Fair Dynamic Rationing

Manshadi, Niazadeh, Rodilitz

Fair Dynamic Rationing

Vahideh Manshadi \AFFYale School of Management, New Haven, CT, \EMAILvahideh.manshadi@yale.edu \AUTHORRad Niazadeh \AFFUniversity of Chicago Booth School of Business, Chicago, IL, \EMAILrad.niazadeh@chicagobooth.edu \AUTHORScott Rodilitz \AFFStanford Graduate School of Business, Stanford, CA, \EMAILrodilitz@stanford.edu

We study the allocative challenges that governmental and nonprofit organizations face when tasked with equitable and efficient rationing of a social good among agents whose needs (demands) realize sequentially and are possibly correlated. As one example, early in the COVID-19 pandemic, the Federal Emergency Management Agency faced overwhelming, temporally scattered, a priori uncertain, and correlated demands for medical supplies from different states. In such contexts, social planners aim to maximize the minimum fill rate across sequentially arriving agents, where each agent’s fill rate is determined by an irrevocable, one-time allocation. For an arbitrarily correlated sequence of demands, we establish upper bounds on the expected minimum fill rate (ex-post fairness) and the minimum expected fill rate (ex-ante fairness) achievable by any policy. Our upper bounds are parameterized by the number of agents and the expected demand-to-supply ratio, yet we design a simple adaptive policy called projected proportional allocation (PPA) that simultaneously achieves matching lower bounds for both objectives (ex-post and ex-ante fairness), for any set of parameters. Our PPA policy is transparent and easy to implement, as it does not rely on distributional information beyond the first conditional moments. Despite its simplicity, we demonstrate that the PPA policy provides significant improvement over the canonical class of non-adaptive target-fill-rate policies. We complement our theoretical developments with a numerical study motivated by the rationing of COVID-19 medical supplies based on a standard SEIR modeling approach that is commonly used to forecast pandemic trajectories. In such a setting, our PPA policy significantly outperforms its theoretical guarantee as well as the optimal target-fill-rate policy.

rationing, fair allocation, social goods, correlated demands, online resource allocation

1 Introduction

In Spring 2020, with the COVID-19 pandemic surging across the US, states were relying on the Federal Emergency Management Agency (FEMA) to provide urgently needed medical equipment from the Strategic National Stockpile. Unequipped for such a widespread emergency, FEMA aimed to ration its limited supplies in order to address states’ current needs while also retaining some of the stockpile in anticipation of future needs. However, the allocation decisions made by FEMA were inconsistent and lacked transparency, which frustrated state officials (Washington Post 2020a).111“We don’t know how the federal government is making those decisions,” said Casey Katims, the federal liaison for Washington state. Because having access to medical equipment can be a matter of life or death for a COVID-19 patient, making allocation decisions which are efficient and equitable is of paramount importance (Emanuel et al. 2020). Achieving efficiency alone is easy: a first-come, first-serve policy allocates all of the supply to meet early-arriving needs. However, such a policy can be unfair to patients in states where needs materialize later.

The above is just one example of a fundamental sequential allocation problem that social planners face when aiming to allocate divisible goods as efficiently and equitably as possible to demanding agents that arrive over time.

1.1 Overview of Contributions

In this paper, we take the first step toward theoretically studying the aforementioned class of problems. We develop a framework for fair dynamic rationing where agents’ one-time needs (demands) for a divisible good realize sequentially and can be arbitrarily correlated. In particular, upon arrival of each agent’s demand, the planner makes an irrevocable decision about their fill rate (FR), i.e., the fraction of the agent’s demand that is satisfied by a one-time allocation. Toward jointly achieving efficiency and equity, the planner aims to maximize the minimum FR, either ex post or ex ante. To assess the performance of sequential allocation policies, we introduce measures of ex-post and ex-ante fairness guarantees. For this general setting:

-

(i)

We establish upper bounds on the ex-post and ex-ante fairness guarantees achievable by any policy. These bounds are parameterized by the supply scarcity (i.e., the expected demand-to-supply ratio) and the number of agents.

-

(ii)

Remarkably, we show that a simple, adaptive, and transparent policy called projected proportional allocation (PPA) simultaneously achieves our upper bounds on the ex-post and ex-ante fairness guarantees for any set of parameters.

-

(iii)

We illustrate the power of adaptivity by characterizing the ex-post guarantee of the optimal target-fill-rate policy and showing that such a non-adaptive policy cannot achieve our upper bounds.

-

(iv)

Finally, we demonstrate the effectiveness of our policy through an illustrative case study motivated by the allocation of COVID-19 medical supplies based on a model of demand which was used by the White House.

Introducing a framework for fair dynamic rationing: We study the allocation of a divisible good to agents arriving over time with varying levels of demand. We assume the demand sequence is drawn from an arbitrary but known joint distribution across all agents. To account for heterogeneity in the demand level of different agents, we set each agent’s utility to be its FR. In our base model, we focus on the objective of maximizing the minimum FR across all agents. Such an objective—which is in the spirit of Rawlsian justice—maximizes the utility of the worst-off agent. As such, it takes fairness into consideration along with efficiency.222In Section 5, we generalize our objective function. Due to the stochasticity of the demand sequence, we consider two versions of this objective function: the expected minimum FR and the minimum expected FR (see eq. ex-post and eq. ex-ante, respectively, as well as the subsequent discussion).

Like other online stochastic optimization problems, our sequential allocation problem can be formulated as a dynamic program (DP), and it similarly suffers from the curse of dimensionality as well as other practical limitations such as a lack of interpretability. (We provide further discussion of the DP in Remark 3.7, and in Appendix 7 we formally present the DP, illustrate its exponential size, and discuss other practical drawbacks.) Consequently, we aim to design sequential allocation policies that perform well while being practically appealing and computable in polynomial time. We assess the performance of a policy by computing its ex-post and ex-ante fairness guarantees for any given supply scarcity and number of agents. In defining our notions of such guarantees, we use the minimum FR achievable under deterministic demand as a normalization factor (see Definitions 2.1, 2.2, and 2.3 and their related discussion in Section 2) to separate the impact of demand stochasticity from the impact of supply scarcity. The ex-post (resp. ex-ante) fairness guarantee of a policy serves as a lower bound on the expected minimum (resp. minimum expected) FR that the policy achieves relative to our normalization factor under all possible joint demand distributions.

Establishing upper bounds: In order to gain insight into the difficulty of achieving equity and efficiency in sequential allocation, we develop upper bounds on the achievable fairness guarantees of any policy, even policies which cannot be computed in polynomial time. For intuition, consider the following example with two agents. The first agent has demand of , where is a Bernoulli random variable with success probability . The second agent has demand , where is an independent Bernoulli random variable with success probability . In other words, the demand sequence is equally likely to be , , or . For such an instance, no sequential policy can distinguish between the latter two scenarios after observing the first demand, which leads to a sub-optimal decision. Building on the above intuition, in Sections 3.1 and 3.5, we establish upper bounds on the ex-post and ex-ante guarantees of any policy (see Theorems 3.4 and 3.20).

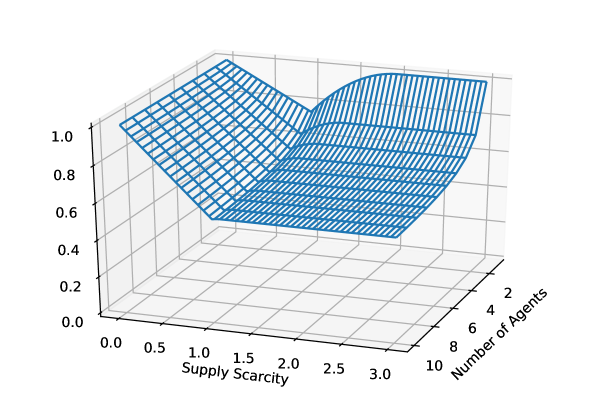

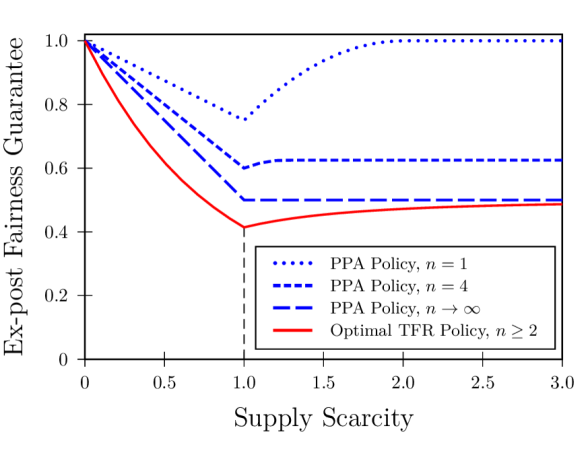

As we later show, these bounds are indeed tight. Thus, conducting comparative statics with respect to the supply scarcity and the number of agents reveals several insights (see Figure 1): when demand is small relative to supply, the bounds on both fairness guarantees deteriorate with increased demand. However, in the over-demanded regime, the bounds are independent of the supply scarcity. Further, in both the under-demanded and over-demanded regimes, the ex-post fairness guarantee worsens with more agents. On the other hand, the ex-ante fairness guarantee is independent of the number of agents. This highlights the fundamental difference in our notions of fairness: the objective corresponding to ex-post fairness is concerned with fairness along all samples paths, whereas the objective corresponding to ex-ante fairness is only concerned with marginal fairness (see the related discussion in Section 2).

