General Hannan and Quinn Criterion for Common Time Series

Abstract

This paper aims to study data driven model selection criteria for a large class of time series, which includes ARMA or AR() processes, as well as GARCH or ARCH(), APARCH and many others processes. We tackled the challenging issue of designing adaptive criteria which enjoys the strong consistency property. When the observations are generated from one of the aforementioned models, the new criteria, select the true model almost surely asymptotically. The proposed criteria are based on the minimization of a penalized contrast akin to the Hannan and Quinn’s criterion and then involved a term which is known for most classical time series models and for more complex models, this term can be data driven calibrated. Monte-Carlo experiments and an illustrative example on the CAC 40 index are performed to highlight the obtained results.

SAMM, Université Paris 1 Panthéon-Sorbonne, FRANCE Key words: Time series, Model selection, consistency, data driven, HQ criterion.

1 Introduction

A common solution in model selection is to choose the model, minimizing a penalized based criterion which is the sum of two terms: the first one is the empirical risk (least squares, likelihood) that measures the goodness of fit and the second one is an increasing function of the complexity which aims to penalize large models and control the bias.

Therefore a challenging task when designing a penalized criterion is the specification of the penalty term. Considering leading model selection criteria (BIC, AIC, Cp, HQ to name a few), one can see that the penalty term is a product of the model dimension with a sequence which is specific to the criteria. Indeed, a criterion is designed according to the goal one would like to achieve. The classical properties for model selection criteria include consistency, efficiency (oracle inequality, asymptotic optimality), adaptative in the minimax sense.

In this paper, we focus on consistency property which aims at identifying the data generating process with high probability or almost surely. Hence, it requires the assumption whereby there exists a true model in the set of competitive models and the goal is to select this with probability approaches one as the sample size tends to infinity. In [BKK20], they studied model selection criteria regarding consistency in a large class of time series, which is the interest of this paper. The leading criterion obtained in this framework is the BIC; with a relatively heavy penalty, it ensures the selection of quite simple models. Moreover, several papers have established the consistency property in particular settings. For instance, [HQ79] shows that the Hannan and Quinn (HQ) penalty with leads to a consistent choice of the true order in the framework of AR type models. One year later, [Han80] (or [HD12]) extended this result for ARMA models.

Also, it has been proven in several contexts, that the BIC criterion [Sch78] enjoys the consistency property: [Shi86] in the density estimation using hypothesis testing for autoregressive moving average models, [LMH04] in density estimation for independent observations, [BKK20] for a general class of time series, to name a few.

Compare to HQ penalty, the BIC penalty does not have the slowest rate of increase and then it can very often choose very simple models possible wrongs for small samples [HQ79]. Moreover, the HQ criterion has been derived for linear time series: AR models in [HQ79], ARMA models in [Han80] and [HD12]. Is the HQ penalty still strongly consistent for heteroscedastic nonlinear models such as GARCH, APARCH or ARMA-GARCH? And what about a general class including linear and non linear models as well?

That raises a challenging question of designing robust penalties for most classical time series models enjoying the model selection consistency. This is the issue we want to address in this paper for a general class of times series called affine causal and defined below.

Class A process belongs to if it satisfies:

| (1.1) |

where is a sequence of zero-mean independent identically distributed random vectors (i.i.d.r.v) satisfying with and , : are two measurable functions.

For instance,

-

•

if and , then is an AR process;

-

•

if and , then is an ARCH process.

Note that, numerous classical time series models such as ARMA(), GARCH(), ARMA()-GARCH() (see [DGE93] and [LM03]) or APARCH processes (see [DGE93]) belongs to .

The study of this type of process more often requires the classical regularity conditions on the functions and , which are not restrictive at all and remain valid in various time serie models. Let us recall these conditions for or and a compact set.

Hypothesis A: Assume that and there exists a sequence of non-negative real numbers such that satisfying:

In addition, if the noise admits -order moments (for ), let us define:

| (1.2) |

Under this assumption, [DW08] showed that there exists a stationary and ergodic solution to (1.1) with -order moment for any . Moreover, [BW09] studied the consistency and the asymptotic normality of the QMLE of for .

The main contribution of this paper is the generalization of the HQ criterion to affine causal class: we provide a minimal multiplicative penalty term so that all penalties of the form with ensure the strong consistency property for affine causal models under some mild conditions on the Lipschitz coefficients of functions ( denotes the size of the model ). Monte Carlo experiments have been conducted in order to attest the accuracy of our new criteria.

