remarkRemark \newsiamremarkhypothesisHypothesis \newsiamthmclaimClaim \headersMAP Inference on Random Dot Product GraphsD. Wu, D. Palmer, and D. DeFord

Maximum A Posteriori Inference of Random Dot Product Graphs via Conic Programming††thanks: Submitted to the editors January 6, 2021. \funding

Abstract

We present a convex cone program to infer the latent probability matrix of a random dot product graph (RDPG). The optimization problem maximizes the Bernoulli maximum likelihood function with an added nuclear norm regularization term. The dual problem has a particularly nice form, related to the well-known semidefinite program relaxation of the maxcut problem. Using the primal-dual optimality conditions, we bound the entries and rank of the primal and dual solutions. Furthermore, we bound the optimal objective value and prove asymptotic consistency of the probability estimates of a slightly modified model under mild technical assumptions. Our experiments on synthetic RDPGs not only recover natural clusters, but also reveal the underlying low-dimensional geometry of the original data. We also demonstrate that the method recovers latent structure in the Karate Club Graph and synthetic U.S. Senate vote graphs and is scalable to graphs with up to a few hundred nodes.

keywords:

random dot product graph, maximum a posteriori, Bayesian inference, regularization, maximum likelihood estimation, inference, conic programming, convex relaxation, clustering, graph embedding, latent vectors, low rank, consistency62F15, 90C35, 65F55, 68R10, 15B48

1 Introduction

Real-world networks appearing in neuroscience, sociology, and machine learning encode an enormous amount of structure in a combinatorial form that is challenging to analyze. A promising analytical approach is to make this structure manifest as geometry. Generative random graph models offer a statistically rigorous way to formulate these problems.

Among the simplest random graph models is the well-known Erdös-Rényi graph , a random graph on nodes with independent edge probabilities all equal to . Because all vertices look the same in this model, it is too weak to explain common latent structures that appear in real graphs, such as clusters.

It is natural to hypothesize that such structures appear due to underlying affinities between nodes. For example, nodes in a social network represent people who might cluster together based on their shared interests. This hypothesis suggests a natural geometric random graph model in which nodes have latent vectors of characteristics, and edge probabilities come from the inner products of these vectors. This model, first studied by Young and Scheinerman [44], is called the random dot product graph (RDPG). In fact, many random graph models, including the Erdös-Rényi graph and the stochastic block model (SBM) [1] can be viewed as special cases of the RDPG model.

In this paper, we study the problem of recovering the latent vectors from a graph under the RDPG assumption. While the asymptotic behavior of the RDPG model has been analyzed carefully, we show that with an appropriate prior, the maximum a posteriori (MAP) problem can be formulated as a convex cone program, featuring a single semidefinite cone constraint coupled to many exponential cone constraints. This problem is easy to formulate, and it is solvable in polynomial time via commodity conic solvers [4, 29]. Moreover, we show that under mild sparsity and nondegeneracy assumptions the solution for a closely related model is asymptotically consistent, and that in practice, our method can reveal a variety of latent geometry in RDPGs. In doing so, we take first steps towards connecting the subfields of latent vector graph models and conic programming.

1.1 Preliminaries

Let be a simple undirected unweighted graph with nodes and edges. For distinct and , we write if , and if . In the RDPG model, every node in the graph comes with a latent vector , and edge probabilities are given by the inner products of these latent vectors, . We assemble these edge probabilities into the edge probability matrix . It is important to note that diagonal elements of do not have any probabilistic interpretation since our graphs are assumed to be simple. Conditioned on , an RDPG with adjacency matrix has entries that are independent Bernoulli random variables with corresponding parameters . That is, we have

An implicit assumption of the RDPG model is that the embedding satisfies the constraints for all . One can either view the node embeddings as fixed or themselves drawn from a latent vector distribution. Although most prior works use the linear dot product structure, the recent work of O’Connor et al. [28] forms the edge probability matrix from the latent vectors using a more general link function such as the logistic sigmoid function.

The primary problem of interest is the inference of either the probability matrix or the latent vectors from one sample of . Note that for a fixed , the latent embedding is only unique up to a -dimensional orthogonal transformation. However, it is still possible to extract an embedding from via a Cholesky decomposition or eigendecomposition.

1.2 Maximum Likelihood

In this paper we solve an MAP problem with conic programming to recover the probability matrix and latent vectors of an RDPG. In this section, we first formulate the maximum likelihood problem, and then we show that regularization is necessary to recover a nontrivial solution.

Observe that is positive semidefinite (PSD) by construction. Conversely, if is PSD then it can be decomposed as for some where . Given an adjacency matrix , this leads to the following maximum likelihood problem Eq. MLE:

| (MLE) | ||||||||

| subject to: | ||||||||

where the notation means that is PSD. It is important to note that the diagonal entries of are unconstrained. This makes Eq. MLE highly underconstrained—as we show below, the solution reproduces with nonzero diagonal entries to ensure semidefiniteness.

Proposition 1.1.

There exists an optimal solution of Eq. MLE whose off-diagonal entries coincide with those of .

Proof 1.2.

For feasible , we have , with equality achieved at . Similarly, , with equality achieved at . Thus, the objective function can be maximized by setting if and if , so long as the semidefiniteness constraint is satisfied. As the diagonal of is unconstrained, we can ensure by shifting the diagonal. In particular, for sufficiently large .

1.3 Regularization and MAP estimate

In view of Proposition 1.1, it is prudent to regularize Eq. MLE to obtain a nontrivial solution. We do so with the hope of encouraging low rank solutions, which are of particular theoretical and practical interest. For example, low rank solutions are easier to visualize. In addition, low-rank solutions to semidefinite optimization problems are often more efficient to compute via specialized algorithms that take advantage of the low rank, such as the Bürer-Monteiro method and extensions [10, 8, 14]. One might hope that such low-rank methods would extend to the optimization problems featured in this paper.

With the goal of a low-rank estimate in mind, we choose a prior that encourages the vector of eigenvalues of the probability matrix to be sparse. One such prior is the Laplace distribution on . This aligns with a common heuristic for encouraging low rank solutions, which penalizes the nuclear norm , where are the singular values of [33, 18]. Some justification for the heuristic can be provided by noting that the nuclear norm is the convex envelope of the rank function, i.e. , where denotes the operator norm of . The nuclear norm of a PSD matrix is just its trace. This leads to the following refinement Eq. REG of Eq. MLE, which can be interpreted as an MAP estimation problem under the aforementioned Laplace prior, parametrized by a real scalar :

| (REG) | ||||||||

| subject to: | ||||||||

As with any inference technique, the MAP estimate varies with the observed realization ; given a nondegenerate true edge probability matrix , any simple undirected graph is realizable, including the empty graph. As such, we cannot expect to prove deterministic bounds on inference performance; probabilistic results are more reasonable.

