Percolation framework for the loss distribution of smart contract risks

\runauthorPetar Jevtić and Nicolas Lanchier

\addressSchool of Mathematical and Statistical Sciences

Arizona State University

Tempe, AZ 85287, USA.

petar.jevtic@asu.edu

nicolas.lanchier@asu.edu

Probabilistic Framework For Loss Distribution

Of Smart Contract Risk††thanks: The

numerical results presented in this work are produced by the joint invention of the authors.

The invention is patent pending under the heading

“Systems and methods for a simulation program of percolation model for the loss distribution of smart contracts caused by a cyber attack or contagious failure”.

Abstract

Smart contract risk can be defined as a financial risk of loss due to cyber attacks on or contagious failures of smart contracts. Its quantification is of paramount importance to technology platform providers as well as companies and individuals when considering the deployment of this new technology. That is why, as our primary contribution, we propose a structural framework of aggregate loss distribution for smart contract risk under the assumption of a tree-stars graph topology representing the network of interactions among smart contracts and their users. Up to our knowledge, there exist no theoretical frameworks or models of an aggregate loss distribution for smart contracts in this setting. To achieve our goal, we contextualize the problem in the probabilistic graph-theoretical framework using bond percolation models. We assume that the smart contract network topology is represented by a random tree graph of finite size, and that each smart contract is the center of a random star graph whose leaves represent the users of the smart contract. We allow for heterogeneous loss topology superimposed on this smart contract and user topology and provide analytical results and instructive numerical examples.

[class=AMS] \kwd[Primary ]60K35

smart contracts, cyber risk, operational risk, loss modeling, random graphs, insurance

1 Introduction

Technology. In its core, blockchain technology represents an open but distributed ledger where transactions between parties are recorded in verifiable and immutable ways [8]. Blockchains emerged in global public spheres in 2008 with the advent of Bitcoin digital currency, and was conceptually and analytically founded by the now legendary work of [16].

Prescient when voiced and skillfully phrased by [23], smart contracts are first defined as “a set of promises, specified in digital form, including protocols within which the parties perform on these promises”. From a software engineering perspective, smart contracts can be described as self-executing scripts running on blockchain platforms that can be both private, public or consortium and semi-private blockchains.

Present and future. Today, the penetration of blockchain technology is a wide spread phenomenon across industries and its use is accelerating [9]. The largest public blockchain platform that offers smart contract capabilities is Ethereum. The digital currency of the Etherium platform is Ether (ETH) which has market capitalization111See https://coinmarketcap.com/currencies/ethereum/. around 27 billion USD, with 24h volume of trade around 9 billion USD. The number222See https://cointelegraph.com/news/ethereum-smart-contracts-up-75-to-almost-2m-in-march. of platform hosted smart contracts, i.e., blockchain stored scripts that can be coded in Solidity language, has recently reached almost 2 million.

The promises of increased efficiencies of economic transactions and automated interactions between economical agents, novel ways of resource utilization and monetization, data integrity and privacy [21], etc. are tantalizing (see [22] or [25]). Blockchain enabled technologies, which includes smart contract technology, are estimated to produce business value-add growth by 2025 ranging in 176 billion USD333See Lovelock, J. and Furlonger, D., 2017. Three Things CIOs Need to Know About the Blockchain Business Value Forecast. Published by Gartner.. Most strikingly, the World Economic Forum [20] survey of 800 information and communications executives and experts reveals belief that around ten percent of global GDP would be found on blockchain systems by year 2027. Therefore, it is increasingly being recognized that, associated with digital assets, in conjunction with smart contracts, blockchain technology offers novel ways of organizing the economy and even the society across myriad of everyday interactions.

Risk. As any novel technology, the smart contract technology comes with its own risks [17] that expose its users to potentially unforeseen liabilities. Contagious losses can originate from many sources starting with coding errors [1], malicious cyber attacks [14] or even under-optimized smart contracts [3]. Notwithstanding the smaller ones, the losses can be of considerable size, and the now infamous 2016 Ethereum DAO attack [15], where over 50 million USD worth of Ethereum were misappropriated, looms large as an example of a potential liability. Another example is the 2017 parity multi-signature wallet attack444See https://cointelegraph.com/news/parity-multisig-wallet-hacked-or-how-come where around 30 million USD then equivalent value of Ethers was stolen and subsequently due to exploited code vulnerability the equivalent of around 150 million USD permanently rendered inaccessible. Also, in 2018, MyEtherWallet555See https://www.theverge.com/2018/4/24/17275982/myetherwallet-hack-bgp-dns-hijacking-stolen-ethereum. had its about 17 million USD worth in Ether stolen. Sadly, the future does not appear without clouds as the current research suggests. The recent findings [17] show that at least around 30,000 current Ethereum smart contracts are at risk due to their particular characteristics.

That is why in this work, we define a smart contract risk as a risk of financial loss due to cyber attacks or contagious failures of smart contracts. The risk can originate from the smart contract under consideration, or its users, or other smart contracts the smart contract under consideration communicates with during the course of its execution, or their users. The losses may be the result of misappropriation or misallocation of funds belonging to wallets of users or smart contracts under consideration. Consequently, from management perspective, if liability is left poorly understood, the risks arising from application of this novel technology may jeopardize platform providers or stifle decisions for their faster adoption.

Challenge. The characterization of loss distribution is widely used approach for quantification of the frequency and severity distributions of operational risk losses (see [19]). In practice, the empirical loss distribution becomes available after sufficient time has passed so that sufficiently large number of loss observations can be collected. Unfortunately, in the case of smart contract risk, due to the lack of data, there exist no empirical loss distributions in proper sense . What is currently available is a handful of recorded losses spread across smart contract platforms and partially recorded as anecdotes in the academic literature. In particular, there is insufficient information for the creation of empirical loss distributions and thus characterization of the risk from a statistical/empirical perspective. Sadly, in short term, the future offers no hope here. In fact, this situation suggests a different approach, namely the creation of structural models for the loss distribution, which this work addresses. To our knowledge, this is the first work that is concerned with the characterization of smart contract risks from probabilistic perspective and develops credible and practical structural models for the loss distribution. As such, this work paves the way for insurers to price smart contract risks, which is highly relevant in decisions for creating new smart contract risk related insurance product lines.

