Coherence and Concentration in Tightly-Connected Networks

Abstract

The ability to achieve coordinated behavior—engineered or emergent—on networked systems has attracted widespread interest over several fields. This interest has led to remarkable advances in developing a theoretical understanding of the conditions under which agents within a network can reach an agreement (consensus) or develop coordinated behavior, such as synchronization. However, much less understood is the phenomenon of network coherence. Network coherence generally refers to nodes’ ability in a network to have a similar dynamic response despite heterogeneity in their individual behavior. In this paper, we develop a general framework to analyze and quantify the level of network coherence that a system exhibits by relating coherence with a low-rank property of the system. More precisely, for a networked system with linear dynamics and coupling, we show that, as the network connectivity grows, the system transfer matrix converges to a rank-one transfer matrix representing the coherent behavior. Interestingly, the non-zero eigenvalue of such a rank-one matrix is given by the harmonic mean of individual nodal dynamics, and we refer to it as the coherent dynamics. Our analysis unveils the frequency-dependent nature of coherence and a non-trivial interplay between dynamics and network topology. We further show that many networked systems can exhibit similar coherent behavior by establishing a concentration result in a setting with randomly chosen individual nodal dynamics.

I Introduction

Coordinated behavior in network systems has been a popular subject of research in many fields, including physics [2], chemistry [3], social sciences [4], and biology [5]. Within engineering, coordination is essential for the proper operation of many networked systems including power networks [6, 7], data and sensor networks [8, 9], and autonomous transportation [10, 11, 12, 13]. While there exist many expressions of this behavior, two forms of coordination have particularly received thorough attention by the control community: Consensus and synchronization.

Consensus [4, 11, 12, 13, 14, 15, 16], on one hand, refers to the ability of the network nodes to asymptotically reach a common value over some quantities of interest. Many extensions of this problem include the study of robustness and performance of consensus networks in the presence of noise [12, 13, 14], time-delay [15, 16], and switching graph topology [16]. Synchronization [5, 8, 9, 10, 17, 18, 19], on the other hand, refers to the ability of network nodes to follow a commonly defined trajectory. Although for nonlinear systems synchronization is a structurally stable phenomenon, in the linear case [17, 10, 18, 19], synchronization requires the existence of a common internal model that acts as a virtual leader [18, 19].

A closely related notion of coordination emerges when looking at how the network agents collectively respond to disturbances. In this setting, agents with noticeably different input-output responses, can present a similar, i.e., coherent, response when interconnected. A vast body of work, triggered by the seminal paper [13], has quantitatively studied the role of the network topology in the emergence of coherence. Examples include, directed [14] and undirected [20] consensus networks, transportation networks [13], and power networks [7, 21, 22, 23]. The key technical approach amounts to quantify the level of coherence by computing the -norm of the system for appropriately defined nodal disturbance and performance signals. Broadly speaking, the analysis shows a reciprocal dependence between the performance metrics and the non-zero eigenvalues of the network graph Laplacian, validating the fact that strong network coherence (low -norm) results from the high connectivity of the network (large Laplacian eigenvalues). Unfortunately, the analysis strongly relies on a homogeneity [13, 14, 20, 21, 22, 23] or proportionality [7] assumption of the nodal transfer functions, and thus fails to characterize how individual heterogeneous node dynamics affect the overall coherent network response.

In this paper, we seek to overcome these limitations by formalizing network coherence by the presence of a low-rank structure, of the system transfer matrix, that appears when the network feedback gain is high. More precisely, we show that for linear networks, as the network’s effective algebraic connectivity (a frequency-dependent notion to be later defined) grows, the system transfer matrix converges to a rank-one transfer matrix with identical element-wise transfer functions. Interestingly, this transfer function is given by the harmonic mean of individual nodal dynamics, which we refer to as coherent dynamics. Furthermore, we provide the concentration result of such coherent dynamics in large-scale stochastic networks where the node dynamics are given by random transfer functions.

This frequency domain analysis provides a deeper characterization of the role of both, network topology and node dynamics, on the coherent behavior of the network. In particular, our results make substantial contributions towards the understanding of coordinated and coherent behavior of network systems in many ways:

-

•

We present a general framework in frequency domain to analyze the coherence of heterogeneous networks. We show that network coherence emerges as a low rank structure of the system transfer matrix as we increase the effective algebraic connectivity–a frequency-varying quantity that depends on the network coupling strength and dynamics.

-

•

Unlike previous works, our analysis applies to networks with heterogeneous nodal dynamics, and further provides an explicit characterization in the frequency domain of the coherent response to disturbances. Thus, in this way, our results highlight the contribution of individual nodal dynamics to the network’s coherent behavior.

-

•

The analysis further suggests that network coherence is a frequency-dependent phenomenon. That is, the ability for nodes to respond coherently depends on the frequency composition of the input disturbance. We further explicitly connect our frequency domain analysis to time domain notions of coherence.

-

•

By providing an exact characterization of network’s coherent dynamics, our analysis can be further applied in settings where only distributional information of the netwok composition is known. More precisely, we show that the coherent dynamics of tightly-connected networks with possibly random nodal dynamics are well approximated by a deterministic transfer function that only depends on the statistical distribution of node dynamics.

Prior works on coherence primarily study homogeneous networks [13, 22, 23] and proportional networks [7], where the network can be diagonalized into individual dynamics, each corresponding to one eigenvalue of the network Laplacian. However, such techniques to study coherence cannot be generalized to non-proportional heterogeneous networks. In fact, in such setting, it is a priori unclear what a good representation of the coherent response is. Our new frequency domain framework allows one to analyze coherence in general heterogeneous networks.

Notably, the problem of characterizing coherent dynamics is unique to heterogeneous networks, since the coherent dynamics for homogeneous networks are exactly equal to the common nodal dynamics. In real applications, however, such as power networks, such characterization is relevant to model reduction [24, 25, 26] and control design [27]. Our analysis provides, in the asymptotic sense, the exact characterization of coherent dynamics that can be used in control design for heterogeneous networks.

The paper is organized as follows. In Section III and Section IV we present respectively the point-wise and uniform convergence results of network transfer matrix as the network connectivity increases. In Section V, the dynamics concentration in large-scale networks is discussed. In Section VI, we apply our analysis to consensus networks and synchronous generator networks. Conclusions are presented in Section VII.

Notation: For a vector , denotes the -norm of , and for a matrix , denotes the th smallest singular value of , denotes the spectral norm of . Particularly, if is real symmetric, we let denote the th smallest eigenvalue of . For two sets , we let denote the set difference.

We let denote the identity matrix of order , denote column vector , denote the set and denote the set of positive integers. Also, we write complex numbers as , where .

II Problem Setup

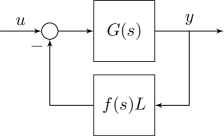

Consider a network consisting of nodes (), indexed by with the block diagram structure in Fig.1. is the Laplacian matrix of the weighted graph that describes the network interconnection. We further use to denote the transfer function representing the dynamics of network coupling, and to denote the nodal dynamics, with , being an SISO transfer function representing the dynamics of node .

