Market Design for Tradable Mobility Credits

Abstract

Tradable mobility credit (TMC) schemes are an approach to travel demand management that have received significant attention in recent years as a promising means to mitigate the adverse environmental, economic and social effects of urban traffic congestion. This paper proposes and analyzes alternative market models for a TMC system – focusing on market design aspects such as allocation/expiration of tokens, rules governing trading, transaction fees, and regulator intervention – and develops a methodology to explicitly model the dis-aggregate behavior of individuals within the market. Extensive simulation experiments are conducted within a combined mode and departure time context for the morning commute problem to compare the performance of the alternative designs relative to congestion pricing and a no-control scenario. The simulation experiments employ a day-to-day assignment framework wherein transportation demand is modeled using a logit-mixture model with income effects and supply is modeled using a standard bottleneck model.

The results indicate that small fixed transaction fees can effectively mitigate undesirable behavior in the market without a significant loss in efficiency (total welfare) whereas proportional transaction fees are less effective both in terms of efficiency and in avoiding undesirable market behavior. Further, an allocation of tokens in continuous time can be beneficial in dealing with non-recurrent events and avoiding concentrated trading activity. In the presence of income effects, despite small fixed transaction fees, the TMC system yields a marginally higher social welfare than congestion pricing while attaining revenue neutrality. Further, it is more robust in the presence of forecasting errors and non-recurrent events due to the adaptiveness of the market. Finally, as expected, the TMC scheme is more equitable (when revenues from congestion pricing are not redistributed) although it is not guaranteed to be Pareto-improving when tokens are distributed equally.

keywords:

Tradable Mobility Credits; Demand Management; Traffic Management; Simulation1 Introduction

Historically, transportation network inefficiencies and externalities such as congestion and vehicular emissions have been addressed through road pricing, which although used in several cities worldwide, is plagued by issues of inequity and public acceptability [Tsekeris and Voß, 2009, de Palma and Lindsey, 2011]. An alternative approach to travel demand management that has received increasing attention in the transportation domain in recent years is quantity control – in particular, tradable mobility credit (TMC) schemes [Fan and Jiang, 2013, Grant-Muller and Xu, 2014, Dogterom et al., 2017]. Within a TMC system, a regulator provides an initial endowment of mobility credits or tokens to potential travelers. In order to use the road network or transportation system, users need to spend a certain number of tokens (i.e., tariff) that could vary with the attributes or performance of the specific mobility alternative used. The tokens can be bought and sold in a market at a price determined by token demand and supply.

In principle, TMC schemes are appealing since they offer a means of directly controlling quantity, they are revenue neutral in that there is no transfer of money to the regulator, and they are viewed as being less vertically inequitable than congestion pricing [de Palma and Lindsey, 2020]. Despite these promises, several important questions remain with regard to the design and functioning of the market within TMC schemes, an aspect critical to the effective operationalization of these schemes. For instance, how should the allocation and expiration of tokens be designed? What rules should govern trading behavior in the market so as to avoid undesirable speculation and trading (see Brands et al. [2020] for more on this), and yet ensure efficiency and revenue neutrality? How should the regulator intervene in the market in the presence of special or non-recurrent events? What is the role and impact of transaction fees? Despite the large body of literature on TMCs, issues of market design, market dynamics and market behavior have received relatively little attention although being critical to the successful real-world deployment of a TMC scheme.

This paper aims to address these issues and contributes to the existing literature in several respects. First, we propose alternative market models (focusing on all aspects of market design including allocation/expiration of credits, rules governing trading, transaction fees, regulator intervention, and price dynamics) for a TMC system and develop a methodology that explicitly models the dis-aggregate behavior of individuals within the market. Second, we conduct extensive simulation experiments within a departure time and mode choice context for the morning commute problem to compare the performance of the alternative designs relative to congestion pricing and a no-control scenario. The simulation experiments employ a day-to-day assignment framework wherein transportation demand is modeled using a logit-mixture model (with income effects) and supply is modeled using a standard bottleneck model. The experiments yield insights into market design and the comparative performance of the TMC system relative to congestion pricing.

The results indicate that small fixed transaction fees can effectively mitigate undesirable behavior in the market without a significant loss in efficiency (total welfare) whereas proportional transaction fees are less effective both in terms of efficiency and in avoiding undesirable market behavior. Further, an allocation of tokens in continuous time provides the TMC system with additional flexibility (compared to a lump-sum allocation) and can be beneficial in dealing with non-recurrent events. With regard to the relative performance vis-a-vis congestion pricing, the results indicate that the TMC scheme attains a marginally higher social welfare (under income effects and a small fixed transaction fee). Further, the TMC scheme is more robust in the presence of forecasting errors (during the optimization of the toll profiles) and by adjusting token allocation, can achieve a higher welfare than congestion pricing when actual demand and supply differs from the anticipated demand and/or supply. Finally, as expected, the TMC scheme is more equitable (when revenues from congestion pricing are not redistributed) although it is not guaranteed to be Pareto-improving when tokens are distributed equally.

The paper addresses a growing and imminent need to develop methodologies to realistically model TMCs that are suited for real-world deployments and can help us better understand the performance of these systems – and the impact in particular, of market dynamics.

The rest of the paper is organized as follows. Section 2 presents a review of the literature and identifies contributions of our paper. Section 3 and 4 propose a market design for TMCs and a framework for modeling market behavior, respectively. Section 5 introduces the simulation model, including demand, supply and day-to-day learning. Section 6 describes findings from extensive simulation experiments and Section 7 provides concluding remarks and directions for further research.

2 Review of Literature

Although early work on the use of tradable mobility credits (TMCs; also termed TCS or Tradable Credit Schemes in the literature) in transportation date back several years [Verhoef et al., 1997, Raux, 2007, Goddard, 1997], formulations of the market and network equilibrium for TMCs is more recent, pioneered by the work of Yang and Wang [2011] who proposed a user equilibrium variant for a TMC. Their work, along with advancements in technology and the widely recognized limitations of congestion pricing, has spurred interest in TMCs for transportation network management. Extensive reviews may be found in Grant-Muller and Xu [2014], Fan and Jiang [2013], Dogterom et al. [2017]. We provide a brief summary of existing literature, limiting our attention to that of mobility management (in the context of both entire networks and single bottlenecks) although applications may also be found in parking.

In the model of Yang and Wang [2011], the regulator distributes a pre-specified number of credits to travelers, charges a link-specific credit tariff and allows trading of credits within a market. They identify conditions under which the network and market equilibrium are unique. Extensions to their model have been proposed to incorporate heterogeneity in the value of time [Wang et al., 2012] and multiple user classes [Zhu et al., 2015] using variational inequality formulations to establish existence and uniqueness of the equilibrium. He et al. [2013] employed a similar equilibrium approach considering allocations of credits to not just individual travelers, but to transportation firms such as logistics companies and transit agencies; the effect of transaction costs in a TMC scheme with two types of markets (auction-based and negotiated) is considered by Nie [2012]. In contrast with the aforementioned TMC schemes, Kockelman and Kalmanje [2005], Gulipalli and Kockelman [2008] proposed a system of credit-based congestion pricing (termed CBCP) where credits are allowances used to pay tolls.

TMC schemes have also been studied in the context of managing congestion at a single bottleneck (or simple two route networks) by achieving peak spreading. Nie and Yin [2013] modeled a tradable credit scheme that manages commuters’ travel choices and attempts to persuade commuters to spread their departure times evenly within the rush hour and between alternative routes (see also Nie [2015]) whereas Tian et al. [2013] investigated the efficiency of a tradable travel credit scheme for managing bottleneck congestion and modal split in a competitive highway/transit network with heterogeneity. Along related lines, Xiao et al. [2013] studied a tradable credit system (consisting of a time-varying credit charge at the bottleneck wherein the credits can be traded and the price is determined by a competitive market) to manage morning commute congestion with both homogeneous and heterogeneous users. More recently, Bao et al. [2019] examined the existence of equilibria under tradable credit schemes using different models of dynamic congestion and Akamatsu and Wada [2017] proposed a tradable bottleneck credit scheme where the regulator issues link- and time-specific credits required for passing through a certain link or bottleneck in a pre-specified time period. Liu et al. [2022] considered distance-based token tariffs in a TMC scheme within a departure-time setting and examined its performance using a trip-based MFD supply model.

In contrast with the previously described literature that largely focus on variants of the standard user equilibrium under TMC schemes, a related stream of research examines the design of the TMC schemes using bi-level optimization formulations in different contexts [Wu et al., 2012, Bao et al., 2017, Wang et al., 2014]. On the other hand, the comparison of efficiency properties of tradable credits and congestion pricing has received relatively lesser attention. de Palma et al. [2018] performed a comparative analysis of the two instruments in a simple static transportation network (see also Seshadri et al. [2021] for a within-day dynamic setting) and showed that as long as there is no uncertainty, price and quantity regulation are equivalent as in the regular market case studied by Weitzman [1974]. In the presence of uncertainty and strongly convex congestion costs, the TMC instrument outperforms the pricing instrument in efficiency terms (see also de Palma and Lindsey [2020] for comparisons in the case with one route and time period under elastic demand). Akamatsu and Wada [2017] reached similar conclusions (see also Shirmohammadi et al. [2013]), demonstrating the equivalence of the tradable permit system and a congestion pricing system when the road manager has perfect information of transportation demands. On the behavior side, several stated preference studies have highlighted the importance of key factors from the perspective of behavioral economics and cognitive psychology towards tradable credits [Dogterom et al., 2017].

To the best of our knowledge, Brands et al. [2020] is the only study thus far to examine issues of market design for tradable credits. They conducted a lab-in-the-field experiment in a parking context and examine performance of the credit system empirically in terms of several criteria including undesirable speculation, price stability and transaction costs.

In summary, despite the large body of research on TMCs, several gaps remain. First, the modeling of the market has received little attention and almost all the studies employ an equilibrium approach to model the credit market (with the notable exception of Ye and Yang [2013] who model the price and flow dynamics of a tradable credit scheme). The literature has – to the best of our knowledge – thus far not attempted to realistically model the disaggregate behavior of individuals within the market. This would enable the consideration of empirically observed phenomena such as loss aversion, endowment effects, mental accounting, day-to-day learning [Dogterom et al., 2017]. Second, despite being a critical step towards real-world deployment, design aspects of the credit market have received little attention. In particular, features such as token allocation/expiration, trading, intervention, and transaction fees, and their impact on efficiency and market behavior remain to be studied. Finally, income effects, which impact both efficiency and equity, have received relatively little attention (with the exception of Wu et al. [2012] who consider it in a route choice setting). This paper aims to address these gaps by proposing and analyzing alternative market designs of the TMC system and investigating their performance relative to congestion pricing using realistic models of traveler behavior (with heterogeneity and income effects) and congestion.

3 Market Design

In this section, we focus on market design for a tradable credit scheme. Within the TMC scheme, the regulator provides a token endowment to all potential travelers. Although our design is generic, the application we explore involves a daily commute context where in order to use the network at a particular time-of-day (e.g., for a given departure time interval), travelers have to pay a pre-specified toll in tokens that does not vary from day to day. In other words, the toll in tokens is dynamic and varies by time-of-day, but is fixed across days. The rationale for this assumption is that modifying the toll in tokens from day to day would involve communicating the tariff or toll structure on a daily basis, which is complicated, particularly in large general networks (for instance, the electronic road pricing or ERP scheme in Singapore includes dynamic tolls, which are revised only every three months or longer). The market design we propose can be used for other applications including parking management.

The regulator operates a market where tokens can be bought and sold at a prevailing market price and may also levy pre-specified transaction fees for buying and selling. The market price of the token varies across days and is adjusted by the regulator to achieve revenue neutrality, considering the demand and supply of tokens in the market. All transactions take place between an individual and the regulator directly, who guarantees all buying and selling requests. This central market with a regulator who acts as a price setting intermediary is similar to the virtual bank in Brands et al. [2020], who note that such a market can significantly reduce transaction costs (associated with information acquisition, negotiation, finding a potential buyer or seller etc.) compared to designs that involve consumer to consumer trading (and over existing designs such as Dutch and English auctions, sealed-bid auctions and Vickrey auction markets). The regulator may also intervene in the token market within the day by controlling token market price, token allocation, and transaction fees to manage non-recurrent events.

With regard to the token allocation or endowment, we adopt a ‘continuous time’ approach wherein tokens are acquired (provided by the regulator) at a certain rate over the entire day and each token has a lifetime (i.e., it expires after a certain period specified by the regulator). The expiration of tokens will avoid undesirable consequences of the TMC system that can compromise public acceptability such as speculative behavior and hedging in the market. The ‘continuous’ allocation avoids concentrated trading activities and excessive trading near a boundary (a time period when a large amount of tokens expire at the same time, such as for instance, in a lump-sum allocation). It also provides more degrees of freedom for the regulator to intervene than that of a ‘lump sum’ allocation which distributes tokens at the beginning of each day. A comparison between the two allocation approaches will be performed through numerical experiments presented in Section 6.6.

As a result, each individual acquires tokens at a constant rate over the entire day (credited into a wallet) and each token has a lifetime to avoid speculation and hoarding. Let denote traveler ’s token account (or wallet) balance at time on day . A full wallet state indicates that the number of tokens in the wallet has reached a maximum (), and in the absence of travelling or selling, does not change since the acquisition of new tokens is balanced by an expiry of old tokens. Thus, a full wallet implies that the oldest token in an individual’s account has an age of . In contrast, when the account is not in a full wallet state, it increases by an amount in a unit time interval .

Several additional assumptions regarding market design are noteworthy – these serve to avoid quantity buildup and market manipulation. First, travelers can only buy tokens from the regulator at the time of traveling for immediate use, i.e., only if they wish to travel and are short of tokens. Second, when they sell tokens to the regulator, they have to sell all tokens in their wallet. Third, buying and selling cannot happen at the same time, i.e. travelers can sell all tokens anytime except at the time of buying. Note that the second assumption differs from the design of Brands et al. [2020], who assume that tokens can be traded per piece, and implications of this assumption warrant more investigation, particularly when the market prices vary within-day. Since a large part of our experiments do not involve within-day dynamic prices and given that it considerably simplifies the modeling of selling behavior, we defer the relaxation of this assumption to future research.

3.1 Account Evolution

Let denote the toll in tokens to travel at time , represent the departure time of traveler on day and represent the duration of one day. Note that in the simulation framework (Section 5), time will be discretized into intervals of a specified size; for now, we treat it as continuous. Let denote the allocation rate, denote token lifetime, and denote traveler ’s token account balance at time on day . At time on day , traveler can perform one and only one of the following actions:

-

1.

Perform a trip if .

-

(a)

If , she consumes tokens. Her account balance at , , can be written as:

(1) where the cap ensures that tokens with life greater than expire.

-

(b)

If , she needs to buy tokens. Her account balance becomes:

(2) since all of and the newly bought tokens are used to travel.

-

(a)

-

2.

Does nothing. Her account balance becomes:

(3) -

3.

Sells all tokens . Her account balance becomes:

(4)

3.2 Buying and Selling

The token market price is fixed within day (in the absence of non-recurrent events) and is only adjusted day to day. Details of the price adjustment process are discussed in Section 3.3. We assume that the regulator levies a two-part (fixed and proportional) transaction fee for both buying and selling transactions. Let , () denote the proportional part of selling and buying transaction fees (this component of the transaction fee is proportional to the amount of the trade), and , () denote the fixed part of selling and buying transaction fees. The effect of transaction fees on market behavior and efficiency will be examined in Section 6.4.

The revenue obtained from selling tokens () with transaction fees on day at time can be written as,

| (5) |

where is the token market price adjusted for the proportional selling transaction fee. Transaction fees and price are not expressed in function inputs for conciseness.

The cost of buying tokens () with transaction fees at time on day can be written as,

| (6) |

where is the token market price adjusted for the proportional buying transaction fee.

3.3 Price Adjustment

The marketplace dictates the token price on day , which is adjusted according to an apriori rule established by the regulator to achieve revenue neutrality. The price is modified daily with a deterministic rule considering the regulator revenue (net revenue from all buying and selling transactions of users) from the previous day as follows

| (7) |

where currently is a constant parameter representing the price change. is a constant parameter representing a regulator revenue threshold to adjust the price and ensures that price will not fluctuate for small regulator revenues close to zero. Price is ensured to be positive and below a certain cap as follows:

| (8) |

Although token price is typically constant within a day, the regulator may intervene in the market to adjust the market price during a day in the presence of unusual events. For example, if road capacity drops because of an accident, or if demand increases due to a concert, the regulator can intervene, increasing token price in a certain period to discourage travel and reduce congestion. Numerical experiments are conducted to study this in Section 6.6.

Market elements discussed in this section are summarized in Table 1.

| Elements | Design | Motivation |

| Allocation | Lump-sum | Simple; automated trading |

| Continuous | Avoid concentrated trading; additional control | |

| Expiration | Lifetime | Avoid quantity buildup |

| Transaction fee | Proportional | Avoid undesirable market behavior (e.g. frequent selling) |

| Fixed | ||

| Price adjustment | Day to day constant adjustment | Balance demand and supply |

| Market rules governing trading | ||

4 Market Behavior

As buying behavior is governed by the previously specified buying rule, this section primarily discusses individual selling behavior. It is assumed that the individual selling decision and mobility decision (departure time and mode) are inter-dependent. In other words, selling decisions are made conditional on a departure time/mode chosen at the beginning of the day, which in turn is based on a forecast of the account balance over the entire day. This forecast is based on historical travel and selling decisions of the user and his/her past experience (described in more detail in Section 5.1.3). We note that one could think of this selling behavior as a strategy or an automated operation performed through (or programmed into) for example a smartphone application, since in practice, it may be onerous to expect users to constantly make these selling decisions ‘manually’. In this respect, one may also view it as an element in the overall design of the tradable credit scheme. However, note that our modeling framework does not preclude the use of an actual behavioral model of selling in the market (in place of the selling strategy we formulate next), which would require the collection of empirical data; we defer this to future research.

From the perspective of simply maximizing profit (which is a reasonable selling strategy), the decision to sell can be formulated as a dynamic programming or optimal control problem, where the optimal selling strategy is characterized by Bellman’s equation [Kirk, 2004]. However, this is complicated, both from the standpoint of computational complexity and system design, and instead, we derive a simpler heuristic approach to characterize an individual’s selling strategy.

At time on day , assume traveler has an upcoming planned trip at a time denoted by , where if , and , if . Given the next trip, a conditional profit function , which represents the profit obtained by selling all tokens at time (with no further selling until the next departure ) can be written as follows,

| (9) | ||||

where represents the expected account balance at the time of the next trip . Since it is assumed there will be no further selling until the next departure , it can be written as,

| (10) |

For other notation in the conditional profit function , represents the toll in tokens of traveling at departure time . A buying cost is incurred only if the toll at is greater than or equal to traveler ’s expected account balance (i.e. ), which is represented by the indicator function. Note that in defining the profit function above, we have made the critical assumption that if a decision to sell at the current time is made, no further selling will occur until the next trip. This simplification allows us to derive an optimal selling strategy analytically and is partly justifiable given that we also assume that during selling, an individual needs to sell all tokens in her wallet, and that prices do not vary within-day. However, observe that the selling strategy we derive, when applied, involves a decision made at every time point , implying that it does not preclude the possibility of an individual making multiple selling decisions in the time period until the next trip if this is beneficial.

Under our assumptions, at time on day , traveler will consider selling tokens only if the profit value is positive, i.e., . If the profit value is positive, she may still decide to wait if the derivative of the profit function is positive (meaning that the profit is expected to increase if she defers the decision to sell). Therefore, the selling strategy depends on both the profit function and its derivative, which can be analyzed from the following three cases:

-

1.

(no tokens need to be bought for the next trip)

The profit function can be written as

(11) and the derivative can be written as

(12) which implies that profit will continue to increase until a full wallet is reached. It does not make sense to wait longer at a full wallet because newly acquired tokens simply replace expired tokens. Hence, selling should be at a full wallet.

However, it is worth noting that, without fixed transaction fees, the selling revenue at full wallet is the same as that obtained from selling every time when one receives new tokens. In fact, as long as one avoids token expiration, any selling strategy is equivalent in the absence of fixed transaction fees. It is fixed transaction fees that prevent frequent selling.

-

2.

(tokens need to be bought for the next trip)

The profit function can be written as

(13) and its derivative can be written as

(14) which is always negative since given or is greater than 0. This implies that profit obtained from waiting and selling at any time in the future (until the next trip) is guaranteed to be less than the profit from selling now. Hence, she should sell now if the profit is positive.

Without transaction fees, the profit function can be written as

(15) and its derivative can be written as

(16) which means that as long as account balance is not full, it does not matter whether one sells now or later. However, once we introduce fixed transaction fees, it is better to sell at a full wallet to minimize the number of transactions. With additional proportional transaction fees, it is better to sell immediately and not worth waiting anymore as the derivative is always negative.

-

3.

(the expected account balance is just enough to cover the toll of the next trip)

The profit function can be written as

(17) but its derivative does not exist because the conditional profit function is discontinuous at due to the transaction fees of buying. To avoid any buying transaction fees (either fixed or proportional), it is optimal to sell immediately if profit is positive. Without transaction fees, similarly, it does not matter whether one sells now or later as long as token expiration is avoided.

Based on the analysis in this section, the effect of fixed transaction fees is to prevent multiple transactions while the effect of proportional transaction fees is to make one sell as soon as possible when the conditional profit is positive (if tokens need to be bought for the next trip). The proportional transaction fee is not preferable because it does not prevent frequent selling but instead prevents selling at a full wallet. Numerical experiments in Section 6 will provide further justification for the use of only a fixed transaction fee from an efficiency perspective.

The selling strategy for an individual at any time on day considering positive transaction fees is summarized in Algorithm 1.

