Non-directed polymers in heavy-tail random environment

in dimension

Abstract.

In this article we study a non-directed polymer model in dimension :

we consider a simple symmetric random walk on which interacts with a random environment,

represented by i.i.d. random variables .

The model consists in modifying

the law of the random walk up to time (or length) by the exponential of

where is the range of the walk, i.e. the set of visited sites up to time , and are two parameters.

We study the behavior of the model in a weak-coupling regime, that is taking vanishing as the length goes to infinity,

and in the case where the random variables have a heavy tail with exponent .

We are able to obtain precisely the behavior of polymer trajectories under all possible weak-coupling regimes with :

we find the correct transversal fluctuation exponent

for the polymer (it depends on and )

and we give the limiting distribution of the rescaled log-partition function. This extends existing works

to the non-directed case and to higher dimensions.

2010 Mathematics Subject Classification:

82D60, 60K37, 60G70

Keywords:

Random polymer, Random walk, Range, Heavy-tail distributions, Weak-coupling limit, Super-diffusivity, Sub-diffusivity

1. Introduction

We consider in this paper a non-directed polymer model in which a simple symmetric random walk on (with ) interacts with a random environment. This model is closely related to the celebrated directed polymer model, for which we refer to [17] for a complete overview. The main difference here is that the random walk is not directed: it can come back to a site that has already been visited, but the interaction is however counted only once (in the spirit of the excited random walk, see [3]). The model can also be viewed as a randomly perturbed version of random walks penalized or rewarded by their ranges, depending on the positivity or negativity of the external field. The non-directed polymer model was first introduced by [25] (with exponential moment conditions on the environment) and its study was followed in [5] with a detailed analysis in dimension . Here, we investigate the case of a heavy-tail random environment, in analogy with [7, 19, 24] for the directed polymer model — our results can be viewed as a extension of [7, 19, 24] to a non-directed setting (and to higher dimensions).

1.1. The non-directed polymer model

Let be a simple symmetric random walk on with . We denote the probability and expectation with respect to by and respectively. Let be a field of i.i.d. random variables (the environment), independent of . The probability and expectation with respect to are denoted by and respectively.

The non-directed polymer model up to time is defined via the following Gibbs’ transform: for a given realization of the random environment and for (the inverse temperature) and (an external field), let

| (1.1) |

where is the range of the random walk up to time . The partition function is the constant which makes a probability measure and is equal to

| (1.2) |

Note that if (i.e. when there is no disorder) and , then (1.1) becomes the model of a random walk penalized by its range, defined by . That model has been well-studied (starting with the seminal work [21]) and is now well-understood: with high -probability, is close to a -dimensional ball with an explicit radius without holes (see [11, 4, 20]).

When is non-trivial, the model (1.1) describes a self-attracting (if ) or self-repulsing (if ) polymer interacting with a random environment. At each site, the polymer chain interacts with the disorder exactly once, which may model a screened interaction, one monomer “absorbing” all the interaction at a specific site. We have chosen to stick to this setting in order to pursue the study initiated in [5, 25], which considers this model as a disordered version of a random walk penalized by its range.

Remark 1.1.

One could study a polymer interacting repeatedly with the disorder, that is

(note that the term in the Hamiltonian is a constant and thus does not change the measure). In that case, large values of will play an overwhelming role in the measure, since their effect can be accumulated by returning repeatedly to a given site. One can therefore expect a very strong localization phenomenon, the polymer staying on one site with the largest possible , with high probability. In the literature, this model is referred to as the parabolic Anderson model and the one-site localization for heavy-tailed environment has been proven in [13], see [28] for a continuous-time version of the result.

The main goal is then to understand the shape of typical polymer trajectories under the measure , as . One of the main question is to know if and how the presence of the environment perturbs the structure of the typical trajectories of the walk. In particular, one is interested in describing the end-to-end (or wandering) exponent and the fluctuation (or volume) exponent , that are loosely speaking defined as:

For comparison, let us stress that the random walk in dimension , is replaced in the directed polymer model by a directed random walk in dimension . In particular, the parameter does not have any influence on the polymer measure, since the number of visited sites is deterministic (and no site is visited twice). An important feature of the directed polymer model is that a phase transition is known to occur: when have an exponential moment, if is (striclty) smaller than some critical value , then trajectories are diffusive (, ), whereas if is (stricly) larger than trajectories exhibit some localization properties and are conjectured to have a super-diffusive behavior (at least in low dimensions) — for instance, in dimension it is conjectured that and . The critical value is known to be in dimension and (hence there is no phase transition) and in dimension with . We refer to [17] and references therein for more details.

In the non-directed case, however, the parameter plays an important role, and random walk trajectories with a large range are rewarded or penalized (depending on whether is positive or negative). In analogy with the directed polymer model, the presence of a random environment should still have a stretching effect. The competition between the folding effect of range penalties and the stretching effect of a random environment has been recently investigated in detail in the case of dimension , [5] (in particular, it has been found that when ). But such a study appears difficult in higher dimension, because the range of the simple random walk then has a complex geometry. However, in the case of a heavy-tail random environment, the localization features of the model become more salient, since a few sites in the environment will have a much higher value than the others: we are indeed able to describe quite precisely the behavior of the non-directed polymers in that case. This generalizes the study in [7, 19] to the case of non-directed polymers and to higher dimensions. Let us stress that as a by-product of our results we have that in the heavy-tail setting there is no phase transition: in any dimension.

Weak-coupling regime.

A recent approach for studying disordered system, initiated in [1], and which has been developed extensively over the past few years, is to consider weak-coupling regimes, see e.g. [6, 14, 15, 19, 25]. The idea is to take the inverse temperature vanishing as goes to infinity. In the papers cited above, the goal is to find the appropriate scaling for in order for the partition function to converge to a non-trivial random variable. This regime is called of intermediate disorder: loosely speaking, it corresponds to a regime in which disorder just kicks in, in the sense that it is still felt in the limit, but is not strong enough to make the (averaged) disordered measure singular with respect to the reference measure.

We will assume that there is some and some such that

| (1.3) |

and we will write ; we may also consider the case or . We think of as a parameter one can play with, which tunes the speed at which goes to zero. We could actually work with general sequences (in particular, the important relation is (1.5) below), but we stick to the pure power case (1.3) in order to clarify the exposition — it will capture all the essential features of the model, see Remark 2.3.

Let us also stress that we will consider fixed, seen as a centering term for the disorder .

Heavy-tail environment.

Our main assumption in this paper is that are i.i.d. random variables, with a pure power tail behavior. We assume that there exists some such that

| (1.4) |

Also here, we could consider a more general asymptotic behavior in (1.4), for instance replacing the pure power by with a slowly varying function. However, we stick to the pure power case as in (1.4) for the sake of clarity — again, it will capture all the essential features of the model.

For simplicity, we also assume that , but this does not hide anything deep.

1.2. Heuristics for the phase diagram

Let us present a Flory argument to guess the wandering and fluctuation exponents. The idea is to find the correct transversal fluctuations (with ) such that the entropic cost for the random walk to stretch to a distance is balanced by the possible energetic gain from high weights contained in a ball of radius . At the exponential level:

-

•

the entropic cost is of order ;

-

•

the energetic gain is of order , where is the order of the maximal weight in a ball of radius .

Hence, the energy-entropy balance leads to the relation

| (1.5) |

In the case we are interested in, that is if with , this gives with verifying

| (1.6) |

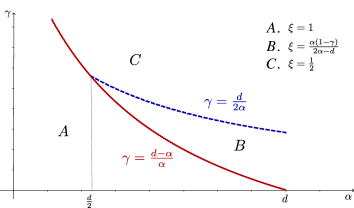

provided that , that is (note that this range of parameter is non-empty only if ). However, this picture should fail when is large (in particular when ), because then the strategy of visiting mostly high-energy sites should be outperformed by a collective optimization (that is still poorly understood, especially in dimension ). We refer to [10] for a discussion on that matter. We therefore focus our attention on the case .

