Estimation of Tempered Stable Lévy Models of Infinite Variation

José E. Figueroa-López

Department of Mathematics & Statistics, Washington University in St. Louis, St. Louis, MO 63130, U.S.A. (Email: figueroa-lopez@wustl.edu). Research supported in part by the NSF Grants: DMS-2015323, DMS-1613016.Ruoting Gong

Department of Applied Mathematics, Illinois Institute of Technology, Chicago, IL 60616, U.S.A. (Email: rgong2@iit.edu).Yuchen Han

Department of Mathematics & Statistics, Washington University in St. Louis, St. Louis, MO 63130, U.S.A. (Email: y.han@wustl.edu).

Abstract

Truncated realized quadratic variations (TRQV) are among the most widely used high-frequency-based nonparametric methods to estimate the volatility of a process in the presence of jumps. Nevertheless, the truncation level is known to critically affect its performance, especially in the presence of infinite variation jumps. In this paper, we study the optimal truncation level, in the mean-square error sense, for a semiparametric tempered stable Lévy model. We obtain a novel closed-form 2nd-order approximation of the optimal threshold in a high-frequency setting. As an application, we propose a new estimation method, which combines iteratively an approximate semiparametric method of moment estimator and TRQVs with the newly found small-time approximation for the optimal threshold. The method is tested via simulations to estimate the volatility and the Blumenthal-Getoor index of a generalized CGMY model and, via a localization technique, to estimate the integrated volatility of a Heston type model with CGMY jumps. Our method is found to outperform other alternatives proposed in the literature when working with a Lévy process (i.e., the volatility is constant), or when the index of jump intensity is larger than in the presence of stochastic volatility.

MSC 2000 subject classifications: 60G51, 62M09.

Keywords and phrases: Threshold estimator, high-frequency estimation, Lévy models, method of moment estimators, optimal parameter tuning.

1 Introduction

Lévy processes have experienced a revival in the past years, propelled by the need for more realistic modeling of irregular behavior in many phenomena of nature and society. These fundamental building blocks of stochastic modeling have been widely applied in many fields, including statistical physics, meteorology, seismology, insurance, finance, and telecommunication.

While, in principle, Lévy models offer ideal conditions for estimation purposes, two main bottlenecks complicate their estimation. Firstly, their marginal distributions often lack tractable or closed-form representations. In those situations, the marginal distributions must be approximated by Fourier, Monte Carlo, or other numerical methods, which makes the estimation slower and noisier. The second issue comes from the need to handle high-frequency sampling data of the process. This type of data has been widely available in finance during the last years and is increasingly more common in other fields. The two just-mentioned issues have rendered traditional statistical methods such as likelihood and Bayesian estimation unfeasible. We refer the reader to [6] for more information about Lévy processes and their application in finance, [16] for a survey on frequentist parametric estimation of Lévy process, and [22] for more information about Bayesian estimation methods.

In this paper, we study a new method for the estimation of the parameters of a Lévy model. A semiparametric model is considered in which the jump component is assumed to exhibit small jumps that behave like those of a -stable Lévy process. Specifically, the class of tempered stable processes introduced in [8]111The term “tempered stable” is understood here in a more general sense than in several classical sources of financial mathematics (e.g., [2], [6], [15]) and even more general than in [19]. In fact, such class of Lévy processes is called thetempered-stable-like Lévy processes in [8]. and [11] is considered. We focus on models of infinite variation (i.e., ), which are arguably the most relevant for financial applications (see [1], [3], and [7]). The estimation of semiparametric Lévy models of infinite jump variation under high-frequency data is not well developed. Jacod and Todorov [13] were the first to introduce an efficient estimator of the integrated volatility of an Itô semimartingale model in the presence of a Lévy jump model of infinite variation with Blumenthal-Getoor index or when the jump component is symmetric. Their estimator is based on locally estimating the volatility from the empirical characteristic function of the increments of the process over time blocks of decreasing length. Recently, Mies [17] proposed an efficient estimation method for Lévy models based on a type of approximate semiparametric method of moments with scaling. Specifically, for some suitable moment functions and a scaling factor , [17] proposed to look for the parameters such that

(1.1)

where is the superposition of a Brownian motion and independent stable Lévy processes closely approximating in a certain sense. The distribution measure of depends on some parameters , including the volatility of , and denotes the expectation with respect to . Above, is the -th increment of a generic process given evenly spaced random samples over a fixed time interval (i.e., with ). If were assumed to follow a parametric Lévy model and we replaced with in (1.1), we will recover a standard Method of Moment Estimator (MME). However, we are assuming that is semiparametric and that it can be approximated closely enough by a parametric Lévy model . The scaling , which is taken to converge to at the order of , is also a new feature of this method compare to the standard MME.

The moment functions and the scaling factor in (1.1) critically affect the performance of the estimators. To determine an appropriate scaling , we connect it to the threshold parameter of a Truncated Realized Quadratic Variation (TRQV),

(1.2)

which is known to be a consistent estimator for the integrated volatility of a general semimartingale model. Again, above and we are assuming regular sampling observations with and . Next, note that by taking in (1.1), we recover the TRQV (1.2), which suggests the relationship . That is, plays the same role as the threshold in TRQV.

Recently, [10] studied the problem of optimal thresholding of TRQV (1.2) under the mean-square error. Specifically, in the case of a Lévy process with volatility , it is shown that the threshold that minimizes the mean-square error, , solves the equation:

where . By analyzing the small-time asymptotic behavior of (i.e., when so that ), [10] proved that the optimal threshold for a Lévy process with a -stable jump component behaves like

(1.3)

where is the time span between observations and, as usual, means as . The proportionality constant roughly tells us that the higher the jump activity is, the lower the optimal threshold has to be if we want to discard the higher noise represented by the small jumps. This fact opens the door to an iterative method to estimate . We can first estimate and using, for instance, the method of moments (1.1). We can then use the TRQV with the threshold .

