Reproducing kernel Hilbert spaces, polynomials and the classical moment problem

Abstract

We show that polynomials do not belong to the reproducing kernel Hilbert space of infinitely differentiable translation-invariant kernels whose spectral measures have moments corresponding to a determinate moment problem. Our proof is based on relating this question to the problem of the best linear estimation in continuous time one-parameter regression models with a stationary error process defined by the kernel. In particular, we show that the existence of a sequence of estimators with variances converging to implies that the regression function cannot be an element of the reproducing kernel Hilbert space. This question is then related to the determinacy of the Hamburger moment problem for the spectral measure corresponding to the kernel.

AMS Subject Classification: 46E22, 62J05, 44A60

Keywords and Phrases: Reproducing kernel Hilbert spaces, classical moment problem, best linear estimation, continuous time regression model

1 Introduction

1.1 Main results

Let , , be a positive definite kernel on and define as the corresponding Reproducing Kernel Hilbert Space (RKHS). We assume that has a non-empty interior and is an infinitely differentiable (on the diagonal) translation-invariant kernel so that , where is a non-constant positive definite function infinitely differentiable at the point . Clearly, the function is even so that for all . Without loss of generality, we suppose .

It is well-known, see e.g. Corollary 4.44 in Steinwart and Christmann, (2008), that in the case of the Gaussian (squared exponential) kernel

| (1.1) |

the constant function does not belong to . This result has been generalized to arbitrary polynomials in Minh, (2010). The purpose of this paper is to significantly extend these results (previously only known for the case of the Gaussian kernel) to a substantially larger class of kernels.

In the main part of the paper, we consider the case . In this case, by Bochner’s theorem (Bochner and Chandrasekharan,, 1949), there exists a measure , such that the function can be represented in the form

| (1.2) |

The measure is called spectral measure. As function is even and , is a probability measure symmetric around the point 0. The moments of this measure (in the case of their existence) will be denoted by . Since we assume in (1.2) is infinitely differentiable and even, we have

| (1.5) |

where .

The classical Hamburger moment problem is to give necessary and sufficient conditions such that a given real sequence is in fact a sequence of moments of a distribution defined on the Borel sets of . In particular, the sequence is a sequence of moments of some distribution if and only if the Hankel matrices are positive semidefinite for all ; see e.g. Shohat and Tamarkin, (1943); Schmüdgen, (2017) among many others. The Hamburger moment problem is called determinate if the sequence of moments determines the measure uniquely.

The main results of this paper are Theorems 1.1 and 1.2 formulated below. These theorems provide sufficient conditions ensuring that the polynomials do not belong to the RKHS . The proofs are given in Section 2.5.

Theorem 1.1

Let and assume that the spectral measure in (1.2) has infinite support and no mass at the point 0. If the Hamburger moment problem for this measure is determinate, then the non-zero constant functions do not belong to the RKHS .

Theorem 1.2

Theorem 1.2 can be considered as a corollary of Theorem 1.1 and therefore the result of Theorem 1.1 is more fundamental. In the very important particular case (see the sufficient condition for moment determinacy (1.3) and related discussion in Section 1.3), when the function is real analytic and vanishes at infinity while is bounded, contains only those analytic functions that vanish at infinity. This is formally proven in Karvonen, (2021) and basically follows from the fact that if then is a point-wise limit of the sums with , which necessarily vanish at infinity.

Combining Theorems 1.1 and 1.2 with their variations in the cases when the spectral measure has finite support (see Section 3.1) and when this measure has positive mass at 0 (see Theorem 3.1), we obtain the following corollary.

Corollary 1.1

Let and the Hamburger moment problem for the spectral measure be determinate. Then we have the following:

-

(a)

the constant functions , , belong to if and only if has a positive mass at the point 0;

-

(b)

if additionally is a real analytic function, then does not contain non-constant polynomials on .

1.2 Implications and related results

Gaussian process (GP) models deal with an unknown deterministic function assuming that it is a realization of Gaussian process (field) with some mean and covariance kernel, which are perhaps parameterized. The popularity of the GP model comes from its transparency, flexibility and computational tractability; it is used as a general-purpose technique to model, explore and exploit unknown functions. As a result, methods based on the GP models constitute much of the modern statistical toolkit for function approximation, interpolation and prediction (Stein,, 1999; Wendland,, 2004), integration (Briol et al.,, 2019), machine learning (Rasmussen and Williams,, 2006; Steinwart and Christmann,, 2008), space-filling (Pronzato and Zhigljavsky,, 2020), signal processing (Cambanis and Masry,, 1983), probabilistic numerics (Hennig et al.,, 2015) and global optimization (Zhigljavsky and Žilinskas,, 2021). The practical application areas of the GP model are vast, and we refer the references in the cited papers and to the work of Schulz et al., (2018), Archetti and Candelieri, (2019) among others.

Consider the common framework of GP regression (simple kriging), where the a function to be approximated () is considered as a realization of a GP, say , with mean zero, covariance

| for all , | (1.6) |

and may be unknown; see Rasmussen and Williams, (2006) for more details. Let the kernel be strictly positive definite, be an -point design consisting of distinct points and be the vector of exact observations of at the points of . The conditional process is again Gaussian with conditional mean

| (1.7) |

and covariance function

| (1.8) |

where and . Straightforward calculation shows that the conditional mean is the best linear predictor of and is the corresponding mean squared prediction error at the point .

GP regression is equivalent to kernel interpolation, see e.g. Scheuerer et al., (2013), Section 3.3 in Kanagawa et al., (2018) and Chapter 3 in Paulsen and Raghupathi, (2016). More precisely, the conditional mean is the minimal-norm interpolant to among all functions in , where we use the norm on denoted below by . This property implies in particular that if then , where this inequality holds for any and any set of points . If then the conditional mean is still an element of but its norm tends to infinity as grows and becomes denser. Therefore, there is a fundamental difference between the complexity of the approximation problem of depending on whether or . Correspondingly, properties of all other techniques based on the use of the GP model also heavily depend on whether an unknown function of interest belongs to the corresponding RKHS. We also refer to the work of Steinwart et al., (2006) and to Section 4.4 in Steinwart and Christmann, (2008) for a discussion on the importance of this issue for the learning performance of support vector machines (SVMs) in the case of the Gaussian kernel (1.1) as well as for the difficulty of deciding whether a given function belongs to the RKHS for a chosen kernel . In GP regression, knowing that the non-zero constant functions do not belong to the RKHS is especially important as it can be used to justify omitting function centering; see, for example, Assumption 2 in Lee et al., (2016).

