printacmref=false \affiliation \institutionBrown University \cityProvidence, RI \affiliation \institutionBrown University \cityProvidence, RI \affiliation \institutionBrown University \cityProvidence, RI

Learning Competitive Equilibria in Noisy Combinatorial Markets

Abstract.

We present a methodology to robustly estimate the competitive equilibria (CE) of combinatorial markets under the assumption that buyers do not know their precise valuations for bundles of goods, but instead can only provide noisy estimates. We first show tight lower- and upper-bounds on the buyers’ utility loss, and hence the set of CE, given a uniform approximation of one market by another. We then develop a learning framework for our setup, and present two probably-approximately-correct algorithms for learning CE, i.e., producing uniform approximations that preserve CE, with finite-sample guarantees. The first is a baseline that uses Hoeffding’s inequality to produce a uniform approximation of buyers’ valuations with high probability. The second leverages a connection between the first welfare theorem of economics and uniform approximations to adaptively prune value queries when it determines that they are provably not part of a CE. We experiment with our algorithms and find that the pruning algorithm achieves better estimates than the baseline with far fewer samples.

Key words and phrases:

Competitive Equilibria Learning, Noisy Combinatorial Markets, PAC Algorithms for Combinatorial Marketsnone

1. Introduction

Combinatorial Markets (CMs) are a class of markets in which buyers are interested in acquiring bundles of goods, and their values for these bundles can be arbitrary. Real-world examples of CMs include: spectrum auctions Cramton et al. (2002) allocation of landing and take-off slots at airports Ball et al. (2006); internet ad placement Edelman et al. (2007); and procurement of bus routes Cantillon and Pesendorfer (2006). An outcome of a CM is an assignment of bundles to buyers together with prices for the goods. A competitive equilibrium (CE) is an outcome of particular interest in CMs and other well-studied economic models Bikhchandani and Mamer (1997); Walras (2003). In a CE, buyers are utility-maximizing (i.e., they maximize their utilities among all feasible allocations at the posted prices) and the seller maximizes its revenue (again, over all allocations at the posted prices).

While CEs are a static equilibrium concept, they can sometimes arise as the outcome of a dynamic price adjustment process (e.g., Cheung et al. (2020)). In such a process, prices might be adjusted by an imaginary Walrasian auctioneer, who poses demand queries to buyers: i.e., asks them their demands at given prices. Similarly, we imagine that prices in a CM are set by a market maker, who poses value queries to buyers: i.e., asks them their values on select bundles.

One of the defining features of CMs is that they afford buyers the flexibility to express complex preferences, which in turn has the potential to increase market efficiency. However, the extensive expressivity of these markets presents challenges for both the market maker and the buyers. With an exponential number of bundles in general, it is infeasible for a buyer to evaluate them all. We thus present a model of noisy buyer valuations: e.g., buyers might use approximate or heuristic methods to obtain value estimates Fujishima et al. (1999). In turn, the market maker chooses an outcome in the face of uncertainty about the buyers’ valuations. We call the objects of study in this work noisy combinatorial markets (NCM) to emphasize that buyers do not have direct access to their values for bundles, but instead can only noisily estimate them.

In this work, we formulate a mathematical model of NCMs. Our goal is then to design learning algorithms with rigorous finite-sample guarantees that approximate the competitive equilibria of NCMs. Our first result is to show tight lower- and upper-bounds on the set of CE, given uniform approximations of buyers’ valuations. We then present two learning algorithms. The first one—Elicitation Algorithm; —serves as a baseline. It uses Hoeffding’s inequality Hoeffding (1994) to produce said uniform approximations. Our second algorithm—Elicitation Algorithm with Pruning; —leverages the first welfare theorem of economics to adaptively prune value queries when it determines that they are provably not part of a CE.

After establishing the correctness of our algorithms, we evaluate their empirical performance using both synthetic unit-demand valuations and two spectrum auction value models. The former are a class of valuations central to the literature on economics and computation Lehmann et al. (2006), for which there are efficient algorithms to compute CE Gul and Stacchetti (1999). In the spectrum auction value models, the buyers’ valuations are characterized by complements, which complicate the questions of existence and computability of CE. In all three models, we measure the average quality of learned CE via our algorithms, compared to the CE of the corresponding certain market (i.e., here, “certain” means lacking uncertainty), as a function of the number of samples. We find that often yields better error guarantees than using far fewer samples, because it successfully prunes buyers’ valuations (i.e., it ceases querying for values on bundles of goods that a CE provably does not comprise), even without any a priori knowledge of the market’s combinatorial structure.

As the market size grows, an interesting tradeoff arises between computational and sample efficiency. To prune a value query and retain rigorous guarantees on the quality of the learned CE, we must solve a welfare-maximizing problem whose complexity grows with the market’s size. Consequently, at each iteration of , for each value query, we are faced with a choice. Either solve said welfare-maximizing problem and potentially prune the value query (thereby saving on future samples), or defer attempts to prune the value query, until more is known about the market. To combat this situation, we show that an upper bound on the optimal welfare’s value (rather than the precise value) suffices to obtain rigorous guarantees on the learned CE’s quality. Such upper bounds can be found easily, by solving a relaxation of the welfare-maximization problem. Reminiscent of designing admissible heuristics in classical search problems, this methodology applies to any combinatorial market, but at the same time allows for the application of domain-dependent knowledge to compute these upper bounds, when available. Empirically, we show that a computationally cheap relaxation of the welfare-maximization problem yields substantial sample and computational savings in a large market.

Related Work

The idea for this paper stemmed from the work on abstraction in Fisher markets by Kroer et al. Kroer et al. (2019). There, the authors tackle the problem of computing equilibria in large markets by creating an abstraction of the market, computing equilibria in the abstraction, and lifting those equilibria back to the original market. Likewise, we develop a pruning criterion which in effect builds an abstraction of any CM, where then compute a CE, which is provably also an approximate CE in the original market.

The mathematical formalism we adopt follows that of Areyan Viqueira et al. Areyan Viqueira et al. (2020). There, the authors propose a mathematical framework for empirical game-theoretic analysis Wellman (2006), and algorithms that learn the Nash equilibria of simulation-based games Vorobeychik and Wellman (2008); Vorobeychik (2010). In this paper, we extend this methodology to market equilibria, and provide analogous results in the case of CMs. Whereas intuitively, a basic pruning criterion for games is arguably more straightforward—simply prune dominated strategies—the challenge in this work was to discover a pruning criterion that would likewise prune valuations that are provably not part of a CE.