The constraints of Eq. REG are of semidefinite program (SDP) type, but the objective function is nonlinear. The problem can be rewritten as a convex cone program. Introducing new variables for and for , and noting that at optimality these inequalities turn into equalities, we can express the original objective function in a manifestly convex form. We can encode these inequalities with exponential cones. Conveniently, including these inequalities for all also automatically enforces the inequality constraints . We state the definitions of the primal and dual exponential cones below for reference [4].

Definition 1.3 (exponential cones).

The primal exponential cone is the set

The dual exponential cone is its conic dual

Applying these transformations, we obtain the following convex cone program, equivalent to Eq. REG:

| (CREG) | ||||||

| subject to: | ||||||

The cone program Eq. CREG is the main subject of study in this paper. Moreover, it can be easily implemented with convex optimization interfaces such as CVXPY [20, 2] that rely on solvers that support both semidefinite and exponential cone programming such as SCS [29] and MOSEK [4]. As we will see later, the dual conic program turns out to have an appealing interpretation. Finally, we remark that given the binary matrix of Proposition 1.1, one approach (quite different from ours) that is particularly suited for clustering tasks is to attempt to factor into the product of two low-rank binary matrices [45]. However, since binary edge probability matrices are degenerate from the generative perspective, our cone program is more appropriate for the RDPG model. Furthermore, our method recovers richer geometrical structure than simple clusters.

1.4 Related work

Prior work on RDPG latent vector recovery has focused on spectral methods such as the adjacency spectral embedding (ASE) and Laplacian spectral embedding (LSE); see [6] for a comprehensive review. Assuming the latent vectors reside in , the ASE entails taking the top- eigenvector approximation of the adjacency matrix . It is known that this provides a consistent estimate of the latent vectors, up to an orthogonal transformation [38]. Furthermore, asymptotic normality results exist for the ASE [7] and LSE [37]. In addition to these theoretical results, these spectral techniques have been applied to graph machine learning, including vertex nomination [43, 3], vertex embedding and classification [36, 12], and joint embedding [40] problems.

One limitation of the ASE is the requirement that the embedding dimension is known in advance. In order to address these limitations, Yang et al. [42] have recently proposed a framework for simultaneously discovering the rank and number of clusters for SBMs using an extended ASE and the Bayesian information criterion. We instead propose a cone program with an adjustable regularization hyperparameter, so that our method does not require a priori knowledge of . Empirically, we show that our method (which applies for general RDPGs) leads to a cross validation procedure for rank discovery. Furthermore, our method outperforms the vanilla ASE on clustering tasks and spectral norm distance, even when the true is known.

Maximum likelihood (ML) approaches to recovering matrix structure or solving graph problems are common in the literature. Arroyo et al. [5] studied the graph matching problem in corrupted graphs via ML estimators. For the specific problem of latent vector recovery, Choi et al. [13] studied ML estimation for the SBM and showed that the when the number of blocks is , the fraction of misclassified nodes converges in probability to 0. For latent vector graphs with a logistic sigmoid link function, O’Connor et al. [28] give a spectral approximation algorithm that is asymptotically equivalent to ML latent vector recovery, but do not directly study consistency results. Our cone program does not directly depend on any spectral algorithms, but we are still able to study consistency and likelihood properties.

This work joins a body of literature that applies convex relaxation methods to broader statistical inference problems, such as Logistic PCA [15, 23], angular synchronization [35], and compressed sensing [17, 11]. In fact, semidefinite relaxations, which are special cases of cone programs, have been used to study SBM inference [1]. The convex relaxation method has also been fruitfully applied to low rank matrix recovery, by relaxing the nonconvex rank function to a nuclear norm or max norm [17, 11]. Standard statistical learning theory arguments are used to bound the generalization error. Equipped with our cone program relaxation, we demonstrate a novel application of tools from conic programming to the problem of RDPG inference.

Our proof technique for consistency bounds takes inspiration from the matrix completion literature, but some care must be taken because of the failure of a Lipschitz-like criterion. Our approach also adds a trace penalty term rather than restricting the feasible set, which leads to looser requirements for the true when formulating consistency results.

1.5 Main contributions

We summarize our main contributions below. We lay down theoretical foundations for the RDPG inference problem using a convex cone programming approach. We believe that the inference and conic optimization perspective offers insights that have not been leveraged in the study of these latent vector models. Our analysis, which centers around the study of our cone program’s optimality conditions, yields interesting theoretical properties of the inference problem.

After taking the dual in Section 2, we use the primal-dual optimality conditions to derive an explicit relationship between the primal and dual optimal solutions and (see Propositions 2.5 and 3.1). Based on our bounds on the entries of and , we attempt to control their ranks. Unfortunately, we demonstrate a counterexample and a fundamental barrier to using our proof technique to prove that decreases arbitrarily as (see Proposition 3.6). On the other hand, we see in Sections 3.2 and 3.3 that our optimality bounds lead to asymptotic likelihood bounds and consistency bounds for a slightly modified model (see Theorems 3.11 and 3.15, respectively).

In Section 4, we show empirical evidence that our inference approach indeed recovers fine-grained latent vector geometry. Moreover, our algorithm’s single regularization hyperparameter enables the use of simple cross-validation and a parameter sweep to discover the rank of . Our cross-validation experiments provide strong evidence for uniqueness of the optimal regularization parameter and rank. Discussion and conclusions follow in Section 5.

2 Dual cone program

In order to analyze the optimal solutions of Eq. CREG, it is fruitful to analyze its dual program. Proofs of the following propositions are provided in Appendix A. As a first step, we verify Slater’s condition, which is sufficient for strong duality [9]:

Lemma 2.1.

The feasible region of Eq. CREG has an interior point.

Proof 2.2.

Set for all , for all and . For sufficiently large , is positive definite and furthermore , so Slater’s condition holds.

Proposition 2.3.

We can further reduce the dual as follows:

Lemma 2.4.

The following relations hold at optimality:

-

1.

If and , then and .

-

2.

If and , then and .

-

3.

If and , then and .

-

4.

If and , then and .

Imposing these relations explicitly, we arrive at the following reduced formulation, which agrees with Eq. DREG at optimality:

| (DCREG) | ||||

| subject to: | ||||

Using the complementary slackness conditions for the exponential cones, we obtain the following explicit relationships between and .

Proposition 2.5.

Proof 2.6.

Suppose and . The KKT conditions Eqs. 2 and 3 together with Lemma 2.4 imply that

| (4) |

Recall from the definition of Eq. CREG that ; at optimality this inequality becomes an equality. Applying Lemma A.2, we see that Eq. 4 has the unique solution , so as desired. On the other hand, if , then the KKT conditions yield . Thus Lemma A.2 also yields .

The other two statements for follow similarly.

These explicit relationships between and lead to bounds on the entries of , including the following corollary.

Corollary 2.7.

Suppose . If , then , and if , then .

Proof 2.8.

Since and , it follows that . The conclusions then follow upon applying Proposition 2.5.

Note that can be decomposed as , where . Thus the rows of lie on the -sphere with radius , and is the dot product between the th and th rows of . By Proposition 2.5, it follows that if , the indices where correspond to the indices where . Similarly, if , the indices where correspond to the indices where .