When , then since the transversal fluctuations cannot exceed , the energetic gain should always overcome the entropic cost: we should have . On the other hand, when for or for , then the energetic gain can never overcome the entropic cost of reaching distance much larger than : we should have .

To summarize, one should have the following three regions when .

-

A.

If and , then .

-

B.

If and , then .

-

C.

If and , then .

We refer to Figure 1 below for a graphical representation of these regions, and to [7, Fig. 1] for a comparison with the corresponding picture in the directed polymer in dimension (where conjectures for larger values of have the merit to exist). Our main results consist in establishing this phase diagram.

1.3. Definition of quantities arising in the scaling limit

Our results additionally provide the scaling limit of the log-partition function in all weak-coupling regimes when . In order to describe the limit, let us introduce the continuum counterparts of the random environment and of random walk trajectories, and define the corresponding notion of energy and entropy.

The continuum environment arises as the extremal field of : we let be a Poisson point process on of intensity . With a slight abuse of notation (it will not draw any confusion), we denote its law by . We also let

| (1.7) |

which represents the set of allowed paths (corresponding to scaling limits of random walk trajectories). Then, for a path , we define its energy

| (1.8) |

To define the entropic cost, let us observe that we have the following large deviation principles for the simple random walk: for and (we omit integer parts to lighten notation), cf. Lemma B.1 in Appendix

where is a given rate function; we stress that if and if , with the norm of .

We then define two different entropic cost functions for a path — or rather for the image — depending on whether the path comes from the scaling of a random walk trajectory with wandering exponent or . In the case , we define

| (1.9) |

where the infimum is over

| (1.10) |

In the case , we define analogously

| (1.11) |

The second identity comes from the fact that: (i) the right-hand side is a lower bound for the left-hand side (by Cauchy–Schwarz inequality); (ii) the lower bound is attained for the parametrization of by its length, that is choosing such that for .

Let us also stress that for all , so that for all .

The continuous energy-entropy variational problem that we expect to arise as the scaling limit of the log-partition function are , the entropy term being one of (1.9) or (1.11) depending on the scaling considered. As an important part of the proofs, we will show that these continuous variational problems are well-defined.

2. Main Results

Before we state our results, let us define more precisely what we intend when we say that the polymer has transversal fluctuations .

Definition 2.1.

We say that has transversal fluctuations of order under if for any there exists some such that for all large enough

We separate our results according to the different regions we consider. In all the rest of the paper, we work in dimension .

Notational disclaimer. For two sequences , we write if , if , and if .

2.1. Region A: ,

Our first result gives the scaling limit of the model in region A of Figure 1. This is the analogue of what Auffinger and Louidor [2] proved in the context of the directed polymer model in dimension : the following result therefore generalizes [2] to the non-directed framework and to higher dimensions.

Theorem 2.2.

Remark 2.1.

Let us stress that by an extended version of Skorokhod representation theorem, see [27, Cor. 5.12], one can upgrade the convergence (2.1) to an almost sure one. More precisely, if we look at as a function of and the continuous limit , then by [27, Cor. 5.12], the convergence in distribution in Theorem 2.2 implies that there exist some random elements and defined on the same probability space such that , and such that almost surely.

It therefore makes sense to work conditionally on , even at the discrete level. We have the following corollary, which says that conditionally on , transversal fluctuations are of order .

Proposition 2.3.

Let and let be such that . Then has transversal fluctuations of order under .

Let us now give some property on the variational problem , and in particular state that it is well-defined.

Proposition 2.4.

When , the variational problem defined in (2.1) is a.s. finite for all . Moreover, letting , we have that if and if .

Remark 2.2.

We could have formulated the convergence in distribution in Theorem 2.2 as follows:

However, in the case , this would only give that goes to . The formulation of Theorem 2.2 allows us to treat the case , in which is much larger than — in particular, it includes the case . In that case, the entropy term disappears in , even though the constraint that paths have a finite entropy has to remain (for instance to avoid having paths of length larger than ).

2.2. Region B: ,

In region B, our result is the analogous to Theorem 2.5 in [7] in the context of the directed polymer model in dimension : this generalizes [7] to the non-directed framework and to higher dimensions. Here, we will fix the parameter to be equal to , which is well defined since .

Theorem 2.5.

Let us stress that the choice of is crucial because the contribution of the small values of the environment (that is ) to the partition function is negligible only if we center the random variables . This centering term is also needed in the directed case, cf. Section 4.2 Eq. (4.27) of [7].

The fact that the variational problem is well-defined in the case is non-trivial, and relies on (non-directed) entropic last-passage percolation (E-LPP) estimates, introduced in [9]. Properties of the variational problem are summarized in the following Proposition, which is the analogous of [8, Thm. 2.4] (and generalizes it to the non-directed case and to higher dimensions).

Proposition 2.6.

If , the variational problem defined in (2.2) is a.s. positive and finite for all . Moreover, for any , and we have the scaling relation

| (2.3) |

On the other hand, if , we have a.s., for all .

Remark 2.3.

If we consider more general sequences , then the corresponding transversal fluctuations are given by the relation (1.5), that is . In analogy with [7, Thms. 2.5–2.7], we should find three different scaling limits in region B, according to whether (corresponding to the bulk of region B Theorem 2.5 above), or (corresponding to boundary regions between region B and region C). We have chosen here to consider only pure powers for (and for ) in order to keep the exposition clearer — the arguments from [7] could be adapted here but it would significantly lengthen the paper.

2.3. Region C: ,

In region C, we will show that transversal fluctuations of the polymer are of order . As a preliminary remark, let us stress that for any (omitting integer parts to lighten notation), we have the following asymptotics for . Setting if and if , we have

| (2.4) |

where is the escape probability and is the heat kernel of a -dimensional Brownian motion with covariance matrix . The asymptotics (2.4) can be derived from Uchiyama’s results [32]: see [32, Thm. 1.6] for the case of dimension and [32, Thm. 1.7] for dimensions .

In region C, the cases , and , need to be treated separately, similarly to the case of the directed polymer model [7].

Case

We start with the case , , which is easier to state. Let us introduce some quantities that arise in the limit: we stress that different objects arise depending on the dimension.

Proposition 2.7.

In dimension , define

| (2.5) |

where we recall that . Then the random variable is well-defined if .

Proposition 2.8.

We are now ready to state our results in the case , . It is the analogous of Theorem 1.4 in [19] for the directed polymer model in dimension : it generalizes [19] to the non-directed case and to higher dimensions. Here again, we need to fix .

Theorem 2.9.

Let and let be such that . Then has transversal fluctuations of order under . We also have the following convergences in distribution, as :

• If (in particular ), then setting for , for , and for we have:

| (2.7) |

for some explicit constant ; recall has been defined in (2.5).

Remark 2.4.

Let us stress that when , in dimension we have (assume to simplify), so in particular it goes to as . One can easily check that we always have when (and thus, ), so the centering in (2.7) is non-trivial.

Case

In this second case, recall Theorem 2.2 and Proposition 2.4. If and as , then the scaling limit of the log-partition function has been identified as . However, when we have when , with a.s.: in that case, the scaling limit is thus trivial. Our next result shows that when , then transversal fluctuations are necessarily of order ; this has to be compared with Proposition 2.3 which asserts that transversal fluctuations are of order when . This shows that when we cannot have intermediate fluctuations between and : the system exhibits a sharp phase transition at the critical point . Our result is the analogous of Theorem 2.12 in [7], and generalizes it to the non-directed case and to higher dimensions.

Let us define another quantity, analogous to defined in (2.6).

Proposition 2.10.

For , define

| (2.9) |

with defined in (2.4) and the intensity measure for . If , then is a.s. finite in any dimension . If , then is a.s. finite if and only if .

