Risk-sensitive safety analysis using

Conditional Value-at-Risk*

Abstract

This paper develops a safety analysis method for stochastic systems that is sensitive to the possibility and severity of rare harmful outcomes. We define risk-sensitive safe sets as sub-level sets of the solution to a non-standard optimal control problem, where a random maximum cost is assessed via Conditional Value-at-Risk (CVaR). The objective function represents the maximum extent of constraint violation of the state trajectory, averaged over a given percentage of worst cases. This problem is well-motivated but difficult to solve tractably because the temporal decomposition for CVaR is history-dependent. Our primary theoretical contribution is to derive computationally tractable under-approximations to risk-sensitive safe sets. Our method provides a novel, theoretically guaranteed, parameter-dependent upper bound to the CVaR of a maximum cost without the need to augment the state space. For a fixed parameter value, the solution to only one Markov decision process problem is required to obtain the under-approximations for any family of risk-sensitivity levels. In addition, we propose a second definition for risk-sensitive safe sets and provide a tractable method for their estimation without using a parameter-dependent upper bound. The second definition is expressed in terms of a new coherent risk functional, which is inspired by CVaR. We demonstrate our primary theoretical contribution via numerical examples.

Conditional Value-at-Risk, Stochastic optimal control, Safety analysis, Markov decision processes.

1 Introduction

Control-theoretic formal verification methods for dynamical systems typically fall in the robust domain [20, 21, 22, 23, 24] or in the stochastic domain [25, 26, 27, 28]. Robust methods for formal verification assume that uncertain disturbances lack probabilistic descriptions, live in bounded sets, and exhibit adversarial behavior. These assumptions are appropriate if probabilistic information about disturbances is not available, and if the conservative policy or safety specification that results from a pessimistic world view is useful in practice. However, when one considers formal verification as a design tool for safety-critical systems in the digital world today, it is reasonable to assume that simulation tools or sensor data are available to estimate probabilistic descriptions for disturbances. Moreover, it is reasonable to consider the following world view: disturbances need not be adversarial, but rare harmful outcomes are still possible.

Control-theoretic stochastic formal verification methods do assume that disturbances are probabilistic and can be non-adversarial [25, 26] or adversarial [27, 28] in nature. These methods compute the probability of safety or performance by using expected indicator cost functions. The expectation, however, is not designed to quantify the features in the tails of a distribution, and the probability of a harmful outcome need not indicate its severity. Thus, formal verification methods at the intersection of the robust and stochastic domains are emerging. A method for distributionally robust safety analysis has been proposed [29], and methods that use risk measures to assess harmful tail costs, e.g., [30] and our prior work [38], have been introduced.111A risk measure (risk functional) is a map from a set of random variables to the extended real line. Exponential utility, Value-at-Risk, CVaR, and Mean-Deviation are examples [37]. The terms risk measure and risk functional are interchangeable.

While the notion of risk-sensitive formal verification is recent, it is related to the notion of risk-sensitive Markov decision processes (MDPs), which dates back to the early 1970s. In 1972, Howard and Matheson studied risk-sensitive MDPs on finite state spaces, where the cost is evaluated in terms of exponential utility [1]. This idea was transferred to linear control systems by Jacobson in 1973 [2] and was further developed in later decades. For example, see the seminal works by Whittle [4, 35] and di Masi and Stettner [3]. The exponential utility of a non-negative random cost assesses the risk of in terms of the moments of and is parametrized by a non-zero scalar . Under appropriate conditions, tends to as and if is sufficiently small [4]. The risk-averse setting corresponds to . However, if is too negative, the controller can suffer from a phenomenon called “neurotic breakdown” in the linear-quadratic-Gaussian setting [4].

Hence, the notion of risk-sensitive MDPs has been generalized beyond exponential utility. Kreps used the expectation of a utility function as a risk-sensitive performance criterion for MDPs [7]. Ruszczyński defined a risk-sensitive performance criterion for MDPs in terms of a composition of risk measures [47]. State-space augmentation has been used to optimize the cumulative cost of a MDP, where the cost is assessed via CVaR [16] or a certainty equivalent risk measure [17]. The former problem is called a CVaR-MDP. Convex analytic methods have been used to solve MDPs with expected utility or CVaR criteria via state-space augmentation and infinite-dimensional linear programming [34]. A temporal decomposition for CVaR [40, 41] has been used to propose a dynamic programming (DP) algorithm on an augmented state space to solve a CVaR-MDP problem approximately [31]. Analysis at the intersection of mean field games, linear systems, and risk measures with connections to CVaR is provided by [32].

Ruszczyński’s approach [47] and MDPs that assess cumulative costs via expectation or exponential utility are time-consistent problems. That is, these problems satisfy Bellman’s Principle of Optimality on the original state space.222Different meanings for time consistency have been proposed, e.g., see [47, 5, 6]. We refer to the meaning for time consistency from [6]. However, a CVaR-MDP is time-inconsistent. Several solution concepts for time-inconsistent problems have been proposed. For example, a game-theoretic solution concept is studied in [8], which considers the problem as a game against one’s future self. Another popular approach is to focus on pre-commitment strategies that cannot be revised at later stages. Optimal or nearly optimal pre-commitment strategies can be obtained using the structure of CVaR; see [16, 34, 39], for example. Although an optimal pre-commitment strategy is globally optimal only at the initial stage, maintaining suitable empirical performance at later stages is possible, particularly when the time horizon is not too long [18]. In mean-CVaR asset allocation problems, optimal pre-commitment strategies are shown to be effective even with long time horizons [19].

A line of research that falls between risk-sensitive MDPs and standard risk-neutral MDPs is risk-constrained MDPs [33, 42, 30, 34]. Here, the goal is to minimize an expected cumulative cost subject to a risk constraint that limits the extent of a cost. Refs. [33, 42, 30], for example, express this constraint in terms of CVaR.

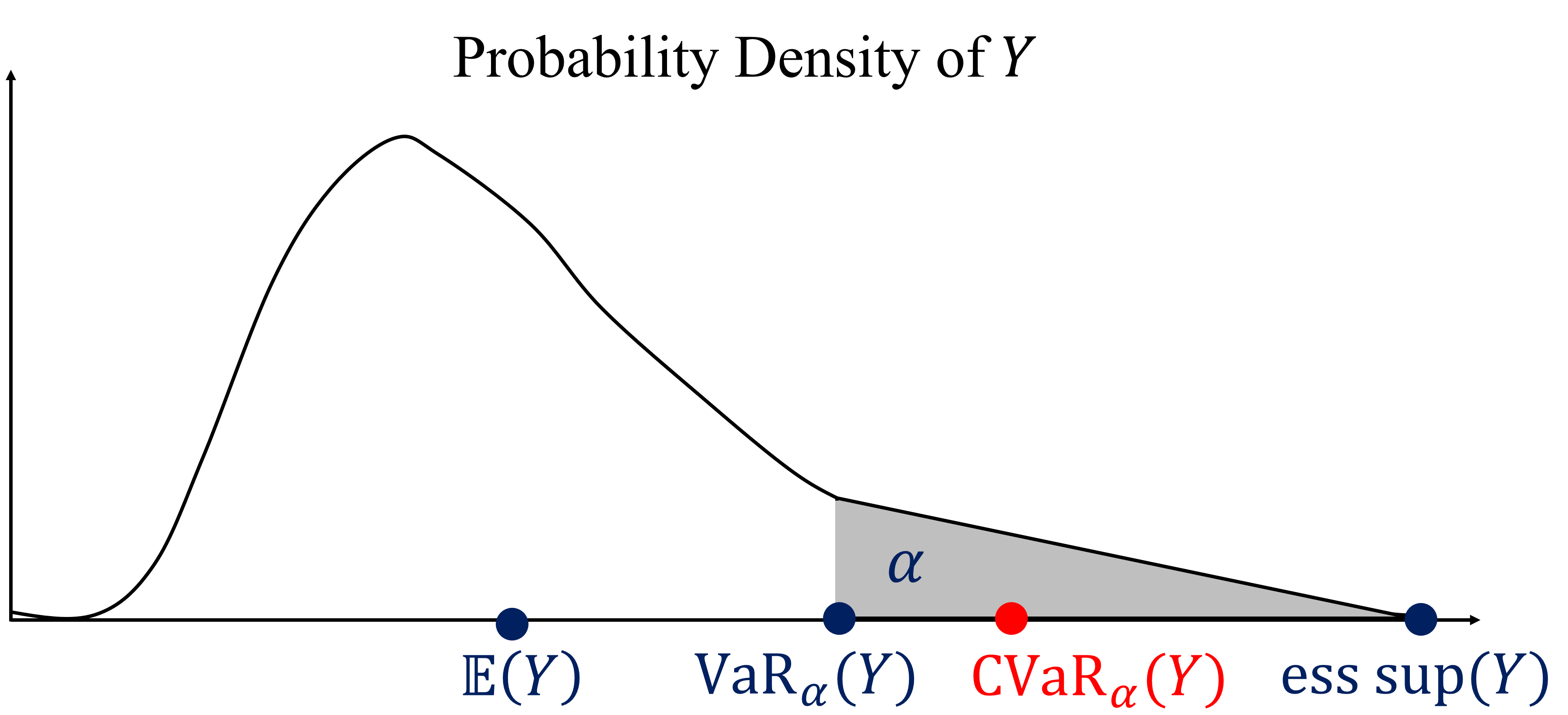

The additional effort required to solve time-inconsistent problems, including CVaR-MDPs, may be justified for safety-critical applications. A strong theoretical basis for using CVaR to assess harmful tail costs has been in development since the early 2000s, e.g., see [36] and the references therein. Informally, CVaR represents the expected cost in the % worst cases, where (Fig. 1). CVaR quantifies the more harmful tail of a distribution, and managing this tail is paramount in safety-critical applications.

