CRPS Learning

Abstract

Combination and aggregation techniques can significantly improve forecast accuracy. This also holds for probabilistic forecasting methods where predictive distributions are combined. There are several time-varying and adaptive weighting schemes such as Bayesian model averaging (BMA). However, the quality of different forecasts may vary not only over time but also within the distribution. For example, some distribution forecasts may be more accurate in the center of the distributions, while others are better at predicting the tails. Therefore, we introduce a new weighting method that considers the differences in performance over time and within the distribution. We discuss pointwise combination algorithms based on aggregation across quantiles that optimize with respect to the continuous ranked probability score (CRPS). After analyzing the theoretical properties of pointwise CRPS learning, we discuss B- and P-Spline-based estimation techniques for batch and online learning, based on quantile regression and prediction with expert advice. We prove that the proposed fully adaptive Bernstein online aggregation (BOA) method for pointwise CRPS online learning has optimal convergence properties. They are confirmed in simulations and a probabilistic forecasting study for European emission allowance (EUA) prices.

keywords:

Combination , Aggregation , Online , Probabilistic , Forecasting , Quantile , Time Series , Distribution , Density , Prediction , SplinesJEL:

C15 , C18 , C21 , C22 , C53 , C58 , G17 , Q471 Introduction

Combination and aggregation methods are gaining popularity in forecasting, especially in meteorology, energy, economics, finance, and machine learning communities (Hsiao & Wan, 2014; Atiya, 2020; Petropoulos et al., 2020). As the predictive accuracy of different forecasting methods may vary over time, several methods learn about this behavior. So there are time-varying and adaptive weighting schemes. Also, in probabilistic forecasting, where we aim to predict the full predictive distribution or density, many combination methods exist, such as the Bayesian model averaging (BMA) (Raftery et al., 2005; Fragoso et al., 2018). However, individual forecasters may perform differently in different parts of the distribution. For instance, one is more accurate in the center while others are more accurate in the distribution’s tails. Thus, intuitively, it makes sense to exploit this potential of varying performance across the distribution, as we will do in this manuscript.

There are various ways to combine distribution function forecasts to receive a target distribution forecast. The most popular linear approaches are combining across probabilities (vertical aggregation) and combining across quantiles (horizontal aggregation, Vincentization) (Lichtendahl Jr et al., 2013; Busetti, 2017). Both principles are valid and have their pros and cons, depending on the forecasters’ objective. In econometric and statistical literature, forecast combination with respect to the Kullback-Leibler divergence is popular. This approach corresponds to minimizing the log-score of density and usually utilizes the combination across probabilities (Gneiting & Ranjan, 2013; Aastveit et al., 2014; Kapetanios et al., 2015; Aastveit et al., 2019).

Other recent publications focus on forecast combination with respect to the continuous ranked probability score (CRPS), a strictly proper scoring rule for distributions, which does not require a density (Gneiting & Raftery, 2007). For instance, Raftery et al. (2005) combine density forecasts using BMA with refinement by minimizing the CRPS. Jore et al. (2010); Opschoor et al. (2017); Thorey et al. (2017); V’yugin & Trunov (2020) and Zamo et al. (2021) use an exponential weighting scheme based on combination across probabilities. A polynomial CRPS learning algorithm is applied in Thorey et al. (2018). Korotin et al. (2019, 2020) analyze properties of exponential weighting learning algorithms for forecasting distributions, including a CRPS based algorithm. Also, Zhang et al. (2020) show an application for probabilistic electricity demand forecasting where they optimize combination weights with respect to the CRPS. Lin et al. (2018) and Van der Meer et al. (2018) apply density-based aggregation methods with weights optimized with respect to the CRPS, the latter for the Gaussian case.

Additionally, plenty of forecast combination applications evaluate the predictive performance of distribution forecasts in terms of CRPS but do not optimize with respect to it. Some authors like Bai et al. (2020) and Zamo et al. (2021) also compute combination weights based on inverse CRPS-weighting in probabilistic oil price and wind speed forecasting. However, all applications mentioned above consider time-varying weights but ignore the potentially varying performance within the distribution.

It turns out that aggregation across quantiles is a useful tool for considering varying performance within our forecasters’ distribution when aiming for optimal CRPS. Therefore, instead of searching for optimal weights, we are looking for optimal weight functions. Furthermore, the weight functions shall be chosen pointwise so that the resulting distribution forecast has minimal CRPS. Thus combination weights assigned to a forecast can be larger in areas of the distribution where this forecast performs better.

This manuscript contributes to the probabilistic forecasting literature, as we

-

i)

Introduce a probabilistic forecast combination framework for pointwise CRPS learning based on aggregation across quantiles.

-

ii)

Prove that the proposed pointwise CRPS learning outperforms standard CRPS learning methods.

-

iii)

Study combination techniques based on B-Splines and P-Splines to model the combination weight functions.

-

iv)

Analyze a fully adaptive CRPS based Bernstein online aggregation (BOA) algorithm that satisfies theoretical guarantees on the convergence rates.

-

v)

Conduct simulation studies and show an application for probabilistic forecasting of European emission allowance (EUA) prices.

In the proceeding Section 2, we introduce the relevant basics on forecast combination, batch and online learning, and risk. We continue in Section 3 by studying the basics of the CRPS, introducing CRPS learning and its optimality properties, and discussing batch estimation techniques that utilize quantile regression. In Section 4, we briefly review the online learning concept of prediction with expert advice. Then we introduce the CRPS based BOA algorithm and provide a theorem for the optimality of convergence rates. Section 5 discusses extensions to the CRPS learning algorithm, e.g., by considering P-Splines, and includes implementation remarks. In Section 6, we present simulation studies that evaluate the properties of the proposed algorithm and compare the performance with other existing algorithms. Finally, we illustrate the procedure by applying it to probabilistic forecasting of European emission allowances prices in Section 11. Section 8 summarizes and concludes.

2 Relevant Aspects on Forecast Combination

2.1 Notation and Basics

We first require some notation. Let be the number of forecasters (often referred to as experts) that we want to aggregate. Denote the forecast of expert for the prediction target at time . This forecast could be a forecast for the mean or median of . could also be the distribution function of or its inverse. We assume that is predicted sequentially given all information available until .

We want to use weights at time for expert to define the linear forecast combination by

| (1) |

Many applications restrict to convex combinations, i.e. and . A common aggregation procedure is the naive combination method, also known as uniform aggregation or simple average where . More sophisticated aggregation or combination rules assign the weights based on the prediction target, but also the past performance or the model fit.

In general, all combination rules for can be distinguished in batch learners and online learners. Batch learning algorithms potentially evaluate all past information (e.g. , and ) for updating . However, online learners, only evaluate the most recent information (e.g. , , ) to compute . Obviously, the latter algorithms tend to be substantially faster in practice as less information has to be evaluated. Sometimes, both approaches can be converted into each other (Hoi et al., 2018). A standard batch learning example is ordinary least squares (OLS). In a rolling or expanding window context the corresponding online learning counterpart is recursive least squares (RLS) (Lee et al., 1981). Another popular online learning procedure is the Kalman filter, which corresponds to a ridge regression problem in batch learning (Diderrich, 1985).

For the prediction target, there might be proper scoring rules available (Gneiting & Raftery, 2007). A scoring or loss function takes as first input a forecast and as a second input the prediction target . The loss function is strictly proper, if it can identify the true prediction target. Popular loss functions used for point forecasting include the -loss which is strictly proper for mean predictions and the -loss which is strictly proper for median predictions (Gneiting, 2011a). For distribution functions the CRPS is a strictly proper scoring rule333The underlying distribution has to be in , so it requires a finite first moment. which we consider in Section 3.

2.2 Risk and its Optimality

According to Wintenberger (2017, p. 120), the risk is a suitable measure for predictive accuracy. The risk of our forecast combination is given by

| (2) |

where contains all information available at time . For simplicity we will denote the risk of expert by which can be computed with (2) by choosing the -th unit vector for in the definition (1).

A suitable combination rule may satisfy two properties in iid settings.444In the iid setting we assume that is iid where is some external input, such that depends on with corresponding filtration The first is the so called model selection property. This means that the risk of our forecast combination is asymptotically not worse than risk of the best individual expert .

Even stricter properties are called linear and convex aggregation properties. In the former, the performance of our forecast combination is compared to the best linear combination with aggregation weights and risk . In the convex aggregation property it is compared to the best convex combination with and risk .

The convex combination can never be worse than the best individual expert. Similarly, the linear combination will never be worse than the best convex one. It turns out that satisfying the convex and linear property comes at the cost of slower possible convergence. The optimal convergence rate in for the linear and convex properties is which is standard in asymptotic statistics while the selection property can yield the fast rate .

Based on Wintenberger (2017, p.121), an algorithm has optimal rates if

| (3) | ||||

| (4) | ||||

| (5) |

which characterises optimal dependence on time and the number of experts . Learning algorithms may satisfy (3), (4) and even (5) depending on the loss function and regularity conditions on and . A key contribution of this manuscript is a fully adaptive online learning algorithm that almost satisfies (3) and (4) in a CRPS learning setting.

3 Fundamentals on CRPS Learning

3.1 Basics on the CRPS

The CRPS is a scoring rule for evaluating probabilistic forecasts with respect to corresponding observations. The CRPS is defined as follows:

| (6) |

where is the distribution function and the observation. The CRPS is strictly proper and widely used in forecasting (Gneiting & Katzfuss, 2014; Jordan et al., 2019). Now, we want to use an important characterization of the CRPS. To utilize it, we require to be uniquely defined (e.g. has a pdf). It is based on the quantile loss (QL, also known as quantile score, pinball score, and asymmetric piecewise linear score), which is a strictly proper scoring rule for quantile forecasts (Gneiting, 2011a). The quantile loss is defined as

| (7) |

for a probability , quantile forecast at probability for the target value . The CRPS can be written as scaled integral on over (Gneiting & Ranjan, 2011, p. 414):

| (8) |

Representation (8) has a clear advantage. It allows us to move from distribution-based evaluation procedures to an integral of quantile forecasts, which is easier to handle (Gneiting, 2011a, b).

We can approximate the CRPS by

| (9) |

for an equidistant dense grid with and for all . Clearly, induces , , and the approximation converges to the CRPS.