Mathematical Conceptualization. Conceptually, we envision the smart contract under consideration as the root vertex of a random tree call graph [5, 18]. Call graphs are comprised of vertices that are smart contracts interacting directly or indirectly with the smart contract under consideration during its execution. These smart contracts can be seen as offspring of the root smart contract in an undirected tree graph. For their proper performance, these smart contracts might rely on the execution of some other smart contracts which they call. Those would be, in turn, their offspring and so on up to some distance from the root smart contract. Here, random graphs are used to conceptualize the dynamical nature of call graphs. At any given time, the smart contract under consideration can have different patterns of communication with some (or none) offspring smart contracts which, in turn, might have smart contracts they communicate with in temporally inhomogeneous ways. The authors of [5] investigated nearly 200,000 smart contracts on Etherium platform and, among those that call other smart contracts, which was a majority, they found that only a small number of call graphs had loops. This motivates the use of tree graphs, i.e., graphs with no loop, to model the network of smart contracts. Each of the smart contracts in this structure may in principle have users it interacts with. Assuming that the users are not shared among different smart contracts, the random tree-stars graph structure naturally emerges.

We use a two-parameter bond percolation model to describe the contagion process among smart contracts and their users. Bond percolation was introduced in [2]. For a pedagogical and thorough introduction to percolation, we refer the reader to [6], while a brief overview of the main results is available in [13, chapter 13]. There is a wide variety of contagion processes one can choose from as a model component in framework building. However, to our knowledge, there is no extensive empirical study of contagions in smart contracts (certainly a valuable research question to be addressed in the future) so the choice of contagion process is left to the modelers. That is why, given the lack of an empirical study, it is natural to assume that the way smart contracts interact is strongly influenced by random factors and the topology of the call graph. All considered, in our framework we use bond percolation as a starting model of contagion among the models that account for both stochasticity and network structure, and leave other choices to future research.

As a final modeling choice in our proposed framework, we also include a configuration of monetary assets on the network, i.e., we attach a monetary asset with a certain dynamic value to each node of the network, either of user type or of smart contract type. Simply put, we assume that users and smart contracts, in their wallets, hold some assets that have a monetary value at any given time. This arrangement of monetary values across the network constitutes a cost topology. The compromise of a node in the network (due to a cyber attack, an operational failure, etc.) entails the loss of the monetary asset and its value. To account for the dynamical nature of these assets across time and over the evolving network, we assume that the asset values are represented by random variables. The percolation model then defines the contagion process stemming from the event of a node being compromised given a particular temporal instance of the tree-stars network topology. Finally, the sum of all the losses, given the particular first node being compromised and the realization of the associated contagion process, characterizes one observation point in the aggregate loss distribution due to cyber attacks or operational failures of smart contracts.

In this setting, we give analytical and numerical results related to the mean and the variance of the aggregate loss distribution.

We emphasize that our results hold for arbitrarily large random tree-stars graphs, and for all possible choices of the parameters of the bond percolation

model and the distribution of the asset values.

The rest of this paper is organized as follows. In Section 2, the mathematical framework to model loss due to cyber attacks and/or operational failures is developed. Section 3 presents the main analytical and numerical results about the mean and variance of the loss distribution. The remaining section contains the proofs of the analytical results.

2 Framework for the aggregate loss

We model the aggregate loss up to time

using a continuous-time Markov chain that consists of the combination of a Poisson process representing the times at which contagions strike,

the random graph representing the evolving connections among smart contracts and users, a percolation process on this random graph modeling the

spread of the contagion, and a collection of independent random variables on the vertex set representing the evolving monetary assets.

For the purpose of understanding the main characteristics of loss distribution and risk pricing, the main objective is to study the mean and the variance of the

random variable .

From a probabilistic perspective, random graphs relevant for our problem consist of the composition of a random tree and a

collection of random stars.

The former models the connections among the smart contracts whereas the latter models the connections between smart contracts and users.

Because the network consists of a two layers, it is natural to include two percolation parameters:

one parameter representing the probability that the contagion spreads across an edge connecting two smart contracts and another parameter representing

the probability that the contagion spreads across an edge connecting a smart contract and a user.

Similarly, we consider two different distributions for the local costs (monetary assets), one modeling the loss resulting from a smart contract’s wallet

being compromised, and another one modeling the loss resulting from a user’s wallet being compromised. More precisely, the process is constructed using the following components:

-

•

A Poisson process with intensity .

-

•

A random graph consisting of the combination of a random rooted tree with radius and offspring distribution described by a random variable , and random stars with degree described by a random variable , with probability mass functions

-

•

Two percolation parameters .

-

•

A random variable describing the loss due to a smart contract being compromised.

-

•

A random variable describing the loss due to a user being compromised.

The process evolves as follows. At the arrival times

of the Poisson process, we let be a realization of the random graph modeling the connections among smart contracts and users

at the time of the th contagion.

To construct this random graph, we draw edges starting from a root 0, meaning edges with probability , and additional edges starting

from each of the subsequent vertices using the same probability distribution.

The construction stops after steps, which results in

where represents the set of smart contracts. Then, from each smart contract , we independently draw edges, meaning edges with probability , thus creating

The leaves of the star represent the users connected to smart contract , and we assume that each user is connected to only one smart contract. Letting be the set of all users, and be the set of all edges connecting a user to a smart contract, the construction results in a random graph

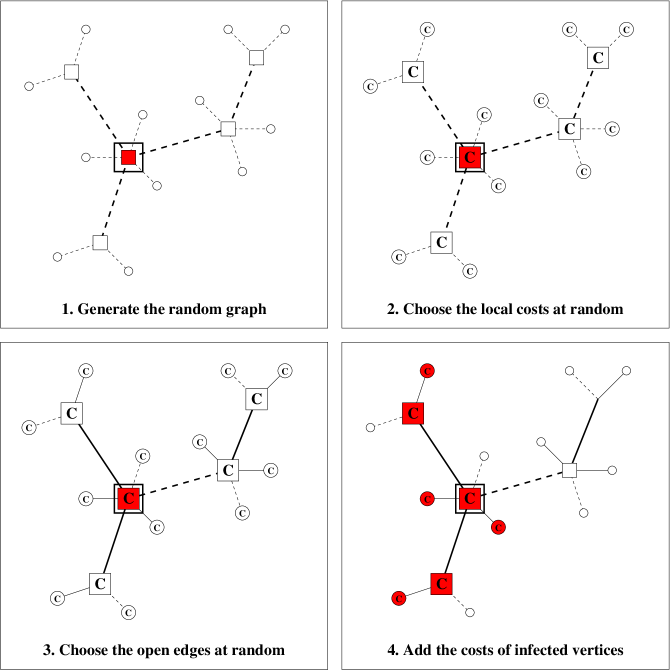

See the top-left panel of Figure 1 for a picture where the squares represent the smart contracts and the circles represent the users.

