Optimal reinsurance problem under fixed cost and exponential preferences

Abstract

We investigate an optimal reinsurance problem for an insurance company facing a constant fixed cost when the reinsurance contract is signed. The insurer needs to optimally choose both the starting time of the reinsurance contract and the retention level in order to maximize the expected utility of terminal wealth. This leads to a mixed optimal control/optimal stopping time problem, which is solved by a two-step procedure: first considering the pure-reinsurance stochastic control problem and next discussing a time-inhomogeneous optimal stopping problem with discontinuous reward. Using the classical Cramér-Lundberg approximation risk model, we prove that the optimal strategy is deterministic and depends on the model parameters. In particular, we show that there exists a maximum fixed cost that the insurer is willing to pay for the contract activation. Finally, we provide some economical interpretations and numerical simulations.

Keywords: Optimal Reinsurance; Mixed Control Problem; Optimal Stopping; Transaction Cost.

MSC Classification codes: 93E20, 91B30, 60G40, 60J60.

1. Introduction

Insurance business requires the transfer of risks from the policyholders to the insurer, who receives a risk premium as a reward. In some cases, it could be convenient to cede these risks to a third party, which is the reinsurance company. From the operational viewpoint, a risk-sharing agreement helps the insurer reducing unexpected losses, stabilizing operating results, increasing business capacity and so on. By means of a reinsurance treaty, the reinsurance company agrees to idemnify the primary insurer (cedent) against all or part of the losses which may occur under policies which the latter issued. The cedent will pay a reinsurance premium in exchange for this service. Roughly speaking, this is an insurance for insurers. When subscribing a reinsurance treaty, a natural question is to determine the (optimal) level of the retained losses.

Optimal reinsurance problems have been intensively studied by many authors under different criteria, especially through expected utility maximization and ruin probability minimization, see for example [De Finetti, 1940], [Bühlmann, 1970], [Gerber, 1969], [Irgens and Paulsen, 2004], [Brachetta and Ceci, 2019] and references therein.

The main novelty of this article is that subscription costs are considered. In practice, when the agreement is signed, a fixed cost is usually paid in addition to the reinsurance premium. This aspect has not been investigated by nearly all the studies, except for [Egami and Young, 2009] and [Li et al., 2015]. In the former work the authors discussed the reinsurance problem subject to a fixed cost for buying reinsurance and a time delay in completing the reinsurance transaction. They solved the problem considering a performance criterion with linear current reward and showed that it is optimal to buy reinsurance when the surplus lies in a bounded interval depending on the delay time. In the latter paper, under the criterion of minimizing the ruin probability, the original problem is reduced to a time-homogeneous optimal stopping problem. In particular, the authors show that the fixed cost forces the insurer to postpone buying reinsurance until the surplus process hits a certain level.

Hence the presence of a fixed cost is closely related to the possibility of postponing the subscription of the reinsurance agreement. This, in turn, involves an optimal stopping problem, which is attached to the optimal choice of the retention level, which is a well known stochastic control problem. The novelty of our paper consists in considering this mixed stochastic control problem under the criterion of maximizing the expected utility of terminal wealth. The strategy of the insurance company consists of the retention level of a proportional reinsurance and the subscription timing. When the contract is signed, a given fixed cost is paid and the optimal retention level is applied. We use a diffusion approximation to model the insurer’s surplus process (see [Schmidli, 2018]). The insurance company has exponential preferences and is allowed to invest in a risk-less bond.

As already mentioned, this setup leads to a combined problem of optimal stopping and stochastic control with finite horizon, which we will solve by a two-step procedure. First, we provide the solution of the pure reinsurance problem (with starting time equal to zero). Next, we discuss an optimal stopping time problem with a suitable reward function depending on the value function of the pure reinsurance problem. Differently to [Egami and Young, 2009] and [Li et al., 2015], the associated optimal stopping problem turns out to be time-inhomogeneous and with discontinuous stopping reward with respect to the time. We provide an explicit solution, also showing that the optimal stopping time is deterministic. Moreover, we find that only two cases possible, depending on the model parameters. When the fixed cost is greater than a suitable threshold (whose analytical expression is available), the optimal choice is not to subscribe the reinsurance; otherwise, the insurer immediately subscribes the contract.

The paper is organized as follows. In Section 2, we describe the model and formulate the problem as a mixed stochastic control problem, that is a problem which involves both optimal control and stopping. In Section 3 we discuss the pure reinsurance problem (without stopping) by solving the associated Halmilton-Jacobi-Bellman equation. Section 4 is devoted to the reduction of the original (mixed) problem to a suitable optimal stopping problem, which is then investigated in Section 5. Here we provide a Verification Theorem and we solve the associated variational inequality. In Section 6 we give the explicit solution to the original problem and we discuss some economic implications of our results. Finally, in Section 7 some numerical simulations are performed in order to better understand the economic interpretation of our findings.

