Convergence of the Deep BSDE method for FBSDEs with non-Lipschitz coefficients

Abstract

This paper is dedicated to solving high-dimensional coupled FBSDEs with non-Lipschitz diffusion coefficients numerically. Under mild conditions, we provided a posterior estimate of the numerical solution that holds for any time duration. This posterior estimate validates the convergence of the recently proposed Deep BSDE method. In addition, we developed a numerical scheme based on the Deep BSDE method and presented numerical examples in financial markets to demonstrate the high performance.

Keywords Forward-backward SDEs, deep neural networks, stochastic control.

1 Introduction

Let be a complete probability space, a standard -dimensional Brownian motion, a fixed terminal time, the natural filtration generated by and augmented by the -null sets. By we denote the space of -adpated -valued stochastic process satisfying . The following coupled forward-backward stochastic differential equation (FBSDE) is considered in this paper:

| (1.1) |

where , , are in , , respectively.

The coefficients , , , are all deterministic. The existence and uniqueness of the solution to the fully-coupled FBSDEs has been widely explored and we refer to [12, 10, 13, 11, 9] for details. Recently, the Deep BSDE method [6] was proposed for numerically solving high-dimensional BSDEs and parabolic PDEs. This method has high efficiency in approximating the accurate solution due to neural networks’ universal approximation capability. The convergence of the Deep BSDE method for FBSDEs has been extensively studied when the coefficients are sufficiently regular, see [7, 8]. A posterior estimate was used to bound the estimated error of the numerical solution. Hence, the original numerical solution problem can be reformulated as a stochastic optimization problem. A neural network is then used to optimize the posterior estimate and obtain the numerical solution.

In this paper, we apply the Deep BSDE method to FBSDEs with non-Lipschitz diffusion coefficients which have important applications, e.g., Cox-Ingersoll-Ross (CIR) model [2]. The forward stochastic differential equation admits a unique solution when the diffusion coefficient is uniformly Hölder continuous with order . The detailed proof can be found in [14, 15]. The CIR process has received a lot of attention in computational finance. The strong convergence of various discretization schemes has been demonstrated in [4, 5, 1]. Our main contribution is to provide a posterior estimate for non-Lipschitz FBSDEs that is valid for any time duration. To the best of our knowledge, this is the first theoretical result that supports the convergence of the Deep BSDE method for non-Lipschitz FBSDEs. Due to the non-Lipschitz diffusion coefficient, it is difficult to balance the order of the estimate between the forward and backward equations. We apply a series of Yamada-Watanabe functions [14, 15] to solve this imbalance and bound the error of the time discretization. In the previous studies [7, 8], the diffusion coefficient of the forward equation is assumed to be Lipschitz continuous and the time duration is required to be sufficiently small. We extend the posterior estimate to arbitrary time duration only under mild assumptions on the decoupling field of FBSDE (1.1).

This paper will be organized as follows. In the following section, we first formulate our main results, including theorems and numerical algorithms. Sections 3–5 are devoted to proving the main theorems. Section 6 includes numerical examples to demonstrate the application in finance.

2 Main Results

2.1 Assumptions

The problem we mainly focus on is the numerical algorithm for FBSDEs with non-Lipschitz diffusion coefficient . We will make the following assumptions:

Assumption 1.

We assume the diffusion coefficient has the following form

where is the -th component of .

Assumption 2.

Coefficients are uniformly Lipschitz continuous and is uniformly Hölder continuous with order .

-

1.

-

2.

-

3.

-

4.

where , , , and are given positive constants.

Remark 2.1.

Assumption 3.

We assume the following PDE

| (2.1) |

has a unique classical solution . Here denotes the Hessian with respect to argument .

Assumption 4.

We assume is uniformly Lipschitz continuous,

where is a given positive constant.

2.2 Main Theorems

To solve FBSDEs (1.1) numerically, we introduce the following stochastic optimal control problem. Consider an -dimensional SDE system :

| (2.2) |

with the aim of minimizing the objective functional

| (2.3) |

We view as the control of the system and assume . Under the regularity assumption on the coefficients, we have the existence and uniqueness of system (2.2). This result can be found in [14, 15]. It is simple to verify that the solution of FBSDE (1.1) is the optimal control.

Our first result demonstrates that the difference between any control and the optimal control can be bounded by the objective functional. Thus, we can solve the original FBSDE (1.1) by finding the optimal control of system (2.2).

Theorem 2.1.

Then, we consider the Euler-Maruyama scheme of system (2.2) to obtain the numerical solution to equation (1.1). Let be the discrete-time step and . is the state of the following discrete system under the control :

| (2.4) |

with the aim of minimizing the objective functional

To characterize the error of time discretization, we define the modulus of continuity of the control as

Theorem 2.2.

