Forward indifference valuation and hedging of basis risk under

partial information

![[Uncaptioned image]](/html/2101.00251/assets/x1.png)

Abstract

We study the hedging and valuation of European and American claims on a non-traded asset , when a traded stock is available for hedging, with and following correlated geometric Brownian motions. This is an incomplete market, often called a basis risk model. The market agent’s risk preferences are modelled using a so-called forward performance process (forward utility), which is a time-decreasing utility of exponential type. Moreover, the market agent (investor) does not know with certainty the values of the asset price drifts. This market setting with drift parameter uncertainty is the partial information scenario. We discuss the stochastic control problem obtained by setting up the hedging portfolio and derive the optimal hedging strategy. Furthermore, a (dual) forward indifference price representation of the claim and its PDE are obtained. With these results, the residual risk process representing the basis risk (hedging error), pay-off decompositions and asymptotic expansions of the indifference price in the European case are derived. We develop the analogous stochastic control and stopping problem with an American claim and obtain the corresponding forward indifference price valuation formula.

I dedicate this work to my parents.

“Be happy for this moment. This moment is your life.”

Omar Khayyám, Persian mathematician, astronomer, and poet

Acknowledgments

I would like to thank my supervisor Professor Dr Michael Monoyios for his guidance, constructive suggestions and encouragement for this research work. I would also like to express my great appreciation to my employer d-fine, that made it possible for me to study at Oxford University by granting me a full scholarship. Finally, I wish to thank my parents for their restless support and encouragement throughout my studies.

1 Introduction

A fundamental theory of mathematical finance is the problem of a market agent who invests in a financial market in order to maximise trxivehe expected utility of his terminal wealth under his individual preferences. Problems of expected utility maximisation go back at least to the two seminal articles of Merton [90], [91] (see also Merton [92]), who studied the framework of time-continuous models, and the seminal article of Samuelson [119] treating the time-discrete case. Merton derived a non-linear partial differential equation (Hamilton-Jacobi-Bellman (HJB) equation) for the value function of the maximisation problem using methods from stochastic control theory.

The modern approach for solving such problems uses dual characterisations of portfolios through defining an appropriate set of martingale measures. Harrison and Pliska [49] developed a general stochastic model of a continuous, multi-dimensional, complete market and obtained the corresponding general Black-Scholes pricing formula. The setting of a complete market, where the martingale measure is unique, was also studied by Pliska [112], Cox and Huang [27], [28] and by Karatzas, Lehoczky and Shreve [70]. One of the main results is, that the marginal utility of the optimal terminal wealth is equal to the density of the martingale measure modulo a constant.

The setting of an incomplete market, where perfect hedging is not possible, is a more difficult case and was studied via time-discrete models by He and Pearson [50] and by Karatzas, Lehoczky, Shreve and Xu [71], who realised that the use of dual methods from convex analysis provided comprehensive solutions to stochastic control problems. The dual variational problem of the primal problem is formulated and solved with convex dual relationship as Bismut [17] demonstrated. Kramkov and Schachermayer [77] studied the classical utility maximisation problem under weaker assumptions on the model and on the utility function. Rogers [115] delved deeper into the theory by applying methods from functional analysis and presented various examples solved with duality methods (see also Žitković [138] and Berrier, Rogers and Tehranchi [16]). Davis [29], [30], Rouge and Karoui [118], Henderson and Hobson [51], [53], Musiela and Zariphopoulou [104] investigated utility-based hedging in an incomplete market case, where hedging becomes imperfect and a hedging error, the basis risk, remains. It is the risk associated with the trading of a derivative security on a non-traded underlying asset, hedged with a imperfectly correlated traded asset. Examples are weather derivatives or options on illiquid securities. Ankirchner and Imkeller [6] introduced a typical example for a cross hedge, where an airline company wants to manage kerosene price risk. Ankirchner et al. [5], [7], [8] dealt also with applied basis risk models. Monoyios [95] derived perturbation series giving accurate analytic approximations for the price and hedging strategy of the claim using an exponential utility and carried out an numerical performance analysis between the improved optimal hedge and the naive hedge with the traded asset. Kallsen and Rheinländer dealt with classical utility-based pricing and hedging using an quadratic hedging approach and extended the results obtained by Mania and Schweizer [87], Becherer [13] and Kramkov and Sîrbu [78]. Zariphopoulou [136] studied optimisation models with power utility and produced reduced form solutions of the indifference price by applying a distortion method to the indifference price PDE. The setting with exponential utility in a multi-dimensional model was treated by Musiela and Zariphopoulou [104]. Monoyios [96] derived representations for the optimal martingale measures in a two-factor Markovian model by using the distortion power solution for the primal problem to obtain a dual entropic representation of the stochastic control problem. We refer to the introductions of the aforementioned papers for more references in the field of classical utility-based optimisation problems.