Under this setting, we can compactly express the transfer matrix from the input signal vector to the output signal vector by

| (1) |

Many existing networks can be represented by this structure. For example, for the first-order consensus network [15, 11], , and the node dynamics are given by . For power networks [22, 7], , are the dynamics of the generators, and is the Laplacian matrix representing the sensitivity of power injection w.r.t. bus phase angles. Finally, in transportation networks [12, 11], represent the vehicle dynamics whereas describes local inter-vehicle information transfer.

Throughout this paper, we make the following assumptions, all of which are mild and commonly satisfied by several models that analyze the above-mentioned applications.

Assumption 1.

The closed-loop system (1) satisfies:

-

1.

All and are rational proper transfer functions;

-

2.

Laplacian matrix is real symmetric;

-

3.

Any pole of is not a zero of any of .

A straight forward application of the symmetry assumption in comes from its eigendecomposition

| (2) |

where , , and with .

Using now (2) we can rewrite as

| (3) |

As mentioned before, we are interested in characterizing the behavior of the closed-loop system of (1) as the connectivity of , i.e. , increases. To gain some insight we first consider the following simplified example.

II-A Motivating Example: Homogeneous Node Dynamics

Suppose are homogeneous, i.e., . Then using (3) one can decompose as follows

| (4) |

where the network dynamics decouple into two terms: 1) the dynamics that is independent of network topology and corresponds to the coherent behavior of the system; 2) the remaining dynamics that are dependent on the network structure via both, the eigenvalues and the eigenvectors . Notice that , then is dominant in as long as (later referred as effective algbraic connectivity), is large enough to make the norm of the second term in (4) sufficiently small. Following such observation, we can find two regimes where the coherent dynamics is dominant:

-

1.

(High network connectivity) for almost every , except for the poles of , the following holds:

Furthermore, one can verify that if a compact set contains neither zeros nor poles of , the following holds:

-

2.

(High gain in coupling dynamics) If is a pole of , and , then

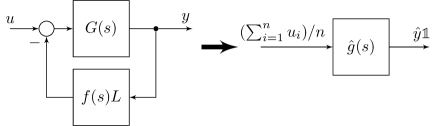

Such convergence results suggest that if 1) the network has high algebraic connectivity, or 2) our point of interest in frequency domain is close to pole of , the response of the entire system is close to one of . We refer as the coherent dynamics111We also refer as the coherent dynamics since transfer matrix of the form is uniquely determined by its non-zero eigenvalue . in the sense that in such system, the inputs are aggregated, and all nodes have exactly the same response to the aggregate input. Therefore, coherence of the network corresponds, in the frequency domain, to the property that the network’s transfer matrix approximately having a particular rank-one structure, and thus coherence increases as we increase the network connectivity, as depicted in Fig. 2.

The aforementioned analysis can be extended to the case with proportionality assumption, i.e., for some and , where one can still obtain decoupled dynamics through proper coordinate transformation [7]. However, it is challenging to characterize the coherent dynamics without the proportionality assumption. Our work precisely aims at understanding the coherent dynamics of non-proportional heterogeneous networks.

Remark 1.

In this paper, we write most of our convergence results in the high connectivity regime as the limit of differences in norm when for simplicity. However, one does not require infinitely high connectivity to achieve coherence. These limits suggests, under sufficiently high connectivity, the transfer matrix is, in some sense, close to coherent dynamics . The precise non-asymptotic result is presented in Lemma 4. Moreover, notice that in the other regime around pole of , we only requires the network to be connected.

II-B The Goal of This Work

In this paper, we would like to show that even when are heterogeneous, similar convergence result still holds. More precisely, we will, in the following sections, discuss the point-wise and uniform convergence of to a transfer matrix of the form , as the effective algebraic connectivity increases. However, unlike the homogeneous node dynamics case where the coherent behavior is driven by , we will show that the coherent dynamics are given by the harmonic mean of , i.e.,

| (5) |

Such asymptotic analyses under high connectivity serve two main purposes. Firstly, using the coherent dynamics , one can infer the point-wise convergence of as increases. In particular, we show that

-

1.

For a point that is neither a pole nor a zero of , converges to ;

-

2.

Poles of are asymptotically poles of ;

-

3.

Zeros of are asymptotically zeros of .

Secondly, uniform convergence of explains the coherent behavior/response of a tightly-connected network subject to disturbances. To see the connection, recall the Inverse Laplace Transform [28, Theorem 3.20] computes the system time-domain response by integration on the line in frequency domain with a suitable . Then uniform convergence of on this line would show that time-domain response of the network converges to one of the coherent dynamics as network connectivity increases. However, we will see that such convergence does not hold for most networks through our analysis and subsequent examples, which suggests that the coherence we analyze here is a frequency-dependent phenomenon. On that note, one generally resort to weaker convergence results on a line segment for some , which, once established, justifies the coherent behavior of tightly-connected networks subject to low-frequency disturbances (see Section IV-D). Since the set above is a compact subset of , we are mostly discussing the uniform convergence results over compact sets. Moreover, we also show the convergence in the other regime: is coherent around the pole of . This suggests that the network responses coherently, when subject to input signals that has its frequency component concentrate around pole of , and we show such an example in power networks in Section VI.

One additional feature of our analysis is that it can be further applied in settings where the composition of the network is unknown and only distributional information is present. More precisely, we will extend such convergence results by considering a tightly-connected network where node dynamics are given by random transfer functions. As the network size grows, the coherent dynamics converges in probability to a deterministic transfer function. We term such a phenomenon, where a family of uncertain large-scale tightly-connected systems concentrates to a common deterministic system, dynamics concentration.

Remark 2.

In order for the frequency domain analysis provided to be meaningful, it is necessary that both the transfer functions and are stable. Since our primary focus is on the interpretation of the frequency domain results, we are largely working under the tacit assumption that these transfer functions are stable whenever required. Some simple passivity motivated criteria that ensure stability even as becomes arbitrarily large are given in Theorem 2. It should also be noted that there exist a range of scalable stability criteria in the literature that can be used to guarantee internal stability of the feedback setup in Figure 2. Perhaps the most well known is that if each is strictly positive real, and is positive real, then the transfer functions and

are stable (see e.g. [29]). Alternative approaches that can be easily adapted to our framework that give criteria that allow for different classes of transfer functions include [30, 31, 32].

II-C Preliminaries

Before presenting our results, we first state a few facts and preliminary results that are used in later proofs.

II-C1 Basic Results on Vectors and Matrices

The following results can be found in [33].

-

•

Norm Inequalities: Let and , we have

2-Norm compatibility: (6) 2-Norm sub-multiplicativity: (7) Cauchy-Schwarz: (8) -

•

Inverse of Block Matrix: For block matrix with being square matrices, its inverse can be written as

(9) where , provided that all relevant inverses exist.

II-C2 Inequalities for singular values

We also provide several inequalities for matrix singular values from [33, 7.3.P16] which will be used in our proofs.

Lemma 1 (Weyl’s Inequality).

Let be square matrices of order , the following inequalities hold:

| (10a) | ||||

| (10b) | ||||

| (10c) | ||||

Lemma 1 allows us to obtain a useful bound on the spectral norm of . We state it as another Lemma as it will be repeatedly used in sections III and IV:

Lemma 2.

Let be square matrices of order . If , then the following inequality holds:

Proof.