It should be noted that the upper bound of the time discretization error is affected by the control used . In practice, however we can limit the admissible control in a space of processes with sufficient time regularity. To be more specific, for any constants , we define the admissible control set as

By Theorems 2.1 and 2.2, we have the following discrete-time version posterior estimate.

Theorem 2.3.

Remark 2.3.

We point out that includes most cases of interest. Recall the solution to FBSDE (1.1) satisfies . Then, we have for some if is -Hölder continuous. This condition does not exclude some important cases such as . Moreover, given , it is not hard to show

2.3 Deep BSDE Method

Based on the Deep BSDE Method [6], we present our numerical algorithm. For a given accuracy, Theorem 2.3 enables us to approximate the solution to FBSDE (1.1) by minimizing the objective functional . The Euler-Maruyama scheme of the forward SDE (2.2) can be written as

| (2.5) |

where denotes .

We represent the control as where is the parameter to be optimized. Here, the feedback control is a forward neural network with uniformly bounded derivatives with respect to . Therefore, the feedback control is contained in some throughout the training. Thanks to the universal approximation capability of neural networks, we may approximate the optimal feedback control by . Our Deep BSDE network’s forward propagation is written as

| (2.6) |

with initial value , , and .

We denote as the batch size, i.e., we generate paths of Brownian motion in one batch. For each path, we compute iteratively using (2.6). Then, we approximate the objective functional by Monte Carlo simulation. The complete algorithm is shown below.

3 Continuous-time Posterior Estimate

From now on, we mainly consider a one-dimensional case that can be easily generalized to the multi-dimensional case. For the simplicity of notations, we denote , , , , , by , , , , , respectively. The constant can be changed from one line to the next.

We present a series of Yamada-Watanabe type [14] functions to approximate the absolute value function. will be used repeatedly in our proof. Let satisfy the following conditions:

-

•

-

•

-

•

-

•

-

•

We can show that for any and

-

•

,

-

•

,

-

•

.

Applying Itô’s formula to , we obtain

| (3.1) |

where

and

Since satisfies equation (2.1), we have

Plugging the above estimate into (3.1), we obtain

Therefore, we have

From Gronwall inequality, we show

| (3.2) |

Similarly, applying Itô’s formula to , we have

Notice that

| (3.3) |

and

| (3.4) |

Then, combining the properties of we get

Here the constant does not depend on . Let , it follows from Gronwall inequality that

| (3.5) |

In view of estimate (3.2), we obtain

| (3.6) |

Again, by Assumptions 3, 4, and estimate (3.2), we have

Now, we begin to estimate the second moment of errors. Applying Itô’s formula to we obtain

Plugging estimates (3.2), (3), (3.4), and (3.6), we have

By Gronwall inequality, we show

| (3.7) |

Moreover, by Assumption 4 and estimate (3.2), we have

| (3.8) |

Applying Itô’s formula to we get

Combining with the fact that

we show

Together with estimates (3.7) and (3), we have

| (3.9) |

4 Time Discretization Error

This section proves Theorem 2.2.

Recall that satisfies the following forward SDE

| (4.1) |

and

We have

| (4.2) |

By , , and we denote , , and , respectively.

Lemma 4.1.

We assume Assumption 2 holds. Let be the state of system (4.1) under the control . We have for some constant

Here the constant does not depend on the choice of and .

Proof.

Lemma 4.2.

We assume Assumption 2 holds. Let be the state of system (4.1) under the control . We have for some constant

Here the constant does not depend on the choice of and .

Proof.

Without loss of generality, we assume . It follows from Lemma 4.1 and Assumption 2 that

Similarly,

Therefore, we obtain

∎

We denote , , , , by , , , , , respectively. From Itô’s formula, we have

For the second term, by Lemma 4.2, we have

| (4.5) |

For the third term, it also follows from Lemma 4.2 that

| (4.6) |

Applying Itô’s formula to , we get

For the second term, we have

| (4.7) |

For the third term,

| (4.8) |

Notice the fact that

Hence, by estimates (4), (4), (4), and (4.8), we have

We set . From Gronwall inequality, we have

Similarly, we apply Itô’s formula to and . Following standard arguments, we have

Hence, we prove Theorem 2.2.

