Fluctuation theory for one-sided Lévy processes with a matrix-exponential time horizon

Abstract.

There is an abundance of useful fluctuation identities for one-sided Lévy processes observed up to an independent exponentially distributed time horizon. We show that all the fundamental formulas generalize to time horizons having matrix exponential distributions, and the structure is preserved. Essentially, the positive killing rate is replaced by a matrix with eigenvalues in the right half of the complex plane which, in particular, applies to the positive root of the Laplace exponent and the scale function. Various fundamental properties of thus obtained matrices and functions are established, resulting in an easy to use toolkit. An important application concerns deterministic time horizons which can be well approximated by concentrated matrix exponential distributions. Numerical illustrations are also provided.

Key words and phrases:

functions of matrices, rational Laplace transform, scale function, Wiener-Hopf factorization1. Introduction

A spectrally-negative Lévy process is a natural generalization of the classical Cramér-Lundberg risk process. This class of processes allows for a rich fluctuation theory, which has been extensively applied to various insurance risk and financial models. This theory, see [6] for a recent review, is crucial in the analysis of risk processes in a wide range of settings including alternative ruin concepts, dividends, capital injections, loss-carry-forward taxation, and optimal control. An important assumption here is that the time horizon is either infinite or is given by an independent exponential random variable. Its rate is often referred to as the killing rate of the Lévy process.

In applications a deterministic time horizon is often needed. In this case Erlangization [4] is a popular approach, where the deterministic time is approximated using the Erlang distribution. In fact, more general phase-type (PH) distributions can be used when the interest is in a random time horizon, and the analysis often goes via fluid flow models and Markov additive processes [32, 5]. Matrix exponential (ME) distributions, equivalently distributions with rational transforms, form yet a broader class which has been successfully employed in modeling claim sizes [27]. Some preliminary investigations concerning ME time horizons have been carried out in [29, Ch. 6]. Importantly, there exist much more concentrated ME distributions as compared to PH (read Erlang) distributions for the same order [20]. Such concentrated ME distributions have been recently suggested by [19] for a general purpose numerical transform inversion method, and in various scenarios it has outperformed some classical methods.

In this paper we provide a comprehensive fluctuation theory for spectrally-negative Lévy processes with an independent ME time horizon . Importantly, the classical formulas preserve their structure in this generalized context. The basic idea is to analytically continue a given formula in the rate to the right half of the complex plane and then apply it to , the negative of the ME generator matrix, using functional matrix calculus. In particular, we extend the positive root of the Laplace exponent and the scale matrix which play a fundamental role in fluctuation identities, and establish their essential properties. We also consider the Wiener-Hopf factorization and generalize various known formulas for the supremum/infimum and the terminal value. Further identities can be extended in a rather straightforward way using the results and properties of this paper. In the common case when the ME generator is diagonalizable, an ME formula can be seen as a linear combination of the respective classic formulas but for possibly complex killing rates. This links to the inversion method of [19] when their concentrated ME distributions are used.

Our theory brings new insights also for PH time horizons. In particular, we show that and correspond to some fundamental objects in the theory of Markov additive processes, where the same level process is used in each phase. These convenient representations seem to be new. Furthermore, our analytic method results in neat formulas avoiding somewhat cumbersome time-reversed quantities as in [5].

The remainder of this paper is organized as follows. This introductory section is concluded by providing some basic notation for ME distributions and Lévy processes. In Section 2 we present the general idea and the essential tools from the theory of functional matrix calculus. The next three sections deal with the natural extension of the fundamental fluctuation theory including scale functions and a variety of exit problems. Section 6 presents the analogue of the classical Wiener–Hopf factorization and a suite of related identities. The next two sections contain examples and numerics, respectively. We conclude by discussing an open problem concerning Lévy processes observed at the epochs of an independent renewal process with ME inter-arrival times.