To quantify the financial loss, we attach a random local cost to each vertex representing the loss resulting from vertex being compromised. More precisely, we let

be independent.

Considering two different distributions for the local costs is motivated by the fact that the loss due to a smart contract being compromised in principle may be significantly

different from the loss due to a user being compromised.

See the top-right panel of Figure 1 for a picture.

To model the contagion itself, we use the framework of percolation theory, and more precisely, bond percolation (percolation on the edges).

That is, we let

be independent. Following the terminology of percolation theory, edges with are said to be open. See the bottom-left panel of Figure 1 for a picture where the solid edges are open and the dashed edges are closed. Given that the contagion starts at vertex , which we call from now on the origin of the contagion, the set of vertices that get compromised is

called the open cluster starting at .

See the bottom-right panel of Figure 1 for a picture where the open cluster starting at the root is represented in red.

For the purpose of loss modeling, we are only interested in the vertices being compromised and their cost in certain subsets depending on the

origin of the contagion.

Therefore, instead of just considering the total size and the total cost of the contagion, we define more generally two collections of random

variables as follows.

For every subset , we let be the number of vertices in that are compromised at time .

In equation, this can be written as

Similarly, we define the financial loss restricted to subset as

the sum of the local costs of all the vertices that are in subset and that are compromised, i.e., in the open cluster starting at the origin of

the contagion.

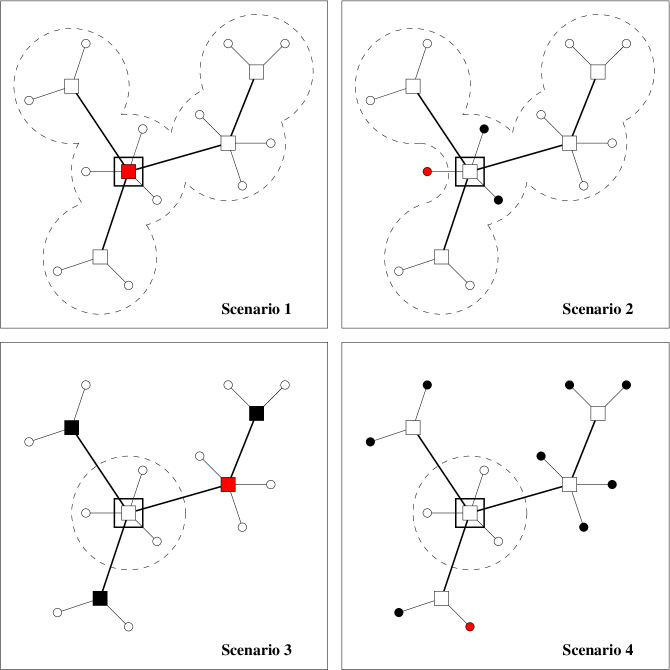

To complete the mathematical description of the loss resulting from a single contagion, we still need to explain how the origin and the subset are chosen. There are four distinct risk scenarios, and we assume that scenario occurs with probability at each arrival time of the Poisson process independently of everything else. The four scenarios are as follows.

-

1.

The contagion is due to the smart contract at the root being compromised. In this case, the origin of the contagion is the root and the loss is the total loss over all the network so

-

2.

The contagion is due to a user of the smart contract at the root compromising this smart contract. In this case, the origin is chosen uniformly at random from the set of users of the root, and the loss that is of interest is the total loss except for the user which originates the compromising activity, so

-

3.

The contagion is due to one of the smart contracts excluding the root being compromised. In this case, the origin of the contagion is chosen at random from the set of smart contracts other than the root and, from the perspective of the smart contract at the root, the loss which is of interest is the loss restricted to the smart contract at the root and its users so

-

4.

The contagion is due to a user of one of the smart contracts other than the root compromising this smart contract. In this case, the origin is chosen uniformly at random from the set of users of the smart contracts other than the root, and the loss which is of interest is again the loss restricted to the smart contract at the root and its users so

See Figure 2 for a picture of the four scenarios. Note that the four sets representing the possible origins of the contagion in the four scenarios form a partition of the network, therefore our model and analysis cover all possibilities.

Finally, the random variable is defined as the aggregate financial loss caused by all the contagions that occur between time zero and time . In equation,

For the purpose of loss distribution characterization and risk pricing, the main objective is to compute the expected value and the variance of the aggregate loss . Since the financial losses resulting from different contagions are independent, and because the losses resulting from contagions of the same type are identically distributed, the mean and variance of the aggregate loss can be deduced from the mean and variance of the loss resulting from a single contagion. In particular, we first focus on the loss resulting from a single contagion of type , and drop all the superscripts referring to the number of the contagion to avoid cumbersome notations.

3 Main results

This section presents our analytical and numerical results about the loss distribution.

Analytical results. As previously mentioned, we first study the loss resulting from a single contagion in the context of scenario , for . To keep the notation short, we write

for all , and similar notation for the cost. Also, the conditional probability of an event given the distribution of the origin are written as

and similar notation for the conditional mean, variance and covariance. The superscript emphasizes that the contagion starts from a smart contract, while the superscript emphasizes that the contagion starts from a user. The mean and variance of the loss resulting from a contagion in scenario are written and , respectively. In particular,

and similarly for the variance. We first recall a result from [10] that will be useful later to study the mean and variance in scenarios 1 and 2. In the absence of users, i.e.,

in which case the parameter and the distribution are unimportant, the mean and the variance of the size of the contagion have already been studied in detail by the authors in [10]. Using the notation above, their result gives exact expressions of the mean and the variance of the size given that the contagion starts from the root of the graph. To state this result, let

be the mean and the variance of the number of edges starting from each smart contract and connecting two smart contracts. Comparing the size of the contagion with the number of individuals up to generation in a certain branching process gives the following result from [10].

Theorem 1

– For a contagion starting at the root,

Our first result below shows how the conditional mean and variance of the total loss relate to the conditional mean and variance of the size given that the contagion starts from a smart contract . This can be used in combination with Theorem 1 to obtain the conditional mean and variance in scenario 1. To state our result, as we did for , we let

be the mean and the variance of the number of users connected to a given smart contract. By conditioning on the size , one can express the conditional mean and variance of the loss as a function of the conditional mean and variance of as follows.

