Predictive Optimization

with Zero-Shot Domain Adaptation

Abstract

Prediction in a new domain without any training sample, called zero-shot domain adaptation (ZSDA), is an important task in domain adaptation. While prediction in a new domain has gained much attention in recent years, in this paper, we investigate another potential of ZSDA. Specifically, instead of predicting responses in a new domain, we find a description of a new domain given a prediction. The task is regarded as predictive optimization, but existing predictive optimization methods have not been extended to handling multiple domains. We propose a simple framework for predictive optimization with ZSDA and analyze the condition in which the optimization problem becomes convex optimization. We also discuss how to handle the interaction of characteristics of a domain in predictive optimization. Through numerical experiments, we demonstrate the potential usefulness of our proposed framework.

Keywords— Predictive optimization, Zero-shot domain adaptation, Convex optimization

1 Introduction

Prediction in a new domain without any training samples, called zero-shot domain adaptation (ZSDA) Yang and Hospedales (2015a, b), is an important task in domain adaptation. To this end, an approach to utilize domain descriptions Yang and Hospedales (2015a, b), called domain attributes, has been developed. A goal of ZSDA is to obtain predictions in an unseen domain in which we did not observe any training samples. An application of ZSDA is the sales prediction of new products; regarding domains as products and given product attributes and sales data, we can use ZSDA to the sales prediction of a customer for a new product. Thanks to ZSDA, we can predict the response of input in an unseen domain; however, one potential aspect of ZSDA has been overlooked.

We demonstrate another potential of ZSDA; by reversing the ZSDA prediction process, we can optimize domain attributes so that an evaluation metric of responses over customers is maximized, referred to as attribute optimization as shown in Figure 1. That is, instead of predicting responses given new domain attributes as in ZSDA, our task is to find new domain attributes given a prediction. In our example of new product prediction, we optimize an average of new product sales with respect to product attributes over a pre-specified customer group. The obtained product attributes would be useful for designing a new product.

Our attribute optimization task can be regarded as predictive optimization Ito and Fujimaki (2017); Donti et al. (2017); Ito et al. (2018), in which the goal is to optimize predicted outputs in terms of input variables. There are various applications of predictive optimization: water distribution management Žliobaite and Pechenizkiy (2010), retail price optimization Ito and Fujimaki (2016, 2017), and grid scheduling Donti et al. (2017). However, existing studies of predictive optimization mainly focus on a single domain, and the case of multiple domains has yet to be considered. While we can use existing methods for each domain independently, it would not exploit the structures and similarities across multiple domains. Moreover, it is not straightforward to optimize domain attributes for finding, e.g., a promising product in existing methods.

In this paper, we propose a novel simple framework for attribute optimization. Given domain attributes, inputs, and responses, our framework first trains a prediction function and then optimizes a measure computed by predicted outputs to find a new domain attribute. Our method can handle continuous and discrete domain attributes and concave measure functions as objective functions. Moreover, it can deal with cases when two or more domain-attribute variables are dependent, i.e., the interaction of domain attributes. By regarding domains as objects, domain attributes as designs, and objective functions as sales, quality, or durability, we use attribute optimization to discover the design of new best-selling, high-quality, and durable objects. Our attribute optimization framework can be applied to the following concrete tasks:

-

•

New product design: Consider that we are given sales, consumer features, and product characteristics data to design a new product by combining best-selling products’ ingredients. Our framework easily satisfies this demand by regarding domains as products, domain attributes as product characteristics, features as consumer features, and the objective function as sales.

-

•

New tourist spot design: Suppose that we are given reputations of tourist spots, tourist features, and characteristics of tourist spots data to design a new tourist spot on the basis of characteristics of tourist spots. Our framework easily fits this task by regarding a domain as a tourist spot, domain attributes as characteristics of a tourist spot, features as tourist features, and the objective function is the average reputation.

Our technical contributions for achieving the above-mentioned attribute optimization framework are as follows:

- •

-

•

We devise conditions on objective functions and constraints whose corresponding optimization problem can be cast to convex optimization, which is quickly solvable by off-the-shelf solvers (Section 4.3).

-

•

We provide practical examples of objective functions and constraints that meet the devised conditions (Section 5).

-

•

We describe how to handle interactions between domain-attribute variables. We show that the second-order interaction of - domain attributes can be relaxed to semidefinite programming (Section 6).

-

•

We establish theoretical analyses of the proposed framework, which bounds the generalization error of the prediction method and approximation factors of the optimization method (Section 7).

-

•

We demonstrate the potential usefulness of our proposed method on synthetic and benchmark datasets (Section 8).

2 Related work

2.1 Predictive optimization

Predictive optimization has been applied to several real-world applications such as water distribution management (Žliobaite and Pechenizkiy, 2010), retail price optimization Ito and Fujimaki (2016, 2017), grid scheduling Donti et al. (2017), and inventory optimization (Ohsaka et al., 2020). In existing work, a set of input-output samples is collected from a target domain; we train a prediction function and then optimize features of input to maximize a certain measure of output in the target domain. For example, in price optimization, we have sales for each item at a certain price. We first train a model to output the sales of an item from a price. We then optimize the prices of items such that the total sales is maximized. In existing work, the way of using item information, i.e., domain attributes, is not considered. In addition, prediction and optimization including features of input and domain attributes are not trivial.