1.1. Matrix-exponential distributions

A positive random variable is said to have a matrix–exponential (ME) distribution if it has a density on the form

where is a row vector (bold Greek) with elements, is a matrix called the ME generator, and is a column vector (bold Roman); all being real valued. According to [12, Thm. 4.2.9] it is always possible to choose a (canonical) representation satisfying and hence , where is a vector of ones. Nevertheless, it may be convenient to allow for an arbitrary ME representation and so we write . We also define a column vector , which is in the case of a canonical representation (this vector often appears as the ast vector in the formulas below).

The eigenvalues of must have strictly negative real parts, and the Laplace transform of is a rational function:

where is the identity matrix. The opposite implication is also valid: any positive distribution with a rational Laplace transform is an ME distribution, [12, Thm. 4.1.17].

The class of ME distributions is strictly larger than the class of phase-type (PH) distributions, where and can be seen as a probability vector and a sub-intensity matrix of a transient Markov chain . The density of the life time of this chain started according to coincides with . In this case we write . As mentioned before, a much better approximation of a positive deterministic number can be achieved using ME distributions as compared to Erlang or any other PH distribution for a fixed number of dimensions , see [20].

1.2. Lévy processes

Consider a Lévy process , that is, a process with stationary and independent increments. We assume that is a spectrally-negative Lévy process, meaning that has no positive jumps and its paths are not non-increasing a.s. Such a process is characterized by the Lévy-Khintchine formula providing an expression for the Laplace exponent :

with and parameters , where the latter is a measure satisfying .

Define the running supremum and analogously the running infimum for . The first passage times are denoted by

In some cases we start the Lévy process at and then we write and to signify the starting value.

2. The toolkit

2.1. The basic idea

We start with a simple observation which is fundamental for this work. Let for denote a restriction of the path of to the time interval . One may think of sending the path at time to some isolated absorbing state. For an independent exponential random variable of rate and an arbitrary (measurable) non-negative functional there is the identity:

| (1) |

which is essentially the Laplace transform of in time variable. Importantly, for a one-sided Lévy process and a variety of functionals , this expression is explicit (often in terms of the scale function defined below), see [6] and references therein for a long list of formulas. The main reason is that killing at , by the memory-less property, preserves stationarity and independence of increments.

Letting be independent of we get a similar matrix-form expression:

Laplace transforms are analytic in their region of convergence, so the function in (1) is analytic for . Since the eigenvalues of are all in , [12], we may then apply to the matrix , as we next explain in Section 2.2, to obtain

| (2) |

where is for a canonical representation. The main difficulty is to analytically continue the formula corresponding to to the half plane , and to establish some important properties of the involved components.

Furthermore, we allow to be a defective ME in the sense that the total mass may be strictly less than . It is still true that the eigenvalues of are in . The basic example is for some and a non-defective , which allows to incorporate discounting into the formula:

Here we have independent exponential killing of rate , whereas in phase-type setting it is natural to consider phase-dependent killing allowing to weigh time spent in each phase differently, see [22] for further details and applications. A somewhat related useful trick corresponds to considering which has distribution, see Remark 7.

2.2. Matrix calculus

For a function analytic on some open connected domain and a matrix with eigenvalues in it is standard to define via Cauchy’s integral formula

where the closed simple curve contains the eigenvalues of in its interior [18]. An equivalent definition of proceeds via the Jordan canonical form of . In particular, in the diagonalizable case we have . In fact, both definitions can be given without requiring to be connected. In the following we mostly work with the domain and the matrix , where is an ME generator. For convenience we state some basic calculus rules, see [18, Ch. 1].

Lemma 1.

Let be a matrix and two analytic functions on their respective domains. Under the condition on eigenvalues belonging to the respective domain we have

-

•

commutes with ,

-

•

the eigenvalues of are given by applied to the eigenvalues of ,

-

•

and ,

-

•

,

-

•

for a power series convergent on some domain it holds that

-

•

for a -finite measure and convergent on some domain it holds that

The classic example of a matrix exponential is, of course, consistent with this theory.