Jha and Zick Jha and Zick (2020) have also tackled the problem of learning CE in CM.111The market structure they investigate is not identical to the structure studied here. Thus, at present, our results are not directly comparable. Whereas our approach is to accurately learn only those components of the buyers’ valuations that determine a CE (up to PAC guarantees), their approach bypasses the learning of agent preferences altogether, going straight for learning a solution concept, such as a CE. It is an open question as to whether one approach dominates the other, in the context of noisy CMs.

Another related line of research is concerned with learning valuation functions from data Balcan et al. (2012); Balcan and Harvey (2011); Lahaie and Parkes (2004). In contrast, our work is concerned with learning buyers’ valuations only in so much as it facilitates learning CE. Indeed, our main conclusion is that CE often can be learned from just a subset of the buyers’ valuations.

There is also a long line of work on preference elicitation in combinatorial auctions (e.g., Conen and Sandholm (2001)), where an auctioneer aims to pose value queries in an intelligent order so as to minimize the computational burden on the bidders, while still clearing the auction.

Finally, our pruning criterion relies on a novel application of the first welfare theorem of economics. While prior work has connected economic theory with algorithmic complexity Roughgarden and Talgam-Cohen (2015), this work connects economic theory with statistical learning theory.

2. Model

We write to denote the set of positive values in a numerical set including zero. Given an integer , we write to denote the first integers, inclusive: i.e., . Given a finite set of integers , we write to denote the power set of .

A combinatorial market is defined by a set of goods and a set of buyers. We denote the set of goods by , and the set of buyers by . We index an arbitrary good by , and an arbitrary buyer by . A bundle of goods is a set of goods . Each buyer is characterized by their preferences over bundles, represented as a valuation function , where is buyer ’s value for bundle . We assume valuations are normalized so that , for all . Using this notation, a combinatorial market—market, hereafter—is a tuple .

Given a market , an allocation denotes an assignment of goods to buyers, where is the bundle assigned to buyer . We consider only feasible allocations. An allocation is feasible if for all such that . We denote the set of all feasible allocations of market by . The welfare of allocation is defined as . A welfare-maximizing allocation is a feasible allocation that yields maximum welfare among all feasible allocations, i.e., . We denote by the welfare of any welfare-maximizing allocation , i.e., .

A pricing profile is a vector of pricing functions, one function for each buyer, each mapping bundles to prices, . The seller’s revenue of allocation given a pricing is . We refer to pair as a market outcome—outcome, for short. Given an outcome, buyer ’s utility is difference between its attained value and its payment, , and the seller’s utility is equal to its revenue.

In this paper, we are interested in approximations of one market by another. We now define a mathematical framework in which to formalize such approximations. In what follows, whenever we decorate a market , e.g., , what we mean is that we decorate each of its components: i.e., .

It will be convenient to refer to a subset of buyer–bundle pairs. We use the notation for this purpose.

Markets and are compatible if and . Whenever a market is compatible with a market , an outcome of is also an outcome of . Given two compatible markets and , we measure the difference between them at as . When , this difference is precisely the infinity norm. Given , and are called -approximations of one another if .

The solution concept of interest in this paper is competitive equilibrium222A competitive equilibrium is always guaranteed to exists Bikhchandani et al. (2002).. A competitive equilibrium consists of two conditions: the utility-maximization (UM) condition and the revenue-maximization (RM) condition. UM ensures that the allocation maximizes buyers’ utilities given the pricings, while RM ensures that the seller maximizes its utility. Together, both conditions constitute an equilibrium of the market, i.e., an outcome where no agent has an incentive to deviate by, for example, relinquishing its allocation. We now formalize this solution concept, followed by its relaxation, central when working with approximate markets.

Definition 0 (Competitive Equilibrium).

Given a market , an outcome is a competitive equilibrium (CE) if:

-

(UM)

-

(RM)

Definition 0 (Approximate Competitive Equilibria).

Let . An outcome is a -competitive equilibrium (-CE) if it is a CE in which UM holds up to :

-(UM)

For , we denote by the set of all -approximate CE of , i.e., is a -approximate CE of . Note that is the set of (exact) CE of market , which we denote .

Theorem 3 (Competitive Equilibrium Approximation).

Let . If and are compatible markets such that , then .

Proof.

We prove that: , for . This result then implies when ; likewise, it (symmetrically) implies when .

Let and be compatible markets s.t. . Suppose is a -competitive equilibrium of . Our task is to show that , interpreted as an outcome of , is a -competitive equilibrium of .

First, note that the RM condition is immediately satisfied, because and do not change when interpreting as an outcome of . Thus, we need only show that the approximation holds for the UM condition:

| (1) | |||||

| (2) | |||||

| (3) |

3. Learning Methodology

We now present a formalism in which to model noisy combinatorial markets. Intuitively, a noisy market is one in which buyers’ valuations over bundles are not known precisely; rather, only noisy samples are available.

Definition 0 (Conditional Combinatorial Markets).

A conditional comb. market consists of a set of conditions , a set of goods , a set of buyers , and a set of conditional valuation functions , where . Given a condition , the value is ’s value for bundle .

Definition 0 (Expected Combinatorial Market).

Let be a conditional combinatorial market and let be a distribution over . For all , define the expected valuation function by , and the corresponding expected combinatorial market as .

The goal of this work is to design algorithms that learn the approximate CE of expected combinatorial markets. We will learn their equilibria given access only to their empirical counterparts, which we define next.

Definition 0 (Empirical Combinatorial Market).

Let be a conditional combinatorial market and let be a distribution over . Denote by a vector of samples drawn from according to distribution . For all , we define the empirical valuation function by , and the corresponding empirical combinatorial market as .

Observation 1 (Learnability).

Let be a conditional combinatorial market and let be a distribution over . Let and be the corresponding expected and empirical combinatorial markets. If, for some , it holds that , then the competitive equilibria of are learnable: i.e, any competitive equilibrium of is a -competitive equilibrium of with probability at least .

Theorem 3 implies that CE are approximable to within any desired guarantee. The following lemma shows we only need a finitely many samples to learn them to within any probability.

Lemma 0 (Finite-Sample Bounds for Expected Combinatorial Markets via Hoeffding’s Inequality).

