Quantum option pricing using Wick rotated imaginary time evolution

Abstract

In this paper we reformulate the problem of pricing options in a quantum setting. Our proposed algorithm involves preparing an initial state, representing the option price, and then evolving it using existing imaginary time simulation algorithms. This way of pricing options boils down to mapping an initial option price to a quantum state and then simulating the time dependence in Wick’s imaginary time space. We numerically verify our algorithm for European options using a particular imaginary time evolution algorithm as proof of concept and show how it can be extended to path dependent options like Asian options. As the proposed method uses a hybrid variational algorithm, it is bound to be relevant for near-term quantum computers.

I Introduction

Numerical methods are commonly used for pricing financial derivatives and are also used extensively in modern risk management. In general, advanced financial asset models are able to capture nontrivial features that are observed in financial markets. Due to the probabilistic nature of these assets, the calculation of their fair price based on existing information from the markets is a valuable business problem. The seminal work of Black and Scholes ushered in a new era of the option pricing theory Black and Scholes (1973) after which the notion of option pricing models expanded rapidly and attracted considerable attention. More often than not, these asset pricing models are multi-dimensional and complex, as a consequence of which, one does not have closed-form solutions. As is the case for any complex problem that lacks a closed-form solution, extensive effort has been devoted to development of alternative solutions to the option pricing problem.

A wide range of studies have focused on the numerical realization of the option pricing problem, ranging from stochastic simulations to numerical solutions of partial differential equations. Numerical techniques for pricing options can be classified into three main categories: Tree methods Cox et al. (1979); Rendleman (1979), Partial Difference methodsReisinger and Wissmann and Monte-Carlo methodsBoyle (1977); Giles (2015); L’Ecuyer (2009). The Binomial Tree method is simple to implement and provides reasonably accurate results. However, it is mainly used for pricing “simple” options, with constant volatility. The major drawback of the binomial method is that it is computationally resource intensive; it requires even more than what is needed for other methods that give comparably accurate resultsBroadie and Detemple (1996). Because of this, it is not applied to more complex derivatives. Since asset pricing is inherently probabilistic and is described by stochastic differential equations, Partial Difference methods can be used to price financial derivatives by solving the stochastic differential equations (SDE) that the latter satisfies. Finally in Monte-Carlo methods, one produces a large number of paths that the price of the underlying asset could follow in subsequent time steps using the solution of the SDE that characterizes it. When these simulations were initially presented as a forward-looking technique, it had been impossible to value American options and ,in general, path-dependent options. A large body of work has since been devoted to developing new approaches that enable Monte Carlo simulations to implement backward-looking algorithms which solve this inadequacyGrant et al. (1997); Ibanez and Zapatero (2004). In order to determine the optimal exercise strategy, some additional numerical procedures must be embedded in the Monte Carlo method when pricing early exercisable products, e.g. American options, Bermudan options, etc. Monte-Carlo methods usually lack efficiency, while the other two methods are plagued by the curse of dimensionality in high-dimensional settings. Therefore, industries like finance are in constant search for novel computing paradigms that might serve solutions to these computationally expensive but industrially valuable problems. There has also recently been a lot of interest in leveraging the power of machine learning tools, mainly the use of neural networks, to solve various forms of option pricingDe Spiegeleer et al. (2018); Ferguson and Green (2018); Hahn (2013); McGhee (2018).

Quantum computing promises to solve many of the existing problems that are otherwise infeasible to solve using classical computers. Today’s quantum computers belong to the Noisy Intermediate-Scale Quantum (NISQ)Preskill (2018) regime and are plagued with various shortcomings such as decoherence and read-out errors that limit the applicability of this technology to practical problems. Although not ideal, algorithms exploiting the power of NISQ era quantum computers have provided new ways of solving computationally intensive problems in fields such as machine learningBiamonte et al. (2017); Havlíček et al. (2019); Gao et al. (2018) and quantum chemistryGanzhorn et al. (2019); Kandala et al. (2017). NISQ friendly quantum algorithms have also been proposed in hybrid settings as subroutines for computationally resource intensive parts of classical algorithmsMoll et al. (2018); Parrish et al. (2019).

Quantum algorithms for solving computationally hard financial problems have recently been proposed for topics ranging from portfolio optimizationRebentrost and Lloyd (2018); Woerner and Egger (2019); Egger et al. (2020) to pricing optionsZoufal et al. (2019); Martin et al. (2019); Kaneko et al. (2020); Rebentrost et al. (2018). As mentioned previously, the most numerically tractable method of option pricing is to use classical Monte-Carlo methods, which have been extended to quantum settings in recent works. RefStamatopoulos et al. (2020); Martin et al. (2019); Rebentrost et al. (2018) pointed out that one can achieve a theoretical quadratic speedup number of Monte-Carlo samples with the use of Quantum Amplitude Estimation (QAE)Brassard et al. (2002) as a subroutine for measuring the expectation value of an evolved price. However, canonical QAE uses quantum phase estimation as a subroutine and is not practical for near term quantum processors due to required circuit depth. Several methods using tools like maximum likelihood estimation have been developed to make QAE and QMC more practical for NISQ era quantum devicesSuzuki et al. (2020); Brown et al. (2020). For instance, RefKaneko et al. (2020) showed that one can, in practice, formulate a circuit that can be used to simulate the path dynamics of a given asset, but so far the proposed methods are not NISQ-friendly. RefVazquez and Woerner (2020) showed that one can create a NISQ efficient method to prepare the final probability state of the option price that obeys a Heston stochastic model. This method can in principle be extended to state preparation of any stochastic differential equation. In this paper, we propose an algorithm that reformulates the classical option pricing problem in the quantum setting. The key idea is to recast the pricing problem as a set of differential equations, which then maps to evolving a quantum wave function in imaginary time

We start in Section II by briefly describing the option pricing problem and then reformulating it in the quantum setting. In Section III, we outline the proposed algorithm which is made up of two independent parts which we discuss in Section IV and Section V. We show numerical results to validate our proposal in Section VI and finally end with a summary of our findings and suggestions for future work.

II Financial Hamiltonian

We start by considering a stock price , which is modeled as a random stochastic variable obeying Geometric Brownian motion that satisfies the equationBlack and Scholes (1973)

| (1) |

Here and are the expected return and volatility of the stock which for the discussion, we will assume to be time independent i.e. and , and finally is the Brownian process satisfying and . One can then consider a function dependent on a stochastic variable satisfying Eq. 1 and time , which satisfies the following time derivative due to Ito calculus,

| (2) |

The Black-Scholes-Merton (BSM) model Black and Scholes (1973); Merton (1973) is then obtained by removing the Brownian randomness of the stochastic process by introducing a random process correlated to Eq. 2. This is often termed as hedging and is done by constructing a a portfolio , whose evolution is governed by

| (3) |

where is the short term risk free interest rate. A possible choice of is . In this context, is called the option and the portfolio is made up of an option and an amount of underlying stock proportional to . Combining Eq. 2 and Eq. 3, one finally arrives at the BSM equation given by

| (4) |

It is necessary to note that there are many assumptions underpinning the above result. We have assumed a constant interest rate , an option continuously re-balanced within the portfolio, the absence of arbitrage and finally infinitesimal divisibility of stocks with no transaction costs. Because of the first order and second order nature of time, and asset value in Eq. 4 needs boundary conditions w.r.t and one boundary condition w.r.t . For a European call option, the value of at expiry time is given by where is the exercise price. The second condition involves the boundary that as . And finally, the boundary condition for time trivially involves .

Without loss of generality, we now re-scale the two independent variables by defined by and . To explicitly see the analogy w.r.t Quantum mechanics, we redefine . This re-scaling changes Eq. 4 to

| (5) |

Notice that one can now associate a quantum mechanical formalism and interpret the option price in continuous basis , the underlying security price. This now elegantly extends the time dependence as as the projection of the time evolved option price state. Eq. 5 thus reduces to the form , where the BSM Hamiltonian is given as . Note that the resulting Hamiltonian is not Hermitian because of the operator. It can be shown that this Non-Hermiticity can be taken care of by making a similarity transformationBagarello (2020) which finally results in an effective Hermitian Hamiltonian

| (6) |

where . Thus to find the option price at time which is given by the state , one starts by evolving the initial state with the Hermitian Hamiltonian in the Wick’s rotated imaginary time space resulting in

| (7) |

where is a normalization factor.

