∎

22email: denis.belomestny@uni-due.de 44institutetext: John Schoenmakers44institutetext: WIAS Berlin, Germany

44email: john.schoenmakers@wias-berlin.de

From optimal martingales to randomized dual optimal stopping

Abstract

In this article we study and classify optimal martingales in the dual formulation of optimal stopping problems. In this respect we distinguish between weakly optimal and surely optimal martingales. It is shown that the family of weakly optimal and surely optimal martingales may be quite large. On the other hand it is shown that the Doob-martingale, that is, the martingale part of the Snell envelope, is in a certain sense the most robust surely optimal martingale under random perturbations. This new insight leads to a novel randomized dual martingale minimization algorithm that doesn’t require nested simulation. As a main feature, in a possibly large family of optimal martingales the algorithm efficiently selects a martingale that is as close as possible to the Doob martingale. As a result, one obtains the dual upper bound for the optimal stopping problem with low variance.

JEL Classification G10 G12 G13

Keywords:

Optimal stopping problem, Doob-martingale, Randomization.MSC:

91G6065C0560G401 Introduction

The last decades have seen a huge development of numerical methods for solving optimal stopping problems. Such problems became very prominent in the financial industry in the form of American derivatives. For such derivatives one needs to evaluate the right of exercising (stopping) a certain cash-flow (reward) process at some (stopping) time , up to some time horizon . From a mathematical point of view this evaluation comes down to solving an optimal stopping problem

Typically the cash-flow depends on various underlying assets and/or interest rates and as such is part of a high dimensional Markovian framework. Particularly for high dimensional stopping problems, virtually all generic numerical solutions are Monte Carlo based. Most of the first numerical solution approaches were of primal nature in the sense that the goal was to construct a “good” exercise policy and to simulate a lower biased estimate of In this respect we mention, for example, the well-known regression methods by Longstaff & Schwartz J_LS2001 , Tsiklis & Van Roy J_TV2001 , and the stochastic mesh approach by Broadie & Glasserman J_BrGl , and the stochastic policy improvement method by Kolodko & Schoenmakers J_KS2006 . For further references we refer to the literature, for example Gl and the references therein.

In this paper we focus on the dual approach developed by Rogers J_Rogers2002 , and Haugh & Kogan J_HK2004 , initiated earlier by Davis & Karatzas J_DK1994 . In the dual method the stopping problem is solved by minimizing over a set of martingales, rather than a set of stopping times,

| (1.1) |

A canonical minimizer of this dual problem is the martingale part, of the Doob(-Meyer) decomposition of the Snell envelope

which moreover has the nice property that

| (1.2) |

That is, if one would succeed in finding , the value of can be obtained from one trajectory of only.

Shortly after the development of the duality method in J_Rogers2002 and J_HK2004 , various numerical approaches for computing dual upper bounds for American options based on it appeared. May be one of the most popular methods is the nested simulation approach by Andersen & Broadie J_AB2004 , who essentially construct an approximation to the Doob martingale of the Snell envelope via stopping times obtained by the Longstaff & Schwartz method J_LS2001 . A few years later, a linear Monte Carlo method for dual upper bounds was proposed in J_BelBenSch . In fact, as a common feature, both J_AB2004 and J_BelBenSch aimed at constructing (an approximation of) the Doob martingale of the Snell envelope via some approximative knowledge of continuation functions obtained by the method of Longstaff & Schwartz or in another way. Instead of relying on such information, the common goal in later studies J_DesFarMoa , J_SchZhaHua , J_Bel , J_BelHilSch , was to minimize the expectation functional in the dual representation (1.1) over a linear space of generic “elementary” martingales. Indeed, by parameterizing the martingale family in a linear way and replacing the expectation in (1.1) by the sample mean over a large set of trajectories, the resulting minimization comes down to solving a linear program. However, it was pointed out in J_SchZhaHua that in general there may exist martingales that are “weakly” optimal in the sense that they minimize (1.1), but fail to have the “almost sure property” (1.2). As a consequence, the estimator for the dual upper bound due to such martingales may have high variance. Moreover, an example in J_SchZhaHua illustrates that a straightforward minimization of the sample mean corresponding to (1.1) may end up with a martingale that is asymptotically optimal in the sense of (1.1) but not surely optimal in the sense of (1.2), when the sample size tends to infinity. As a remedy to this problem, in J_Bel variance penalization is proposed, whereas in J_BelHilSch the sample mean is replaced by the maximum over all trajectories.