Achieving upper bounds: Since our upper bounds apply to all sequential policies including the optimal online policy (namely, the exponential-sized DP), it would be reasonable if no policy could achieve these upper bounds in polynomial-time. However, we show that not only are these upper bounds achievable, but they can be achieved by our PPA policy. To motivate our policy, let us consider a hypothetical situation where the demand sequence is known a priori. In that case, the optimal allocation under both objectives is to equalize the FRs and then maximize that FR (see eq. 1 and its related discussion). Alternatively, this can be written as a deterministic DP with a simple solution: at each time period, proportionally allocate the remaining supply based on the current demand and the total future demand (see Section 3.2 and Appendix 8). When demand is stochastic, our PPA policy simply replaces all the future random demands by their projected values, namely, their conditional expectations (see eq. 4).

In Sections 3.3 and 3.5, we analyze the ex-post and ex-ante fairness guarantees of the PPA policy and show that it achieves the best of both worlds: our lower bounds on the PPA policy’s guarantees match the corresponding upper bounds for any supply scarcity and any number of agents. These two analyses rely on delicate inductive arguments. For ex-post fairness, we establish a lower bound on the value-to-go function of our PPA policy by analyzing the evolution of the minimum FR and progressively constructing a worst-case joint distribution for demand (see Lemma 3.10 in Section 3.3). For ex-ante fairness, we demonstrate that the expected demand-to-supply ratio before the arrival of each agent is non-increasing when following the PPA policy, which enables us to bound the marginal expected FR for each agent (see Appendix 11).

We highlight that beyond enjoying the best possible guarantees, our PPA policy is practically appealing: it is computationally efficient, interpretable, and transparent. In addition, it does not require full distributional knowledge, as it only relies on the first conditional moments of the joint distribution for demand. Policies which rely on detailed distributional knowledge can be prone to errors or perturbations (see Remark 3.7 and Appendix 7.4).

Establishing sub-optimality of target-fill-rate policies: In addition to showing that our PPA policy achieves the best possible guarantees, we extend our work to studying the subclass of target-fill-rate (TFR) policies. A TFR policy commits upfront to a fill rate , and upon arrival of each agent, it allocates a fraction of that agent’s demand until it exhausts the supply. Our study of TFR policies is motivated by two reasons: (i) since such policies are transparent and easy-to-communicate, they are frequently used in practice, including at the outset of the COVID-19 pandemic when an initial formula allocated a fixed percentage of states’ estimated needs (Washington Post 2020a), and (ii) TFR policies are a natural yet powerful class of non-adaptive policies (see Section 3.4). Consequently, comparing the performance of TFR policies with that of our adaptive PPA policy sheds light on the limitations of making non-adaptive decisions.

Intuitively, a TFR policy can perform poorly because it does not take advantage of information that reduces future uncertainty. For instance, consider a setting with two agents where the second agent’s demand is perfectly correlated with the first agent’s demand. A simple adaptive policy—such as our PPA policy—will perform optimally in such a setting because demand is deterministic upon the first agent’s arrival. The PPA policy achieves such performance by crucially leveraging information about the second agent’s demand when determining the first agent’s fill rate. In contrast, a TFR policy targets the same fill rate regardless of the first agent’s demand, and consequently cannot ensure that sufficient supply remains for the second agent. Based on this intuition, in Section 3.4, we provide a tight bound on the ex-post fairness guarantee of the optimal TFR policy (see Theorem 3.13), which can be considerably lower than the corresponding guarantee of our adaptive PPA policy (see Figure 4(a)). On the other hand, we show that if the coefficient of variation of total demand is low, then the optimal TFR policy can provide a stronger guarantee than our PPA policy (see Proposition 3.14 and Figure 4(b)).

To characterize the ex-post fairness guarantee of the optimal TFR policy, we construct the worst-case total demand distribution against such a policy. In the proof, we establish a rather surprising connection to the literature on monopoly pricing and Bayesian mechanism design (see Hartline (2013) for more details on this literature). In particular, upon mapping the problem of finding the worst-case instance into the quantile space, our problem reduces to a constrained version of the (single-item) monopoly pricing problem (see Remark 3.19). We identify two key properties of the worst-case distribution in this constrained monopoly pricing problem, and by exploiting the connection to our original problem, we end up with the desired characterization of the worst-case total demand distribution against the optimal TFR policy. Due to this connection, our proof technique and corresponding results can be of independent interest (e.g., see Alaei et al. (2019) for proof techniques and results in the same spirit).

Illustrative case study: To demonstrate the effectiveness of our policy, in Section 4 we conduct a numerical case study motivated by the allocative challenges that FEMA faced at the beginning of the COVID-19 pandemic (as discussed at the beginning of this section). Borrowing from the epidemiology literature around the COVID-19 pandemic, we develop a simple compartmental SEIR model that governs the need for medical supplies in different inter-connected locations. Using such a model, we demonstrate that the demand is highly variable and has complex correlation structure across locations (see Figure 6). Our simulation results illustrate the superior performance of our PPA policy compared to both its ex-post fairness guarantee and the optimal TFR policy. Further, the results suggest that our PPA policy performs nearly as well as the DP solution (which, as we discuss, suffers from many practical limitations). Additionally, our simulation results demonstrate the efficiency of our policy as well as its robustness to model mis-specification (see Table 2).

Allocating medical supplies in a pandemic is just one motivating example of the challenges that arise when a governmental or nonprofit organization aims to ration supply among agents whose (a priori uncertain and correlated) needs realize sequentially. Other examples include the allocation of emergency aid when a natural disaster such as a hurricane or wildfire impacts multiple locations over time (Wang et al. 2019), as well as the distribution of food donations by mobile pantries that sequentially visit agencies (Lien et al. 2014).333As explained in detail in Lien et al. (2014), even though the daily demand for food donations from different agencies are not temporally scattered, they will only be observed by the operators upon their arrival at the sites. Our proposed policy can effectively guide transparent allocation decisions in such contexts while also providing a guarantee on the fairness level of the process. Finally, as discussed in Section 5, our framework can be enriched to account for other practical considerations, such as (i) generalized objective functions that enable the social planner to balance equity and efficiency to varying degrees, and (ii) rationing multiple types of resources (see Corollaries 5.21, 5.22, and 5.23 in Section 5.2).

1.2 Related Work

We conclude this section by discussing how our work relates to and contributes to several streams of literature.

Fairness in static resource allocation: Considerations of fairness and its trade-off with efficiency have frequently arisen in the resource allocation literature in operations research and computer science.444Other recent papers have focused on fairness in the contexts of pricing (Cohen et al. 2019), information acquisition (Cai et al. 2020), targeted interventions (Levi et al. 2019), service levels (Jiang et al. 2019), and online learning (Gupta and Kamble 2019). See also the work of Cayci et al. (2020) that considers fair resource allocation with online learning. We begin by discussing papers which study fairness in static (one-shot) allocation settings. The seminal work of Bertsimas et al. (2011) considers a general setting where a central decision-maker allocates divisible resources to agents, each with a different utility function. Focusing on two commonly used notions of fairness in allocation, max-min and proportional fairness, the authors characterize the efficiency loss due to maximizing fairness (see also Bertsimas et al. 2012 and Bertsimas et al. 2013). If demand was deterministic in our setting, the optimal allocation would coincide with that of the max-min objective in Bertsimas et al. (2011). Namely, for both objectives, the optimal allocation consists of maximized equal FRs.

Focusing on indivisible goods, Donahue and Kleinberg (2020) considers the trade-off between fairness and utilization when demand is distributed across different agents. A priori, only demand distributions are known. However, after a one-shot allocation decision, all demand values realize. The fairness notion considered in this line of work is in the same spirit of our notion of ex-ante fairness: they require that an individual’s chance of receiving the resource should not significantly depend on the group to which the individual belongs. Similarly, by maximizing the minimum expected FR, we aim to reduce the impact of an agent’s place in the sequence of arrivals. Sharing similar motivation to our paper, Pathak et al. (2020) and Grigoryan (2021) consider equitable COVID-19 vaccine allocation. However, the settings (e.g., offline and deterministic), models, and techniques in both papers differ drastically from those in this work.