5 Simulation Framework

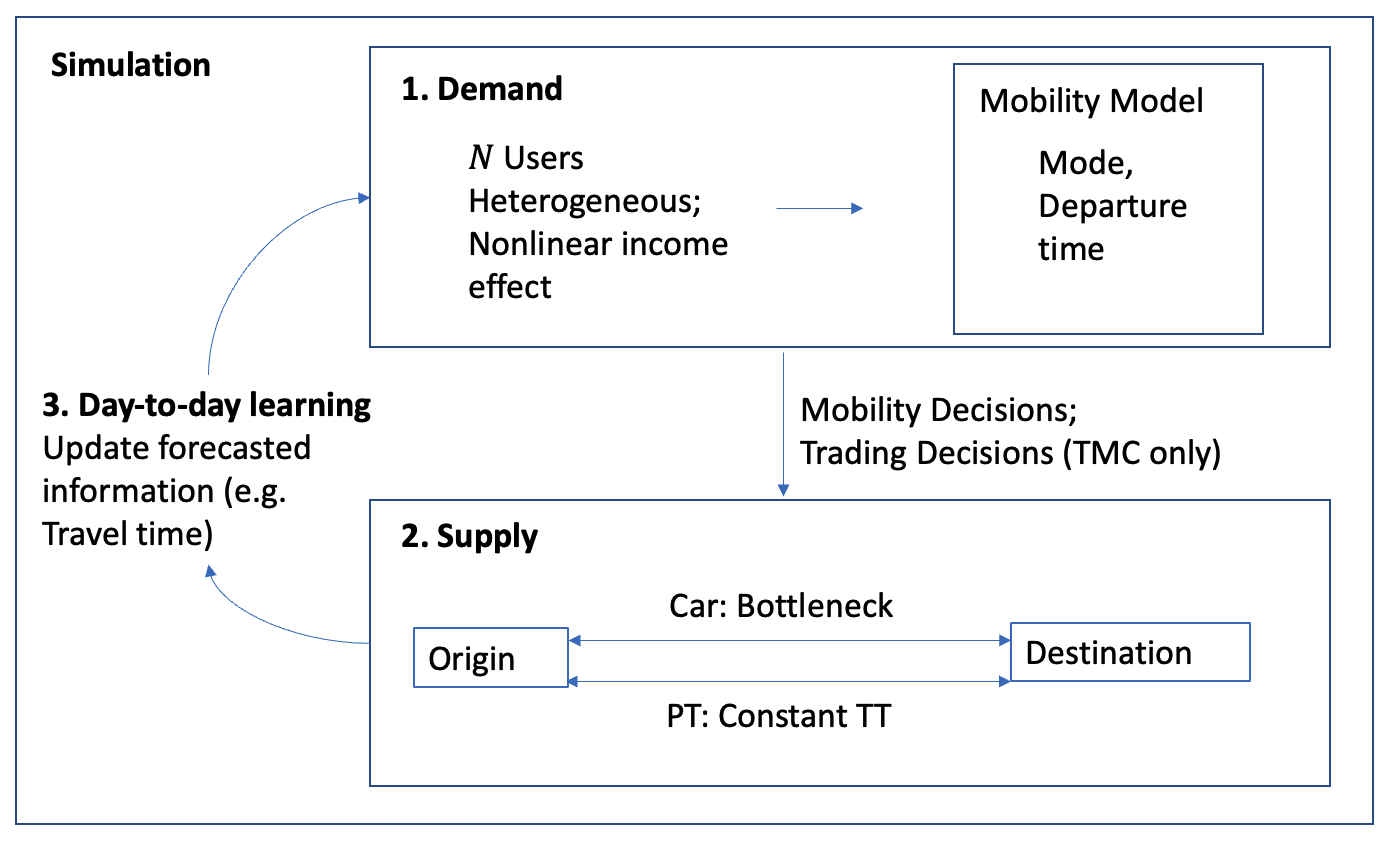

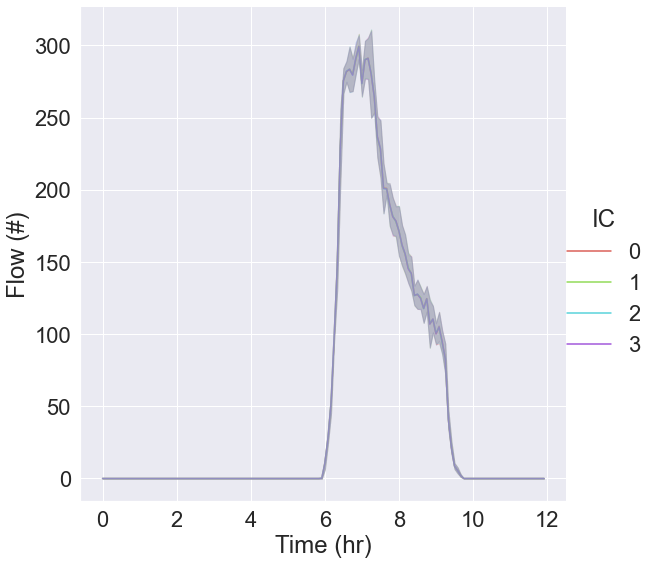

This section describes the modeling and simulation framework for evaluating the performance of the designed instruments including a no-toll or no-control benchmark, referred to as NT, congestion pricing, referred to as CP, and the tradable mobility credit scheme termed TMC. The overall simulation framework is shown in Figure 1.

travelers perform a daily commute between a single origin-destination pair. For the sake of simplicity, each traveler performs a single morning trip and a single evening trip. Only their morning commute trip will be explicitly simulated and their evening trip is assumed to be a mirror of the morning trip.

At the beginning of each day, every traveler uses forecasted information of travel times, schedule delays and their account balance over the entire day to make a pre-day mobility decision, which is the combination of a choice of mode (between car and public transit, hereafter PT) and departure time (over a individual set of departure time choices) for their morning commute trip. Travelers who choose to drive may be subject to a time-of-day toll. For TMC, the time-of-day toll profile is in units of tokens. Note that mobility credits can only be used for toll road payment. The individual mobility decision is modeled using a logit mixture model allowing for heterogeneity and non-linear income effects.

Next, the mobility decisions along with trading decisions – which occur over the entire day (i.e., are within-day) – are simulated on a simple network connected by a single driving path and an alternative public transit (PT) line. Congestion (for driving) is modeled by a point queue model (bottleneck of finite capacity), in which a queue develops once flow exceeds capacity. Travel time of PT is assumed to be constant.

Travelers’ day-to-day learning is modeled through an exponential smoothing filter to update forecasts of travel time and account balance over the day. The day-to-day framework in Figure 1 is used to simulate the evolution of the system state (departure flows, travel times) until a measure of convergence has been reached. The performance measures (overall welfare, distribution of user benefits, congestion, and mode shares) at convergence are used to evaluate the different instruments.

In the following sections, we first describe the models of demand, supply and day-to-day learning, termed the system model, in more detail. Next, we discuss social welfare computation and the simulation-based toll optimization problem (to determine optimal tolls) for the different instruments. Relevant notation is summarized in Table 2.

| Variables | Description |

| Departure time interval | |

| Simulation time step | |

| Day | |

| Start time of interval | |

| Duration of departure time interval | |

| Duration of simulation time step | |

| Size of desired arrival window | |

| Individual | |

| Value of time of individual | |

| Value of schedule delay early/late of individual | |

| Coefficient of nonlinear income effect | |

| Nonlinear income effect adjustment parameter | |

| Random component scale parameter of individual | |

| Random utility component for mobility decision of individual | |

| Disposable income of individual | |

| Departure time choice set of individual | |

| Mode choice set of individual | |

| Desired arrival time of individual | |

| Departure time window size parameter | |

| Market price | |

| Toll of instrument in | |

| Forecasted travel time of choice | |

| Expected cost for mobility decision | |

| Account balance of individual at time | |

| Token lifetime | |

| Token allocation rate | |

| Free flow travel time | |

| Delay in queue at | |

| Number of drivers in queue at | |

| Weights on previous day’s forecasts | |

| Variable associated with instrument |

5.1 System Model

As noted previously, the setting we consider involves users traveling between a single origin-destination pair connected by a path containing a bottleneck of finite capacity and a PT line. Users wish to arrive at the destination within a certain “preferred arrival time window” in the morning, and can choose between PT and car. If they decide to drive, they can adjust their departure times to avoid congestion (similar to the model in Ben-Akiva et al. [1984], which is a dynamic extension of De Palma and Lefevre [1983]). The system is modeled using a stochastic process approach that can be viewed as a simplification of the model in Cascetta and Cantarella [1991], who consider the stochastic assignment problem in general networks. Day to day adjustment is modeled using suitable learning and forecasting filters, within-day departure time decisions and mode choices are modeled using a logit-mixture model, and supply is modeled using a point queue model. We refer to Cantarella and Cascetta [1995] and Watling [1999] for a nuanced discussion of terminology and a detailed description of deterministic and stochastic process models.

The mobility demand model, network model, and demand-supply interactions are discussed in detail next.

5.1.1 Demand Model

The demand model (preday mobility decision) is a combined model of departure time and mode choice. Unless otherwise specified, the discussion in this subsection pertains to a specific day (we omit in all quantities for notational convenience). The day is discretized into time intervals of size (let the set of all time intervals in the day be denoted by , and it is assumed that each individual has a preferred/desired arrival time (more specifically, users are assumed to wish to arrive within a time window of size centered around ; this is discussed in more detail later). The day is also discretized into smaller time intervals of size of size , which is the resolution of the supply model and trading (selling) decisions.

The choice set of mode for individual is defined as , where represents car and represents transit. The choice set of feasible departure time intervals is individual-specific and defined as , where is a parameter, and represents the initial departure time interval on day 0, which is computed based on the preferred arrival time and the free flow travel time. Thus, the departure time choice set consists of time intervals of size centered around the preferred departure time interval on day 0, . Note that because we model income effects, the individual departure time choice set is also subject to a budget constraint (i.e., an individual cannot choose a departure time that is not affordable). Thus, we define the set of feasible departure time intervals under instrument ( for the No Toll scenario, congestion pricing, and the tradable mobility credit scheme respectively), as . Under the No Toll scenario, . We will revisit the budget constraint later when discussing income effects. Let represent an individual’s mobility decision as a combination of mode and departure time choice ().

Each individual is assumed to be rational and wishes to maximize her money-metric utility from the choice situation. The utility of the mobility decision for individual is denoted by , which consists of two parts: a systematic utility which is a function of observable variables and a random utility component that represents the analyst’s imperfect knowledge. is assumed to follow an i.i.d. extreme value distribution with zero mean and individual specific scale parameter . It is also assumed that the individual random error component is perfectly correlated across days and across instruments (i.e. remains the same before the ‘change’ and after the ‘change’) assuming before and after periods are not too far apart (e.g., McFadden [2001], de Palma and Kilani [2005]). This assumption can be relaxed in future work (see for example Delle Site and Salucci [2013], Zhao et al. [2008]).

The systematic money-metric utility for individual departing in time interval by car under instrument is denoted by , where . is a vector of forecasted information in the systematic utility that affects the choice of departure time interval for driving and consists of five components. The first is forecasted/expected travel time , which determines the expected schedule delay early (second component) and schedule delay late (third component). The fourth component is expected cost which is explained in more detail next. The last component is remaining income, which is equal to the disposable income for transportation minus expected cost .

The marginal utility of an additional unit of travel time for individual is denoted by . For simplicity, we assume travelers have common knowledge of forecasted travel times (more on this in section 5.1.3). The desired arrival time window for individual is defined as , where represents the center of the period and represents arrival flexibility. If she arrives outside of the desired time period, she incurs a schedule delay. The marginal utility of an additional unit of schedule delay early is and an additional unit of schedule delay late is , where from empirical evidence (e.g., Small [1982]).

The expected cost warrants additional discussion. Under the No Toll (NT) scenario, it is equal to the operational cost (fuel cost). Under pricing (), it is equal to the toll in dollars charged for departing in time interval , , plus the operational cost , which can be written as

| (18) |

Under the TMC () scheme, it depends on an individual’s expected opportunity cost of tokens (which can be negative if one has a net revenue from selling tokens) plus the operation cost as follows:

| (19) |

Recall that the selling revenue of tokens with transaction fees () and token price () can be written as (selling revenue function),

| (20) |

and similarly, the buying cost of tokens can be written as (buying cost function),

| (21) |

Let be the start time of interval , be the expected account balance at time , the beginning time of the time interval . If a traveler does not need to pay any toll, she can sell the entire day’s token allocation completely. Hence, the opportunity cost (or negative opportunity benefit) is equal to the negative of selling revenue of the entire day’s allocation, .

If a traveler needs to pay a toll in but the expected account balance is greater or equal to (no buying), her opportunity cost is equal to the negative of selling revenue of the one-day allocation minus the toll in tokens , which can be written as

| (22) |

However, if she does not have enough account balance to cover the toll , she has to buy additional tokens equal to in order to travel in . The amount of tokens she can sell for profit is equal to the one-day allocation minus her expected account balance since all of her tokens will be used for toll payment if she departs in . The opportunity cost can be written as

| (23) |

In summary, the expected opportunity cost of departing by car in interval depends on an individual’s forecasted account balance , market price , the toll in tokens and transaction fees as follows:

| (24) |

Note that if transaction fees are zero, the opportunity cost in Equation 24 reduces to the one-day allocation minus the toll in tokens times token price, i.e., . In the absence of non-linear income effects, can be ignored because it is a constant (appearing in all alternatives) that does not affect the choice and the expression reduces to , which is intuitive.

Regarding the income effect, the diminishing marginal utility of income suggests that as an individual’s income increases, the extra benefit to that individual decreases. It is thus natural to model this nonlinear effect of remaining income by a quasiconcave function (as per McFadden [2017]). Hence, we add the remaining income plus a natural log of the remaining income to the systematic money-metric utility.

The utility of an individual driving and departing in time interval (choosing a mobility decision ) under instrument can thus be written as,

| (25) | ||||

where

| (26) |

| (27) |

Schedule delay of the evening trip is ignored because it is assumed to be more flexible.

The systematic money-metric utility function of user who departs in time interval by PT is denoted as , where . Since the travel time and headway of PT are constant, we only need to consider one departure time interval , which has a corresponding arrival time closest to the desired arrival time . For PT, the input vector for the systematic utility consists of four components: PT travel time , expected waiting time , expected PT cost and remaining income .

The marginal utility of an additional unit of PT travel time of individual is assumed to be the same as that of car travel time, . The marginal utility of an additional unit of waiting time is .

The expected PT cost is equal to the PT fare under the No Toll (NT) scenario and pricing. Under the TMC scheme, it depends on an individual’s expected opportunity cost of tokens and the PT fare , where is equal to the negative of selling revenue of a full wallet since travelers who choose PT can sell all of their tokens acquired in one day for maximum return. It can be written as .

Hence, the expected PT cost under the TMC scheme can be written as

| (28) |

The utility of an individual using PT who departs in interval (choosing a mobility decision ) can be thus written as,

| (29) | ||||

5.1.2 Supply Model

The network is assumed to be a single origin-destination pair connected by a single path containing a bottleneck of fixed capacity [Arnott et al., 1990]. A first-in-first-out (FIFO) queue develops once the flow of travelers exceeds . The free flow travel time is and the extra delay time for a traveler departing from home at time is . Thus, the total travel time for a traveler departing from home at time is:

| (30) |

Let be the number of travelers in the queue at time . The delay at time is derived from the deterministic queuing model as follows:

| (31) |

where and when there is no congestion.

Note that within our simulation, the capacity is defined for time intervals of size . The travel time for a given departure time interval is obtained by averaging the travel times of all travelers departing in . Further, the exact time of departure of a traveler within the supply model is randomly (uniformly) drawn within the chosen departure time interval .

The alternative PT line has a constant travel time . Its headway is also constant, which is equal to twice the expected waiting time .

5.1.3 Day-to-Day Learning

Let denote the actual or experienced car travel time on day of choice under instrument , where . As we specified in the demand model, travelers are assumed to make their choices of departure time according to forecasted car travel times from their memory and learning. We use an exponential smoothing filter, a type of homogeneous filter [Cantarella and Cascetta, 1995], to model the learning and forecasting process by weighting actual and forecasted costs of the previous day as follows:

| (32) |

where is a learning weight given to the previous day’s realized travel time.

Under the TMC scheme, in order to obtain the individual forecasted account balance on day , denoted by , the individual forecasted departure time is first computed by applying a similar filter as follows:

| (33) |

where .

5.2 Simulation-based optimization

The problem of determining the optimal toll in dollars for congestion pricing, and the optimal toll in tokens for the TMC scheme, can be formulated as a simulation-based optimization problem with the objective of maximizing total social welfare (). The social welfare of the CP and TMC instruments is calculated relative to the NT scenario and is equal to the sum of user benefits () and regulator revenue (). Under congestion pricing (P), the regulator revenue is given by,

| (34) |

where is the mobility decision, which is a combination of mode and departure time choice; is an indicator if traveler chooses mobility choice given toll vector ; is equal to the toll payment for driving () or the PT fare payment for PT (); and is the set of feasible departure time intervals taking into account budget constraints.

Under the TMC scheme, the regulator revenue consists of two parts. The first part is the sum of PT fare payments and the second part is the sum of tokens bought (by individuals) minus tokens sold over one day. can be written as,

| (35) |

where is cost of buying function and is revenue of selling function; and are indicators of buying or selling at given the toll in tokens . Note that the price adjustment mechanism described in Section 3.3 is designed to ensure that the regulator revenue of the TMC scheme (second part in Equation 35) at equilibrium is close to zero, thereby achieving revenue neutrality.

The user benefits, which are a measure of consumer well being can be computed in three ways in the presence of non-linear income effects (we refer the reader to McFadden [2017] for a detailed discussion): Market Compensating Equivalent (MCE), Hicksian Compensating Variation (HCV), and Hicksian Equivalent Variation (HEV). MCE is equal to the difference in indirect utilities between a “but for” scenario and “as is” scenario, scaled to money metric units by dividing by the marginal utility of income (MUI) at the “as is” scenario. It differs from the commonly used Marshallian consumer surplus (MCS) only in the MUI scaling factor. It can be easily computed when the indirect utility function and its derivatives are known. HCV is equal to the net decrease in the “but for” scenario income that equates utility in the two scenarios while HEV is equal to the net increase in the “as is”” scenario income that equates utility in the two scenarios.

A potential drawback of these three measures is that their ethical implications are not defensible as pointed out by Blackorby and Donaldson [1990]. Well-being measured in units of income treat increases in income as equally socially valuable no matter who receives them. This is not the case with net utility improvement since the nonlinear effect of income improvement is captured by the income effect term in the utility specification (lower income users have a higher marginal utility of income). Hence, we measure user benefits () under instrument as the sum of all users’ net experienced utilities relative to NT denoted as (along the lines of De Palma and Lindsey [2004]). Since the utilities adopted in this study are money-metric, the net utility amount serves as a meaningful measurement of improvement directly. An individual ’s net experienced utility is the difference between maximum utility under instrument and under NT, which can be written as,

| (36) |

where is a vector of experienced variables under instrument and is a vector of experienced variables under .

Hence, the user benefits can be written as

| (37) |

As noted before, in the case of the CP scheme, we determine the toll in dollars which maximizes social welfare , computed at the equilibrium (or after convergence of the day-to-day model). For the TMC system, in addition to the toll in tokens, which is optimized, other parameters like the allocation rate and transaction fees are set exogenously (explained in more detail in Section 6.3). This is formulated as,

| (38) | ||||

| s.t. | ||||

where can be either or ; the toll profile is a set of toll values over the entire day. represents all input data for simulation, such as individual income, preferred arrival time, and choice attributes. represents all model parameters, such as demand model coefficients, bottleneck capacity, user learning weights, and market parameters for the TMC scheme. The function is the system model discussed in Section 5.1. The toll function that we consider is a step toll profile (of the kind implemented in Singapore and Stockholm), which consists of five step toll values and six break points.

Clearly, our optimization problem has no closed-form since the objective function for a given toll profile is the outcome of a simulation of the stochastic process (a simulation-based optimization problem), or more specifically, the system model presented in 5.1, which includes traveler behavior, regulator states and actions, and the resulting network and market conditions. In order to solve this simulation-based optimization problem, a differential evolution (DE) algorithm is adopted as it is derivative-free and performs well for global optimization problems of this kind [Storn and Price, 1997].

5.2.1 Differential evolution algorithm

In this section, we illustrate the application of the DE algorithm. Let represent the decision variables of the simulation-based optimization problem (i.e., the parameters of the step toll profile). The DE algorithm essentially has three iterative operators, mutation, crossover and selection, to iteratively improve candidate solutions.

The mutation operator uses individuals from the current solution population to generate variant vectors. The th variable of vector at generation , , is given by

| (39) |

where , , is a scale factor and is the solution population size.

Next, the crossover operator creates a trial vector by combining the variant vector and original vector as follows,

| (40) |

where is the crossover rate, represents a random uniformly distributed variable within , and is a random integer in ensuring at least one variable of the trial vector is from the variant vector .

Finally, the selection operator produces the next generation of vectors by comparing the original vector and the trial vector in terms of social welfare as follows,

| (41) |

6 Numerical Experiments

This section describes numerical experiments that examine the performance of the TMC scheme using the simulation framework described in Section 5. Data and parameters of the demand model, supply model, and the day-to-day learning model are introduced in Section 6.1. The parameters are calibrated based on empirical evidence to represent a realistic base case. Selected parameters will be varied in later experiments. The objectives of the experiments are to: 1) examine the overall performance of the TMC system under alternative market designs – more specifically, the effect of transactions fees in avoiding undesirable market behavior whilst retaining efficiency, 2) compare the efficiency and equity of the TMC scheme (market design based on experiments under 1) and CP under varying levels of congestion, heterogeneity, income effects, and 3) examine the robustness (adaptiveness) of the TMC scheme with a lump sum allocation versus a continuous allocation in the presence of unusual events.