Let be a conditional combinatorial market, a distribution over , and an index set. Suppose that for all and , it holds that where . Then, with probability at least over samples , it holds that , where . (Proof in the Appendix)

Hoeffding’s inequality is a convenient and simple bound, where only knowledge of the range of values is required. However, the union bound can be inefficient in large combinatorial markets. This shortcoming can be addressed via uniform convergence bounds and Rademacher averages (Bartlett and Mendelson, 2002; Areyan Viqueira et al., 2019; Koltchinskii, 2001). Furthermore, sharper empirical variance sensitive bounds have been shown to improve sample complexity in learning the Nash equilibria of black-box games (Areyan Viqueira et al., 2020). In particular, to obtain a confidence interval of radius in a combinatorial market with index set , Hoeffding’s inequality requires samples. Uniform convergence bounds can improve the term arising from the union bound, and variance-sensitive bounds can largely replace dependence on with variances. Nonetheless, even without these augmentations, our methods are statistically efficient in , requiring only polynomial sample complexity to learn exponentially large combinatorial markets.

3.1. Baseline Algorithm

(Algorithm 2) is a preference elicitation algorithm for combinatorial markets. The algorithm places value queries, but is only assumed to elicit noisy values for bundles. The following guarantee follows immediately from Lemma 7.

Theorem 8 (Elicitation Algorithm Guarantees).

Let be a conditional market, be a distribution over , an index set, a number of samples, , and . Suppose that for all and , it holds that . If outputs on input , then, with probability at least , it holds that .

Proof.

The result follows from Lemma 7. ∎

3.2. Pruning Algorithm

elicits buyers’ valuations for all bundles, but in certain situations, some buyer valuations are not relevant for computing a CE—although bounds on all of them are necessary to guarantee strong bounds on the set of CE (Theorem 3). For example, in a first-price auction for one good, it is enough to accurately learn the highest bid, but is not necessary to accurately learn all other bids, if it is known that they are lower than the highest. Since our goal is to learn CE, we present (Algorithm 1), an algorithm that does not sample uniformly, but instead adaptively decides which value queries to prune so that, with provable guarantees, ’s estimated market satisfies the conditions of Theorem 3.

Input: .

A conditional combinatorial market ,

a distribution over ,

a sampling schedule ,

a failure probability schedule ,

a pruning budget schedule ,

a valuation range , and

a target approx. error .

Output:

Valuation estimates , for all ,

approximation errors ,

failure probability ,

and CE error .

Input: .

A conditional combinatorial market ,

a distribution over ,

an index set ,

sample size ,

failure prob. , and

valuation range .

Output:

Valuation estimates , for all ,

and an approximation error .

(Algorithm 1) takes as input a sampling schedule , a failure probability schedule , and a pruning budget schedule . The sampling schedule is a sequence of strictly decreasing integers , where is the total number of samples to take for each pair during ’s -th iteration. The failure probability schedule is a sequence of the same length as , where is the -th iteration’s failure probability and is the total failure probability. The pruning budget schedule is a sequence of integers also of the same length as , where is the maximum number of pruning candidate pairs. The algorithm progressively elicits buyers’ valuations via repeated calls to . However, between calls to , searches for value queries that are provably not part of a CE; the size of this search is dictated by the pruning schedule. All such queries (i.e., buyer–bundle pairs) then cease to be part of the index set with which is called in future iterations.

In what follows, we prove several intermediate results, which enable us to prove the main result of this section, Theorem 13, which establishes ’s correctness. Specifically, the market learned by —with potentially different numbers of samples for different pairs—is enough to provably recover any CE of the underlying market.

Lemma 0 (Optimal Welfare Approximations).

Let and be compatible markets such that they -approximate one another. Then .

Proof.

Let be a welfare-maximizing allocation for and be a welfare-maximizing allocation for . Let be the maximum achievable welfare in market . Then,

The first inequality follows from the optimality of in , and the second from the -approximation assumption. Likewise, , so the result holds. ∎

The key to this work was the discovery of a pruning criterion that removes pairs from consideration if they are provably not part of any CE. Our check relies on computing the welfare of the market without the pair: i.e., in submarkets.

Definition 0.

Given a market and buyer–bundle pair , the -submarket of , denoted by , is the market obtained by removing all goods in and buyer from market . That is, .

Lemma 0 (Pruning Criteria).

Let and be compatible markets such that . In addition, let be a buyer, bundle pair, and be the -submarket of . Finally, let upper bound , i.e., . If the following pruning criterion holds, then is not allocated to in any welfare-maximizing allocation of :

| (4) |

Proof.

Let and be welfare-maximizing allocations of markets and , respectively. Then,

| (5) | ||||

| (6) | ||||

| (7) | ||||

| (8) | ||||

| (9) |

The first inequality follows from Lemma 9. The second follows from Equation (4) and the third because is an upper bound of . The fourth inequality follows from the assumption that , and by Lemma 9 applied to submarket . Therefore, the allocation where gets cannot be welfare-maximizing in market . ∎

Lemma 11 provides a family of pruning criteria parameterized by the upper bound . The closer is to , the sharper the pruning criterion, with the best pruning criterion being . However, solving for exactly can easily become a bottleneck, as the pruning loop requires a solution to many such instances, one per pair (Line 12 of Algorithm 1). Alternatively, one could compute looser upper bounds, and thereby trade off computation time for opportunities to prune more pairs, when the upper bound is not tight enough. In our experiments, we show that even relatively loose but cheap-to-compute upper bounds result in significant pruning and, thus, savings along both dimensions—computational and sample complexity.

To conclude this section, we establish the correctness of . For our proof we rely on the following generalization of the first welfare theorem of economics, which handles additive errors.

Theorem 12 (First Welfare Theorem Roughgarden (2010)).

For , let be an -competitive equilibrium of . Then, is a welfare-maximizing allocation of , up to additive error .

Theorem 13 (Elicitation Algorithm with Pruning Guarantees).

Let be a conditional market, let be a distribution over , and let .

Suppose that for all and , it holds that , where .

Let be a sequence of strictly increasing integers, and a sequence of the same length as such that and .

If

outputs

on input

, then the following holds with probability at least :

1.

2.

Here is the empirical market obtained via , i.e., the market with valuation functions given by .

Proof.

To show part 1, note that at each iteration of , Line 5 updates the error estimates for each after a call to (Line 4 of ) with input failure probability . Theorem 8 implies that each call to returns estimated values that are within of their expected value with probability at least . By union bounding all calls to within , part 1 then holds with probability at least .

