High-Dimensional Low-Rank Tensor Autoregressive Time Series Modeling

Abstract

Modern technological advances have enabled an unprecedented amount of structured data with complex temporal dependence, urging the need for new methods to efficiently model and forecast high-dimensional tensor-valued time series. This paper provides a new modeling framework to accomplish this task via autoregression (AR). By considering a low-rank Tucker decomposition for the transition tensor, the proposed tensor AR can flexibly capture the underlying low-dimensional tensor dynamics, providing both substantial dimension reduction and meaningful multi-dimensional dynamic factor interpretations. For this model, we first study several nuclear-norm-regularized estimation methods and derive their non-asymptotic properties under the approximate low-rank setting. In particular, by leveraging the special balanced structure of the transition tensor, a novel convex regularization approach based on the sum of nuclear norms of square matricizations is proposed to efficiently encourage low-rankness of the coefficient tensor. To further improve the estimation efficiency under exact low-rankness, a non-convex estimator is proposed with a gradient descent algorithm, and its computational and statistical convergence guarantees are established. Simulation studies and an empirical analysis of tensor-valued time series data from multi-category import-export networks demonstrate the advantages of the proposed approach.

Abstract

This supplementary material provides all technical proofs and details about the algorithms for the proposed LTR and (T)SSN estimators. To be specific, Appendix S1 presents the proofs of theoretical results for the nuclear-norm-regularized estimators in Section 3 of the main paper, while Appendix S2 gives the proofs of the non-convex approach in Section 4. Appendix S3 presents the ADMM algorithm for the (T)SSN estimator. Finally, Appendix S4 discusses two special cases of the proposed LRTAR model and their connections with some existing models in the literature.

aSchool of Mathematical Sciences, Shanghai Jiao Tong University, China

bDepartment of Statistics, University of Connecticut, United States of America

cDepartment of Statistics and Actuarial Science, University of Hong Kong, China

Keywords: global trade flows; high-dimensional time series; non-convex tensor regression; nuclear norm; tensor decomposition; tensor-valued time series

1 Introduction

The rapid improvement in data collection capability has enabled the generation of increasingly more comprehensive economic datasets. Meanwhile, significant progress has been made in unifying data collection standards. These advances have led to an abundance of comparable disaggregated time series datasets across countries, which are further categorized by various dimensions like regions, industries, goods categories, and demographics. Such multidimensional datasets can often be organized as multi-way arrays, forming tensor-valued time series. Moreover, this type of detailed time series data is common in finance, where it can be formed, e.g., by categorizing stock returns based on various firm characteristics dimensions, or asset returns across asset classes, regions, and sectors. The availability of extensive disaggregated data, in turn, provides new opportunities to advance techniques for modeling complex dynamic systems like the global economy and financial markets.

The motivation behind the study of tensor-valued time series stems from the modeling of temporal and cross-sectional dependencies in panel data. To illustrate, first consider the panel data for countries, where represents time, and is a vector containing observations of different economic variables for country with . For example, Bussière et al., (2012) models the international trade by fitting a Global Vector Autoregressive (GVAR) model (Pesaran et al.,, 2004) to which includes the aggregate export and import volumes of country , and , as key variables. Compared to previous methods, Bussière et al., (2012)’s approach has two major strengths: (1) it captures interdependencies across countries, i.e. cross-country spillovers; (2) it jointly models exports and imports, allowing for co-movements between them, which is important as exporting firms typically import components.

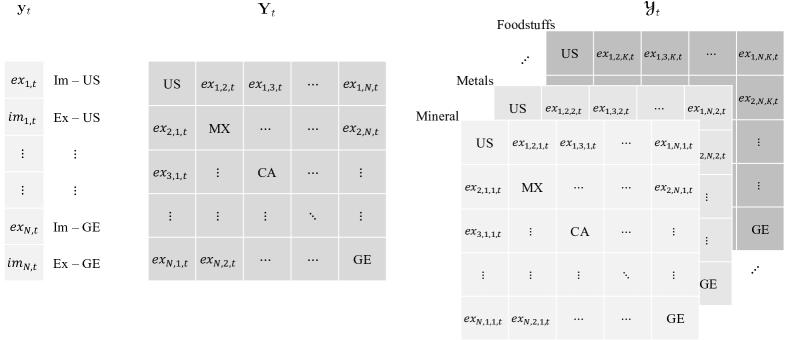

However, aggregate-level exports and imports data are limited in providing a comprehensive understanding of global trade dynamics. They do not provide information about how exports from one country are distributed among importing countries. By contrast, a much more detailed perspective on the trade flows can be gained from the disaggregated data , where represents exports from one specific country (country ) to another specific country (country ) for all possible pairs of countries. Note that is an matrix-valued time series, and by convention ’s are set to zero. Since and , the disaggregated series contains all information of the aggregate series. Furthermore, we can have an even more granular view by further breaking down into additional dimensions. For instance, the data can be divided into different product categories, resulting in the tensor-valued time series , where represents exports of product category from country to country ; see Figure 1 for an illustration.

More broadly, this paper considers autoregressive modeling of a general tensor-valued time series , where the total number of series can be much larger than . A naïve method is to apply models for panel data to the vectorized series , such as the vector autoregressive (VAR) model,

| (1) |

and then perform dimension reduction for the unknown transition matrix via generic regularization methods such as the Lasso (Basu and Michailidis,, 2015; Han et al.,, 2015), or data-specific methods (Pesaran et al.,, 2004; Canova and Ciccarelli,, 2013; Guo et al.,, 2016; Zhu et al.,, 2017; Zheng and Cheng,, 2021) which impose parameter restrictions based on pre-determined network structures. However, the vectorization undermines the model interpretability that could have been a valuable advantage of multi-dimensional data. For example, it would be much easier to gain meaningful insights into the global trade flow from the multi-category import-export data mentioned above if patterns across exporting countries, importing countries, and product categories can be separately interpreted. In particular, adopting a multi-dimensional approach, as proposed in this paper, enables us to address the following questions, which cannot be answered using the vector model:

-

(i)

Among all countries, whose exporting activities are the driving forces of the global trade flow? Are there any geographical groupings among them?

-

(ii)

Similar to (i), what about the importing activities?

-

(iii)

Among all product categories, which ones are the driving forces of the global trade flow? Are there any grouping patterns?

-

(iv)

Do the past and present states of the dynamic system (i.e., predictor and response) have the same grouping patterns across exporting countries, importing countries, and product categories?

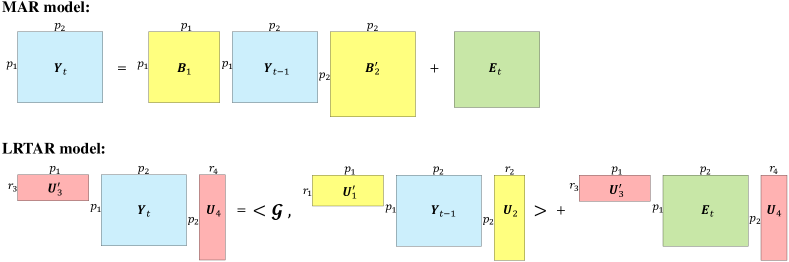

Specifically, for the tensor-valued time series , this paper proposes the Low-Rank Tensor Autoregressive (LRTAR) model by folding the transition matrix in (1), with , into the -th-order transition tensor which is assumed to have Tucker ranks with being possibly much smaller than , where for . This implies the Tucker decomposition , where and , and consequently the low-dimensional structure of the process as follows:

where and can be viewed as and factors summarizing the dynamic information across all dimensions. Moreover, each loading matrix reveals interpretable patterns for a particular dimension of the present or past state of ; see Section 2.4 for more detailed descriptions in the context of import-export data. The proposed model has the following features:

-

•

Similar to panel data models, it captures both cross-sectional and temporal dependencies. However, by leveraging the tensor structure, it dissects the cross-sectional information into different dimensions, allowing for separate interpretations in each dimension.

-

•

Simultaneous dimension reduction is achieved across all dimensions of the transition tensor via the low-Tucker-rank assumption. This approach does not rely on predetermined parameter restrictions derived from the user’s prior knowledge or beliefs about the network structure.

-

•

The low-Tucker-rank assumption implies that factors are extracted across all dimensions of the response and its lagged predictor. The factor loadings facilitate the discernment of patterns in each dimension (i.e., mode) of the tensor-valued observation.

