,, 1988; de Paula Ferrari and Cribari-Neto,, 1993) in quantile regressions, which we would like to leave for future research.

| Tests | size: | |||

|---|---|---|---|---|

| Using | 0.017 | 0.063 | 0.127 | 0.215 |

| Using | 0.016 | 0.066 | 0.131 | 0.215 |

| Using (, with no update) | 0.012 | 0.052 | 0.098 | 0.196 |

| Using (analytic, with no update) | 0.012 | 0.052 | 0.102 | 0.198 |

| Using (, 2 times updating ) | 0.014 | 0.062 | 0.126 | 0.221 |

| Using (analytic, 2 times updating ) | 0.014 | 0.061 | 0.125 | 0.219 |

| Using () | 0.080 | 0.150 | 0.201 | 0.272 |

| Using | 0.017 | 0.069 | 0.129 | 0.223 |

| Tests | size: | |||

|---|---|---|---|---|

| Using | 0.008 | 0.050 | 0.104 | 0.206 |

| Using | 0.007 | 0.050 | 0.105 | 0.207 |

| Using (, with no update) | 0.01 | 0.046 | 0.084 | 0.168 |

| Using (analytic, with no update) | 0.009 | 0.044 | 0.083 | 0.168 |

| Using (, 2 times updating ) | 0.011 | 0.049 | 0.098 | 0.192 |

| Using (analytic, 2 times updating ) | 0.01 | 0.048 | 0.097 | 0.19 |

| Using () | 0.049 | 0.104 | 0.153 | 0.229 |

| Using | 0.011 | 0.05 | 0.094 | 0.203 |

| Tests | size: | |||

|---|---|---|---|---|

| Using (, with no update) | 0.024 | 0.052 | 0.095 | 0.169 |

| Using (analytic, with no update) | 0.023 | 0.054 | 0.093 | 0.168 |

| Using (, 2 times updating ) | 0.021 | 0.055 | 0.095 | 0.188 |

| Using (analytic, 2 times updating ) | 0.022 | 0.055 | 0.098 | 0.186 |

| Using | 0.067 | 0.118 | 0.16 | 0.256 |

4 Empirical Results

We study four US stock prices which are the Dow Jones Composite Average (DJCA), the NASDAQ 100 Index (NASDAQ100), the S&P 500, and the Wilshire 5000 Total Market Index (Will5000ind). We implement inference tests using the adaptive random bandwidth method with and which is not updated in simulations in this section. Each stock price time series has 2448 daily prices, ranging from 8th April 2010 to 30th December 2019. The price data were converted to return rates by multiplying 100 with the difference of the natural logarithm of the daily prices. The obtained return time series of each stock contains 2447 observations which of the last 400 observations are used for the out-of-sample testing after the first 2047 observations are used to estimate the model.

The 1-day VaRs of a return time series are the opposite conditional 1-day quantiles of this time series. There are four different CAViaR models considered in this section to model the conditional quantiles of the stock return time series. The 1-day VaRs are estimated via the four different CAViaR specifications and the estimation results are shown in Table 4, 5, 6 and 7 respectively. Each table contains the estimated parameters in a specified model, the corresponding standard errors obtained by the adaptive random bandwidth method with and , the resulted two-sided p-values on parameter significance, the optimized value of the quantile regression objective function (RQ), the percentage of times the VaR is exceeded, and the p-values of dynamic quantile (DQ) tests, both in-sample and out-of-sample. The model estimations, the in-sample DQ tests as well as the out-of-sample DQ tests in this empirical study are set up in the same way of Section 6 of Engle and Manganelli, (2004).

