Integrated Optimization of Predictive and Prescriptive Tasks††thanks: \hrefhttps://www.abstractsonline.com/pp8/#!/6818/presentation/11528This work was presented in INFORMS Annual Meeting, Seattle, Washington, October 20-23, 2019.

Abstract

In traditional machine learning techniques, the degree of closeness between true and predicted values generally measures the quality of predictions. However, these learning algorithms do not consider prescription problems where the predicted values will be used as input to decision problems. In this paper, we efficiently leverage feature variables, and we propose a new framework directly integrating predictive tasks under prescriptive tasks in order to prescribe consistent decisions. We train the parameters of predictive algorithm within a prescription problem via bilevel optimization techniques. We present the structure of our method and demonstrate its performance using synthetic data compared to classical methods like point-estimate-based, stochastic optimization and recently developed machine learning based optimization methods. In addition, we control generalization error using different penalty approaches, and optimize the integration over validation data set.

Keywords: Prescriptive, Predictive, Regression, Progressive Hedging Algorithm, Machine Learning, Bilevel Optimization.

1 Introduction

Today we are living in a world called the information age. The exponential growth of data availability, ease of accessibility in computational power, and more efficient optimization techniques have paved the way for massive developments in the field of predictive analytic. Particularly when organizations have realized the benefits of predictive methods in improving their efficiency and gaining an advantage over their competitors, these predictive techniques become more powerful. There is a mutual relationship between predictive and prescriptive analytics. We cannot deny the role of optimization techniques while obtaining predictive models because most of the predictive models are trained over the minimization of a loss or maximization of a gain function. On the other hand, prescriptive models containing uncertainty need the estimated inputs from predictive analytics to handle uncertainty in optimization parameters. Although these statistical (machine) learning methods have been provided well-aimed predictions for uncertain parameters in many different fields of science, scenario-based stochastic optimization introduced by [8] and similar works in [7], [16], [13], and [17] are widely preferred techniques in order to tackle uncertainty in decision problems. One of the reasons why these stochastic or robust optimization methods or similar solutions provided by [3] and [5] do perform better than point estimate-based optimization is that training process of statistical learning methods does not take into account optimal actions because traditional learning algorithms measure prediction quality based on the degree of closeness between true and predicted values. This gap between prescriptive and predictive analytics leads point estimate-based decisions to a failure in the prescription phase.

There are different variables and parameters in prediction and prescription tasks. Prediction tasks mainly have components such as feature data, response data, and the parameters connecting these two via a function. Prescription problems generally have cost vector parameters in the objective function, right-hand-side and left-hand-side parameters in the constraints, and decision variables. Our interest in this paper is to fit a predictive function with responses and feature data, and feed prescriptive model parameters by this fitted function.

For the sake of uniformity, we use the same notation the rest of this paper. We indicated feature data with , responses with , parameter of predictive algorithm with , and decision variables with . Responses () are the bridge parameter connecting predictive and prescriptive tasks.

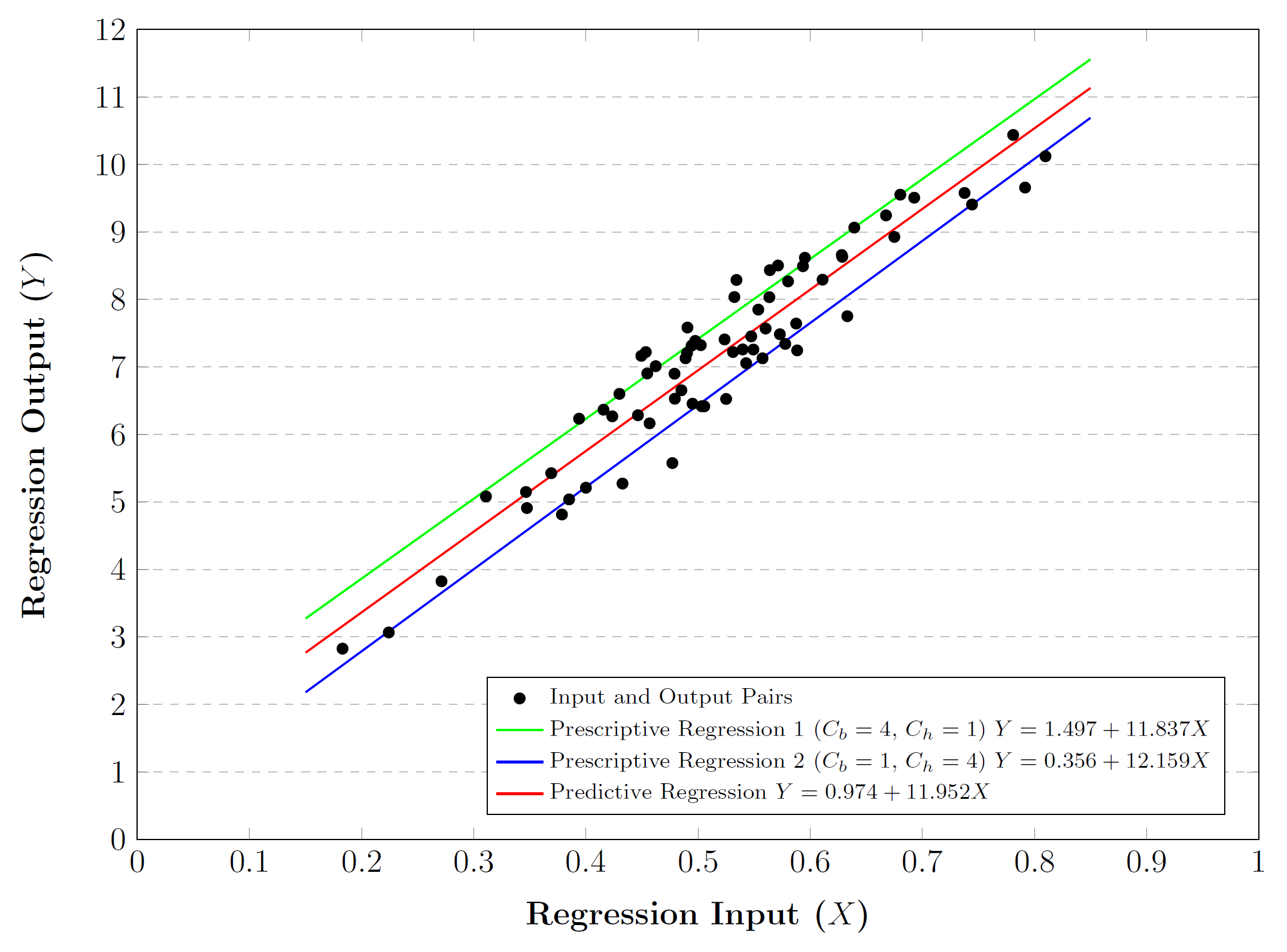

In order to visualize our motivation, imagine a newsvendor problem with a cost function, , containing holding cost () and backordering cost () with demand parameter (). In the company of feature data, a predictive regression model can be built for future demand as where in order to minimize cost function.

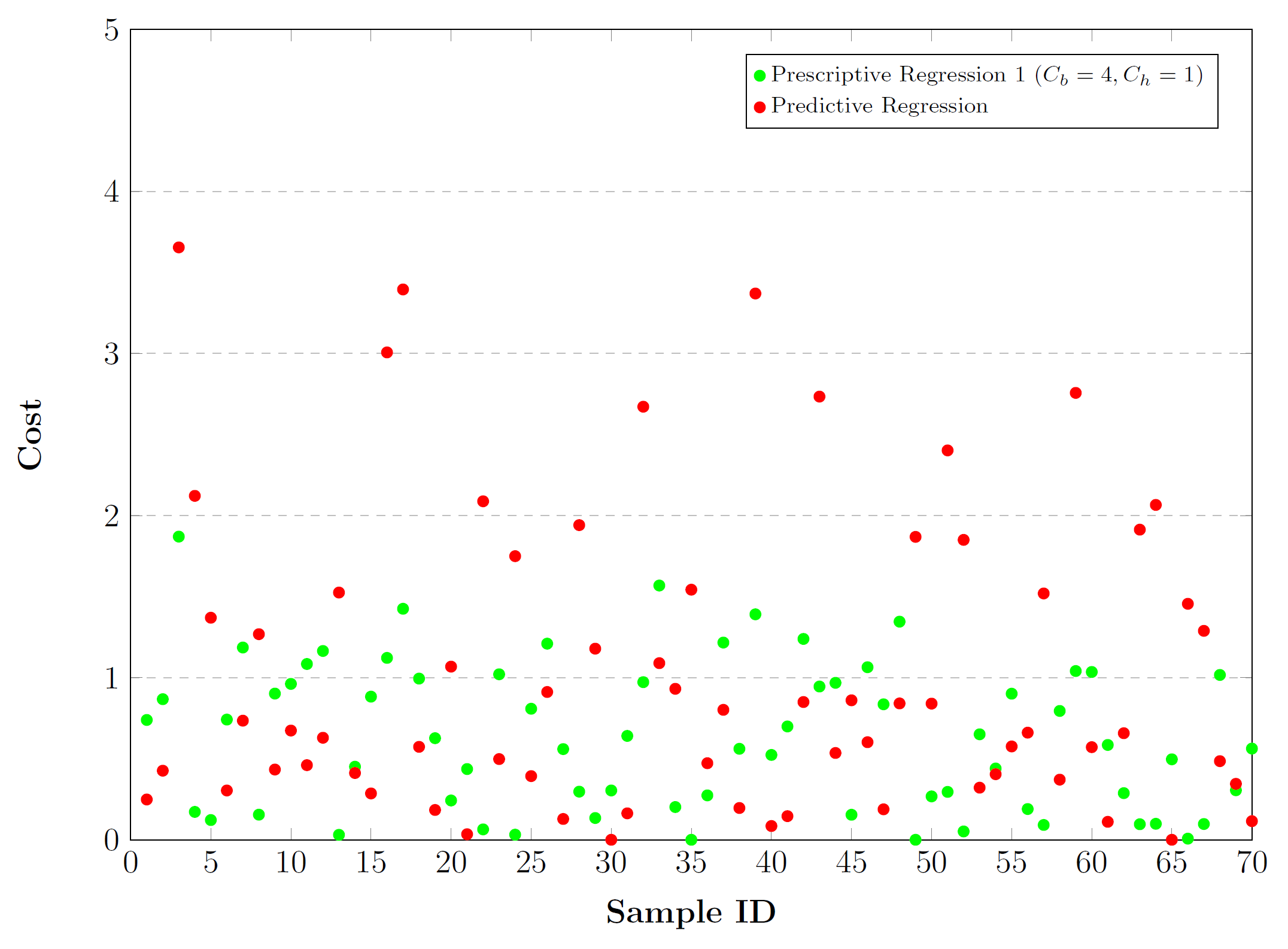

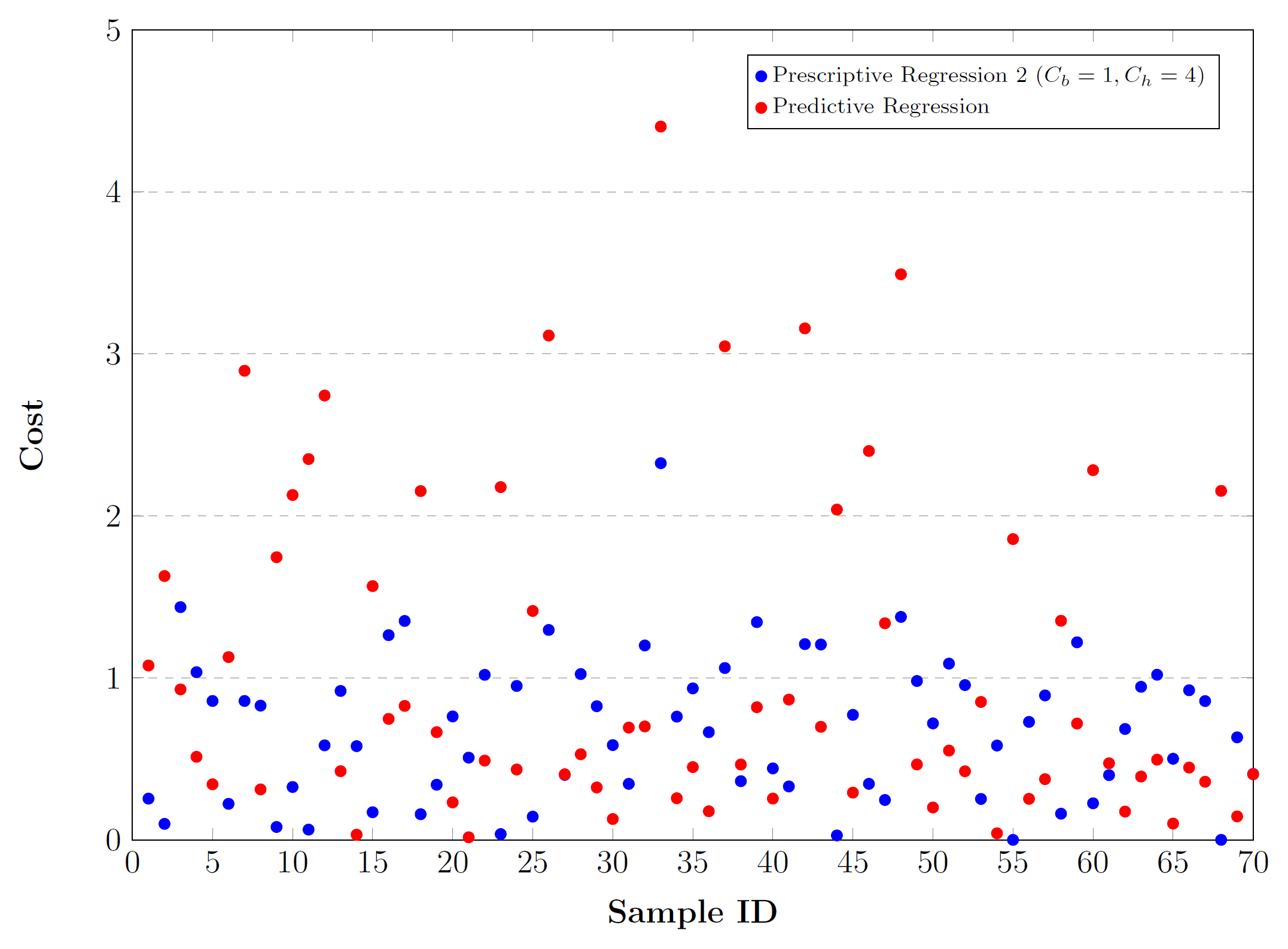

However, the training criteria of this predictive regression model will be based on closeness between true and predicted responses via a loss function, the predictive regression model will not capture the effect of holding and backordering costs in the cost function, and future predictions will most probably fail in prescription stage. In Figure 11(a), one predictive regression and two different prescriptive regression models (considering holding and backordering costs) are presented based on two different scenario. When backordering cost is greater than holding cost, using prescriptive regression 1 gives a lower cost on the average since it keeps predictions higher in order to avoid shortage cost as seen in Figure 11(b). Similarly, when holding cost is greater than backordering cost, using prescriptive regression 2 gives a lower cost on the average since it keeps predictions lower in order to avoid holding cost as seen in Figure 11(c). The question is how to obtain such a predictive model directly caring the characteristics of prescriptive model.

In this paper, our purpose is to build a framework for predictive regression model caring the characteristics of prescriptive model and providing best decisions. We will call our framework as ”Integrated Predictive and Prescriptive Optimization” (IPPO). While IPPO is seeking the most accurate predictive regression model, the desired predictive regression model will tackle uncertainty by providing best actions in prescription stage.

2 Related Work

There have been recent developments in supervised machine learning algorithms (classification and regression tasks), but no matter what kind of learning algorithm is employed, the common and final task is generally to train these algorithms in order to find the closest predictions to true values. Latest works in the literature show that scientists are realizing that training machine learning models solely based on a prediction criterion like mean squared error, mean absolute error, or log-likelihood loss is not enough when these noisy predictions will be parameters of prescription tasks. Bengio [4] is one of the first works considering this issue and building an integrated framework for both prediction and prescription tasks, he emphasized the importance of evaluation criteria of predictive tasks. His neural network model was not designed to minimize prediction error, but instead to maximize a financial task where those noisy predictions are used as input. Another integrated framework developed by Kao et al.[12] trains parameters of regression model based on an unconstrained optimization problem with quadratic cost function. It is a hybrid algorithm between ordinary least square and empirical optimization. Tulabandhula and Rudin [20] minimizes a weighted combination of prediction error and operational cost, but operational cost must be assessed based on true parameters. Bertsimas and Kallus [6] add a new dimension to this field by introducing the conditional stochastic optimization term. This simple but efficient idea leverages non-parametric machine learning methods in order to assign weights into train data points for a given test data point, then calculates optimal decisions over stochastic optimization based on calculated weights. However, this methodology is using machine learning tools outside of prescription problem. A different approach developed by Ban and Rudin [1] considers the decision variables as a function of auxiliary data, but this method may fail if the connection between optimal decisions and parameters in a constrained optimization problem, or may end up with indefeasible decisions. Oroojlooyjadid et al.[14] and Zhang and Gao [21] built an extension of [1] since both papers approach to the solution from the same perspective, but they solve the problem via neural network to capture the non-linearity between auxiliary data and decisions. One more neural network based integrated task is proposed by Donti et al. [9], and primarily they focus on quadratic stochastic optimization problems since they are tuning neural network parameters by differentiating the optimization solution to a stochastic programming problem. One of the latest works in integrating predictive and prescriptive tasks is developed by Elmachtoub and Grigas [10] which aims to find parameter of linear regression model inside of decision problem via a new loss function. This method minimizes the difference between objective value provided by true parameters and objective value where decisions provided by predicted parameters are assessed.

