Neural networks-based algorithms for stochastic control and PDEs in finance 111This paper is a contribution for the Machine Learning for Financial Markets: a guide to contemporary practices, Cambridge University Press, Editors: Agostino Capponi and Charles-Albert Lehalle. This study was supported by FiME (Finance for Energy Market Research Centre) and the “Finance et Développement Durable - Approches Quantitatives” EDF - CACIB Chair.

Abstract

This paper presents machine learning techniques and deep reinforcement learning-based algorithms for the efficient resolution of nonlinear partial differential equations and dynamic optimization problems arising in investment decisions and derivative pricing in financial engineering. We survey recent results in the literature, present new developments, notably in the fully nonlinear case, and compare the different schemes illustrated by numerical tests on various financial applications. We conclude by highlighting some future research directions.

1 Breakthrough in the resolution of high dimensional non-linear problems

The numerical resolution of control problems and nonlinear PDEs– arising in several financial applications such as portfolio selection, hedging, or derivatives pricing–is subject to the so-called “curse of dimensionality”, making impractical the discretization of the state space in dimension greater than 3 by using classical PDE resolution methods such as finite differences schemes. Probabilistic regression Monte-Carlo methods based on a Backward Stochastic Differential Equation (BSDE) representation of semilinear PDEs have been developed in [Zha04], [BT04], [GLW05] to overcome this obstacle. These mesh-free techniques are successfully applied upon dimension 6 or 7, nevertheless, their use of regression methods requires a number of basis functions growing fastly with the dimension. What can be done to further increase the dimension of numerically solvable problems?

A breakthrough with deep learning based-algorithms has been made in the last five years towards this computational challenge, and we mention the recent survey by [Bec+20]. The main interest in the use of machine learning techniques for control and PDEs is the ability of deep neural networks to efficiently represent high dimensional functions without using spatial grids, and with no curse of dimensionality [Gro+18], [Hut+20]. Although the use of neural networks for solving PDEs is not new, see e.g. [DPT94], the approach has been successfully revived with new ideas and directions. Neural networks have known a increasing popularity since the works on Reinforcement Learning for solving the game of Go by Google DeepMind teams. These empirical successes and the introduced methods allow to solve control problems in moderate or large dimension. Moreover, recently developed open source libraries like Tensorflow and Pytorch also offer an accessible framework to implement these algorithms.

A first natural use of neural networks for stochastic control concerns the discrete time setting, with the study of Markov Decision Processes, either in a brute force fashion or by using dynamic programming approaches. In the continuous time setting, and in the context of PDE resolution, we present various methods. A first kind of schemes is rather generic and can be applied to a variety of PDEs coming from a large range of applications. Other schemes rely on BSDE representations, strongly linked to stochastic control problems. In both cases, numerical evidence seems to indicate that the methods can be used in large dimension, greater than 10 and up to 1000 in certain studies. Some theoretical results also illustrates the convergence of specific algorithms. These advances pave the way for new methods dedicated to the study of large population games, studied in the context of mean field games and mean field control problems.

The outline of this article is the following. We first focus on some schemes for discrete time control in Section 2 before presenting generic machine learning schemes for PDEs in Subsection 3.1. Then we review BSDE-based machine learning methods for semilinear equations in Subsection 3.2.1. Existing algorithms for fully non-linear PDEs are detailed in Subsection 3.2.2 before presenting new BSDE schemes designed to treat this more difficult case. Numerical tests on CVA pricing and portfolio selection are conducted in Section 4 to compare the different approaches. Finally, we highlight in Section 5 further directions and perspectives including recent advances for the resolution of mean field games and mean field control problems with or without model.

2 Deep learning approach for stochastic control

We present in this section some recent breakthrough in the numerical resolution of stochastic control in high dimension by means of machine learning techniques. We consider a model-based setting in discrete-time, i.e., a Markov decision process, that could possibly be obtained from the time discretization of a continuous-time stochastic control problem.

Let us fix a probability space equipped with a filtration representing the available information at any time ( is the trivial -algebra). The evolution of the system is described by a model dynamics for the state process valued in :

| (2.1) |

where is a sequence of i.i.d. random variables valued in , with -measurable containing all the noisy information arriving between and , and is the control process valued in . The dynamics function is a measurable function from into , and assumed to be known. Given a running cost function , a finite horizon , and a terminal cost function, the problem is to minimize over control process a functional cost

| (2.2) |

In some relevant applications, we may require constraints on the state and control in the form: , . for some subset of . This can be handled by relaxing the state/constraint and introducing into the costs a penalty function : , and . For example, if the constraint set is in the form: , then one can take as penalty functions:

| (2.3) |

where are penalization parameters (large in practice) see e.g. [HE16].

2.1 Global approach

The method consists simply in approximating at any time , the feedback control, i.e. a function of the state process, by a neural network (NN):

| (2.4) |

where is a feedforward neural network on with parameters , and then to minimize over the global set of parameters the quantity (playing the role of loss function)

where is the state process associated with the NN feedback controls:

This basic idea of approximating control by parametric function of the state was proposed in [GM05], and updated with the use of (deep) neural networks by [HE16]. This method met success due to its simplicity and the easy accessibility of common libraries like TensorFlow for optimizing the parameters of the neural networks. Some recent extensions of this approach dealt with stochastic control problems with delay, see [HH21]. However, such global optimization over a huge set of parameters may suffer from being stuck in suboptimal traps and thus does not converge, especially for large horizon . An alternative is to consider controls with a single neural network giving more stabilized results as studied by [FMW19]. We focus here on feedback controls, which is not a restriction as we are in a Markov setting. For path-dependent control problems, we may consider recurrent neural networks to take into consideration the past of state trajectory as input of the policy.

2.2 Backward dynamic programming approach

In [Bac+21], the authors propose methods that combine ideas from numerical probability and deep reinforcement learning. Their algorithms are based on the classical dynamic programming (DP), (deep) neural networks for the approximation/learning of the optimal policy and value function, and Monte-Carlo regressions with performance and value iterations.

The first algorithm, called NNContPI, is a combination of dynamic programming and the approach in [HE16]. It learns sequentially the control by NN and performance iterations, and is designed as follows:

| (2.5) |

The second algorithm, refereed to as Hybrid-Now, combines optimal policy estimation by neural networks and dynamic programming principle, and relies on an hybrid procedure between value and performance iteration to approximate the value function by

neural network on with parameters .

| (2.7) |

| (2.8) |

The convergence analysis of Algorithms NNContPI and Hybrid-Now are studied in [Hur+21], and various applications in finance are implemented in [Bac+21]. These algorithms are well-designed for control problems with continuous control space or a ball in . In the case where the control space is finite, it is relevant to randomize controls, and then use classification methods by approximating the distribution of controls with neural networks and Softmax activation function.