Also falling within the category of static allocation of indivisible goods, a stream of papers in computer science considers allocation problems when agents’ valuations are deterministically known. For deterministic algorithms, recent research has centered on the existence of allocations which satisfy certain fairness properties, such as envy-freeness up to any good (see, e.g., Chaudhury et al. (2020) and references therein). For randomized algorithms, the closest to our work is the recent work of Freeman et al. (2020), which uses notions of ex-post and ex-ante fairness and explores whether both can be achieved simultaneously. They develop a randomized algorithm that is approximately fair ex post and precisely fair ex ante. We ask a similar question, albeit in a dynamic divisible-good setting with random and correlated demand, and we affirmatively answer it: our PPA policy exactly achieves the best possible fairness guarantee ex post as well as ex ante (see Theorems 3.9 and 3.20).

Fairness in dynamic resource allocation: We now turn our attention to papers that consider fairness in dynamic (online) allocation settings. In terms of modeling, closest to our work are Lien et al. (2014) and Sinclair et al. (2020). Motivated by the distribution of food donations by mobile pantries,555For other examples of work in this application area, see Solak et al. (2014), Orgut et al. (2018), and Eisenhandler and Tzur (2019). Lien et al. (2014) introduced the problem of sequential resource allocation which coincides with our base model and the ex-post fairness objective function, in that it aims to maximize the expected minimum FR (although it only studies the special case of independent demands). The recent work of Sinclair et al. (2020) considers a similar model; however, it focuses on a multi-criteria objective which is based on an allocation’s distance from the optimal offline Nash Social Welfare solution. We note that their notion of fairness is also different in nature from ours.666In Sinclair et al. (2020), their notion of fairness is with respect to the absolute allocation, i.e., if possible, agents’ allocation should be equalized regardless of differences in their needs. In contrast, we aim for an allocation which is proportional to need.

The algorithmic aspects of both Lien et al. (2014) and Sinclair et al. (2020) consist of designing novel heuristics and numerically evaluating them against a relevant benchmark (the intractable DP solution and the Nash Social Welfare solution, respectively). On the other hand, we take a theoretical approach and analyze fairness guarantees for the policies we design. Further, we provide upper bounds on the performance of any policy (including the DP solution), which serves a dual purpose: (i) it establishes that our policy is the best possible one if we aim to achieve both ex-ante and ex-post fairness guarantees, and (ii) it highlights the fundamental limits of achieving equity in a dynamic setting.

A related stream of papers in computer science study fair division problems in dynamic settings (Walsh 2011, Kash et al. 2014, Aleksandrov et al. 2015), albeit based on different motivating applications and with different objectives. Consequently, the dynamic aspects of these papers differ from our modeling approach. Walsh (2011) studies a setting where agents arrive over time but allocation decisions are not required to be immediate. In a similar direction, Kash et al. (2014) and Aleksandrov et al. (2015) consider models where agents remain in the system and can receive multiple allocations. Beyond the model dynamics, these papers allow for an arbitrary sequence of arriving agents (e.g., an adversarial arrival model). Moreover, their results pertain to obtaining envy-free allocations, and hence do not rely on a direct comparison of agent’s utilities. In contrast, in our setting agents’ demands are drawn from a known (arbitrarily correlated) joint distribution, and our results center on direct comparisons based on agents’ fill rates (which play the role of the utilities in our model).

In settings with multiple types of resources, Azar et al. (2010) and Bateni et al. (2016) study online versions of Fisher markets and develop policies with fairness guarantees under two different arrival models. The former assumes an adversarial model whereas the latter considers demand that belongs to a general class of stochastic processes.777We remark that papers considering general convex objective functions, such as Agrawal and Devanur (2014) and Balseiro et al. (2020), admit many common fairness objective functions as special cases. See also Mehta (2012) for more details. There are fundamental differences between our work and the aforementioned papers. Just to name one, the settings of Azar et al. (2010) and Bateni et al. (2016) are motivated by online advertising, where demanding agents (advertisers) are offline and items (impressions) arrive in an online fashion. Demanding agents have a large budget compared to the price of each arriving item, and they derive item-specific utilities. Consequently, the fairness notion is concerned with the total utility of each agent, which is a function of all items allocated to it during the horizon. In contrast from such a setting, demanding agents in our work arrive in an online fashion while the supply side is offline, and each demanding agent receives a single allocation. The recent works of Ma and Xu (2020) and Nanda et al. (2020) are closer to our setting in that the demanding agents arrive online; however, they differ in several aspects: (i) the underlying arrival process is known i.i.d. where arriving demand belongs to various groups, (ii) they focus on group-level fairness, and (iii) they consider a matching setting, i.e., allocating indivisible goods.

The objectives of ex-post and ex-ante fairness which we study in our problem bear some resemblance to the objective in the online contention resolution scheme (OCRS) problem, although the two problems are not directly comparable. The OCRS is basically a rounding algorithm that aims to uniformly preserve the marginals induced by a fractional solution while obtaining feasibility of the final allocation. This technique has found application in many settings such as Bayesian online selection, oblivious posted pricing mechanisms, and stochastic probing models (see, e.g., Alaei 2014, Feldman et al. 2016, and Lee and Singla 2018). The OCRS problem diverges from ours because that setting focuses on designing randomized policies for allocating indivisible goods, while our focus is on divisible goods (consequently, restricting to deterministic policies is without loss).

Dynamic allocation of social goods: On a broader level, our paper is related to the literature on dynamic allocation of social goods and services, such as public housing, donated organs, and emergency care. Examples of centralized allocation policies include Kaplan (1984), Ashlagi et al. (2013), Agarwal et al. (2019), and Ashlagi et al. (2019); examples of decentralized mechanisms are Leshno (2019), Anunrojwong et al. (2020), and Arnosti and Shi (2020). For the most part, the aforementioned papers focus on the analysis of social welfare in steady-state models where both demand and supply dynamically arrive. We complement this literature by focusing on equitable allocation in a non-stationary framework where a fixed amount of supply must be rationed across demand that arrives over time.

Further, our work is broadly related to the growing literature on dynamic mechanism design without money (Balseiro et al. 2019, Gorokh et al. 2019, 2021). These papers study settings with repeated interaction between a principal and agents, and they assume that agents’ valuations are drawn independently across individuals and across time. Our framework differs from such settings in several key aspects: (i) each agent only interacts once with the social planner, (ii) agents’ demands can be arbitrarily correlated, and (iii) as explained below, agents are non-strategic.

In our work, we abstract away from strategic behavior and assume that agents do not control the timing of their demand (i.e., the order of their arrival) nor can they misrepresent their demand, either individually or as a coalition. Several papers in the supply chain and social choice literature (see, e.g., Sprumont 1991, Lee et al. 1997, Cachon and Lariviere 1999) study incentive issues that arise when demand for a resource exceeds its capacity in various other contexts with no access to monetary mechanisms (as is the case in our setting). In particular, Lee et al. (1997) shows that proportional allocation (which is the static version of our proposed PPA policy) can induce strategic behavior as agents may benefit from over-stating their demand. However, such strategic considerations are often inapplicable in our motivating applications. In contexts such as a pandemic or a natural disaster, the sequence of realized demand is exogenous. Furthermore, demand is verifiable in these settings, and false reporting can be severely punished under the Disaster Fraud Act.888For one such example, see https://www.oig.dhs.gov/news/press-releases/2019/02202019/manhattan-us-attorney-announces-53-million-proposed-settlement-lawsuit-against-new-york-city-fraudulently-obtaining.

Online resource allocation: From a technical point of view, our work is related to the rich literature on online resource allocation and prophet inequalities, which started from the seminal work of Krengel and Sucheston (1978) and Samuel-Cahn et al. (1984). For an informative survey, we refer the interested reader to Lucier (2017). We highlight that in terms of modeling demand, our work departs from the prevailing approaches in this literature, namely adversarial, i.i.d., or random permutation arrival models. In our work, we assume that the sequence of demands can be arbitrarily correlated and the joint distribution is known in advance. In terms of modeling demand, our work is closest to a few papers that consider prophet inequalities with correlated demand (Rinott and Samuel-Cahn 1992, Truong and Wang 2019, Immorlica et al. 2020). However, the nature of the online decisions is different; in our model, a fraction of a divisible good is allocated to each arriving demand, whereas in prophet inequality settings, an indivisible good is allocated to a single agent.

Finally, our PPA policy relies on re-optimizing the FR by replacing all future random demands by their expected values. As such, it is related to the stream of papers in revenue management and dynamic programming that theoretically analyze the performance of such heuristics. Great examples of work in this direction include Ciocan and Farias (2012), Jasin and Kumar (2012), Balseiro and Brown (2019), and Calmon et al. (2020).

