Variable Screening for Sparse Online Regression

Abstract

Sparsity-promoting regularizers are widely used to impose low-complexity structure (e.g. -norm for sparsity) to the regression coefficients of supervised learning. In the realm of deterministic optimization, the sequence generated by iterative algorithms (such as proximal gradient descent) exhibit “finite activity identification” property, that is, they can identify the low-complexity structure of the solution in a finite number of iterations. However, many online algorithms (such as proximal stochastic gradient descent) do not have this property owing to the vanishing step-size and non-vanishing variance. In this paper, by combining with a screening rule, we show how to eliminate useless features of the iterates generated by online algorithms, and thereby enforce finite sparsity identification. One advantage of our scheme is that when combined with any convergent online algorithm, sparsity properties imposed by the regularizer can be exploited to improve computational efficiency. Numerically, significant acceleration can be obtained.

Keywords: Non-smooth regularization, sparsity promoting regularization, stochastic gradient descent, screening rules, finite activity identification

1 Introduction

1.1 Background

Regression plays a fundamental role in various fields including machine learning, statistics and data science. Meanwhile, sparse regularizations, such as -norm regularization, have been increasingly popular in recent years. In this paper, we are interested in the following sparsity-promoting regression problem

| () |

The expectation is taken over random variable whose probability distribution is supported on some compact domain and is a trade-off parameter to balance the loss and the sparsity promoting regularizer .

Popular choices of the loss function include the squared loss, logistic loss and the squared hinge loss, while popular choices for include the -norm for enforcing sparsity Tibshirani (1996), the -norm for enforcing group sparsity Yuan and Lin (2006) and the -norms for enforcing sparsity within groups Simon et al. (2013). Throughout this paper, we assume the following basic assumptions:

-

(H.1)

For each , is convex, differentiable, and has -Lipschitz continuous gradient for some .

-

(H.2)

The regularization function is a convex and group decomposable norm (with non-overlapping groups). That is, given and a partition on such that , we have

where is a norm on with being the cardinality of .

Empirical loss minimization

In practice, instead of minimizing the loss function over the distribution , one can draw samples from and deals with the empirical loss

where samples are drawn from , with positive weights which sum to 1. A popular choice of is uniform weights, i.e. . Correspondingly, () becomes the following regularized empirical loss

| () |

1.1.1 Dimension reduction via (safe) screening

The purpose of using sparsity-promoting regularizers is so that the solution of the optimization problem () has as few non-zeros coefficients as possible. In high dimensional statistics, (safe) screening techniques are popular approaches for filtering out features whose corresponding coefficients are , hence achieving dimension reduction; See El Ghaoui et al. (2010); Tibshirani et al. (2012); Ndiaye et al. (2017) and the references therein. Safe feature elimination was first proposed by El Ghaoui et al. (2010) for -norm regularized problems. The rules introduced were static, where features are screened out as a preprocessing step, and sequential rules where one solves a sequence of optimization problems with a decreasing list of parameters , so that solutions of an optimization problem with are used to screen out features when solving with . Since this work, several extensions have been proposed Liu et al. (2014); Wang et al. (2014); Xiang et al. (2011).

Dynamic screening rules were later proposed by Bonnefoy et al. (2015), where the safe screening regions are updated along the iterates of a solver. Another work in this direction is the so-called gap-safe rules Ndiaye et al. (2015, 2017) where the calculation of the safe regions along the iterates are done via primal-dual duality gap. The presented work is largely inspired by Ndiaye et al. (2017), where we dynamically construct safe regions by computing an “online” primal-dual duality gap.

1.2 Our contributions

Though screening techniques are algorithm agnostic, they have been investigated mostly for the deterministic or batched algorithms (where one evaluates the full gradient or at each iteration). For large-scale problems, batched methods (e.g. proximal gradient descent) may be impractical and it is preferable to use online ones Bottou and Cun (2004): that at each iteration step , draw a sample randomly from the distribution and perform the update

| (1.1) |

where is a subgradient (see Eq. (A.1)). This is a special instance of stochastic gradient descent and dates back to Robbins and Monro (1951); Kiefer et al. (1952).

To deal with the non-smoothness imposed by the regularizer , various stochastic schemes are proposed in the literature, such as truncated gradient Langford et al. (2009) or stochastic versions of proximal gradient descent Duchi and Singer (2009) (Prox-SGD)

where is called the proximal mapping of , and has closed form expressions for the above sparsity promoting regularizers Combettes and Pesquet (2011). Note that Prox-SGD is equivalent to (1.1) by taking . However, for the standard Prox-SGD, due to the vanishing step-size and non-vanishing variance in the stochastic gradient estimates, the generated sequence tends to have full support for all even though the sought after solution is sparse Xiao (2010); Lee and Wright (2012); see also Poon et al. (2018) for an explicit example. As a result, one cannot easily exploit the sparsity-promoting structure of for computational gains.

In this paper, we address the non-sparseness problem (i.e. no support identification) of online algorithms by combining them with the idea of safe screening rules El Ghaoui et al. (2010); Ndiaye et al. (2017). More precisely, our contributions are as follows.

-

(i)

By adapting gap-safe screening rules of Ndiaye et al. (2017) to online algorithms, we propose an online-screening rule. The proposed rule only needs to evaluate function values at the sampled data, hence has low per iteration complexity. In particular, we show how to construct a “dual certificate” along the iterations which allows us to apply gap-safe rules to screen out certain features. Moreover, this certificate can be built alongside any convergent online algorithms.

-

(ii)

The consequence of screening rules for online optimization is support identification of , i.e. dimension reduction, which allows us to locate features of interests. More importantly, significant computational gains can be obtained as per iteration complexity scales from (the dimension of the variable ) to (the sparsity of the solution ).

Remark 1.1.

An interesting feature of many batched optimization methods such as proximal gradient descent Lewis and Wright (2016); Lewis (2002); Liang et al. (2017) and coordinate descent Klopfenstein et al. (2020), is that they exhibit “finite activity identification”, where after a finite number of iterations, all iterates will have the same sparsity structure as the solution. Although one cannot check a-priori whether activity identification has been achieved, one can heuristically exploit this property for computational gains by switching to higher order methods once the support is sufficiently small.

When the optimization problem has a finite sums structure (), one can consider variance-reduced stochastic methods, such as proximal-SAGA and proximal-SVRG. These methods also enjoy finite activity identification properties Poon et al. (2018) and just as for the deterministic methods, one can also heuristically exploit this property for computational gains. Moreover, screening rules (such as Algorithm 1) can be applied and this leads to substantial performance gains in practice.