2. Problem formulation

2.1. Model formulation

Let be a finite time horizon and assume that is a complete probability space endowed with a filtration satisfying the usual conditions.

Let us denote by the surplus process of an insurance company. There is a wide range of risk models in the actuarial literature, see for instance [Grandell, 1991] and [Schmidli, 2018]. In the Cramér-Lundberg risk model the claims arrival times are described by the sequence of claims arrival times , with -a.e. , while the corresponding claim sizes are given by . In particular, the number of occurred claims up to time is equal to

and it is assumed to be a Poisson process with constant intensity , independent of the sequence . Moreover, are i.i.d. random variables with common probability distribution function , , having finite first and second moments denoted by and , respectively. In this context the surplus process is given by

| (2.1) |

where is the initial capital and denotes the gross risk premium rate. We can show that for any

In this paper we use the diffusion approximation of the Cramér-Lundberg model (2.1), see for example [Grandell, 1991]. Precisely, we assume that the surplus process follows this stochastic differential equation (SDE):

where is a standard Brownian motion, and denotes the insurer’s net profit, that is . In particular, under the expected value principle we have that and hence , with representing the insurer’s safety loading.

We allow the insurer to invest her surplus in a risk-free asset with constant interest rate :

hence the wealth process evolves according to

| (2.2) |

The explicit solution of the SDE (2.2) is given by the following equation:

| (2.3) |

Now let denote an -stopping time. At time the insurer can subscribe a proportional reinsurance contract with retention level , transferring part of her risks to the reinsurer. More precisely, represents the percentage of retained losses, so that means full reinsurance, while is equivalent to no reinsurance. In order to buy a reinsurance agreement, the primary insurer pays a reinsurance premium . When the reinsurance contract is signed at time , the Cramér-Lundberg risk model (2.1) is replaced by the following equation:

Under the expected value principle we have that , , with the reinsurer’s safety loading satistying (preventing the insurer from gaining a risk-free profit).

Let us denote by the reserve process in the Cramér-Lundberg approximation associated with a given reinsurance strategy when the reinsurance contract is signed at time . Following [Eisenberg and Schmidli, 2009], under the expected value principle, follows

| (2.4) |

where denotes the reinsurer’s net profit. We set (non-cheap reinsurance). The wealth process under the strategy evolves according to this SDE:

| (2.5) |

which admits this explicit representation:

| (2.6) |

We assume that a constant fixed cost is paid when the reinsurance contract is subscribed. The insurer decides when the reinsurance contract starts and which retention level is applied. Hence the insurer’s strategy is a couple , with . Let be the indicator process of the contract starting time. For -a.s. , the total wealth associated with a given strategy is given by

Equation (2.7) can be written more explicitly as

| (2.9) |

In our setting the null reinsurance corresponds to the choice , -a.s., to which we associate the strategy and

2.2. The utility maximization problem

The insurers’ objective is to maximize the expected utility of the terminal wealth:

| (2.10) |

where is the utility function representing the insurer’s preferences and the class of admissible strategies (see Definition 2.1 below).

We focus on CARA (Constant Absolute Risk Aversion) utility functions, whose general expression is given by

where is the risk-aversion parameter. This utility function is highly relevant in economic science and particularly in insurance theory. Indeed, it is commonly used for reinsurance problems (e.g. see [Brachetta and Ceci, 2019] and references therein).

The optimization problem is a mixed optimal control problem. That is, the insurer’s controls involve the timing of the reinsurance contract subscription and the retention level to apply.

Definition 2.1 (Admissible strategies).

We denote by the set of admissible strategies , where is an -stopping time such that and is an -predictable process with values in . Let us observe that the null strategy is included in . When we want to restrict the controls to the time interval , we will use the notation .

Proposition 2.1.

Let , then

Proof.

3. The pure reinsurance problem

In order to have a self-contained article, in this section we briefly investigate a pure reinsurance problem, which corresponds to the problem (2.10) with fixed starting time . Precisely, we deal with

where denotes the class of admissible strategies , which are all the -predictable processes with values in . Let us denote by the value function associated to this problem, that is

| (3.1) |

with denoting the restriction of to the time interval and denotes the process satisying equation (2.5) with initial data . It is well known that the value function (3.1) can be characterized as a classical solution to the associated Hamilton-Jacobi-Bellman (HJB) equation:

| (3.2) |

where, using equations (2.4) and (2.5), the generator of the Markov process is given by

Under the ansatz , the HJB equation reads as

where

Solving the minimization problem we find the unique minimizer:

Under the additional condition

| (3.3) |

simplifies to

| (3.4) |

Using this expression we readily obtain that

| (3.5) |

By classical verification arguments, we can verify that the value function given in (3.1) takes this form:

| (3.6) |

and, under the condition (3.3), equation (3.4) provides an optimal reinsurance strategy.