2 Model and Preliminaries

Problem setup: Consider a planner that is using a sequential allocation policy—also referred to as an online policy—to allocate a divisible resource of supply among agents. Without loss of generality, we normalize the total supply so that . Agents arrive sequentially over time periods , and we index agents according to the period in which they arrive. Once agent arrives, their demand is realized and observed by the planner. Based on the observed demand and the history up to time period , the sequential policy makes an irrevocable decision by allocating an amount of the resource to this agent. The allocated amount cannot exceed the agent’s realized demand nor can it exceed the remaining supply before agent ’s arrival, which we denote by . Thus, is a feasible allocation if . Given the feasible allocation and the demand , agent ’s fill rate (FR) is defined as .999If , we set the FR to as a convention. After allocating to agent , the remaining supply before the arrival of agent is .

To model the uncertainty about future demands, we consider a Bayesian setting where the ’s are stochastic and arbitrarily correlated such that ) is drawn from a joint distribution known by the planner. A key characteristic of a demand sequence is the expected demand-to-supply ratio, which we call the supply scarcity as defined formally below.

Definition 2.1 (Supply Scarcity)

The supply scarcity of a demand sequence drawn from a joint distribution is given by:

Since we normalize the supply to be , the supply scarcity is equal to the total expected demand.

For simplicity of presenting our results, we consider joint distributions that assign non-zero probability to at least one sample path of demands with . Equivalently, we assume is not deterministically equal to zero.111111This assumption is without loss of generality, as one can alternatively re-define to be the smallest index such that is deterministically equal to zero for .

As detailed earlier, our setup is motivated by the distributional operations of a governmental or nonprofit organization. Consequently, we focus on an egalitarian planer that intends to balance the equity and efficiency of the allocation. To this end, the planner’s objective is to maximize the minimum achieved FR among the agents, i.e., , given the uncertainty in the demands. Maximizing such an objective has its roots in the classic literature on welfare economics (e.g., Arrow 1963) and has been studied more recently in similar contexts in operations research (e.g., Lien et al. 2014). It provides equity through its focus on the worst FR across all agents—in contrast to the sum of FRs—and provides efficiency by aiming to maximize this FR—in contrast to allocating an equally minimal amount of the resource to all agents.121212We consider a broader class of objectives that subsumes the minimum FR in Section 5.2.

Before introducing our objective function, we comment on our assumptions that the supply is fixed a priori and that we make a one-time allocation decision for each agent. In some applications, supply can get replenished over time, and there can be multiple allocations to the same agent. However, in our motivating applications there is a time urgency that we aim to incorporate into our model: as one example, during a pandemic it may take months to replenish the national stockpile of medical resources such as ventilators.131313During the first peak of the COVID-19 pandemic in the US, it took a few months to produce ventilators, and there were concerns that those ventilators would be ready too late (Washington Post 2020b). In the meantime, a “pandemic wave” may last only a few weeks, which makes any potential second shipment less valuable or even unnecessary. (For instance, the need for ventilators may greatly reduce a few weeks after the peak.) The same features exist in response to a natural disaster, as providing relief is most valuable in the immediate aftermath.

Objectives & fairness guarantees: Since demands are a priori uncertain in the setup described above, the planner should consider appropriate metrics to aggregate over uncertain outcomes. We now formally define the planner’s objectives by considering two different metrics: the ex-post minimum FR and the ex-ante minimum FR. For any sequential allocation policy , the ex-post minimum FR of policy is its expected minimum FR, i.e.,

| (ex-post) |

where is the sequence of allocations generated by . On the other hand, the ex-ante minimum FR of policy is its minimum expected FR, i.e.,

| (ex-ante) |

For a randomized policy , we abuse notation and again use and to denote the expectation of the above two quantities over the policy ’s internal randomness.141414In principle, we allow randomization of our policies in this paper; however, as will be clear later, all of our proposed policies are deterministic and no randomization is needed to obtain our targeted performance guarantees.

These two objectives represent two different notions of fairness: eq. ex-post aims for equity in outcomes, whereas eq. ex-ante aims for equity in expected outcomes. We largely focus on the ex-post minimum FR for two main reasons. First, when allocating supplies in response to a rare event like a pandemic or natural disaster, agents only observe one realized outcome. Because the ex-ante minimum FR is only concerned with marginal fairness, it can have unfair outcomes for every sample path, i.e., every realized demand sequence. In contrast, the ex-post minimum FR considers each full sample path; every sample path with positive probability which results in an unfair outcome reduces . Second, by Jensen’s inequality, the ex-post minimum FR serves as a lower bound on the ex-ante minimum FR, i.e., for any policy ,

However, for a fixed ex-post minimum FR, achieving a higher ex-ante minimum FR is desirable because it reduces systematic biases against a particular agent, e.g., the last-arriving agent. In the extreme case where , one particular agent receives the smallest FR, regardless of the sample path. On the other hand, implies that the worst-off agent varies across different sample paths.

Having defined our notions of fairness, we first observe that if the sequence of demand is deterministic, then the policy that maximizes both the ex-post and the ex-ante minimum FR is simply equalizing all FRs. Namely, this policy achieves a FR equal to:

| (1) |

Inspired by the above observation, we define a normalization factor that will help us with providing more informative performance guarantees.

Definition 2.2 (Normalization Factor)

Given a joint demand distribution with total expected demand of , the normalization factor represents the optimum ex-post and ex-ante minimum FR if is replaced by a deterministic distribution (over demand sequences) with an identical total expected demand .

To see why we introduce the normalization factor , note that the above observation in eq. 1 highlights that even without stochasticity in the demand sequence, when total demand exceeds supply we cannot guarantee a minimum FR better than . This is simply due to the “scarcity of supply.” However, if the sequence of demands is stochastic (and possibly correlated), an ex-post or ex-ante minimum FR of may not be always achievable by an online allocation decision maker due to the “scarcity of information,” i.e., the unknown realizations of future demands. Consequently, we use to enable us to decouple the effect of supply scarcity from the effect of stochasticity in the demand sequence on the quality of online allocation decisions.

We emphasize that is not a benchmark in the sense that it does not serve as an upper bound on the achievable ex-post (or ex-ante) minimum FR for all joint demand distributions with a total expected demand of . Due to the stochastic nature of demand and convexity in our objectives, it is possible that when taking expectation over the realized demand sequence, we can achieve ex-post and ex-ante minimum FR’s that are higher than . However, as explained above, serves as an informative normalization factor to decouple the effects of supply scarcity and information scarcity.151515 In Remark 3.5 and Proposition 3.6 of Section 3.1, we explain that the offline solution is too powerful to allow for a constant-factor competitive ratio. Hence, we do not use that solution as a benchmark.

Consequently, we evaluate policies based on how they perform relative to . For a policy and a joint demand distribution , we say that the policy achieves ex-post fairness (resp. ex-ante fairness) of (resp. ). We aim to design a policy with guarantees on both ex-post and ex-ante fairness that hold universally for all joint demand distributions with agents and supply scarcity . We refer to the universal lower bounds of a policy as its fairness guarantees, which we formally define below.

Definition 2.3 (Ex-post/Ex-ante Fairness Guarantee)

A sequential allocation policy achieves an ex-post fairness guarantee (resp. ex-ante fairness guarantee) of (resp. ), if for all and ,

where denotes the domain of joint demand distributions with agents and total expected demand of .

Our goals are (i) to understand the limits of achieving fairness in sequential allocation by computing upper bounds on the achievable guarantees, and (ii) to obtain tight lower bounds by designing policies with strong ex-post guarantees as well as ex-ante guarantees. We show in Section 3 that no gap exists between the achievable upper and lower bounds under both ex-post and ex-ante notions. More specifically, we show how to obtain exactly matching upper and lower bounds for both notions of fairness using a single adaptive policy.

3 Optimal Bounds on Fairness Guarantees

In this section, we present our main results for the setting introduced in Section 2. First, we focus on ex-post fairness in Section 3.1 and establish parameterized upper bounds on the ex-post fairness guarantee achievable by any sequential allocation policy—whether adaptive or non-adaptive, computationally efficient (i.e., with polynomial running time) or not. Then, somewhat surprisingly, we show that such upper bounds can be achieved by our policy, which is introduced and analyzed in Sections 3.2 and 3.3. Next, to illustrate the power of our simple adaptive algorithm, in Section 3.4 we characterize the ex-post fairness guarantee of the best policy which non-adaptively aims for a particular target fill rate, and we show that our policy performs favorably compared to such a policy. Finally, in Section 3.5 we turn our attention to the notion of ex-ante fairness, and we show that our policy also achieves the best possible ex-ante fairness guarantee.