II-C3 Grounded Laplacian Matrix

For a Laplacian matrix , we select an index set . Then the grounded Laplacian is the principal submatrix of obtained by removing the rows and columns corresponding to the index set . The following lemma relates the eigenvalues of and .

Lemma 3.

Given a symmetric Laplacian matrix , let be its grounded Laplacian corresponding to a index set with . Then for the least eigenvalue of , the following inequality holds:

The proof is shown in the Appendix.-A. This lower bound shows that for weighted graphs with fixed network size , as , we also have . This result is used in section III and IV when we present the convergence analysis regarding zeros of .

Now we are ready for the main results of this paper, and we start with the exact characterization of coherent dynamics of tightly-connected networks by proving the point-wise convergence of .

III Point-wise Coherence

In this section, we analyze the strength of network coherence at a single point in the frequency domain. We start with an important lemma revealing how such coherence is related to algebraic connectivity and feedback dynamics .

Lemma 4.

Proof.

Let , such that (3) becomes

Then it is easy to see that

| (12) |

where is the first column of identity matrix . The first equality holds by noticing that is the first column of , and the last equality comes from the fact that multiplying by a unitary matrix preserves the spectral norm.

We now write in block matrix form:

where , and we use the fact that .

Notice that and , we have

| (13) |

where (13) follows from the norm compatibility (6) and that matrix 2-norm is sub-multiplicative (7).

Also, by Lemma 2, when , the following holds:

| (14) |

Again (14) uses the fact that , the function is decreasing in and increasing in , and, by our assumption, .

Lemma 4 provides an upper bound for the incoherence measure we are interested in, namely how far apart the system transfer matrix is, at a particular point in the frequency domain, from being rank-one with coherent direction . Notice that this incoherence measure also provide upper bounds for

thus the transfer function from any input channel to any node output is approximately , if the incoherence measure is small.

We make following additional remarks:

Lemma 4 provides a non-asymptotic rate for our incoherence measure

| (18) |

A large value of is sufficient to have the incoherence measure small, and we term this quantity as effective algebraic connectivity. We see that there are two possible ways to achieve such point-wise coherence: Either we increase the network algebraic connectivity , by adding edges to the network and increasing edge weights, etc., or we move our point of interest to a pole of . This point-wise coherence via effective connectivity provides the basis of our subsequent analysis. Moreover, such coherence could be achieved by practical networks, and in Section VI, we apply our results to understand the coherent response of power generator networks.

Secondly, the upper bound is frequency-dependent since it is provided at a single point in the -domain. To see such dependence, notice that near a pole of has large effective algebraic connectivity, hence the system is more coherent around poles of ; On the contrary, near a pole of requires large for the condition of Lemma 4 to hold, and readers can check that near a zero of requires large , therefore for at these points, it is more difficult for us to upper bound the incoherence measure by Lemma 4. Such dependence makes it challenging to understand the network coherence uniformly in the entire frequency domain.

Last but not least, Although Lemma 4 provides a sufficient condition for the network coherence to emerge, i.e. the increasing effective algebraic connectivity, it is still unknown whether such a condition is necessary. In other words, we do not know whether low effective algebraic connectivity means some kind of incoherence. This problem seems trivial for the extreme case: if or , the feedback loop vanishes, and every node responses independently, but certainly not otherwise.

When the condition in Lemma 4 is satisfied, the system is asymptotically coherent, i.e. converges to as the effective algebraic connectivity increases. As we mentioned above, we can achieve this by increasing either or , provided that the other value is fixed and non-zero. Subsection III-A considers the former and Subsection III-B the latter.

Before presenting with the results, we define

Definition 1.

For transfer function and , is a generic point of if is neither a pole nor a zero of .

As we have seen through the discussions above, we always require some generic point assumptions for either , , or both. Those points are of the most interest in this paper but we will provide some results for the cases where the generic assumption fails.

III-A Convergence at Generic Points of

In this section we keep fixed and present the point-wise convergence result of as increases. This requires to be a generic point of .

Notice that for any that is also a generic point of , we can always find such and large enough for the upper bound in (11) to hold. Furthermore, given fixed and , one can let the upper bound be arbitrarily small by increasing , which leads to the point-wise convergence of , as stated in the following theorem.

Theorem 1.

Proof.

Theorem 1 establishes the emergence of coherence at generic points of . This forms the basis of our analysis, yet requires such satisfying generic conditions. A more careful analysis shows that, as , the pole of is asymptotically a pole of , and the zero of is asymptotically a zero of , as stated in the following two theorems.

Theorem 2.

Proof.

Similarly to the proof of Lemma 4, we define and now we need to show that grows unbounded as .

Write in block matrix form:

by noticing that because is a pole of .

Inverting in its block form gives

| (19) |

where now is given by .

Then from (19), when is large enough, we can lower bound by

| (20) |

where in the second inequality, we simply use the fact that the norm of a vector is lower bounded by its first entry.

Because is a pole of , it cannot be a zero of any ; otherwise this would lead to the contradiction . Therefore, is upper bounded by some . Similarly to (13) and (14), we have and . Then (20) can be lower bounded by

This lower bound holds when , and it grows unbounded as , which finishes the proof. ∎

Remark 3.

Theorem 2 does not suggest whether the network is asymptotically coherent at poles of . Our incoherence measure is undefined at such poles. Alternatively, for the pole of , one can prove that when as , we have the limit , for some determined by with . We leave the formal statement to Appendix.-B. This suggests that has the desired rank-one structure for coherence. While the normalized transfer matrix is not discussed in this paper due to the space constraints, such formulation is better for understanding the network coherence at the poles of .

Next, the convergence result regarding the zeros of is stated as

Theorem 3.

Proof.

Since is a zero of , it is the zero of at least one . Without loss of generality, suppose for and for .

If , then . We only consider the non-trivial case when . The transfer matrix is now given by

| (21) |

where and is the grounded Laplacian of by removing the first rows and columns.

Remark 4.

The limit in Theorem 3 can still be written as , because is a zero of . However, we here emphasize the fact that the system is not coherent at under normalization because does not converge to for any .

So far, we have shown point-wise convergence of towards the transfer function , from which we assess how network coherence emerges as connectivity increases. In Remark 3 and 4 we see that the incoherence measure is insufficient for understanding the asymptotic behavior at zeros or poles of , and that the alternative measure is a good complement for such purpose.222As increases, for pole of , the latter measure converges to given suitable conditions but not for the former; for zero of , the opposite result holds; for generic point of , both incoherence measures converge to . The latter measure, , focuses more on the relative scale of eigenvalues of . In this paper, we mostly use the former, , and particularly when presenting the uniform convergence results; because we are interested in connecting these results to the network time-domain response.

III-B Convergence Regarding Poles of

As mentioned before, when is a pole of , it is a singularity of . Under certain conditions, one can observe that high-gain in plays a role similar to . The result uses Lemma 4 and is stated as follows.

Theorem 4.

Proof.

Since is neither a zero nor a pole of , such that , we have and for some .

By Lemma 4, , the following holds

Taking on both side, notice that , the limit of right-hand side is 0. ∎

In other words, at pole of , the network effect is infinitely amplified. The effective algebraic connectivity grows unbounded as approaching the pole of . As a result, the frequency response of is exactly the one of . Hence network coherence naturally arises around poles of .