4. Reduction to an optimal stopping problem

We can show that the mixed stochastic control problem (2.11) can be reduced to an optimal stopping problem. Let us denote by is the set of -stopping times such that .

Theorem 4.1.

5. The optimal stopping problem

In this section we discuss the optimal stopping problem (4.1):

Let us observe that

while choosing and in the right hand side of (4.1), we get that

| (5.1) |

respectively.

Now denote by the Markov generator of the process :

| (5.2) |

with .

Remark 5.1.

From the theory of optimal stopping (see, for instance [Øksendal, 2003]), when the cost function is continuous and the value function

is sufficiently regular, it can be characterized as a solution to the following variational inequality:

| (5.3) |

This is a free-boundary problem, whose solution is the function and the so-called continuation region, which is defined as

| (5.4) |

Moreover, it is known that the first exit time of the process from the region

provides an optimal stopping time.

In our optimal stopping problem (4.1), the cost function is

which is not continuous on , hence the classical theory on optimal stopping problems does not directly apply.

In view of the preceding remark, we now prove a Verification Theorem which applies to our specific problem.

Theorem 5.1 (Verification Theorem).

Let be a function satisfying the assumptions below and (the continuation region) be defined by

| (5.5) |

Suppose that the following conditions are satisfied.

-

1.

There exists such that .

-

2.

, is w.r.t in and , separately, and w.r.t. ;

-

3.

and ;

-

4.

is a solution to the following variational inequality

(5.6) -

5.

the family is uniformly integrable.

Moreover, let the first exit time from the region of the process , that is

with the convention if the set on the right-hand side is empty.

Then on and is an optimal stopping time for problem (4.1).

Proof.

For any let us take the sequence of stopping times such that . We first prove that,

| (5.7) |

Due to the specific form of the continuation region we have two cases. If , since , applying Dynkin’s formula111Notice that we use a localization argument, so that is the first exit time of a bounded set and, as s consequence, is not required to have a compact support (see [Øksendal, 2003, Theorem 7.4.1]). we get that for any arbitrary stopping time

Now letting in (5.7), recalling that and using Fatou Lemma we get that

hence , . To prove the opposite inequality we consider four different cases.

-

1.

If the stopping region is not empty, that is , we know that , hence , which implies and is optimal for problem (4.1).

-

2.

If the stopping region is not empty, for , we have that , otherwise by continuity of both the functions if (or ) the same inequality holds in a neighborhood of which contradicts that , . Then and is optimal for problem (4.1).

-

3.

If the continuation region is not empty, that is , , repeating the localization argument with the stopping time , we get

as a consequence and is optimal for problem (4.1).

-

4.

Finally, for by assumption , , is optimal for problem (4.1) and this concludes the proof.

∎

Lemma 5.1.

Let as defined in equation (3.10). The families and are uniformly integrable.

Proof.

Recalling that by (3.7), we have that , hence the statement follows by the uniformly integrability of the family

It is well known that if for any arbitrary and any stopping time

then the proof is complete. To this end, we observe that

∎

The guess for the continuation region given in the assumption of the Verification Theorem follows by the next result.

Lemma 5.2.

The set

| (5.8) |

is included in the continuation region, that is

Moreover, the following equation holds:

where

| (5.9) |

In particular, only three cases are possible, depending on the model parameters:

-

1.

if

then and , so that , implying that ;

-

2.

if

then and ; in this case ;

-

3.

if

then and , so that .

Proof.

First let us observe that and the family is uniformly integrable by Lemma 5.1. Now choose , let be a neighborhood of with , where denotes the first exit time of from . Then by Dynkin’s formula

Hence and .

Next, recalling (5.2), we have that

so that if and only if

| (5.10) |

that is, using (3.5),

Using a change of variable , we can rewrite the inequality as

Since the associated equation admits two different solutions, so that the inequality (5.10) is satisfied by

Recalling (3.3), we can verify that

so that the inequality reads as

Depending on the model parameters, we can see that only the three cases above are possible. Equivalently, if and only if . ∎

Remark 5.2.

We need the following preliminary result to provide an explicit expression for the value function of the problem (4.1).

Lemma 5.3.

The function , , with any positive constant and as given in equation (3.10), is a solution to the PDE

, .

In particular, is a solution to the PDE with boundary condition .

Proof.

Using the ansatz , we can reduce the PDE to the following equation:

which is equivalent to this ODE:

where the function is given in (3.9).

Since the solution of the ODE is , we get the expression of as above.

Finally, setting , satisfies the PDE above with the terminal condition .