Theorem 2

– For all ,

where the mean and variance of are

Taking in the theorem gives the mean and variance of the total loss as a function of the mean and variance of which, in turn, are given in Theorem 1. In particular, combining Theorems 1 and 2 directly gives the mean and variance in the first scenario. Even though the result is an obvious corollary of the first two theorems, we state it as a theorem for completeness.

Theorem 3 (scenario 1)

Recall that, in scenario 2, the contagion starts from one of the users of the root contract chosen uniformly at random. This user tries to compromise the network and the relevant loss consists of the cumulative cost of all the compromised vertices except for the originator. The key idea to study this scenario is to condition on the state of edge , where is a user of the root contract, in order to express the conditional mean and variance of the loss given that the contagion starts from as a function of the mean and variance given that the contagion starts from the root. Because the latter is known from Theorem 3, this leads to an explicit expression for the mean and variance in scenario 2. More precisely, we have the following theorem.

Theorem 4 (scenario 2)

In the last two scenarios, the objective is to study the loss restricted to the root contract and its users when the contagion starts from outside this set. This is more difficult than the first two scenarios, but we can derive exact expressions in the context of deterministic graphs. Note however that the contagion process is still stochastic. More precisely, we assume that

In this case, and , therefore Theorem 2 gives

| (1) |

Because in scenarios 3 and 4 the loss is strictly positive if and only if the root gets compromised, it can be proved that the mean and variance when the contagion starts from outside are connected to the mean and variance in (1) through the probability of the event

The probability of this event and how the mean and variance in scenarios 3 and 4 are related to (1) above are given in the following theorem.

Theorem 5 (scenarios 3 and 4)

– For and ,

In scenarios 3 and 4, the mean and variance are then given by

where and are given in (1).

Our last task is to combining Theorems 3–5 to deduce the mean and variance of the aggregate financial loss up to time . Recall that scenario occurs with probability at each arrival time of the Poisson process independently of everything else, and let

By the thinning property of Poisson processes, the processes are independent Poisson processes with intensity , from which it follows that

In particular, conditioning on , we get

| (2) |

Using also that the contagions at different times (and therefore the loss resulting from these contagions) are independent, and applying the law of total variance,

| (3) |

Combining (2) and (3) with all our theorems gives explicit expressions for the mean and the variance of the random variable , as desired for the purpose of insurance pricing.

Numerical results. Under various parameter settings, we investigate the expectation and variance of loss distribution666The characterization of and allow for straight forward calculation of actuarial fair risk, expectation principle based as well as standard deviation principle based risk premium for smart contract risk ([4] and [11]). of smart contract risk given the developed model.

Without loss of generality we assume and have the profit loading factor . Further, we assume , thus the attacks occur at rate one per unit of time777In practice, for parameter , a platform provider would use it’s internal statistics related to attack rates.. For illustrative purposes, two choices of probability mass function for random smart contract tree edge formation are considered.

First, the smart contract tree with probabilistic formation of edges under consideration is characterized by the probability mass function .

Hence, for each vertex, i.e., smart contract, the probability of zero offspring with this choice is equal to zero.

The probability of one offspring of a smart contract is and the probability of two offspring of a smart contract is .

Thus, a given smart contract will, with probability 0.4, have one offspring smart contract it communicates with and, with probability 0.6,

two offspring smart contracts it communicates with.

Second, we consider a deterministic smart contract tree characterized by the probability mass function of edge formation .

In number of smart contract vertices, this tree dominates stochastically the above chosen tree with probabilistic formation,

given the same radius .

Across all experiments the common radius of the trees is chosen to be .

Under the assumption of log-normal distributions for both and , we allow for three cost

topologies (see Table 1).

These costs materialize when smart contract and user wallets are compromised.

The cost topologies under consideration are characterized by three cases of means and standard deviations.

The choice of expectation of cost for the smart contracts (see second column in the table)

is stylized, kept to 10,000 monetary units, and made consistent across all cost cases.

Similarly, the choice of expectation of cost for the users (see fourth column)

is stylized, kept to 1,000 monetary units, and made consistent across all cost cases as well.

The standard deviation of cost for the smart contracts (see third column)

in a stylized fashion is allowed to change across cases, alternating between 0 and 5,000.

Similarly, the standard deviation of cost for the users (see fifth column)

is also allowed to change across cases, alternating between 0 and 500.

| Smart Contracts | Users | |||

| Expectation | Deviation | Expectation | Deviation | |

| Cost | of Cost | of Cost | of Cost | of Cost |

| Topology | ||||

| I | 10000 | 0 | 1000 | 0 |

| \cdashline1-5[0.4pt/1pt] II | 10000 | 5000 | 1000 | 0 |

| \cdashline1-5[0.4pt/1pt] III | 10000 | 0 | 1000 | 500 |

Two cases for the probability of smart contract edge contagion888In practice, to choose the probability of the edge contagion , a platform provider (e.g. Ethereum) may perform risk classification by clustering their ecosystem of smart contracts across a predetermined set of features.

The academic literature [7, 12, 24] or best

practices (e.g. https://consensys.github.io/smart-contract-best-practices/) can guide the choice of such features.

Alternatively, to create best practices, platform providers should consult smart contract audit providers that perform pre deployment smart contract analysis

and consulting.

Regretfully, the true value of is unknowable and practically unattainable.

Thus, for found risk classes, according to their riskiness, and based on its judgment, a platform provider should impute values of edge contagion given their own internal expert knowledge. are considered:

low probability of edge contagion characterized by and high probability of edge contagion characterized by .

Likewise, two cases for the probability of user edge contagion999In practice, to choose the probability of the edge contagion , a platform provider should make considerations similar to when choosing parameter . are considered:

low probability of user edge contagion characterized by and high probability of user edge contagion characterized by .

Within this numerical experiment setting, to calculate the moments for loss distribution of smart contract risk, we perform ten million simulations.

Our unreported trials confirm that this number of simulations is sufficient to achieve desired prices stability and accuracy.

This is additionally supported by the congruency between the simulation based results and the analytical results, as shown in Tables 2

and 3 where the difference between simulation and analytical results does not exceed one percent.

For the sake of brevity, and because our findings based on numerical simulations are the same in all four scenarios, we only investigate the first

and third scenarios101010The simulation results for scenario 2 and scenario 4 are available on request..

Recall that, in scenario 1 (see Table 2), the contagion starts from the root contract.

Here, there are several insights that can be deduced from our numerical results.

-

•

First, everything else being fixed, offspring distributions that result in a stochastically higher number of vertices (for both smart contracts and users) consistently lead to higher means and variances. Hence, the stochastic “size” of the interactions impacts the moments: the bigger the network, the higher the moments.

