Data separation is a well-studied phenomenon that can cause problems

in the estimation and inference

from binary response models.

Complete or quasi-complete separation occurs when

there is a combination of regressors in the model whose value can

perfectly predict one or both outcomes. In such cases, and such

cases only, the maximum likelihood estimates and the corresponding

standard errors are infinite. It is less widely known

that the same can happen in further microeconometric models.

One of the few

works in the area is Santos Silva and Tenreyro (2010) who note

that the finiteness of the maximum likelihood estimates in Poisson regression depends on the data configuration

and propose a strategy to detect and overcome the

consequences of data separation. However, their approach can lead to

notable bias on the parameter estimates when the regressors are

correlated. We illustrate how bias-reducing adjustments to the

maximum likelihood score equations can overcome the consequences of

separation in Poisson and Tobit regression models.

keywords:

Bias reduction , Data separation , Shrinkage

JEL:

C13, C24, C25, C52

1 Sources of separation in regression models

Suppose that the non-negative random variable has a distribution with a point

mass at zero.111Note that the discussion here extends to the

case where the support of the response is bounded below or above. If

the lower boundary is a constant , we can use

. Similarly, if the upper boundary is

, we can use . Suppose that the

distribution function of is

(), where the scalar parameter is a

centrality measure (e.g., the mean), and the parameter

represents higher-order characteristics of the distribution (e.g.,

dispersion).

A regression model can be formulated as

(1)

(2)

where is a vector of regressors with

, which is observed along with , and

is a monotonically increasing function that links

to and a parameter vector . The model specification

in (1) and (2) covers a range of models, including

models for binary, multinomial, ordinal, and count models,

models for limited dependent

variables such as the Tobit model

and its extensions, and zero-inflated and two-part or hurdle models.

The existence of a point mass at zero implies that

, where

is the density or probability mass function

corresponding to .

The simplest but arguably often-encountered occurrence of data

separation in practice is when there is a regressor

such that for all

with . Assuming that

are independent conditionally on

, the log-likelihood for the

model defined by (1) and (2) can be decomposed as

(4)

where indicates the sub-vector formed from a vector after

omitting its -th component.

Term (4) is exactly the log-likelihood without the -th

regressor and based only on the observations with . Under

the extra assumption that is monotonically

decreasing with (which is true, for example, in Poisson

and Tobit regression models), will diverge to

during maximization, so that (4) achieves its

maximum value of . Then, the maximization of term (4)

with respect to yields the maximum likelihood (ML)

estimate of . So, the ML estimate of will

be the same as the ML estimate obtained by maximizing the

log-likelihood without the -th regressor over the subset of

observations with .

As Santos Silva and Tenreyro (2010) show for Poisson

regression,

the same situation can occur more generally, when

separation occurs for a certain linear combination of regressors. Our

discussion above extends their considerations

beyond log-link models and Poisson regression.

2 Estimating regression models with separated data

Albert and Anderson (1984) showed that infinite estimates in

multinomial logistic regression occur if and only if there is data

separation. Since then, the consequences of infinite estimates to

estimation and inference have been well-studied for binomial and

multinomial responses.

A popular remedy in the statistics literature is to replace the ML

estimator with shrinkage estimators that are guaranteed to take finite

values (see, for example Gelman et al., 2008, for using shrinkage priors in the

estimation of binary regression models). The

probably most-used estimator of this kind comes from the solution of

the bias-reducing adjusted score equations in Firth (1993)

(see, for example, Heinze and Schemper 2002 and

Zorn 2005 for accessible detailed accounts),

which guarantee

estimators with smaller asymptotic bias than what the ML estimator

typically has (Firth, 1993; Kosmidis and Firth, 2009).

In contrast, the majority of methods that have been put forward in the

econometrics literature are typically based on omitting the regressors

that are responsible for the infinite estimates. Such practice can be

problematic as we discuss in the following sections.

2.1 Omitting regressors affected by separation

Santos Silva and Tenreyro (2010) show that the regressors

responsible for separation in Poisson models can be easily identified

by running a least squares regression on the non-boundary observations

and checking for perfect collinearity among the regressors. The same

strategy is also applicable for Tobit regression models.

Having identified the collinear regressors associated with

separation, Santos Silva and Tenreyro (2010) propose to simply

omit those and re-estimate the model using the full data set with

all observations. The same strategy is also adopted in

Cameron and Trivedi (2013, Chapter 6.2), who suggest to drop

the separating regressor from the binary model part of a count data

hurdle model.