One the other hand, while activity identification is not present in many online algorithms (with the exception of regularized dual averaging Xiao (2010)), we make use of screening in this work to enforce such a property. This idea is inspired by the recent work of Sun and Bach (2020), where the authors developed a gap-safe rule for conditional gradient descent. One highlight of their work is that through safe screening, identification is achieved whereas simply running conditional gradient descent will never do. In this work, we combine this idea with the gap-safe rules Ndiaye et al. (2017) to tackle the stochastic setting, where we dynamically construct safe regions by computing an “online” duality gap.

Paper organization

The rest of the paper is organized as follows. We recall the basics of screening rules for sparsity-promoting regression problems in Section 2. Theoretical analysis of our online-screening rule is presented in Section 3. Numerical experiments on LASSO and sparse logistic regression problems are provided in Section 4. Finally, in the appendix we collect some basics of convex analysis and the proofs of the main theorems.

2 Safe screening for sparse regularization

Before introducing our algorithm, we first provide some background on screening rules, with particular focus on the gap-safe rule from Ndiaye et al. (2017). Given a sparsity-promoting norm , its dual norm and sub-differential are respectively defined by

Note that if is group decomposable, then we have

2.1 Safe screening

Below we summarize a few key facts about the support of solutions to (), and refer to Hastie et al. (2015); Vaiter et al. (2015) for further details. Let be a global minimizer of the regularized empirical loss (), the first-order optimality condition entails

| (2.1) |

This is equivalent to saying that is a minimizer if and only if

| (2.2) |

The fundamental idea behind screening rule comes from the above optimality condition, that given any sub-group , we have

| (2.3) |

The converse is also true under the non-degeneracy condition , where denotes the relative interior Hastie et al. (2015); Vaiter et al. (2015).

Take the -norm for example, i.e. , this means that takes value only on the support of . Moreover, in (2.2) is precisely the solution of the dual problem of ()

| () |

where

is the dual constraint set. Since the vector certifies the support of , it is hence called the dual certificate. The above message implies that, if is known, we can identify an index set which includes the support of the solution, that is

Consequently, one can restrict to optimization over instead. This can lead to huge computation gains if tightly estimates the true support which very often is much smaller than the dimension of the problem.

In general, computing (hence ) is generally as difficult as finding . However, the entries where saturates (takes values ) can be estimated more readily. This is exactly the idea of safe screening, which constructs a “safe region” such that . Then instead of using (2.3) to determine the zero entries of , one can consider the relaxed criteria: first let , then if For the rest of the paper, we shall call as the safe region. The following result, which can be found in El Ghaoui et al. (2010), illustrates how to perform screening rules based on a safe region . Let be the center of and .

There are several ground rules for constructing a safe region :

-

•

The supremum of the dual norm over the safe region, i.e. , is easy to compute.

-

•

The size of the safe region should be as small as possible: as the most trivial safe region is the whole space which screens out nothing, while the best one is which screens out all useless features.

In the literature, various safe regions have been proposed. The very first safe screening work by El Ghaoui et al. (2010) introduced the idea of static screening and sequential screening. For static safe screening, screening is only implemented as a pre-processing of data, hence it is crucial to construct a good safe region such that the amount of discarded features is as many as possible. If we have a finite sequence of regularization parameter for such that . Then static screening can be applied to each which results in sequential screening. For both static and sequential screening, the volume of the safe regions is always bounded way from which limits the potential of screening. In addition to the safe region proposed in El Ghaoui et al. (2010), other safe regions include dual polytope projection safe sphere Wang et al. (2013) and safe dome Xiang et al. (2016). Dynamic screening rules were later proposed in Ndiaye et al. (2015, 2017), where they combine screening rules and numerical methods such that the constructed safe regions are generated by the sequence of the numerical scheme. As a result, the safe region can eventually converge to the dual certificate and screen out all useless features. Our approach will follow the idea of dynamic screening.

2.1.1 Gap-safe screening

In a series of work Ndiaye et al. (2015, 2016, 2017), the authors develop a gap-safe rule for screening, where the “gap” refers to the duality gap between the primal function () and dual function (). For any and , the duality gap is defined by

Let and be a primal and dual solution respectively, then strong duality holds and

As a result, the duality gap is always non-negative.

Since the loss function is differentiable with -Lipschitz continuous gradient, the dual problem is -strongly concave with . Then for any and , (Ndiaye et al., 2017, Theorem 6). Therefore, letting

| (2.4) |

one obtains the following safe sphere:

Now given a numerical scheme, at each iteration, is explicitly available and one can compute a dual feasible variable by projecting on to the dual feasible set . In particular, define

| (2.5) |

It follows by using Holder’s inequality and the fact that is positive homogeneous that the distance from to the true dual solution (see (2.2)) is bounded by

Hence, if .

2.2 Gap-safe screening for Prox-SGD

Screening rules are algorithm agnostic. That is to say, given an algorithm with iterates , one can always compute a safe region for screening. As a result, we can incorporate screening to proximal stochastic gradient descent when the problem to solve has a finite sum empirical loss of the form (). This is the most straightforward way of carrying out screening rule, and indeed, a similar screening strategy was recently proposed for ordered weighted -norm regularized regression in Bao et al. (2020).

For the finite sum problem, consider an algorithm of the following general form: for each , sample uniformly at random from the finite data

| (2.6) |

We have for SGD, with , while for Prox-SGD . Algorithm 1 combines (2.6) with safe screening rules.

Remark 2.1.

Algorithm 1 has two loops of iterations: the inner loop is the standard stochastic gradient update, while for the outer loop is screening with certain safe rules. Note that the outer loop makes use of which is evaluated over the entire dataset. Such a setting is reminiscent of the SVRG algorithm Johnson and Zhang (2013), where the full gradient of the loss function at an anchor point needs to be computed. Likewise, the choice of steps for inner loop, the value of in Algorithm 1 should be of the order of , to balance the overhead of computing .

Remark 2.2.

For Algorithm 1, all the aforementioned safe screening rules can be applied; see El Ghaoui et al. (2010); Liu et al. (2014); Ndiaye et al. (2015, 2017) and the references therein. However, for online learning, this is no longer true, since for online learning it is expensive or even impossible to obtain the projected point , let alone construct the safe region using (2.5). Hence, in what follows, we propose an approach to compute an online gap and construct a safe region without the need to project onto the constraint set.

3 Screening for online algorithms

For large-scale problems online optimization methods, it is unrealistic or impossible to compute the dual variable . Consequently, one cannot construct the safe region for screening. However, for the gap-safe screening rule, since its safe region is built on function duality gap, it is possible to generalize the rule to the online setting via stochastic approximations. The purpose of this section is to build such a generalization. The roadmap of this section is described below:

-

1.