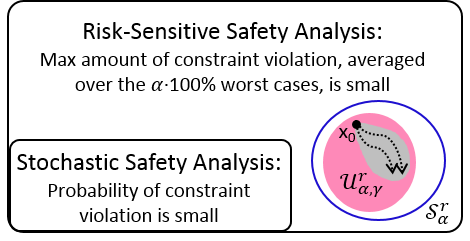

This paper proposes a method to assess how well a stochastic system can remain within a desired operating region with respect to a range of worst-case perspectives. We call this method risk-sensitive safety analysis (Fig. 2). Its foundation is a non-standard optimal control problem that evaluates a random maximum cost via CVaR. The objective function represents the maximum extent of constraint violation of the state trajectory, averaged over the % worst cases, where is a risk-sensitivity level. This problem is difficult to solve tractably because the temporal decomposition for CVaR is history-dependent [40, 41]. We define risk-sensitive safe sets as sub-level sets of the solution to this non-standard problem. These sets are powerful tools for safety analysis. Indeed, they assess system behavior on a spectrum of worst cases, while being sensitive to the possibility and severity of rare harmful outcomes.

Our primary theoretical contribution is to derive computationally tractable under-approximations to risk-sensitive safe sets. We derive these under-approximations by proving the following: for any control policy and any initial state, the CVaR of a maximum cost is upper bounded by a scaled logarithm of an expected cumulative cost, where the stage cost has a specific analytical form. For this proof, we use various properties of CVaR and the log-sum-exponential approximation to the maximum. The latter approximation depends on a parameter, . For a fixed , the solution to one MDP problem is required to obtain the under-approximations for any family of risk-sensitivity levels. We provide practical insights on how to choose such a parameter in the experimental section.

Our method provides a novel, theoretically guaranteed upper bound to the CVaR of a maximum cost for the purpose of safety analysis without the need to augment the state space. (Augmenting the state space may be less tractable in some settings, e.g., when the range of the augmented state is large.) In contrast, existing methods aim to compute the CVaR of a cumulative cost via state-space augmentation. By taking different approaches to augment the state space, Refs. [16] and [34] minimize the CVaR of a cumulative cost, and Ref. [31] minimizes the CVaR of a cumulative cost approximately. These related works are focused on controller synthesis but are not focused on safety analysis.

Our secondary theoretical contribution is to propose a second definition for risk-sensitive safe sets and provide a tractable method for their estimation without using a parameter-dependent upper bound. The second definition is expressed in terms of a new risk functional, which is inspired by CVaR and has certain desirable properties. In particular, we prove that this risk functional admits an upper bound that can be computed via DP (on the original state space and without an additional parameter that requires tuning). This result forges a new path to estimate risk-sensitive safety criteria with desirable computational attributes.

Organization. We present notation and background on CVaR in Sec. 2. Our primary and secondary theoretical contributions are provided in Sec. 3 and Sec. 4, respectively. We develop computational examples of a temperature system and a stormwater system to demonstrate our primary theoretical contribution in Sec. 5. Sec. 6 presents conclusions and directions for future work.

2 Background on Conditional Value-at-Risk

We use the following notation. If is a metrizable space, is the Borel sigma algebra on . If is a probability space and , is the associated space, and is the associated norm. Typically, we use upper-case letters to denote random variables or sets, whereas lower-case letters denote deterministic quantities, including parameters. Exceptions are the length of a time horizon is expressed in terms of and denotes expectation.

Next, we present a standard definition for CVaR and facts about CVaR that are relevant to this work.333Additional names for CVaR include Average Value-at-Risk, Expected Shortfall, and Expected Tail Loss. We present the definition for CVaR that is used by Shapiro and colleagues, e.g., [37, 9, 10]. Let be a random variable with finite first moment, representing a cost, defined on a probability space . That is, let , where smaller realizations of are preferred. The Conditional Value-at-Risk of at the risk-sensitivity level is defined by

| (1) |

where is the expectation with respect to (w.r.t.) . We note the following consequences of the Definition (1):

-

1.

.

-

2.

If , then and for .

Definition (1) is not the most intuitive, so we present an alternative definition that explains the names Conditional Value-at-Risk and Average Value-at-Risk. The alternative definition is written in terms of the Value-at-Risk of at level , which is given by

| (2) |

where is the probability of the event . In other words, is the generalized inverse cumulative distribution function of at level , or equivalently, the left-side -quantile of the distribution of [10]. The CVaR of at level is equivalent to an average of the Value-at-Risk [37, Thm. 6.2]:

| (3) |

The above equation explains the commonly used name Average Value-at-Risk. Now, to explain the name Conditional Value-at-Risk, suppose that the cumulative distribution function is continuous at . Continue to assume that and . Then, is a conditional expectation that is expressed in terms of the Value-at-Risk [37, Thm. 6.2]:

| (4) |

Equation (4) means that represents the expected value of in the worst cases.

CVaR is a commonly cited example of a coherent risk functional [37, 10]. Coherent risk functionals are a class of risk functionals, first proposed by Artzner et al. [11], that satisfy four properties, which are particularly meaningful in applications where sensitivity to risk is critical. We present these properties in the context of CVaR at level , where below.

-

1.

Monotonicity. If for almost every (a.e.) , then . That is, a random cost that is larger than another almost everywhere incurs a larger risk.

-

2.

Subadditivity. . If is the (random) stage cost of a control system at time , then the risk of the cumulative cost over a finite horizon is at most the sum of the risks of the stage costs.

-

3.

Translation equivariance. If , then .

-

4.

Positive homogeneity. If , then .

The last two properties ensure that shifting or scaling a random variable provides an analogous transformation to the risk of the random variable. In particular, the expectation operator satisfies the four properties above and thus is a coherent risk functional. We use some of these properties in our proofs. We also use the fact that a real-valued coherent risk functional can be represented in terms of a supremum over a family of expectations.444The family of expectations has specific properties that are out of the scope of this paper. The representation was developed over several years, e.g., see [11, 13, 14, 10]. This representation takes the following form for CVaR at level [10]: for any ,

| (5a) | |||

| where the definitions of and follow. if and only if is a probability measure that is absolutely continuous with respect to , i.e., of the form , where and . is a set of densities defined by | |||

| (5b) | |||

3 CVaR-Based Risk-Sensitive Safety Analysis

We use the CVaR functional to pose a safety analysis problem. We consider a stochastic system evolving on a discrete, finite-time horizon and start with the standard set-up for this setting. Let and be Borel spaces, representing the set of states and the set of controls of the system, respectively. Define the sample space , where is a finite sequence of states and controls that may be realized on a time horizon of length and is given. The random state and the random control are projections. That is, for any of the form above, define and , where the coordinates of have casual dependencies, to be described. The initial state is fixed arbitrarily at . The system’s evolution is affected by -valued random disturbances with a common distribution , where is a Borel space. is independent of the states, controls, and for any . The distribution of conditioned on is defined as follows: for any ,

| (6) |

where is a Borel-measurable map that models the system dynamics. We use the typical class of random, history-dependent policies . Each takes the form , where each is a Borel-measurable stochastic kernel on given .

The above set-up is standard in discrete-time stochastic control. One reason is that, given and , the set-up allows the construction of a unique probability measure that characterizes the system’s evolution, provided that the system is initialized at and uses the policy (Ionescu-Tulcea Theorem). The measure permits the prediction of the system’s performance over time under uncertainty. Random costs incurred by the system are defined on , a probability space parametrized by and . The notation is the expectation operator with respect to .

3.1 On Evaluating a Random Cost via CVaR

We use to define a random cost for the system and to evaluate this cost via CVaR. Suppose that there is a constraint set , where the state trajectory of the system should remain inside. It may be impossible for the system to remain inside always due to random disturbances in the environment. Let be a bounded Borel-measurable function that represents a notion of distance between a state realization and the boundary of . Specifically, is the extent of constraint violation of , a realization of the random state . More specifically, if is outside of and far from the boundary of , then has a large positive value. However, if is inside of , then may be

-

1.

zero, if one does not favor certain trajectories inside of , or

-

2.

a more negative value when is more deeply inside of , if one favors trajectories that remain deeply inside of .

Using , we define a random -valued cost that quantifies the maximum extent of constraint violation of the state trajectory: for any ,

| (7) |

In other words, quantifies how well the random state trajectory satisfies the safety criterion to remain inside of . Hence, quantifies the safety of the random state trajectory, which is defined with respect to the constraint set via the function . A deterministic (and continuous-time) version of (7) is used in Hamilton-Jacobi reachability analysis, a robust safety analysis method for (non-stochastic) uncertain systems, which has been established over the past 15 years; e.g., see [21, 43, 24], and the references therein. A standard choice for is a clipped signed distance function with respect to [43, p. 8]. In our numerical example of a thermostatically controlled load, we use to quantify how far a state realization can be inside or outside of ∘C (Sec. 5.1).

It holds that and . The function composed with is an element of because is bounded and Borel measurable and is Borel measurable. Thus, is a point-wise maximum of finitely many functions in . Therefore, inherits the measurability properties of these functions and is essentially bounded. Since is a probability space, is a subset of , and it follows that as well.

3.2 Risk-Sensitive Safe Sets

Definition 1 (Risk-Sensitive Safe Sets)

Let and be given. The -risk-sensitive safe set for a given policy is defined by

| (9) |

The -risk-sensitive safe set is defined by

| (10) |

We denote the infimum in (10) by . Risk-sensitive safe sets are well-motivated. These sets represent the sets of initial states from which the maximum extent of constraint violation of the state trajectory, averaged over the % worst cases, can be made sufficiently small. The maximum extent of constraint violation of the state trajectory is the real-valued random variable . We allow to be negative so that decision-makers can encode preferences for trajectories remaining deeper inside of over trajectories near the boundary of , if desired. In our numerical example of a thermostatically controlled load, we allow to take on both negative and non-negative values to express a preference for trajectories that remain closer to 20.5 (Sec. 5.1). In our numerical example of a stormwater system, however, we choose a non-negative to utilize all capacity in the water storage tanks without penalty (Sec. 5.2).

Using CVaR to define risk-sensitive safe sets is well-justified from a decision-theoretic point of view because CVaR is a coherent risk measure. That is, CVaR satisfies the axioms of monotonicity, subadditivity, positive homogeneity, and translation equivariance. Sec. 2 provides intuitive interpretations for these axioms. Besides having an axiomatic justification, CVaR has the useful interpretation of quantifying the upper tail of a distribution. Indeed, CVaR provides a quantitative characterization of risk aversion by representing the expected cost in the % worst cases, where is selected by the decision-maker. This interpretation is exact if continuous random variables in are evaluated.