2.3. The diagonalizable case and relation to an inversion method

Here we assume that is diagonalizable:

| (3) |

where are the eigenvalues of . Hence the density is a sum of exponential terms:

| (4) |

It is easy to see that every such density corresponds to some ME representation with a diagonalizable exponent matrix. According to (2) we then have

Here again it is necessary to have a formula for anlytically continued to , and this requires proving some basic properties of the involved terms.

Taking an ME distribution concentrated around some deterministic value, say 1, we may obtain an approximation of . In [20] one particular family of such distributions was explored. They provided an efficient numerical procedure for determining the respective parameters in (4), and published online a list of such parameters up to the order . As demonstrated by [19] this leads to a general procedure for numerical inversion of Laplace transforms.

The diagonalizable case may initially seem much simpler. With the right perspective and tools, however, the general case is not more difficult as we demonstrate below. Nevertheless the diagonalizable case is convenient for numerics and in some other special situations, see also Section 7.2.

3. The supremum and first passage

The first passage process is crucial to the analysis of fluctuations of . By the strong Markov property of and absence of positive jumps we see that is a (possibly killed) subordinator, that is a Lévy process with non-decreasing paths a.s. Here we also use the well known fact a.s. Let be its Laplace exponent:

| (5) |

It has the following Lévy-Khintchine representation:

where the parameters satisfy . Note that the class of functions with such a representation coincides with the class of Bernstein functions [31, Thm. 3.2], and it is closely related to completely monotone functions. The parameters can be identified from the basic fact that is the unique positive solution of for [9, Sec. VII].

The above Lévy-Khintchine representation of is analytic on and hence we may apply it to a matrix with eigenvalues in to get

| (6) |

Here we use Lemma 1 and its slightly generalized version in regard to the integral. Now we can easily apply the basic idea in (2) to the functional to get an explicit formula for with an independent . In fact, quite a bit more can be said. In this regard we state the following Lemma which is proven in Appendix.

Lemma 2.

For any it holds that and . Moreover, for with it must be that . In particular, is the unique solution of in for any .

This result can also be useful when directly considering the diagonalizable case in (4). We are now ready to prove our main result concerning the supremum and first passage time for an ME time-horizon.

Theorem 3.

Let be independent of . Then

which amounts to

Moreover, given in (6) solves the equation , and it is the unique solution among matrices with eigenvalues in .

Proof.

The case is well understood, as it can be analyzed in the framework of a Markov additive processes. Consider the Markov chain formed by tracking the original phase at first passage times, and let be its subintensity matrix. It is now immediate that the supremum is . The following representation of implied by Theorem 3 seems to be new.

Corollary 4.

For the intensity matrix of the Markov chain is given by .

Proof.

4. The scale function and two-sided exit

The so-called scale function defined for all killing rates plays a fundamental role in the fluctuation theory of one-sided Lévy processes. It is the unique continuous, non-decreasing function identified by its transform

| (7) |

see [9, Thm. VII.8]. The scale function is strictly positive for and it solves the basic two-sided exit problem:

| (8) |

It is well known that for any the function may be analytically continued to via the identity

| (9) |

where is the -th convolution of , see [11, 24] or [25, Sec. 3.3]. Furthermore, the transform (7) is still true for any and all . The following Lemma extends a basic property of the scale function to , see Appendix for the proof. This result is not true for with and, in fact, the zeros for negative have been employed in [11].

Lemma 5.

It holds that for all and all .

According to (9) we define

| (10) |

for any square matrix . In order to claim invertibility of we must assume that the eigenvalues of are in . The above theory extends to the ME-time horizon in the following way.

Theorem 6.

For a square matrix with eigenvalues in the matrix-valued function in (10) is continuous, invertible for positive arguments, and is uniquely determined by the transform

where is the spectral radius of .

Moreover, for independent of there is the identity:

Proof.

Continuity in readily follows from the power series representation of and the dominated convergence theorem. It also yields the transform expression via Fubini’s theorem (cf. [25, Sec. 3.3])

when exceeds which is equivalent to . Uniqueness is established by viewing this transform as a matrix of transforms of continuous (not necessarily positive) functions [33, Ch. II].

