ARGONNE NATIONAL LABORATORY

9700 South Cass Avenue

Argonne, Illinois 60439

Convergence Analysis of Fixed Point Chance Constrained Optimal Power Flow Problems

J. J. Brust, M. Anitescu

Mathematics and Computer Science Division

Preprint ANL/MCS-P9431-0121

January 2022

The submitted manuscript has been created by UChicago Argonne, LLC, Operator of Argonne National Laboratory (“Argonne”). Argonne, a U.S. Department of Energy Office of Science laboratory, is operated under Contract No. DE-AC02-06CH11357. The U.S. Government retains for itself, and others acting on its behalf, a paid-up nonexclusive, irrevocable worldwide license in said article to reproduce, prepare derivative works, distribute copies to the public, and perform publicly and display publicly, by or on behalf of the Government. The Department of Energy will provide public access to these results of federally sponsored research in accordance with the DOE Public Access Plan. http://energy.gov/downloads/doe-public-accessplan

Convergence Analysis of Fixed Point Chance Constrained Optimal Power Flow Problems

Abstract

For optimal power flow problems with chance constraints, a particularly effective method is based on a fixed point iteration applied to a sequence of deterministic power flow problems. However, a priori, the convergence of such an approach is not necessarily guaranteed. This article analyses the convergence conditions for this fixed point approach, and reports numerical experiments including for large IEEE networks.

Index Terms:

Fixed point method, Chance Constraints, Stochastic Optimizations, AC Optimal Power FlowI Introduction

Chance constrained optimization problems are often computationally very challenging. However, when modeling the effects of uncertainty on optimal power networks, potentially large chance constrained optimization problems arise [1, 2, 3, 4, 5]. Typically, stochastic optimal power flow models are developed by reformulating a widely accepted deterministic model. One such “classical” model is the AC optimal power flow model (AC-OPF) [6]. Because AC-OPF has multiple degrees of freedom with respect to the problem variables, various stochastic power flow paradigms can be derived from it. In particular, one can define different subsets of variables as stochastic variables. For instance, in [7] power generation is regarded as being stochastic (with constant demands), resulting in probabilistic objective functions. This article develops a chance constrained AC optimal power flow model (CC-AC-OPF) in which the objective function is deterministic, and the demands can be stochastic. This enables direct interpretation of the meaning of the optimal objective function values, and can be more realistic, when in practice demand is more of an uncertainty source as compared to supply. Yet, independent of how the stochastic power flow model is formulated it typically yields a chance constrained optimization problem. In order to also solve large instances of the resulting CC-AC-OPF problems, a fixed point iteration on a sequence of modified, related, and simpler deterministic AC-OPF problems is solved. Iterative methods that solve a sequence of simpler problems have been very effective on a variety of recent power systems problems [8, 9, 10]. In the context of chance-constrained optimization, such an approach has been successfully used in [11, 12, 13] among more. However, prior to this work, there did not exist analytical criteria for when one can expect this fixed point iteration to converge. Therefore, this article describes a convergence analysis of the chance constrained fixed point iteration and tests the method on a set of standard IEEE networks. The numerical experiments report results for networks with up to 9000 nodes. To summarize, the contributions of this work are: (1) The formulation of a new CC-AC-OPF model with a deterministic objective function, derived from uncertain demands; (2) The application and analysis of a fixed-point algorithm for an implicit chance constrained problem. Even though the use of iterative (fixed-point) techniques is widespread in power systems problems, previously no rigorous analysis had been undertaken for this formulation. In particular, we disentangle effects of model parameters and network properties on the convergence; (3) We include numerical experiments on large test cases. The article is organized as follows: Sections I.A—D are preliminary and review the AC optimal power flow model and how a chance-constrained model is obtained from it. Section II lists the fixed-point algorithm. We highlight that the reformulation and iterative solution of chance-constrained AC-OPF has been proposed in [11], however a rigorous analysis of its convergence has not yet been developed. Therefore, Section III analyzes convergence properties of the fixed-point algorithm, while numerical experiments are described in Section IV. Finally, we conclude with Section V.

I-A AC Power Flow (Preliminary)

The power network is defined by nodes (buses) and edges (lines). Associated to each bus is a voltage magnitude, , frequency and power generation or consumption at the bus, for . In particular, let be the real power generated at bus , the corresponding reactive power and , the real and reactive demands, respectively. The buses are furthermore divided into two groups: generators and loads. The indexing sets are , and , which are related to the set of all buses by (also ). Throughout, we will use the indexing sets as subscripts to bold font vector variables. Note that in our setup each bus fits exactly into one of the two categories (though one can easily set a virtual zero load at a node). It is customary to assume that the network contains one reference bus (typically at ). Load buses do not have active power generation and are thus defined by , where are vectors that contain the ’s and ’s. The power flow in the system is described by the power flow equations, which couple the variables (e.g., [6, Sections III-IV]). Specifically, let denote the entries of the network’s admittance matrix and define the quantities , and . With these definitions, the power flow equations, for , are

| (1) | ||||

when grouped by busses. If we let be the vector containing then in vector notation (1) is expressed as , where represents the nonlinear equations in (1). Note, however, that is linear in , a fact we will use later. Moreover, is regarded as a parameter and not a variable.

I-B AC Optimal Power Flow (Preliminary)

Optimal power flow determines the best set of variables that satisfy the network constraints. In addition to the power flow equations from (1), branch current bounds are typically included in the optimization problem. In particular, let be the set of all line connections, i.e., the set of index pairs that describe all line connections (e.g., if bus is connected to bus , then ). Subsequently, the so-called branch current constraints are , for constant current limits . In vector notation these constraints are represented as . It is also desirable to include “hard” bounds on the generation variables, such as , where , represent constant lower and upper bounds. The AC optimal power flow (AC-OPF) problem, for a cost function , is thus formulated as

| (2) | ||||

| (3) | ||||

The cost function is typically a convex quadratic function that only depends on the real power generation. Specifically, for cost data and . A local solution of (2) is called the optimal power flow point, or OPF point.