Risk-sensitive safe sets generalize probabilistic safe sets [25] by quantifying the maximal extent of constraint violation at a given risk-sensitivity level rather than the probability of constraint violation. Risk-sensitive safe sets quantify how much constraint violation occurs on average in the worst cases, whereas probabilistic safe sets [25] quantify whether or not constraint violation occurs with some probability. Indeed, let be a maximum tolerable probability of constraint violation. Choose , , and , where if and if . Then, the -risk-sensitive safe set is

| (11) |

which is the maximal probabilistic safe set at the -safety level [25] for the system of Sec. 3. (Ref. [25] considers discrete-time stochastic hybrid systems that evolve under Markov policies.)

Risk-sensitive safe sets indicate higher degrees of safety as decreases and decreases. We state this fact formally next.

Lemma 1

Suppose that and . Then, . If , then .

Proof 3.1.

Let and . Since and , . Since and is bounded, there exists a such that for almost every . Since CVaR is monotonic and , . Take the infimum over to obtain , which holds for any . Now, suppose . Then, . Since , we have , which shows that . The proof for the last statement is similar.

The risk-sensitive safe set specifies that the of the worst constraint violation of the state trajectory must be below a given threshold. In contrast, the safe set in [30] specifies that for each the of the constraint violation of the state at time must be below a given threshold. Hence, assesses the risk of the entire trajectory, whereas the safe set in [30] is concerned with the risk of each state in the trajectory separately. A specification that assesses the risk of the entire trajectory may be preferable in certain applications because this approach treats the trajectory as a unified entity representing the behavior of a control system.

3.3 Under-Approximation Method

Risk-sensitive safe sets are well-motivated but difficult to compute due to the presence of the CVaR and the maximum. Before presenting our approach to estimate risk-sensitive safe sets, we describe related methods in further detail.

Several methods in the literature apply state-space augmentation techniques to estimate the risk of a random cost incurred by a MDP.555An approach that does not require state-space augmentation is to evaluate a cumulative cost via a composition of risk functionals [47]. We take inspiration from this idea in Sec. 4. Bäuerle and Ott use dynamic programming (DP) to minimize the CVaR of a sum of stage costs by defining an augmented state space [16]. The range of the second state is , where is the stage cost at time [16, Remark 5.1]. This state-space augmentation approach has been extended to optimize certainty equivalent risk functionals for MDPs [17]. A certainty equivalent approximates the sum of the expectation and a function of the variance under particular conditions [17], and more generally, characterizes risk aversion in terms of functions of moments. However, CVaR provides a quantitative characterization of risk aversion by penalizing a random cost in a given fraction of the worst cases.

Chow et al. proposed a DP algorithm to minimize approximately the CVaR of a cumulative cost via state-space augmentation, where the additional state ranges from 0 to 1 [31]. This approach is expected to be more tractable than the approach in [16]; compare the ranges of the additional states. However, it is not known if the algorithm in [31] provides an upper bound or a lower bound to the solution to a CVaR-MDP problem. The algorithm in [31] is based on a CVaR Decomposition Theorem [40, Thm. 6] [41, Thm. 21, Lemma 22], which requires knowledge of the history of a stochastic process. How to remove the history dependence and apply the Decomposition Theorem to derive the algorithm in [31] is still an open research question.

The algorithms invented by [16, 31] aim to minimize the CVaR of a cumulative cost subject to the dynamics of a MDP. The algorithm proposed by [40] aims to minimize the CVaR of a more general cost (not necessarily a sum) but is history-dependent, which limits its computational tractability. The proof of the DP algorithm in [40] requires an exchange between an essential supremum and an expectation, whose validity in multi-stage settings for MDPs with Borel state and control spaces is not known.

Here, we propose a method to provide tractable, theoretically guaranteed under-approximations to risk-sensitive safe sets, which we define via CVaR. We focus on CVaR due to its quantitative characterization of risk aversion and since we aim to assess the degree of safety of a control system in terms of rarer, higher-consequence outcomes. In contrast, a certainty equivalent assesses risk in terms of functions of variance and other moments. In particular, variance does not distinguish between rarer, higher-consequence outcomes in the upper tail and rarer, lower-consequence outcomes in the lower tail. Unlike the methods [16, 31, 17], our method does not use state-space augmentation because this technique typically reduces computational tractability. For this reason, we do not augment the state space with the running maximum over each time period . The range of may be large since the bounds of may be large. Instead of using state-space augmentation to handle the CVaR and the maximum, we use a scaled expectation to upper bound the CVaR and a log-sum-exponential function to upper bound the maximum, . Our first main result is below.

Theorem 3.2 (Upper Bound for CVaR of ).

For any , , , and , it holds that

| (12) |

The quantity represents the maximum extent of constraint violation of the state trajectory, averaged over the % worst cases, when the system uses the policy and starts from the state . The right-hand-side of (12) can be estimated more readily than for small and provides a conservative approximation to . If is small, more samples of are required to estimate since small corresponds to rarer larger realizations of . (We are more interested in using small for safety-critical applications.) Theorem 3.2 is powerful because it can be used to estimate the performance of any control policy with respect to . Policies may be designed for different objectives, e.g., efficiency in power or fuel consumption, robustness to bounded adversarial disturbances, robustness to bounded non-linearities, etc. It may be beneficial to estimate their performance with respect to a risk-sensitive safety criterion, such as , efficiently. The proof of Theorem 3.2 requires two lemmas.

Lemma 3.3 (CVaR-Expectation Inequality).

Let be a probability space, such that a.e. w.r.t. , and . Then, .

A version of the inequality is stated without proof in [10]. We provide a short proof below.

Proof 3.4.

Start from the CVaR definition (1), and select . Then, . Since a.e., a.e., so .

Lemma 3.3 provides an upper bound for CVaR in terms of the expectation and the risk-sensitivity level when non-negative random variables are evaluated. In addition to Lemma 3.3, the proof of Theorem 3.2 requires the following result, which relates the CVaR of the logarithm to the logarithm of the CVaR.

Lemma 3.5 (CVaR-Log Inequality).

Let and . Suppose that there are real numbers such that for every . Then, .

Proof 3.6.

Let and (5b). Define , where . is a probability space, and is finite. View as a random variable on . It holds that for all , and is a convex function from to . Thus, by Jensen’s Inequality, . Moreover, since is non-negative and bounded everywhere, is non-negative and bounded a.e., and by using the definition of , it follows that

| (13) |

Since is arbitrary in the analysis above, the inequality (13) holds for all . In addition, we have by (5), because , and for all . Thus, . Since the natural logarithm is increasing,

| (14) |

By (13) and (14), it holds that for all . Since the supremum is the least upper bound, we conclude that .

Proof 3.7 (Theorem 3.2).

Note the log-sum-exp approximation for the maximum [44, Sec. 3.1.5, p. 72]: If and , then

| (15) |

Let , , , and . Recall that , where we have presented and at the start of Sec. 3. Since is -valued,

| (16) |

Since is bounded and is a sum of finitely many exponential functions of , there exist real numbers such that for every . It follows that satisfies the assumptions of Lemma 3.5, and thus,

| (17) |

By the inequality in (15) and by the definitions of and , the inequality holds a.e. w.r.t. . Since CVaR is monotonic and positively homogeneous, and since ,

| (18) |

We use (17) and (18) to find that

| (19) |

Note that such that . Indeed, and so is also an element of , hence . is bounded everywhere, and in particular, from below by a real number . Therefore, . Consequently, . In addition, the assumptions of Lemma 3.3 are satisfied, and therefore,

| (20) |

We use the conclusion of Theorem 3.2 to define particular subsets of the state space. First, we call these sets approximations, and then, we prove that they are under-approximations to risk-sensitive safe sets in Theorem 3.9.

Definition 3.8 (Approximations to Risk-Sensitive Safe Sets).

Let , , and be given. The -approximation set for a given policy is defined by

| (21) |

The -approximation set is defined by

| (22) |

We denote the infimum in (22) by

| (23) |

where is the set of randomized history-dependent policies, which also includes deterministic Markov policies. Estimating is the critical step for estimating the sets . The problem of estimating is a Markov decision process problem. Thus, and a deterministic Markov policy such that for all can be computed via dynamic programming, in principle, if a measurable selection condition holds.666Measurable selection conditions, e.g., see [45, Chapter 3.3] or [15], are commonly invoked to guarantee the existence of a policy that optimizes or nearly optimizes an expected cumulative cost subject to a MDP. Therefore, for a fixed , an algorithm to estimate , where is a family of risk-sensitivity levels, exists and is tractable. The next theorem shows that the sets in Definition 3.8 are under-approximations to risk-sensitive safe sets (Definition 1).

Theorem 3.9.

Proof 3.10.

Eq. (24) follows from Theorem 3.2. Let , , , and be given. Let . Then,

| (26) |

where the left-hand-side is bounded below by a positive real number since is as well. It follows that is finite. Since the natural logarithm is increasing and , we have

| (27) |

By Theorem 3.2, it holds that

| (28) |

Combine (27) and (28) to find that , which shows that and proves (24). Now, to prove (25), let , which implies that

| (29) |

Let be given. Since the left-hand-side of (29) is finite, there is a such that

| (30) | ||||

where the second line holds by (29). Note that the quantity is finite. Take the logarithm of (30) and then divide by to obtain

| (31) |

By Theorem 3.2, it holds that

| (32) |

Therefore, . Since , it follows that

| (33) |

Consequently, we have

| (34) |

This analysis holds for any . Let , and use the continuity of the logarithm to obtain

| (35) |

Since , we conclude that . Since any is also an element of , it holds that .

Since we have shown that and are subsets of the risk-sensitive safe sets, and , respectively, we now refer to and as under-approximations.

Remark 3.11 (Assessment of Approximation Errors).