Although we have derived the European option pricing Hamiltonian, a similar Hamiltonian for Asian path-dependent options can be derivedVecer and is shown to be a time-dependent Hamiltonian given by

| (8) |

where . It should be noted that both the Hamiltonian kernels resemble a heat equation and the deep analogy between stochastic equations and Heat/diffusion equations has been exploited in various contexts.

III Quantum Algorithm

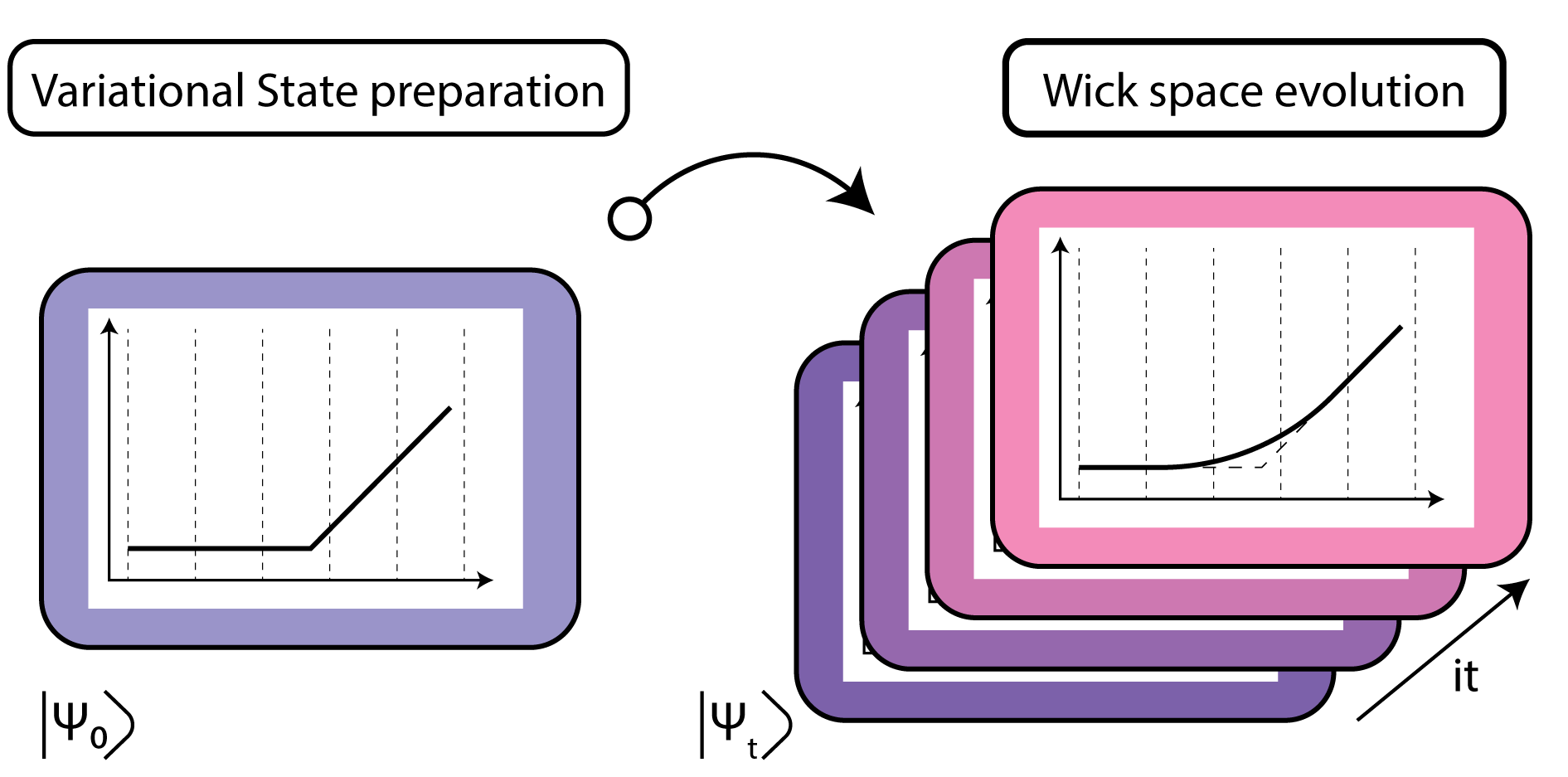

We start with encoding the initial boundary conditions of the option price into initial quantum state, and then evolve it with the Hamiltonian corresponding to the pricing method in imaginary time. We define the basis of an n-qubit system in independent orthogonal states spanning the space of underlying security prices discretized into pieces. We then write ,the value of the option price when the underlying asset is at price at time until maturity, as , where for all time , after which the results are finally scaled to get the actual cost. We start with the boundary condition that , where is the normalization factor. As mentioned before, for a system with Hamiltonian , evolving in real time , the time propagator is given by . The corresponding propagator in Wick rotated imaginary time () is given by the propagator which is a non-unitary operator. Therefore, our algorithm consists of two major parts, preparing the initial state and Wick rotated imaginary time evolution.

IV Variational State preparation

The first step of the algorithm involves the preparation of the initial state shown in Fig. 1. We start by using a parameterized quantum circuit to varaitionally prepare the initial state of the system. Expressivity of such a parameterized quantum circuit depends on the number of parameters used; more parameters generally lead to higher variational flexibility, but come with the cost of having not-so-NISQ friendly circuits (i.e deeper quantum circuits) and are often plagued by difficultly in optimization McClean et al. (2018). The goal of finding parameterized circuits which minimize the circuit depth and maximize the accuracy and expressivity has led to a number of approaches such as hardware efficient ansatz, physically motivated fixed ansatz, adaptive ansatz etc..