-

•

Second, across all parameter settings, the fact that both smart contracts and users costs change in time (which is captured by random variables with differently parameterized distributions) makes an impact on the moments of loss distribution. Further, as expected, increasing the variance of the the costs while keeping their expectation fixed results in an increase of the variance of loss distribution. Also, the impact of variability of costs of smart contracts versus variability of costs of users is, in principle, different.

Recall that, in scenario 3 (see Table 3), the origin of the contagion is chosen uniformly at random from the set of smart contracts other than the root. Following the analytical results, the simulations for this scenario were only performed when the tree-stars graph is deterministic. Here, several insights can be deduced from our numerical results.

-

•

First, across all parameter settings in scenario 3, when compared to the corresponding settings in scenario 1, we observe significantly lower moments of the loss distribution.

-

•

Second, similarly to scenario 1, higher the levels of contagion parameters higher the moments.

Given the high dimension of the parameter space of the model and the number of scenarios, many more numerical investigations are conceivable. They are not given here both because of the constrains of space and because of the essentially intuitively obvious impact of the parameters. More importantly, we point out that the analytical results can be used to obtain the exact values of the moments in the context of scenarios 1 and 2, whereas they are limited to deterministic smart contracts/users networks in the context of scenarios 3 and 4. In contrast, the simulation based approach does not suffer any such constraints. In addition, the almost perfect match between our analytical and numerical results in the cases covered by our theorems validates our numerical results. In particular, our simulations are reliable enough to give extremely good approximations of the moments in all four scenarios and for any possible choices of the random tree-stars graph and network topology.

| Analytical Results | Simulation Results | ||||||

| Number of simulations: 10000000. | Expectation | Deviation | Expectation | Deviation | |||

| Contagion scenario: | of Loss | of Loss | of Loss | of Loss | |||

| Cost | Smart contracts | Users | Contagion | ||||

| Topology | |||||||

| [0.0,0.0,1.0] | [0.0,0.0,0.0,0.0,1.0] | (0.8,0.8) | 68112.00 | 21666.32 | 68103.05 | 21668.17 | |

| [0.0,0.0,1.0] | [0.0,0.1,0.2,0.3,0.4] | (0.8,0.8) | 63984.00 | 20423.47 | 63986.51 | 20429.11 | |

| [0.0,0.4,0.6] | [0.0,0.0,0.0,0.0,1.0] | (0.8,0.8) | 51722.88 | 21560.68 | 51729.05 | 21564.09 | |

| [0.0,0.4,0.6] | [0.0,0.1,0.2,0.3,0.4] | (0.8,0.8) | 48588.16 | 20307.61 | 48589.85 | 20304.28 | |

| \cdashline2-8[0.4pt/1pt] | [0.0,0.0,1.0] | [0.0,0.0,0.0,0.0,1.0] | (0.8,0.2) | 55728.00 | 17757.75 | 55726.09 | 17764.73 |

| [0.0,0.0,1.0] | [0.0,0.1,0.2,0.3,0.4] | (0.8,0.2) | 54696.00 | 17414.61 | 54695.96 | 17412.82 | |

| [0.0,0.4,0.6] | [0.0,0.0,0.0,0.0,1.0] | (0.8,0.2) | 42318.72 | 17664.04 | 42308.19 | 17666.34 | |

| [0.0,0.4,0.6] | [0.0,0.1,0.2,0.3,0.4] | (0.8,0.2) | 41535.04 | 17326.01 | 41532.69 | 17326.06 | |

| \cdashline2-8[0.4pt/1pt] I | [0.0,0.0,1.0] | [0.0,0.0,0.0,0.0,1.0] | (0.2,0.8) | 20592.00 | 11514.53 | 20590.19 | 11514.84 |

| [0.0,0.0,1.0] | [0.0,0.1,0.2,0.3,0.4] | (0.2,0.8) | 19344.00 | 10856.65 | 19340.23 | 10853.55 | |

| [0.0,0.4,0.6] | [0.0,0.0,0.0,0.0,1.0] | (0.2,0.8) | 18775.68 | 9816.03 | 18779.33 | 9820.13 | |

| [0.0,0.4,0.6] | [0.0,0.1,0.2,0.3,0.4] | (0.2,0.8) | 17637.76 | 9263.84 | 17638.57 | 9260.89 | |

| \cdashline2-8[0.4pt/1pt] | [0.0,0.0,1.0] | [0.0,0.0,0.0,0.0,1.0] | (0.2,0.2) | 16848.00 | 9438.48 | 16848.34 | 9437.55 |

| [0.0,0.0,1.0] | [0.0,0.1,0.2,0.3,0.4] | (0.2,0.2) | 16536.00 | 9255.56 | 16535.89 | 9257.05 | |

| [0.0,0.4,0.6] | [0.0,0.0,0.0,0.0,1.0] | (0.2,0.2) | 15361.92 | 8050.01 | 15365.43 | 8055.28 | |

| [0.0,0.4,0.6] | [0.0,0.1,0.2,0.3,0.4] | (0.2,0.2) | 15077.44 | 7892.24 | 15077.99 | 7893.62 | |

| [0.0,0.0,1.0] | [0.0,0.0,0.0,0.0,1.0] | (0.8,0.8) | 68112.00 | 24462.81 | 68099.27 | 24461.01 | |

| [0.0,0.0,1.0] | [0.0,0.1,0.2,0.3,0.4] | (0.8,0.8) | 63984.00 | 23369.17 | 63964.57 | 23373.77 | |

| [0.0,0.4,0.6] | [0.0,0.0,0.0,0.0,1.0] | (0.8,0.8) | 51722.88 | 23723.89 | 51731.94 | 23722.85 | |

| [0.0,0.4,0.6] | [0.0,0.1,0.2,0.3,0.4] | (0.8,0.8) | 48588.16 | 22591.12 | 48592.92 | 22584.33 | |

| \cdashline2-8[0.4pt/1pt] | [0.0,0.0,1.0] | [0.0,0.0,0.0,0.0,1.0] | (0.8,0.2) | 55728.00 | 21079.32 | 55729.30 | 21082.61 |

| [0.0,0.0,1.0] | [0.0,0.1,0.2,0.3,0.4] | (0.8,0.2) | 54696.00 | 20791.07 | 54694.60 | 20789.54 | |

| [0.0,0.4,0.6] | [0.0,0.0,0.0,0.0,1.0] | (0.8,0.2) | 42318.72 | 20247.92 | 42319.76 | 20247.80 | |