The above four CAViaR specifications have been defined as the adaptive CAViaR, the symmetric absolute value CAViaR, the asymmetric slope CAViaR, and the indirect GARCH respectively in the Section 3 of Engle and Manganelli, (2004). In the implementation of the adaptive model in this emprical study, we follow Engle and Manganelli, (2004) and set .

| Stock Name | DJCA | NASDAQ100 | S&P500 | Will5000ind |

|---|---|---|---|---|

| -0.0538 | -0.1366 | -0.0772 | -0.0803 | |

| s.e.() | 0.0192 | 0.0324 | 0.0283 | 0.0259 |

| p-value() | 0.0051* | 0.0000* | 0.0063* | 0.0019* |

| 0.8913 | 0.8536 | 0.8651 | 0.8613 | |

| s.e.() | 0.0276 | 0.0356 | 0.0344 | 0.0344 |

| p-value() | 0.0000* | 0.0000* | 0.0000* | 0.0000* |

| -0.0175 | 0.0381 | 0.0264 | 0.0158 | |

| s.e.() | 0.0325 | 0.0717 | 0.0732 | 0.0831 |

| p-value() | 0.5918 | 0.5950 | 0.7179 | 0.8487 |

| -0.3069 | -0.3626 | -0.4249 | -0.4226 | |

| s.e.() | 0.0667 | 0.0673 | 0.1214 | 0.1153 |

| p-value() | 0.0000* | 0.0000* | 0.0005* | 0.0002* |

| RQ | 205.1100 | 253.9000 | 215.3800 | 219.3200 |

| Exceedance in-sample ( ) | 5.0166 | 5.0639 | 5.0166 | 5.0166 |

| Exceedance out-of-sample | 4.7326 | 4.8746 | 4.5906 | 4.5433 |

| DQ in-sample (p value) | 0.4306 | 0.5140 | 0.3094 | 0.4425 |

| DQ out-of-sample (p value) | 1.0000 | 1.0000 | 1.0000 | 1.0000 |

| Stock Name | DJCA | NASDAQ100 | S&P500 | Will5000ind |

|---|---|---|---|---|

| -0.0507 | -0.1310 | -0.0544 | -0.0521 | |

| s.e.() | 0.0405 | 0.0641 | 0.0430 | 0.0315 |

| p-value() | 0.2103 | 0.0410* | 0.2064 | 0.0984 |

| 0.8546 | 0.8127 | 0.8495 | 0.8676 | |

| s.e.() | 0.0418 | 0.0629 | 0.0544 | 0.0324 |

| p-value() | 0.0000* | 0.0000* | 0.0000* | 0.0000* |

| -0.2375 | -0.2492 | -0.2485 | -0.2161 | |

| s.e.() | 0.0266 | 0.0785 | 0.0775 | 0.0311 |

| p-value() | 0.0000* | 0.0015* | 0.0013* | 0.0000* |

| RQ | 210.7300 | 263.0400 | 223.5300 | 227.3200 |

| Exceedance in-sample () | 5.0166 | 5.0166 | 5.0166 | 5.0166 |

| Exceedance out-of-sample () | 5.3952 | 5.2532 | 4.9219 | 4.9692 |

| DQ in-sample (p value) | 0.2306 | 0.3548 | 0.0470* | 0.1537 |

| DQ out-of-sample (p value) | 1.0000 | 1.0000 | 1.0000 | 1.0000 |

| Stock Name | DJCA | NASDAQ100 | S&P500 | Will5000ind |

|---|---|---|---|---|

| 0.0651 | 0.2152 | 0.0878 | 0.0758 | |

| s.e.() | 0.0325 | 0.1069 | 0.0384 | 0.0414 |

| p-value() | 0.0450* | 0.0442* | 0.0223* | 0.0670 |

| 0.8741 | 0.7930 | 0.8290 | 0.8566 | |

| s.e.() | 0.0247 | 0.0444 | 0.0261 | 0.0258 |

| p-value() | 0.0000* | 0.0000* | 0.0000* | 0.0000* |

| 0.2551 | 0.3775 | 0.3638 | 0.2964 | |

| s.e.() | 0.2169 | 0.2031 | 0.2096 | 0.2041 |

| p-value() | 0.2395 | 0.0631 | 0.0826 | 0.1465 |

| RQ | 209.4600 | 262.4600 | 222.1100 | 226.5200 |

| Exceedance in-sample () | 4.9692 | 5.0166 | 5.0639 | 5.0639 |

| Exceedance out-of-sample () | 5.3005 | 5.2059 | 4.6853 | 4.8273 |

| DQ in-sample (p value) | 0.3678 | 0.4108 | 0.2887 | 0.4216 |

| DQ out-of-sample (p value) | 1.0000 | 1.0000 | 1.0000 | 1.0000 |

| Stock Name | DJCA | NASDAQ100 | S&P500 | Will5000ind |

|---|---|---|---|---|

| -0.6980 | -0.7027 | -0.9827 | -1.5480 | |

| s.e.() | 0.0768 | 0.0760 | 0.0520 | 0.0014 |

| p-value() | 0.0000* | 0.0000* | 0.0000* | 0.0000* |

| RQ | 213.4500 | 272.7100 | 226.9600 | 231.9700 |

| Exceedance in-sample ( ) | 4.4487 | 4.8746 | 4.6380 | 4.3067 |

| Exceedance out-of-sample | 4.7799 | 5.1585 | 4.8746 | 4.4960 |

| DQ in-sample (p value) | 0.6518 | 0.9802 | 0.9545 | 0.2118 |

| DQ out-of-sample (p value) | 1.0000 | 1.0000 | 1.0000 | 1.0000 |