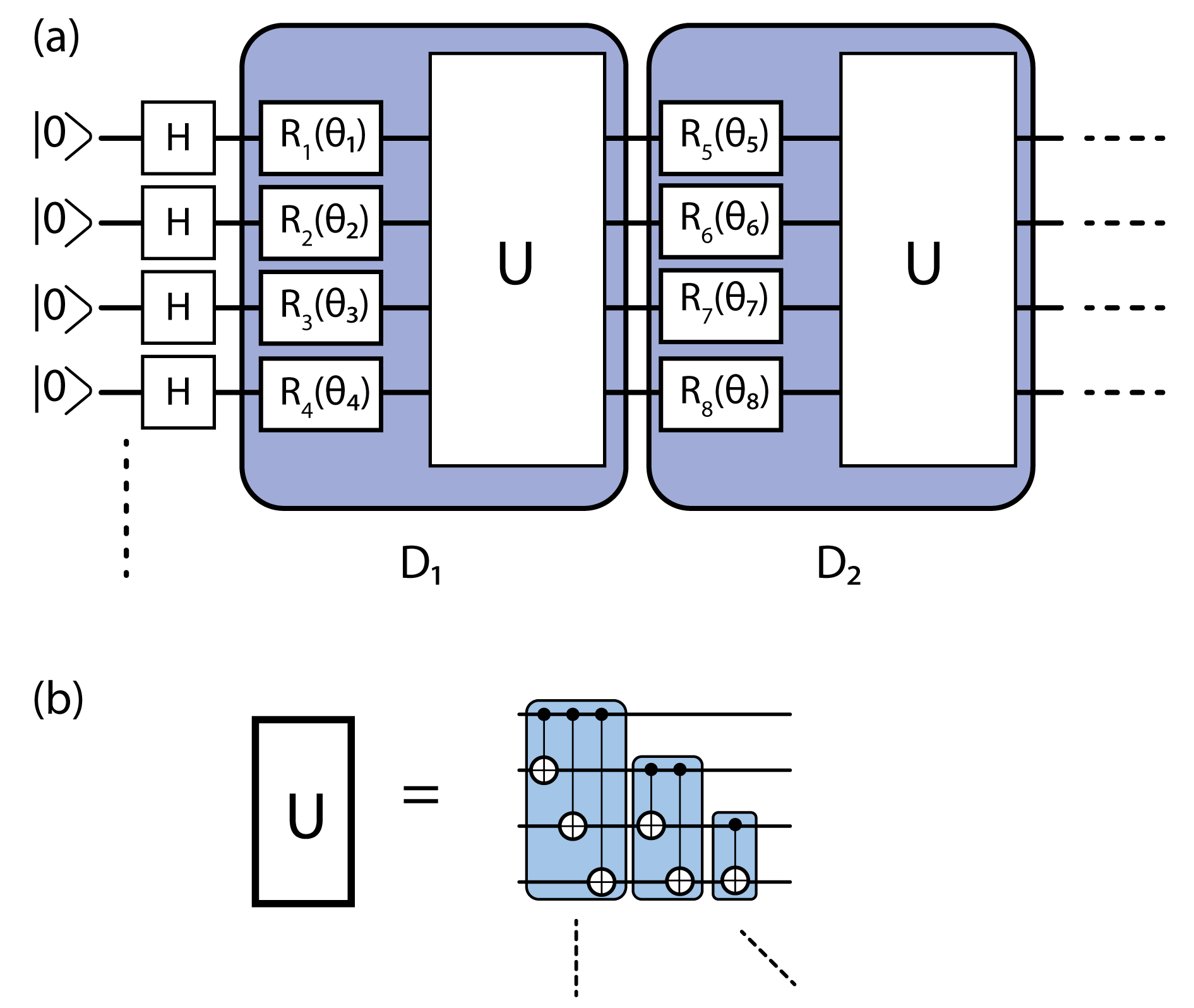

Although any circuit that is expressive enough to represent the initial boundary condition can be used, we choose two specific PQCs that are suitable for each subroutine mentioned in the subsequent sections. For the Variational Hilbert space evolution, we start with superimposing the state by applying Hadamard gate, after which we make layer unitary () given by sets of single qubits and randomly chosen rotation gates where and , followed by a two qubit entanglement layer consisting of pairwise s. The resulting circuit has parameters that are to be optimized and is shown in Fig. 2, where is the number of qubits.

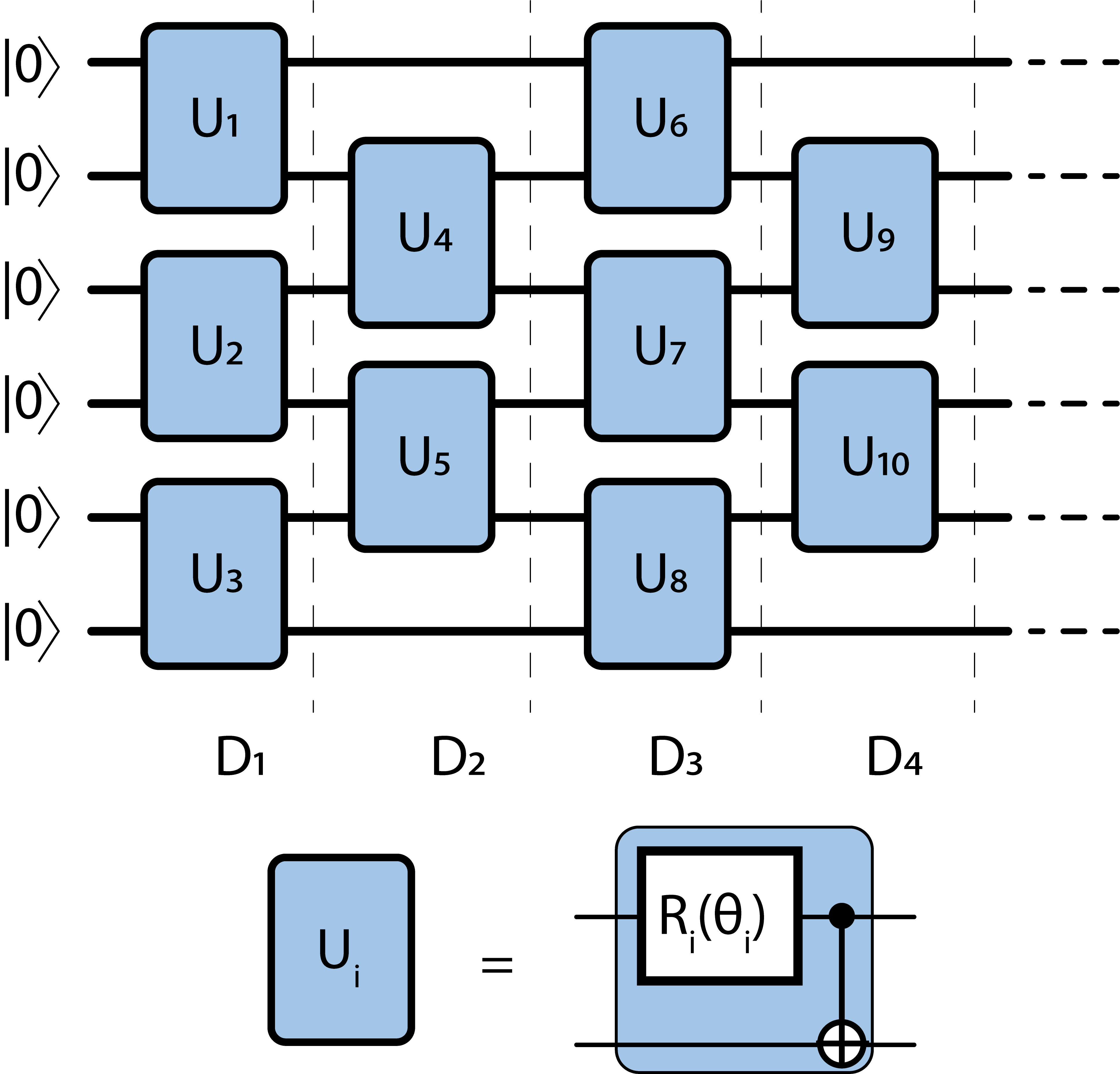

For the second hardware efficient method, we chose an ansatz as shown in Fig. 3. Each depth unitary at depth () is made up of the nearest neighbor two qubit entanglement gates () starting from either the first or second qubit. is made up of randomly chosen single qubit rotation gate where and followed by a . This is more hardware efficient than the previously introduced ansatz since only nearest neighbour qubit connectivity is required as opposed to an arbitrary qubit connectivity, which in turn reduces the total amount of gates and circuit depth.

Imaginary time evolution is often used as a tool for driving an initial wave function towards the ground state of a given system. In that case, as long as errors due to an imperfect ansatz do not cause the evolution to become trapped in local minima, one does not care about the path of true imaginary time evolution, as ultimately, the system will always be driven towards the ground state. By contrast, our anzatz does not only need to be expressive enough to represent the initial and final state, but also the intermediate states, thus building anzats circuits that are well suited to imaginary time evolution is an intersting problem that will be addressed in future work.

V Wick space evolution

In this section we describe two algorithms that can be used to imaginary time evolve the financial Hamiltonians. The first method, detailed in Section V.0.1 involves approximating the state vector using a variational parametrized ansatz which is then evolved by evolving the parameters of the ansatz circuit. In the second method, we use variational algorithm similar to the Variational Quantum Eigensolver introduced in RefBenedetti et al. (2020), where a hardware efficient variational circuit is used to simulate individual terms in the Hamiltonian by minimizing a cost function. This is explained in Section V.0.2.

V.0.1 Variational Hilbert space evolution

up-to a factor. The red qubit is the ancilla qubit where the final measurement is made.

