11email: {zhaowenqi,lihui0729,yuanyuming}@huobi.com

Understand Volatility of Algorithmic Stablecoin: Modeling, Verification and Empirical Analysis

Abstract

An algorithmic stablecoin is a type of cryptocurrency managed by algorithms (i.e., smart contracts) to dynamically minimize the volatility of its price relative to a specific form of asset, e.g., US dollar. As algorithmic stablecoins have been growing rapidly in recent years, they become much more volatile than expected. In this paper, we took a deep dive into the core of algorithmic stablecoins and shared our answer to two fundamental research questions, i.e., Are algorithmic stablecoins volatile by design? Are they volatile in practice? Specifically, we introduced an in-depth study on three popular types of algorithmic stablecoins and developed a modeling framework to formalize their key design protocols. Through formal verification, the framework can identify critical conditions under which stablecoins might become volatile. Furthermore, we performed a systematic empirical analysis on real transaction activities of the Basis Cash stablecoin to relate theoretical possibilities to market observations. Lastly, we highlighted key design decisions for future development of algorithmic stablecoins.

Keywords:

Stablecoins Modeling framework Empirical analysis.1 Introduction

As cryptocurrencies on blockchain are notoriously known as volatile, i.e., Their prices often fluctuate rapidly, stablecoins are proposed to peg their value to some external assets, e.g., US dollar. In contrast to “unstable” cryptocurrencies, e.g., Bitcoin [19], Ethereum [24], a stablecoin is able to minimize the volatility of its price relative to the pegged asset based on different mechanisms. The most common kind of stablecoins is backed-stablecoin, i.e., The value of a stablecoin is backed by external assets, e.g., commodity, fiat money or cryptocurrency as collateral. For example, the USDC stablecoin is backed by US dollar [5]. Unlike backed-stablecoins, algorithmic stablecoins, which are commonly not backed by other assets, have been gaining an increasing level of popularity in recent years due to the capability to stabilize its price via decentralized algorithms (i.e., smart contract) without degrading too much capital efficiency. In general, this is realized by controlling the money supply of algorithmic stablecoins, which is similar to printing and destroying money in central banks. In this paper, we mainly focus on algorithmic stablecoins and will use the term interchangeably with “stablecoin” (Backed-stablecoins are not the main target in this work.).

Assuming that a stablecoin is pegged to US dollar, a smart contract is designed to dynamically manage its supply to minimize price volatility. We simply explain the algorithm as follows and will further the discussion later. When the price of the stablecoin exceeds one US dollar, the contract “produces” more coins and distributes them to the market. As a result, the price of the stablecoin should accordingly drop. In cases where the price of the stablecoin is lower than one US dollar, the smart contract decreases the supply of it in order to gradually lift its price back to one dollar. In practice, the aforementioned general algorithm can be instantiated by different models to achieve a more robust control over stablecoins. While many interesting research attempts aim at inventing such models, there is relatively little study on the other side, i.e., Do they really work?

In this paper, we described a fundamental analysis on the volatility of algorithmic stablecoins, both theoretically and empirically. Our attempt of this study is to answer two fundamental research questions, which are:

-

Research Question 1:

Are algorithmic stablecoins volatile by design?

-

Research Question 2:

Are algorithmic stablecoins volatile in practice?

Our goal of the analysis described in this paper is to provide a more comprehensive understanding on the protocols of stablecoins (at both design and implementation level) with a specific focus on their volatility, which we believe is critical in the optimization of existing stablecoins and creation of potential future designs. We summarize our main contributions as follows.

-

•

We introduced an in-depth protocol analysis on the designs of three popular types of algorithmic stablecoins. Moreover, we developed a general formal modeling and verification framework for stablecoins, which can be used to identify specific hidden criteria under which stablecoins might become volatile.

-

•

We further conducted a systematic empirical study of the Basis Cash stablecoin based on real transaction activities on Ethereum and manged to relate theoretical possibilities (that stablecoins might be volatile) to market observations (unexpected volatile prices) between Dec 2020 to Jan 2021.

2 Background

We classify algorithmic stablecoins into three categories, i.e., rebase-style, seigniorage share and partial-collateral. In this section, we briefly explain key designs of all three types of stablecoins with popular projects as examples.

2.1 Rebase (Ampleforth)

The rebase-style stablecoins manage price-elastic ERC20 tokens, i.e., The total supply of a stablecoin is non-fixed and adjusted adaptively on a routine basis. More specifically, the adjustment is automatically realized via the “rebase” process, which gradually stabilize the price of a target stablecoin near a specific peg, e.g., one US dollar. We use Ampleforth [1] as an example for illustration.