2.1 Connection to MAXCUT

Inspecting Eq. DCREG and noting that , it follows for that we have the following problem with an objective that is homogeneous in :

| (5) | ||||||

| subject to: | ||||||

In fact, this is an instance of the SDP relaxation of maxcut with weight matrix equal to the adjacency matrix [22]. This suggests that Eq. CREG has deeper connections to classical combinatorial graph structure recovery problems. This also implies that the off-diagonal entries of the optimal do not change in the region . In particular, we recover as in Proposition 1.1.

3 Main results

We now derive our major results on the behavior of optimal solutions to Eq. CREG and Eq. DREG. Naturally, an optimal solution to the MAP problem will still tend towards larger probabilities where there are edges and smaller probabilities where there are nonedges. However, the penalty term also constrains the norms of the individual latent vectors.

These bounds on the inferred probability matrix allow us to further study properties of the inference problem, such as consistency, in Section 3.3. Perhaps unsurprisingly, our bounds depend on node degrees and the regularization parameter . In fact, we show that for all and , so the probabilities and latent vector lengths can be made arbitrarily small for sufficiently large . These bounds follow solely from the complementary slackness conditions and basic facts about PSD matrices.

Proposition 3.1.

Suppose that , and write for all . Then the following bounds hold.

| (6) | |||||

| (7) | |||||

| (8) |

Additionally, if , we have:

| (9) | |||||

| (10) |

Proof 3.2.

The complementary slackness condition (see Proposition 2.3) furnishes us with equations. Focusing on the diagonal entries and applying Proposition 2.5 provides crude bounds on the entries of and .

In particular, from , we obtain for each

| (11) |

Since , and the sum over has terms, we have , which proves the second inequality of Eq. 6. Since the first and third terms of Eq. 11 are nonnegative, the sum over must be nonpositive, so . Eq. 8 follows by symmetry.

In a PSD matrix, every submatrix is PSD, so we have

which is Eq. 7. On the other hand, we have

where the last inequality follows from Corollary 2.7. Hence the first inequality of Eq. 6 holds.

A couple points are worth noting. If node is isolated, i.e. , then the learned latent vector is the zero vector. More generally, the maximum size of is controlled by the connectivity of nodes and . Finally, we immediately obtain the following corollary characterizing the trace of .

Corollary 3.3.

Let be the number of edges in . We have

| (12) |

Furthermore, if then

| (13) |

Proof 3.4.

Remark 3.5.

With , as discussed in Section 2.1, the dual cone program reduces to maxcut, and the corollary gives . In this case, we can construct an explicit optimal solution to Eq. MLE that saturates the trace bound for . Indeed, the signless Laplacian , where , is PSD, its off-diagonal entries are those of , and [16]. Also for , the discussion in Section 2.1 implies for .

3.1 Rank of optimal solutions

Since our problem is aimed at recovering low rank solutions, it behooves us to study the rank of optimal solutions. We propose a strategy for analyzing the rank, partly motivated by our bounds on the trace of optimal solutions. We construct an example where ; hence, no deterministic bound can show that , although a probabilistic rank bound may still hold. Furthermore, we establish that in the regime where , the naive trace-rank inequality furnished by the convex envelope relationship can only show that . Hence, the trace-rank inequality gives the best possible deterministic bound in that regime. In doing so, we narrow the possible hypotheses for a positive rank reduction theorem.

The relevant optimality condition for studying the rank comes from the PSD constraint that . It follows that . Therefore, we can upper-bound by lower-bounding . It is natural to formulate bounds using the trace, as the trace is the convex envelope of rank. More precisely, for any , . Conveniently, by construction, so it remains to upper-bound the operator norm . To that end, we hope to apply the Gershgorin disks theorem.

However, we now show that for sufficiently large , this method cannot show that .

Proposition 3.6.

Let be an optimal solution to Eq. DREG. Then for any , the tightest bound offered by Gershgorin is . Furthermore, this bound is tight.

Proof 3.7.

If , then Proposition 3.1 implies that for all . Therefore for , Proposition 2.5 implies that . Even if we assume that for all and for all , Gershgorin gives

To see that this bound is tight, consider the graph consisting of disconnected 2-cliques. From Proposition 3.1, for all . Similarly, for , and Eq. 11 implies that for . Then the rank of is clearly .

Remark 3.8.

The phenomenon of vanishing entries of posing an obstruction to rank results can be generalized as follows. For , let be the set of pairs with such that . Form the complement of the induced subgraph of . For any positive , if this complement graph contains a -clique, then , as there are at least mutually orthogonal latent vectors. In Sections 3.2 and 3.3 we will see how vanishing entries are also troublesome for consistency results.

3.2 Likelihood bounds

Armed with the results of previous sections, we hope to study consistency results. We argue that for Eq. CREG, it is natural to formulate consistency results in terms of the Kullback-Leibler (KL) divergence. However, we find that the KL divergence is not well behaved. Instead, we are able to show that the (closely related) difference in Bernoulli log likelihoods of the true and the inferred is with high probability.

To begin the discussion, we define the following notation and link the Bernoulli likelihood function to the KL divergence away from the diagonal.

Definition 3.9.

The Bernoulli likelihood given an adjacency matrix is defined as

This is precisely the objective function in Eq. MLE. We denote the regularized objective function by

Definition 3.10.

We define the matrix KL-divergence between and to be the mean off-diagonal entrywise divergence—that is,

We define the quantity only on the off-diagonal entries because the diagonal entries of do not carry probabilistic meaning. For a fixed , the definitions imply that

| (14) |

where the expectation is taken with respect to the random adjacency matrix distributed according to . All subsequent expectations, unless noted otherwise, are also taken with respect to .

Let be sampled i.i.d. from . Denote by the optimal solution to Eq. CREG with realization and hyperparameter . We hope to develop an upper bound on . We first claim that it is impossible to obtain a finite deterministic bound on this quantity. Suppose that for all , so that is the empty graph with positive probability. Assuming is indeed the empty graph and is nonempty, it follows that . However, we can still hope for a probabilistic bound. For example, if one could identify conditions on under which with high probability, then the results of Section 3.3 apply.

Nevertheless, it is clear that the likelihood function of Eq. CREG merits its own study. We present our main result in this direction below; the details of the proof are provided in Appendix B. The upshot is that with high probability, the likelihood difference is .

Theorem 3.11.

Let and let . Then we have

| (15) |

Furthermore, for and , we have

| (16) |

and

| (17) |

with probability at least . Here, we have defined , the entropy of the edge probability matrix.

Proof 3.12 (Proof sketch).

Since is feasible for the convex program Eq. CREG,

| (18) | ||||

| (19) |

Rearranging yields Eq. 15. To show Eqs. 16 and 17, we first use a recent Bernoulli concentration result [46, Corollary 1] to bound with high probability. Then we bound by constructing primal and dual feasible points and applying Corollary 3.3.