2 Model Selection Consistency

2.1 Model Selection Procedure

Let assume be a trajectory of a stationary affine causal process , where is unknown. The goal of the consistency property is to come up with this true model given a set of candidate model such that .

A -dimensionnal model can be viewed as a set of causal functions with . is the parameter set of the model .

The consistency property will be study using the MLE first. Extension to QMLE will be done afterwards.

The MLE is derived from the conditional (with respect to the filtration ) log-likelihood of when

is supposed to be a Gaussian standard white noise.

Due to the linearity of a causal affine process, we deduce that this conditional log-likelihood (up to an additional constant) is defined for all by:

| (2.1) |

where , and .

From now on, we drop the Gaussian assumption of the noise. Let a finite family of candidate models containing the true one . According to Proposition 1 in [BKK20], all these models can be included into a big one with parameter space . For each specific model , we define the Gaussian MLE as

| (2.2) |

To select the true model , we consider a penalized contrast ensuring a trade-off between times the maximized log-likelihood, which decreases with the size of the model, and a penalty increasing with the size of the model. Therefore, the choice of the "best" model among the estimated can be performed by minimizing the following criteria

| (2.3) |

where an increasing sequence depending on the number of observations and the dimension . There exist several possible choices of including

Basically the principle is that by increasing the size, the likelihood increases also. The question is whether this increase in complexity is offset by a sufficient increase in likelihood. If the answer is no, then the least complex model is used, even if it is less likely. If the answer is affirmative, then we accept to work with a more complex model. Of course, all the difficulty lies in the choice of weights between likelihood and complexity, and thus ultimately in the specification of the penalty multiplicative term .

What is the better weighting term of the model complexity? The aim here is by leveraging the increasing rate of the likelihood, to propose a data driven in order to guarantee the strong consistency property to our model selection procedure i.e.

| (2.4) |

2.2 Assumptions

Some mild conditions will be required to prove the consistency of the considered model selection criteria.

The following assumption is well-known as the identifiability one and is always required in order to guarantee the unicity of the global maximum of the MLE at the true parameter . That is:

Assumption A1: For all ,

Another required assumption concerns the differentiability of or on . This type of assumption has already been considered in order to apply the QMLE procedure (see [BW09], [SM06], [Whi82]).

The following condition provides the invertibility of the Fisher’s information matrix of and was used to prove the asymptotic normality of the QMLE (see [BW09]).

Assumption A2: One of the families or is a.e. linearly independent.

Note that the definitions of the conditional log-likelihood requires that their denominators do not vanish.

Hence, we will suppose in the sequel that the lower bound of (which is reached since is compact) is strictly positive:

Assumption A3: such that for all .

Next we assume the existence of the eighth order moment of the noise.

Assumption A4: .

We end the list of assumptions by assuming a suitable relation between the Fisher Information matrix and the limiting Hessian matrix of the log-likelihood defined as follows

with .

Assumption A5: There exist absolutes constants and such that for any verifying ,

| (2.5) |

where and are two integers such that , ,

.

For most classical affine causal models, A5 is verified (see Proposition 2). However, for more complex models such as ARMA-GARCH with , is hard to handle.

2.3 Consistency Result

Before stating the main result of this section, we give important intermediate results. All proof of the results stated in this subsection can be found in Section 4.

The following Proposition suggests the existence of a term that will be the keystone of this work.

Proposition 1.

Let any affine causal model. For any model with , and under A1-A5, there exist , , , such that

| (2.6) |

For every , let us denote by the following term that will be used several times

| (2.7) |

Now we state a result which provides the values of both and for most classical affine causal models.

Proposition 2.

Under the assumptions and notation of Proposition 1, we have

-

•

If (for instance for Gaussian noise), then , and ;

-

•

If the parameter identifying an affine causal model can be decomposed as with and , then , and

The second configuration in Proposition 2 includes classical time series

-

•

GARCH(), APARCH type models and related ones, ;

-

•

ARMA() models, if the variance of the noise is known and otherwise.

We can now state the first main result of this paper.

Theorem 2.1.

Let be an observed trajectory of an affine causal process belonging to where is an unknown vector belonging to . Let also be a finite family of candidate models such that . If assumptions A1-A5 hold, there exist , , and a minimal constant such that

for any with

| (2.8) |

it holds for the selected model according to (2.3)

| (2.9) |

Remark 1.

-

1.

For classical configurations as seen in Proposition 2, this result gives a generalization of Hannan and Quinn criterion.