In this paper we first extend the study of surely optimal martingales in J_SchZhaHua to the larger class of weakly optimal martingales. As a principal contribution, we give a complete characterization of weakly and surely optimal martingales and moreover consider the notion of randomized dual martingales. In particular, it is shown that in general there may be a fullness of martingales that are optimal but not surely optimal. In fact, straightforward minimization procedures based on the sample mean in (1.1) may typically return martingales of this kind, even if the Doob martingale of the Snell envelope is contained in the martingale family (as illustrated already in J_SchZhaHua , though at a somewhat pathological example with partially deterministic cash-flows). As another main contribution we will show that the Doob martingale plays a distinguished role within the family of all optimal martingales. Namely, it will be shown that by randomizing the arguments in the path-wise maximum for each trajectory in a particular way, any non-Doob optimal martingale can be turned to a suboptimal one. More specifically, we will prove that there exists a particular “optimal randomization” such that the Doob martingale, perturbed or randomized with it, remains guaranteed (surely) optimal, while any other surely or weakly optimal martingale turns to a suboptimal one. Of course, as a rule this “optimal randomization” is not directly known or available in practical applications. But, it turns out that by just incorporating some simple randomization due to uniform random variables, sample mean minimization may return a martingale that is closer to the Doob-martingale than one obtained without randomization. We thus end up with a martingale with low variance, which in turn guarantees that the corresponding upper bound based on (1.1) is tight (see J_Bel andJ_SchZhaHua ). Compared to J_BelHilSch and J_Bel , the benefit of this new randomized dual approach is its computational efficiency: From the experiments we conclude that it may be sufficient to add on for each trajectory simple i.i.d. uniform random variables to (some of) the arguments of the maximum. An extensive numerical analysis of the here presented randomized dual martingale approach will certainly be an interesting subsequent study but is considered beyond the scope of this article.

The structure of the paper is as follows. Section 2 carries out a systematic theoretical analysis of optimal martingales. In Section 3 we deal with randomized optimal martingales and the effect of randomizing the Doob-martingale. More technical proofs are given in Section 4 and some first numerical examples are presented in Section 5.

2 Characterization of optimal martingales

Since practically any numerical approach to optimal stopping is based on a discrete exercise grid, we will work within in a discrete time setup. That is, it is assumed that exercise (or stopping) is restricted to a discrete set of exercise times for some time horizon and some For notational convenience we will further identify the exercise times with their index and thus monitor the reward process at the “times”

Let be a filtered probability space with discrete filtration An optimal stopping problem is a problem of stopping the reward process in such a way that the expected reward is maximized. The value of the optimal stopping problem with horizon at time is given by

| (2.1) |

provided that was not stopped before In (2.1), is the set of -stopping times taking values in and the process is called the Snell envelope. It is well known that is a supermartingale satisfying the backward dynamic programming equation (Bellman principle):

Along with a primal approach based on the representation (2.1), a dual method was proposed in J_Rogers2002 and J_HK2004 . Below we give a short self contained recap while including the notions of weak and sure optimality.

Let be the set of martingales adapted to with By using the Doob’s optimal sampling theorem one observes that

| (2.2) |

for any We will say that a martingale is weakly optimal, or just optimal, at for some if

| (2.3) |

The set of all martingales (weakly) optimal at will be denoted by The set of martingales optimal at for all is denoted by We say that a martingale is surely optimal at for some if

| (2.4) |

The set of all surely optimal martingales at will be denoted by The set of surely optimal martingales at for all is denoted by Note that, obviously,

Now there always exists at least one surely optimal martingale, the so-called Doob-martingale coming from the Doob decomposition of the Snell envelope Indeed, consider the Doob decomposition of that is,

| (2.5) |

where is a martingale with and is predictable with It follows immediately that

| (2.6) |

and so is non-decreasing due to the fact that is a supermartingale. One thus has by (2.5) on the one hand

and due to (2.2) on the other hand

Thus, it follows that (2.4) holds for arbitrary hence Furthermore we have the following properties of the sets and

Proposition 1

The sets and for and are convex.

As an immediate consequence of Proposition 1; if there exist more than one weakly (respectively surely) optimal martingale, then there exist infinitely many weakly (respectively surely) optimal martingales.

