A fractional generalization of the Dirichlet distribution and related distributions

Abstract

This paper is devoted to a fractional generalization of the Dirichlet distribution. The form of the multivariate distribution is derived assuming that the partitions of the interval are independent and identically distributed random variables following the generalized Mittag-Leffler distribution. The expected value and variance of the one-dimensional marginal are derived as well as the form of its probability density function. A related generalized Dirichlet distribution is studied that provides a reasonable approximation for some values of the parameters. The relation between this distribution and other generalizations of the Dirichlet distribution is discussed. Monte Carlo simulations of the one-dimensional marginals for both distributions are presented.

MSC 2010: 60E05; 33E12, 60G22.

Key Words and Phrases: Fractional Dirichlet distribution, Generalized Dirichlet distribution, Three-parameter Mittag-Leffler functions, Fractional Poisson process. Wealth distribution. Power-law tails.

1 Introduction

Let us consider a finite sequence of positive random variables . For instance, these variables can represent the wealth of economic agents if indebtedness is not allowed. Let us denote the sum as . In the wealth interpretation this is the total wealth. If we define the wealth fraction of the -th agent as , we get a partition of the interval represented by the sequence such that almost surely. We are particularly interested in multivariate distributions for the sequence whose one-dimensional marginals have heavy tails. If we further assume that the random variables are independent and identically distributed, there is a nice and immediate relationship with point processes of renewal type. In this case, the variables can be interpreted as inter-event intervals and the partial sums , with , are the epochs of the events.

In order to clarify the relationship, we start by recalling some basic facts on the time-fractional Poisson process as we are going to use and generalize it in the next section. From [1, 14] we know that the time-fractional Poisson process , , can be defined as a renewal process with independent and identically distributed inter-event waiting times , , with probability density function

| (1.1) |

where

| (1.2) |

is the two-parameter Mittag–Leffler function. Note that for , the waiting times are exponentially distributed and is the homogeneous Poisson process. Moreover, the Laplace transform of the probability density (1.1) takes a very compact form. Indeed, we have

| (1.3) |

Let us now indicate with , , the random occurrence time of the -th event of the stream of events defining . From the renewal structure of we readily obtain that the Laplace transform of reads

| (1.4) |

which in turn corresponds to the Laplace transform of a function involving the three-parameter Mittag–Leffler function (also known as the Prabhakar function – see [7]). In particular, the three-parameter Mittag–Leffler function is defined as

| (1.5) |

and we know by direct calculation that (see e.g. [15], formula (2.3.24))

| (1.6) |

where , , , . Using (1.6), we obtain

| (1.7) |

Remark 1.1.

Note that, for , the above density reduces to that of an distributed random variable. This can be seen by simply noticing that

| (1.8) |

Remark 1.2.

The distribution is a special case of the distribution. Consider a sequence of independent random variables each following a Gamma distribution of parameter . It is well known that their sum is still a Gamma of parameter . Then the sequence of fractions has a joint -dimensional Dirichlet distribution of parameters with density

| (1.9) |

with and is independent of .

The proof of the results in Remark 1.2 can be found in several textbooks and lecture notes (see e.g. [2], Lemma 1.5).

Remark 1.3.

The random variables have the following asymptotic behaviour for [8]:

| (1.10) |

therefore, their sums belong to the basin of attraction of the -stable subordinator.

Remark 1.4.

This paper contains the following material. Section 2 concerns the definition and properties of the fractional Dirichlet distribution. Section 3 mirrors section 2 and is devoted to the generalized Dirichlet distribution. Section 4 explains how to simulate the fractional Dirichlet distribution and presents the results of Monte Carlo simulations in order to illustrate the relation between the fractional Dirichlet distribution and the generalized Dirichlet distribution.

2 Construction of the fractional Dirichlet distribution

Based on Remark 1.1 and Remark 1.2, we now define a generalization of the Gamma distribution and we immediately present a fractional generalization of the Dirichlet distribution.