6.1 Data and Model Parameters

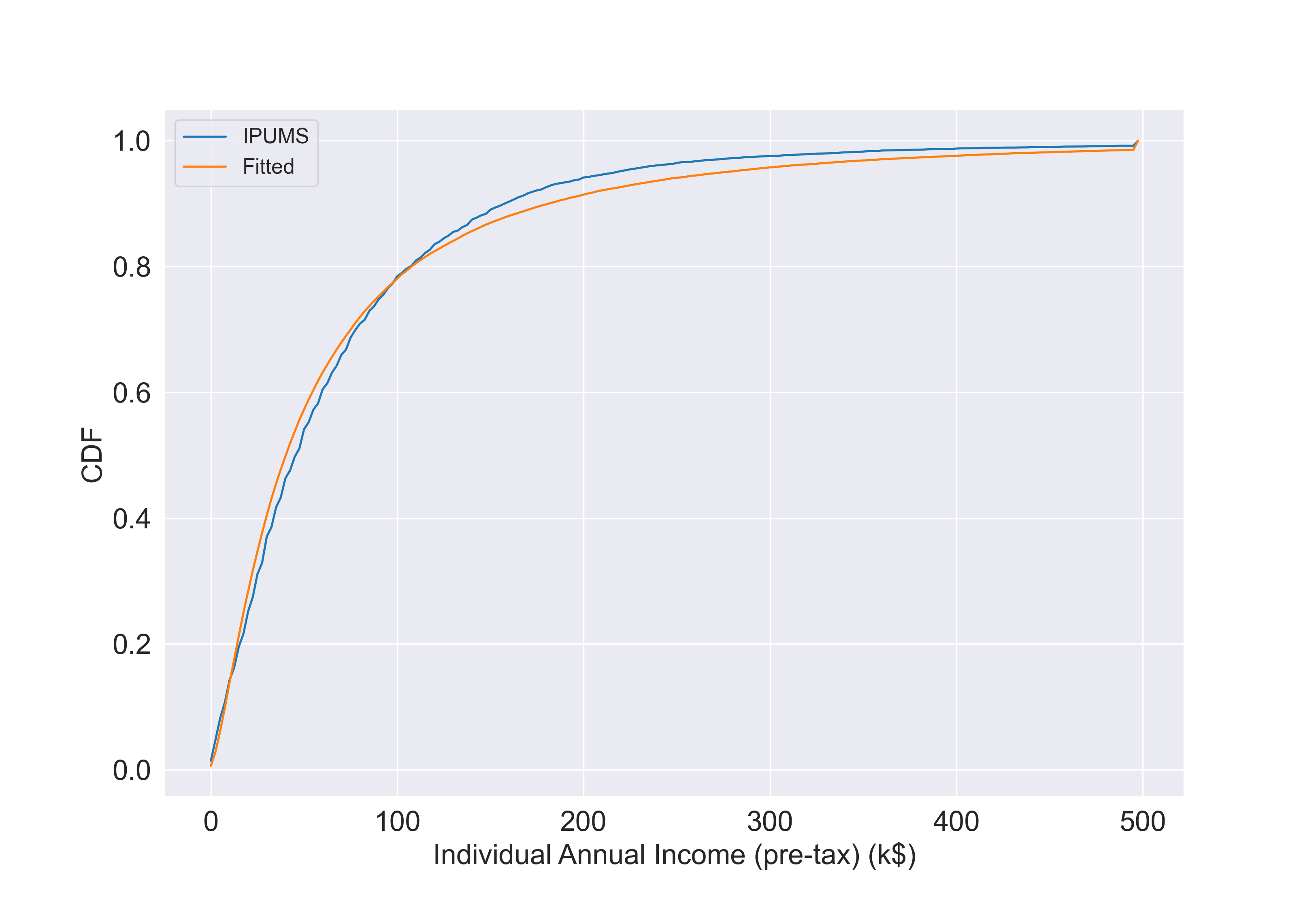

The demand model requires both choice attributes and individual characteristics as input data. The individual characteristics include disposable income and preferred arrival time . Recall that disposable income in our context is defined as personal net income after taxes and subtracting necessary living expenses (e.g. housing, health, food). The individual pre-tax annual income is assumed to follow a lognormal distribution and is fitted using the Integrated Public Use Microdata Series (IPUMS) 2019 census data [Ruggles et al., 2021]. The cumulative distribution function (CDF) of IPUMS data and fitted data are shown in Figure 2. Note that all annual incomes greater than 500 thousand dollars are grouped together. As we can see, the lognormal distribution fits the income distribution reasonably well.

Individual daily income is computed as the annual income divided by 260 working days per year and the individual hourly wage rate is computed by dividing daily income by 8 working hours per day. The minimum wage rate is set to $7.25 per hour as per the U.S. Department of Labor. It is less straightforward to obtain disposable income after taxes since necessary living expenses could vary significantly based on income and disaggregate data on this is sparse. Based on average data from the Bureau of Labor Statistics [U.S. Bureau of Labor Statistics, 2019], we assume that each traveler’s daily disposable income after taxes and necessary living expenses is equal to 60% of their pre-tax daily income.

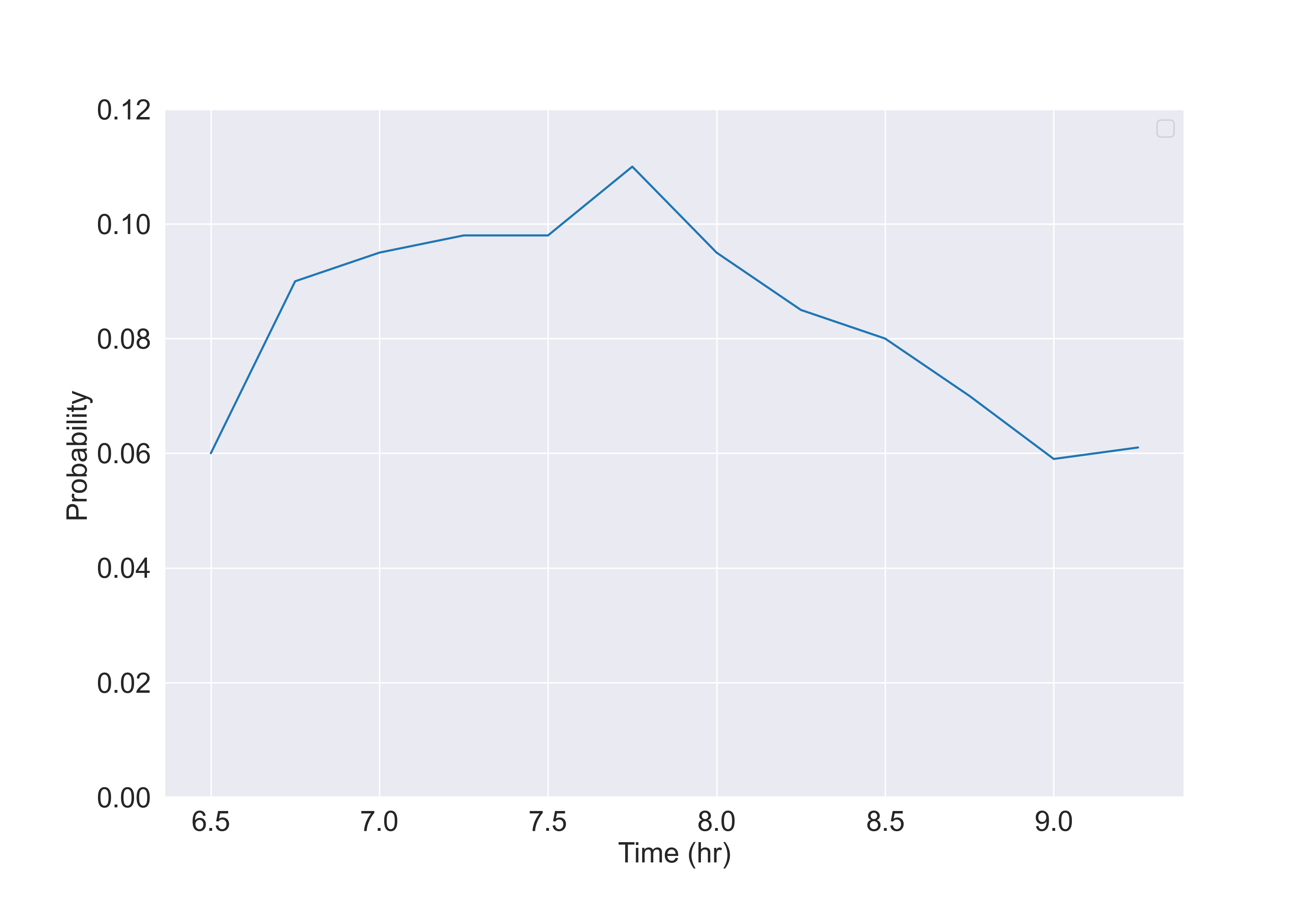

The preferred departure time distribution (preferred arrival time minus the free flow travel time) is based on a recent empirical study of road users in Stockholm [Kristoffersson and Engelson, 2018], and is shown in Figure 3. For simplicity, the size of the preferred arrival window is set to 0, which implies that individuals have a single preferred arrival time as in the standard Vickrey model. The departure time window size parameter is set to 30, which means the individual departure time choice set ranges over a 60-minute interval.

Empirical evidence (e.g. Small et al. [2005]) indicates that there is significant heterogeneity in the value of time across drivers. We assume that the individual value of time is perfectly correlated with income and is one third of the wage rate [White, 2016]. Note that this assumption will be relaxed in some experimental scenarios to consider different levels of heterogeneity.

Values of schedule delay early and late are also likely to be distributed across individuals. Due to the lack of empirical data on this, the literature on bottleneck models incorporate heterogeneity by making assumptions on the ratios between values of schedule early/late to values of time. Proportional heterogeneity (first considered by Vickrey [1973]) assumes that values of time and schedule delays vary proportionally or in other words, the ratio of the parameters is identical for all individuals [Van den Berg and Verhoef, 2011]. Ratio heterogeneity assumes that the values of schedule delays are fixed and only values of time are distributed [De Palma and Lindsey, 2002]. As a result, ratios of parameters are distributions. Van Den Berg and Verhoef [2011] considers a more general heterogeneity, assuming the ratio of values of time to values of schedule delay early follows a symmetric triangular distribution from 1 to 3 based on intuition and ratio of values of schedule delay late to values of schedule delay early is a constant 3.9 based on Arnott et al. [1990]. Along similar lines, we assume that the ratio of values of schedule delay early to values of time follows a triangular distribution from 0.1 to 1 with a mode at 0.5. The ratio of values of schedule delay late to is assumed to follow a triangular distribution from 1 to 3 with a mode at 2 (the selection of the modes as 0.5 and 2 are based on Small [2012]). The bounds are set based the empirical relationship [Small, 2012].

Further, as pointed out by Small [2012], waiting times are onerous compared to in–vehicle times by multiples of two to three by most assessments. For simplicity, the ratio of values of time to values of waiting time is assumed to be a constant equal to 3. With regard to the income effect, is set to 2 and is calibrated to be 3 to have the highest marginal utility of income to be less than 1.34 [Layard et al., 2008].

The scale parameter is known to be both confounded with the systematic utility and inversely related to error variance within the choice data [Ben-Akiva et al., 1985]. As pointed out in the literature (e.g. Louviere and Eagle [2006]), the modeled heterogeneity can come from heterogeneity in individual coefficients and scale heterogeneity that is shared across coefficients. We assume the scale parameter follows a lognormal distribution. The mean value is calibrated based on price elasticity (discussed subsequently) and the coefficient of variation is set to 0.5 based on judgement.

Next, we calibrate the mean value of the scale parameter to ensure that the aggregate price elasticities of the mobility model (for departure time choice) are reasonable and accord with empirical evidence. The price elasticity of peak hour demand (7 AM - 8AM) is computed assuming there exists a flat toll profile during the period from 6:30-9:30 AM. From the literature, the aggregate elasticities of peak hour travel vary greatly from case to case as they are dependent on the model structure, physical environment, activity type, initial toll levels and many other factors. Ding et al. [2015] estimated the elasticity of departing during the peak in Washington D.C. to be -0.0906 for driving alone. Sasic and Habib [2013] estimated that the elasticity of departing by car in the AM peak for work trips in Toronto is between -0.067 to -0.12. Holguin-Veras et al. [2005] found price elasticity of using crossings (tunnels and bridges) in NYC ranges from -0.31 to -1.97 for weekdays depending on the time-of-day. When there is no initial toll, the price elasticity simply represents fuel price elasticity. Lipow [2008] estimated fuel price elasticity as -0.17 and Gillingham [2014] estimated fuel price elasticity in California as -0.15.

| Toll | to | to | to | Total | ||

| 0 | -0.34 | -0.29 | -0.12 | 0.00 | 0.00 | -0.19 |

| 2.5 | -1.14 | -0.59 | -0.10 | -0.04 | -0.03 | -0.38 |

| 5 | -1.57 | -1.07 | -0.20 | -0.09 | -0.06 | -0.53 |

From calibration, the mean of scale parameter is determined to be 0.5. The corresponding price elasticities across different income groups and initial toll levels are presented in Table 3. As we can see, low income users are more sensitive to price than high income users, and when there is no toll, the aggregate price elasticity is similar to the empirical fuel elasticity. As the toll level increases, the aggregate price elasticity also increases and is similar to empirical values found in Holguin-Veras et al. [2005].

Regarding the supply model, the free flow speed of car is set to be 45mph [Ali et al., 2007] and the one way driving distance is assumed to be 18 miles (free flow travel time of 24 minutes). The operational cost of driving is assumed to be composed of only fuel cost, which is equal to $3.13 (driving distance times 1/23 gallon per mile times 4 dollars per gallon). For public transit, based on the New York City MTA data, the fare is set to $ 2, average speed is 25mph, and headway is 10 minutes. The PT distance is also assumed to be 18 miles, and the resulting PT travel time is 43 minutes since both headway and travel time of PT are constant. The expected waiting time is assumed to be 5 minutes.

| Variables | Description | Values |

| Population | ||

| Duration of a simulation time step | 1 min | |

| Duration of a departure time interval | 5 min | |

| Size of desired arrival window | 0 min | |

| Departure time window size parameter | 30 | |

| Coefficient of nonlinear income effect | 3 | |

| Nonlinear income effect adjustment parameter | 2 | |

| Bottleneck capacity (per min) | 39 | |

| Free flow travel time | mins | |

| Operation cost of car | $3.13 | |

| PT travel time | mins | |

| Expected waiting time | mins | |

| Operation cost of PT | $2 | |

| Learning weights | 0.1 |

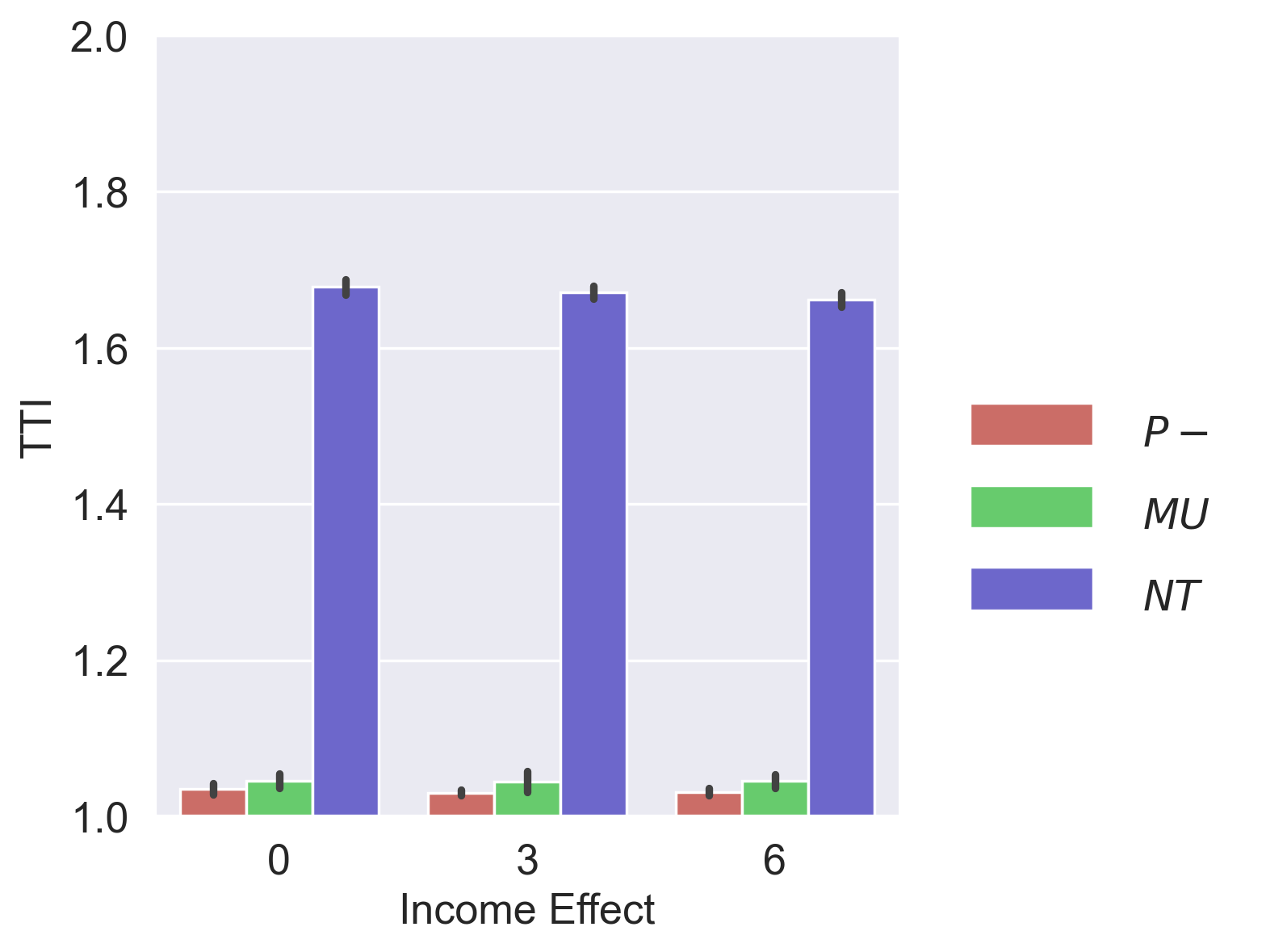

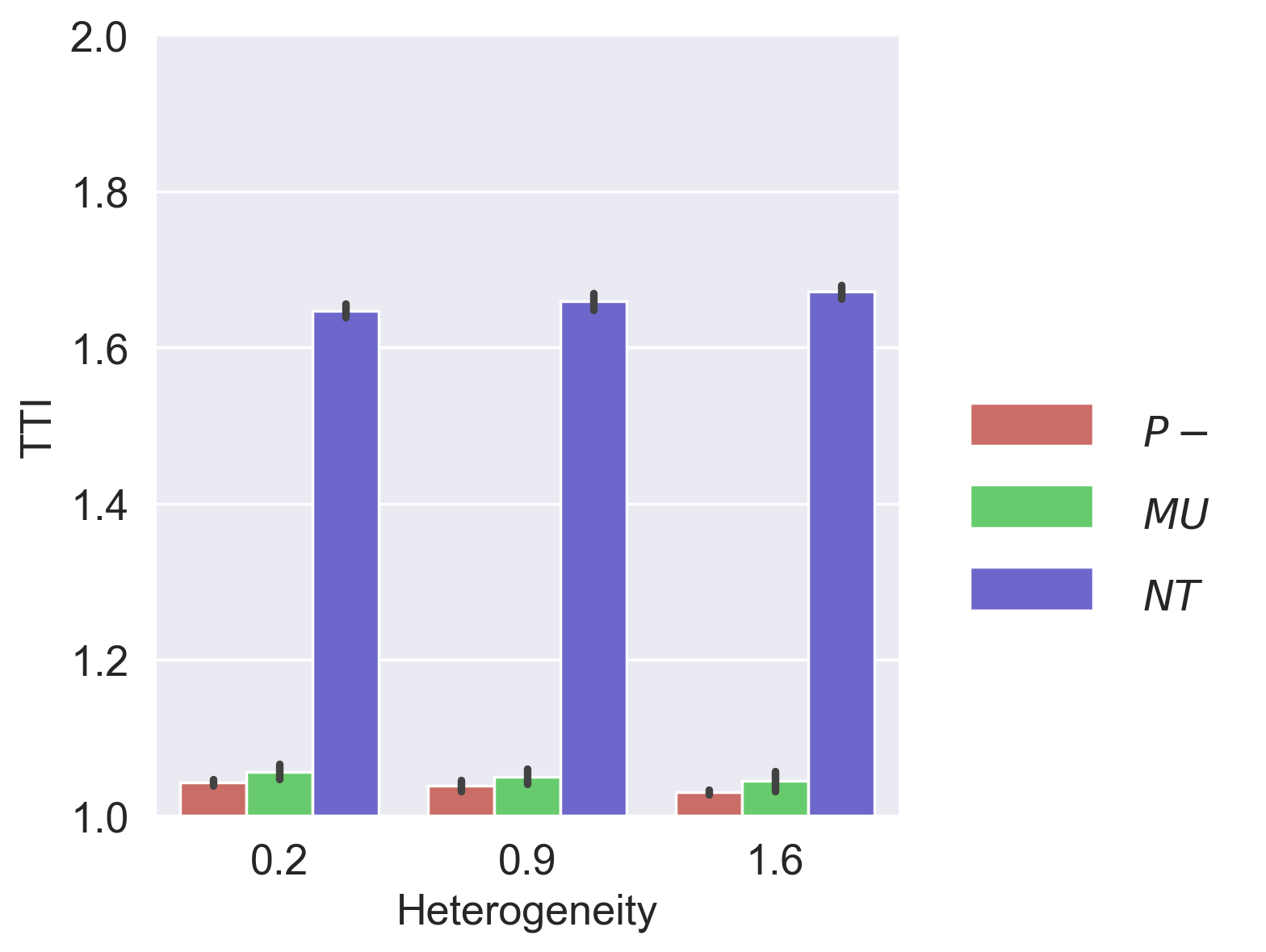

The bottleneck capacity is determined based on a calibration of the travel time index (TTI), which represents the ratio between actual travel time and free flow travel time. The base case capacity is determined to be 2340 vehicles per hour to have a reasonable level of congestion with a TTI of 1.68 [Chen, 2010] under the no toll (NT) scenario.

As described in Section 5.1.3, an exponential smoothing filter is adopted to update travel time information and individual departure time. The greater the learning weights are, the more unstable the system becomes [Cantarella and Cascetta, 1995]. The learning weights and are assumed to be 0.1.