5 Discrete-time Posterior Estimate

This section proves Theorem 2.3. Recall that we assume

Without loss of generality, we may assume is sufficiently large such that

for some and any . By Assumption 2, we have

By Theorem 2.2, we have

| (5.1) |

Similarly,

| (5.2) |

By Theorem 2.1, we obtain

| (5.3) |

Combining above estimates and Assumption 2, we have

This implies

| (5.4) |

Therefore, by Theorems 2.1 and 2.2, we have

| (5.5) |

Furthermore, we have

| (5.6) | ||||

| (5.7) |

6 Numerical Results

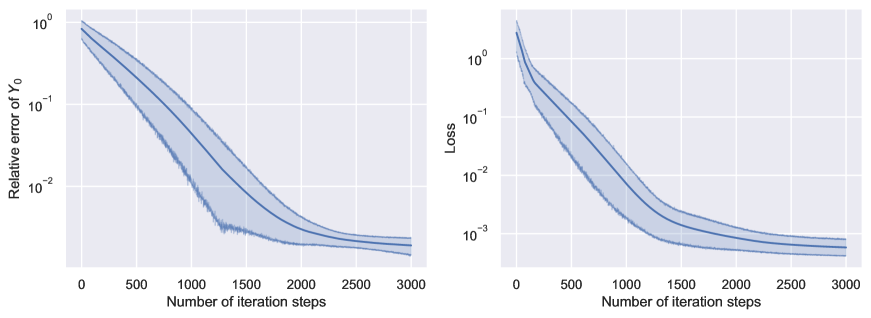

In this section, we present two numerical examples. The first is a one-dimensional model for which we can obtain an analytical solution; the second is a multi-dimensional case that can only be solved numerically. Recall that , where is constructed with two hidden layers of dimensions . We use rectifier function (ReLU) as the activation function and implement Adam optimizer. Both examples in this section are computed based on 1000 sample paths. The number of time partition is set to . We run each example independently 10 times to get the average result. All the parameters will be initialized using a uniform distribution. Related source codes can be referred to https://github.com/YifanJiang233/Deep_BSDE_solver.

Example 1.

The first example considers the bond price using the CIR model. Let be the short rate following a CIR process

Assume is the zero-coupon bond paying 1 at maturity . We have

Actually, satisfies the following BSDE

On the other hand, has an explicit solution

where . It is straightforward to check that Assumptions 1-4 are satisfied.

In this case, we have . We set , then from direct computation, the prescribed initial value is . Initial parameter is selected by a uniform distribution on .

| Step | Mean of | Standard deviation of | Mean of loss | Standard deviation of loss |

|---|---|---|---|---|

| 500 | 0.4643 | 9.58E-2 | 8.46E-2 | 1.27E-1 |

| 1000 | 0.4136 | 2.55E-2 | 7.13E-3 | 1.23E-2 |

| 2000 | 0.3972 | 1.21E-3 | 8.47E-4 | 6.23E-4 |

| 3000 | 0.3972 | 3.69E-4 | 5.80E-4 | 3.20E-4 |

We use algorithm 1 to obtain the numerical solution. By means of Theorems 2.1 and 2.2, converges to the analytical solution. In Figure 1, we illustrate the relative error of the bond price, and the loss is plotted against the number of iteration steps. The shaded area represents the confidence interval after 10 independent runs. Numerical simulations have well demonstrated the theoretical result.

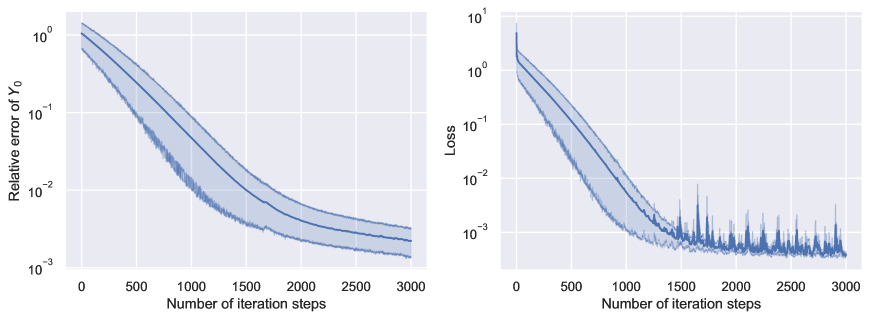

Example 2.

Our second example considers the bond price using the multi-dimensional CIR model. Let be the short rate following a multi-dimensional CIR process, i.e., each component of follows a CIR process,

Assume is the zero-coupon bond paying 1 at maturity . Under nonarbitrage condition, it is natural that

Hence, we have

Assume . Following standard arguments, we have

We set , , and . , , and are selected in . The initial value is selected by a uniform distribution on . Because solving the equation explicitly is difficult, we set the mean value of after 3000 iterations as the convergence limit and calculate the relative error of in 10 runs.