By design, the rebasing of Ampleforth is activated at 2am UTC on a daily basis. At the time of rebase, new coins are minted and distributed to all accounts proportionally based on their corresponding balances when the price of Ampleforth is higher than its peg. Given that the price of Ampleforth is $1.2 with its peg to be $1 (i.e., 20% relate to peg), an account with 100 coins is rebased to own 120. On the other hand, holding coins might be automatically proportionally burned when the price falls below the peg.

2.2 Seigniorage Share (Basis Cash)

The seigniorage share model for algorithmic stablecoins commonly introduces two types of cryptocurrencies, i.e., coins as a stablecoin and shares as ownership of seigniorage. In principle, shares are used to increase the supply of coins when the price of a coin is above its intended peg. In addition to these two cryptocurrencies, seigniorage-style stablecoins often issue a redeemable bond as an incentive for buyers when the price goes down below the peg. We use the Basis Cash [2] stablecoin for further explanation. Basis Cash introduces three types of cryptocurrencies:

-

•

BAC. BAC is the stablecoin and issued by the Basis Cash with a peg of $1.

-

•

BAS. BAS stands for Basis Shares, which is a seigniorage ERC20 token and provides inflationary gains of BAC. The design purpose of BAS is to prevent the price of BAC from going too high via dynamically increasing its supply. Currently, BAS can be earned via participating in yield farming, i.e., deposit liquidity in decentralized finance platforms (e.g., Uniswap [6]).

-

•

BAB. BAB refers to Basis Bond whose price is mathematically determined by the price of BAC , i.e., . Particularly, BAB offers an incentive for holders to earn BAB in a cost-effective way. The design purpose behind is to push BAC back to one dollar when its price falls below $1.

The general protocol of Basis Cash is designed to stabilize the price of BAC via adaptively controlling the supply of it. This is realized based on the two key mechanisms, i.e., expansion and contraction, respectively. We simply describe the processes as below.

Expansion. The mechanism of expansion aims at increasing the supply of BAC in order to stabilize its price when it rises over the one dollar peg. In the design of Basis Cash, expansion is automatically activated in two settings. First, BAC will be minted and distributed as a reward to BAS holders. That said, for anyone who owns a specific amount of BAS, the expansion process proportionally assigns new BAC to his or her account. In the second case, owners of BAB are allowed to redeem BAC with their BAB at a 1:1 price, which also result in a quantity growth of BAC. Due to the increased supply in both situations, the expansion is expected to gradually make the price of BAC to decrease.

Contraction. In contrast to the process of expansion, contraction is designed to shrink the supply of BAC. To this end, an incentive is introduced in Basis Cash to encourage buyers to exchange BAB with BAC when the price of BAC is below one dollar. In the particular situation, one BAC is guaranteed to generate more than one BAB based on their price dependency as aforementioned. Moreover, the protocol of Basis Cash ensures that a specific amount of BAB is able to redeem the same amount of BAC when the price of BAC grows above $1 and required conditions are met. Based on the design of contraction, th price of BAC is anticipated not to fall too far from its peg.

2.3 Partial-Collateral (Frax)

In contrast to the two types of algorithmic stablecoins, an emerging class called fractional-algorithmic protocol is recently proposed as a combination of fully-collateral and fully-algorithmic ones. Compared to existing collateral-style stablecoins, e.g., DAI, partial-collateral protocols introduce less custodial risks and avoid over-collateralization. On the other hand, it is designed to enforce a relatively tight peg with higher level of stability than purely algorithmic designs. We use the Frax project [4] below for illustration.

Particularly, Frax is the first attempt to implement the partial-collateral protocol of stablecoins. It introduces a two-token system, i.e., FRAX as a stablecoin pegged to $1 and FXS as a governance token, respectively. A collateral ratio is dynamically determined very hour with a step of 0.25% in the protocol to control at what percentage of peg the collateral is required to take to stabilize the value of FRAX. In cases where , $0.5 must be in other types of stablecoins as collateral to mint a new FRAX. It becomes fully collateral when and a pure algorithmic stablecoin if .

The collateral ratio is 1.0 at genesis. In principle, minting a specific amount of FRAX involves placing of the value as collateral and burning of the value with FXS. As the price goes above its peg, the protocol provides the incentive for investors to mint new FRAX. Accordingly, the increased supply of FRAX is expected to gradually enforce the price to decrease. In cases where the price falls below the peg, the protocol allows investors to swap a combination of collateral and FXS valued $1 with a single FRAX whose value is lower than $1. Such incentives can potentially produce FRAX purchases and rise its price as well.