3 Integrated Predictive and Prescriptive Optimization

Given a decision problem (DP) with parameter uncertainty, our goal is to estimate the predictive relationship between responses (uncertain parameters of the decision problem) and a set of input features such that the prescriptive modeling of the decision problem using the predicted responses results in the best decisions. We consider decision problems that can be formulated as an optimization model. Further, the statistical relationship between uncertain parameters (Y) and input features (X) can be approximated through a parametric regression model, i.e., , where is a vector of parameters and is an error term and is some function describing the relationship between Y and X. Without loss of generality, given the estimates of uncertain parameters , we define the deterministic decision problem (DP) as follows:

| (1a) | ||||

| s.t. | (1b) | |||

| (1c) | ||||

In the above formulation, denote the decision variables, and denote the estimates of the uncertain parameters in the objective and constraints set, respectively. Let () denote the optimal solution of DP given , i.e. satisfying and }. The uncertain parameters in DP are estimated through a parametric regression model. Let’s assume given the historical data for the response Y and explanatory features X, the prediction problem (PP) using parametric regression is expressed as:

| (2) |

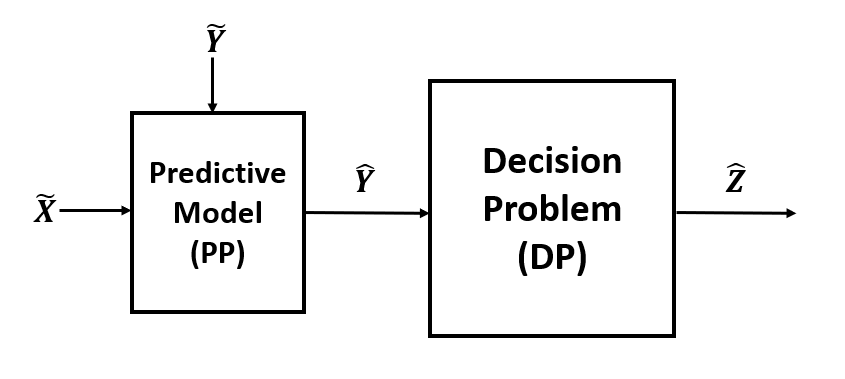

In classical approach, the predictive (PP) and prescriptive (DP) tasks which are often treated independently and often in a sequence, i.e., first predict (using PP) and then prescribe (using DP). This process is illustrated in Figure 2.

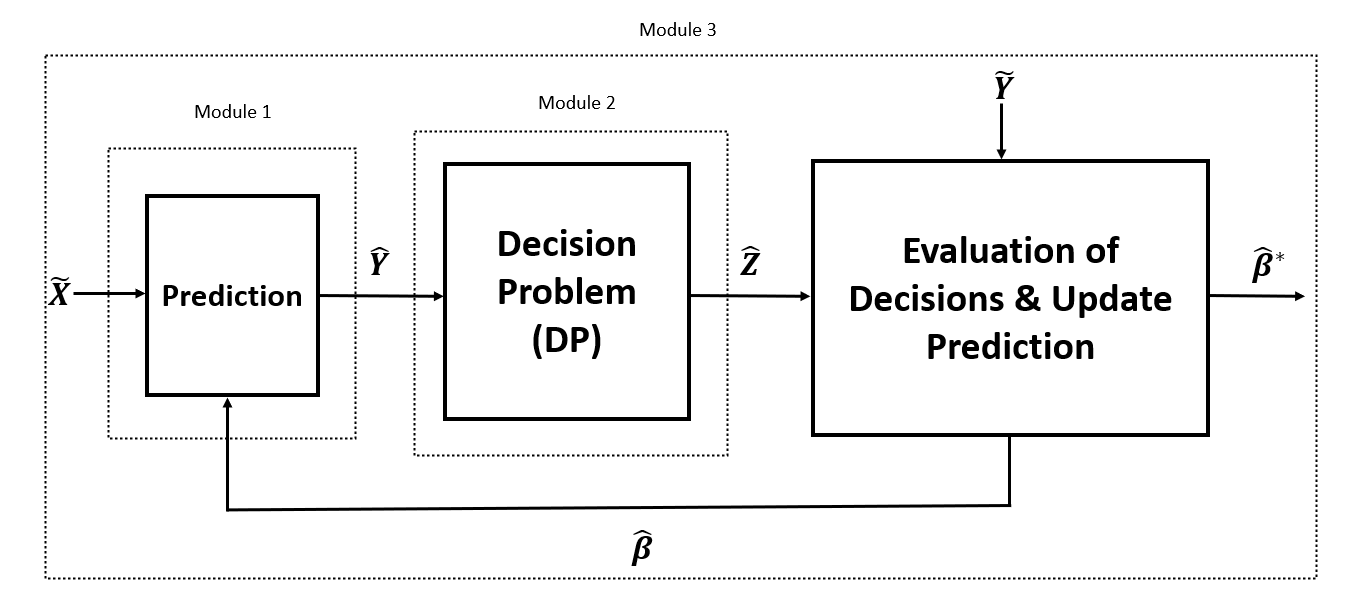

We herein develop an integrated framework joining the predictive (PP) and prescriptive (DP). Three modules of the integration framework are as follows:

-

1.

Given a set of independent features, a predictive regression model generating responses which are input to the optimization model as part of the input parameter set (Module 1),

-

2.

An optimization model prescribing decisions based on input parameters (Module 2),

-

3.

Another optimization model evaluating the quality of prescribed decisions with respect to ground truth in the response space and updating the parameters of the predictive model (Module 3).

Figure 3 illustrates these three modules. The sequential predictive and prescriptive tasks (modules 1 and 2) are concurrently optimized through the module 3. While module 1 is a prediction model, modules 2 and 3 are decision optimization problems with their respective decisions influencing one another. The embedding structure of modules 1 and 2 within module 3 is similar to those of bilevel optimization problems.

Hence, we model the integration framework as a nested optimization model. In the next section we model the integrated prediction and prescription problem as a bilevel optimization model.

3.1 Bilevel Models and Solving Techniques

Bilevel problems are nested optimization problems where an upper-level optimization problem is constrained by a lower-level optimization problem [2]. A common application of the bilevel problems is a static leader-follower game in economics [18], where the upper level decision maker (leader) has complete knowledge of the lower level problem (follower). Decision variables of the upper level serve as parameters of the lower level.

We model the integrated framework for the prediction and prescription tasks as a bilevel optimization problem. The upper-level problem jointly determines the parameters of the regression model () and prescription decisions. At lower level, we make decisions with the help of predicted parameters, and we evaluate these actions with respect to true parameters by fixing those ”here-and-now” decisions () at upper level problem in constraint 3d, so that we integrate all proposed steps in one framework formulated as in (3a)-(3g).

| (3a) | ||||

| s.t. | (3b) | |||

| (3c) | ||||

| (3d) | ||||

| (3e) | ||||

| (3f) | ||||

| (3g) | ||||

The most popular solution technique for bilevel optimization problems is to transform bilevel problem into single level problem by replacing objective function of lower level problem with Karush–Kuhn–Tucker (KKT) conditions [2]. The KKT conditions appear as dual and complementarity constraints, that is why KKT conditions require convexity, so this approach is limited to convex lower level problems. Complementarity constraints (4h and 4i) convert the problem nonlinear models; thus, these constraints are replaced with logic constraints by defining new binary variables and sufficiently enough an M parameter. With this final touch, bilevel model turns into a mixed-integer problem, and it can be solved by traditional solvers as in form (4a)-(4j).

| (4a) | ||||

| s.t. | (4b) | |||

| (4c) | ||||

| (4d) | ||||

| (4e) | ||||

| (4f) | ||||

| (4g) | ||||

| (4h) | ||||

| (4i) | ||||

| (4j) | ||||

3.2 Controlling Generalization Error in IPPO

Our model is developed based on finding best decision in train data set. In order to ensure quality of prediction model in external data set, we propose three different ways to control generalization error within this framework by regularizing predictive model parameters. The first method is to rewrite objective function as weighted average of predictive error and prescriptive error as shown in formulation (5a)-(5g) where . When , we solve pure bilevel optimization model without generalization error, and when , we ignore the prescription part, and optimize directly predictive algorithm solely, and that leads us to point estimate-based prescriptions.

| (5a) | ||||

| s.t. | (5b) | |||

| (5c) | ||||

| (5d) | ||||

| (5e) | ||||

| (5f) | ||||

| (5g) | ||||

The second method uses predictive error term again, but in a way that it can be restricted by a constraint. However this restriction cannot be less than the loss value which is provided by predictive model solely because constraining loss less than the optimal () makes optimization model indefeasible, this method is shown in formulation (6a)-(6h) with a restriction parameter .

| (6a) | ||||

| s.t. | (6b) | |||

| (6c) | ||||

| (6d) | ||||

| (6e) | ||||

| (6f) | ||||

| (6g) | ||||

| (6h) | ||||

The last method is to shrink predictive model parameters by penalizing with a penalty coefficient as [19] introduced, this model is formulated in (7a)-(7g).

| (7a) | ||||

| s.t. | (7b) | |||

| (7c) | ||||

| (7d) | ||||

| (7e) | ||||

| (7f) | ||||

| (7g) | ||||

3.3 Proposed Decomposition Method for IPPO

Bilevel optimization problems are NP-hard, and it is not easy to solve. However, our proposed predictive and prescriptive integrated methodology has a unique feature. All the defined variables belong to its own scenario except the regression parameters. Regression parameters are common for all scenarios. After converting bilevel to a single level problem by applying KKT conditions, our model becomes a two-stage mixed-integer program whose first stage variables are regression parameters. Here, we create copies of regression parameters across all scenarios and make the problem fully scenario-based decomposable, but we need to include a non-anticipativity or implementability constraint to ensure all regression parameters are equal each other for all scenarios. Progressive hedging algorithm (PHA) proposed by [15] can be used as decomposition techniques for our two stage mixed-integer problem. In our framework, we will provide best candidate solution as initial regression parameters for depicted Figure 3, and PHA solves all scenario problems independently, then we wıll update regression parameters ıteratıvely. These steps repeat until a convergence is satisfied.

| (8a) | ||||

| s.t. | (8b) | |||

| (8c) | ||||

For better understanding, let’s consider the formulation in (8a)-(8c), indicates first stage variable, and indicates second stage variable for scenario.

| (9a) | ||||

| s.t. | (9b) | |||

| (9c) | ||||

| (9d) | ||||

In the formulation (9a)-(9d), first stage variable is duplicated, and variables are created for each scenario, but they are linked via non-anticipativity constraint 9d. By relaxing constraint 9d, all scenarios can be easily solved in a parallel way.

PHA iterates and converges to a common solution taking into account all the scenarios belonging to the original problem. We show the details and steps for basic PHA in Algorithm 1. Let be penalty factor, be stopping criteria, and be dual prices for non-anticipativity constraint 9d.

4 Experimental Setup

In this part, we discuss why and how we select predictive and prescriptive model, then we will introduce parameters and variables of these two tasks. Next, we explain data creation process step by step, and we will show formulation of integrated predictive and prescriptive task.

4.1 Prescriptive and Predictive Model Selection

We validate the performance of integrated predictive and prescriptive methodology and compare it with various well-known and recently developed methods. We perform numerical experiments on two different prescriptive models. The first one is well-known newsvendor problem used by [1], but we extend it from single product to multi-product newsvendor problem ( products), and we use different costs for each scenario (production , holding, and backordering) instead of fix costs in order to increase the complexity of problem. Extensive form of classical newsvendor problem with multi-product is expressed as formulated in (10a)-(10d).

| (10a) | ||||

| s.t. | (10b) | |||

| (10c) | ||||

| (10d) | ||||

| Decision Variables for Newsvendor Problem | |

|---|---|

| Amount of regular order done in advance for product | |

| Amount of shortage for product in scenario | |

| Amount of surplus for product in scenario | |

| Parameters for Newsvendor Problem | |

| Cost of order for product in scenario | |

| Cost of backordering for product in scenario | |

| Cost of hold for product in scenario | |

| Amount of demand for product in scenario | |

The second prescriptive model is two-stage shipment planning problem leveraged by [6] where there is a network between warehouses and locations. The goal is to produce and hold a product at a cost in warehouses to satisfy the future demand of locations. Then the product is shipped, when needed, from warehouses to locations with transportation cost. In case current total supply in warehouses does not satisfy the demand of locations, the last-minute production takes place with a higher cost. The extensive form of two-stage shipment problem is formulated as follow in (11a)-(11d).

| (11a) | ||||

| s.t. | (11b) | |||

| (11c) | ||||

| (11d) | ||||

| Decision Variables | |

|---|---|

| Amount of production done in advance at warehouse | |

| Amount of production done last minute at warehouse in scenario | |

| Amount of shipment from warehouse to location in scenario | |

| Parameters | |

| Cost of production done in advance at warehouse | |

| Cost of production done last minute at warehouses | |

| Cost of shipment from warehouse to location in scenario | |

| Amount of demand at location in scenario | |

As for predictive model, since we embed the predictive model inside of prescriptive model, we choose linear regression model as in 12 to maintain the linearity of prescriptive model. However, other predictive methodologies still can be applied to capture nonlinearity outside of this integrated framework as preprocess, and dimensionality can be reduced between feature variables and responses especially in high dimensional data as built in deep learning, then these converted feature variables can be embedded inside of prescriptive model via linear regression again as described above.

| (12) |

4.2 Data Generation

In both experiments, we randomly generate feature variables of predictive model based on a dimensional multivariate normal distribution with size of observations, , i.e., , where and . Then, we choose the true parameters of our predictive model, linear regression in our case, as matrix for slopes and intercepts. Next, we calculated response according to the model , where is independently generated noise term and follows normal distribution, i.e., . Here the standard deviation of added noise controls the correlation between feature values and responses (Responses represent demand is in both prescriptive problems). To see the behavior of our method and other methods, we have employed 10 different noise standard deviations, thus we create 10 different feature and response pairs with different correlations. we measure these correlations based on R-Square value of a linear regression model. As for shipment cost, we randomly simulate its matrix as from warehouse to location based on uniform distribution for each scenario. In newsvendor problem. we create order, backordering, and holding costs again based on uniform distribution , , and for each scenario and product, respectively. Out of created observations, we randomly choose train, validation, and test sets from observations with size of , respectively. This splitting process is repeated by times, and all results are reported based on the average cost of these replications in both problems.

4.3 IPPO Formulations

We modify newsvendor and two-stage shipment problems here for integration process. First, we introduce variable to make predictions for demand via linear regression. Then we also introduce counterpart decision variables of original variables in newsvendor and shipment models because these counterpart decision variables will be made based on predicted demands. In our lower level, we make decisions based on output of predictive algorithm, linear regression, and submit these decisions to the upper level, so that we can evaluate the quality of these decisions based on true parameters in 13d and 14d.

| (13a) | ||||

| s.t. | (13b) | |||

| (13c) | ||||

| (13d) | ||||

| (13e) | ||||

| (13f) | ||||

| (13g) | ||||

| (13h) | ||||

| (13i) | ||||

We modify newsvendor and two-stage shipment problems here for integration process. First, we introduce variable to make predictions for demand via linear regression. Then we also introduce counterpart decision variables of original variables in newsvendor and shipment models because these counterpart decision variables will be made based on predicted demands. In our lower level, we make decisions based on output of predictive algorithm, linear regression, and submit these decisions to the upper level, so that we can evaluate the quality of these decisions based on true parameters. Constraints 13d and 14d undertake this task.

Detailed formulation of integrated newsvendor problem and two stage shipment problem is provided below in (13a)-(13i) and (14a)-(14i), respectively. If controlling generalization error is needed, one of the recommendations formulated in subsection 3.2 can be included in these models.