Following Endo et al. (2020), we started by first writing out finance Hamiltonians as with real coefficients and observables , that are tensor products of Pauli matrices. Our Hamiltonian contains operators of the form , which are then converted using finite difference methods, converted to a tri-diagonal form in the subspace while operators of the form are trivially diagonal. This is shown in detail in Appendix A. In the variational Hilbert space method, instead of directly calculating the state , we approximate it using an dimensional variational circuit made up of parameters giving us , using a variational quantum anzats as shown in Fig. 2 and discussed in Section IV. Thus our entire circuit can be written as . We start by variationally finding that best approximates our initial condition . We then use MacLachlan’s variational principleMcLachlan (1964) to translate the time propagation of state to time evolve the variational vector , which in turn propagates . MacLachlan’s variational principle is given by

| (9) |

where is the norm of the quantum state . Following the same for , one gets the first order equation of that dictates the evolution of the parameters, which is given by Yuan et al. (2019)

| (10) |

where:

| (11) | ||||

| (12) |

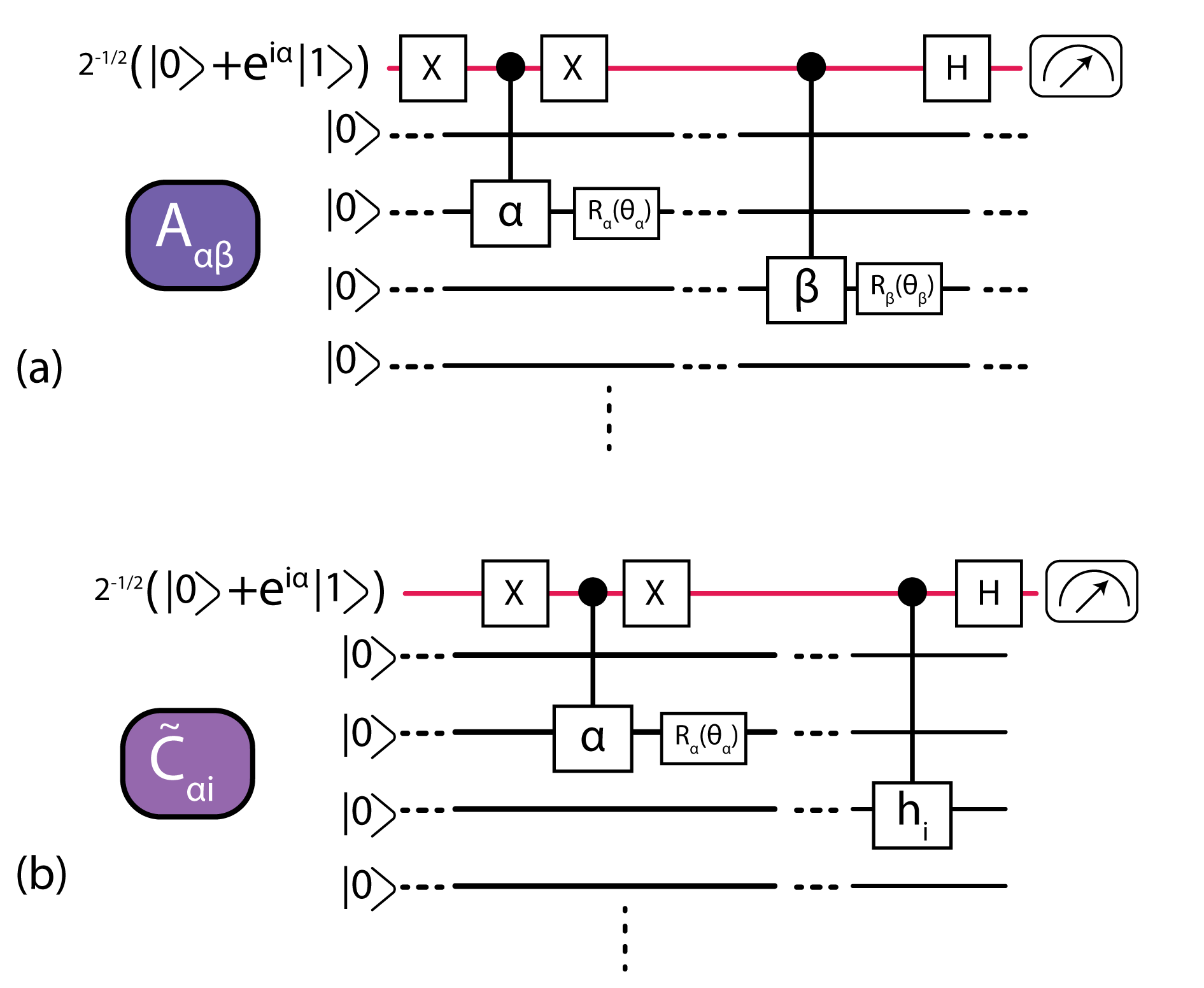

Here and are the Hamiltonian terms. The idea behind the variational Hilbert space evolution algorithm comes from the fact that quantities and can be efficiently measured using a quantum circuit as shown in RefLi and Benjamin (2017). This is because where with , the Pauli gate corresponding to and where . Hence, the calculation of Eq. 11 and Eq. 12 reduces to

| (13) | ||||

| (14) | ||||

| (15) |

Each of the above terms can be calculated using the circuit shown in Fig. 4(a) while terms are calculated by circuits shown in Fig. 4(b) (up-to a factor). Note that both the circuits have an extra ancilla which essentially measures the real part of each term. Here is for and for .

Having calculated and at time , one can invoke Eq. 10 to calculate the updated as . We have used the Euler finite difference formula for approximating Eq. 10, where more sophisticated numerical approximations and higher order terms as discussed in Appendix A can very well be used to increase accuracy. Hence by propagating in time, we generate . Once we have a set of time depedent s, we can plug them back to the initial parameterized quantum circuit to extract the option price at these discretized times.

V.0.2 Hardware efficient variational evolution

By using the ideas introduced in RefBenedetti et al. (2020), we want to propagate our hamiltonian . Note that ’s, in general, need not commute with each other. We then approximate the evolution of state by expanding as a Trotter product

| (16) | ||||

with for imaginary time evolution and for dividing the time into steps. refers to the term applied in time step. The first step involves variationally approximating the initial state , which is given by , then the first application of on state results in with where

| (17) |

It can be shown thatBenedetti et al. (2020) minimization of is the same as maximization of

Thus generalizing the above discussion, for the term in Eq. 16, the state vector after applying terms in the Trotter product is variationally obtained by calculating the angles that maximize given by

| (18) |

where is the optimal angle in the previous step. Further, using the fact that , we can further reduce our maximization function Eq. 18 as

| (19) |

It was shown in RefNakanishi et al. (2020); Vidal and Theis (2018); Parrish et al. (2019); Ostaszewski et al. (2019) that parameterized circuits of the type shown in Figure 2 have a very efficient coordinate-wise optimization algorithm that eliminates the computation of costly gradients. Essentially, one finds the optimal angle for one gate while fixing all others to their current values, and sequentially cycles through all gates. This is easy to carry out, as in each step, the energy has a sinusoidal form with period . For the gate in the circuit, one obtains the update rule for finding the angle as

| (20) | ||||

where with the current parameter .

As noted by RefBenedetti et al. (2020), the calculation of terms in Eq. 19 can easily be carried out out in a Hardware efficient manner reducing both the number of CNOTs and ancilla qubits as compared to the method outlined in subsubsection V.0.1. This new method also avoids the need to calculate matrix inversion.