From here, we can apply Hoeffding’s inequality to shift the bound’s dependence on to dependence on with high probability, yielding the following corollary.

Corollary 3.13.

Suppose . Then with high probability, .

3.3 Consistency guarantees for a modified program

We now turn to formulating a consistency bound after slightly modifying Eq. CREG. In particular, we impose the mild assumption that for . We think of these as nontriviality conditions—they ensure that no node has expected degree less than or greater than . Under this model, we obtain that with high probability, the KL divergence is . We also identify conditions under which this bound is effective.

With these new constraints, the primal problem becomes

| (REG-MOD) | ||||||||

| subject to: | ||||||||

With the additional constraints in Eq. REG-MOD, a duality analysis produces the following bound (cf. Corollary 3.3); see Appendix B for the complete proof. To state the result we recall the notation introduced in Remark 3.8. We extend the notation in a few ways. First, we let denote the set of indices where . Next, we define and , extending the definition to in the obvious way. Finally, we define .

Proposition 3.14.

We assume that the true is feasible for Eq. REG-MOD, so that . For clarity, we denote by the centered random variable . Recalling Eq. 18, but this time adding and subtracting expectations, we find that

Theorem B.1 gives us concentration of , so it suffices to obtain a probabilistic upper bound on . We bound this quantity over a compact neighborhood of rather than directly bounding it for . In particular, define the set to be the intersection of the feasible set of Eq. REG-MOD with the trace ball centered at the origin with radius . Clearly , and since Proposition 3.14 controls , is a compact subset of the original feasible set. Thus it suffices to probabilistically upper-bound .

Indeed, this can be achieved through a similar approach to that in [17]; the details of the proof are left to Appendix C. The upshot is that for sparse enough graphs, we indeed obtain consistency as the number of nodes in the RDPG increases.

Theorem 3.15.

Let be an optimal solution to Eq. REG-MOD, and suppose is feasible for Eq. REG-MOD. Then there is an absolute constant , such that with probability at least , we have

A quick application of Proposition 3.14 and Theorem B.1 yields the following corollary.

Corollary 3.16.

With high probability, we have

where is the expected number of observed edges.

Remark 3.17.

There are two sources of the probabilistic nature of the bound: and the concentration of . We can for example take and in Theorem B.1.

We discuss the shape of the bound and its implications. Note that a priori

since for every feasible we have . Further inspection of Corollary 3.16 reveals that under certain conditions on and , Theorem 3.15 nontrivially improves on this bound and gives consistency as .

Corollary 3.18.

Suppose . Then the optimal with respect to the bound in Corollary 3.16 satisfies . If we further have and , then with high probability.

Remark 3.19.

Note that owing to Lemma C.1, the assumption on is the tightest possible one. The exact assumption on can potentially be relaxed if the proof of Proposition 3.14 is refined.

4 Experimental results

We investigate the performance of the inference technique for a variety of tasks. We find that the learned embedding appears to be pushed towards lower and lower ranks as the regularization hyperparameter is increased. Motivated by this, we examine regularization profiles that demonstrate that Eq. CREG improves on the ASE in the spectral norm distance. This naturally leads to a cross validation procedure to select an embedding dimension. Through visualization and cluster analysis, we also find that our method recovers latent geometry better than the ASE in synthetic and more realistic networks.

The two primary quantities of interest for a solution to Eq. CREG are (1) its fit to the true and (2) its rank, which we denote by . The former, which measures consistency, is difficult to measure directly with real data because we do not usually know . Similarly, we might not know the true dimension of the underlying latent vector distribution, so we must balance other considerations to select a value of the regularization parameter . As a first step towards understanding how affects , we present the spectra in Fig. 1, which illustrates an inverse relationship between and . This makes sense since Eq. CREG is an MAP problem where controls the strength of the Laplace prior on the spectrum of . In subsequent sections we also observe this phenomenon of approximate low rank solutions as we increase ; a similar phenomenon has been studied in related matrix completion problems [33].

To examine how well our inference procedure recovers the rank and geometry of the true , we turn to synthetic data, sampled from an RDPG with a known latent vector distribution. In Section 4.2, we consider three classes of synthetic data: the SBM with a fixed block probability matrix, latent vector distributions supported on , and latent vector distributions supported on the unit ball in .

4.1 Implementation details

The convex cone program Eq. CREG was implemented in CVXPY using the MOSEK [4] and SCS [29] solvers. Both solvers support semidefinite and exponential cone constraints, but differ in their algorithms: MOSEK uses an interior point method, while SCS uses the alternating direction method of multipliers (ADMM). In general, we found that MOSEK converges to more accurate solutions than SCS. On the other hand, as SCS uses the first-order ADMM, it can handle larger problem instances.

Given , we measured the closeness of fit between and by directly computing . In order to compute , we used the eigvalsh function in the scipy.linalg package, with a tolerance of for MOSEK and for SCS. These thresholds were selected based on empirical observations of eigenvalue spectra for such as the one shown in Fig. 1, and reflect a disparity in numerical precision between the solvers.

4.2 Synthetic data experiments

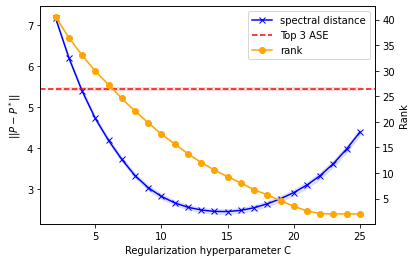

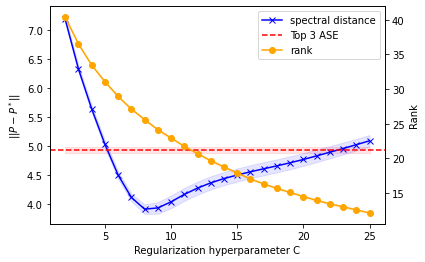

In order to evaluate the consistency of Eq. CREG, we conducted the following three experiments, all using MOSEK for conic optimization. In each experiment, we sampled latent vectors from a fixed distribution and formed a probability matrix . Keeping fixed, we then generated RDPGs, and for each RDPG we ran the inference problem for with a step size for . We computed spectral distance and for each RDPG and each value of .

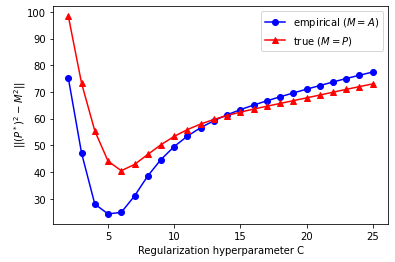

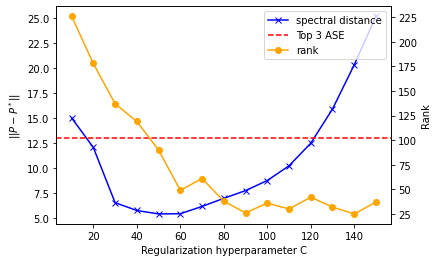

Interestingly, although the spectral norm distance does not achieve its local minimum where , we will later see that the 3D and 2D visualizations are still salient. We also point out the smoothness of the cross validation curve and the clear local minimum for the spectral norm at , with , corresponding to a significant dimensionality reduction from the original rank 50 solution.