Three approximations are required for the proof above. First, we use a soft-maximum, under which we have

| (36) |

where , and there are positive constants and (which depend on , , and the bounds of ) such that everywhere. The inequality (36) implies an improved approximation with larger values of or smaller values of . However, since it is not feasible to optimize directly, our next step is to leverage the CVaR-log inequality provided by Lemma 3.5. The associated error is given by

| (37) |

Since the range of is , it follows that . Therefore, we anticipate a smaller error when has a smaller range, which occurs when is smaller, for example.

The last approximation is , which of course is poor as . However, for a fixed , we anticipate that this approximation performs well when has a fat (upper) tail, which we state formally in the following lemma.

Lemma 3.12 (Tightness of ).

Assume the conditions of Lemma 3.5, and let . Suppose that for some finite , it holds that

| (38) |

Then, .

Remark 3.13 (Fat tail condition (38)).

The second inequality in (38) means that the cumulative VaR in the upper -fraction of the distribution of , , is at least times greater than the cumulative VaR in the lower -fraction of the distribution of , . The maximum value of that satisfies (38) is , which gives a measure of tail “fatness.” For example, if the distribution of is a standard log-normal with parameters and , and if , then numerical integration yields If is increased to 2 under the same conditions, then .

Next, we prove Lemma 3.12.

Proof 3.14 (Lemma 3.12).

From Theorem 3.9, we obtain tractable under-approximations to risk-sensitive safe sets. In practice, one selects manually and then estimates (23) for a family of risk-sensitivity levels. For a fixed , only one MDP problem on the original state space needs to be solved for any family of risk-sensitivity levels because is a standard MDP problem scaled by . In Sec. 5, which presents numerical examples, we take one approach to choose a suitable value of manually by visual inspection. Before proceeding to the numerical examples, we present one additional theoretical contribution.

4 Toward a Parameter-Independent Safety Analysis Framework

Previously, we have defined risk-sensitive safe sets in terms of the CVaR of a maximum random cost. However, this risk-sensitive safety criterion is difficult to optimize exactly without using state-space augmentation, which motivated us to derive a parameter-dependent upper bound. One may wonder whether there is another coherent risk functional (ideally related to CVaR) that admits an upper bound, which can be computed via DP on the original state space without an additional parameter that requires tuning. The answer is indeed positive, as presented below.

Definition 4.15 (Proposed Risk Functional).

Let , , , and be given. Let be a set of tuples of densities. Each tuple takes the form , where the properties of the densities follow. For each , is Borel measurable, and for every , it holds that . Here, is the set of Borel-measurable functions of the form such that a.e. w.r.t. and . We define by

| (41) |

Remark 4.16 (Interpretation for ).

is related to the set of densities in the CVaR representation given by (5). If the probability space is , then , where .

Remark 4.17 (Interpretation for ).

Although we do not yet have an exact interpretation for , we provide a preliminary interpretation here. The quantity is a distributionally robust expectation of , such that an uncertainty perturbs the system’s nominal transition law at each time . may depend on the current time, state, and control. Moreover, strikes a balance between the expectation and CVaR, as formalized below.

Lemma 4.18 (Coherence of , relation to CVaR).

The risk functional is coherent. In addition, for any , the inequality holds.

Proof 4.19.

We use the risk functional (41) to define a safe set.

Definition 4.20 (-Risk-Sensitive Safe Set).

For any and , define .

Definition 4.20 is inspired by Definition 1, and the form of (41) is inspired by the representation for CVaR in (8b)–(8c). We emphasize a key distinction. In (41), there is a function for each that depends on the current state and control. In (8b)–(8c), however, each function in depends on the entire history. The “separable” structure of (41) allows us to derive a DP algorithm on the original state space to upper bound without using a parameter that requires tuning. In this section, we make two assumptions.

Assumption 1 (Properties of )

We consider the case when is cumulative. The functions for all and are bounded and upper semi-continuous (usc).

Assumption 2 (Continuity property of )

The transition kernel (6) is continuous in total variation; that is, if , then .

Remark 4.21 (Example that satisfies Assumption 2).

Suppose that has a continuous non-negative density and in (6) has the form , where is a vector space with field , and are continuous, and is non-zero. Then, by Scheffé’s Lemma, Assumption 2 is satisfied. We note that continuity of is a typical condition in stochastic control, e.g., see [15, p. 209], and requiring additional structure on the dynamics to achieve tractable algorithms is standard. For example, under some assumptions the dynamics may be decomposed into overlapping systems, to obtain conservative under-approximations to reachable sets for continuous-time, non-stochastic systems [55, 23]. A mixed monotone structure has been assumed to approximate reachable sets for discrete-time non-stochastic systems, with applications to traffic safety [56, 57]. More broadly, additive continuous noise is a realistic assumption in many domains, e.g., additive Gaussian noise in information theory and control (classical references include [4, 58]) and additive Brownian motion in continuous-time epidemiological modeling [59, 60].

Boundedness and upper semi-continuity of for all ensures that for any and . Also, boundedness of ensures that the iterates of a DP recursion are bounded, which we use to show that a supremum over of the form is attained (Lemma 6.23, Appendix). This attainment and Assumption 2 together guarantee that the supremum is usc in (Lemma 6.27, Appendix). The upper semi-continuity of the supremum permits the derivation of an upper bound for via DP.

Theorem 4.22 (DP to Upper Bound ).

A proof for Theorem 4.22 is in the Appendix, where we include supporting results as well.

Theorem 3 is exciting for two main reasons: 1) it provides a more numerically tractable way to estimate safe sets (the upper bound does not have a parameter that requires tuning, and the algorithm does not require an augmented state space); and 2) more broadly, the result initiates new avenues for tractable solutions to risk-sensitive safety analysis problems.

5 Numerical Examples

Here, we present examples of risk-sensitive safe sets and their under-approximations as in Definition 1 for a temperature system and a stormwater system.777We used the Tufts Linux Research Cluster (Medford, MA) with MATLAB (The Mathworks, Inc.). Our code is available from https://github.com/risk-sensitive-reachability/IEEE-TAC-2021. For each example, we have chosen a value of by exploring increasing integer values and then stopping the exploration when improvements in the estimates of were no longer apparent.

5.1 Temperature System

Consider a thermostatically controlled load evolving on a finite-time horizon via a deterministic Markov policy ,

This model is from [29, 48]. is the -valued random temperature () of a thermal mass at time . is the -valued control at time . The amount of power supplied to the system decreases as the value of the control increases from 0 to 1. is a -valued, iid stochastic process that arises due to environmental uncertainties. We consider three discrete distributions for the disturbance process, where each distribution has a distinct skew (left skew, no skew, or right skew). In each distribution, the minimum disturbance value is , and the maximum disturbance value is 0.5 . Table 1 provides the model parameters.

| Symbol | Description | Value |

| time delay | (no units) | |

| temperature shift | 32 | |

| thermal capacitance | 2 | |

| control efficiency | 0.7 (no units) | |

| constraint set | ||

| range of energy transfer to/from thermal mass | 14 kW | |

| thermal resistance | 2 | |

| duration of | h | |

| length of discrete time horizon | 12 (= 1 h) | |

| control space | (no units) | |

| state space | ||

| h hours, kW kilowatts, degrees Celsius. | ||

We have chosen to quantify the extent of constraint violation of the state with respect to the constraint set . is a temperature range, where the state trajectory should remain inside whenever possible. For different values of (see next paragraph), we have implemented classical DP with linear interpolation to estimate

| (43) |

and a deterministic Markov policy such that for all . DP on continuous state and control spaces is implemented typically via discretization and interpolation. In particular, we have discretized the set of controls and the set of states uniformly at a resolution of 0.1. To improve efficiency of DP, approximate DP methods are being developed, e.g., see [49, 50], and the references therein. While these methods are exciting, we leave investigations of their applicability to risk-sensitive safety analysis for future work.