The matrices and commute for any and so the order of matrix multiplication is arbitrary. Unlike the classical case, the matrix does not need to have positive entries, see Section 8

Remark 7.

Theorem 6 readily implies an expression for the transform and it is only required to take the ME distribution of for an independent exponential random variable .

Finally, for the matrix valued function coincides with the matrix valued scale function of the Markov additive process , where is an independent Markov chain defining the PH distribution, see [23]. This can be easily seen by comparing the transforms.

5. The second scale function and further identities

The Skorokhod reflection of at starting from an arbitrary is defined by

where the non-decreasing process is often called a regulator. The first passage time of the reflected processes is denoted by

Then the second scale function , and three (closely related) basic identities are given by

| (11) | ||||

for all and , see [23, Thm. 2], [6], [25, Eq. (58)]. The last identity for is interpreted in the limiting sense.

Lemma 8.

For any and the function is analytic. It is non-zero for .

This result and our usual arguments based on (2) lead to the following extension of the above formulas.

Theorem 9.

For a square matrix with eigenvalues in the matrix function

is continuous and invertible. Moreover, for independent of , there are the identities

for all and , and in the last identity is such that the inverse is well-defined.

Furthermore, we may also obtain the distribution of with reflecting/terminating barriers at an independent ME time. For example, has a density

where is a zero matrix for negative arguments, see, e.g., [11, Thm. 1] for the case of exponential killing.

6. The Wiener-Hopf factorization

6.1. The general case

The Wiener-Hopf factorization [9, Thm. VI.5] holds for a general Lévy process , not necessarily one-sided. It states that is independent of for an exponential random variable of rate independent of . Furthermore, by time reversal the two quantities are equal in law to and , respectively. For an ME-horizon we have a vector factorization:

Proposition 10.

Let be independent of a general Lévy process . Then for Borel sets we have

where both terms are finite vector-valued signed measures.

Proof.

Just note that

extend this identity to and apply the functions on both sides to using Lemma 1. By conditioning on we get the result. Countable additivity and finiteness of each term is easy to see. ∎

6.2. The factors in spectrally-negative case

In the case of a spectrally-negative Lévy process both terms in Proposition 10 can be written in a more explicit form. Recall that is exponential of rate , whereas the law of is given by

see [11, Eq. (8)].

Proposition 11.

For a square matrix with eigenvalues in we have

Proof.

The first statement follows by applying to . We get the second from the above representation of . Recall that the function has been discussed in Section 5. ∎

Note that the above expression can be written in terms of using the obvious identity

Let us mention that the known bivariate transform [9, Thm. VII.4] can also be easily extended:

for such that the latter inverse is well-defined.

6.3. On the derivative of the scale function

It is well known that is differentiable in apart from countably many points with the right derivative well-defined for all . Furthermore, where

| (12) |

By convention we choose the right derivative and note that . The following basic result is proven in Appendix.

Lemma 12.

For any it holds that

and the series is absolutely convergent.

6.4. An application to financial mathematics

Exponentials of Lévy processes are used extensively in financial mathematics to model stock prices. They also appear in so–called unit–linked (or equity linked) life insurance models where an option is exercised upon death of an insured. In this context it is important that one can specify the distribution of the time horizon in a general and tractable way. In [16] the time horizon is assumed to have a density which is a linear combination (not necessarily being a mixture) of exponential densities, the class of which is dense in the class of distributions on the positive reals. In this way the classical Wiener–Hopf decomposition can be employed for each of the terms in the combination. They further assume that jumps (in both directions) are also combinations of exponentials, leading to a rational Lévy exponent. Below we provide a respective formula for an arbitrary ME time horizon and a spectrally-negative Lévy process.

In financial mathematics context, the following identity is well known:

see [26, Cor. 9.3] and references therein. One may also derive this identity in a few different ways using the above presented formulas in the classical setting of . Now we can extend this result to ME time horizon, where we also include the second Wiener-Hopf factor. The following result can be proven using (13) and other related ME formulas, but it is much easier to simply extend the desired formula from exponential to ME time.

Lemma 13.