3 Machine learning algorithms for nonlinear PDEs

By change of time scale, Markov decision process (2.1)-(2.2) can be obtained from the time discretization of a continuous-time stochastic control problem with controlled diffusion dynamics on

| (3.1) |

and cost functional to be minimized over control process valued in

| (3.2) |

In this case, it is well-known, see e.g. [Pha09], that the dynamic programming Bellman equation leads to a PDE in the form

| (3.3) |

where is the so-called Hamiltonian function. The numerical resolution of such class of second-order parabolic PDEs will be addressed in this section.

3.1 Deterministic approach by neural networks

In the schemes below, differential operators are evaluated by automatic differentiation of the network function approximating the solution of the PDE. Machine learning libraries such as Tensorflow or Pytorch allow to efficiently compute these derivatives. The studied PDE problem is

| (3.4) |

with a space differential operator, a subset of .

Deep Galerkin Method [SS17].

The Deep Galerkin Method is a meshfree machine learning algorithm to solve PDEs on a domain, eventually with boundary conditions. The principle is to sample time and space points according to a training measure, e.g. uniform on a bounded domain, and minimize a performance measure quantifying how well a neural network satisfies the differential operator and boundary conditions. The method consists in minimizing over neural network , the loss

| (3.5) |

with independent random variables in . [SS17] also prove a convergence result (without rate) for the Deep Galerkin method. This method is tested on financial problems by [AA+18]. A major advantage to this method is its adaptability to a large range of PDEs with or without boundary conditions. Indeed the loss function is straightforwardly modified according to changes in the constraints one wishes to enforce on the PDE solution. A related approach is the deep parametric PDE method, see [KJY20], and [GW20] applied to option pricing.

Other approximation methods

-

(i)

Physics informed neural networks [RPK19]. Physics informed neural networks use both data (obtained for a limited amount of samples from a PDE solution), and theoretical dynamics to reconstruct solutions from PDEs. The convergence of this method in the Second Order linear parabolic (or elliptic) case is proven in [SDEK20], see also [GAS20].

-

(ii)

Deep Ritz method [EY18]. The Deep Ritz method focuses on the resolution of the variational formulation from elliptic problems where the integral is evaluated by randomly sampling time and space points, like in the Deep Galerkin method [SS17] and the minimization is performed over the parameters of a neural network. This scheme is tested on Poisson equation with different types of boundary conditions. [MZ19] studies the convergence of the Deep Ritz algorithm.

3.2 Probabilistic approach by neural networks

3.2.1 Semi-linear case

In this paragraph, we consider semilinear PDEs of the form

| (3.6) |

for which we have the forward backward SDE representation

| (3.7) |

via the (non-linear) Feynman-Kac formula: , , , see [PP90].

Let be a subdivision with modulus , , satisfying , and consider the Euler-Maruyama discretization defined by

| (3.8) |

where , . Sample paths of act as training data in the machine learning setting. Thus our training set can be chosen as large as desired, which is relevant for training purposes as sit does not lead to overfitting.

The time discretization of the BSDE (3.7) can be written in backward induction as

| (3.9) |

which can be described as conditional expectation formulae

| (3.10) |

where is a notation for the conditional expectation w.r.t. .

The essence of this method is to write down the backward equation (3.9) as a forward equation. One approximates the initial condition and the component at each time by networks functions taking the forward process as input. The objective function to optimize is the error between the reconstructed dynamics and the true terminal condition. More precisely, the problem is to minimize over network functions , and sequences of network functions , , , the global quadratic loss function

| (3.11) |

where is defined by forward induction as

starting from . The output of this scheme, for the solution to this global minimization problem, supplies an approximation of the solution to the PDE at time , and approximations of the solution to the PDE (3.6) at times evaluated at , i.e., of , . The convergence of this algorithm through a posteriori error is studied by [HL20], see also [JL21]. A variant is proposed by [CWNMW19] which introduces a single neural network instead of independent neural networks. This simplifies the optimization problem and leads to more stable solutions. A close method introduced by [Rai18] uses also a single neural network and estimates as the automatic derivative in space of . We also refer to [JO19] for a variation of this deep BSDE scheme to curve-dependent PDEs arising in the pricing under rough volatility model, to [NR19] for approximations methods for Hamilton-Jacobi-Bellman PDEs, and to [KSS20] for extension of deep BSDE scheme to elliptic PDEs with applications in insurance.

Deep Backward Dynamic Programming (DBDP) [HPW20].

The method builds upon the backward dynamic programming relation (3.9) stemming from the time discretization of the BSDE, and approximates simultaneously at each time step the processes with neural networks trained with the forward diffusion process as input. The scheme can be implemented in two similar versions:

-

1.

DBDP1. Starting from , proceed by backward induction for , by minimizing over network functions , and the quadratic loss function

and update as the solution to this local minimization problem.

-

2.

DBDP2. Starting from , proceed by backward induction for , by minimizing over network functions the quadratic loss function

(3.12) (3.13) (3.14) where is the automatic differentiation of the network function . Update as the solution to this local minimization problem, and set .

The output of DBDP supplies an approximation of the solution and its gradient to the PDE (3.6) on the time grid , . The study of the approximation error due to the time discretization and the choice of the loss function is accomplished in [HPW20].

Variants and extensions of DBDP schemes

-

(i)

A regression-based machine learning scheme inspired by regression Monte-Carlo methods for numerically computing condition expectations in the time discretization (3.10) of the BSDE, is given by: starting from , proceed by backward induction for , in two regression problems:

-

(a)

Minimize over network functions

(3.15) and update as the solution to this minimization problem

-

(b)

Minimize over network functions

(3.16) and update as the solution to this minimization problem.

Compared to these regression-based schemes, the DBDP scheme simultaneously estimates the pair component through the minimization of the loss functions (or for the second version), . Interestingly, the convergence of the DBDP scheme can be confirmed by computing at each time step the infimum of loss function, which should vanish for the exact solution (up to the time discretization). In contrast, the infimum of the loss functions in usual regression-based schemes is unknown for the true solution as it is supposed to match the residual of -projection. Therefore the scheme accuracy cannot be directly verified.

-

(a)

-

(ii)

The DBDP scheme is based on local resolution, and was first used to solve linear PDEs, see [SVSS18]. It is also suitable to solve variational inequalities and can be used to valuate American options as shown in [HPW20]. Alternative methods consists in using the Deep Optimal Stopping scheme [BCJ19] or the method from [Bec+19a]. Some tests on Bermudan options are also performed by [LXL19] and [FTT19] with some refinements of the Deep BSDE scheme.