| [0.0,0.4,0.6] | [0.0,0.1,0.2,0.3,0.4] | (0.8,0.2) | 41535.04 | 19953.72 | 41533.41 | 19953.31 | |

| \cdashline2-8[0.4pt/1pt] II | [0.0,0.0,1.0] | [0.0,0.0,0.0,0.0,1.0] | (0.2,0.8) | 20592.00 | 13099.02 | 20588.87 | 13099.83 |

| [0.0,0.0,1.0] | [0.0,0.1,0.2,0.3,0.4] | (0.2,0.8) | 19344.00 | 12524.65 | 19340.46 | 12525.41 | |

| [0.0,0.4,0.6] | [0.0,0.0,0.0,0.0,1.0] | (0.2,0.8) | 18775.68 | 11485.40 | 18769.41 | 11478.62 | |

| [0.0,0.4,0.6] | [0.0,0.1,0.2,0.3,0.4] | (0.2,0.8) | 17637.76 | 11017.20 | 17640.30 | 11023.83 | |

| \cdashline2-8[0.4pt/1pt] | [0.0,0.0,1.0] | [0.0,0.0,0.0,0.0,1.0] | (0.2,0.2) | 16848.00 | 11317.46 | 16848.22 | 11314.42 |

| [0.0,0.0,1.0] | [0.0,0.1,0.2,0.3,0.4] | (0.2,0.2) | 16536.00 | 11165.37 | 16537.00 | 11164.44 | |

| [0.0,0.4,0.6] | [0.0,0.0,0.0,0.0,1.0] | (0.2,0.2) | 15361.92 | 10018.12 | 15366.09 | 10021.09 | |

| [0.0,0.4,0.6] | [0.0,0.1,0.2,0.3,0.4] | (0.2,0.2) | 15077.44 | 9891.79 | 15078.96 | 9894.34 | |

| [0.0,0.0,1.0] | [0.0,0.0,0.0,0.0,1.0] | (0.8,0.8) | 68112.00 | 21666.32 | 68112.36 | 21757.41 | |

| [0.0,0.0,1.0] | [0.0,0.1,0.2,0.3,0.4] | (0.8,0.8) | 63984.00 | 20423.47 | 63989.54 | 20492.10 | |

| [0.0,0.4,0.6] | [0.0,0.0,0.0,0.0,1.0] | (0.8,0.8) | 51722.88 | 21560.68 | 51716.16 | 21634.02 | |

| [0.0,0.4,0.6] | [0.0,0.1,0.2,0.3,0.4] | (0.8,0.8) | 48588.16 | 20307.61 | 48579.16 | 20368.48 | |

| \cdashline2-8[0.4pt/1pt] | [0.0,0.0,1.0] | [0.0,0.0,0.0,0.0,1.0] | (0.8,0.2) | 55728.00 | 17757.75 | 55731.34 | 17786.87 |

| [0.0,0.0,1.0] | [0.0,0.1,0.2,0.3,0.4] | (0.8,0.2) | 54696.00 | 17414.61 | 54692.31 | 17438.72 | |

| [0.0,0.4,0.6] | [0.0,0.0,0.0,0.0,1.0] | (0.8,0.2) | 42318.72 | 17664.04 | 42317.99 | 17686.78 | |

| [0.0,0.4,0.6] | [0.0,0.1,0.2,0.3,0.4] | (0.8,0.2) | 41535.04 | 17326.01 | 41537.19 | 17338.98 | |

| \cdashline2-8[0.4pt/1pt] III | [0.0,0.0,1.0] | [0.0,0.0,0.0,0.0,1.0] | (0.2,0.8) | 20592.00 | 11514.53 | 20591.05 | 11567.02 |

| [0.0,0.0,1.0] | [0.0,0.1,0.2,0.3,0.4] | (0.2,0.8) | 19344.00 | 10856.65 | 19345.33 | 10903.39 | |

| [0.0,0.4,0.6] | [0.0,0.0,0.0,0.0,1.0] | (0.2,0.8) | 18775.68 | 9816.03 | 18774.70 | 9875.13 | |

| [0.0,0.4,0.6] | [0.0,0.1,0.2,0.3,0.4] | (0.2,0.8) | 17637.76 | 9263.84 | 17636.26 | 9308.82 | |

| \cdashline2-8[0.4pt/1pt] | [0.0,0.0,1.0] | [0.0,0.0,0.0,0.0,1.0] | (0.2,0.2) | 16848.00 | 9438.48 | 16844.12 | 9452.76 |

| [0.0,0.0,1.0] | [0.0,0.1,0.2,0.3,0.4] | (0.2,0.2) | 16536.00 | 9255.56 | 16533.49 | 9265.07 | |

| [0.0,0.4,0.6] | [0.0,0.0,0.0,0.0,1.0] | (0.2,0.2) | 15361.92 | 8050.01 | 15356.57 | 8062.96 | |

| [0.0,0.4,0.6] | [0.0,0.1,0.2,0.3,0.4] | (0.2,0.2) | 15077.44 | 7892.24 | 15076.54 | 7904.62 | |

| Analytically Calculated Premium | Simulation Based Premium | ||||||

| Number of simulations: 10000000. | Expectation | Deviation | Expectation | Deviation | |||

| Contagion scenario: | of Loss | of Loss | of Loss | of Loss | |||

| Cost | Smart contracts | Users | Contagion | ||||

| Topology | |||||||

| [0.0,0.0,1.0] | [0.0,0.0,0.0,0.0,1.0] | (0.8,0.8) | 9152.00 | 6122.99 | 9151.82 | 6122.94 | |

| I | [0.0,0.0,1.0] | [0.0,0.0,0.0,0.0,1.0] | (0.8,0.2) | 7488.00 | 5024.34 | 7487.80 | 5023.78 |

| [0.0,0.0,1.0] | [0.0,0.0,0.0,0.0,1.0] | (0.2,0.8) | 1232.00 | 3847.64 | 1231.56 | 3847.14 | |

| [0.0,0.0,1.0] | [0.0,0.0,0.0,0.0,1.0] | (0.2,0.2) | 1008.00 | 3151.20 | 1008.40 | 3151.87 | |

| [0.0,0.0,1.0] | [0.0,0.0,0.0,0.0,1.0] | (0.8,0.8) | 9152.00 | 7404.35 | 9151.30 | 7404.43 | |