One problem in practice is that explicit solutions for the CRPS are only available for limited parametric cases (Jordan et al., 2019). Additionally, except for mentioned limited parametric cases, reporting the exact full predictive distributions is impossible in many applications. It always requires some degree of approximation. A typical option for reporting is to report many quantiles on a dense grid of probabilities as in the CRPS approximation (9). A popular choice for such a grid contains all percentiles, i.e. , see e.g. Hong et al. (2016). The usage of this reporting method has the additional advantage, that next to methods that forecast other forecast methods that only predict the quantiles on a dense grid are applicable. The latter is particularly relevant for quantile regression methods.

3.2 CRPS learning and its optimality

Now, we discuss the learning theory with respect to the CRPS (8). As pointed out in the introduction, Thorey et al. (2018) and V’yugin & Trunov (2020) consider CRPS learning by aggregating across probabilities

| (10) |

for some combination weights and expert forecasts . As far as we know, there is no consideration of methods that aggregate across quantiles

| (11) |

for CRPS learning. Both aggregation rules (10) and (11) can be used to evaluate combination methods with respect to the optimality properties (3), (4) and (5).

As we evaluate our predictions by the CRPS a consistent choice for the loss is the CRPS itself. For the corresponding risk in (2), we receive with (8) and Fubini

| (12) | ||||

| (13) | ||||

| (14) |

This shows that the CRPS based risk can be represented as integral over the pointwise risk scaled by 2. Using (2) the latter can be computed as well by

| (15) |

where . The calculations show, that (11) is a useful baseline for pointwise CRPS learning. Hence, we introduce weight functions on at time for expert to define the forecast pointwise by

| (16) |

for all . Now, we are interested in finding such that has minimal CRPS. Clearly, for constant in (16) we are in the standard setting (11).

When analysing the optimality of CRPS learning algorithms, we can consider (2) on a pointwise basis for the quantile loss. Thus, we denote the risks by , , and for the forecast combination, the best expert and the best convex and linear combination based on the quantile loss and quantile forecasts for probability . For the evaluation it is useful to consider the corresponding scaled integrals as joint measures

| (17) | |||

| (18) |

for each which we scale by 2 due to (8). Further, we denote the cumulative risks of the forecast combination, the best expert and the best convex and linear combination based on the CRPS and distribution forecasts by , , and respectively. As pointwise optimization looks for optimalities on larger spaces we have the following Proposition:

Proposition 1.

It holds

| (19) | ||||

| (20) | ||||

| (21) |

The inequalities are strict if and only if the weights associated to are not constant for any , providing that the integrals exist.

Thus, pointwise procedures which have the risk always have the potential to outperform standard procedures with constant weights functions and risk . But, of course, no improvement can be expected if the optimal weight functions are constant. Otherwise, the inequalities of Proposition 1 will be strict.

If we would like to know in advance if it is worth considering the pointwise combination, then we require a pointwise evaluation with respect to the quantile loss on selected probabilities resp. parts of the distributions. For instance, suppose we want to combine two experts A and B. Then, suppose expert A performs significantly better in one part of the distribution and expert B in another part. In that case, it is a clear sign that a pointwise combination should be considered. Sometimes, no explicit formal evaluation of the experts is required because the model characteristics and assumptions imply different predictive accuracy in some distribution parts. For instance, this is the case if two experts A and B have different supports. If, for example, A is always positive and B might take negative values, then the predictive performance for lower quantiles must differ, and the pointwise combination is advantageous.

3.3 CRPS learning using quantile regression

We have seen that pointwise CRPS learning has the potential to outperform standard CRPS learning methods. Still, the optimal pointwise weights in (16) have to be estimated. Theoretically, a pointwise approach has to be applied to all such that the weight function can be specified. As we can never evaluate infinitely many values for we have to consider some finite-dimensional representation for the weight functions that are bounded on the unit interval . A suitable option is to represent the weight functions by a finite-dimensional representation using basis functions.

So let be bounded basis functions on with . A popular choice are B-Splines as local basis functions as they allow fast computation due to sparsity. The weight functions are then represented by

| (22) |

with parameter vector . Given historic forecasts we can estimate the -dimensional parameter matrix by minimizing the corresponding CRPS using (8)

| (23) | ||||

| (24) |

where the second line uses the shift invariance of the quantile loss and quantile regression notation , Koenker (2017).

Still, computing (24) requires the evaluation of all distribution forecasts. As discussed this is often not possible in practice. If we restrict the evaluation to the grid of probabilities problem (24) simplifies with (9) to

| (25) |

In general, quantile regression problems can be solved efficiently using linear programming solvers (Koenker, 2017). However, (25) is not a simple quantile regression problem, but a joint quantile regression (Sangnier et al., 2016; Chun et al., 2016). The parameters are active for multiple quantiles. Thus, adequate estimation of requires solving the optimization problem with respect to parameters which can be computationally costly if and are large.

However, if we choose the basis so that on for then (25) can be disentangled into separate quantile regression problems. This is

| (26) |

for where are the experts for the -quantile.

Quantile regression (26) will lead to linear optimality (21) on , as long as standard regularity conditions required for the quantile regression are satisfied (Koenker & Hallock, 2001). However, we might assume further restrictions to reduce the estimation risk, e.g., the solution is a convex combination. Taylor & Bunn (1998) discussed many related plausible restrictions for quantile combination concerning bias correction, positivity, affinity, among others.

3.4 Quantile crossing

All pointwise combination methods for the CRPS (as e.g. (26)) suffer from the potential problem of quantile crossing (Chernozhukov et al., 2010). This problem occurs if we have for some with .

One way to solve this problem is to impose the monotonicity constraint on the optimization objective (Bondell et al., 2010). Another suitable and universal approach is to rearrange (i.e., sort) the predictions so that no quantile crossing occurs. As shown in Chernozhukov et al. (2010), this procedure will never reduce the forecasting performance in terms of the quantile loss. Thus, we recommend utilizing it always in practice.

However, we remark that for the special case of constant weight functions , quantile crossing is no issue if no expert suffers from quantile crossing. So they satisfy for with , and thus it holds .

4 Online CRPS Learning

We have seen that quantile regression is a suitable approach for CRPS learning. Still, it is a batch learning approach that might be computationally costly. Therefore, we study online learning methods for CRPS learning. First, we cover relevant aspects of online learning methods usually referred to as prediction with expert advice, which is discussed in detail in Cesa-Bianchi & Lugosi (2006). This literature is driven a lot by game theory and optimization (Hoi et al., 2018). Most of the results hold for deterministic time series but hold similarly in a stochastic setting that we consider (Wintenberger, 2017). However, there are also connections to econometric and statistical literature that we will briefly mention as well.

4.1 Basics on prediction with expert advice

A key element in Cesa-Bianchi & Lugosi (2006) is the so called regret that measures the predictive accuracy of expert until time . It evaluates the past performance of the experts compared to the performance of the forecaster with respect to a target loss

| (27) |

with the instantaneous regret . In non-stochastic settings the regret satisfies , see (2).

Given the regret vector various aggregation rules can be defined. Popular aggregation rules include the polynomial weighted aggregation (PWA) Cesa-Bianchi & Lugosi (2006, p. 12) and the exponentially weighted aggregation (EWA, also called exponentially weighted average forecaster or Hedge algorithm) Cesa-Bianchi & Lugosi (2006, p. 14). The EWA utilizes the operator on the regret vector, scaled by a learning rate which may be regarded as a tuning parameter. Thus, the EWA is a combination rule defined for prior weight vector by

| (28) | ||||

| (29) |

where the second line corresponds to the vector notation of the line above with coordinatewise evaluation of involved multiplications and functions, and as Hadamard product. The EWA is also analyzed and applied in econometrics and statistics literature (Jore et al., 2010; Dalalyan et al., 2012; Opschoor et al., 2017). Due to the positivity of the exponential function will always be a convex combination.

As shown in Cesa-Bianchi & Lugosi (2006, p. 17), Kakade & Tewari (2008) and Gaillard et al. (2014), EWA (29) satisfies selection optimality (3) if the loss is exp-concave and is chosen correctly. This holds for example for the -loss and bounded on with .

To achieve convex aggregation optimality (4) for a learning algorithm, usually the gradient trick is applied Cesa-Bianchi & Lugosi (2006, p. 22). For the gradient trick, we define the linearized version of the loss as where is the subgradient of in its first coordinate evaluated at forecast combination 555This linearized version is sometimes also called pseudo-loss function Devaine et al. (2013).. Replacing in (29) by yields the gradient version of the EWA. This gradient based EWA (EWAG) algorithm (often referred as exponentiated gradient aggregation, EGA) with exp-concave losses and bounded satisfies both (3) and (4). Unfortunately, the quantile loss that is a key element in CRPS learning is not exp-concave. Hence, we study a more advanced algorithm.

4.2 Bernstein online aggregation (BOA)

Some more advanced algorithms are based on the EWA (29) and use a second-order refinement based on the variance estimate

| (30) |

of the instantaneous regret to receive better convergence and stability properties. For instance, Koolen & Van Erven (2015) and Wintenberger (2017) introduce such algorithms. In the former, this is called Squint; in the latter, Bernstein online aggregation (BOA). Both algorithms share very similar properties and coincide in specific situations (Gaillard & Wintenberger, 2018; Mhammedi et al., 2019). We focus on the BOA, as it was designed for stochastic settings that we consider. The BOA algorithm Wintenberger (2017, p. 121) is defined by

| (31) | ||||

| (32) |

with . As discussed above, the gradient trick can be applied by replacing with leading to the gradient-based BOA algorithm (BOAG).

The second-order refinement in the BOA(G) compared to the EWA(G) along with adequate tuning of allows weakening the exp-concavity assumption on the loss while retaining optimality with respect to (3) and (4). For example, Wintenberger (2017) proves an estimate for BOAG under convex losses that depends on . Adequately setting requires two ingredients.

First, it requires multiple learning rates such that they can be optimized individually for each expert . The second requirement is time-adaptive learning rates based on the so-called doubling trick (Cesa-Bianchi & Lugosi, 2006, p. 17). The time adaptivity of the learning rates depends on a range estimate of the regret and the variance estimate . The fully adaptive BOAG algorithm with multiple learning rates from Wintenberger (2017, p. 124) contains both ingredients:666Note that we consider a minor adjustment concerning some rounding issues in comparison to Wintenberger (2017) which does not change the algorithm’s convergence properties.

| (33a) | ||||

| (33b) | ||||

| (33c) | ||||

| (33d) | ||||

| (33e) | ||||

| (33f) | ||||

using also in Hadamard power notation, and as elementwise positive and negative part of , and elementwise evaluation of , and .