In this paper, we first extend the result of [10] to allow for a general tempered stable Lévy process. Furthermore, we propose a new approximation for of the form:

(1.4)

where controls the overall intensity of jumps. The approximation (1.4) says that if is small (relative to ) then the threshold can be loosened up (in fact, as as it should be). In practice is small compare to and (1.4) provides a significant correction compare to (1.3). We then proceed to devise a new method to estimate the volatility, the index of jump activity , and by combining a variation of the approximate semiparametric method of moments in [17], TRQVs, and the approximate optimal threshold (1.4). Compared to [17] we introduce simpler moment functions , and a systematic and objective method to tune the scaling factor in (1.1). The performance of the proposed procedure is superior to the efficient methods of [13] and [17]. Finally, as in [13], we use a localization technique to estimate the integrated volatility of an Itô semimartingale. Specifically, the idea is to split the time horizon into small blocks where the process is approximately Lévy and, hence, its volatility level can be estimated using our method. For values of , our method outperforms the method proposed by [13].

The rest of this paper is organized as follows. Section 2 provides the framework and assumptions as well as some known preliminary results from the literature. Section 3 obtains the asymptotic behavior of and derives (1.3). The second-order approximation (1.4) is derived in Section 4 as well as a numerical assessment of the approximations in the case of a CGMY jump component. The new method to estimate the parameters of a tempered stable Lévy model is presented in Section 5 together with an analysis of its performance via Monte Carlo simulations. The proofs are deferred to an appendix section.

2 The Model and Some Preliminary Results

Throughout, and , and we let be a complete filtered probability space on which all stochastic processes are defined, where satisfies the usual conditions. We consider a Lévy process of the form

(2.1)

where is a Wiener process and is an independent pure-jump tempered stable Lévy process with Lévy triplet . The Lévy measure is assumed to be absolutely continuous with a density of the form

(2.2)

Here, , , and is a bounded Borel-measurable function. Concretely, we make the following assumptions on .

Assumption 2.1.

(i)

, as ;

(ii)

There exist such that

(iii)

;

(iv)

For any , ;

(v)

.

Remark 2.2.

The class of Lévy processes considered above is sometimes termed tempered stable processes (or tempered-stable-like processes as in [8]) and includes a wide range of models appearing in finance. Roughly, the conditions above amount to say that the small jumps of behave like those of a -stable Lévy process. We refer the reader to [12] for further background about this class. The parameter is called the index of jump activity and coincides with the Blumenthal-Getoor index, which controls the jump activity of in that for all and , where is the jump of at time . The range of Y considered here (namely, ) is the most relevant for financial applications based on several econometric studies of high-frequency financial data (cf. [1] and [7]) and short-term option pricing data (cf. [12]).

Using a density transformation technique in [20, Section 6.33], we can change the probability measure from to another locally absolutely continuous measure , under which is a -stable Lévy process and is a standard Brownian motion independent of . Concretely, let

Note that is the Lévy measure of a -stable Lévy process and, also,

Next, define such that, for any ,

(2.3)

By virtue of [20, Theorem 33.1], a necessary and sufficient condition for the measure transformation from to to be well defined is given by

which can be shown to follow from Assumption 2.1(i) & (ii) (cf. [12, Lemma 2.1]). Under , is a Lévy process with Lévy triplet , and is a standard Brownian motion which is independent of . In particular, under , the centered process , given by

is a strictly -stable process with its skewness, scale, and location parameters given by , , and , respectively. Let denote the marginal density of under . It is well known (cf. [20, (14.37)] and references therein) that

so that

The processes and can be expressed in terms of the jump-measure of the process and its compensator (under ), as follows:

(2.4)

(2.5)

where

The existence of the integral defining follows from Assumption 2.1(i) & (ii). Clearly, and are independent one-sided -stable processes with scale, skewness, and location parameters given by , , and , respectively, so that

Moreover, it can be shown that (cf. [9, Lemma 2.1]) there exists a universal constant , such that for any ,

(2.6)

Combining (2.5) and (2.6), we deduce that there exists a constant such that, for any ,

(2.7)

Furthermore, using (14.34) in [20] and an argument similar to that in the proof of [9, Lemma 2.1], we can show that:

(2.8)

(2.9)

where above, without loss of generality, we use the same constant as in (2.7).

3 Main Result

The TRQV, defined as

(3.1)

is one of the most commonly used estimators for the integrated volatility of an Itô semimartingale. Above, for , where are evenly spaced observations of over a fixed time horizon , so that for , with . One of its drawbacks is the necessity of tuning the threshold up, which strongly affects the performance of the estimator. It is shown in [10] that, for a Lévy process with volatility , there exists a unique threshold , which minimizes the mean-square error, . Furthermore, the minimizer is such that

(3.2)

and solves the equation

(3.3)

where . Therefore, in order to determine the asymptotic behavior of the optimal threshold , we need to study the asymptotic behavior of as both and in such a way that , as . Our main theoretical result accomplishes this for the tempered stable Lévy processes of Section 2, and its proof is deferred to Appendix A.

The following result gives the asymptotic behavior of the optimal threshold . Its proof is similar to that of [10, Proposition 2] and is outline below for completeness and also to motivate some approximation methods proposed below.

Corollary 3.2.

Under Assumption 2.1, the optimal threshold is such that

(3.4)

Furthermore, setting , we have, as ,

(3.5)

Proof.

For simplicity, we take so that . With and using the asymptotic behavior of described in Theorem 3.1, we can write (3.3) as

where h.o.t. means “higher-order terms” as . In view of (3.2) and since , we have

Dividing by , rearranging the terms, and taking logarithms of both sides, we deduce that

which can be written as

(3.6)

Dividing by and using (3.2), we obtain the first result (3.4). For the second asymptotics, note that (3.4) implies that

Finally, plugging the above in (3.6) and solving for gives the desired asymptotics.

∎

The proportionality constant of the previous result is intuitive and roughly tells us that the higher the jump activity is, the lower the optimal threshold has to be if we want to discard the higher noise represented by the jumps and to catch information about the Brownian component.

4 Other Approximations and Illustration for a CGMY Model

In this section, we introduce other approximations to the optimal threshold derived from the formulas in Theorem 3.1 and the proof of Corollary 3.2. We then illustrate their performance in the case of a Lévy process with a CGMY jump component (cf. [5]). The CGMY model is considered a prototypical jump process of infinite activity in finance. In the notation of the Lévy density (2.2), a CGMY model is given by

Thus, the conditions of Assumption 2.1 are satisfied with and .