3 Modeling and Verification

3.1 Modeling of Stablecoin

We highlighted a formal modeling framework for stablecoins. More formally, is a network consisting of six types of timed automata [7], each of which is a tuple . is the finite set of states. is the initial state. is a set of non-negative real numbers as clock variables. is a set of accepting states. is a set of actions and is a set of invariants assigned to states. Given that is constraint function, is a collection of state transitions , where and are source and destination states, is an action, is the condition to enable the transition and is the set of clocks to be reset.

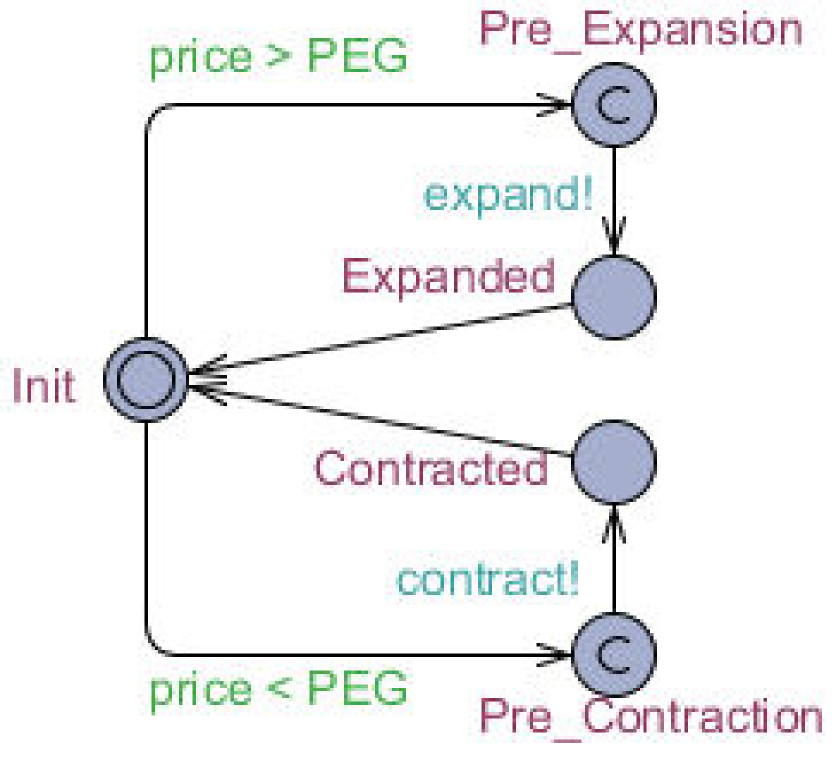

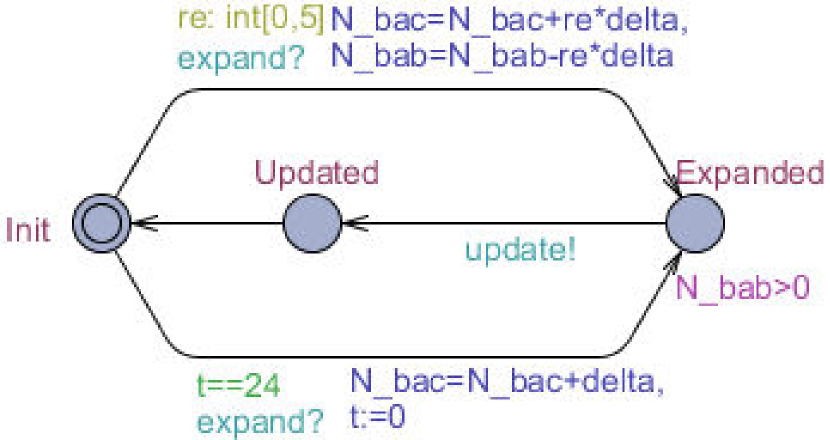

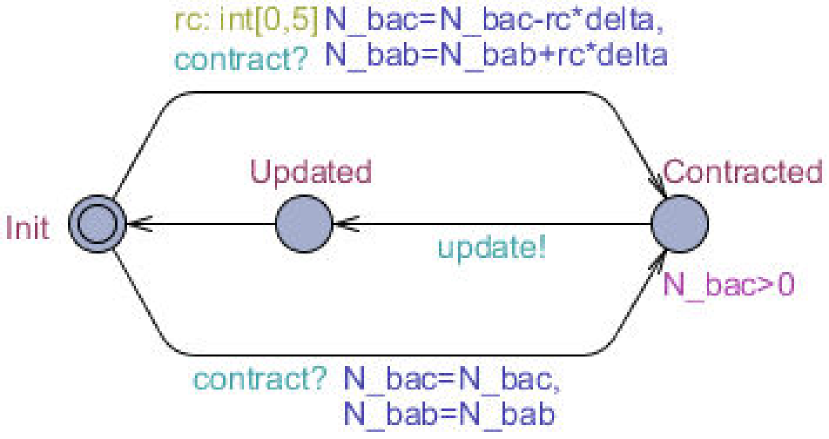

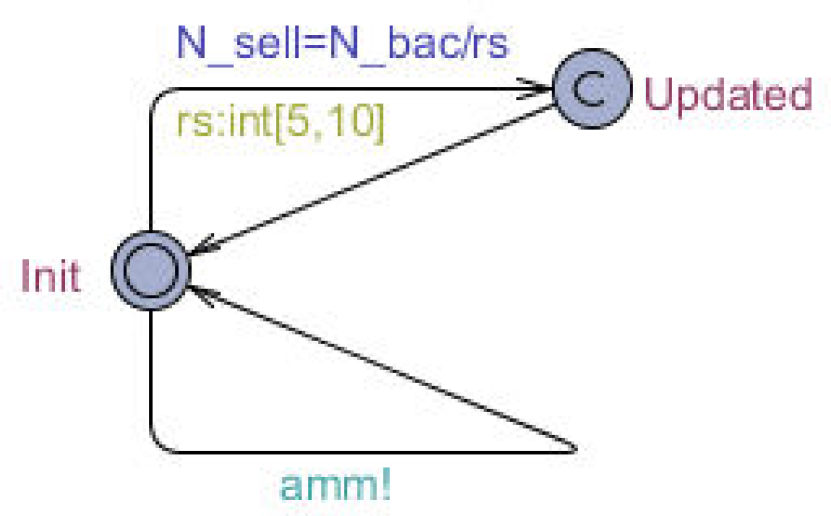

Moreover, provides communication through four classes of synchronized channels . Specifically, and are designed to trigger expansion and contraction procedures. simulates market trading activities and generates a new price of stablecoin. synchronizes