IV Uniform Coherence

We now leverage the point-wise convergence results of Section III to characterize conditions for uniform convergence. This will allow us to connect our analysis with time domain implications, as discussed in II-B.

We start by showing uniform convergence of over compact regions that do not contain any zero or pole of . While the uniform convergence does not hold over regions containing such zeros or poles in general, we prove that in some special cases, the uniform convergence around zeros of does hold. Finally, we provide a sufficient condition for uniform convergence of on the right-half plane, which implies the system converges in norm.

IV-A Uniform Convergence Around Generic Points of

Again, similarly to the point-wise convergence, we discuss uniform convergence of over set that satisfies the following assumption

Assumption 2.

satisfies and .

Such an assumption guarantees all points in the closure of are generic points of . This property prevents any sequence of points in that asymptotically eliminates or amplifies the network effect on the boundary of . In subsequent sections, we denote and .

Recall that in Section III, point-wise convergence is proved by choosing such that the conditions in Lemma 4 are satisfied at a particular point . Then, finding universal that work for every in a set suffices to show uniform convergence over . Such a process is straightforward if is compact:

Theorem 5.

Proof.

On the one hand, since does not contain any pole of , is continuous on the compact set , and hence bounded [35, Theorem 4.15]. On the other hand, because does not contain any zero of , every must be continuous on , and hence bounded as well. It follwos that is bounded on , and the conditions of Lemma 4 are satisfied for all with a uniform choice of and . By (11), we have

where . We finish the proof by taking on both sides. ∎

As we already discussed in Remark 3, if contains poles of , is not a good incoherence measure as it is undefined. The rest of the section mainly discusses the uniform convergence result around zeros of .

IV-B Uniform Convergence Around Zeros of

We first define the notion of Nodal Multiplicity of a point in complex plane w.r.t. a given network.

Definition 2.

Given , the Nodal Multiplicity of is defined as

where denotes the set cardinality.

By definition, any zero of must have positive nodal multiplicity. Our finding is that zeros with nodal multiplicity exactly have a special property, which is shown in the following Lemma.

Lemma 5.

The proof is shown in Appendix -D. Notice that for given , the bound is valid for any , therefore we can prove uniform convergence over compact regions that only contain zeros of with nodal multiplicity .

Theorem 6 (Uniform convergence around points with ).

Proof.

For zeros with nodal multiplicity strictly larger than , the analysis is rather complicated. We first look once again at the homogeneous node dynamics setting of Section II to provide some insight.

Example 1.

Consider again a homogeneous network with node dynamics and , where the transfer matrix is given by

The poles of include 1) the poles of , and 2) any point that satisfies for a particular . Notice that if is large, every solution to is close to one of the zeros of . As we increase , which effectively increases every , one can check that at most poles asymptotically approach each zero of , provided that are distinct. As a result, uniform convergence around any zero of cannot be obtained due to the presence of poles of close to them.

Such observation also seems to hold in general for networks with heterogeneous node dynamics . That is, if a zero of is a zero with nodal multiplicity strictly larger than , then we expect it to “attract” poles of . But it is difficult to formally prove it since we cannot exactly locate the poles of in the absence of homogeneity.333We can still exactly locate the poles of when proportionality is assumed, i.e. for some and rational transfer function . Such a case can be regarded as the homogeneous case by considering a scaled version of . Surprisingly, there are certain cases where we can still quantify the effect of those poles of approaching a zero of . This essentially disproves the uniform convergence for such cases.

Theorem 7 (Uniform Convergence Failure).

The proof is shown in Appendix -C. Although Theorem 7 only disproves the uniform convergence around one particular type of zero of , namely, such zero must have nodal multiplicity and it must be a real zero with multiplicity 1 for all , we believe a similar result holds for any zero that is “shared” by multiple . However, a complete proof is left for future research.

We now provide another point of view of this phenomenon. Suppose in a network of size 2, is exclusively zero of and exclusively zero of . If and are close enough, there must be a pole of in the small neighborhood of or . To be more clear, see the following example.

Example 2.

Let , then and are the zeros respectively. The coherent dynamics is given by

has a pole that is in both -neighborhoods of and .

By Theorem 2, we know that is asymptotically a pole of , in other words, there is a pole of approaching , as the network connectivity increases. Moreover, and being close enough suggests that is close to and , as we see in the example. Consequently, two zeros being close introduces a pole of asymptotically approaching a small neighborhood of . Consider the limit case where the two zeros collapse into a shared zero of , we should expect a pole of approaching this shared zero.

A similar argument can be made for zeros of different nodes being close to each other, introducing poles of in the small neighborhood that asymptotically attract poles of . This is by no means a rigorous proof of how uniform convergence fails around a zero “shared” by multiple , but rather a discussion providing intuition behind such behavior.

At this point, we have proved uniform convergence of on a compact set that does not include 1) zeros of with Nodal Multiplicity larger than , or 2) poles of .

In particular, we find that zero with Nodal Multiplicity larger than , i.e. it is ”shared” by multiple , attracts pole of as network connectivity increases, which suggests that uniform convergence of fails around such point. Although we only provide the proof for special cases as in Theorem 7, we conjecture such a statement is true in general and we left more careful analysis for future research.

IV-C Uniform Convergence on Right-Half Complex Plane

Aside from uniform convergence on compact sets, uniform convergence over the closed right-half plane is of great interest as well. If we were to establish uniform convergence over the right-half plane for a certain , then given to be stable, the convergence in -norm of towards could be guaranteed, i.e., converges to as a system. One trivial consequence is that we can infer the stability of with a large enough by the stability of . Furthermore, given any input signal, we can make the difference between output responses of and arbitrarily small by increasing the network connectivity.

Unfortunately, for most networks, we encounter with the same issue we have seen when dealing with zeros of : When is strictly proper, as , thus, can be viewed as a zero of by regarding as functions defined on extended complex plane . Then for networks that include more than one node whose transfer functions are strictly proper, there will be poles of approaching as increases. Notice that those poles could approach either from the left-half or right-half plane. Apparently, the uniform convergence on the right-half plane will not hold if the latter happens, but even when the former happens, we still need to quantify the effect of such poles because they are approaching the boundary of our set . A similar argument can be made for any set of the form , which we mentioned in II-B.

Although proving (or disproving) uniform convergence on the right-half plane for general networks is quite challenging, it is much more straightforward for networks consist of only non-strictly proper nodes, as shown in the following theorem:

Theorem 8 (Sufficient condition for uniform convergence on right-half plane).

Proof.

Given , we define the following sets:

Apparently, . Then we can show uniform convergence on right-half plane by proving uniform convergence on respectively:

Firstly, because all are not strictly proper, each converges to some non-zero value as . Then we can choose large enough so that for some . Moreover, for some because is stable. Then the conditions in Lemma 4 are satisfied, we have

| (23) |

where . Taking on both side of (23), we have the uniform convergence on .

Secondly, notice that is compact, contains no pole of and has , the uniform convergence is shown by Theorem 6. ∎

IV-D Connection to Time Domain Response

As discussed in Section II-B, we are interested in the uniform convergence of network transfer matrix because uniform convergence result on the line would allow us to show coherence in time-domain response through the inverse Laplace transform [28, Theorem 3.20]

However, we have seen in Section IV-C establishing such uniform convergence is challenging when are strictly proper. Nonetheless, if we assume the input signal decays sufficiently fast in high frequency range, we can prove the following:

Theorem 9.