Monoyios [97] explored the impact of drift parameter uncertainty in an incomplete market model having an European option on a non-traded asset hedging a correlated traded stock. He developed analytic expansions for the indifference price and hedging strategies. The key approach is the development of a filtering approach, the Kalman-Bucy filter, in which the investor updates the market price of risk parameter from the observations of the asset prices. Applications of filtering can be found in Kallianpur [65], Rogers and Williams [116] and Fujisaki et al. [47]. Filtering originates from signal processing by Wiener [135] and Kolmogorov [60] during the 1940s. In the 1960s, it was further development by Kalman and Bucy [67], [68]. The setting, in which the investor does not observe the assets’ Brownian motions is called the partial information scenario. Problems under partial information scenarios were also studied by Rogers [114], Lakner [82] and Brendle [21]. Monoyios [98] used a two-dimensional Kalman-Bucy filter with Gaussian prior distribution in a partial information model and derived the optimal hedging strategy and indifference price representations using dual methods. Dependent on the prior estimations of the asset price drifts, the price representations formulas uses the minimal entropy martingale measure or the minimal martingale measure.

Musiela and Zariphopoulou [105], [106], [107] introduced a new class of forward utilities (forward performances) that are generated forward in time. They discussed associated value functions, optimal investment strategies and indifference price representations. They defined the concept of forward performance processes in order to quantify the dynamically changing preferences of an investor. Independently, Henderson defined in [52] and Henderson and Hobson [54] analysed the same class of dynamic utilities, but called them horizon-unbiased. Forward utilities are defined by the dynamic programming principle and ensure more flexibility as they are specified for today and not for a fixed future time. Berrier and Theranchi [15] broadened the definitions by adding a process for the investor’s consumption.

In this work, we investigate the utility-based valuation of European and American claims on a non-traded asset , when a correlated traded stock is available for hedging, with and following correlated geometric Brownian motions, and when the agent’s risk preferences are modelled using the forward performance process from Musiela and Zariphopoulou [106], and when the agent does not know with certainty the values of the asset price drifts. Since the market becomes incomplete, we retain an unhedgeable (basis) risk. The basis risk model will first be constructed under a standard full information hypothesis, where the drifts of both assets are known constants. In this setting, the utility-based valuation of European claims on has been well studied, using classical (as opposed to forward) exponential utility. The partial information case, where the asset drifts are taken as unknown constants, whose values are filtered from price observations, has also been studied for European claim valuation using classical utility (see, for example, Monoyios [98]). The thesis will investigate the valuation and hedging of European and then American claims on with a exponential forward utility under partial information. We apply the partial information model with the Kalman-Bucy filter from Monoyios [98] to get analogous results for valuation and hedging with forward instead of classical utility. The novel approach is the embedding of the specific partial information model, making the market prices of risks depending on both asset prices, into the aforementioned forward performance framework. We compare the optimal hedging strategies and indifference price representations for European and American claims associated with forward and classical utility under the partial information scenario. One of the key results is the change of optimal measure from the minimal entropy martingale measure to the minimal martingale measure . In the European option’s case, we obtain the dual representation of the forward indifference price with its semi-linear PDE of second order, the residual risk, a pay-off decomposition of the European claim and an asymptotic expansion of the forward indifference price. In the case of an American claim, we define the control and stopping problem and derive the dual representation of the forward indifference price under the partial information model.