VI Results

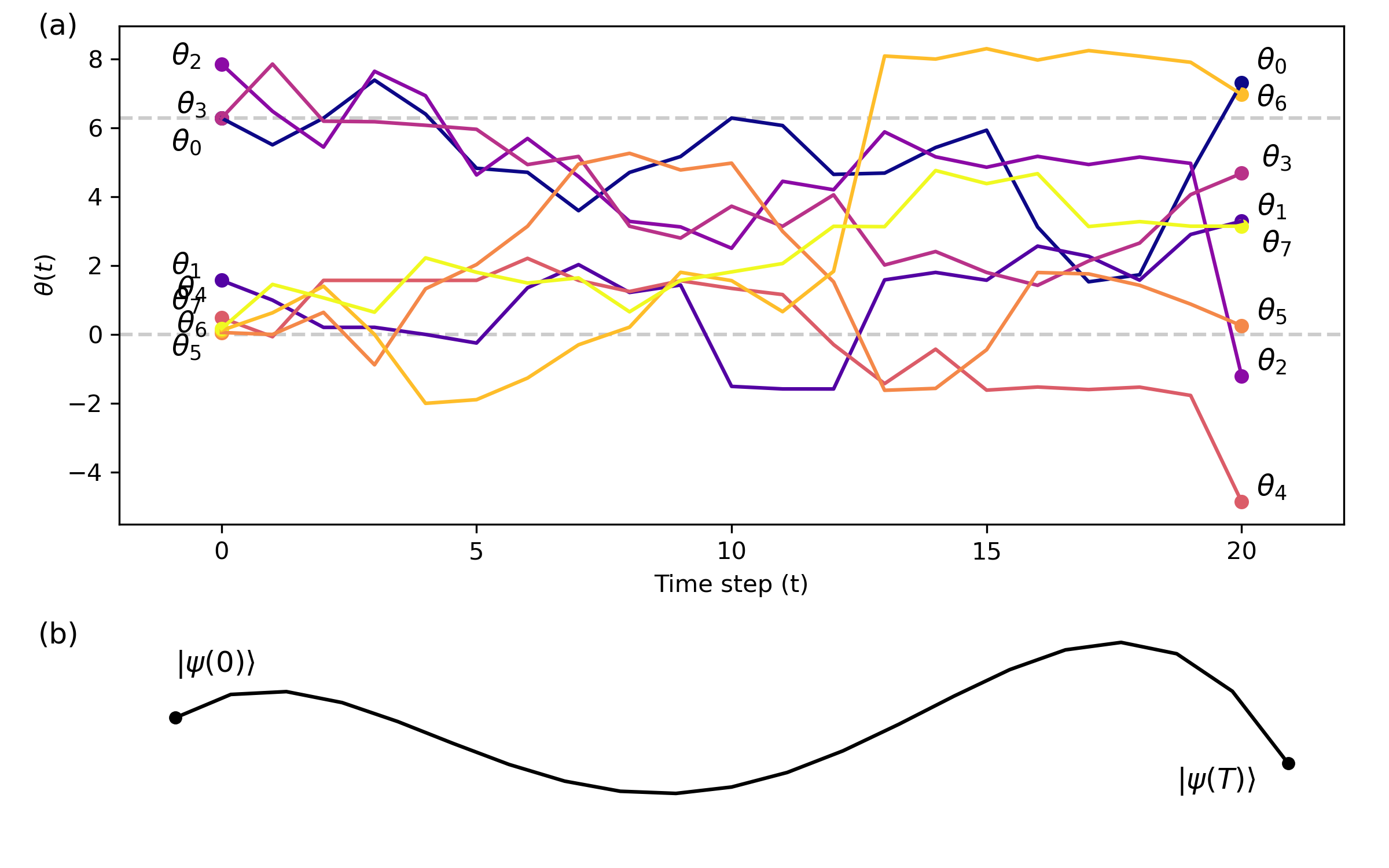

In this section, we show the numerical results obtained using the Variational Hilbert space evolution algorithm described in Section V.0.1. For simplicity, we calculate the option price using a varational Hilbert space evolution subroutine, although this can be replaced by the hardware efficient evolution. To illustrate the evolution of the wave function by evolving the variational parameters, we use a 4 qubit system. Restricting ansatz depth to , we have variational parameters that are time evolved using Eq. 10. This is shown in Fig. 5(a), where we plot the time evolution of each parameter for 20 Trotter steps. Even though our goal is to evolve the quantum state by a small time step in its Hilbert space (shown as illustration in Fig. 5(b)), one can see from Fig. 5(a) that the change in variational parameters for each individual time step is neither small nor trivial. This is associated with the deep connection to quantum generalization of natural gradients as explained in Ref.Stokes et al. (2020). Eq. 10 essentially relates the non-trivial relationship between a translation step in parameter space, and the corresponding translation in the problem space, which in our case is the Hilbert space. The 2D tensor in the update rule is the well known Fubini-Study metric tensor Wilczek and Shapere (1989); Hackl et al. (2020); Koczor and Benjamin (2019) which accounts for the non-uniform effect of the parameter’s gradients on the quantum states.

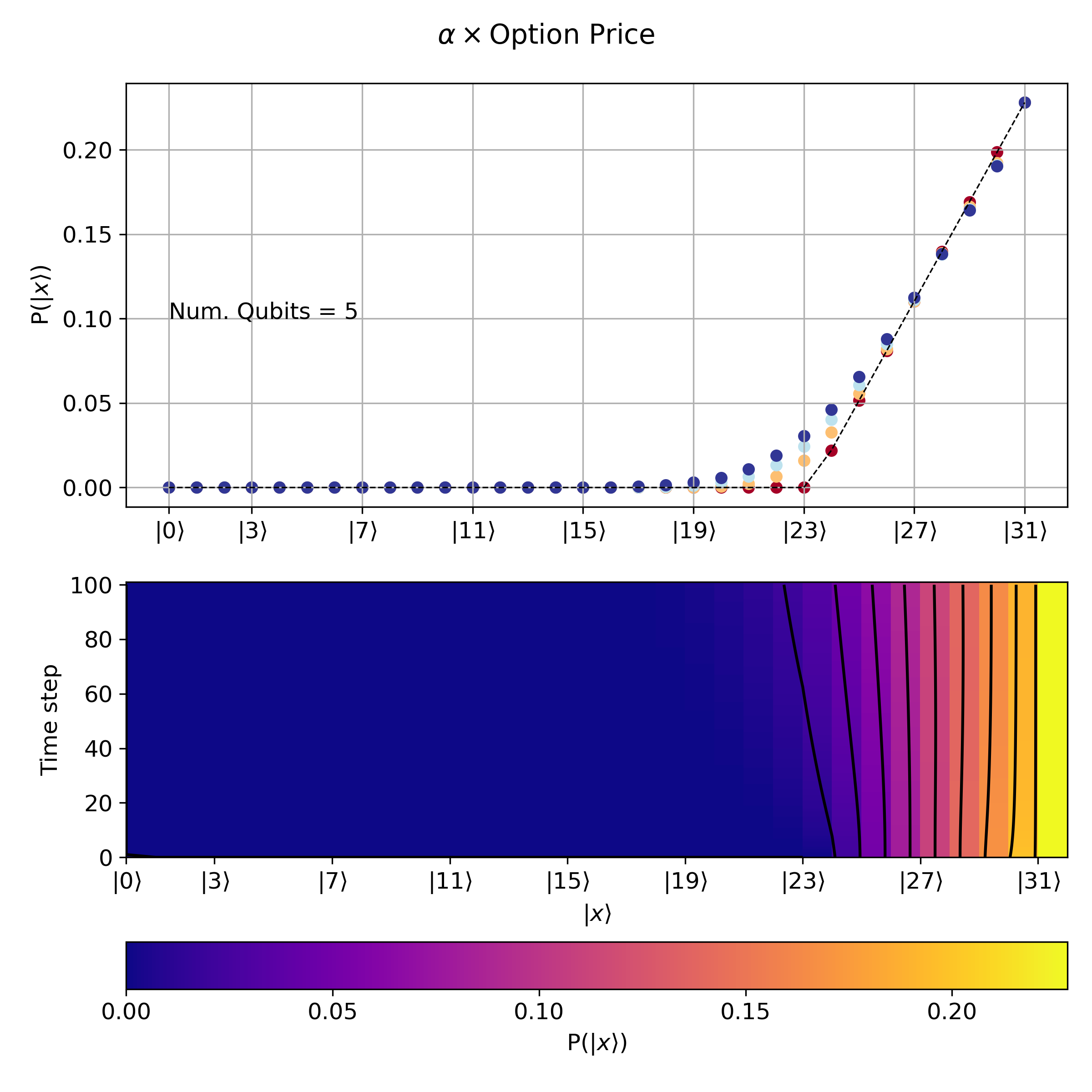

Moving beyond the evolution of parameters to better simulate the option pricing, we now use a 5 qubit system with depth ansatz to time evolve the system. The result of this simulation is shown in Fig. 6. We decompose our final time step into Trotter steps and thus our time and spatial discretization is given by . In the top part of the figure, we plot the probability of each state at different time steps indicated by the color of the plot with red being and blue being , and where the dotted line shows the initial starting state. The actual option value corresponding to each price is then obtained by scaling the probability to arbitrary units. The lower part of the figure shows the same data plotted in 2D with the price on the axis, the time step on the axis, and probability/scaled option value shown as a color map. One can now look more closely at the non linear effect of time evolution on the option pricing around state .

Here we want to discuss possible sources of errors in the algorithm. There are five main types of errors that propagate within the algorithm. 1. Errors due to limited expressivity of the variational circuit in describing the trial wave function. 2. Errors that come from approximating the Hamiltonian and Troterization. 3. Errors in the approximate numerical integration methods employed in Eq. 10, which is always going to be approximate because of the finite discretization of both time and space. 4.Shot noise in measuring equation coefficients and and finally 5.Errors due to noise in the quantum machines. Errors due to variational anzats can be systematically improved by making the circuit more expressive by increasing the depth and also by adapting better techniques to optimize the initial parameters. Errors due to Troterization can be reduced by adding higher order trotter terms. While we have used a simple euclidean finite difference method for integrating Eq. 10, more sophisticated techniques like Adams-Moulton or Newton-Cotes can be used to drastically reduce errors.