We remark that Gaillard & Wintenberger (2018, Theorem 2.1) prove that the fully adaptive BOAG satisfies selection optimality under mild regularity conditions: There exist a such that for it holds that

| (34) |

if the considered loss is convex -Lipschitz and weak exp-concave in its first coordinate (see Appendix, Proof of Theorem Appendix for a formal definition, including the role of ). It is clear that for the algorithm satisfies (3), despite for the term. This term is the standard price we have to pay for online calibration of the learning rates (Gaillard et al., 2014, p. 4). Furthermore, is satisfied by every Lipschitz convex loss, and any leads to fast convergence rates.

Furthermore, Wintenberger (2017) proves in Theorem 4.3 that the same BOA algorithm satisfies that there exist a such that for it holds that

| (35) |

if the loss is convex and the variance satisfies . Thus, the algorithm is almost optimal with respect to (4), only the term leads to a small lack of optimality.

4.3 CRPS online learning and its optimality

As mentioned in the previous section, a key ingredient to achieving better convergence properties is considering gradient-based algorithms. Therefore, we require the subgradient of the quantile loss. It is defined in (36).

| (36) |

Unfortunately, the quantile loss is not exp-concave. Thus an application of the EWAG does not guarantee optimal convergence properties. In contrast, the CRPS is exp-concave for random variables with bounded support (Korotin et al., 2019, p. 12). Thus, when considering learning algorithms with the structure (10) we receive that the corresponding EWA algorithms satisfy selection optimality (3) and for gradient based algorithms additionally convex optimality (4). However, those optimalities hold with respect to the risks and , and suffer from the lack of optimality (19) and (20).

For optimality of pointwise CRPS learning algorithms with respect to and we have to consider the BOAG algorithm (33) and analyze the quantile loss further concerning (34) and (35). By (36) it is clear that the quantile loss is convex. Thus, the fully adaptive BOAG satisfies (35) with respect to . However, if (34) holds is not obvious. As piecewise linear function is Lipschitz continuous. To check if weak exp-concavity holds for we have to investigate the conditional quantile risk . The convexity properties of depend on the conditional distribution :

Proposition 2.

Let be a univariate random variable with (Radon-Nikodym) -density with , then for the second subderivative of the quantile risk of it holds for all that

Additionally, if is a continuous Lebesgue-density with for some constant on its support then is is -strongly convex.

This quantile risk characterization is interesting as it provides a results on the convexity behavior independent of . Note that the requirements for -strong convexity are somewhat restrictive, e.g. must be bounded. But, we will use the proposition for , and may be bounded even though is unbounded.

Proposition 2 is valuable for us because strong convexity with implies weak exp-concavity (Gaillard & Wintenberger, 2018, p. 4). Hence, if it holds for , it implies almost optimality of the fully adaptive gradient-based BOA with multiple learning rates for the quantile loss . This is sufficient to deduce the selection and convexity optimality (3) and (4) of pointwise CRPS learning with respect to and , despite the term:

Theorem 1.

The assumption for the convex aggregation property is very mild; we only require the convergence of the variance terms . This is satisfied if the instantaneous regret sequence is stationary. In contrast, the requirements for the selection property are more restrictive as the assumption on the density of implies that it has to be bounded. We remark that the optimality of Theorem 1 holds even though quantile crossing might happen, see Subsection (3.4). Of course, Theorem 1 is more of a theoretical value, as we can never evaluate the quantile loss for infinitely many probabilities in practice. As mentioned, a common reporting situation considers a dense equidistant grid of probabilities . So quantile forecasts for are revealed every time for each expert and provide a suitable approximation of the CRPS, see (9).

4.4 Relationship to Bayesian model averaging

Bayesian model averaging (BMA) is a popular combination method in the econometric literature (Fragoso et al., 2018; Aastveit et al., 2019). Raftery et al. (2005) introduced how BMA can be used for forecasting. On the first view, there is no clear link between the learning theory explained in the previous subsection and BMA.

BMA under uninformative priors can be approximated by (29) while replacing the regret by the negative Bayesian information criterion (BIC) and choosing

| (37) |

with -dimensional BIC-vector (Hansen, 2008). Thus, exchanging the regret which measures the past predictive performance by a measure for model validility leads directly to BMA. This BMA approximation procedure has been used in different combination tasks (Cheng & Hansen, 2015; Maciejowska et al., 2020). The BIC values of the expert models could be computed in a batch setting, or in an online setting, e.g. using RLS or Kalman filtering.

However, as we minimize the CRPS or the quantile loss, we should adjust the BIC definition in (37) with respect to the considered loss. To do so, we consider a definition of the BIC based on the quantile loss as used by Lu & Su (2015) and Wang & Zou (2019). For each probability we define

| (38) |

where is the sample size (calibration window length) of the considered model, the (effective) degrees of freedom in the model and the residuals. When replacing by this turns to the standard least square BIC, which corresponds to the likelihood-based BIC under the normality assumption. We see that BMA requires some in-sample model to evaluate residuals, while this is not required for online learning algorithms like EWA or BOA. Still, the non-parametric definition (38) also allows for applications where the prediction task is performed by quantile regression (on the dense grid ). The key difference between the BMA approximation as used in (37) and EWA (29) is that EWA evaluates the quantile loss of the past forecasts at time whereas BMA evaluates the quantile loss of the most recent model.

From the applied point of view, nothing stops us from replacing the BIC in (37) by another information criterion. Alternatively, the factor can be replaced by another learning rate :

| (39) |

In this case, we may search for optimal values based on data-driven methods, e.g., on past performance. We recommend this procedure, as the BMA approximation (37) is derived for the likelihood-based BIC, whereas the utilization of the quantile loss-based BIC (38) might require a different scaling.

5 CRPS learning extensions and implementation remarks

This section briefly covers extensions to the considered CRPS learning algorithms and provides some implementation remarks. The extensions hold for online learning methods in the same way as for standard batch procedures based on quantile regression. First, we discuss a penalized smoothing procedure for the weights in CRPS learning algorithms. Next, we discuss forgetting in learning algorithms and extensions by the three simple shrinkage operators: fixed shares, soft-thresholding, and hard-thresholding. Note that the extensions are mainly motivated by intuition, application in similar situations in statistics and machine learning, and less by theoretical results. We partially back up the extension features by simulation and empirical studies afterward.

5.1 Penalized smoothing

Our weight functions are modeled as linear combinations of basis functions as explained in Subsection 3.3. The corresponding function space, resp. the basis function restrict the shape of possible weight function estimates. If we consider B-Splines as a basis, it is relatively straightforward to extend this standard smoothing method to penalized splines (P-Splines), at least in batch learning settings (Wang, 2011). The idea of P-Splines is to regularize the roughness of the fitted curve. This is particularly useful if a high number of basis functions is considered. For example, in the extreme case, the number of basis functions equals the size of the probability grid , as in situation (26).

Theoretically, we can extend (24) by a roughness penalty term:

| (40) | |||

A standard choice for would penalize the weight functions based on their second derivative, as applied in generalized additive models (GAM) (Wood, 2017). However, this increases the difficulty of the optimization problem even further and makes it impractical for applications.

Fortunately, there is a suitable penalized smoothing alternative that can be applied to in batch and online settings, based on (25). The idea is to smooth the weight functions after the estimation (i.e., updating) step. Therefore, we take another set of bounded basis functions on that we will use for penalized smoothing.

Then we can represent the weights as

with parameter vectors . We estimate by penalized - and -smoothing which minimizes for each given by

| (41) |

with differential operator of order . The differential order characterizes the type of smoothing penalty. The parameter chracterises the roughness penalty and mixes between the penalty in the first and second derivative. Typically, is considered along with cubic B-Splines to penalize for roughness (Wang, 2011; Wood, 2017). However, we prefer using here. As for , we are smoothing towards constant weights over for . and not towards a linear relationship between weights and probabilities as for . From our point of view, there is no clear argument in CRPS learning that supports shrinkage towards a linear relationship. In contrast, shrinkage towards a constant brings us directly to the non-pointwise CRPS-learning theory of constant weight functions. However, this does not mean that the penalized smoothing situation with gives the same result as the plain CRPS learning approach with . The first simulation study (see 6.1) gives more insights. Our simulation experiments show that the choice leads to suitable results in practice.

In applications, we are considering the function based optimization problem (41) only on the equidistant probability grid of size . If we consider a B-Spline basis functions , then an explicit solution based on ordinary least squares exists for (41). If the basis functions have additionally equidistant knots, this explicit solution has a simple ridge regression representation. The smoothed weights matrix is then given by

| (42) |

with matrix , penalty matrix and denotes the difference operator.

At first glance, it seems odd that we consider another basis for the penalized smoothing approach than we used for the original basis for the weight function representation. However, we do so mainly to emphasize that these can be regarded as two separate problems. Indeed, for applications we recommend to use the same basis . The latter shows excellent empirical performance and is easier to implement and communicate.

A penalized smoothing algorithm for CRPS learning using BOA (33) is presented in Algorithm 1 where and . The attentive reader will notice that the algorithm uses the BOA update step not for the weights vectors as in (33) but for the matrices. However, the algorithm has the same objective as in (25). Thus, may be regarded as weight functions for the expert predictions. The special case leads to constant weight functions with respect to the CRPS. For on (e.g. choosing linear B-Splines with equidistant knots of distance ) coincides with the pointwise application of BOA (33) with respect to on . In this case Algorithm 1 satiesfies Theorem 1 on as well.

Moreover, we want to remark that the initial weight matrix has to be transformed in the -space to receive an initial . Thus, we have to solve . In general is not invertible, but a simple application of the pseudoinverse yielding is completely sufficient for applications.

In practice, it is crucial to choose an adequate tuning parameter . Therefore, we recommend choosing based on the past performance of the forecaster as described in Subsection 5.4. Note that the application of smoothing in (42) may look suboptimal as we optimize with respect to the squared loss, not to the CRPS as in (40). However, we can still optimize with respect to the target CRPS.