Proposition 2

It holds that for some if and only if for any optimal stopping time satisfying

one has that

Proof

It will be shown below that the class of the optimal martingales may be considerably large. In fact, any such martingale can be seen as a perturbation of the Doob martingale For this, let us introduce some further notation and define with by convention and let, for be the first optimal stopping time strictly after That is, if we define recursively

where There so will be a last number, say, with Further, the family defined by

| (2.8) |

is a consistent optimal stopping family in the sense that and that implies

The next lemma provides a corner stone for an explicit structural characterization of (weakly) optimal martingales.

Lemma 1

if and only if is an adapted martingale with such that the identities

hold.

The following lemma anticipates sufficient conditions for a martingale to be optimal, that is, to be a member of

Lemma 2

Let be an adapted sequence with and consider the “shifted” Doob martingale

Let be the unique number such that for any If satisfies for all

| (2.9) | ||||

| (2.10) |

for and , then satisfies the identities (i)-(ii) in Lemma 1.

Corollary 1

Proof

Indeed, take such that If then and (2.12) and (2.13) imply with via (2.11),

respectively, which in turn imply (2.9) (note that ) and (2.10), respectively. Further if we have to distinguish between and In both cases (2.9) is trivially fulfilled, while (2.10) is void in the first case, and in the second case it reads,

which is implied by (2.11) and (2.14) for The converse direction, that is from (2.9) and (2.10) to (2.12), (2.13), (2.14), goes similarly and is left to the reader.

Corollary 2

Interestingly, the converse to Corollary 2 is also true and we so have the following characterization theorem.

Theorem 2.1

The proofs of Lemmas 1-2 and Theorem 2.1 are given in Section 4. In fact, Theorem 2.1 reveals that, besides the Doob martingale, there generally exists a large set of optimal martingales From Theorem 2.1 we also obtain a characterization of the surely optimal martingales which is essentially the older result in J_SchZhaHua , Thm. 6 (see Section 4 for the proof).

Corollary 3

In applications of dual optimal stopping, hence dual martingale minimization, it is usually enough to find martingales that are “close to” surely optimal ones, merely at some specific point in time , that is, . Naturally, since we may expect that in general the family of undesirable (not surely) optimal martingales at a specific time may be even much larger than the family characterized by Theorem 2.1. A characterization of and is given by the next theorem, where we take without loss of generality. The proof is given in Section 4.

Theorem 2.2

After dropping the nonnegative term in the right-hand-sides of (2.16) and (2.18) we may obtain tractable sufficient conditions for a martingale to be optimal or surely optimal at a single date, respectively. In the spirit of Corollary 1 they may be formulated in the following way.

Corollary 4

Remark 1

While the class of optimal martingales may be quite large in general, it is still possible that it is just a singleton (containing the Doob martingale only). For example, let the cash-flow be a martingale itself, then it is easy to see that the only optimal martingale (at ) is (the proof is left as an easy exercise).

3 Randomized dual martingale representations

Let be some auxiliary measurable space that is “rich enough”. Let us consider random variables on that are measurable with respect to the -field While abusing notation a bit, and are identified with and respectively. Let further be the given “primary” measure on and be an extension of to in the sense that

In particular, if is -measurable, then for some , that is, does not depend on We now introduce randomized or “pseudo” martingales as random perturbations of -adapted martingales of the form (2.11). Let be random variables on such that for Then

| (3.1) |

is said to be a pseudo martingale. As such, is not an -martingale but is. The results below on pseudo-martingales provide the key motivation for randomized dual optimal stopping. All proofs in this section are deferred to Section 4.

Proposition 3

For any of the form (3.1) one has the upper estimate

| (3.2) |

If that is,

| (3.3) |

and the random perturbations satisfy in addition

| (3.4) |

with defined in (2.5), then one has the almost sure identity

| (3.5) |

Moreover, for the first optimal stopping time (see (2.8)) one must have that a.s., and if is strict in the sense that

then is the only time where

Due to the following theorem, any (weakly or surely) optimal non Doob martingale turns to a non optimal one in the sense that

| (3.6) |

after a particular “optimal” randomization.

Theorem 3.1

Suppose that and let be a sequence of random variables as in Proposition 3, given by

| (3.7) |

where the are assumed to be i.i.d. distributed on independent of with It is further assumed that the r.v. have a joint continuous density supported on with . As such the randomizers (3.7) satisfy (3.4), and Proposition 3 thus provides an upper bound (3.2) due to the pseudo martingale Now, for the randomized martingale one has (3.6) if with positive probability.