updates between , and . Particularly, we presented a formal model of Basis Cash in Figure 1. The framework is general to other types of stablecoins. Due to page limits, we selected Basis Cash because it manifests a typical model and was one of the most popular markets at the time of writing.

-

•

models the main protocol with five states, i.e., initial state, Pre_Expansion and Expanded states when price is above the peg, Pre_Contraction and Contracted states when price is below the peg. The channels of expand () and contract () are activated on two transitions to enable the processes of expansion and contraction.

-

•

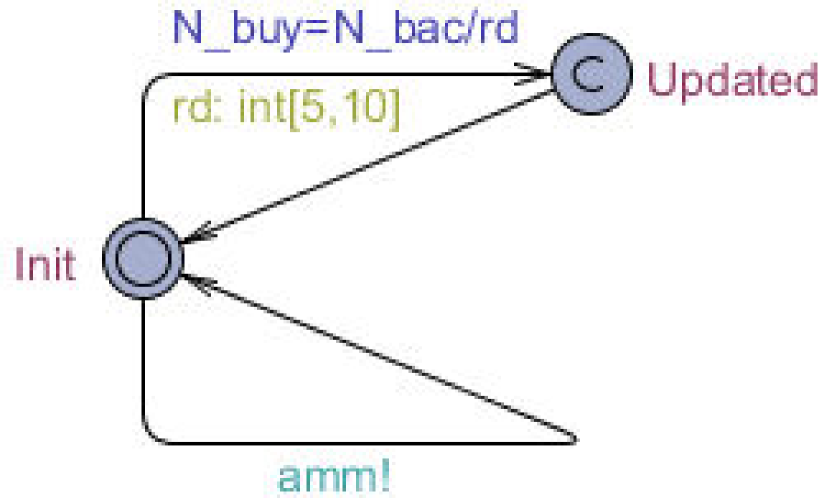

automata defines a process with a clock and a three states. responds to expansion requests from . An expanding transition is executed to grow the supply of stablecoins (i.e., global variable N_bac). The transition is allowed if is at an expansion point (e.g., 24:00 UTC). For Basis Cash, creates two expansion transitions and synchronizes with via the update channel ().