Comparing with the results in Section 6 of Engle and Manganelli, (2004), we can see the standard errors obtained by the adaptive random bandwidth method is much smaller relatively to the size of estimated parameters. We use significance level 5% to reject a parameter equal to zero as well as DQ tests. “ * ” denotes the rejections in Table 4, 5, 6 and 7. Each of the four models shows almost the same rejection results for the stock return time series. Remarkably, it is observed that the coefficient of the VaR autoregressive term is highly significant from zero in all the four models for each stock return time series. This further supports the standpoint of CAViaR specifications, confirming that the phenomenon of volatility clustering can be associated with the autoregressive VaR behaviour. The VaR exceedance in percentage indicates the realized risk level in applications. Dynamic quantile (DQ) tests based on the independence information regarding are used to test model misspecification. We see a rejection in the in-sample DQ test on the symmetric absolute value model for the S&P500 but the realized VaR exceedances (in-sample and out-of-sample) are much close to 5% in Table 5. So it can be complementary to judge CAViaR model specifications by looking at both VaR exceedances and inference tests like DQ tests.

In contract to the significance of , the coefficient of is insignificant in the indirect GARCH(1,1) model for all the stock return time series, see Table 6. And the coefficient of is insignificant in the asymmetric slope model, see Table 4. Although the coefficient of is significant in the symmetric absolute model for all the stock return time series (see Table 5), it is mainly due to the significant explanatory role of based on the results of the asymmetric slope model which the symmetric absolute model is nested in. The significance results of in the adaptive model for each stock return time series suggest that the 5% 1-day VaR can be associated with its 1-day lagged VaR violation which equals one if and zero otherwise. The significance results together implies that negative movements of a stock is significantly influential on its 5% 1-day VaR in the next day.

In terms of the model goodness of fit, we look at the RQ results. The asymmetric slope model presents the lowest RQ result for each stock return time series among the four models despite that it has the most coefficients.

Overall, all the four stock return time series present the same strong associations with the lagged 5% 1-day VaR in interpreting the present 5% 1-day VaR. The asymmetric slope model and the adaptive CAViaR are satisfying for all the four stock returns in terms of data interpretation and model performance concerns.

5 Conclusions

We found that the inference test performance in CAViaR models is not robust and unsatisfying due to the estimation of the conditional probability densities of time series. We found that the existing density estimation methods cannot fully adapt to time-varying conditional probability densities of CAViaR time series. So in this paper we have developed a method called adaptive random bandwidth which can robustly approximate the time-varying conditional probability densities of CAViaR time series by Monte Carlo simulations. This method not only avoids the haunting problem of choosing an optimal bandwidth but also ensures the reliability of CAViaR analysis based on the asymptotic normality of the model parameter estimator. In theory, our proposed method can be extended to general quantile regressions including multivariate cases easily and robustly. This method also has the potential to achieve the second-order accuracy to Wald tests of nonlinear restrictions (Phillips and Park,, 1988; de Paula Ferrari and Cribari-Neto,, 1993) in quantile regressions.

References

- de Paula Ferrari and Cribari-Neto, (1993) de Paula Ferrari, S. L. and Cribari-Neto, F. (1993). On the corrections to the wald test of non-linear restrictions. Economics Letters, 42(4):321–326.

- Duffie and Pan, (1997) Duffie, D. and Pan, J. (1997). An overview of value at risk. Journal of derivatives, 4(3):7–49.