-

(iii)

The Deep Splitting (DS) scheme in [Bec+19] combines ideas from the DBDP2 and regression-based schemes. Indeed the current regression-approximation on is estimated by the automatic differentiation of the neural network computed at the previous optimization step. The current approximation of is then computed by a regression-type optimization problem. It can be seen as a local version of the global algorithm from [Rai18] or as a step by step Feynman-Kac approach. As the scheme is a local one, it can be used to valuate American options. The convergence of this method is studied by [GPW20].

-

(iv)

Local resolution permits to add other constraints such as constraints on a replication portfolio using facelifting techniques as in [KLW20].

-

(v)

The Deep Backward Multistep (MDBDP) scheme [GPW20] is described as follows: for , minimize over network functions , and the loss function

(3.17) (3.18) and update as the solution to this minimization problem. This output provides an approximation of the solution to the PDE (3.6) at times , .

MDBDP is a machine learning version of the Multi-step Forward Dynamic Programming method studied by [BD07] and [GT14]. Instead of solving at each time step two regression problems, our approach allows to consider only a single minimization as in the DBDP scheme. Compared to the latter, the multi-step consideration is expected to provide better accuracy by reducing the propagation of errors in the backward induction as it can be shown comparing the error estimated in [GPW20] and [HPW20] both at theoretical and numerical level.

3.2.2 Case of fully non-linear PDEs

In this paragraph, we consider fully non-linear PDEs in the form

| (3.19) |

For this purpose, we introduce a forward diffusion process in as in (3.7), and associated to the linear part of the differential operator in the l.h.s. of the PDE (3.19). Since the function contains the dependence both on the gradient and the Hessian , we can shift the linear differential operator (left hand side) of the PDE (3.19) into the function . However, in practice, this linear differential operator associated to a diffusion process is used for training simulations in SGD of machine learning schemes. We refer to Section 3.1 in [PWG21] for a discussion on the choice of the parameters , . In the sequel, we assume for simplicity that , and is a constant invertible matrix.

Let us derive formally a BSDE representation for the nonlinear PDE (3.19) on which we shall rely for designing our machine learning algorithm. Assuming that the solution to this PDE is smooth , and denoting by the triple of -adapted processes valued in , defined by

| (3.20) |

a direct application of Itô’s formula to , yields that satisfies the backward equation

| (3.21) |

Compared to the case of semi-linear PDE of the form (3.6), the key point is the approximation/learning of the Hessian matrix , hence of the -component of the BSDE (3.21). We present below different approaches for the approximation of the -component. To the best of our knowledge, no theoretical convergence result is available for machine learning schemes in the fully nonlinear case but several methods show good empirical performances.

Deep 2BSDE scheme [BEJ19].

This scheme relies on the 2BSDE representation of [Che+07]

| (3.22) |

with . The idea is to adapt the Deep BSDE algorithm to the fully non-linear case. Again, we treat the backward system (3.22) as a forward equation by approximating the initial conditions and the components of the 2BSDE at each time by networks functions taking the forward process as input, and aiming to match the terminal condition.

Second order DBDP (2DBDP) [PWG21].

The basic idea is to adapt the DBDP scheme by approximating the solution and its gradient by network functions and , and then Hessian by the automatic differentiation of the network function (or double automatic differentiation of the network function ), via a learning approach relying on the time discretization of the BSDE (3.21). It turns out that such method approximates poorly inducing instability of the scheme: indeed, while the unique pair solution to classical BSDEs (3.7) completely characterizes the solution to the related semilinear PDE and its gradient, the relation (3.21) does not allow to characterize directly the triple . This approach was proposed and tested in [PWG21] where the automatic differentiation is performed on the previous value of with a truncation which allows to reduce instabilities.

Second Order Multistep schemes.

To overcome the instability in the approximation of the -component in the Second order DBDP scheme, we propose a finer approach based on a suitable probabilistic representation of the -component for learning accurately the Hessian function by using also Malliavin weights. We start from the training simulations of the forward process on the uniform grid , , and notice that , as and are constants. The approximation of the value function and its gradient is learnt simultaneously on the grid but requires in addition a preliminary approximation of the Hessian in the fully non-linear case. This will be performed by regression-based machine learning scheme on a subgrid , which allows to reduce the computational time of the algorithm.

We propose three versions of second order MDBDP based on different representations of the Hessian function. For the second and the third one, we need to introduce a subgrid , of modulus , for some , with .

-

-

Version 1: Extending the methodology introduced in [PWG21], the current -component at step can be estimated by automatic differentiation of the -component at the previous step while the other -components are estimated by automatic differentiation of their associated -components:

(3.23) -

-

Version 2: The time discretization of (3.21) on the time grid , where denotes an approximation of the triple

leads to the standard representation formula for the component:

(3.24) (recall that denotes the conditional expectation w.r.t. ), with the Malliavin weight of order one:

(3.25) By direct differentiation, we then obtain an approximation of the component as

(3.26) Moreover, by introducing the antithetic variable

(3.27) we then propose the following regression estimator of on the grid for with

(3.28) -

-

Version 3: Alternatively, the time discretization of (3.21) on yields the iterated conditional expectation relation:

(3.29) By (double) integration by parts, and using Malliavin weights on the Gaussian vector , we obtain a multistep approximation of the -component:

(3.30) for , where

(3.31) By introducing again the antithetic variables

(3.32) we then propose another regression estimator of on the grid with

(3.33) (3.34) (3.35) (3.36) (3.37) for , and . The correction term evaluated at time in does not add bias since

(3.38) for all , and by Taylor expansion of at second order, we see that it allows together with the antithetic variable to control the variance when the time step goes to zero.

Remark 3.1.

In the case where the function has some regularity property, one can avoid the integration by parts at the terminal data component in the above expression of . For example, when is , is alternatively replaced in expression by , while when it is it is replaced by .

Remark 3.2.

We point out that in our machine learning setting for the versions 2 and 3 of the scheme, we only solve two optimization problems by time step instead of three as in [FTW11]. One optimization is dedicated to the computation of the component but the and components are simultaneously learned by the algorithm.

We can now describe the three versions of second order MDBDP schemes for the numerical resolution of the fully non-linear PDE (3.19). We emphasize that these schemes do not require a priori that the solution to the PDE is smooth.

| (3.39) | |||

| (3.40) |

| (3.41) |

| (3.42) | |||

| (3.43) |

| (3.44) | |||

| (3.45) | |||

| (3.46) | |||

| (3.47) | |||

| (3.48) |

| (3.49) | |||

| (3.50) |

The proposed algorithms 3, 4, 5 are in backward iteration, and involve one optimization at each step. Moreover, as the computation of requires a further derivation for Algorithms 4 and 5, we may expect that the additional propagation error varies according to , and thus the convergence of the scheme when is large. In the numerical implementation, the expectation in the loss functions are replaced by empirical average and the minimization over network functions is performed by stochastic gradient descent.