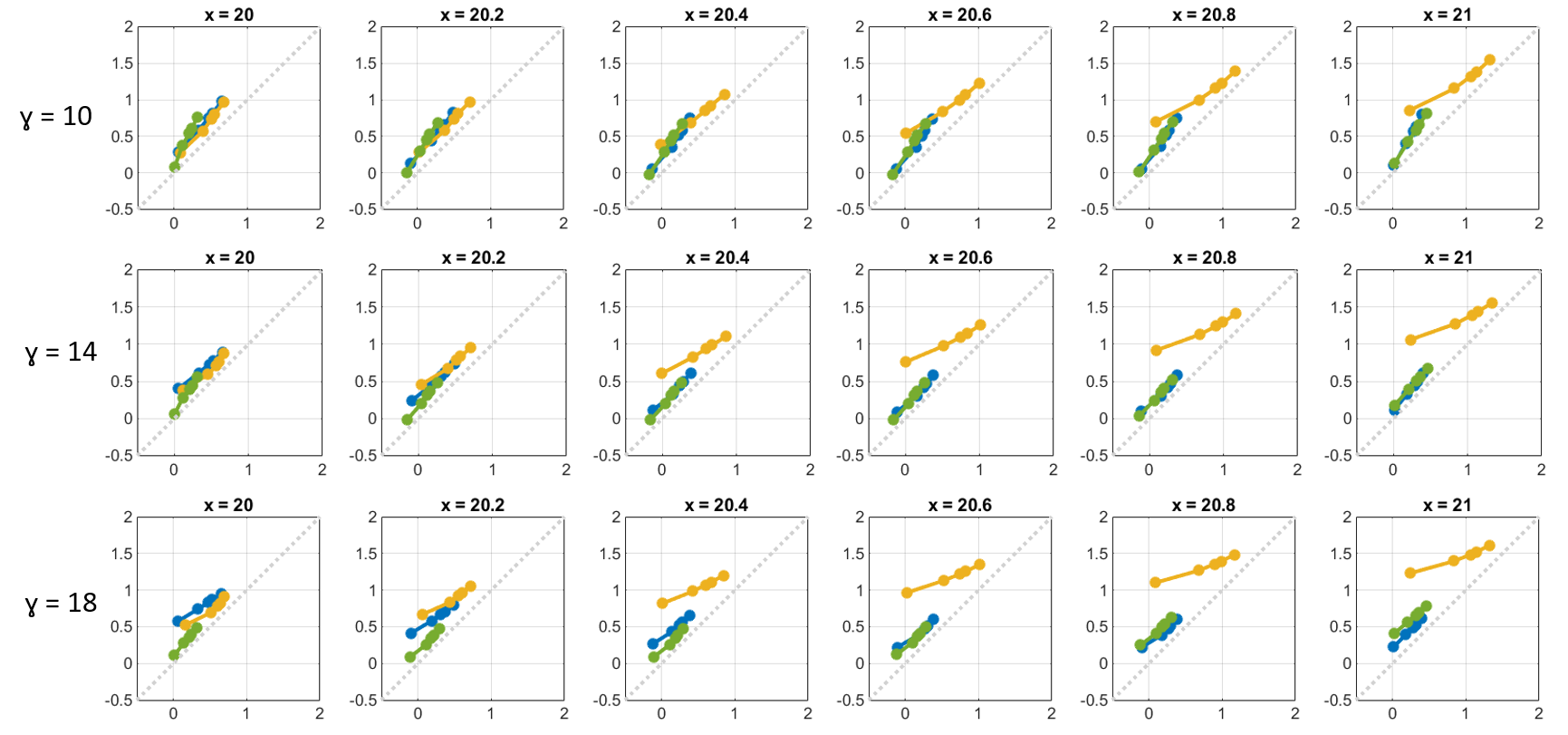

We have used because for all and , the stage cost is at most , a large number that a personal computer can handle. We have considered risk-sensitivity levels from nearly risk-neutral () to more risk-averse ( near 0). Specifically, we have chosen . A typical risk-sensitivity level is or , and we have considered smaller values of as well. For and , we have estimated (23) by dividing our estimate of (43) by . Let denote the state space grid. By using our estimate of , we have simulated 100,000 trajectories from each initial state to generate an empirical distribution of . Then, for each , we have used a consistent CVaR estimator [37, p. 300] to estimate .

Fig. 3 provides a visual summary of the inequality that we have proved in Theorem 3.2:

| (44) |

Each plot in Fig. 3 shows estimates of the right-hand-side of (44) on the vertical axis versus estimates of the left-hand-side of (44) on the horizontal axis for the 5 values of in . In each plot, each solid colored line consists of 5 points, one for each . Points associated with smaller values of (more risk-averse) are positioned farther away from the origin. In each plot, there are three solid colored lines, one for each distribution of the disturbance process. In each plot, and an initial state are fixed. We have chosen initial states inside or on the boundary of the constraint set . Fig. 3 is consistent with the inequality that we have proved in Theorem 3.2 since the solid colored lines are located above the gray line of slope 1. Fig. 3 suggests that there is no unique value of that provides the best approximation for all initial states , risk-sensitivity levels , and disturbance distributions.

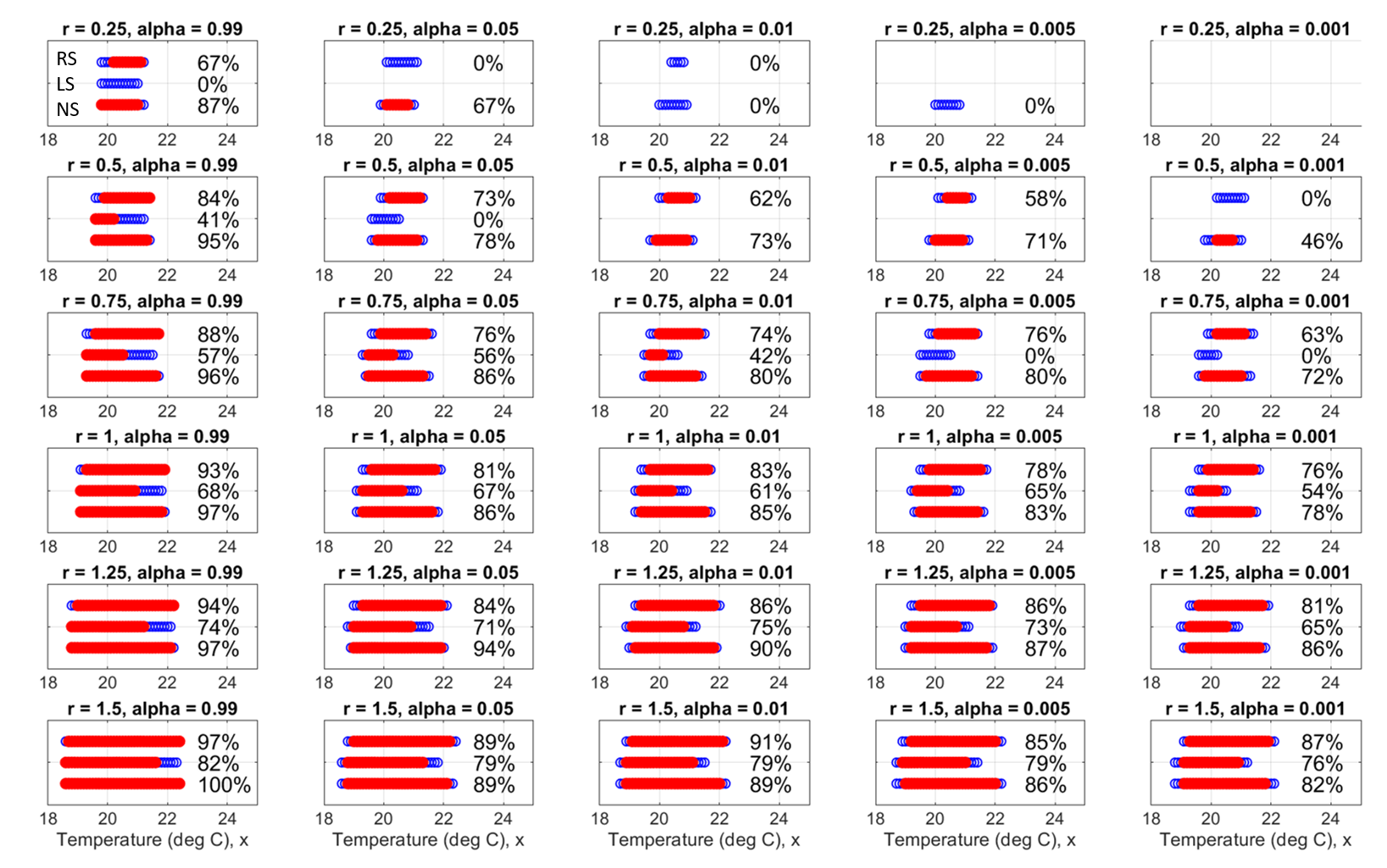

However, by Theorem 3.9, we have flexibility in choosing the value of . In particular, we favor the quality of the approximations for small values of due to our focus on safety and present sets using as an example of a value that reflects this preference (Fig. 4).888Higher-quality approximations are those in which the estimates of the under-approximations are generally closer to the estimates of the risk-sensitive safe sets when considering all three disturbance distributions. We suggest an approach to quantify the quality of the approximations in Fig. 4. Fig. 4 provides estimates of the -risk-sensitive safe set for (9)

and the -under-approximation set (22)

Note that .999Recall that is a policy that satisfies . That is, is an optimal policy for the MDP problem that defines . In Fig. 4, estimates of (solid red) and (white circles with blue boundary) are shown for the risk-sensitivity levels and various with . The estimates of are subsets of the estimates of , which we expect by Theorem 3.9. The estimates of form an increasing sequence of subsets as increases and increases, which is consistent with Lemma 1.

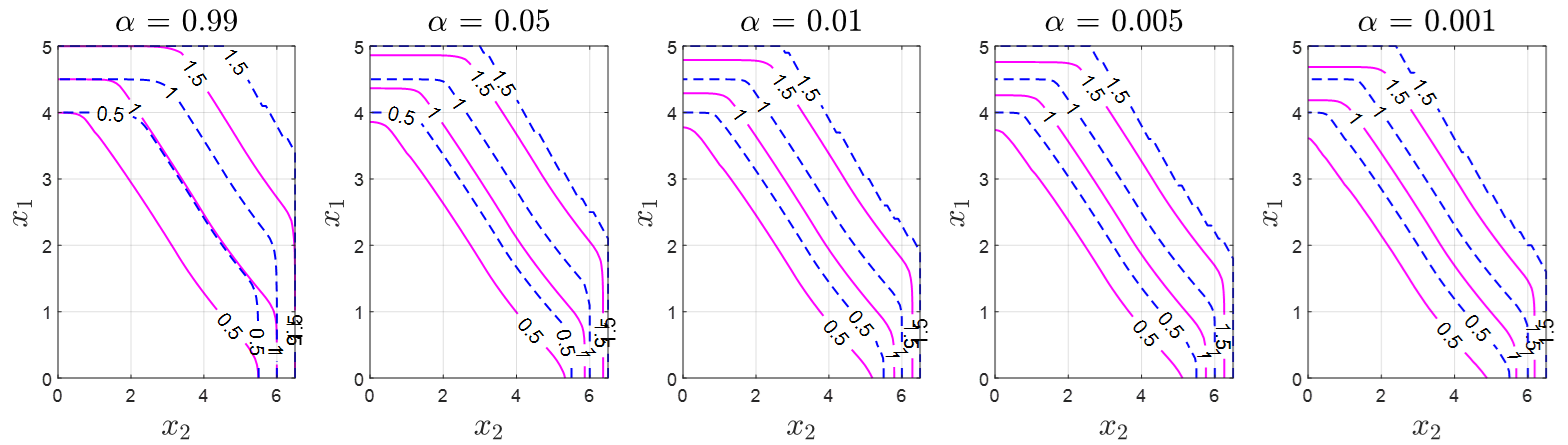

5.2 Stormwater System

Next, we illustrate risk-sensitive safety analysis using a gravity-driven stormwater system with an automated valve. Consider a two-tank stormwater system evolving on a finite-time horizon using a deterministic Markov policy , . Let . The state is the -valued random water elevations in the tanks at time (ft, ft). is the -valued valve setting at time (closed to open). is a -valued, iid stochastic process of surface runoff. is the duration of . The function is given by

Model parameters are in Table 2. The constraint set specifies the maximum water elevations that the tanks can hold without surcharge. The stage cost is the maximum surcharged water level when the system occupies the state .