However, this strategy only leads to consistent estimates if the

omitted regressors are, in fact, not relevant, or were constructed to

specifically indicate a zero response (e.g., in the artificial

data set used in the illustrations

of Santos Silva and Tenreyro, 2011). In contrast, when a highly

informative regressor is omitted, separation will be replaced by a

systematic misspecification of the model

(Heinze and Schemper, 2002; Zorn, 2005). In that situation,

consistent estimates can be obtained by not only omitting the

regressor but also the observations responsible for separation, i.e.,

considering only the first term (4) in the likelihood and

dropping (4).

2.2 Bias reduction

Kosmidis and Firth (2020) have formally shown that, in

logit

regression models with full-rank model matrix, the bias-reduced (BR)

estimators coming from the adjusted score equations in

Firth (1993) (i) have always finite value and (ii) shrink

towards zero in the direction of maximizing the Fisher information

about the parameters. There are also strong empirical findings that

the finiteness of the BR estimator extends beyond

logit models.

A desirable feature of the bias-reducing adjustments to the score

functions is that they are asymptotically dominated by the score

functions. As a result, inference that relies on the BR estimates

(Wald tests, information criteria, etc.) can

be performed as usual by simply using the BR estimates in place of the

ML estimates. This makes BR estimation a rather attractive alternative

approach for dealing with separation, without omitting regressors.

While bias reduction is a well-established remedy for data separation

in

binary

regression models, it is less well known that it is

effective also in more general settings such as generalized nonlinear

models (Kosmidis and Firth, 2009), and, as illustrated here, the

models in Section 1.

3 Illustration

Similarly to Santos Silva and Tenreyro (2011), we consider models

with intercept and regressors and

. The values for are

generated from a uniform distribution as

. The values for

are, then, generated from Bernoulli distributions as

if and

otherwise, in order to allow for

correlation between the two regressors.

The responses for the Poisson model are generated

from (1) using and

the Poisson distribution for (with known dispersion ). The responses for the Tobit model are generated

from a latent normal distribution

with variance and subsequent censoring by setting

all negative responses to .

For illustration purposes, we generate a single artificial data set

involving regressor values with , and Poisson

and Tobit responses using , and

. In both cases, separation occurs due to the extreme

value for the coefficient of . In the Appendix, we carry out

a thorough simulation study with data sets for a range of

combinations of and and so that separation

occurs with smaller probability.

We estimate the models from the artificial data using ML and BR

estimation using all observations, and ML estimation of the

reduced model after omitting either by using just the subset

of the data set with (ML/sub), or all

observations as proposed by Santos Silva and Tenreyro (2010)

(ML/SST).

The bias-reducing adjusted score equations for the Poisson regression

are , where is

a -vector of zeros and

with

(Firth, 1992). It is solved with the brglm_fit method

from the R package brglm2 (Kosmidis, 2020). For the

Tobit model we derived the adjusted score equations along with an

implementation in the R package brtobit (Köll et al., 2021).

The derivations are tedious but not complicated and are provided in the Appendix.

Table 1: Comparison of different approaches when

dealing with separation in a Poisson model.

N is the number of observations used.

ML

BR

ML/sub

ML/SST

(Intercept)

x2

x3

Log-likelihood

N

Table 2: Comparison of different approaches when

dealing with separation in a Tobit model.

N is the number of observations used.

ML

BR

ML/sub

ML/SST

(Intercept)

x2

x3

(Variance)

Log-likelihood

N

Tables 1 and 2 show the results from

estimating the Poisson and Tobit models, respectively, with the four

different strategies. The following remarks can be made:

1.

Standard ML estimation using all observations leads to a large

estimate of with even larger standard error. As a result,

a standard Wald test results in no evidence against the hypothesis

that should not be in the model, despite the fact that using

when generating the data makes perhaps the

most influential regressor.222The estimates for and

the corresponding standard errors are formally

infinite. The displayed finite values are the result of stopping

the iterations early according to the convergence criteria used

during maximization of the likelihood. Stricter convergence

criteria will result in estimates and standard errors

that diverge further.

2.

The ML/sub strategy, i.e., estimating the model without

only for the 0 observations with , yields exactly the same estimates as ML because it optimizes the

term (4), after setting (4) to zero.

3.

Compared to ML and ML/sub, BR has the advantage of returning a

finite estimate and standard error for

. Hence a Wald test can be directly used to examine the

evidence against

. The other parameter estimates and the log-likelihood

are close to ML. Similarly to binary response models, bias reduction

here slightly shrinks the parameter estimates of

and towards zero.