For the proposed model, this paper introduces two types of high-dimensional estimation methods: (i) convex estimators via nuclear norm regularizations and (ii) the non-convex estimator. For (i), we consider the general setting where the transition tensor is approximately low-rank, and develop convex estimation methods based on different nuclear norm regularizations. Firstly, to encourage low-rankness along all modes, we study the widely-used Sum of Nuclear (SN) norm regularizer, defined as the sum of nuclear norms of all one-mode matricizations. However, due to the fat-and-short shape of the one-mode matricizations, the SN regularized estimator suffers from serious efficiency loss and hence performs even worse than the conventional Matrix Nuclear (MN) norm regularized estimator (Negahban and Wainwright,, 2011) which simply penalizes the nuclear norm of the transition matrix in (1). Thus, we further introduce a novel Sum of Square-matrix Nuclear (SSN) norm regularizer, defined as the sum of nuclear norms of all square matricizations of . The SSN reguarlized estimator is provably more efficient than the SN regularized one; see Theorem 3 and the first simulation experiment in Section 5.1. In addition, we propose a truncated variants of the SSN estimator and prove its rank selection consistency when is exactly low-Tucker-rank under mild conditions.

However, the consistency of the SSN estimator requires that grows faster than . Thus, it may not be applicable to high-dimensional tensor-valued time series datasets with large ’s. This motivates us to consider a non-convex estimation method to further improve the estimation efficiency and relax the sample size requirement. Specifically, under the assumption that is exactly low-rank, this paper develops an estimator via non-convex (NC) optimization based on the explicit Tucker decomposition structure. A gradient descent algorithm is proposed for the NC estimator, with rigorous statistical and computational convergence guarantees. Compared with the convex estimators via nuclear norm regularizations, the consistency of the NC estimator only requires that grows faster than , which makes it attractive under high dimensionality. Although this approach requires initial values and known tensor ranks, the ridge-type ratio estimator can be used for determination of tensor ranks and initialization of the gradient descent algorithm.

This work is related to the literature on matrix-variate regression and tensor regression for independent data. The matrix-variate regression in Ding and Cook, (2018) has the same basic bilinear form, while an envelope method was introduced to further reduce the dimension. Raskutti et al., (2019) proposed a multi-response tensor regression model, where they mainly studied the third-order coefficient tensor and the SN regularization which is known to be statistically sub-optimal for higher-order tensor estimation. By contrast, we study the model for general higher-order tensor-valued time series. Moreover, our SSN estimator has a much faster statistical convergence rate than the SN estimator. For the non-convex tensor estimation problem, Chen et al., (2019) and Han et al., (2022) studied non-convex projected gradient descent methods for tensor regression. Our NC estimator can be viewed as a higher-order extension of the estimation approach in Han et al., (2022). In addition, existing literature on tensor regression has only considered independent data or Gaussian time series data, whereas we allow sub-Gaussianity of the time series. This is a non-trivial relaxation, since unlike the Gaussian case, sub-Gaussian time series cannot be linearly transformed into independent samples.

The rest of the paper is organized as follows. Section 2.1 introduces basic notation and tensor algebra. Section 2.2 presents the proposed LRTAR model. A series of nuclear-norm-regularized estimation methods are covered in Section 3, where we develop the non-asymptotic theory for three regularized estimators and rank selection consistency for the truncated estimator. Section 4 proposes a non-convex estimation approach and presents its computational guarantees and statistical efficiency improvement. Section 5 presents simulation studies and a real data analysis. Section 6 concludes with a brief discussion. We provide all technical proofs, algorithms, and additional discussions in a separate online supplementary file.

2 Tensor Decomposition and Tensor Autoregression

2.1 Preliminaries: Notation and Tensor Algebra

Tensors, also known as multi-dimensional arrays, are natural higher-order extensions of matrices. The order of a tensor is known as the dimension, way or mode, so a multi-dimensional array is called an -th order tensor. We introduce some important notations and concepts of tensor operation in this subsection, and refer readers to Kolda and Bader, (2009) for a detailed review of basic tensor algebra.

Throughout this paper, we denote vectors by boldface small letters, e.g. , , matrices by boldface capital letters, e.g. , , and tensors by boldface Euler capital letters, e.g. , . For any two real-valued sequences and , we write if there exists a constant such that for all , and write if . In addition, write if and . We use to denote a generic positive constant, which is independent of the dimensions and the sample size.

For a generic matrix , we let , , , , , and denote its transpose, Frobenius norm, operator norm, nuclear norm, vectorization, and -th largest singular value, respectively. For any matrix , recall that the nuclear norm and its dual norm, the operator norm, are defined as

| (2) |

For any square matrix , we let and denote its minimum and maximum eigenvalues. For any real symmetric matrices and , we write if is a positive semidefinite matrix.

Matricization, also known as unfolding, is the process of reordering the elements of a third- or higher-order tensor into a matrix. The most commonly used matricization is the one-mode matricization defined as follows. For any -th-order tensor , its mode- matricization , with , is the matrix obtained by setting the -th tensor mode as its rows and collapsing all the others into its columns, for . Specifically, the -th element of is mapped to the -th element of , where

| (3) |

The above one-mode matricization can be extended to the multi-mode matricization by combining multiple modes to rows and combining the rest to columns of a matrix. For any index subset , the multi-mode matricization is the -by- matrix whose -th element is mapped from the -th element of , where

| (4) |

Note that the modes in the multi-mode matricization are collapsed following their original order . Moreover, it holds , where is the complement of . In addition, the one-mode matricization defined above is simply .

We next review the concepts of tensor-matrix multiplication, tensor generalized inner product and norm. For any -th-order tensor and matrix with , the mode- multiplication produces an -th-order tensor in defined by

| (5) |

For any two tensors and with , their generalized inner product is the -th-order tensor in defined by

| (6) |

where . In particular, when , it reduces to the conventional real-valued inner product. In addition, the Frobenius norm of any tensor is defined as .

Some basic properties of the tensor generalized inner product are as follows. Let , , and be tensors with . If , then . If with , then . Moreover,

| (7) |

where , and when , .

Finally, we summarize some concepts and useful results of the Tucker decomposition (Tucker,, 1966; De Lathauwer et al.,, 2000). For any tensor , its Tucker ranks are defined as the matrix ranks of its one-mode matricizations, namely , for . Note that ’s are analogous to the row and column ranks of a matrix, but are not necessarily equal for third- and higher-order tensors. However, the Tucker ranks must satisfy the condition

| (8) |

If only one of the ’s is equal to the maximum rank , (8) is equivalent to ; that is, the maximum Tucker rank must be no greater than the product of the other ranks.

Suppose that has Tucker ranks . Then has the following Tucker decomposition:

| (9) |

where for are the factor matrices and is the core tensor. If has the Tucker decomposition in (9), then we have the following results for its one- and multi-mode matricizations:

| (10) |

and

| (11) |

where and are matrix Kronecker products operating in the reverse order within the corresponding index sets.

2.2 Low-Rank Tensor Autoregression

For the tensor-valued time series , we propose the following Low-Rank Tensor Autoregressive (LRTAR) model:

| (12) |

where is the -th-order transition tensor which is assumed to have Tucker ranks with , is the generalized tensor inner product defined in (6) with and , and is the mean-zero random error at time with possible dependencies among its contemporaneous elements.

By Section 2.1, admits the following Tucker decomposition:

| (13) |

where is the core tensor, and are factor matrices for . Note that for any nonsingular matrices for , it holds

Thus, although the coefficient tensor in (12) is identifiable, its Tucker decomposition in (13) suffers from rotational indeterminacy. To pin down the rotation matrices ’s, a special Tucker decomposition, called the higher-order singular value decomposition (HOSVD), is commonly considered (Kolda and Bader,, 2009). In the HOSVD, the factor matrix is defined as the tall orthonormal matrix consisting of the top left singular vectors of , for . This further implies that the core tensor has the all-orthogonal property as follows: is a diagonal matrix for . We will formally discuss the identification conditions of and ’s in Section 2.3.

Denote and . Note that by (7), model (12) can be written into the VAR form in (1) with transition matrix , i.e.,

| (14) |

where and .

By the VAR representation in (14), we immediately have the necessary and sufficient condition for the existence of a unique strictly stationary solution to model (12) as follows.

Assumption 1.

The spectral radius of is strictly less than one.

2.3 Model Identification

To measure the extent of dimension reduction for the parameter space through the low-Tucker-rank assumption on , it is necessary to rule out the rotational indeterminacy of the Tucker decomposition. As mentioned in Section 2.2, the HOSVD can be used to solve the rotational indeterminacy. Specifically, under the HOSVD, we have

| (15) |

for . Thus, (15) provides a convenient way for us to compute the effective number of degrees of freedom for the proposed LRTAR model. Specifically, by subtracting the number of constraints induced by (15) from the total number of parameters in and ’s, we can obtain that the effective number of degrees of freedom for model (12) is

| (16) |

This is substantially smaller than the total number of parameters in , i.e., , with . For the example with and , if , then the number of parameters will be reduced from to 280.

While the HOSVD avoids the rotational indeterminacy, it is still not necessarily unique in general. It is possible, however, to guarantee the uniqueness of the HOSVD under the additional assumption that the singular values of each one-mode matricization are distinct for . Under this assumption, each contains the left singular vectors of corresponding to the largest singular values which are all distinct. To further avoid the indeterminacy due to sign switches of the singular vectors, it suffices to require that the first nonzero element in each column of is positive. As a result, such an HOSVD will be unique.