Recall that by an extended version of Skorokhod representation theorem [27, Cor. 5.12] (cf. Remark 2.1), it makes sense to work conditionally on or , even at the discrete level. If , we need to take and if , then may be any real number.

Theorem 2.11.

Let , and let be such that . Then conditionally on the event (i.e. ) the polymer has transversal fluctuations of order under . Moreover, conditionally on , we have the following convergences in distribution, as .

2.4. Comparison with directed polymers

As we stressed in the introduction of this paper, the model (1.1) is closely related to the directed polymer model — our results can be seen as an extension of existing results to a non-directed setting and to higher dimension. Let us now briefly discuss this relation by comparing the techniques exploited in the present article with the one developed for the directed polymer.

• In Region A our results extend [2, 24], where the authors considered the directed polymer in dimension . In this region, only a few points give an energy contribution to the variational problem: the random walk linearly interpolates between these points to get the maximal energy reward to compensate the entropy cost. The fact that we can approximate the problem by considering only a finite number of points allows us to extend and exploit the techniques introduced for the directed case: the scheme of the proof is very close to the one in [2].

• In Region B, our results extend the analysis performed in [7] to the non-directed framework. In particular our techniques are based on the non-directed Entropy-controlled last passage percolation (E-LPP) introduced in [9] (as an extension of the directed E-LPP of [8]), a crucial step consisting in showing that we can restrict the partition function to trajectories staying at scale . The extension to a non-directed setting and to higher dimension is the main novelty here, as discussed in Appendix A. Overall, the proof follows the same scheme as in [7], but several adaptations are needed, with some tedious technicalities.

• In region C, we perform a polynomial expansion analysis, in the same spirit as in [19] for the directed polymer model with heavy-tail disorder. The crucial difference here is that in our non-directed case the geometry of the range plays a central role in the behavior of the model (and so in the polynomial expansion analysis). We therefore have to use here a local central limit theorem for the range, considering the probability that a point at scale belongs to the range , i.e. . Even if the proofs in region C start from the same idea as in [19], the technical treatment of the polynomial expansion requires new ideas and becomes more technical and dimension dependent. Let us stress that the case of dimension requires particular care, because then scales as , compared to the polynomial behavior in dimension .

To conclude, let us comment on the limiting random variables that appear in Theorems 2.9-2.11; note that they indeed depend on the dimension. The random variable (see Propositions 2.8-2.10) appears when , in dimensions or when : it is the analogous of defined in [19, p. 4011] (see also [19, Thm. 1.4]). When , then in dimensions , analogously to [19, Thm. 1.2] a normal random variable appears, whereas in dimension a new random variable pops up (see Proposition 2.7 for the definition of ), which to our knowledge has no analogous in the literature.

2.5. Further comments and conjectures

Our article solves completely the case , but there are several aspects that remain to be tackled:

-

•

In Region B and in Region C with , the parameter is needed to be set equal to to center the environment: the case of a general should be investigated;

-

•

More precise statements on the convergence of paths could be extracted from our results, in particular one could try to prove in some cases a localization of the trajectories near an optimal path;

-

•

The case is still a challenge: the wandering exponent is not known — except in the intermediate disorder regime (Region C), where (but one still has to understand the corrrect scaling for ).

In this section, we develop further on these aspects, we comment their relation with the literature, and we present some open problems and conjectures.

2.5.1. About the external field

It is not hard to see that in Region A, the parameter is unimportant. On the other hand, for Region B and for Region C with , we can see from the proofs (cf. Sections 6-8) that a centering is needed, so needs to be fixed equal to . In order to make the proofs more transparent (which are already quite technical) and to simplify some non-central arguments, we have chosen to stick to a non-negative disorder: this is used in particular in Region A and B (they are related to the discrete energy-entropy variational problems, cf. Section 4). This also has the advantage to illustrate when a centering of the environment is crucial or not. Without the assumption of non-negativity of the disorder, the proofs may require some extra technical work, and one should still center the by the parameter when needed (or take and ).

Furthermore, we can also consider a more general setting for our non-directed polymer model, by considering the following:

with and (note that in this article, is simply ). The above model can be viewed as a perturbed version of a random walk penalized by its range and is more challenging. The case of the dimension has been analyzed thoroughly, see [5]. In particular, we can expect that when is large enough (at least compared to ), i.e. when the penalty by the size of the range dominates, then the polymer folds into a ball (similarly to [4, 11, 20]). However, contrary to the homogeneous model where the center of the ball is random, the location of the ball may be completely determined by the environment, since the polymer tends to maximize the sum of ’s seen in the ball—see [12] for the one-dimensional case. On the other hand, there should be a regime where a balance is found between the energy and the entropy (the penalization by the range is negligible—this is somehow the focus of this article), and a regime where a balance is found between the penalization by the range and the energy (the entropic cost of having an unusual range being out-weighted by the range penalty). For , the phase diagram of the above model should be similar to the one found in the one-dimensional case, cf. [5].

2.5.2. About the geometry of the range

In this paper we consider the scaling limits of the logarithmic partition function and we describe the transversal fluctuations of the walk. Such results are the starting point to push further the analysis of the geometry of the range . In this setting we conjecture that the limits of the logarithmic partition function contain all the information to describe the geometry of the random walk. To be more precise, in Region A and B we conjecture that the supremum of the variational problem and is attained by some unique continuous path that we call and respectively, by analogy with [2, 8]. We then conjecture that the typical range of the random walk is concentrated around these paths. More precisely, if we look at a path as a set, i.e. if we consider its support in , then we conjecture that under the hypothesis of Theorem 2.2, for any ,

| (2.12) |

and under the hypothesis of Theorem 2.5, for any ,

| (2.13) |

where and is the coupling between the discrete and continuous disorder introduced in Remark 2.1.

In region C we expect that converges to a continuous limit, which should be a random perturbation of a Brownian motion range (but a precise statement is harder to state).

2.5.3. About the intermediate disorder regime (region C)

In [25], Huang considers the intermediate disorder regime of the model (that is a regime where but disorder has a non-trivial effect), in the case of a disorder with finite exponential moment, i.e. (or roughly speaking, ). More precisely, Huang [25] shows that, taking

| (2.14) |

for some and taking , then converges in distribution toward a random variable , given by an explicit Wiener chaos expansion.

Our Theorem 2.9 is the analogue of this result in the case (and any dimension ). In particular, (2.7)-(2.8) states that the choice is the correct scaling in order to observe non-trivial fluctuations for . Analogously to what is done in [19] for the directed polymer, one could try to extend our Theorem 2.11 to the case , i.e. to study the intermediate disorder regime for all values of . We leave this as an open problem, but let us comment on the expected results.

In dimension , we expect that the correct intermediate disorder scaling is for all (the scaling limit is then given by Theorem 2.9) and that one reaches the scaling given in (2.14) for all , with then the scaling limit as in [25].

In dimension , we expect that the correct intermediate disorder scaling is for all , with a scaling limit similar to Theorem 2.9, and that one reaches the scaling given in (2.14) for all , with then the same scaling limit as in [25]. A way to understand this comes from (2.7): loosely speaking, it says that in dimension , taking we get that for some random variable . This approximation may remain valid for some but it must fail when becomes of order (that is when reaches the value ), at which point all terms in the polynomial chaos expansion of the partition function are of the same order.

In dimension , the correct intermediate disorder scaling should be for any , with a scaling limit similar to Theorem 2.9. Indeed, the convergence (2.7) states that taking we have for some random variable : since in dimension and in dimension , we have that for any . In that case, we should therefore have that , with fluctuations of order . Additionally, for disorder with exponential moments (i.e. ), the approximation suggests that: in dimension , one should take to observe a non-trivial scaling limit for (disorder is marginally relevant); in dimension , one should have that has a non-trivial limit for small (but fixed) — in other words, there is a weak disorder phase (disorder is irrelevant), in analogy with the directed polymer model in dimension .