- Engle and Manganelli, (2004) Engle, R. F. and Manganelli, S. (2004). Caviar: Conditional autoregressive value at risk by regression quantiles. Journal of Business & Economic Statistics, 22(4):367–381.

- Hecq and Sun, (2020) Hecq, A. and Sun, L. (2020). Selecting between causal and noncausal models with quantile autoregressions. Studies in Nonlinear Dynamics & Econometrics, 1(ahead-of-print).

- Hendricks and Koenker, (1992) Hendricks, W. and Koenker, R. (1992). Hierarchical spline models for conditional quantiles and the demand for electricity. Journal of the American statistical Association, 87(417):58–68.

- Huber et al., (1967) Huber, P. J. et al. (1967). The behavior of maximum likelihood estimates under nonstandard conditions. In Proceedings of the fifth Berkeley symposium on mathematical statistics and probability, volume 1, pages 221–233. University of California Press.

- Koenker, (2005) Koenker, R. (2005). Quantile regression. Cambridge University Press.

- Koenker and Xiao, (2006) Koenker, R. and Xiao, Z. (2006). Quantile autoregression. Journal of the American Statistical Association, 101(475):980–990.

- Lagarias et al., (1998) Lagarias, J. C., Reeds, J. A., Wright, M. H., and Wright, P. E. (1998). Convergence properties of the nelder–mead simplex method in low dimensions. SIAM Journal on optimization, 9(1):112–147.

- Machado and Silva, (2013) Machado, J. A. and Silva, J. (2013). Quantile regression and heteroskedasticity. https://jmcss. som. surrey. ac. uk/JM_JSS. pdf. Accessed, 5(7):2015.

- Phillips and Park, (1988) Phillips, P. C. and Park, J. Y. (1988). On the formulation of wald tests of nonlinear restrictions. Econometrica: Journal of the Econometric Society, pages 1065–1083.

- Powell, (1991) Powell, J. L. (1991). Estimation of monotonic regression models under quantile restrictions. Nonparametric and semiparametric methods in Econometrics, pages 357–384.

- Storn and Price, (1997) Storn, R. and Price, K. (1997). Differential evolution–a simple and efficient heuristic for global optimization over continuous spaces. Journal of global optimization, 11(4):341–359.

- Weiss, (1991) Weiss, A. A. (1991). Estimating nonlinear dynamic models using least absolute error estimation. Econometric Theory, 7(1):46–68.

- White, (2014) White, H. (2014). Asymptotic theory for econometricians. Academic press.

Appendix A Nonlinearity of parameters in CAViaR models

Nonlinearity of parameters in CAViaR models differentiates CAViaR from linear quantile regressive models. In this appendix, we would like to illustrate the nonlinearity explicitly by showing the gradient, and the Hessian matrix of a CAViaR model.

| (48) |

where , and the operators and are defined as . This model can be rewritten by continuously substituting lagged conditional quantiles such as

| (49) | ||||

where the last line comes from . If , (49) reveals explicitly the nonlinear pattern of parameters in this CAViaR model. From this explicit form, we can further get the gradient and the Hessian matrix of the CAViaR model (48) to emphasize the roles of the parameters.

A.1

The gradient of at a conditional quantile index of interest can be derived as follows:

| (50) | ||||

By knowing (49), we substitute

into in (50) and get

| (51) | ||||

Now we can see the role of the parameters explicitly. shows up in all the elements of the gradient in a nonlinear form which makes it doubtless that the Hessian matrix does not fade out with either.

A.2 Hessian matrix

The second partial derivatives of exist as does, which can be seen from the derivation of the Hessian matrix of as follows:

| (52) | ||||

Considering the rewritten form of, the gradient of, and the Hessian matrix of this CAViaR model, it might raise a caution of estimating those variables by using estimated parameters because the persistent appearance of the parameters can give a slow convergence rate. That is how in essence the nonlinearity of parameters in CAViaR models differentiates CAViaR from linear quantile regressive models.