-

•

automata abstracts the contraction process. Similar to , a transition is provided to refine the decrease of supply via updating a global variable Another transition is designed to model that the supply stays unchanged (investors can choose not to swap BAB with BAC).

-

•

and are designed to model the behavior of sellers and buyers in an exchange. They generate random trading requests through the channel.

-

•

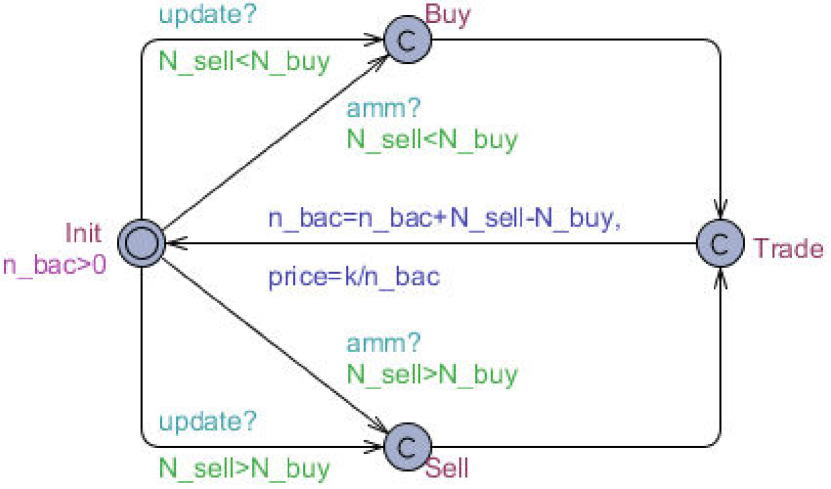

introduces an abstract model of decentralized exchanges (DEX) with automatic market making (AMM), e.g., Uniswap [6]. defines Sell and Buy states to indicate whether it is a buyer’s market (i.e., more sellers than buyers) or seller’s market (the other way around). New prices are computed based on AMM and its pool of stablecoins.

3.2 Formal Verification

We further highlight important formal specifications to define stability properties (or non-volatility) of stablecoins with temporal logic [21]. Specifically, stability (non-volatility) is specified through the following two properties ( and are quantifiers, i.e., for all paths and for all states of a path in the state space [21]).