To show part 2, note that only pairs for which Equation (4) holds are removed from index set (Line 14 of ). By Lemma 11, no such pair can be part of any approximate welfare-maximizing allocation of the expected market, . By Theorem 12, no such pair can be a part of any CE. Consequently, contains accurate enough estimates (up to ) of all pairs that may participate in any CE. Part 2 then follows from Theorem 3. ∎

4. Experiments

The goal of our experiments is to robustly evaluate the empirical performance of our algorithms. To this end, we experiment with a variety of qualitatively different inputs. In particular, we evaluate our algorithms on both unit-demand valuations, the Global Synergy Value Model (GSVM) Goeree and Holt (2010), and the Local Synergy Value Model (LSVM) Scheffel et al. (2012). Unit-demand valuations are a class of valuations central to the literature on economics and computation Lehmann et al. (2006) for which efficient algorithms exist to compute CE Gul and Stacchetti (1999). GSVM and LSVM model situations in which buyers’ valuations encode complements; CE are not known be efficiently computable, or even representable, in these markets.

While CE are always guaranteed to exist (e.g., Bikhchandani et al. (2002)), in the worst case, they might require personalized bundle prices. These prices are computationally complex, not to mention out of favor Hinz et al. (2011). A pricing is anonymous if it charges every buyer the same price, i.e., for all . Moreover, an anonymous pricing is linear if there exists a set of prices , where is good ’s price, such that . In what follows, we refer to linear, anonymous pricings as linear prices.

Where possible, it is preferable to work with linear prices, as they are simpler, e.g., when bidding in an auction Kwasnica et al. (2005). In our present study—one of the first empirical studies on learning CE—we thus focus on linear prices, leaving as future research the empirical333Note that all our theoretical results hold for any pricing profile. effect of more complex pricings.444Lahaie and Lubin Lahaie and Lubin (2019), for example, search for prices in between linear and bundle.

To our knowledge, there have been no analogous attempts at learning CE; hence, we do not reference any baseline algorithms from the literature. Rather, we compare the performance of , our pruning algorithm, to , investigating the quality of the CE learned by both, as well as their sample efficiencies.

4.1. Experimental Setup.

We first explain our experimental setup, and then present results. We let denote the continuous uniform distribution over range , and , the discrete uniform distribution over set , for .

Simulation of Noisy Combinatorial Markets.

We start by drawing markets from experimental market distributions. Then, fixing a market, we simulate noisy value elicitation by adding noise drawn from experimental noise distributions to buyers’ valuations in the market. We refer to a market realization drawn from an experimental market distribution as the ground-truth market. Our experiments then measure how well we can approximate the CE of a ground-truth market given access only to noisy samples of it.

Fix a market and a condition set , where . Define the conditional market , where , for . In words, when eliciting ’s valuation for , we assume additive noise, namely . The market together with distribution over is the model from which our algorithms elicit noisy valuations from buyers. Then, given samples of , the empirical market is the market estimated from the samples. Note that is the only market we get to observe in practice.

We consider only zero-centered noise distributions. In this case, the expected combinatorial market is the same as the ground-truth market since, for every it holds that . While this noise structure is admittedly simple, we robustly evaluate our algorithms along another dimension, as we study several rich market structures (unit-demand, GSVM, and LSVM). An interesting future direction would be to also study richer noise structures, e.g., letting noise vary with a bundle’s size, or other market characteristics.

Utility-Maximization (UM) Loss

To measure the quality of a CE computed for a market in another market , we first define the per-buyer metric as follows,

i.e., the difference between the maximum utility could have attained at prices and the utility attains at the outcome . Our metric of interest is then defined as,

which is a worst-case measure of utility loss over all buyers in the market. Note that it is not useful to incorporate the SR condition into a loss metric, because it is always satisfied.

In our experiments, we measure the UM loss that a CE of an empirical market obtains, evaluated in the corresponding ground-truth market. Thus, given an empirical estimate of , and a CE in , we measure , i.e., the loss in at prices of CE . Theorem 3 implies that if is an -approximation of , then . Moreover, Theorem 8 yields the same guarantees, but with probability at least , provided the -approximation holds with probability at least .

Sample Efficiency of .

We say that algorithm has better sample efficiency than algorithm if requires fewer samples than to achieve at least the same accuracy.

Fixing a condition set , a distribution over , and a conditional market , we use the following experimental design to evaluate ’s sample efficiency relative to that of . Given a desired error guarantee , we compute the number of samples that would be required for to achieve accuracy . We then use the following doubling strategy as a sampling schedule for , , rounding to the nearest integer as necessary, and the following failure probability schedule , which sums to .

Finally, the exact pruning budget schedules will vary depending on the value model (unit demand, GSVM, or LSVM). But in all cases, we denote an unconstrained pruning budget schedule by , which by convention means that at every iteration, all active pairs are candidates for pruning. Using these schedules, we run with a desired accuracy of zero. We denote by the approximation guarantee achieved by upon termination.

4.2. Unit-demand Experiments

A buyer is endowed with unit-demand valuations if, for all , . In a unit-demand market, all buyers have unit-demand valuations. A unit-demand market can be compactly represented by matrix , where entry is ’s value for , i.e., . In what follows, we denote by a random variable over unit-demand valuations.

We construct four different distributions over unit-demand markets: Uniform, Preferred-Good, Preferred-Good-Distinct, and Preferred-Subset. All distributions are parameterized by and , the number of buyers and goods, respectively. A uniform unit-demand market is such that for all . When , each buyer has a preferred good , with and . Conditioned on , ’s value for good is given by . Distribution Preferred-Good-Distinct is similar to Preferred-Good, except that no two buyers have the same preferred good. (Note that the Preferred-Good-Distinct distribution is only well defined when .) Finally, when , each buyer is interested in a subset of goods , where is drawn uniformly at random from the set of all bundles. Then, the value has for is given by , if ; and 0, otherwise.

In unit-demand markets, we experiment with three noise models, low, medium, and high, by adding noise drawn from , and , respectively. We choose .

| Distribution | ||||

|---|---|---|---|---|

| Uniform | 0.0018 | 0.0020 | 0.0074 | 0.0082 |

| Preferred-Good | 0.0019 | 0.0023 | 0.0080 | 0.0094 |

| Preferred-Good-Distinct | 0.0000 | 0.0020 | 0.0000 | 0.0086 |

| Preferred-Subset | 0.0019 | 0.0022 | 0.0076 | 0.0090 |

Unit-demand Empirical UM Loss of .