∎

Before proving the main result of this section, which is Theorem 5.2, we compare , given in (3.10), with .

Lemma 5.4.

Let

| (5.11) |

then we distinguish two cases:

-

1.

if , then ;

-

2.

if , then there exists such that and .

Proof.

Let us observe that the inequality writes as

that is

We distinguish three cases:

-

(i)

when , we have that by Remark 5.2 and it easy to verify that is increasing in , while it is decreasing in . Hence, it takes the maximum value at . As a consequence, if we have that , being .

Otherwise, if there exists such that , that is , and , that is ;

-

(ii)

when , by Lemma 5.2 we get that is increasing in and we can repeat the same arguments as in the previous case to distinguish the two casese and , obtaining the same results;

-

(iii)

when , by Remark 5.2 we know that is decreasing in , so that , that is , . Moreover, in this case .

Summaring, we obtain our statement. ∎

We now prove some properties of the continuation region.

Proposition 5.1.

Let

| (5.12) |

Then we distinguish two cases:

-

1.

if , then ,

-

2.

if , then , where is the unique solution to equation

Proof.

We apply Lemma 5.4. In Case 1, we have that , that is . In Case 2, we have that , which implies , and this concludes the proof. ∎

Now we are ready for the main result of this section.

Theorem 5.2.

Let be given in (5.11). The solution of the optimal stopping problem (4.1) takes different forms, depending on the model parameters. Precisely, we have two cases:

-

1.

if , then the continuation region is , the value function is

and is an optimal stopping time;

-

2.

if , then , where is the unique solution to , the value function is

(5.13) and , given by

(5.14) is an optimal stopping time.

Proof.

We prove the two cases separately, applying Theorem 5.1 in each one.

Case 1

The continuation region is by Proposition 5.1, hence assumption 1 of Theorem 5.1 is fulfilled. Moreover, . Observing that

the assumption 2 of Theorem 5.1 is clearly matched. The assumption 3 is implied by Lemma 5.4. Moreover, the variational inequality (5.6) (assumption 4) is fulfilled by Lemma 5.3. Finally, by Lemma 5.1 the last condition in Theorem 5.1 is fulfilled.

Case 2

clearly satisfies the first assumption of Theorem 5.1. Taking

observing that Lemma 5.4 ensures the existence of such that when , the smoothness conditions of the second assumption are matched. Moreover, according to Lemma 5.4, and the assumption 3 is fulfilled. That the variational inequality (5.6) is satisfied by is a consequence of the results of Section 3 and of Lemma 5.3. Finally, Lemma 5.1 implies the fifth assumption of Theorem 5.1 and the proof is complete. ∎

6. Solution to the original problem

As a direct consequence of the results obtained in the previous section and Theorem 4.1, we provide an explicit solution to the optimal reinsurance problem under fixed cost given in (2.11).

Theorem 6.1.

Let us define

| (6.1) |

Two cases are possible, depending on the model parameters:

Proof.

Let us briefly comment the two cases of Theorem 6.1. Case 1 corresponds to no reinsurance. That is, the insurer is not willing to subscribe a contract at any time of the selected time horizon. Besides the insurer, this result is relevant for the reinsurance company. We have proven that there exists a threshold (see equation (6.1)), which represents the maximum initial cost that the insurer is willing to pay to buy reinsurance. If the reinsurer chooses a subscription cost higher than , then the insurer will not buy protection from her.

In Case 2, at any time , the insurer immediately subscribes the reinsurance agreement if the time instant has not passed, applying the optimal retention level from that moment on; otherwise, if , no reinsurance will be bought.

We notice that it is never optimal to wait for buying reinsurance. That is, it is convenient either to immediately sign the contract, or not to subscribe at all.

In particular, at the starting time , given an initial wealth , we have these cases:

-

1.

if , then , that is no reinsurance is purchased;

-

2.

if , then , that is the optimal choice for the insurer consists in stipulating the contract at the initial time, selecting the optimal retention level (as in the pure reinsurance problem).

By the expression (6.1) we can show that is increasing with respect to and , while it is decreasing with respect to . More details will be given in the next section by means of numerical simulations.

Another relevant result for the reinsurance company is the following.

Proposition 6.1.

For any fixed cost there exists (depending on ) such that

-

1.

if , then

and , that is no reinsurance is purchased;

- 2.

Proof.

Following Theorem 6.1 and its proof, we can write the condition as

To simplify our computations, let us consider this inequality for any . The discriminant must be positive, otherwise the existence of in Theorem 6.1 is not guaranteed anymore. The solutions of the associated equations are

Since

only is relevant because of the condition (3.3). That is a consequence of the existence of in Theorem 6.1. If was not positive, then for any value of and this would contradict Theorem 6.1. Setting concludes the proof. ∎

The last result is interesting for the reinsurer. In Section 3 we have already stated that the condition (see equation (3.3)) is required in order that the reinsurance agreement is desirable. In presence of a fixed initial cost, now we know that there exists a threshold , which is smaller than , such that the insurer will never subscribe the contract if .