In both formulations, there will be a trade-off between lower and upper problems, such that lower problem minimizes its own cost based on variables provided by upper level problem, and upper level problem minimizes its own objective value based on prescriptions provided by lower level problem. To be able to solve bilevel model, we need to add optimality conditions for lower level problem based on KKT conditions. We introduce dual variables for lower level constraints, and write these conditions, but KKT conditions bring nonlinearity because of complementary slackness, so new binary variables can be defined, and SOS constraints and big M method can be used. After introducing KKT conditions, predictive task integrated two stage shipment problem becomes a mix integer problem with single level, and this formulation is given in (4a)-(4j).

| (14a) | ||||

| s.t. | (14b) | |||

| (14c) | ||||

| (14d) | ||||

| (14e) | ||||

| (14f) | ||||

| (14g) | ||||

| (14h) | ||||

| (14i) | ||||

4.4 Convergence to Stochastic Optimization

The Equation in 12 defines the linear regression where the output is a weighted combination of inputs plus an intercept. Linear regressions are generally trained based on mean squared deviations. In our proposed integrated model, this Equation in 12 produces predictions for each scenario, and lower level objective and constraints prescribes decisions based on these predictions as seen in (13f)-(13i) and (14f)-(14i) for each scenario again. If level of correlation between and goes to zero, slopes of predictive model in 12 or the feature variable contributions goes to zero, and predictions will be all equal each other thanks to intercepts. The same prediction for all scenarios will prescribe the same decisions across all scenarios as seen in forwarded decisions from lower level to upper level in (13d) and (14d). This converts our integrated methodology to a single level problem and becomes scenario formulation of a two-stage stochastic problem as shown in (9a)-(9d).

5 Computational Results

This section discusses the performance of our integrated methodology and other methods under different circumstances. All results for these experiments are obtained from Gurobi python API [11]. We compared results of various well-known methods like Point-Estimate-Based Optimization, Stochastic Optimization, and recent methods like Conditional Stochastic Optimization (kNN), and The Feature-Based Optimization by [6], [1], respectively. We investigate the behaviors of these methods under different correlations between features and responses , and evaluate performance of validation data set to see if generalization error is needed.

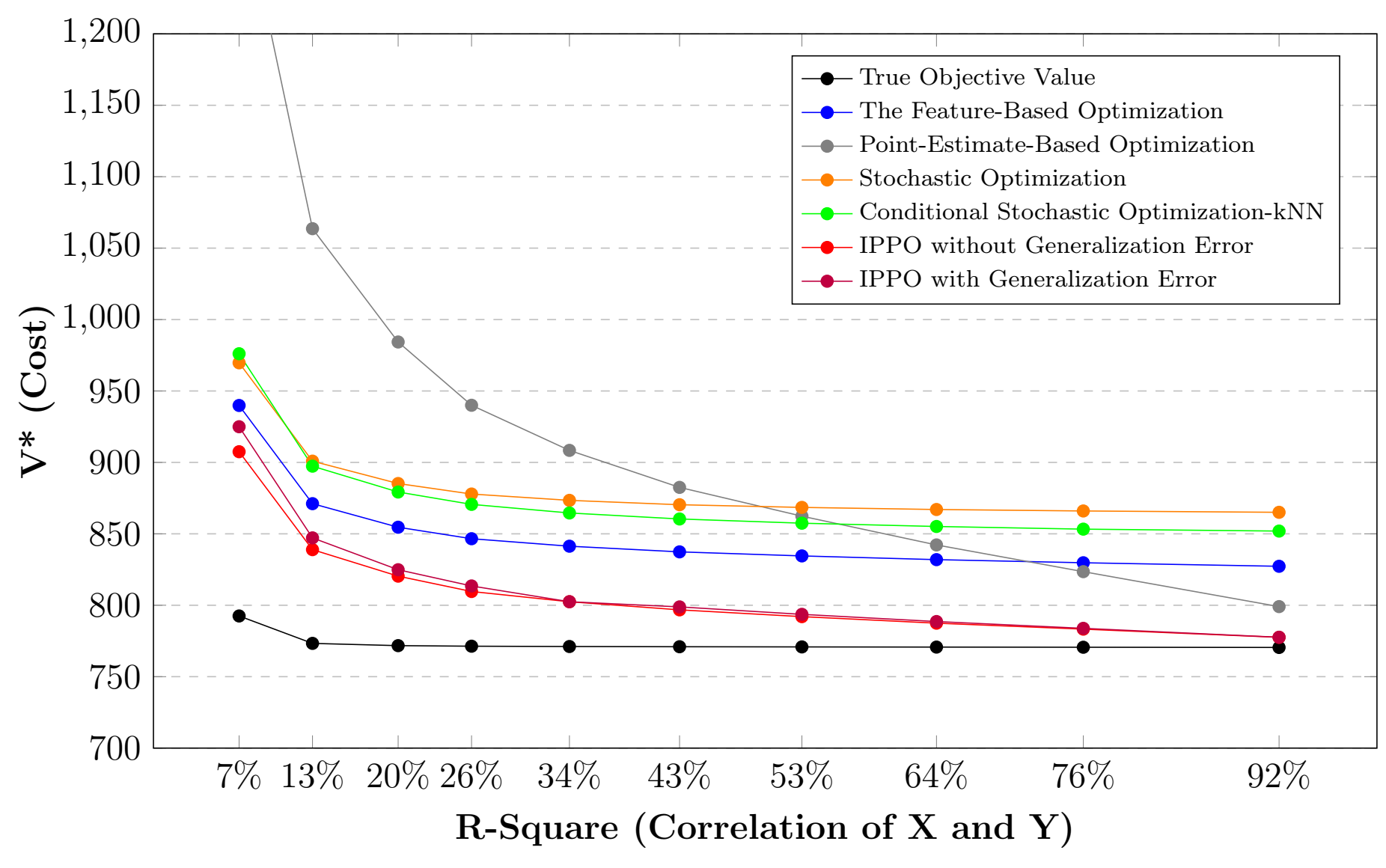

5.1 Newsvendor Problem

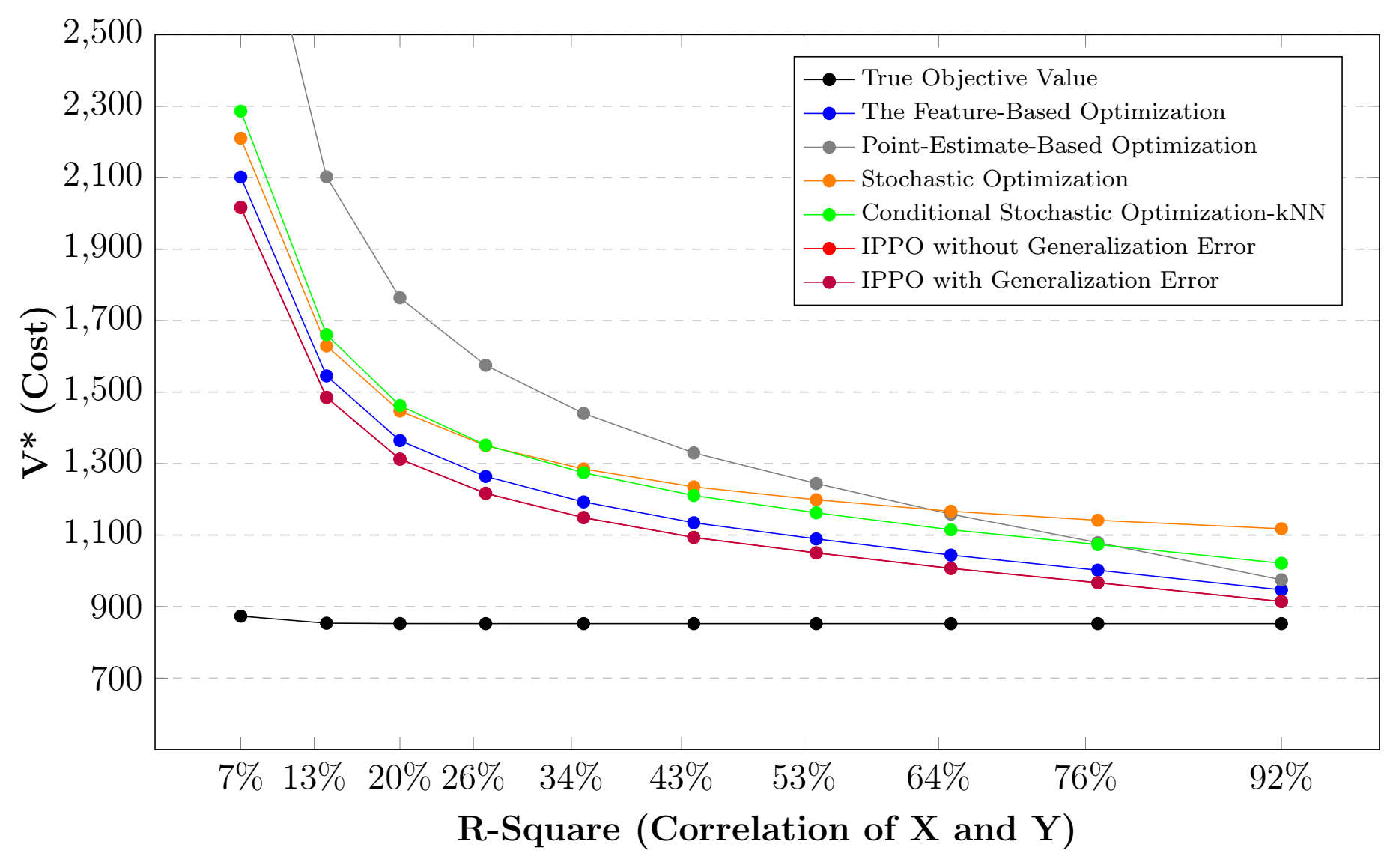

First and common feature of all methods, as we see in Figure 4, solution quality improves when we increase the correlation between features (side info) and responses, and this is expected because the more information is provided, the better results are obtained. However, improvement rates are different in each method. Second, kNN from [6] gives better result compared to stochastic optimization (k neighbors value is optimized over validation data set). The reason why it gives better solution is because it leverages specific neighbors in train data, instead of minimizing expected cost over all train data, eliminates irrelevant scenarios, search optimal solution by minimizing expected cost around neighbors.

| Correlation between X and Y | True Objective Values | IPPO | Performance | Optimal Regularization Parameter | Optimal Neighbors for kNN | ||||||

| Mean | Max | Min | S.Dev. | Mean | Max | Min | S.Dev. | ||||

| %7 | 873.5 | 924.8 | 815.0 | 27.2 | 2016.3 | 2118.5 | 1897.9 | 58.3 | %7 | 1 | 41 |

| %13 | 853.7 | 892.9 | 813.6 | 21.0 | 1484.9 | 1549.1 | 1410.3 | 35.0 | %10 | 1 | 41 |

| %20 | 852.7 | 889.5 | 814.5 | 19.6 | 1312.5 | 1369.6 | 1252.7 | 28.3 | %11 | 1 | 31 |

| %26 | 852.5 | 889.2 | 815.3 | 19.0 | 1216.8 | 1270.1 | 1164.7 | 25.0 | %13 | 1 | 28 |

| %34 | 852.5 | 889.4 | 816.1 | 18.6 | 1148.9 | 1199.4 | 1102.0 | 22.9 | %15 | 1 | 28 |

| %43 | 852.5 | 889.6 | 816.8 | 18.3 | 1093.3 | 1141.6 | 1050.7 | 21.4 | %17 | 1 | 22 |

| %53 | 852.5 | 889.8 | 817.3 | 18.2 | 1050.1 | 1096.5 | 1010.9 | 20.4 | %20 | 1 | 16 |

| %64 | 852.5 | 890.0 | 817.8 | 18.1 | 1006.9 | 1051.5 | 971.0 | 19.5 | %24 | 1 | 16 |

| %76 | 852.5 | 890.2 | 818.3 | 18.0 | 966.7 | 1009.7 | 933.4 | 18.8 | %31 | 1 | 10 |

| %92 | 852.5 | 890.4 | 818.9 | 17.9 | 914.2 | 955.0 | 881.2 | 18.2 | %53 | 1 | 5 |

| Correlation between X and Y | True Objective Values | IPPO | Performance | Optimal Regularization Parameter | Optimal Neighbors for kNN | ||||||

| Mean | Max | Min | S.Dev. | Mean | Max | Min | S.Dev. | ||||

| %7 | 873.0 | 972.6 | 688.7 | 59.2 | 2229.5 | 2546.0 | 1987.2 | 140.0 | %7 | 1 | 41 |

| %13 | 851.3 | 929.5 | 711.3 | 44.0 | 1596.6 | 1774.5 | 1431.6 | 80.2 | %9 | 1 | 41 |

| %20 | 849.1 | 924.9 | 724.4 | 40.5 | 1391.9 | 1527.4 | 1248.6 | 63.4 | %10 | 1 | 31 |

| %26 | 848.2 | 922.4 | 731.7 | 39.3 | 1278.3 | 1391.2 | 1148.2 | 55.0 | %12 | 1 | 28 |

| %34 | 847.7 | 920.9 | 737.2 | 38.7 | 1197.6 | 1293.9 | 1075.7 | 50.0 | %14 | 1 | 28 |

| %43 | 847.3 | 921.2 | 741.8 | 38.4 | 1131.6 | 1214.2 | 1016.3 | 46.2 | %16 | 1 | 22 |

| %53 | 847.0 | 925.1 | 745.5 | 38.3 | 1080.3 | 1154.2 | 970.4 | 43.7 | %18 | 1 | 16 |

| %64 | 846.7 | 929.1 | 749.1 | 38.4 | 1029.0 | 1103.7 | 925.0 | 41.8 | %22 | 1 | 16 |

| %76 | 846.4 | 932.7 | 752.4 | 38.6 | 981.3 | 1061.2 | 882.6 | 40.5 | %28 | 1 | 10 |

| %92 | 846.1 | 937.5 | 756.8 | 38.9 | 919.0 | 1007.0 | 827.2 | 39.5 | %47 | 1 | 5 |

We observe that value of k neighbors increases when correlation level between and decreases. Since this correlation decreases, kNN tends to minimize expected cost over more train data as we reported in Table 1 and 2. We did not include result of [10] in Figure 4 and 6 because [10] build their method when there is an uncertainty in cost vector of objective function.

Since IPPO methodology fully leverages side information and evaluates decisions with respect to true parameters inside of integrated framework, it gives the best solution.