I-C Chance Constrained AC Optimal Power Flow (Preliminary)

In order to introduce uncertainty related to e.g., renewable energy into the OPF problem (2) we regard the demand terms in (1) (i.e., ) as forecasted values with possible error. Specifically, these stochastic quantities are represented as

| (4) |

where and represent forecasting errors. For compactness, the stochastic errors are represented by the vector . Here we assume is normal, and relaxing this assumption yields different approaches. The chance constrained AC-OPF model in this Section is developed such that the objective function only depends on deterministic variables. When the objective function represents cost, deterministic values are meaningful and important. Since the power flow equations in (1) are overdetermined, i.e., , this system has degrees of freedom. Subsequently, let represent a vector of deterministic variables and a vector of stochastic variables. The stochastic power flow equations are represented as

| (5) |

If these equations reduce to the power flow equations in (1). Note that the power flow equations couple the variables and that the uncertainty in depends on the uncertainty in the demands “”, since . We set to reflect the change in variables for the stochastic optimal power flow problem and note that the objective function is deterministic. Let represent a vector of inequalities with non-negative probability constraints, for which each element in the left hand side corresponds to a cumulative probability (for ) and each element of is in the interval . Then the chance constrained (stochastic) optimal power flow problem is given by

| subject to | (6) | ||||

| (7) | |||||

| (8) | |||||

Observe that the problem in (6) includes chance constraints (probability constraints) on the line flow limits (7) and the stochastic variables (8), while deterministic limits are set on . Here and correspond to model parameters for setting probability thresholds.

I-C1 Computing Chance Constraints

To practically compute the chance constraints in problem (6), the stochastic variables are linearized around the error (zero mean). This is equivalent to assuming that is sufficiently small, which we proceed to do in the rest of the paper. In particular,

| (9) |

Note that and that are deterministic. Thus the expectation and variance of are , and , respectively. Alternatively, more accurate dynamics of the stochastic variables may be based on a order expansion . When the covariance of the uncertainty has a particular structure (e.g., diagonal) then the mean of the expansion can be determined analytically. The expansion’s covariance is more involved and may need to be estimated. Another possibility to include nonlinearities might be a quadratic model of the load: , where .* and are element-wise multiplications and squares. For computational efficiency we use the probabilities of the linearized random variables. For instance, the constraints from (8) are written as

| (10) |

To handle the vector of probabilities in (10) one can use a Bonferroni bound [14], in which each individual variable for satisfies an individual highly conservative probability constraint. However, when the variables are independent (or can be treated as such) then the probabilities can be separated without restrictions. The mean of is , while the variance can also be explicitly computed. Define

| (11) |

and let be the r column of the identity matrix. Moreover, denote . With this the variance of is . In turn, when the variables can be treated independently, individual probability constraints, such as (where is the normal distribution function) can be represented as

where is the inverse cumulative distribution function. Defining the constraints are represented as

| (12) |

Similarly, for and , defining the remaining probability constraints are represented as with

| (13) |

Note that depend on and , e.g., , which we will use later. Moreover the inequality in (12) is deterministic and thus straightforward to compute once is known. Second, when is a small number (which is typically the case) then and . Thus the values are regarded as constraint tightenings and represent the effects of stochasticity in the constraints. Note that when other distributions are desired, one can substitute the c.d.f. (above (12) and elsewhere) with another one. Since investigations about distributional robustness have been previously conducted by other researchers we refer to [15, Sec. III.A] for in-depth discussions.

I-C2 Computing

The partial derivatives in (12) are obtained by using the power flow equation

First, note from (5) that . Second, the partial derivatives are only needed at , which yields the representation with the convention . Since the so-called Jacobian matrix of partial derivatives is given by

| (14) |

The elements of this matrix can be computed from (1). Note that only the last equations in (1) depend on . Subsequently, we define the indices and , as well as , and . With this, the elements of the Jacobian from (14) are:

| (15) | ||||

The partial derivatives are defined by an inverse. This inverse is typically well defined for regular optimal power flow problems, as described in [7, Section III. B] and [16] (if numerically the Jacobian matrix becomes (nearly) singular, it may be corrected by shifting its diagonal elements by adding a multiple of the identity matrix). Therefore, the smallest singular value of is positive, i.e., . A positive lower bound for the smallest singular value of a matrix is described in [17, Theorem 1]. Let denote the column of and let be the row of . Then a lower bound for the smallest singular value is:

where , and where the determinant is . This means that

| (16) |

where are finite constants. In order to compute solves with (which is part of computing the constraints in (12) and (13)) the LU factorization is based on the decomposition , where is a permutation matrix, is a unit lower triangular matrix and is an upper triangular matrix. The determinant and the bounds in (16) are thus available “without extra expense” based on solves with , by multiplying the diagonal elements of , since and is upper triangular. Since the determinant can often become large (even if a matrix is well conditioned) a possibly preferable approach of computing constant is to exploit the inequality . Note that computing can be inexpensive since is computed as part of e.g., (12).

I-D Implicit Chance Constrained Optimal Power Flow

An optimal power flow problem that combines components of the AC-OPF problem in (2) and of the chance constrained problem in (6) is obtained by using the constraints from (12) and (13). This reformulated problem incorporates stochastic effects, while at the same time enables efficient computations. The corresponding implicit chance-constrained AC-OPF problem is:

| (17) | ||||

where are computed using (12) and is computed using (13). The problem can be seen to be implicit with regards to probability constraints, because the effects of uncertainty are implicitly included in the tightenings of some constraints by the non-negative ’s.