As a learned CE is a CE of a learned market, we require a means of computing the CE of a market—specifically, a unit-demand market . To do so, we first solve for the555Since in all our experiments, we draw values from continuous distributions, we assume that the set of markets with multiple welfare-maximizing allocations is of negligible size. Therefore, we can ignore ties. welfare-maximizing allocation of , by solving for the maximum weight matching using Hungarian algorithm Kuhn (1955) in the bipartite graph whose weight matrix is given by . Fixing , we then solve for prices via linear programming Bikhchandani et al. (2002). In general, there might be many prices that couple with to form a CE of . For simplicity, we solve for two pricings given , the revenue-maximizing and revenue-minimizing , where revenue is defined as the sum of the prices.

For each distribution, we draw 50 markets, and for each such market , we run four times, each time to achieve guarantee . then outputs an empirical estimate for each . We compute outcomes and , and measure and . We then average across all market draws, for both the minimum and the maximum pricings. Table 1 summarizes a subset of these results. The error guarantees are consistently met across the board, indeed by one or two orders of magnitude, and they degrade as expected: i.e., with higher values of . We note that the quality of the learned CE is roughly the same for all distributions, except in the case of and Preferred-Good-Distinct, where learning is more accurate. For this distribution, it is enough to learn the preferred good of each buyer. Then, one possible CE is to allocate each buyer its preferred good and price all goods at zero which yields near no UM-Loss. Note that, in general, pricing all goods at zero is not a CE, unless the market has some special structure, like the markets drawn from Preferred-Good-Distinct.

Unit-demand Sample Efficiency

We use pruning schedule and for each pair, we use the Hungarian algorithm Kuhn (1955) to compute the optimal welfare of the market without . In other words, in each iteration, we consider all active pairs as pruning candidates (Algorithm 1, Line 11), and for each we compute the optimal welfare (Algorithm 1, Line 14).

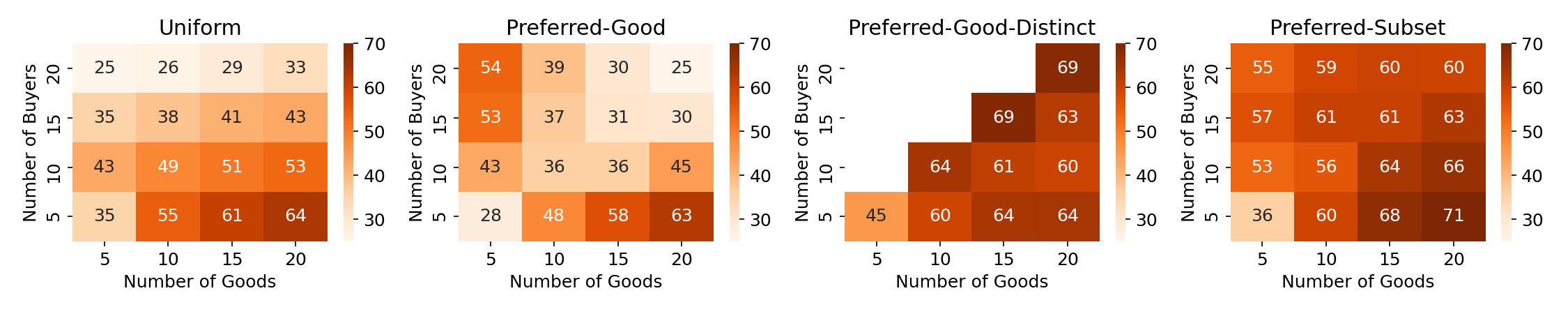

For each market distribution, we compute the average of the number of samples used by across 50 independent market draws. We report samples used by as a percentage of the number of samples used by to achieve the same guarantee, namely, , for each initial value of . Figure 1 depicts the results of these experiments as heat maps, for all distributions and for , where darker colors indicate more savings, and thus better sample efficiency.

A few trends arise, which we note are similar for other values of . For a fixed number of buyers, ’s sample efficiency improves as the number of goods increases, because fewer goods can be allocated, which means that there are more candidate values to prune, resulting in more savings. On the other hand, the sample efficiency usually decreases as the number of buyers increases; this is to be expected, as the pruning criterion degrades with the number of buyers (Lemma 11). While savings exceed 30% across the board, we note that Uniform, the market with the least structure, achieves the least savings, while Preferred-Subset and Preferred-Good-Distinct achieve the most. This finding shows that is capable of exploiting the structure present in these distributions, despite not knowing anything about them a priori.

Finally, we note that sample efficiency quickly degrades for higher values of . In fact, for high enough values of (in our experiments, ), might, on average, require more samples than to produce the same guarantee. Most of the savings achieved are the result of pruning enough pairs early enough: i.e., during the first few iterations of . When is large, however, our sampling schedule does not allocate enough samples early on. When designing sampling schedules for , one must allocate enough (but not too many) samples at the beginning of the schedule. Precisely how to determine this schedule is an empirical question, likely dependent on the particular application at hand.

4.3. Value Models

In this next set of experiments, we test the empirical performance of our algorithms in more complex markets, where buyers valuations contain synergies. Synergies are a common feature of many high-stakes combinatorial markets. For example, telecommunication service providers might value different bundles of radio spectrum licenses differently, depending on whether the licenses in the bundle complement one another. For example, a bundle including New Jersey and Connecticut might not be very valuable unless it also contains New York City.

Specifically, we study the Global Synergy Value Model (GSVM) Goeree and Holt (2010) and the Local Synergy Value Model (LSVM) Scheffel et al. (2012). These models or markets capture buyers’ synergies as a function of buyers’ types and their (abstract) geographical locations. In both GSVM and LSVM, there are 18 licenses, with buyers of two types: national or regional. A national buyer is interested in larger packages than regional buyers, whose interests are limited to certain regions. GSVM has six regional bidders and one national bidder and models geographical regions as two circles. LSVM has five regional bidders and one national bidder and uses a rectangular model. The models differ in the exact ways buyers’ values are drawn, but in any case, synergies are modeled by suitable distance metrics. In our experiments, we draw instances of both GSVM and LSVM using SATS, a universal spectrum auction test suite developed by researchers to test algorithms for combinatorial markets Weiss et al. (2017).

| GSVM | LSVM | |||||||

|---|---|---|---|---|---|---|---|---|

| UM Loss | UM Loss | |||||||

| 1.25 | ||||||||

| 2.50 | ||||||||

| 5.00 | ||||||||

| 10.0 | ||||||||

Experimental Setup.