5.2 Forgetting

Suppose we expect structural breaks in either the prediction target or the expert forecasts. In that case, it makes sense to reduce the weight of past information compared to recent information. Therefore, algorithms are sometimes extended by a forgetting factor (also called discounting factor). Exponential forgetting is usually preferred in online learning due to the recursive structure. The regret (27) can be written recursively as . The regret with forgetting factor discounts the regret in the definition above

| (43) |

where corresponds to no forgetting. In practice, optimal values are usually close to . We want to highlight that in online procedures forgetting should be applied to all recursive hidden state variables. In case of the fully adaptive BOA (33) these are the regret vector , the range vector and the variance vector . For the quantile regression setting exponential forgetting corresponds to the weighted regression problem

Even though exponential forgetting is popular in online learning, we cannot expect to preserve any asymptotic guarantees because the exponential function decays too fast Cesa-Bianchi & Lugosi (2006, p.32). However, polynomial discounts can be considered to keep convergence guarantees. However, exponential forgetting dominates the academic literature on online learning, see, e.g., Guo et al. (2018); Messner & Pinson (2019); Ziel (2021).

5.3 Shrinkage operators

In statistical learning theory, shrinkage operators help to reduce overfitting problems by shrinking a solution. The P-Spline smoothing can be interpreted as a shrinkage operator applied to the weight functions . However, simple shrinkage operators can also be applied to .

We want to briefly discuss three shrinkage operators that are sometimes used in online learning settings: the fixed share operator , the soft-thresholding operator , and the hard-thresholding operator . They are defined as

| (44) | ||||

| (45) | ||||

| (46) |

for some , and .

The fixed share operator shrinks towards the naive combination. The naive combination is preferable if there is no prior information on the expected performance of the experts available. For some shrinkage problems, even theoretical guarantees for improvements exist (Tu & Zhou, 2011; Cesa-Bianchi et al., 2012). In the online learning context it is used, e.g., in Cesa-Bianchi et al. (2012); Gonzalez et al. (2021).

The thresholding operators and are also sometimes considered in online learning contexts (Dalalyan et al., 2012; Gaillard & Wintenberger, 2017). Thresholding is a technique to receive sparse solutions. Both appear in several situations for specific linear model estimators. Most notably, soft-thresholding is the key operator in the coordinate descent algorithm for estimating the lasso (Friedman et al., 2007). Let us remark that the application of any of the threshold operators potentially violates affinity constraints (incl. the convexity constraint). In those situations, projections to the desired solution space should be applied.

5.4 Implementation Remarks

Algorithm 1 is implemented along with other algorithms (e.g. EWA(G) Gaillard & Goude (2015), ML-Poly(G) Gaillard et al. (2014)) in the freely available R-package profoc (Berrisch & Ziel, 2021). The functions are implemented using RcppArmadillo to limit computation time Eddelbuettel & Sanderson (2014), sparse matrix algebra is utilized since the basis matrices are usually sparse, and, in the case of P-Smoothing, the hat-matrix in (42) will be pre-computed as it stays constant during learning. The profoc package also supports batch learners for comparison purposes.

Next to the P-Spline smoothing parameters ( and ), the forget parameter () and shrinkage operator parameters (, , and ), profoc offers even more tuning parameters, e.g., for choosing non-equidistant grids for the B-Spline basis and for choosing basis functions of different degrees.

We recommend choosing the parameter combination based on the past cumulative performance of the forecaster. This approach is also implemented in profoc. It considers all possible parameter combinations at each step. Finally, it selects the combination weights corresponding to the parameter combination with the lowest cumulative loss up to .

6 Simulation Study

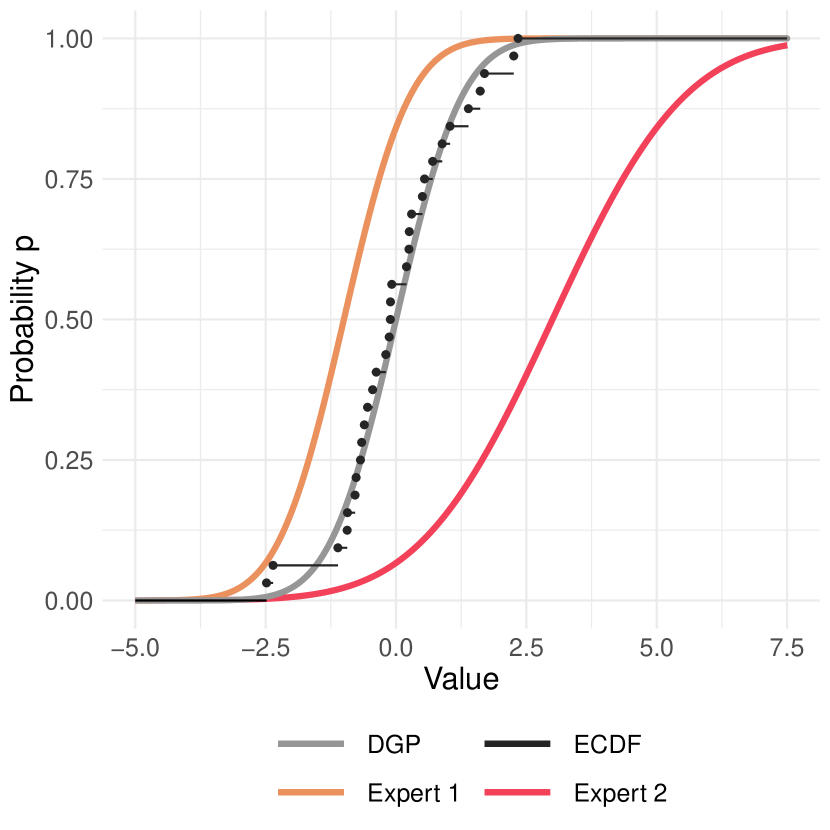

We present three simulation studies in this chapter. The first compares different smoothing methods and discusses the role of . The second compares the performance of different online learning algorithms while still using the simple data generating process (DGP) used for the first simulation. After that, a third study presents the application of an exponential forget (see (43)) in an environment of changing optimal weights. Each study presents the mean of 1000 repetitions. We always use experts as it allows us to compute the optimal weight functions analytically. We initialize the weights uniformly: and use percentiles as probability grid .

6.1 Smoothing Methods

The DGP for the first two studies is kept simple. We consider two experts with constant predictions over time. The true process is standard normal:

| (47) |

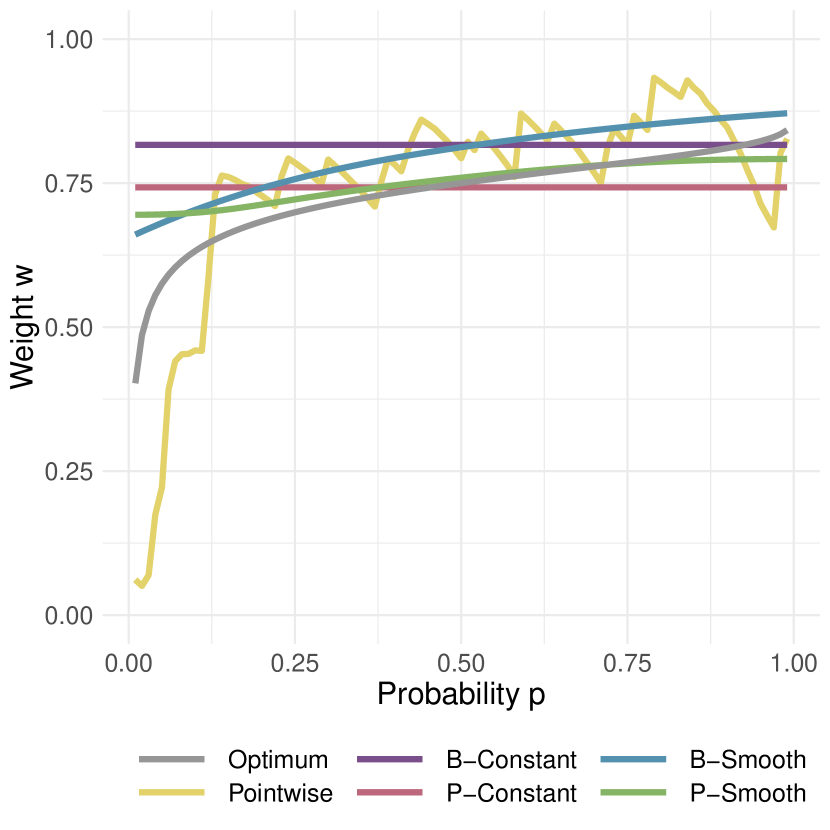

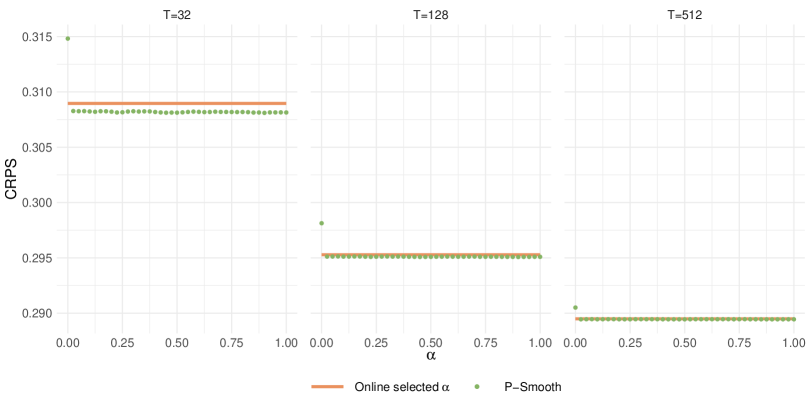

That is, optimal weight functions do not change over time. However, they are not constant over all . We use this DGP to compare the following specifications of the proposed BOAG algorithm 1. First, the basis is specified so that , which means that no smoothing is applied. We refer to this as the Pointwise solution. The first smooth solution B-Smooth is obtained by considering cubic B-spline basis’ with equidistant knots and knot distances of . The knot distance is selected in each step with respect to the past performance. Further, the standard CRPS-Learning solution B-Constant is considered by using the constant basis . Another specification P-Smooth uses P-Spline smoothing with . The smoothing parameter is chosen from an exponential grid based on the past performance. The last model which is considered approximates the limiting case of by using and is denoted by P-Constant. We choose the knot distance for B-Smooth and for P-Smooth based on the past performance of the forecaster as described in Subsection 5.4.