II Method

The solution of the potentially large nonlinear optimization problem in (17) can be computed directly. However, the computation of the ’s adds nonlinearities, because they depend on the matrix , which is an inverse. Because of this, the problem in (17) is still computationally difficult. Instead of solving (17) directly, an iterative scheme, which computes an approximate solution of (17), by solving a sequence of simpler problems has been proposed in [11]. Such an algorithm is stated as:

Algorithm 1 1: Inputs: , , , , , , , , , ; 2: for 3: Solve (17) with ,, fixed and obtain ; 4: Compute ,,, using (12) and (13); 5: if then 6: Stop. Return ; 7: else 8: ; 9: end if

Note that Algorithm 1 stops when the changes in the ’s become small. However no criteria have yet been specified for when one can expect the iteration to converge. Therefore, we analyze conditions for which one can expect Algorithm 1 to converge.

III Analysis

The analysis of Algorithm 1 is based on the insight that this iterative algorithm is a fixed point iteration. Therefore, in order to derive its convergence conditions, we investigate the convergence conditions of the fixed point iteration. Throughout this section, the problem from (17) is reformulated as

| (18) | ||||

with , , , ( inequality constraints in (17)) and . Our analysis is consistent with classical nonlinear programming sensitivity results [18, 19], however is different because of the fixed point component of the algorithm. In classical nonlinear programming is taken as an independent perturbation parameter, with focus on the sensitivities of with respect to . However, because the (implicit) chance-constrained problem also contains the dependence we are led to also acknowledge the interplay of and . Recall that a fixed point, say , of a continuous function/mapping, say , can be defined by the two conditions

| (19) |

(see for instance [20, Sec. 10.1] and [21, Sec. 6.3] on fixed points.) These two conditions are generalizations of a scalar fixed-point (FP) to vector valued functions. Condition 1 represents the definition of a FP, which is a point that remains unchanged after being mapped. Condition 2 is a sufficient condition for a fixed point mapping to converge [20, Theorem 10.6]). This condition implies that recursive mappings of a fixed-point are characterized by vanishing derivatives (successively applying the mapping results in a stable point, which make such mapping be sometimes called a contraction [20, Theorem 10.6]). Note that Algorithm 1 in line 5 checks whether the differences in successive constraint tightenings are small, i.e., this is a numerical check of Condition 1. We further analyze properties of Condition 2 to obtain insights into the convergence behavior of the algorithm. Now, to closer investigate the relation between the variables in Algorithm 1, define the mapping in line 3 that determines from by (i.e., ), and the operation in line 4 that determines from by (i.e., ). Then the statements in the algorithm recursively define the next iterates, starting from , , , so that,

This means that there is a mapping that generates from and one that generates from . In particular, if then and vice-versa. Our analysis is based on the assertion that if Condition 2 in (19) holds, then (and ) is a fixed point.

First, we describe the basic properties of a solution to (18), which enables the use of results from nonlinear programming later on, and also the establishing of reasonable assumptions.

III-A Basic Conditions

A solution to the nonlinear programming problem (18) is characterized by a set of conditions for the Lagrangian:

where and . Subsequently, the Karush-Kuhn-Tucker (KKT) [22, 23] optimality conditions are the set of nonlinear conditions that define a solution of (18):

| (20) | ||||

The set of active inequality constraints is defined as

A solution to (III-A) can be found when the columns of the constraint Jacobians are linearly independent, i.e., when

| (21) |

are linearly independent. Moreover, second order conditions (which state that the Lagrangian Hessian is positive definite in the nullspace of the constraint derivatives) ensure strict local optimality of a KKT point. Finally, if the active set is unchanged in a small neighborhood around , then changes in with regards to changes in are continuous. Summarizing we assume the three conditions. Assumptions (Analysis):

| A.1: | Linear independence in the constraint Jacobians (21) |

|---|---|

| A.2: | Second order sufficient conditions hold for (18) |

| A.3: | Strict complementary slackness: . |

The first two assumptions state that a local minimum for the problem in (18) exists. The third ensures continuity of derivatives, such as and . We further assume access to a solver that can find a local minimum when it exists. Because of the continuity of partial derivatives the active set at a (local) solution does not change. A numerical investigation of a zig-zag behavior of Algorithm 1 due to a disconnected feasible set can be found in [15]. Note that when changes in the constraint tightenings are not abrupt, but smooth, assuming continuity is reasonable. We like to note that [15, Sec. V.A] empirically observed that in cases where tightenings are small (relative to other terms) the algorithm converged more frequently on linear programs.

III-B Analysis Outline

A goal of the analysis is to deduce properties of the quantity (in order to investigate when Condition 2 in (19) will hold). To achieve this first a representation of is needed, which is derived in Part I. Subsequently, the representation of depends on changes in variables and constraints that are developed as the sensitivities and in Part II. Ultimately, Part III uses the previous outcomes to deduce and implications. (We use the notation to denote the element of )

| Part I: | Representation of |

|---|---|

| Part II: | Sensitivities and |

| Part III: | Bound on and Implications |

To develop a representation for we analyze the expression

which is (12) with explicit dependencies on and . (The conditions for (13) are done in a similar way, with an additional constant for the derivatives of the line flow constraints: ).