Given and a real input signal vector with its Laplace transform . Suppose for some , , , we have

-

1.

is finite;

-

2.

-

3.

;

-

4.

, for any Laplacian matrix ;

Let be the response of -th node when the network input is , and let be the response of to . Then there exists , such that If , we have

The proof is shown in Appendix -F. The non-asymptotic rate has hidden constant that implicitly depends on ,, and the choice of . It is yet independent of .

Theorem 9 made several assumptions: The first one makes sure we can integrate on . The second condition requires the input signal decays sufficiently fast in high-frequency range. The third assumption relies on the stability of and can be verified easily. The last assumption is generally hard to verify, but it holds when the network satisfies additional properties. To present the result, we first define the following

Definition 3.

A rational transfer function is positive real (PR) if

A rational transfer function is output strictly passive (OSP) if

for some .

With these definition, we have

Theorem 10.

Suppose all are OSP, and is PR. There exists , such that given any positive semidefinite matrix , we have

V Coherence and Dynamics Concentration in Large-scale Networks

Until now we looked into convergence results of for networks with fixed size . However, one could easily see that such coherence does not depend on the network size . In particular, the right-hand side of (11) only depends on via as long as the bounds regarding , i.e. and do not scale with respect to . This implies that coherence can emerge as the network size increases. This is the topic of this section.

More interestingly, in a stochastic setting where all are unknown transfer functions independently drawn from some distribution, their harmonic mean eventually converges in probability to a deterministic transfer function as the network size increases. Consequently, a large-scale stochastic network concentrates to deterministic a system. We term this phenomenon dynamics concentration.

V-A Coherence in Large-scale Networks

To start with, we revise the problem settings to account for variable network size: Let be a sequence of transfer functions, and be a sequence of real symmetric Laplacian matrices such that has order , particularly, let . Then we define a sequence of transfer matrix as

| (24) |

where . This is exactly the same transfer matrix shown in Fig.1 for a network of size . We can then define the coherent dynamics for every as

| (25) |

For certain family of large-scale networks, the network algebraic connectivity increases as grows. For example, when is the Laplacian of a complete graph of size with all edge weights being , we have . As a result, network coherence naturally emerges as the network size grows. Recall that to prove the convergence of to for fixed , we essentially seek for , such that and for in a certain set. If it is possible to find a universal for all , then the convergence results should be extended to arbitrarily large networks, provided that network connectivity increases as grows. To state this condition formally, we need the notion of uniform boundedness for a family of functions.

Definition 4.

Let be a family of complex functions indexed by . Given , is uniformly bounded on if

Now we are ready to show uniform convergence of :

Theorem 11.

Proof.

Remark 5.

Similarly to Theorem 5, uniform convergence is achieved on a set away from zeros or poles of . The uniform boundedness condition is preventing any point in the closure of from asymptotically becoming a zero of any or a pole of as increases.

V-B Dynamics Concentration in Large-scale Networks

Now we consider the cases where the node dynamics are unknown (stochastic). For simplicity, we constraint our analysis to the setting where the node dynamics are independently sampled from the same random rational transfer function with all or part of the coefficients are random variables, i.e. the nodal transfer functions are of the form

| (27) |

for some , where , are random variables.

To formalize the setting, we firstly define the random transfer function to be sampled. Let be the sample space, the Borel -field of , and a probability measure on . A sample thus represents a -dimensional vector of coefficients. We then define a random rational transfer function on such that all or part of the coefficients of are random variables. Then for any , is a rational transfer function.

Now consider the probability space . Every give an instance of samples drawn from our random transfer function:

where is the -th element of . By construction, are i.i.d. random transfer functions. Moreover, for every , are i.i.d. random complex variables taking values in the extended complex plane (presumably taking value ).

Now given a sequence of real symmetric Laplacian matrices, consider the random network of size whose nodes are associated with the dynamics and coupled through . The transfer matrix of such a network is given by

| (28) |

where .

Then under this setting, the coherent dynamics of the network is given by

| (29) |

Now given a compact set of interest, and assuming suitable conditions on the distribution of , we expect that the random coherent dynamics would converge uniformly in probability to its expectation

| (30) |

for all , as . The following Lemma provides a sufficient condition for this to hold.

Lemma 6.

The proof is shown in Appendix -E. This lemma suggests that our coherent dynamics , as increases, converges uniformly on to its expected version . Then provided that the coherence is obtained as the network size grows, we would expect that the random transfer matrix to concentrate to a deterministic one , as the following theorem shows.

Theorem 12.

Proof.

Firstly, notice that

The second term converges to as by Lemma 6. For the first term, we show below that it becomes exactly for large enough . Still, we assume and are uniformly bounded on by respectively. By Lemma 4, choosing large enough s.t.

then we can choose even larger such that the probability on the right-hand side is because as . ∎

Remark 6.

Lemma 6 requires to be uniformly bounded on . That is, for , is a bounded complex random variable. In [1], a weaker condition, that is a sub-Gaussian complex random variable, is considered. This allows to show that point-wise convergence in probability can be achieved whenever grows polynomially in .

In summary, because the coherent dynamics of the tightly-connected network is given by the harmonic mean of all node dynamics , it concentrates to its harmonic expectation as the network size grows. As a result, in practice, the coherent behavior of large-scale tightly-connected networks depends on the empirical distribution of , i.e. a collective effect of all node dynamics rather than every individual node dynamics. For example, two different realizations of large-scale network with dynamics exhibit similar coherent behavior with high probability, in spite of the possible substantial differences in individual node dynamics.

VI Application: Aggregate Dynamics of Synchronous Generator Networks

In this section, we apply our analysis to investigate coherence in power networks. For coherent generator groups, we find that generalized typical aggregate generator models which are often used for model reduction in power networks [37]. Moreover, we show that heterogeneity in generator dynamics usually leads to high-order aggregate dynamics, making it challenging to find a reasonably low-order approximation.

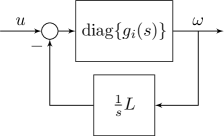

Consider the transfer matrix of power generator networks [7] linearized around its steady-state point, given by the following block diagram:

This is exactly the block structure shown in Fig. 1 with . Here, the network output, i.e., the frequency deviation of each generator, is denoted by . Generally, the are modeled as strictly positive real transfer functions and we assume is connected.

VI-A Coherence Analysis

We utilize the convergence results from previous sections to characterize the coherent behavior of such networks. We still denote the coherent dynamics as defined in (5).

Firstly, Notice that is a pole of , then by Theorem 4, is exactly , which suggests that in steady state, frequency outputs are the same for all generators. Moreover, another consequence of Theorem 4 is as follows.

Claim 1.

Given fixed , , such that

Proof.

This is the direct application of Theorem 4 according to the definition of the limit. ∎

The claim suggests that the network is naturally coherent in the low-frequency range. In other words, for any fixed network , there is a low-frequency range such that the network responds coherently to disturbances in that frequency range. Additionally, we know that such frequency range can be arbitrarily wide, given sufficiently large network connectivity, suggested by the following claim.