In contrast, our approach optimizes domain attributes to maximize a certain measure of output for a set of fixed input samples. In other words, we can find a prospective target domain for specific input samples through the optimized domain attributes. Moreover, existing studies often consider a single domain while our study considers multiple domains. To the best of our knowledge, this is the first study of predictive optimization for multiple domains with its attribute information.

2.2 Data-driven design

An application of our method is data-driven design for new products. For this purpose, several methods based on machine learning have been proposed recently (Koutra et al., 2017; Kang et al., 2017; Vo and Soh, 2018). Among them, Koutra et al. (2017) is related to our problem setting, which considers multiple domains. They also considered optimization of a domain for fixed target users and applied their method to movie design for target users by regarding a domain as a movie. The method learns user-preferences through a tripartite graph of users, movies, and movie attributes. The movie attributes are optimized by a greedy approach, which is optimal under specific assumptions (Koutra et al., 2017).

Compared with the work of (Koutra et al., 2017), our method is not limited to data having graph structures and enables us to use various prediction models and optimization algorithms, as shown in Section 4. In addition, we demonstrate the effectiveness of our method on various real-world datasets in Section 8.

3 Background

3.1 Problem settings

Let be a feature vector and be a response in a domain , where is a positive integer and denotes the number of domains. We have a set of observations for each , where is the number of samples in . For each domain, we assume that a description of a domain is available and they can be expressed as domain-attribute variables. We denote a domain-attribute vector for by and a set of domain-attribute vectors by . We define a dataset as .

Let be a prediction function and be a set of target feature vectors. Let be an objective function that returns a gain of a domain described by . That is, we measure the value in a domain through . An example of is a mean response: , where denotes the size of a set.

The goal of the attribute optimization problem is to find a new domain-attribute vector optimized for a gain function.

3.2 Feature-unaware approach (FUA)

An approach to optimize domain attributes is that we first learn a function from to, e.g., the mean of , and then find which maximizes the learned function. We call the above approach the feature-unaware approach (FUA). Specifically, let be the average of responses of domain . As a function, we use a linear model defined as , where is the parameter vector. We then train with by, say, regularized least squares, i.e., ridge regression. Let be the estimated parameter obtained after training. To optimize domain attributes, an approach is to select a domain-attribute variable whose corresponding weight of to satisfy the user-defined and system-derived constraints. Another approach is to formulate an optimization problem and solve it.

The FUA is simple, but it ignores dependence on features . We thus cannot optimize domain-attributes for each or a group of , and cannot use the measure taking a distribution of features into account, which will be introduced in Section 5.1. Moreover, since the number of training samples is , the use of complex models, such as neural networks, for leads to ill-posed problems, resulting in that an inaccurate estimation of response. In contrast, our proposed approach takes features of input into account. Moreover, we can use complex models for estimating response since the number of training samples is much larger than the FUA.

4 Proposed method

Our method consists of two steps: i) a prediction step that estimates a prediction function from , and ii) an optimization step that solves an optimization problem under a user-preferred gain function.

4.1 Prediction step

In the prediction step, we train a parameterized prediction function, , with a training dataset . A simple example of is , where are the parameters to be learned. For a fixed domain-attribute vector , we can regard as a prediction function for a specific domain , e.g., .

Let be a loss function. By solving the following optimization problem, we obtain a learned prediction function as

where is the regularization functional and is the regularization parameter.

With the learned prediction function, we can estimate a response of even in a domain never seen before. Let be a domain-attribute vector for an unseen domain. We can obtain a prediction in a domain that did not appear in a training dataset as .

Our idea is to reverse the aforementioned prediction process for finding a new domain-attribute vector that is likely to get a high gain as shown in Figure 1. That is, instead of obtaining a prediction given , we find such that a prediction-based gain function is maximized.

4.2 Optimization step

After we obtained a learned prediction function , we move on to the optimization step. As is a set of target feature vectors, we can regard it as a set of target users. On the basis of , we compute an estimate of an objective function .

For a user-preferred gain function, we can find a promising domain-attribute vector by solving the following optimization problem:

| (1) |

where and are an inequality and equality constraint function, respectively. An example of a constraint is a budget constraint; if is the - vector and is defined as a cost vector, a budget constraint can be expressed as , where is the user-specified constant.

By solving the optimization problem in Eq. (1), we obtain a domain-attribute vector that is potentially new and will achieve a high gain. In the subsequent section, we explain the conditions in which the optimization problem can be solved efficiently.

4.3 Linear-in-attribute model (LAM)

In this section, we reveal conditions in which an optimization problem is regarded as a convex optimization problem.

We first define a model of a prediction function:

Definition 4.1 (Linear-in-attribute model).

A linear-in-attribute model (LAM) is defined as

| (2) |

where is a basis function vector whose parameters are to be learned with training data and ⊤ denotes the transpose of a vector or matrix.

We denote the learned basis function vector by ; an estimated response function is expressed as .

Let be a prediction function. We then define a functional computing gain given .

Definition 4.2 (Aggregate functional).