2.5.4. About the transversal fluctuations in the case

Let us now consider the case of fixed and let us recall the Flory argument presented in Section 1.2: for , the energetic gain of a polymer in a box of size is of order , while the entropic cost of going at distance is of order . The energy-entropy balance leads to the prediction that . This should hold as long as . In particular, if we should have that : this is what is proven (in a more general framework) in the present paper, see Theorem 2.2 (Region A).

When , in comparison with the directed polymer literature (see e.g. [23]), we may conjecture that there exists some such that for we have and for we have , where is the fluctuation exponent obtained for a disorder with finite exponential moments. Such should therefore solve the equation , that is ; by convention when . This fact has indeed been proven in dimension in [5], in the non-directed setting of the present paper: in that case we have if , if and for all .

The question in dimension remains quite mysterious (both for non-directed and directed polymers), in particular because the fluctuation exponent is unknown. It is expected that, at least in low dimensions, there is some critical value below which (which would lead to ) and above which (which would lead to ). In view of the previous subsection, one could argue that in dimension we have , but for now this is purely speculative. Let us also mention that the existence of an upper critical dimension above which for all is still controversial, see e.g. [29]. In order to extend the analysis of the problem to , a first step would be to study the existence and dependence on the parameters of the conjectured exponent .

2.6. Organization of the rest of the paper

We now present the organization of the paper and describe how the proofs are organized.

In Section 3 we prove that the variational problems , and the random variables and are well-defined (i.e. Propositions 2.4, 2.6, 2.7, 2.8 and 2.10). Along the way we discuss their main properties.

In Section 4 we present the main auxiliary results about the discrete approximation of the energy-entropy variational problems and that we use to prove Theorems 2.2-2.5. These results extend the analogue results obtained in [8, 9] to the -dimensional and non-directed case; they are related to the Entropy-controlled Last-Passage Percolation (E-LPP). Some results on the non-directed version of the E-LPP are postponed to the Appendix A.

In Section 5 we prove Theorem 2.2, i.e. region A. To prove this, we first reduce to a partition function restricted to the largest weights , see (5.1), by showing that the contribution of all smaller weights is negligible, see Lemma 5.1. We then show that , properly rescaled, converges to the continuous variational problem restricted to the largest weights, see Lemma 5.2.

In Section 6 we prove Theorem 2.5. As a crucial first step, in Section 6.1, we show that we can restrict the partition function to trajectories staying at scale , see Proposition 6.1. To achieve this, we need to show that the entropic cost to reach a distance cannot be overcompensated by an energetic gain at scale : this is the purpose of Lemma 6.2. This relies once again on controlling the contribution of different ranges of weights to the partition function; the most technical part actually consists in controlling the contribution of intermediate weights, which requires a detailed analysis to match the energetic gain with the entropic cost. Once trajectories have been reduced to being at scale , the convergence of the partition function is performed in Section 6.2, see Proposition 6.3; the strategy of the proof is similar to what is done in Section 5 for region A.

In Section 7 we prove Theorem 2.9. The idea of the proof is based on a truncation of the environment (7.3) which allows us to prove that the main contribution comes from trajectories that stay at scale . The convergence of the partition function defined on the truncated environment is presented in Lemma 7.2. Its proof is based on a polynomial expansion analysis (7.11) in which we show that the convergence is led by the first term. Different random limits arise depending on the tail exponent and the dimension . If the limit is Gaussian in small dimensions () and in high dimension () the limit is described by the averaged (w.r.t. the random walk) sum of the environment on , see the definition (2.5) of . If the limit conveys the heavy-tail structure of the environment, see the definition (2.6) of .

In Section 8 we prove Theorem 2.11. The most technical issue consists in showing that conditionally on the main contribution to the partition function comes from trajectories that stay at scale , see Section 8.1; in particular, this shows that trajectories cannot have intermediate scale. Then, the strategy is similar to that used in Section 7, combining a truncation of the environment and using a polynomial expansion.

Finally, we collect in Appendix several technical estimates. As mentioned above, Appendix A provides useful results for the non-directed E-LPP. In Appendix B, we collect some simple random walk estimates: large and moderate deviations, probabilities that a given set is visited, intersection of ranges of independent walks. In Appendix C, we give estimates on exponential moments of a truncated version of the environment.

3. Properties of the limiting variational problems and random variables

In this section, we prove the well-posedness of the variational problems and (in Section 3.2, together with some of their properties), of (in Section 3.3) and of and (in Section 3.4).

3.1. Some notation: order statistics and truncated energy

We introduce some notation to describe the contribution of large weights to the variational problems , . For we define

| (3.1) |

and for a realization of , we set . Then, the energy along a path is given by

| (3.2) |

In the ball we can also label the points of by using the order statistics:

| (3.3) |

where the distribution of is given as follows:

- (i)

-

(ii)

are i.i.d. uniform random variables on , independent of ; these are the location of the weights;

We then define the truncated analogue of (3.2):

| (3.4) |

and we also let

Remark 3.1.

Notice that if verifies with , then the length of the path is bounded by , and so we have .

3.2. On the variational problems and

Recall that and are defined respectively in (2.2) and (2.1). Here, we prove Propositions 2.4-2.6: We mostly focus on the first one (i.e. on ): we treat along the way, since the results follow from a simple comparison with (recall that for all ), or with identical arguments.

Before we start, let us stress that for almost every realization of , the maps and are non-decreasing and continuous. The proof of this fact is identical to that of [8, Thm. 2.4] (see Section 4.5 in [8]), so we omit it.

Proof of the scaling relation (2.3)

Consider the Poisson Point Process on with intensity . If we consider, for , the scaling tranformation , then we have that ; notice also that and . Therefore, since , by applying the scaling , we get

so that . This implies (2.3). ∎

Finiteness of (and of )

For any interval let us define

| (3.5) |

In such a way, we have that

Using the scaling properties of and that having implies (see Remark 3.1), we get that

| (3.6) |

The following lemma is the key result to prove the finiteness of . Its proof is similar to that of [8, Lemma 4.1] and is based on entropy-controlled last-passage percolation (E-LPP) estimates. We postpone its proof to Appendix A.

Lemma 3.1.

Let . For any there is a constant such that for any ,

In particular, it shows that for any we have that is a.s. finite.

Using Lemma 3.1 we can conclude the proof of the finiteness of when . For any , using (3.6) and Lemma 3.1 we get that for any

| (3.7) |

Then, for any , a union bound gives

| (3.8) |

where we split the series at and used that for , and for . Since , we obtain that is smaller than a constant (that depends on ) times

In particular, for any there is some constant such that for any

| (3.9) |

This concludes the proof that is a.s. finite when . Also, since can be chosen arbitrarily close to , this proves that for any .∎

Remark 3.2.

Positivity of (and of )

Let us consider the random set, for any

| (3.11) |

If , let and be the straight line from the origin to , which verifies . Therefore, on the event , we have

| (3.12) |

Notice that are independent Poisson random variables with mean

Hence, we get that if : this proves that (by and the independence of ), so that almost surely, for any . ∎

Infiniteness of for

As far as the case is concerned, since are independent, the Borel-Cantelli lemma ensures that a.s. for infinitely many . This proves that almost surely, for infinitely many , that is a.s. when . ∎

Remark 3.4.

Note that we have proven that a.s. for all , for any . The reason is that in that case trajectories with cannot exit the ball of radius ; there is no contradiction with the fact that when .

Case , proof of

We now prove the part in Proposition 2.4, i.e. that for sufficiently small when , or equivalently a.s. We proceed as in [31, Section 6].

Let be a maximizer of , which a.s. exists (and is unique) — the proof of the existence and uniqueness of a maximizer is identical to that given in [8, Sec. 4.6]. In the following preliminary result we show that for any , if is small, then has a small entropy (and is therefore confined in a small ball around the origin). We denote the length of by .

Lemma 3.2.