Definition 2.1 (Fractional Gamma distribution).

Remark 2.1.

The Laplace transform of reads

| (2.12) |

By means of (2.11), we will construct a generalization of the Dirichlet distribution. We consider independent random variables , , distributed as fractional Gamma random variables of parameters , , , , respectively. Furthermore, define the sum , set , , and consider the transformation

| (2.13) |

Note that, from (2.12), the distribution of is fractional Gamma as well, i.e. , where . The joint pdf of the vector reads

| (2.14) | ||||

The joint probability density function of is then obtained by marginalization. Hence,

| (2.15) | ||||

Remark 2.2.

On the -dimensional simplex the probability density of the random vector , where a.s., writes

| (2.16) | ||||

Notice that for the integral in the rhs of (2.16) can be easily solved and the Dirichlet is obtained. In this case is uniformly distributed on for , .

If with , we have

| (2.17) |

which is symmetric but not uniform.

If we let instead (again symmetric) we obtain

| (2.18) |

2.1 Properties

The derivation of the marginal moments can be done explicitly using the formulas in Section 2.2 of [5].

Proposition 2.1.

Let be a random vector distributed with pdf (2.15). For each , we have,

| (2.19) | |||

| (2.20) |

P r o o f..

By Proposition 2 of [5] we have

| (2.21) | ||||

Similarly, the second moment writes

| (2.22) | ||||

and hence after some computation

| (2.23) |

Remark 2.3.

Notice that the first factor of the variance (2.20) is in fact the variance of a one-dimensional marginal of a Dirichlet distribution. It follows that the marginals are overdispersed with respect to those of a Dirichlet distribution.

We now proceed by analyzing the aggregation property and therefore the marginal distributions.

Proposition 2.2 (Aggregation property).

P r o o f..

An immediate corollary of this result is

Corollary 2.1 (Marginal distribution).

Consider the distribution defined in equation (2.15). Then its marginal on is given by

| (2.24) | ||||

As the three-parameter Mittag-Leffler function has a representation as an -function [15],

| (2.27) |

for suitable choices of and , the marginal distribution (2.24) can be expressed in terms of an -function too.

Proposition 2.3.

If is the random variable with pdf (2.24), then

| (2.28) | |||

P r o o f..

In the integral (2.24) set

| (2.29) |

Denote with the resulting integral and observe that

| (2.30) |

For and we have

| (2.33) |

For by using (2.33) and Theorem 2.9 in [12], we have

| (2.34) | ||||

Set in (2.34) with and use (2.29) to recover If is sufficiently small, the poles , do not coincide with the poles Then, according to Theorem 1.1 in [12], the -function in (2.28) makes sense for all as The claim follows by taking the limit as of

Remark 2.4.

According to Theorem 1.3 and 1.4 [12], since

| (2.35) | ||||

the -function in (2.28) has a power series expansion. The following propositions rely on this property.

Proposition 2.4.

For and not a positive integer

| (2.36) |

where

| (2.37) |

P r o o f..

Remark 2.5.

Proposition 2.5.

For and not a positive integer

| (2.40) |

where

| (2.41) | ||||

P r o o f..

3 An alternative generalization

We now give an alternative generalization with desirable properties which in addition approximates the fractional Dirichlet distribution with density (2.15) for appropriate values of the parameters.

Let us thus consider a random vector , , with the following probability density function:

| (3.43) | ||||

for , , , , , .

For the sake of clarity we check that as given in (3.43) is a genuine probability density function. This will follow by proving that

| (3.44) |

in the rhs of (3.43) plays the role of a normalization coefficient.

Theorem 3.1.

We have

| (3.45) | ||||

P r o o f..