We first describe how to construct online dual certificates and primal/dual objectives, which consist of the following aspects: a) the dual problem of the online problem (); b) online duality gap via stochastic approximations; c) online dual certificate; d) convergence guarantees. These are provided in Section 3.1.

- 2.

- 3.

3.1 Online dual certificates and objectives

Given an online method, at each step we sample from the distribution and evaluate

| (3.1) |

In what follows, we define an online dual point that is constructed as weighted average of the past evaluated points and define online primal and dual objectives that are again weighted averages of the past selected functions and , where denotes the convex conjugate of loss function .

3.1.1 Online dual problem and duality gap

The dual problem of the primal problem () takes the following form

| () |

where we maximize over -measurable functions . The derivation of () can be found in Appendix A.2. Note that it admits a unique maximizer, since is -strongly convex due to the fact that is -Lipschitz. The problems () and () are referred as primal and dual problems and their solutions are related: any minimizer of () is related to the optimal solution of () by and

| (3.2) |

Observe that the primal and dual objective functions are expectations. We now discuss their online ergodic estimations over the sampled data. At time step , given a primal variable , define the online primal objective

| (3.3) |

where , and

For each step , denotes the dual variable of that step. Let , the online dual objective for reads: let

| (3.4) |

Remark 3.1.

Note that the primal variable has a fixed dimension of , while the dimension of the dual variable grows with iteration .

We make the following standard assumption (Robbins and Monro, 1951) on :

| (3.5) |

Typical choices are for .

It is straightforward to check (Lemma A.4 (i)) that there exists a decreasing sequence such that

| (3.6) |

Using , in our previous notation of empirical () and (), we have and , and they are related by

Definition 3.1 (Online duality gap).

Let be as in (3.1) and , define the online duality gap as

| (3.7) |

Remark 3.2.

Since is not necessarily a dual feasible point, the online duality gap is not guaranteed to be non-negative. On the other hand, while can be computed in an online fashion, the feasible point , in , which is the projection of onto the constraint set cannot be computed online.

3.1.2 An online estimate of the dual certificate

With the online duality gap, we now construct a dual certificate from and . Since the primal variable converges to , it is natural to define a candidate point, for , as

| (3.8) |

In the notation introduced in (3.6), we can write

| (3.9) |

3.1.3 Convergence results

Before presenting our online-screening rule, we provide some theoretical convergence analysis of the above online estimates. To this end, we need the following assumptions

-

(i)

let be compact sets, and assume there exists such that:

-

(ii)

assume that converges to a minimizer with .

Define

Under assumption (3.5), one can show (see Lemma A.4) that as and if with , then .

We first establish uniform convergence of the online objective to its expectation , and uniform convergence of the corresponding dual certificate to .

Proposition 3.1.

The following result holds

-

(i)

Let be a compact set of , then almost surely .

-

(ii)

Let be the dual certificate associated to , we have uniform convergence to defined in (3.2):

where the implicit constant in the Big- depends on , the dimension of (it comes from the equivalence between norms in finite dimensions, and ).

We also have convergence of the online certificate of (3.9) to , and the online gap evaluated at converging points also converges to zero.

Proposition 3.2 (Convergence of the online estimate).

The proofs can be found in the Appendix A.3.

3.2 Online-screening

In this section, we derive a screening rule for solutions to the online objective based on the certificate of (3.9) and of (3.7). In the following, let be as in (3.9), be as in (3.1) and let where is the maximizer of (3.4).

Lemma 3.1 (Screen gap).

Let and , then there holds

Moreover, for all ,

where, and

Remark 3.3.

The above holds for any and . In our numerics, we choose where is an “anchor point” which is updated periodically (see Algorithm 2).

Remark 3.4.

By combining Lemma 3.1 with Proposition 2.1, we obtain the following proposed screening rule for online optimization algorithm.

Corollary 3.1 (Online screen rule).

Let . Then, given any , if

Remark 3.5.

The above screening is safe for the online problem in the sense that it will not falsely remove features which are in the solution of . However, the support of may not necessarily coincide with that of the global minimizer of (). Hence, our rule is not necessarily safe for the objective expectation (). Further discussions on the safety of our rule can be found in Sections 3.4 and 4.2.4.

A sequential screening strategy

We can directly apply Corollary 3.1 to screen out variables while running SGD. However, the effectiveness of this rule will depend on the proximity of to the optimal point . We therefore propose to progressively update this anchor point .

Let and denote . Let for be such that . Given , let be the optimal dual solution to

| (3.10) | ||||

| such that |

Note that (3.10) is dual to the primal problem

The corresponding dual certificate of (3.10) is

For each , applying Lemma 3.1 with , and , we get

| (3.11) |

where Summing (3.11) over and denoting for , we obtain

| (3.12) |

where

Lastly define

we have satisfying

| (3.13) |

where . Note that the residual term now depends on the sequence which converges to as . We can therefore expect the RHS of (3.13) to converge to 0 as . Having established how to progressively update the anchor point, we are finally able to present our online-screening rule for online optimization algorithms in the next section.

3.3 Screening procedure

Consider an online algorithm of the following form: for , draw sample , and compute

| (3.14) |

where is the algorithm operator, and again in the case of SGD, and for Prox-SGD. We state our screening framework for online optimization methods in Algorithm 2.

Next we provide some discussions on how to compute some key values of the algorithm, for instance the terms described in (3.12) and (3.13).

-

•

It is straightforward to compute and , as we have and

-

•

While for , it takes the following form

where . The second term is straightforward: define for all and repeat over : and

To compute : during the first iterations, let and

and note that . Then for iteration , we have: and

At iteration : define and

Note that we in fact have .

We conclude this section by few remarks.

Remark 3.6.

-

(i)

Computational pains and gains. Our screening rule adds several computational overheads to the original online optimization problem, and all of them are of complexity. Denote by the dimension of the problem at current iteration.

-

–

For the inner loop of Algorithm 2, line 10-12 computing the dual certificate and primal/dual function values are of complexity.

-

–

For the outer loop of Algorithm 2, all computations are at most .

Overall, the computational overheads added by screening is per iteration where is the dimension of at iteration step .

On the other hand, our screening rule can effectively remove useless features along iteration. Suppose the sparsity of is which is much smaller than and our screening rule manages to screen out all useless features, then eventually for all large enough, which in turn means the computational overheads are negligible.

-

–

-

(ii)

Effect of the exponent . For Algorithm 2, the weight parameter , specified by the exponent , determines how important the latest iterate is. As a result, is crucial to the screening behaviour of Algorithm 2. In general the value of lies in . As we shall see in the numerical experiments, the smaller the value of , the more aggressive the screening rule which makes Algorithm 2 unsafe. While for larger choice of , the screening is much more passive, hence safer.