4.

Finally, the estimates from ML/SST, where regressor is

omitted and all observations are used, appear to be far from the values

we used to generate the data. This is due to the fact that is

not only highly informative but also correlated

with .

Moreover, the simulation experiments in the Appendix provide evidence that the

BR estimates are always finite, and result in Wald-type intervals with

better coverage.

References

Albert and Anderson (1984)

Albert, A., Anderson, J.A.,

1984.

On the existence of maximum likelihood estimates in

logistic regression models.

Biometrika 71,

1–10.

doi:10.1093/biomet/71.1.1.

Amemiya (1973)

Amemiya, T., 1973.

Regression analysis when the dependent variable is

truncated normal.

Econometrica 41,

997–1016.

doi:10.2307/1914031.

Cameron and Trivedi (2013)

Cameron, A.C., Trivedi, P.K.,

2013.

Regression Analysis of Count Data.

2nd ed., Cambridge University

Press, New York.

Firth (1992)

Firth, D., 1992.

Bias reduction, the Jeffreys prior and GLIM, in:

Fahrmeir, L., Francis, B.,

Gilchrist, R., Tutz, G. (Eds.),

Advances in GLIM and Statistical Modelling:

Proceedings of the GLIM 92 Conference, Munich,

Springer, New York. pp.

91–100.

Firth (1993)

Firth, D., 1993.

Bias reduction of maximum likelihood estimates.

Biometrika 80,

27–38.

doi:10.1093/biomet/80.1.27.

Gelman et al. (2008)

Gelman, A., Jakulin, A.,

Pittau, M.G., Su, Y.S.,

2008.

A weakly informative default prior distribution for

logistic and other regression models.

The Annals of Applied Statistics

2, 1360–1383.

doi:10.1214/08-aoas191.

Gourieroux (2000)

Gourieroux, C., 2000.

Econometrics of Qualitative Dependent Variables.

Cambridge University Press,

Cambridge.

Heinze and Schemper (2002)

Heinze, G., Schemper, M.,

2002.

A solution to the problem of separation in logistic

regression.

Statistics in Medicine 21,

2409–2419.

doi:10.1002/sim.1047.

Köll et al. (2021)

Köll, S., Kosmidis, I.,

Kleiber, C., Zeileis, A.,

2021.

brtobit: Bias-Reduced Tobit Regression

Models.

URL: https://R-Forge.R-project.org/projects/topmodels/.

R package version 0.1-1/r1146.

Kosmidis and Firth (2009)

Kosmidis, I., Firth, D.,

2009.

Bias reduction in exponential family nonlinear

models.

Biometrika 96,

793–804.

doi:10.1093/biomet/asp055.

Kosmidis and Firth (2010)

Kosmidis, I., Firth, D.,

2010.

A generic algorithm for reducing bias in parametric

estimation.

Electronic Journal of Statistics

4, 1097–1112.

doi:10.1214/10-ejs579.

Kosmidis and Firth (2020)

Kosmidis, I., Firth, D.,

2020.

Jeffreys-prior penalty, finiteness and shrinkage in

binomial-response generalized linear models.

Biometrika doi:10.1093/biomet/asaa052.

R Core Team (2020)R Core Team, 2020.

R: A Language and Environment for

Statistical Computing.

R Foundation for Statistical

Computing. Vienna.

URL: https://www.R-project.org/.

Santos Silva and Tenreyro (2010)

Santos Silva, J.M.C., Tenreyro, S.,

2010.

On the existence of the maximum likelihood estimates

in Poisson regression.

Economics Letters 107,

310–312.

doi:10.1016/j.econlet.2010.02.020.

Santos Silva and Tenreyro (2011)

Santos Silva, J.M.C., Tenreyro, S.,

2011.

Poisson: Some convergence issues.

Stata Journal 11,

207–212.

doi:10.1177/1536867x1101100203.

Zorn (2005)

Zorn, C., 2005.

A solution to separation in binary response models.

Political Analysis 13,

157–170.

doi:10.1093/pan/mpi009.

Appendix A Bias-reducing adjusted score functions for Tobit regression

The Tobit model is one of the classic models of microeconometrics. Fundamental results were obtained by Amemiya (1973). A detailed account of basic properties is available in, e.g., Gourieroux (2000). Here we provide the building blocks for bias-reduced estimation of the Tobit model.