Observe that the lhs of (3.45) can be rewritten as

| (3.46) | ||||

where . Apply the change of variables for , in multivariate integration. Thus, we have

| (3.47) | ||||

where for and is the Jacobian of the transformation. Note that

| (3.48) |

By putting (3.47) and (3.48) in (3.46) we have

| (3.49) |

Apply the change of variables for , in multivariate integration. Then, we have for , and is the Jacobian of this transformation. From (3.49)

| (3.50) |

where

| (3.51) |

Observe that in (3.51) can be rewritten as

| (3.52) | ||||

With the change of variable and by recalling the Mellin trasform of , we recover

| (3.53) | ||||

Now, replace in (3.50) with the closed form (3.53). This leads us to

| (3.54) |

where

| (3.55) | ||||

By comparing the integral in (3.55) with that in (3.52), we observe that the former has the same expression of the latter with replaced by Thus, by recurring to the same arguments employed to compute we recover

| (3.56) | ||||

Replacing in (3.54) with the closed form (3.56) we get

| (3.57) | ||||

where

| (3.58) | ||||

which indeed has the same expression of and with suitable updates of . The result follows by iterating from up to the computation of

| (3.59) | ||||

with

| (3.60) | ||||

We obtain the closed form expression

| (3.61) | ||||

with for The last replacement with gives

| (3.62) |

from which the claimed result follows by observing that

Remark 3.1.

Remark 3.2.

On the -dimensional simplex the probability density of the random vector , where a.s., writes

| (3.64) | ||||

with . In short we write .

Notice that for the Dirichlet is obtained. In this case the random vector is uniformly distributed on for , . If instead we only let ,

| (3.65) |

which is symmetric but clearly not uniform. If (again symmetric) we obtain

| (3.66) |

Remark 3.3.

The alternative generalized Dirichlet distribution considered in this section (i.e. that with pdf (3.43)) can be derived by the same procedure described in Section 2 with distributed as Gamma, . Note that the random variable such that , , is Gamma-distributed, , is a special case of the generalized Gamma distribution (see e.g. [11], Section 8.7). In particular, has pdf

| (3.67) |

and Laplace transform (from (2.3.23) of [15] and the definition of Wright functions)

| (3.68) |

Remark 3.4.

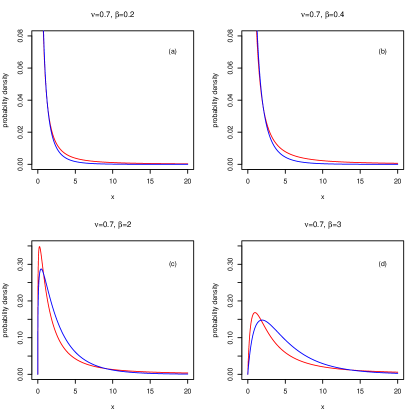

The generalized Dirichlet pdf (3.43) turns out to be a reasonably good approximation of the fractional Dirichlet pdf (2.15) for (see for example Fig. 3). A partial explanation is that for and the fractional Gamma pdf (2.11) has a rather similar shape to the generalized Gamma pdf (3.67), as Fig. 1 shows for and . For the fractional Dirichlet pdf exhibits a behaviour different from the generalized Dirichlet pdf (see for example Fig. 2). Indeed, Fig. 1 shows a different shape of the fractional Gamma pdf compared to the generalized Gamma pdf for and .

Proposition 3.1 (Conjugate distribution).

P r o o f..

The proof is a straightforward application of Bayes theorem. The reparametrization in (3.69) is such that , , are the event probabilities (i.e. ).

3.1 Representation in terms of Dirichlet random variables

In order to derive a meaningful representation in terms of Dirichlet random variables for the random vector , we first recall the definitions of two related classes of random vectors (see [10]).

Definition 3.1 (Liouville distribution of the first kind).

Let be an absolutely continuous random vector supported on the -dimensional positive orthant, i.e. . It is said to have Liouville distribution of the first kind if its joint probability density function writes

| (3.70) |

where , , and is a positive continuous function satisfying , with . Further, we write .

Definition 3.2 (Liouville distribution of the second kind).

Let be an absolutely continuous random vector supported on . It is said to have Liouville distribution of the second kind if its joint probability density function writes

| (3.71) |

where , , and is a positive continuous function satisfying , with . Further, we write .