- (iii)

3.4 Safety checks

Though our screening rule is adapted from gap-safe rule, which is guaranteed to be safe, i.e. only removes useless features and keeps all the active ones, applying Algorithm 2 alone is not guaranteed to be safe. This is due to the fact that the rule we derive is with respect to the online objective which is not the original objective (). As a result, potentially our screening rule can falsely remove useful features. However, this can be avoided by incorporating safe guard step, for instance, we can combine Algorithm 2 with the strong rules developed in Tibshirani et al. (2012) to avoid false removal.

In the online setting, it is impossible to check the optimality condition as in the strong rules paper of Tibshirani et al. (2012) to avoid false removal. However we can offer confidence intervals on the safety of the reconstructed solution:

-

(i)

Given a computed solution and support , we can check the optimality of by computing for , for and Note that if satisfies and , then is indeed an optimal solution.

-

(ii)

By Hoeffding’s inequality, where for all . So, with probability at least , provided that

In implementation, one can periodically compute to check the safety of the computed support with confidence estimates.

Remark 3.7.

It can also be noted that in both Algorithm 1 and Algorithm 2, the screening will be carried out until the termination of the iteration which actually is not necessary. Therefore in practice, one can terminate the screening once the support of the iterates is small enough. Take online screening for example, one terminate the screening if the size of the support of drops below . However, the safety check using should be continue until the termination of the algorithm to ensure safeness.

4 Numerical results

In this part, we present experiments to demonstrate the performance of our proposed online screen algorithm111Matlab code for reproducing our experiments are available at https://github.com/jliang993/sgd-screening. All the experiments are performed on a ThinkStation P620 with 32-core CPU, 256GB memory and Ubuntu 20.04 system.

4.1 Online experiments

We first consider an online problem of the following form,

where is drawn from the uniform distribution on with and for a sparse vector with non-zero entries and is Gaussian noise with mean 0 and variance . Both standard Prox-SGD and Prox-SGD with online screening (“OS-Prox-SGD”) are considered. For OS-Prox-SGD, the iteration contains two phases:

-

(a)

For the first phase, which accounts for of total number of iteration, screening is not applied and it is simply the plain Prox-SGD.

-

(b)

For the second phase, online screen is applied. In this part, since screening can reduce dimension of , we can consider two scenarios222Note that this experiment is synthetic, and we show both cases simply to illustrate what happens if dimension reduction can also be exploited for more efficient sampling: either draw new samples in the smaller dimension or in the original dimension . As a result, two different implementations are considered

-

(1)

We do not reduce the sample complexity, i.e. sample in the original space . Denoted as “OS-Prox-SGD-1”.

-

(2)

Sample in the smaller dimension obtained by screening, i.e. we draw from hence reducing sample complexity. Denoted as “OS-Prox-SGD-2”.

-

(1)

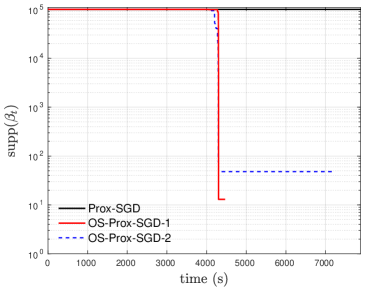

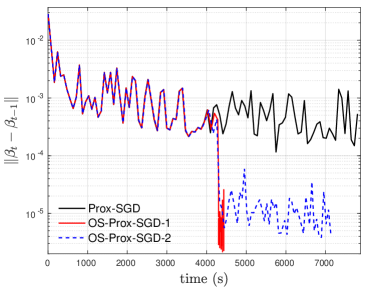

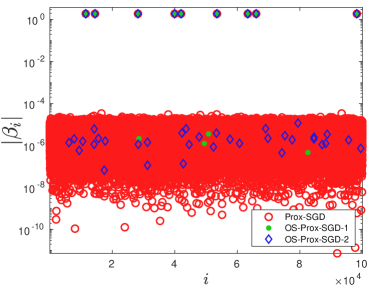

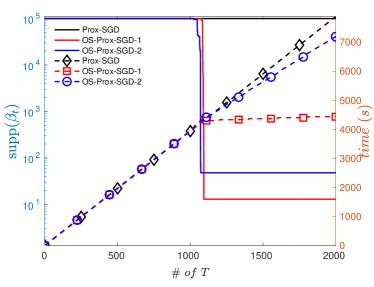

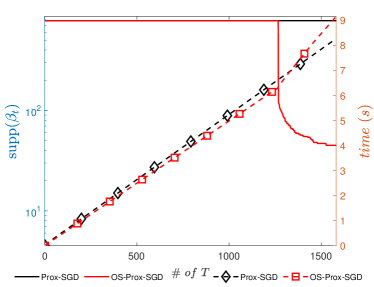

The maximum number of iteration in this test is set as , and obtained observations are provided in Figure 1:

-

•

Figure 1(a) shows the dimension of over time. As can be seen, our screening scheme manages to significantly reduce the dimension of the variable. Note that for the presented example, OS-Prox-SGD-1 provides better dimension reduction that OS-Prox-SGD-2. In our implementations, we also observed cases where OS-Prox-SGD-2 provides better dimension reduction. This very likely is caused by the sampling step since the samples corresponding to the non-zero elements of are different.

-

•

In Figure 1(b), relative error also becomes smaller after screening starts, this is mainly because almost all very small elements (around scale ) are screened out.

-

•

Figure 1(c) demonstrates the outputs of the two schemes, from which we observe that online screening effectively reduces the dimension of the problem.

-

•

Lastly in Figure 1(d), we provide a comparison between size of support of and wall clock CPU time. For the horizontal axis, we set . We have the following wall clock CPU time for the three schemes.

Method Prox-SGD OS-Prox-SGD-1 OS-Prox-SGD-2 overall CPU time (s) 8852 5044 7828 sampling time (s) 5973 3273 5886 residual (s) 2879 1771 1942 It can be seen that, in terms of computational time, online screening provides around 30% or even more acceleration. While in terms of sample time, nearly 50% the sampling time of Prox-SGD is saved.

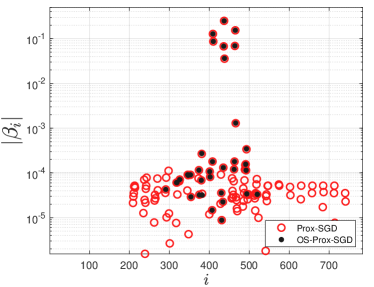

In terms of real-world data, we also consider the extended MNIST dataset, MNIST8m333https://www.csie.ntu.edu.tw/~cjlin/libsvm/, which contains more than 8 million images of digits. Digits and are used for the experiments, in total there are more than 1.5 million images of them. Iteration with only one pass through the data is made, hence, this can be treated as an online problem. In Figure 2 we provide our numerical observation, which is very close to the observations in Figure 1, except in this experiment, we do not observe improvements in running time. This is mainly caused by two factors: the small dimension of the problem and the images are sparse which makes the coefficients of Prox-SGD is sparse. Nonetheless, it demonstrates the ability of screening to precisely identify relevant features.