We have identified a discrete distribution for the disturbance process with the approximate statistics, mean (12.2 cfs), variance (9.9 cfs2), and skew (0.74), where cfs is cubic feet per second. In previous work, we obtained runoff samples by simulating a design storm in PCSWMM (Computational Hydraulics International), which extends the US Environmental Protection Agency’s Stormwater Management Model [52, 53]. In this previous work, the empirical distribution had positive skew, and the mean was about 12.2 cfs [52], which are reflected in the current distribution (not shown in the interest of space).

In Fig. 5, we show estimates of risk-sensitive safe sets and their under-approximations using for 5 risk-sensitivity levels (see also Table 3). The shape of the contour of indicates a critical trade-off between the maximum initial water elevations in the two tanks from which the system meets a desired degree of safety. The similarity in the shapes of and is notable, suggesting that may be a useful tool for inferring these critical trade-offs in networked water systems.

| Symbol | Description | Value |

| surface area of tank 1 | 28292 ft2 | |

| surface area of tank 2 | 25965 ft2 | |

| discharge coefficient | 0.61 (no units) | |

| acceleration due to gravity | 32.2 | |

| maximum water level in tank 1 | 3.5 ft | |

| maximum water level in tank 2 | 5 ft | |

| circle circumference-to-diameter ratio | 3.14 | |

| radius of drain | ft | |

| radius of valve | ft | |

| duration of | 5 min | |

| length of discrete time horizon | 24 ( 2 h) | |

| control space | (no units) | |

| state space | ||

| invert elevation of pipe from base of tank 1 | 1 ft | |

| invert elevation of pipe from base of tank 2 | 2.5 ft | |

| elevation from base of tank 2 to orifice | 1 ft | |

| ft feet, s seconds, min minutes, h hours. | ||

6 Concluding Remarks

This paper develops trajectory-wise safety specifications for control systems that quantify the severity of random harmful outcomes and thereby generalize classical stochastic safety analysis. Our primary contribution is to develop a tractable, interpretable safety analysis method with theoretical guarantees that assesses the upper tail of a cost distribution by using CVaR. It is notable that our method provides a parameter-dependent upper bound to the CVaR of a maximum cost without augmenting the state space. We have developed compelling numerical examples, which demonstrate the utility and tractability of our under-approximation approach. Moreover, we have proposed a risk-sensitive safe set definition in terms of a new coherent risk functional, inspired by CVaR, that admits a parameter-independent upper bound. We show that this upper bound can be computed via DP on the original state space by proving the regularity of a supremum over a function space for a class of transition kernels. Numerical investigations of leveraging our approximation to provide an efficient preliminary estimate to the exact CVaR is an exciting future direction. For instance, we have recently demonstrated the usefulness of efficient approximate “warm-start” computations to examine the effect of different design changes to stormwater infrastructure [61]. More broadly, combining techniques from approximate dynamic programming, stochastic rollout, and risk-sensitive safety analysis could lead to novel controller synthesis algorithms for higher-dimensional systems.

| ft | 74.3 | 77.3 % | 76.6 % | 76.0 % | 72.5 % |

| ft | 82.9 % | 84.2 % | 83.1 % | 83.0 % | 81.2 % |

| ft | 84.4 % | 75.6 % | 71.2 % | 69.9 % | 66.0 % |

| This table provides the percentages for the sets in Fig. 5 (stormwater system, ). | |||||

Appendix

Lemma 6.23 (Attainment of Supremum).

Let be Borel measurable and bounded, and let . Define the function by

| (45) |

Then, for any , there is a such that

| (46) |

Proof 6.24.

Let , and fix the probability space . Denote for brevity, and view as a subset of with the weak topology. Define the functional by

| (47) |

It suffices to show that is weakly continuous and is weakly compact. Weak continuity follows from two well-known facts: 1) a linear functional on a normed vector space is weakly continuous if and only if it is strongly continuous [54, Prop. 2.5.3], and 2) a linear functional on a normed vector space is strongly continuous if and only if it is bounded [12, Prop. 5.2]. By applying standard techniques, it follows that is a bounded linear functional on a normed vector space, and thus, is weakly continuous. As is a bounded and weakly closed subset of , is weakly compact by the Banach-Alaoglu Theorem [37, p. 401]. Here, we use the fact that is reflexive, and hence, the weak and weak* topologies of are the same. We provide details about weak closedness in a footnote.101010For weak closedness, recall the fact [51, Thm. 3.7]: Let be a Banach space, and let be a convex subset of . Then, is closed in the weak topology if and only if it is closed in the strong topology. Since is convex, to show that is weakly closed, it suffices to show that is strongly closed. Strong closedness of follows from 1) strong convergence implying weak convergence and 2) strong convergence implying the existence of a subsequence that converges a.e. to the same limit function [46, Thms. 2.5.1 & 2.5.3]. Let converge strongly to . The first fact ensures that , and the second fact ensures that a.e., and thus, .

We use similar techniques to prove Lemma 6.25. Lemma 6.25 is needed to guarantee that a supremum over (45) is upper semi-continuous in .

Lemma 6.25 (Existence of weakly convergent subsequence).

Let be a probability measure on , the set of functions such that a.e. w.r.t. , and . Then, there exist and such that converges to in the weak topology of .

Proof 6.26.

The proof requires two facts. The first fact is [51, Thm. 3.18]: Assume that is a reflexive Banach space, and let be a (uniformly) bounded sequence in . Then, there is a subsequence that converges in the weak topology. is a reflexive Banach space, and for all . Thus, there exist and such that converges weakly to . Moreover, it holds that using [51, Thm. 3.7] (Footnote 10). Indeed, is a convex subset of , and is strongly closed in . Thus, is weakly closed in , which implies that .

We use Lemma 6.25 to prove the next supporting result.

Lemma 6.27 (Properties of ).

Proof 6.28.

Boundedness of follows from -a.e.-boundedness of for any . Now, is usc if and only if

is closed for every . Let and converging to be given, and we shall show that . It suffices to show that there exist and with such that

Indeed, if so, then

Denote and for brevity. By Lemma 6.23, for every ,

Since a.e. w.r.t. ,

where . Define

It follows that with everywhere. Also, it holds that , where

and . By Lemma 6.25, there exist and such that converges to in the weak topology of . It holds that , and we explain why next. For any , it holds that everywhere, and it follows that

where

The quantity is the total variation of the signed measure evaluated at the set . By the weak convergence of to in , as . By Assumption 2, as .

Now, for every , we use the triangle inequality and everywhere boundedness of to find that

where

satisfies for all , and

By the weak convergence of to in , as , and by Assumption 2, as . We choose

and it follows that is usc.

We use the upper semi-continuity of to prove Theorem 4.22.

Proof 6.29 (Theorem 4.22).

Proceed by induction. is usc and bounded. Now, assume that for some , is usc and bounded. Then, is Borel measurable and bounded, which implies that is usc and bounded by Lemma 6.27. Since is a sum of usc and bounded functions, is usc and bounded. By [15, Prop. 7.34], we conclude that is usc and bounded, and for every , there is a Borel-measurable function such that for all .

A DP argument completes the proof, which we outline below.111111A conditional expectation is not unique everywhere in general [46, Th. 6.3.3]. However, for the sake of simplicity, we write that a relation with a conditional expectation holds everywhere, following the proof of [45, Th. 3.2.1]. Let be the set of randomized Markov policies. For , define the random cost-to-go by

and note that . For any and , we denote the -conditional expectation of given by , where . For any and , the following recursion (“law of iterated expectations”) holds: for and ,

| (48a) | |||

| where is defined by | |||

| (48b) | |||

with for each . For any policy , we have

| (49) |

Let be given. Then, for each , there exists a Borel-measurable function such that

| (50) |

Define , which is a deterministic Markov policy and thus is an element of (the class of randomized history-dependent policies) as well. Hence,

It suffices to prove that

| (51) |

for all , , and . Indeed, by setting in (51) and taking the supremum over , we would derive . Since is arbitrary, the desired statement would be shown. The sufficient condition (51) holds by an inductive argument.121212The base case holds because for all . Now, assume that for some , it holds that for all and . Let and be given. Since is a deterministic Markov policy, we have By the induction hypothesis and from the definition of , it follows that Since , we derive . Then, we complete the induction using the second inequality in (50), namely .

Acknowledgments

The authors extend their sincerest gratitude to the four anonymous reviewers whose feedback was invaluable in improving the rigor and presentation of this work. The authors gratefully acknowledge many discussions with Jonathan Lacotte, Yuxi Han, Zhiyan Ding, and Michael Lim during the development of an earlier version of this paper. The authors are also thankful for advice provided by Serdar Yüksel, Nicole Bäuerle, Ludovic Tangpi, Michael Fauß, Alois Pichler, and Raymond Kwong.

References

- [1] R. A. Howard and J. E. Matheson, “Risk-sensitive Markov decision processes,” Management Science, vol. 18, no. 7, pp. 356–369, 1972.

- [2] D. H. Jacobson, “Optimal stochastic linear systems with exponential performance criteria and their relation to deterministic differential games,” IEEE Transactions on Automatic Control, vol. 18, no. 2, pp. 124–131, 1973.

- [3] G. B. di Masi and L. Stettner, “Risk-sensitive control of discrete-time Markov processes with infinite horizon,” SIAM Journal on Control and Optimization, vol. 38, no. 1, pp. 61–78, 1999.

- [4] P. Whittle, “Risk-sensitive linear/quadratic/Gaussian control,” Advances in Applied Probability, vol. 13, no. 4, pp. 764–777, 1981.

- [5] A. Shapiro, “On a time consistency concept in risk averse multistage stochastic programming,” Operations Research Letters, vol. 37, no. 3, pp. 143–147, 2009.

- [6] K. Boda and J. A. Filar, “Time consistent dynamic risk measures,” Mathematical Methods of Operations Research, vol. 63, no. 1, pp. 169–186, 2006.

- [7] D. Kreps, “Decision problems with expected utility critera, I: Upper and lower convergent utility,” Mathematics of Operations Research, vol. 2, no. 1, pp. 45–53, 1977.