Remark 3.5.

If we let , , , in (3.70), then is distributed as an inverted Dirichlet.

If, in (3.71), we choose , , , we have that is distributed as a Dirichlet.

Proposition 3.1 of [10] tells us what is the relationship between Liouville distributions of the first and of the second kind (and hence between the Dirichlet and the inverted Dirichlet). Specifically, if and we consider the transformation

| (3.72) |

then , where

| (3.73) |

Plainly, the converse relation is true as well: inverting (3.73) (letting ) we have

| (3.74) |

As a simple example, considering , (inverted Dirichlet), we readily obtain (Dirichlet).

Now, by exploiting the above definition we prove the following distributional representation for .

Proposition 3.2.

Let be distributed with pdf (3.43). Then the random vector such that

| (3.75) |

is distributed as a Dirichlet.

P r o o f..

Let us define the random vector such that

| (3.77) |

and let . Combining the transformations in the proof of Theorem 3.45 and of Remark 3.1 we see that has pdf

| (3.78) |

and hence (i.e. an inverted Dirichlet distribution).

By using the mentioned transformations between Liouville distributions of first and second kinds we have that (Dirichlet), where

| (3.79) |

and (3.75) follows.

Finally, a rewriting of the components of in terms of those of , leads easily to (3.76).

4 Monte Carlo Simulations

The simulation of the random variables for the fractional Dirichlet distribution is straightforward based on the construction presented in section 2. First, one needs to generate random variables with density (2.11) and one can use the mixture representation discussed in [4]

where is -distributed and is strictly positive-stable distributed with as the Laplace transform of the probability density function. Summing the to get and dividing by gives .

Remark 4.1.