However, despite the non-uniqueness of the Tucker decomposition, the transition tensor itself is uniquely defined. Thus, the identification problem will not be an issue for the estimation of the low-Tucker-rank tensor . Indeed, in Sections 3 and 4, we will introduce two types of methods to estimate . None of them requires a unique Tucker decomposition of . In practice, we can first obtain a consistent estimator by the methods in Sections 3 and 4, i.e., , or , and then apply the HOSVD to to obtain the corresponding unique estimates and ’s. That is, is calculated as the top left singular vectors of with the first nonzero element in each column being positive, and .

Furthermore, it is worth noting that the column space of is unique and identifiable, although suffers from rotational indeterminacy; this is similar to the loading matrix in factor models. Thus, we can treat and to be equivalent for any orthogonal rotation , as they correspond to the same factor interpretation. Moreover, for the orthonormal matrix , is the projection matrix of its column space. This projection matrix is unique and identifiable as for any orthogonal matrix . Hence, in practice, we can use the unique projection matrix to interpret the estimated low-dimensional factor loadings; see the empirical analysis in Section 5.2.

2.4 Multi-Dimensional Dynamic Factor Interpretations

To illustrate the interpretation of the proposed LRTAR model, we consider the monthly import-export data among 22 countries for 15 product categories studied in Chen et al., (2022), where is the observed Export-Import-Product tensor in month , with the -th entry of corresponding to the export of product from country to country ; see Section 5.2 for a detailed analysis of this dataset.

For simplicity, we first consider the proposed model with for the data obtained by aggregating all 15 product categories, denoted , where each row represents an exporting country and each column represents an importing country. In this case, , where , with being much smaller than 22, and . Suppose that ’s satisfy (15). Then the proposed LRTAR model for the matrix-valued time series implies that

| (17) |

Note that in (17), and are both projected onto a low-dimensional space via and , while is projected onto another low-dimensional space via and . This provides a multi-dimensional dynamic factor interpretation of the import-export data as follows. According to (17), the dynamic of the international market is driven by the low-dimensional lagged (predictor) matrix factor , whereas the effect of the past information—encapsulated by the predictor tensor factor —on the present state of the market is manifested through the low-dimensional (response) matrix factor . For the predictor factor, and provide factor loadings along the directions of exporting and importing countries, respectively. Similarly, and provide those for the response factor. From a dynamical system point of view, the predictor factor and the response factor can be interpreted as the input and output of the economic system, respectively, while the core tensor characterizes the predictive relationship between and .

The factor interpertation also applies to the general case with . For the multi-category import-export data with , (17) is extended to

| (18) |

where and can be viewed as loadings of exporting countries, importing countries, and product categories for the predictor and response tensor factors, respectively. The predictor tensor factor drives the dynamic of the market, and the response tensor factor reflects the reaction of the market to the past information.

Remark 1.

In the literature on high-dimensional VAR models, a popular dimension reduction method is to impose sparsity on coefficients; see a recent review in Basu and Matteson, (2021). It is especially suitable for high-dimensional data where only a small subset of the variables are correlated, which is often the case in biological applications, e.g., the discovery of gene regulatory networks (Shojaie et al.,, 2012). However, in some economic and financial applications, most variables are expected to be somewhat correlated. This will often lead to many small but nonzero coefficient estimates under sparse estimation. As a result, the estimated sparse model could be hard to interpret. Rather, when pervasive cross-sectional dependency is observed in the data, it is probably more reasonable to assume that the variables in an economic or financial system are driven by some common factors. The LRTAR model provides the supervised multi-dimensional dynamic factor interpretation, which is the key advantage of the proposed model over the sparse modeling approach.

Remark 2.

While we focus on the lag-one tensor autoregression for simplicity, the proposed model can be readily extended to the case with a general lag order; see the discussion in Section 6.

Remark 3.

In Appendix S4 of the supplementary file, we further explore the relationship between the proposed LRTAR model and the tensor factor model in Chen et al., (2022). Note that the latter is an unsupervised learning method and cannot be used directly for forecasting, unless an explicit dynamic structure is imposed on the latent factor process. To build a connection with our model, we adapt the tensor factor model by assuming that their latent factor process follows an autoregressive model. We can show that the proposed model is more flexible than the tensor factor model with autoregressive factors.

3 Convex Estimation via Nuclear Norm Regularization

In Sections 3.1–3.3, we consider a series of convex estimation methods for the proposed model via different nuclear norm regularizations. Throughout the rest of this paper, the true value of the coefficient tensor is denoted by . While our estimation methods in Sections 3.1 and 3.2 will be developed from the exact low-Tucker-rank structure of the transition tensor, our theoretical analysis will allow to be approximately low-Tucker-rank, which includes the exact low-rankness as a special case. In other words, the proposed LRTAR model will be used as a working model.

3.1 Regularization via One-Mode Matricization

In model (12), the exactly low-rank transition tensor is subject to the constraints , for . A commonly used convex relaxation of such Tucker rank constraints is the regularization via the sum of nuclear (SN) norms of all the one-mode matricizations,

| (19) |

The SN norm has been widely used in the literature (Gandy et al.,, 2011; Tomioka et al.,, 2011; Liu et al.,, 2013; Raskutti et al.,, 2019) to simultaneously encourage the low-rankness for all modes of a tensor. This leads us to the SN norm regularized estimator

| (20) |

where is the tuning parameter. Note that if instead of , only one single nuclear norm, say , is penalized, then the resulting estimator will only encourage the low-rankness for the first mode of , while failing to do so for all the other modes, and hence will be less effective than the above SN estimator.

To derive the estimation error bound for , we make the following assumption on the random error .

Assumption 2.

Let , where is a sequence of random vectors, with and , and is a positive definite matrix. In addition, the entries of are mutually independent and -sub-Gaussian, i.e., , for any and .

Assumption 2 implies that are , which is standard in the literature on high-dimensional time series models. It may be relaxed to the weakly dependent case through strong mixing conditions as in Wong, (2017). The sub-Gaussianity condition in Assumption 2 is milder than the commonly used normality assumption in the literature (Basu and Michailidis,, 2015; Raskutti et al.,, 2019). This relaxation is made possible through establishing a novel martingale-based concentration bound in the proof of the deviation bound; see Lemma S5 in Appendix S1.4 of the supplementary file. The covariance matrix captures the contemporaneous dependency in , and the constant controls the tail heaviness of the marginal distributions.

For any , let be a matrix polynomial, where is the set of complex numbers. Let and , where is the conjugate transpose of . It can be shown that under Assumption 1; see also Basu and Michailidis, (2015) for more discussions on the connection between the spectral density of the VAR process and the two quantities. In addition, define the positive constants

Note that our theoretical analysis does not require , and to be fixed as the dimension grows.

In practice, it could be too stringent to assume that is exactly low-rank. In this section, we relax it to the following approximately low-rank assumption: We assume that all one-mode matricizations of the underlying true transition tensor belong to the set of approximately low-rank matrices, namely for some , where are the radii for all modes,

| (21) |

is the set of approximately low-rank matrices defined by the norm of the singular values, for , and for . For the convenience of notation, we let . Note that when , is the set of -by- rank- matrices. For , the restriction on requires that the singular values decay to zero under a polynomial rate, and it is more general than the exactly low-rank assumption.

Theorem 1.

By Theorem 1, when , the estimation error bound scales as ; note that the factor in the error bounds is canceled by the in the rate of . When , and are bounded, and , namely is exactly low-rank with Tucker ranks , the error bound reduces to and it is comparable to that in Tomioka et al., (2011) for tensor regression.

However, recent research in tensor analysis (e.g., Mu et al.,, 2014; Raskutti et al.,, 2019) shows that the SN norm regularization approach can be suboptimal. For our model, this is mainly because is an unbalanced fat-and-short matricization of a higher-order tensor. Specifically, an essential intermediate step in the proof of Theorem 1 is to establish the deviation bound, where we need to upper bound the operator norm of a sub-Gaussian random matrix with the same dimensions as ; see Lemma S5 in Appendix S1.3 of the supplementary file. The order of this operator norm will be dominated by the larger of the row and column dimensions of the matrix , and hence by the column dimension , which eventually appears in the error bound. As a result, the imbalance of the matricization leads to the efficiency bottleneck of the SN estimator.

On the other hand, since the reduced-rank VAR model can be regarded as an overparameterization of the proposed LRTAR model, alternatively one may focus on the low-rankness of the transition matrix in the VAR representation in (14), and adopt the matrix nuclear (MN) estimator (Negahban and Wainwright,, 2011) to estimate ,

| (23) |

where is the tuning parameter. Note that the multi-mode matricization is a square matrix. Thus, the loss of efficiency due to the unbalanced matricization can be avoided, which is confirmed by the following theorem.

Theorem 2.