Figure 1 presents an example of the combination task. It shows the cumulative distribution function of the DGP and both experts as well as the empirical cumulative distribution function of a sample (left side). Further, it shows the resulting optimal weight function (gray) as well as combination weights calculated by various specifications of the proposed BOAG algorithm 1 (right side). Evaluating the performance using this figure is not possible since it only presents one single sample. However, we observe that the true combination weights vary over . That is, B-Constant and P-Constant will never convergence against the optimum.

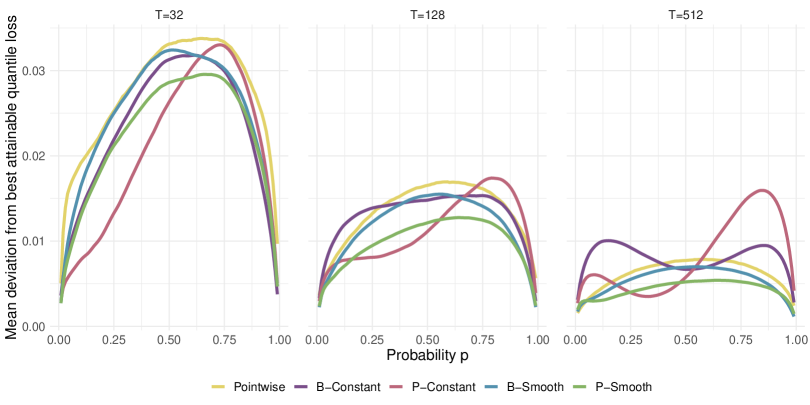

Figure 2 shows the results of this first study. It depicts the mean distance to the best possible loss with respect to . The results are presented for 32, 128, and 512 observations. The distance to the best possible loss decreases as the number of observations increases, as expected. The pointwise solution outperforms both constant solutions if a sufficient amount of observations is supplied. Furthermore, both smoothing methods improve over the pointwise solution regardless of the sample size. The P-Smooth specification yields the best results overall.

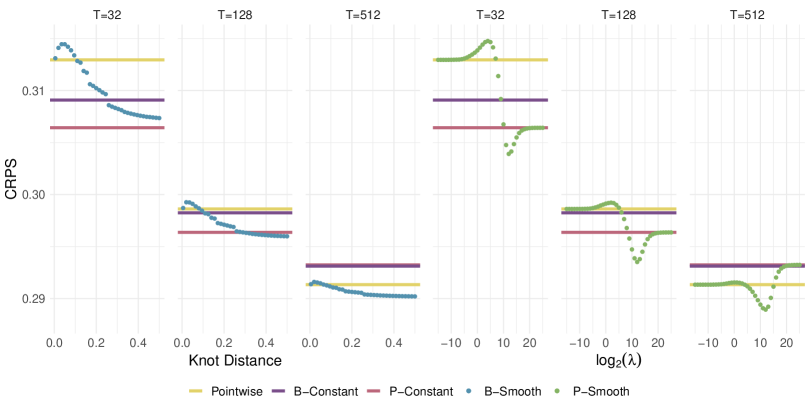

The results of the B-Smooth and P-Smooth specifications depend on the knot distance of the basis and respectively. Figure 3 illustrates this relation. It depicts the average CRPS for different values and knot distances. It is noteworthy that P-Constant clearly outperforms B-Constant for small while for large both specifications coincide with regards to their performance. Note that B-Constant applies a single learning rate at all quantiles while P-Constant assigns learning rates pointwise for each quantile. This shows that pointwise evaluation procedures potentially outperform constant ones even if both assign constant weights in the end.

The left hand side of Figure 3 shows that for B-Smooth a large knot distance (i.e, less knots) is preferable. This is caused by the DGP that produces smooth weight functions. Evaluating the P-Smooth solution with respect to shows that yields the lowest CRPS. Figure 3 also shows that P-Smooth yields better results than B-Smooth which was already apparent in Figure 2.

The P-Smooth results presented in Figures 2 and 3 were obtained using . Figure 4 shows that all yield similar results. Therefore, setting is reasonable as it ensures penalization with respect to slope and roughness.

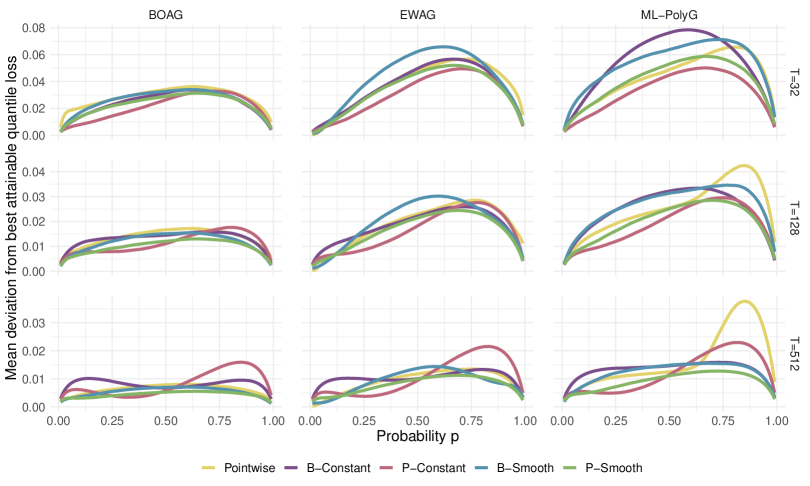

6.2 Popular learning algorithms compared

This second simulation study uses the same DGP (47) to compare the proposed BOAG (1) with other popular learning algorithms. In particular, we compare to EWAG777We consider an -grid of . (29) and the gradient version of the ML-Poly algorithm (ML-PolyG Gaillard et al. (2014)).

Figure 5 presents the results of this study. The columns show the algorithms, while the rows depict different sample sizes. Analogous to the first study, we show the distance to the best possible loss. This distance decreases with increasing sample size for all three algorithms. However, the BOAG algorithms show lower distances for all sample sizes compared to EWAG and ML-PolyG. Additionally, we see that the constant solutions do not converge to zero since the true are not constant over .

To summarize, BOAG shows the fastest convergence indeed. Moreover, the results also support the application of the P-Smooth specification.

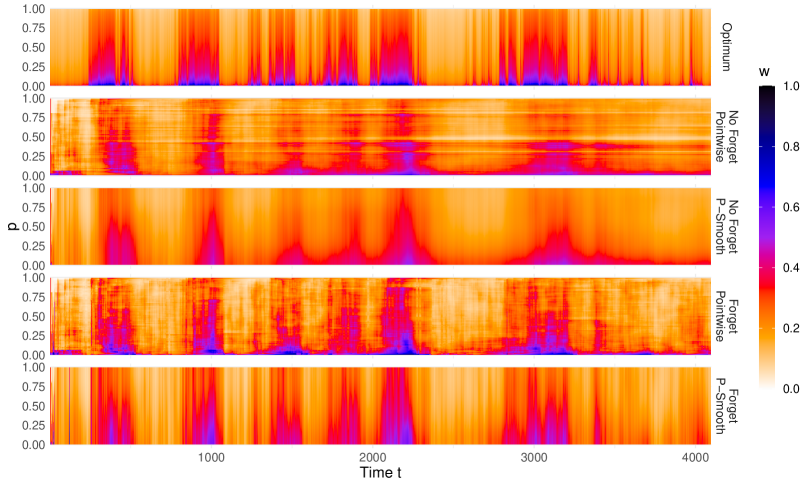

6.3 Changing weights

Now consider the following DGP with changing optimal weights. This DGP is set up as follows:

| (48a) | ||||

| (48b) | ||||

We use this DGP to illustrate the importance of the forget operator (43). Taking the entire history of regrets into account is suboptimal in settings with changing optimal weights. This is illustrated by Figure 6. It shows the optimal weights of expert two as well as weights obtained from BOAG with- and without an exponential forget for Pointwise and P-Smooth specifications. The models with forget are calculated by considering a -grid of forget rates and selecting in each step with respect to the past performance. The colors of Figure 6 represents the weights assigned to expert two over time (x-axis) and for every (y-axis).

Figure 6 shows that the solutions without forget fail at precisely adjusting their weights in the long-term. Using a forget results in a more rapid weight adjustment which is favorable here. However, this Figure only presents a single example.

Table 1 presents the average CRPS and respective standard deviations from 1000 simulation runs. The lowest CRPS was obtained by considering the forget grid as described above and using the P-Smooth specification.

| No Forget | Forget | ||

|---|---|---|---|

| Pointwise | P-Smooth | Pointwise | P-Smooth |

7 Application

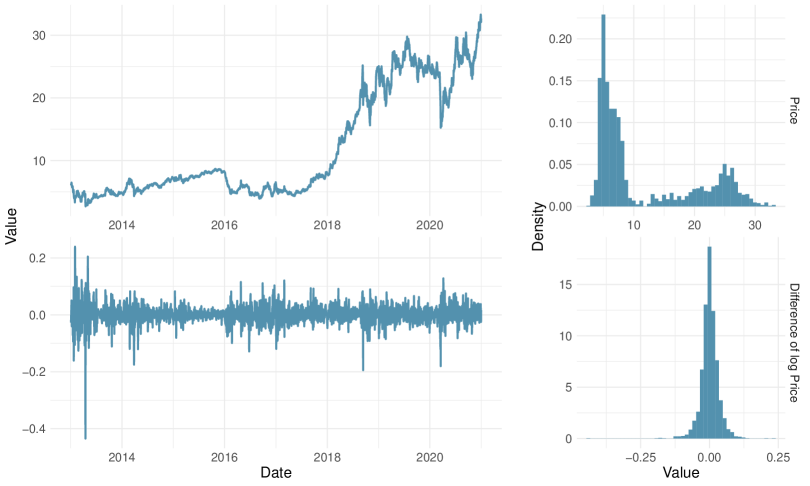

Now we apply the proposed CRPS learning algorithm to a forecasting task in environmental finance. More precisely, we present a study for forecasting the prices of the European emission allowances (EUA) as traded in the European Union Emissions Trading Scheme (EU ETS). As highlighted by Segnon et al. (2017), and Dutta (2018) ARIMA-GARCH-type models dominate the econometric finance literature, see e.g. Liu et al. (2021). However, machine learning methods, mainly considering artificial neural networks, are utilized as well (Atsalakis, 2016; Hao et al., 2020; García & Jaramillo-Morán, 2020). One of the reasons is likely the rather uncertain effect of external impact factors (Koop & Tole, 2013).