Assume now that the factor in (1.6) is unknown and that the maximum likelihood estimator (MLE) of is constructed from the observations of the function at the points ; see Section 3.5. If is indeed a realization of the GP with covariance (1.6), it follows by the well-known results on microergodicity (see Chapter 6 in Stein,, 1999) that almost surely (a.s.) as and becomes dense in . Note, however, that such realizations do not belong to a.s. and if then as . This observation is a consequence of the useful relation (see equation (3.4) in Karvonen et al.,, 2020) and the relation , which has already been mentioned. This is in full agreement with Corollary 3.3 below, which states that if and only if (assuming becomes dense in as ). Our numerical studies in Section 5 of this paper show, however, that for finite sample sizes the asymptotic behaviour of has much less effect on uncertainty quantification in GP regression than the smoothness of the function and its flatness at .

The problem of deciding whether a given function belongs to the RKHS for a chosen kernel is well-known in literature, see e.g. Section 3.4 in Paulsen and Raghupathi, (2016). This problem is well-studied in the case of kernels with finite number of derivatives, (Ritter,, 2007; Ritter et al.,, 1995; Karvonen et al.,, 2020). For infinitely differentiable kernels, only the case of Gaussian kernel (1.1) is well-understood; see Minh, (2010) for most advanced results. In a preprint citing the present paper, Karvonen, (2021) gives further new results for analytic translation-invariant kernels with .

1.3 Sufficient conditions for moment determinacy

There are many sufficient conditions for moment determinacy of probability measures, see e.g. Lin, (2017), Schmüdgen, (2017) and Stoyanov, (2013, Chapter 11). The following sufficient condition for moment determinacy of a measure with moments in the Hamburger moment problem, the so-called Carleman condition, is one of the most commonly used:

| (1.9) |

Note that if a probability measure has finite moments for all and satisfies (1.9), then for any the measure of Theorem 1.2 with moments also satisfies (1.9).

Less known than (1.9) is the following sufficient condition for the moment determinacy (in the Hamburger moment problem) of a measure :

see Theorem 30.1 in Billingsley, (2008). This condition is clearly equivalent to the assumption (A.3): the random variable (r.v.) with distribution has moment generating function and, see Theorem 1 in Lin, (2017), to (A.4): this is one of the most known and easiest to verify sufficient conditions for moment determinacy. Theorem 2.13 in Wainwright, (2019) yields that the assumptions (A.2)–(A.4) are also equivalent to the assumption (A.5): the r.v. is sub-exponential. In view of this assumption, the tail behaviour of is a natural indicator of the degree of moment-determinacy of .

The conditions (A.2)–(A.5) are stronger than the Carleman condition (1.9) in the sense that any of them implies (1.9). A technique of constructing measures satisfying the Carleman condition (1.9) but violating , and hence all other assumptions in (A.2)–(A.5), is given in Stoyanov, (2013), Section 11.9.

In view of (1.5) and symmetry of , for all integers This yields that (A.2) coincides with the assumption that is a real analytic function at the point , see Definition 1.1.5 and Corollary 1.1.16 in Krantz and Parks, (2002). Summarizing, if is a real analytic at , then the corresponding spectral measure is moment-determinant in the Hamburger sense. It is not difficult, however, to construct moment-determinant (in the Hamburger sense) spectral measures which do not satisfy (A.2); see Sections 11.9 and 11.10 in Stoyanov, (2013). For such measures, the corresponding functions are symmetric, positive definite and infinitely differentiable but not real analytic at . Nevertheless, for practical purposes the class of functions which are symmetric, positive definite and real analytic can be considered as the main class of functions , for which the corresponding spectral measures are moment determinant in the Hamburger sense. Note also that if the function is real analytic then all functions in have to be analytic too; see Sun and Zhou, (2008).

Let us give four examples of kernels whose spectral measures satisfy the Carleman condition (1.9) and hence assumptions of Theorems 1.1, 1.2 and Corollary 1.1 (we will return to these kernels in Sections 4 and 5). The spectral density corresponding to the spectral measure will be denoted by , so that . In examples (E.1)–(E.4) below, we also provide asymptotic expressions for . In view of (1.9), the rate of divergence of (as ) can also be used to characterize the degree of moment-determinacy of (additionally to the tail behaviour of ).

-

(E.1)

Gaussian kernel: , (), , .

-

(E.2)

Cauchy kernel: , (), , , so that as .

-

(E.3)

The kernel whose spectral density is a symmetric Beta-density:

with and .

Here we have as . -

(E.4)

with ; here the spectral measure is concentrated at with masses yielding , and for all .

1.4 Main steps in the proofs and the structure of the remaining part of the paper

Section 2 is devoted to proving Theorems 1.1 and 1.2; the proofs are given in several steps. The main idea in our approach is to relate the problem of interest to properties of the best linear unbiased estimate (BLUE) in linear regression models, which will be worked out in Sections 2.1 and 2.2. Sections 2.3 and 2.4 provide different characterizations of the moment determinacy of spectral measures and finally the proofs will be completed in Section 2.5. We now explain the different steps in more detail.

In Section 2.1 we consider a one-parameter linear regression model with and a regression function and show that in this case , the BLUE of , exists and its variance is strictly positive, see Lemma 2.1. We also show that in the case , the BLUE does not exist and establish in Lemma 2.2 that for proving , it is sufficient to construct a sequence of linear unbiased estimators of the unknown parameter with variances tending to Such a sequence is constructed in Section 2.2 for the location scale model and an explicit expression for the variance of these estimators in terms of the ratio of determinants

| (1.10) |

of Hankel-type matrices of the moments of the spectral measure is derived in Lemma 2.4. In Section 2.3 we establish several properties of moment-determinant symmetric measures which we use in Section 2.4 for building up an equivalence between the moment determinacy of the spectral measures and the statement that the sequence (1.10) converges to zero. This is arguably the most important step in the proof of both theorems (see Lemma 2.7). Finally, these results are combined in the proofs of Theorem 1.1 and 1.2 in Section 2.5.

In Section 3 we consider several extensions and interpretations of the main results. In Section 3.1 we consider spectral measures with finite support, while Section 3.2 discusses the multivariate case. This discussion is continued in Sections 3.3–3.5, where we also consider general metric spaces. In Section 3.3 we explain a technique of characterizing the inclusion via suitable discretization of the set and show that is the limit of variances of the related discrete BLUEs. These results are used in Section 3.4, where we prove that the constant function belongs to if and only if the spectral measure has positive mass at . In Section 3.5 we show that the problem of parameter estimation in a one-parameter regression model is equivalent to the problem of estimating the variance of a Gaussian process (field). Thus we are able to relate our findings to the estimation problems considered in Xu and Stein, (2017) and Karvonen et al., (2020). In Section 3.6 we return to the one-dimensional case and give an interpretation of Theorem 1.1 in terms of the -error of the best approximation of a constant function by polynomials of the form .