4.2 More experiments on LIBSVM data

In this part, we present experiments for the following -regularized finite sum problem

where with being either

-

(i)

the quadratic loss , a.k.a. the LASSO formulation,

-

(ii)

the logistic loss with , a.k.a. sparse logistic regression (SLR).

For both cases, we compare the performances of the standard proximal stochastic gradient descent (Prox-SGD), Algorithm 1 (FS-Prox-SGD), Algorithm 2 (OS-Prox-SGD). Both screening operations will be terminated if the size of the support drops below . For OS-Prox-SGD, the safety check is tested throughout the iterations. The details of settings of our experiments are as follows:

- •

-

•

Step-sizes of three algorithms are the same, which is .

-

•

The maximum number of iterations for all schemes is set as the . Both FS-Prox-SGD and OS-Prox-SGD will be terminated if either maximum number of iteration is reached or the wall-clock CPU time exceeds that of Prox-SGD.

-

•

Regularization parameter: we choose . In our experiments for the LASSO problem, we choose . While for SLR problem, various choices are chosen and provided below.

-

•

For both screening schemes, we set , i.e. screening is applied every steps.

-

•

Safety checks Every steps, we apply a safety check — for the current iterate , we compute the full certificate, find the coefficients where the optimality condition is violated and then add them back to the support of the . If the maximum number of iteration is , then in total we will have 6 times safety check.

The following LIBSVM datasets are used, with four relatively small-scale ones and four large-scale ones. 444All datasets can be downloaded from https://archive.ics.uci.edu/ml/datasets.php and https://www.csie.ntu.edu.tw/~cjlin/libsvm/.

| Name | ||

| colon-cancer | 62 | 2,000 |

| leukemia | 38 | 7,129 |

| breast-cancer | 44 | 7,129 |

| gisette | 6,000 | 5,000 |

| Name | ||

|---|---|---|

| arcene | 200 | 10,000 |

| dexter | 600 | 20,000 |

| dorothea | 1,150 | 100,000 |

| rcv1 | 20,242 | 47,236 |

4.2.1 Dimension reduction of screening schemes

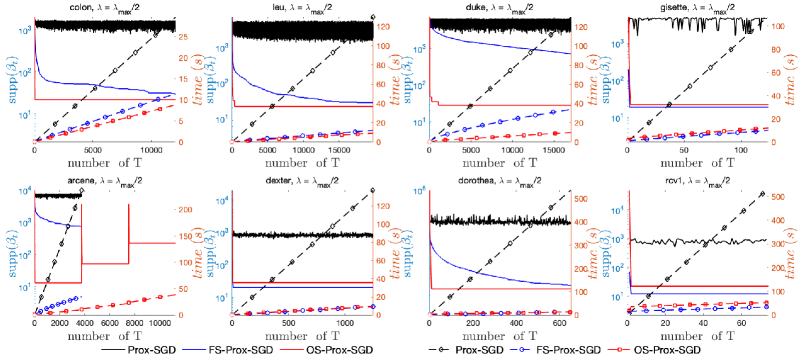

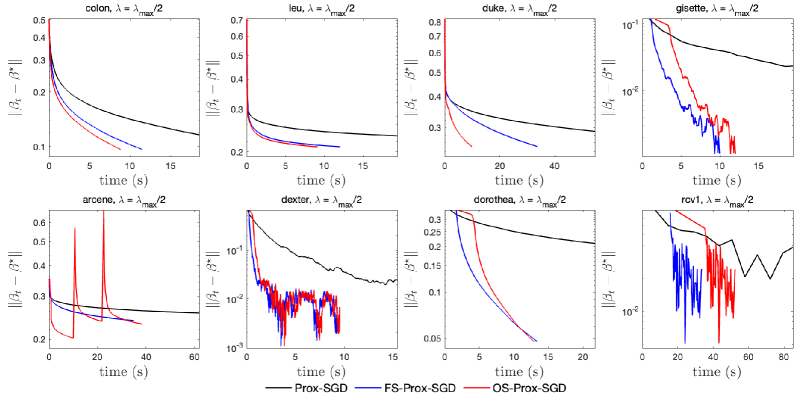

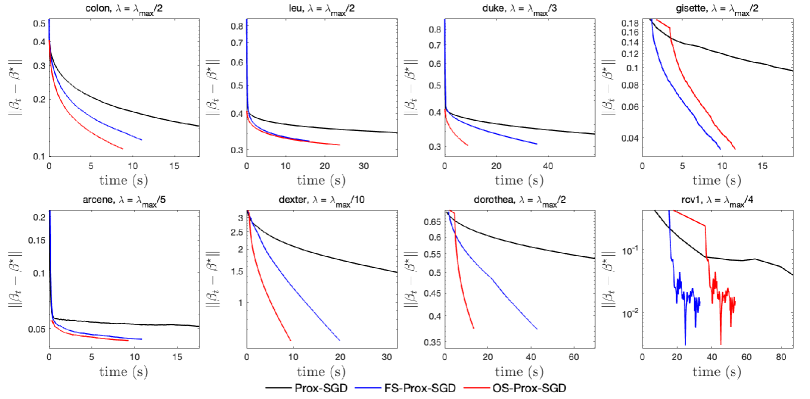

We first compare the support identification properties of Prox-SGD, FS-Prox-SGD and OS-Prox-SGD, which are shown in Figure 3 (LASSO) and Figure 4 (SLR), respectively. For each figure, two quantities are provide: size of support over number of epochs of for solid lines and elapsed time over number of epochs for dashed lines. For LASSO problem, we obtain the following observations,

-

•

Prox-SGD, black lines in all figures, indeed does not have support identification property, as the size of support is oscillating and does not decrease.

-

•

Both FS-Prox-SGD and OS-Prox-SGD can effectively reduce the dimension of the iterates and provide CPU time-gain. The dimension reduction of OS-Prox-SGD in general is sharper than that of FS-Prox-SGD, which means it can significantly reduce the dimension of the problem at the very early stages.

Remark 4.1.

It can be observed that for the arcene dataset, the support of online screening has two jumps which is caused by our safety check operation. Once our safety check identifies unsafeness of the current iteration, we reset the iteration to the last safe state with extra random perturbation which results in the jump of support size. When reset happens, we also increase the value of so as to make our online screening less aggressive. We shall discuss this in more details in Section 4.2.4.