| II | [0.0,0.0,1.0] | [0.0,0.0,0.0,0.0,1.0] | (0.8,0.2) | 7488.00 | 6525.13 | 7486.59 | 6524.63 |

| [0.0,0.0,1.0] | [0.0,0.0,0.0,0.0,1.0] | (0.2,0.8) | 1232.00 | 4139.76 | 1229.37 | 4133.33 | |

| [0.0,0.0,1.0] | [0.0,0.0,0.0,0.0,1.0] | (0.2,0.2) | 1008.00 | 3501.91 | 1007.76 | 3500.73 | |

| [0.0,0.0,1.0] | [0.0,0.0,0.0,0.0,1.0] | (0.8,0.8) | 9152.00 | 6168.12 | 9152.88 | 6168.27 | |

| III | [0.0,0.0,1.0] | [0.0,0.0,0.0,0.0,1.0] | (0.8,0.2) | 7488.00 | 5038.12 | 7490.12 | 5036.94 |

| [0.0,0.0,1.0] | [0.0,0.0,0.0,0.0,1.0] | (0.2,0.8) | 1232.00 | 3857.33 | 1232.50 | 3857.91 | |

| [0.0,0.0,1.0] | [0.0,0.0,0.0,0.0,1.0] | (0.2,0.2) | 1008.00 | 3154.16 | 1007.68 | 3153.85 | |

Conclusion. In this paper, we develop a dynamic structural percolation model for the aggregate loss distribution due to cyber attacks on and contagious failures of smart contracts assuming a tree-stars topology of smart contracts and their users. By focusing on network topologies where cycles are not allowed and by imposing, based on percolation theory, parsimonious contagion processes on such networks, coupled with the introduction of a topology of costs, we distinguish four different use cases or scenarios. Based on them, we robustly reduce the complexity of smart contract risk phenomena and allow for its effective modeling and loss distribution characterization. From a modeling standpoint, we allow for the dynamic nature of smart contracts and their users’ topology, as well as temporal uncertainty of costs both for smart contracts and users, which is captured using random variables with various distributions. Within a rigorous mathematical framework through probabilistic analysis, we characterize the mean and variance, which are the main aspects of the loss distribution of smart contract risk. Because smart contract risk may represent a significant emerging liability for platform providers, companies and individuals which adopt this technology, our work can prove to be of considerable value to decision-makers while simultaneously supporting the penetration of this nascent technology in the economy, and thus unleashing its new potentials.

There are two immediate opportunities for further research following this work. First, modeling smart contract risk in a general star-fully connected graph, to account for loops in call graphs. Second, modeling a collection (or ecosystem) of smart contracts with random interconnections, in order to ultimately characterize the aggregate risk smart contract platform providers can face.

4 Proofs

4.1 Theorem 2.

In this subsection, we prove Theorem 2 which shows how the mean and variance of the total loss relate to the mean and variance of the number of smart contracts being compromised. In this section and the next ones, we will repeatedly use that

where is the function

First, we compute the conditional mean and variance of the loss restricted to a smart contract and its users, given that the contagion starts from this smart contract, which corresponds to the second set of equations in the theorem.

Lemma 6

– For all ,

Proof.

To begin with, we write

| (4) |

Note also that, given that the contagion starts at smart contract , each of the users of this contract, say , is compromised with probability , therefore

| (5) |

Using (4) and (5), and conditioning on ,

| (6) |

while using also independence,

| (7) |

Taking the expected value in (6) gives

which proves the first part of the lemma. Using the law of total variance and adding the expected value of (7) and the variance of (6), we also get

which proves the second part of the lemma. ∎

We now show how the mean and variance of the total loss across the network relate to the mean and variance of the number of compromised smart contracts, and the mean and variance in Lemma 6, which corresponds to the first set of equations in the theorem.

Lemma 7

– For all ,

Proof.

4.2 Theorem 4 (scenario 2).

This subsection deals with scenario 2 where the contagion starts from one of the users of the root chosen uniformly at random. This user compromises the system and the relevant loss is the cumulative cost of all the compromised vertices, except for the originator. To begin with, we prove the theorem when the contagion starts from a deterministic vertex who is a user of the smart contract at the root. The main idea is to condition on whether

is open or closed in order to derive a relationship between the mean and variance of the loss when the contagion starts from and their counterparts when the contagion starts from the root, for which an explicit expression is known from Theorem 3.

Lemma 8

– For all ,

Proof.

Because the loss whenever edge is closed and the contagion starts at the root, and that edge is open with probability ,

This completes the proof. ∎

We now prove a weak version of the first part of Theorem 4 with the contagion starting from a specific user of the root rather than a user chosen uniformly at random.

Lemma 9

– For all ,

Proof.

Because when is closed,

| (9) |

Taking the expected value and applying Lemma 8, we conclude

This completes the proof. ∎

We now study the variance of the loss.

Lemma 10

– For all ,

Proof.

Let , . Because the unique self-avoiding path connecting and goes through the root, given that the contagion starts from the root, the events that gets compromised and that gets compromised are independent. This implies that

Since in addition the are independent,

Using also that when the contagion starts at the root,

Recalling that in distribution, the result follows. ∎

Lemma 11

– For all ,

Proof.

Because the expressions of the mean and variance given in Lemmas 9 and 11 are constant across all possible choices of the user of the smart contract at the root, the two lemmas hold more generally when the origin of the contagion is chosen uniformly at random from the set of all users of the root, a general result proved in the next lemma for any random variable.

Lemma 12

– Let be any random variable such that

Then and .

Proof.

Let be a realization of the random graph, and let be the number of users of the root for this realization. Observe that

| (11) |

where the sums are over the set . Then,

Similarly, taking the mean in the second equation in (11) gives

| (12) |

Also, using that the covariance is

taking the variance in the first equation in (11) gives

| (13) |

Using (12) and (13), and the law of total variance, we get

This completes the proof. ∎

4.3 Theorem 5 (scenarios 3 and 4).

Recall that, in scenarios 3 and 4, the contagion starts from a vertex outside , in which case the loss we are interested in is the cumulative loss of the smart contract at the root and the users of this smart contract. The starting point and common idea behind the proof of all the statements in Theorem 5 is the following: for all vertices

the unique self-avoiding path connecting and must go through the root. This implies that, when the contagion starts from vertex , the loss only if the root gets compromised. In particular, the conditional expected loss in both scenarios reduces to

| (14) |

and similarly for the conditional variance,

| (15) |

Equations (14) and (15) indicate that the mean and variance of the loss can be expressed using the mean and variance of the random variable . We now focus on scenario 3 in which the contagion starts from a smart contract chosen uniformly at random among all the smart contracts excluding the root. To begin with, we compute the mean of , which is the probability of .