An aggregate functional computes gain from and . That is, the computed gain is given by . For the sake of brevity, we omit the notation and use .

Let us denote by . A gain function is expressed as . We then have the following proposition that characterizes a gain function:

Proposition 4.1.

If is a concave function and is a LAM, the gain function is concave.

Proof.

Without loss of generality, we assume . The second derivative of with respect to is given by , where and . The second term becomes zero because is linear in attributes, i.e., . Since is concave, . The first term is thus non-positive. Then, , concluding that is concave. ∎

Proposition 4.1 leads to the following corollary:

Corollary 4.1.1.

If a LAM, , and convex constraints, and , are used and is concave, the optimization problem in Eq. (1) is a convex optimization problem.

For convex optimization problems, we can use efficient off-the-shelf solvers to obtain a solution. In Section 5.1 and 5.2, we introduce useful candidates of , , and . Note that for higher accuracy, one can use non-convex models, rather than LAM, and use Bayesian optimization Mockus et al. (1978), but we do not pursue that direction because non-convex optimization is often time-consuming than convex optimization.

5 Examples of objective functions and constraints

5.1 Aggregate functionals

We introduce concave aggregate functionals. Recall that is a prediction function.

Mean response:

A standard choice of is a mean response defined as

With , the mean response with respect to is expressed as . For simplicity, we refer to the mean response aggregate functional as the mean gain function. A mean response can be interpreted easily; in our example of product sales prediction, maximization of a mean response over all users with respect to corresponds to finding a product that is likely to be preferred by all users on average.

On the implementation side, a mean response is linear, resulting in being concave by Proposition 4.1. It thus enables us to obtain a solution efficiently under convex constraints.

Conditional value at risk (CVaR):

A mean response is simple and a standard choice but it does not take into account a distribution of responses. In practical applications, we are sometimes interested in a tail of a distribution, in particular, a group of customers whose responses are relatively lower than others. If we maximize an objective that can capture a left tail of a response distribution, it corresponds to avoiding the situation in which users will put a lower rating on an object.

To treat a left tail of a response distribution, we can use conditional value at risk (CVaR) Rockafellar and Uryasev (2000, 2002) at a significance level , defined as

For brevity, we refer to the CVaR-based aggregate functional as the CVaR-based gain function.

A useful property of CVaR is concavity; the CVaR-based gain function with the LAM becomes concave from Proposition 4.1.

5.2 Constraints

In this section, we introduce constraints that can be used in practical applications.

Continuous domain attributes:

If a domain-attribute variable is a continuous value and a mean response is used as an objective function, we can maximize the objective function as much as we can by increasing the magnitude of the domain-attribute variable; it is, however, meaningless. To avoid such a useless solution, we normalize a domain-attribute vector and add a constraint such that an obtained solution is also normalized.

More specifically, we first preprocess all the continuous domain-attribute vector in training data such that ,111 If the domain-attribute vector consists of continuous and (after-mentioned) categorical variables, we split the vector into a continuous and a categorical domain-attribute part and apply normalization to the continuous part. and then add as constraints to an optimization problem. As long as the objective function and other constraints are convex, the optimization problem with the constraint is still a convex optimization problem. To be precise, the optimization problem is second-order cone programming Boyd and Vandenberghe (2004).

Categorical domain attribute:

In a number of applications, we may want to use a categorical type of variable as a domain attribute. We can encode such a categorical variable to a - vector, called the encoded domain attribute, as a binary domain attribute. However, optimization over binary variables results in a - integer programming, which is NP-hard. We thus use a relaxation technique to avoid solving NP-hard optimization problems.

If categories are encoded as an -dimensional domain-attribute vector, choosing from categories can be expressed as convex constraints: and . After solving the optimization problem, we round the obtained solution to binary variables. By the relaxation, we can handle categorical domain attributes under a convex optimization framework.

Budget limitation:

In practice, we may need to pay attention to the cost of a domain-attribute variable. Suppose that a domain-attribute vector is element-wise non-negative, i.e., . Let be a total budget and be a cost vector whose each element is a cost of using a corresponding domain-attribute variable. To reflect budget limitation, we add the convex constraint as a budget limitation to an optimization problem.

6 Interaction of domain attributes

Interaction of domain attributes, i.e., the dependency of variables, is important, in practice. In this section, we explain the means to handle interactions of domain attributes.

LAM with domain-attribute interaction:

One approach is to make an interaction term, e.g., for , and use the extended domain-attribute vector by concatenating these interaction terms with the original domain-attribute vector. Then, we can use the LAM, meaning that Proposition 4.1 holds. For example, if we are interested in the second-order interaction only, the extended domain-attribute vector is simply expressed as , where and denotes the Kronecker product222 For vectors and , .. The prediction model taking the second-order interaction into account is still linear in the extended domain-attribute vector ; by redefining , , where . Although the LAM can be extended to handle domain-attribute interactions, we use the LAM without domain-attribute interactions in our experiments. This is because we next develop a model for handling the interaction of domain attributes efficiently.