Let and consider independent of , such that the real parts of the eigenvalues of exceed when . Then for we have

| (14) |

assuming that is not an eigenvalue of .

Proof.

Recall that assuming . If then this condition is always satisfied, and otherwise it is equivalent to . Now for we have

In the case this identity readily extends to and the result follows from (2). Otherwise, the formula is true for such that and we may use (2) by assumption on the eigenvalues of . Finally, if had an eigenvalue then would be an eigenvalue of according to . Thus is invertible. ∎

7. Examples

7.1. Strictly stable Lévy processes

A strictly stable (or self-similar) Lévy process, , is characterized by the property that has the law of for any and some , see [30, Ch. 3]. In the spectrally-negative case it must be that , where corresponds to a Brownian motion. If we (without real loss of generality) fix the scale parameter so that , then we readily get

| (15) |

Such processes have received a great deal of attention in the literature, see, for example, [10, 8, 13].

Here we derive explicit formulas for the basic objects appearing in the above fluctuation identities. Firstly, and thus

The other formulas are based on the Mittag-Leffler function:

which is analytic for . The scale function is given in terms of the derivative of the Mittag-Leffler function [11]: . Noting that

we arrive at the formula

From the well known identity [17, Sec. 4.3] we then obtain

Results concerning the second scale function are formulated in the following lemma.

Lemma 14.

In the stable case there are the identities for

where denotes the lower incomplete Gamma function.

Proof.

We readily find that leading to the first formula. For the second identity, simply write in terms of its series expansion and interchange summation and integration, which can be justified by a dominated convergence argument. ∎

7.2. The scale function in the case of ME jumps

Here we assume that the generator matrix is diagonalizable, see (3), which readily gives

Thus it is sufficient to obtain for .

Assume that has finite jump activity and the jump distribution is ME. In other words we consider a Cramér-Lundberg process with ME jumps possibly perturbed by an independent Brownian motion. The classical () scale function is explicit in this case, see [15, 25]. It is given in terms of the zeros of the rational function . Importantly, this result readily extends to any :

assuming that the roots are distinct. Indeed, its transform is which is a partial fraction decomposition of . The case of non-distinct roots, which is a bit more cumbersome, is also analogous to the case .

8. Numerics

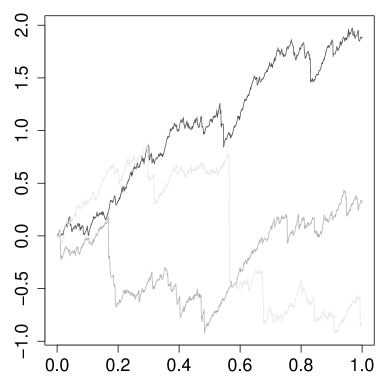

For the purpose of illustration we consider a strictly stable Lévy process with and as discussed in Section 7.1, and an ME density

This is a genuine matrix exponential distribution which is not of phase–type. A (canonical) representation is given by

and the eigenvalues for are . Some paths of and the ME density are depicted in Figure 1.

Our numerical experiments are carried out in R language. All the implemented formulas are checked against simulations, where the process is sampled on the grid with step size . The time horizon is simulated by inversion which uses a numerical root finding routine. The number of sampled paths is set to . Note that there is both a systematic error due to sampling on the grid and a Monte Carlo error.

Firstly, we compute

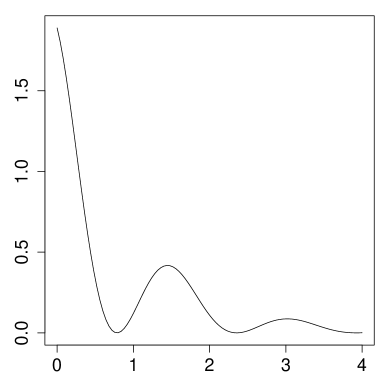

Secondly, the scale function is implemented using diagonalization and the standard Mittag-Leffler function, see Section 7.1. We provide its entries in Figure 2. Observe that these need not be positive or monotone. Note also that one may expect numerical issues for larger argument values, and so it may be useful to rewrite certain formulas in terms of a normalized version .