For any fixed , -a.s., for any there exists such that for all ; in particular, since we get that .

Proof.

We can now deduce that there exists such that if . Let and as in Lemma 3.2, that is for all . Moreover define . Then, since , we get that if

| (3.14) |

For any , since , we can find some such that . Then with probability large than ,

| (3.15) |

Now, if , then . Otherwise, if , we use the following union bound for

| (3.16) |

Now, setting and , we get that for any

where for the last inequality we used the scaling above with to get that has the same law as , together with Lemma 3.1. With the definition of , we end up with

| (3.17) |

where we used that to see that the sum is finite. Finally, we have

| (3.18) |

Letting first and then , we conclude that for . ∎

3.3. Well-posedness of

We now prove Proposition 2.7. Notice that the condition ensures that so in particular exists. Let us denote for simplicity. We prove that converges -a.s., using Kolmogorov’s three-series theorem.

Before we turn to the control of the three series, let us stress that when we have

| (3.19) |

where is the Green function. The fact that the sum is finite is due to the fact that as in dimension and that .

We now control the three series in Kolmogorov’s three-series theorem.

(ii) The second series is

where we used that and for any .

(iii) The third series is

where we used that is bounded by a constant times if , by a constant times if and by a constant if . The fact that the second series is finite comes from the fact that with as and with . This concludes the proof of Proposition 2.7. ∎

3.4. Well-posedness of

In this part, we prove Propositions 2.8 and 2.10, starting with the second one. Let us stress that by (2.4), is a radially decreasing function, with the following asymptotics:

| (3.20) | ||||

| (3.21) |

Proof of Proposition 2.10.

Proof of Proposition 2.8.

Recall that we deal here with the case with dimensions . Recalling the definition (2.6) of , and using Proposition 2.10, we simply need to show that

To simplify notation, we only treat the case ; the case is identical. Now, by [27, Theorem 10.15], we need to show that

| (3.22) |

Note that when we have : hence, the restriction of the above intergral to is bounded by

which is finite thanks to the asymptotics (3.20)-(3.21) of .

On the other hand, using that , we also get that the restriction of the integral in (3.22) to is bounded by

| (3.23) |

For the first inequality we used that there are constants such that for all . For the second inequality, we used that: (i) in the first term we have , which is integrable on ; (ii) in the second term we bounded the volume of the ball of radius by a constant times . To conclude, we get that the first integral in (3.23) is always finite, while we use that to get that the second integral is finite. ∎

4. Discrete approximation of the variational problems

In this section, we present the main auxiliary results that we use to prove Theorems 2.2-2.5; they are also of independent interest. They extend analogous results obtained in [8, 9] to the -dimensional case. We start with the definition of important quantities that are used throughout the rest of the article, then we state the convergence result.

4.1. Discrete energy-entropy variational problems

Let us introduce the discrete analogue of the variational problem in (2.2). It will appear naturally when considering the log-partition function with trajectories restricted to staying in a ball of radius ; when the scale is some other entropy functional need to be considered, analogously to (1.9) — we will treat that case afterwards.

Discrete entropy of a set of points.

For any set of ordered distinct points (with a slight abuse of notation, we sometimes interpret as a subset of ), we define the entropy related to the set by

| (4.1) |

where by convention. Note that the entropy of a set depends on the order of the points of . Note also that if we consider the linear interpolation of the points of , we recover the continuous entropy (1.11).

We also introduce the entropy for a -step random walk to visit (see Lemma B.4):

| (4.2) |

The second identity is due to the fact that the infimum is attained for .

Energy (and truncated energy) of a set of points.

For , let

be the ball in with radius centered at the origin. We can write the random environment in using its ordered statistic: we let be the -th largest value of and its position. Then is a random permutation of and

| (4.3) |

The energy collected by a set and its contribution from the largest weights () are defined by

| (4.4) |

where means that there is some such that , with a slight abuse of notation. Let us also set .

Discrete variational problem.

Let us now define the discrete variational problem

| (4.5) |

We also define the analogous variational problems restricted to the largest weights and beyond the -th largest weight by

| (4.6) | ||||

| (4.7) |

The following result gives an explicit bound on the tail of the (discrete) variational problem. It will be useful to prove that small weights have a negligible contribution to the variational problems, uniformly in . Its proof relies on E-LPP estimates and is very similar to [8, Prop. 2.6]; its proof is included in Appendix A.

Proposition 4.1.

The following hold true:

-

•

There exists a constant , such that for any , , , and ,

(4.8) -

•

There exists a constant , such that for any , , , and ,

(4.9)

Adaptation for trajectories at scale .

We also define entropy arising when considering trajectories at a scale instead of . For and , let us define the -step entropy

| (4.10) |

where is the large deviation rate function for the random walk, see Lemma B.1. Also, we let . Note that if we consider the linear interpolation of the points of , recovers the continuous entropy (1.11).

Let us stress that we have for all , since , cf. Lemma B.1. Then, we can define the analogous variational problems as in (4.5), (4.6) and (4.7), replacing the entropy with . One difference here is that we only consider trajectories at scale : we therefore take (notice also that if has one point outside , recalling that if ). We define

| (4.11) | ||||

| (4.12) | ||||

| (4.13) |

Using that , we get that , and similarly for and . Proposition 4.1 therefore remains valid for the variational problems (4.12)-(4.13), up to a change in the constants.

4.2. Convergence of the discrete variational problem to the continuous one

In this section, we prove that the discrete variational problems (4.5) and (4.11), when properly rescaled, converge to their continuous counterparts (2.2) and (2.1).

Recall the definition (3.1) of , the set of paths staying in (the ball of radius ), and the definition (3.4) of , the contribution to from the largest weights in . We have the following convergences

Proposition 4.2.

Let , let and . Let be such that . Then, for any we have that

| (4.14) |

We also have that, for any fixed ,

| (4.15) |

Finally, by monotonicity, we have almost surely.

We have the analogous statement for the discrete variational problem (4.12).

Proposition 4.3.

Let . We let such that . Then, for any we have that

| (4.16) |

We also have that almost surely.

Notice that the restriction in (4.16) is harmless since we have for all .

Proof of Propositions 4.2 and 4.3.

Let us define for simplicity. We label the points according to the ordered statistics , see (4.3). In the same way, in the ball we label the points of according to the ordered statistic , cf. (3.3). Then, by the Skorokhod representation theorem (cf. [18, Section 9.4], also in the same spirit of Remark 2.1), we have that for any fixed ,

Then, for each , thanks to the continuous mapping theorem, we get that converges to , where is the linear interpolation of (see the definitions (4.4) of and (3.4) of ). We also obtain that converges to . Since the maxima in (4.6) and (4.14) are over finitely many terms (in fact ), we get (4.14). The convergence (4.16) in Theorem 4.3 follows from exactly the same argument taking (here ), and using that converges to .

Finally, (4.15) simply follows from the monotonicity in , and the fact that which is finite almost surely. The limits and also follow by monotonicity. ∎

5. Region A: proof of Theorem 2.2 and Proposition 2.3

In this section, we prove Theorem 2.2. First of all, notice that for any we have

Hence, we get

Since , the terms go to and we therefore only need to prove the result for . In the rest of this section, we will write for simplicity. We only treat the case where for notational clarity; the case where follows in a similar manner.

5.1. Convergence of the rescaled log-partition function

Let us prove Theorem 2.2. Our strategy is based on three steps: Step 1. most of the contribution to comes from some large disorder weights; Step 2. the log-partition function, when restricted to finitely many weights and rescaled by , has a weak limit; Step 3. combine the first two steps to conclude the proof of the convergence.

Let us introduce some notation. Recall the order statistics defined in (4.3). For any , we define, for

| (5.1) | ||||

| (5.2) |

Step 1. For any fixed and , by Hölder’s inequality, we have

so that for any fixed , since the disorder is positive, we get

| (5.3) |

We now show that the last term in (5.3) can be made arbitrarily small compared with by choosing large: this is the content of the following lemma.