The following corollary states that an optimally randomized non Doob martingale in which is thus suboptimal in the sense of (3.6) due to the previous theorem, cannot have zero variance. The proof relies on Theorem 3.1.

Corollary 5

Let as in Theorem 3.1, and . Then if and only if

Discussion

Proposition 3 provides us with a remarkable freedom of perturbing the Doob martingale randomly while (3.5) remains true. The bottom line of Theorem 3.1 is that randomization under condition (3.4) of an optimal, or even surely optimal, but non-Doob martingale results in a non optimal (pseudo) martingale, while any randomization of the Doob martingale under (3.4) remains a surely optimal pseudo martingale. This is an important feature, since in this way martingale candidates that are optimal but not equal to the (surely optimal) Doob martingale can be sorted out by randomization.

4 Proofs

4.1 Proof of Lemma 1

4.2 Proof of Lemma 1

Suppose that is a martingale with such that Lemma 1-(i) and (ii) hold. Then (ii) implies for that

| (4.1) |

Now take arbitrarily, and let be such that (Note that is unique and measurable). Then due to Lemma 1-(i) and (4.1),

On the other hand, one has (see (2.8)). Thus, by Proposition 2, and hence since was taken arbitrarily.

Conversely, suppose that So for any

by Proposition 2. For one thus has

and for it holds that

That is, (i) is shown. Next, for any it holds

which implies (ii).

4.3 Proof of Lemma 2

Assume that is adapted with and that satisfies (2.9) and (2.10). For and we may write,

| (4.2) | ||||

By taking in (4.2) and using we then get

and thus

So from (2.9) we obtain with

i.e. Lemma 1-(i) for If and Lemma 1-(i) is trivially fulfilled. So let us consider and Analogously, we then may write for

| (4.3) |

It is easy to see that (4.3) is also valid for due to our assumption Thus, for and taking we get from (4.3),

whence (4.3) implies for

that is Lemma 1-(i) holds also for

4.4 Proof of Theorem 2.1

Let us now consider the converse and assume that with Then is adapted and may be written in the form (2.11) where the are -measurable and for Since Lemma 1-(i) implies that for

| (4.6) |

since for each with one has because We now show for any with that (2.9) holds with by backward induction. For it follows from (4.6). Now suppose that for some with it holds that

| (4.7) |

One has by construction

Hence, since with and (!), and taking -conditional expectations,

using the induction hypothesis (4.7). In view of (4.6) it follows that (2.9) holds for

Next, on the other hand, implies by Lemma 1-(ii) that for any fixed ,

| (4.8) |

Suppose that and hence Then (4.8) implies by (2.11) after a few manipulations,

with the usual convention Thus, either the last three sums are zero due to or we may use that for We thus get for

| (4.9) |

In particular, due to for this gives

| (4.10) |

Let us now show that (2.10) holds for and

4.5 Proof of Corollary 3

4.6 Proof of Theorem 2.2

(i): Due to Proposition 2, if and only if

with which is equivalent with

| (4.11) | ||||

| (4.12) |

Since for (4.11) reads

| (4.13) |

which in turn is equivalent with (2.15). Indeed, suppose that (4.13) holds. Then (2.15) clearly holds for Now assume that (2.15) holds for Then, by backward induction,

By next taking -conditional expectations we get (2.15) for For the converse, just take in (2.15). We next consider (4.12), which may be written as

Using the Doob decomposition of the Snell envelope (2.5), and that this is equivalent with (2.16).

(ii): Suppose that One has that if and only if

Since a.s., this implies a.s., and so by that by the sandwich property. Now note that is also a martingale with a.s. Let us write (assuming that )

That is, is -measurable with so and thus a.s. By proceeding backwards in the same way we see that for all which implies

whence for i.e. (2.17). Since (2.18) follows from (2.16) with Conversely, if (2.17) and (2.18) hold, then

and due to (2.18), for each

by (2.5). That is and so

4.7 Proof of Proposition 3

4.8 Proof of Theorem 3.1

Let let be as stated, and let us assume that

| (4.15) |

We then have to show that By using (2.5) we may write

By (4.15) we must have

| (4.16) |

We observe that

using due to Proposition 3. By Doob’s sampling theorem, and so (4.16) implies by the sandwich property,

| (4.17) |

Let us fix some and assume that Due to (3.7) we thus have that,

| (4.18) |

(note that and for ). Since implies by (2.15) Now assume that for some but small enough, the set

has positive probability. Since on one has

we then obtain a contradiction with (4.18), because Thus for any we must have that This in turn implies that