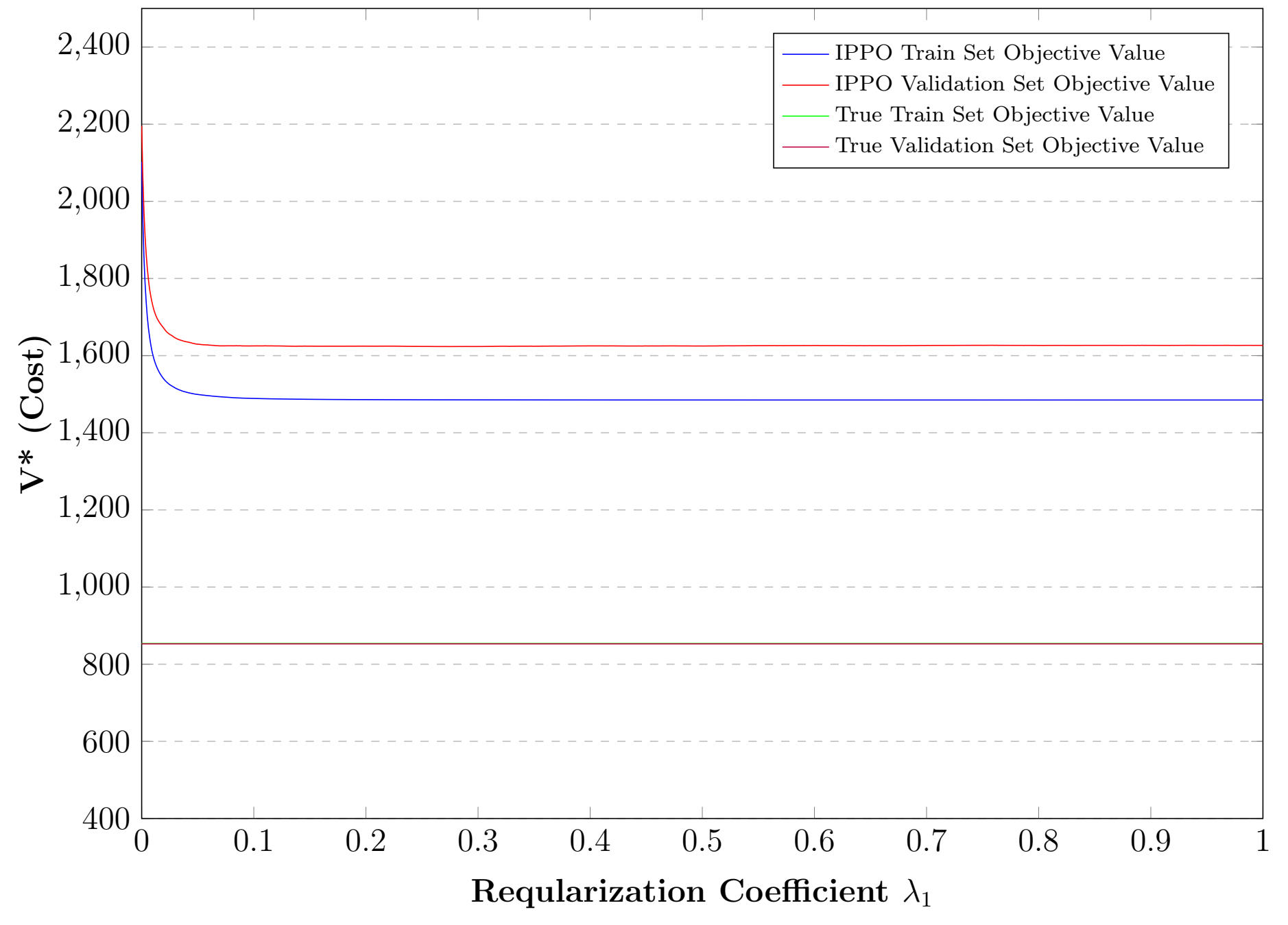

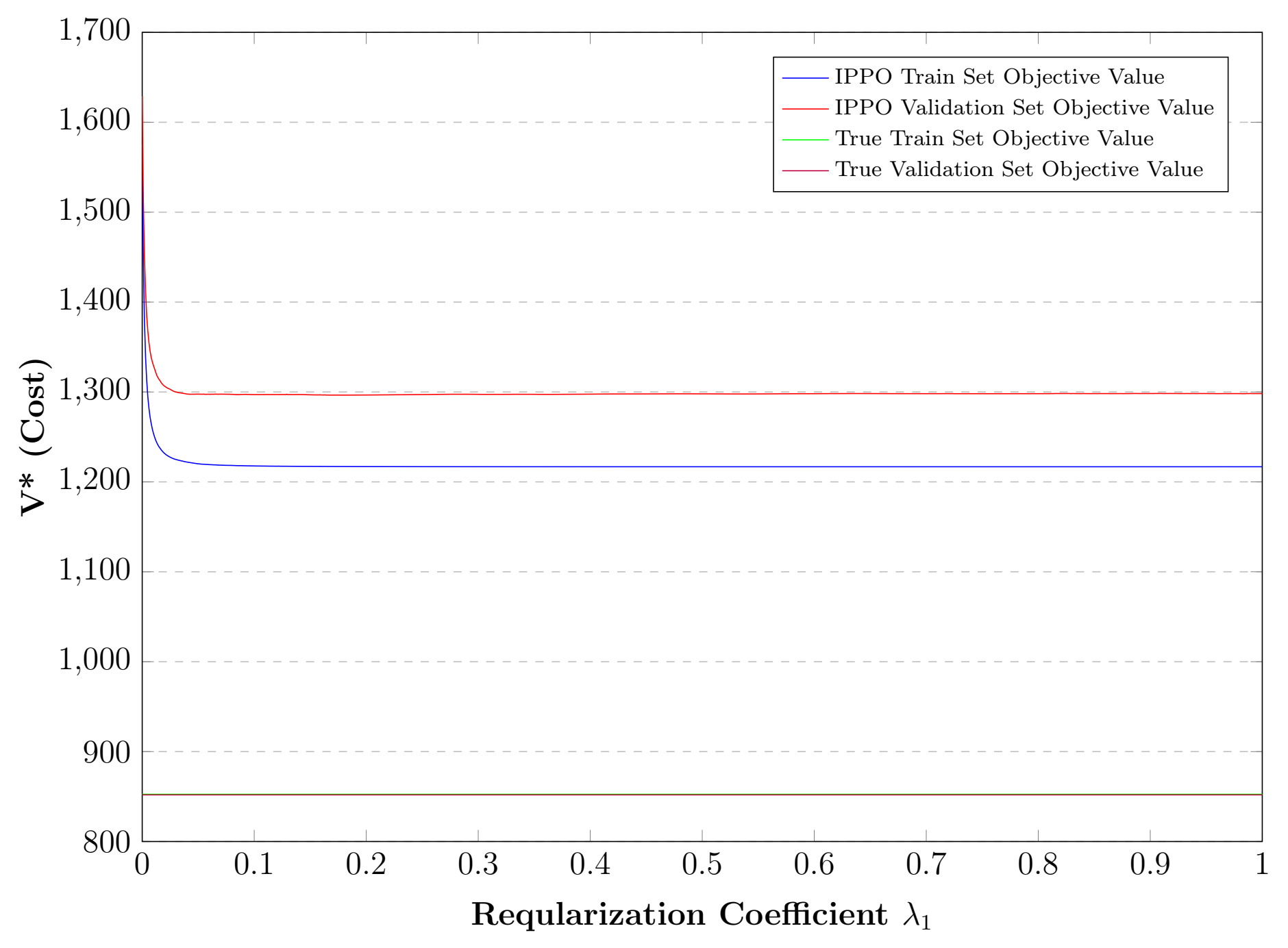

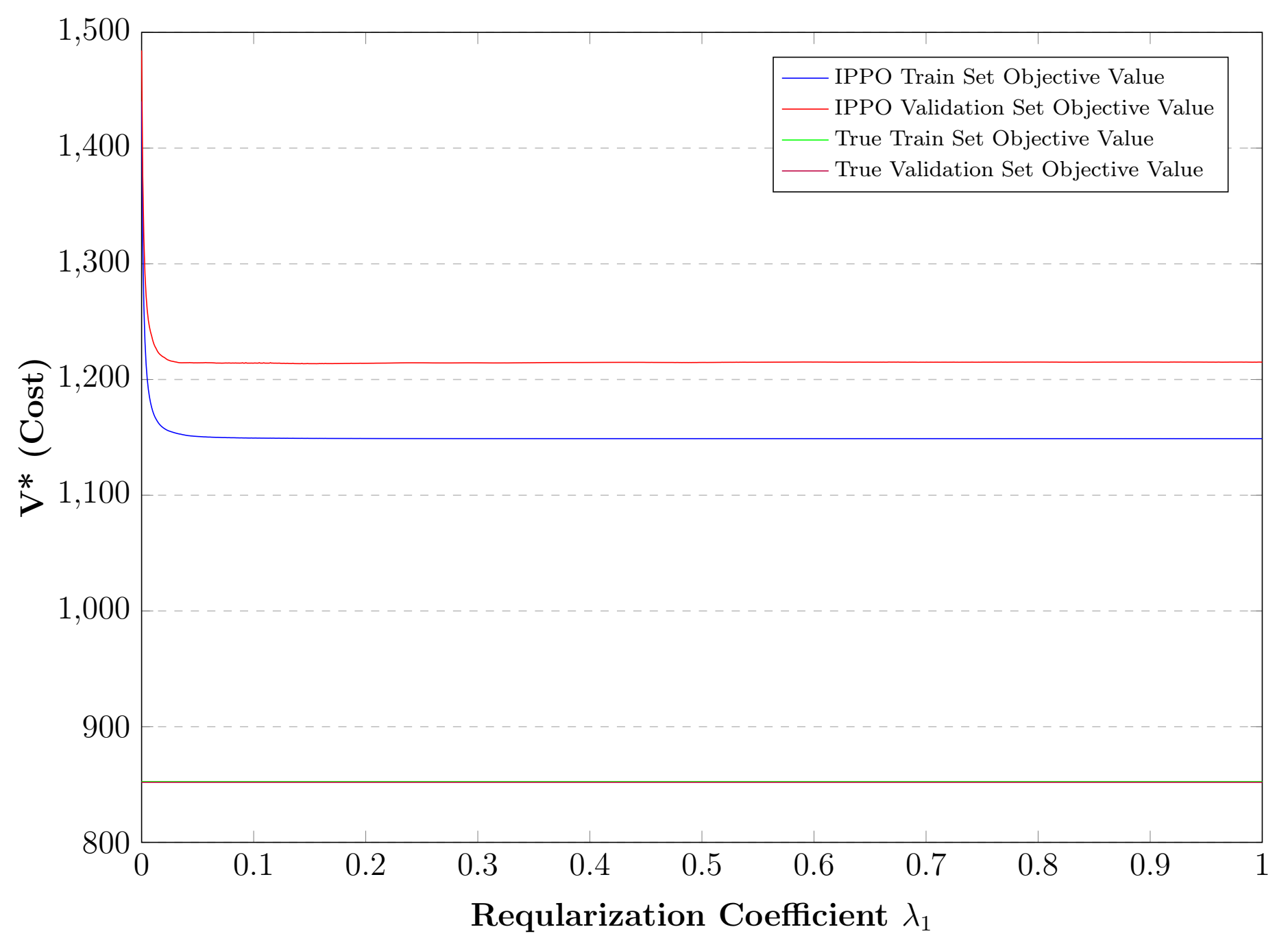

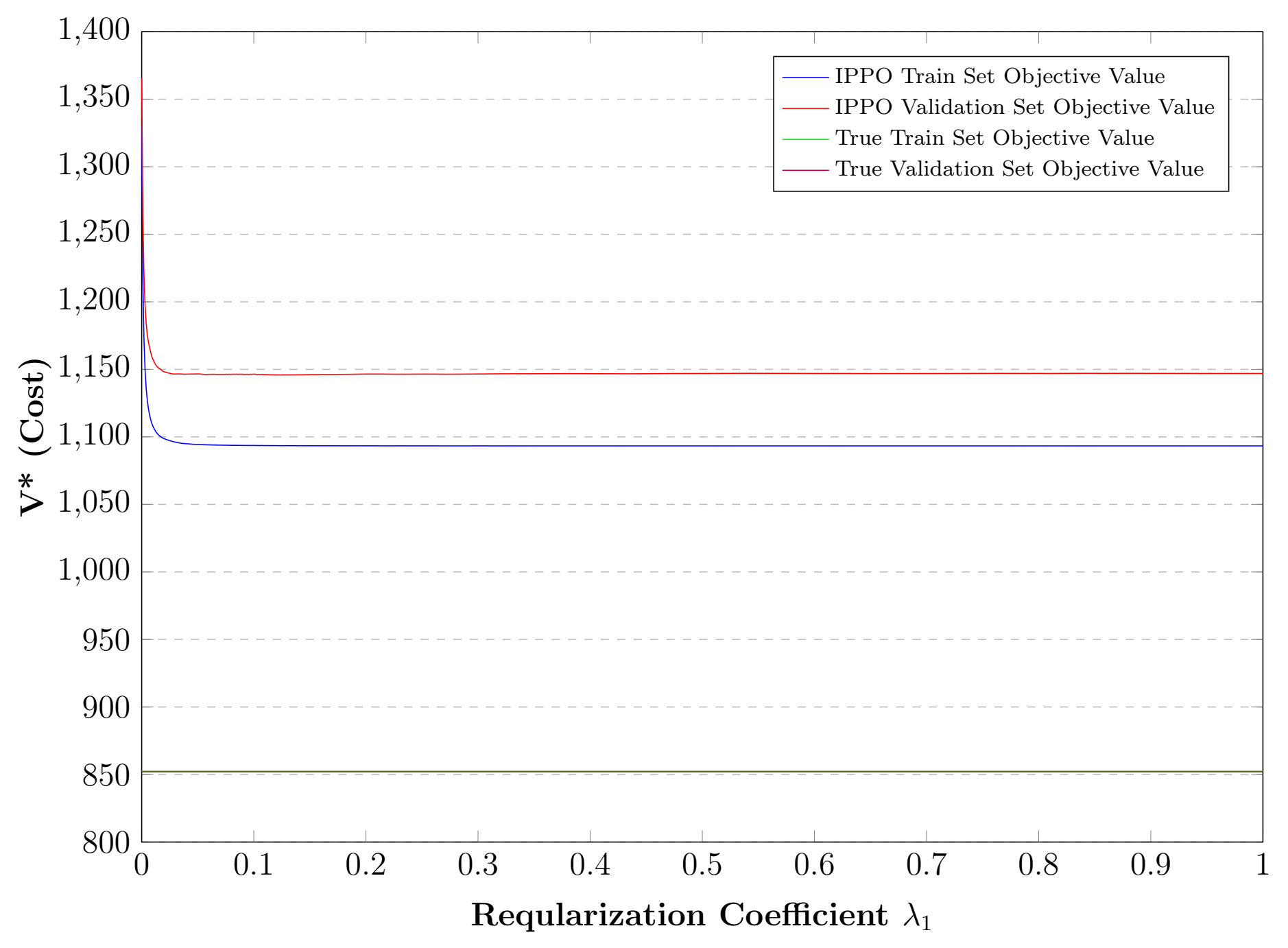

In newsvendor problem, we did not observe over-fitting issue, and there is no need to control generalization error. As we report in Figure 5, regardless of correlation level between and , validation and train performance improve constantly until where no generalization is needed. That is why IPPO with and without generalization error in Figure 4 overlaps.