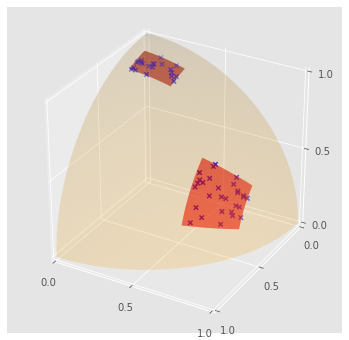

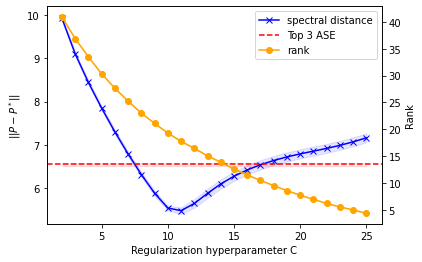

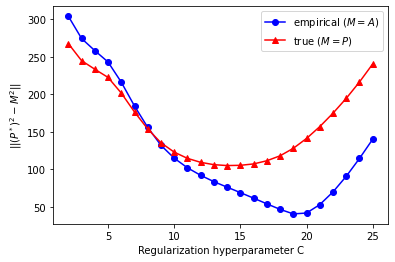

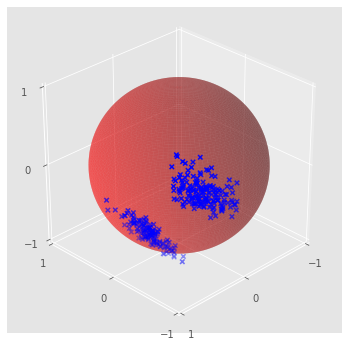

In Fig. 3(b), we show the results from the two balls in the nonnegative unit ball depicted in Fig. 2(b). We chose this example because the latent vectors do not all have the same Euclidean norm, which could reasonably be interpreted as a disparity in the intrinsic popularities of nodes in the RDPG. In Fig. 3(b), we see that the light blue shaded band representing the two–standard deviation interval is wider. Indeed, since the intra-cluster probabilities are not close to 1 (unlike the previous experiment), there is higher variance in the realizations of the RDPG. Nevertheless, we observe a local minimum at for the cross validation curve and a monotonic relationship between and .

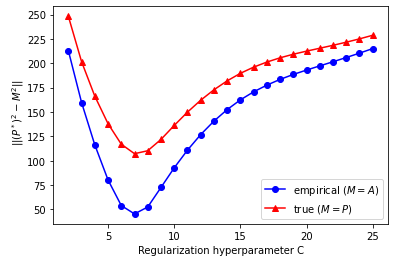

In Fig. 3(c), we depict the results from an SBM with blocks of respective size 15, 10, and 25, using the block probability matrix . Although the SBM had three clusters (as the block probability matrix is ), the cross validation graph is visually similar to that in Fig. 3(b), where the ground truth only contained two clusters.

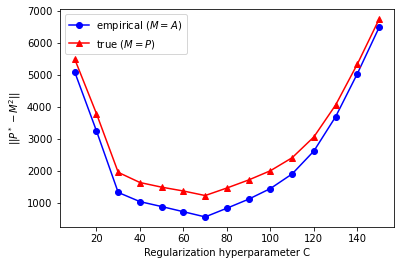

In Figs. 3(a), 3(b), and 3(c), it is apparent that our method beats the ASE in terms of spectral norm distance, even when the ASE is given oracle access to . Even if is unknown, the same cross validation procedure can be used by simply replacing with in the metric. However, we found experimentally that using does not perform as well as using for cross validation purposes. Hence we computed the latter metric for the inferred solutions in the earlier experiments to obtain the curves in Figs. 4(a), 4(b), and 4(c). Interestingly, the shapes of the two curves are very similar, especially in Figs. 4(b) and 4(c). More importantly, they have similar local minima as a function of . Thus, it is reasonable to use this cross validation technique to select the best and thus single out a preferred embedding or rank.

4.3 Visualization through latent vector extraction

Given the solution for some in Eq. DREG, we can extract an embedding by taking the top 2 or 3 eigenvectors and scaling them by the square roots of their eigenvalues. We have seen that selecting via cross validation can recover better solutions measured by the spectral norm; the hope is that the same effect can also be observed visually.

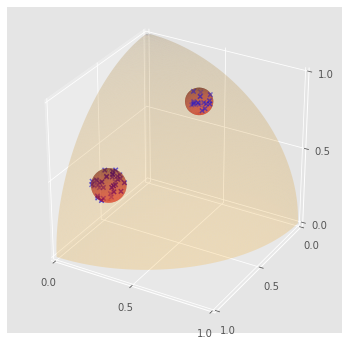

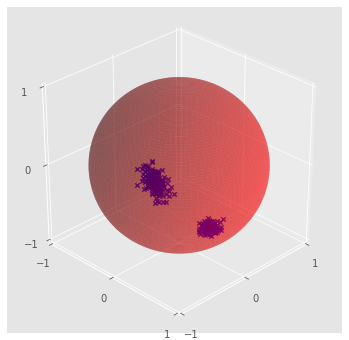

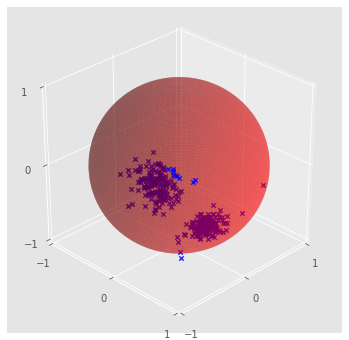

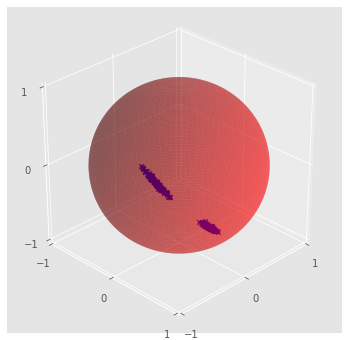

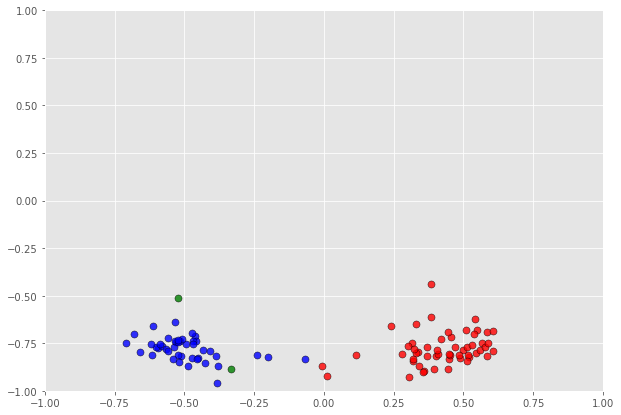

We conducted the following experiment to demonstrate the improvement in visualization capabilities in 3 dimensions over the ASE and the applications of the inference technique to larger graphs. Starting from the synthetic distribution illustrated in Fig. 2(a), we generated an RDPG with 300 nodes; note the two clusters on that support the distribution. Using SCS, we computed the regularization profile and cross validation plot for with a step size of 10 (shown in Figs. 5(c) and 5(d)) and selected the best in spectral norm distance. We then visually compared the top-3 eigenvector embedding with the top-3 eigenvector ASE. Figure 5(a) demonstrates that the ASE, while approximately recovering the geometry of the latent vector distribution, is more diffuse than the corresponding visualization in Fig. 5(b). In particular, notice in Fig. 5(b) that fewer of the embeddings lie outside of , and that the geometry more closely matches that displayed in Fig. 2(a).