Claim 2.

, we have

Loosely speaking, the generator network is coherent for certain low-frequency range and the width of such frequency range increases when the network is more connected ( increases).

Furthermore, notice that can be regarded as a zero of , around which the network effect diminishes, i.e. for sufficiently large , the effective algebraic connectivity can be arbitrarily small. Hence given any fixed , there is a high-frequency range such that the network does not exhibit coherence under disturbances within such range.

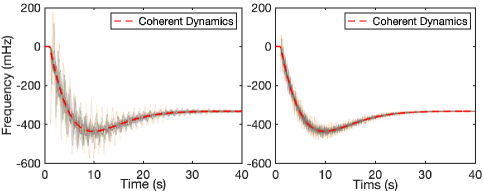

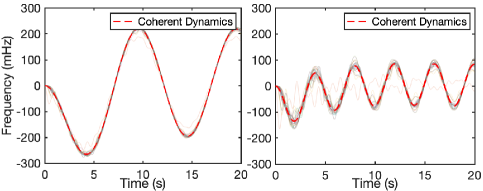

We verify our analysis with simulations on the Icelandic power grid [39]. As shown in Fig. 4, the network step response is more coherent, i.e. response of every single node (generator) is getting closer to the one of the coherent dynamics , when the network connectivity is scaled up. For the plot on the right, the connectivity is scaled up to 10 times the original. Then Fig. 5 shows such coherence is also frequency-dependent, where the generators respond less coherently under disturbances of higher frequency.

The discussions and simulations above suggest that the coherent dynamics characterize well the overall response/behavior of generators. This leads to a general methodology to analyze the aggregate dynamics of such networks, that we describe next.

VI-B Aggregate Dynamics of Generator Networks

Let

Our analysis suggests that the transfer function representing a network of generators is close within the low-frequency range, for sufficiently high network connectivity . We can also view as the aggregate generator dynamics, in the sense that it takes the sum of disturbances as its input, and its output represents the coherent response of all generators.

Such a notion of aggregate dynamics is important in modeling large-scale power networks[37]. Generally speaking, one seeks to find an aggregate dynamic model for a group of generators using the same structure (transfer function) as individual generator dynamics, i.e. when generator dynamics are modeled as , where is a vector of parameters representing physical properties of each generator, existing works [24, 26, 25] propose methods to find aggregate dynamics of the form for certain structures of . Our justifies their choices of , as shown in the following example.

Example 3.

For generators given by the swing model where are the inertia and damping of generator , respectively. The aggregate dynamics are

| (31) |

where and .

Here the parameters are . The aggregate model given by (31) is consistent with the existing approach of choosing inertia and damping as the respective sums over all the coherent generators.

However, as we show in the next example, when one considers more involved models, it is challenging to find parameters that accurately fit the aggregate dynamics.

Example 4.

For generators given by the swing model with turbine droop

| (32) |

where and are the droop coefficient and turbine time constant of generator , respectively. The aggregate dynamics are given by

| (33) |

Here the parameters are . This example illustrates, in particular, the difficulty in aggregating generators with heterogeneous turbine time constants. When all generators have the same turbine time constant , then in (33) reduces to the typical effective machine model

where , i.e. the aggregation model is still obtained by choosing parameters as the respective sums of their individual values.

If the are heterogeneous, then is a high-order transfer function and cannot be accurately represented by a single generator model. The aggregation of generators essentially asks for a low-order approximation of . Our analysis reveals the fundamental limitation of using conventional approaches seeking aggregate dynamics with the same structure of individual generators. Furthermore, by characterizing the aggregate dynamics in the explicit form , one can develop more accurate low-order approximation [40]. Lastly, we emphasize that our analysis does not depend on a specific model of generator dynamics , hence it provides a general methodology to aggregate coherent generator networks.

VII Conclusions

This paper provides various convergence results of the transfer matrix for a tightly-connected network. The analysis leads to useful characterizations of coordinated behavior and justifies the relation between network coherence and network effective algebraic connectivity. Our results suggest that network coherence is also a frequency-dependent phenomenon, which is numerically illustrated in generator networks. Lastly, concentration results for large-scale tightly-connected networks are presented, revealing the exclusive role of the statistical distribution of node dynamics in determining the coherent dynamics of such networks.

As we already see from the numerical example of synchronous generator networks, when the network is coherent, the entire network can be represented by its aggregate dynamics, because the network has all non-zero eigenvalue being sufficiently large to make the dynamics associated with these eigenvalues negligible. One could extend such observation to less coherent networks which has large eigenvalues except for a few small eigenvalues. We can utilize the same frequency domain analysis to these networks, but instead of only keeping the coherent dynamics, we retain the dynamic associated with all the small eigenvalues (These dynamics are generally coupled due to the heterogeneity in node dynamics). In this way, we can accurately capture the important modes in the network dynamics while significantly reduce the complexity of our model.

Furthermore, for large-scale networks with multiple coherent groups, or communities in a more general sense, one could model the inter-community interactions by replacing the dynamics of each community with its coherent one, or more generally, a reduced one. Although clustering, i.e. finding communities, for homogeneous networks can be efficiently done by various methods such as spectral clustering [41] [42], it is still open for research to find multiple coherent groups in heterogeneous dynamical networks.

-A Proof of Lemma 3

Proof.

To avoid confusion, here we let denote all one vector of length .

Without loss of generality, assume . Then is the principal submatrix of by removing first rows and columns.

By [fiedler73, 3.5], the matrix

is positive semi-definite. Now let where is the unit eigenvector correspoding to , we have

We also have , then the desired lower bound on is obtained:

∎

-B Convergence of Normalized Transfer Function at Poles of

We present here the formal statement regarding the Remark 3 on the convergence of normalized transfer function at poles of .

Proposition 13.

Here is well-defined since must be positive definite, otherwise it contradicts the fact that .

Proof.

Since

where is defined as in (19). The desired result follows once we show that , and . Recall that and

For the first limit, we have

The second limit comes from

and

along with the fact that both the upper and the lower bound converge to . To see the limit, notice that

and

The last limit is obtained from

and the fact that .

To show the limit of the ratio in the end, notice that

where

Here we use the fact that for some invertible square matrices , we have

provided that . To finish the proof, we see that

This shows that

which is the desired limit. ∎

-C Proof of Theorem 7

Proof.

Let be the open ball centered at with radius .

Notice that is a zero of and it is in the interior of , then given , , s.t. , and .

Suppose the above is true for some , then

Apparently we only need to find such and also show that

By the assumption, every , can be written as

Here, is rational and we denote

where and , . We let and .

Since for , is rational and is not a pole of , s.t. , are holomorphic on , i.e. every has expansion

where is the -th derivative of . For every , expand in Taylor series, then using Cauchy’s estimation formula [freitag1977complex], we have ,

where .

For , can be expanded as

where . And we also have

where .

Now for , we start from

| (-C.1) |

For , the numerator can be lower bounded by

| (-C.2) |

Then, let

which is semi-positive definite. the denominator can be upper bounded by

| (-C.3) |

Suppose , then for , we have

-

1.

is symmetric and has eigenvalue 0. Then ;

-

2.

.