Theorem 2 shows that, with , the estimation error bound for scales as , where is the singular value radius of . This result is comparable to that in Negahban and Wainwright, (2011) for reduced-rank VAR models, yet we relax both the singular value constraint and the normality assumption on the random error in their paper. This estimation error bound is clearly smaller than that in Theorem 1, as in general can be much larger than when . Therefore, adopting square matricization can indeed improve the estimation performance.

The idea of using square matricization to improve efficiency was adopted by Mu et al., (2014) in low-rank tensor completion problems. Their proposed method, called the square deal, is to first unfold a general higher-order tensor into a matrix with similar numbers of rows and columns, and then use the MN norm as the regularizer. However, despite the advantage of over , Theorem 2 reveals another drawback of . That is, the error bounds for will increase as the radius for the singular values of becomes larger. In other words, unless we have prior knowledge that the -“norm” of singular values of is truly small, may not be desirable in practice.

On the other hand, although the SN regularizer in (19) suffers from inefficiency due to the imbalance of one-mode matricizations, it has the attractive feature of simultaneously encouraging low-rankness across all modes of , and thus is more efficient than its counterpart which considers only one single one-mode matricization, say, . Similarly, if we can encourage low-rankness across all possible square matricizations of , the estimation performance may be further improved upon . This motivates us to propose a new regularization approach in the next subsection.

Remark 4.

Since our statistical theory is non-asymptotic, the dimensions ’s, approximate or exact Tucker ranks such as ’s in Theorem 1, and any other quantities appearing in the error bounds are all allowed to diverge to infinity. Our results show how these quantities explicitly affect the error bounds. However, for simplicity of understanding the convergence rates, one may assume that , and are fixed; see Table 1. For example, it is common to assume that . In addition, when the spectral radius of is bounded away from one, it can be shown that is also bounded away from zero.

3.2 Regularization via Square Matricization

Motivated by the discussion at the end of Section 3.1, we propose a novel convex regularizer which improves upon both SN and MN regularizers in (19) and (23), by simultaneously encouraging low-rankness across all possible square matricizations of .

For any -th-order tensor , its multi-mode matricization will be a square matrix, with , if the index set is chosen as

where each index is set to either or , for . For instance, is the square matricization formed by setting for all . Moreover, if has Tucker ranks , then the rank of the matricization is at most . Therefore, if we penalize the sum of nuclear norms of all such squares matricizations, which we call the sum of square-matrix nuclear (SSN) norms for simplicity, then the resulting estimator would enjoy the efficiency gain from both the use of square matricizations and simultaneous incorporation of many rank constraints.

Obviously, there are possible choices of the index set that corresponds to a square matricization . However, since , when defining the SSN norm, we only need to include one of and its complement . A simple way to do so is to choose only sets containing the index one. That is, fix and choose or for . This results in totally chosen index sets, denoted by . Note that . For example, when , we have four chosen index sets, and .

Based on the above choice of the index sets, we introduce the following SSN norm,

| (24) |

For a tuning parameter , the corresponding estimator is defined as

| (25) |

If the rank of one-mode matricizations , each square matricization is also low-rank with . Similarly, if all s are approximately low-rank, the square matricizations are approximately low-rank as well. In contrast to the SN norm in (19) which directly matches the Tucker ranks for , the SSN norm encourages the low-Tucker-rank structure of by simultaneously encouraging low-rankness of all square matricizations ’s. The following theorem gives the theoretical results for .

Theorem 3.

| SN | MN | SSN | |

|---|---|---|---|

| Sample size | |||

| Estimation error |

By Theorem 3, when , the estimation error bound scales as , and reduces to in the exactly low-rank setting for when , and are bounded. For a clearer comparison among the three estimators and , we summarize the main results of Theorems 1–3 in Table 1. First, both and have much smaller error bounds and less stringent sample size requirements than , due to the diverging dimension in the results of the latter. This reaffirms the advantage of the square matricizations.

Secondly, comparing to , since the factor in the error bounds of is the average of all for , can protect us from the bad scenarios where the -“norm” of the singular values of is relatively large. If all the ’s are of the same order, then the error upper bounds for and in Table 1 will be similar. However, our simulation results in Section 5.1 show that clearly outperforms under various settings, even when . Indeed, the error bounds for in Theorem 3 is likely to be loose, which is believed to be caused by taking the upper bounds on the dual norm of the SSN norm in the proof of Lemma S3; see Appendix S1.3 of the supplementary file for details. By contrast, the error bounds for are minimax-optimal (Negahban and Wainwright,, 2011). Therefore, although our theoretical results are not sharp enough to distinguish clearly between the error rates of and , we conjecture that the actual rate of the former is generally smaller than that of the latter. Methodologically, this is also easy to understand because, unlike , simultaneously encourages the low-rankness across all square matricizations of rather than just on .

Remark 5.

While our SSN regularization is proposed in the time series context, the idea of imposing joint penalties on all (close to) square matricizations of the coefficient tensor may be extended to general higher-order tensor estimation problems. It can also be refined to accommodate particular structures of the data. For example, if some of the modes of the tensor-value time series , namely , are equal, then even a greater number of possible square matricizations of can be formed, resulting in improved estimation efficiency.

3.3 Truncated Regularized Estimation

While the estimation methods in Sections 3.1 and 3.2 do not require exact low-rankness of the true transition tensor , sometimes imposing exact low-rankness is more desirable if one wants to interpret the underlying dynamic tensor factor structures. As discussed in Section 2.4, the Tucker ranks determine the dimensions of the dynamic factors. For greater model interpretability, we further consider the case that is exactly low-rank and propose a truncation method to consistently estimate its true Tucker ranks .

Let be a threshold parameter to be chosen properly. Given the estimator , for each , we calculate the singular value decomposition (SVD) of the mode- matricization with the singular values arranged in descending order. Next we truncate the SVD by retaining only singular values greater than , and take their corresponding left singular vectors to define the matrix . Then, the truncated core tensor is defined as

based on which we propose the truncated sum of square-matrix nuclear (TSSN) estimator

To derive the theoretical results on rank selection, we make the following assumption on the exact Tucker ranks and the magnitude of the singular values.

Assumption 3.

For all , for all , and there exists a constant such that . As , the threshold parameter satisfies , where .

Assumption 3 requires that has exact Tucker ranks which do not diverge too fast. The smallest positive singular value for each is assumed to be bounded away from the threshold when the sample size is sufficiently large. Since Assumption 3 involves unknown quantities, it cannot be used directly for determining in practice. Instead, we recommend using a data-driven threshold parameter to be described below.

The rank selection consistency of the truncation method and the asymptotic estimation error rate of are given by the following theorem.

Theorem 4.

Similar to Gandy et al., (2011), the SSN estimation can be solved by the alternating direction method of multipliers (ADMM) algorithm, while the truncation can be done by the standard HOSVD; see Appendix S3 of the supplementary file for details. For the tuning parameter selection, since the cross-validation method is unsuitable for time series or intrinsically ordered data, we apply the Bayesian information criterion (BIC) to select the optimal , where the number of degrees of freedom is defined as . For the threshold parameter of the truncated estimator, we recommend to practitioners, where is the optimal tuning parameter selected by the BIC. Similarly, the BIC can be used for tuning parameter selection for SN and MN estimators as well.

Remark 6.

The Tucker ranks of must satisfy , where ; see also the discussion below (8). In practice, if the ranks selected by the truncated estimator fail to satisfy this condition, that is, when exceeds the product of the other ranks (i.e., ), where , we recommend the following selection procedure for rank adjustments. First, for each that is not equal to , we increase it until the above condition on Tucker ranks is met, while fixing the other ranks, and obtain the adjusted truncated estimator. Next, for all adjusted estimators, we select the most suitable ranks via BIC. For example, if the TSSN estimator produces the Tucker ranks , we consider adjusted ranks , , , or , and then select the one with the smallest BIC.

4 Non-convex Tensor Regression Estimation

4.1 Non-convex Estimation

While significant efficiency improvement can be achieved by the square matricization in Section 3.2, the consistency of the SSN and TSSN estimators still requires the sample size grows faster than the overall dimension . To further lower the sample size requirement and improve the estimation efficiency, this section proposes a non-convex estimation method for the LRTAR model under the assumption that is exactly low-rank.

First, we assume that the true Tucker ranks are known. Following Han et al., (2022), we can estimate the transition tensor via the non-convex (NC) optimization:

| (27) |

where the regularization terms are used to prevent ’s from being singular and balance the scale of tensor decomposition components, and are tuning parameters.

To further understand the regularization terms for ’s, let and be the squared loss functions with respect to and its Tucker decomposition, respectively. While the optimization in (27) is unconstrained, any solution will satisfy . Otherwise, we can always find some nonsingular matrices , for , such that and . In this case, , while the regularization terms for reduce to zero. This will result in a contradiction with the definition of minimizers. Note that we do not require , i.e., may not be orthonormal. Moreover, we do not require the uniqueness of and ’s, since we only need the resulting from (27); see also Han et al., (2022). However, as discussed in Section 2.3, after obtaining , we can apply the HOSVD to to obtain the uniquely defined orthonormal estimates ’s and all-orthogonal estimate .