However, the -conditional expectation of the left-hand-side is zero (Doob’s sampling theorem). Hence,

by the sandwich property. Since was arbitrary, this obviously implies that

| (4.19) |

Let us next assume that for some We then have due to (3.7) and (4.17),

| (4.20) |

For (2.16) implies that where it is noted that due to and Similarly, we next assume that for some the set

has positive probability. Then on on has

which gives a contradiction with (4.20) however because We so conclude that

and by taking the -conditional expectation again, that for We had already (4.19), and therefore we finally conclude that hence

4.9 Proof of Corollary 5

If one has due to Proposition 3. Let us now take with and assume that From here we will derive a contradiction. As in the proof of Theorem 3.1 we write

| (4.21) |

Now, implies by Theorem 3.1 that

| (4.22) |

That is, due to (4.21) and (4.22), there exists a constant such that

Using (3.7) and the fact that always and this implies

| (4.23) |

Consider the stopping time Then, using and (4.23), we must have that almost surely. Since is a martingale, Doob’s sampling theorem then implies hence a contradiction. That is, the assumption was false.

5 Numerical examples

5.1 Simple stylized numerical example

We first reconsider the stylized test example due to (J_SchZhaHua, , Section 8), also considered in J_BelHilSch , where , , , and is a random variable which uniformly distributed on the interval . The optimal stopping time is thus given by

and the optimal value is . Furthermore, it is easy to see that the Doob martingale is given by

As an illustration of the theory developed in Sections 2-3, let us consider the linear span as a pool of candidate martingales and randomize it according to (3.7). We thus consider the objective function

| (5.1) |

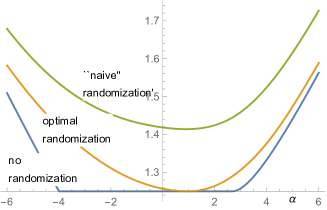

for some fixed where are i.i.d. random variables with uniform distribution on Note that for this example and is the non-decreasing predictable process from the Doob decomposition. Moreover, it is possible to compute (5.1) in closed form (though we omit detailed expressions which can be conveniently obtained by Mathematica for instance). In Figure 1 (left panel) we have plotted (5.1) for and together with the objective function

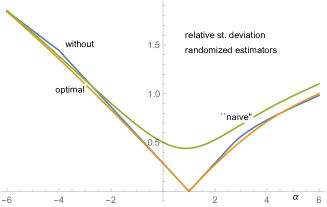

due to a “naive” randomization, not based on knowledge of the factor Also, in Figure 1 (right panel), the relative standard deviations of the corresponding random variables

are depicted as a function of

From (J_SchZhaHua, , Section 8) we know that, and from the plot of in Figure 1 (left panel) we see that, for . On the other hand, the right panel plot shows that may be relatively large for and that the Doob martingale (i.e. ) is the only surely optimal one in our parametric family. Moreover, the objective function due to the optimal randomization attains its unique minimum at the Doob martingale, i.e. for Further, the variance of the corresponding optimally randomized estimator attains its unique minimum zero also at Let us note that these observations are anticipated by Theorem 3.1 and Corollary 5. The catch is that for each the randomized fails to be optimal in the sense of (3.6). We also see that both the optimal and the “naive” randomization render the minimization problem to be strictly convex. Moreover, while the minimum due to the “naive” randomization lays significantly above the true solution, the argument where the minimum is attained, say, identifies nonetheless a martingale that virtually coincides with the Doob optimal one. That is, and is optimal corresponding to variance , which can be seen in the right panel.

5.2 Bermudan call in a Black-Scholes model

In order to exhibit the merits of randomization based on the theoretical results in this paper in a more realistic case, we have constructed an example that contains all typical features of a real life Bermudan option, but, is simple enough to be treated numerically in all respects on the other hand.