From (-C.3) and (10c), we have

| (-C.4) |

Combing (-C.1)(-C.2)(-C.4), let large enough such that , we have

Since

by (10a), we can have arbitrarily large by increasing .

In summary, we can pick for the expansion of to exist, then pick , which also determines , and let

Then we conclude that s.t. ,

which implies

∎

-D Proof of Lemma 5

Proof.

We denote the open ball centered at with radius .

By assumptions, we have and . Without loss of generality, we assume . For , we have

| (-D.1) |

Consider any set , we have

For the second term, since is rational and is a zero of , by continuity of , such that

| (-D.2) |

Now we bound the first term. To start with, notice that . Without loss of generality, assume and . Then again by continuity of , such that

| (-D.3) |

On the other hand, since is a zero of , one can pick such that

| (-D.4) |

We let and we would like to bound by under sufficiently large . This would imply, together with (-D.2), that

The remaining of this proof is to bound by .

We write in block form as , by separating its first row and column from the rest. Here is a grounded Laplacian of , and is invertible as long as according to Lemma 3.

Since , we have , which gives

| (-D.5a) | |||

| (-D.5b) |

We use these equalities later.

We define and . Through some computation, we can write in the following block form

where

.

Then an upper bound of is given by

| (-D.6) |

Now we bound every term in (-D.6) for through following steps:

1) We firstly bound . By Woodbury matrix identity [33, 0.7.4], we have

| (-D.7) |

| (-D.8) |

When , the following holds:

| (-D.9) |

which when combined with (-D.4) gives the following bound on :

| (-D.10) |

2) For , when , we have:

| (Lemma 2) | ||||

| (-D.11) |

3) Lastly, for , when , we have

| (Lemma 2) | ||||

| (-D.12) |

-E Proof of Lemma 6

Proof.

It suffices to show that ,

| (-E.1) |

since .

By the assumptions, , and are uniformly bounded by and , respectively on . Then, at any , both and are random variables bounded within . We can simply bound their variances by

Then it follows that

| and | ||||

By definition of in (29), we have and , then by Chebyshev’s inequality, for , we have

| (-E.2) |

On the other hand, we have

| (-E.3) |

Then given , , the following holds:

By taking on both sides, we prove that converges point-wise to on .

We now show that is also stochastic equicontinuous on . For the definition of stochastic equicontinuity, please refer to [36]. We already assumed that , . Then , we have

where the last inequality is from our third assumption and also the fact that (identically distributed as random functions). By [36, Corollary 2.2], the inequality above is sufficient to establish stochatic equicontinuity of on , and combining point-wise convergence and the fourth assumption that is uniform continuous, we get the uniform convergence of to on , which gives (-E.1). ∎

-F Proofs of Theorem 9 and 10

Proof of Theorem 9.

When the input to the network is , the output response of the -th node is

where is the -th column of the identity matrix .

Using Mellin’s inverse formula [28, Theorem 3.20], we have

where

By our assumption,

Similarly, we have .

For the remaining term, we have

Since is a compact set that satisfies the assumption in Theorem 6, we have

Therefore, for sufficienly large , we have

.

Combining the upperbounds for , we have

Notice that the choice of does not depends on time , hence this inequality holds for all . ∎

Proof of Theorem 10.

For each , we have, by the OSP property,

Let , we have

or equivalently,

Since are all OSP, then is positive real [38]. A positive real function that is not zero function has no zero nor pole on the left half plane. Therefore are invertible for all , which ensures that is invertible for all . Then

which is

| (-F.4) |

Notice that

then from (-F.4) and the fact that is PR, we have

Now for sufficiently large , we have

since its Schur complement for large .

Therefore,

which is exactly,

This shows that

which is equivalent to

∎

References

- [1] H. Min and E. Mallada, “Dynamics concentration of large-scale tightly-connected networks,” in IEEE 58th Conf. on Decision and Control, 2019, pp. 758–763.

- [2] P. C. Bressloff and S. Coombes, “Travelling waves in chains of pulse-coupled integrate-and-fire oscillators with distributed delays,” Physica D: Nonlinear Phenomena, vol. 130, no. 3-4, pp. 232–254, 1999.

- [3] I. Z. Kiss, Y. Zhai, and J. L. Hudson, “Emerging coherence in a population of chemical oscillators,” Science, vol. 296, no. 5573, pp. 1676–1678, 2002.

- [4] M. H. DeGroot, “Reaching a consensus,” Journal of the American Statistical Association, vol. 69, no. 345, pp. 118–121, 1974.

- [5] R. E. Mirollo and S. H. Strogatz, “Synchronization of pulse-coupled biological oscillators,” SIAM Journal on Applied Mathematics, vol. 50, no. 6, pp. 1645–1662, 1990.

- [6] Y. Jiang, R. Pates, and E. Mallada, “Performance tradeoffs of dynamically controlled grid-connected inverters in low inertia power systems,” in 56th IEEE Conf. on Decision and Control, 12 2017, pp. 5098–5105.

- [7] F. Paganini and E. Mallada, “Global analysis of synchronization performance for power systems: Bridging the theory-practice gap,” IEEE Trans. Automat. Contr., vol. 65, no. 7, pp. 3007–3022, 2020.

- [8] E. Mallada, X. Meng, M. Hack, L. Zhang, and A. Tang, “Skewless network clock synchronization without discontinuity: Convergence and performance,” IEEE/ACM Transactions on Networking (TON), vol. 23, no. 5, pp. 1619–1633, 10 2015.

- [9] E. Mallada, “Distributed synchronization in engineering networks: The Internet and electric power girds,” Ph.D. dissertation, Electrical and Computer Engineering, Cornell University, 01 2014.

- [10] R. Sepulchre, D. Paley, and N. Leonard, “Stabilization of planar collective motion with limited communication,” IEEE Trans. Automat. Contr., vol. 53, no. 3, pp. 706–719, 2008.

- [11] R. Olfati-Saber, J. A. Fax, and R. M. Murray, “Consensus and cooperation in networked multi-agent systems,” Proceedings of the IEEE, vol. 95, no. 1, pp. 215–233, 2007.

- [12] A. Jadbabaie, J. Lin, and A. Morse, “Coordination of groups of mobile autonomous agents using nearest neighbor rules,” IEEE Trans. Automat. Contr., vol. 48, no. 6, pp. 988–1001, 2003.

- [13] B. Bamieh, M. R. Jovanovic, P. Mitra, and S. Patterson, “Coherence in large-scale networks: Dimension-dependent limitations of local feedback,” IEEE Trans. Automat. Contr., vol. 57, no. 9, pp. 2235–2249, 2012.

- [14] E. Tegling, B. Bamieh, and H. Sandberg, “Localized high-order consensus destabilizes large-scale networks,” in 2019 American Control Conference (ACC), July 2019, pp. 760–765.

- [15] R. Olfati-Saber and R. Murray, “Consensus problems in networks of agents with switching topology and time-delays,” IEEE Trans. Automat. Contr., vol. 49, no. 9, pp. 1520–1533, 2004.

- [16] Y. Ghaedsharaf, M. Siami, C. Somarakis, and N. Motee, “Centrality in time-delay consensus networks with structured uncertainties,” arXiv preprint arXiv:1902.08514, 2019.