The partial gradients of the squared loss with respect to and are defined as

| (28) |

where , and denotes the tensor outer product. The problem in (27) can be solved by the gradient descent algorithm: for ,

| (29) |

with the initial values , where is the total number of iterations and is the step size of each iteration. The final output is , and we may apply the HOSVD to to ensure the identifiability of the Tucker decomposition.

4.2 Computational and Statistical Convergence Analysis

In this subsection, we present the main properties of the NC estimation method. Theoretical analysis of this method is challenging due to the non-convex nature of the problem. To show that the proposed method is valid, we derive the linear convergences of gradient descent iterates to the ground truth up to a statistical error. First, we introduce some regulatory conditions, namely the restricted strong convexity, restricted strong smoothness, and deviation bound conditions.

Definition 1.

The squared loss function is restricted strongly convex with parameter and restricted strongly smooth with parameter , such that for any low-rank tensors with Tucker ranks ,

| (30) |

Definition 2.

For the given Tucker ranks , denote as

| (31) |

The restricted strong convexity and smoothness consitions are essential for convergence analysis of a large number of non-convex optimization problems (Jain and Kar,, 2017). The deviation bound characterizes the magnitude of the statistical noise projected onto the low-rank tensor spaces. Moreover, for the true value , denote by , , and the largest singular value, the smallest nonzero singular value, and condition number of along all modes, respectively. Now, we state a deterministic upper bound on the estimation error and a linear rate of convergence for the proposed gradient descent algorithm.

Theorem 5.

Suppose that the squared loss function satisfies the restricted strong convexity, restricted strong smoothness and deviation bound conditions in Definitions 1 and 2, and is low-rank with known Tucker ranks . For the gradient descent iterates with parameters , , and size step from some small , if the initial bound is satisfied, for all

| (32) |

with .

Theorem 5 presents a set of conditions for the convergence of the gradient descent iteratives for . The first term in the right hand side of (32) corresponds to the optimization error, whereas the second term corresponds to the statistical error. This bound shows that the estimation error of the iterates decreases exponentially to a statistical limit. When the RSC parameter and all nonzero singular values of along all modes are bounded and bounded away from zero, the rates of paramters remain constant.

Remark 7.

For the initialization, if is a constant number, the initial bound can be satisfied for any consistent intial value . When ’s are large, may diverge to infinity as ’s increase, and hence the initial condition for could be relaxed.

Following the spectral dependency measure in Section 3, we define the restricted strong smoothness parameter for the tensor AR process . For the tensor AR process satisfying Assumptions 1 and 2, we can derive the following statistical convergence results of the gradient descent iteratives.

Theorem 6.

Theorem 6 presents the estimation error upper bound after a sufficient number of iterations. When , , and are bounded, the statistical convergence rate scales as . Under the exact low-rank condition in , compared with the SSN estimator with a rate of , the rate of the non-convex NC estimator is improved significantly. In other words, to achieve consistency, the sample size requirement is reduced from to . For high-dimensional matrix-valued () and tensor-valued () time series data, the relaxation of sample size requirement is essential, since it is usually difficult or even impossible to collect a large number of samples, when is large as in the import-export network data discussed in Section 1.

4.3 Rank Selection and Initialization

In practice, we need to determine the Tucker ranks in order to apply the proposed non-convex estimation method. When the sample size is sufficiently large, i.e., , one may apply the TSSN method described in Section 3.3 to select the ranks. When the dimensions ’s are large, we recommend giving a pre-specified upper bound , and then calculate the estimate based on the rank upper bounds . Denote the singular values of its mode- matricization by , and each rank can be selected by the ridge-type ratio estimator (Wang et al.,, 2022)

| (35) |

where is a positive sequence depending on and .

The proposed method is not sensitive to the choice of as long as it is greater than . Thus, by the multidimensional factor interpretation, we can choose to be reasonably large. For example, for the import-export network data described in Section 2.4, we may set . The ridge parameter is essential for consistent rank selection, and we suggest using based on the simulation experiments in Section 5. Similar to the TSSN estimator, the Tucker ranks selected by the ridge-type ratio estimator may not satisfy condition (8) and we may adjust the selected ranks by the approach in Remark 6. The rank selection consistency is established in the following theorem.

Theorem 7.

Suppose that all conditions in Theorem 6 hold, , , , and , where . Then , for , as .

The conditions in this theorem reduce to and as , when , , , and are bounded. Thus, the sample size requirement is reduced to , which significantly relaxes that in Theorem 4 for the TSSN method.

Moreover, for the initialization of the proposed estimation methodology, we may first select the rank upper bounds and randomly initialize the algorithm by adding a random perturbation to obtained under the rank upper bounds. The refined tensor ranks are selected by the ridge-type ratio estimator, and then the HOSVD is applied to the previous initial value to obtain . The satisfactory performance of this initialization procedure is observed in our simulation experiments.

5 Numerical Studies

In this section, we present numerical studies to support the methodological and theoretical results obtained in the previous sections. In Section 5.1, we present the finite-sample performance of various estimation methods proposed in Sections 3 and 4. In Section 5.2, we model the import-export network data via the LRTAR and other vector-valued and tensor-valued time series models in the literature.

5.1 Simulation Experiments

We present two simulation experiments to examine the finite-sample performance of the proposed high-dimensional estimation methods. Throughout this section, we generate the data from model (12) with . The entries of are generated independently from and rescaled such that . The matrices are generated by extracting the leading singular vectors from Gaussian random matrices while ensuring the stationarity condition in Assumption 1. In these two experiments, we consider four cases of data generating processes. In cases (a) and (b), we consider and Tucker ranks , or ; while in cases (c) and (d), we consider and Tucker ranks , or . Both pairs of cases differ in the setting for ’s: (a) and (b) ; (c) and (d) .

The first experiment aims to compare the performance of four nuclear-norm-penalized estimators discussed in Section 3, namely the SN, MN, SSN and TSSN estimators, when the sample size is relatively large. For each setting, we repeat 500 times and conduct the estimation using SN, MN, SSN, and TSSN. The nuclear-norm-penality tuning parameter and truncation parameter are selected by the BIC described in Section 3.3. In Figure 2, the average estimation errors are plotted against for cases (a) and (b), and for cases (c) and (d). First, it can be seen that the SN estimator is much inferior to the other three estimators, which is due to its use of the unbalanced one-mode matricizations. Secondly, the SSN and TSSN estimators outperform the MN estimator in all cases, and their advantage is remarkably clear even when . In addition, the rank selection performance of the TSSN method is summarized in Table 2. In general, the TSSN estimator can consistently select the tensor ranks when is large, and performs the best among these four, probably because it yields a more parsimonious model which improves the estimation efficiency. The results in experiment 1 verify the efficiency improvement in the proposed SSN and TSSN estimators.

| Case (a) | Case (b) | ||||||

|---|---|---|---|---|---|---|---|

| (1,1,1,1) | (2,2,1,1) | (2,2,2,2) | (1,1,1,1) | (2,2,1,1) | (2,2,2,2) | ||

| 800 | 96.2 | 93.8 | 90.0 | 82.6 | 79.6 | 75.2 | |

| 1000 | 98.4 | 98.0 | 94.8 | 86.4 | 84.4 | 81.8 | |

| 1200 | 100 | 100 | 99.2 | 93.2 | 94.0 | 88.0 | |

| 1400 | 100 | 99.8 | 100 | 98.4 | 97.8 | 96.2 | |

| Case (c) | Case (d) | ||||||

| (1,1,1,1,1,1) | (2,2,2,1,1,1) | (2,2,2,2,2,2) | (1,1,1,1,1,1) | (2,2,2,1,1,1) | (2,2,2,2,2,2) | ||

| 1000 | 93.2 | 91.8 | 92.2 | 81.4 | 81.0 | 77.6 | |

| 1200 | 96.6 | 93.2 | 92.6 | 88.2 | 90.4 | 85.6 | |

| 1400 | 99.4 | 98.8 | 99.0 | 91.4 | 93.6 | 92.8 | |

| 1600 | 99.6 | 99.2 | 98.8 | 96.2 | 97.0 | 97.2 | |

The second experiment aims to verify the performance of NC estimator when the sample size is relatively small. We consider for cases (a) and (b), and for cases (c) and (d). Since the NC estimator requires the pre-determined Tucker ranks, we consider two estimators, namely the NC estimator with the true Tucker ranks (denoted by NC-true) and NC estimator with Tucker ranks estimated by the ridge-type ratio estimator in Section 4 (denoted by NC-est). When applying the gradient descent algorithm, we simply set and use the TSSN estimator to obtain the initial values of and ’s. The default gradient descent step size is , and it will be reduced to if the default one fails to converge. In addition, the random initialization method is also adopted for the NC-est estimator. The average estimation errors of the non-convex methods are summarized in Figure 3 and the rank determination of the ridge-type ratio estimator is collected in Table 3. As the ridge-type ratio estimator can consistently estimate the Tucker ranks, the performance of NC-true and NC-est estimators is quite similar. When the sample size is small, NC-true method performs slightly better.