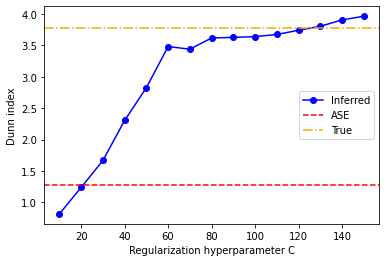

We also demonstrate the clustering effects of increasing regularization. Using the same 300 node RDPG, we compare the top-3 eigenvector visualizations for various values of in Figs. 6(a), 6(b), and 6(c). The shape of the embedding remains relatively consistent as is increased. As is increased, the numerical rank of decreases, and the two clusters become more compact.

In order to quantify this notion, we use the Dunn index [21]; larger Dunn indices correspond to more compact clusters. In Fig. 6(d) we see that as is increased, the Dunn index also increases. Notice that the ASE has a low Dunn index, and that as increases, the learned embeddings approach a Dunn index close to that of the true embedding. Furthermore, the best embedding (around ) determined in Figs. 5(c) and 5(d) has a similar Dunn index to the true embedding.

4.4 Realistic network experiments

We first study embeddings of the Karate Club Graph. We solved the inference problem for with a step size of . In Fig. 7(b), we select the smallest with and compare the latent vector visualization to that of the top-2 eigenvector ASE. The color of each node represents which community it belongs to. Comparing the two embeddings, we note that the positions of the communities are swapped, which illustrates the inherent nonidentifiability of the embedding. The shrinkage effects of increasing regularization are also apparent. Although both the ASE and our method make the communities linearly separable, our method tightens the clusters more than the ASE does.

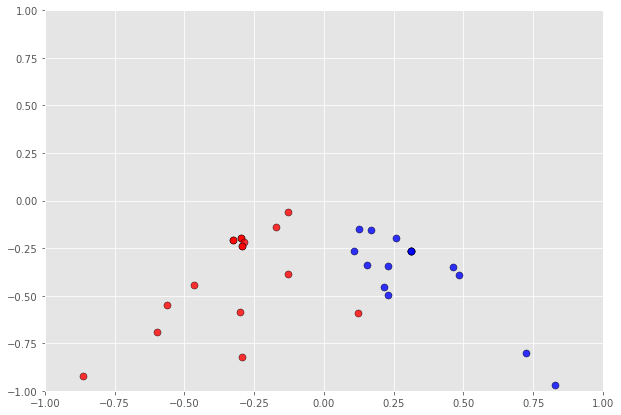

Fig. 8 depicts the results of an experiment using synthetic data generated from the voting patterns of the 114th U.S. Senate. We choose this session as all senators were active throughout the entire session. Similar latent space models [30, 31] and network analyses of community detection from voting data have been studied in [19, 25, 26, 27, 32, 41]. The edge probability is defined to be the fraction of votes in which and voted the same way. If this vote agreement data fits the RDPG assumption, our inference procedure should be able to recover two well defined clusters corresponding to the Democratic and Republican political parties. Indeed, Fig. 8(b) reveals an inferred embedding that displays the two clusters prominently. Moreover, the nodes in the middle represent the more moderate senators, suggesting that the model recovers accurate detailed geometry.

5 Conclusions

We have presented a conic programming approach to MAP inference of latent vector embeddings of RDPGs. Our inference technique offers a different perspective on recovering RDPG latent geometry compared to existing methods which typically center around spectral decompositions of graph matrices. The conic formulation led to a surprisingly explicit relationship between the primal and dual problems. Importantly, the exponential cone constraints yield an exact algebraic relationship between the optimal solutions to the primal and dual problems, whereas the semidefinite cone constraint and trace regularization lead to bounds on the optimal solutions.

Some of the limitations of our analysis stem from a lack of nontrivial lower bounds on . For example, while we’ve shown the impossibility of a useful deterministic bound on rank for large , a better handle on elementwise lower bounds would likely produce a nontrivial rank reduction result for small . Similarly, lower bounds would enable a probabilistic KL consistency result that does not require the model to be altered. In particular, if one is able to prove that , then the results of Section 3.3 immediately follow.

The experimental results show that it is often possible to recover solutions of arbitrary rank by varying the regularization parameter . It is not possible to do so for all realizations, as established by Proposition 3.6. Nevertheless, we conjecture that with high probability, the rank of inferred embeddings can be reduced nontrivially, say to order . Although we were not able to prove spectral norm consistency of the extracted embedding, the results of our cross validation and visualization experiments suggest nontrivial improvements on the ASE over a certain bounded range of values. Furthermore, we observe that as increases arbitrarily, the spectral norm distance worsens, which agrees with the theoretical guarantee that the entries of are .

The proposed conic optimization problem is solved via second-order methods using MOSEK and via the first-order ADMM method using SCS. For the algorithm to be of interest for larger graphs, there would likely need to be a first-order implementation that could exploit low-rank complexity reductions. In this vein, an extension of the Bürer-Monteiro method [14], along with more theoretical guarantees of optimality, would be particularly interesting.

Appendix A Derivation of dual program

Proof A.1 (Proof of Proposition 2.3).

Form the Lagrangian of Eq. CREG, with notation defined as in Section 2. Swapping the and operators and eliminating the primal constraints by enforcing the dual constraints, we obtain

Collecting terms involving each primal variable, we obtain

where and .

This is in turn equivalent to the following dual program:

| (22) | ||||||||

| subject to: | ||||||||

These explicit constraints follow from Lagrangian duality, or alternatively by noting that the outer minimization necessarily avoids inner objective values of .

Recall from Definition 1.3 that

Applying the explicit constraints in Eq. 22, we simplify the dual objective function as follows:

-

•

For , simplifies to . Also, implies that . Since there are no other constraints on , and since we are minimizing , it follows that at optimality for . Hence we can rewrite the as .

-

•

For , the constraint for simplifies to . Similarly, implies that , and at optimality . Hence we can rewrite as . Putting these steps all together, the objective function becomes

Thus we obtain Eq. DREG, as desired.

We now prove the following simple lemma which is useful in the proof of Proposition 2.5 and Lemma 2.4.