Lemma 13

– For and ,

Proof.

To simplify the notation, we introduce

and denote by the distance between the root and the origin of the contagion. Using that the number of contracts at distance from the root is , the probability mass function of the distance can be written as follows: for all ,

| (16) |

Note also that, given that the contagion starts at , the root gets compromised if and only if the unique self-avoiding path from to the root is open. Because this path has edges and those edges are independently open with probability , we get

| (17) |

Combining (16) and (17), we deduce that

Recalling the definition of and , the lemma follows. ∎

The next natural step is to compute the variance of . To do so, we will use the following preliminary result about the covariance.

Lemma 14

– For all ,

Proof.

Lemma 15

– For and ,

Proof.

Using the previous results, we can now study the loss in scenario 3.

Lemma 16

– For and ,

Proof.

Finally, we deal with scenario 4 in which the contagion starts from a vertex chosen uniformly at random from the set of users excluding the users of the root contract. As previously, we start by computing the expected value of , which is the probability of .

Lemma 17

– For and ,

Proof.

Because , all the contracts have the same number of users, from which it follows that the distance in scenarios 3 and 4 are related as follows:

| (23) |

In addition, for all , the unique self-avoiding path from to the root has edges in the subset and one edge in the subset therefore

| (24) |

Combining (23) and (24), we conclude that

and the proof is complete. ∎

Using (23), and repeating the proof of Lemma 14, give

| (25) |

It also follows from (24) that when so

| (26) |

Repeating the proof of Lemma 15 using (25), and (26) in place of (18),

| (27) |

Finally, using (14) and (15) like in the proof of Lemma 16, together with (27), we get the mean and variance given in the second part of Theorem 5.

Acknowledgments

This work is partially supported by the NSF grant #CNS-2000792. Additionally, Petar Jevtić expresses his gratitude to the ASU Center for Assured and Scalable Data Engineering, for their financial support and guidance.

References

- [1] Nicola Atzei, Massimo Bartoletti, and Tiziana Cimoli. A survey of attacks on ethereum smart contracts (sok). In Principles of Security and Trust, pages 164–186. Springer, 2017.

- [2] S. R. Broadbent and J. M. Hammersley. Percolation processes. I. Crystals and mazes. Proc. Cambridge Philos. Soc., 53:629–641, 1957.

- [3] Ting Chen, Xiaoqi Li, Xiapu Luo, and Xiaosong Zhang. Under-optimized smart contracts devour your money. In Software Analysis, Evolution and Reengineering (SANER), 2017 IEEE 24th International Conference on, pages 442–446. IEEE, 2017.

- [4] Paul Embrechts. Actuarial versus financial pricing of insurance. The Journal of Risk Finance, 1(4):17–26, 2000.

- [5] M Frowis and R Bohme. In code we trust?: Measuring the control flow immutability of all smart contracts deployed on ethereum. LNCS, 10436:357–372, 2017.

- [6] G. R. Grimmett. Percolation. Springer-Verlag, New York, 1989.

- [7] Ilya Grishchenko, Matteo Maffei, and Clara Schneidewind. A semantic framework for the security analysis of ethereum smart contracts. In International Conference on Principles of Security and Trust, pages 243–269. Springer, 2018.

- [8] Marco Iansiti and Karim R Lakhani. The truth about blockchain. Harvard Business Review, 95(1):118–127, 2017.

- [9] CB Insights. Banking is only the start: 20 big industries where blockchain could be used. CB Insights, 25, 2016.

- [10] Petar Jevtić and Nicolas Lanchier. Dynamic structural percolation model of loss distribution for cyber risk of small and medium-sized enterprises for tree-based LAN topology. Insurance Math. Econom., 91:209–223, 2020.

- [11] Rob Kaas, Marc Goovaerts, Jan Dhaene, and Michel Denuit. Modern actuarial risk theory: using R, volume 128. Springer Science & Business Media, 2008.

- [12] Sukrit Kalra, Seep Goel, Mohan Dhawan, and Subodh Sharma. Zeus: Analyzing safety of smart contracts. NDSS, 2018.

- [13] Nicolas Lanchier. Stochastic modeling. Springer, 2017.

- [14] Yuval Marcus, Ethan Heilman, and Sharon Goldberg. Low-resource eclipse attacks on ethereum’s peer-to-peer network. IACR Cryptology ePrint Archive, 2018:236, 2018.

- [15] Muhammad Izhar Mehar, Charles Louis Shier, Alana Giambattista, Elgar Gong, Gabrielle Fletcher, Ryan Sanayhie, Henry M Kim, and Marek Laskowski. Understanding a revolutionary and flawed grand experiment in blockchain: The dao attack. Journal of Cases on Information Technology (JCIT), 21(1):19–32, 2019.

- [16] Satoshi Nakamoto. Bitcoin: A peer-to-peer electronic cash system. 2008.

- [17] Ivica Nikolić, Aashish Kolluri, Ilya Sergey, Prateek Saxena, and Aquinas Hobor. Finding the greedy, prodigal, and suicidal contracts at scale. In Proceedings of the 34th Annual Computer Security Applications Conference, pages 653–663, 2018.

- [18] Barbara G Ryder. Constructing the call graph of a program. IEEE Transactions on Software Engineering, (3):216–226, 1979.

- [19] Pavel V Shevchenko. Modelling operational risk using Bayesian inference. Springer Science & Business Media, 2011.

- [20] Deep Shift. Technology tipping points and societal impact. In World Economic Forum Survey Report, 2015.

- [21] David Shrier, Weige Wu, and Alex Pentland. Blockchain & infrastructure (identity, data security). Massachusetts Institute of Technology-Connection Science, 1(3), 2016.

- [22] Melanie Swan. Blockchain: Blueprint for a new economy. ” O’Reilly Media, Inc.”, 2015.

- [23] Nick Szabo. Smart contracts: building blocks for digital markets. EXTROPY: The Journal of Transhumanist Thought,(16), 1996.

- [24] Sergei Tikhomirov, Ekaterina Voskresenskaya, Ivan Ivanitskiy, Ramil Takhaviev, Evgeny Marchenko, and Yaroslav Alexandrov. Smartcheck: Static analysis of ethereum smart contracts. 2018.

- [25] Mark Van Rijmenam and Philippa Ryan. Blockchain: Transforming Your Business and Our World. Routledge, 2018.