Lemma 5.1.

Assume that . For any and any , there are some and some such that for any and we have

Proof.

Notice that for any realization of the range, we have

where we recall the notation (4.4) for . We have used here that any set of points visited by the random walk before time must verify and hence have a -step entropy (recall the definitions (4.1)-(4.2)). We therefore get that

Now, we simply have to use Lemma A.4 (noting that ), which states that for any and any

Fixing large enough so that the upper bound is smaller than (uniformly for ) and then choosing large enough so that , we obtain the conclusion of Lemma 5.1. ∎

Step 2. Once the number of weights is fixed, we can prove the following convergence in distribution.

Proposition 5.2.

For any positive integer and real number , we have the following convergence in distribution

where is defined in (4.16).

Proof.

Let us denote the set of the (random) positions of the largest weights in . Then, we can write

where we used the convention that the points of are ordered, i.e. , and used some abuse of notation in writing . Also, let us note that we use the notation to state that the points in are visited in the correct order by the random walk, and that no other point in is visited. We then have the following lower and upper bounds:

where again we used the conventions that are ordered points in and that we denoted the fact that the points in are visited in the correct order by the random walk. Recalling the definition (4.6) of the discrete variational problem , we can therefore rewrite

| (5.4) |

In view of the convergence in Proposition 4.3, we therefore only have to prove that the upper and lower bounds are negligible. More precisely, since there are only finitely many terms in the infimum (or in the supremum) and since with , we only have to prove that for any distinct indices , the (random) subset of verifies

| (5.5) |

Note that for any fixed , for any we have

The points in are therefore at distance at least from each other, with -probability larger than . Thanks to Lemma B.3 — and to the definition (4.10) of —, this shows that

| (5.6) |

with high -probability. Notice also that and that with high -probability (using Lemma B.4 and that the points in are distant by at least with high -probability). From (5.6), we therefore also get that

with high -probability. This proves (5.5) and concludes the proof. ∎

Step 3. Conclusion. Note that, as stressed in Proposition 4.3, we have almost surely. Due to the continuity in (see Section 3.2) we also have that a.s.

The conclusion of the proof is then just a matter of combining the different steps in the correct order. For any fixed , (i) we choose sufficiently small (in (5.3)) and then so that for any both and are at distance less than from with -probability larger than ; (ii) we fix some large enough so that the conclusion of Lemma 5.1 holds, with . The conclusion then follows by applying Proposition 5.2 to both sides of the inequality (5.3) (by Skorokhod’s representation theorem, cf. Remark 2.1, we can work as if the convergence in Proposition 5.2 is an almost sure convergence). ∎

5.2. Transversal fluctuations: proof of Proposition 2.3

Since the transversal fluctuations are at most , we therefore only have to prove that for any there exists some such that for all large enough

with large -probability conditionally on .

The same proof as above can easily be adapted to show that we have the following convergence in distribution (it can be upgraded to an almost sure convergence by Skorokhod’s representation theorem)

| (5.7) |

where we set , and is defined in (3.1).

This shows in particular, using Skorokhod’s representation theorem (see Remark 2.1), that

| (5.8) |

Noting that a.s., then conditionally on having we can choose small enough so that is negative, with high (conditional) -probability. From the convergence in (5.8), on the event we have that goes to , that is goes to (exponentially fast). This concludes the proof. ∎

6. Region B: proof of Theorem 2.5

In this section we prove Theorem 2.5. Recall that we choose : we denote and by and respectively. Recall that and that with . Define , which turns out to be the end-to-end critical exponent, and note that we have for the range of parameters considered.

Let (this notation is used in the rest of the paper). For any , we split as follows

| (6.1) |

where .

We divide the proof into three parts: Step 1. we show that is small for large with high -probability, which shows that is negligible compared with ; Step 2. we show that , when suitably rescaled, converges in distribution to ; Step 3. we let and we conclude our main result.

The main difference here with respect to Section 5 is the fact that we need to control the partition function with trajectories (we had in the previous section): this brings many additional technical difficulties and makes the first step much more difficult.

6.1. Step 1. Controlling

We prove the following estimate, slightly more general than what we need.

Proposition 6.1.

Suppose that for all , for some constant . There exist positive constants and , such that for any sequence , we can find such that for any we have

Proof.

We partition the interval into blocks

| (6.2) |

and we divide the partition function according to the value of :

| (6.3) |

By applying Cauchy–Schwarz inequality, we have

| (6.4) |

Then, a simple random walk estimate gives that there are some constants such that for all and all

| (6.5) |

To obtain this, we can for instance use a union bound on the different coordinates, to reduce to one-dimensional random walk estimates, for which such an inequality is classical, see e.g. [22].

We formulate the following result in a general manner, since it will also be useful when . We still write , with when and any real number when .

Lemma 6.2.

Assume that and let be a sequence verifying and . Define . For any constant , there exist constants and such that for sufficiently large

| (6.8) |

As a consequence, when , if then letting we get that . Hence, one can choose such that for any we have

| (6.9) |

The proof is analogous to that of Lemma 4.1 in [7]; let us warn the reader that it is quite technical.

Proof of Lemma 6.2.

Let us note that the bound is trivial if . We will therefore assume that for all ; in particular we have .

Let us split into three pieces, that we will control separately. By Hölder’s inequality (using also that ), we have

| (6.10) |

where we defined, for any ,

| (6.11) | ||||

| (6.12) | ||||

| (6.13) |

where is a constant depending on and will be chosen later (it will be of the form for some ). We now deal with the three terms separately.

First term: (6.11).

We want to show that by properly choosing of the form for a well chosen , we have for large enough

| (6.14) |

Let , where is fixed (small enough). We consider the partition function restricted to the largest weights, as follows

| (6.15) |

where is the ordered statistics introduced in (4.3).

Now, since , we have that

| (6.16) |

where we have used Lemma 5.1 in [8] for the last inequality (see (A.12) in Appendix). We now choose ; recall that . In particular, note that for some , and so it goes to infinity as .

Since if has been fixed small enough, we therefore get that with probability larger than we have

| (6.17) |

We stress that on this event we have , and we now turn to . Recall the notation (4.4) of . By Lemma B.4, we have that

(recall that we view as an ordered subset of ). Therefore, recalling the definition (4.6) of the variational problem , we have, setting

| (6.18) |

Then for large enough, using the definition of , we get

| (6.19) |

where is a fixed constant (appearing in (6.14)). Recalling the definition , we therefore get that

| (6.20) |

Then, one simply needs to use Proposition 4.1 to get that the last term is bounded by a constant times . This, together with (6.16), establishes (6.14).

Second term: (6.12).

We now show that there exists some , such that for any and large enough,

| (6.21) |

We again decompose , according to the contribution of different ranges of values in the environment. We fix (appearing in the definition of and above) small enough so that (recall ). Then, for , we set

| (6.22) | ||||

| (6.23) |

where we used the definition of above. Note that , and that each pair has a similar form to , and let us stress that and for any . Now, let be the smallest integer such that , and note that for such we have .

Then, thanks to Hölder’s inequality, we have

| (6.24) |

where we have set

| (6.25) |

Thanks to an union bound we only need to show that for any ,

| (6.26) |

to get (6.21).

By the same argument used for , see (6.16)-(6.17), we get that

| (6.27) |

with probability larger than . Hence, as above, we are reduced to controlling

| (6.28) |

We split the sum in (6.28) at some level (this is needed in (6.30) below) and we use Lemma B.4 to bound the probability for . We get

| (6.29) |

where we have set

We now use Entropic LPP estimates to control the last infimum. We let

where we used the definition (6.23) and the fact that together with the definition . Then, thanks to Theorem A.1 in Appendix, we obtain

so that using the definition of , we end up with

where we have used in the last inequality that (and took small enough). By a union bound, this leads to

| (6.30) |

Moreover, on this event, we get that for large enough

where we used in the last inequality that for some (recall (6.23)), and that goes to infinity. Now using that , we get that for large enough

| (6.31) |

Note also that goes to as : going back to (6.29), we therefore get that on the event considered in (6.30), for large enough we have .