In Section 4, for two specific classes of kernels we derive explicit results on the rates of convergence to of the ratio of determinants (1.10). In the case of Gaussian kernel (1.1), we detail and improve one of the asymptotic expansions of Theorem 3.3 in Xu and Stein, (2017). Finally, in Section 5 we discuss results of a numerical study for uncertainty quantification in GP regression in relation to the theoretical results of this paper.

2 Parameter estimation, moment determinacy and proofs of main results

2.1 BLUE in a one-parameter regression model

Consider a one-parameter regression model with stationary correlated errors:

| , , . | (2.1) |

Here is a scalar parameter, is a given regression function and is an infinitely differentiable positive definite function with making the kernel defined by an infinitely differentiable correlation kernel. For constructing estimators of the parameter , the observations of the process along with observations of all of its derivatives , , can be used.

An estimator for the parameter is called linear, if it is a linear function of the observations (in our case of the process and its derivatives). An unbiased estimator satisfies for all . The best linear unbiased estimator (BLUE) of is defined as an unbiased estimator such that , where is any linear unbiased estimator of . If the kernel is differentiable and the BLUE exists, then for its computation all available derivatives of are used, see Dette et al., (2019). In general, the BLUE may not exist but the next lemma shows that it does exist when .

Lemma 2.1

If , then the BLUE in model (2.1) exists and

The statement of lemma follows from Theorem 6C (p. 975) of Parzen, (1961). Formally, only the case is considered in Parzen, (1961), but Parzen’s proof does not use the structure of and is therefore valid for a general metric space .

Lemma 2.2

If there exists a sequence of linear unbiased estimators of in model (2.1) such that as , then .

Proof. Assume that . By Lemma 2.1, the continuous BLUE exists and var. From the definition of the BLUE,

for all . We have arrived at a contradiction and hence .

2.2 A family of estimators in the location scale model

Consider the location scale model

| (2.2) |

where is an infinitely differentiable at 0 positive definite function. Choose any interior point and set . For construction of the estimator , which we will apply in Lemma 2.2, we use the following observations: the observation at the point and mean-square derivatives of the process at the point :

| (2.3) |

As discussed in Section 1.3, for the main class of kernels of interest, the RKHS is a subset of analytic functions. If we observe everywhere on [0,1], then, since and are analytic, we also know all for all and any integer . Again, because of the analyticity, observing everywhere on is the same as observing for any and any integer . This yields that in practice we do not need to directly observe for constructing estimators of .

The following result provides a necessary and sufficient condition for the existence of the derivatives. For a proof, see page 164 (Section 12) in Yaglom, (1986).

Lemma 2.3

Let be an interior point of . The mean-square derivative of the stationary process in (2.2) at the point exists if and only if , where

| (2.4) |

is the -th moment of the spectral measure corresponding to the kernel in Bochner’s theorem.

As we have assumed that the kernel is infinitely differentiable at 0, all moments () exist. As an immediate consequence of the existence of all moments and the representation (1.2), for the random variables defined in (2.3), we obtain by Lemma 2.3

| (2.5) |

for all Note that all derivatives of odd order vanish as the function is symmetric around the point .

Next, we introduce the random variables , . The observations (2.3) used for constructing the discrete BLUE in model (2.2) can then be rewritten as

Moreover, the covariance matrix of the vector is the Hankel matrix

| (2.6) |

where are the moments defined in (2.4).

Assume that the spectral measure has infinite support. In this case, the matrices are positive definite for all (see, for example, Proposition 3.11 in Schmüdgen,, 2017) and the discrete BLUE is obtained as

| (2.7) |

where and denotes the first coordinate vector in .

Lemma 2.4

Proof. The expression (2.8) follows from the standard formula

for the

variance of the BLUE and Cramér’s rule for computing elements of a matrix inverse; in our case, coincides with the top-left element of the matrix .

Observing Lemma 2.2 we conclude that a non-vanishing constant function does not belong to if In the following sections we relate this condition to the moment determinacy of the spectral measure.

Remark 2.1

Let us briefly consider the case where the spectral measure has a positive mass at the point . Consider the location scale model (2.2) and let

| (2.10) |

denote the spectral measure corresponding to a nonnegative definite and symmetric kernel , where , is the Dirac measure at the point and is a symmetric probability measure on with no mass at 0. The measure is symmetric around the point with even moments and

Recall the definition of the matrix in (2.6) and define the matrices

and the corresponding determinants

where is defined in (2.9). Using standard formulas of linear algebra we obtain

In accordance with (2.8), the variance of , the BLUE of constructed similarly to but for the spectral measure , is given by

This implies that cannot converge to and Lemma 2.2 is not applicable if the spectral measure has a positive mass at the point .

In Theorem 3.1 of Section 3.4 we will prove that for any compact set the constant functions indeed belong to ,

if the spectral measure has a positive mass at the point .

2.3 Moment-determinacy of the spectral measure

Consider the spectral measure introduced in equation (1.2). As a spectral measure, is a symmetric measure (around ) on the real line and we have assumed that does not have a positive mass at the point . Moreover, we have assumed making a probability distribution. In the following we relate to a (unique) measure on the nonnegative axis . Loosely speaking, if a real valued random variable has distribution , then is the distribution of the random variable . In the opposite direction, if the nonnegative random variable has distribution , then has distribution , where denotes a random sign.

For a more formal construction we follow the arguments in Section 3.3 of Schmüdgen, (2017) and denote by the Borel sigma field on , define and , . Then for any symmetric (Radon) measure on , the measure defined by

| (2.11) |

defines a measure on . Conversely, if is a measure on , then

| (2.12) |

defines a symmetric measure on . It now follows from Theorem 3.17 in Schmüdgen, (2017) that the relations (2.11) and (2.12) define a bijection from the set of all symmetric measures on onto the set of all measures on .

The even moments of a symmetric probability measure on are related to the moments of the measure from (2.11) by

| (2.13) |

and as a consequence the determinants and in (2.9) can be represented as

| (2.14) |

Similarly to the case of the Hamburger moment problem, the Stieltjes moment problem is to give necessary and sufficient conditions such that a real sequence is in fact a sequence of moments of a measure on the Borel sets of ; that is for all . The Stieltjes moment problem is determinate if the sequence of moments determines the measure uniquely. For a proof of the following result, which relates the Hamburger and Stieltjes moment problem, see Heyde, (1963, Lemma 1), Schmüdgen, (2017, Proposition 3.19) and Stoyanov, (2013, Sect. 11.10).