Recall that we focus on the morning commute and hence, we simulate half a day (12 hours) with a simulation time interval of 1-minute, yielding 720 time intervals, . The market elements (allocation, expiration, and price adjustment) and trading behavior are also simulated for the first half. The second half of a day is assumed to be a mirror of the first half. The departure time interval () is assumed to be 5 minutes and the population size is 7500. Descriptions and values of key parameters are summarized in Table 4.

6.2 Existence and Uniqueness of Equilibrium

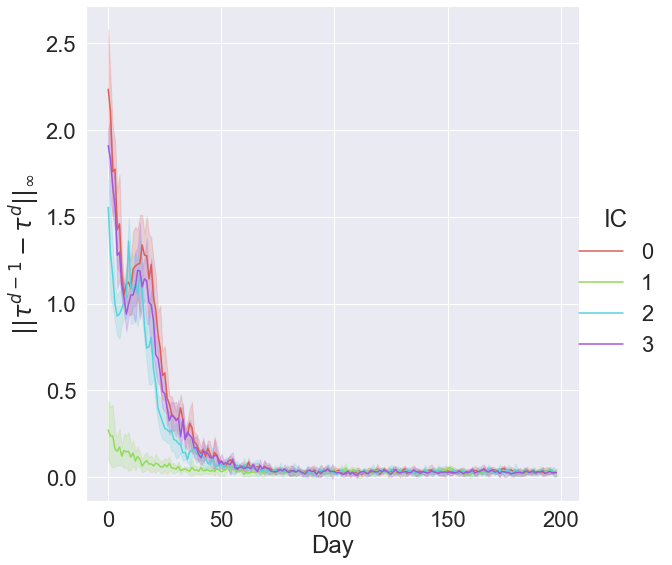

Existence and uniqueness of equilibrium in the bottleneck model have been widely studied (e.g. Hendrickson and Kocur [1981], Hurdle et al. [1983], Smith [1984], Daganzo [1985]), although heterogeneity is typically limited to the desired arrival time. Lindsey [2004] considers a more general heterogeneity in values of time, desired arrival times, and values of schedule delay and establishes conditions for existence and uniqueness of a deterministic departure time user equilibrium in the bottleneck model. De Palma et al. [1983] examine a stochastic user equilibrium where travelers are assumed to have identical systematic travel cost functions. They show that the equilibrium departure rate is unique but their findings cannot be directly applied to our model as we consider heterogeneity. Miyao and Shapiro [1981] establish conditions for the existence, uniqueness and stability of equilibrium for discrete choice models. Although their framework is relatively general, it assumes individuals have the same choice set whereas in our case, choice sets (for departure time choices) are individual specific. To the best of our knowledge, there are no analytical results on uniqueness of the equilibrium for our specific model. However, simulations with different initial conditions suggests that the day-to-day model converges to the same equilibrium solution. The tests on equilibrium and stationarity are summarized in A.

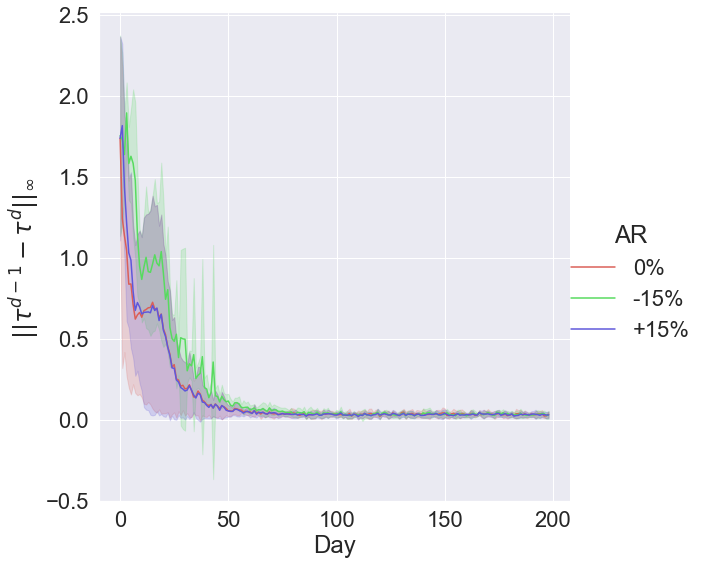

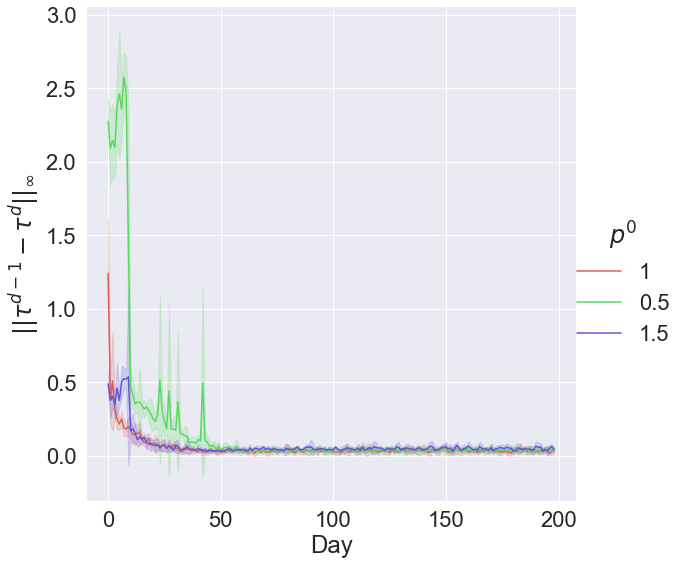

Note that the travel time of driving is used as a representative measure of the system state partly because it is central to the day-to-day learning process of travelers (alternatively, departure flows could also be used). The infinity norm (supremum norm) of day ’s travel time vector of driving and day ’s travel time vector of driving is calculated and used as a measure of convergence across days. This is given by,

| (42) |

where is the vector of travel times of day defined over a set of time intervals .

6.3 Optimization of tolls in TMC and Congestion Pricing

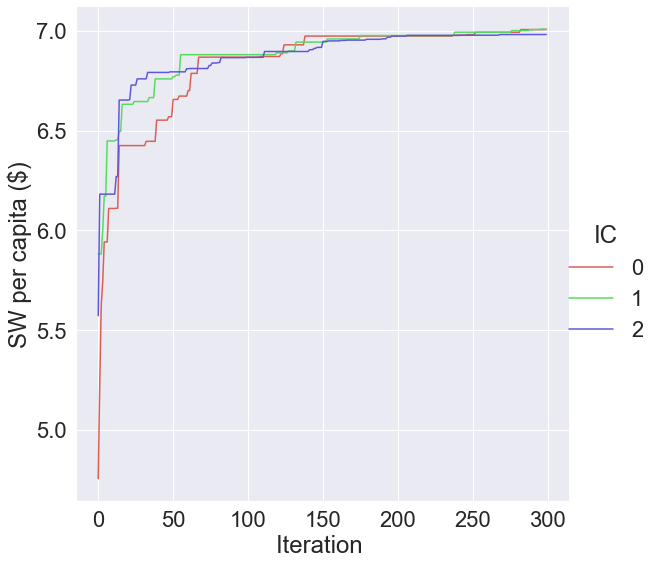

As discussed in Section 5.2.1, the time-of-day step toll profile is optimized using a type of metaheuristic algorithm known as Differential Evolution (DE). Metaheuristic algorithms have been shown to work well for nonconvex and nonlinear toll design problems (e.g. Shepherd and Sumalee [2004], Zhang and Yang [2004]). The population size of the DE algorithm is set to 15. Using data and parameters discussed in Section 6.1, we first examine the performance of the optimization algorithm for the congestion pricing (CP) instrument using three different initial populations (with 15 candidates). Next, the performance of the optimized TMC instrument and convergence properties are examined.

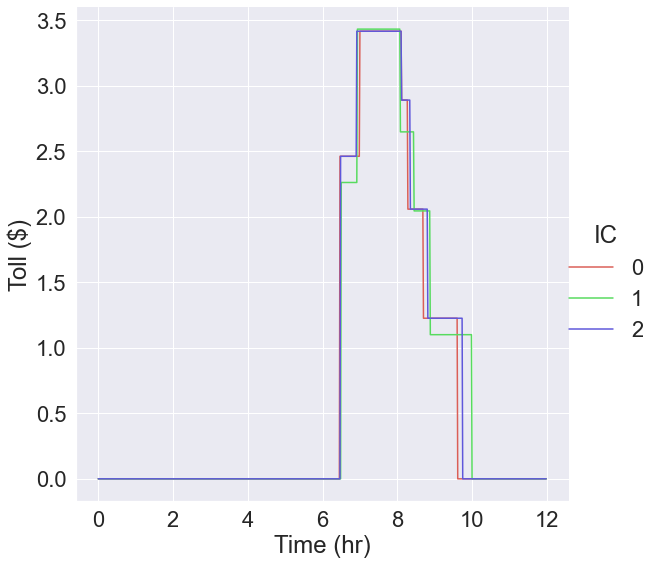

For CP, the convergence of social welfare along with the optimal time-of-day step toll profile with three different initial populations are shown in Figure 4. The algorithm converges to the same optimal welfare (within a tolerance of $0.01) for three different initial populations. The optimal toll profiles are near identical although there are minor differences at the locations when the toll changes (‘steps’).

For the TMC instrument, we set the total daily allocation of tokens for each individual as the per capita regulator revenue from congestion pricing (this should in theory yield a 1 dollar equilibrium market price and a toll in tokens that is identical to the optimal toll in dollars from CP, assuming there are no transaction costs and income effects). Note that the daily allocation can be set arbitrarily. Next, we optimize the toll profile in tokens given the specified token allocation. We assume that tokens are distributed uniformly to everyone and are allocated in continuous time. Every traveler is assumed to have a random account balance at the beginning of the simulation (to reflect different times of entry into the system; more on this in Section 6.4). Recall also that we assume the evening period is a mirror of the morning period, and hence we only simulate half a day, and assume the lifetime of tokens is 720 minutes. For simplicity, in these experiments, transaction fees are set to zero. Other parameters of the TMC are summarized in Table 5.

| Variables | Description | Values |

| Token allocation rate | 0.00285 per min | |

| Token lifetime | 720 mins | |

| Proportional transaction fee of buying/selling | $0 | |

| Fixed transaction fee of buying/selling | $0 | |

| Initial token price | $1 | |

| Price change | $0.05 | |

| Regulator revenue threshold | $300 |

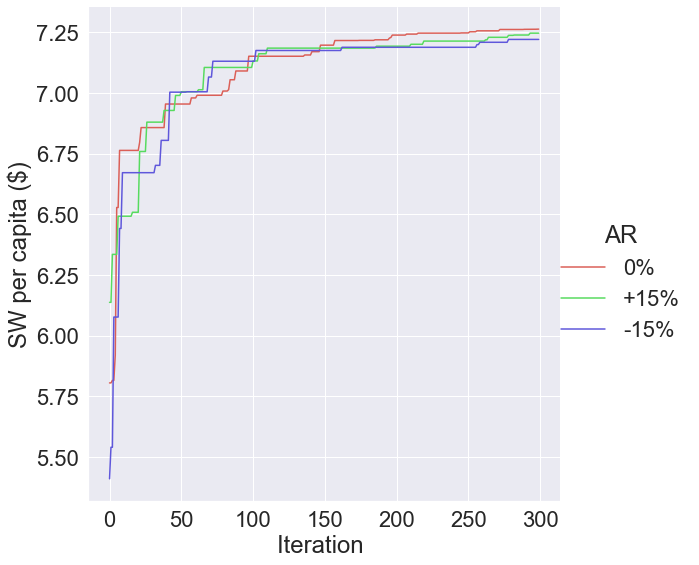

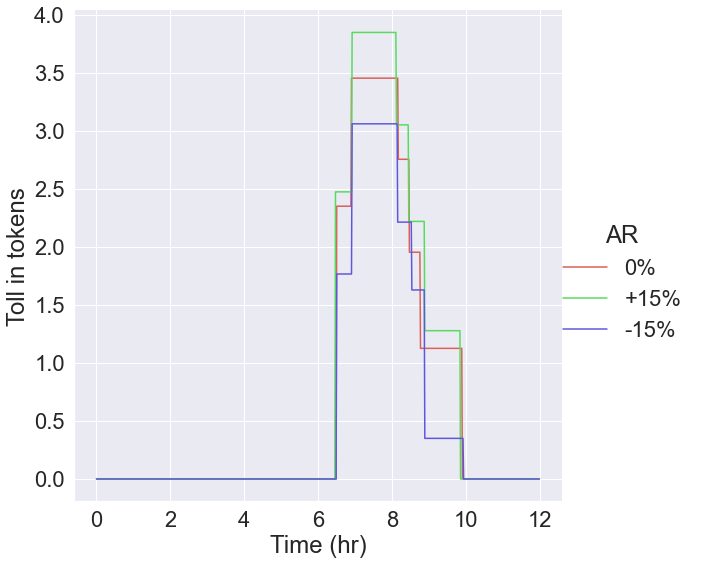

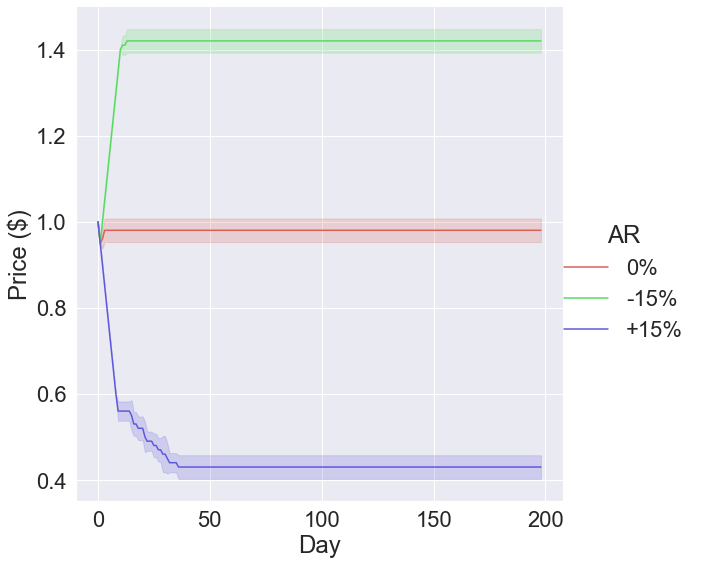

The convergence of the optimized objective values (social welfare) along with the optimal time-of-day step toll profile in tokens with three different allocation rates ranging from 15% less than the baseline to 15% more than the baseline are shown in Figure 5. As we can see, the different allocation rates converge to the same social welfare (within a tolerance of $0.02) at the end of 300 iterations. The token price of the baseline allocation rate is close to $1 (as expected) while the lower allocation rate has a higher token price of $1.1 and the higher allocation rate has a lower token price equal to $0.9. This is consistent with our expectation that the lower allocation rate leads to a higher token price due to less supply and vice versa. The optimal toll profiles in tokens in Figure 5(b) show that the lower allocation rate leads to the overall higher tolls in tokens and vice versa, again, as expected. Interestingly, due to the non-linear income effects, the social welfare of the TMC scheme is slightly greater than that of congestion pricing (we return to this later).

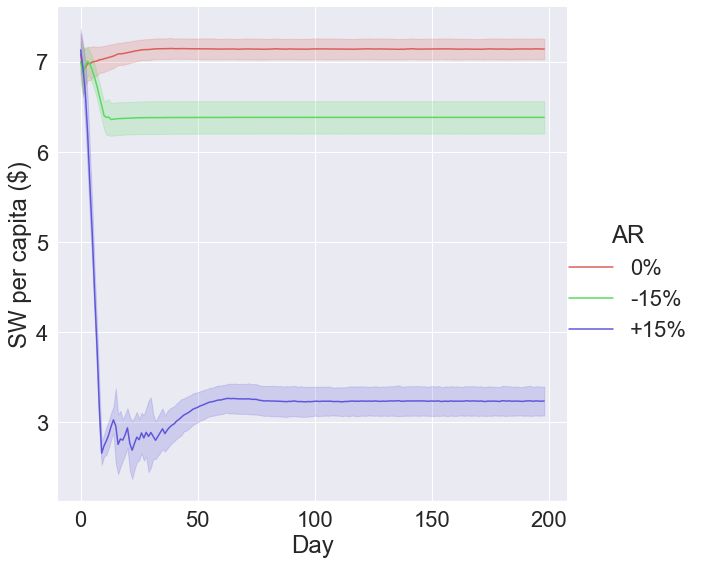

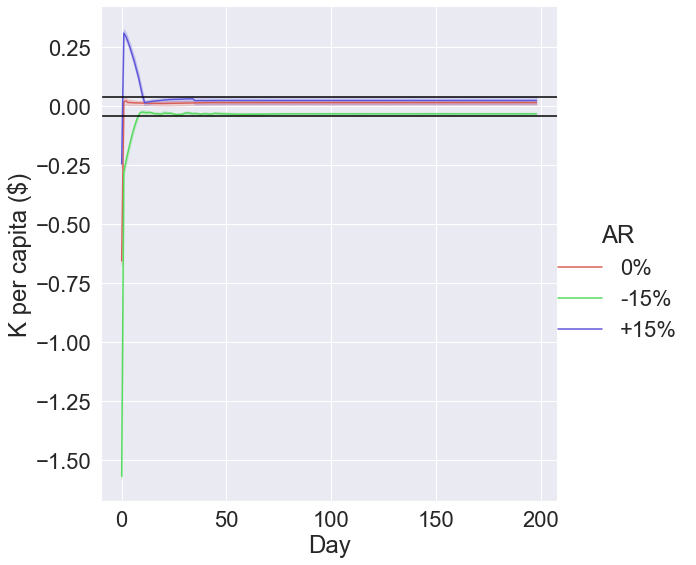

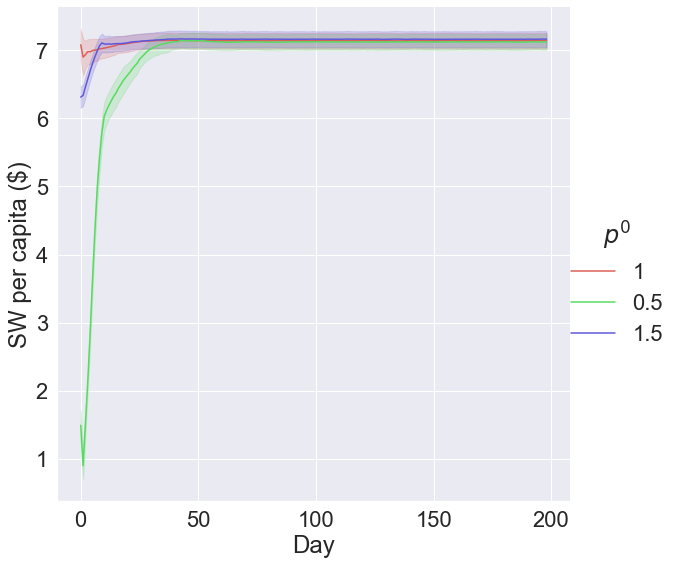

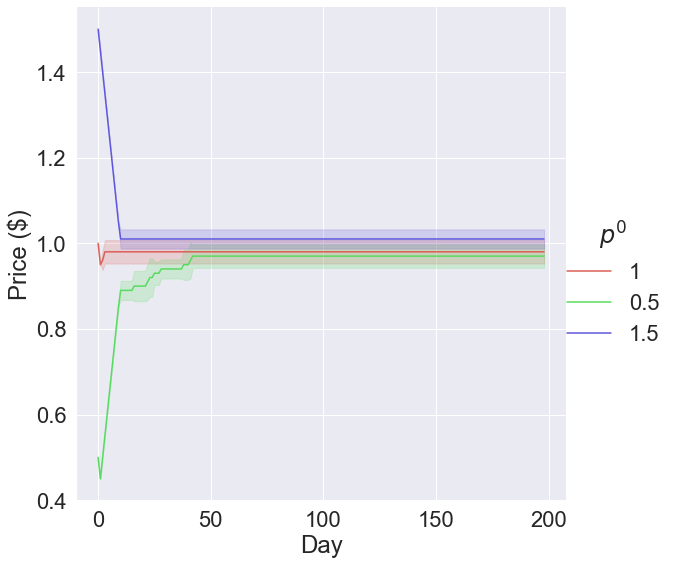

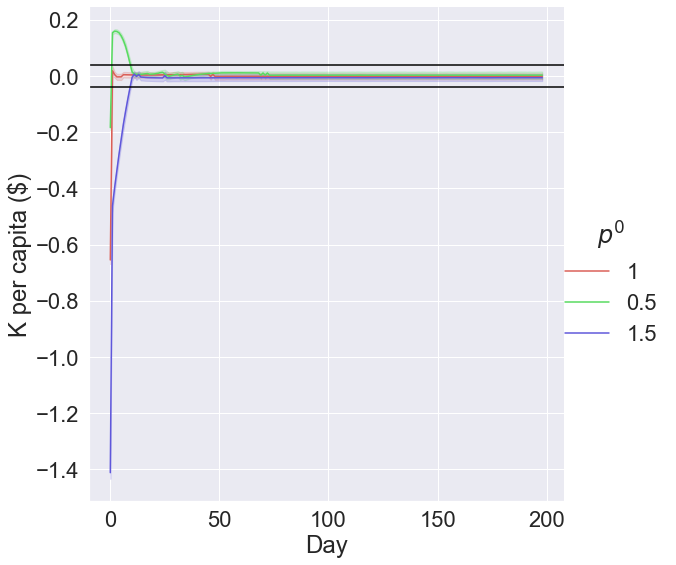

Given that disaggregate market behavior is modeled, it is also worthwhile to examine stability and convergence of the market prices. We examine this under different allocation rates (where the toll in tokens is not varied and is set to the optimal profile under the baseline allocation rate) and convergence of social welfare, market price, regulator revenue, and travel time of driving are shown in Figure 6. As we can see, since tolls are not re-optimized, different allocation rates lead to different social welfare and price values. The results also indicate stability of the credit market, and that the variation of equilibrium price and welfare with allocation rate is intuitive. The effect of various initial market prices on convergence of token price and social welfare are also examined in B.