3.1 Upper Bound on Ex-post Fairness Guarantee

We begin this section by establishing a fundamental limit on ex-post fairness for any allocation policy when faced with stochastic and sequential demands. The main result of this subsection is the following theorem:

Theorem 3.4 (Upper Bound on Ex-post Fairness Guarantee)

Given a fixed number of agents and supply scarcity , no sequential allocation policy obtains an ex-post fairness guarantee (see Definition 2.3) greater than , defined as

| (2) |

See Figure 1 for an illustration of this upper bound as a function of the supply scarcity and the number of agents . Per Definition 2.3, the ex-post fairness guarantee is relative to the achievable minimum FR when demands are deterministic, namely . Consequently, this upper bound provides insight into the unavoidable loss in efficiency and equity when demands are a priori uncertain and realize sequentially. In particular, we remark that the achievable fairness guarantee crucially depends on the supply scarcity. In the regime where , which we refer to as the under-demanded regime, initially worsens as increases before hitting its minimum (for any fixed ) when expected demand equals supply, i.e., at . This suggests that the stochastic nature of demand is most harmful when expected demand exactly equals supply. On the other hand, in the over-demanded regime where , the achievable fairness guarantee is independent of . Given that we are usually in the over-demanded regime in our motivating applications, Theorem 3.4 ensures that supply scarcity does not contribute to the loss in fairness due to uncertain, correlated, and sequential demand. Fixing , the upper bound always decreases with , implying that achieving fairness can be more challenging for a larger population of agents with stochastic demands, even if the total expected demand of the population remains the same. Finally, we highlight that the bound is always at least regardless of the supply scarcity and the number of agents, and it attains its minimum when and .

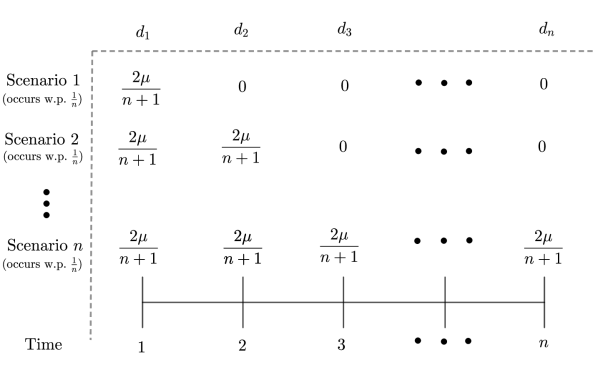

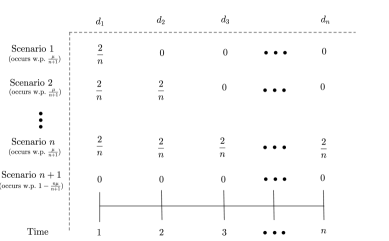

The proof of Theorem 3.4 relies on establishing two hard instances with similar structures, one for and one for . The details of the proof are presented in Appendix 6.1. Here, we present the instance for the over-demanded regime along with a sketch of our analysis. In this instance, there are possible equally-likely scenarios, i.e., scenario happens with probability for . In scenario , the first agents have equal demand of and the rest have no demand. We illustrate this instance in Figure 2(a).161616We remark that similar settings can occur in practice. As one example, consider the challenge of allocating limited disaster-relief supplies to towns damaged by a hurricane which may continue on its destructive path or may veer back out to sea.

First, note that the total supply scarcity for the above hard instance is (as shown in Appendix 6.1). Next, consider any sequential policy that faces a non-zero demand from agent . The policy cannot distinguish among possible scenarios . Consequently, its allocation decision for agent will be independent of the scenario. In light of this observation, any policy can be sufficiently described by a set of (possibly random) allocations with expected values , such that if agent has non-zero demand, then they receive an expected allocation . Given , the minimum FR for scenario is

| (3) |

where the first inequality is due to the expectation of a minimum being less than the minimum over expectations (Jensen’s inequality).

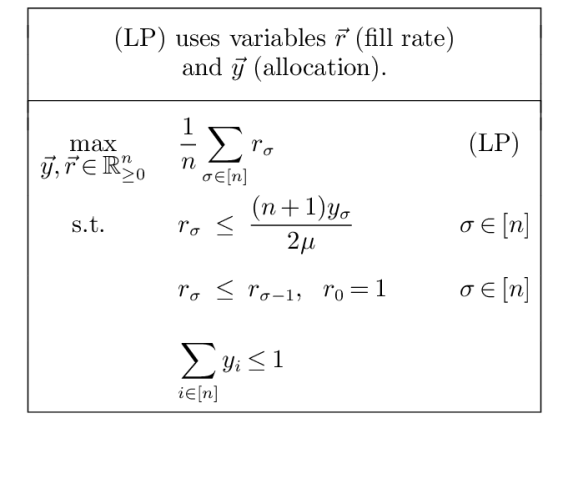

In order to establish our upper bound, we set up a factor-revealing linear program as presented in Figure 2(b). The LP maximizes the expected minimum FR subject to three sets of natural constraints that must hold for any sequential policy:

-

•

The minimum FR in scenario cannot exceed the FR for agent , as shown in eq. 3.

-

•

The minimum FR in scenario is at most the minimum FR in scenario .

-

•

The total amount of expected allocations cannot exceed the available supply of .

In Appendix 6.1, we provide an upper bound on the optimal value of this LP by presenting a feasible solution to its dual. To complete the proof of Theorem 3.4, we must scale by to translate this upper bound on the expected minimum FR into an upper bound on ex-post fairness (see Definition 2.3).

We finish this subsection with two important remarks regarding (i) the use of the offline solution as a benchmark and (ii) the shortcomings of the optimum online solution.

Remark 3.5 (Comparison with Offline Solution)

In sequential decision making problems, it is common to evaluate the performance of a policy by comparing it to the offline solution, i.e., the optimum solution that observes the entire demand sequence before making any decisions (see, e.g., Mehta 2012 and references therein). However, in our setting, such an offline solution proves to be too powerful, in the sense that it is impossible to achieve a constant-factor guarantee compared to such a solution. In the following proposition (proven in Appendix 6.2), we use the same example as shown in Figure 2(a) to establish this impossibility result.

Proposition 3.6 (Comparison with Offline Solution)

Given a fixed number of agents , there exists a supply scarcity such that no sequential allocation policy can guarantee more than a fraction of the expected minimum fill rate achieved by the offline solution.

In light of the above proposition, we focus on establishing absolute guarantees on the expected minimum fill rate. However, as explained in Section 2 (see Definition 2.2 and its related discussion), we use the normalization factor to disentangle the effects of supply scarcity from the effects of sequential decision-making when faced with a stochastic demand sequence.

Remark 3.7 (Optimum Online Solution)

A natural candidate for a policy that may achieve the upper bound on the ex-post fairness guarantee – given by eq. 2 – is the optimal online policy which can be found via a DP. In Appendix 7, we formally present the underlying DP. However, we also illustrate that there are significant limitations and drawbacks to a DP approach for maximizing the expected minimum FR in this setting. First, (i) as we show in Appendix 7.2, the state space of such a DP is exponentially large for arbitrarily correlated demands, which makes the DP intractable (in particular, the state space is exponential in the number of agents ). Nevertheless, in Appendix 7.3 we present an FPTAS for the special case of independent demand. Even beyond computational challenges, (ii) solving the DP requires full distributional knowledge, (iii) such a DP solution does not necessarily perform well for our second objective function, i.e., maximizing the ex-ante minimum FR, and (iv) the DP decisions may lack transparency and interpretability, which are highly desirable properties in our motivating applications. (For an illustration of points (iii) and (iv), see Example 7.28 in Appendix 7.4; for a summary of the drawbacks of the DP, see Table 3).

Remarkably, in the following subsection, we design a simple adaptive policy that not only achieves the best possible ex-post fairness guarantee of , but also offers several corresponding advantages over a DP solution: (i) it can be computed efficiently, (ii) it only requires knowledge of the conditional first moments of agents’ demands, and (iii) its decisions can be clearly explained. Additionally, as shown in Section 3.5, it simultaneously attains the best-possible ex-ante fairness guarantee.

3.2 Projected Proportional Allocation Policy

We introduce our policy, referred to as the projected proportional allocation (PPA) policy, through the following simple intuition. Consider a planner that (magically) has access to all the demand realizations . As already discussed in Section 2, to maximize the minimum FR when the demand realizations are known a priori, the planner should equalize the FR of all agents by allocating to each agent . If is at most the initial supply (which we normalize to ), then each agent obtains a full allocation of in such a solution. This results in the maximum equal FR of . Otherwise, all the agents will have an equal FR of , which is when each demand is equal to its expected value.

This solution can alternatively be obtained by solving a DP that returns allocations maximizing the minimum FR. By a simple induction argument, given the remaining supply at period , this DP maintains the following invariant at each period (refer to Appendix 8 for details):

| (4) |

Notably, the above invariant suggests a sequential implementation of the optimal solution at each period that only uses the knowledge of (i.e., the current demand at period ) and (i.e., the total future demand from period to ). Now consider a setting with incomplete information, namely, with only knowledge of the current sample path of the observed demands up to period , which we denote by . Our PPA policy implements a version of the above policy by replacing the exact realization of total future demand with the conditional first moment of this random variable given the current sample path. More precisely:

Note that the conditional expected future demand given all previously-realized demands is a function of ; however, for ease of notation, we use without any input arguments.