| (expansion-validity) |

| (contraction-validity) |

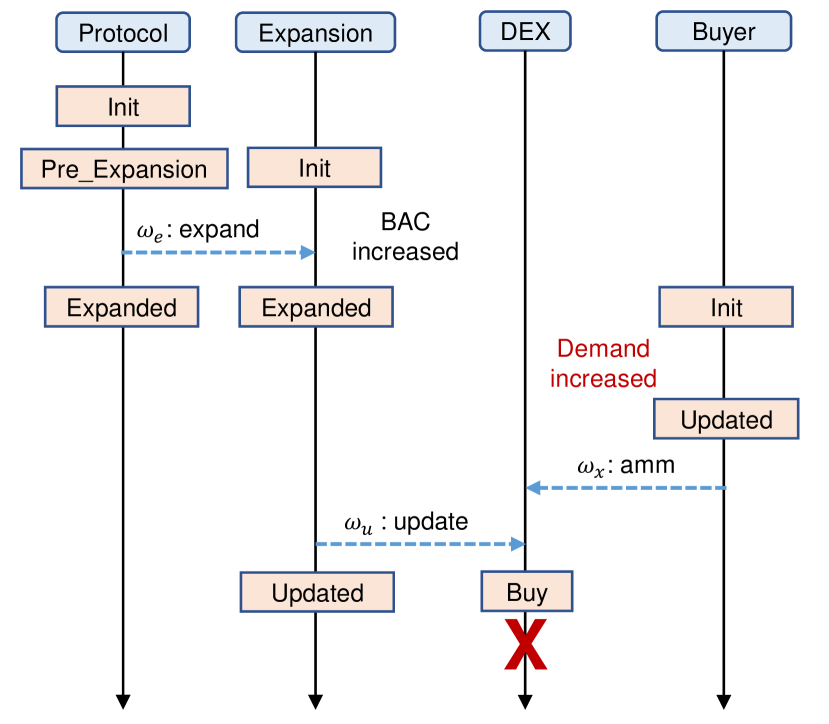

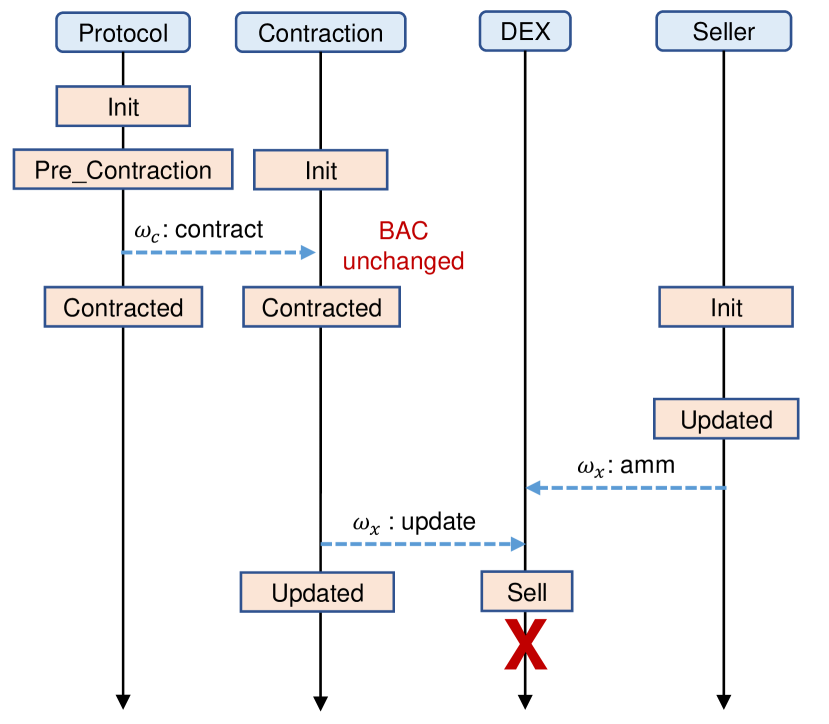

Specifications of Stability (Non-Volatility). Two properties are specified as in expansion-validity and contraction-validity to formalize the resilience against price fluctuation (with Basis Cash as an example). As formalized by expansion-validity, in cases where is at state Expansion and is at Validated (i.e., expansion has been enforced), must not stay at the state of Buy for the price to fall, i.e., buyer’s market. Similarly, when is at Contraction and is at Validated, must not be at the state of Sell, i.e., seller’s market.

Counter-Example Analysis. We verified the model of Basis Cash with the Uppaal model checker for timed automata [16]. Figure 2 shows two counter-examples of the stability properties, i.e., conditions under which Basis Cash might become volatile. Figure 2(a) describes a trading scenario where expansion validity is violated. Specifically, a demand growth of BAC occurs when the expansion process is started to mint and distribute new stablecoins. As a result, DEX goes to the state of Buy instead of Sell to trigger a counter-example. In terms of contraction-validity, Figure 2(b) demonstrates another potential volatility of Basis Cash. When the price of BAC goes down below its peg, the contraction allows investors to swap BAB with BAC. However, in cases where the swap does not happen therefore supply of BAC stays unchanged, the contraction-validity is violated since DEX goes to the state of Sell instead of Buy as expected.

4 Empirical Analysis

Based on the formal modeling and verification of Basis Cash, we now describe an empirical analysis with real market observations. Queries and data used are available (https://explore.duneanalytics.com/dashboard/winky) on the Dune Analytics [3] platform.

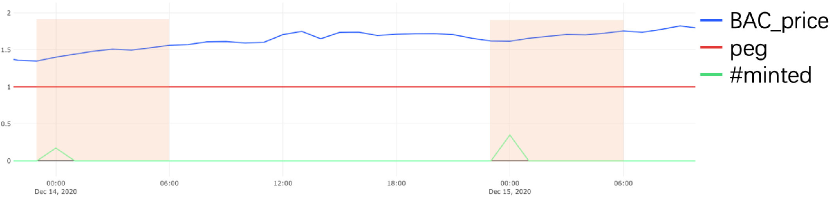

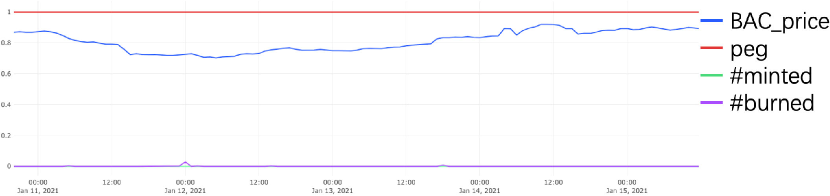

Normal Cases. Figure 3(a) and 3(b) shows two cases where expansion and contraction worked well. As highlighted in Figure 3(a), as new BAC were minted, its price gradually went down. Similarly, as a number of BAC were burned for contraction in Figure 3(b), its price started to rise.