III-C Part I: Representation of

In this section we first make the relation between and explicit. Thus the matrix is represented as a function of and i.e., where (cf. (14)). For notation, we will be using the following definition

| (22) |

and write Because Condition 2 in (19) involves partial derivatives, we take the partial derivative with respect to (the ‘th’ tightening), so that denoting in the right hand side. This expression provides a basis for what the matrix of partial derivatives will look like. For indices the elements of the matrix of sensitivities with respect to the vector is

| (23) |

Note that since is a row vector and is a column vector the entries in (23) can be written as

| (24) |

where represents the angle between and . Since therefore the elements of the matrix in (23) are

From (22) it holds that , which yields the subsequent inequalities

| (25) |

Note that and are constants, with upper bounds and . Therefore, a bound for fully specifies (25), and thus the elements of .

III-D Part II: Sensitivities and

In order to derive a bound on , recall that . Therefore, note that we can make use of the identity

Specifically, defining the vector then

| (26) |

With a bound on (from (16)), it remains to derive an upper bound on . Next we describe the essential components for such a bound, based on the elements of the derivative matrices

The elements of can be computed from (15) once

| (27) |

for , are known. This is the case, because and , for , (in e.g., (15)) can be computed from these quantities. In order to develop expressions for the derivatives in (27) we use the vector variable (from (18)), which contain elements and . Subsequently results from classical nonlinear programming theory, based on assumptions A.1 — A.3, ensure the existence of a parametrized solution to (18) with dependence on , defined by

Selecting a set of rows in extracts and thus also and . The derivative of w.r.t. can be computed from the KKT conditions

| (28) |

From (28) it holds that

and . Thus is obtained by extracting elements from . The existence of the inverse and hence the derivatives of are guaranteed by [18, Theorem 3.2]. Because the derivatives are finite a bound of the form exists, which implies , and , . Having deduced bounds on the sensitivities and now the partial derivatives of can be analyzed. Specifically, the partial derivatives of are computed from (15) from which . Since the power flow equations hold with equality at a solution, we simplify the summations in (15), using the definitions , as e.g., (and correspondingly for the other terms). Then for and as well as and

These derivatives can be bounded with limits on , and (i.e., all elements that appear in the expression of the derivatives). Since all these individual elements are bounded by , and since the terms are bounded, too (they depend on ), the maximum element will be bounded by a constant, as well. Denote this constant by , then

With this, since and , we obtain the upper bound

| (29) |

III-E Part III: Bound on and Implications

The analysis from the previous section has implications for the convergence of Algorithm 1. In particular, since (cf. Section I-C2) a bound on the magnitude of can be found. By combining (25) and (29) one sees that

where the second inequality is based on (26) and the third on (29). Since typically only inequality constraints are active at the solution, and since the upper bound is

| (30) |

If the right hand side in (30) is less than one then Condition 2 in (19) of the fixed point iteration is guaranteed to hold. In other words

| (31) |

III-F Computing a Bound Estimate

The upper bound in (30) is composed of the parts

The quantities and are related to the uncertainty in the model, whereas is problem (network specification) dependent. For instance, is reduced by reducing the probability constraints in (6). Concretely, if all then . Secondly, if is small enough (sufficiently small uncertainty) then from (19) the fixed point iteration is guaranteed to converge. Although the bounds may be known to be conservative, we show that if the uncertainty is small enough convergence is achieved. Such an insight may be useful if the uncertainty can be scaled (e.g., using shorter model horizons) so that its magnitude becomes smaller. Such conclusions apply to basically any type of Algorithm 1 as long as is used in forming . Finally, the bound (30) includes the network dimension . In numerical experiments, we observe that setting enables the solution of large networks. Before applying Algorithm 1 for multiple iterations the bound in (30) can be qualitatively used to asses the convergence behavior of the method. In particular, at , use to compute parts of the right hand side in (30). Computing is available from or (or a LU factorization of ). The computation of can be approximated by first estimating from a lower bound on the smallest singular value of using [17] (as for (16)), calling such an estimate . Because appears linearly in the inequalities (for appropriately defined ) and in no other constraints, the expression simplifies. Subsequently, and , for a constant . Because the estimate for may be reasonably small near a solution, and because would incur extra computational expenses we set its value to . If the computed bound, say exceeds a fixed threshold (say ), set . Moreover, we include a scaling factor in computing the line flow constraint tightenings from (13), thus . Note that for no scaling is included. An overview of the constants is summarized in a table. Furthermore, the quantity captures specific problem sensitivities to relevant factors such as magnitude of and number of active constraints. This quantity can be computed at the beginning of applying Algorithm 1, is often inexpensive, and is expected to be small for guaranteed convergence.

| Constant | Meaning | Computation |

|---|---|---|

| Distribution bound () | ||

| Magnitude inv. power flow Jac. | or eq. (16) | |

| Magnitude of power flow Jac. deriv. w.r.t | ||

| Number of active inequality constraints (w/o deter. vars) |

(w/o constraints on ) |

|

| Problem sensitivity to inv. Jac. and active constraints |

(If is not known it can be bounded by )

IV Numerical Experiments

This section describes numerical experiments on a set of standard IEEE test problems. Typically, solving large chance-constrained optimization problems is numerically very challenging. Even directly solving the reformulated problem in (17) with state-of-the-art general purpose methods becomes quickly intractable. Therefore, for larger networks we apply Algorithm 1 to approximately solve (17). Our implementation of Algorithm 1 uses Julia 1.1.0 [24] and the modeling libraries JuMP v0.18.6 [25] and StructJuMP [26]. In particular, in order to solve the AC-OPF problem from (2) and its modifications in Line 3 of Algorithm 1 we use the general purpose nonlinear optimization solver IPOPT [27]. The stopping criteria in Algorithm 1 are set as , , , . Unless otherwise stated, we set , and , and . The initial values are computed as the midpoint between the upper and lower bounds . The maximum number of iterations for Algorithm 1 is set as 50. The test cases are summarized in Table II:

| Problem | Reference | ||

|---|---|---|---|

| IEEE 9 | [6] | ||

| IEEE 30 | [6, 28] | ||

| IEEE 118 | [6] | ||

| IEEE 300 | [6] | ||

| IEEE 1354pegase | [29] | ||

| IEEE 2383wp | [6] | ||

| IEEE 2869pegase | [29] | ||

| IEEE 9241pegase | [29] |

The numerical experiments are divided into three parts. Experiment I compares solutions to (17) using a direct solver (i.e., IPOPT) or the iterative approach from Algorithm 1. Experiment II reports results on the test problems from Table II. Experiment III describes convergence tests according to our analysis, outcomes for problems with perturbed loads and an investigation of joint and disjoint relative frequencies on the IEEE 9 problem.