For this illustrative application, we ignore external regressors as in Benz & Trück (2009) and Dutta (2018). We consider daily EUA prices of the month-ahead future covering the full Phase III period from January 2013 until December 2020. The price data with all observations and the corresponding differences of log prices is illustrated in Figure 7.

For the probabilistic CRPS learning study that we evaluate on we consider a selection of five plausible experts. These are an exponential smoothing model, a quantile regression approach, and three ARIMA-GARCH-type models. The models are selected to cover a relatively broad range of features, e.g., conditionally homoskedastic and heteroskedastic, light tails and heavy tails, stationary and instationary, parametric and non-parametric. We consider the following models for the log-prices :

-

i)

Simple exponential smoothing with additive errors (ETS-ANN):

with and . -

ii)

Quantile regression (QuantReg):

For each we assume . -

iii)

ARIMA(1,0,1)-GARCH(1,1) with Gaussian errors (ARMA-GARCH):

with , and . -

iv)

ARIMA(0,1,0)-I-EGARCH(1,1) with Gaussian errors (I-EGARCH):

with , and . -

v)

ARIMA(0,1,0)-GARCH(1,1) with student-t errors (I-GARCHt):

with , and .

We estimate the parameters of model ii) using quantile regression for each separately. All the other models are estimated using maximum likelihood. We conduct a rolling window forecasting study with a window length of 250, which covers about a year. This design gives us out-of-sample observations.

Concerning the combination methods, we consider uniform weighting (, Naive) the online learning methods EWAG, BOAG, ML-PolyG and BMA (39). Additionally, we consider two quantile regression batch learners based on (25) with a rolling window size of 30. One of the quantile regressions without any constraints QRlin and the other with convexity constraint QRconv.

We consider the Pointwise, B-Constant, P-Constant, B-Smooth and P-Smooth specifications (see Section 6.1). However, the general B-Smooth specifications (see (25)) using quantile regression were excluded from the experiment because of their very high computational cost. The standard CRPS-learning specification B-Constant was used in combination with ML-PolyG in Thorey et al. (2018). Further, Zamo et al. (2021) considered EWA and EWAG using B-Constant.

For the P-smoothing methods we consider and the -grid where the latter value approximates the situation. For the B-spline smoothing methods we consider 19 cubic B-spline basis on equidistant knot distances with distances where is a linear grid from to of size 19. We augment the 19 basis functions by the constant function. For EWAG and BMA we specify an -grid of learning rates additionally. We choose the tuning parameters online based on the past performance of the forecaster as described in Subsection 5.4.

Table 2 presents the results. It shows the CRPS difference of the considered experts and aggregation methods with respect to the Naive aggregation procedure and aggregated across time. Additionally, the table shows the p-value of the Diebold-Mariano test (DM-test), which tests if the considered forecaster provides better forecasts than Naive.

| ETS-ANN | QuantReg | ARMA-GARCH | I-EGARCH | I-GARCHt |

| 2.101 (>.999) | 1.358 (>.999) | 0.520 (.993) | 0.511 (.999) | -0.037 (.406) |

| BOAG | EWAG | ML-PolyG | BMA | QRlin | QRconv | |

|---|---|---|---|---|---|---|

| Pointwise | -0.170 (.055) | -0.089 (.175) | -0.141 (.112) | 0.032 (.771) | 3.482 (>.999) | -0.019 (.309) |

| B-Constant | -0.118 (.146) | -0.049 (.305) | -0.090 (.218) | 0.038 (.834) | 4.002 (>.999) | 0.539 (.996) |

| P-Constant | -0.138 (.020) | -0.070 (.137) | -0.133 (.026) | 0.039 (.851) | 5.275 (>.999) | 0.009 (.683) |

| B-Smooth | -0.173 (.062) | -0.065 (.276) | -0.141 (.118) | -0.042 (.386) | - | - |

| P-Smooth | -0.182 (.039) | -0.107 (.121) | -0.160 (.065) | 0.040 (.804) | 3.495 (>.999) | -0.012 (.369) |

We observe that all experts except I-GARCHt perform clearly worse than the Naive. When looking at the aggregation methods, we see that the online learning methods BOAG, EWAG and ML-PolyG tend to outperform Naive. We receive the best results using BOAG. Moreover, P-Smooth provides better results than Pointwise for the three online learners. In contrast, B-Smooth fails to do so. Still, we see that the lowest p-value is obtained for BOAG using P-Constant. The reason is that pointwise and smoothing procedures lead to more volatile predictions. Furthermore, we observe that the quantile regression methods are hardly worth considering, especially regarding the high computational effort. Therefore we exclude them from the proceeding graphs and focus on online methods.

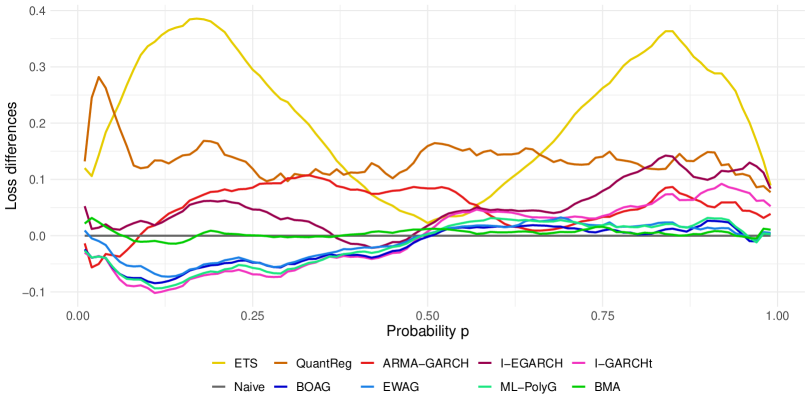

Figures 8 and 9 present the main results when evaluating forecasting performance with respect to Naive across probabilities and time. From the quantile loss differences in Figure 8 we see that the experts’ performance varies clearly across the probability, as mentioned a key sign that pointwise CRPS learning should be considered. The ETS-ANN performs fine in the center and poorly otherwise. The I-GARCHt performs very well in the lower part of the distribution but in the upper part not clearly better than other experts. Our benchmark, the Naive combination, performs better than all experts in the upper part of the distribution and worse than I-GARCHt in the lower part. The BMA performs similarly. The other learning methods BOAG, EWAG and ML-PolyG exhibit similar pattern, in the lower part of the distribution they perform similarly to best single expert I-GARCHt, and in the upper part similarly to Naive.

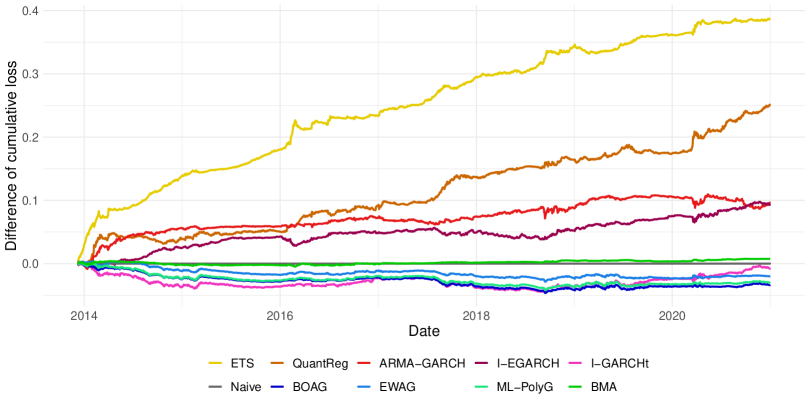

From the cumulated CRPS differences in Figure 9 we see that the overall results also hold over time. The likely most interesting observation is that in the first year, I-GARCHt performs better than the combination methods. Thereafter BOAG, EWAG and ML-PolyG catch up and eventually overtake the I-GARCHt. The reason may be that the learners require some time to stabilize. We do not consider 3- or 4-parametric distributions to limit the computation effort.

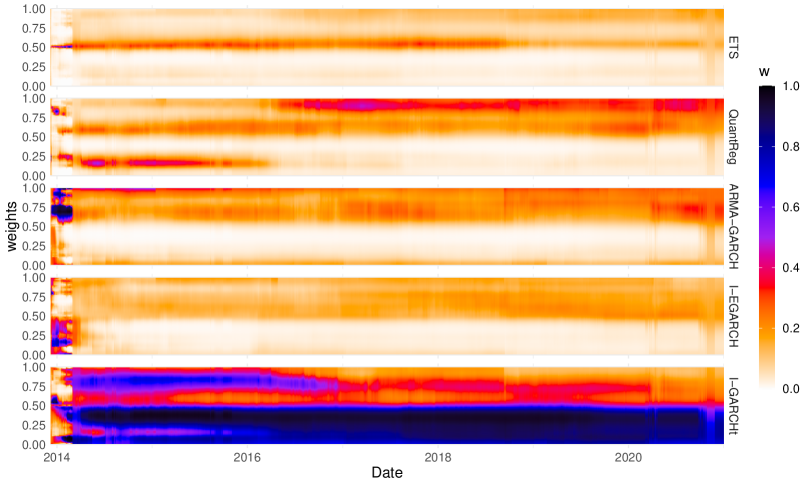

Figure (10) presents the weight functions in the last time step for the five specifications of the BOAG, which is the best online learning method. We see that for Pointwise the weights vary substantially over . Also, it is noteworthy that the weights of both constant solutions differ to a moderate extent. Furthermore, we observe that P-Smooth leads to more flexible (i.e., locally smoothed) weights than the B-Smooth, which applies a global smoothing.

Figure 11 relates to the right tile of Figure (10) as it illustrates the evolution of the weight functions over time for BOAG with the P-Smooth specification. Indeed, we observe that the weights change rapidly in the initial period. Overall, we see that the performance pattern of (8) translates to the weight functions. The I-GARCHt dominated the weight in the lower part of the distribution. Only in the extreme tails, the ARMA-GARCH contributes all the time. For the first two years, the quantile regression QuantReg also contributes to the weight function in the lower part of the distribution. However, the weights in the upper part of the distribution are much closer to the Naive combination.

8 Summary and Conclusion

This paper presented a framework for probabilistic forecast combination that aims to minimize the CRPS.

The key idea is to aggregate probabilistic expert predictions with combination weights that vary in time and parts of the distribution. The time-adaptivity is relevant to account for the changing performance of the experts. The variation of the weights in the distribution is important to consider that, e.g., some experts perform better in the center of the distribution while others perform better in the distributions’ tails. We prove that we can expect improvements in performance in those situations by considering pointwise optimization of the weight functions (see Proposition 1).