On average, the value a buyer has for an arbitrary bundle in either GSVM or LSVM markets is approximately 80. We introduce noise i.i.d. noise from distribution whose range is 2, or 2.5% of the expected buyer’s value for a bundle. As GSVM’s buyers’ values are at most 400, and LSVM’s are at most 500, we use valuation ranges and for GSVM and LSVM, respectively. We note that a larger noise range yields qualitatively similar results with errors scaling accordingly.

For the GSVM markets, we use the pruning budget schedule . For each pair, we solve the welfare maximization problem using an off-the-shelf solver.666We include ILP formulations and further technical details in the appendix. In an LSVM market, the national bidder demands all 18 licenses. The welfare optimization problem in an LSVM market is solvable in a few seconds.777Approximately 20 seconds in our experiments, details appear in the appendix. Still, the many submarkets (in the hundreds of thousands) call for a finite pruning budget schedule and a cheaper-to-compute welfare upper bound. In fact, to address LSVM’s size complexity, we slightly modify , as explained next.

A two-pass strategy for LSVM

Because of the complexity of LSVM markets, we developed a heuristic pruning strategy, in which we perform two pruning passes during each iteration of . The idea is to compute a computationally cheap upper bound on welfare with pruning budget schedule in the first pass, use this bound instead of the optimal for each active . We compute this bound using the classic relaxation technique to create admissible heuristics. Concretely, given a candidate pair, we compute the maximum welfare in the absence of pair , ignoring feasibility constraints:

After this first pass, we undertake a second pass over all remaining active pairs. For each active pair, we compute the optimal welfare without pair , but using the following finite pruning budget schedule . In other words, we carry out this computation for just a few of the remaining candidate pairs. We chose this pruning budget schedule so that one iteration of would take approximately two hours.

One choice remains undefined for the second pruning pass: which candidate pairs to select out of those not pruned in the first pass? For each iteration , we sort the in descending order according to the upper bound on welfare computed in the first pass, and then we select the bottom pairs (180 during the first iteration, 90 during the second, etc.). The intuition for this choice is that pairs with lower upper bounds might be more likely to satisfy Lemma 11’s pruning criteria than pairs with higher upper bounds. Note that the way candidate pairs are selected for the second pruning pass uses no information about the underlying market, and is thus widely applicable. We will have more to say about the lack a priori information used by in what follows.

Results.

Table 2 summarizes the results of our experiments with GSVM and LSVM markets. The table shows 95% confidence intervals around the mean number of samples needed by and to achieve the indicated accuracy () guarantee for each row of the table. The table also shows confidence intervals around the mean guarantees achieved by , denoted , and confidence intervals over the UM loss metric. Several observations follow.

Although ultimately a heuristic method, on average uses far fewer samples than and produces significantly better guarantees. We emphasize that is capable of producing these results without any a priori knowledge about the underlying market. Instead, autonomously samples those quantities that can provably be part of an optimal solution. The guarantees are slightly worse in the LSVM market than for GSVM, where we prune all eligible pairs. In general, there is a tradeoff between computational and sample efficiency: at the cost of more computation, to find more pairs to prune up front, one can save on future samples. Still, even with a rather restricted pruning budget (compared to hundreds of thousands potentially active pairs), achieves substantial savings compared to in the LSVM market.

Finally, the UM loss metric follows a trend similar to those observed for unit-demand markets, i.e., the error guarantees are consistently met and degrade as expected (worst guarantees for higher values of ). Note that in our experiments, all 40 GSVM market instances have equilibria with linear and anonymous prices. In contrast, only 18 out of 32 LSVM market do, so the table reports UM loss over this set. For the remaining 32 markets, we report here a UM loss of approximately regardless of the value of . This high UM loss is due to the lack of CE in linear pricings which dominates any UM loss attributable to the estimation of values.

5. Conclusion and Future Directions

In this paper, we define noisy combinatorial markets as a model of combinatorial markets in which buyers’ valuations are not known with complete certainty, but noisy samples can be obtained, for example, by using approximate methods, heuristics, or truncating the run-time of a complete algorithm. For this model, we tackle the problem of learning CE. We first show tight lower- and upper-bounds on the buyers’ utility loss, and hence the set of CE, given a uniform approximation of one market by another. We then develop learning algorithms that, with high probability, learn said uniform approximations using only finitely many samples. Leveraging the first welfare theorem of economics, we define a pruning criterion under which an algorithm can provably stop learning about buyers’ valuations for bundles, without affecting the quality of the set of learned CE. We embed these conditions in an algorithm that we show experimentally is capable of learning CE with far fewer samples than a baseline. Crucially, the algorithm need not know anything about this structure a priori; our algorithm is general enough to work in any combinatorial market. Moreover, we expect substantial improvement with sharper sample complexity bounds; in particular, variance-sensitive bounds can be vastly more efficient when the variance is small, whereas Hoeffding’s inequality essentially assumes the worst-case variance.

Acknowledgements

This work was supported by NSF Award CMMI-1761546 and by DARPA grant FA8750.

References

- (1)

- Areyan Viqueira et al. (2020) Enrique Areyan Viqueira, Cyrus Cousins, and Amy Greenwald. 2020. Improved Algorithms for Learning Equilibria in Simulation-Based Games. In Proceedings of the 19th International Conference on Autonomous Agents and Multiagent Systems, AAMAS ’20, Auckland, New Zealand, May 9-13, 2020, Amal El Fallah Seghrouchni, Gita Sukthankar, Bo An, and Neil Yorke-Smith (Eds.). International Foundation for Autonomous Agents and Multiagent Systems, 79–87. https://dl.acm.org/doi/abs/10.5555/3398761.3398776

- Areyan Viqueira and Greenwald (2020) Enrique Areyan Viqueira and Amy Greenwald. 2020. Learning Competitive Equilibria in Noisy Combinatorial Markets. In Proceedings of the 2nd Games, Agents, and Incentives Workshop (GAIW@ AAMAS 2020).

- Areyan Viqueira et al. (2019) Enrique Areyan Viqueira, Amy Greenwald, Cyrus Cousins, and Eli Upfal. 2019. Learning Simulation-Based Games from Data. In Proceedings of the 18th International Conference on Autonomous Agents and MultiAgent Systems. International Foundation for Autonomous Agents and Multiagent Systems, 1778–1780.