IV-A Experiment I

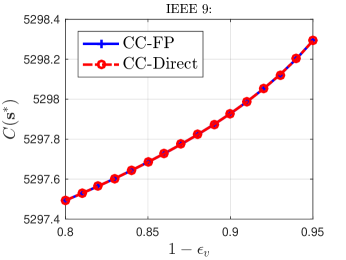

This experiment compares the optimal objective function values of solving (17) directly (CC-Direct) using IPOPT or using Algorithm 1 with a fixed point approach (CC-FP). Solving (17) in JuMP becomes computationally intractable beyond , because the inverse, , and its derivatives are continuously recomputed. For this reason, we compare CC-Direct and CC-FP for the 9 bus and 30 bus cases (which are both tractable by the direct approach). For the purpose of this comparison we switched the line flow tightening off (i.e., ) while all other tightenings are applied. In particular, we compare the solved objective function values after perturbing the problem formulation slightly. Specifically, we compare the computed objective function values when the values change the probability constraints. (Varying other parameters yields similar results). The outcomes of the 9 bus network are in Figure 1.

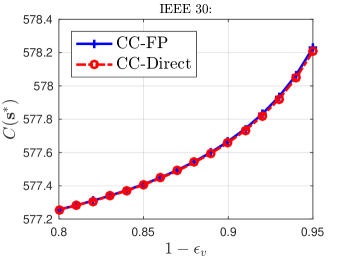

Figure 2 contains the outcomes of applying both approaches on the 30 bus network.

Observe in both figures that the optimal objective function values, i.e., , increase as the values of increase. This is because larger values of correspond to stricter chance constraints. Importantly, observe that the objective function values are virtually equivalent for these test cases, as the values of the blue and red curves nearly exactly match up. However, the main advantage of Algorithm 1 is that it scales to larger cases, too.

IV-B Experiment II

Experiment II reports results of applying Algorithm 1 (CC-FP) and a direct solver (CC-Direct) to the problem from (17) on the test problems in Table II. For CC-FP the number of iterations, time and “optimal” objective values are reported. For CC-Direct the “optimal” objective values and the time are reported. Algorithm 1 converged on all of the reported problems. These problems include large network instances, too. Observe in Table III that for problems on which both solvers can be used, the optimal objective function values are close to each other. However, for large problems only Algorithm 1, based on a fixed point iteration, is practical. For consistency with Figs. 1 and 2 the line flow tightenings are switched off in the first two cases, while all tightenings are applied on all other problems.

| IEEE | CC-FP | CC-Direct | |||

|---|---|---|---|---|---|

| Its. | Obj. (Cost/h) | Time(s) | Obj. (Cost/h) | Time(s) | |

| 4 | 5297.928 | 0.0504 | 5297.928 | 0.3075 | |

| 4 | 577.6665 | 0.1688 | 577.6592 | 148.36 | |

| 3 | 129662.0 | 0.4710 | >5h | ||

| 5 | 720090.3 | 4.3123 | >5h | ||

| 3 | 74069.38 | 75.039 | >5h | ||

| 3 | 1868551. | 236.27 | >5h | ||

| 3 | 133999.3 | 316.80 | >5h | ||

| 3 | 315912.6 | 3255.2 | >5h | ||

IV-C Experiment III

In this experiment we investigate three further important aspects of the analysis and the algorithm. Before proceeding, we note that in Algorithm 1 it can happen that the constraint tightenings become large enough that adjusted upper bound constraints fall below a lower bound constraint (or vice-versa). Since this situation implies an inconsistent constraint, we restore consistency by re-setting this particular constraint to its original, yet with a scaled feasible interval (to reflect some tightening). Use of this correction mechanism increases the robustness of the method, meaning that Algorithm 1 converges more often. Nevertheless, our analysis indicates that a sufficiently small value of will guarantee convergence. However, other network dependent factors such as or (number of active constraints) are also relevant for convergence on specific problems. We capture the conclusion that a sufficiently small guarantees convergence, and that relatively large values of and typically result in non-convergence using all test problems from Table II.