We adopt the parameter setting

(4.1)

These values are similar to those used in [12]222[12] considers the asymmetric case with and . Here, we take in order to simplify the simulation of the model. Our values of , , and are the same as in [12]., who themselves took them from an empirical study in [14]. We take year and , which corresponds to a frequency of minute (assuming trading days and trading hours per day).

To compute , we use Monte Carlo and the change of probability measure (2.3). Concretely, under , we have the following representation:

where and are independent one-sided -stable random variables with common scale, skewness, and location parameters given by , , and , respectively. Such a distribution can be simulated efficiently333In our code, we use the R package stabledist to generate them..

We consider two different approximations of the equation (3.3) defining the optimal threshold . For the first approximation, we replace (where ) in (3.3) with its leading order terms as given by Theorem 3.1, namely,

(4.2)

For the second approximation, we take a simplified version of (3.5), only keeping those terms that are found to be significant:

(4.3)

Interestingly, as , we have , which makes sense. The approximation (4.3) says that if is small (relative to ) then the threshold can be loosened up.

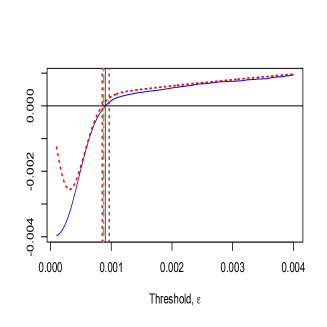

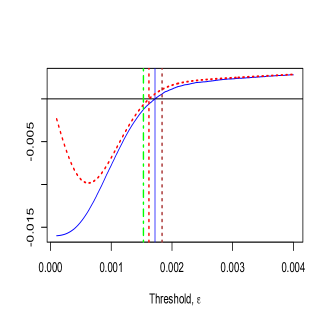

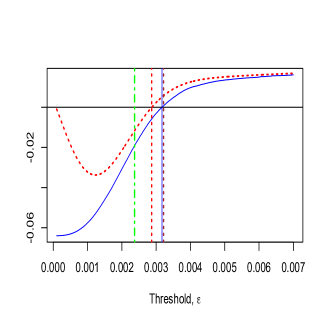

Figure 1 shows the graphs of the left-hand expressions of (3.3) (solid blue) and the approximation (4.2) (dashed red) against for three different values of : , , and . The solid blue vertical line is the “true” optimum threshold , the dotted brown vertical line shows with given as in approximation (4.3), and the dotted/dashed vertical green line is the approximation derived in (3.4) of Corollary 3.2. We also show the vertical line passing at the root of (4.2) (vertical dashed red). It is evident that for the considered values of and , the root of (4.2) and are reasonably good approximations of . However, we cannot say the same about , which is a good approximation of only for small values of and, otherwise, it underestimates .

Figure 1: Graphs of the respective left-hand expressions of (3.3) (solid blue) and (4.2) (dashed red) against for (left panel), (center panel), and (right panel), respectively. We also show the vertical lines (solid blue), (dashed red), (dotted brown), and (dotted/dashed green). The parameters for the CGMY model are set as , , , and .

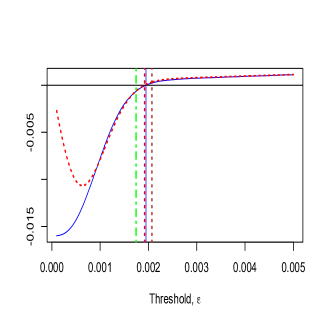

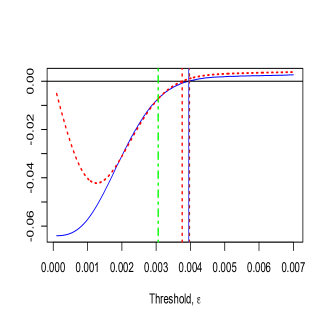

Next, we consider the value of , while all the other CGMY parameter values remain unchanged. Figure 2 below shows the graphs of the left-hand expressions of (3.3) (solid blue) and (4.2) (dashed red), against for three different values of : , , and . The Equation (4.2) derived from Theorem 3.1 is a relatively accurate approximation of (3.3), especially for larger values of . As before, the approximation (3.4) established in Corollary 3.2 is accurate for small and medium values of but not for larger values. The approximation (4.3) is reasonably accurate for all considered values of .

Figure 2: Graphs of the respective left-hand expressions of (3.3) (solid blue) and (4.2) (dashed red) against for (left panel), (center panel), and (right panel), respectively. We also show the vertical lines (solid blue), (dashed red), (dotted brown), and (dotted/dashed green). The parameters for the CGMY model are set as , , , and .

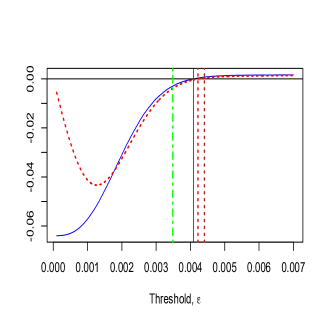

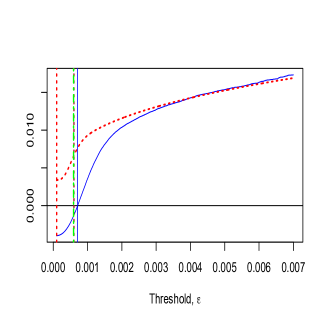

Finally, we consider the value of . All the other CGMY parameter values remain the same. The approximations are shown in Figure 3. We deduce that for such a large value of , the approximation (4.2) derived from Theorem 3.1 is not accurate anymore, though it improves as gets larger. On the other hand, the other suggested approximation (4.3) is still relatively accurate to approximate the optimal threshold (the root of (3.3)). We again have that for small and medium values of , the approximation (3.4) is good, which is not the case for large values of .

Figure 3: Graphs of the respective left-hand expressions of (3.3) (solid blue) and (4.2) (dashed red) against for (left panel), (center panel), and (right panel), respectively. We also show the vertical lines (solid blue), (dashed red), (dotted brown), and (dotted/dashed green). The parameters of the CGMY model are set as , , , and .