4 Numerical applications

We test our different algorithms on various examples and by varying the state space dimension. If not stated otherwise, we choose the maturity . In each example we use an architecture composed of 2 hidden layers with neurons. We apply Adam gradient descent [KB14] with a decreasing learning rate, using the Tensorflow library [Aba+16]. Each numerical experiment is conducted using a node composed of 2 Intel® Xeon® Gold 5122 Processors, 192 Go of RAM, and 2 GPU nVidia® Tesla® V100 16Go. We use a batch size of 1000.

4.1 Numerical tests on credit valuation adjustment pricing

We consider an example of model from [HL17] for the pricing of CVA in a -dimensional Black-Scholes model

| (4.1) |

with , given by the nonlinear PDE

| (4.2) |

with a straddle type payoff. We compare our results with the DBDP scheme [HPW20] with the ones from the Deep BSDE solver [HJE17]. The results in Table 1 are averaged over 10 runs and the standard deviation is written in parentheses. We use ReLu activation functions.

| Dimension | DBDP [HPW20] | DBSDE [HJE17] |

|---|---|---|

| 1 | 0.05950 (0.000257) | 0.05949 (0.000264) |

| 3 | 0.17797 (0.000421) | 0.17807 (0.000288) |

| 5 | 0.25956 (0.000467) | 0.25984 (0.000331) |

| 10 | 0.40930 (0.000623) | 0.40886 (0.000196) |

| 15 | 0.52353 (0.000591) | 0.52389 (0.000551) |

| 30 | 0.78239 (0.000832) | 0.78231 (0.001266) |

We observe in Table 1 that both algorithms give very close results and are able to solve the nonlinear pricing problem in high dimension . The variance of the results is quite small and similar from one to another but increases with the dimension. The same conclusions arise when solving the PDE for the larger maturity .

4.2 Portfolio allocation in stochastic volatility models

We consider several examples from [PWG21] that we solve with Algorithms 3 (2EMDBDP), 4 (2MDBDP), and 5 (2M2DBDP) designed in this paper. Notice that some comparison tests with the 2DBSDE scheme [BEJ19] have been already done in [PWG21]. For a resolution with , the execution of our multitep algorithms takes between 10000 s. and 30000 s. (depending on the dimension) with a number of gradient descent iterations fixed at 4000 at each time step except 80000 at the first one. We use tanh as activation function.

We consider a portfolio selection problem formulated as follows. There are risky assets of uncorrelated price process with dynamics governed by

| (4.3) |

where is a -dimensional Brownian motion, is the market price of risk of the assets, is a positive function (e.g. corresponding to the Scott model), and is the volatility factor modeled by an Ornstein-Uhlenbeck (O.U.) process

| (4.4) |

with , and a -dimensional Brownian motion, s.t. , with . An agent can invest at any time an amount in the stocks, which generates a wealth process governed by

The objective of the agent is to maximize her expected utility from terminal wealth:

| (4.5) |

It is well-known that the solution to this problem can be characterized by the dynamic programming method (see e.g. [Pha09]), which leads to the Hamilton-Jacobi-Bellman for the value function on :

with a Sharpe ratio , for . The optimal portfolio strategy is then given in feedback form by , where is given by

| (4.6) | |||

| (4.7) |

for .

We shall test this example when the utility function is of exponential form: , with , and under different cases for which explicit solutions are available. We refer to [PWG21] where these solutions are described.

-

(1)

Merton problem. This corresponds to a degenerate case where the factor , hence the volatility and the risk premium are constant (). We train our algorithms with the forward process

(4.8) -

(2)

One risky asset: . We train our algorithms with the forward process

(4.9) (4.10) We test our algorithm with , , for which we have an explicit solution.

-

(3)

No leverage effect, i.e., , . We train with the forward process

(4.11) (4.12) We test our algorithm with , , , , for which we have an explicit solution.