As in the previous example we take , and specify the (discounted) cash-flows as functions of the (discounted) stock prices by

| (5.2) |

For we take the Black-Scholes model

| (5.3) |

where and independent of As such we have a stylized example of a Bermudan call option under a Black-Scholes model with two (non-trivial) exercise dates if . Note that usually a Bermudan call is considered for a fixed strike and a dividend paying stock, yielding a non-trivial optimal stopping time. Though increasing strikes here look somewhat unusual, it is simple for presentation while, mathematically, the effect is the same as for a dividend paying stock and a fixed strike. For the continuation function at we thus have

| (5.4) |

where is the standard normal density. While abusing notation a bit we will denote the cash-flows by and respectively. For the (discounted) option value at one thus has

Further we obviously have

The Doob martingale for this example is thus given by

and the non-decreasing predictable component is given by

For demonstration purposes we will quasi analytically compute the optimal randomization coefficient in (3.7),

by using a Black(-Scholes) type formula

and a numerical integration for obtaining the target value . We now consider two martingale families.

- (M-Sty)

-

For any we set

(5.5) Note that

- (M-Hermite)

-

Using that the (probabilistic) Hermite polynomials given by

are orthogonal with respect to the standard Gaussian density we consider a martingale family

(5.6) with obvious definition of (note that ). Since our mere goal is to exhibit the effect of randomization, for the examples below we restrict ourselves to the choice

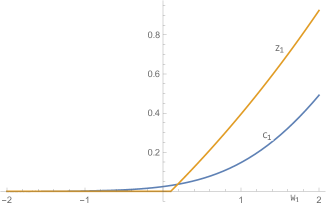

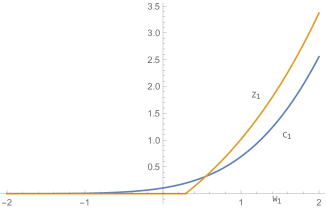

The parameters in (5.2) and (5.3) are taken to be such that with a medial probability optimal exercise takes place at In particular, we consider two cases specified with parameter sets

| (Pa1) | |||

| (Pa2) |

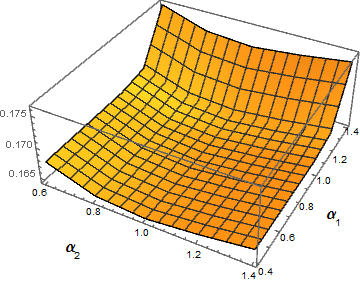

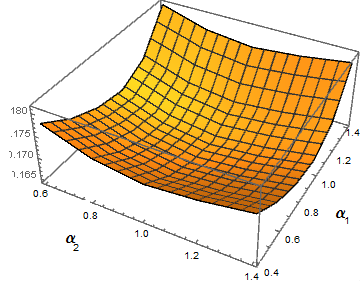

respectively. From Figure 2 we see that the probability of optimal exercise at is almost 50% for (Pa1) and almost 30% for (Pa2). Let us visualize on the basis of martingale family (M-Sty) and parameters (Pa1) the effects of randomization. Consider the objective function

| (5.7) |

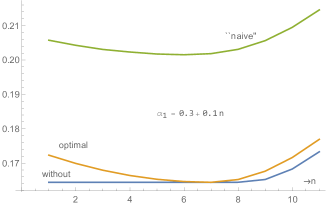

where scales the randomization due to i.i.d. random variables uniformly distributed on . I.e., for there is no randomization and gives the optimal randomization. Now restrict (5.7) to the sub domain (while slightly abusing notation), i.e. and The function i.e. (5.7) without randomization is visualized in Figure 3, where expectations are computed quasi-analytically with Mathematica. From this plot we see that the true value is attained on the line for various (i.e. not only in ). On the other hand, i.e. (5.7) with optimal randomization, has a clear strict global minimum in , see Figure 4. Let us have a closer look at the map for and respectively, and also at due to the “naive” randomization

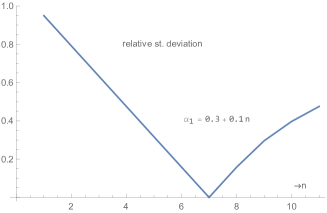

where the scale parameter is taken to be roughly the option value. (It turns out that the choice of this scale factor is not critical for the location of the minimum.) In fact, the results, plotted in Figure 5, tell there own tale. The second panel depicts the relative deviation of

In fact, similar comments as for the example in Section 5.1 apply. The “naive” randomization attains its minimum at which we red off from the tables that generated this figure. We thus have found the martingale which may be virtually considered surely optimal, as can be seen from the variance plot (second panel). Analogue visualizations for the parameter set (Pa2) with analogue conclusions may be given, though are omitted due to space restrictions.