-

2.

For more complex models, the values of and are unknowns (at least until a better relationship between matrix and is found) and so is also unknown. In these cases, we propose to use adaptive methods such as slope heuristic algorithm or dimension jump [AM09] to calibrate .

Let us mention that our result generalizes the strong consistency obtained by [HQ79] for AR models as the affine causal class also contains GARCH models. It furthermore generalizes the result [HD12] for ARMA models.

Theorem 2.1 gives a theoretical guarantee on the consistency of the model selection procedure. However, it does not say anything about the convergence (and its rate) of the parameter estimate resulting from the model selection . The following results shows that the final estimate is consistent and verifies a CLT.

In this subsection, we have used the MLE contrast without any distribution assumption on the noise to derive a consistency property. However, the contrast as in (2.1) depends on all the past values of the process , which are unobserved. In the next subsection, we will propose an extension of Theorem 2.1 based on QMLE which does not require knowledge of the initial values of the process.

2.4 Extension of Theorem 2.1 when using QMLE.

The goal of this subsection is to sharpen the conditions on the sequence found in [BKK20]. Before stating the result, let recall a little bit some definitions and notations used in [BKK20] about QMLE. Following the definition of , the quasi-likelihood is

| (2.14) |

where , and .

For each specific model , we define the Gaussian QMLE as

| (2.15) |

The choice of the "best" model among the estimated can be performed by minimizing the penalized contrast

| (2.16) |

In this framework, we do not consider long memory process and then we define the class a subset of in which every process has Lispchitz coefficients satisfying the following conditions

It is then straightforward to see that every process in the class verifies the following condition:

Condition :

This finding allows to propose a sharpen generalization of both Theorem 3.1 in our previous paper [BKK20] and a similar result in [Ken20].

Before stating the result using QMLE, it is important as in [BKK20] or [BW09], to distinguish the special case of NLARCH processes which includes for instance GARCH or ARCH processes. In such case, let us define the class:

Class : A process belongs to if it satisfies:

| (2.17) |

Therefore, if then, . In case of the class , we will use the assumption . The new set of stationary solutions is for :

| (2.18) |

Finally, we propose to restrict class to as done with by considering all the process checking the condition

so that

We can now state the second main result.

Theorem 2.3.

Let be an observed trajectory of an affine causal process belonging to (or ) where is an unknown vector belonging to (or ). Let also be a finite family of candidate models such that . If assumptions A1-A5 hold, there exist , , and a minimal constant such that

for any with

| (2.19) |

it holds for the selected model according to (2.16)

| (2.20) |

All the comments made about the Theorem 2.1 remain valid here. Moreover, recently, [Ken20] requires heavy penalties to ensure the strong consistency for the process in the class . Indeed, according to [Ken20], it is necessary that verified to obtain (2.20) which is a stronger condition since the HQ criterion does not fulfill this condition and it is well known that HQ criterion is strongly consistent (see for instance [HQ79]). Moreover, the new penalties found in this paper does not satisfy this condition, yet we ensure strongly consistency.

Also, let us mention that for small samples, heavy penalties such as those in [Ken20] can very often choose very simple models possible wrongs [HQ79].

Remark 2.

Our results show that, asymptotically heavy penalties such as BIC penalty will ensure the consistency property. However, in practise, these penalties are used for fixed and most for small samples and it is important to point out their drawbacks. Very often, in the family of competitive models , there are misspecified and underfitted models (). Since the difference for every , making the penalty, heavy could offset this positivity and can lead to the selection of some underfitted models and then wrong models. To be more convincing of that, see the simulations (DGP III) experiments in Section 3.

2.5 Algorithm of Calibration of the minimal constant

There exist several ways to calibrate the minimal constant including the dimension jump (presented below) and the data-driven slope estimation. Indeed, once an estimation of is obtained, many studies advocates the choice of which turn out to be optimal ([Mas07], [AM09] among others). Now we present the dimension jump algorithm.

Algorithm 1.

Dimension Jump [AM09]

-

1.

Compute the selected model as a function of

-

2.

Find such that is "huge" for and "reasonnably small" for ;

-

3.

Select the model

This algorithm has been implemented in [BMM12] which gives several details including the grid for values.

Let us notice that, in view of obtaining penalties, there is no need to calibrate the constant for most classical time series models. However, since the fourth order moment of the noise is unknown, a consistent estimate of this term is required. To do that, we proceed as in the estimation of the variance of the noise as in the Mallows Cp.