To summarize, while for values of , the approximation (4.2) may be the most accurate, this is not the case anymore for larger values of . On the other hand, the approximation (4.3) is reasonably good for a large range of values of . Due to this reason, in our simulations of Section 5, we use (4.3) to assess the finite sample performance of the proposed estimation method below.

5 A New Method To Estimate The Volatility

In this section, we propose a new method for estimating the volatility and other parameters of a tempered-stable Lévy process using the TRQV (3.1) and the approximations of the optimal threshold derived in Section 3. Then, we illustrate the method in the case of a CGMY Lévy process. Finally, using a localization technique, we adapt our method to estimate the integrated variance under a Heston stochastic volatility model with CGMY jumps and compare it to the method proposed by [13], which is known to be efficient when .

5.1 Estimation of Stable-Like Lévy Measures

As shown by (3.3) and the asymptotic expansion of Theorem 3.1, the optimal threshold depends on the volatility, and vice versa. It is then natural to consider an iterative method to estimate . But before this, we need to estimate and . Several methods have been proposed in the literature for this purpose (see, e.g., [1], [4], and [18]). Mies [17] recently proposed an efficient method using the method of moments. In this part, we adapt and modify this method and apply it in combination with the approximations of Theorem 3.1 to estimate the optimal threshold of the TRQV and subsequently the other parameters , , and .

Consider a Lévy process with characteristic triplet . The approach of [17] builds on the assumption that can be well approximated by the superposition of stable Lévy measures in the sense that

(5.1)

(5.2)

for some , where is given by

(5.3)

for some , , and such that

for some . We want to estimate given observations, , of the process at known times . As before, we assume the sampling times are evenly spaced and we done the time step between observations as . Conditions (5.1), (5.2), and (5.3) essentially say that we can approximate by a fully specified Lévy process with characteristic triplet and, hence, with the decomposition

where is a standard Brownian motion and , , are independent -stable processes, independent of , each with Lévy density , respectively.

Mies [17] proposed to estimate the parameters, , of the approximating process using the method of moments. We now proceed to briefly review her method. The first step is to choose moment functions , one for each parameters of , and a suitable scaling factor , where “” hereafter means “proportional to”. Next, define the MME to be a solution of the following equation

(5.4)

where and denotes the expectation such that is determined by the parameter vector . Since is fully specified and, thus, its characteristic function is available, can be computed by, e.g., Fourier methods.

Our idea is to combine a version of Mies’ method with our results in Section 3 to improve our estimation of and . Concretely, we propose to first find the roots of and plug them into a suitable approximation of Equation (3.3) to obtain an estimate of the optimal threshold . This can in turn be used to estimate the volatility via thresholding. To solve the equations (5.4), we propose to solve an optimization problem with objective function of the form

(5.5)

where

This particular weights are motivated by the scaling of the Central Limit Theorem for established in [17, Lemma 5.4].

For simplicity, suppose we only want to estimate , , and (the method can easily be adapted to estimate more parameters of ). We then propose the following procedure:

1.

Start with some initial values and a suitable scaling factor (to be specified later on).

2.

Find the roots of , which we call , by minimizing the objective function in (5.5).

3.

Using , we solve a suitable approximation of (3.3) (e.g., (4.2) or (4.3)) to get an estimation of the optimal threshold , denoted by . This estimate is then used to compute an estimate of as

4.

Fix and use moment functions to find

by solving

(5.6)

or minimizing

(5.7)

5.

Using and solving the same approximating equation as in Step 3, we obtain a new estimation of , denoted by , and update by

Remark 5.1.

We could stop right after Step 3 and make our final estimate of the volatility. However, our simulation results show that Step 4 significantly improves our estimates of when . We could also follow the Steps 15 and repeat Steps 4 and 5 iteratively by letting until the sequence of estimates stabilizes. This approach, however, tends to increase the sample error of the estimators. In the steps 2 and 4 above, there is no guarantee that the roots therein exist in a finite sample setting. This is another reason to use the minimum (or local minimum) of and instead of solving (5.4) and (5.6), respectively.

5.2 Estimation of a Lévy Process with CGMY Jump Component

In this subsection, we apply the method introduced in the previous subsection to the case of a CGMY jump component and compare it to the estimators of Mies [17] and Jacod and Todorov [13]. Specifically, we work with simulated data from the model (2.1) where , is a pure-jump CGMY Lévy process, independent of the Brownian motion , with Lévy measure

We use the same values of , , and as in (4.1), but with different values of and . We consider observations of a minutes frequency over a one-year ( days) time horizon with a trading time of hours per day (so that ). It should be clarified that we are indeed in the same setting as that of Subsection 5.1 since, as , . This suggests us to take in (5.3) and to use a -stable process to approximate the CGMY process because only the parameters , , and are of primary interest. Then Assumptions (5.1)(5.3) are satisfied with and , , where is a -stable process with Lévy measure . The parameters of the approximating model are .

Next, we choose the moment functions as

(5.8)

and a suitable scaling factor to be specified below. These functions are simpler than the ones proposed in [17, Section 4] and were chosen because of their superior performance. Even though the moment functions (5.8) do not meet the strict constraints imposed in [17] (see Assumptions (F1)(F2) therein), we believe that most of the assumptions therein are not needed for the validity of the asymptotic theory in [17]. This will be investigated in a future work together with an objective and systematic method to calibrate the moment functions.

To determine a suitable scaling factor , we will connect it to the threshold parameter of the TRQV estimator (3.1). The key observation is to analyze the moment equation corresponding to the function , namely,

which, after some trivial simplifications, can be written as

This suggests that has a similar role to that of the threshold in the TRQV estimator; namely, the choice of should ensure that is dominated by the Brownian component or, equivalently, to eliminate the increments in which the jump component of dominates the Brownian component. Hence, in what follows, we will fix as , where and is a suitable initial estimate of . We consider the following initial values for :

(5.9)

where

Broadly, we recommend to use the loose estimator as our initial value if the volatility is “large” (say, 0.4 or larger), and, otherwise, use the tighter estimator .