| Case (a) | Case (b) | ||||||

|---|---|---|---|---|---|---|---|

| (1,1,1,1) | (2,2,1,1) | (2,2,2,2) | (1,1,1,1) | (2,2,1,1) | (2,2,2,2) | ||

| 50 | 77.2 | 69.2 | 70.4 | 69.6 | 57.4 | 55.4 | |

| 100 | 82.2 | 77.2 | 78.6 | 74.2 | 62.2 | 63.8 | |

| 150 | 88.4 | 85.0 | 87.2 | 82.8 | 70.6 | 72.4 | |

| 200 | 94.0 | 92.4 | 93.2 | 90.8 | 87.0 | 78.8 | |

| Case (c) | Case (d) | ||||||

| (1,1,1,1,1,1) | (2,2,2,1,1,1) | (2,2,2,2,2,2) | (1,1,1,1,1,1) | (2,2,2,1,1,1) | (2,2,2,2,2,2) | ||

| 80 | 71.2 | 69.4 | 68.4 | 68.2 | 70.4 | 73.2 | |

| 160 | 82.8 | 79.8 | 78.0 | 79.8 | 76.0 | 55.8 | |

| 240 | 88.2 | 84.0 | 84.4 | 88.2 | 87.8 | 87.8 | |

| 320 | 97.0 | 92.0 | 92.6 | 98.0 | 99.2 | 97.6 | |

5.2 Real Data Analysis

We analyze the multi-category import-export network data in Chen et al., (2022), which consists of the monthly export data among 22 countries, including 19 European countries (Belgium, Bulgaria, Denmark, Finland, France, Germany, Greece, Hungary, Iceland, Ireland, Italy, Norway, Poland, Portugal, Spain, Sweden, Switzerland, Turkey, and the United Kingdom) and 3 North American countries (Canada, Mexico, and the United States). The products are classified into 15 categories, including industrial and algricultural products. Hence, the import-export network data in each month form a Export-Import-Product tensor, and the data is collected from January 2010 to December 2016. Following Chen et al., (2022), the missing diagonal values for the export from any country to itself are treated as zero. A three-month moving average of the series is applied to alleviate the possible effect of incidental transactions, so the total available sample size is which is much smaller than the overall dimension of the data .

Let be the tensor-valued time series and denote . For comparison, we consider the following seven candidate models:

-

1.

The proposed LRTAR model: , with . The model is estimated using the SSN, TSSN and NC methods, respectively.

-

2.

Sparse vector autoregression (SVAR): , where is a sparse matrix. We estimate the sparse VAR model via the Lasso estimator discussed in Basu and Michailidis, (2015).

-

3.

Low-rank vector autoregression (LRVAR): , where is a low-rank matrix. The model is estimated by the MN estimator in Section 3.

-

4.

Vector factor model (VFM): , where is the low-dimensional vector-valued latent factor, and is the loading matrix. The model is estimated by the method in Lam et al., (2012), and for prediction, the estimated factors are then fitted by a VAR(1) model.

-

5.

Multilinear tensor autoregression (MTAR): , where and are coefficient matrices. The model is estimated by the iterative least squares method similar to Chen et al., (2021).

-

6.

Tensor factor model (TFM): , where is the low-dimensional tensor-valued latent factor, and ’s are the loading matrices. The TFM is esimated by the method in Chen et al., (2022), and for prediction, the estimated factors are fitted by a VAR(1) model.

-

7.

Factor augmented vector autoregressive model (FAVAR): the vectorized time series is decomposed into two parts , where contains the trading data between the United States and Germany under the categories of the largest volume “Machinery and Electrical” and “Transportation”, and contains the rest of data. The FAVAR model (Bernanke et al.,, 2005; Stock and Watson,, 2016) with and is used to model the data.

We first focus on the results of the proposed LRTAR model. The overall dimension is much larger than the sample size , which violates the sample size requirements of nuclear-norm-regularized estimators. Hence, we try all combinations of Tucker ranks, with each rank ranging from 1 to 3, and the best ranks selected by the BIC are . By the multi-dimensional dynamic factor interpretation in (18), these six ranks indicate the numbers of factors for “export predictor”, “import predictor”, “product predictor”, “export response”, “import response”, and “product response.” In other words, the total number of factors for predictors () is smaller than that for responses (), showing that the low-dimensional information summarized from predictors is more compact than that of responses. It is also interesting to see that the numbers of factors for predictors and responses selected by LRTAR are smaller than those selected by the tensor factor model, , in Chen et al., (2022).

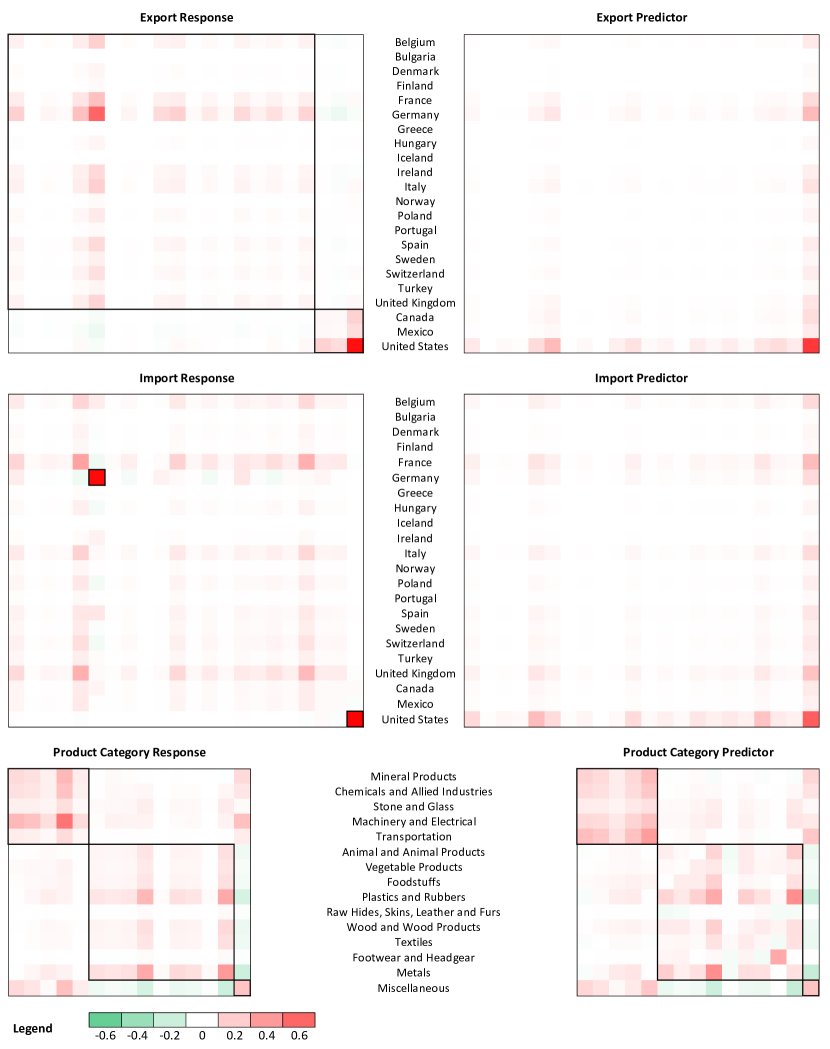

As the factor matrices ’s are not uniquely defined, we present the estimates of the identifiable projection matrices by LRTAR-NC with being orthonormal in Figure 4. The estimated projection matrices of these six factor loadings offer a clear and interesting interpretation of inter-regional trading flow, which helps us answer the four questions in Section 1. For the first two questions about the driving forces of the exporting and importing activities, the estimated factor matrices , , and present some numerical hints. Specifically, for the responses of export and import (first two plots in the left panel of Figure 4), the exporting countries are clearly classified into two geographical factors, one for European countries and one for North American countries, while the import countries are categorized into another two factors, United States factor and Germany factor. For the predictors, the factor loadings for exporting and importing countries (see the first two plots in the right panel of Figure 4) are both dominated by the United States. In other words, to forecast the trading volume in Europe and North America, the historical trading data of the United States, in both import and export, are most predictive. However, the future import and export value have a clear geographical grouping pattern.