We study the resulting CRPS learning approach for batch and online learning methods. The combination weight functions are modeled by a linear combination of basis functions, where we suggest B-Splines. We show that quantile regression can be used for CRPS learning but can be computationally costly. In contrast, we show that online aggregation is a suitable solution in practice. We prove that under mild regularization constraints, the fully adaptive BOA can yield almost888There is a small lack of optimality due to an term which results from the adaptive learning rates. optimal convergence rates with respect to the selection problem and the convex aggregation problem (see Theorem 1). In simple words, the proposed BOA for CRPS learning guarantees fast convergence to the best expert and standard convergence to the best convex combination of all experts. To achieve optimal convergence rates, we require some convexity assumptions on the quantile risk of the predictive target distribution. Proposition 2 helps to characterize those convexity properties.

Furthermore, we discuss relationships to BMA and extensions to the proposed B-Spline-based CRPS learning method. Most notably, we discuss P-Spline smoothing and propose a corresponding fully adaptive BOA procedure for CRPS-learning. This online learning algorithm yields preferable probabilistic forecasting performance in simulation studies and an application to probabilistic forecasting of European emission allowance prices.

Multiple slightly different variations of the BOA exist in the literature (Wintenberger, 2017; Brégère & Huard, 2021). The differences concern the cumulative regret, the weights, and the fact that is forced to be an integer exponentiation with base 2 in Wintenberger (2017) while the integer condition is relaxed in Brégère & Huard (2021). The profoc R-Package Berrisch & Ziel (2021) implements relevant BOA versions, various related online learning procedures (e.g. EWA, ML-Poly) and quantile regression-based methods for CRPS-learning. Additionally, B-spline and P-spline smoothing can be applied to all algorithms.

Further research could go in various directions. We restrict ourselves to equidistant quantile grids, as it is a popular reporting option for probabilistic forecasts. However, it only approximates the CRPS. Precise CRPS learning methods for popular parametric distributions could be studied in more depth. It seems plausible that faster algorithms can be achieved, as we would not have to evaluate a dense grid of quantiles.

Moreover, we considered pointwise aggregation across quantiles (see (16)) for CRPS learning. Alternatively, we could study pointwise aggregation across probabilities by considering

| (49) |

This is more popular in the density combination literature (Aastveit et al., 2014; Kapetanios et al., 2015) but, to our knowledge, not studied for estimating optimal weight functions. In this CRPS learning the weighting scheme (49) could utilize the standard definition of the CRPS (6). However, the unbounded support of the weight functions in (49) creates a more complicated CRPS learning problem. The main reason is that suitable consideration of basis functions should depend on the distribution of the prediction target, esp. appropriate range, location, and scale parameters. However, it might be worth investigating it further. Another interesting path of research may be the consideration of pointwise combination methods for distributional forecasts with respect to other scoring rules, e.g., the log-score.

Finally, further investigations could go into the direction of online aggregation methods that utilize the expert predictions and simultaneously the in-sample (i.e., training) performance of the experts (e.g., in BMA). Such a procedure is studied in Adjakossa et al. (2020) for the -loss.

References

- Aastveit et al. (2014) Aastveit, K. A., Gerdrup, K. R., Jore, A. S., & Thorsrud, L. A. (2014). Nowcasting GDP in real time: A density combination approach. Journal of Business & Economic Statistics, 32, 48–68.

- Aastveit et al. (2019) Aastveit, K. A., Mitchell, J., Ravazzolo, F., & van Dijk, H. K. (2019). The Evolution of Forecast Density Combinations in Economics. In Oxford Research Encyclopedia of Economics and Finance.

- Adjakossa et al. (2020) Adjakossa, E., Goude, Y., & Wintenberger, O. (2020). Kalman recursions aggregated online. arXiv preprint arXiv:2002.12173, .

- Atiya (2020) Atiya, A. F. (2020). Why does forecast combination work so well? International Journal of Forecasting, 36, 197–200.

- Atsalakis (2016) Atsalakis, G. S. (2016). Using computational intelligence to forecast carbon prices. Applied Soft Computing, 43, 107–116.

- Bai et al. (2020) Bai, L., Li, X., Wei, Y., & Wei, G. (2020). Does crude oil futures price really help to predict spot oil price? New evidence from density forecasting. International Journal of Finance & Economics, .

- Benz & Trück (2009) Benz, E., & Trück, S. (2009). Modeling the price dynamics of CO2 emission allowances. Energy Economics, 31, 4–15.

- Berrisch & Ziel (2021) Berrisch, J., & Ziel, F. (2021). profoc: Probabilistic Forecast Combination Using CRPS Learning. https://profoc.berrisch.biz/, https://cran.r-project.org/web/packages/profoc, https://github.com/BerriJ/profoc.

- Bondell et al. (2010) Bondell, H. D., Reich, B. J., & Wang, H. (2010). Noncrossing quantile regression curve estimation. Biometrika, 97, 825–838.

- Brégère & Huard (2021) Brégère, M., & Huard, M. (2021). Online hierarchical forecasting for power consumption data. International Journal of Forecasting, .

- Busetti (2017) Busetti, F. (2017). Quantile aggregation of density forecasts. Oxford Bulletin of Economics and Statistics, 79, 495–512.

- Cesa-Bianchi et al. (2012) Cesa-Bianchi, N., Gaillard, P., Lugosi, G., & Stoltz, G. (2012). Mirror descent meets fixed share (and feels no regret). Advances in Neural Information Processing Systems, 25, 980–988.

- Cesa-Bianchi & Lugosi (2006) Cesa-Bianchi, N., & Lugosi, G. (2006). Prediction, learning, and games. Cambridge university press.

- Cheng & Hansen (2015) Cheng, X., & Hansen, B. E. (2015). Forecasting with factor-augmented regression: A frequentist model averaging approach. Journal of Econometrics, 186, 280–293.

- Chernozhukov et al. (2010) Chernozhukov, V., Fernández-Val, I., & Galichon, A. (2010). Quantile and probability curves without crossing. Econometrica, 78, 1093–1125.

- Chun et al. (2016) Chun, H., Lee, M. H., Fleet, J. C., & Oh, J. H. (2016). Graphical models via joint quantile regression with component selection. Journal of Multivariate Analysis, 152, 162–171.

- Dalalyan et al. (2012) Dalalyan, A. S., Salmon, J. et al. (2012). Sharp oracle inequalities for aggregation of affine estimators. The Annals of Statistics, 40, 2327–2355.

- Devaine et al. (2013) Devaine, M., Gaillard, P., Goude, Y., & Stoltz, G. (2013). Forecasting electricity consumption by aggregating specialized experts. Machine Learning, 90, 231–260.

- Diderrich (1985) Diderrich, G. T. (1985). The Kalman Filter from the Perspective of Goldberger-Theil Estimators. The American Statistician, 39, 193–198.

- Dutta (2018) Dutta, A. (2018). Modeling and forecasting the volatility of carbon emission market: The role of outliers, time-varying jumps and oil price risk. Journal of Cleaner Production, 172, 2773–2781.

- Eddelbuettel & Sanderson (2014) Eddelbuettel, D., & Sanderson, C. (2014). RcppArmadillo: Accelerating R with high-performance C++ linear algebra. Computational Statistics & Data Analysis, 71, 1054–1063.

- Fragoso et al. (2018) Fragoso, T. M., Bertoli, W., & Louzada, F. (2018). Bayesian model averaging: A systematic review and conceptual classification. International Statistical Review, 86, 1–28.

- Friedman et al. (2007) Friedman, J., Hastie, T., Höfling, H., Tibshirani, R. et al. (2007). Pathwise coordinate optimization. Annals of applied statistics, 1, 302–332.

- Gaillard & Goude (2015) Gaillard, P., & Goude, Y. (2015). Forecasting electricity consumption by aggregating experts; how to design a good set of experts. In Modeling and stochastic learning for forecasting in high dimensions (pp. 95–115). Springer.

- Gaillard et al. (2014) Gaillard, P., Stoltz, G., & Van Erven, T. (2014). A second-order bound with excess losses. In Conference on Learning Theory (pp. 176–196). PMLR.

- Gaillard & Wintenberger (2017) Gaillard, P., & Wintenberger, O. (2017). Sparse accelerated exponential weights. In Artificial Intelligence and Statistics (pp. 75–82). PMLR.

- Gaillard & Wintenberger (2018) Gaillard, P., & Wintenberger, O. (2018). Efficient online algorithms for fast-rate regret bounds under sparsity. In Proceedings of the 32nd International Conference on Neural Information Processing Systems (pp. 7026–7036).

- García & Jaramillo-Morán (2020) García, A., & Jaramillo-Morán, M. A. (2020). Short-term European Union Allowance price forecasting with artificial neural networks. Entrepreneurship and Sustainability Issues, 8, 261.

- Gneiting (2011a) Gneiting, T. (2011a). Making and evaluating point forecasts. Journal of the American Statistical Association, 106, 746–762.

- Gneiting (2011b) Gneiting, T. (2011b). Quantiles as optimal point forecasts. International Journal of forecasting, 27, 197–207.

- Gneiting & Katzfuss (2014) Gneiting, T., & Katzfuss, M. (2014). Probabilistic forecasting. Annual Review of Statistics and Its Application, 1, 125–151.

- Gneiting & Raftery (2007) Gneiting, T., & Raftery, A. E. (2007). Strictly proper scoring rules, prediction, and estimation. Journal of the American statistical Association, 102, 359–378.

- Gneiting & Ranjan (2011) Gneiting, T., & Ranjan, R. (2011). Comparing density forecasts using threshold-and quantile-weighted scoring rules. Journal of Business & Economic Statistics, 29, 411–422.

- Gneiting & Ranjan (2013) Gneiting, T., & Ranjan, R. (2013). Combining predictive distributions. Electronic Journal of Statistics, 7, 1747–1782.

- Gonzalez et al. (2021) Gonzalez, P. L. M., Brayshaw, D. J., & Ziel, F. (2021). A new approach to extended-range multimodel forecasting: Sequential learning algorithms. Quarterly Journal of the Royal Meteorological Society, .

- Guo et al. (2018) Guo, W., Xu, T., Tang, K., Yu, J., & Chen, S. (2018). Online sequential extreme learning machine with generalized regularization and adaptive forgetting factor for time-varying system prediction. Mathematical Problems in Engineering, 2018.