Semidefinite programming approach:

In Section 5.2, we explained the relaxation approach for a binary domain attribute, i.e., the constraint is relaxed to . While the relaxation approach is useful, if our interest is the second-order interaction of binary domain attributes, we can use the theoretically-supported algorithm Ito and Fujimaki (2017) inspired by the Goemans and Willamson’s MAX-CUT approximation algorithm Goemans and Williamson (1995).

Since the original purpose of the algorithm developed by Ito and Fujimaki (2017) is for price optimization, we modify it for the domain attribute optimization problem. To this end, let us first define the model taking into account the second-order binary domain-attribute interaction as

Definition 6.1 (Quadratic-in-binary-attribute model).

A quadratic-in-binary-attribute model (QBM) is defined as

where is a basis function to be learned and is a positive integer that controls flexibility of the QBM, similarly to factorization machines Rendle (2010). Note that in the binary domain attribute case, a linear term, i.e., , is included in the quadratic term because of for any .

We can check that the QBM can be expressed as , where , . The QBM with linear constraints is binary quadratic programming (BQP), which is difficult to optimize in general. However, for certain special cases, we can solve BQP efficiently.

We next introduce a constraint to domain-attribute vectors:

Definition 6.2 (Choice constraint).

For a set of indices , a choice constraint is .

Hereafter, if we use the choice constraints, we assume that the index sets for the choice constraints satisfies the following condition: The index sets satisfies , where denotes the size of a set.

For the mean response and the QBM with the choice constraints, the BQP optimization problem can be relaxed to the following semidefinite programming (SDP):

| (3) |

where is the set of real symmetric semidefinite matrices of size Boyd and Vandenberghe (2004),

, and is the -dimensional all-ones vector. We round the obtained solution to the binary domain-attribute vector on the basis of the randomized search algorithm proposed in Ito and Fujimaki (2017).

An advantage of the SDP formulation is that if we further add convex constraints to the optimization problem in Eq. (3), the optimization problem is still SDP. Thus, thanks to the SDP formulation, we can obtain the solution efficiently rather than solving the BQP.

7 Theoretical analyses

In this section, we present two theoretical properties of our proposed algorithm. Specifically, in Section 7.1, we show generalization error bounds of the prediction method used in Section 4.1. In Section 7.2, we present approximation factors of the optimization method used in Section 4.2. All the proofs are given in Appendix A.

7.1 Generalization error bound

In this analysis, we consider the case where the feature mapping function can be expressed as , where is the parameter matrix, is the vector of basis functions, i.e., , and is fixed in advance. Then, LAM can be expressed as the bilinear function model .

The key idea is to reformulate the prediction model into

where , , and . Accordingly, we express a set of training samples drawn from a distribution as , where . We assume that there exists the target labeling function , . We next respectively define the expected and empirical risks as and , where is the expectation over .

We also assume the loss function for a real number . Besides, we assume that there exists a such that for all and , and there exists such that . Similarly, we assume that and , leading to . We denote a function class of by .

Fix , then, we have the following proposition:

Proposition 7.1.

Fix , then, for any , the following inequality holds with probability at least for any :

where .

This result shows that for the same domain, i.e., the domain characterized by the training attributes, the generalization error bound converges with the order , which is the optimal without any additional assumption (Mendelson, 2008).

Next, we consider generalization error bounds on the domain characterized by the optimized attribute vectors. Compared with the above analysis, it requires to measure the difference between the source (training attribute vectors) and target (optimized attribute vectors) domains. Let and be distributions of the target and source domains, respectively. We regard that and are independently drawn from distributions and , respectively, where is an test/optimized domain-attribute vector. We then analyze the generalization error bounds of ZSDA on the basis of a tool for domain adaptation. More specifically, we have training samples from the source domain with distribution and evaluate the performance on the target domain with distribution .

We first define and , and denote the corresponding empirical approximators by and , respectively. By definition, we have and . Similarly, and , where is the number of samples in the domain and is the target labeling function in . To measure the difference between two distributions and , we use the discrepancy distance (Mansour et al., 2009) defined as

Let and be the minimizers of and , respectively. We assume that for all and . Under the above assumptions, we have the following proposition:

Proposition 7.2.

For any , the following inequality holds with probability at least for any :

This result shows that the target expected error in the left-hand side is upper-bounded by the source empirical error plus additional constants and confidence terms.

7.2 Approximation factor

We here analyze the attribute optimization step in our framework from a complexity-theoretic point of view. In a nutshell, we show that the non-negative linear counterpart of attribute optimization is a generalization of packing integer programs Raghavan (1988), and it is NP-hard in general but approximable if the vectors representing constraints are “sparse.” For the sake of simplicity of analysis, we make the following assumptions:

-

•

The objective function is given by , where is a mean response and follows a LAM model; i.e., for a non-negative vector function .

-

•

Constraint functions and are non-negative and linear; i.e., for each , there exists a vector and a scalar such that , and for each , there exists a vector and a scalar such that .

The attribute optimization problem under the above assumptions (hereafter called non-negative attribute optimization; NAO) can be written as follows:

| (4) |

Hereafter, Eq. (4) is referred to as NAO_mix if contains both binary and real-valued variables, and NAO_01 if contains only binary variables. NAO_01 is a special case of NAO_mix.