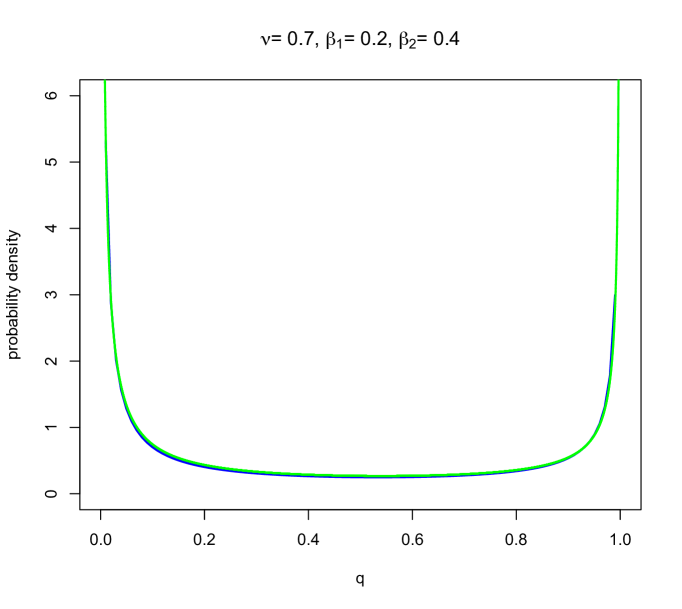

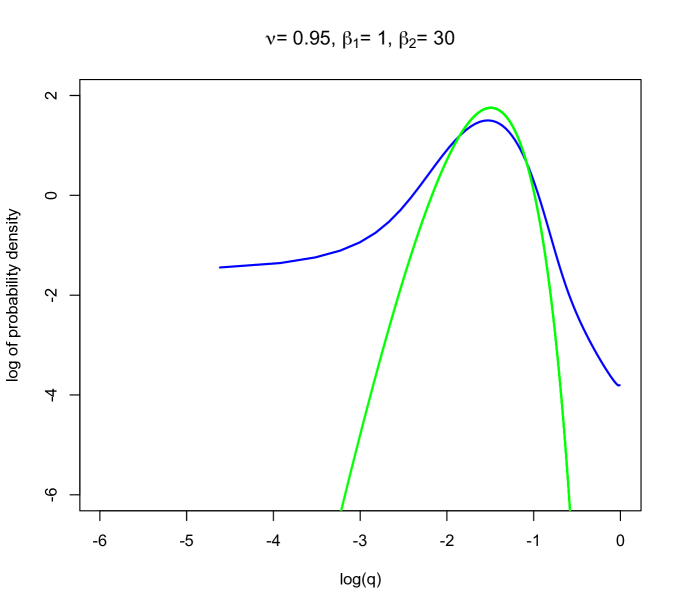

The behaviour of the fractional Dirichlet distribution in the case is shown in Fig. 2 for , , . In this case, the generalized Dirichlet distribution is not a good approximation.

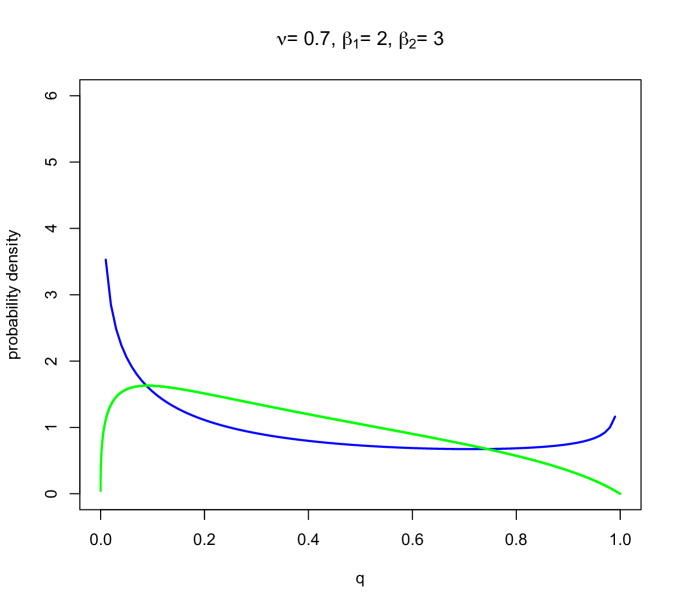

This is not the case for , , and where the generalized Dirichlet distribution is a reasonably good approximation of the fractional Dirichlet distribution. This is represented in Fig. 3.

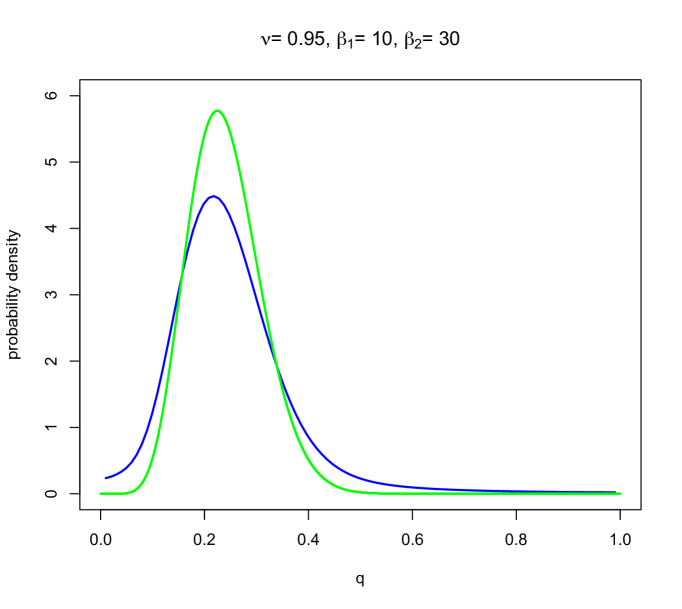

For larger values of the parameters , one gets a unimodal distribution in both cases as shown in Fig. 4 for , , , .

In Fig. 5, the heavy character of the right tail of the generalized Dirichlet distribution is highlighted by the log-log plot.

Acknowledgements

F. Polito has been partially supported by the project “Memory in Evolving Graphs” (Compagnia di San Paolo/Università degli Studi di Torino).