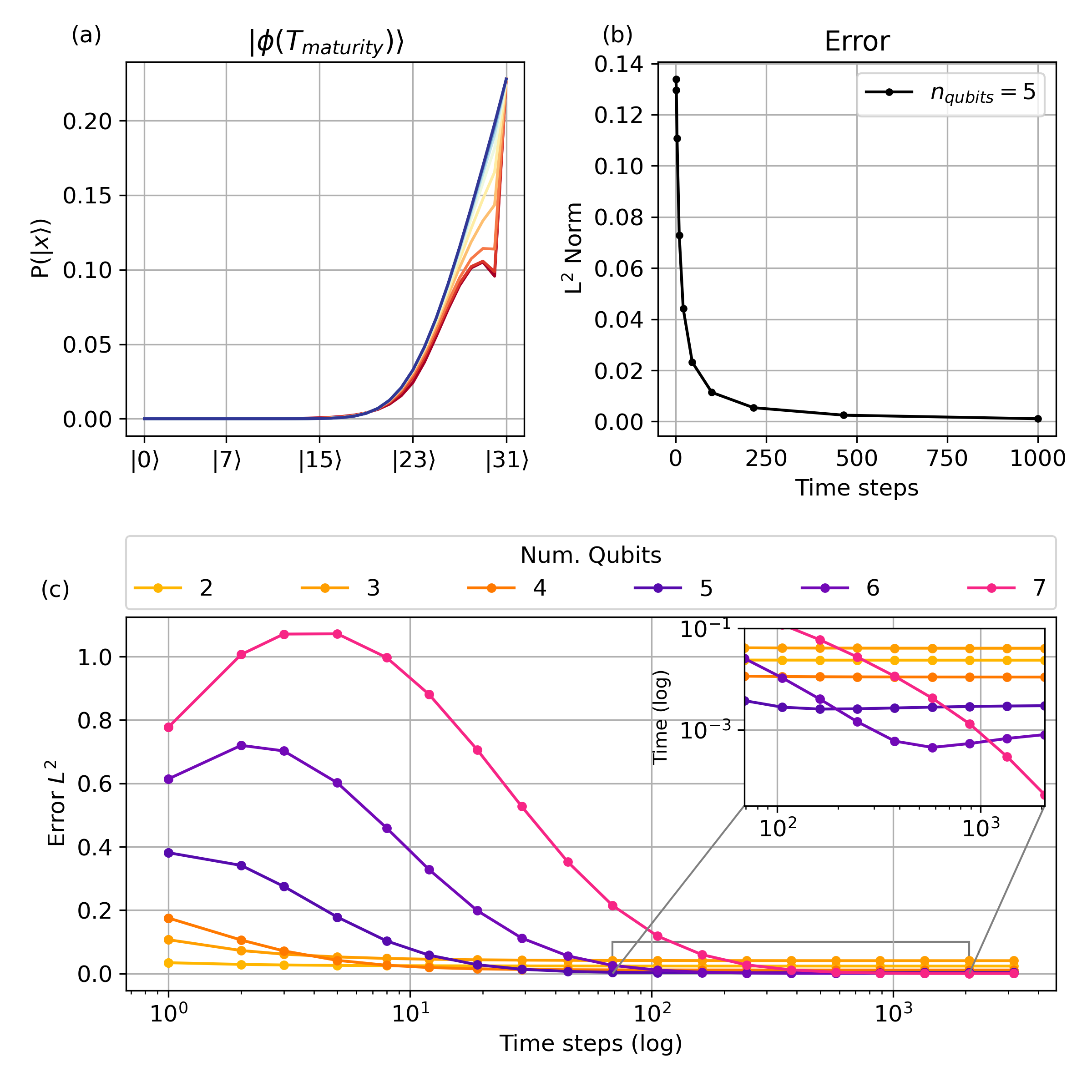

Errors due to finite time step descritization are found to be sensitive and closely coupled to the space descritization, i.e number of qubits. This is to be expected as the entire algorithm boils down to solving a finite difference solution of the classical Eq. 10. Classical finite difference solutions have errors given by, where is the number of time steps and is the number of spatial bins. This is because of the first order and second order nature of the differential equation involved. Thus the time step must be quadratically smaller than the spatial step for comparable accuracy. This is demonstrated in Fig. 7, where in (a) for a given space descritization of , we plot the option price at maturity time for various time descritization steps with red being and blue being (each curve independently normalized). In (b) we plot the error as measured by norm distance from the analytic solution as a function of . As discussed earlier, accuracy of the final result can be systematically increased by either increasing or , but in a non-trivial manner as discussed in Appendix A. We show this in (c), where we plot the mean squared error instead of for various and numbers of qubits (or equivalently ). This shows the non-trivial relationship between the errors as for a given one needs to have a sufficiently large to see systematic improvement in error as one increases . For instance, close to , one sees that going from 2 qubits to 7 qubits increases the errors, while there is a threshold around after which the error of a 7 qubit space discretization is smaller than that of a 2 qubit one (shown in the inset). Nonetheless, as , for where is the error due to spatial and time discretization. This can also be seen by comparing the final values of the error shown in the inset, where the errors are arranged such that the system with the largest number of spatial steps has the least error, as expected.

VII Conclusion

In this work, we have shown that one computationally resource intensive but industrially relevant class of financial problems, i.e option pricing, can be reformulated as a quantum imaginary time evolution of a wave function problem. Quantum Monte Carlo methods offer a theoretical speed up to this problem, but are still impractical for near term quantum devices due required unattainable circuit depth. The importance of our work lies in transferring the solution of this computationally resource intensive financial problem into a hybrid classical/quantum domain where it may become practical for near term quantum devices. We have presented a proof of concept demonstration for European option pricing problem, but it can be extended to other option pricing problems such Asian options.

The proposed algorithm consists of two main parts, namely the initial state preparation and the imaginary time propagation. For the imaginary time propagation we described two different algorithms, namely variational Hilbert state evolution and the Hardware efficient variational evolution. After outlining the basic mechanisms of both of the imaginary time evolution algorithms, we selected the former method for numerically evaluating the value of the option price as proof of concept. While the method used for numerical simulation (Variational Hilbert space evolution Section V.0.1) can be considered NISQ friendly, it still requires arbitrarily distant qubit connectivity and numerical matrix inversion with dimensions that scale w.r.t required accuracy/free parameters. This is overcome by the Hardware efficient variational evolution algorithm (Section V.0.2), which includes only the nearest neighbor connectivity and does not require matrix inversion. Presented algorithms can systematically be tuned for accuracy; either by increasing the number of qubits or by increasing the number of parameters without dramatic change in depth of the circuits.

A good choice of variational ansatz is crucial for the proposed method. Future work could focus on further exploration of better anzats for parameterized quantum circuits for state preparations that are specifically tuned and inspired for option curves. For example, one could find shorter depth circuits that might not be expressive in exploring the entire Hilbert space, but do occupy just the space needed to represent option prices for the time span of interest. Other imaginary time evolution methods, such as the one introduced in RefMotta et al. (2019); Gomes et al. (2020); Yao et al. (2020) could be explored further as an alternative to the method presented above.

VIII Acknowledgement

We thank Oktay Goktas, Edwin Tham, Faiyaz Hasan, Cara Alexander and Jalani Kanem for useful discussions regarding both quantum and classical option pricing. We are grateful to Elliot Macgowan for his useful feedback on the manuscript. Numerical results in this study were performed using IBM Quantum’s Qiskit SDKAbraham et al. (2019). We were informed of similar work done in RefKubo et al. (2020), while preparing the manuscript.

*

Appendix A Hamiltonian approximation

As shown in Eq. 6 and Eq. 8 evaluation of and involves evolution of the kinetic energy operator . Given a small number , the derivative of order for a singlevariate function satisfies the equationHildebrand (1987)

| (21) |

where , and , are integers with greatest common divisor . This leads to three main categories of numerical approximations. Forward-difference methods, where . Backward-difference methods, when and finally mixed difference when . Note that in the case of forward difference and back difference, the resulting approximate differential matrix is bound to be not symmetric and hence non hermitian. Although non hermitian Hamiltonians can be simulated by variational hilbert space evolution algorithmEndo et al. (2020), we here choose the simpler mixed difference approximation where the resulting differential operator can be made hermitian. We choose the special choice that , which is often referred to as central difference method. We use , to reduce the discretized form of kinetic energy operator

| (22) |

where . This results in our Hamiltonian being in hermitian tridiagonal form given by

| (23) |

where is the required boundary condition. Note that one can systematically improve this approximation by increasing and . This comes at the cost of increasing the number of terms in the pauli decomposition and thus increases the size of the matrix and in Eq. 10. For example, one can make approximation by setting which results in pentadiognal band matrix with diagonal elements and off diagonal elements given by and . Note that the form of Eq. 21 forces all resulting approximations to result in sparse matrices which are computationally tractable. Further more, the same univariate derivative euler approximation is also used in approximating time derivativeEq. 10 resulting in errors of oder . Thus in the classical case, one need to choose time and spatial discretization that approximately satisfies to have similar orders of accuracy.