- Balcan et al. (2012) Maria-Florina Balcan, Florin Constantin, Satoru Iwata, and Lei Wang. 2012. Learning Valuation Functions. In COLT 2012 - The 25th Annual Conference on Learning Theory, June 25-27, 2012, Edinburgh, Scotland (JMLR Proceedings, Vol. 23), Shie Mannor, Nathan Srebro, and Robert C. Williamson (Eds.). JMLR.org, 4.1–4.24. http://proceedings.mlr.press/v23/balcan12b/balcan12b.pdf

- Balcan and Harvey (2011) Maria-Florina Balcan and Nicholas J. A. Harvey. 2011. Learning submodular functions. In Proceedings of the 43rd ACM Symposium on Theory of Computing, STOC 2011, San Jose, CA, USA, 6-8 June 2011, Lance Fortnow and Salil P. Vadhan (Eds.). ACM, 793–802. https://doi.org/10.1145/1993636.1993741

- Ball et al. (2006) MO Ball, G Donohue, and K Hoffman. 2006. Auctions for the safe, efficient and equitable allocation of airspace system resources. Cramton P, Shoham Y, Steinberg R, eds. Combinatorial Auctions.

- Bartlett and Mendelson (2002) Peter L Bartlett and Shahar Mendelson. 2002. Rademacher and Gaussian complexities: Risk bounds and structural results. Journal of Machine Learning Research 3, Nov (2002), 463–482.

- Bikhchandani and Mamer (1997) Sushil Bikhchandani and John W Mamer. 1997. Competitive equilibrium in an exchange economy with indivisibilities. Journal of economic theory 74, 2 (1997), 385–413.

- Bikhchandani et al. (2002) Sushil Bikhchandani, Joseph M Ostroy, et al. 2002. The package assignment model. Journal of Economic theory 107, 2 (2002), 377–406.

- Cantillon and Pesendorfer (2006) Estelle Cantillon and Martin Pesendorfer. 2006. Auctioning bus routes: The London experience. . (2006).

- Cheung et al. (2020) Yun Kuen Cheung, Richard Cole, and Nikhil R Devanur. 2020. Tatonnement beyond gross substitutes? Gradient descent to the rescue. Games and Economic Behavior 123 (2020), 295–326.

- Conen and Sandholm (2001) Wolfram Conen and Tuomas Sandholm. 2001. Preference elicitation in combinatorial auctions. In Proceedings 3rd ACM Conference on Electronic Commerce (EC-2001), Tampa, Florida, USA, October 14-17, 2001, Michael P. Wellman and Yoav Shoham (Eds.). ACM, 256–259. https://doi.org/10.1145/501158.501191

- Cramton et al. (2002) Peter Cramton et al. 2002. Spectrum auctions. Handbook of telecommunications economics 1 (2002), 605–639.

- Edelman et al. (2007) Benjamin Edelman, Michael Ostrovsky, and Michael Schwarz. 2007. Internet advertising and the generalized second-price auction: Selling billions of dollars worth of keywords. American economic review 97, 1 (2007), 242–259.

- Fujishima et al. (1999) Yuzo Fujishima, Kevin Leyton-Brown, and Yoav Shoham. 1999. Taming the Computational Complexity of Combinatorial Auctions: Optimal and Approximate Approaches. In Proceedings of the Sixteenth International Joint Conference on Artificial Intelligence, IJCAI 99, Stockholm, Sweden, July 31 - August 6, 1999. 2 Volumes, 1450 pages, Thomas Dean (Ed.). Morgan Kaufmann, 548–553. http://ijcai.org/Proceedings/99-1/Papers/079.pdf

- Goeree and Holt (2010) Jacob K Goeree and Charles A Holt. 2010. Hierarchical package bidding: A paper & pencil combinatorial auction. Games and Economic Behavior 70, 1 (2010), 146–169.

- Gul and Stacchetti (1999) Faruk Gul and Ennio Stacchetti. 1999. Walrasian equilibrium with gross substitutes. Journal of Economic theory 87, 1 (1999), 95–124.

- Hinz et al. (2011) Oliver Hinz, II-Horn Hann, and Martin Spann. 2011. Price discrimination in e-commerce? An examination of dynamic pricing in name-your-own price markets. Mis quarterly (2011), 81–98.

- Hoeffding (1994) Wassily Hoeffding. 1994. Probability inequalities for sums of bounded random variables. In The Collected Works of Wassily Hoeffding. Springer, 409–426.

- Jha and Zick (2020) Tushant Jha and Yair Zick. 2020. A Learning Framework for Distribution-Based Game-Theoretic Solution Concepts. In Proceedings of the 21st ACM Conference on Economics and Computation. 355–377.

- Koltchinskii (2001) Vladimir Koltchinskii. 2001. Rademacher penalties and structural risk minimization. IEEE Transactions on Information Theory 47, 5 (2001), 1902–1914.

- Kroer et al. (2019) Christian Kroer, Alexander Peysakhovich, Eric Sodomka, and Nicolás E. Stier Moses. 2019. Computing Large Market Equilibria using Abstractions. In Proceedings of the 2019 ACM Conference on Economics and Computation, EC 2019, Phoenix, AZ, USA, June 24-28, 2019, Anna Karlin, Nicole Immorlica, and Ramesh Johari (Eds.). ACM, 745–746. https://doi.org/10.1145/3328526.3329553

- Kuhn (1955) Harold W Kuhn. 1955. The Hungarian method for the assignment problem. Naval research logistics quarterly 2, 1-2 (1955), 83–97.

- Kwasnica et al. (2005) Anthony M Kwasnica, John O Ledyard, Dave Porter, and Christine DeMartini. 2005. A new and improved design for multiobject iterative auctions. Management science 51, 3 (2005), 419–434.

- Lahaie and Lubin (2019) Sébastien Lahaie and Benjamin Lubin. 2019. Adaptive-Price Combinatorial Auctions. In Proceedings of the 2019 ACM Conference on Economics and Computation, EC 2019, Phoenix, AZ, USA, June 24-28, 2019, Anna Karlin, Nicole Immorlica, and Ramesh Johari (Eds.). ACM, 749–750. https://doi.org/10.1145/3328526.3329615

- Lahaie and Parkes (2004) Sébastien Lahaie and David C. Parkes. 2004. Applying learning algorithms to preference elicitation. In Proceedings 5th ACM Conference on Electronic Commerce (EC-2004), New York, NY, USA, May 17-20, 2004, Jack S. Breese, Joan Feigenbaum, and Margo I. Seltzer (Eds.). ACM, 180–188. https://doi.org/10.1145/988772.988800

- Lehmann et al. (2006) Benny Lehmann, Daniel Lehmann, and Noam Nisan. 2006. Combinatorial auctions with decreasing marginal utilities. Games and Economic Behavior 55, 2 (2006), 270–296.