6.4 TMC design and market behavior

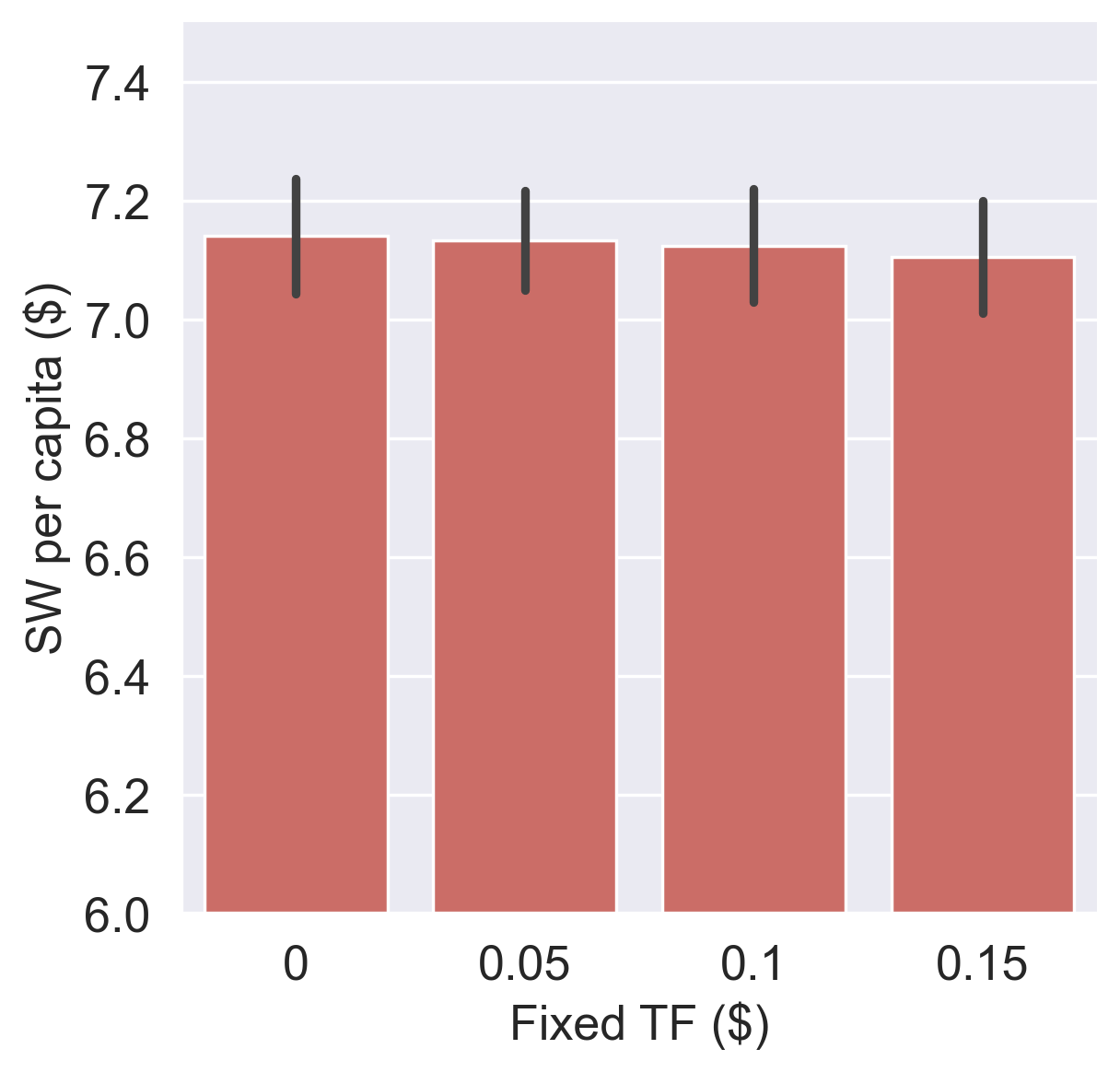

In the literature, a transaction fee has been used to prevent undesirable market behavior like frequent selling. For example, Brands et al. [2020] apply a small transaction fee of 0.01 euro to prevent frequent selling in their experiment. However, it has also been shown that transaction fees could reduce system efficiency [Nie, 2012]. Our analysis in Section 4 shows that a fixed transaction fee has the effect of preventing multiple transactions while the proportional transaction fees has the effect of making one sell as soon as possible when the conditional profit is positive (if buying is required at the time of the next trip). As an alternative to transaction fees, the regulator may also impose a minimum threshold (in dollar amounts) below which transactions are not permitted.

Numerical experiments in this section examine the effect of proportional and fixed transaction fees on social welfare and undesirable behavior. Specifically, undesirable behavior is defined as buying back tokens sold previously. We deem this undesirable because we would like to have users strictly being either sellers or buyers (not both). Sellers are the ones who travel in the off peak (or by transit) and sell their tokens while buyers are the those with a high willingness to pay to travel by car during the peak period.

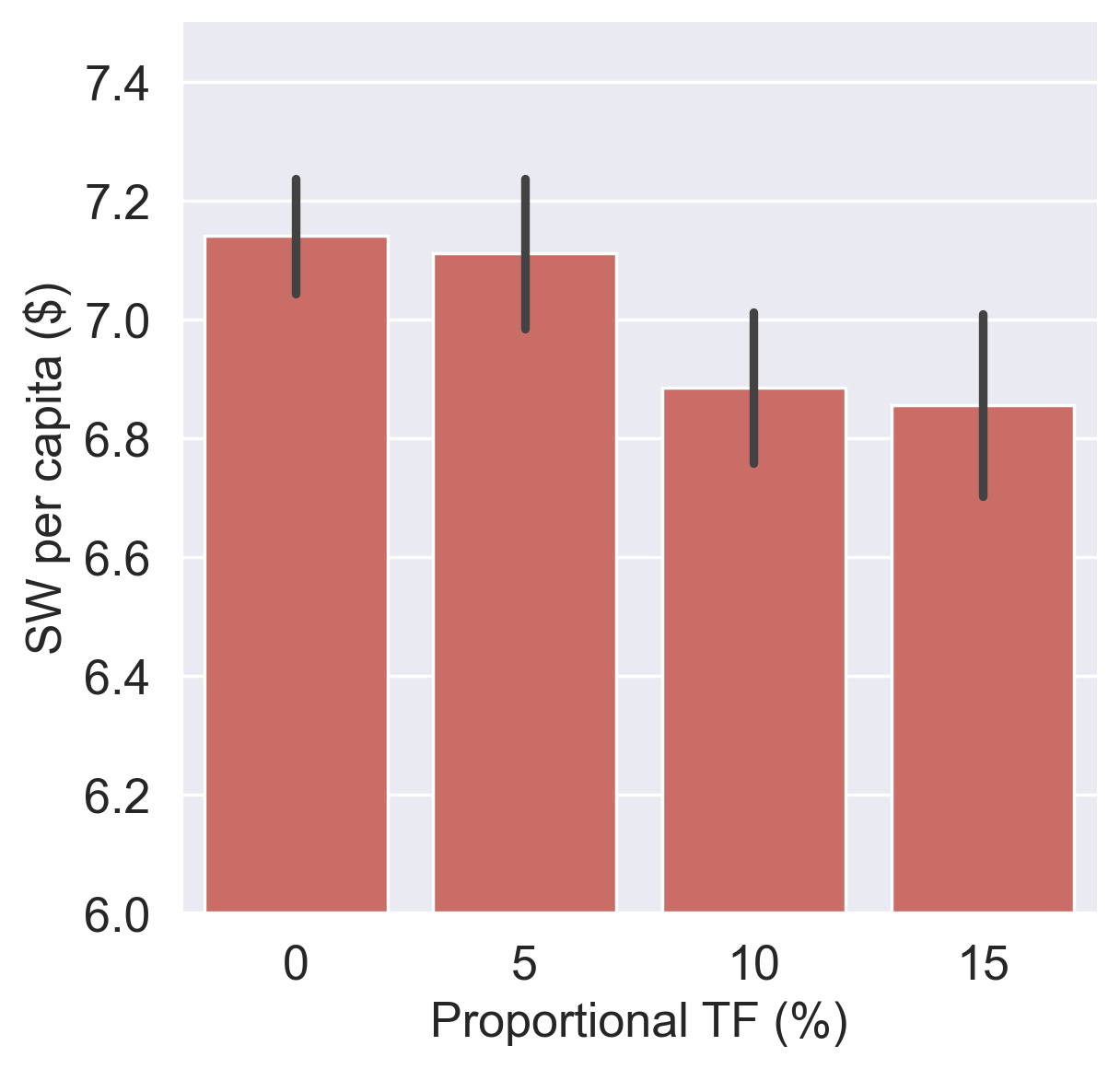

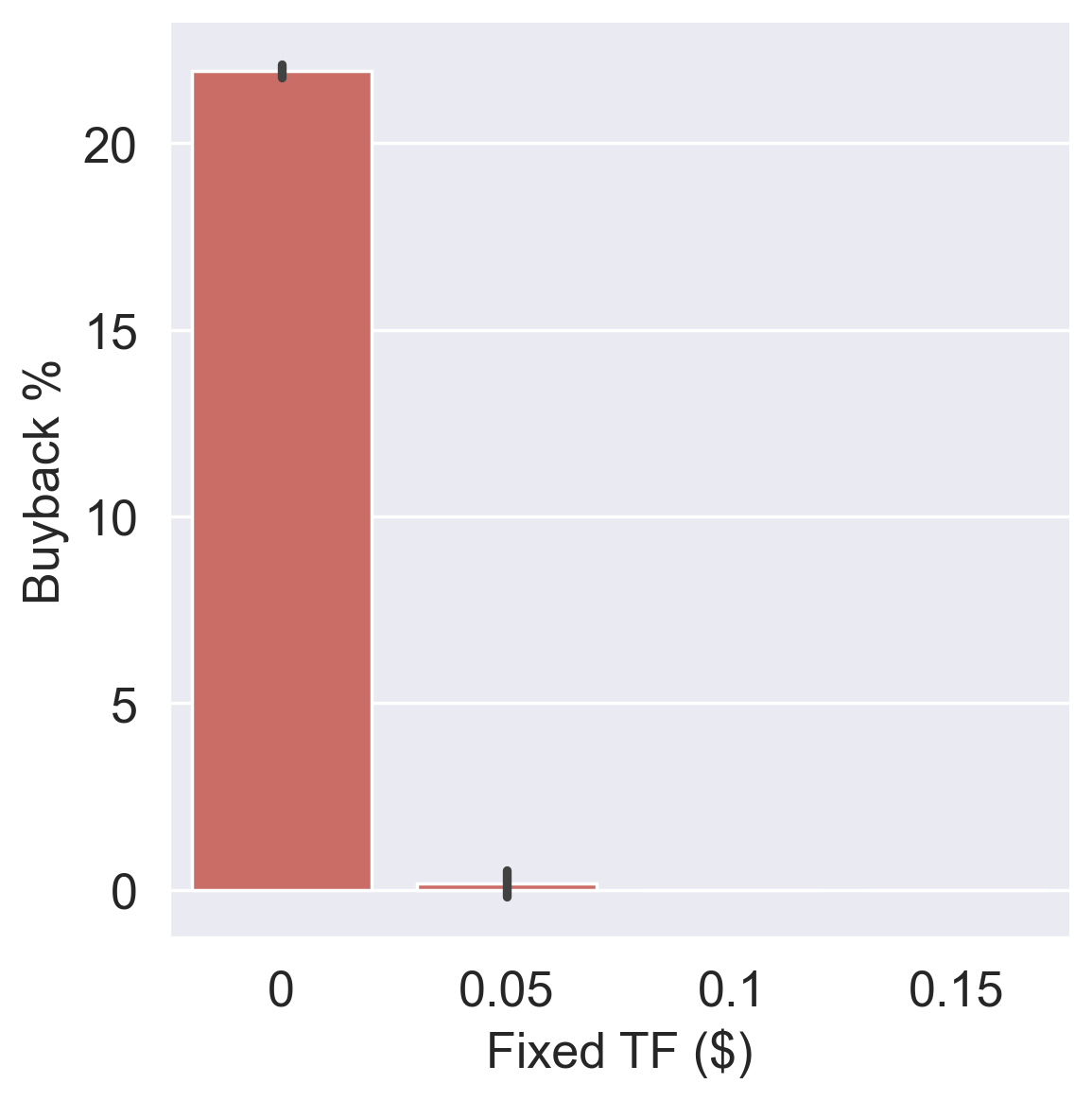

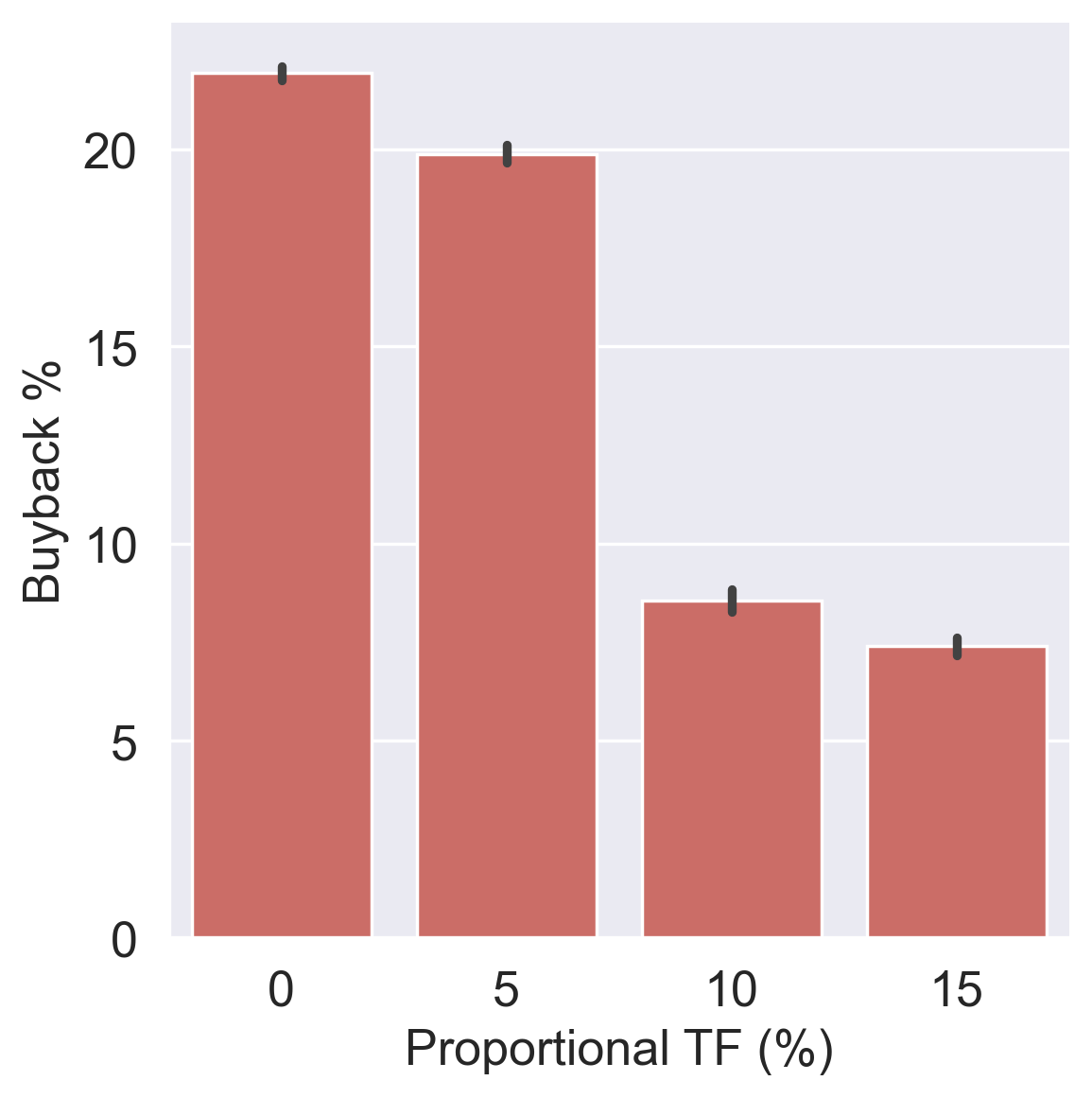

For simplicity, the fixed transaction fees of buying and selling are varied together with the proportional transaction fees set to zero and vice versa. The effects of fixed and proportional transaction fees on social welfare and buyback behavior are shown in Figure 7. From the simulation experiments, a small fixed transaction fee (5 cents in this study) is seen to be able to eliminate buyback behavior in Figure 7(c) and reduce welfare only slightly in Figure 7(a). On the other hand, there are higher social welfare losses in the case of the proportional transactions fees in Figure 7(b), which is also less effective in reducing buyback behavior in Figure 7(d). This is consistent with the findings from the literature on efficiency losses from proportional transaction costs [Nie, 2012].

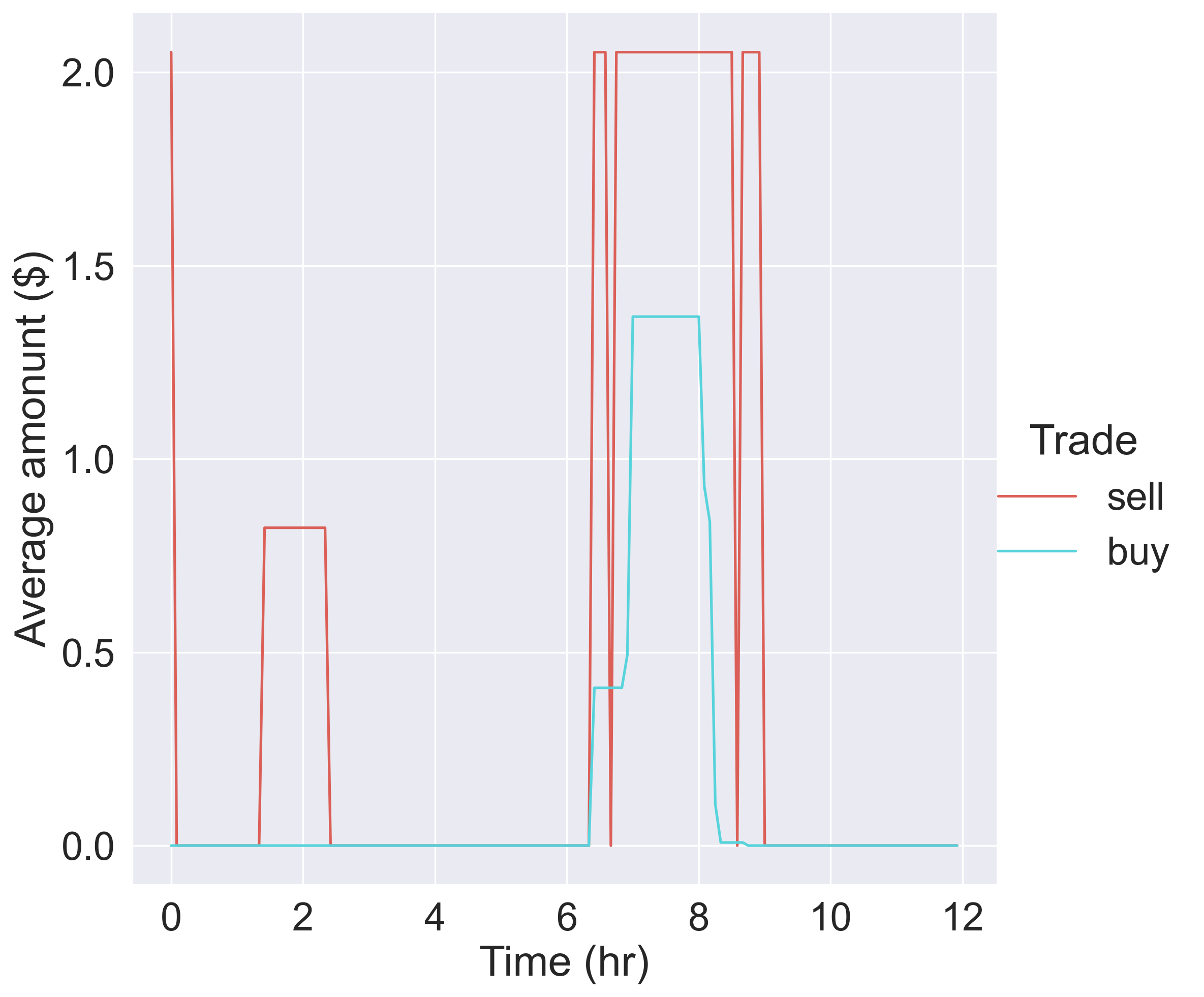

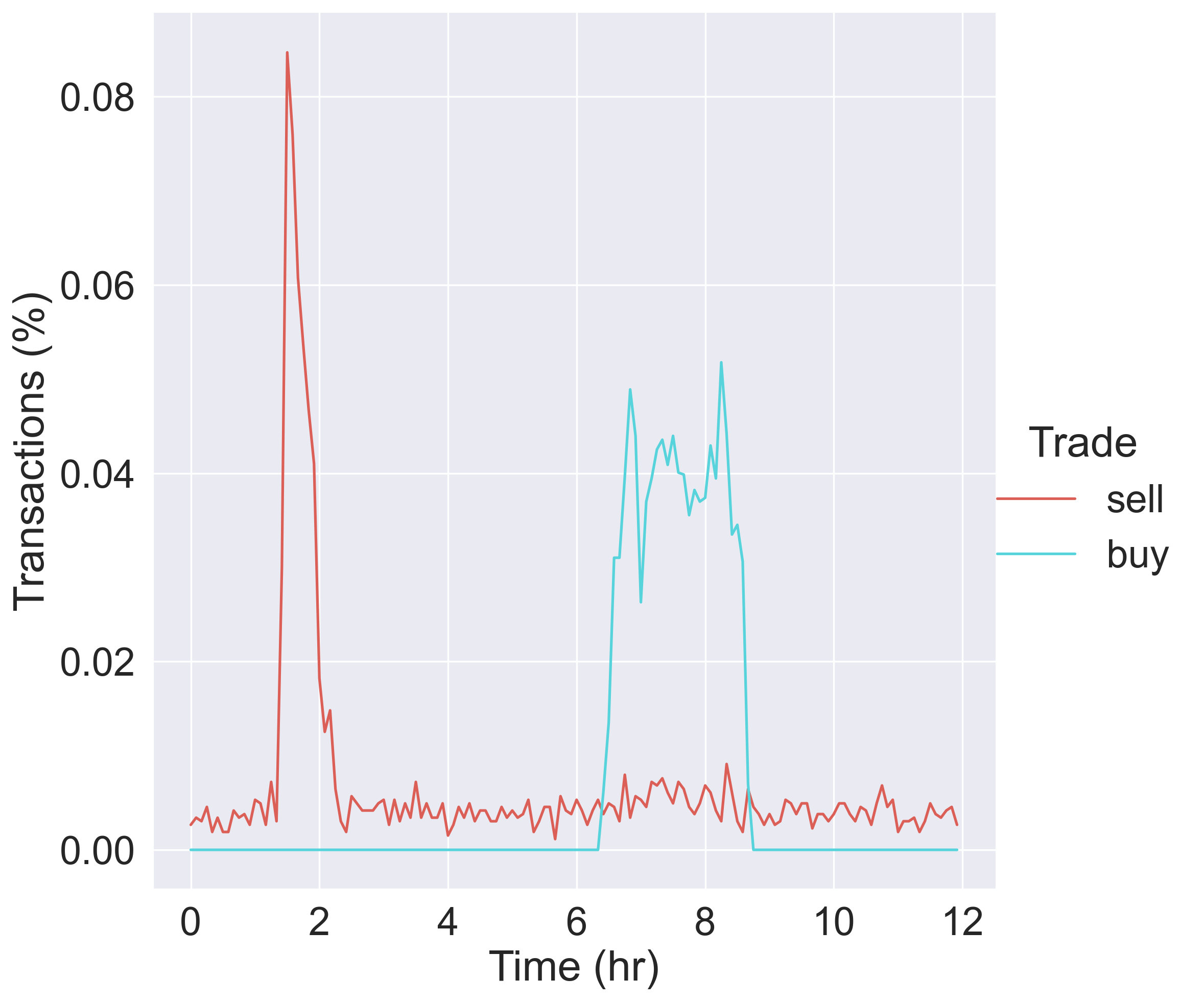

Next, we examine the effect of full initial account balances and random initial account balances on the transaction numbers and amount by time-of-day at equilibrium. The plots are based on simulations with a particular random seed because stochasticity can make the visualizations hard to interpret.