We highlight that the PPA policy is simple, computationally efficient, and solely uses first-moment knowledge about the future demands. Consequently, the PPA policy does not need to know the order of future arrivals. Further, because the allocation decisions of the PPA policy depend smoothly on the first moment of future demand, these decisions are robust to small changes in the scale of any marginal distribution. Yet, as we show in Sections 3.3 and 3.5, this simple policy remarkably achieves the best possible guarantee for both notions of fairness (ex-post and ex-ante), even though these two notions are quantitatively different whenever .

We now point out an important technical property of the PPA policy that will help us in establishing these key results.

Remark 3.8

The PPA policy can only run out of supply at the end of period if , or equivalently, only if all future demands are deterministically equal to zero, conditional on the current realized sample path of demands . This property holds simply because

To conclude this section, we note that one can consider a policy similar to our PPA policy but with a slightly different updating rule that is monotone non-increasing in the fill rate. In particular, suppose the allocation at any time is given by , where is the minimum FR before the arrival of agent . In words, this alternative policy ensures that in each time period we do not have a fill rate larger than the current minimum FR. While such an alternative policy achieves weakly larger ex-post fairness than our PPA policy, the two policies provide an identical ex-post fairness guarantee (see Section 3.3). Furthermore, this alternative policy suffers from a significant drawback: by definition, it systematically disfavors late-arriving agents. In fact, the minimum FR under this policy is always attained by the last agent (agent ) as long as that agent’s demand is non-zero, which leads to a sub-optimal ex-ante fairness guarantee. In sharp contrast, our PPA policy avoids systematically disfavoring late-arriving agents; consequently, in Section 3.5 we show that our PPA policy achieves the best possible ex-ante fairness guarantee.

3.3 Ex-post Fairness of PPA Policy

In this section, we analyze the ex-post fairness guarantee of our PPA policy. In the following theorem, we show that this simple policy indeed achieves the best possible ex-post fairness guarantee.

Theorem 3.9 (Ex-post Fairness Guarantee of PPA Policy)

Given a fixed number of agents and supply scarcity , the PPA policy achieves an ex-post fairness guarantee (see Definition 2.3) of at least (defined in eq. 2).

3.3.1 Proof of Theorem 3.9

In order to prove the above theorem, we would have liked to analyze the evolution of the minimum FR, which we denote with at the end of period , i.e., for . Instead, we consider the evolution of a closely related stochastic process, which makes the analysis simpler. We define this surrogate stochastic process as follows:

| (5) |

First, we note that , . Next, recall that denotes the remaining supply after agent arrives and receives an allocation. We observe that under the PPA policy, evolves according to

| (6) |

With the above observations, the main step of the proof is carefully analyzing the evolution of under the PPA policy, which enables us to lower bound the final expected minimum FR in the following lemma.

Lemma 3.10 (Lower Bound on Expected Minimum FR)

Since the objective of our dynamic decision-making problem has no per-stage rewards and consists only of a terminal reward (i.e., the minimum FR), Lemma 3.10 can be thought of as establishing a lower bound on the value-to-go function of the PPA policy. Before providing the proof for this key lemma, we lay out the two remaining steps that finish the proof of Theorem 3.9: (i) plugging into inequality (7) to obtain a lower bound on , and (ii) scaling the obtained lower bound result by our normalization factor, namely , which provides an ex-post fairness guarantee (see Definition 2.3).

Proof 3.11

Proof of Lemma 3.10: We will show that inequality (7) holds via backwards induction. The base case of is trivial as it follows from the observation we made earlier: .

Now let us consider . Instead of proving inequality (7), we prove a stronger result:

| (8) |

Establishing inequality (8) means that the inequality in (7) holds for any realization of agent ’s demand. Consequently, it will hold when we take an expectation over agent ’s demand. In order to prove inequality (8), we consider two different cases that can arise depending on the remaining supply , agent ’s demand , and the future expected demand . In the following, we introduce and analyze these cases separately.

-

(i)

Sufficient supply (): Recall that according to the PPA policy, . Therefore, in this case, either , i.e., the PPA policy meets the entire demand, or , i.e., the PPA policy attains an FR of at least . According to the dynamics specified in (5) and (6), this implies

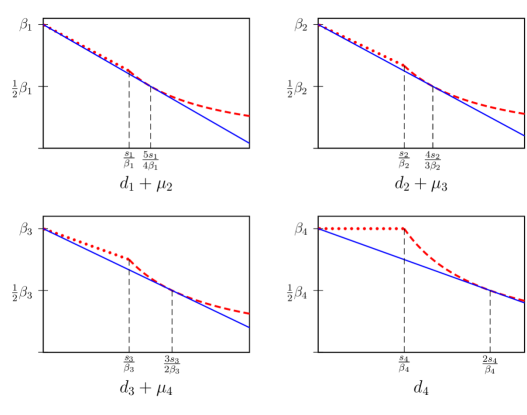

Using our inductive hypothesis when ,

(9) The lower bound given by is a linear function of , as illustrated by the dotted red lines in all panels of Figure 3 (in the regime where ). This linear function has a non-positive slope and an intercept of . We can further lower bound this function for any by another linear function with the same intercept of and a smaller (more negative) slope. In particular, since , we have:

(10) which proves inequality (8) in the sufficient supply case (see the blue lines in all panels of Figure 3).

- (ii)

The lower bound given by is a convex homographic function of , as illustrated by the dashed red lines in all panels of Figure 3 (in the regime where ). To further lower bound this function by a linear function, note that for any variable the following inequality holds:

The proof of the above inequality is purely algebraic and we omit it for brevity. Substituting in this inequality, we have:

| (12) |

which proves inequality (8) in the insufficient supply case (again, see the blue lines in all panels of Figure 3).

3.4 Simple Non-adaptive Policies and Ex-post Fairness

As discussed in the previous sections, our PPA policy is adaptive, that is, the FR for agent (and its corresponding allocation decision) can depend not only on the observed demand but also on the exact sample path up to time as well as the remaining supply . In contrast to an adaptive policy, a non-adaptive policy commits to a sequence of feasible allocation maps upfront, where is the allocation decision for agent when agent has demand .191919For ease of presentation, we focus on deterministic non-adaptive policies. This is without loss of generality, as the ex-post fairness of any randomized non-adaptive policy must be weakly dominated by the ex-post fairness of one of the deterministic policies that it randomizes over. If the non-adaptive policy’s allocation decision exceeds the remaining supply , then agent instead receives the entire remaining supply.

For settings that we consider, adaptivity can indeed help with improving the expected minimum FR of a policy. As an example, compare running our PPA policy versus the best non-adaptive policy on an instance with three agents. In this instance, the demands follow one of the two possible sample paths or with equal probabilities , where and . After agent ’s demand is realized, the PPA policy knows exactly which sample path is happening. By calculating the exact total demand of agents and , it obtains the optimal expected minimum FR of for small . However, a non-adaptive policy cannot distinguish between the two possible sample paths after agent ’s demand is realized. Therefore, without loss of generality, it targets a FR of for agent and obtains an expected minimum FR of for small , which attains its maximum equal to at any .

In applications that allow for adaptivity, our PPA policy obtains the optimal ex-post fairness guarantee while also having the desirable properties of transparency and interpretability. However, adaptivity is not admissible in some practical scenarios—e.g., when the social planner should commit to an allocation plan in advance for even more transparency or due to legal restrictions.202020As discussed in the introduction, the initial strategy for allocating medical supplies at the beginning of COVID-19 pandemic had the form of a target-fill-rate policy, which is a canonical non-adaptive strategy as we will discuss soon. Motivated by such scenarios, we study two simple and natural canonical classes of non-adaptive policies: those that fix the sequence of allocation decisions a priori, namely they specify one allocation vector , and “smarter” policies which fix the sequence of fill rates a priori. In Appendix 9, we show that the ex-post fairness guarantee for the former subclass is vanishing as gets large. Therefore, we focus on the latter subclass, which is formally defined as follows.

Definition 3.12 (Target-fill-rate Policies)

A target-fill-rate (TFR) policy is any policy which pre-determines a target fill rate . Then, for every arriving agent , the policy must either allocate sufficient supply to meet the target or allocate all remaining supply, i.e.,

In the following theorem, we provide a tight bound on the ex-post fairness guarantee (Definition 2.3) achievable by the optimal TFR policy—defined as the one that maximizes ex-post fairness for the given joint demand distribution. We remark that setting one threshold is without loss of generality because the ex-post fairness guarantee of a policy which pre-determines a sequence of target fill rates is upper bounded by that of a TFR policy with the same target fill rate for all agents. We also highlight that in addition to achieving a lower ex-post fairness guarantee compared to our adaptive policy, finding the best TFR policy requires full knowledge of the total demand distribution—in contrast to our PPA policy which only requires knowing the first conditional moments of the future total demand at each time.