We will discuss the relation between NAO and a discrete optimization problem called packing integer programs (PIPs) Raghavan (1988). Our first result is that NAO_01 includes PIPs as a special case, implying a hardness-of-approximation result of NAO_01.

Theorem 7.1.

There exists a polynomial-time reduction from PIPs to NAO_01. It is thus NP-hard to approximate NAO_01 within a factor of for any , where is the dimension of a domain-attribute vector.

Having known that NAO_01 is hard in general, we restrict the class of input structures to study the approximability of NAO_mix. For each , let be the number of constraints that appears in; i.e.,

The column sparsity is then defined as . Our second result states that we can approximate NAO_mix accurately if is bounded.

Theorem 7.2.

There exists a polynomial-time -factor approximation algorithm for NAO_mix, where is the column sparsity of an input instance.

The above theorem means that we can find a domain-attribute vector that has an objective value at least times the optimum of Eq. (4) in polynomial time. Practically, we can assume the column sparsity to be small; e.g., in experimental evaluation, is at most . Our approximation algorithm makes use of an approximation algorithm for PIPs by Bansal et al. (2012), which conceptually works as follows: (1) it solves the linear programming relaxation of PIPs and applies a randomized rounding on the obtained solution to compute a binary vector , and (2) it repeatedly picks an index with the largest entry that violates some constraints and assigns . Note that in practice, the above procedure is equivalent to the simple rounding method described in Section 5.2.

8 Experiments

In this section, we report experimental evaluations of our proposed method on both toy datasets and real-world datasets.

8.1 Common settings

We first describe the common settings between both toy and real-world datasets.

Evaluation:

To evaluate the performance, we used a domain-wise dataset split, i.e., domain-attribute vectors for testing do not appear in training. Let and , where maps the original index to the permuted index, and and respectively denote the number of training and test domains. The dataset was split into and such that . In our experiment, we split a dataset into training and test datasets.

For each test set of features for test domain , we optimized the domain attributes, denoted by . Let be an evaluation function appropriately defined for each experiment. In the artificial datasets, was the ground-truth function used for data generation. In the real-world datasets, we regarded the LAM trained with “all” the samples, including the samples from the training and test domains, as since we cannot access .

With the optimized domain-attribute vector , we computed the average and relative standard deviation333 The relative standard deviation is the standard deviation over divided by the mean . over , denoted by and , respectively. As evaluation metrics, we used and .

Prediction models:

For comparison, we used the FUA with linear ridge regression. Specifically, we trained with , where is the intercept. We then maximized in a feasible domain, where is the estimated parameter. We refer to this method as FUA-Mean. The above attribute optimization can be regarded as the use of the mean gain function in our proposed method, but it does not take the dependency of features into account in both the prediction and optimization steps. Due to the FUA’s nature, we cannot use the CVaR-based gain function in the same way as our proposed method.

We used a four-layer neural network (---) for the feature mapping function of the LAM. For QBM, we used a three-layer neural network (--) for and set . For the hidden layers of neural networks, we used the ReLU activation function (Glorot et al., 2011) and batch normalization (Ioffe and Szegedy, 2015). We further split the training data into training and validation data. We then trained the neural network with the Adadelta optimizer (Zeiler, 2012) until epochs, and we used the model that achieved the lowest validation error for inference. We refer to LAM/QBM with the mean gain function as LAM-Mean/QBM-Mean and refer to LAM with the CVaR gain function and as LAM-CVaR.

8.2 Mean vs. CVaR-based gain function

We here show the effect of the mean and CVaR-based gain functions.

Data:

We considered an attribute vector to consist of continuous () and binary () variables, i.e., . Each element of the continuous variables was drawn from the standard Gaussian distribution, denoted by , and the continuous variables were then normalized such that . For the categorical variables, one of the elements was chosen uniformly at random.

For a response function, we used , where each element of was drawn from . The response was then observed by , where was drawn from . We drew attribute vectors and samples for each object, i.e., we had , where . We set as and drew each element of from , where denotes a uniform distribution with the range .

| FUA-Mean | LAM-Mean | LAM-CVaR |

|---|---|---|

| 3.24 (0.54) | 3.28 (0.52) | 2.86 (0.46) |

Results:

Table 1 summarizes the averages of and over trials, showing that the mean gain function was better than the CVaR-based gain function in terms of the average response, while the latter gain function was stable in terms of standard deviation.

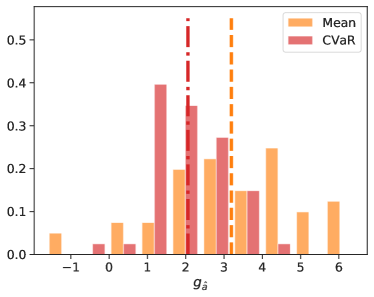

To visualize why the standard deviation of the CVaR-based gain function was lower than that of the mean gain function, we plotted two histograms of the obtained responses of the attributes obtained by the mean and CVaR-based gain functions, respectively, in Figure 2, which illustrates that the response distribution obtained by the CVaR-based gain function was narrower than that obtained by the mean gain function. This is because the CVaR-based gain function took into account the response distribution, in particular, the left-tail of the distribution, resulting in the relative standard deviation of the obtained responses being smaller while the average response remained high, almost comparable to that obtained by the mean gain function in this synthetic data experiment.