Lemma A.2.

Let be a positive real number. If or , then . Similarly, let be a negative real number. If or , then .

Proof A.3.

First suppose . By inspection, satisfies . Since is monotonic, is the unique solution. Since is strictly convex and has a critical point at , is the unique solution. The case of follows similarly.

Proof A.4 (Proof of Lemma 2.4).

Note that is constrained by a single inequality and is being minimized in the objective function. Thus, at optimality, the inequality becomes tight, and we have . By a similar argument, at optimality. These considerations reduce the dual to the following form, equivalent at optimality:

| (23) | ||||||||

| subject to: | ||||||||

We simplify the dual further by considering each pair individually:

-

•

Suppose . Substituting for , the corresponding objective term is . If , then by Lemma A.2 this has a unique minimum at , which is in the feasible region. Thus in this case , and the objective term reduces to .

On the other hand, if , then due to domain constraints and monotonicity of the objective, the minimizer is , so . Thus, in this case the objective term is .

-

•

Next, consider the term where . If , then this has a unique minimum at by Lemma A.2. Furthermore, the constraint is satisfied. These terms vanish in the objective function. However, if , then the optimal choice for is . In this case , which simplifies the objective term to , thus proving the claim.

Appendix B Proofs of likelihood bounds

We begin by restating the recent Bernoulli concentration result from [46].

Theorem B.1 ([46, Corollary 1]).

For , with , and all , we have

Proof B.2 (Proof of Theorem 3.11).

We construct an upper bound by way of a dual-feasible solution to Eq. DCREG in the restricted domain of symmetric diagonally dominant matrices, which are manifestly PSD. We construct a dual-feasible, diagonally dominant as follows.

| (24) |

In fact, for , Eq. 24 is optimal for symmetric, diagonally dominant . To see this, note the following facts.

-

•

The objective function of Eq. DCREG is monotonically nondecreasing in .

-

•

When we impose diagonal dominance, the program decouples for each .

-

•

The non-edge contribution to the objective function is nonnegative and vanishes for .

Using these facts, the restricted program decouples to the following for each :

| (DCREG-RES) | |||||

| subject to: | |||||

The assumption that ensures that the feasible set is nonempty. In fact, Eq. DCREG-RES can be analytically minimized using AM-GM to see that indeed we should take .

Thus , and combining this with Corollary 3.3, we obtain

| (25) |

For the upper bound on , note that the scaled signless Laplacian in Remark 3.5 achieves objective value for Eq. CREG. Hence applying Theorem B.1 again we obtain Eq. 17.

Appendix C Proofs of consistency results

Lemma C.1.

For any RDPG generated by edge probability matrix , we have

| (26) |

Proof C.2.

The first equality immediately follows from the generative model. For the inequality, note that since is PSD, we have . Summing over all , we obtain , and the result follows by symmetry of .

Now we take the dual of Eq. REG-MOD in hopes of obtaining a similar trace bound to Corollary 3.3. We introduce dual variables and for . Taking the Lagrangian and swapping and as before, we obtain

The KKT conditions require the gradient of the Lagrangian with respect to to vanish at optimality. We do casework on and .

-

•

If , then we obtain .

-

•

If , then we obtain .

-

•

If , then we obtain .

Hence in the dual problem, and , from which it follows that . The KKT conditions also require that , , and . Considering the diagonal entries of the latter constraint as before (see Proposition 3.1) we obtain

| (27) |

We now bound the edge terms by way of the KKT conditions.

-

•

If , then . Hence .

-

•

If , then recalling that , we have .

Before combining these two bounds, we define and . We have

| (28) |

We now turn to bounding the nonedge terms.

-

•

If , then . Hence .

-

•

If , then . Hence .

-

•

If , then again recalling that , we have .

Hence

| (29) |

Having done all of the legwork, now we are ready to quickly prove Proposition 3.14.

Proof C.3 (Proof of Proposition 3.14).

Plug Eq. 28 and Eq. 29 into Eq. 27. Summing over and dividing by , we obtain Eq. 20. Equation 21 immediately follows since .

Proof C.4 (Proof of Theorem 3.15).

Much of the following proof takes inspiration from [17], although there are a few key modifications that must be made to adapt their technique. The first key observation is that and are -Lipschitz on the interval . In order to apply the contraction principle [24, Theorem 4.12], under typical hypotheses we need a Lipschitz function which vanishes at . However, upon closer examination of its proof, it suffices for our purposes to show that for some and all . It is not hard to see that the minimum such is . Applying symmetrization [39, Section 6.4] by introducing symmetric Bernoulli variables , followed by contraction [24], we arrive at

In the third line we have defined the random matrix by for and , and we have used the fact that . Now we have , since is PSD. By [34, Theorem 1.1] we have that there is some absolute constant so that . We thus have that

where we have used the definition of in the last line. Dividing through by , and applying Markov’s inequality with parameter we arrive at the desired inequality.

Acknowledgments

We would like to thank Justin Solomon and Chris Scarvelis for their thoughtful comments. We would also like to thank Nicolas Boumal and Aude Genevay for helpful discussions.

References

- [1] E. Abbe, Community detection and stochastic block models: recent developments, The Journal of Machine Learning Research, 18 (2017), pp. 6446–6531.

- [2] A. Agrawal, R. Verschueren, S. Diamond, and S. Boyd, A rewriting system for convex optimization problems, Journal of Control and Decision, 5 (2018), pp. 42–60.

- [3] J. Agterberg, Y. Park, J. Larson, C. White, C. E. Priebe, V. Lyzinski, et al., Vertex nomination, consistent estimation, and adversarial modification, Electronic Journal of Statistics, 14 (2020), pp. 3230–3267.

- [4] M. ApS, The MOSEK Modeling Cookbook. Version 3.2.2B, 2020, https://docs.mosek.com/modeling-cookbook/expo.html.

- [5] J. Arroyo, D. L. Sussman, C. E. Priebe, and V. Lyzinski, Maximum likelihood estimation and graph matching in errorfully observed networks, arXiv preprint arXiv:1812.10519, (2018).

- [6] A. Athreya, D. E. Fishkind, M. Tang, C. E. Priebe, Y. Park, J. T. Vogelstein, K. Levin, V. Lyzinski, and Y. Qin, Statistical inference on random dot product graphs: a survey, The Journal of Machine Learning Research, 18 (2017), pp. 8393–8484.

- [7] A. Athreya, C. E. Priebe, M. Tang, V. Lyzinski, D. J. Marchette, and D. L. Sussman, A limit theorem for scaled eigenvectors of random dot product graphs, Sankhya A, 78 (2016), pp. 1–18.

- [8] N. Boumal, V. Voroninski, and A. Bandeira, The non-convex burer-monteiro approach works on smooth semidefinite programs, in Advances in Neural Information Processing Systems, 2016, pp. 2757–2765.

- [9] S. Boyd and L. Vandenberghe, Convex Optimization, Cambridge University Press, 2004, https://doi.org/10.1017/CBO9780511804441.