- [8] T. Bjork and A. Murgoci, “A theory of Markovian time-inconsistent stochastic control in discrete time,” Finance and Stochastics, vol. 18, pp. 545–592, 2014.

- [9] L. Xin and A. Shapiro, “Bounds for nested law invariant coherent risk measures,” Operations Research Letters, vol. 40, no. 6, pp. 431–435, 2012.

- [10] A. Shapiro, “Minimax and risk averse multistage stochastic programming,” European Journal of Operational Research, vol. 219, no. 3, pp. 719–726, 2012.

- [11] P. Artzner, et al., “Coherent measures of risk,” Mathematical Finance, vol. 9., no. 3, pp. 203–228, 1999.

- [12] G. B. Folland, Real Analysis: Modern Techniques and their Applications, 2nd Edition. New York: John Wiley & Sons, 1999.

- [13] H. Follmer and A. Schield, Stochastic Finance: An Introduction in Discrete Time, 2nd Edition. De Gruyter Studies in Mathematics, 2004.

- [14] A. Ruszczyński and A. Shapiro, “Optimization of convex risk functions,” Mathematics of Operations Research, vol. 31, no. 3, pp. 433–452, 2006.

- [15] D. P. Bertsekas and S. Shreve, Stochastic Optimal Control: The Discrete-Time Case. Belmont: Athena Scientific, 1996.

- [16] N. Bäuerle and J. Ott, “Markov decision processes with Average-Value-at-Risk criteria, Mathematical Methods of Operations Research, vol. 74, no. 3, pp. 361–379, 2011.

- [17] N. Bäuerle and U. Rieder, “More risk-sensitive Markov decision processes,” Mathematics of Operations Research, vol. 39, no. 1, pp. 105–120, 2014.

- [18] B. Rudloff, A. Street, and D. M. Valladao, “Time consistency and risk averse dynamic decision models: Definition, interpretation and practical consequences,” European Journal of Operational Research, vol. 234, no. 3, pp. 743–750, 2014.

- [19] P. A. Forsyth, “Multiperiod mean Conditional Value at Risk asset allocation: Is it advantageous to be time consistent?,” SIAM Journal on Financial Mathematics, vol. 11, no. 2, pp. 358–384, 2020.

- [20] D. P. Bertsekas and I. B. Rhodes, “On the minimax reachability of target sets and target tubes,” Automatica, vol. 7, no. 2, pp. 233–247, 1971.

- [21] I. M. Mitchell, A. M. Bayen, and C. J. Tomlin, “A time-dependent Hamilton-Jacobi formulation of reachable sets for continuous dynamic games,” IEEE Transactions on Automatic Control, vol. 50, no. 7, pp. 947–957, 2005.

- [22] K. Margellos and J. Lygeros, “Hamilton-Jacobi formulation for reach-avoid differential games,” IEEE Transactions on Automatic Control, vol. 56, no. 8, pp. 1849–1861, 2011.

- [23] M. Chen, S. L. Herbert, M. S. Vashishtha, S. Bansal, and C. J. Tomlin, “Decomposition of reachable sets and tubes for a class of nonlinear systems,” IEEE Transactions on Automatic Control, vol. 63, no. 11, pp. 3675–3688, 2018.

- [24] M. Chen and C. J. Tomlin, “Hamilton-Jacobi reachability: Some recent theoretical advances and applications in unmanned airspace management,” Annual Review of Control, Robotics, and Autonomous Systems, vol. 1, no. 1, pp. 333–358, 2018.

- [25] A. Abate, M. Prandini, J. Lygeros, and S. Sastry, “Probabilistic reachability and safety for controlled discrete time stochastic hybrid systems,” Automatica, vol. 44, no. 11, pp. 2724–2734, 2008.

- [26] S. Summers and J. Lygeros, “Verification of discrete time stochastic hybrid systems: A stochastic reach-avoid decision problem,” Automatica, vol. 46, no. 12, pp. 1951–1961, 2010.

- [27] M. Kamgarpour, J. Ding, S. Summers, A. Abate, J. Lygeros, and C. Tomlin, “Discrete time stochastic hybrid dynamical games: Verification and controller synthesis,” in Proceedings of the IEEE Conference on Decision and Control, 2011, pp. 6122–6127.

- [28] J. Ding, M. Kamgarpour, S. Summers, A. Abate, J. Lygeros, and C. Tomlin, “A stochastic games framework for verification and control of discrete time stochastic hybrid systems,” Automatica, vol. 49, pp. 2665–2674, 2013.

- [29] I. Yang, “A dynamic game approach to distributionally robust safety specifications for stochastic systems,” Automatica, vol. 94, pp. 94–101, 2018.

- [30] S. Samuelson and I. Yang, “Safety-aware optimal control of stochastic systems using Conditional Value-at-Risk,” in Proceedings of the American Control Conference, 2018, pp. 6285–6290.

- [31] Y. Chow, A. Tamar, S. Mannor, and M. Pavone, “Risk-sensitive and robust decision-making: A CVaR optimization approach,” in Advances in Neural Information Processing Systems, 2015, pp. 1522–1530.

- [32] J. F. Bonnans, P. Lavigne, and L. Pfeiffer, “Discrete-time mean field games with risk-averse agents,” ESAIM: Control, Optimisation and Calculus of Variations, vol. 27, no. 44, pp. 1–27, 2021.

- [33] V. Borkar and R. Jain, “Risk-constrained Markov decision processes,” IEEE Transactions on Automatic Control, vol. 59, no. 9, pp. 2574–2579, 2014.

- [34] W. B. Haskell and R. Jain, “A convex analytic approach to risk-aware Markov decision processes,” SIAM Journal on Control and Optimization, vol. 53, no. 3, pp. 1569–1598, 2015.

- [35] P. Whittle, Risk-sensitive Optimal Control, Chichester: Wiley, 1990.

- [36] R. T. Rockafellar and S. Uryasev, “Conditional Value-at-Risk for general loss distributions,” Journal of Banking & Finance, vol. 26, no. 7, pp. 1443–1471, 2002.

- [37] A. Shapiro, D. Dentcheva, and A. Ruszczyński, Lectures on Stochastic Programming: Modeling and Theory. Society for Industrial and Applied Mathematics, Mathematical Programming Society, 2009.

- [38] M. P. Chapman, J. Lacotte, A. Tamar, D. Lee, K. M. Smith, V. Cheng, J. F. Fisac, S. Jha, M. Pavone, and C. J. Tomlin, “A risk-sensitive finite-time reachability approach for safety of stochastic dynamic systems,” in Proceedings of the American Control Conference, pp. 2958–2963, 2019.

- [39] C. W. Miller and I. Yang, “Optimal control of Conditional Value-at-Risk in continuous time,” SIAM Journal on Control and Optimization, vol. 55, no. 2, pp. 856–884, 2017.

- [40] G. C. Pflug and A. Pichler, “Time-inconsistent multistage stochastic programs: Martingale bounds,” European Journal of Operational Research, vol. 249, no. 1, pp. 155–163, 2016.

- [41] G. C. Pflug and A. Pichler, “Time-consistent decisions and temporal decomposition of coherent risk functionals,” Mathematics of Operations Research, vol. 41, no. 2, pp. 682–699, 2016.

- [42] B. P. G. Van Parys, D. Kuhn, P. J. Goulart, and M. Morari, “Distributionally robust control of constrained stochastic systems,” IEEE Transactions on Automatic Control, vol. 61, no. 2, pp. 430–442, 2015.

- [43] A. Akametalu, “A learning-based approach to safety for uncertain robotic systems,” Ph.D. thesis, Electrical Engineering and Computer Sciences, University of California Berkeley, USA, 2018.

- [44] S. Boyd and L. Vandenberghe, Convex Optimization. Cambridge: Cambridge University Press, 2004.

- [45] O. Hernández-Lerma and J. B. Lasserre, Discrete-Time Markov Control Processes: Basic Optimality Criteria. New York: Springer, 1996.

- [46] R. B. Ash, Real Analysis and Probability. New York: Academic Press, 1972.

- [47] A. Ruszczyński, “Risk-averse dynamic programming for Markov decision processes,” Mathematical Programming, vol. 125, no. 2, pp. 235–261, 2010.

- [48] R. E. Mortensen and K. P. Haggerty. “A stochastic computer model for heating and cooling loads,” IEEE Transactions on Power Systems, vol. 3, no. 3, pp. 1213–1219, 1988.

- [49] P. M. Esfahani, et al., “From infinite to finite programs: Explicit error bounds with applications to approximate dynamic programming,” SIAM Journal on Optimization, vol. 28, no. 3, pp. 1968–1998, 2018.

- [50] D. P. Bertsekas, Reinforcement Learning and Optimal Control. Belmont: Athena Scientific, 2019.

- [51] H. Brezis, Functional Analysis, Sobolev Spaces and Partial Differential Equations. New York: Springer, 2010.

- [52] M. P. Chapman, K. M. Smith, V. Cheng, D. L. Freyberg, and C. Tomlin, “Reachability analysis as a design tool for stormwater systems,” in Proceedings of the IEEE Conference on Technologies for Sustainability, pp. 1–8, 2018.

- [53] L. A. Rossman, Storm Water Management Model User’s Manual, Version 5.0. National Risk Management Research Laboratory, Office of Research and Development, US EPA, Cincinnati, 2010.

- [54] R. E. Megginson, An Introduction to Banach Space Theory. New York: Springer Science & Business Media, 1998.

- [55] M. Chen, S. Herbert, and C. J. Tomlin, “Exact and efficient Hamilton-Jacobi guaranteed safety analysis via system decomposition,” in Proceedings of the IEEE International Conference on Robotics and Automation (ICRA), pp. 87–92, 2017.

- [56] S. Coogan and M. Arcak, “Efficient finite abstraction of mixed monotone systems,” in Proceedings of the 18th International Conference on Hybrid Systems: Computation and Control, pp. 58–67, 2015.

- [57] S. Coogan, M. Arcak, and C. Belta, “Formal methods for control of traffic flow: Automated control synthesis from finite-state transition models,” IEEE Control Systems Magazine, vol. 37, no. 2, pp. 109–128, 2017.