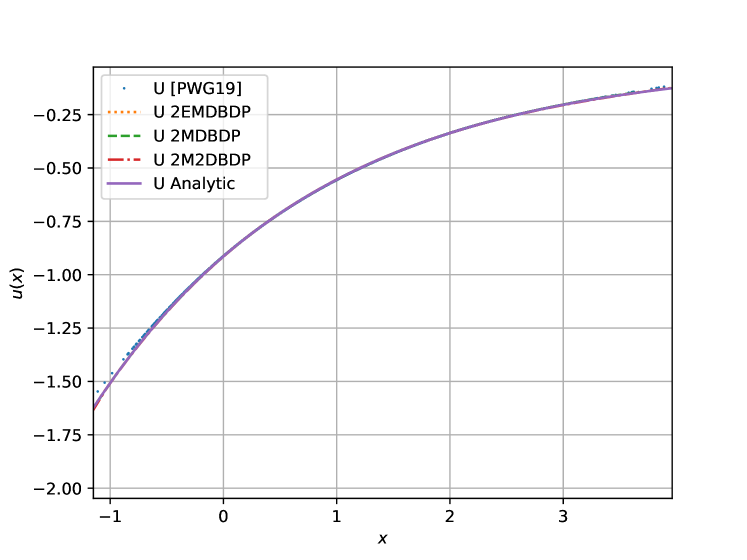

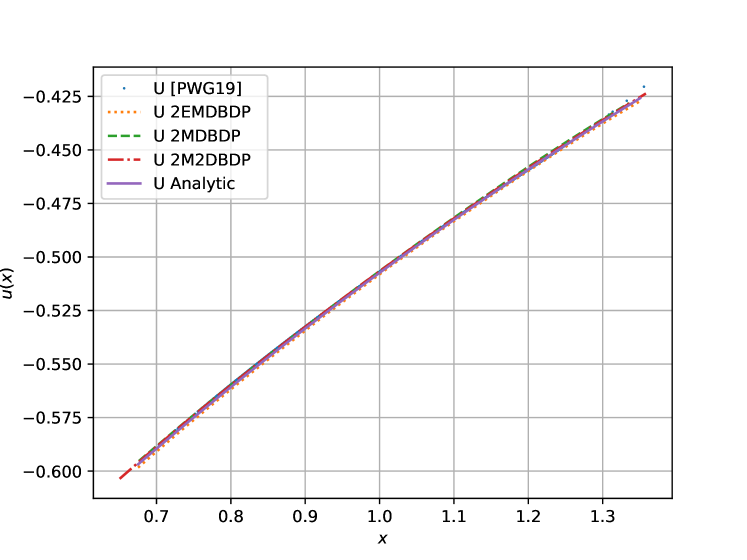

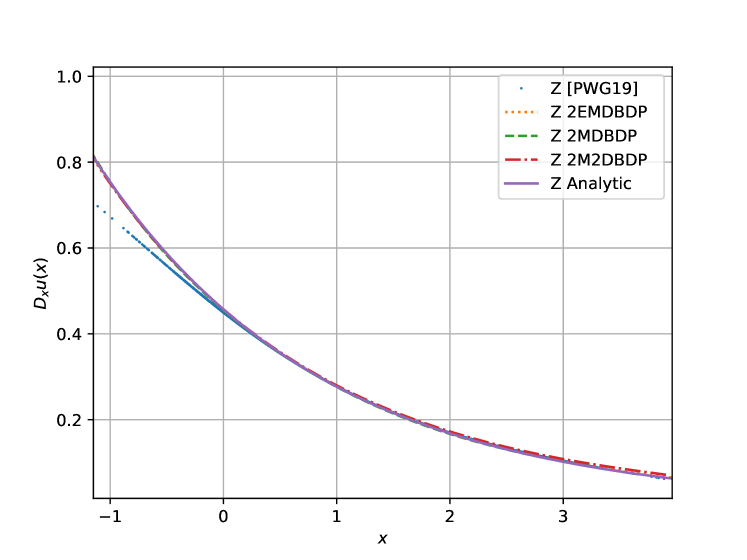

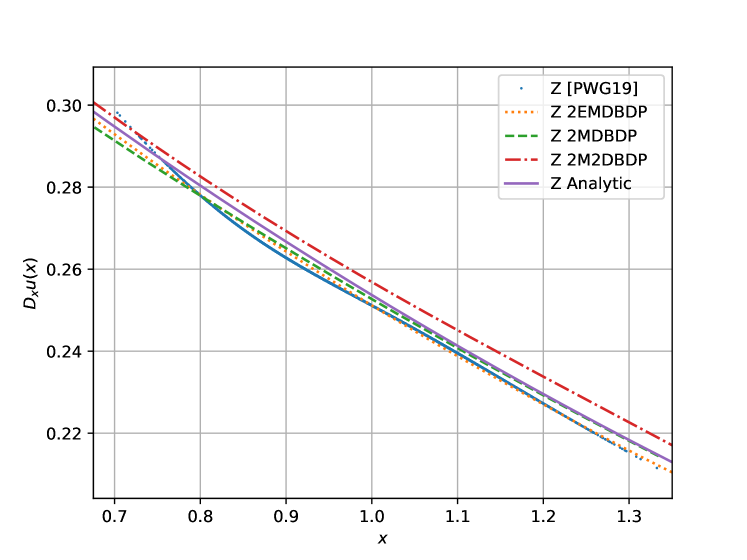

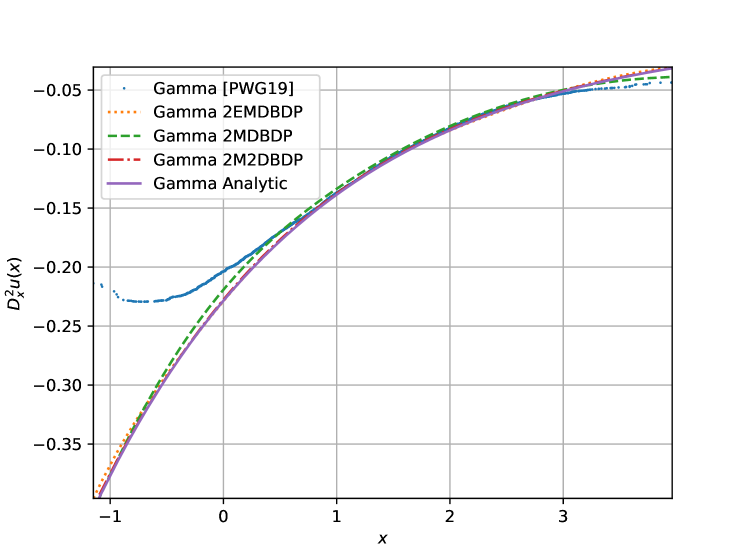

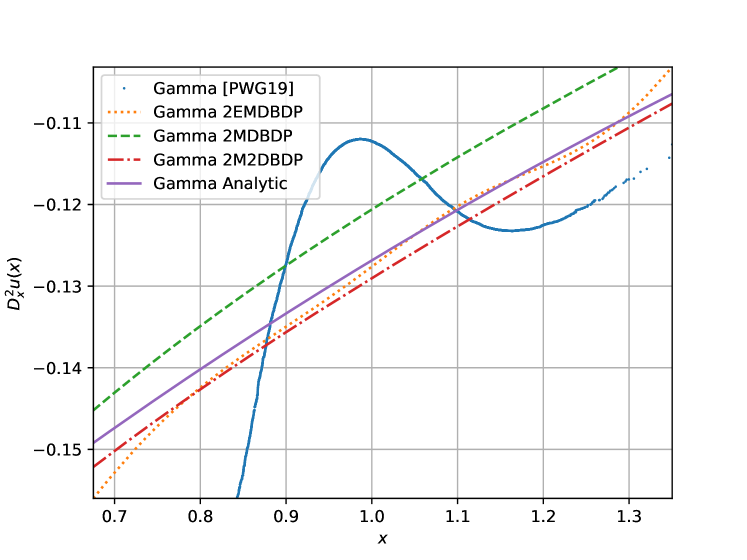

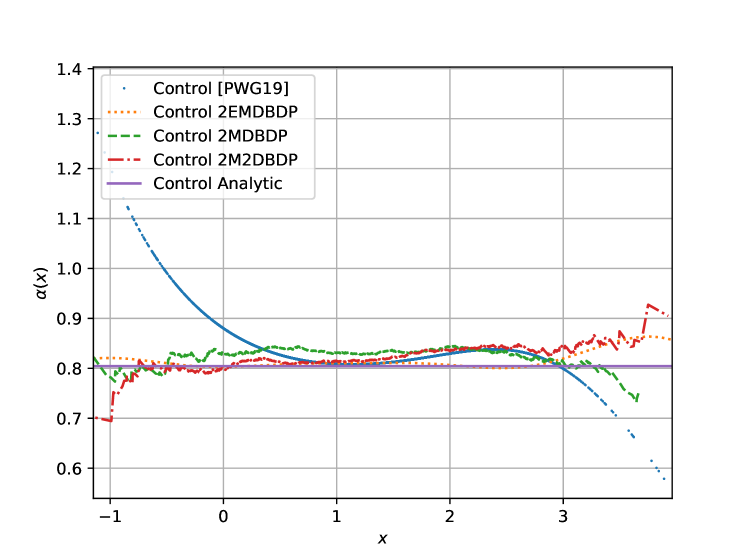

Merton Problem. We take , , , , , We plot in Figure 1 the neural networks approximation of , and the feedback control (for one asset) computed from our different algorithms, together with their analytic values (in orange). As also reported in the estimates of Table 2, the multistep algorithms improve significantly the results obtained in [PWG21], where the estimation of the Hessian is not really accurate (see blue curve in Figure 1).