Lemma 2.5

Let be a symmetric probability measure on . The Hamburger moment problem for is determinate if and only if the Stieltjes moment problems for the measure defined by (2.11) is determinate.

Note that for the equivalence in Lemma 2.5 to hold, the assumption that does not have mass at is not required. This assumption, however, is needed in the next lemma.

Lemma 2.6

Let be a symmetric probability measure on with no mass at the point . The Hamburger moment problem for is determinate if and only if the Hamburger moment problem for the measure defined by (2.11) is determinate.

Proof. Using the result of Theorem A in Heyde, (1963) (see also (Stoyanov,, 2013, p.113) and (Schmüdgen,, 2017, Remark 2.12)), if the Stieltjes moment problems for the measure is determinate and the measure has no mass at 0, then the Hamburger moment problems for this measure is also determinate. From Lemma 2.5, the required equivalence follows.

2.4 Relating moment-determinacy of the measure to

Lemma 2.7

Proof. (i) Assume that the moment problem for the measure is determinate. Let denote the class of all polynomials of degree and define

for any , which is not a root of the th orthogonal polynomial with respect to the measure (see equation (2.26) in Lemma 2.11 of Shohat and Tamarkin,, 1943). Then

exists, by Theorem 2.6 in Shohat and Tamarkin, (1943). As the point is not a support point of the measure and all roots of the orthogonal polynomials with respect to the measure are located in supp we have from Corollary 2.6 in Shohat and Tamarkin, (1943) that

Moreover, by the discussion on p. 72 (middle of the page) in Shohat and Tamarkin, (1943) it follows that is exactly the ratio , where and are the determinants in (2.14). Hence the moment determinacy for the measure implies as .

(ii) To prove the converse, assume that as . Let be the smallest eigenvalue of the matrix . Theorem 1.1 in Berg et al., (2002) states that the condition

is necessary and sufficient for the moment-determinacy of the measure .

2.5 Proof of Theorem 1.1 and 1.2

Proof of Theorem 1.1.

Use Lemma 2.2 with the estimator defined in (2.7).

By Lemma 2.4 the variance of this estimator is given by (2.8).

From Lemma 2.7, the determinacy of the measure is equivalent to as .

By Lemma 2.5, this is also equivalent to the moment determinacy of the spectral measure .

Proof of Theorem 1.2. Assume that the function in (2.1) is a polynomial of degree . Take derivatives of both sides in (2.1). The model (2.1) thus reduces to , , where is the new parameter, are new observations and is the new error process. From (2.178) in Yaglom, (1986), the autocovariance function of the process is given by

From (1.2), the spectral measure associated with the kernel is

. Hence, the statement for the case when is a polynomial of degree is reduced to the case of the constant function proved in Theorem 1.1; this theorem is applicable as the measure does not have mass at 0 for any .

3 Extensions of Theorems 1.1 and 1.2 and further discussion

In this section we discuss several extensions of the results derived in Sections 1 and 2. In particular, we consider spectral measures with positive mass at the point and extends the results to the multivariate case. Moreover, we briefly indicate a relation of our results to the optimal approximation of a constant function by polynomials with no intercept.

3.1 Spectral measures with finite support

If the spectral measure in (1.2) has finite support, say with and , then the matrices in (2.6) are invertible for but

| (3.1) |

Consequently, observing Lemma 2.4 we have in this case

Therefore, by Lemma 2.2 a non-vanishing constant function does not belong to if the corresponding spectral measure has finite support.

The relation (3.1) follows, observing the representation

where and are the masses of the measure at the points . As is a sum of rank one matrices, it is singular whenever . On the other hand, in the case we have by the Vandermond determinant formula

which shows that is nonsingular. Finally, if we have (in the Loewner ordering)

where the matrix on the right-hand side is positive definite.

3.2 Multivariate case

Consider the location scale model (2.2) but assume that is a subset of with non-empty interior. Extensions of Theorems 1.1 and 1.2 to the multivariate case, when , essentially follow from the one-dimensional results because it is sufficient to use derivatives of the process with respect to one variable for construction of estimators and subsequent application of Lemma 2.2. In the following discussion we consider two cases for the kernel using the notation , and . We also denote by and the vectors and with -th component removed, respectively.

Case 1: Assume that is a product kernel, that is

| (3.2) |

where for all the kernel (defined on a subset of ) satisfies and is a non-constant positive definite function infinitely differentiable at the point . Denote by the spectral measure for and define . To construct the sequence of estimators for the application of Lemma 2.2, we can use the derivatives with respect to the -th coordinate for any . Therefore, Corollary 1.1 can be generalized as follows.

Corollary 3.1

Assume that and the kernel has the form (3.2). Then we have the following:

-

(a)

If the measure has a positive mass at the point , then the constant functions belong to .

-

(b)

If for at least one the Hamburger moment problem for the measure is determinate and the measure does not have a positive mass at the point then any non-vanishing constant function does not belong to .

-

(c)

If for at least one the Hamburger moment problem for the measures is determinate for all , then does not contain non-constant polynomials on .

Note that the set in Corollary 3.1 does not have to be a product of one-dimensional sets. Moreover, we also point out that the assumption (3.2) can be generalized to kernels of the form

where is a positive definite and suitably differentiable kernel on and is a non-constant positive definite function infinitely differentiable at the point .

Case 2: The kernel satisfies

where is a positive definite function on . Consider the spectral measure corresponding to by Bochner‘s theorem, that is

| (3.3) |

and denote by

the th the marginal distribution of the measure (), where denotes the indicator function of the set . In this case, we can generalize Corollary 1.1 as follows.

Corollary 3.2

If the spectral measure does not have a positive mass at the point and if for at least one the Hamburger moment problems for the measures proportional to are determinate for all , then does not contain non-vanishing polynomials.

The case when the spectral measure has positive mass at the point is treated similarly in one-dimensional and multi-dimensional cases, see Section 3.4.

3.3 Discretization of space and the limit of discrete BLUEs

In Section 3.4 below we will prove that constant functions belong to if the spectral measure has positive mass at the point . The proof requires an auxiliary result which is of own interest and shows that in the case the variance of the continuous BLUE is the limit of the variances of discrete BLUEs, after a suitable discretization of has been performed.

Lemma 3.1

Let be a compact in , be a sequence of distinct points in such that and

| (3.4) |

Let be the BLUE of in model (2.1) from the observations of . Then if and only if var as .