- Nisan et al. ([n.d.]) Noam Nisan, Tim Roughgarden, Eva Tardos, and Vijay V Vazirani. [n.d.]. Algorithmic Game Theory, 2007. Google Scholar Google Scholar Digital Library Digital Library ([n. d.]).

- Roughgarden (2010) Tim Roughgarden. 2010. Algorithmic game theory. Commun. ACM 53, 7 (2010), 78–86. https://doi.org/10.1145/1785414.1785439

- Roughgarden and Talgam-Cohen (2015) Tim Roughgarden and Inbal Talgam-Cohen. 2015. Why Prices Need Algorithms. In Proceedings of the Sixteenth ACM Conference on Economics and Computation, EC ’15, Portland, OR, USA, June 15-19, 2015, Tim Roughgarden, Michal Feldman, and Michael Schwarz (Eds.). ACM, 19–36. https://doi.org/10.1145/2764468.2764515

- Saltzman (2002) Matthew J Saltzman. 2002. COIN-OR: an open-source library for optimization. In Programming languages and systems in computational economics and finance. Springer, 3–32.

- Scheffel et al. (2012) Tobias Scheffel, Georg Ziegler, and Martin Bichler. 2012. On the impact of package selection in combinatorial auctions: an experimental study in the context of spectrum auction design. Experimental Economics 15, 4 (2012), 667–692.

- Vorobeychik (2010) Yevgeniy Vorobeychik. 2010. Probabilistic analysis of simulation-based games. ACM Trans. Model. Comput. Simul. 20, 3 (2010), 16:1–16:25. https://doi.org/10.1145/1842713.1842719

- Vorobeychik and Wellman (2008) Yevgeniy Vorobeychik and Michael P. Wellman. 2008. Stochastic search methods for nash equilibrium approximation in simulation-based games. In 7th International Joint Conference on Autonomous Agents and Multiagent Systems (AAMAS 2008), Estoril, Portugal, May 12-16, 2008, Volume 2, Lin Padgham, David C. Parkes, Jörg P. Müller, and Simon Parsons (Eds.). IFAAMAS, 1055–1062. https://dl.acm.org/citation.cfm?id=1402368

- Walras (2003) Léon Walras. 2003. Elements of Pure Economics: Or the Theory of Social Wealth. Routledge. https://books.google.com/books?id=hwjRD3z0Qy4C

- Weiss et al. (2017) Michael Weiss, Benjamin Lubin, and Sven Seuken. 2017. SATS: A Universal Spectrum Auction Test Suite. In Proceedings of the 16th Conference on Autonomous Agents and MultiAgent Systems, AAMAS 2017, São Paulo, Brazil, May 8-12, 2017, Kate Larson, Michael Winikoff, Sanmay Das, and Edmund H. Durfee (Eds.). ACM, 51–59. http://dl.acm.org/citation.cfm?id=3091139

- Wellman (2006) Michael P. Wellman. 2006. Methods for Empirical Game-Theoretic Analysis. In Proceedings, The Twenty-First National Conference on Artificial Intelligence and the Eighteenth Innovative Applications of Artificial Intelligence Conference, July 16-20, 2006, Boston, Massachusetts, USA. AAAI Press, 1552–1556. http://www.aaai.org/Library/AAAI/2006/aaai06-248.php

Appendix

Theoretical Proofs

Proof.

(Lemma 7 of the main paper)

Let be a conditional combinatorial market, a distribution over , and an index set. Let be a vector of samples drawn from . Suppose that for all and , it holds that where . Let and . Then, by Hoeffding’s inequality Hoeffding (1994),

| (10) |

Now, applying union bound over all events where ,

| (11) |

| (12) |

Where the last equality follows because the summands on the right-hand size of eq. 12 do not depend on the summation index. Now, note that eq. 12 implies a lower bound for the event that complements ,

| (13) |

The event is equivalent to the event . Setting and solving for yields .

The results follows by substituting in eq. 13.

∎

Mathematical Programs

For our experiments, we solve for CE in linear prices. To compute CE in linear prices, we first solve for a welfare-maximizing allocation and then, fixing , we solve for CE linear prices. Note that, if a CE in linear prices exists, then it is supported by any welfare-maximizing allocation Roughgarden and Talgam-Cohen (2015). Moreover, since valuations in our experiments are drawn from continuous distributions, we assume that the set of welfare-maximizing allocations for a given market is of negligible size.

Next, we present the mathematical programs we used to compute welfare-maximizing allocations and find linear prices. Given a combinatorial market , the following integer linear program, (14), computes a welfare-maximizing allocation . Note this formulation is standard in the literature Nisan et al. ([n.d.]).

| (14) |

Given a market and a solution to (14), the following set of linear inequalities, (15), define all linear prices that couple with allocation to form a CE in . The inequalities are defined over variables where is good ’s price. The price of bundle is then .

| (15) |

The first set of inequalities of (15) enforce the UM conditions. The second set of inequalities states that the price of goods not allocated to any buyer in must be zero. In the case of linear pricing, this condition is equivalent to the RM condition. In practice, a market might not have CE in linear pricings, i.e., the set of feasible solutions of (15) might be empty. In our experiments, we solve the following linear program, (16), which is a relaxation of (15). In linear program (16), we introduce slack variables to relax the UM constraints. We define as objective function the sum of all slack variables, , which we wish to minimize.

| (16) |

As reported in the main paper, for each GSVM market we found that the optimal solution of (16) was such that , which means that an exact CE in linear prices was found. In contrast, for LSVM markets only 18 out of 50 markets had linear prices () whereas 32 did not (.

Experiments’ Technical Details

We used the COIN-OR Saltzman (2002) library, through Python’s PuLP (https://pypi.org/project/PuLP/) interface, to solve all mathematical programs. We wrote all our experiments in Python, and once the double-blind review period finalizes, we will release all code publicly. We ran our experiments in a cluster of 2 Google’s GCloud c2-standard-4 machines. Unit-demand experiments took approximately two days to complete, GSVM experiments approximately four days, and LSVM experiments approximately eight days.