For the moment functions in Step 4 of the algorithm in Subsection 5.1 (the ones used to correct estimates of and while fixing that of ), we choose

(5.10)

Finally, we use the approximation (4.3) in Steps 3 and 5 of the algorithm outlined in Subsection 5.1. For clarity and easy reference, we outline below the precise estimation procedure for the case of the CGMY model.

1.

Start with some initial guesses . Here we take , , and when or when , as defined in (5.9). Given , we fix the scaling factor .

2.

Find the roots of with the moment functions in (5.8), which we call , by minimizing the objective function in (5.5).

3.

Using , we apply the second-order approximation (4.3) to get an estimate of , denoted by , and compute its corresponding TRQV estimator .

4.

Fix and then use the moment functions in (5.10) with to get the estimates by solving the roots of in (5.6) or minimizing in (5.7)444In Steps 2 and 4, we choose the minimization method. We use the R function nloptr from the package nloptr with the algorithm NLOPT__LD__LBFGS.

5.

Using , we again apply (4.3) to get a new estimate of , denoted by . This threshold is plugged into the TRQV estimator to compute a final estimation of , denoted by .

We compare the simulated performance of our estimator to the estimator (which could be considered the plain estimator proposed by [17]) and the estimator in [13]. In the latter one, we use the equation (5.3) therein with and , which is reasonable since the volatility is constant and there is no need to localize the estimator (so we only need one block). We take the scaling factor , as proposed in the simulation portion of [17], and for the term of equation (5.3) in [13]. [13] suggests to use and , where is the bipower variation, which we also tried in our simulation, but obtained worst results. In fact, we tried different parameters settings for , , , and , and select the values with the best performance. In each simulation, we divided the one-year data into months and compute the estimate of for each month, and then take the average of these monthly estimators as .

The results are summarized in Tables 16 for different parameter settings. The tables report the sample means, standard deviations (SDs), sample mean and SD of relative errors, and MSEs for different parameter settings based on simulations. We also report the TRQV estimator, denoted by , using the threshold given in (4.3) with the true values of , , and . Finally, we also report the TRQV estimator, denoted by , corresponding to the true optimal threshold obtained by solving (3.3) after finding via a large scale Monte Carlo experiment.

Tables 13 show that, when , the MSEs of , , , and are getting smaller in each step. The MSE of is about , , and lower than the MSE of , for , respectively, while this is , , and lower than the MSE of , for , respectively. Similarly, as shown in Tables 46, when , the MSEs of , , , and are also getting smaller in each step. The MSE of is about , , and lower than the MSE of , for , respectively. The MSE of are , , and lower than the MSE of , for , respectively. So the iterative method has a good performance and significantly improves the MSEs of the estimators and . Regarding the estimates of and , we notice that the second step estimates and (obtained from fixing and then applying (5.6)) are significantly better than the first step estimates and when . When , there is no significant improvement.

Sample Mean

Sample SD

Mean of

Relative Error

SD of

Relative Error

MSE

0.083128

0.001101

1.078190

0.027526

1.8612E-03

0.045788

0.001450

0.144696

0.036257

3.5602E-05

0.038116

0.008910

0.361281

0.318223

1.8172E-04

1.649710

0.028049

-0.029582

0.016499

3.3158E-03

0.003361

0.000105

0.053750

0.032827

4.0365E-08

0.043465

0.002063

0.086634

0.051572

1.6264E-05

0.039492

0.009402

0.410411

0.335795

2.2046E-04

1.649803

0.030043

-0.029528

0.017672

3.4224E-03

0.003219

0.000122

0.009143

0.038203

1.5703E-08

0.040622

0.002467

0.015561

0.061681

6.4747E-06

0.060648

0.003161

0.516191

0.079013

4.3631E-04

0.037780

0.000326

-0.055490

0.008160

5.0331E-06

0.040061

0.000350

0.001528

0.008747

1.2615E-07

Table 1: Estimation based on simulated -minute observations of paths over a one-year time horizon. The parameters are , , and . We take . In this case, we compute and .

Sample Mean

Sample SD

Mean of

Relative Error

SD of

Relative Error

MSE

0.048487

0.000569

0.212166

0.014213

7.2347E-05

0.034272

0.001892

-0.143197

0.047310

3.6390E-05

0.009674

0.004040

-0.654512

0.144291

3.5218E-04

1.718718

0.052867

0.145812

0.035245

5.0632E-02

0.003300

0.000184

-0.122242

0.048974

2.4517E-07

0.036122

0.002019

-0.096961

0.050470

1.9118E-05

0.018535

0.009119

-0.338043

0.325676

1.7275E-04

1.618217

0.071105

0.078811

0.047403

1.9031E-02

0.003470

0.000206

-0.077027

0.054674

1.2614E-07

0.037833

0.001989

-0.054178

0.049722

8.6521E-06

0.043206

0.001006

0.080159

0.025152

1.1293E-05

0.041920

0.000393

0.048008

0.009837

3.8424E-06

0.040460

0.000371

0.011491

0.009284

3.4918E-07

Table 2: Estimation based on simulated -minute observations of paths over a one-year time horizon. The parameters are , , and . We take . In this case, we compute and .

Sample Mean

Sample SD

Mean of

Relative Error

SD of

Relative Error

MSE

0.042889

0.000460

0.072221

0.011491

8.5567E-06

0.039098

0.001497

-0.022549

0.037431

3.0552E-06

0.006717

0.004401

-0.760116

0.157188

4.7235E-04

1.620586

0.059843

0.200434

0.044328

7.6798E-02

0.004171

0.000238

-0.013883

0.056241

6.0045E-08

0.039907

0.000981

-0.002313

0.024514

9.7007E-07

0.049001

0.031537

0.750027

1.126331

1.4356E-03

1.285035

0.105981

-0.048123

0.078504

1.5452E-02

0.004374

0.000181

0.034146

0.042847

5.3710E-08

0.040596

0.000718

0.014911

0.017949

8.7122E-07

0.040842

0.000634

0.021061

0.015858

1.1121E-06

0.040789

0.000389

0.019736

0.009719

7.7435E-07

0.040235

0.000378

0.005870

0.009440

1.9770E-07

Table 3: Estimation based on simulated -minute observations of paths over a one-year time horizon. The parameters are , , and . We take . In this case, we compute and .