Theorem 3.13 (Ex-post Fairness Guarantee of Optimal TFR Policy)

Given any number of agents and supply scarcity , the optimal TFR policy achieves an ex-post fairness guarantee (see Definition 2.3) of .

In Figure 4(a), we compare the guarantee of the optimal TFR policy against our PPA policy for different model primitives, and . First, we note that when is not too large, our PPA policy achieves a considerably higher guarantee. Next, we highlight that the ex-post fairness guarantee for the optimal TFR policy does not depend on the number of agents .212121We elaborate on the intuition behind this behavior when we present the hard instance for establishing the upper bound of Theorem 3.13. This is in contrast to the ex-post guarantee for the PPA policy , which worsens as the number of agents increases. Furthermore, the guarantee in Theorem 3.13 has a unique minimum of when . This once again suggests that the stochastic nature of demand is most harmful when expected demand exactly equals supply. Before presenting the proof of Theorem 3.13 (which we defer to Section 3.4.2), we first discuss a special case where TFR policies can provide a substantially stronger fairness guarantee.

3.4.1 Optimal TFR Policy for Low-Variance Distributions

Having presented our general result for the optimal TFR policy, we note that we make no assumption about the demand distribution in the statement of Theorem 3.13, aside from parameterizing the result by the expected total demand. Because non-adaptive policies such as the optimal TFR policy cannot update their decisions based on new information, we would expect their performance to suffer when the variance of total demand is high (fixing its expectation). For instance, the worst-case distributions that establish our parameterized tight bound for TFR policies (see Theorem 3.13) all have a coefficient of variation (CV) greater than . Inspired by this observation, in the following proposition we provide an alternative lower bound on the ex-post fairness guarantee of the optimal TFR policy that is parameterized by an upper bound on the CV.

Proposition 3.14 (Optimal TFR Policy for Bounded Coefficient of Variation)

Suppose the coefficient of variation for total demand is at most . (Equivalently, suppose the standard deviation of total demand is at most .) Then for any supply scarcity , the optimal TFR policy achieves an ex-post fairness guarantee (see Definition 2.3) of at least

| (13) |

We provide the proof of Proposition 3.14 in Appendix 10.2. We do not have a closed-form expression for this improved lower bound, but the single-variable concave maximization problem in (13) is easy to solve numerically. We note that the lower bound on the guarantee of the optimal TFR policy approaches as the CV approaches , regardless of the supply scarcity .

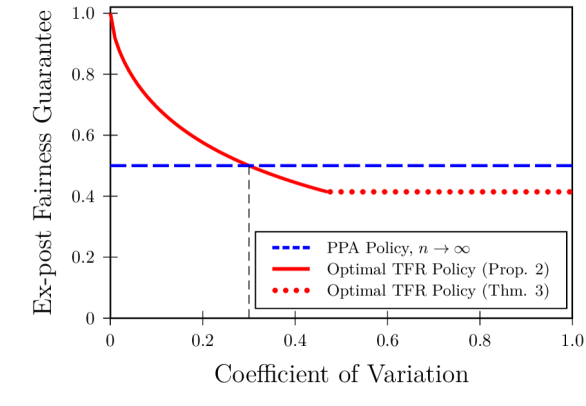

Even though the lower bound in Proposition 3.14 is not necessarily tight, as long as the CV is sufficiently small, this lower bound improves upon the bound in Theorem 3.13 (which holds for an arbitrary coefficient of variation).222222The value for at which the two bounds cross depends on the supply scarcity . Numerically, we find that if , the lower bound in Proposition 3.14 provides a better guarantee for any . Furthermore, this bound establishes that in settings where the CV is below a threshold, the optimal TFR policy can provide an improved guarantee relative to the PPA policy.

In Figure 4(b), we illustrate the lower bound on the optimal TFR policy when the supply scarcity , as a function of the CV (solid red line when the bound is given by Proposition 3.14, dotted red line when the bound is given by Theorem 3.13). We compare this lower bound to the infimum of all lower bounds provided by the PPA policy. (This infimum, shown by the dashed blue line, occurs when , and it is equal to as given by Theorem 3.9.) In the case shown (where ), the lower bound on the guarantee of the optimal TFR policy given by Proposition 3.14 dominates the bound given by Theorem 3.13 when the CV is below . Importantly, the optimal TFR policy can provide improvement compared to the PPA policy if the CV is less than .232323For the sake of brevity, we only show this comparison when the supply scarcity , but similar results hold for other supply scarcity levels.

Thus, in cases where total demand is known to be well-concentrated, such as in instances with a large number of i.i.d. demands, TFR policies can perform quite well. In contrast, the PPA policy is particularly valuable when demand is correlated and highly variable. We emphasize that such demand sequences may arise in our motivating applications, such as when responding to a pandemic or natural disaster. In our case study presented in Section 4, we present a simple example for the COVID-19 pandemic based on commonly-used epidemiology models which exhibits correlation across demands and a high coefficient of variation for total demand.

3.4.2 Proof of Theorem 3.13

We now provide a proof of Theorem 3.13, with some details deferred until Appendix 10.1. We begin by placing a lower bound on the performance of the optimal TFR policy, and we then demonstrate the existence of a matching upper bound.

Proof 3.15

Proof of lower bound: For any target fill rate , a TFR policy will achieve that fill rate if . Let us define as the cumulative distribution function (CDF) of the random variable , where . For ease of notation, we use to denote the domain of all such CDFs. Given a CDF , a TFR policy with target fill rate achieves an expected minimum fill rate of at least , which implies that the optimal TFR policy attains an expected minimum fill rate of at least . In the following lemma, we establish a lower bound on , which enables us to lower-bound the ex-post fairness guarantee that the optimal TFR policy achieves.

Lemma 3.16 (Tight Lower Bound for Optimal TFR Policy)

Given a fixed number of agents and supply scarcity , the following holds:

| (14) |

This infimum is attained by the following CDF

| (15) |

where .

Before presenting the proof of the above lemma in Section 3.4.3, which is the key step of the proof of Theorem 3.13, we establish a matching upper bound and complete the proof of the theorem.

Proof 3.17

Proof of upper bound: We show a matching upper bound by considering a two-agent instance. In this instance, only the first agent has stochastic demand. In particular, for (defined in eq. 15) and deterministically. Note that . For any target fill rate where , supply will be exhausted before the arrival of agent with probability , in which case the minimum FR will be . Therefore, the expected minimum fill rate of the optimal TFR policy in this instance is at most

where the equality follows from Lemma 3.16.

By allowing , we conclude that there exists an instance where the expected minimum fill rate of the optimal TFR policy is , which matches the lower bound from above. We remark that the construction of the above two-agent example clarifies why our upper bound does not depend on the number of agents: we can modify the example to an -agent one where the total demand of the first agents have correlated demand equal to for and the last agent has a deterministic demand of .

With the above (matching) bounds, we complete the proof of Theorem 3.13 by scaling this tight bound by our benchmark for deterministic demand, namely , to arrive at the guarantee stated in Theorem 3.13. \Halmos

3.4.3 Proof of Lemma 3.16 and Connections to Monopoly Pricing

Having laid out the proof steps of Theorem 3.13, we now provide a constructive proof of the key lemma, i.e., Lemma 3.16. We do so by identifying properties of the worst-case distribution against the optimal TFR policy, which enables us to exactly characterize that distribution.

To aid in this proof, we introduce a one-to-one mapping of each target fill rate into the quantile space, such that quantile corresponds to TFR if and only if there is sufficient supply to meet a fraction of demand with probability exactly . We start by describing notation for this transformation, along with some basic properties, in the following definition. For simplicity of exposition, we assume all the distributions playing the role of are non-atomic.242424This assumption is without loss of generality, as one can always add an infinitesimal continuous perturbation to each distribution, which does not change any of the arguments in this proof.

Definition 3.18 (TFR in Quantile Space)

Given a (non-atomic) CDF and inverse total demand , we define the following mappings.

-

•

TFR-to-quantile map : The quantile corresponding to TFR is . In words, the probability of being able to meet a fraction of total demand is . This map is monotone non-increasing.

-

•

Quantile-to-TFR map : The TFR corresponding to quantile is . In words, is the TFR for which the probability of being able to meet a fraction of total demand is . This map is monotone non-increasing and is the inverse of the TFR-to-quantile map, i.e., .

-

•

The expected achievable fill rate (EAFR) curve : For , is the EAFR when the probability of meeting demand (given the TFR) is exactly equal to , i.e., the EAFR obtained by targeting a fill rate .

Remark 3.19

In light of the above transformation, we remark that there is a reduction from our setup to a single-parameter Bayesian mechanism design problem in which a monopolistic seller has an item to sell to a single buyer with private valuation , where is the common prior valuation distribution. See Alaei et al. (2019) for an example of such a setting; also refer to Hartline (2013) for more details on monopoly pricing. In this reduction, target fill rates correspond to prices and the EAFR corresponds to the expected revenue in monopoly pricing (accordingly, the EAFR curve also corresponds to the revenue curve). The problem in this parallel monopoly pricing setting is identifying the worst-case distribution satisfying , so that we minimize the maximum revenue obtained from selling the item at prices constrained to be in the interval .