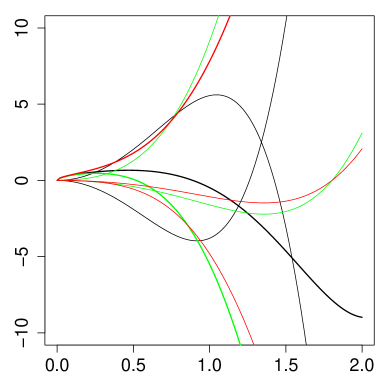

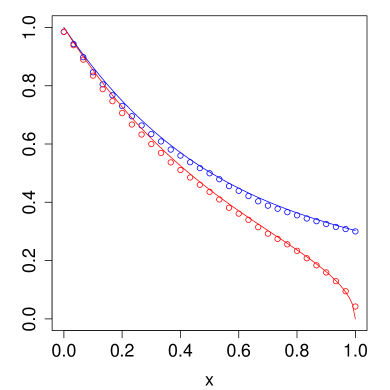

Having the basic constituents and , we may now illustrate our formulas The one- and two-sided first passage probabilities, and , obtained using Theorem 3 and Theorem 6 are presented in Figure 3 (Left). For comparison, we also provide simulated values of these probabilities, and note that these are rather close to the exact values obtained from our formulas.

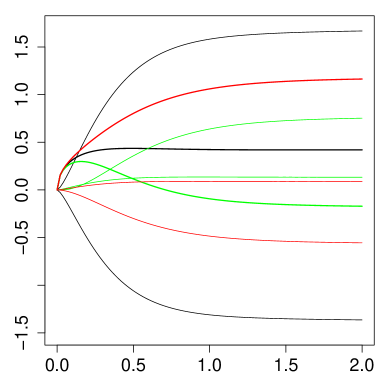

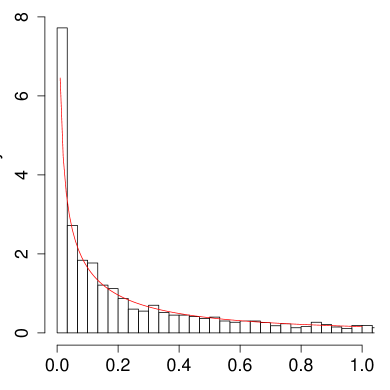

Next, we consider the density of which can be easily obtained from (13). Its expression involves and we refer to Section 7.1 for the corresponding formula. In Figure LABEL:fig:hist (Right) we plot this density over a histogram of simulated values of . Again we observe an agreement between the exact formula and simulations.

9. ME inter-observation times: an open problem

An important application of the fluctuation theory for an exponential time horizon concerns risk processes observed at the epochs of an independent Poisson process, see [3] a references therein for a suite of identities. Generalization of these identities to the case when observation epochs form an independent renewal process with ME inter-arrival times is not straightforward, and requires further study. In the case of PH inter-arrivals one may resort to the existing theory for Markov additive process, which we now demonstrate. For an alternative approach in the case of Erlang interarrival times see [1].

Let be the epochs of an independent renewal process with inter-arrival times. Define the ruin time as , which corresponds to the first observation of the process while it is negative. A slight adaptation of [2, Thm. 4.1] and its proof to the present setting yields the following result.

Proposition 15.

For any and interarrival distribution there is the formula

Note that is the transition rate matrix of the first passage Markov chain for the model with termination according to the given PH distribution, see Corollary 4. Furthermore, is the transition rate matrix of the Markov chain representing the PH distribution which is restarted according to upon termination. It corresponds to a recurrent Markov chain, and without real loss of generality we may assume it is irreducible. Thus has a single eigenvalue at 0. Nevertheless coincides with the scale matrix of our Markov additive process, which can be seen by comparing the transforms.