Let us now pass on to a Monte Carlo setting, where we mimic the approach in real practice more closely. Based on simulated samples of the underlying asset model, i.e. we consider the minimization

| (5.8) |

for (no randomization) and (optimal randomization), along with the minimization

| (5.9) |

based on a “naive”randomization where the coefficients are pragmatically chosen. In (5.8) and (5.9) stands for a generic linearly structured martingale family, such as (5.5) and (5.6) for example. The minimization problems (5.8) and (5.9) may be solved by linear programming (LP). They may be transformed into a suitable form such that the (free) LP package in R can be applied. This transformation procedure is straightforward and spelled out in J_DesFarMoa for example. In the latter paper it is argued that the required computation time scales with due to the sparse structure of the coefficient matrix involved in the LP setup. However, taking advantage of this sparsity requires a special treatment of the implementation of the linear program in connection with more advanced LP solvers (as done in J_DesFarMoa ). Since this paper is essentially on the theoretical justification of the randomized duality problem (along with the classification of optimal martingales), we consider an in-depth numerical analysis beyond scope of this paper.

For both parameter sets (Pa1) and (Pa2), and both martingale families (5.5) and (5.6) with we have carried out the LP optimization algorithm sketched above. We have taken and for the “naive” randomization

In the Table 1, for (Pa1), and Table 2, for (Pa2), we present for the minimizers the in-sample expectation , the in-sample standard deviation and the path-wise maximum due to a single trajectory followed by the corresponding “true” values based on a large “test” simulation of samples.

(Pa1)

(Pa2)

The results in tables Tables 1-2 show that even a simple (naive) randomization at leads to a substantial variance reduction (up to times) not only on training samples but also on the test ones. We think that for more structured examples and more complex families of martingales even more pronounced variance reduction effect may be expected. For example, in general it might be better to take Wiener integrals, i.e. objects of the form where runs through some linear space of basis functions, as building blocks for the martingale family. Also other types of randomization can be used, for example one may take different distributions for the r.v. However all these issues will be analyzed in a subsequent study.

References

- [1] Leif Andersen and Mark Broadie. A Primal-Dual Simulation Algorithm for Pricing Multi-Dimensional American Options. Management Science, 50(9):1222–1234, 2004.

- [2] Denis Belomestny. Solving optimal stopping problems via empirical dual optimization. The Annals of Applied Probability, 23(5):1988–2019, 2013.

- [3] Denis Belomestny, Christian Bender, and John Schoenmakers. True upper bounds for Bermudan products via non-nested Monte Carlo. Math. Finance, 19(1):53–71, 2009.

- [4] Denis Belomestny, Roland Hildebrand, and John Schoenmakers. Optimal stopping via pathwise dual empirical maximisation. Appl. Math. Optim., 79(3):715–741, 2019.

- [5] M. Broadie and P. Glasserman. A stochastic mesh method for pricing high-dimensional American options. Journal of Computational Finance, 7(4):35–72, 2004.

- [6] M.H.A. Davis and I. Karatzas. A deterministic approach to optimal stopping. Kelly, F. P. (ed.), Probability, statistics and optimisation. A tribute to Peter Whittle. Chichester: Wiley. Wiley Series in Probability and Mathematical Statistics. Probability and Mathematical Statistics. 455-466, 1994.

- [7] V.V. Desai, V.F. Farias, and C.C. Moallemi. Pathwise optimization for optimal stopping problems. Management Science, 58(12):2292–2308, 2012.

- [8] Paul Glasserman. Monte Carlo methods in financial engineering, volume 53. Springer Science & Business Media, 2003.

- [9] Martin Haugh and Leonid Kogan. Pricing American options: A duality approach. Oper. Res., 52(2):258–270, 2004.

- [10] Anastasia Kolodko and John Schoenmakers. Iterative construction of the optimal Bermudan stopping time. Finance Stoch., 10(1):27–49, 2006.

- [11] Francis A. Longstaff and Eduardo S. Schwartz. Valuing American options by simulation: a simple least-squares approach. Review of Financial Studies, 14(1):113–147, 2001.

- [12] Leonard C. G. Rogers. Monte Carlo valuation of American options. Mathematical Finance, 12(3):271–286, 2002.

- [13] John Schoenmakers, Jianing Zhang, and Junbo Huang. Optimal dual martingales, their analysis, and application to new algorithms for Bermudan products. SIAM J. Financial Math., 4(1):86–116, 2013.

- [14] J. Tsitsiklis and B. Van Roy. Regression methods for pricing complex American style options. IEEE Trans. Neural. Net., 12(14):694–703, 2001.