Remark 6.1.

Recalling that (see Section 2, we can give a deeper interpretation of the previous result. Indeed, we have proven the existence of a maximum safety loading , which cannot be exceeded by the reinsurer, otherwise the reinsurance contract will not be subscribed.

7. Numerical simulations

In this section we use some numerical simulations in order to further investigate the results obtained in Section 6. Unless otherwise specified, all the simulations are performed according to the parameters of Table 1 below.

| Parameter | Value |

|---|---|

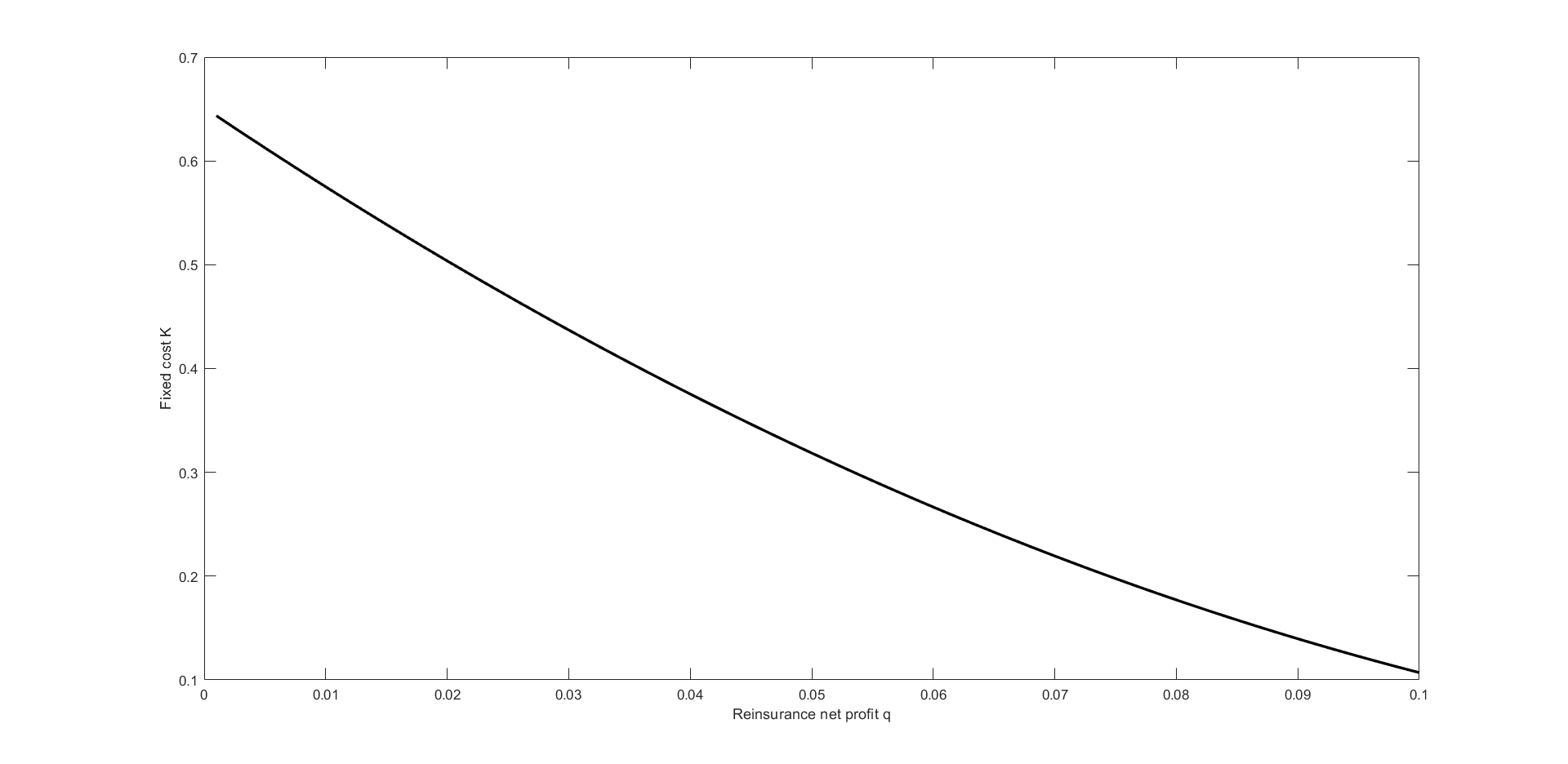

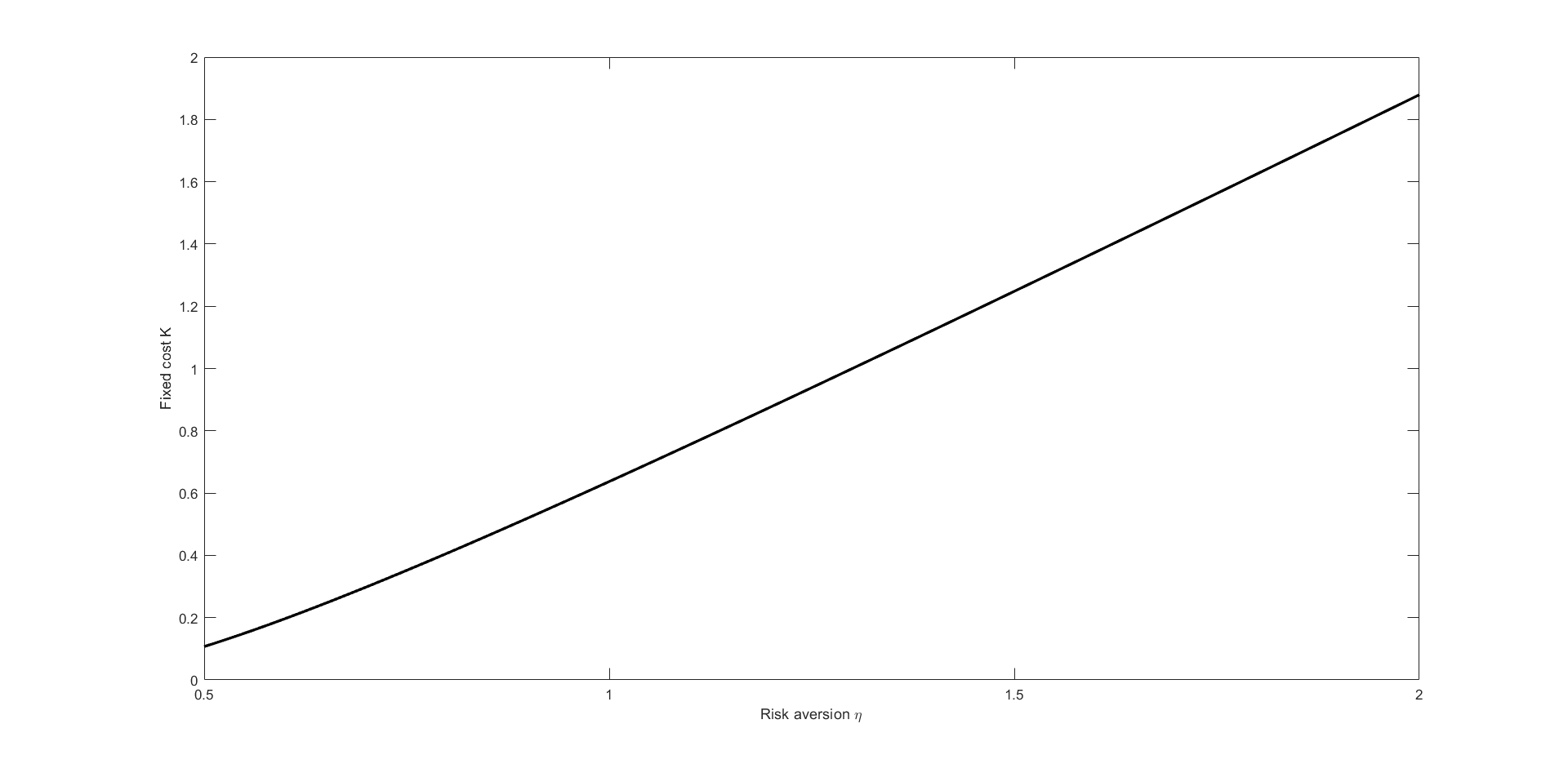

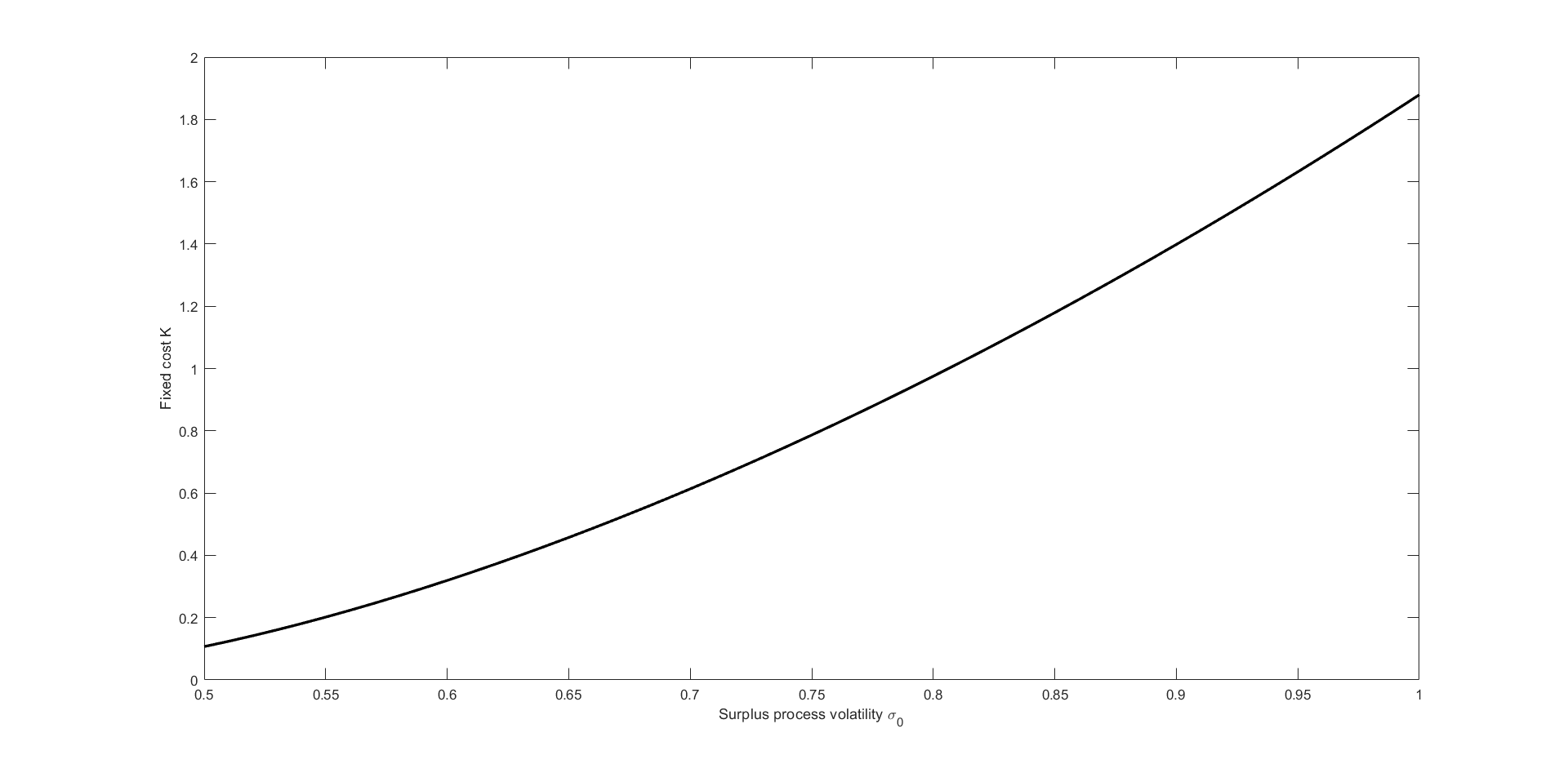

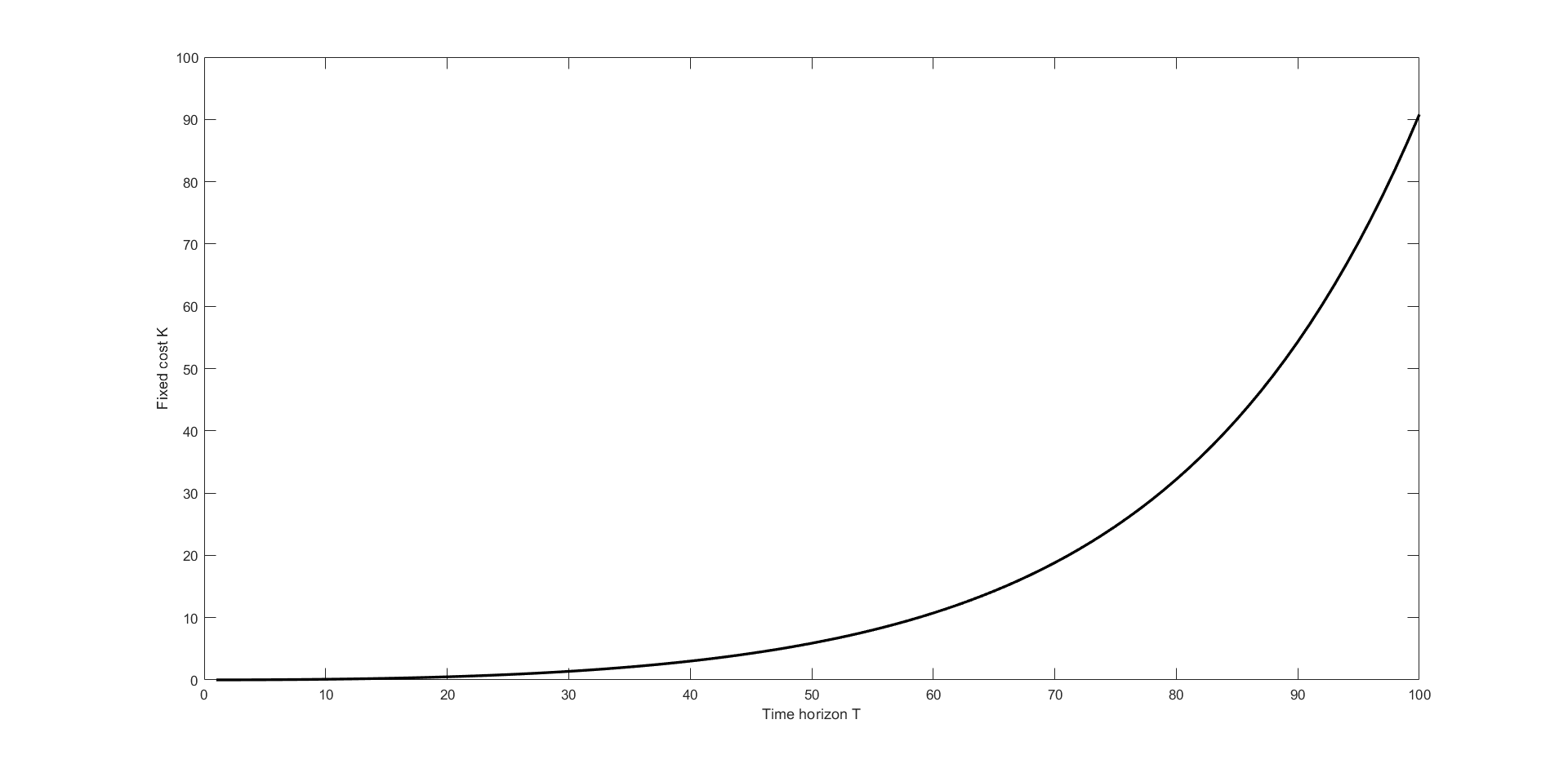