A consistent estimator of can be :

where we suppose that is the "largest" model in the family , typically the largest order of a family of time series. As a result an estimator of the constant to consider in the penalty is

-

•

for GARCH family and related ones;

-

•

for ARMA family with known variance.

3 Numerical Experiments

In this section, several numerical experiments are conducted to assess the consistency property (Section 2) of our new criteria.

3.1 Monte Carlo: Consistency

This subsection studies the performance of the model selection criteria found in Section 2. We have considered three different Data Generating Process (DGP):

| DGP I | ||||

| DGP II | ||||

| DGP III |

where will be a white Gaussian noise with variance one at first and a Student with 5 degrees of freedom on the other hand. For the first and the second DGP, we considered as competitive models all the models in the family defined by:

Therefore, there are candidate models as in [BKK20]. The goal is to compare the ability of selecting the true model for , ( in accordance with the condition (2.19) and . Moreover, from Theorem 2.2 does not need to be estimated and worth one half for Gaussian noise. But for Student noise, for the DGP I and for DGP II. The Table 1 presents the results of the selection procedure. As we can notice, the three penalties have a good consistency property. Moreover, for relatively small, the penalty is better than both others. For larger , is the best the penalty to consider.

| W | |||||

|---|---|---|---|---|---|

| DGP I | T | ||||

| Gaussian | O | ||||

| W | |||||

| DGP II | T | ||||

| Gaussian | O | ||||

| W | |||||

| DGP I | T | ||||

| Student | O | ||||

| W | |||||

| DGP II | T | ||||

| Student | O |

For DGP III, as we want to exhibit the possible "non consistency" of BIC for small samples, we have considered as the competitive set, the hierarchical family of AR models

for . In Table 2 below the percentage of selected order based on 1000 independent replications are presented for the above three penalties.

| 61.5 96 99 | 46 83.5 97 | 29.5 59 87.5 | 19.5 45.5 76.5 | 3.0 9.5 38.5 | 0 0.5 5.0 | |

| 15 3.0 1.0 | 25 13 2.5 | 44 37.5 12.5 | 50.5 49.5 22.5 | 68 86.5 61 | 72.5 96 94.5 | |

| 23.5 1.0 0 | 29 3.5 0.5 | 26.5 3.5 0 | 30 5.0 1.0 | 29 4.0 0.5 | 27.5 3.5 0.5 |

These results invite us to be cautious when using the BIC for small sample sizes, whereas the proposed adaptive penalty is more robust, as it at least allow us to recover an overfitted model that is less harmful than a wrong model most often chosen by the BIC.

3.2 Real Data Analysis: financial time series

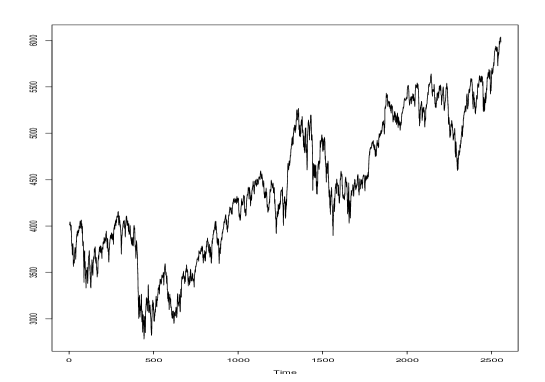

CAC 40 is a benchmark French stock market index and is highly regarded in many statistical studies . Let consider the daily closing prices of the CAC 40 index from January 1st, 2010 to December 31st, 2019 plotted in Figure 1. Over the period under review, the CAC 40 increased.