An extension of Proposition 15 to an arbitrary positive initial capital can be obtained from the strong Markov property of the associated Markov additive process. Furthermore, the limit obtained by has an explicit form in terms of a solution to a certain Sylvester equation, which is derived analogously to [2, Thm. 4.2]. It is an interesting open question on how to generalize the above result to ME inter-arrival times where a probabilistic interpretation is not readily available.

Appendix A Remaining proofs

Proof of Lemma 2.

The first statement is well known, and it readily follows from (5). For any a standard application of optional stopping yields

Noting that we may extend this identity to all . Next, we assume that and let . Bu the dominated convergence we readily obtain

which is a standard identity but now extended to such that . But now

according to 5 continued to . Thus indeed and the uniqueness result is obvious. ∎

Proof of Lemma 5.

For any and there is the identity (see [28, Eg. (6)] for ):

which readily follows by taking transforms of both sides in and using (7). Here we apply Fubini on the left hand side and in that respect we note the bound which readily follows from (9). Moreover, for and we also have

obtained by analytic continuation. Thus if then for all , but then from the above formula we get for all , contradicting the basic fact that for . ∎

Proof of Lemma 8.

Use (9) to observe that

where the series is absolutely convergent. Thus can be analytically continued to .

Proof of Lemma 12.

Recall that is the th convolution power of the non-decreasing, non-negative scale function ; here we drop the subscript to simplify notation. We start by observing for any that

| (16) | |||

Note that are non-decreasing functions of and so the first term is upper bounded by . The second term is upper bounded by

where the first inequality is obtained by dropping out the term . But

for all and hence the dominated convergence theorem can be applied.

∎

Acknowledgments

The second author gratefully acknowledges the financial support of Sapere Aude Starting Grant 8049-00021B “Distributional Robustness in Assessment of Extreme Risk”.

References

- [1] H. Albrecher, E. C. Cheung, and S. Thonhauser. Randomized observation periods for the compound Poisson risk model: the discounted penalty function. Scandinavian Actuarial Journal, 2013(6):424–452, 2013.

- [2] H. Albrecher and J. Ivanovs. A risk model with an observer in a Markov environment. Risks, 1(3):148–161, 2013.

- [3] H. Albrecher, J. Ivanovs, and X. Zhou. Exit identities for Lévy processes observed at Poisson arrival times. Bernoulli, 22(3):1364–1382, 2016.

- [4] S. Asmussen, F. Avram, and M. Usabel. Erlangian approximations for finite-horizon ruin probabilities. Astin Bull., 32(2):267–281, 2002.

- [5] S. Asmussen and J. Ivanovs. A factorization of a Lévy process over a phase-type horizon. Stoch. Models, 34(4):397–408, 2018.

- [6] F. Avram, D. Grahovac, and C. Vardar-Acar. The , scale functions kit for first passage problems of spectrally negative Lévy processes, and applications to control problems. ESAIM Probab. Stat., 24:454–525, 2020.

- [7] C. Berg, K. Boyadzhiev, and R. Delaubenfels. Generation of generators of holomorphic semigroups. Journal of the Australian Mathematical Society. Series A. Pure Mathematics and Statistics, 55(2):246–269, 1993.

- [8] V. Bernyk, R. C. Dalang, and G. Peskir. The law of the supremum of a stable Lévy process with no negative jumps. Ann. Probab., 36(5):1777–1789, 2008.

- [9] J. Bertoin. Lévy processes, volume 121 of Cambridge Tracts in Mathematics. Cambridge University Press, Cambridge, 1996.

- [10] J. Bertoin. On the first exit time of a completely asymmetric stable process from a finite interval. Bull. London Math. Soc., 28(5):514–520, 1996.

- [11] J. Bertoin. Exponential decay and ergodicity of completely asymmetric Lévy processes in a finite interval. Ann. Appl. Probab., 7(1):156–169, 1997.

- [12] M. Bladt and B. F. Nielsen. Matrix-exponential distributions in applied probability, volume 81 of Probability Theory and Stochastic Modelling. Springer, New York, 2017.

- [13] G. Coqueret. On the supremum of the spectrally negative stable process with drift. Statist. Probab. Lett., 107:333–340, 2015.