Denote by the log-likelihood function for a Tobit

regression model with full-rank, model matrix with

rows the -vectors , and a -vector of

parameters with regression

parameters and variance . Then,

, where if

and if , , and is the standard normal

distribution function at . The score vector is

where and is the density function of the standard normal distribution at .

The observed information matrix, , has the form

where, setting ,

As shown in Kosmidis and Firth (2010), a BR estimator for

results as the solution of the adjusted score equations

, where the vector has -th

component

. In the above expression,

and

, where

is the expected

information matrix. The R package

brtobit implements , , and

, and solves the bias-reducing adjusted score equations

for general Tobit regressions using the quasi Fisher-scoring scheme

proposed in Kosmidis and Firth (2010).

The matrices , and have the

same block structure as and, directly by their

definition, closed-form expressions for their blocks result by taking

expectations of the appropriate products of blocks of and

. By direct inspection of the expressions for

and , the required expectations result by noting that

, ,

, , and by computing

. For the

latter expression, note that

, and that some algebra gives

where .

The expected information,

has elements

Furthermore, for ,

and for ,

where

Appendix B Simulation

The aim of the simulation experiment is to compare the performance of

the BR and ML estimator in count and limited dependent variable models

with varying probabilities of infinite ML estimates. The comparison

here is in terms of bias, variance, and empirical coverage of nominally

Wald-type confidence intervals based on the asymptotic

normality of the estimators. Our results were obtained using

R 4.0.3 (R Core Team, 2020).

Random variables were generated using the default methods for the relevant distributions, which in turn rely on uniform random numbers obtained by the Mersenne

Twister, currently R’s default generator.

The same data generating process as in Section 3 of the main paper is

considered, with the coefficient of the binary regressor set to

the less extreme value . The amount of correlation

between and varies with

so that increasing the value of

leads to decreasing the probability of infinite estimates. The

sample sizes we consider are . For

each combination of and , independent samples are

simulated, and the parameters of the Poisson and Tobit regression

models in Section 3 are estimated using maximum likelihood and bias

reduction. The estimates are then used to compute simulation-based

estimates of the bias, variance, and coverage probability for

.

For the ML estimator, the bias, variance, and coverage probabilities

are computed conditionally on the finiteness of the ML estimates. We

classify an ML estimate as infinite if the corresponding estimated

standard error exceeds . In effect, we are assuming that if the

standard error exceeds , the Fisher scoring iteration for ML

stopped while moving along an asymptote on the log-likelihood surface,

hence, at a point where the inverse negative hessian has at least one

massive diagonal element. The heuristic value is conservative

even for . This has been verified through a pilot simulation

study to estimate the variance of the reduced-bias estimator, which

has the same asymptotic distribution as the ML estimator. No

convergence issues were encountered and the maximum estimated

standard error of the reduced-bias estimators accross simulation

settings, parameters, and sample sizes was for Tobit and

for Poisson regression.

For BR estimation, the estimates appear to be always finite. So, we

estimate biases, variances and coverage probabilities both

conditionally on the finiteness of the ML estimates and

unconditionally. We note here that a direct comparison of conditional

and unconditional summaries is not formally valid, but gets more and

more informative as the probability of infinite estimates decreases.