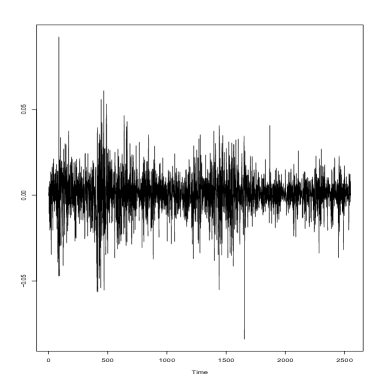

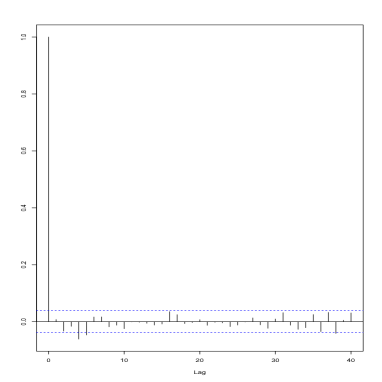

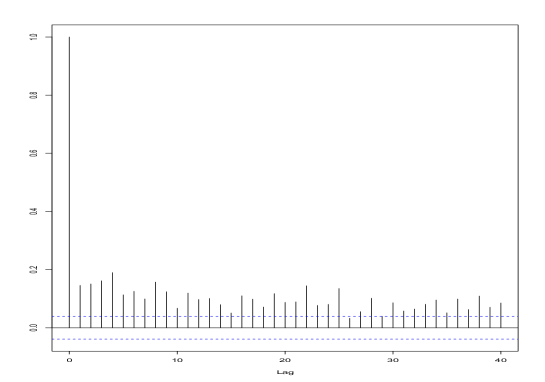

To analyze this type of data, it is common to consider the returns (see Figure 2). We can see that the return values display some small auto-correlations. Also, from Figure 3, the squared returns of CAC 40 are strongly auto-correlated. These facts suggest that the strong white noise assumption cannot be sustained for this log-returns sequence of the CAC 40 index.

Hence, let consider the competitive set of models used in the previous subsection in order to propose the best suitable model for these data:

Using the adaptive penalty and the BIC criterion, we find out that the GARCH() is the best model over with respect to both criteria. This fact is in accordance with [FZ10] which found the same result using the returns of the CAC 40 index from March 2, 1990 to December 29, 2006.

4 Proofs

4.1 Proof of Theorem 2.1

Usually, this proof is divided into two parts: one has to show that as tends to infinity the probability of overfitting goes to zero and so is the probability of misspecification.

4.1.1 Overfitting Case

Let such as . We want to show that a.s. asymptotically. We have

| (4.1) | |||||

therefore, a necessary and sufficient condition to avoid overfitting can be stated by taking on both sides of the inequality (4.1); that is by virtue of definition (2.7)

| (4.2) |

i.e.,

which is fulfilled for any constant such as in (2.8). Indeed, and

where the inequality holds since that implies and . Hence the associated criterion will avoid overfitting.

4.1.2 Misspecification/Underfitting Case

All misspecified/underfitted models are contained in the set

The proof is exactly as the one done in [BKK20]. But for the sake of completeness, we give here some important steps of the proof.

The goal is to show that for every , it holds

| (4.3) |

Let . From Proposition 2 in [BKK20] and using continuous mapping Theorem

| (4.4) |

where

Let us denote by . Using conditional expectation, we obtain

| (4.5) |

But,

Thus from (4.5),

Since for any and for , we deduce that

-

•

If then and

-

•

Otherwise, then

and from assumption A1, since and , we necessarily have so that Then .

As a consequence,

That establishes (4.3) by virtue of (2.8) and as all the considered models are finite dimensional. ∎

In the sequel, we state and prove several lemmas to which we referred to when proving above main results.

4.1.3 Proof of Theorem 2.3

4.1.4 Proof of Proposition 1

Proof.

Applying a second order Taylor expansion of around for sufficiently large such that which are between and yields (as since is a local extremum):

From the mean value Theorem, and for large , there exists between and such that, :

| (4.6) |

Also, using Lemma 4 of [BW09] and continuous mapping Theorem, we deduce that:

| (4.7) |

On the other hand, under A2 condition, is an invertible matrix and there exists sufficiently large such that is invertible. Therefore, from (4.6), it follows

The next step of the proof consists in handling the quadratic form by applying the law of iterated logarithm (LIL).

We claim that

| (4.8) |

Proof of the claim: First, since the covariance matrix of is , it follows that the covariance matrix of the vector is the identity matrix. Moreover, as

where

| (4.9) |

and

| (4.10) |

hold from [BW09] under A4. Finally, one can see that the element of can be rewritten as

where . By virtue of (4.9), we have

Hence, any component of verifies the LIL. That is for any ,

This fact concludes the proof of the claim (4.8).

Hence writing

it follows

∎

4.1.5 Proof of Proposition 2

It is sufficient to show that

| (4.11) |

where I is the identity matrix and O the null matrix. From [BW09], we have for and :

| (4.12) |

1/ If , then and the result is straightforward.

2/ For the second configuration, from [BKK21], we have

As a covariance matrix, is positive definite. Therefore the square root of is unique and blocks diagonal. Thus,

which gives (4.11). ∎

4.2 Technical Lemmas

Lemma 1.

Let (or ) and (or ) with . Assume that assumption A3 holds. Then for , it holds

| (4.13) |

Proof.