Moreover, if , the continuous BLUE of in model (2.1) exists and

Proof.

Let , denote the restriction of on , and define as the RKHS corresponding to the kernel .

By Theorem 6 in Section 1.4.2 of Berlinet and Thomas-Agnan, (2011) we have for , the restriction of on , that and

Consequently, the sequence of (var is monotonously decreasing so that

the limit exists for any . Moreover, for all .

If we have by Proposition 3.9 in Paulsen and Raghupathi, (2016) that

Conversely, if var as for some , we can use

the equivalence between (1) and (2) in Theorem 3.11 of Paulsen and Raghupathi, (2016) to deduce that .

Recall that the explicit expression for the variance of the discrete BLUE of Lemma 3.1 is given by

| (3.5) |

where

| (3.6) |

Since the kernel is assumed to be strictly positive definite, the matrix is invertible for all

3.4 Spectral measures with positive mass at the point

In this section, we investigate the case, where the spectral measure has a positive mass at the point in more detail. In particular, we show that in this case the constant functions belong to . To be precise, assume that the covariance kernel of the error process has the form

| (3.7) |

where and is a strictly positive definite kernel on a compact set . Note that in the particular case and with having the spectral measure , we obtain the representation (2.10) for the spectral measure .

Theorem 3.1

Let be a compact set and assume the kernel has the form (3.7) with . Then then the constant functions belong to .

Proof. Consider the location scale model

| (3.8) |

and let denote a sequence of distinct points in such that (3.4) is satisfied. Let be the BLUE of in the model (3.8), constructed on the observations of Define , and . As the covariance kernel is strictly positive definite, the matrix is invertible for all , . Therefore, the BLUE is unique and given by

Its variance is

For simplicity of notation, denote . The same arguments as given in the proof of Lemma 3.1 show that for any , the sequence is monotonously increasing with some limit . Observing the representation

(for all and ), we have

This implies

and therefore it follows that

| (3.9) |

3.5 Estimation of the variance of a Gaussian random field

Let be a compact set, and let denote of a Gaussian random process (field) on with a strictly positive definite covariance kernel on , where the kernel is known but is unknown. For estimating we assume that one can observe at distinct points . Then it is easy to deduce (see, for example, p.140 in Xu and Stein, (2017)) that the corresponding log-likelihood function is

| (3.10) |

where and are defined by (3.6). Moreover, a simple calculation shows that the maximum likelihood estimator (MLE) of is given by

| (3.11) |

Comparing (3.11) with (3.5) we get

| (3.12) |

and by Lemma 3.1 we obtain the following corollary.

Corollary 3.3

Let be a compact set in , a strictly positive definite kernel on and a function on . If is a sequence of distinct points in satisfying (3.4) and is the MLE of constructed from the observations under the assumption that is a realization of a GP with zero mean and covariance (1.6), then if and only if

3.6 Best polynomial approximation

Let denote the space of square integrable functions with respect to the measure on the real line and define to be the space of of polynomials of degree . For we consider the -distance

between the constant function and the even polynomial of degree with no intercept. A well know result in approximation theory (see, for example, Achieser,, 1956, p. 15-16) shows that

| (3.13) |

where are the (even) moments of the spectral measure defined in (2.4) and the last equality is a consequence of Lemma 2.4.

From this representation it follows that as if and only if non-zero constant functions can be approximated by polynomials of the form with arbitrary small error. Moreover, for any polynomial on , we have

where the measure is defined by (2.11), and . From Corollary 2.3.3 in Akhiezer, (1965), it therefore follows that the set of all polynomials is dense in the space if the measure on is the (unique) solution of a determinate Hamburger moment problem. As the function belongs to we thus obtain from (3.13) another proof of the fact that if has no mass at and is moment-determinate in the Hamburger sense then . Note that this is almost equivalent to the ‘if’ statement in the important Lemma 2.7.

4 Rates of convergence

In this section, we derive for several specific classes of correlation kernels explicit results on the rate of convergence of the ratio , see (2.8), where and are the determinants defined in (2.9).

4.1 Gaussian kernel

We first consider the case of the Gaussian kernel with and . Assuming for simplicity , we obtain that the spectral measure is absolute continuous with density

The moments of even order of the measure are given by

where From (1.9), the corresponding Hamburger moment problem is determinate and therefore non-vanishing constant functions (and all polynomials) do not belong to the corresponding RKHS. We now investigate the variance of the discrete BLUE defined in (2.7), which is given by the ratio of the determinants and .

It follows from results in Lau and Studden, (1988) that the determinant of the Hankel matrix defined in (2.9) has the representation

| (4.1) |

where are the coefficients of the three-term recurrence relation

| (4.2) |

of the monic orthogonal polynomials with respect to measure (, , ). Observing the three-term recurrence relation

for the Laguerre polynomials (orthogonal with respect to ) we can identify the coefficients in (4.2). More precisely, the monic polynomials

satisfy a three-term recurrence relation of the form (4.2) with , see Dette and Studden, (1992), Lemma 2.2 (b). As we have and therefore obtain

| (4.3) |

Now we move on to the determinant Note that we have

for , where and the density is defined by , . Therefore,

where , . Consequently,

and it follows

Since

we obtain

| (4.4) |

The expansion (4.4) details the asymptotic relation formulated as Theorem 3.3 in Xu and Stein, (2017) in the case . Note that formula (4.4) also corrects a minor mistake in this reference, which gives as the leading term.

4.2 Spectral measure with Beta distribution

For measures with a compact support the determinants and can be conveniently evaluated using the theory of canonical moments, see e.g. Dette and Studden, (1997). Exemplarily, we consider the symmetric Beta distribution on the interval with density

| (4.5) |

where and denotes the Beta-function. For later purposes we also introduce the Beta distribution on the interval with density

| (4.6) |

where the . The canonical moments of the Beta-distribution with density (4.6) are given by

| (4.7) |

see e.g. formula (1.3.11) in Dette and Studden, (1997). It is easy to see that the distribution on the interval related to the distribution in (4.5) by the transformation (2.11) is a Beta () distribution. Therefore, it follows from (4.7) that the corresponding canonical moments are given by

| (4.8) |

Now Theorem 1.4.10 in Dette and Studden, (1997) gives

| (4.9) |

where and (observing (4.8))

| (4.10) |

For the calculation of the determinant we note the relation

| (4.11) |

where are the moments of the Beta() distribution. Consequently, we obtain from Theorem 1.4.10 in Dette and Studden, (1997) that

| (4.12) | |||||

where are the canonical moments of Beta distribution, that is

and

| (4.13) |

we obtain

| (4.14) | |||||

where the expansion in the last line follows by straightforward but tedious calculation using Stirling’s formula.