In Figure 2, we illustrate the relative error of the bond price under the multi-dimensional CIR model as well as a loss against the number of iteration steps. The shaded area represents the confidence interval based on 10 independent runs. Numerical simulations show that also converges well after around iteration steps.

| Step | Mean of | Standard deviation of | Mean of loss | Standard deviation of loss |

|---|---|---|---|---|

| 500 | 0.3773 | 8.77E-2 | 1.15E-1 | 1.66E-1 |

| 1000 | 0.3228 | 2.03E-2 | 5.51E-3 | 8.33E-3 |

| 2000 | 0.3100 | 1.63E-3 | 4.50E-4 | 1.12E-4 |

| 3000 | 0.3095 | 8.28E-4 | 3.89E-4 | 7.20E-5 |

7 Conclusions

In this paper, we presented a posterior estimate to bound the error of a given numerical scheme for non-Lipschitz FBSDEs. We demonstrated that the proposed posterior estimate holds for continuous-time FBSDEs and extended it to the estimate for the discrete Euler-Maruyama scheme. Some numerical examples in bond pricing are presented to demonstrate the Deep BSDE method’s dependability.

We extend the results in previous studies [7, 8] to a broader class of FBSDEs arising from the pricing problem in financial markets. It is also worth mentioning that the posterior estimates in [7, 8] require a sufficiently short time duration. By adaptation of the four-step method [10], we demonstrate the posterior estimate holds for arbitrary finite time duration if the decoupling field has bounded derivatives.

Our next step is to extend the current result to McKean-Vlasov type FBSDEs where a careful analysis of the derivative of the decoupling field concerning distribution is required. Another direction is to solve the Dirichlet problem of semilinear parabolic equations by the Deep BSDE method. In this case, the first hitting time of the boundary is critical to the posterior estimate.

Acknowledgments

This research has been supported by the EPSRC Centre for Doctoral Training in Mathematics of Random Systems: Analysis, Modelling, and Simulation (EP/S023925/1).

References

- [1] Aurelien Alfonsi, Affine diffusions and related processes: simulation, theory and applications, Bocconi & Springer Series 6, Bocconi University Press, 2015.

- [2] John C Cox, Jonathan E Ingersoll Jr, and Stephen A Ross, A theory of the term structure of interest rates, Theory of Valuation, World Scientific, 2005, pp. 129–164.

- [3] Jaksa Cvitanic and Jianfeng Zhang, The steepest descent method for forward-backward sdes, Electronic Journal of Probability 10 (2005), 1468–1495.

- [4] Griselda Deelstra and Freddy Delbaen, Convergence of discretized stochastic (interest rate) processes with stochastic drift term, Applied Stochastic Models and Data Analysis 14 (1998), no. 1, 77–84.

- [5] Steffen Dereich, Andreas Neuenkirch, and Lukasz Szpruch, An euler-type method for the strong approximation of the cox–ingersoll–ross process, Proceedings of the Royal Society A 468 (2012), 1105–1115.

- [6] Weinan E, Jiequn Han, and Arnulf Jentzen, Deep learning-based numerical methods for high-dimensional parabolic partial differential equations and backward stochastic differential equations, Communications in Mathematics and Statistics 5 (2017), no. 4, 349–380.

- [7] Jiequn Han and Jihao Long, Convergence of the deep bsde method for coupled fbsdes, Probability, Uncertainty and Quantitative Risk 5 (2020), no. 1, 1–33.

- [8] Shaolin Ji, Shige Peng, Ying Peng, and Xichuan Zhang, Three algorithms for solving high-dimensional fully coupled fbsdes through deep learning, IEEE Intelligent Systems 35 (2020), no. 3, 71–84.

- [9] Jin Ma, J-M Morel, and Jiongmin Yong, Forward-backward stochastic differential equations and their applications, no. 1702, Springer Science & Business Media, 1999.

- [10] Jin Ma, Philip Protter, and Jiongmin Yong, Solving forward-backward stochastic differential equations explicitly—a four step scheme, Probability Theory and Related Fields 98 (1994), no. 3, 339–359.

- [11] Etienne Pardoux and Shanjian Tang, Forward-backward stochastic differential equations and quasilinear parabolic pdes, Probability Theory and Related Fields 114 (1999), no. 2, 123–150.

- [12] Shige Peng, Probabilistic interpretation for systems of quasilinear parabolic partial differential equations, Stochastics and Stochastics Reports (Print) 37 (1991), no. 1-2, 61–74.

- [13] Shige Peng and Zhen Wu, Fully coupled forward-backward stochastic differential equations and applications to optimal control, SIAM Journal on Control and Optimization 37 (1999), no. 3, 825–843.

- [14] Toshio Yamada and Shinzo Watanabe, On the uniqueness of solutions of stochastic differential equations, Journal of Mathematics of Kyoto University 11 (1971), no. 1, 155–167.

- [15] , On the uniqueness of solutions of stochastic differential equations ii, Journal of Mathematics of Kyoto University 11 (1971), no. 3, 553–563.

- [16] Jianfeng Zhang, Backward stochastic differential equations, Backward Stochastic Differential Equations, Springer, 2017, pp. 79–99.