IV-C1 Experiment III.A

This experiment varies the default value as with . For a sufficiently small value of (here ) all problems are guaranteed to converge. Moreover, lower values of and represent lower sensitivity of a problem to increases in . Table IV reports the outcomes on all test problems. This table contains explicit values for all parameters from Table III. Thus the bound estimate from (30) can be computed. Particularly, note that when all the bounds are (cf. the row labeled Cond. 30). Moreover, when all problems with bound estimate converged (i.e., IEEE {9,118,1354,2869,9241}). This is consistent with (III-E). Since Condition 2 in (19) is sufficient and our analysis develops an upper bound, networks with bound estimate larger than 1 many also converge. However, when the upper bound is less than 1 then convergence of Algorithm 1 is implied. Additionally, problems IEEE have the smallest values indicating their tolerance to larger values. Problem IEEE has the largest value and is viewed as being more sensitive to non-convergence. Ultimately all problems are non-convergent. Prior to this IEEE tend to converge on more instances while these networks have the smallest values.

| IEEE | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| 0.012 | 0.12 | 1.2e+02 | 1.2e+04 | 1.2e+06 | ||||||

| 0.063 | 0.63 | 6.3e+02 | 6.3e+04 | 6.3e+06 | ||||||

| Conv. | N | N | ||||||||

| Cond. 30 | 0.0072 | 0.072 | 72 | 7.2e+03 | 7.2e+05 | |||||

| 0.0011 | 0.011 | 11 | 1.1e+03 | 1.1e+05 | ||||||

| 0.08 | 0.8 | 8e+02 | 8e+04 | 8e+06 | ||||||

| Conv. | N | N | N | N | ||||||

| Cond. 30 | 0.62 | 6.2 | 6.2e+03 | 6.2e+05 | 6.2e+07 | |||||

| 7.2e-05 | 0.00072 | 0.72 | 72 | 7.2e+03 | ||||||

| 0.045 | 0.45 | 4.5e+02 | 4.5e+04 | 4.5e+06 | ||||||

| Conv. | N | N | N | |||||||

| Cond. 30 | 0.069 | 0.69 | 6.9e+02 | 6.9e+04 | 6.9e+06 | |||||

| 1.1e-05 | 0.00011 | 0.11 | 11 | 1.1e+03 | ||||||

| 0.19 | 1.9 | 1.9e+03 | 1.9e+05 | 1.9e+07 | ||||||

| Conv. | N | N | N | N | ||||||

| Cond. 30 | 0.73 | 7.3 | 7.3e+03 | 7.3e+05 | 7.3e+07 | |||||

| 5.5e-07 | 5.5e-06 | 0.0055 | 0.55 | 55 | ||||||

| 0.0013 | 0.013 | 13 | 1.3e+03 | 1.3e+05 | ||||||

| Conv. | N | |||||||||

| Cond. 30 | 0.089 | 0.89 | 8.9e+02 | 8.9e+04 | 8.9e+06 | |||||

| 1.8e-07 | 1.8e-06 | 0.0018 | 0.18 | 18 | ||||||

| 0.092 | 0.92 | 9.2e+02 | 9.2e+04 | 9.2e+06 | ||||||

| Conv. | N | N | ||||||||

| Cond. 30 | 0.56 | 5.6 | 5.6e+03 | 5.6e+05 | 5.6e+07 | |||||

| 1.2e-07 | 1.2e-06 | 0.0012 | 0.12 | 12 | ||||||

| 0.00078 | 0.0078 | 7.8 | 7.8e+02 | 7.8e+04 | ||||||

| Conv. | N | |||||||||

| Cond. 30 | 0.057 | 0.57 | 5.7e+02 | 5.7e+04 | 5.7e+06 | |||||

| 1.2e-08 | 1.2e-07 | 0.00012 | 0.012 | 1.2 | ||||||

| 0.002 | 0.02 | 20 | 2e+03 | 2e+05 | ||||||

| Conv. | N | N | ||||||||

| Cond. 30 | 0.093 | 0.93 | 9.3e+02 | 9.3e+04 | 9.3e+06 | |||||

IV-C2 Experiment III.B

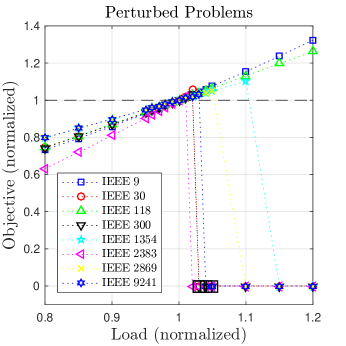

This experiment investigates outcomes on all test problems when loads are perturbed (representing stressed system conditions). In particular, the algorithm is applied to all problems with loads varying between — of their original values. Figure 3 displays the outcomes in which optimal objective values relative to the original optimal value are compared. Overall, the optimal objective values exhibit a linear relation with changes in the loads.

IV-C3 Experiment III.C

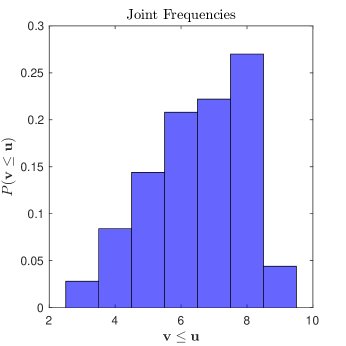

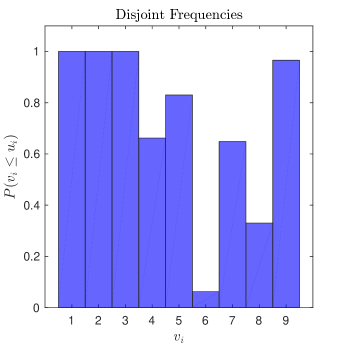

This experiment investigates the relation of joint and individual (disjoint) probabilities. For the IEEE 9 bus case, we sample 500 multivariate random vectors with zero mean and positive definite dense covariance. The voltage constraints on generator buses (for this 9 bus case i.e., 1,2 and 3) are deterministic . The voltages at the remaining load buses are unbounded. The problem is re-solved after random loads and are simulated. The joint relative frequencies of the vector constraint (the constant vector has elements ) are displayed on the top of Figure 4. The individual relative frequencies for each bus are at the bottom of the figure.

V Conclusion

We briefly summarize limitations and future work of the analysis before concluding.