Oberman and Zariphopoulou [108] and Leung and Sircar [83] studied the valuation and hedging of American options in a basis risk model under full information using classical utility. Leung, Sircar and Zariphopoulou [84] investigated the full information model using forward utility to price executive stock options (ESOs). ESOs are American calls issued by a company to its employees (mostly executives) as a form of variable payments as instruments for motivation (cf. Kraizberg et al. [76], Chen et al. [23], Brandes et al. [20]). We extend the framework of Leung, Sircar and Zariphopoulou [84] to the partial information model, derive the indifference price valuation and prepare the groundwork for future applications.

The remainder of the dissertation is organised as follows. In Section 2 the basis risk market model in the full and partial information scenarios, the concept of filtering and forward utilities defined via a certain class of risk tolerance functions are treated. The forward utility-based valuation and hedging problem with an European option is dealt in Section 3. It begins with the setting of perfect hedging in a complete market and continues with the incomplete market case, followed by the formulation of the performance maximisation of the investor’s hedging portfolio. The problem is solved with dual methods and results in the optimal hedging strategy and the dual representation formula for the forward indifference price. Furthermore, the residual risk of the strategy, option’s pay-off decompositions and an asymptotic expansion for the forward indifference price are derived. In Section 4 we set up the partial information model with an American option, which can be early exercised and develop the (dual) optimal control and stopping optimisation problem and obtain the entropic representation of the forward indifference price. We conclude in Section 5 by performing an analysis of essential model assumptions and results obtained in this work, and discuss alternatives from present topics as well as future directions for research.

2 Basis risk model

In this section the financial market is modelled by a basis risk model premised on the geometric Brownian motion. A distinction is made in the assumption of the asset price Sharpe ratios, which leads to the full information scenario for certain Sharpe ratios and partial information scenario for uncertain Sharpe ratios. The Kalman-Bucy filtering approach is developed and applied to the partial information scenario to transform it into the case of full information. Lastly, the concept of forward utility is introduced as a dynamic extension of the classical utility theory and used within the basis risk model. Herein, a useful function called local risk tolerance serves the classification of forward utility functions.

2.1 Full information scenario

The classical basis risk model defined in this subsection was initially explored by Davis [30]. Consider a filtered probability space as the setting of a financial market, where the terminal filtration is generated by the two-dimensional standard -Brownian motion with correlation between the Wiener processes and . A traded stock price follows a geometric Brownian motion process given by

| (1) |

in which the stock’s volatility and its market price of risk (MPR) or Sharpe ratio with drift are known constants. For simplicity, the risk-free market interest rate is taken to be zero. A non-traded asset follows the correlated geometric Brownian motion

| (2) |

with and known constants. The Brownian motion from the non-traded asset dynamics is correlated with the stock’s Brownian motion according to with a known constant as the correlation coefficient. In the case , the market is called complete and perfect hedging is possible; see Subsection 3.1. If , the market is called incomplete.

An investor with initial wealth dynamically rebalances his portfolio allocations between the stock and the riskless money market account according to his -predictable (portfolio or trading) strategy (), that is an -integrable process representing the number of shares held in the portfolio (respectively the cash amount invested in the stock). Contextually, both and are called strategy. Under self-financing trading condition, the investor’s portfolio wealth is denoted by the positive process and satisfies

| (3) |

The process given by the stochastic integral

represents the profit and loss from trading up to time . The next definition gives the space of admissible trading strategies to make the market model suitable for measure changes.

Definition 2.1.1 (Relative entropy and admissible strategies).

The set of equivalent local martingale measures and its subset of measures with finite relative entropy

| (4) |

between and are assumed to be non-empty. The set of admissible strategies is

| (5) |

where is the superset of -predictable and -integrable strategies. An admissible strategy satisfies almost surely for each . ∎

Condition (5) for admissible strategies is taken from Becherer [12, pp. 28–29] (see also Mania and Schweizer [87, p. 2116]) and appears as one of the candidate sets () examined in Delbaen et al. [33, p. 104]. The latter paper prove that for three different choices of the resulting primal and dual problem have the same value and thus establish in particular a robustness result for the duality of classical exponential utility-based hedging.

The relative entropy was introduced in information theory by Kullback and Leibler [80] and developed by Kullback in his book [79]. It is with equality if and only if . The profit and loss process is identical to and hence the martingale property in (5) holds also for the wealth process . With the choice of admissible strategies, arbitrage opportunities for the investor are excluded. More on arbitrage and self-financing strategies can be found in Jeanblanc et al. [61, pp. 81–84]. Since the MPRs are assumed to be constants, the investor has access to the so-called background filtration and hence is able to observe the Brownian motion process , as well as the stock price process . This set-up is referred to as a full information scenario.