We finally mention the special cases (the spectral measure is a uniform spectral density on the interval with corresponding kernel function ) and (the spectral measure is the arcsine distribution on and the corresponding kernel is , where is the Bessel function of the first kind) for which the expansions are given, respectively, by

| (4.15) | |||||

as Interestingly, the ratio in (4.15) is the squared ratio of (4.4).

5 Some results of numerical studies and discussions

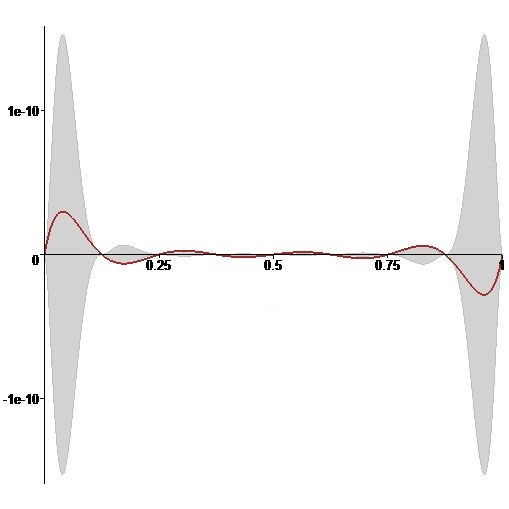

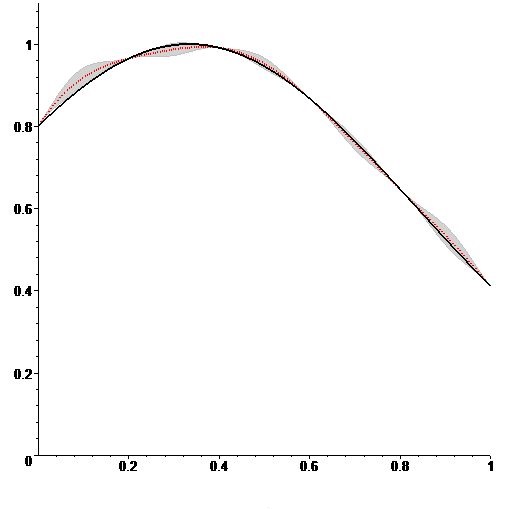

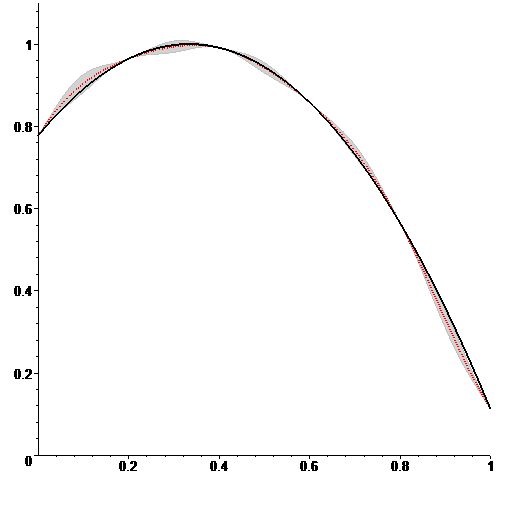

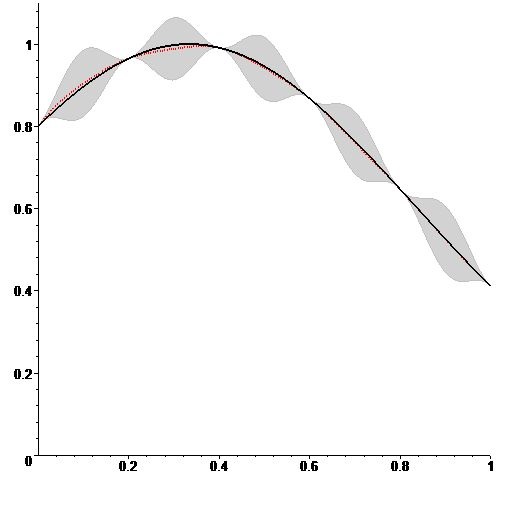

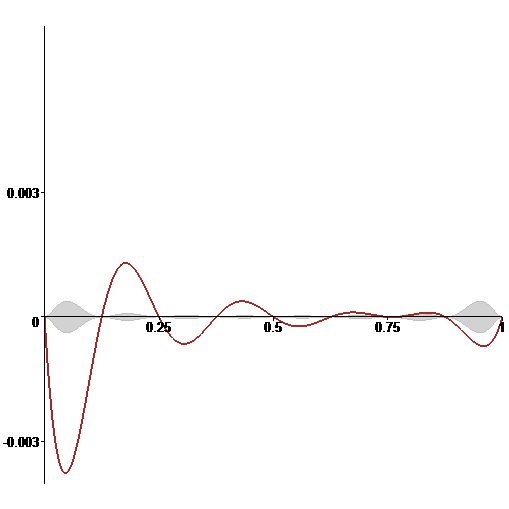

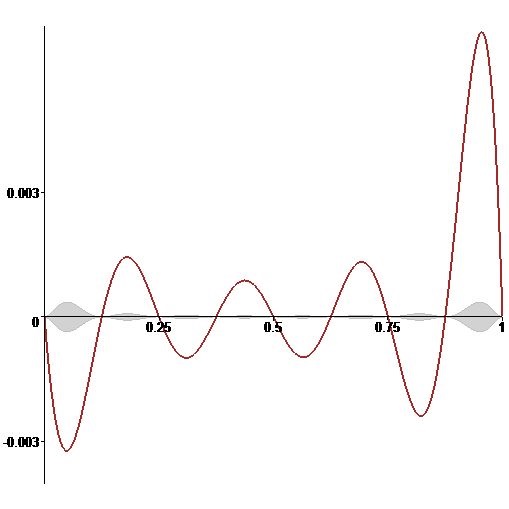

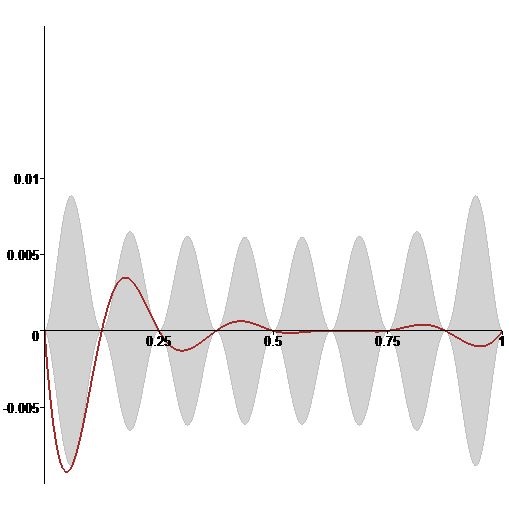

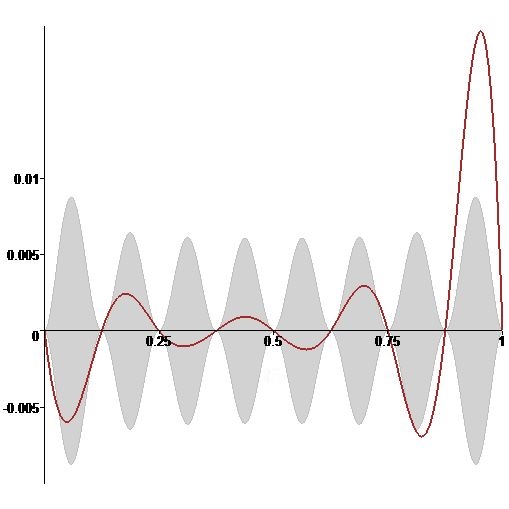

We have made extensive numerical studies to assess the uncertainty quantification in GP regression, as introduced in Section 1.2 for functions and ; some of our results are illustrated in the figures below. At the end of this section, we summarize our conclusions. Different kernels (including Matérn kernels and the kernels discussed at the end of Section 1.3) have been investigated as well. In the figures below, we use , Gaussian and Cauchy kernels (see (E.1) and (E.2) at the end of Section 1.3) and the two functions

These two functions look similar but we note that and for both kernels with the correlation lengths considered below. Visually, the chosen kernels also look similar but it turns out that they exhibit completely different behaviour.

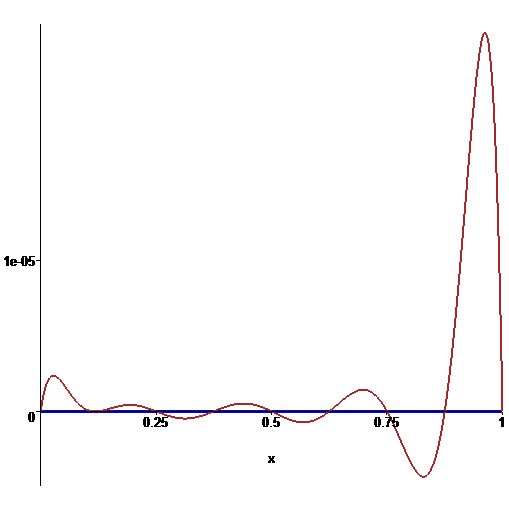

In Figs. 1 and 2 we plot either or in solid black, the kernel approximation computed by (1.7) in dotted red and the so-called kriging confidence regions in grey, where is the kernel variance computed by (1.8) and is the MLE of computed by (3.11). The main reason for providing Figs. 1 and 2 is the demonstration of the big difference in the width of the confidence regions for the Gaussian and Cauchy kernels. In Figs. 3, 4 and 5, we plot the deviation in brown and confidence bounds in filled grey. Again, the left and right panels show the results for the functions and , respectively. The points , where observations of are taken, are equally spaced on the interval with , .

The results for the Gaussian kernel are depicted on Figs. 1 and 3. The corresponding results for the Cauchy kernel can be found Figs. 2 and 4. It is clear from comparing left and right panels in Figs. 1–4 that kernel approximations for are significantly more accurate than for . The two chosen kernels (Gaussian with and Cauchy with ) look very similar but have different tail behaviour of the corresponding spectral density: the tail of the spectral density of the Cauchy kernel has a heavier tail. The confidence regions for the regression function constructed by the Cauchy kernel are rather wide and resemble the regions for the Matérn kernels with shape parameters 3/2 and 5/2 having similar correlation lengths. The confidence regions in the case of Gaussian kernel are much narrower (in fact, far too narrow) and the confidence regions for the kernels in (E.3) and (E.4) of Section 1.3 are even narrower; the spectral measures for these kernels have finite support.