In addition, for the third question, the factor loadings for product category, and , also have a clear grouping pattern. For both responses and predictors, the product categories can be classified into two factors, “heavy industry factor” (mineral, chemical, machinery, electrical and transportation products) and “agricultural and light industry factor” (animal, vegetable, leather, wood, textiles products). Hence, we may interpret the estimated factor matrices in LRTAR as variable grouping patterns in export, import, and product categories for responses and predictors, respectively. Finally, by comparing the predictor and response factor loadings, we observe that the geographical grouping patterns of both exporting and importing countries are significantly different between past and present states (i.e., predictor vs. response), whereas the grouping patterns of product categories remain almost the same.

Next, we compare the forecasting performance of seven candidate models through both average in-sample and out-of-sample forecasting errors. The average in-sample forecasting error is calculated based on the fitted models for the entire data, while the average out-of-sample forecasting error is calculated based on the rolling forecast procedure as follows. From January 2015 () to December 2016 (, we fit the models using all the available data until time and obtain the one-step-ahead forecast . Then, we obtain the average of the rolling forecasting errors, excluding the missing diagonal entries. The number of parameters in each candidate model (LRTAR-SSN is excluded because it produces shrinkage of singular values instead of exactly low-rank structure) and the average in-sample and out-of-sample forecasting errors are summarized in Table 4.

| Model | LRTAR | SVAR | LRVAR | VFM | MTAR | TFM | FAVAR | |||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| SSN | TSSN | NC | ||||||||||

| No. of par. | NA | 2643 | 190 | 9543 | 43560 | 21789 | 2386 | 2525 | 36305 | |||

| IS | norm | 1362 | 1409 | 1563 | 713 | 896 | 906 | 1263 | 1076 | 943 | ||

| norm | 74 | 79 | 89 | 62 | 88 | 61 | 83 | 79 | 67 | |||

| OOS | norm | 2018 | 1533 | 1083 | 2362 | 2218 | 1545 | 1432 | 1211 | 1224 | ||

| norm | 127 | 109 | 99 | 176 | 218 | 134 | 123 | 114 | 119 | |||

As shown in Table 4, all vector time series models have smaller in-sample forecasting errors and larger out-of-sample forecasting errors than their tensor counterparts, as they fail to utilize the multi-dimensional structure of the tensor data. For out-of-sample forecasting, LRTAR-NC significantly outperforms the other models in terms of average and maximum errors, as this model is much more parsimonious and can prevent overfitting effectively.

6 Conclusion and Discussion

Efficient modeling and forecasting of high-dimensional tensor time series data is an important and emerging research topic. This paper makes the first thorough attempt to address this problem from the perspective of autoregressive modeling. By assuming the exact or approximately low-Tucker-rank structure of the transition tensor, the model exploits the low-dimensional tensor dynamic structure of the high-dimensional time series data, and summarizes the complex temporal dependencies into interpretable dynamic factors.

Under the high-dimensional setting, we investigate two estimation approaches, nuclear-norm-regularized methods and non-convex methods. For the former, based on the special structure of the transition tensor, a novel convex regularizer, the SSN, is proposed, gaining efficiencies from both the square matricization and simultaneous penalization across modes. For the latter, an integrated computational and statistical analysis is provided for the gradient descent algorithm. The nuclear-norm-regularized estimators can handle the general case with approximate low-rankness, and the non-convex estimator gains efficiency improvement under the exactly low-rank setting.

We discuss several directions for future research. First, in addition to the low-rank models, sparse plus low-rank models (Basu et al.,, 2019; Miao et al.,, 2023) have been extensively studied in the literature of high-dimensional vector autoregression. It is also of interest to extend the proposed model in this direction, i.e., the parameter tensor can be decomposed into two components, the low-rank component and sparse component . Specically, is low-Tucker-rank as we discuss in this paper, and can capture the additional sparse autoregressive relationship between responses and predictors.

Second, while this paper focuses on the pure autoregressive model, the fundamental idea of leveraging the tensor-valued data and imposing the low-Tucker-rank assumption for dimension reduction can be extended to more complex settings. Similar to panel data models, exogenous variables can be further added into the regression, resulting in LRTAR-X models. For example, for the multi-category import-export data in Section 5.2, it is possible to consider , where the vector may contain global variables such as the return of the oil price, and the matrix or tensor may contain other country-level macroeconomic indicators such as the GDP growth rate. When the dimensions of and are high, a low-dimensional structure, such as sparsity, group sparsity or low-rankness, can be imposed on and to improve the estimation efficiency.

Third, in the proposed model, all variables in are treated with equal importance because the primary objective is to capture the complex dependence structures of a global system using granular data. However, if there are other priority variables to forecast, represented by the vector , then we may extend the proposed method to the joint model,

where can be assumed to have low Tucker ranks.

Fourth, the proposed methods can be generalized to the LRTAR model of finite lag order , defined as , where are -th-order Tucker low-rank coefficient tensors. Then, one may consider the SSN regularized estimation by minimizing . In addition, the NC estimator can be defined as the minimizer of , which can be implemented by the gradient descent algorithm.

Finally, heavy-tailed distributions and outliers are commonly observed in empirical economic and financial datasets. Robust estimation methods against the heavy-tailed distribution for high-dimensional VAR models have been investigated recently (Liu and Zhang,, 2022; Wang and Tsay,, 2022), and it is of practical importance to investigate the robust methods for the proposed model.

Acknowledgement

We are grateful to the editor, Serena Ng, the associate editor, and three anonymous referees for their valuable comments that led to the substantial improvement of this paper. We would also like to thank Dan Yang for sharing the multi-category import-export network data for the empirical analysis. Wang was supported by the National Natural Science Foundation of China Grant 12301352 and Shanghai Sailing Program for Youth Science and Technology Excellence (23YF1420300). Zheng was supported by the National Science Foundation Grant DMS-2311178. Li was supported by the Hong Kong Research Grant Council Grants 17306519 and 17313722.

References

- Bai and Wang, (2016) Bai, J. and Wang, P. (2016). Econometric analysis of large factor models. Annual Review of Economics, 8:53–80.

- Basu et al., (2019) Basu, S., Li, X., and Michailidis, G. (2019). Low rank and structured modeling of high-dimensional vector autoregressions. IEEE Transactions on Signal Processing, 67:1207–1222.

- Basu and Matteson, (2021) Basu, S. and Matteson, D. S. (2021). A survey of estimation methods for sparse high-dimensional time series models. ArXiv preprint arXiv:2107.14754.

- Basu and Michailidis, (2015) Basu, S. and Michailidis, G. (2015). Regularized estimation in sparse high-dimensional time series models. Annals of Statistics, 43:1535–1567.

- Bernanke et al., (2005) Bernanke, B. S., Boivin, J., and Eliasz, P. (2005). Measuing the effects of monetary policy: a factor-augmented vector autoregressive (FAVAR) approach. The Quarterly Journal of Economics, 120:387–422.

- Boyd et al., (2011) Boyd, S., Parikh, N., Chu, E., Peleato, B., Eckstein, J., et al. (2011). Distributed optimization and statistical learning via the alternating direction method of multipliers. Foundations and Trends® in Machine learning, 3:1–122.

- Bussière et al., (2012) Bussière, M., Chudik, A., and Sestieri, G. (2012). Modelling global trade flows: results from a gvar model. Globalization and Monetary Policy Institute Working Paper 119, Federal Reserve Bank of Dallas.

- Candes and Plan, (2011) Candes, E. J. and Plan, Y. (2011). Tight oracle inequalities for low-rank matrix recovery from a minimal number of noisy random measurements. IEEE Transactions on Information Theory, 57:2342–2359.

- Canova and Ciccarelli, (2013) Canova, F. and Ciccarelli, M. (2013). VAR Models in Macroeconomics: New Developments and Applications: Essays in Honor of Christopher A. Sims, chapter Panel vector autoregressive models: a survey, page 205–246. Emerald Group Publishing Limited, Bingley.

- Chen et al., (2019) Chen, H., Raskutti, G., and Yuan, M. (2019). Non-convex projected gradient descent for generalized low-rank tensor regression. The Journal of Machine Learning Research, 20(1):172–208.

- Chen et al., (2021) Chen, R., Xiao, H., and Yang, D. (2021). Autoregressive models for matrix-valued time series. Journal of Econometrics, 222:539–560.

- Chen et al., (2022) Chen, R., Yang, D., and Zhang, C.-H. (2022). Factor models for high-dimensional tensor time series. Journal of the American Statistical Association, 117:94–116.

- De Lathauwer et al., (2000) De Lathauwer, L., De Moor, B., and Vandewalle, J. (2000). A multilinear singular value decomposition. SIAM Journal on Matrix Analysis and Applications, 21:1253–1278.

- Ding and Cook, (2018) Ding, S. and Cook, R. D. (2018). Matrix variate regressions and envelope models. Journal of the Royal Statistical Society: Series B, 80:387–408.

- Gandy et al., (2011) Gandy, S., Recht, B., and Yamada, I. (2011). Tensor completion and low-n-rank tensor recovery via convex optimization. Inverse Problems, 27:025010.