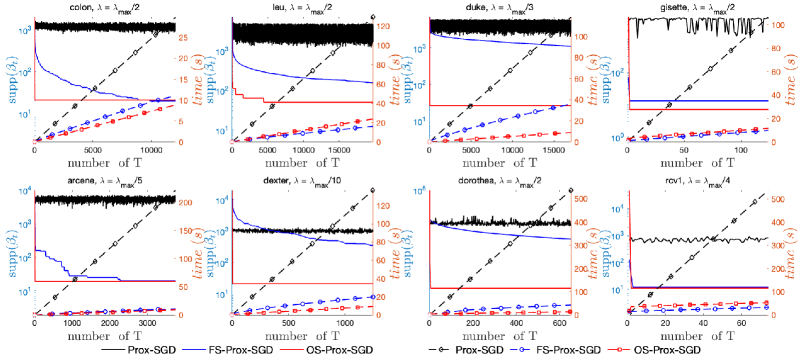

For SLR problems, the choice of is provided in each sub-figure of Figure 4. Overall, similar observations are obtained compared to those of LASSO problems. For the arcene data, no resets caused by the safety check. We observe from above that, for both problems, when online-screening works, it can achieve dimension reduction at the very early stage of the iteration, which means practically it is more attractive than the full-screening scheme, since in practice, stochastic algorithms are run for limited number of epochs.

4.2.2 LASSO problem

In this part, we present absolute error comparisons and solution quality comparisons for the LASSO problem. Error comparisons are displayed in Figure 5. Similarly to the wall-clock time comparisons in Figure 3, the faster algorithm yields faster error decays. For arcene data, the resets of safety check also result in jump of error.

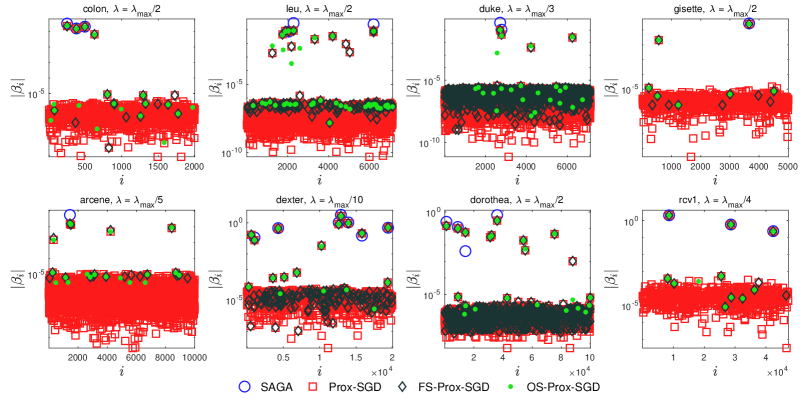

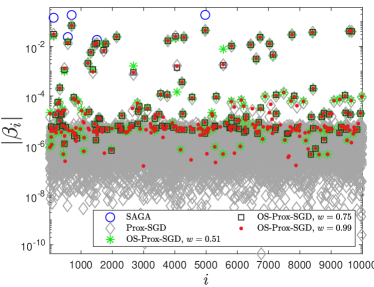

In Figure 6, we provide comparisons of the final outputs obtained by the algorithms. For reference, the output of SAGA with optimality guarantee is included.

-

•

It can be observed that for Prox-SGD, non-identification can be observed by the large number of tiny values around or below .

-

•

In general, there are discrepancies between the outputs of Prox-SGD schemes and the solution by SAGA, which means SGD schemes need more number of iterations.

-

•

Screening can be effective in screening out these tiny values, with online-screening overall being slightly better than full-screening.

4.2.3 Sparse logistic regression

For SLR problems, the comparisons of error-time and solution quality are provided in Figure 7 and Figure 8 respectively. Similar to the LASSO problem, the error comparison is in consistent with time comparisons of Figure 4.

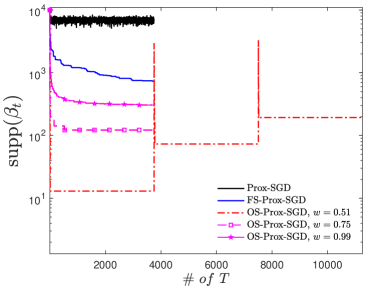

4.2.4 Aggressiveness of

In this last part of numeric experiments, we discuss the aggressiveness of the exponent parameter in Algorithm 2 and comment on the resets caused by safety check of online-screening for LASSO on arcene dataset. For the purpose of comparison, three initial choices of are tested, and . Note that should be smaller than . We describe the impact of over two quantities: dimension reduction and final output.

In our implementation, the value of will increase by every time reset happens, until its value reaches . The results for LASSO and arcene dataset are provided below in Figure 9, from which we observe the followings

-

•

Dimension reduction For all choices of the exponent , there is a sharp dimension reduction at the beginning stages of the iterations. The smaller the value of , the sharper the reduction.

-

•

Final output The larger the value of , the less sparse the output. Note that for initial value of , after two resets, its values is increased to .

Finally, it is worth mentioning that the wall clock time for all three choices of are very close and around 10 seconds.

5 Conclusion

Online optimization algorithms are widely used for solving large-scale problems arising from machine learning, data science and statistics. However, when combined with sparsity promoting regularizers, online methods can break the support identification property of these regularizers. In this paper, we combined the well established safe screening technique with online optimization methods which allows online methods to discard useless features along the iteration, hence achieving dimension reduction. Numerical result demonstrated that dramatic wall time gains can be achieved for classic regression tasks over real datasets.

Acknowledgements

We would like to thank the anonymous reviewers who greatly help to improve the quality of this work. Jingwei Liang acknowledges support from the Shanghai Municipal Science and Technology Major Project (2021SHZDZX0102) and the support from SJTU and Huawei ExploreX Funding (SD6040004/033).

The authors report there are no competing interests to declare.

Appendix A Appendix

A.1 Preliminary

A.1.1 Convex analysis

The sub-differential of a proper convex and lower semi-continuous function is a set-valued mapping defined by

| (A.1) |

Lemma A.1 (Descent lemma (Bertsekas, 1999)).

Suppose that is convex continuously differentiable and is -Lipschitz continuous. Then, given any ,

Lemma A.2 (Fenchel-Young inequality).

Let be proper, convex and lower semicontinuous, then for all , with equality if .

A.1.2 A stochastic Arzela-Ascoli result

We recall a stochastic Arzela-Ascoli result from Andrews (1992); see also (Rao, 2008, Theorem 11.3.2). Let be compact, for each and , let be a real measurable function on . Let be the closed ball of radius centred at .