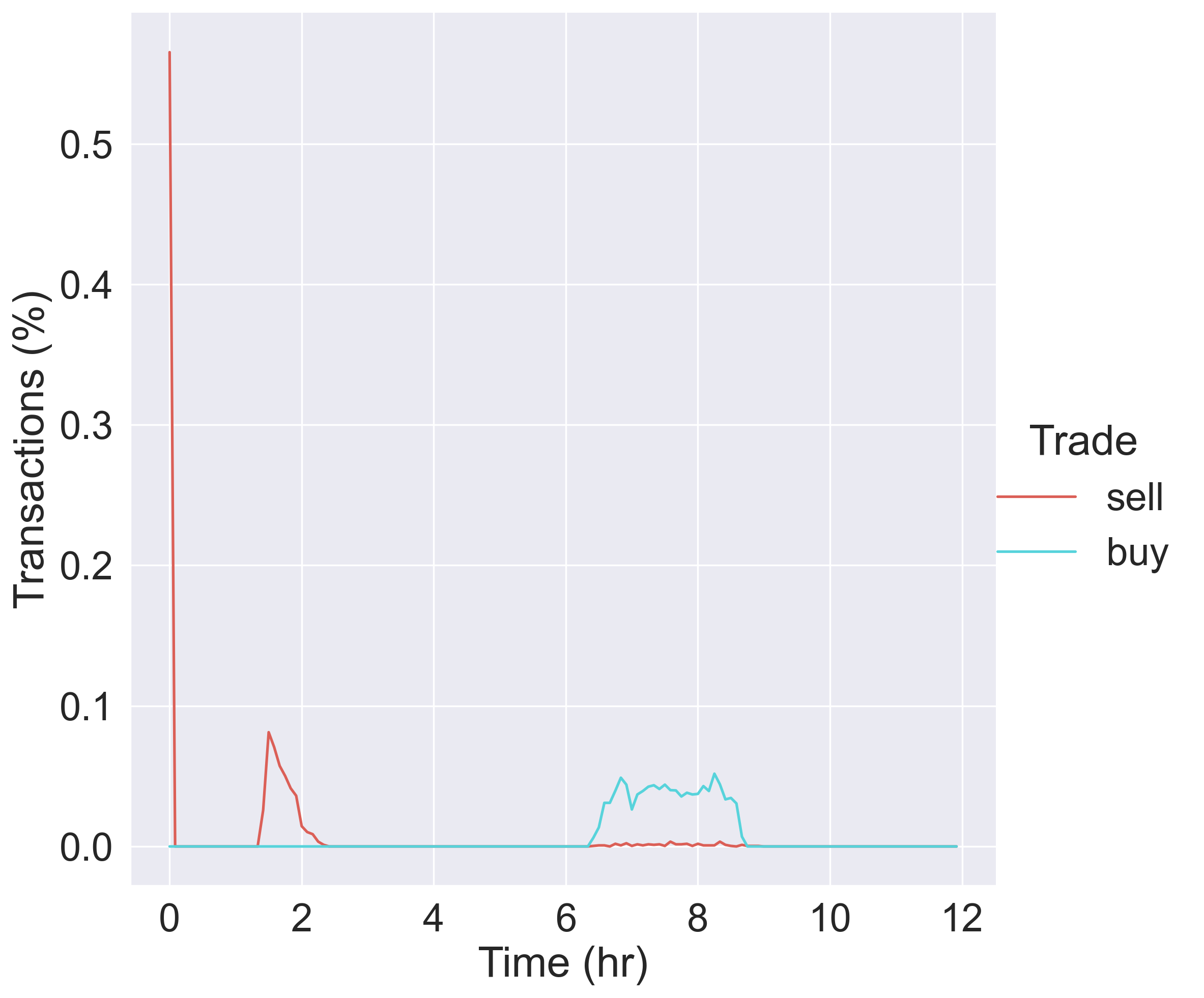

In Figure 8(a), the numbers of buying and selling transactions as a percentage of the corresponding total number by time-of-day at equilibrium for full initial account balances are plotted. As we can see, buying transactions only happen in the peak hour because travelers can only buy tokens at time of traveling if they are short of tokens. In contrast, selling transactions happen at the beginning of the day, in the early morning, and peak hour, which can be explained by the plot of the average transaction amount by time-of-day for full initial account balances in Figure 8(b). For travelers selling at the beginning of the day, all of them sell at full wallets as shown in Figure 8(b) (2.052 tokens as equilibrium token price is $1) because they travel in the off peak and do not need to use tokens; for travelers that sell in the early morning (around 2AM), their account balances at time of selling are not full because their future token allocations until their departure times can cover their toll and it is optimal for them to sell now; for travelers that sell in the peak period, they sell at full wallets because their account balances reach the full wallet after paying small toll charges. The selling behavior is consistent with the derived selling strategy but the excessive trading at the beginning of the day may be undesirable and avoiding this was in fact one of the motivations of the continuous allocation.

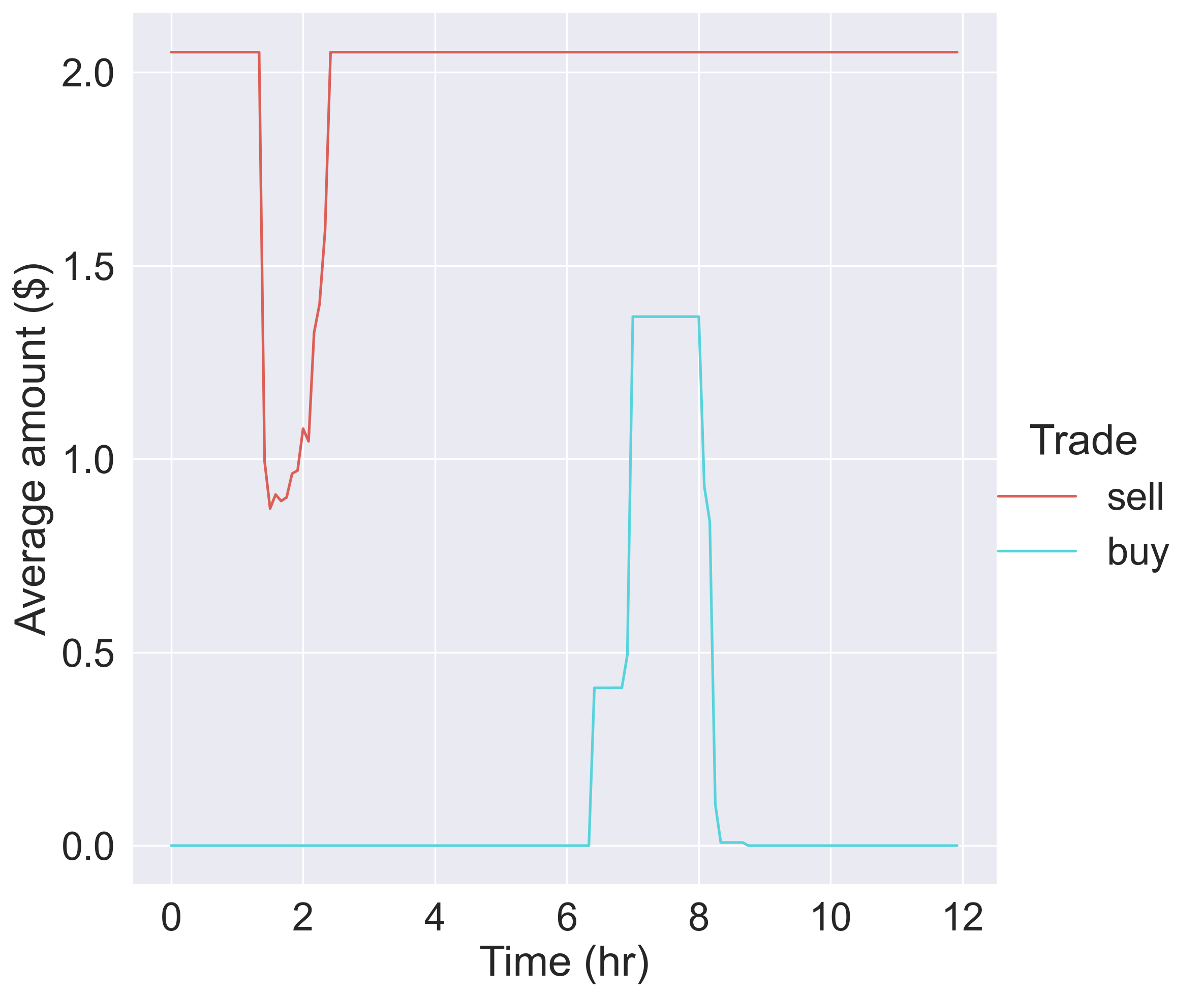

In practice, it is plausible that travelers will register for the program at different times in the day (one may think of the system as being implemented via a smartphone app). As a result, their account balances at the beginning of the day will be different, and we now assume the initial account balances are distributed uniformly between 0 and the maximum account balance (2.052 tokens). As shown in Figure 8(c), the selling transactions are now spread across the day with a relatively mild peak in the early morning (around 2AM). Apart from these travelers who sell in the early morning not at full wallets, other travelers sell only at full wallets as shown in in Figure 8(d). Under this assumption, we see a much more desirable pattern of transactions over the day, and the usefulness of the continuous allocation. However, the fact that different initial account states lead to different patterns of selling behavior at equilibrium is a problematic property of the system (despite the fact that the optimal welfare and associated market prices and flows are unique), and one that deserves further investigation.