According to Definition 3.18, is equivalent to for any TFR . Based on this insight, to prove Lemma 3.16, it is sufficient to show that

| (16) |

Consider all cumulative distribution functions . We first identify two additional constraints on that do not change the infimum in eq. 16. These constraints enable us to find the worst-case distribution that achieves the infimum value which establishes the desired result.

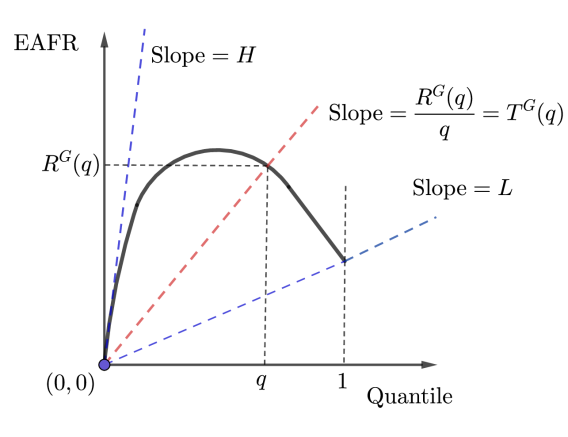

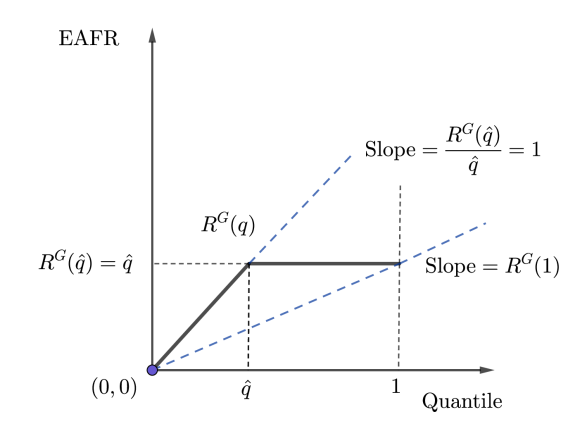

Before proceeding, we develop intuition using an illustrative example of the EAFR curve shown in Figure 5(a). In general, if one draws as a function of (i.e., in the quantile space), then the slope of the line connecting the point to is equal to . This slope is monotone non-increasing in for any CDF according to Definition 3.18. Hence, given the EAFR curve , the support of the feasible fill rates is equal to , where and . The two constraints that we will add below, as stated in Claims 1 and 2, imply that the outer optimization problem in eq. 16 will remain unchanged if we require the EAFR curve to be (i) flat over quantiles corresponding to target fill rates in , i.e., quantiles in the interval , and (ii) a straight line with slope for quantiles in the interval . With these two additional constraints, in Claim 3 we find the worst-case CDF, which has an EAFR curve as shown in Figure 5(b).

Claim 1 (Equal EAFR)

Adding the constraint to the outer optimization in eq. 16 does not change its infimum value.

We prove Claim 1 by contradiction: we show that for any CDF , if the above condition does not hold, we can slightly modify to design a new distribution which has an EAFR curve with a lower maximum value. The details are presented in Appendix 10.1.1. The above claim readily implies that we can focus on distributions for which the EAFR curve is flat in the interval .

Next, we claim that we can restrict our attention to distributions where there is no probability mass for . Said differently, the support of inverse demand is .

Claim 2 (Restricted Support for Inverse Demand)

Adding the constraint for all and to the outer optimization in eq. 16 does not change its infimum value.

We also prove Claim 2 by contradiction: we show that for any CDF , if there is probability mass on , we can construct a CDF which has an EAFR curve with a lower maximum value by shifting that mass to . The details are presented in Appendix 10.1.2. Again, note that this claim implies that we can focus on distributions for which the EAFR curve starts with a straight line up to quantile .

Given the two claims above, the distribution that attains the infimum in eq. 16 must satisfy the two constraints introduced. Figure 5(b) summarizes the effect of these two restrictions on .

Claim 3 (Worst-case CDF)

We prove Claim 3 in Appendix 10.1.3. Since the EAFR curve has a maximum value of , we have shown that the optimal TFR policy always achieves an EAFR of at least . This completes the proof of Lemma 3.16. \halmos

3.5 Ex-ante Fairness

In this section, we study our second notion of fairness, namely, ex-ante fairness. As we did for ex-post fairness, we first establish an upper bound on the ex-ante fairness guarantee achievable by any policy. More importantly, we then show that our PPA policy achieves this worst-case ex-ante fairness bound. The following theorem establishes our matching upper and lower bounds on the ex-ante fairness guarantee.

Theorem 3.20 (Ex-ante Fairness Guarantee of PPA Achieves Upper Bound)

Given a fixed number of agents and supply scarcity , no sequential allocation policy obtains an ex-ante fairness guarantee (see Definition 2.3) greater than , defined as

| (17) |

Further, the PPA policy achieves an ex-ante fairness guarantee of at least .

Like its counterpart for ex-post fairness, depends on the supply scarcity, , and is at its lowest when expected demand equals supply, which highlights the loss due to stochasticity when trying to achieve efficiency and equity ex ante. However, unlike the bound for ex-post fairness, the ex-ante fairness bound is independent of the number of agents. In fact, this bound is identical to the ex-post fairness bound in the single-agent case, i.e. (which is shown by the dotted line in Figure 4(a)).

For intuition about this relationship, note that one feasible policy is to allocate supply to each agent proportional to their expected demand. Since the ex-ante problem only depends on marginal FRs, this reduces ex-ante fairness to the minimum ex-ante fairness across single-agent instances (where in each instance, the supply scarcity is ). In a single-agent instance, ex-ante fairness is equal to ex-post fairness, which implies that any lower bound on single-agent ex-post fairness also serves as a lower bound on ex-ante fairness with agents. Furthermore, since demands can be perfectly correlated, any single-agent instance can be expressed as an instance with agents for any . This implies that any upper bound on single-agent ex-post fairness also serves as a upper bound on ex-ante fairness with agents.

To prove the upper bound in Theorem 3.20, we build on the hard instances from the proof of Theorem 3.4. To prove the lower bound, we use ideas similar to the proof of Theorem 3.9. We show that when following the PPA policy, the expected FR for each agent is a decreasing and convex function of the ratio of expected remaining demand to remaining supply upon their arrival. We inductively place an upper bound on the ex-ante expected value of that ratio for each agent, which enables us to provide a lower bound on ex-ante fairness. See Appendix 11 for a detailed proof.

4 Numerical Results

We complement our theoretical developments with an illustrative case study motivated by the allocative challenges of rationing medical supplies in the midst of a pandemic. First, we describe a simple compartmental model that governs the need for medical supplies experienced by different locations, which is based on models used to forecast the COVID-19 pandemic. We illustrate that in such a setting, the demand is sequential, highly variable, and has complex correlation structure due to network effects. Then, we study this dynamic rationing problem within our framework and illustrate the effectiveness of our PPA policy by comparing it to (i) its theoretical guarantee (presented in Theorem 3.9), (ii) the optimal TFR policy (defined in Section 3.4), and (iii) a DP approach (similar to the one described in Appendix 7). We conclude this section by demonstrating the efficiency of our policy as well as its robustness to mis-specification of model parameters.

4.1 Pandemic Demand Model

We model the spread of a pandemic across inter-connected locations using a standard SEIR (susceptible, exposed, infectious, recovered) model, with different compartments for different locations. Such compartmental models are commonly-used and frequently influence practice. (See, e.g., Morozova et al. 2021.) Each location represents an agent in our allocation framework, and we use the peak number of infected individuals in a location as a proxy for that agent’s need.

4.1.1 SEIR Model Dynamics

In the following, we briefly overview the SEIR model that we borrow from the epidemiology literature (Anderson and May 1992, Diekmann and Heesterbeek 2000). In this model, there are locations where location has population . Individuals interact with each other according to a time-varying rate (which we will specify later). Individuals in location predominantly interact with members of their own location, but a small fraction of their interactions occur with a member of an adjacent location , where is equally likely to be any of location ’s neighbors (denoted by the set ). When a susceptible individual interacts with an infectious individual, the susceptible individual becomes exposed. Exposed individuals become infectious after a random time drawn from an exponential distribution with mean , and infectious individuals become recovered after a random time drawn from an exponential distribution with mean . For large networks, this system approaches the deterministic dynamics presented in (18), with , , , representing the fraction of the population that is susceptible, exposed, infected, and recovered (respectively) in location at time . We will use these dynamics to simulate pandemic trajectories.

| (18) |

4.1.2 SEIR Model Primitives