Sample Mean

Sample SD

Mean of

Relative Error

SD of

Relative Error

MSE

0.233102

0.003657

0.456887

0.022855

5.3573E-03

0.164513

0.003573

0.028205

0.022332

3.3133E-05

0.044023

0.010945

0.572264

0.390893

3.7654E-04

1.641484

0.029400

-0.034421

0.017294

4.2884E-03

0.007081

0.000133

0.004358

0.018910

1.8717E-08

0.162042

0.003665

0.012764

0.022907

1.7603E-05

0.051271

0.009833

0.831099

0.351195

6.3823E-04

1.619172

0.022776

-0.047546

0.013397

7.0519E-03

0.007028

0.000167

-0.003155

0.023635

2.8259E-08

0.160897

0.004536

0.005605

0.028350

2.1380E-05

0.177376

0.017487

0.108603

0.109294

6.0774E-04

0.159377

0.001432

-0.003894

0.008947

2.4375E-06

0.161471

0.001461

0.009193

0.009133

4.2992E-06

Table 4: Estimation based on simulated -minute observations of paths over a one-year time horizon. The parameters are , , and . We take . In this case, we compute and .

Sample Mean

Sample SD

Mean of

Relative Error

SD of

Relative Error

MSE

0.184729

0.002771

0.154558

0.017316

6.1921E-04

0.150140

0.005615

-0.061628

0.035094

1.2876E-04

0.010208

0.004122

-0.635430

0.147228

3.3355E-04

1.750480

0.033385

0.166986

0.022257

6.3855E-02

0.007357

0.000442

-0.124190

0.052650

1.2838E-06

0.150856

0.004893

-0.057151

0.030584

1.0756E-04

0.021081

0.004636

-0.247106

0.165562

6.9362E-05

1.635476

0.038174

0.090317

0.025449

1.9811E-02

0.007556

0.000369

-0.100445

0.043904

8.4791E-07

0.153194

0.004645

-0.042537

0.029031

6.7897E-05

0.161593

0.008238

0.009958

0.051485

7.0396E-05

0.161458

0.001550

0.009112

0.009684

4.5267E-06

0.161165

0.001548

0.007280

0.009678

3.7547E-06

Table 5: Estimation based on simulated -minute observations of paths over a one-year time horizon. The parameters are , , and . We take . In this case, we compute and .

Sample Mean

Sample SD

Mean of

Relative Error

SD of

Relative Error

MSE

0.172473

0.002347

0.077956

0.014667

1.6108E-04

0.154598

0.007496

-0.033763

0.046851

8.5376E-05

0.003444

0.002236

-0.877006

0.079863

6.0801E-04

1.762248

0.118304

0.305369

0.087633

1.8394E-01

0.008141

0.000684

-0.120849

0.073887

1.7204E-06

0.154037

0.004898

-0.037268

0.030615

5.9550E-05

0.016458

0.010854

-0.412220

0.387637

2.5103E-04

1.523080

0.171764

0.128208

0.127233

5.9460E-02

0.007751

0.002270

-0.162936

0.245181

7.4310E-06

0.156800

0.005165

-0.020002

0.032280

3.6916E-05

0.158787

0.009349

-0.007584

0.058430

8.8874E-05

0.160665

0.001567

0.004155

0.009797

2.8988E-06

0.160439

0.001562

0.002746

0.009763

2.6332E-06

Table 6: Estimation performance based on simulated -minute observations of paths over a one-year time horizon. The parameters are , , and . We take . In this case, we compute and .

5.3 Integrated Variance Estimation for a Stochastic Volatility Model with Jumps

In this subsection, we apply the method in the previous subsection to estimate the integrated variance under a stochastic volatility model with a CGMY jump component. We also examine the finite sample performance of the resulting estimator and compare it with the estimator of Jacod and Todorov [13]. The basic idea is to split the time-period into smaller subintervals so that would be approximately constant in each subinterval and, hence, is approximately Lévy within that interval. We then apply the method developed in Subsection 5.1 to each subinterval to estimate the volatility level in each subinterval and finally aggregate the resulting estimates to estimate the integrated volatility.

Specifically, we consider the following Heston model:

where and are two independent standard Brownian motions and is a CGMY Lévy process independent of and . The parameters of the volatility specification are set as

The values of and above are borrowed from [23]. In the simulation, we experiment with values of and , and compute the estimated integrated volatility for one day under two different estimators.

We consider -second observations over a one-year ( days) time horizon with trading hours per day. We set , which corresponds to blocks per day. As mentioned above, we treat the stochastic volatility as a constant volatility in each block, so that we can estimate the integrated volatility for each block by computing our estimator with all the estimation parameters specified as in Subsection 5.2. We then add the integrated volatilities for the blocks to compute our daily estimator of the integrated volatility for that day. For the estimator of [13], we use both equations (4.2) and (5.3) therein with (number of observation in each block), , and , where is the bipower variation of the previous day. To assess the accuracy of the different methods, we compute the Median Absolute Deviation (MAD) around the true value, , over simulation paths.