8.3 Effect of interaction of domain attributes

Data:

We considered a -dimensional attribute vector to consist of binary variables with , , and . The categorical attribute was chosen from each group uniformly at random. For a response function, we used , where , and each element of was drawn from . The response was then observed by , where was drawn from . We drew attribute vectors and samples for each object, i.e., we had , where . We set as and drew each element of from , where denotes a uniform distribution with the range .

Results:

Table 2 summarizes the averages of and over trials, showing that the obtained gain of QBM was larger than that of FUA and LAM. This result shows that when there is a dependency between domain-attribute variables, models incorporating such a domain-attribute interaction attain higher performance for attribute optimization.

| FUA-Mean | LAM-Mean | QBM-Mean |

|---|---|---|

| 2.06 (0.94) | 2.08 (0.93) | 2.20 (0.97) |

8.4 Real-world datasets

We next evaluate the performance on benchmark datasets. The statistics of the datasets are summarized in Table 3, and the details are given below.

Sushi:

The SUSHI444 Sushi is a Japanese dish containing vinegared rice. Preference (Sushi) Dataset (Kamishima, 2003) consists of consumer ratings for sushi, features of consumers, and domain attributes of each kind of sushi.555 http://www.kamishima.net/sushi/ The rating of sushi is done by five-grade evaluation (from to ), the mean rating is , and the median rating is . For the description (domain attributes) of sushi, we used the style of sushi, the type of sushi, the oiliness, and the normalized price. In this dataset, the type and style of sushi are categorical domain-attributes, and the oiliness and normalized price are continuous domain-attributes. The task was to find better combinations of domain attributes of sushi.

For the consumer features, we used gender, range of ages, the prefecture in which until years the consumer had lived longest, the prefecture in which the consumer currently lives, and the total time taken for stating their preference of sushi. We then converted the characteristics introduced above into numerical vectors and finally obtained -dimensional feature vectors and -dimensional domain-attribute vectors.

Coffee:

The coffee quality dataset contains reviews.666 The dataset was downloaded from https://github.com/jldbc/coffee-quality-database. Note that we deleted samples that have missing entries. Reviews are given for beans and farms. We used the information for a farm as features and that for a bean as domain attributes. Specifically, the “Country of Origin,” “Certification Body,” and “Altitude”777 If the altitude is given as a range, e.g., -, we used the mean value. in the dataset were used as features, and the “Species,” “Processing Method,” and “Variety” were used as domain attributes. The “Total Cup Points” were used as the score (reward). The full score is , the minimum and maximum scores in the dataset are and , respectively, the mean score is , and the median score is . The number of possible choices of domain attributes is species, processing methods, and varieties. The goal was to find a combination of a processing method, species, and variety of coffee for a specific farm.

Book:

We used goodbooks-10k (Book).888 https://github.com/zygmuntz/goodbooks-10k. The Book dataset collects ratings of books from readers. The range of ratings is from to , the mean rating is , and the median rating is . Since there were items without ratings, we used mean imputation to focus on the effect of our method for simplicity.

We used “Age” and “Country“ as the features of readers, and we used tags of books annotated by users in the book-rating platform as domain attributes. We manually extracted book tags that were likely to be relevant to ratings. Examples of extracted tags are “biography,” “comedy,” and “fiction.” After preprocessing, that is, one-hot encoding, we had ratings of books () from readers ().

Results:

Table 4 summarizes the averages of and over trials, showing that i) LAM with the mean gain function achieved a higher response than the other methods, and ii) LAM with the CVaR gain function tended to produce results with smaller variances among them.

In the real-world datasets, the obtained performance difference between the FUA and the proposed method was larger, compared with the artificial datasets. Since the difference between the different sets of features in the real-world datasets was larger than that in the artificial datasets, the proposed method, taking features into account to optimize attributes, returned more suitable domain attributes than the FUA. These results imply that attribute optimization is a promising means of cooperating with humans in designing new products. On the basis of the results presented by our method, humans can continue further trial and error to find a better description of new products. Another aspect of using our method is that it reduces the cost of designing products and services for each customer because our method is aware of customers’ features. The proposed method will allow us to provide products and services tailored to each customer, which will improve customer satisfaction.

| Dataset | ||||

|---|---|---|---|---|

| Sushi | 50,000 | 31 | 15 | 100 |

| Coffee | 1,161 | 63 | 36 | 23 |

| Book | 7,282 | 64 | 77 | 169 |

| Dataset | FUA-Mean | LAM-Mean | LAM-CVaR |

|---|---|---|---|

| Sushi | 3.79 (0.11) | 3.85 (0.11) | 3.76 (0.10) |

| Coffee | 74.7 (0.09) | 99.4 (0.05) | 98.2 (0.04) |

| Book | 4.76 (0.18) | 7.00 (0.16) | 6.17 (0.10) |

9 Conclusion

Zero-shot domain adaptation is useful in real-world applications, e.g., predicting the sales of a new product for which labeled data are not available. While existing studies focus on improving the prediction accuracy, we considered a reverse process for prediction that can be categorized as predictive optimization. To this end, we proposed a simple framework for predictive optimization with zero-shot domain adaptation and analyzed the conditions in which optimization problems become convex. Furthermore, we discussed the way of handling interactions of variables representing a domain description. Through numerical experiments, we demonstrated the potential effectiveness of the proposed framework.