In Figure 5 we plot the deviations and confidence regions for kernel approximation with Gaussian kernel ; the Gaussian kernel with is perfectly suited for function . A naive visual inspection of the two functions might suggest the Gaussian kernel should also work well for but, as we can observe from Figure 5 (right), it is not so for . The confidence region on Figure 5 (right) cannot be seen as the deviations are on average times larger than .

From the numerical studies partially illustrated in these figures we make the following conclusions concerning uncertainty quantification in GP regression models with infinitely differentiable translation-invariant kernels:

-

•

if , then the kriging confidence regions for are always inaccurate;

-

•

the heavier are the tails of the spectral measure of the kernel, the wider are the confidence regions;

-

•

if the tail of the spectral measure of the kernel is light and the function does not belong to the respective RKHS, then the kernel approximation of appears to be rather inaccurate and the confidence regions seem to be missing almost entirely;

-

•

if the function does not belong to the respective RKHS, then as , but this has little effect on the size of the confidence intervals, at least for small ;

-

•

for kernels with light tails of the respective spectral measures, the kernel approximation is accurate and confidence regions are adequate only if the shape of precisely matches the shape of the kernel functions , as in Figure 5 (left).

Acknowledgements This research was partially supported by the research grant DFG DE 502/27-1 of the German Research Foundation (DFG). The authors are grateful to Timo Karvonen (Alan Turing Institute) for intelligent discussions, spotting an essential typo and pointing out several important references. We would also like to thank both referees and especially the associate editor for their constructive and very valuable comments on earlier versions of this paper.

References

- Achieser, (1956) Achieser, N. I. (1956). Theory of Approximation. Frederick Ungar Publishing Co., N.Y.

- Akhiezer, (1965) Akhiezer, N. (1965). The Classical Moment Problem and Some Related Questions in Analysis. Oliver & Boyd.

- Archetti and Candelieri, (2019) Archetti, F. and Candelieri, A. (2019). Bayesian Optimization and Data Science. Springer.

- Berg et al., (2002) Berg, C., Chen, Y., and Ismail, M. E. (2002). Small eigenvalues of large Hankel matrices: The indeterminate case. Mathematica Scandinavica, 90:67–81.

- Berlinet and Thomas-Agnan, (2011) Berlinet, A. and Thomas-Agnan, C. (2011). Reproducing Kernel Hilbert Spaces in Probability and Statistics. Springer.

- Billingsley, (2008) Billingsley, P. (2008). Probability and Measure. John Wiley & Sons, forth edition.