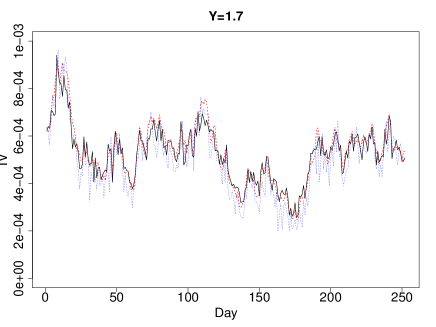

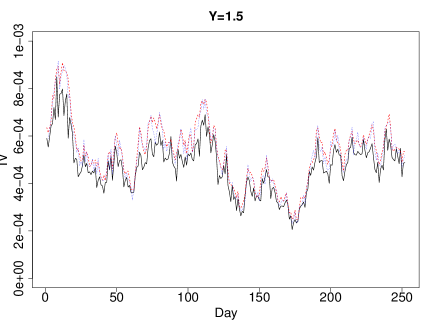

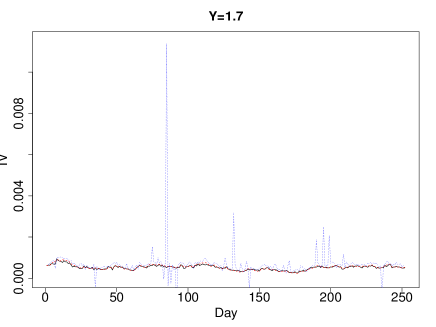

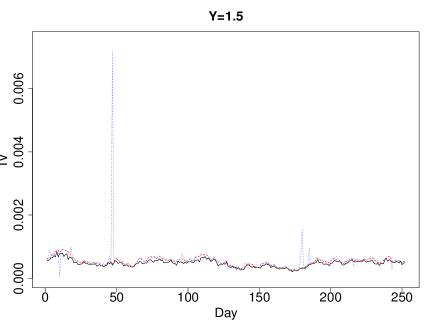

Figure 4 shows the estimated integrated volatility for each day computed by our MME (solid black line) and the JT estimator in [13] (dotted blue line) (see Eq. (5.3) therein), and the true daily integrated volatility (dashed red) for simulation path. When , the JT estimator tends to jitter around the true value, while our MME exhibits better performance. This behavior is further corroborated by Table 7, which shows the MADs of both our MME and JT estimator for different days based on simulated paths. However, when , the JT estimator outperforms our MME, as shown in the right panel of Figure 4 and Table 7. Now, it is important to point out that the daily estimate (5.3) of [13] is based on more data than that used in our estimates. Indeed, the estimator (5.3) in [13] employs a debiasing procedure, whose debiasing term consists of two components: one that can be computed using the data in each day and another term, depending only on , that is computed using the data during the whole time horizon (in this case, one year worth of data). To explore the performance of the estimator using only contemporary data, we also analyze the performance of the estimator (4.2) in [13], which can be computed using only the data collected in each day. When (left panel of Figure 5), the daily estimated integrated volatility (4.2) in [13] overestimates the true integrated volatility, and produces extremely large or small estimates at some points. We also observe this behavior when (right panel of Figure 5), but the estimate is much more stable and outperforms our MME most of the time, as shown in Table 7. To summarize, when is large, our approach performs fairly well for the stochastic volatility model.

Figure 4: Graphs of the daily integrated volatility estimates for (left panel) and (right panel), respectively. The dashed red line is the true daily integrated volatility, while the solid black (respectively, dotted blue) line shows the daily estimates using our MME (respectively, (5.3) in [13]).

Figure 5: Graphs of the daily integrated volatility estimates for (left panel) and (right panel), respectively. The dashed red line is the true daily integrated volatility, while the solid black (respectively, dotted blue) line shows the daily estimates using our MME (respectively, (4.2) in [13]).

Method

Day 2

Day 52

Day 102

Day 152

Day 202

Day 252

MAD.MME

2.4498E-05

3.7819E-05

3.4568E-05

3.7059E-05

3.7501E-05

2.7117E-05

MAD.JT (4.2)

1.0087E-04

9.6535E-05

1.1127E-04

1.0820E-04

1.0253E-04

1.0623E-04

MAD.JT (5.3)

5.0516E-05

4.6288E-05

4.7421E-05

4.9100E-05

5.2230E-05

4.3879E-05

MAD.MME

6.8551E-05

6.6529E-05

5.6600E-05

6.4519E-05

6.3395E-05

6.2592E-05

MAD.JT (4.2)

1.9978E-05

1.9429E-05

1.8714E-05

1.7270E-05

2.0778E-05

2.2255E-05

MAD.JT (5.3)

1.3410E-05

1.1542E-05

1.0880E-05

9.5053E-06

1.6174E-05

1.4615E-05

Table 7: The MADs for our MME and the estimators in [13] for arbitrary sampled days. The results are based on simulated -second observations of paths over a one-year time horizon with and , respectively.

Acknowledgements

The authors are grateful to the Editor and two anonymous referees for their multiple suggestions that help to improve the original manuscript.

By conditioning on and using the fact that , for all , we have that

(A.8)

Let be the density of under , and recall the Fourier transform and its inverse transform defined by

In what follows, we set

(A.9)

(A.10)

Then, we deduce that

where

(A.11)

(A.12)

with and . Hence, we have

(A.13)

(A.14)

(A.15)

(A.16)

(A.17)

By expanding the Taylor series for , as well as for and , we deduce that

(A.18)

(A.19)

(A.20)

where, for and ,

(A.21)

(A.22)

By applying the formula for the integrals of and with respect to on , as well as the asymptotics for the Kummer’s function , as , we deduce that

and that

In the asymptotic formulas for the Kummers function in the expression of above, the first term vanishes if are infinity. This happens when is a nonpositive integer. Similarly, in the asymptotic formulas for the Kummers function in , the first term vanishes if is a nonpositive integer. Hence, for and , as ,

(A.23)

(A.24)

Therefore, by combining (A.20), (A.23), and (A.24), we obtain that

The asymptotics of the last term above follows from (A.13) and (A.25), namely

(A.30)

(A.31)

For the first term in (A.29), by expanding the Taylor series for , as well as for and below, and using (A.21) and (A.22), we have

(A.32)

(A.33)

(A.34)

(A.35)

(A.36)

(A.37)

as , where we have used the asymptotic formulas (A.23) and (A.24) in the last equality. Finally, for the second term in (A.29), again by expanding the Taylor series for , , and below, and using (A.21), (A.22), (A.23), and (A.24), we deduce that

(A.38)

(A.39)

(A.40)

(A.41)

(A.42)

(A.43)

as . Therefore, by combining (A.29), (A.31), (A.37), and (A.43), we obtain that

(A.44)

It remains to analyze the asymptotic behavior of . We first note that there exists a universal constant , such that

(A.45)

(A.46)

where the last inequality above follows from (A.25). Moreover, by (2.7), as ,

(A.47)

(A.48)

(A.49)

(A.50)

Therefore, by combining (A.46) and (A.50), we obtain that

(A.51)

Finally, by combining (A.7), (A.8), (A.25), (A.44), and (A.51), we conclude that

(A.52)

Step 1.2. We now study the asymptotic behavior of , defined in (A.6), as . Let us first consider the following decomposition

(A.53)

(A.54)

The first term can be bounded as follows: as ,

(A.55)

To deal with , for any , we further decompose as

where the first integral is well-defined in light of Assumption 2.1-(i) & (ii), so that

For the first term , note that

where the last integral is finite since in a neighborhood of the origin,

which is integrable with respect to in view of Assumption 2.1-(ii). As for the terms , due to the self-similarity of and the fact that (since ), the monotone convergence theorem implies that , as . Hence, we obtain that

(A.56)

By combining (A.54), (A.55), and (A.56), we conclude that

(A.57)

Finally, from (A.6), (A.52), and (A.57), we obtain that

(A.58)

as , which completes the analysis in Step 1.