Third term: (6.13)

We now show that there exists a constant such that

| (6.33) |

To bound (6.33) we note that there is some such that for . Therefore, for large enough (so that ), we obtain

| (6.34) |

Note that as soon as (our assumption implies that ). Hence, using also that , we get that

| (6.35) |

where we used that the truncated expectation is bounded by a constant times if , by a constant times if , and by a constant if .

Then by Markov’s inequality and (6.35), we have that

| (6.36) |

It suffices to show that . Since , we get that:

If then

| (6.37) |

because .

If on the other hand , we can choose sufficiently small, such that

| (6.38) |

using that for the third inequality and that for the last inequality. All together, this proves (6.33).

6.2. Step 2: convergence of

We now prove the following convergence.

Proposition 6.3.

Assume that . Then for all we have the following convergence in distribution

where is defined in (4.15).

Once trajectories are restricted to staying in a ball of radius , the proof of the convergence is very similar to the proof in Section 5. We follow the same steps: (i) first we show that most of the contribution to the partition function comes from large disorder weights; (ii) we prove that the log-partition function, when restricted to finitely many weights, converges in distribution; (iii) we send the number of weights to infinity.

Step 2.(i)-a. First of all, we show that we can restrict the partition function to weights . Recall the notations in (6.13), and define analogously by replacing with inside (6.13); take . For any , by Hölder’s inequality, we have

| (6.39) |

and by applying Hölder’s inequality to , we also have for any

| (6.40) |

Note that if and large enough, we have

so that we can replace and by and respectively, where

| (6.41) |

We need to control the upper bound for (6.39) and the lower bound for (6.40) (note that ). Now notice that adapting (6.36), we easily get that for any , any

which goes to as (the proof of (6.35) is carried out for but it is easily adapted to any ). For , a slight modification in (6.34)-(6.35) is needed. Note that we have , which gives an extra term in (6.35) for and it follows that

Notice also that thanks to (6.21), we also have that for any

Using Hölder’s inequality as in (6.39) and (6.40), we are therefore reduced to showing that for any we have the following convergence in distribution

| (6.42) |

Step 2.(i)-b. We now show that we can restrict the partition function to a finite number of weights. Analogously to Section 5 (see (5.1)-(5.2)), we define for any ,

| (6.43) | ||||

| (6.44) |

where we consider the order statistics in the (discrete) ball of radius . Recall that .

Thanks to Hölder’s inequality, we get that for any , analogously to (5.3), then for large enough we have

| (6.45) |

with probability going to as (more precisely on the event . Recall (6.16) and in Proposition 4.3). We now prove the analogous of Lemma 5.1 to show that the last term is negligible.

Lemma 6.4.

For any and any , we have

Proof.

Note that we easily have, as in the calculation leading to (6.18),

| (6.46) |

Then

Note that since with fixed, the first term goes to as (recall ). For the second term, using that we get that for any

where the constant depends on . Then, using Proposition 4.1-(4.9), provided that is large enough so that , we get

for some exponent . This concludes the proof of Lemma 6.4. ∎

Step 2.(ii). Once the number of weights is fixed, we can prove the following convergence in distribution. The proof is identical to that of Proposition 5.2 (replacing with ) and is omitted.

Proposition 6.5.

6.3. Step 3: letting

Going back to (6.1), the conclusion of the convergence in Theorem 2.5 simply follows from Step 1 (Proposition 6.1) and Step 2 (Proposition 6.3). Indeed, thanks to Proposition 6.1, we get that if has been fixed large enough, then with probability we have for large enough

Using Proposition 6.3 and noting that a.s. and then letting concludes the proof of (2.1) (recall that converges to as , by monotonicity).

6.4. Transversal fluctuations

Let us first prove that the transversal fluctuations are at least of order , analogously to what is done in Section 5.2. Notice that for any we have thanks to Proposition 6.3 and (2.1) (using Skorokhod’s representation theorem, cf. Remark 2.1)

| (6.47) |

Since we have and a.s., we can choose small enough so that is negative with high -probability. From (6.47), on the event we have that goes to : this concludes the proof that transversal fluctuations are at least of order .

Then we prove that the transversal fluctuations are at most of order . We have that

The second term above converges to , which is positive a.s.. For the first term, we have that with -probability larger than by Proposition 6.1. Therefore, vanishes exponentially fast with -probability close to for small enough , which concludes the result.

7. Region C: proof of Theorems 2.9

We will prove the result in the case . We start with the case before we turn to the case . We again use the notation for .

7.1. The case

We first focus on the convergence (2.7) of Theorem 2.9. For simplicity, we treat the case where decays at most polynomially; the case where decays faster (and thus ) is even simpler. Note that the condition implies in particular that , and recall the definition (2.5) of in dimension .

To simplify the notation, let us suppose that and observe that the convergence (2.7) is equivalent to

| (7.1) |

since both imply that converges to in probability.

Step 1. Truncation of the environment. Let us set

| (7.2) |

where and let us define the truncated environment

| (7.3) |

Let us also define . The next lemma compares the partition function with its counterpart with the truncated environment .

Lemma 7.1.

Let . Assume that for some constant . Then for any , we have that in -probability.

Proof.

First, we show that we can reduce the partition function to trajectories with transversal fluctuations at most . Assume that , with , then for any

| (7.4) |

This result is identical to Proposition 6.1, replacing with (so is replaced with ): the proof is identical and relies on Lemma 6.2 (in which we can take ), so we omit it. Thanks to (7.4), we can therefore choose a sequence going to infinity (let us take ) in order to get that for any , goes to in probability.

On the other hand, using Cauchy-Swartz inequality we also have that

| (7.5) |

Now, since , (see Lemma C.1). In particular, since , we get that , so goes to as since . Also, the last probability in (7.5) is bounded by . By Markov’s inequality, we therefore get that goes to in probability, using again that .

Step 2. Convergence of the partition function with truncated environment. To conclude the proof of Theorem 2.9-(2.7), and in view of (7.1) and Lemma 7.1 (recall we assumed that decays at most polynomially), we simply need to show the following lemma. For simplicity, let us assume that and let us denote the centering term in Theorem 2.9-(2.7); note that (cf. Remark 2.4) . Recall the definition (2.5) of , and recall that we have set for , for and for .

Lemma 7.2.

Assume that . If , then we have the following convergence in distribution

| (7.8) |

If and , then we have .

Remark 7.1.

We included here the result for since the proof is identical to that of (7.8); this will be useful to treat the case .

As a preliminary to the proof of Lemma 7.2, let us collect some important estimates. Thanks to Lemma C.1, we get that and when and when . In particular, we have

| (7.9) |

Note that (7.9) implies that .

Also, define , which will be used in both lemmas. Note that and that thanks to Lemma C.1, we get as for

| (7.10) |

In fact, we have that when . The bounds (7.9)-(7.10), combined with the fact that , will be used extensively throughout the proof.

Proof of Lemma 7.2.

Note that for any . Writing this with so that , we expand the product in the partition function as follows:

| (7.11) |

where we set

| (7.12) |

where means that the points are visited in this given order; in particular, we do not have the combinatorial term .

We now control all terms, starting with .

Last term in (7.11). We show that converges in probability to zero. Since , we only need to control the second moment of . Because the are independent, we easily get that

| (7.13) |

Now, using the fact that and Markov’s property, we get

where we also used that goes to , as seen above. We denote . Then, we have as , as outlined in Lemma B.5 in the appendix. Using the bound (7.10) on , we conclude that by ,

| (7.14) |

This readily goes to as .