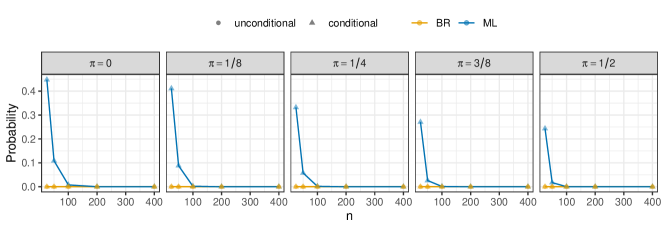

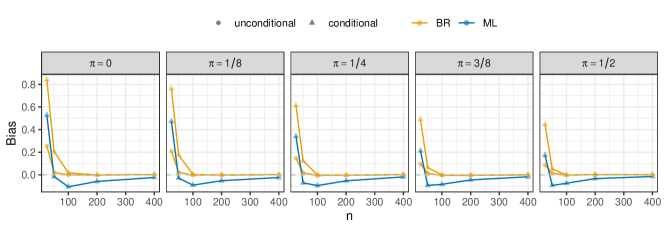

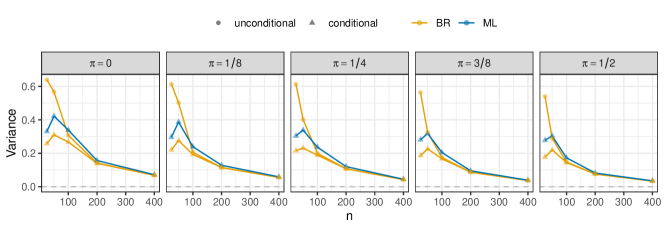

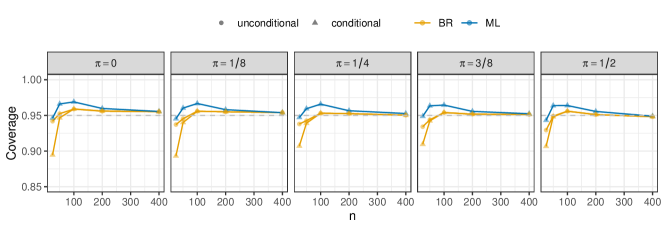

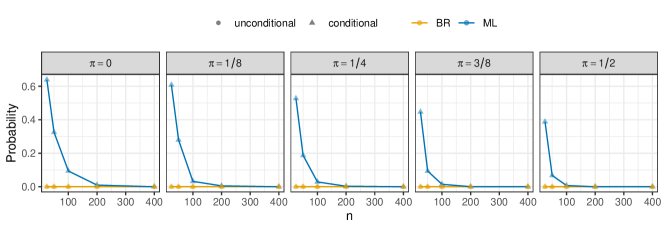

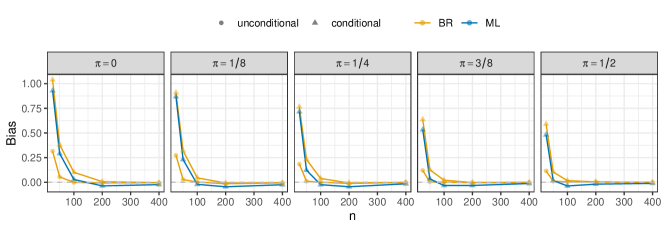

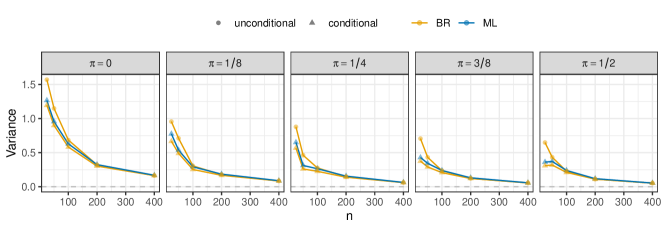

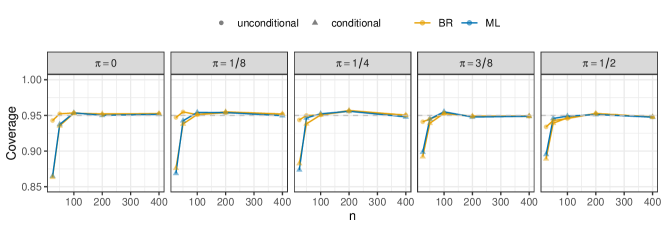

Figures 4, 4, 4, and

4 show the estimated probability that the ML and BR

estimate of are infinite, the estimated bias, the estimated

variance, and the estimated coverage probability of Wald-type

confidence intervals, respectively, for the Poisson

model. Figures 8, 8, 8,

and 8 show the corresponding results for the Tobit

model.

The results for Poisson and Tobit regression lead to similar insights:

1.

Bias reduction via adjusted score functions always yields finite

estimates.

2.

The BR estimator has bias close to zero even for small sample

sizes.

3.

Wald-type confidence intervals based on BR estimates have

good coverage properties.

4.

The variances of the BR and ML estimator get closer to each

other and closer to zero as increases. This is exactly what the

theory suggests because the score functions asymptotically

dominate the bias-reducing adjustments.

Figure 1: Probability of infinite estimates for (Poisson).

Figure 2: Bias of estimates for (Poisson).

Figure 3: Variance of estimates for (Poisson).

Figure 4: Coverage of Wald-type confidence intervals for (Poisson).

Figure 5: Probability of infinite estimates for (Tobit).

Figure 6: Bias of estimates for (Tobit).

Figure 7: Variance of estimates for (Tobit).

Figure 8: Coverage of Wald-type confidence intervals for (Tobit).