Definition A.1.

We say that is strongly stochastically equi-continuous (SSE) on if for all there exists such that

and for all almost surely.

To check that is SSE, it is sufficient to show that

-

a)

where is a non-random function that is continuous in uniformly over and .

-

b)

For all , converge to 0 almost surely.

-

c)

for all almost surely, where is a random variable such that almost surely.

Theorem A.1 (Stochastic Arzela-Ascoli).

Let be compact. Suppose that is SSE and point-wise convergent to 0 (for all , almost surely). Then almost surely

A.2 Derivation of the dual problem ()

Denote and , applying the Fenchel-Young (in)equality twice we obtain

where the final line is an equality if , which is the case at an optimal primal solution . Therefore, it follows that

On the other hand, taking any -measurable function ,

where we apply the Fenchel-Young inequality for the first inequality and the definition of convex conjugate for the second.

Therefore, the dual problem is and strong duality holds. Finally, note that is the indicator function on the dual constraint set .

A.3 Proofs of Section 3.1

We prove Propositions 3.1 and 3.2 in this section. The proofs are provided for completeness although they use standard techniques, see for example Lee and Wright (2012). Similar results can be found in Mairal (2013) (though we relax the condition of to simply ). We make use of the following lemma.

Lemma A.3 (Super-martingale convergence (Robbins and Siegmund, 1971)).

Let be a set of random variables with for all . Let be non-negative random variables which are functions of random variables in , such that

-

(i)

.

-

(ii)

with probability 1.

Then, and converges to a non-negative random variable with probability 1.

Lemma A.4.

For some and random variables . Suppose and . Let with and . Then the following results hold

-

(i)

.

-

(ii)

.

-

(iii)

. In particular,

If with , then .

-

(iv)

Suppose that where are iid random variables with . Then, almost surely and

-

Proof.

The first two statements are straightforward. For the third one, we have as

Since by assumption, , we have as . Moreover, . As a result, we have

For , define . Then, is a Martingale and . By Azuma-Hoeffding inequality, given any ,

Hence converges to in probability.

To show that it converges almost surely, let . We will make use of Lemma A.3 to show that this converges to 0 almost surely. Note that

Taking expectation with respect to , it follows that

Since , it follows from Lemma A.3 that converges almost surely, and this converges almost surely to 0 since converges to 0 in probability. In particular, converges to almost surely. ∎

Now we are ready to prove Proposition 3.1.

- Proof of Proposition 3.1.

Claim (i)

First note that for each , with probability 1, as , by (iv) of Lemma A.4. Note that is strongly stochastically equi-continuous in : by the mean value theorem there exists , where is the ball of radius with , such that

For some point ,

where we have used that fact that is -Lipschitz. By boundedness of and , there exists such that

By Lemma A.4 (iv), we know that with probability 1,

Therefore, we arrive at where . It follows that

is stochastically equi-continuous in on compact sets. Hence, by Arzela-Ascoli (Theorem A.1), it follows that converges uniformly to on compact sets.

Claim (ii)

Denote . Note that given , . We show convergence in the dual norm (and convergence in infinity norm is then immediate from equivalence of norms in finite dimensions). By the triangle inequality and recalling that ,

| (A.2) |

To bound the first term on the RHS, let and , then

By strong convexity of (c.f. the proof of Lemma 3.1), we have

It follows that

| (A.3) | ||||

where and .

Almost sure convergence

Convergence in expectation

Taking expectations in (A.3) yields

where we applied Jensen’s inequality for the inequality and used optimality of to deduce . To bound the RHS, we note that (by the equivalence of norms) for some ,

We then apply Lemma A.4 to for each followed by the union bound to obtain

Therefore,

It follows where the implicit constant depends on . ∎

- Proof of Proposition 3.2.

Let be the -algebra generated by . Note

Therefore we get

where and we used and is Lipschitz with constant . Taking expectations,

By the Silverman-Toeplitz theorem (Natarajan, 2017, Thm 1.1), since and , as . Fix , and define for ,

This is a martingale with bounded difference

By Azuma-Hoeffding inequality we get . Therefore, by the union bound, . The RHS converges to 0 as by (iii) of Lemma A.4 and and the following bound

Almost sure convergence

Convergence of regularization term

Let us also establish the following convergence

Note that

which converges to 0 almost surely since almost surely we have and

Moreover, since and , we arrive at

Convergence of the duality gap

To show convergence of , recall that and by the Fenchel duality,

| (A.4) |

By adding and subtracting and using (A.4),

Note that, by the mean value theorem, for some between and ,

The same argument can be applied to show

As a result,

where . Convergence follows from (i).∎

A.4 Proofs for Section 3.2

-

Proof of Lemma 3.1.

Since is -Lipschitz smooth, it follows that is -strongly convex, and for any

(A.5) where is such that , the dual constraint set defined in (). Since is a dual optimal point, by Fermat’s rule

Therefore, multiplying (A.5) by and summing from , we obtain

(A.6) Note that by optimality of , for all . Therefore, the first sum in the RHS of (A.6) is bounded by . To bound the second sum, we make the choice : Recall that since is proper, closed and convex, if and only if (Rockafellar and Wets, 2009, Prop 11.3). Hence for , we have and . We can therefore choose . It then follows that

By optimality of , we have for any . Plugging these estimates back into (A.6) yields, for any ,

(A.7) since . Finally, by the Cauchy-Schwarz inequality,

and the result follows by combining this with (A.7). ∎

References

- Andrews (1992) Andrews, D. W. (1992). Generic uniform convergence. Econometric theory 8(2), 241–257.

- Bao et al. (2020) Bao, R., B. Gu, and H. Huang (2020). Fast oscar and owl regression via safe screening rules. In International Conference on Machine Learning, pp. 653–663. PMLR.

- Bertsekas (1999) Bertsekas, D. P. (1999). Nonlinear programming. Athena scientific Belmont.

- Bonnefoy et al. (2015) Bonnefoy, A., V. Emiya, L. Ralaivola, and R. Gribonval (2015). Dynamic screening: Accelerating first-order algorithms for the lasso and group-lasso. IEEE Transactions on Signal Processing 63(19), 5121–5132.

- Bottou and Cun (2004) Bottou, L. and Y. L. Cun (2004). Large scale online learning. In Advances in neural information processing systems, pp. 217–224.

- Combettes and Pesquet (2011) Combettes, P. L. and J.-C. Pesquet (2011). Proximal splitting methods in signal processing. In Fixed-point algorithms for inverse problems in science and engineering, pp. 185–212. Springer.

- Defazio et al. (2014) Defazio, A., F. Bach, and S. Lacoste-Julien (2014). Saga: A fast incremental gradient method with support for non-strongly convex composite objectives. In Advances in Neural Information Processing Systems, pp. 1646–1654.