References

- [1] L. Beghin and E. Orsingher. Fractional Poisson processes and related planar random motions. Electron. J. Probab., 14(61):1790–1827, 2009.

- [2] J. Bertoin. Exchangeable Coalescents. ETH Zurich, 2010.

- [3] L. Bondesson. A general result on infinite divisibility. Ann. Probab., 7(6):965–979, 1979.

- [4] D. O. Cahoy and F. Polito. Renewal processes based on generalized Mittag-Leffler waiting times. Comm. Nonlinear Sci. Numer. Simulat., 18(3):639–650, 2013.

- [5] S. Favaro, G. Hadjicharalambous, I. Prünster. On a class of distributions on the simplex. J. Statist. Plann. Inference, 141(9):2987–3004, 2011.

- [6] D. Fulger, E. Scalas and G. Germano. Monte Carlo simulation of uncoupled continuous-time random walks yielding a stochastic solution of the space-time fractional diffusion equation. Phys. Rev. E, 77, 021122, 2008.

- [7] A. Giusti, I. Colombaro, R. Garra, R. Garrappa, F. Polito, M. Popolizio, F. Mainardi. A practical guide to Prabhakar fractional calculus. Fract. Calc. Appl. Anal. 23(1):9–54, 2020.

- [8] R. Gorenflo and F. Mainardi. Fractional Calculus: Integral and Differential Equations of Fractional Order in Fractals and Fractional Calculus in Continuum Mechanics, A. Carpinteri and F. Mainardi eds., Springer, New York and Wien, 223–276. 1997.

- [9] I. S. Gradshteyn and I. M. Ryzhik. Table of integrals, series, and products. Elsevier/Academic Press, Amsterdam, eighth edition, 2015.

- [10] R. D. Gupta, D. S. P. Richards. Multivariate Liouville distributions. J. Multivariate Anal., 23(2), 233–256, 1987.

- [11] N. L. Johnson, S. Kotz, N. Balakrishnan. Continuous univariate distributions. Vol. 1. Second edition. Wiley Series in Probability and Mathematical Statistics: Applied Probability and Statistics. John Wiley & Sons, Inc., New York, 1994.

- [12] A. A. Kilbas, M. Saigo. -transforms. Theory and applications. Analytical Methods and Special Functions. Vol. 9. Chapman & Hall/CRC, Boca Raton, FL, 2004.

- [13] T. Kozubowski, Mixture representation of Linnik distributions revisited. Stat. Probab. Lett., 38, 157–160, 1998.

- [14] F. Mainardi, R. Gorenflo, and E. Scalas. A fractional generalization of the Poisson processes. Vietnam J. Math., 32(Special Issue):53–64, 2004.

- [15] A. M. Mathai and H. J. Haubold. Special Functions for Applied Scientists. Springer, New York, 2008.

- [16] T. M. Michelitsch, A. P. Riascos. Generalized fractional Poisson process and related stochastic dynamics. Fract. Calc. Appl. Anal. 23(3):656–693, 2020.

- [17] T. M. Michelitsch, A. P. Riascos. Continuous time random walk and diffusion with generalized fractional Poisson process. Phys. A 545, 123294, 18 pp., 2020.

- [18] T. M. Michelitsch, F. Polito, A. P. Riascos. Biased continuous-time random walks with Mittag-Leffler jumps. Fractal and Fractional, 4(4), 51, 2020.

- [19] R. N. Pillai. On Mittag-Leffler functions and related distributions. Ann. Inst. Statist. Math. 42(1):157–161, 1990.

1 Department of Mathematics G. Peano

Università degli Studi di Torino

Via C. Alberto 10, 10123, Torino, Italy

e-mails: elvira.dinardo@unito.it, federico.polito@unito.it

2 Department of Mathematics

University of Sussex

Falmer, Brighton, BN1 9QH, UK

e-mail: e.scalas@sussex.ac.uk (Corr. author)