Step 2. In this step, we will study the asymptotic behavior of the second term in (A.2), as . By (2.3), (2.4), and (2.5), we first have

(A.59)

(A.60)

(A.61)

(A.62)

Clearly,

(A.63)

It remains to analyze the asymptotic behavior of the first two terms in (A.62).

Step 2.1. We begin with the analysis of . Clearly,

(A.64)

(A.65)

(A.66)

By the symmetry of , we note that

In what follows, we let small enough so that .

To study the asymptotic behavior of , as , let us first consider

As for , by Cauchy-Schwarz inequality, (2.5), (A.66), (A.87), and (A.89), we obtain that

(A.105)

(A.106)

(A.107)

Therefore, by combining (A.103), (A.104), and (A.107), we obtain that, as ,

(A.108)

which completes the analysis in Step 3.

Finally, by combining (A.2), (A.58), (A.100), and (A.108), we conclude that, as ,

(A.109)

which completes the proof of the theorem.

References

[1]

Y. Aït-Sahalia and J. Jacod.

Estimating the Degree of Activity of Jumps in High Frequency Data.

Ann. Stat., 37(5A):22022244, 2009.

[2]

D. Applebaum.

Lévy Processes and Stochastic Calculus, 2nd Ed..

Cambridge Stud. Adv. Math., 116, Cambridge University Press, Cambridge, U.K., 2004.

[3]

D. Belomestny.

Spectral Estimation of the Fractional Order of a Lévy Process.

Ann. Stat., 38(1):317351, 2010.

[4]

A. D. Bull.

Near-Optimal Estimation of Jump Activity in Semimartingales.

Ann. Stat., 44(1):5886, 2016.

[5]

P. Carr, H. Geman, D. B. Madan, and M. Yor.

The Fine Structure of Asset Returns: An Empirical Investigation.

J. Bus., 75(2):305332, 2002.

[6]

R. Cont and P. Tankov.

Financial Modelling with Jump Processes.

Chapman & Hall/CRC Financ. Math. Ser., Chapman & Hall/CRC, Boca Raton, FL, U.S.A., 2004.

[7]

J. E. Figueroa-López.

Statistical Estimation of Lévy-Type Stochastic Volatility Models.

Ann. Finance, 8(2):309335, 2012.

[8]

J. E. Figueroa-López, R. Gong, and C. Houdré.

High-Order Short-Time Expansions for ATM Option Prices of Exponential Lévy Models.

Math. Financ., 26(3):516557, 2016.

[9]

J. E. Figueroa-López, R. Gong, and C. Houdré.

Third-Order Short-Time Expansions for Close-to-the-Money Option Prices under the CGMY Model.

Appl. Math. Financ., 24(6):547574, 2017.

[10]

J. E. Figueroa-López and C. Mancini.

Optimum Thresholding Using Mean and Conditional Mean Square Error.

J. Econom., 208(1):179210, 2019.

[11]

J. E. Figueroa-López and S. Ólafsson.

Short-Time Expansions for Close-to-the-Money Options under a Lévy Jump Model with Stochastic Volatility.

Financ. Stoch., 20(1):219265, 2016.

[12]

J. E. Figueroa-López and S. Ólafsson.

Short-Time Asymptotics for the Implied Volatility Skew under a Stochastic Volatility Model with Lévy Jumps.

Financ. Stoch., 20(4):9731020, 2016.

[13]

J. Jacod and V. Todorov.

Efficient Estimation of Integrated Volatility in Presence of Infinite Variation Jumps.

Ann. Stat., 42(3):10291069, 2014.

[14]

R. Kawai.

On Sequential Calibration for an Asset Price Model with Piecewise Lévy Processes.

IAENG Int. J. Appl. Math., 40(4):239246, 2010.

[15]

A. Kyprianou, W. Schoutens, and P. Wilmott.

Exotic Option Pricing and Advanced Lévy Models.

John Wiley & Sons Ltd., ChiChester, England, 2005.

[16]

H. Masuda. Parametric estimation of Lévy processes. In Lévy Matters IV, p. 179-286. Springer.

.

[17]

F. Mies.

Rate-Optimal Estimation of the Blumenthal-Getoor Index of a Lévy Process.

Electronic Journal of Statistics, 14(2):41654206, 2020.

[18]

M. Reiß.

Testing the Characteristics of a Lévy Process.

Stoch. Proc. Appl., 123(7):28082828, 2013.

[19]

J. Rosiński.

Tempering Stable Processes.

Stoch. Proc. Appl., 117(6):677707, 2007.

[20]

K. Sato.

Lévy Processes and Infinitely Divisible Distributions.

Cambridge Stud. Adv. Math., 68, Cambridge University Press, Cambridge, U.K., 1999.

[21]

P. Tankov.

Pricing and Hedging in Exponential Lévy Models: Review of Recent Results.

Paris-Princeton Lectures in Mathematical Finance 2010 (R. Carmona, E. Çinlar, I. Ekeland, E. Jouini, J. A. Scheinkman, and N. Touzi (eds.)), Lect. Notes Math., 2003, 319359, 2010.

[22]

Q. Wang, J.E. Figueroa-López, and T. Kuffner.

Bayesian Inference on Volatility in the Presence of Infinite Jump Activity and Microstructure Noise.

Electronic Journal Of Statistics., 15(1):506553, 2021.

[23]

L. Zhang, P. A. Mykland, and Y. Aït-Sahalia.

A Tale of Two Time Scales: Determining Integrated Volatility with Noisy High-Frequency Data.

J. Am. Stat. Assoc., 100(472):13941411, 2005.