| Average | Standard deviation | Relative error (%) | |

| [PWG21] | -0.50561 | 0.00029 | 0.20 |

| 2EMDBDP | -0.50673 | 0.00019 | 0.022 |

| 2MDBDP | -0.50647 | 0.00033 | 0.030 |

| 2M2DBDP | -0.50644 | 0.00022 | 0.035 |

One asset in Scott volatility model. We take , , , , , , , For all tests we choose , and . We report in Table 3 the relative error between the neural networks approximation of computed from our different algorithms and their analytic values. It turns out that the multistep extension of [PWG21], namely 2EMDBDP scheme, yields a very accurate approximation result, much better than the other algorithms, with also a reduction of the standard deviation.

| Average | Standard deviation | Relative error (%) | |

| [PWG21] | -0.53431 | 0.00070 | 0.34 |

| 2EMDBDP | -0.53613 | 0.00045 | 0.007 |

| 2MDBDP | -0.53772 | 0.00046 | 0.304 |

| 2M2DBDP | -0.53205 | 0.00050 | 0.755 |

No Leverage in Scott model. In the case with one asset we take , , , , , , For all tests we choose , and . We report in Table 4 the relative error between the neural networks approximation of computed from our different algorithms and their analytic values. All the algorithms yield quite accurate results, but compared to the case with correlation in Table 3, it appears here that the best performance in terms of precision is achieved by Algorithm 2M2DBDP.

| Average | Standard deviation | Relative error (%) | |

| [PWG21] | -0.49980 | 0.00073 | 0.35 |

| 2EMDBDP | -0.50400 | 0.00229 | 0.485 |

| 2MDBDP | -0.50149 | 0.00024 | 0.015 |

| 2M2DBDP | -0.50157 | 0.00036 | 0.001 |

In the case with four assets ( , ), we take ,

, ,

, .

The results are reported in Table 5. We observe that the algorithm in [PWG21] provides a not so accurate outcome, while its multistep version (2EMDBDP scheme) divides by the relative error and the standard deviation.

| Average | Standard deviation | Relative error (%) | |

| [PWG21] | -0.43768 | 0.00137 | 0.92 |

| 2EMDBDP | -0.4401 | 0.00051 | 0.239 |

| 2MDBDP | -0.43796 | 0.00098 | 0.861 |

| 2M2DBDP | -0.44831 | 0.00566 | 1.481 |

In the case with nine assets ( , ), we take ,

,

,

,

.

The results are reported in Table 6.

The approximation is less accurate than in lower dimension, but we observe again that compared to one-step scheme in [PWG21] ,

the multistep versions improve significantly the standard deviation of the result. However the best performance in precision is obtained here by the [PWG21] scheme.

| Average | S.d. | Relative error (%) | ||

| [PWG21] | -0.27920 | 0.05734 | 1.49 | |

| 2EMDBDP | -0.26631 | 0.00283 | 3.19 | |

| 2MDBDP | 30 | -0.28979 | 0.00559 | 5.34 |

| 2MDBDP | 60 | -0.28549 | 0.00948 | 3.78 |

| 2MDBDP | 120 | -0.28300 | 0.01129 | 2.87 |

| 2M2DBDP | 30 | NC | NC | NC |

5 Extensions and perspectives

Solving mean-field control and mean-field games through McKean-Vlasov FBSDEs.

These methods solve the optimality conditions for mean-field problems through the stochastic Pontryagin principle from [CD18]. The law of the solution influences the coupled FBSDEs dynamics so they are of McKean-Vlasov type. Variations around the Deep BSDE method [HJE17] are used to solve such a system by [CL19], [FZ20]. [GMW19] uses the Merged method from [CWNMW19] and solves several numerical examples in dimension 10 by introducing an efficient law estimation technique. [CL19] also proposes another method dedicated to mean field control to directly tackle the optimization problem with a neural network as the control in the stochastic dynamics. The player games, before going to the mean-field limit of an infinite number of players, are solved by [Hu19], [HHL20].

Solving mean-field control through master Bellman equation and symmetric neural networks.

[Ger+21] solves the master Bellman equation arising from dynamic programming principle applied to mean-field control problems (see [PW17]). The paper approximates the value function evaluated on the empirical measure stemming from particles simulation of a training forward process. The symmetry between iid particles is enforced by optimizing over exchangeable high-dimensional neural networks, invariant by permutation of their inputs. The companion paper [GPW21] provides a rate for the particle method convergence.

Reinforcement Learning for mean-field control and mean-field games [CLT19, AKS19, AFL20, Gu+20, Guo+20].

Some works focus on similar problems but with unknown dynamics. Thus they rely on trajectories sampled from a simulator and reinforcement learnings– especially Q-learning– to estimate the state action value function and optimal control without a model. The idea is to optimize a neural network by relying on a memory of past state action transitions used to train the network in order for it to verify the Bellman equation on samples from memory replay.

Machine learning framework for solving high-dimensional mean field game and mean field control problems [Rut+20]

This paper focuses on potential mean field games, in which the cost functions depending on the law can be written as the linear functional derivative of a function with respect to a measure. A Lagrangian method with Deep Galerkin type penalization is used. In this case the potential is approached by a neural network and solving mean-field games amounts to solve an unconstrained optimization problem.

Deep quantum neural networks [Sak20]

We briefly mention this work studying the use of deep quantum neural networks which exploit the quantum superposition properties by replacing bits by “qubits”. Promising results are obtained when using these networks for regression in financial contexts such as implied volatility estimation. Future works may study the application of such neural networks to control problems and PDEs.

Path signature for path-dependent PDE [SVSS20]

This work extends previously developed methods for solving state-dependent PDEs to the linear path-dependent setting coming for instance from the pricing and hedging of path-dependent options. A path-dependent Feynman-Kac representation is numerically computed through a global minimization over neural networks. The authors show that using LSTM networks taking the forward process’ path signatures (coming from the rough paths literature) as input yields better results than taking the discretized path as input of a feedforward network.