First term in (7.11). We now show that

| (7.15) |

Let us start with the case . Lemma C.1 gives in that case that . Hence, we get

which goes to as . Indeed, if , we have that : in dimension we get that which goes to since ; in dimension , using that we get that which also goes to since . If , we simply use that , which goes to since . Additionnally, recalling that , we have

where we expanded to get the first inequality (recall that goes to ), and used that in dimension and in dimension (see [26]), together with the definition of . This proves (7.15) in the case .

In the case (in particular ), we use (7.9) to get that

which goes to as , because . This proves (7.15) in the case .

Second term in (7.11). Let us rewrite it as

| (7.16) |

The second term in (7.16) goes to zero in probability. Indeed, it is centered in expectation, and its second moment is bounded by

Using that as (cf. Lemma B.5) and that , see (7.9) and (7.10), this is bounded by a constant times . If this is bounded by so this goes to ; if this is bounded by , so this also goes to , as seen above.

We now rewrite the first term in (7.16) as

| (7.17) |

and we now show that the second term goes to in probability.

If (), we control the expectation of its absolute value. Using that and recalling that , we can perform a Taylor expansion to get that

where we used that , together with a similar bound on , see (7.9). Therefore, the expectation of the absolute value of the second term in (7.17) is bounded by a constant times : this goes to as , thanks to the condition . By Markov’s inequality, the second term in (7.17) goes to in probability.

If , since the expectation of the second term in (7.17) is , we control its second moment: by independence of the , it is equal to

where we have used that , see Lemma B.5. Now, we can use the same Taylor expansion as above, to get that

where we used here that as and that is bounded by if and by a constant if . This shows that the variance of the second term in (7.17) goes to , so this term goes to in probability.

All together, combining (7.11) with (7.14)-(7.15) and (7.16)-(7.17), we have shown that

It therefore only remains to show that

| (7.18) |

Note that in Lemma 7.2, when and we used a centering equal to instead of . This is not an issue since in that case we have that goes to as .

7.2. The case

Note that this regime is nonempty only for . Also, since , we have . Let us stress that, similarly as (7.1) above, the convergence (2.8) is equivalent to the convergence in distribution

| (7.19) |

The steps are the same as in Section 7.1. The case of the dimension is very similar, but some adaptations are needed in dimension .

Step 1. Truncation of the environment. Let us set

| (7.20) |

where . We again define the truncated environment and we set . The next lemma is analogous to Lemma 7.1.

Lemma 7.3.

Let . Assume that for some constant . Then for any , we have that:

-

(i)

if , in -probability;

-

(ii)

if , in -probability.

Before we start the proof, let us stress that Lemma C.1 gives some estimates on : since , we have

| (7.21) |

Proof.

In the case of dimension , the proof is identical to that of Lemma 7.1: the only difference here is that we do not have . Instead, we use (7.21) instead which gives that goes to as ; this was used to bound (7.5).

We therefore focus on the case of dimension ; the idea of the proof is identical, with some adaptation. First of all, analogously to (7.4), we get that for any sequence

| (7.22) |

Again, this is identical to Proposition 6.1, replacing with : in particular, this relies on Lemma 6.2 in which we can take . Therefore, choosing a sequence (we take ), we get that goes to in probability.

Then, as in (7.5), we have that

| (7.23) |

The main difference here is that we cannot use the bound since we do not have as , see (7.21). However, we may use the fact that is of the order to obtain that with high -probability. More precisely, using that (see e.g. [16, Eq. (5.3.39)]) we have that, for a sufficiently large

| (7.24) |

where we used [16, Thm. 8.5.1] for the last inequality. We therefore get that

Now, thanks to (7.21), we get that as . Hence, from (7.23), we get that

so that in -probability thanks to Markov’s inequality.

Step 2. Convergence of the partition function with truncated environment. To conclude the proof of Theorem 2.9-(2.8), and in view of (7.19) and Lemma 7.3, it remains to prove the following lemma. (In dimension , we need to assume that decays slower than any power of , but this does not hide anything deep; one simply needs to use a more restrictive truncation, but this actually simplifies many of the arguments so we do not treat this case.)

Lemma 7.4.

Let . If then we have the following convergence in distribution

Proof.

We use the same notation as in Step 2 of Section 7.1. Defining , and using a polynomial chaos expansion similar to (7.11), we get

| (7.26) |

where we defined as in (7.12). We first prove that the last term is negligible: the computation in follows closely the computations (7.13)–(7.14), while dimension is more delicate. In the second part of the proof we show that the first two terms give the main contribution to the convergence. This part is quite technical and we split it into three steps.

Last term in (7.26). Let us prove that goes to in probability.

We start with the case of dimension , which we essentially already treated. Reasoning as in (7.13)–(7.14), we computed the second moment of in the case : we have that

| (7.27) |

where we bounded , used that in dimension (see Lemma B.5) and the bound (7.10). Since , we obtain

| (7.28) |

This term goes to , which concludes the proof in the case of dimension .

Turning to the case of dimension , we need to be more careful: we cannot simply bound by since we do not have anymore. The calculation of in (7.13) remains valid. Then, decomposing the expectation according to whether or not, we obtain

| (7.29) |

where for the last inequality we used that together with Cauchy–Schwarz inequality. Now, we have that (recall (7.21)) and also that if has been fixed large enough, thanks to (7.24). Hence, summing (7.29) over and using Markov’s property, we finally get that

All together, going back to (7.13), we obtain that when the bound (7.27) is replaced with

Now, we have that by Lemma C.1, that by Lemma B.5 and that by [16, Eq. (5.3.39)]. Using that , we obtain

| (7.30) |

and note that . This term goes to , which concludes the proof when .

First terms in (7.26). We can rewrite these terms as

| (7.31) | ||||

where we used that for the last identity. Let us denote , and the three terms in (7.31). We show that the first two terms are negligible.

Term I. For the first term in (7.31), let us first treat the case of dimension , which is simpler. Using that and , a Taylor expansion gives that it is bounded by a constant times . Hence, using that , we get that

where we used that in dimension . This goes to as .

The case of dimension is a bit more delicate. On the event , we can again use a Taylor expansion, since , so that the term inside the expectation is bounded in absolute value by a constant times . On the event , we bound the absolute value of the term inside the expectation by . We therefore get that

where we used (7.24) for the last inequality. Since , we get that

| (7.32) |

which goes to as , noticing that , and .

Term II. We prove that goes to in probability, by controlling its second moment. Since the are centered and independent, we have

| (7.33) |

We start with the simpler case of dimension . Using that and recalling the definition , we get that

where we used the bounds (7.9)-(7.10) together with the fact that in dimension , see Lemma B.5. Hence, using also that we get that

which goes to as .

In the case of dimension , we proceed as above. Writing and decomposing according to whether we have or not, we get similarly to (7.29)

Summing over and using the bound (7.24) together with and , we get from (7.33) that

For the second inequality, we used the bounds (7.9)-(7.10) (and also that ) and that , see Lemma B.5. Since , we get that

| (7.34) |

which goes to as , using that

Term III. We show the following lemma to control the third term in (7.31).

Lemma 7.5.

Proof of Lemma 7.5.

To prove (7.35), we adapt the method developed in [19, Thm. 1.4]. We consider only the case ; the case can be dealt with similarly, one simply needs to keep track of the dependence in in all estimates — note also that we have as . Also, for , we use the notation .

We prove the convergence of . As in Equation (39) in [19], we fix , , and we define . Recall the definition of in (7.20). We use the following decomposition of :

| (7.36) |

We control each term separately: the first two terms bring the main contribution; we show that the last three terms can be made arbitrarily small by taking small or large.

st term in (7.36). We split the term into

| (7.37) |

For the first term we partition into rectangles with diameter , where . By denoting this partition , a patch of and the center of , we can write the first term above as

| (7.38) |

where we also used that (with by convention when ) and , see (2.4); here denotes errors that are negligible as for fixed .