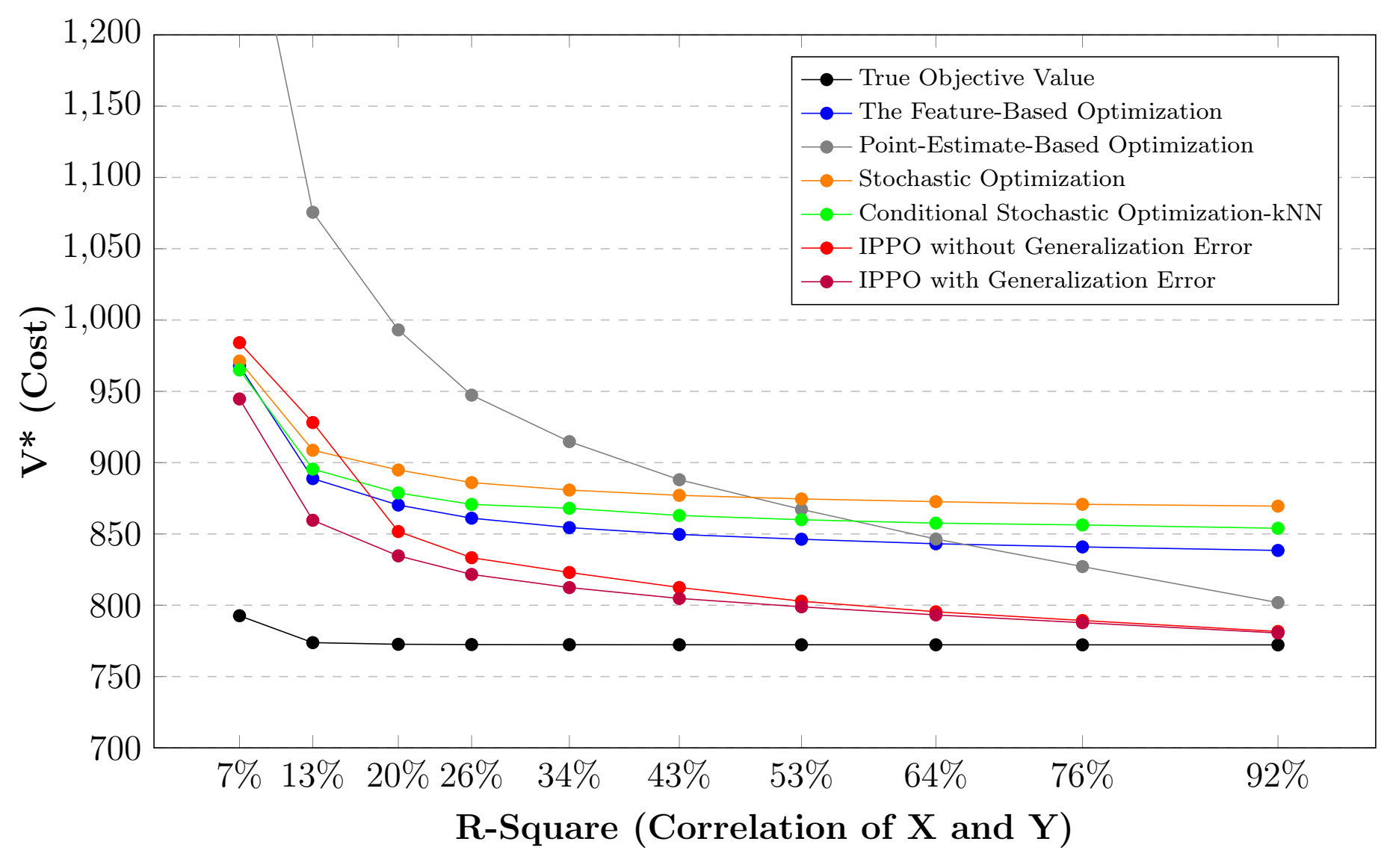

5.2 Two-Stage Shipment Problem

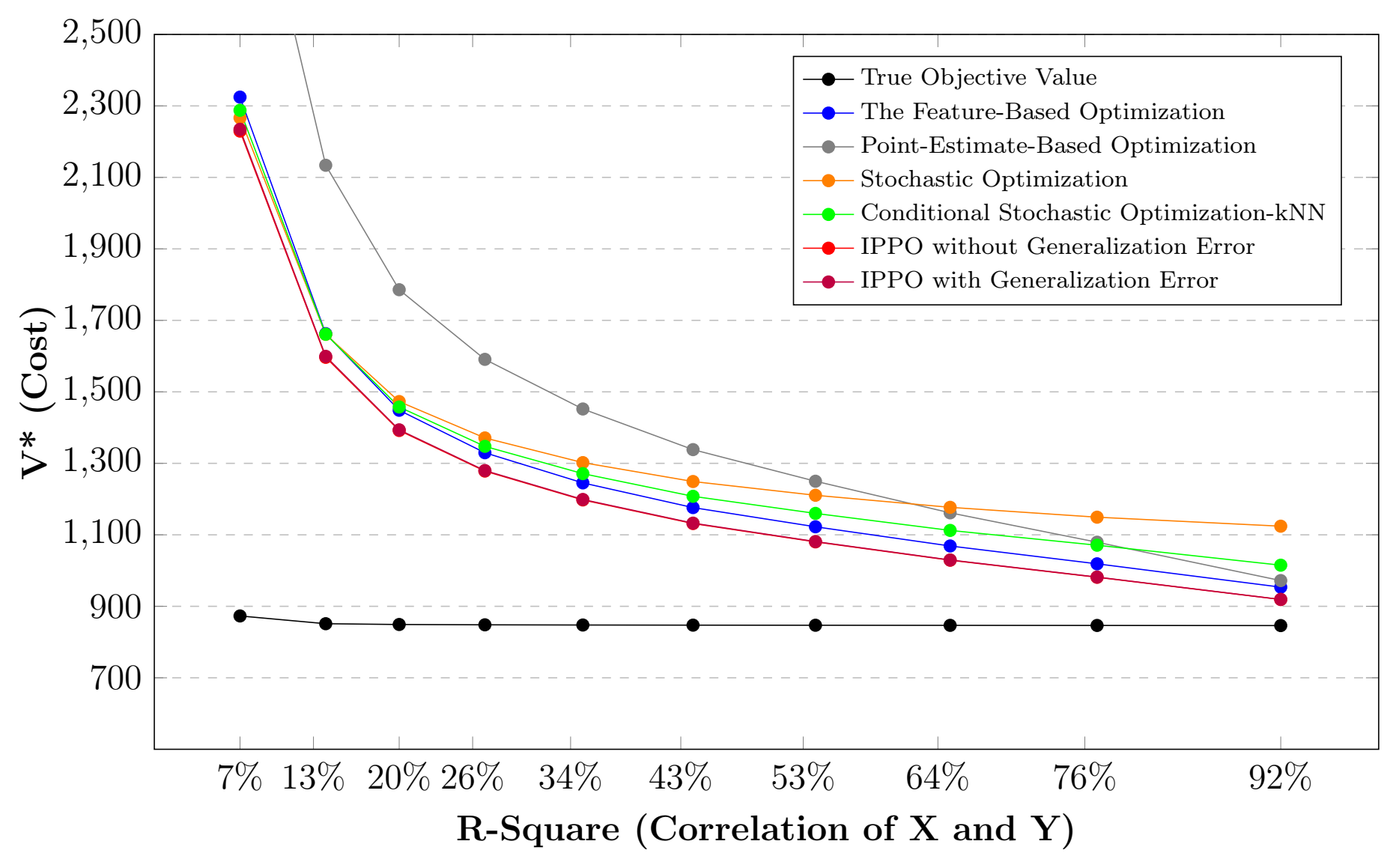

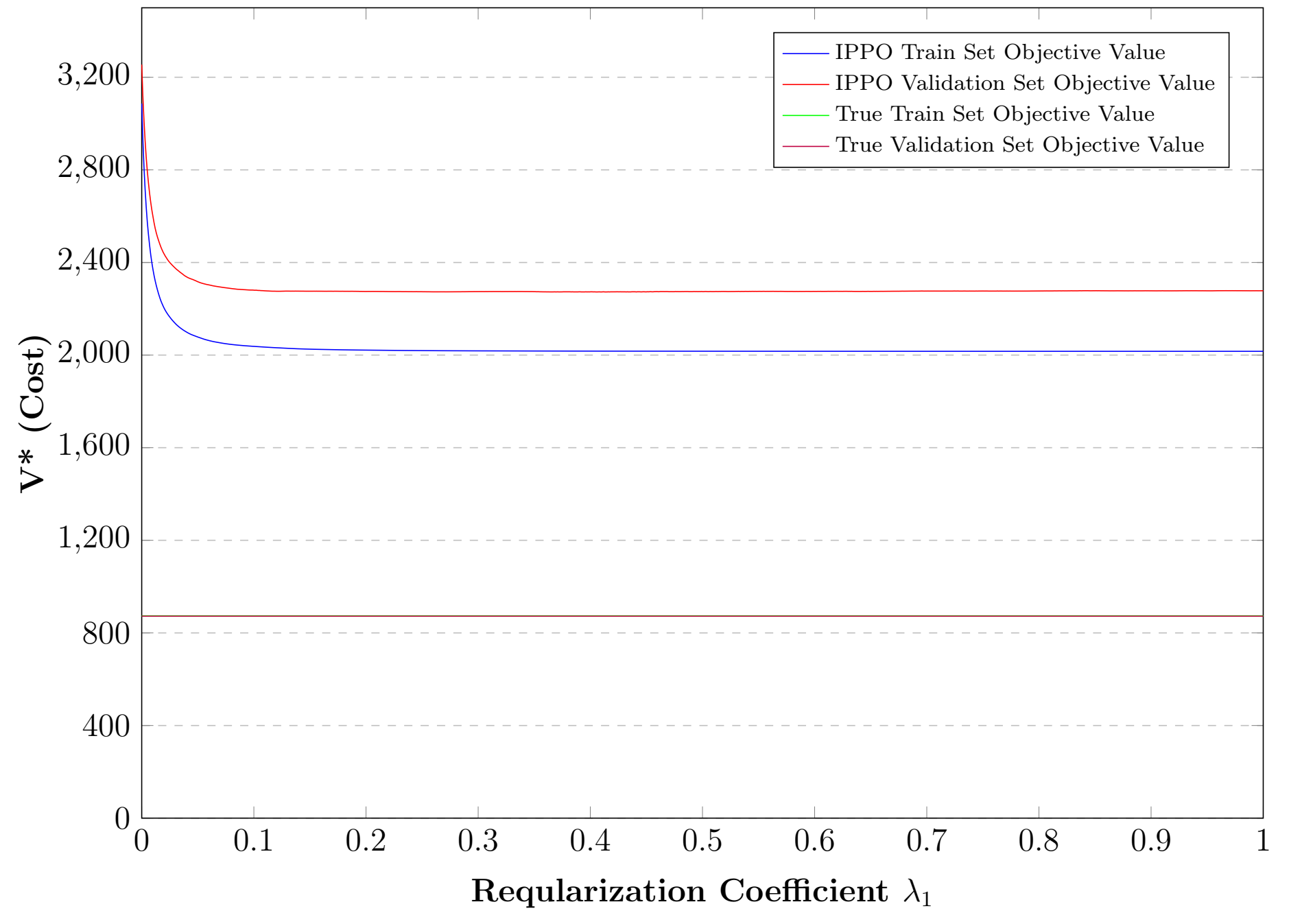

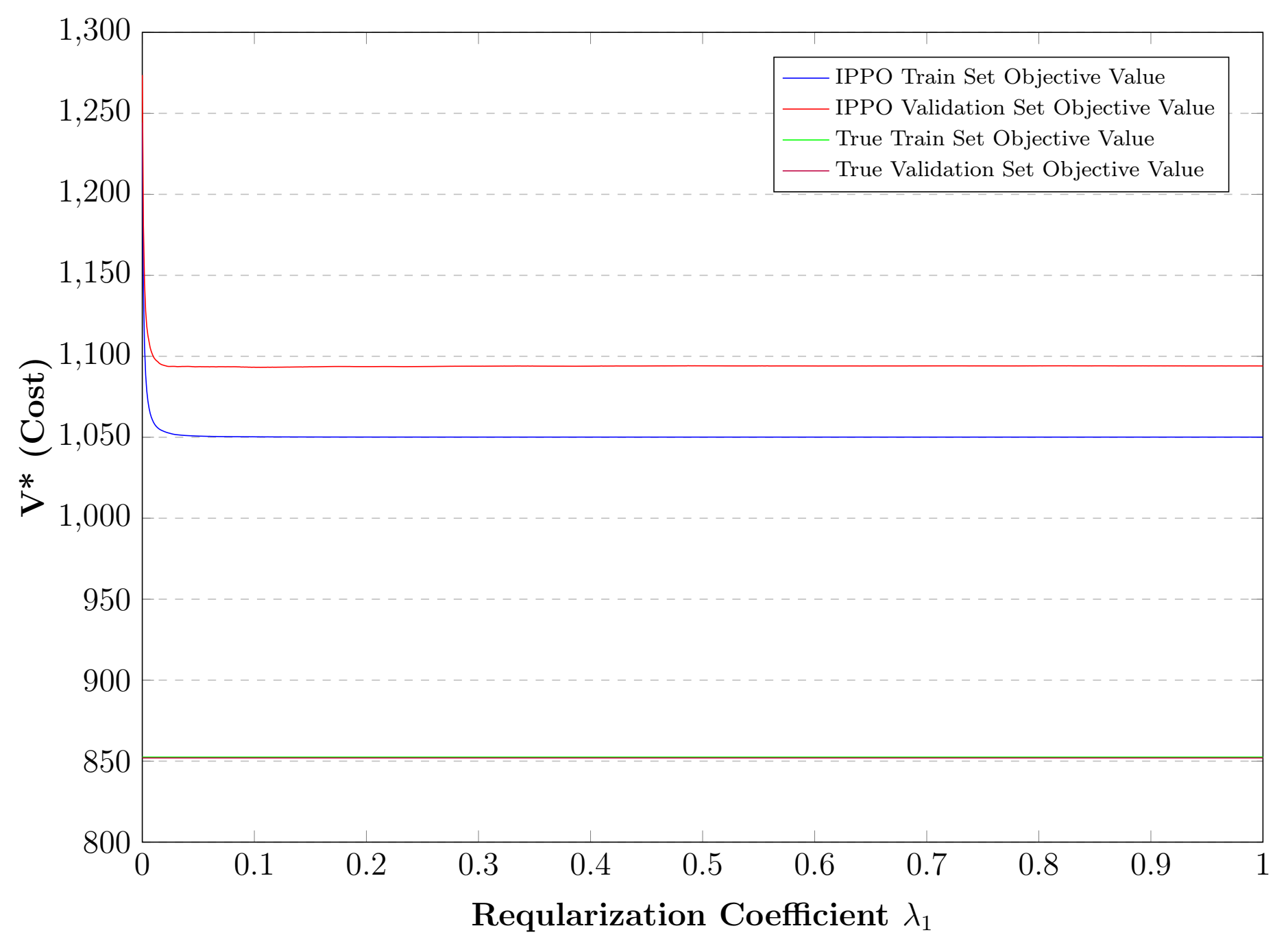

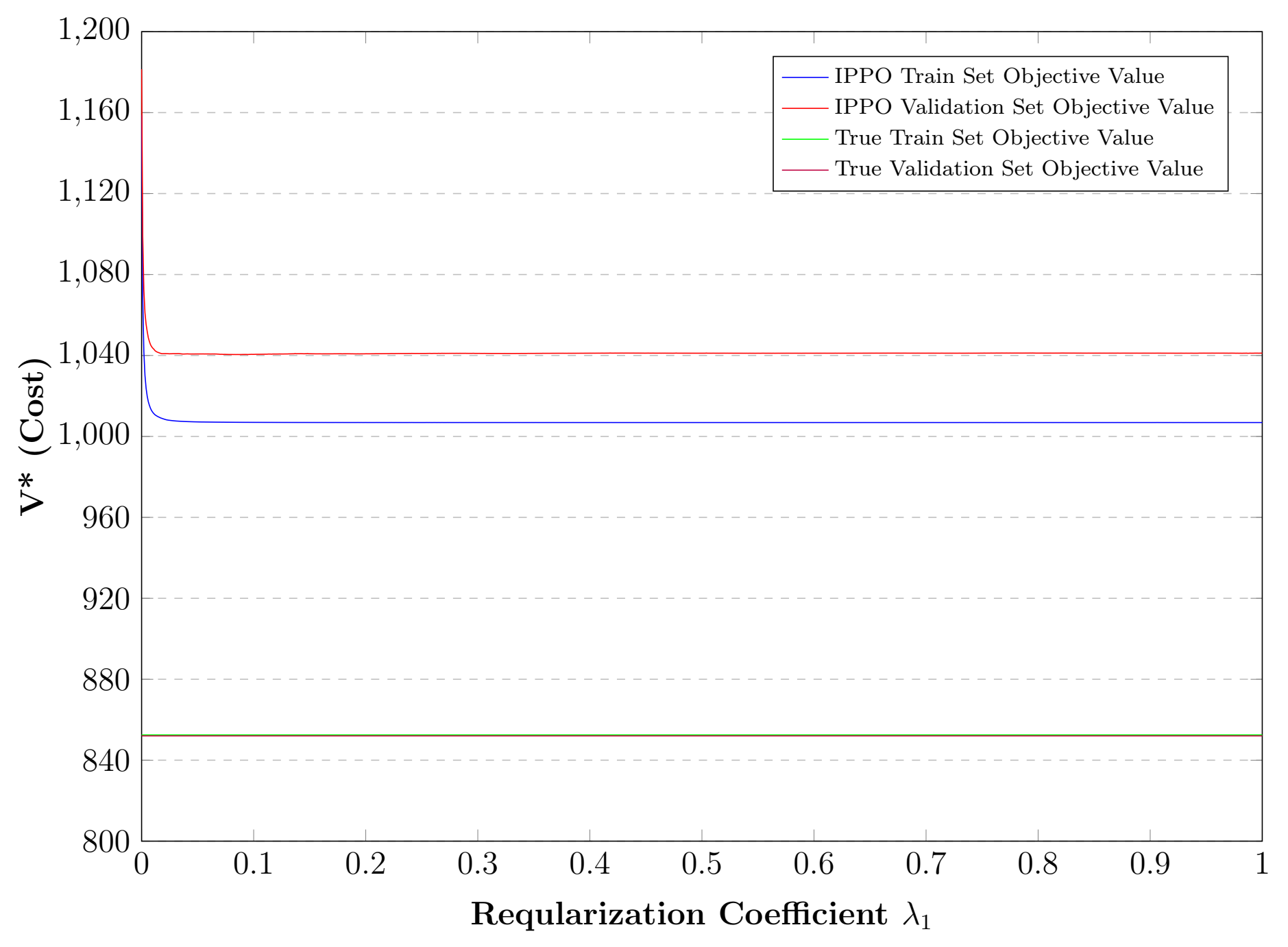

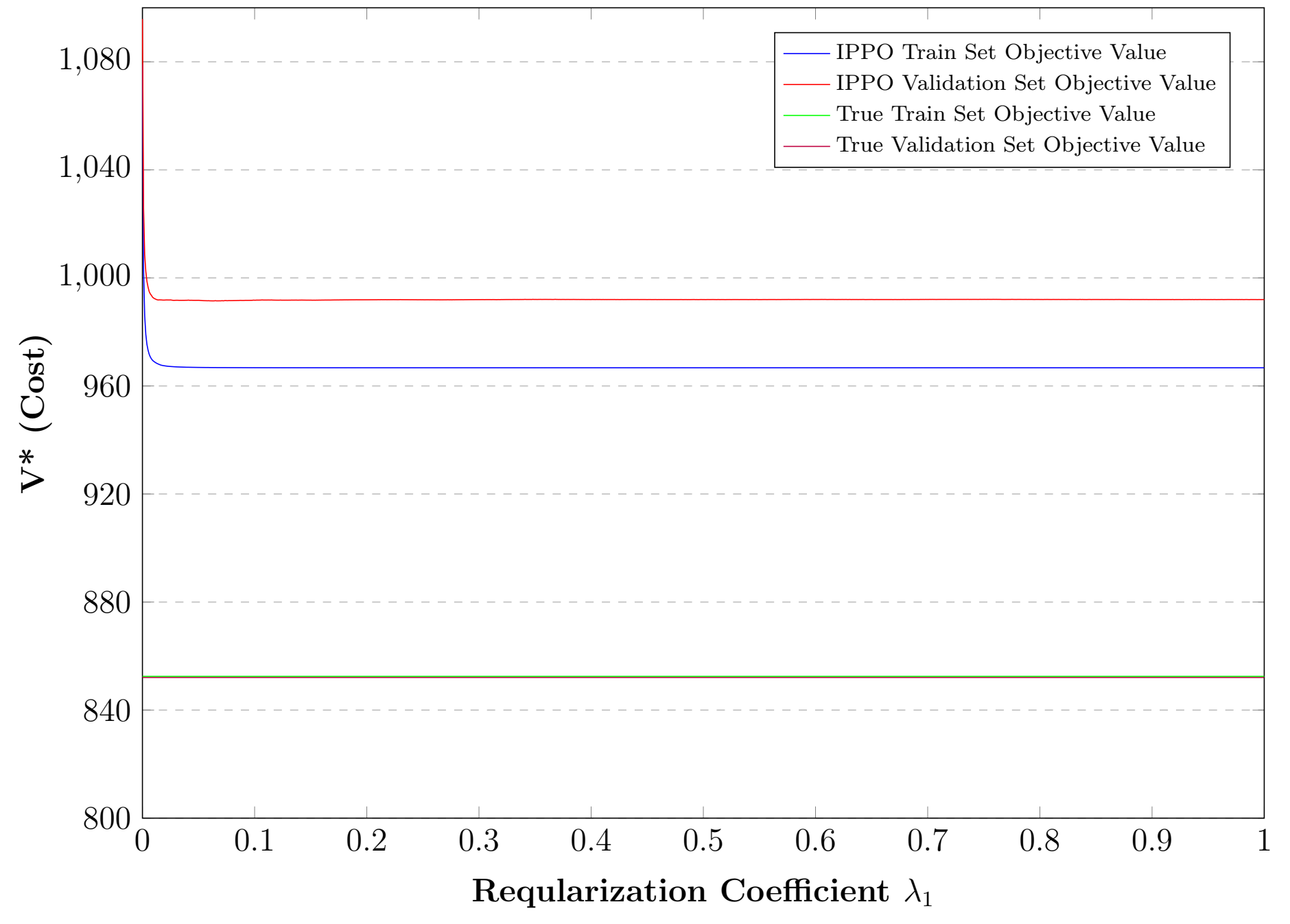

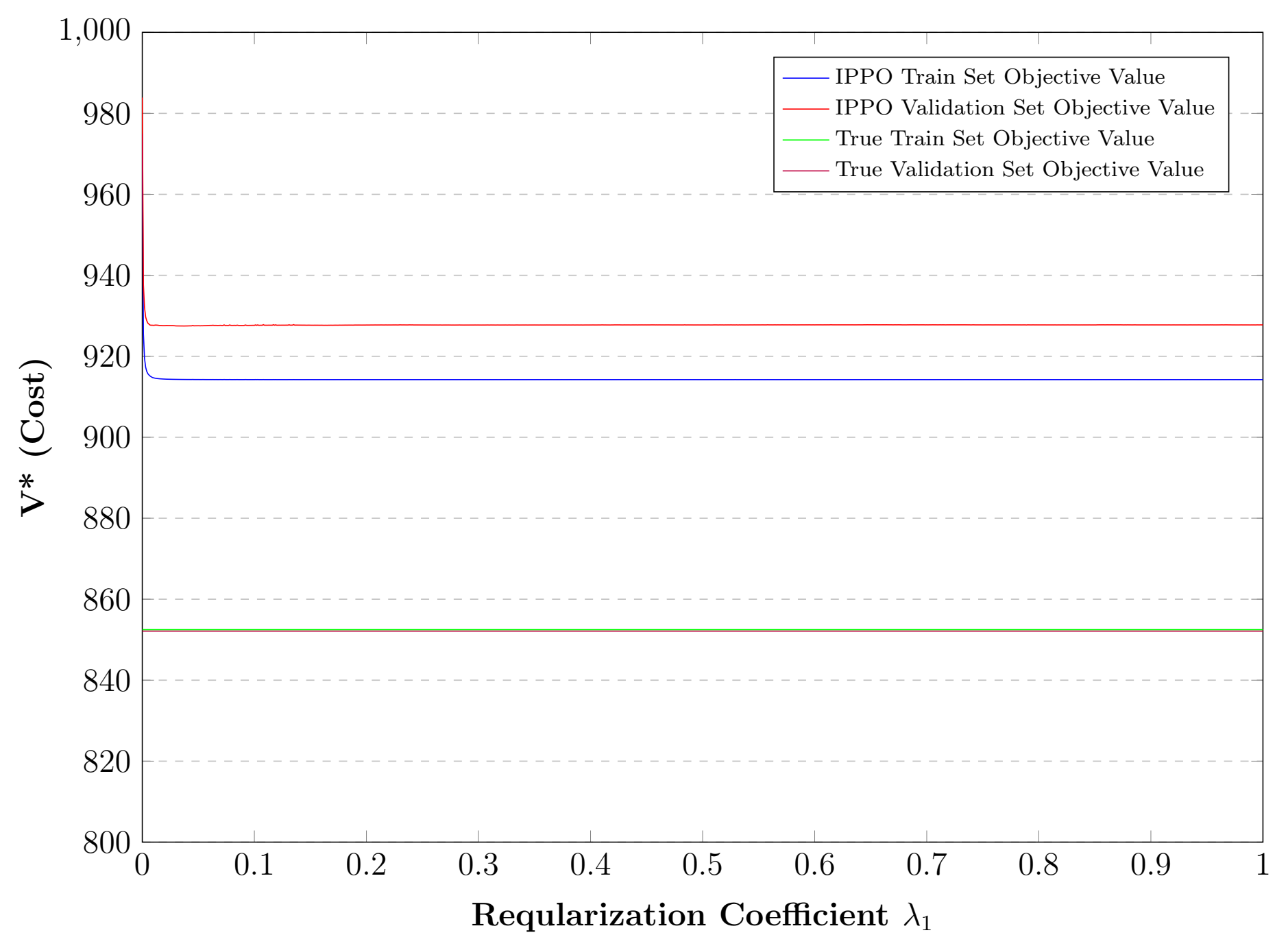

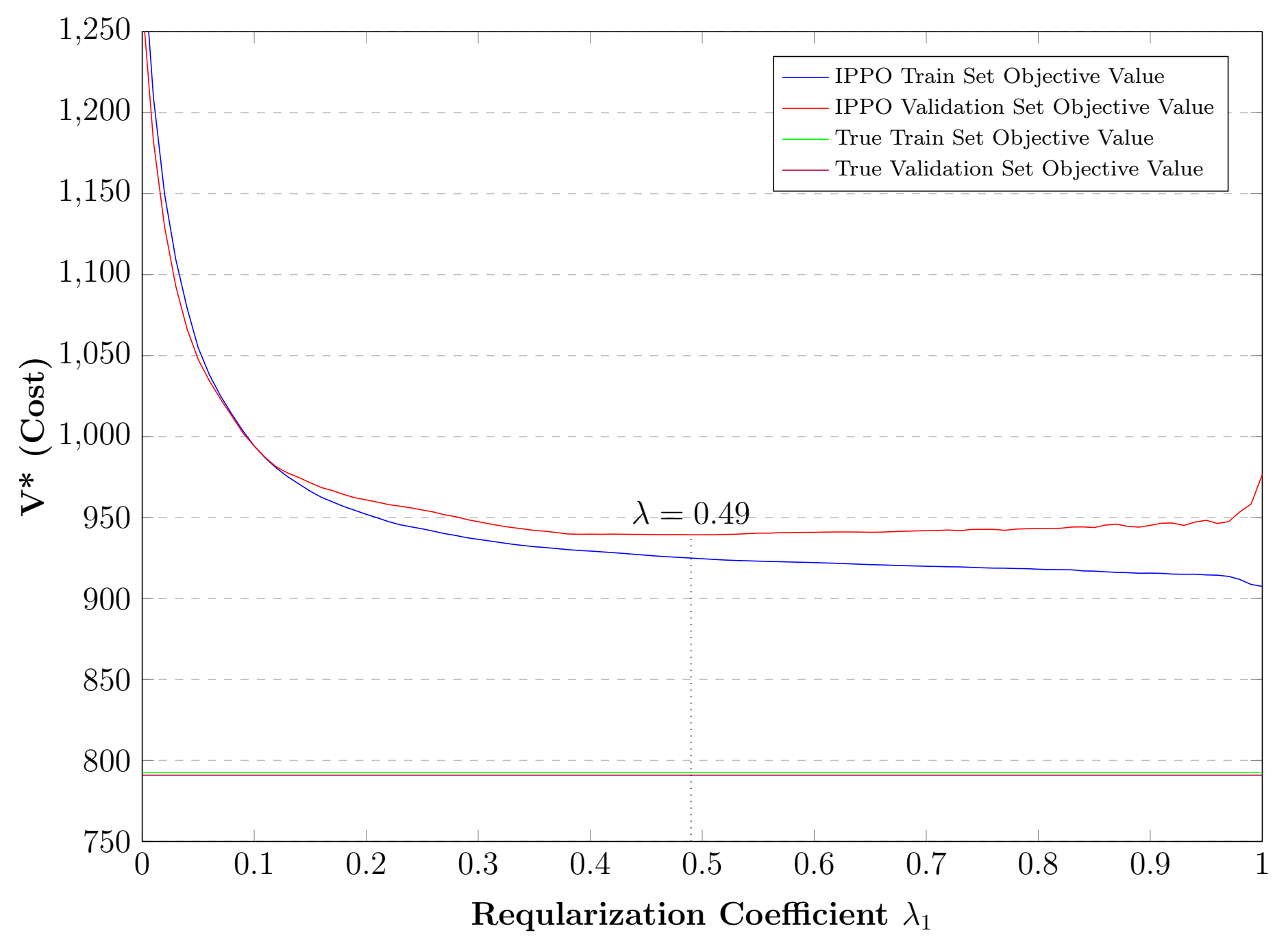

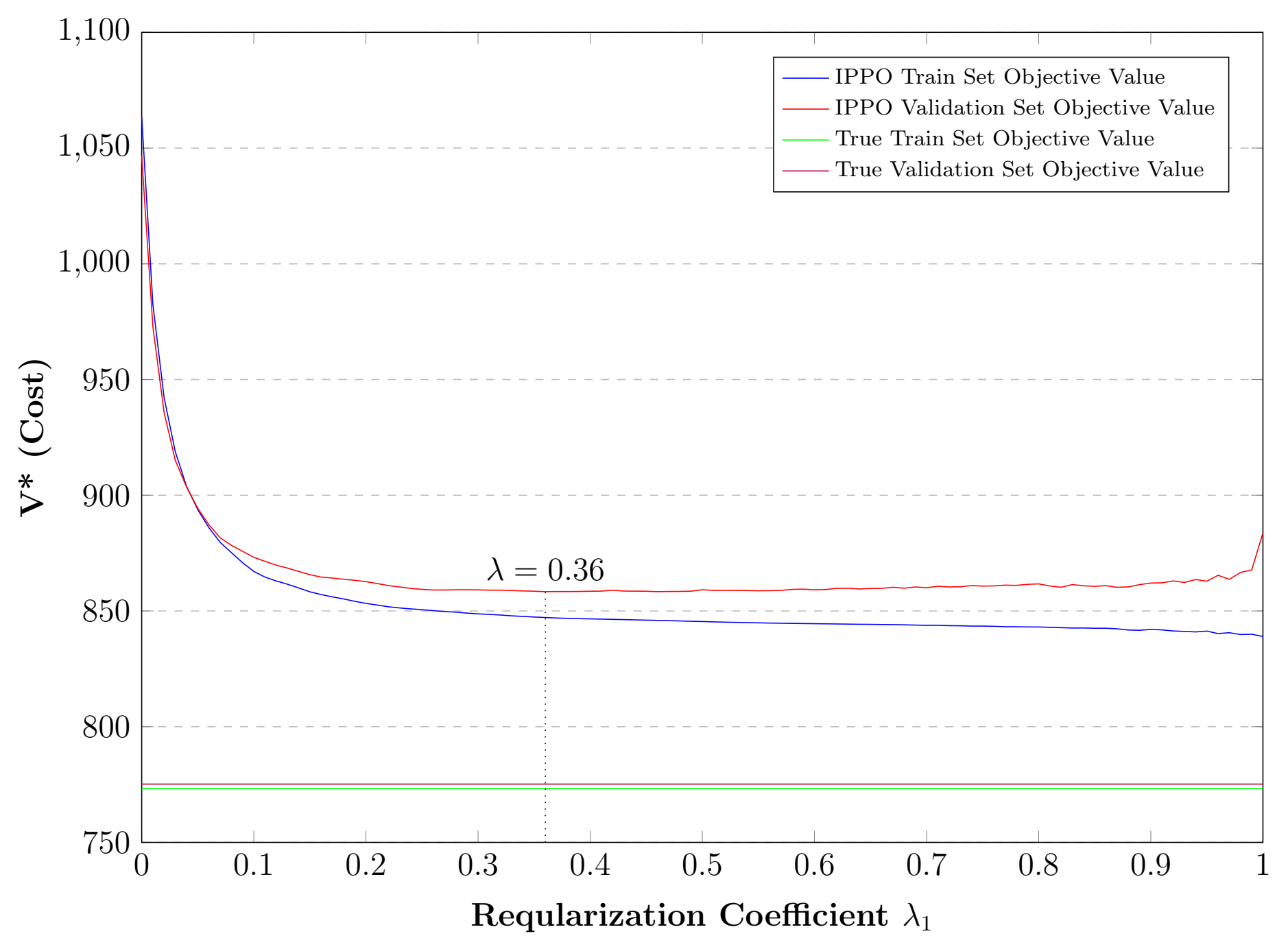

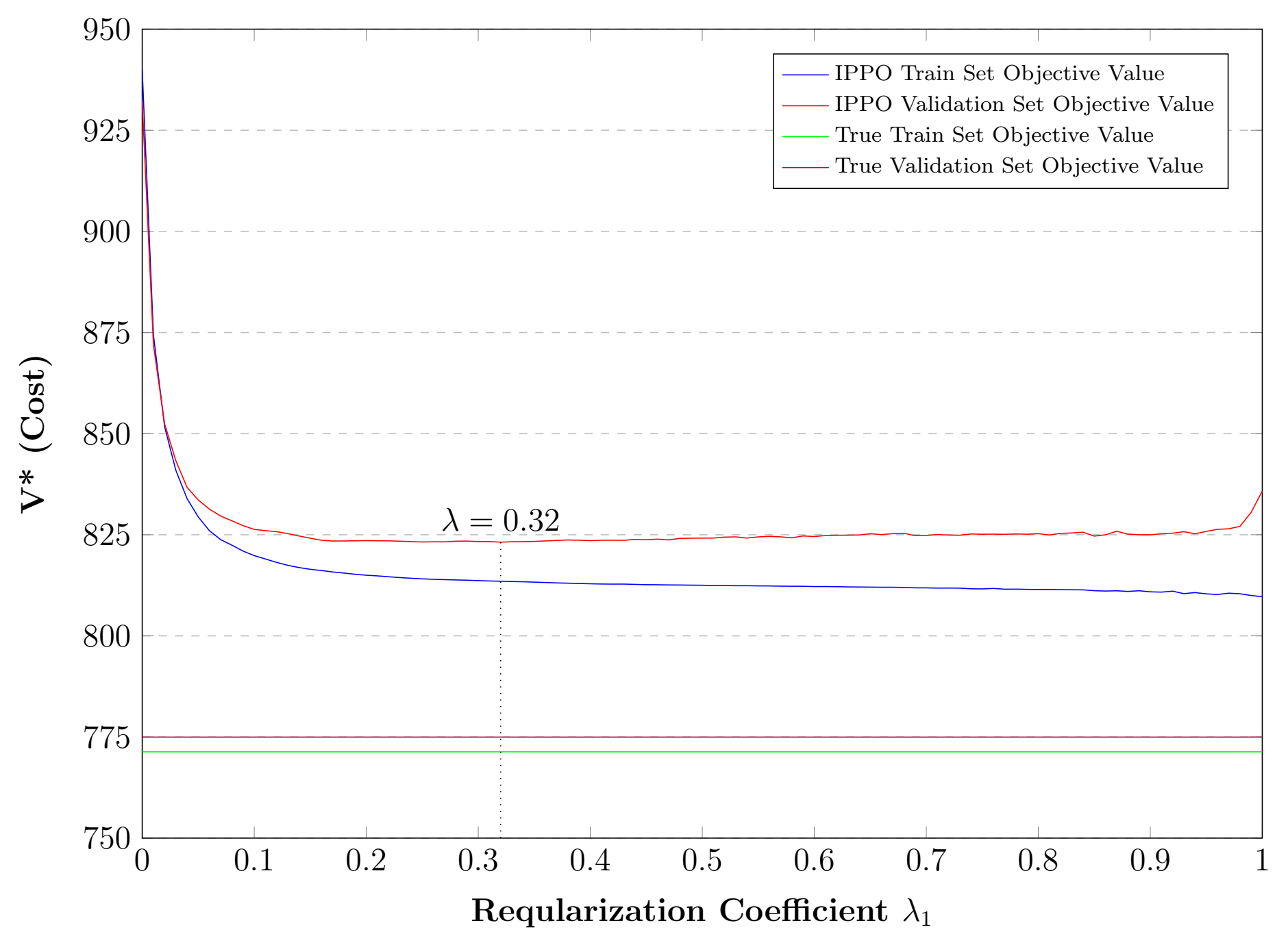

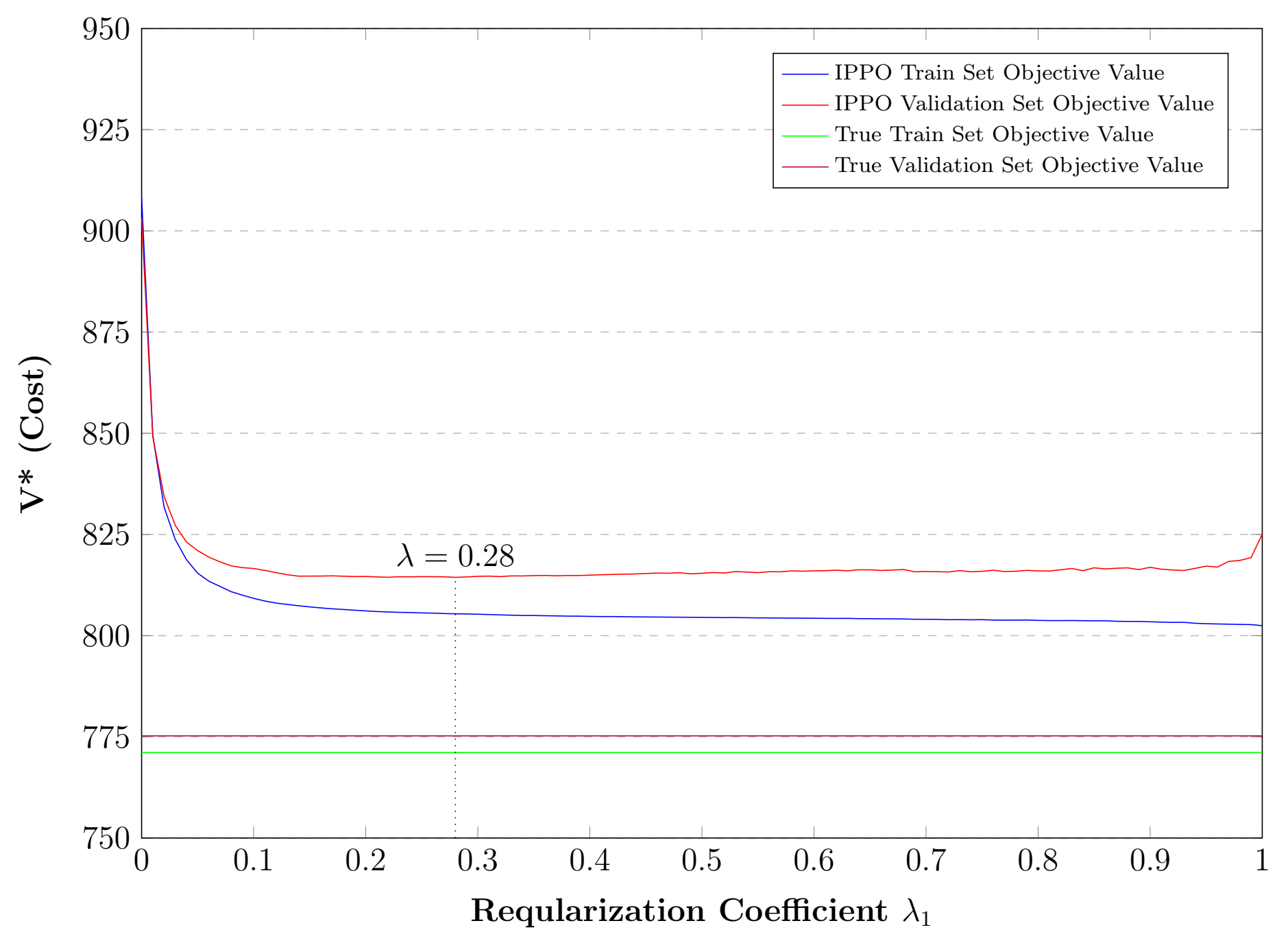

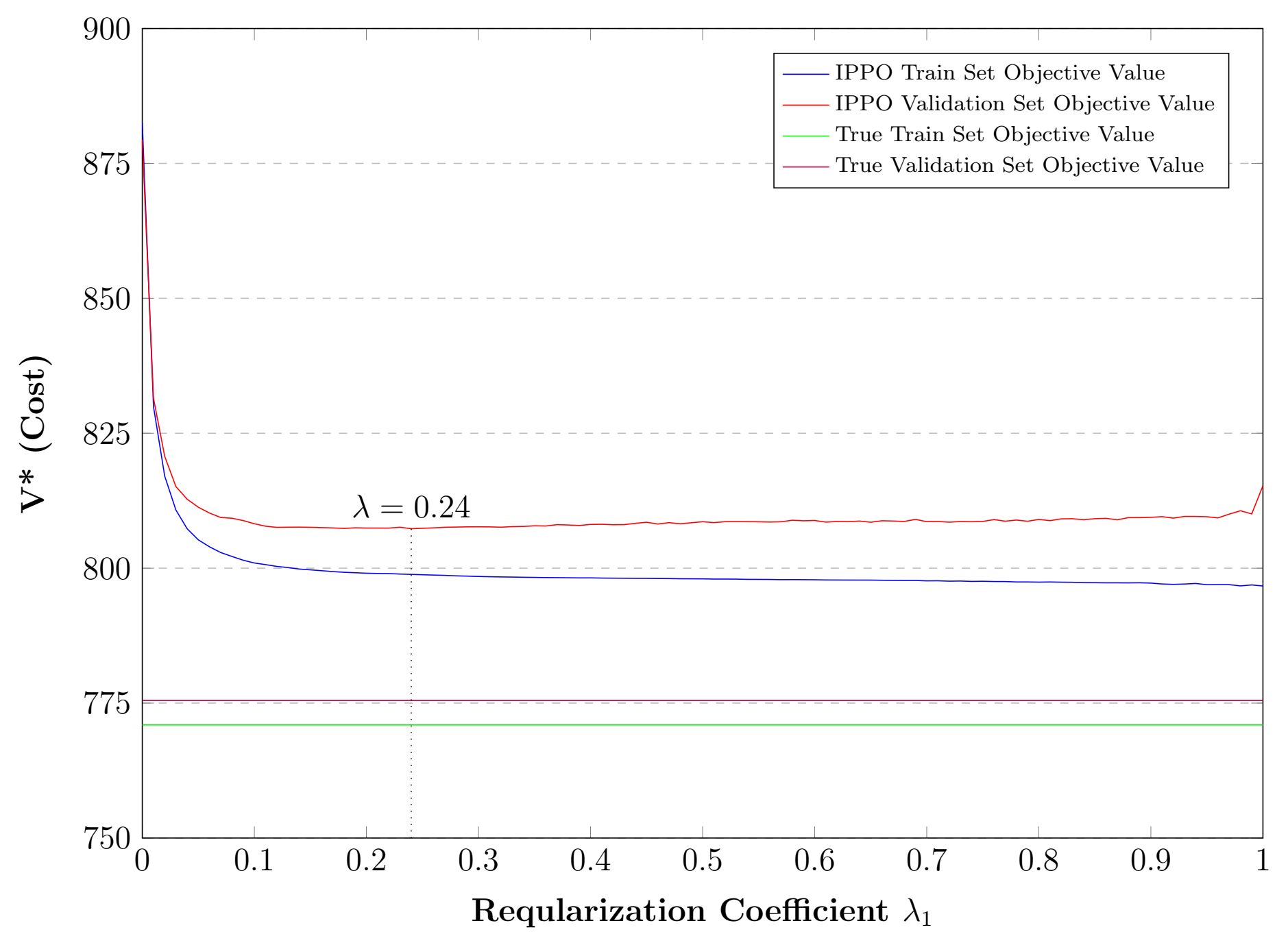

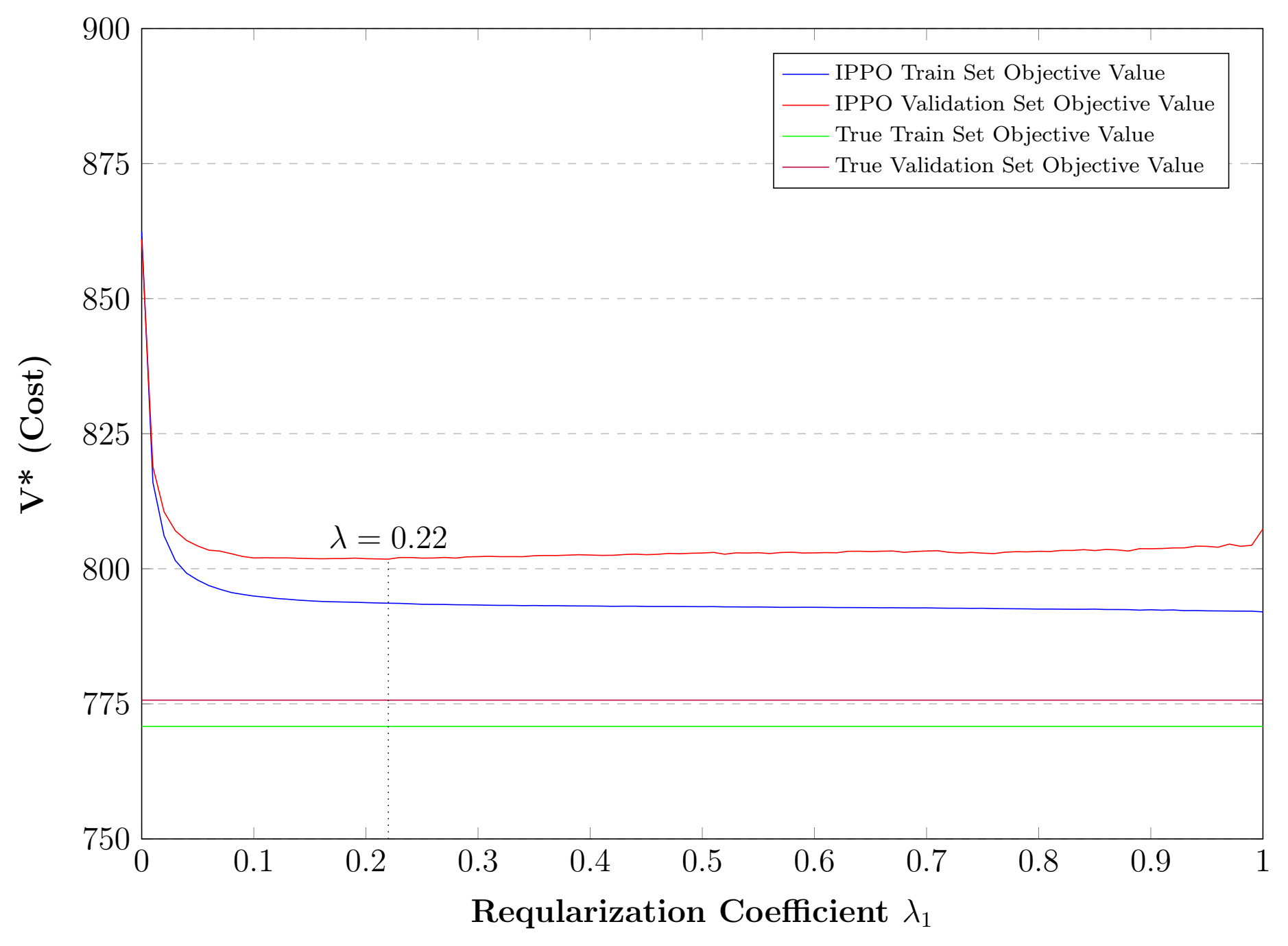

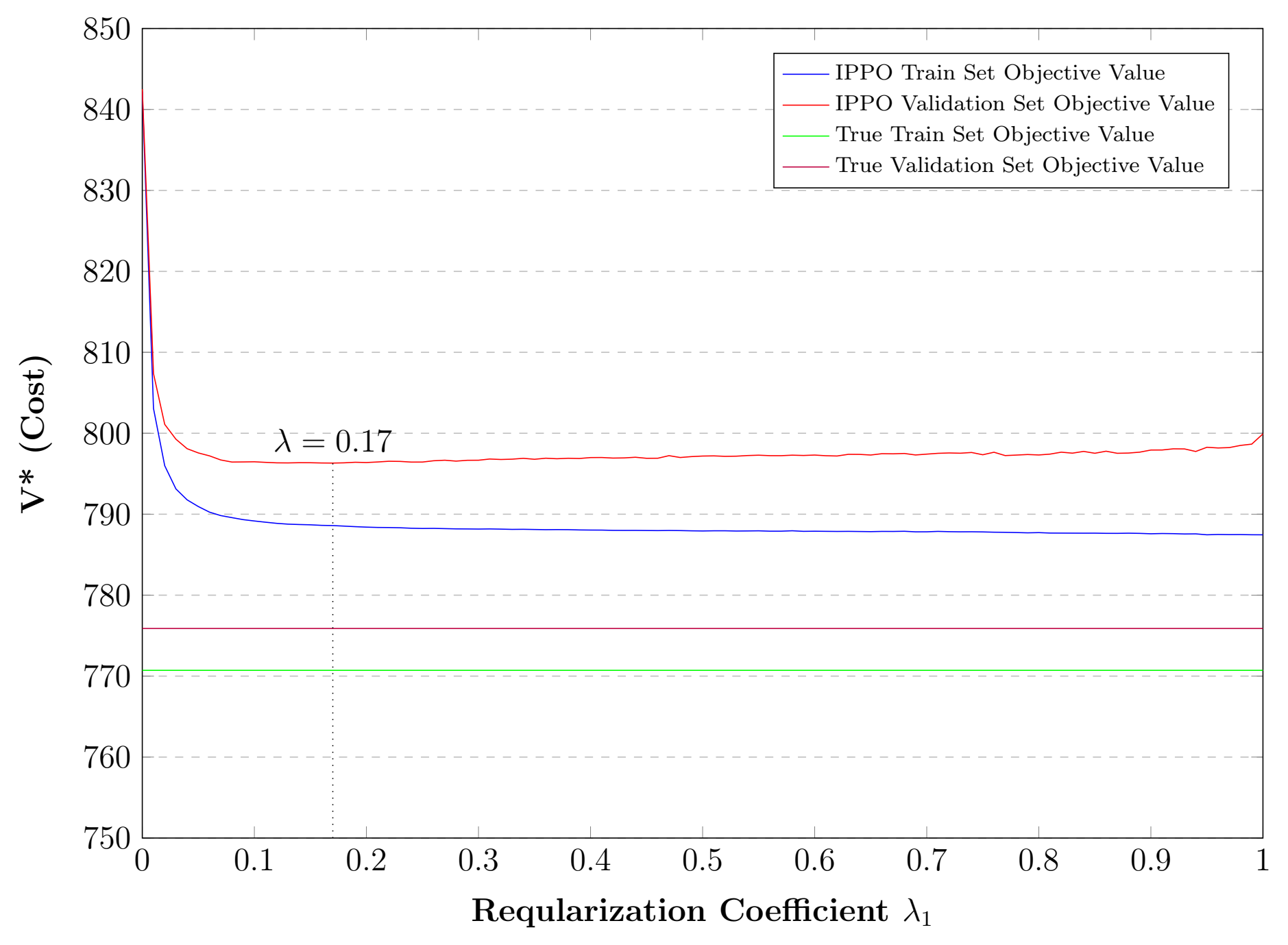

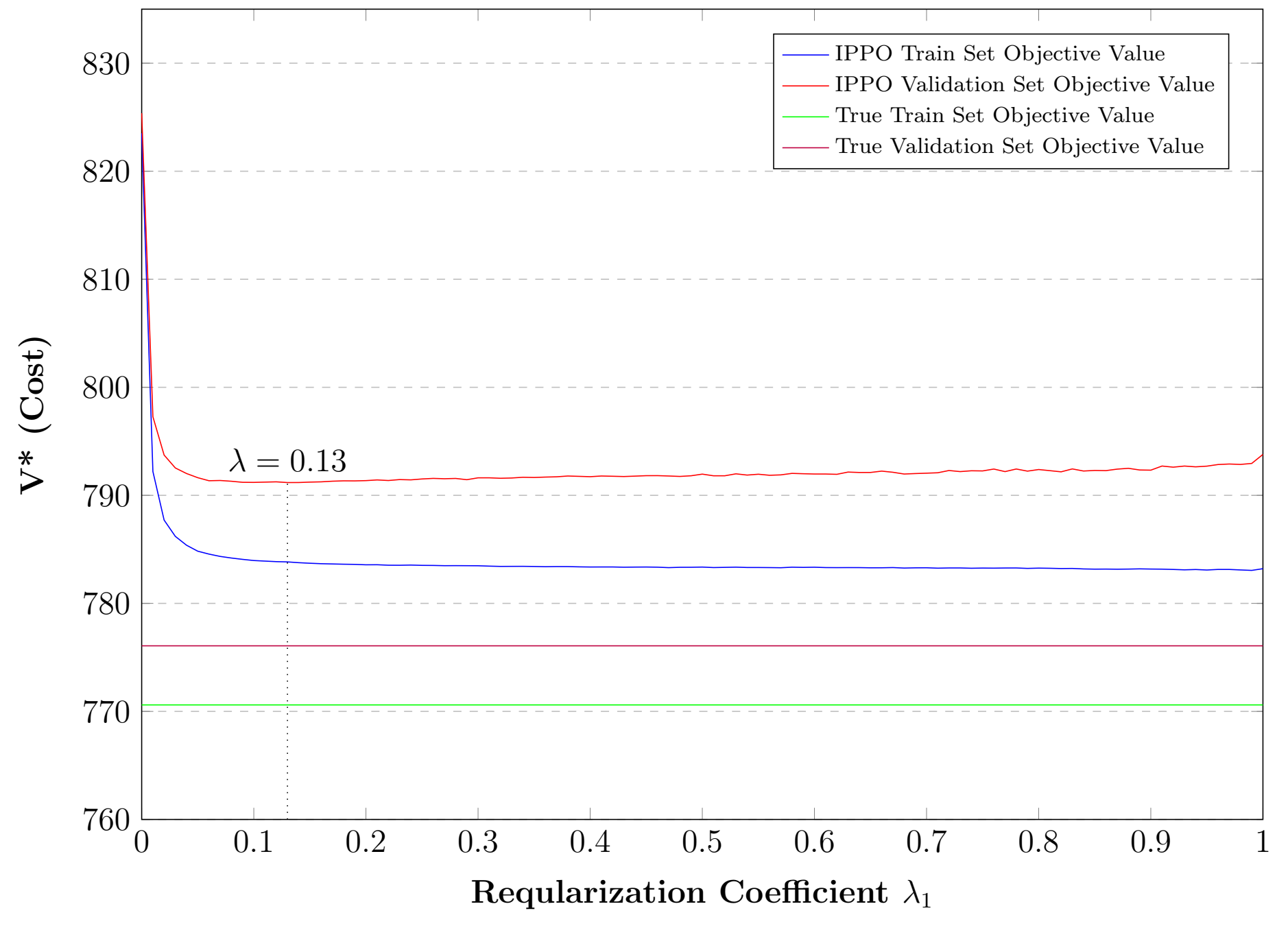

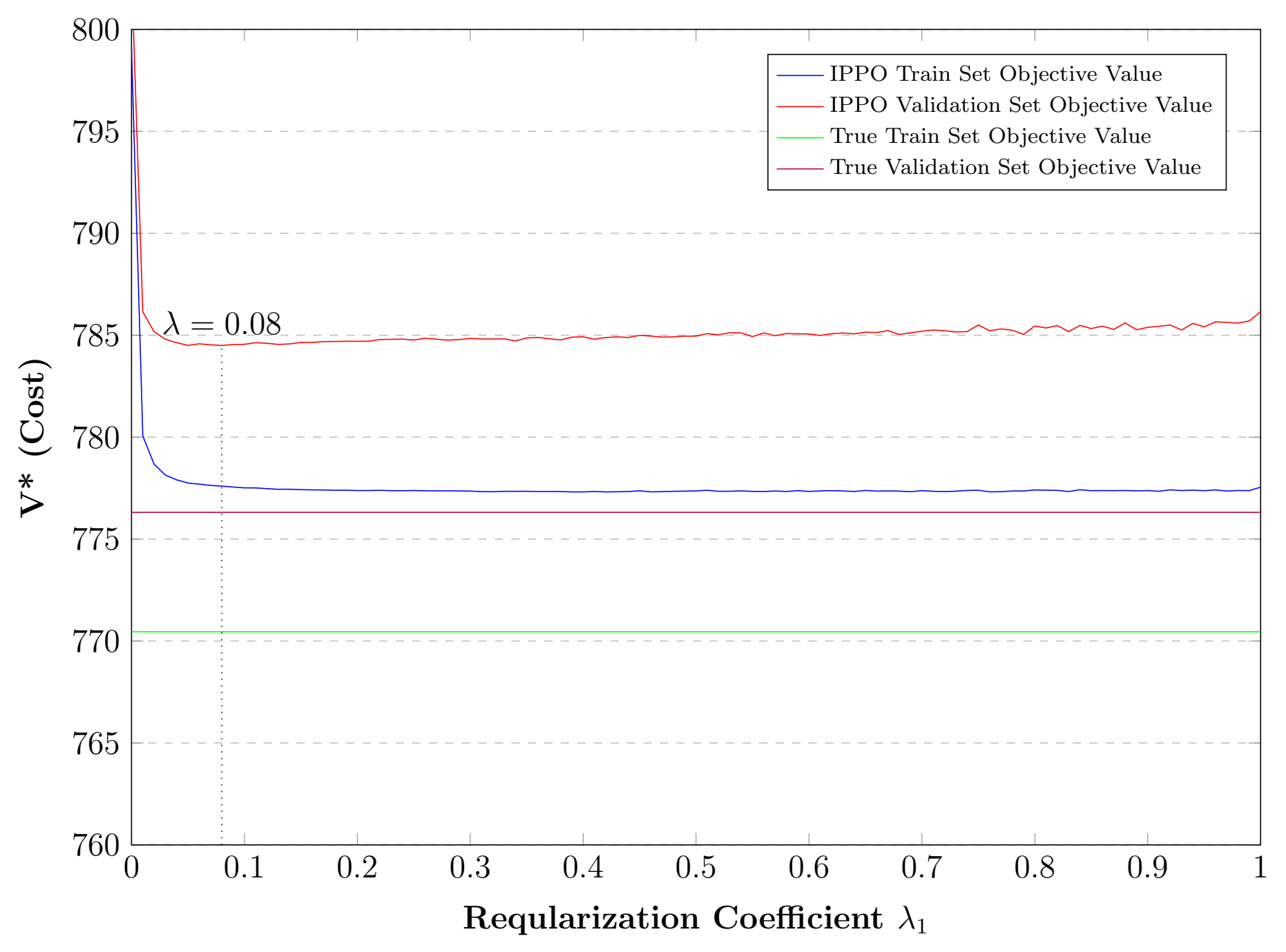

We observe similar behaviors here as in newsvendor problem. Main difference in Two-Stage shipment problem is IPPO overfits in especially low level and correlations since IPPO methodology fully leverages side information and searches best solution for train data set. As we see the effect of regularization coefficient () in Figure 7, train performance constantly improves, but validation performance become worse after some point. In figure 6, we report train and test performance with and without controlling generalization error. Although train performance is better than other methods without controlling generalization error, a better solution is achieved via optimizing regularization coefficient (). Some detailed statistical measures are given in Table 3 for train set and in Table 4 for test set. Performance column is calculated in Equation 15 based on second best method, which is The Feature-Based Optimization. These results are based on 30 replications, mean column is presented in Figure 6.

| (15) |

| Correlation between X and Y | True Objective Values | IPPO | Performance | Optimal Regularization Parameter | Optimal Neighbors for kNN | ||||||

| Mean | Max | Min | S.Dev. | Mean | Max | Min | S.Dev. | ||||

| %7 | 792.5 | 855.7 | 738.0 | 22.2 | 925.0 | 988.4 | 864.1 | 28.4 | %11 | 0.49 | 50 |

| %13 | 773.3 | 820.2 | 728.2 | 18.6 | 847.2 | 889.9 | 798.1 | 21.2 | %32 | 0.36 | 26 |

| %20 | 771.7 | 812.5 | 730.8 | 17.5 | 824.9 | 862.0 | 781.6 | 18.7 | %56 | 0.38 | 28 |