V-A Limitations

Recall that Condition 2 in (19) is a sufficient condition for convergence of a fixed point iteration (such as Algorithm 1). This means that even when the condition does not hold the algorithm may still converge. In particular, when the upper bound in (30) exceeds one the algorithm may still converge. However, when (30) is less than one and assumptions A.1–A.3 from Sec. III.A are satisfied then convergence is guaranteed by the fixed point theorem. Moreover, the components of (30) are computed using upper bounds or estimates as described in Table II and may thus be conservative.

V-B Future Work

Since the analysis is general, it applies basically to all fixed point algorithms which iteratively re-solve power optimization problems parameterized by a sequence of constraint tightenings, . Therefore, in future work one can apply the analysis to the convergence of fixed point approaches for variations such as Robust AC Optimal Power flows, High Voltage Direct Current lines or similar problems. The decomposition of the upper bound in (30) is already detailed. Yet, new work can tighten this upper bound with sharped estimates for the constants, and particularly the constant .

In sum, this article describes a chance constrained AC optimal power flow model with only deterministic variables in the objective, which thus enables immediate interpretation of the optimal function values. By linearizing the stochastic variables, a deterministic nonlinear optimization problem is obtained in lieu of the probabilistic one. Because solving the reformulated optimization problem is computationally challenging, we develop and analyze the convergence criteria for a fixed point algorithm that solves a sequence of modified AC optimal power flow problems and scales to larger network sizes. The analysis connects the variance of uncertainty and constraint probabilities to the convergence properties of the algorithm. In numerical experiments, we compare the fixed point iteration to directly solving the reformulated problem and test the method on IEEE problems, including a network with over 9000 nodes. Certainly our bounds are quite conservative in this version, however this is the first attempt at proving convergence of the approach. This opens up future work, since iteratively resolving a sequence of tractable optimization problems (by holding specific nonlinear terms fixed) has been very effective on a variety of power systems applications.

Acknowledgments

This work was supported by the U.S. Department of Energy, Office of Science, Advanced Scientific Computing Research, under Contract DE-AC02-06CH11357 at Argonne National Laboratory and by NSF through award CNS-51545046. We acknowledge fruitful discussion with Dr. Line Roald, who pointed out that Algorithm 1 was observed to cycle between different points, and encouraged an analysis of its convergence criteria. We also thank Eric Grimm, who helped in carrying out parts of the numerical experiments in Section IV. Careful reading and helpful suggestions of the editor and three anonymous reviewers markedly improved the manuscript.

References

- [1] H. Zhang and P. Li, “Chance constrained programming for optimal power flow under uncertainty,” IEEE Transactions on Power Systems, vol. 26, no. 4, pp. 2417–2424, Nov 2011.

- [2] G. Li and X. P. Zhang, “Stochastic optimal power flow approach considering correlated probabilistic load and wind farm generation,” in IET Conference on Reliability of Transmission and Distribution Networks (RTDN 2011), Nov 2011, pp. 1–7.

- [3] M. Hojjat and M. H. Javidi, “Chance-constrained programming approach to stochastic congestion management considering system uncertainties,” IET Generation, Transmission Distribution, vol. 9, no. 12, pp. 1421–1429, 2015.

- [4] K. Baker, E. Dall’Anese, and T. Summers, “Distribution-agnostic stochastic optimal power flow for distribution grids,” in 2016 North American Power Symposium (NAPS), Sep. 2016, pp. 1–6.

- [5] M. Vrakopoulou, M. Katsampani, K. Margellos, J. Lygeros, and G. Andersson, “Probabilistic security-constrained ac optimal power flow,” in 2013 IEEE Grenoble Conference, June 2013, pp. 1–6.

- [6] R. D. Zimmerman, C. E. Murillo-Sánchez, and R. J. Thomas, “Matpower: Steady-state operations, planning, and analysis tools for power systems research and education,” IEEE Transactions on Power Systems, vol. 26, no. 1, pp. 12–19, Feb 2011.

- [7] M. Lubin, Y. Dvorkin, and L. Roald, “Chance constraints for improving the security of ac optimal power flow,” IEEE Transactions on Power Systems, vol. 34, no. 3, pp. 1908–1917, 2019.

- [8] D. Bienstock, M. Chertkov, and S. Harnett, “Chance-constrained optimal power flow: Risk-aware network control under uncertainty,” Siam Review, vol. 56, no. 3, pp. 461–495, 2014.

- [9] D. Lee, K. Turitsyn, D. K. Molzahn, and L. A. Roald, “Feasible path identification in optimal power flow with sequential convex restriction,” IEEE Transactions on Power Systems, vol. 35, no. 5, pp. 3648–3659, 2020.

- [10] V. Frolov, L. Roald, and M. Chertkov, “Cloud-ac-opf: Model reduction technique for multi-scenario optimal power flow via chance-constrained optimization,” in 2019 IEEE Milan PowerTech, 2019, pp. 1–6.

- [11] L. Roald and G. Andersson, “Chance-constrained ac optimal power flow: Reformulations and efficient algorithms,” IEEE Transactions on Power Systems, vol. 33, no. 3, pp. 2906–2918, May 2018.

- [12] J. Schmidli, L. Roald, S. Chatzivasileiadis, and G. Andersson, “Stochastic ac optimal power flow with approximate chance-constraints,” in 2016 IEEE Power and Energy Society General Meeting (PESGM), July 2016, pp. 1–5.

- [13] Y. Xu, M. Korkali, L. Mili, J. Valinejad, T. Chen, and X. Chen, “An iterative response-surface-based approach for chance-constrained ac optimal power flow considering dependent uncertainty,” IEEE Transactions on Smart Grid, vol. 12, no. 3, pp. 2696–2707, 2021.

- [14] R. G. J. Miller, Simultaneous Statistical Inference. Springer-Verlag New York, 1981.