- [14] B. D’Auria, J. Ivanovs, O. Kella, and M. Mandjes. First passage of a Markov additive process and generalized Jordan chains. J. Appl. Probab., 47(4):1048–1057, 2010.

- [15] M. Egami and K. Yamazaki. Phase-type fitting of scale functions for spectrally negative Lévy processes. J. Comput. Appl. Math., 264:1–22, 2014.

- [16] H. U. Gerber, E. S. Shiu, and H. Yang. Valuing equity-linked death benefits in jump diffusion models. Insurance: Mathematics and Economics, 53(3):615 – 623, 2013.

- [17] R. Gorenflo, A. A. Kilbas, F. Mainardi, S. V. Rogosin, et al. Mittag-Leffler functions, related topics and applications, volume 2. Springer, 2014.

- [18] N. J. Higham. Functions of matrices. Society for Industrial and Applied Mathematics (SIAM), Philadelphia, PA, 2008. Theory and computation.

- [19] G. Horváth, I. Horváth, S. A.-D. Almousa, and M. Telek. Numerical inverse Laplace transformation using concentrated matrix exponential distributions. Performance Evaluation, 137:102067, 2020.

- [20] G. Horváth, I. Horváth, and M. Telek. High order concentrated matrix-exponential distributions. Stoch. Models, 36(2):176–192, 2020.

- [21] J. Ivanovs. One-sided Markov additive processes and related exit problems. BOXPress, 2011. PhD thesis.

- [22] J. Ivanovs. A note on killing with applications in risk theory. Insurance: Mathematics and Economics, 52(1):29 – 34, 2013.

- [23] J. Ivanovs and Z. Palmowski. Occupation densities in solving exit problems for Markov additive processes and their reflections. Stochastic Process. Appl., 122(9):3342–3360, 2012.

- [24] V. S. Koroljuk, V. N. Suprun, and V. M. Šurenkov. A potential-theoretic method in boundary problems for processes with independent increments and jumps of the same sign. Teor. Verojatnost. i Primenen., 21(2):253–259, 1976.

- [25] A. Kuznetsov, A. E. Kyprianou, and V. Rivero. The theory of scale functions for spectrally negative Lévy processes. In Lévy matters II, volume 2061 of Lecture Notes in Math., pages 97–186. Springer, Heidelberg, 2012.

- [26] A. E. Kyprianou. Introductory lectures on fluctuations of Lévy processes with applications. Universitext. Springer-Verlag, Berlin, 2006.

- [27] A. L. Lewis and E. Mordecki. Wiener-Hopf factorization for Lévy processes having positive jumps with rational transforms. J. Appl. Probab., 45(1):118–134, 2008.

- [28] R. L. Loeffen, J.-F. Renaud, and X. Zhou. Occupation times of intervals until first passage times for spectrally negative Lévy processes. Stochastic Process. Appl., 124(3):1408–1435, 2014.

- [29] O. Peralta–Gutiérrez. Advances of matrix–analytic methods in risk modelling. 2018. PhD thesis, Technical University of Denmark.

- [30] K.-i. Sato. Lévy processes and infinitely divisible distributions, volume 68 of Cambridge Studies in Advanced Mathematics. Cambridge University Press, Cambridge, 2013. Translated from the 1990 Japanese original, Revised edition of the 1999 English translation.

- [31] R. L. Schilling, R. Song, and Z. Vondraček. Bernstein functions, volume 37 of De Gruyter Studies in Mathematics. Walter de Gruyter & Co., Berlin, second edition, 2012. Theory and applications.

- [32] D. A. Stanford, F. Avram, A. L. Badescu, L. Breuer, A. da Silva Soares, and G. Latouche. Phase-type approximations to finite-time ruin probabilities in the Sparre-Andersen and stationary renewal risk models. Astin Bull., 35(1):131–144, 2005.

- [33] D. V. Widder. The Laplace Transform. Princeton Mathematical Series, v. 6. Princeton University Press, Princeton, N. J., 1941.