We have previously illustrated how the threshold in equation (6.1) is relevant for the insurer as well as for the reinsurer. Figure 1 shows how this threshold is influenced by the model parameters. As expected, if the reinsurer increases her net profit (for example, increasing the safety loading), then the fixed cost should decrease, see Figure 1a. When the insurer is more risk averse, she is willing to pay a higher fixed cost, see Figure 1b. The same applies when the potential losses increase, that is is high, as in Figure 1c. Figure 1d shows that the more the time horizon, the higher will be .

References

- [Brachetta and Ceci, 2019] Brachetta, M. and Ceci, C. (2019). Optimal proportional reinsurance and investment for stochastic factor models. Insurance: Mathematics and Economics, 87:15 – 33.

- [Bühlmann, 1970] Bühlmann, H. (1970). Mathematical Methods in Risk Theory. Springer-Verlag.

- [De Finetti, 1940] De Finetti, B. (1940). Il problema dei “pieni”. G. Ist. Ital. Attuari, 11:1–88.

- [Egami and Young, 2009] Egami, M. and Young, V. R. (2009). Optimal reinsurance strategy under fixed cost and delay. Stochastic Processes and their Applications, 119(3):1015 – 1034.

- [Eisenberg and Schmidli, 2009] Eisenberg, J. and Schmidli, H. (2009). Optimal control of capital injections by reinsurance in a diffusion approximation. Blätter der DGVFM, (30):1–13.

- [Gerber, 1969] Gerber, H. (1969). Entscheidungskriterien für den zusammengesetzten Poisson-Prozess. Schweiz. Verein. Versicherungsmath. Mitt., 69:185–228.

- [Grandell, 1991] Grandell, J. (1991). Aspects of risk theory. Springer-Verlag.

- [Irgens and Paulsen, 2004] Irgens, C. and Paulsen, J. (2004). Optimal control of risk exposure, reinsurance and investments for insurance portfolios. Insurance: Mathematics and Economics, 35:21–51.

- [Li et al., 2015] Li, P., Zhou, M., and Yin, C. (2015). Optimal reinsurance with both proportional and fixed costs. Statistics & Probability Letters, 106:134 – 141.

- [Øksendal, 2003] Øksendal, B. (2003). Stochastic Differential Equations. Springer-Verlag Berlin Heidelberg.

- [Schmidli, 2018] Schmidli, H. (2018). Risk Theory. Springer Actuarial. Springer International Publishing.