- [58] B. Sinopoli, L. Schenato, M. Franceschetti, K. Poolla, M. I. Jordan, and S. S. Sastry, “Kalman filtering with intermittent observations,” IEEE Transactions on Automatic Control, vol. 49, no. 9, pp. 1453–1464, 2004.

- [59] M. Lefebvre, “Optimally ending an epidemic,” Optimization, vol. 67, no. 3, pp. 399–407, 2018.

- [60] M. Lefebvre, “Computer virus propagation modelled as a stochastic differential game,” Atti della Accademia Peloritana dei Pericolanti-Classe di Scienze Fisiche, Matematiche e Naturali, vol. 98, no. 1, 2020.

- [61] M. P. Chapman, M. Fauss, H. V. Poor, and K. M. Smith, “Risk-sensitive safety analysis via state-space augmentation,” under review for IEEE Transactions on Automatic Control, arXiv preprint arXiv:2106.00776.

[![[Uncaptioned image]](/html/2101.12086/assets/x1.png) ]Dr. Margaret Chapman is an Assistant Professor with the Edward S. Rogers Sr. Department of Electrical and Computer Engineering, University of Toronto, which she joined in July 2020. Her research focuses on risk-averse and stochastic control, with emphasis on safety and applications to healthcare and sustainable cities. Margaret is a recipient of a Leon O. Chua Award for achievement in nonlinear science from UC Berkeley (2021), a US National Science Foundation Graduate Research Fellowship (2014), a Berkeley Fellowship for Graduate Study (2014), and a Stanford University Terman Engineering Scholastic Award (2012). She received her B.S. and M.S. degrees in Mechanical Engineering from Stanford University (2012, 2014) and her Ph.D. degree in EECS from UC Berkeley (2020).

{IEEEbiography}[

]Dr. Margaret Chapman is an Assistant Professor with the Edward S. Rogers Sr. Department of Electrical and Computer Engineering, University of Toronto, which she joined in July 2020. Her research focuses on risk-averse and stochastic control, with emphasis on safety and applications to healthcare and sustainable cities. Margaret is a recipient of a Leon O. Chua Award for achievement in nonlinear science from UC Berkeley (2021), a US National Science Foundation Graduate Research Fellowship (2014), a Berkeley Fellowship for Graduate Study (2014), and a Stanford University Terman Engineering Scholastic Award (2012). She received her B.S. and M.S. degrees in Mechanical Engineering from Stanford University (2012, 2014) and her Ph.D. degree in EECS from UC Berkeley (2020).

{IEEEbiography}[![[Uncaptioned image]](/html/2101.12086/assets/x2.png) ]Dr. Riccardo Bonalli obtained his M.Sc. in Mathematical Engineering from Politecnico di Milano, Italy in 2014 and his Ph.D. in applied mathematics from Sorbonne Universite, France in 2018 in collaboration with ONERA - The French Aerospace Lab, France. He is a recipient of the ONERA DTIS Best Ph.D. Student Award 2018. He was a postdoctoral researcher with the Department of Aeronautics and Astronautics, Stanford University. Currently, Riccardo is a tenured researcher with the Laboratory of Signals and Systems (L2S), Université Paris-Saclay, Centre National de la Recherche Scientifique (CNRS), CentraleSupélec, France. His main research interests concern theoretical and numerical robust optimal control with techniques from differential geometry, statistical analysis, and machine learning and applications in aerospace systems and robotics.

{IEEEbiography}[

]Dr. Riccardo Bonalli obtained his M.Sc. in Mathematical Engineering from Politecnico di Milano, Italy in 2014 and his Ph.D. in applied mathematics from Sorbonne Universite, France in 2018 in collaboration with ONERA - The French Aerospace Lab, France. He is a recipient of the ONERA DTIS Best Ph.D. Student Award 2018. He was a postdoctoral researcher with the Department of Aeronautics and Astronautics, Stanford University. Currently, Riccardo is a tenured researcher with the Laboratory of Signals and Systems (L2S), Université Paris-Saclay, Centre National de la Recherche Scientifique (CNRS), CentraleSupélec, France. His main research interests concern theoretical and numerical robust optimal control with techniques from differential geometry, statistical analysis, and machine learning and applications in aerospace systems and robotics.

{IEEEbiography}[![[Uncaptioned image]](/html/2101.12086/assets/x3.png) ]Mr. Kevin Smith is a Ph.D. candidate in Environmental and Water Resources Engineering at Tufts University and a product developer at OptiRTC, Inc., where he is responsible for developing flexible real-time systems for the continuous monitoring and adaptive control of stormwater infrastructure. Kevin’s research seeks to understand the opportunities and risks associated with semi-autonomous civil infrastructure, especially when considered as a technology for mediating environmental conflicts. Kevin is a recipient of the US National Science Foundation Integrative Graduate Education and Research Traineeship (IGERT) on Water and Diplomacy. Kevin earned his B.A. in Environmental Studies from Oberlin College and his B.S. in Earth and Environmental Engineering from Columbia University.

{IEEEbiography}[

]Mr. Kevin Smith is a Ph.D. candidate in Environmental and Water Resources Engineering at Tufts University and a product developer at OptiRTC, Inc., where he is responsible for developing flexible real-time systems for the continuous monitoring and adaptive control of stormwater infrastructure. Kevin’s research seeks to understand the opportunities and risks associated with semi-autonomous civil infrastructure, especially when considered as a technology for mediating environmental conflicts. Kevin is a recipient of the US National Science Foundation Integrative Graduate Education and Research Traineeship (IGERT) on Water and Diplomacy. Kevin earned his B.A. in Environmental Studies from Oberlin College and his B.S. in Earth and Environmental Engineering from Columbia University.

{IEEEbiography}[![[Uncaptioned image]](/html/2101.12086/assets/Insoon.jpg) ]Dr. Insoon Yang is an Associate Professor of ECE at Seoul National University. He received a Ph.D. in EECS from UC Berkeley in 2015. He was an Assistant Professor of ECE at University of Southern California from 2016 to 2018, and a Postdoctoral Associate with the Laboratory for Information and Decision Systems at Massachusetts Institute of Technology from 2015 to 2016. His research interests are in stochastic control and optimization, and reinforcement learning. He is a recipient of the 2015 Eli Jury Award and a finalist for the Best Student Paper Award at the 55th IEEE Conference on Decision and Control 2016.

{IEEEbiography}[

]Dr. Insoon Yang is an Associate Professor of ECE at Seoul National University. He received a Ph.D. in EECS from UC Berkeley in 2015. He was an Assistant Professor of ECE at University of Southern California from 2016 to 2018, and a Postdoctoral Associate with the Laboratory for Information and Decision Systems at Massachusetts Institute of Technology from 2015 to 2016. His research interests are in stochastic control and optimization, and reinforcement learning. He is a recipient of the 2015 Eli Jury Award and a finalist for the Best Student Paper Award at the 55th IEEE Conference on Decision and Control 2016.

{IEEEbiography}[![[Uncaptioned image]](/html/2101.12086/assets/x4.png) ]Dr. Marco Pavone is an Associate Professor of Aeronautics and Astronautics at Stanford University, where he is the Director of the Autonomous Systems Laboratory and Co-Director of the Center for Automotive Research at Stanford. He is currently on a partial leave of absence at NVIDIA serving as Director of Autonomous Vehicle Research. His main research interests are in the development of methodologies for the analysis, design, and control of autonomous systems, with an emphasis on self-driving cars, autonomous aerospace vehicles, and future mobility systems. He is a recipient of a Presidential Early Career Award for Scientists and Engineers (PECASE), an Office of Naval Research Young Investigator Award, a National Science Foundation Early Career (CAREER) Award, a NASA Early Career Faculty Award, and an Early-Career Spotlight

Award from the Robotics Science and Systems Foundation.

{IEEEbiography}[

]Dr. Marco Pavone is an Associate Professor of Aeronautics and Astronautics at Stanford University, where he is the Director of the Autonomous Systems Laboratory and Co-Director of the Center for Automotive Research at Stanford. He is currently on a partial leave of absence at NVIDIA serving as Director of Autonomous Vehicle Research. His main research interests are in the development of methodologies for the analysis, design, and control of autonomous systems, with an emphasis on self-driving cars, autonomous aerospace vehicles, and future mobility systems. He is a recipient of a Presidential Early Career Award for Scientists and Engineers (PECASE), an Office of Naval Research Young Investigator Award, a National Science Foundation Early Career (CAREER) Award, a NASA Early Career Faculty Award, and an Early-Career Spotlight

Award from the Robotics Science and Systems Foundation.

{IEEEbiography}[![[Uncaptioned image]](/html/2101.12086/assets/x5.png) ]Dr. Claire Tomlin is the Charles A. Desoer Professor of Engineering in the Department of Electrical Engineering and Computer Sciences (EECS), University of California Berkeley (UC Berkeley). She was an Assistant, Associate, and Full Professor in Aeronautics and Astronautics at Stanford University from 1998 to 2007, and in 2005, she joined UC Berkeley. Claire works in the area of control theory and hybrid systems, with applications to air traffic management, UAV systems, energy, robotics, and systems biology. She is a MacArthur Foundation Fellow (2006), an IEEE Fellow (2010), and in 2017, she was awarded the IEEE Transportation Technologies Award. In 2019, Claire was elected to the National Academy of Engineering and the American Academy of Arts and Sciences.

]Dr. Claire Tomlin is the Charles A. Desoer Professor of Engineering in the Department of Electrical Engineering and Computer Sciences (EECS), University of California Berkeley (UC Berkeley). She was an Assistant, Associate, and Full Professor in Aeronautics and Astronautics at Stanford University from 1998 to 2007, and in 2005, she joined UC Berkeley. Claire works in the area of control theory and hybrid systems, with applications to air traffic management, UAV systems, energy, robotics, and systems biology. She is a MacArthur Foundation Fellow (2006), an IEEE Fellow (2010), and in 2017, she was awarded the IEEE Transportation Technologies Award. In 2019, Claire was elected to the National Academy of Engineering and the American Academy of Arts and Sciences.