This Lemma has already been proved in [BKK20] in a more general framework. Let us prove the result for . Other cases can be deduced by using a similar reasoning.

We have for any ,

. Then,

By Corollary 1 of [KW69], (4.13) is established when:

| (4.14) |

1/ If , we deduce

| (4.15) |

Hence,

which is finite by definition of the class , and this achieves the proof.

2/ If ,

| (4.16) |

This fact along with Corollary 1 of [KW69] enable us to conclude the proof in this case. ∎

Lemma 2.

Under the assumptions of Theorem 2.3, for any model with , it holds

| (4.17) |

Proof.

Applying a second order Taylor expansion of around for sufficiently large such that which are between and yields (as since is a local extremum):

But can be rewritten as

First, as along side with Lemma 1, it follows

| (4.18) |

Writing a counterpart of (4.6) using the quasi-functions, we have

Hence can be rewritten as

| (4.19) | |||||

since from (4.7), it holds

and along with Lemma 1, it also holds

5 Acknowledgements

The author thanks Jean-Marc BARDET for proofreads and helpful discussions.

References

- [Aka73] H Akaike. Information theory and an extension of the maximum likelihood principle. Proceedings of the 2nd international symposium on information, Akademiai Kiado, Budapest, 1973.

- [AM09] S. Arlot and P. Massart. Data-driven calibration of penalties for least-squares regression. Journal of Machine learning research, 10:245–279, 2009.

- [BKK20] J.-M. Bardet, K. Kamila, and W. Kengne. Consistent model selection criteria and goodness-of-fit test for common time series models. Electronic Journal of Statistics, 14(1):2009–2052, 2020.

- [BKK21] J.-M. Bardet, K. Kamila, and W. Kengne. Efficient and consistent data-driven model selection for time series. Preprint, 2021.

- [BMM12] J.-P. Baudry, C. Maugis, and B. Michel. Slope heuristics: overview and implementation. Statistics and Computing, 22(2):455–470, 2012.

- [BW09] J.-M. Bardet and O. Wintenberger. Asymptotic normality of the quasi-maximum likelihood estimator for multidimensional causal processes. The Annals of Statistics, 37(5B):2730–2759, 2009.

- [DGE93] Z. Ding, C. Granger, and R.F. Engle. A long memory property of stock market returns and a new model. Journal of empirical finance, 1(1):83–106, 1993.

- [DW08] P. Doukhan and O. Wintenberger. Weakly dependent chains with infinite memory. Stochastic Processes and their Applications, 118(11):1997–2013, 2008.

- [FZ10] C. Francq and J.-M. Zakoian. GARCH models: structure, statistical inference and financial applications. John Wiley & Sons, 2010.

- [Han80] E.J. Hannan. The estimation of the order of an arma process. The Annals of Statistics, 8(5):1071–1081, 1980.

- [HD12] Edward James Hannan and Manfred Deistler. The statistical theory of linear systems. SIAM, 2012.

- [HQ79] Edward J Hannan and Barry G Quinn. The determination of the order of an autoregression. Journal of the Royal Statistical Society: Series B (Methodological), 41(2):190–195, 1979.

- [Ken20] William Kengne. Strongly consistent model selection for general causal time series. Statistics & Probability Letters, page 109000, 2020.

- [KW69] E.G. Kounias and T. Weng. An inequality and almost sure convergence. The Annals of Mathematical Statistics, 40(3):1091–1093, 1969.

- [LM03] S. Ling and M. McAleer. Asymptotic theory for a vector arma-garch model. Econometric theory, 19(2):280–310, 2003.

- [LMH04] E. Lebarbier and T. Mary-Huard. Le critère BIC: fondements théoriques et interprétation. PhD thesis, INRIA, 2004.

- [Mas07] P. Massart. Concentration inequalities and model selection. Springer, 2007.

- [Sch78] G. Schwarz. Estimating the dimension of a model. The Annals of Statistics, 6:461–464, 1978.

- [Shi86] Ritei Shibata. Consistency of model selection and parameter estimation. Journal of Applied Probability, pages 127–141, 1986.

- [SM06] D. Straumann and T. Mikosch. Quasi-maximum-likelihood estimation in conditionally heteroscedastic time series: A stochastic recurrence equations approach. The Annals of Statistics, 34(5):2449–2495, 2006.

- [Whi82] H. White. Maximum likelihood estimation of misspecified models. Econometrica, pages 1–25, 1982.