Finding a promising combination of characteristics of existing products is an important task for manufacturers. While the amount of available data on existing products and consumer reactions is increasing day by day, handling a large amount of data is often difficult for humans without support from computer systems. Our simple formulation could be a guideline for investigating bottlenecks in data-driven design systems and unlock further possibilities in this direction of research.

References

- Bansal et al. (2012) N. Bansal, N. Korula, V. Nagarajan, and A. Srinivasan. Solving packing integer programs via randomized rounding with alterations. Theory Computing, 8(1):533–565, 2012.

- Boyd and Vandenberghe (2004) S. Boyd and L. Vandenberghe. Convex Optimization. Cambridge University Press, 2004.

- Donti et al. (2017) P. Donti, B. Amos, and J. Z. Kolter. Task-based end-to-end model learning in stochastic optimization. In Advances in Neural Information Processing Systems 30, pages 5484–5494, 2017.

- Glorot et al. (2011) X. Glorot, A. Bordes, and Y. Bengio. Deep sparse rectifier neural networks. In Proceedings of the Fourteenth International Conference on Artificial Intelligence and Statistics, pages 315–323, 2011.

- Goemans and Williamson (1995) M. X. Goemans and D. P. Williamson. Improved approximation algorithms for maximum cut and satisfiability problems using semidefinite programming. Journal of the ACM, 42(6):1115–1145, 1995.

- Ioffe and Szegedy (2015) S. Ioffe and C. Szegedy. Batch normalization: Accelerating deep network training by reducing internal covariate shift. In Proceedings of the 32nd International Conference on Machine Learning, pages 448–456, 2015.

- Ito and Fujimaki (2016) S. Ito and R. Fujimaki. Large-scale price optimization via network flow. In Advances in Neural Information Processing Systems 29, pages 3855–3863, 2016.

- Ito and Fujimaki (2017) S. Ito and R. Fujimaki. Optimization beyond prediction: Prescriptive price optimization. In Proceedings of the 23rd ACM SIGKDD International Conference on Knowledge Discovery and Data Mining, pages 1833–1841, 2017.

- Ito et al. (2018) S. Ito, A. Yabe, and R. Fujimaki. Unbiased objective estimation in predictive optimization. In Proceedings of the 35th International Conference on Machine Learning, pages 2181–2190, 2018.

- Kamishima (2003) T. Kamishima. Nantonac collaborative filtering: Recommendation based on order responses. In Proceedings of the 9th International Conference on Knowledge Discovery and Data Mining, pages 583–588, 2003.

- Kang et al. (2017) W.-C. Kang, C. Fang, Z. Wang, and J. McAuley. Visually-aware fashion recommendation and design with generative image models. In IEEE International Conference on Data Mining, pages 207–216, 2017.

- Koutra et al. (2017) D. Koutra, A. Dighe, S. Bhagat, U. Weinsberg, S. Ioannidis, C. Faloutsos, and J. Bolot. PNP: Fast path ensemble method for movie design. In Proceedings of the 23rd ACM SIGKDD International Conference on Knowledge Discovery and Data Mining, pages 1527–1536, 2017.

- Ledoux and Talagrand (1991) M. Ledoux and M. Talagrand. Probability in Banach Spaces: Isoperimetry and Processes. Springer, 1991.

- Mansour et al. (2009) Y. Mansour, M. Mohri, and A. Rostamizadeh. Domain adaptation: Learning bounds and algorithms. In Proceedings of The 22nd Annual Conference on Learning Theory, 2009.

- Mendelson (2008) S. Mendelson. Lower bounds for the empirical minimization algorithm. IEEE Transactions on Information Theory, 54(8):3797–3803, 2008.

- Mockus et al. (1978) J. Mockus, V. Tiesis, and A. Zilinskas. The application of Bayesian methods for seeking the extremum. Towards Global Optimization, 2(117-129), 1978.

- Mohri et al. (2012) M. Mohri, A. Rostamizadeh, and A. Talwalkar. Foundations of Machine Learning. MIT Press, 2012.

- Ohsaka et al. (2020) N. Ohsaka, T. Sakai, and A. Yabe. A predictive optimization framework for hierarchical demand matching. In Proceedings of the 2020 SIAM International Conference on Data Mining, pages 172–180, 2020.

- Raghavan (1988) P. Raghavan. Probabilistic construction of deterministic algorithms: Approximating packing integer programs. Journal of Computer and System Sciences, 37(2):130–143, 1988.

- Rendle (2010) S. Rendle. Factorization machines. In IEEE International Conference on Data Mining, pages 995–1000, 2010.

- Rockafellar and Uryasev (2000) R. T. Rockafellar and S. P. Uryasev. Optimization of conditional value-at-risk. Journal of Risk, 2:21–42, 2000.