- Duchi and Singer (2009) Duchi, J. and Y. Singer (2009). Efficient online and batch learning using forward backward splitting. Journal of Machine Learning Research 10(Dec), 2899–2934.

- El Ghaoui et al. (2010) El Ghaoui, L., V. Viallon, and T. Rabbani (2010). Safe feature elimination for the lasso and sparse supervised learning problems. arXiv preprint arXiv:1009.4219.

- Hastie et al. (2015) Hastie, T., R. Tibshirani, and M. Wainwright (2015). Statistical learning with sparsity: the lasso and generalizations. CRC press.

- Johnson and Zhang (2013) Johnson, R. and T. Zhang (2013). Accelerating stochastic gradient descent using predictive variance reduction. In Advances in neural information processing systems, pp. 315–323.

- Kiefer et al. (1952) Kiefer, J., J. Wolfowitz, et al. (1952). Stochastic estimation of the maximum of a regression function. The Annals of Mathematical Statistics 23(3), 462–466.

- Klopfenstein et al. (2020) Klopfenstein, Q., Q. Bertrand, A. Gramfort, J. Salmon, and S. Vaiter (2020). Model identification and local linear convergence of coordinate descent. arXiv preprint arXiv:2010.11825.

- Langford et al. (2009) Langford, J., L. Li, and T. Zhang (2009). Sparse online learning via truncated gradient. Journal of Machine Learning Research 10(Mar), 777–801.

- Lee and Wright (2012) Lee, S. and S. J. Wright (2012). Manifold identification in dual averaging for regularized stochastic online learning. Journal of Machine Learning Research 13(Jun), 1705–1744.

- Lewis (2002) Lewis, A. S. (2002). Active sets, nonsmoothness, and sensitivity. SIAM Journal on Optimization 13(3), 702–725.

- Lewis and Wright (2016) Lewis, A. S. and S. J. Wright (2016). A proximal method for composite minimization. Mathematical Programming 158(1-2), 501–546.

- Liang et al. (2017) Liang, J., J. Fadili, and G. Peyré (2017). Activity identification and local linear convergence of Forward–Backward-type methods. SIAM Journal on Optimization 27(1), 408–437.

- Liu et al. (2014) Liu, J., Z. Zhao, J. Wang, and J. Ye (2014). Safe screening with variational inequalities and its application to lasso. In International Conference on Machine Learning, pp. 289–297.

- Mairal (2013) Mairal, J. (2013). Stochastic majorization-minimization algorithms for large-scale optimization. In Advances in Neural Information Processing Systems, pp. 2283–2291.

- Natarajan (2017) Natarajan, P. N. (2017). Classical summability theory. Springer.

- Ndiaye et al. (2015) Ndiaye, E., O. Fercoq, A. Gramfort, and J. Salmon (2015). Gap safe screening rules for sparse multi-task and multi-class models. In Advances in neural information processing systems, pp. 811–819.

- Ndiaye et al. (2016) Ndiaye, E., O. Fercoq, A. Gramfort, and J. Salmon (2016). Gap safe screening rules for sparse-group lasso. In Advances in Neural Information Processing Systems, pp. 388–396.

- Ndiaye et al. (2017) Ndiaye, E., O. Fercoq, A. Gramfort, and J. Salmon (2017). Gap safe screening rules for sparsity enforcing penalties. The Journal of Machine Learning Research 18(1), 4671–4703.

- Poon et al. (2018) Poon, C., J. Liang, and C.-B. Schoenlieb (2018). Local convergence properties of saga/prox-svrg and acceleration. In Proceedings of the 35th International Conference on Machine Learning, pp. 4124–4132. PMLR.

- Rao (2008) Rao, S. S. (2008). A course in time series analysis. Technical Report, Texas A&M University.

- Robbins and Monro (1951) Robbins, H. and S. Monro (1951). A stochastic approximation method. The annals of mathematical statistics, 400–407.

- Robbins and Siegmund (1971) Robbins, H. and D. Siegmund (1971). A convergence theorem for non negative almost supermartingales and some applications. In Optimizing methods in statistics, pp. 233–257. Elsevier.

- Rockafellar and Wets (2009) Rockafellar, R. T. and R. J.-B. Wets (2009). Variational analysis, Volume 317. Springer Science & Business Media.

- Simon et al. (2013) Simon, N., J. Friedman, T. Hastie, and R. Tibshirani (2013). A sparse-group lasso. Journal of computational and graphical statistics 22(2), 231–245.

- Sun and Bach (2020) Sun, Y. and F. Bach (2020). Safe screening for the generalized conditional gradient method. arXiv preprint arXiv:2002.09718.

- Tibshirani (1996) Tibshirani, R. (1996). Regression shrinkage and selection via the lasso. Journal of the Royal Statistical Society: Series B (Methodological) 58(1), 267–288.

- Tibshirani et al. (2012) Tibshirani, R., J. Bien, J. Friedman, T. Hastie, N. Simon, J. Taylor, and R. J. Tibshirani (2012). Strong rules for discarding predictors in lasso-type problems. Journal of the Royal Statistical Society: Series B (Statistical Methodology) 74(2), 245–266.

- Vaiter et al. (2015) Vaiter, S., M. Golbabaee, J. Fadili, and G. Peyré (2015). Model selection with low complexity priors. Information and Inference: A Journal of the IMA 4(3), 230–287.

- Wang et al. (2014) Wang, J., J. Zhou, J. Liu, P. Wonka, and J. Ye (2014). A safe screening rule for sparse logistic regression. In Advances in neural information processing systems, pp. 1053–1061.

- Wang et al. (2013) Wang, J., J. Zhou, P. Wonka, and J. Ye (2013). Lasso screening rules via dual polytope projection. In Advances in neural information processing systems, pp. 1070–1078.

- Xiang et al. (2016) Xiang, Z. J., Y. Wang, and P. J. Ramadge (2016). Screening tests for lasso problems. IEEE transactions on pattern analysis and machine intelligence 39(5), 1008–1027.

- Xiang et al. (2011) Xiang, Z. J., H. Xu, and P. J. Ramadge (2011). Learning sparse representations of high dimensional data on large scale dictionaries. In Advances in neural information processing systems, pp. 900–908.

- Xiao (2010) Xiao, L. (2010). Dual averaging methods for regularized stochastic learning and online optimization. Journal of Machine Learning Research 11(Oct), 2543–2596.

- Yuan and Lin (2006) Yuan, M. and Y. Lin (2006). Model selection and estimation in regression with grouped variables. Journal of the Royal Statistical Society: Series B (Statistical Methodology) 68(1), 49–67.