References

- Black and Scholes (1973) F. Black and M. Scholes, Journal of political economy 81, 637 (1973).

- Cox et al. (1979) J. C. Cox, S. A. Ross, and M. Rubinstein, Journal of financial Economics 7, 229 (1979).

- Rendleman (1979) R. J. Rendleman, The Journal of Finance 34, 1093 (1979).

- (4) C. Reisinger and R. Wissmann, .

- Boyle (1977) P. P. Boyle, Journal of financial economics 4, 323 (1977).

- Giles (2015) M. B. Giles, Acta Numerica 24, 259 (2015).

- L’Ecuyer (2009) P. L’Ecuyer, Finance and Stochastics 13, 307 (2009).

- Broadie and Detemple (1996) M. Broadie and J. Detemple, The Review of Financial Studies 9, 1211 (1996).

- Grant et al. (1997) D. Grant, G. Vora, and D. Weeks, Management Science 43, 1589 (1997).

- Ibanez and Zapatero (2004) A. Ibanez and F. Zapatero, Journal of Financial and Quantitative Analysis , 253 (2004).

- De Spiegeleer et al. (2018) J. De Spiegeleer, D. B. Madan, S. Reyners, and W. Schoutens, Quantitative Finance 18, 1635 (2018).

- Ferguson and Green (2018) R. Ferguson and A. Green, arXiv preprint arXiv:1809.02233 (2018).

- Hahn (2013) J. T. Hahn, Option pricing using artificial neural networks: an Australian perspective (Citeseer, 2013).

- McGhee (2018) W. A. McGhee, Available at SSRN 3288882 (2018).

- Preskill (2018) J. Preskill, Quantum 2, 79 (2018).

- Biamonte et al. (2017) J. Biamonte, P. Wittek, N. Pancotti, P. Rebentrost, N. Wiebe, and S. Lloyd, Nature 549, 195 (2017).

- Havlíček et al. (2019) V. Havlíček, A. D. Córcoles, K. Temme, A. W. Harrow, A. Kandala, J. M. Chow, and J. M. Gambetta, Nature 567, 209 (2019).

- Gao et al. (2018) X. Gao, Z.-Y. Zhang, and L.-M. Duan, Science advances 4, eaat9004 (2018).

- Ganzhorn et al. (2019) M. Ganzhorn, D. Egger, P. Barkoutsos, P. Ollitrault, G. Salis, N. Moll, M. Roth, A. Fuhrer, P. Mueller, S. Woerner, I. Tavernelli, and S. Filipp, Phys. Rev. Applied 11, 044092 (2019).

- Kandala et al. (2017) A. Kandala, A. Mezzacapo, K. Temme, M. Takita, M. Brink, J. M. Chow, and J. M. Gambetta, Nature 549, 242 (2017).

- Moll et al. (2018) N. Moll, P. Barkoutsos, L. S. Bishop, J. M. Chow, A. Cross, D. J. Egger, S. Filipp, A. Fuhrer, J. M. Gambetta, M. Ganzhorn, et al., Quantum Science and Technology 3, 030503 (2018).

- Parrish et al. (2019) R. M. Parrish, J. T. Iosue, A. Ozaeta, and P. L. McMahon, “A jacobi diagonalization and anderson acceleration algorithm for variational quantum algorithm parameter optimization,” (2019), arXiv:1904.03206 [quant-ph] .

- Rebentrost and Lloyd (2018) P. Rebentrost and S. Lloyd, “Quantum computational finance: quantum algorithm for portfolio optimization,” (2018), arXiv:1811.03975 [quant-ph] .

- Woerner and Egger (2019) S. Woerner and D. J. Egger, npj Quantum Information 5 (2019), 10.1038/s41534-019-0130-6.

- Egger et al. (2020) D. J. Egger, R. G. Gutierrez, J. C. Mestre, and S. Woerner, IEEE Transactions on Computers , 1 (2020).

- Zoufal et al. (2019) C. Zoufal, A. Lucchi, and S. Woerner, npj Quantum Information 5 (2019), 10.1038/s41534-019-0223-2.

- Martin et al. (2019) A. Martin, B. Candelas, Ángel Rodríguez-Rozas, J. D. Martín-Guerrero, X. Chen, L. Lamata, R. Orús, E. Solano, and M. Sanz, “Towards pricing financial derivatives with an ibm quantum computer,” (2019), arXiv:1904.05803 [quant-ph] .

- Kaneko et al. (2020) K. Kaneko, K. Miyamoto, N. Takeda, and K. Yoshino, “Quantum pricing with a smile: Implementation of local volatility model on quantum computer,” (2020), arXiv:2007.01467 [quant-ph] .

- Rebentrost et al. (2018) P. Rebentrost, B. Gupt, and T. R. Bromley, Phys. Rev. A 98, 022321 (2018).

- Stamatopoulos et al. (2020) N. Stamatopoulos, D. J. Egger, Y. Sun, C. Zoufal, R. Iten, N. Shen, and S. Woerner, Quantum 4, 291 (2020).

- Brassard et al. (2002) G. Brassard, M. Mosca, and A. Tapp, (2002).

- Suzuki et al. (2020) Y. Suzuki, S. Uno, R. Raymond, T. Tanaka, T. Onodera, and N. Yamamoto, Quantum Information Processing 19 (2020), 10.1007/s11128-019-2565-2.

- Brown et al. (2020) E. G. Brown, O. Goktas, and W. K. Tham, “Quantum amplitude estimation in the presence of noise,” (2020), arXiv:2006.14145 [quant-ph] .

- Vazquez and Woerner (2020) A. C. Vazquez and S. Woerner, “Efficient state preparation for quantum amplitude estimation,” (2020), arXiv:2005.07711 [quant-ph] .

- Merton (1973) R. C. Merton, The Bell Journal of economics and management science , 141 (1973).

- Bagarello (2020) F. Bagarello, Mathematical Physics, Analysis and Geometry 23, 1 (2020).

- (37) J. Vecer, .

- McClean et al. (2018) J. R. McClean, S. Boixo, V. N. Smelyanskiy, R. Babbush, and H. Neven, Nature Communications 9 (2018), 10.1038/s41467-018-07090-4.

- Benedetti et al. (2020) M. Benedetti, M. Fiorentini, and M. Lubasch, “Hardware-efficient variational quantum algorithms for time evolution,” (2020), arXiv:2009.12361 [quant-ph] .

- Endo et al. (2020) S. Endo, J. Sun, Y. Li, S. C. Benjamin, and X. Yuan, Physical Review Letters 125, 010501 (2020).

- McLachlan (1964) A. McLachlan, Molecular Physics 8, 39 (1964).

- Yuan et al. (2019) X. Yuan, S. Endo, Q. Zhao, Y. Li, and S. C. Benjamin, Quantum 3, 191 (2019).

- Li and Benjamin (2017) Y. Li and S. C. Benjamin, Physical Review X 7, 021050 (2017).

- Nakanishi et al. (2020) K. M. Nakanishi, K. Fujii, and S. Todo, Phys. Rev. Research 2, 043158 (2020).

- Vidal and Theis (2018) J. G. Vidal and D. O. Theis, “Calculus on parameterized quantum circuits,” (2018), arXiv:1812.06323 [quant-ph] .

- Ostaszewski et al. (2019) M. Ostaszewski, E. Grant, and M. Benedetti, “Quantum circuit structure learning,” (2019), arXiv:1905.09692 [quant-ph] .

- Stokes et al. (2020) J. Stokes, J. Izaac, N. Killoran, and G. Carleo, Quantum 4, 269 (2020).