| %26 | 771.3 | 808.7 | 732.7 | 17.0 | 813.5 | 847.9 | 773.0 | 17.9 | %78 | 0.32 | 28 |

| %34 | 771.1 | 806.1 | 734.0 | 16.7 | 805.4 | 838.0 | 766.8 | 17.3 | %105 | 0.28 | 17 |

| %43 | 771.0 | 804.0 | 735.0 | 16.5 | 798.9 | 830.0 | 761.6 | 16.9 | %138 | 0.24 | 15 |

| %53 | 770.8 | 802.4 | 735.8 | 16.4 | 793.6 | 823.7 | 757.7 | 16.7 | %179 | 0.22 | 15 |

| %64 | 770.7 | 801.0 | 736.7 | 16.3 | 788.6 | 818.7 | 753.7 | 16.5 | %242 | 0.17 | 15 |

| %76 | 770.6 | 801.7 | 737.4 | 16.2 | 783.8 | 814.9 | 750.1 | 16.3 | %347 | 0.13 | 15 |

| %92 | 770.5 | 802.7 | 737.2 | 16.1 | 777.6 | 809.8 | 743.6 | 16.1 | %695 | 0.08 | 13 |

| Correlation between X and Y | True Objective Values | IPPO | Performance | Optimal Regularization Parameter | Optimal Neighbors for kNN | ||||||

| Mean | Max | Min | S.Dev. | Mean | Max | Min | S.Dev. | ||||

| %7 | 792.6 | 903.0 | 691.6 | 51.3 | 944.6 | 1089.4 | 821.4 | 67.6 | %15 | 0.49 | 50 |

| %13 | 773.8 | 857.3 | 690.3 | 40.0 | 859.6 | 932.8 | 766.6 | 46.8 | %34 | 0.36 | 26 |

| %20 | 772.6 | 845.3 | 695.1 | 36.3 | 834.6 | 901.8 | 751.0 | 40.0 | %57 | 0.38 | 28 |

| %26 | 772.4 | 838.6 | 697.9 | 34.5 | 821.6 | 886.0 | 742.4 | 37.2 | %80 | 0.32 | 28 |

| %34 | 772.4 | 834.8 | 700.3 | 33.4 | 812.4 | 874.8 | 736.5 | 35.4 | %105 | 0.28 | 17 |

| %43 | 772.3 | 833.2 | 702.3 | 32.5 | 804.8 | 865.6 | 731.1 | 34.0 | %138 | 0.24 | 15 |

| %53 | 772.3 | 831.9 | 703.6 | 31.9 | 798.9 | 858.5 | 728.0 | 33.0 | %178 | 0.22 | 15 |

| %64 | 772.3 | 830.6 | 704.1 | 31.4 | 793.2 | 851.4 | 724.3 | 32.1 | %238 | 0.17 | 15 |

| %76 | 772.2 | 829.4 | 704.6 | 30.9 | 787.7 | 844.8 | 720.9 | 31.4 | %343 | 0.13 | 15 |

| %92 | 772.2 | 827.8 | 705.3 | 30.4 | 780.6 | 836.1 | 714.4 | 30.6 | %691 | 0.08 | 13 |

6 Conclusion

In this work, we provide an integrated framework fully leveraging feature data to predict responds in order to take best actions in prescriptive task. This methodology can be employed in any prescriptive task whose parameters uncertain with feature data as long as prescriptive model is convex because KKT optimality conditions requires duality, hence limited to convexity. To be able optimize