References

- [AA+18] A. Al-Aradi, A. Correia, D. Naiff, G. Jardim and Y. Saporito “Solving Nonlinear and High-Dimensional Partial Differential Equations via Deep Learning” In arXiv:1811.08782, 2018

- [Aba+16] M. Abadi et al. “TensorFlow: A system for large-scale machine learning” In 12th USENIX Symposium on Operating Systems Design and Implementation (OSDI 16), 2016, pp. 265–283

- [AFL20] A. Angiuli, J.-P. Fouque and M. Laurière “Unified Reinforcement Q-Learning for Mean Field Game and Control Problems” In arXiv:2006.13912, 2020

- [AKS19] B. Anahtarcı, C. Deha Karıksız and N. Saldi “Fitted Q-Learning in Mean-field Games” In arXiv:1912.13309, 2019

- [Bac+21] A. Bachouch, C. Huré, H. Pham and N. Langrené “Deep neural networks algorithms for stochastic control problems on finite horizon: numerical computations” In Methodol. Comput. Appl. Probab, 2021

- [BCJ19] S. Becker, P. Cheridito and A. Jentzen “Deep optimal stopping” In J. Mach. Learn. Res. 20, 2019, pp. 1–25

- [BD07] C. Bender and R. Denk “A forward scheme for backward SDEs” In Stochastic Process. Appl. 117.12, 2007, pp. 1793 –1812

- [Bec+19] C. Beck, S. Becker, P. Cheridito, A. Jentzen and A. Neufeld “Deep splitting method for parabolic PDEs” In arXiv:1907.03452, 2019

- [Bec+19a] S. Becker, P. Cheridito, A. Jentzen and T. Welti “Solving high-dimensional optimal stopping problems using deep learning” In arXiv:1908.01602, 2019

- [Bec+20] C. Beck, M. Hutzenthaler, A. Jentzen and B. Kuckuck “An overview on deep learning-based approximation methods for partial differential equations” In arXiv:2012.12348, 2020

- [BEJ19] C. Beck, W. E and A. Jentzen “Machine Learning Approximation Algorithms for High-Dimensional Fully Nonlinear Partial Differential Equations and Second-order Backward Stochastic Differential Equations” In J. Nonlinear Sci. 29.4, 2019, pp. 1563–1619

- [BT04] B. Bouchard and N. Touzi “Discrete-time approximation and Monte-Carlo simulation of backward stochastic differential equations” In Stochastic Process. Appl. 111.2, 2004, pp. 175 –206

- [CD18] R. Carmona and F. Delarue “Probabilistic Theory of Mean Field Games with Applications vol I. and II.” 83, Probability Theory and Stochastic Modelling Springer, 2018

- [Che+07] P. Cheridito, H.M. Soner, N. Touzi and N. Victoir “Second-order backward stochastic differential equations and fully nonlinear parabolic PDEs” In Comm. Pure Appl. Math. 60.7 Wiley-Liss Inc., 2007, pp. 1081–1110

- [CL19] R. Carmona and M. Laurière “Convergence analysis of machine learning algorithms for the numerical solution of mean-field control and games: II The finite horizon case” In arXiv:1908.01613, 2019

- [CLT19] R. Carmona, M. Laurière and Z. Tan “Model-Free Mean-Field Reinforcement Learning: Mean-Field MDP and Mean-Field Q-Learning” In arXiv:1910.12802, 2019

- [CWNMW19] Quentin Chan-Wai-Nam, Joseph Mikael and Xavier Warin “Machine Learning for Semi Linear PDEs” In J. Sci. Comput. 79, 2019, pp. 1667–1712

- [DPT94] M.W.M. Dissanayake and N. Phan-Thien “Neural network-based approximations for solving partial differential equations” In Commun. Numer. Methods Eng. 10.3, 1994, pp. 195–201

- [EHJ17] W. E, J. Han and A. Jentzen “Deep Learning-Based numerical methods for high dimensional parabolic partial differential equations and backward stochastic differential equations” In Commun. Math. Stat. 5.4, 2017, pp. 349–380

- [EY18] W. E and B. Yu “The Deep Ritz Method: A Deep Learning-Based Numerical Algorithm for Solving Variational Problems” In Commun. Math. Stat. 6, 2018, pp. 1–12

- [FMW19] S. Fécamp, J. Mikael and X. Warin “Risk management with machine-learning-based algorithms” In arXiv:1902.05287, to appear in Journal of Computational Finance, 2019

- [FTT19] M. Fujii, A. Takahashi and M. Takahashi “Asymptotic expansion as prior knowledge in deep learning method for high dimensional BSDEs” In Asia Pacific Financial Markets 26.3, 2019, pp. 391–408

- [FTW11] A. Fahim, N. Touzi and X. Warin “A probabilistic numerical method for fully nonlinear parabolic PDEs” In Ann. Appl. Probab. 21.4 The Institute of Mathematical Statistics, 2011, pp. 1322–1364

- [FZ20] J-.P. Fouque and Z. Zhang “Deep Learning Methods for Mean Field Control Problems with Delay” In Frontiers in Applied Mathematics and Statistics 6, 2020

- [GAS20] C. Gräser and P. A. Alathur Srinivasan “Error bounds for PDE-regularized learning” In arXiv:2003.06524, 2020

- [Ger+21] M. Germain, M. Laurière, H. Pham and X. Warin “DeepSets and derivative networks for solving symmetric PDEs” In arXiv: 2103.00838, 2021

- [GLW05] E. Gobet, J-P. Lemor and X. Warin “A regression-based Monte Carlo method to solve backward stochastic differential equations” In Ann. Appl. Probab. 15.3 The Institute of Mathematical Statistics, 2005, pp. 2172–2202

- [GM05] E. Gobet and R. Munos “Sensitivity analysis using Itô-Malliavin calculus and martingales, and application to stochastic optimal control” In SIAM J. Control Optim. 43.5, 2005, pp. 1676–1713

- [GMW19] M. Germain, J. Mikael and X. Warin “Numerical resolution of McKean-Vlasov FBSDEs using neural networks” In arXiv:1909.12678, 2019

- [GPW20] M. Germain, H. Pham and X. Warin “Deep backward multistep schemes for nonlinear PDEs and approximation error analysis” In arXiv:2006.01496v1, 2020

- [GPW21] M. Germain, H. Pham and X. Warin “Rate of convergence for particles approximation of PDEs in Wasserstein space” In arXiv: 2103.00837, 2021

- [Gro+18] P. Grohs, F. Hornung, A. Jentzen and P. Wurstemberger “A proof that rectified deep neural networks overcome the curse of dimensionality in the numerical approximation of Black-Scholes partial differential equation” In to appear in Memoirs of the American mathematical society, 2018

- [GT14] E. Gobet and P. Turkedjiev “Linear regression MDP scheme for discrete backward stochastic differential equations under general conditions” In Math. Comp. 85, 2014