- Hansen (2008) Hansen, B. E. (2008). Least-squares forecast averaging. Journal of Econometrics, 146, 342–350.

- Hao et al. (2020) Hao, Y., Tian, C., & Wu, C. (2020). Modelling of carbon price in two real carbon trading markets. Journal of Cleaner Production, 244, 118556.

- Hoi et al. (2018) Hoi, S. C., Sahoo, D., Lu, J., & Zhao, P. (2018). Online learning: A comprehensive survey. arXiv preprint arXiv:1802.02871, .

- Hong et al. (2016) Hong, T., Pinson, P., Fan, S., Zareipour, H., Troccoli, A., & Hyndman, R. J. (2016). Probabilistic energy forecasting: Global Energy Forecasting Competition 2014 and beyond. International Journal of Forecasting, 32, 896–913.

- Hsiao & Wan (2014) Hsiao, C., & Wan, S. K. (2014). Is there an optimal forecast combination? Journal of Econometrics, 178, 294–309.

- Jordan et al. (2019) Jordan, A., Krüger, F., & Lerch, S. (2019). Evaluating probabilistic forecasts with scoringRules. Journal of Statistical Software, 90.

- Jore et al. (2010) Jore, A. S., Mitchell, J., & Vahey, S. P. (2010). Combining forecast densities from VARs with uncertain instabilities. Journal of Applied Econometrics, 25, 621–634.

- Kakade & Tewari (2008) Kakade, S. M., & Tewari, A. (2008). On the Generalization Ability of Online Strongly Convex Programming Algorithms. In NIPS (pp. 801–808).

- Kapetanios et al. (2015) Kapetanios, G., Mitchell, J., Price, S., & Fawcett, N. (2015). Generalised density forecast combinations. Journal of Econometrics, 188, 150–165.

- Koenker (2017) Koenker, R. (2017). Computational methods for quantile regression. In Handbook of Quantile Regression (pp. 55–67). Chapman and Hall/CRC.

- Koenker & Hallock (2001) Koenker, R., & Hallock, K. F. (2001). Quantile regression. Journal of economic perspectives, 15, 143–156.

- Koolen & Van Erven (2015) Koolen, W. M., & Van Erven, T. (2015). Second-order quantile methods for experts and combinatorial games. In Conference on Learning Theory (pp. 1155–1175).

- Koop & Tole (2013) Koop, G., & Tole, L. (2013). Forecasting the European carbon market. Journal of the Royal Statistical Society: Series A (Statistics in Society), 176, 723–741.

- Korotin et al. (2019) Korotin, A., V’yugin, V., & Burnaev, E. (2019). Integral Mixabilty: a Tool for Efficient Online Aggregation of Functional and Probabilistic Forecasts. arXiv preprint arXiv:1912.07048, .

- Korotin et al. (2020) Korotin, A., V’yugin, V., & Burnaev, E. (2020). Mixing past predictions. In Conformal and Probabilistic Prediction and Applications (pp. 171–188). PMLR.

- Lee et al. (1981) Lee, D., Morf, M., & Friedlander, B. (1981). Recursive least squares ladder estimation algorithms. IEEE Transactions on Acoustics, Speech, and Signal Processing, 29, 627–641.

- Lichtendahl Jr et al. (2013) Lichtendahl Jr, K. C., Grushka-Cockayne, Y., & Winkler, R. L. (2013). Is it better to average probabilities or quantiles? Management Science, 59, 1594–1611.

- Lin et al. (2018) Lin, Y., Yang, M., Wan, C., Wang, J., & Song, Y. (2018). A multi-model combination approach for probabilistic wind power forecasting. IEEE Transactions on Sustainable Energy, 10, 226–237.

- Liu et al. (2021) Liu, J., Zhang, Z., Yan, L., & Wen, F. (2021). Forecasting the volatility of EUA futures with economic policy uncertainty using the GARCH-MIDAS model. Financial Innovation, 7, 1–19.

- Lu & Su (2015) Lu, X., & Su, L. (2015). Jackknife model averaging for quantile regressions. Journal of Econometrics, 188, 40–58.

- Maciejowska et al. (2020) Maciejowska, K., Uniejewski, B., & Serafin, T. (2020). PCA Forecast Averaging—Predicting Day-Ahead and Intraday Electricity Prices. Energies, 13, 3530.

- Van der Meer et al. (2018) Van der Meer, D. W., Munkhammar, J., & Widén, J. (2018). Probabilistic forecasting of solar power, electricity consumption and net load: Investigating the effect of seasons, aggregation and penetration on prediction intervals. Solar Energy, 171, 397–413.

- Messner & Pinson (2019) Messner, J. W., & Pinson, P. (2019). Online adaptive lasso estimation in vector autoregressive models for high dimensional wind power forecasting. International Journal of Forecasting, 35, 1485–1498.

- Mhammedi et al. (2019) Mhammedi, Z., Koolen, W. M., & Van Erven, T. (2019). Lipschitz adaptivity with multiple learning rates in online learning. In Conference on Learning Theory (pp. 2490–2511). PMLR.

- Opschoor et al. (2017) Opschoor, A., Van Dijk, D., & van der Wel, M. (2017). Combining density forecasts using focused scoring rules. Journal of Applied Econometrics, 32, 1298–1313.

- Petropoulos et al. (2020) Petropoulos, F., Apiletti, D., Assimakopoulos, V., Babai, M. Z., Barrow, D. K., Bergmeir, C., Bessa, R. J., Boylan, J. E., Browell, J., Carnevale, C. et al. (2020). Forecasting: theory and practice. arXiv preprint arXiv:2012.03854, .

- Raftery et al. (2005) Raftery, A. E., Gneiting, T., Balabdaoui, F., & Polakowski, M. (2005). Using Bayesian Model Averaging to Calibrate Forecast Ensembles. Monthly Weather Review, 133, 1155 – 1174.

- Sangnier et al. (2016) Sangnier, M., Fercoq, O., & d’Alché Buc, F. (2016). Joint quantile regression in vector-valued RKHSs. Advances in Neural Information Processing Systems, 29, 3693–3701.

- Segnon et al. (2017) Segnon, M., Lux, T., & Gupta, R. (2017). Modeling and forecasting the volatility of carbon dioxide emission allowance prices: A review and comparison of modern volatility models. Renewable and Sustainable Energy Reviews, 69, 692–704.

- Taylor & Bunn (1998) Taylor, J. W., & Bunn, D. W. (1998). Combining forecast quantiles using quantile regression: Investigating the derived weights, estimator bias and imposing constraints. Journal of Applied Statistics, 25, 193–206.

- Thorey et al. (2018) Thorey, J., Chaussin, C., & Mallet, V. (2018). Ensemble forecast of photovoltaic power with online CRPS learning. International Journal of Forecasting, 34, 762–773.

- Thorey et al. (2017) Thorey, J., Mallet, V., & Baudin, P. (2017). Online learning with the Continuous Ranked Probability Score for ensemble forecasting. Quarterly Journal of the Royal Meteorological Society, 143, 521–529.

- Tu & Zhou (2011) Tu, J., & Zhou, G. (2011). Markowitz meets Talmud: A combination of sophisticated and naive diversification strategies. Journal of Financial Economics, 99, 204–215.

- V’yugin & Trunov (2020) V’yugin, V., & Trunov, V. (2020). Online Aggregation of Probabilistic Forecasts Based on the Continuous Ranked probability score. Journal of Communications Technology and Electronics, 65, 662–676.

- Wang & Zou (2019) Wang, M., & Zou, G. (2019). Jackknife Model Averaging for Composite Quantile Regression. arXiv preprint arXiv:1910.12209, .

- Wang (2011) Wang, Y. (2011). Smoothing splines: methods and applications. CRC Press.

- Wintenberger (2017) Wintenberger, O. (2017). Optimal learning with Bernstein online aggregation. Machine Learning, 106, 119–141.

- Wood (2017) Wood, S. N. (2017). Generalized additive models: an introduction with R. CRC press.

- Zamo et al. (2021) Zamo, M., Bel, L., & Mestre, O. (2021). Sequential aggregation of probabilistic forecasts—Application to wind speed ensemble forecasts. Journal of the Royal Statistical Society: Series C (Applied Statistics), 70, 202–225.

- Zhang et al. (2020) Zhang, S., Wang, Y., Zhang, Y., Wang, D., & Zhang, N. (2020). Load probability density forecasting by transforming and combining quantile forecasts. Applied Energy, 277, 115600.

- Ziel (2021) Ziel, F. (2021). Smoothed Bernstein Online Aggregation for Day-Ahead Electricity Demand Forecasting. arXiv preprint arXiv:2107.06268, .

Appendix

Proof of Proposition 1.

We show (20). Let the pointwise optimal solution with respect to and the optimal solution with respect to CRPS for . With Fubini and (8) it holds

The inequality equality holds strictly if and only if the optimality of is strict on any interval due to the continuity of and the fact that for . This holds, if and only if the weights are not constant for at least one in on the corresponding interval as is one-sided continuous.

Proof of Proposition 2.

We observe that with as convolution operator. Then we receive by exchangability of subgradients in covolutions for the second subgradient that . Further, we have that and with as dirac function in . Thus, the result follows by . The latter statement of the proposition concerning follows as a twice-differentiable real valued function is -strongly convex if and only if . ∎

Proof of Theorem 1.

As we want to apply Theorem 2.1 of Gaillard & Wintenberger (2018) we remark that a loss is convex -Lipschitz and weak exp-concave if

-

(A1)

for some it holds for all and that

-

(A2)

for some , it holds for all and that

As is convex Theorem 4.3 of Wintenberger (2017) implies (35) for all . Similarly, if is bounded and has a pdf Proposition 1 implies that quantile risk at is -strongly convex and satisfies (A2). Furthermore, from (36) we see that is convex Lipschitz with optimal Lipschitz constant . Thus, by Theorem 2.1 of Gaillard & Wintenberger (2018) we receive (34) with . Now, define , the CRPS-approximation and note that . and thus CRPS satisfies (A2) with as does not depend on . Further, with some calculus we observe that has the optimal Lipschitz constant . Hence, for it holds . Thus, CRPS is convex Lipschitz and satiesfies (A1) and the Theorem is implied by Theorem 2.1 of Gaillard & Wintenberger (2018). ∎