predictive and prescriptive tasks at the same time, predictive task must be in a linear form, so this limits the complexity of prediction task. However, alternative methods can be used to capture nonlinearity outside of proposed framework. Our purpose is to train predictive model based on not predictive error, but also based on prescriptive error which is the assessment of decision variables provided by predicted responses with respect to true responses. Bilevel models are NP-hard problems, and it is not easy to solve, but our framework is a special case, where all decision variables are based on scenarios except the parameters of predictive model. Thus this formulation can be easily decomposed by decoupling the parameters of predictive model, and solved by PHA step by step. Also, we demonstrate the behavior of our and other frameworks under different correlation of feature and response data. Finally, we provide our results and compare them to traditional and recently introduced methods, and we perform well with and even without controlling generalization error.

.

References

- [1] G.-Y. Ban and C. Rudin. The big data newsvendor: Practical insights from machine learning. Operations Research, 67:90–108, 2019.

- [2] J. F. Bard. Practical Bilevel Optimization: Algorithms and Applications (Nonconvex Optimization and Its Applications). Springer-Verlag, Berlin, Heidelberg, 2006.

- [3] A. Ben-Tal, L. El Ghaoui, and A. Nemirovski. Robust Optimization. Princeton Series in Applied Mathematics. Princeton University Press, October 2009.

- [4] Y. Bengio. Using a financial training criterion rather than a prediction criterion. International journal of neural systems, 8 4:433–43, 1997.

- [5] D. Bertsimas, D. B. Brown, and C. Caramanis. Theory and applications of robust optimization. SIAM Review, 53(3):464–501, 2011.

- [6] D. Bertsimas and N. Kallus. From predictive to prescriptive analytics. Management Science, 0(0):null, 2020.

- [7] J. R. Birge and F. Louveaux. Introduction to Stochastic Programming. Springer Publishing Company, Incorporated, 2nd edition, 2011.

- [8] G. B. Dantzig. Linear programming under uncertainty. Management Science, 1(3-4):197–206, 1955.