6.5 Performance of the TMC Scheme under varying levels of congestion, heterogeneity and income effects

| Factor | Level 1 | Level 2 | Level 3 |

| Capacity () | -15% | 0% | 15% |

| Income Effect () | 0 | 3 | 6 |

| Heterogeneity (c.o.v) | 0.2 | 0.9 | 1.6 |

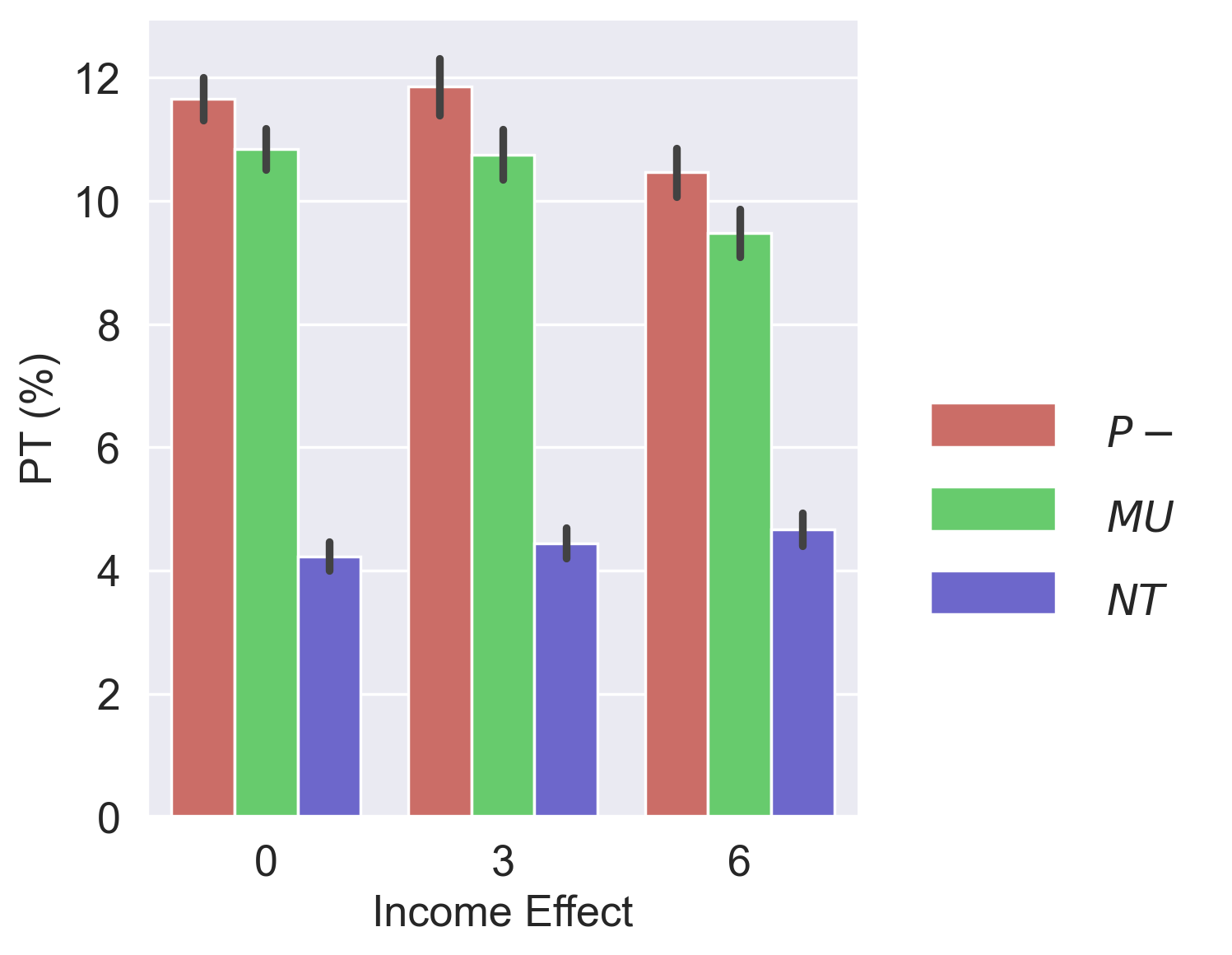

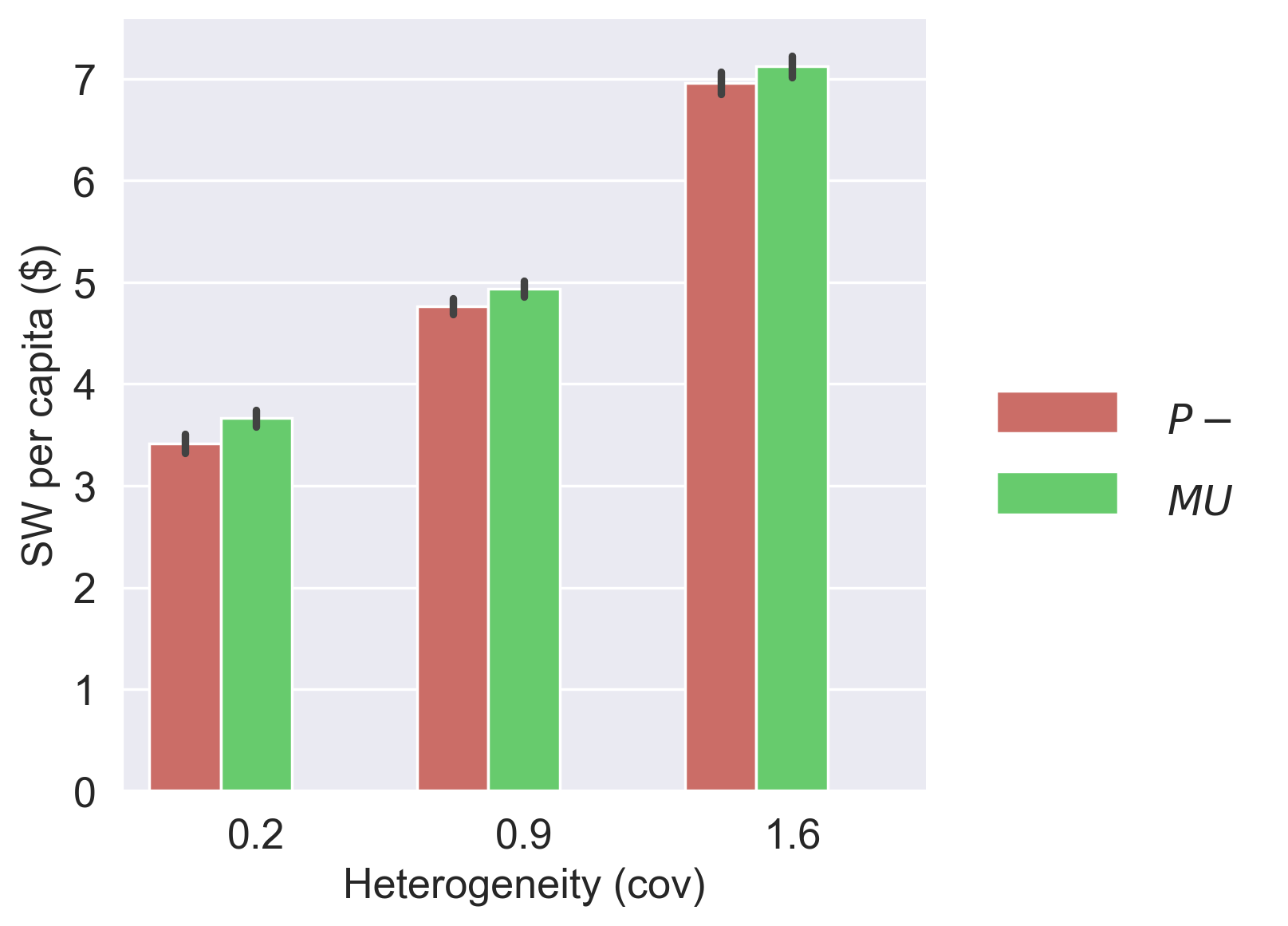

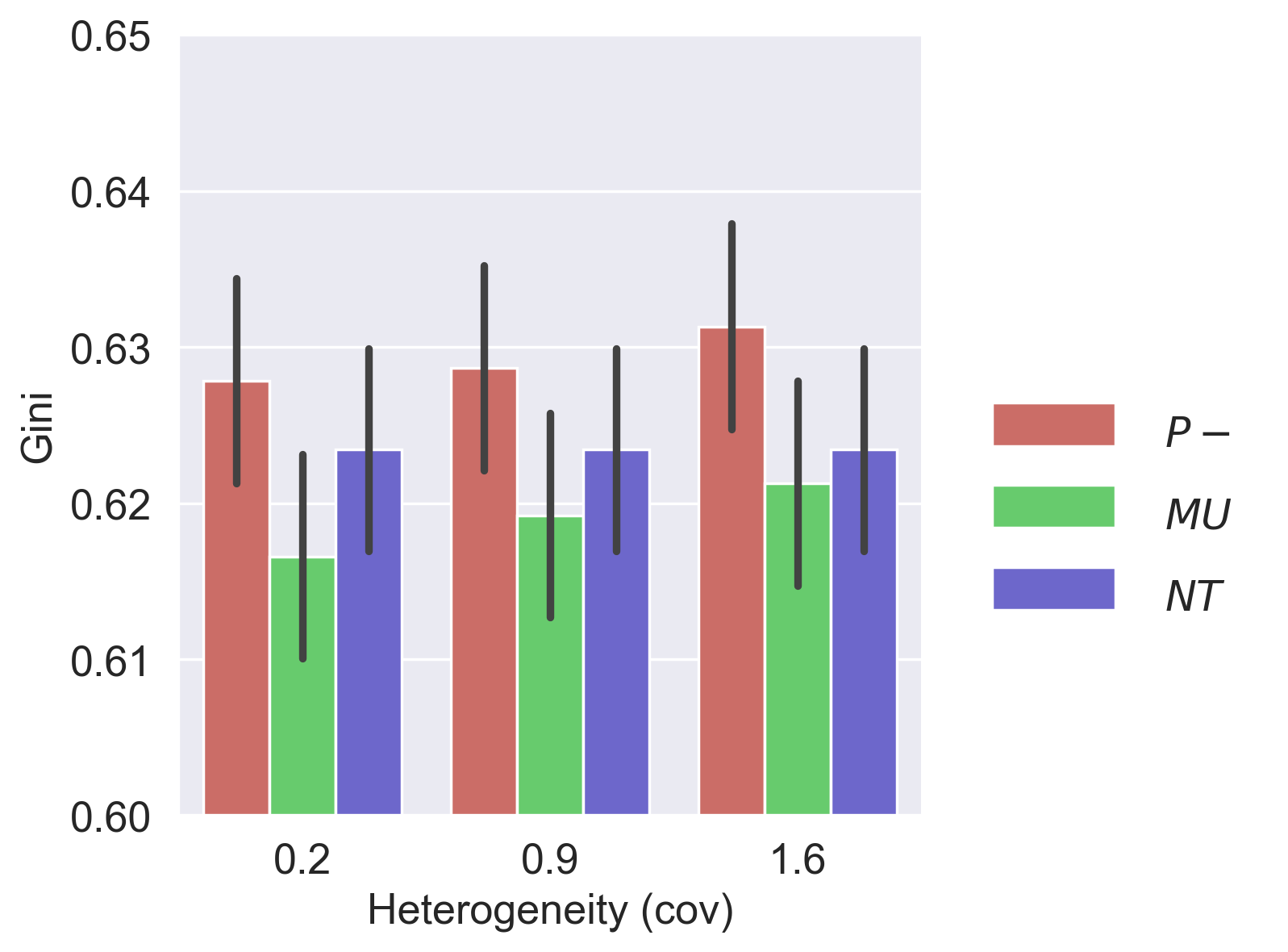

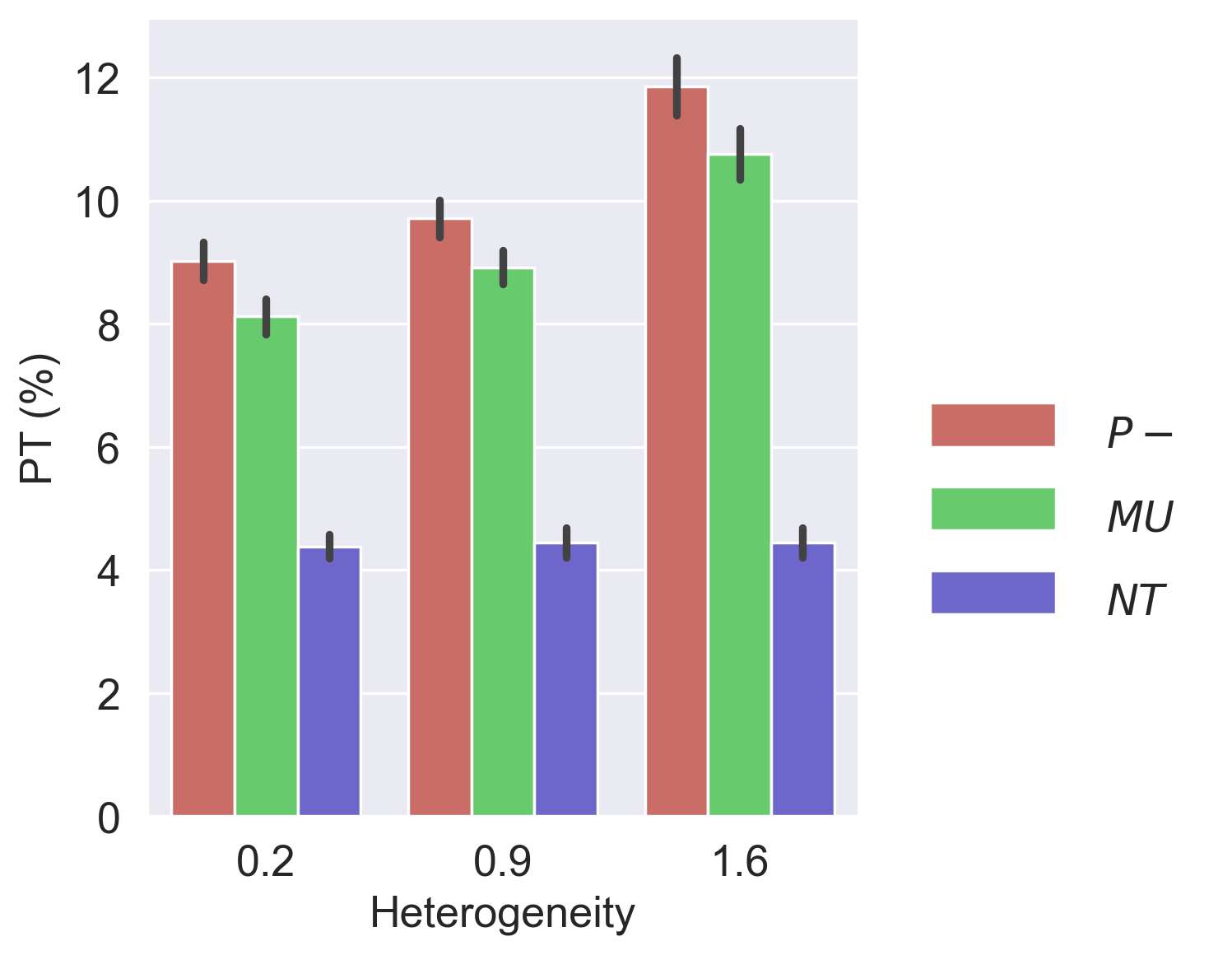

We next examine the performance of the TMC scheme relative to congestion pricing at varying levels of three important experimental factors: capacity, income effect and heterogeneity. For the TMC scheme, fixed transaction fees are set to $0.05 and proportional transaction fees are set to 0 based on the experiments in the previous section. The factors are varied one at a time across three levels as presented in Table 6. Values used in the base case are highlighted in red (when varying a given factor, other factors are fixed at the base level). With regard to capacity, bottleneck capacity is varied from 15% less capacity than the baseline to 15% more capacity than the baseline; for the income effect, the nonlinear income effect coefficient in the utility specification is varied from 0 to 6; for heterogeneity, the coefficient of variation of value of time is varied from 0.2 to 1.6. In the following discussion, the TMC system is denoted by MU (U denotes the uniform allocation of tokens) and congestion pricing is denoted by P to indicate that we do not assume a redistribution of toll revenues in any form. The No-toll scenario is denoted by NT. For each scenario in the experimental design, the two instruments and NT are simulated with five different random seeds until convergence.