- [17] S. Nair and N. Leonard, “Stable synchronization of mechanical system networks,” SIAM Journal on Control and Optimization, vol. 47, no. 2, pp. 661–683, 2008.

- [18] H. Kim, H. Shim, and J. Seo, “Output consensus of heterogeneous uncertain linear multi-agent systems,” IEEE Trans. Automat. Contr., vol. 56, no. 1, pp. 200–206, 2011.

- [19] P. Wieland, R. Sepulchre, and F. Allgöwer, “An internal model principle is necessary and sufficient for linear output synchronization,” Automatica, vol. 47, no. 5, pp. 1068–1074, 2011.

- [20] H. G. Oral, E. Mallada, and D. F. Gayme, “Performance of first and second order linear networked systems over digraphs,” in IEEE 56th Annu. Conf. on Decision and Control, Dec 2017, pp. 1688–1694.

- [21] B. Bamieh and D. F. Gayme, “The price of synchrony: Resistive losses due to phase synchronization in power networks,” in 2013 American Control Conference, 2013, pp. 5815–5820.

- [22] M. Andreasson, E. Tegling, H. Sandberg, and K. H. Johansson, “Coherence in synchronizing power networks with distributed integral control,” in IEEE 56th Annu. Conf. on Decision and Control, Dec 2017, pp. 6327–6333.

- [23] M. Pirani, J. W. Simpson-Porco, and B. Fidan, “System-theoretic performance metrics for low-inertia stability of power networks,” in 2017 IEEE 56th Annual Conference on Decision and Control (CDC), 2017, pp. 5106–5111.

- [24] A. J. Germond and R. Podmore, “Dynamic aggregation of generating unit models,” IEEE Trans. Power App. Syst., vol. PAS-97, no. 4, pp. 1060–1069, July 1978.

- [25] D. Apostolopoulou, P. W. Sauer, and A. D. Domínguez-García, “Balancing authority area model and its application to the design of adaptive AGC systems,” IEEE Trans. Power Syst., vol. 31, no. 5, pp. 3756–3764, Sep. 2016.

- [26] S. S. Guggilam, C. Zhao, E. Dall’Anese, Y. C. Chen, and S. V. Dhople, “Optimizing DER participation in inertial and primary-frequency response,” IEEE Trans. Power Syst., vol. 33, no. 5, pp. 5194–5205, Sep. 2018.

- [27] Y. Jiang, A. Bernstein, P. Vorobev, and E. Mallada, “Grid-forming frequency shaping control in low inertia power systems,” IEEE Control Systems Letters (L-CSS), vol. 5, no. 6, pp. 1988–1993, 12 2021, also in ACC 2021. [Online]. Available: https://mallada.ece.jhu.edu/pubs/2021-LCSS-JBVM.pdf

- [28] G. E. Dullerud and F. Paganini, A course in robust control theory: a convex approach. Springer Science & Business Media, 2013, vol. 36.

- [29] H. Marquez and C. Damaren, “Comments on ”strictly positive real transfer functions revisited,” IEEE Transactions on Automatic Control, vol. 40, no. 3, pp. 478–479, 1995.

- [30] I. Lestas and G. Vinnicombe, “Scalable decentralized robust stability certificates for networks of interconnected heterogeneous dynamical systems,” IEEE Transactions on Automatic Control, vol. 51, no. 10, pp. 1613–1625, 2006.

- [31] U. T. Jönsson and C.-Y. Kao, “A scalable robust stability criterion for systems with heterogeneous lti components,” IEEE Transactions on Automatic Control, vol. 55, no. 10, pp. 2219–2234, 2010.

- [32] R. Pates and E. Mallada, “Robust scale-free synthesis for frequency control in power systems,” IEEE Transactions on Control of Network Systems, vol. 6, no. 3, pp. 1174–1184, 2019.

- [33] R. A. Horn and C. R. Johnson, Matrix Analysis, 2nd ed. New York, NY, USA: Cambridge University Press, 2012.

- [34] H. Min and E. Mallada, “Coherence and concentration in tightly-connected networks,” arXiv preprint arXiv:2101.00981, 2021.

- [35] W. Rudin et al., Principles of mathematical analysis. McGraw-hill New York, 1964, vol. 3.

- [36] W. K. Newey, “Uniform convergence in probability and stochastic equicontinuity,” Econometrica: Journal of the Econometric Society, pp. 1161–1167, 1991.

- [37] J. H. Chow, Power system coherency and model reduction. New York, NY, USA: Springer, 2013.

- [38] H. K. Khalil and J. W. Grizzle, Nonlinear systems. Prentice hall Upper Saddle River, NJ, 2002, vol. 3.

- [39] U. of Edinburgh. Power systems test case archive. Mar. 2003. [Online]. Available: https://www.maths.ed.ac.uk/optenergy/NetworkData/icelandDyn/

- [40] H. Min, F. Paganini, and E. Mallada, “Accurate reduced-order models for heterogeneous coherent generators,” IEEE Contr. Syst. Lett., vol. 5, no. 5, pp. 1741–1746, 2021.

- [41] F. R. Bach and M. I. Jordan, “Learning spectral clustering,” in Advances in Neural Information Processing Systems, 2004, pp. 305–312.

- [42] M. Belkin and P. Niyogi, “Laplacian eigenmaps and spectral techniques for embedding and clustering,” in Advances in Neural Information Processing Systems, 2001, p. 585–591.

![[Uncaptioned image]](/html/2101.00981/assets/graphs/bio_photos/HM.png) |

Hancheng Min is currently working toward the Ph.D. degree at the Department of Electrical and Computer Engineering, Johns Hopkins University. He received the B.Eng. degree in Electrical Engineering and Automation from Tongji University in 2016, and the M.S. degree in Systems Engineering from University of Pennsylvania in 2018. His research interests include analysis and control for large-scale networks, reinforcement learning and deep learning theory. |

![[Uncaptioned image]](/html/2101.00981/assets/graphs/bio_photos/RP.jpg) |

Richard Pates received the M.Eng degree in 2009, and the Ph.D. degree in 2014, both from the University of Cambridge. He is currently an Senior Lecturer at Lund University. His research interests include modular methods for control system design, stability and control of electrical power systems, and fundamental performance limitations in large-scale systems. |

![[Uncaptioned image]](/html/2101.00981/assets/graphs/bio_photos/mallada.jpg) |

Enrique Mallada (S’09-M’13-SM’) is an Assistant Professor of Electrical and Computer Engineering at Johns Hopkins University. Prior to joining Hopkins in 2016, he was a Post-Doctoral Fellow in the Center for the Mathematics of Information at Caltech from 2014 to 2016. He received his Ingeniero en Telecomunicaciones degree from Universidad ORT, Uruguay, in 2005 and his Ph.D. degree in Electrical and Computer Engineering with a minor in Applied Mathematics from Cornell University in 2014. Dr. Mallada was awarded the NSF CAREER award in 2018, the ECE Director’s PhD Thesis Research Award for his dissertation in 2014, the Center for the Mathematics of Information (CMI) Fellowship from Caltech in 2014, and the Cornell University Jacobs Fellowship in 2011. His research interests lie in the areas of control, dynamical systems and optimization, with applications to engineering networks such as power systems and the Internet. |