- Guo et al., (2016) Guo, S., Wang, Y., and Yao, Q. (2016). High-dimensional and banded vector autoregressions. Biometrika, 103:889–903.

- Han et al., (2015) Han, F., Lu, H., and Liu, H. (2015). A direct estimation of high dimensional stationary vector autoregressions. Journal of Machine Learning Research, 16:3115–3150.

- Han et al., (2022) Han, R., Willett, R., and Zhang, A. (2022). An optimal statistical and computational framework for generalized tensor estimation. The Annals of Statistics, 50:1–29.

- Hoff, (2015) Hoff, P. D. (2015). Multilinear tensor regression for longitudinal relational data. Annals of Applied Statistics, 9:1169–1193.

- Jain and Kar, (2017) Jain, P. and Kar, P. (2017). Non-convex optimization for machine learning. Foundations and Trends® in Machine Learning, 10:142–336.

- Kolda and Bader, (2009) Kolda, T. G. and Bader, B. W. (2009). Tensor decompositions and applications. SIAM Review, 51:455–500.

- Lam et al., (2012) Lam, C., Yao, Q., et al. (2012). Factor modeling for high-dimensional time series: inference for the number of factors. Annals of Statistics, 40:694–726.

- Liu et al., (2013) Liu, J., Musialski, P., Wonka, P., and Ye, J. (2013). Tensor completion for estimating missing values in visual data. IEEE Transactions on Pattern Analysis and Machine Intelligence, 35:208–220.

- Liu and Zhang, (2022) Liu, L. and Zhang, D. (2022). Robust estimation of high-dimensional non-Gaussian autoregressive models. arXiv preprint arXiv:2109.10354.

- Miao et al., (2023) Miao, K., Phillips, P. C., and Su, L. (2023). High-dimensional vars with common factors. Journal of Econometrics, 233(1):155–183.

- Mirsky, (1960) Mirsky, L. (1960). Symmetric gauge functions and unitarily invariant norms. Quarterly Journal of Mathematics, 11:50–59.

- Mu et al., (2014) Mu, C., Huang, B., Wright, J., and Goldfarb, D. (2014). Square deal: Lower bounds and improved relaxations for tensor recovery. In International Conference on Machine Learning, pages 73–81.

- Negahban and Wainwright, (2011) Negahban, S. and Wainwright, M. J. (2011). Estimation of (near) low-rank matrices with noise and high-dimensional scaling. Annals of Statistics, 39:1069–1097.

- Negahban and Wainwright, (2012) Negahban, S. and Wainwright, M. J. (2012). Restricted strong convexity and weighted matrix completion: Optimal bounds with noise. Journal of Machine Learning Research, 13:1665–1697.

- Negahban et al., (2012) Negahban, S. N., Ravikumar, P., Wainwright, M. J., Yu, B., et al. (2012). A unified framework for high-dimensional analysis of M-estimators with decomposable regularizers. Statistical Science, 27:538–557.

- Nesterov, (2003) Nesterov, Y. (2003). Introductory lectures on convex optimization: A basic course, volume 87. Springer Science & Business Media.

- Pesaran et al., (2004) Pesaran, M. H., Schuermann., T., and Weiner, S. M. (2004). Modelling regional interdependencies using a global error-correcting macroeconometric model. Journal of Business and Economics Statistics, 22:129–162.

- Raskutti et al., (2019) Raskutti, G., Yuan, M., and Chen, H. (2019). Convex regularization for high-dimensional multi-response tensor regression. Annals of Statistics, 47:1554–1584.

- Shojaie et al., (2012) Shojaie, A., Basu, S., and Michailidis, G. (2012). Adaptive thresholding for reconstructing regulatory networks from time-course gene expression data. Statistics in Biosciences, 4:66–83.

- Stock and Watson, (2011) Stock, J. H. and Watson, M. W. (2011). Dynamic factor models. In Clements, M. P. and Hendry, D. F., editors, Oxford Handbook of Economic Forecasting. Oxford University Press.

- Stock and Watson, (2016) Stock, J. H. and Watson, M. W. (2016). Dynamic factor models, factor-augmented vector autoregressions, and structural vector autoregressions in macroeconomics. In Handbook of macroeconomics, volume 2, pages 415–525. Elsevier.

- Tomioka et al., (2011) Tomioka, R., Suzuki, T., Hayashi, K., and Kashima, H. (2011). Statistical performance of convex tensor decomposition. In Advances in Neural Information Processing Systems (NIPS), pages 972–980.

- Tucker, (1966) Tucker, L. R. (1966). Some mathematical notes on three-mode factor analysis. Psychometrika, 31:279–311.

- Vershynin, (2018) Vershynin, R. (2018). High-Dimensional Probability: An Introduction with Applications in Data Science. Cambridge University Press, Cambridge.

- Wang and Tsay, (2022) Wang, D. and Tsay, R. S. (2022). Rate-optimal robust estimation of high-dimensional vector autoregressive models. arXiv preprint arXiv:2107.11002.

- Wang et al., (2022) Wang, D., Zheng, Y., Lian, H., and Li, G. (2022). High-dimensional vector autoregressive time series modeling via tensor decomposition. Journal of the American Statistical Association, 117:1338–1356.

- Wong, (2017) Wong, K. C. (2017). Lasso Guarantees for Dependent Data. PhD thesis.

- Zheng and Cheng, (2021) Zheng, Y. and Cheng, G. (2021). Finite time analysis of vector autoregressive models under linear restrictions. Biometrika, 108:469–489.

- Zhu et al., (2017) Zhu, X., Pan, R., Li, G., Liu, Y., and Wang, H. (2017). Network vector autoregression. The Annals of Statistics, 45:1096–1123.

Supplementary Material for

“High-Dimensional Low-Rank Tensor Autoregressive Time Series Modeling”

S1 Proofs for Convex Regularized Estimation

In this appendix, we provide the proofs of Theorems 1–4 in Section 3. We start with a preliminary analysis in Appendix S1.1 which lays out the common technical framework for proving the estimation and prediction error bounds of the SN, MN and SSN regularized estimators, and four lemmas, Lemmas S1–S4, are introduced herein. Then in Appendix S1.2 we give the proofs of Theorems 1–4. The proofs of Lemmas S1–S4 are provided in Appendix S1.3, and three auxiliary lemmas are collected in Appendix S1.4

S1.1 Preliminary Analysis

The technical framework for proving the error bounds in Theorem 1–3 consists of two main steps, a deterministic analysis and a stochastic analysis, given in Sections S1.1.1 and S1.1.2, respectively. The goal of the first one is to derive the error bounds given the deterministic realization of the time series, assuming that the parameters satisfy certain regularity conditions. The goal of the second one is to verify that under stochasticity these regularity conditions are satisfied with high probability.

S1.1.1 Deterministic Analysis

Throughout the appendix, we adopt the following notations. We use to denote a generic positive constant, which is independent of the dimensions and the sample size. For any matrix and a compatible subspace , we denote by the projection of onto . In addition, let be the column space of , and let be the complement of the subspace . For a generic tensor , the dual norms of its SSN norm and SN norm, denoted by and , respectively, are defined as

| (S1) |

Moreover, for any two tensors and , their tensor outer product is defined as where

| (S2) |

for any , , .

For the theory of regularized -estimators, restricted error sets and restricted strong convexity are essential definitions. To define the former, we need to first introduce the following restricted model subspaces.

For , denote by and the spaces spanned by the first left and right singular vectors in the SVD of , respectively. Define the collections of subspaces

where

| (S3) |

for . Note that .

Furthermore, for , denote by and the spaces spanned by the first left and right singular vectors in the SVD of the square matricization , respectively, where . Similarly, define the collections of subspaces

where

| (S4) |

for . In particular, as described in Section 3.2, . Thus, and are the subspaces associated with the square matricization .

Then, for simplicity, for any , we denote

| (S5) |

where and . Based on the subspaces defined in (S3) and (S4), we can define the restricted error sets corresponding to the three regularized estimators as follows.

Definition 3.

The restricted error set corresponding to is defined as

| (S6) |

The restricted error set corresponding to is defined as

| (S7) |

The restricted error set corresponding to is defined as

| (S8) |

The first lemma shows that if the tuning parameter is well chosen for each regularized estimator, the estimation error belongs to the corresponding restricted error set.

Lemma S1.

For the SSN estimator, if the regularization parameter , the error belongs to the set .

For the SN estimator, if the regularization parameter , the error belongs to the set .

For the MN estimator, if the regularization parameter , the error belongs to the set .

Following Negahban and Wainwright, (2012) and Negahban et al., (2012), a restricted strong convexity (RSC) condition for the square loss function can be defined as follows.

Definition 4.

The loss function satisfies the RSC condition with curvature and restricted error set , if

| (S9) |

Based on the restricted error sets and RSC conditions, the estimation errors have the following deterministic upper bounds.

Lemma S2.

Suppose that , the RSC condition holds with the parameter and restricted error set , and for some and all ,

| (S10) |

where .