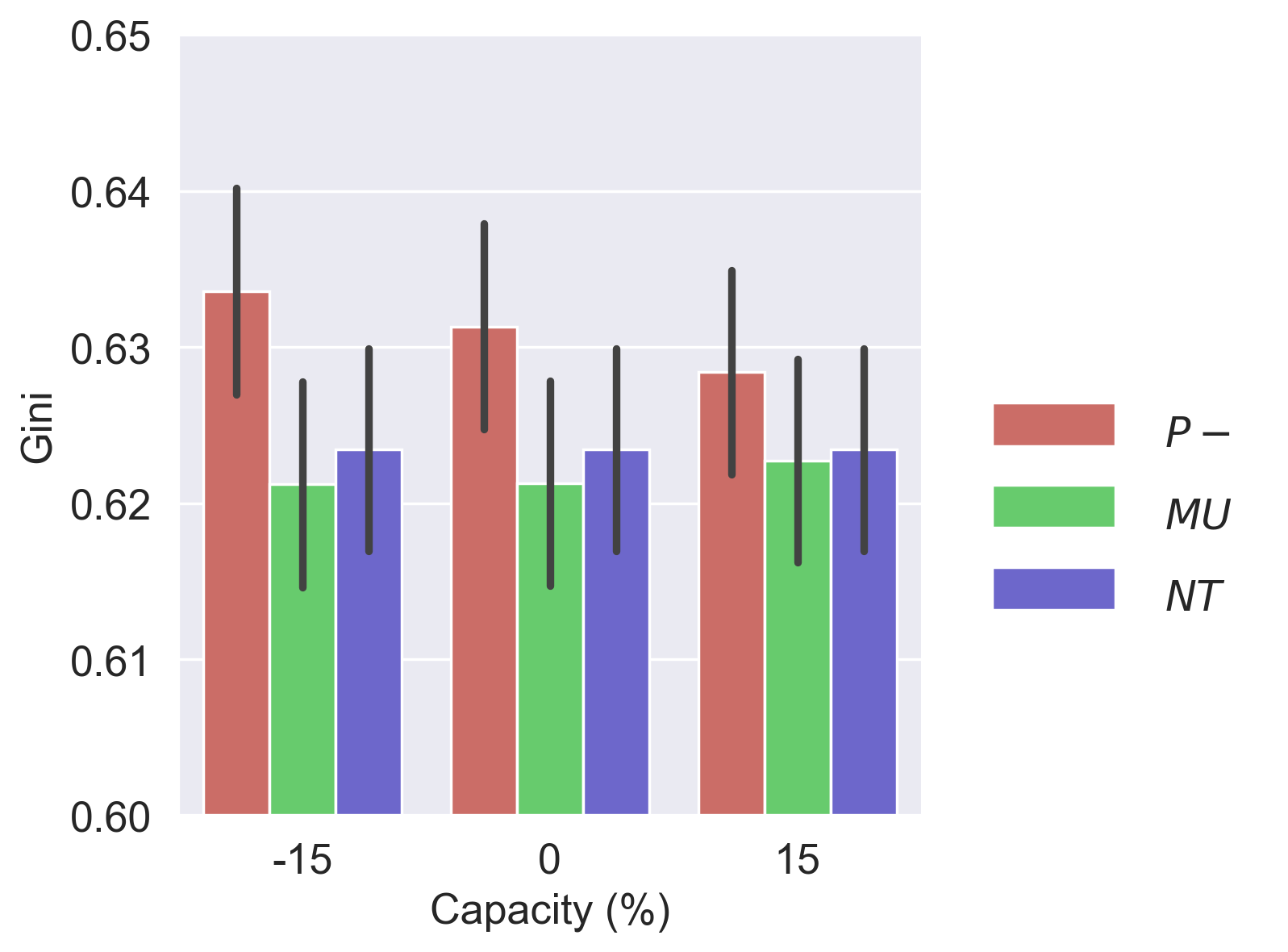

6.5.1 Capacity

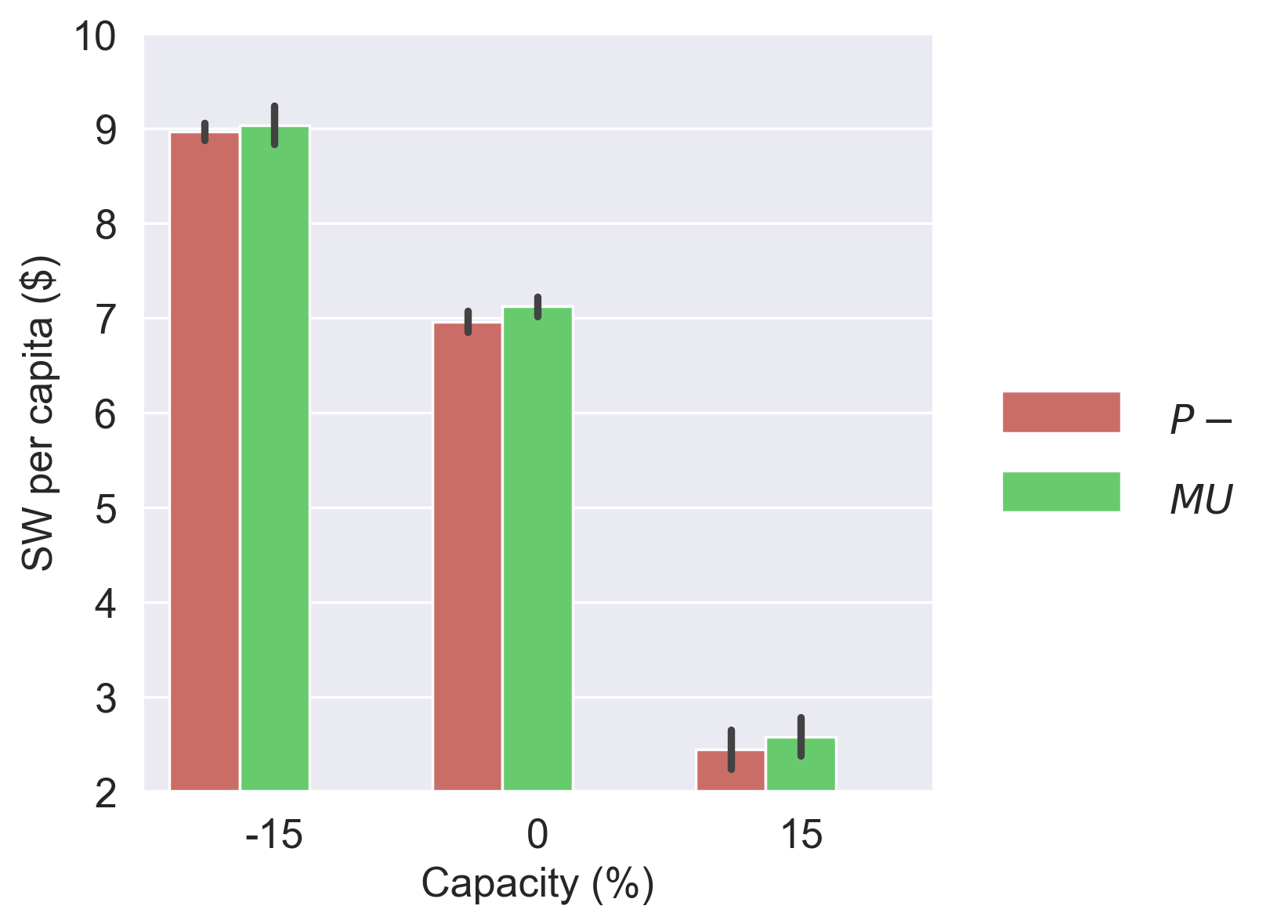

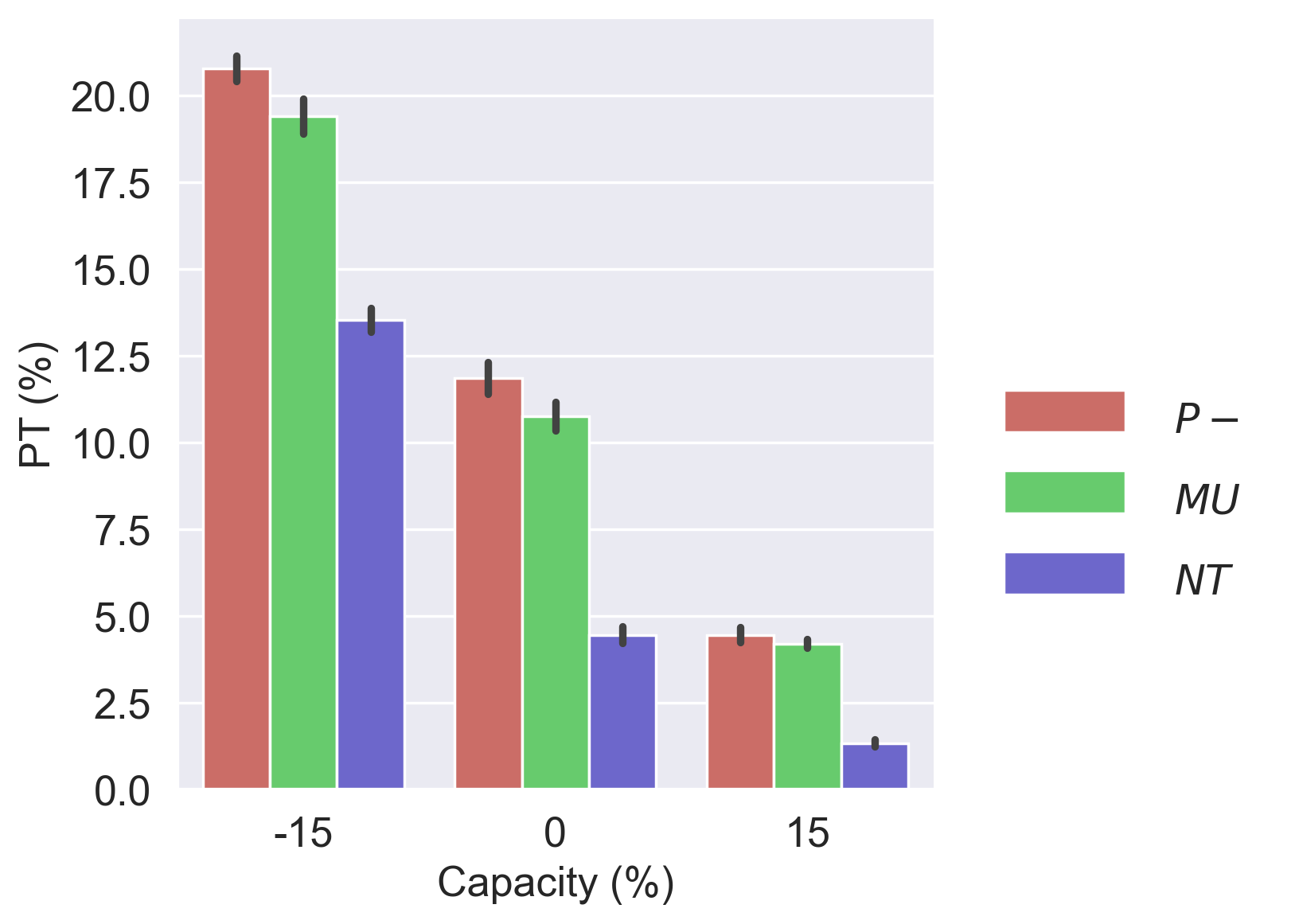

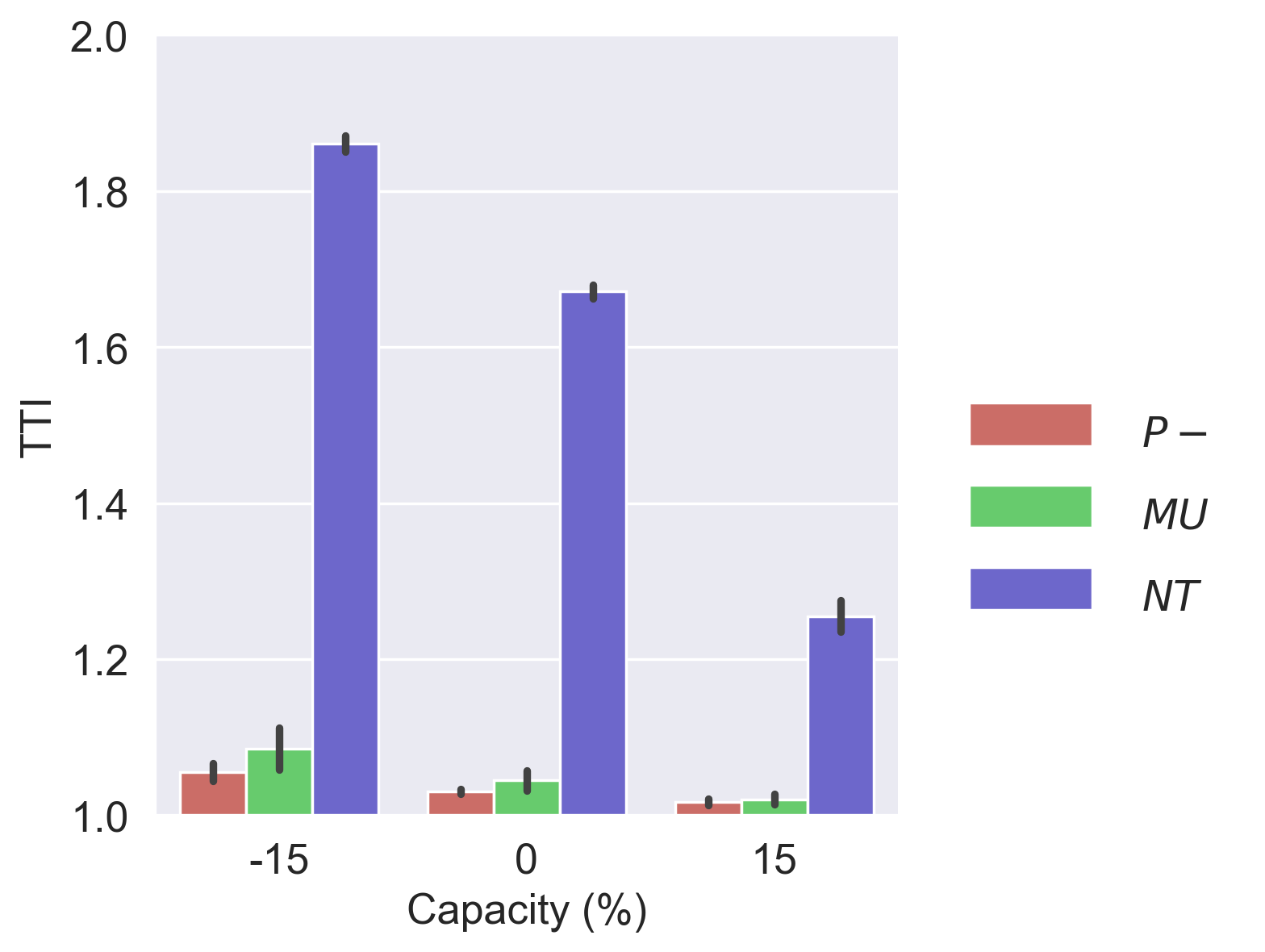

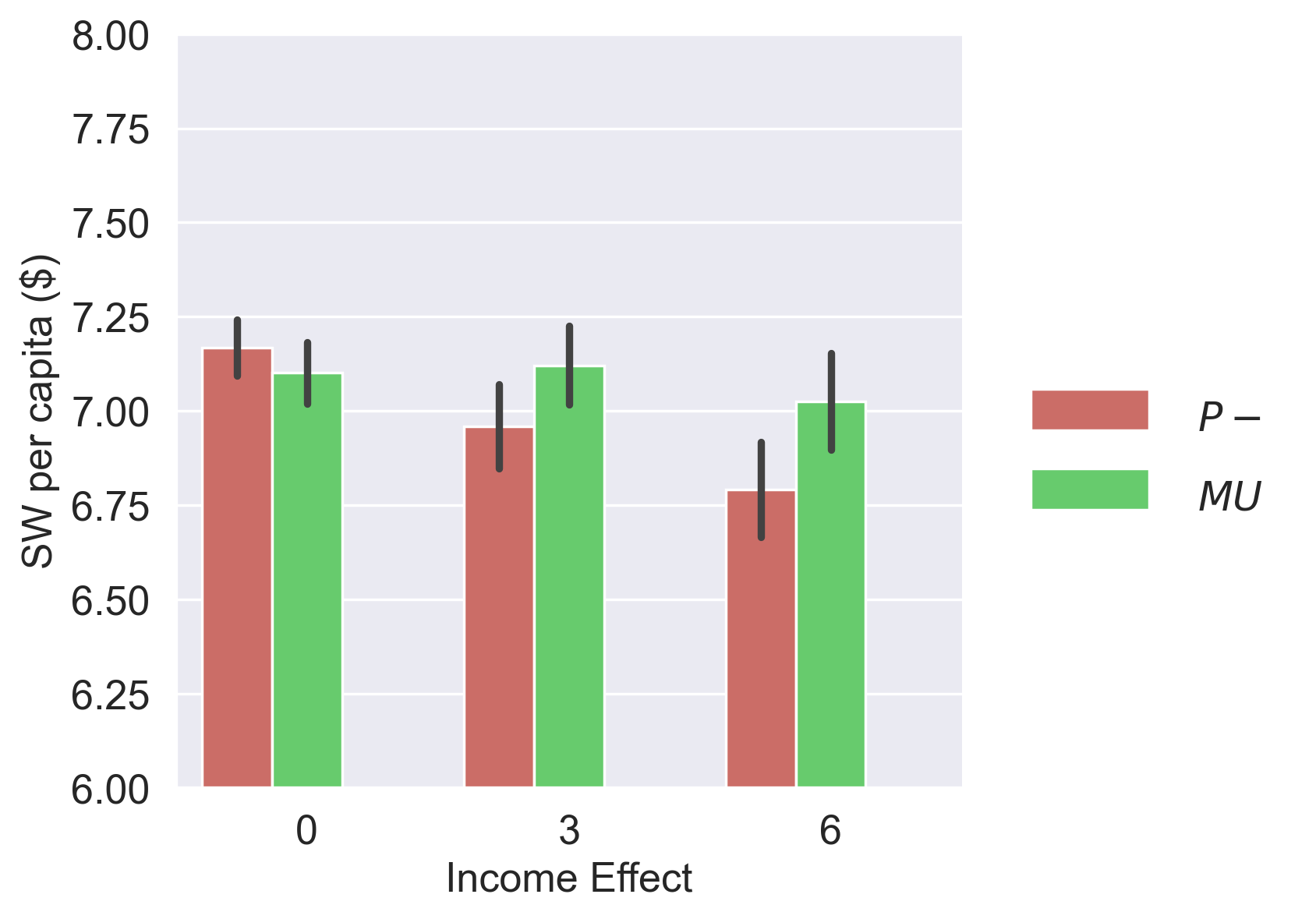

The comparative performance of the various instruments under varying levels of capacity in terms of social welfare (relative to the NT scenario), Gini coefficient, PT share and travel time index (TTI) are shown in Figure 9. First, we observe that the overall welfare of pricing and the TMC scheme are similar at all levels of capacity, and in fact, marginally higher for the TMC scheme despite the small fixed transaction fees (due to the income effect). This is in line with the general finding that both pricing and tradable credits are equivalent in terms of efficiency under deterministic demand/supply and in the absence of transaction costs and income effects (Yang and Wang [2011], de Palma et al. [2018]). As expected, overall welfare gains decrease as the capacity increases and congestion effects are less severe.

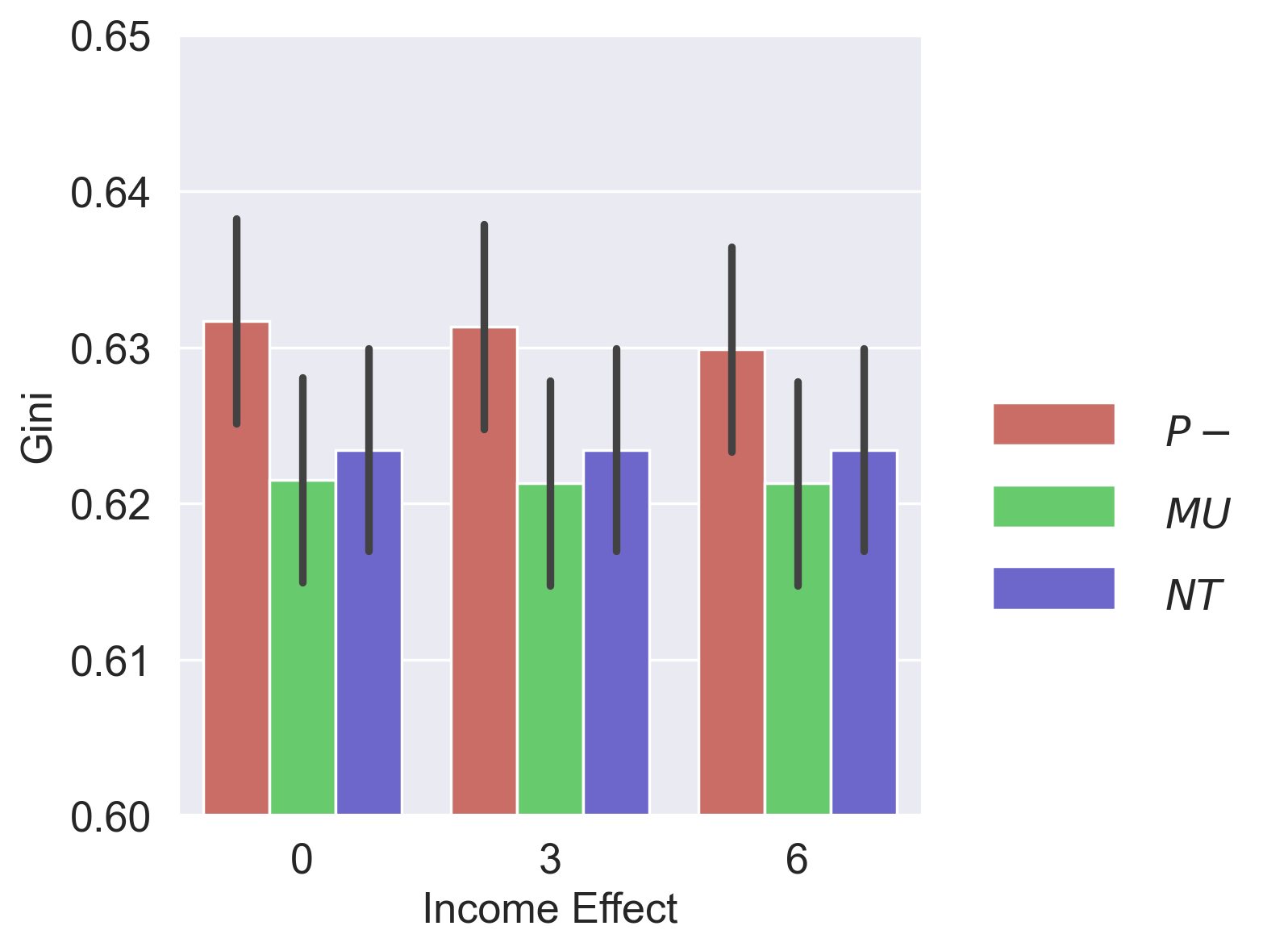

Next, Figure 9(b) shows that when toll revenues are not redistributed, the congestion pricing scheme is regressive, as seen by the increase in the Gini coefficient or GC (computed based on individual disposable income plus user benefit , see Equation 37) relative to the NT case. Observe also that the GC () increases as capacity level decreases, which implies that becomes less equitable because as capacity decreases, the tolls increase to deal with the increasing congestion leading to the greater losses of low income users.

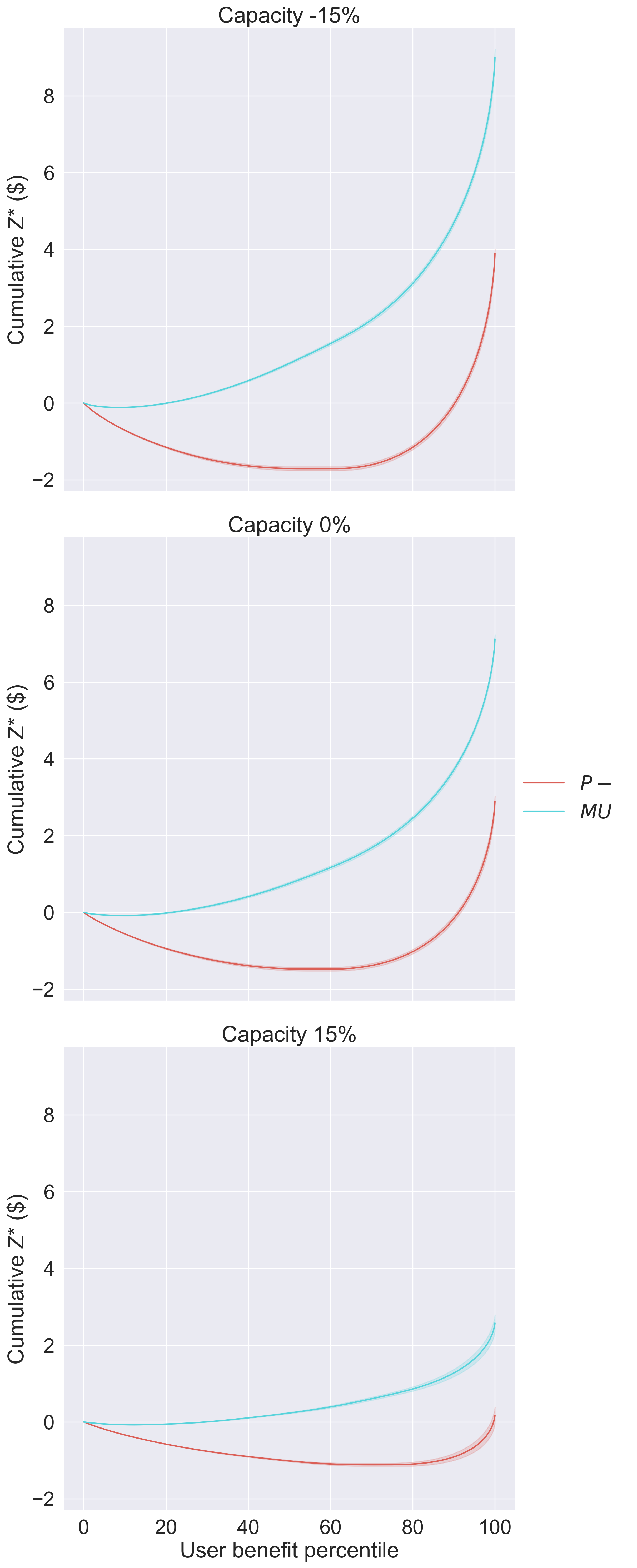

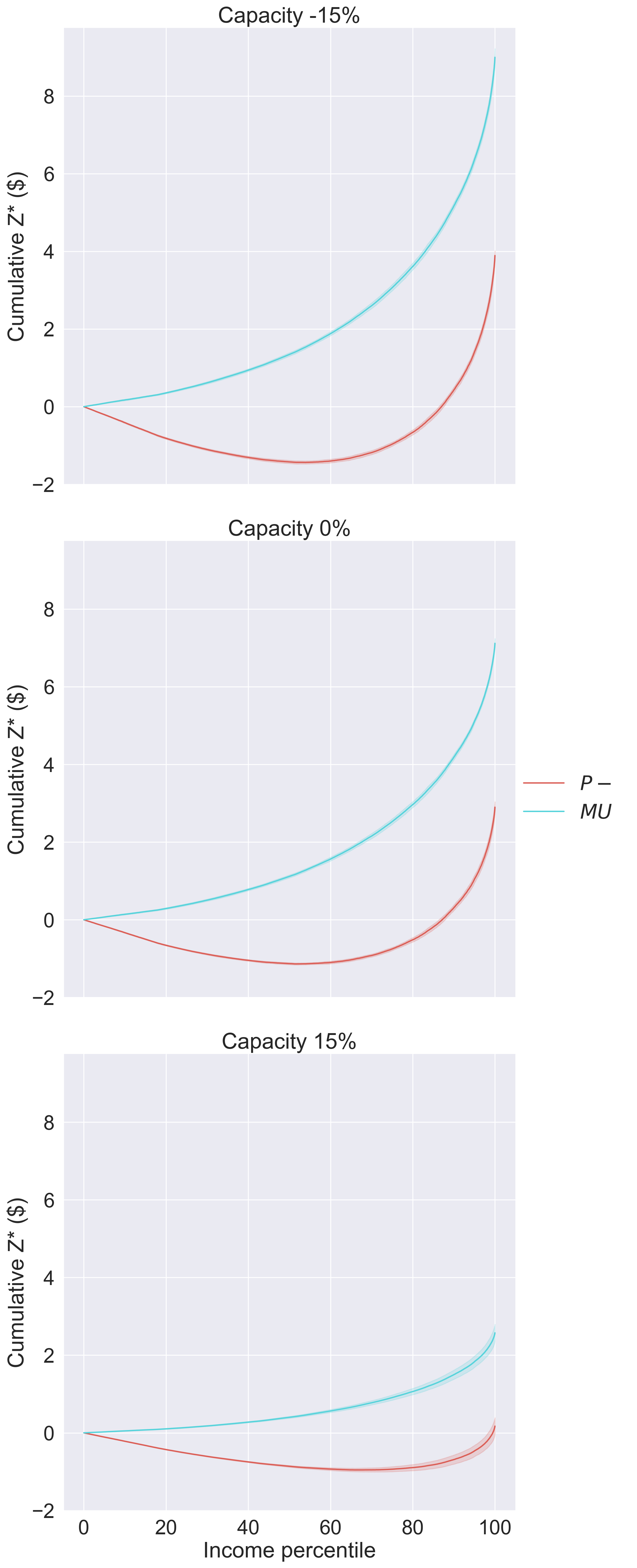

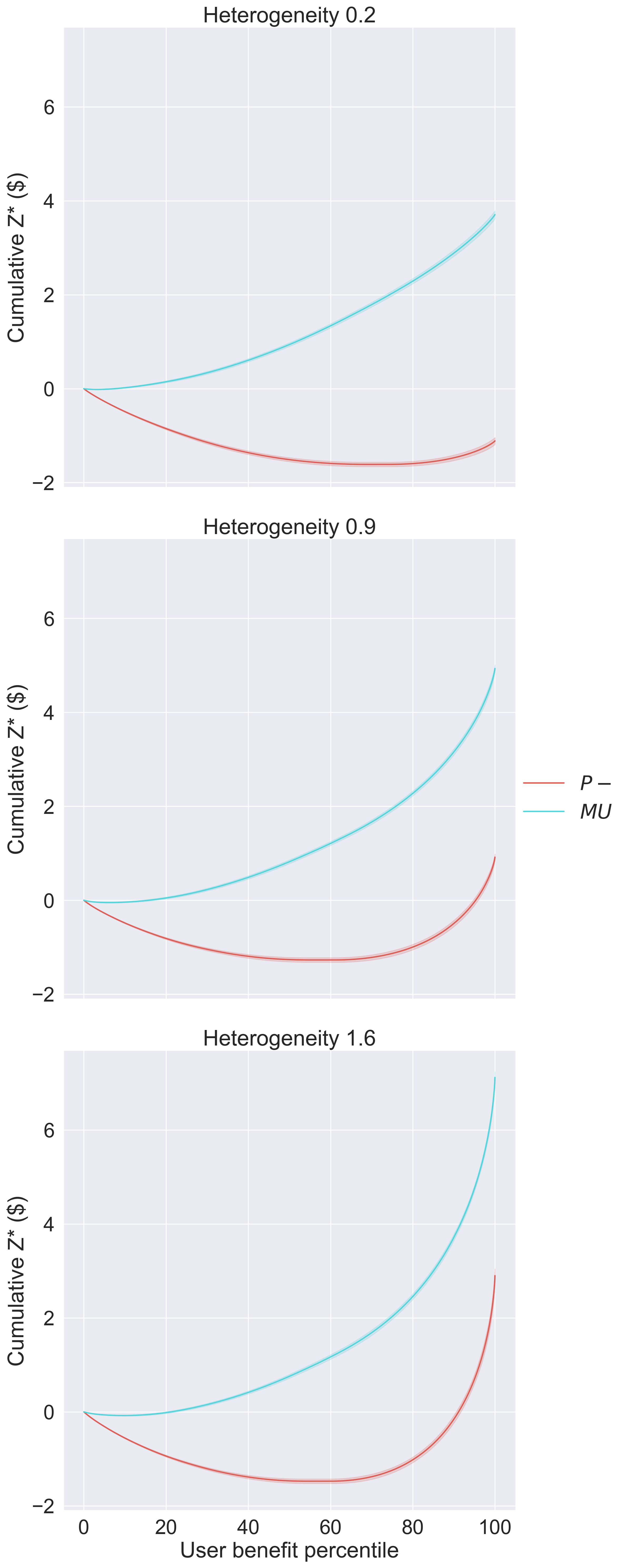

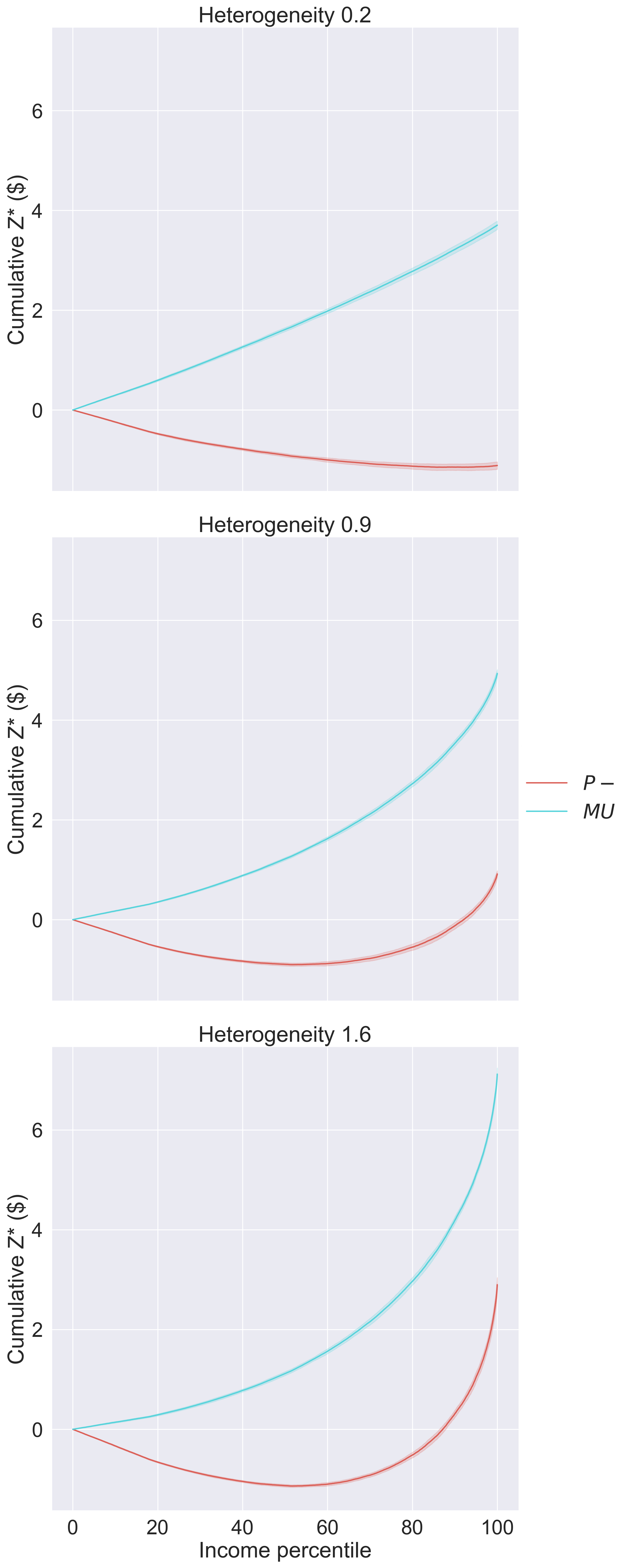

In contrast, the TMC scheme improves the GC relative to the NT case, due to the free uniform allocation of tokens to all travelers (a uniform allocation increases the proportion of cumulative benefits obtained by the travelers with lower values of time). The regressive nature of the congestion pricing scheme can also be observed in Figure 10(a) which plots cumulative user benefits (normalized by population size) as a function of the user benefit percentile and Figure 10(b) which plots cumulative user benefits (normalized by population size) as a function of income percentile. Clearly, at all capacity levels, one can observe that a large proportion of users are worse off from pricing (negative user benefits) whereas in the case of the TMC scheme the proportion of ‘losers’ is significantly smaller. Although not clearly visible in the plots, there are still some ‘losers’ with small negative benefits in the TMC scheme. Thus, under a uniform allocation of tokens, a tradable credit scheme does not necessarily guarantee Pareto improvement. This conclusion accords with the finding in Arnott et al. [1994] that under pricing, even with a uniform revenue rebate, some users may still be worse off. Fan et al. [2022] discuss the conditions under which Pareto Improvement is guaranteed for a tradable credit scheme using the standard bottleneck model with homogeneous users.

It should be pointed out that that the above discussion on the regressiveness of pricing is premised on the assumption that value of time is correlated with income and that there is a one-to-one relationship between VOT and income. Empirical studies have identified other correlates of income and hence, Verhoef and Small [2004] have cautioned against viewing the VOT distribution as simply representing the income distribution (see also Lehe [2020] on this). Moreover, as noted in Eliasson and Mattsson [2006], ultimately, the distributional outcomes of congestion pricing depend largely on how the toll revenues –which can be significantly larger than net user benefits– are used. The ratio between tolls revenues and user benefits under pricing in our experiments are in the range of the empirical values reported in Eliasson and Mattsson [2006].

6.5.2 Income Effect