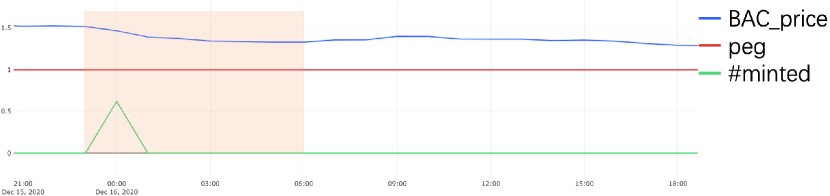

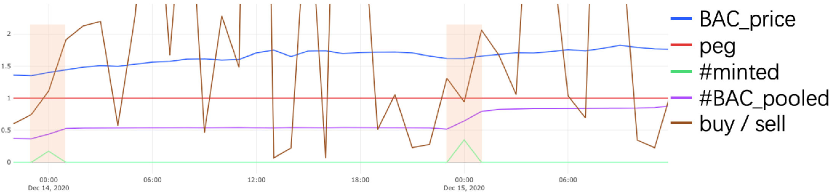

Broken Expansion. Figure 3(c) and 3(e) explains a broken expansion as inferred in §3.2 on Dec 14 and 15, 2020. In Figure 3(c), the expansion started at 00:00 with a collection of new BAC minted. However, its price increased in 7 hours from $1.35 to $1.56 (Dec 14) and from $1.62 to $1.76 (Dec 15), which amounted to a growth of 15.72% and 8.40%. Based on Figure 3(e), the broken expansion was attributed to a rapid increase of demand as marked in Figure 3(e). Since yield-farming on BAC-DAI was very popular at an early stage and led to a extremely high yield rate, the demand of BAC was rapidly lifted even at an expansion point. The popularity of BAC was also reflected by that 92% of the newly minted BAC on Dec 14, 2020 went to the yield-farming pool within 2 hours after expansion.

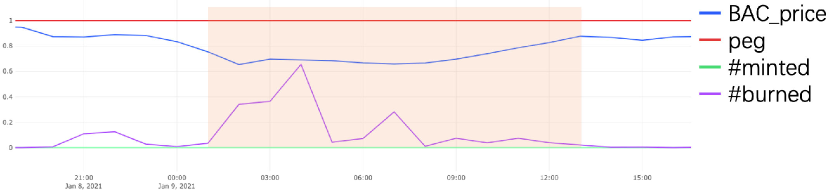

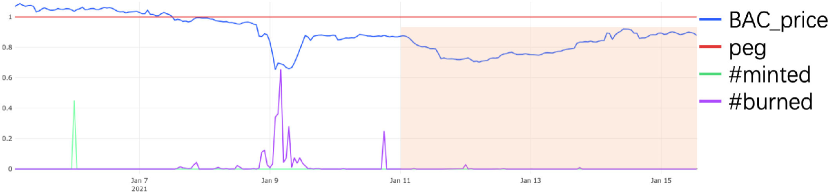

Broken Contraction. The potential volatility due to broken contraction was also confirmed in Figure 3(d) and 3(f). From Jan 11, 2021 to the time of writing, the price of BAC has been staying below its peg according to Figure 3(d) despite that entries of contraction were continuously open. The reason behind was the low participation in contraction, i.e., Many investors were unwilling to burn BAC for BAB due to the fear that they might never be able to redeem. As shown in Figure 3(f), the number of burned BAC (hump) in that period was much smaller than several days ago.

Design Decisions. First, contraction weighs more than expansion to minimize volatility since cryptocurrencies are naturally easier to fall than rise. Interfacing contraction to more ecosystems is a vital complement. Second, the quantity and cycle of algorithmic intervention are essential factors in stablecoin designs. More robust and flexible models are highly desired in this context.

5 Related Work

As stablecoins became popular in recent years, researchers have been suggesting to a new monetary policy for them [14, 11]. Saito et al. proposed to stabilize cryptocurrencies via automatically controlling their supply to absorb both positive and negative demand shocks [22]. Caginalp et al. leveraged asset flow equations to model cryptocurrency and their stability [10]. In the context of algorithmic stablecoins, Ametrano described Hayek Money to achieve stability via rebasing the amount of coins [8]. Sams further designed seigniorage shares to include an elastic supply rule which adjusts the quantity of coins adaptively [23]. On the other hand, design review of stablecoins were al discussed in several research papers and industry reports [12, 18, 17, 20, 9, 13, 15]. Classification of stablecoins were introduced according to different types of collateral and intervention with pros and cons explained.