- Bochner and Chandrasekharan, (1949) Bochner, S. and Chandrasekharan, K. (1949). Fourier Transforms. (AM-19). University Press, Princeton, N.J.

- Briol et al., (2019) Briol, F.-X., Oates, C., Girolami, M., Osborne, M., and Sejdinovic, D. (2019). Probabilistic integration: A role in statistical computation? Statistical Science, 34(1):1–22.

- Cambanis and Masry, (1983) Cambanis, S. and Masry, E. (1983). Sampling designs for the detection of signals in noise. IEEE Transactions on Information Theory, 29(1):83–104.

- Dette et al., (2019) Dette, H., Pepelyshev, A., and Zhigljavsky, A. (2019). The BLUE in continuous-time regression models with correlated errors. Annals of Statistics, 47(4):1928–1959.

- Dette and Studden, (1992) Dette, H. and Studden, W. (1992). On a new characterization of the classical orthogonal polynomials. Journal of Approximation Theory, 71(1):3–17.

- Dette and Studden, (1997) Dette, H. and Studden, W. (1997). The Theory of Canonical Moments with Applications in Statistics, Probability and Analysis. John Wiley & Sons.

- Hennig et al., (2015) Hennig, P., Osborne, M., and Girolami, M. (2015). Probabilistic numerics and uncertainty in computations. Proceedings of the Royal Society A: Mathematical, Physical and Engineering Sciences, 471(2179):20150142.

- Heyde, (1963) Heyde, C. (1963). Some remarks on the moment problem (i). The Quarterly Journal of Mathematics, 14(1):91–96.

- Kanagawa et al., (2018) Kanagawa, M., Hennig, P., Sejdinovic, D., and Sriperumbudur, B. (2018). Gaussian processes and kernel methods: A review on connections and equivalences. arxiv e-prints, art. arXiv preprint arXiv:1807.02582.

- Karvonen, (2021) Karvonen, T. (2021). On non-inclusion of certain functions in reproducing kernel Hilbert spaces. arXiv preprint arXiv:2102.10628.

- Karvonen et al., (2020) Karvonen, T., Wynne, G., Tronarp, F., Oates, C., and Särkkä, S. (2020). Maximum likelihood estimation and uncertainty quantification for Gaussian process approximation of deterministic functions. SIAM/ASA J. on Uncertainty Quantification, 8(3):926–958.

- Krantz and Parks, (2002) Krantz, S. and Parks, H. (2002). A Primer of Real Analytic Functions. Springer.

- Lau and Studden, (1988) Lau, T.-S. and Studden, W. (1988). On an extremal problem of Fejér. Journal of Approximation Theory, 53(2):184–194.

- Lee et al., (2016) Lee, K.-Y., Li, B., and Zhao, H. (2016). Variable selection via additive conditional independence. Journal of the Royal Statistical Society B, 78(5):1037–1055.

- Lin, (2017) Lin, G. D. (2017). Recent developments on the moment problem. Journal of Statistical Distributions and Applications, 4(1):1–17.

- Minh, (2010) Minh, H. Q. (2010). Some properties of Gaussian reproducing kernel Hilbert spaces and their implications for function approximation and learning theory. Constructive Approximation, 32(2):307–338.

- Parzen, (1961) Parzen, E. (1961). An approach to time series analysis. The Annals of Mathematical Statistics, 32(4):951–989.

- Paulsen and Raghupathi, (2016) Paulsen, V. and Raghupathi, M. (2016). An Introduction to the Theory of Reproducing Kernel Hilbert Spaces. Cambridge university press.

- Pronzato and Zhigljavsky, (2020) Pronzato, L. and Zhigljavsky, A. (2020). Bayesian quadrature, energy minimization, and space-filling design. SIAM/ASA Journal on Uncertainty Quantification, 8(3):959–1011.

- Rasmussen and Williams, (2006) Rasmussen, C. and Williams, C. (2006). Gaussian Processes for Machine Learning. MIT Press.

- Ritter, (2007) Ritter, K. (2007). Average-Case Analysis of Numerical Problems. Springer.

- Ritter et al., (1995) Ritter, K., Wasilkowski, G., and Woźniakowski, H. (1995). Multivariate integration and approximation for random fields satisfying Sacks-Ylvisaker conditions. The Annals of Applied Probability, 5(2):518–540.

- Scheuerer et al., (2013) Scheuerer, M., Schaback, R., and Schlather, M. (2013). Interpolation of spatial data–a stochastic or a deterministic problem? European Journal of Applied Mathematics, 24(04):601–629.

- Schmüdgen, (2017) Schmüdgen, K. (2017). The Moment Problem. Springer.

- Schulz et al., (2018) Schulz, E., Speekenbrink, M., and Krause, A. (2018). A tutorial on Gaussian process regression: Modelling, exploring, and exploiting functions. Journal of Mathematical Psychology, 85:1–16.

- Shohat and Tamarkin, (1943) Shohat, J. and Tamarkin, J. (1943). The Problem of Moments. American Math. Soc.

- Stein, (1999) Stein, M. L. (1999). Interpolation of Spatial Data: Some Theory for Kriging. Springer.

- Steinwart and Christmann, (2008) Steinwart, I. and Christmann, A. (2008). Support Vector Machines. Springer.

- Steinwart et al., (2006) Steinwart, I., Hush, D., and Scovel, C. (2006). An explicit description of the reproducing kernel Hilbert spaces of Gaussian RBF kernels. IEEE Trans. on Inform. Theory, 52(10):4635–4643.

- Stoyanov, (2013) Stoyanov, J. M. (2013). Counterexamples in Probability. Courier Corporation.

- Sun and Zhou, (2008) Sun, H.-W. and Zhou, D.-X. (2008). Reproducing kernel Hilbert spaces associated with analytic translation-invariant Mercer kernels. Journal of Fourier Analysis and Applications, 14(1):89–101.

- Wainwright, (2019) Wainwright, M. (2019). High-dimensional statistics: A non-asymptotic viewpoint. Cambridge University Press.

- Wendland, (2004) Wendland, H. (2004). Scattered Data Approximation. Cambridge university press.

- Xu and Stein, (2017) Xu, W. and Stein, M. L. (2017). Maximum likelihood estimation for a smooth Gaussian random field model. SIAM/ASA Journal on Uncertainty Quantification, 5(1):138–175.

- Yaglom, (1986) Yaglom, A. (1986). Correlation Theory of Stationary and Related Random Functions. Volume I: Basic Results. Springer.

- Zhigljavsky and Žilinskas, (2021) Zhigljavsky, A. and Žilinskas, A. (2021). Bayesian and High-Dimensional Global Optimization. Springer.