- [9] P. Donti, B. Amos, and J. Z. Kolter. Task-based end-to-end model learning in stochastic optimization. In I. Guyon, U. V. Luxburg, S. Bengio, H. Wallach, R. Fergus, S. Vishwanathan, and R. Garnett, editors, Advances in Neural Information Processing Systems 30, pages 5484–5494. Curran Associates, Inc., 2017.

- [10] A. N. Elmachtoub and P. Grigas. Smart ”predict, then optimize”. ArXiv, abs/1710.08005, 2017.

- [11] L. Gurobi Optimization. Gurobi optimizer reference manual, 2020.

- [12] Y. Kao, B. V. Roy, and X. Yan. Directed regression. In Y. Bengio, D. Schuurmans, J. D. Lafferty, C. K. I. Williams, and A. Culotta, editors, Advances in Neural Information Processing Systems 22, pages 889–897. Curran Associates, Inc., 2009.

- [13] A. J. Kleywegt, A. Shapiro, and T. Homem-de Mello. The sample average approximation method for stochastic discrete optimization. SIAM Journal on Optimization, 12(2):479–502, 2002.

- [14] A. Oroojlooyjadid, L. V. Snyder, and M. Takác. Applying deep learning to the newsvendor problem. ArXiv, abs/1607.02177, 2016.

- [15] R. T. Rockafellar and R. J.-B. Wets. Scenarios and policy aggregation in optimization under uncertainty. Mathematics of Operations Research, 16(1):119–147, 1991.

- [16] A. Shapiro. Monte carlo sampling methods. In Stochastic Programming, volume 10 of Handbooks in Operations Research and Management Science, pages 353 – 425. Elsevier, 2003.

- [17] A. Shapiro and A. Nemirovski. On complexity of stochastic programming problems. In V. Jeyakumar and A. Rubinov, editors, Continuous Optimization: Current Trends and Modern Applications, pages 111–146. Springer US, Boston, MA, 2005.

- [18] H. Stackelberg. The theory of the market economy. Oxford University Press, New York, Oxford, 1952.

- [19] R. Tibshirani. Regression shrinkage and selection via the lasso. Journal of the Royal Statistical Society, Series B, 58:267–288, 1994.

- [20] T. Tulabandhula and C. Rudin. Machine learning with operational costs. J. Mach. Learn. Res., 14:1989–2028, 2011.

- [21] Y. Zhang and J. Gao. Assessing the performance of deep learning algorithms for newsvendor problem. In ICONIP, 2017.