6 Conclusion

In this paper, we presented an in-depth theoretical and empirical analysis on the volatility of algorithmic stablecoins. We highlighted a formal modeling framework for stablecoins to identified important market criteria under which they might become volatile. Moreover, we related our theoretical findings to transaction activities on stablecoins via a further empirical analysis with real market data. Empirical results showed that potential possibilities predicted in the proposed model were confirmed in practice. Lastly, we highlighted important design decisions for the future development of stablecoin. All data used in this work are available at https://explore.duneanalytics.com/dashboard/winky.

References

- [1] Ampleforth. https://www.ampleforth.org/ (2021)

- [2] Basis Cash. https://basis.cash/ (2021)

- [3] Dune Analytics. https://duneanalytics.com/ (2021)

- [4] Frax. https://frax.finance/ (2021)

- [5] Tether. http://tether.to (2021)

- [6] Uniswap. http://uniswap.io (2021)

- [7] Alur, R., Dill, D.L.: A theory of timed automata. Theoretical computer science 126(2), 183–235 (1994)

- [8] Ametrano, F.M.: Hayek money: The cryptocurrency price stability solution. Available at SSRN 2425270 (2016)

- [9] Bullmann, D., Klemm, J., Pinna, A.: In search for stability in crypto-assets: are stablecoins the solution? ECB Occasional Paper (230) (2019)

- [10] Caginalp, C.: A dynamical systems approach to cryptocurrency stability. arXiv preprint arXiv:1805.03143 (2018)

- [11] Caginalp, C., Caginalp, G.: Opinion: Valuation, liquidity price, and stability of cryptocurrencies. Proceedings of the National Academy of Sciences 115(6), 1131–1134 (2018)

- [12] Clark, J., Demirag, D., Moosavi, S.: Sok: Demystifying stablecoins. Available at SSRN 3466371 (2019)

- [13] Hileman, G.: State of stablecoins (2019). Available at SSRN (2019)

- [14] Iwamura, M., Kitamura, Y., Matsumoto, T., Saito, K.: Can we stabilize the price of a cryptocurrency?: Understanding the design of bitcoin and its potential to compete with central bank money. Hitotsubashi Journal of Economics pp. 41–60 (2019)

- [15] Klages-Mundt, A., Harz, D., Gudgeon, L., Liu, J.Y., Minca, A.: Stablecoins 2.0: Economic foundations and risk-based models. In: Proceedings of the 2nd ACM Conference on Advances in Financial Technologies. pp. 59–79 (2020)

- [16] Larsen, K.G., Pettersson, P., Yi, W.: Uppaal in a nutshell. International journal on software tools for technology transfer 1(1-2), 134–152 (1997)

- [17] Mita, M., Ito, K., Ohsawa, S., Tanaka, H.: What is stablecoin?: A survey on price stabilization mechanisms for decentralized payment systems. In: 2019 8th International Congress on Advanced Applied Informatics (IIAI-AAI). pp. 60–66. IEEE (2019)

- [18] Moin, A., Sekniqi, K., Sirer, E.G.: Sok: A classification framework for stablecoin designs. In: Financial Cryptography (2020)

- [19] Nakamoto, S.: Bitcoin: A peer-to-peer electronic cash system. Tech. rep., Manubot (2019)

- [20] Pernice, I.G., Henningsen, S., Proskalovich, R., Florian, M., Elendner, H., Scheuermann, B.: Monetary stabilization in cryptocurrencies–design approaches and open questions. In: 2019 Crypto Valley Conference on Blockchain Technology (CVCBT). pp. 47–59. IEEE (2019)

- [21] Pnueli, A.: The temporal logic of programs. In: 18th Annual Symposium on Foundations of Computer Science (sfcs 1977). pp. 46–57. IEEE (1977)

- [22] Saito, K., Iwamura, M.: How to make a digital currency on a blockchain stable. Future Generation Computer Systems 100, 58–69 (2019)

- [23] Sams, R.: A note on cryptocurrency stabilisation: Seigniorage shares. Brave New Coin pp. 1–8 (2015)

- [24] Wood, G., et al.: Ethereum: A secure decentralised generalised transaction ledger. Ethereum project yellow paper 151(2014), 1–32 (2014)