Appendix B How to simulate CAViaR data generating processes

Before estimating CAViaR models, we would like to provide a general way to simulate a time series of all conditional quantiles following a CAViaR specification. To generate such a CAViaR data generating process (DGP), it is required to get the information on the parameter specification for every possible quantile so that the conditional distribution of at each time can be constructed no matter which quantile is realized. Indeed, when studying a data set, we might be interested in the 1%-th, 5%-th, 50%-th or 95%-th conditional quantiles. For instance in the climate change literature, extreme positive events are also of interest.

This requirement also applies when generating QAR DGPs. However, simulating CAViaR models is more tedious than QAR simulations because the past conditional distributions also need to be stored over time as they serve for the CAViaR DGP simulation through the model VaR autoregressive terms each time. Let us illustrate the simulation process through an example. First, we need to specify a CAViaR DGP at all quantiles for instance of (4) as follows:

where with , and is i.i.d. in the standard uniform distribution (denoted as ). There is a monotonicity requirement on this model which is that is monotonically increasing in so that the -th quantile () of conditional on can be expressed as . The additional step before simulating is to specify the initial conditional distributions and the initial observations, i.e., and . For example, we can take for any and for , where is denoted as the inverse function of the standard normal distribution.

With the above set-up, we can start the simulation by following the steps below.

-

Step 1:

Simulate a sequence of independently and identically distributed (i.i.d.) in . indicates that is realized as its conditional -th quantile.

-

Step 2:

At time , is realized as its -th quantile which is equal to

-

Step 3:

Store by

This step serves for generating later. For instance, is generated via the information on . Iteratively, it requires the conditional -th quantiles of to be stored for generating .

-

Step 4:

Repeat Step 2 and 3 for until we get .

-

Step 5:

In order to leave out the influence of the given initial values in this simulation, we have to delete the observations in the burn-in period. We delete the first 200 observations and keep the rest as a suitable sample for studying the DGP (4).

The above simulation procedure can be easily adapted to other CAViaR DGPs of which model equations of can be substituted into Step 2 with observed values of any involved predetermined variables.

Appendix C Proofs

C.1 Proof of Theorem 2

Proof.

First, since expectation is a linear function, we can rewrite as follows:

| (53) | ||||

This equality holds when goes to infinity by applying the dominated convergence theorem as we regard the least absolute residuals in as zeros. Denote . We rank from the smallest to largest into . In fact, iterations of a simplex-based direct search method like the Nelder–Mead method for optimizing parameters terminates at the vertices of a simplex in the parameter space (Lagarias et al.,, 1998). That is to say, the iterations in optimizing the -th quantile regression objective function terminate with elements of solved to be zeros. Therefore, we set at . And

| (54) |

where for a well-defined convex function minimization.

Since is i.i.d in with restriction to we can get that for each ,

is a sequence of independent random variables with finite second moments by the assumption of (see Assumption AN1(a) of Engle and Manganelli, (2004) ). Then we can use Kolmogorov’s strong Law of Large Number(see e.g. White,, 2014, Corollary 3.9) and get that

|

|

(55) |

as conditionally on . And we can further get that

| (56) | ||||

where the last two lines are obtained by Taylor’s expansion for at and by knowing and with being a continuous function (see AN1 and AN2 of (Engle and Manganelli,, 2004)) respectively.

Therefore, we have and conclude this proof.

C.2 Proof of Corollary 3

Proof. From Theorem 2, we can obtain that

| (57) |

because when . And

| (58) | ||||

Denote We can derive that

| (59) | ||||

which follows the reasoning of (56), and herein the last line is obtained by knowing and is uniformly bounded by a finite constant according to Assumption AN2 of Engle and Manganelli, (2004) and (54) respectively. Now substitute (59) back to (58) and get that

| (60) | ||||

which leads to

| (61) |

when . Therefore, we obtain the mean square convergence (41) for the mean of the adaptive random bandwidth estimator sequence .

C.3 Proof of Corollary 4

Proof. From the condition (39), we can know that

and

Denote the probability distribution function of as , and .

From (55) in the proof of Theorem 2, we know that

| (62) | ||||

We can further rewrite (62) based on two cases in , namely , since is set to be zero in ARB when .

When , we get

| (63) | ||||

Substitute into (63) and get

| (64) | ||||

where is a special integral known as the exponential integral or the incomplete gamma function .

Analogously, when , we can also get

| (65) |

Therefore, we conclude this proof.