- [Gu+20] H. Gu, X. Guo, X. Wei and R. Xu “Q-Learning Algorithm for Mean-Field Controls, with Convergence and Complexity Analysis” In arXiv:2002.04131, 2020

- [Guo+20] X. Guo, A. Hu, R. Xu and J. Zhang “A General Framework for Learning Mean-Field Games” In arXiv:2003.06069, 2020

- [GW20] K. Glau and L. Wunderlich “The deep parametric PDE method: application to option pricing” In arXiv:2012.06211, 2020

- [HE16] J. Han and W. E “Deep learning approximation for stochastic control problems” In Deep Reinforcement Learning Workshop, 2016

- [HH21] J. Han and R. Hu “Recurrent Neural Networks for Stochastic Control Problems with Delay” In arXiv:2101.01385, 2021

- [HHL20] J. Han, R. Hu and J. Long “Convergence of deep fictitious play for stochastic differential games” In arXiv:2008.05519, 2020

- [HJE17] J. Han, A. Jentzen and W. E “Solving high-dimensional partial differential equations using deep learning” In Proc. Natl. Acad. Sci. USA 115, 2017

- [HL17] P. Henry-Labordere “Deep Primal-Dual Algorithm for BSDEs: Applications of Machine Learning to CVA and IM” In Available at SSRN: https://ssrn.com/abstract=3071506, 2017

- [HL20] J. Han and J. Long “Convergence of the Deep BSDE Method for Coupled FBSDEs” In Probab. Uncertain. Quant. Risk 5.1, 2020, pp. 1–33

- [HPW20] C. Huré, H. Pham and X. Warin “Deep backward schemes for high-dimensional nonlinear PDEs” In Math. Comp. 89.324, 2020, pp. 1547–1580

- [Hu19] R. Hu “Deep fictitious play for stochastic differential games” In arXiv:1903.09376, 2019

- [Hur+21] C. Huré, H. Pham, A. Bachouch and N. Langrené “Deep neural networks algorithms for stochastic control problems on finite horizon: convergence analysis” In SIAM J. Numer. Anal. 59.1, 2021, pp. 525–557

- [Hut+20] M. Hutzenthaler, A. Jentzen, T. Kruse and T.A. Nguyen “A proof that rectified deep neural networks overcome the curse of dimensionality in the numerical approximation of semilinear heat equation” In SN partial differential equations and applications 1.10, 2020, pp. 1–34

- [JL21] Y. Jiang and J. Li “Convergence of the Deep BSDE method for FBSDEs with non-Lipschitz coefficients” In arXiv:2101.01869, 2021

- [JO19] A. Jacquier and M. Oumgari “Deep curve-dependent PDEs for affine rough volatility” In arXiv:1906.02551, 2019

- [KB14] D. P. Kingma and J. Ba “Adam: A Method for Stochastic Optimization” Published as a conference paper at the 3rd International Conference for Learning Representations, San Diego, 2015, 2014

- [KJY20] Y. Khoo, J.Lu and L. Ying “Solving parametric PDE problems with artificial neural networks” In European Journal of Applied Mathematics, 2020, pp. 1–15

- [KLW20] I. Kharroubi, T. Lim and X. Warin “Discretization and Machine Learning Approximation of BSDEs with a Constraint on the Gains-Process” In arXiv preprint arXiv:2002.02675, 2020

- [KSS20] S. Kremsner, A. Steinicke and M. Szölgyenyi “A deep neural network algorithm for semilinear elliptic PDEs with applications in insurance mathematics” In arXiv:2010.15757, 2020

- [LXL19] J. Liang, Z. Xu and P. Li “Deep Learning-Based Least Square Forward-Backward Stochastic Differential Equation Solver for High-Dimensional Derivative Pricing” In arXiv:1907.10578, 2019

- [MZ19] J. Müller and M. Zeinhofer “Deep Ritz revisited” In arXiv:1912.03937, 2019

- [NR19] N. Nüskens and L. Richter “Solving high-dimensional Hamilton-Jacobi-Bellman PDEs using neural networks: perspective from the theory of controlled diffusions and measures on path space” In arXiv:2005.05409, 2019

- [Pha09] H. Pham “Continuous-time Stochastic Control and Optimization with Financial Applications” 61, SMAP Springer, 2009

- [PP90] E. Pardoux and S. Peng “Adapted solution of a backward stochastic differential equation” In Systems & Control Letters 14.1, 1990, pp. 55 –61

- [PW17] H. Pham and X. Wei “Dynamic programming for optimal control of stochastic McKean-Vlasov dynamics” In SIAM J. Control Optim. 55.2, 2017, pp. 1069–1101

- [PWG21] H. Pham, X. Warin and M. Germain “Neural networks-based backward scheme for fully nonlinear PDEs.” In SN Partial Differential Equations and Applications 2.16, 2021

- [Rai18] M. Raissi “Forward-Backward Stochastic Neural Networks: Deep Learning of High-dimensional Partial Differential Equations” In arXiv:1804.07010, 2018

- [RPK19] M. Raissi, P. Perdikaris and G.E. Karniadakis “Physics-informed neural networks: A deep learning framework for solving forward and inverse problems involving nonlinear partial differential equations” In J. Comput. Phys. 378, 2019, pp. 686 –707

- [Rut+20] L. Ruthotto, S. J. Osher, W. Li, L. Nurbekyan and S. W. Fung “A machine learning framework for solving high-dimensional mean field game and mean field control problems” In Proc. Natl. Acad. Sci. USA 117.17 National Academy of Sciences, 2020, pp. 9183–9193

- [Sak20] T. Sakuma “Application of deep quantum neural networks to finance” In arXiv:2011.07319v1, 2020

- [SDEK20] Y. Shin, J. Darbon and G. Em Karniadakis “On the convergence of physics informed neural networks for linear second-order elliptic and parabolic type PDEs” In arXiv:2004.01806, 2020

- [SS17] J. Sirignano and K. Spiliopoulos “DGM: A deep learning algorithm for solving partial differential equations” In J. Comput. Phys. 375, 2017

- [SVSS18] M. Sabate Vidales, D. Siska and L. Szpruch “Unbiased deep solvers for parametric PDEs” In arXiv:1810.05094v2, 2018

- [SVSS20] M. Sabate Vidales, D. Siska and L. Szpruch “Solving path dependent PDEs with LSTM networks and path signatures” In arXiv:2011.10630v1, 2020

- [Zha04] J. Zhang “A numerical scheme for BSDEs” In Ann. Appl. Probab. 14.1 The Institute of Mathematical Statistics, 2004, pp. 459–488