- [15] A. Roald, D. Molzahn, and A. F. Tobler, “Power system optimization with uncertainty and ac power flow: Analysis of an iterative algorithm,” in 10th IREP Symp. Bulk Power Syst. Dynamics Control., 2017.

- [16] D. Bienstock, Electrical Transmission System Cascades and Vulnerability. Philadelphia, PA: Society for Industrial and Applied Mathematics, 2015. [Online]. Available: https://epubs.siam.org/doi/abs/10.1137/1.9781611974164

- [17] Y. Hong and C.-T. Pan, “A lower bound for the smallest singular value,” Linear Algebra and its Applications, vol. 172, pp. 27 – 32, 1992. [Online]. Available: http://www.sciencedirect.com/science/article/pii/0024379592900164

- [18] A. V. Fiacco and J. Kyparisis, “Sensitivity analysis in nonlinear programming under second order assumptions,” in Systems and Optimization, A. Bagchi and H. T. Jongen, Eds. Berlin, Heidelberg: Springer Berlin Heidelberg, 1985, pp. 74–97.

- [19] A. V. Fiacco, “Nonlinear programming sensitivity analysis results using strong second order assumptions,” in Numerical Optimization of Dynamic Systems, L. C. W. Dixon and e. G. P. Szegö, Eds. North-Holland, Amsterdam: Springer Berlin Heidelberg, 1980, pp. 327–348.

- [20] R. Burden and J. Faires, Numerical Analysis. Cengage Learning, 2010. [Online]. Available: https://books.google.com/books?id=zXnSxY9G2JgC

- [21] S. H. Strogatz, Nonlinear Dynamics and Chaos: With Applications to Physics, Biology, Chemistry, and Engineering. Addison-Wesley, 1994.

- [22] W. Karush, “Minima of functions of several variables with inequalities as side conditions,” Master’s thesis, Department of Mathematics, University of Chicago, Illinois, USA, 1939.

- [23] H. W. Kuhn and A. W. Tucker, “Nonlinear programming,” in Proceedings of the Second Berkeley Symposium on Mathematical Statistics and Probability. Berkeley, Calif.: University of California Press, 1951, pp. 481–492. [Online]. Available: https://projecteuclid.org/euclid.bsmsp/1200500249

- [24] J. Bezanson, A. Edelman, S. Karpinski, and V. B. Shah, “Julia: A fresh approach to numerical computing,” SIAM review, vol. 59, no. 1, pp. 65–98, 2017. [Online]. Available: https://doi.org/10.1137/141000671

- [25] I. Dunning, J. Huchette, and M. Lubin, “Jump: A modeling language for mathematical optimization,” SIAM Review, vol. 59, no. 2, pp. 295–320, 2017.

- [26] M. Anitescu and G. C. Petra, “StructJuMP a block-structured optimization framework for jump,” https://github.com/StructJuMP/StructJuMP.jl (retrieved Mar. 27th, 2019), 2019.

- [27] A. Wächter and L. T. Biegler, “On the implementation of an interior-point filter line-search algorithm for large-scale nonlinear programming,” Math. Program., vol. 106, pp. 25–57, 2006.

- [28] O. Alsac and B. Stott, “Optimal load flow with steady-state security,” IEEE Transactions on Power Apparatus and Systems, vol. PAS-93, no. 3, pp. 745–751, May 1974.

- [29] S. Fliscounakis, P. Panciatici, F. Capitanescu, and L. Wehenkel, “Contingency ranking with respect to overloads in very large power systems taking into account uncertainty, preventive, and corrective actions,” IEEE Transactions on Power Systems, vol. 28, no. 4, pp. 4909–4917, Nov 2013.

![[Uncaptioned image]](/html/2101.11740/assets/johannesbrust_pic.jpg) |

Johannes J. Brust Was with the Mathematics and Computer Science Division at Argonne National Laboratory, IL (now Department of Mathematics, University of California, San Diego). He received a M.Sc. in financial engineering from Maastricht University and a Ph.D. in applied mathematics from the University of California, Merced. His research is on effective large scale computational methods applied to optimal power flow problems. |

![[Uncaptioned image]](/html/2101.11740/assets/mihai_pic.jpg) |

Mihai Anitescu Is a senior computational mathematician in the Mathematics and Computer Science Division at Argonne National Laboratory and a professor in the Department of Statistics at the University of Chicago. He obtained his engineer diploma (electrical engineering) from the Polytechnic University of Bucharest in 1992 and his Ph.D. in applied mathematical and computational sciences from the University of Iowa in 1997. He specializes in the areas of numerical optimization, computational science, numerical analysis and uncertainty quantification in which he has published more than 100 papers in scholarly journals and book chapters. He is on the editorial board of the SIAM Journal on Optimization and he is a senior editor for Optimization Methods and Software, he is a past member of the editorial boards of the Mathematical Programming A and B, SIAM Journal on Uncertainty Quantification, and SIAM Journal on Scientific Computing. He has been recognized for his work in applied mathematics by his selection as a SIAM Fellow in 2019. |

The submitted manuscript has been created by UChicago Argonne, LLC, Operator of Argonne National Laboratory (“Argonne”). Argonne, a U.S. Department of Energy Office of Science laboratory, is operated under Contract No. DE-AC02-06CH11357. The U.S. Government retains for itself, and others acting on its behalf, a paid-up nonexclusive, irrevocable worldwide license in said article to reproduce, prepare derivative works, distribute copies to the public, and perform publicly and display publicly, by or on behalf of the Government. The Department of Energy will provide public access to these results of federally sponsored research in accordance with the DOE Public Access Plan. http://energy.gov/downloads/doe-public-accessplan