C.4 Proof of Theorem 5

Proof. Denote that

| (66) |

Note that

| (67) |

It is straightforward to get that

| (68) |

since we know that

from given in Corollary 3 with being uniformly bounded in by Assumption AN1 of Engle and Manganelli, (2004). And

| (69) |

since that which has been proved in Theorem 3 of Engle and Manganelli, (2004) and is uniformly bounded by a finite constant according to Assumption AN2 of Engle and Manganelli, (2004).

Therefore, we have that and conclude this proof.

Appendix D Extra figures

Appendix E Extra test results

-

•

Simulate 1000 samples from the following DGP:

(70) where and the underlying parameters change over as follows:

(71) where is the inverse standard normal probability distribution function. Conditional -th, -th, -th quantiles are estimated for each of the total simulated samples of sample size by regressing the sample onto the full model (25). The results of the Wald test using the adaptive random bandwidth method and the kernel method (22) are listed in Table 8 in which each estimated size is obtained by the percentage rejection rate among the 1000 samples of sample size .

Table 8: The size performances of the Wald test on the restricted model (26) to (25) (, ) quantile index & sample size T methods size: (, 0.016 0.054 0.091 0.179 2 times updating ) 0.026 0.066 0.126 0.21 (, 0.024 0.08 0.134 0.228 2 times updating ) 0.036 0.107 0.176 0.288 (, 0.01 0.045 0.085 0.168 2 times updating ) 0.011 0.053 0.095 0.182 (, 0.015 0.049 0.085 0.192 2 times updating ) 0.009 0.036 0.091 0.197 (, 0.014 0.056 0.087 0.18 2 times updating ) 0 0 0.001 0.026 (, 0.007 0.041 0.076 0.157 2 times updating ) 0 0 0 0.006 -

•

Simulate 1000 samples of the DGP specified as the model (26) with the underlying parameters are given as , where and is the inverse standard normal probability distribution function. Conditional -th, -th, -th quantiles are estimated for each of the total simulated samples of sample size by regressing the sample onto the full model (25). The results of the Wald test using the adaptive random bandwidth method and the kernel method (22) are listed in Table 9 in which each estimated size is obtained by the percentage rejection rate among the 1000 samples of sample size .

Table 9: The size performances of the Wald test on the restricted model (26) to (25) (, ) quantile index & sample size T methods size: (, 0.018 0.06 0.101 0.187 2 times updating ) 0.017 0.064 0.131 0.235 (, 0.019 0.054 0.107 0.19 2 times updating ) 0.035 0.085 0.14 0.245 (, 0.01 0.058 0.103 0.187 2 times updating ) 0.013 0.053 0.103 0.202 (, 0.021 0.061 0.11 0.184 2 times updating ) 0.014 0.058 0.111 0.2 (, 0.014 0.062 0.126 0.221 2 times updating ) 0.017 0.069 0.129 0.223 (, 0.025 0.064 0.1 0.194 2 times updating ) 0.02 0.065 0.118 0.206 -

•

Simulate 1000 samples of the DGP specified as the model (34) with the underlying parameters are given as , where and is the inverse standard normal probability distribution function. Conditional -th, -th, -th quantiles are estimated for each of the total simulated samples of sample size by regressing the sample onto the full model (25). The results of the Wald test using the adaptive random bandwidth method and the kernel method (22) are listed in Table 10 in which each estimated size is obtained by the percentage rejection rate among the 1000 samples of sample size .

Table 10: The size performances of the Wald test on the restricted model (34) to (25) (, ) quantile index & sample size T methods size: (, 0.032 0.069 0.096 0.17 2 times updating ) 0.082 0.137 0.199 0.287 (, 0.052 0.093 0.127 0.19 2 times updating ) 0.143 0.221 0.271 0.341 (, 0.032 0.071 0.121 0.207 2 times updating ) 0.073 0.137 0.207 0.3 (, 0.031 0.063 0.123 0.204 2 times updating ) 0.092 0.156 0.216 0.308 (, 0.021 0.055 0.095 0.188 2 times updating ) 0.067 0.118 0.16 0.256 (, 0.034 0.069 0.118 0.208 2 times updating ) 0.088 0.158 0.212 0.311