- Rockafellar and Uryasev (2002) R. T. Rockafellar and S. P. Uryasev. Conditional value-at-risk for general loss distributions. Journal of Banking & Finance, 26(7):1443–1471, 2002.

- Romera-Paredes and Torr (2015) B. Romera-Paredes and P. Torr. An embarrassingly simple approach to zero-shot learning. In Proceedings of the 32nd International Conference on Machine Learning, 2015.

- Vo and Soh (2018) T. V. Vo and H. Soh. Generation meets recommendation: Proposing novel items for groups of users. In Proceedings of the 12th ACM Conference on Recommender Systems, pages 145–153, 2018.

- Yang and Hospedales (2015a) Y. Yang and T. M. Hospedales. Zero-shot domain adaptation via kernel regression on the Grassmannian. In International Workshop on Differential Geometry in Computer Vision for Analysis of Shapes, Images and Trajectories, 2015a.

- Yang and Hospedales (2015b) Y. Yang and T. M. Hospedales. A unified perspective on multi-domain and multi-task learning. In Proceedings of 3rd International Conference on Learning Representations, 2015b.

- Zeiler (2012) M. D. Zeiler. ADADELTA: An adaptive learning rate method. arXiv preprint arXiv:1212.5701, 2012.

- Žliobaite and Pechenizkiy (2010) I. Žliobaite and M. Pechenizkiy. Learning with actionable attributes: Attention–boundary cases! In IEEE International Conference on Data Mining Workshops, pages 1021–1028, 2010.

- Zuckerman (2007) D. Zuckerman. Linear degree extractors and the inapproximability of max clique and chromatic number. Theory Computing, 3(1):103–128, 2007.

Appendix A Proofs

A.1 Proofs of generalization error bound

Recall the notations and assumptions:

-

•

and are the labeling functions on the target and source domains, respectively.

-

•

for a real number .

-

•

for all and .

-

•

for all and .

-

•

, , , and .

-

•

, , and .

Proof.

From the assumptions, . Let . Based on the standard Rademacher analysis (see, e.g., Mohri et al. (2012), we have for any , the following inequality with probability at least for any :

| (5) |

where and are the empirical and expected Rademacher complexity, is an independent uniform random variables taking values in , and . Let . Then, can be rewritten as . Since is -Lipschitz over , we can use Talagrand’s lemma (Ledoux and Talagrand, 1991): . Furthermore, . For the linear model, the Rademacher complexity can be bounded (see, e.g., Mohri et al. (2012)) as . Replacing with in Eq. (5), we have Proposition 7.1. That is, for any , the following inequality holds with probability at least for any : .

Let . can be rewritten as . We then have . From Eq. (5), we have . Based on the triangle inequality, we have . For any , the following inequality holds with probability at least :

Applying the triangle inequality, we have,

We have, for any , the following inequality holds with probability at least for any :

Replacing with the upper bound, we obtain Proposition 7.2. ∎

A.2 Proofs of approximability

Before going into the proof of the two results above, we define PIPs as follows Raghavan (1988).

Definition A.1 (Packing integer program).

Given vectors , a capacity vector , and a weight vector , the packing integer program (PIP) is defined as the following problem:

We define the column sparsity as .

Proof of Theorem 7.1.

Let , , and be an instance of PIP. We can construct an instance of NAO_01 in polynomial time such that the following conditions are satisfied:

-

•

and satisfy that ,

-

•

the number of inequality constraints is , the number of equality constraints is , and

-

•

for each , it holds that and .

It is easy to verify that the resulting instance of NAO_01 is exactly equivalent to a given instance of PIP; the inapproximability result is thus obvious (see, Bansal et al. (2012); Zuckerman (2007)). ∎

Proof of Theorem 7.2.

Fix an NAO_mix instance .

We first partition an -dimensional domain-attribute vector into continuous domain attributes and binary domain-attributes. Let and be the set of indices for continuous variables and binary variables, respectively. Let us denote and , and denote , , and ; note that . The original NAO_mix (denoted P1) can be rewritten as

We now describe the approximation algorithm for P1. We first consider the linear programming (LP) relaxation of P1 (denoted LP1) that relaxes “” to “”. Since LP1 is an LP instance, we can solve it exactly in polynomial time, e.g., by the ellipsoid method, and denote its optimal solution by . We then create a new instance of NAO_01 (denoted P2) where entries of are fixed to entries of , and relax each equality constraint “” to “”, the resulting NAO_01 instance (denoted P2’) by which is an instance of PIP whose column sparsity is at most . We thus can use Bansal et al. (2012)’s algorithm to find an -factor approximate solution for P2’. We can increase some of the entries of until the equality constraints are satisfied, which does not decrease the objective value. Finally, we return a domain-attribute vector defined as follows:

| (6) |

Since the feasibility of is obvious, we analyze its approximation ratio. Let be an optimal solution for P1. Observe that as is an optimal solution for LP1. We then show that . Recall that Bansal et al. (2012)’s algorithm returns a feasible solution for a PIP instance that has an objective value at least times the optimum value of its LP relaxation. If is an optimal solution for the LP relaxation of P2’, it holds that ; hence, we have that . Consequently,

is an -factor approximate solution to NAO_mix, which completes the proof. ∎