- [10] S. Burer and R. D. Monteiro, A nonlinear programming algorithm for solving semidefinite programs via low-rank factorization, Mathematical Programming, 95 (2003), pp. 329–357.

- [11] T. Cai and W.-X. Zhou, A max-norm constrained minimization approach to 1-bit matrix completion, The Journal of Machine Learning Research, 14 (2013), pp. 3619–3647.

- [12] L. Chen, C. Shen, J. T. Vogelstein, and C. E. Priebe, Robust vertex classification, IEEE Transactions on Pattern Analysis and Machine Intelligence, 38 (2016), pp. 578–590.

- [13] D. S. Choi, P. J. Wolfe, and E. M. Airoldi, Stochastic blockmodels with a growing number of classes, Biometrika, 99 (2012), pp. 273–284.

- [14] D. Cifuentes, On the burer-monteiro method for general semidefinite programs, arXiv preprint arXiv:1904.07147, (2019).

- [15] M. Collins, S. Dasgupta, and R. E. Schapire, A generalization of principal components analysis to the exponential family, in Advances in neural information processing systems, 2002, pp. 617–624.

- [16] D. Cvetković, P. Rowlinson, and S. K. Simić, Signless laplacians of finite graphs, Linear Algebra and its applications, 423 (2007), pp. 155–171.

- [17] M. A. Davenport, Y. Plan, E. Van Den Berg, and M. Wootters, 1-bit matrix completion, Information and Inference: A Journal of the IMA, 3 (2014), pp. 189–223.

- [18] M. A. Davenport and J. Romberg, An overview of low-rank matrix recovery from incomplete observations, IEEE Journal of Selected Topics in Signal Processing, 10 (2016), pp. 608–622.

- [19] D. DeFord and D. Rockmore, A random dot product model for weighted networks, arXiv preprint arXiv:1611.02530, (2016).

- [20] S. Diamond and S. Boyd, CVXPY: A Python-embedded modeling language for convex optimization, Journal of Machine Learning Research, 17 (2016), pp. 1–5.

- [21] J. C. Dunn, A fuzzy relative of the isodata process and its use in detecting compact well-separated clusters, Journal of Cybernetics, (1973).

- [22] M. X. Goemans and D. P. Williamson, Improved approximation algorithms for maximum cut and satisfiability problems using semidefinite programming, Journal of the ACM (JACM), 42 (1995), pp. 1115–1145.

- [23] A. J. Landgraf and Y. Lee, Dimensionality reduction for binary data through the projection of natural parameters, arXiv preprint arXiv:1510.06112, (2015).

- [24] M. Ledoux and M. Talagrand, Probability in Banach Spaces: isoperimetry and processes, Springer Science & Business Media, 2013.

- [25] J. MOODY and P. J. MUCHA, Portrait of political party polarization, Network Science, 1 (2013), p. 119–121.

- [26] P. J. Mucha and M. A. Porter, Communities in multislice voting networks, Chaos: An Interdisciplinary Journal of Nonlinear Science, 20 (2010).

- [27] P. J. Mucha, T. Richardson, K. Macon, M. A. Porter, and J.-P. Onnela, Community structure in time-dependent, multiscale, and multiplex networks, Science, 328 (2010), pp. 876–878.

- [28] L. O’Connor, M. Médard, and S. Feizi, Maximum likelihood latent space embedding of logistic random dot product graphs, arXiv preprint arXiv:1510.00850, (2015).

- [29] B. O’Donoghue, E. Chu, N. Parikh, and S. Boyd, SCS: Splitting conic solver, version 2.1.2. https://github.com/cvxgrp/scs, Nov. 2019.

- [30] S. D. Pauls, G. Leibon, and D. Rockmore, The social identity voting model: Ideology and community structures, Research & Politics, (2015).

- [31] K. T. Poole and H. Rosenthal, A spatial model for legislative roll call analysis, American Journal of Political Science, 29 (1985), pp. 357–384, http://www.jstor.org/stable/2111172.

- [32] M. A. Porter, P. J. Mucha, M. Newman, and A. Friend, Community structure in the united states house of representatives, Physica A: Statistical Mechanics and its Applications, 386 (2007), pp. 414 – 438.

- [33] B. Recht, M. Fazel, and P. A. Parrilo, Guaranteed minimum-rank solutions of linear matrix equations via nuclear norm minimization, SIAM review, 52 (2010), pp. 471–501.

- [34] Y. Seginer, The expected norm of random matrices, Combinatorics, Probability and Computing, 9 (2000), pp. 149–166.

- [35] A. Singer, Angular synchronization by eigenvectors and semidefinite programming, Applied and computational harmonic analysis, 30 (2011), pp. 20–36.

- [36] D. L. Sussman, M. Tang, and C. E. Priebe, Consistent latent position estimation and vertex classification for random dot product graphs, IEEE Transactions on Pattern Analysis and Machine Intelligence, 36 (2014), pp. 48–57, https://doi.org/10.1109/TPAMI.2013.135.

- [37] M. Tang, C. E. Priebe, et al., Limit theorems for eigenvectors of the normalized laplacian for random graphs, The Annals of Statistics, 46 (2018), pp. 2360–2415.

- [38] M. Tang, D. L. Sussman, C. E. Priebe, et al., Universally consistent vertex classification for latent positions graphs, The Annals of Statistics, 41 (2013), pp. 1406–1430.

- [39] R. Vershynin, High-dimensional probability: An introduction with applications in data science, vol. 47, Cambridge university press, 2018.

- [40] S. Wang, J. Arroyo, J. T. Vogelstein, and C. E. Priebe, Joint embedding of graphs, IEEE Transactions on Pattern Analysis and Machine Intelligence, (2019).

- [41] A. S. Waugh, L. Pei, J. H. Fowler, P. J. Mucha, and M. A. Porter, Party polarization in congress: A network science approach, 2011, https://arxiv.org/abs/0907.3509.

- [42] C. Yang, C. E. Priebe, Y. Park, and D. J. Marchette, Simultaneous dimensionality and complexity model selection for spectral graph clustering, Journal of Computational and Graphical Statistics, (2020), pp. 1–20.

- [43] J. Yoder, L. Chen, H. Pao, E. Bridgeford, K. Levin, D. E. Fishkind, C. Priebe, and V. Lyzinski, Vertex nomination: The canonical sampling and the extended spectral nomination schemes, Computational Statistics & Data Analysis, 145 (2020), p. 106916.

- [44] S. J. Young and E. R. Scheinerman, Random dot product graph models for social networks, in International Workshop on Algorithms and Models for the Web-Graph, Springer, 2007, pp. 138–149.

- [45] Z. Zhang, T. Li, C. Ding, and X. Zhang, Binary matrix factorization with applications, in Seventh IEEE international conference on data mining (ICDM 2007), IEEE, 2007, pp. 391–400.

- [46] Y. Zhao, A note on new bernstein-type inequalities for the log-likelihood function of bernoulli variables, Statistics & Probability Letters, (2020), p. 108779.