- Wilczek and Shapere (1989) F. Wilczek and A. Shapere, Geometric phases in physics, Vol. 5 (World Scientific, 1989).

- Hackl et al. (2020) L. Hackl, T. Guaita, T. Shi, J. Haegeman, E. Demler, and I. Cirac, arXiv preprint arXiv:2004.01015 (2020).

- Koczor and Benjamin (2019) B. Koczor and S. C. Benjamin, arXiv preprint arXiv:1912.08660 (2019).

- Motta et al. (2019) M. Motta, C. Sun, A. T. K. Tan, M. J. O’Rourke, E. Ye, A. J. Minnich, F. G. S. L. Brandão, and G. K.-L. Chan, Nature Physics 16, 205 (2019).

- Gomes et al. (2020) N. Gomes, F. Zhang, N. F. Berthusen, C.-Z. Wang, K.-M. Ho, P. P. Orth, and Y. Yao, Journal of Chemical Theory and Computation 16, 6256 (2020).

- Yao et al. (2020) Y.-X. Yao, N. Gomes, F. Zhang, T. Iadecola, C.-Z. Wang, K.-M. Ho, and P. P. Orth, arXiv preprint arXiv:2011.00622 (2020).

- Abraham et al. (2019) H. Abraham, AduOffei, R. Agarwal, I. Y. Akhalwaya, G. Aleksandrowicz, T. Alexander, M. Amy, E. Arbel, Arijit02, A. Asfaw, A. Avkhadiev, C. Azaustre, AzizNgoueya, A. Banerjee, A. Bansal, P. Barkoutsos, A. Barnawal, G. Barron, G. S. Barron, L. Bello, Y. Ben-Haim, D. Bevenius, A. Bhobe, L. S. Bishop, C. Blank, S. Bolos, S. Bosch, Brandon, S. Bravyi, Bryce-Fuller, D. Bucher, A. Burov, F. Cabrera, P. Calpin, L. Capelluto, J. Carballo, G. Carrascal, A. Chen, C.-F. Chen, E. Chen, J. C. Chen, R. Chen, J. M. Chow, S. Churchill, C. Claus, C. Clauss, R. Cocking, F. Correa, A. J. Cross, A. W. Cross, S. Cross, J. Cruz-Benito, C. Culver, A. D. Córcoles-Gonzales, S. Dague, T. E. Dandachi, M. Daniels, M. Dartiailh, DavideFrr, A. R. Davila, A. Dekusar, D. Ding, J. Doi, E. Drechsler, Drew, E. Dumitrescu, K. Dumon, I. Duran, K. EL-Safty, E. Eastman, G. Eberle, P. Eendebak, D. Egger, M. Everitt, P. M. Fernández, A. H. Ferrera, R. Fouilland, FranckChevallier, A. Frisch, A. Fuhrer, B. Fuller, M. GEORGE, J. Gacon, B. G. Gago, C. Gambella, J. M. Gambetta, A. Gammanpila, L. Garcia, T. Garg, S. Garion, A. Gilliam, A. Giridharan, J. Gomez-Mosquera, Gonzalo, S. de la Puente González, J. Gorzinski, I. Gould, D. Greenberg, D. Grinko, W. Guan, J. A. Gunnels, M. Haglund, I. Haide, I. Hamamura, O. C. Hamido, F. Harkins, V. Havlicek, J. Hellmers, Ł. Herok, S. Hillmich, H. Horii, C. Howington, S. Hu, W. Hu, J. Huang, R. Huisman, H. Imai, T. Imamichi, K. Ishizaki, R. Iten, T. Itoko, JamesSeaward, A. Javadi, A. Javadi-Abhari, W. Javed, Jessica, M. Jivrajani, K. Johns, S. Johnstun, Jonathan-Shoemaker, V. K, T. Kachmann, A. Kale, N. Kanazawa, Kang-Bae, A. Karazeev, P. Kassebaum, J. Kelso, S. King, Knabberjoe, Y. Kobayashi, A. Kovyrshin, R. Krishnakumar, V. Krishnan, K. Krsulich, P. Kumkar, G. Kus, R. LaRose, E. Lacal, R. Lambert, J. Lapeyre, J. Latone, S. Lawrence, C. Lee, G. Li, D. Liu, P. Liu, Y. Maeng, K. Majmudar, A. Malyshev, J. Manela, J. Marecek, M. Marques, D. Maslov, D. Mathews, A. Matsuo, D. T. McClure, C. McGarry, D. McKay, D. McPherson, S. Meesala, T. Metcalfe, M. Mevissen, A. Meyer, A. Mezzacapo, R. Midha, Z. Minev, A. Mitchell, N. Moll, J. Montanez, G. Monteiro, M. D. Mooring, R. Morales, N. Moran, M. Motta, MrF, P. Murali, J. Müggenburg, D. Nadlinger, K. Nakanishi, G. Nannicini, P. Nation, E. Navarro, Y. Naveh, S. W. Neagle, P. Neuweiler, J. Nicander, P. Niroula, H. Norlen, NuoWenLei, L. J. O’Riordan, O. Ogunbayo, P. Ollitrault, R. Otaolea, S. Oud, D. Padilha, H. Paik, S. Pal, Y. Pang, V. R. Pascuzzi, S. Perriello, A. Phan, F. Piro, M. Pistoia, C. Piveteau, P. Pocreau, A. Pozas-iKerstjens, M. Prokop, V. Prutyanov, D. Puzzuoli, J. Pérez, Quintiii, R. I. Rahman, A. Raja, N. Ramagiri, A. Rao, R. Raymond, R. M.-C. Redondo, M. Reuter, J. Rice, M. Riedemann, M. L. Rocca, D. M. Rodríguez, RohithKarur, M. Rossmannek, M. Ryu, T. SAPV, SamFerracin, M. Sandberg, H. Sandesara, R. Sapra, H. Sargsyan, A. Sarkar, N. Sathaye, B. Schmitt, C. Schnabel, Z. Schoenfeld, T. L. Scholten, E. Schoute, J. Schwarm, I. F. Sertage, K. Setia, N. Shammah, Y. Shi, A. Silva, A. Simonetto, N. Singstock, Y. Siraichi, I. Sitdikov, S. Sivarajah, M. B. Sletfjerding, J. A. Smolin, M. Soeken, I. O. Sokolov, I. Sokolov, SooluThomas, Starfish, D. Steenken, M. Stypulkoski, S. Sun, K. J. Sung, H. Takahashi, T. Takawale, I. Tavernelli, C. Taylor, P. Taylour, S. Thomas, M. Tillet, M. Tod, M. Tomasik, E. de la Torre, K. Trabing, M. Treinish, TrishaPe, D. Tulsi, W. Turner, Y. Vaknin, C. R. Valcarce, F. Varchon, A. C. Vazquez, V. Villar, D. Vogt-Lee, C. Vuillot, J. Weaver, J. Weidenfeller, R. Wieczorek, J. A. Wildstrom, E. Winston, J. J. Woehr, S. Woerner, R. Woo, C. J. Wood, R. Wood, S. Wood, S. Wood, J. Wootton, D. Yeralin, D. Yonge-Mallo, R. Young, J. Yu, C. Zachow, L. Zdanski, H. Zhang, C. Zoufal, Zoufalc, a kapila, a matsuo, bcamorrison, brandhsn, nick bronn, brosand, chlorophyll zz, csseifms, dekel.meirom, dekelmeirom, dekool, dime10, drholmie, dtrenev, ehchen, elfrocampeador, faisaldebouni, fanizzamarco, gabrieleagl, gadial, galeinston, georgios ts, gruu, hhorii, hykavitha, jagunther, jliu45, jscott2, kanejess, klinvill, krutik2966, kurarrr, lerongil, ma5x, merav aharoni, michelle4654, ordmoj, sagar pahwa, rmoyard, saswati qiskit, scottkelso, sethmerkel, shaashwat, sternparky, strickroman, sumitpuri, tigerjack, toural, tsura crisaldo, vvilpas, welien, willhbang, yang.luh, yotamvakninibm, and M. Čepulkovskis, “Qiskit: An open-source framework for quantum computing,” (2019).

- Kubo et al. (2020) K. Kubo, Y. O. Nakagawa, S. Endo, and S. Nagayama, arXiv preprint arXiv:2012.04429 (2020).

- Hildebrand (1987) F. B. Hildebrand, Introduction to numerical analysis (Courier Corporation, 1987).