Remark 2.1.2 (Solution to the stock price SDE).

To solve (1), firstly apply Itô’s lemma on the logarithmic stock prices,

and the integrate over to obtain

If the MPR or volatility were not constant, then an integral would remain in the expressed solution. ∎

2.2 Partial information scenario

Based on historical data analyses from Ang and Bekaert [4], Clarke et al. [24] and French et al. [45], one might assume that the parameter values for an annual stock return (drift) and volatility are and respectively, so that the Sharpe ratio is per annum. Nevertheless, as outlined in Rogers [114, pp. 144–145], a proper estimation of in the asset price dynamics (1), (2) is practically impossible, due to the lack of long-term historical market data. The subsequent argument for the MPR parameter uncertainty is taken from Monoyios [97, pp. 342–343]. The normalised stock returns can be observed by the investor over a time interval , to make the best estimate

which leads to a 95% confidence interval for . In order to determine with 95% confidence the observation time for the estimated value being 5% to within of its true value , meaning , the equality needs to be solved, which gives years. This calculation shows, how intrinsic the MPR parameter uncertainty in log-normal models is, since reliable historical price data for such a long period is not available, considering that two of the first formal exchanges worldwide, the Frankfurt Stock Exchange and the London Stock Exchange, were established in the late 16th and 17th centuries respectively, according to Holtfrerich [57, p. 77] and Michie [93, p. 15].

The asset volatilities and the correlation are assumed to be known constants, because they can be inferred from quadratic and co-variations

through the best estimators

when price observations are taken to be approximately continuous. The problem of estimating quadratic variation using realised variance is discussed in Barndorff-Nielsen and Shephard [10]. Chakraborti et al. [22] analysed asset correlations on an empirical basis. If the requirement of constant MPRs is omitted, the agent will have no access to the background filtration , but instead, only to the so-called observation filtration , which is generated by the asset price processes and . Hence, only the observation of but not the Brownian motion process is possible. The values of the parameters become uncertain, so they can be modelled as random variables. This set-up is referred to as a partial information scenario. An agent with full information (partial information) is called outsider (insider) (see Henderson, Kladívko and Monoyios [55]).

2.3 Kalman-Bucy filtering

General filtering theory deals with the estimation of an unobservable stochastic process given a related observable process. Treatments of filtering theory can be found in Kallianpur [65, Chapter 10], Rogers and Williams [116, pp. 322–331] and Fujisaki et al. [47]. Wiener [135] and Kolmogorov [60] paved the way for filtering problems in the frequency domain in signal processing theory during the 1940s. In the 1960s linear filtering theory was developed further by Kalman [67] and Kalman and Bucy [68], where filtering problems were considered in the time rather than frequency domain with state space representations.

The partial information scenario can be converted into a full information scenario by changing from the background to the observation filtration using the so-called Bayesian approach in a Kalman-Bucy filtering framework. Following Monoyios [98], the asset MPRs are modelled as -random variables with a given initial distribution conditional on .

Definition 2.3.1 (Observation and signal process).

Define the two-dimensionalobservation process by

| (6) |

given the dynamics (1) and (2), generating the observation filtration , . The corresponding unobservable signal process is given by

| (7) |

which is an unknown two-dimensional constant in this market model. Moreover, assume a Gaussian prior distribution

| (8) |

for given constant parameters . ∎

From Remark 2.1.2, the solutions of the asset prices to the SDEs (1), (2) are

| (9) | ||||

from which the observation process may be expressed as deterministic functions of the asset prices and time,

For any process expressed by a function of time and current asset prices, the abbreviation may be used. The SDEs of the observation and signal process (6), (7) are

According to (8), an unbiased estimator of is Gaussian with initial estimations for .

The idea behind the Kalman-Bucy filter is to choose a prior distribution with specific parameter values for the MPR process and continuously update it over time. The prior distribution initialises the probability law of conditional on , and through filtering done in the next definition, this is updated with the evolution of the asset prices under the observation filtration . An in-depth discussion of this filtering procedure is made in Section 5. We describe in Remark 2.3.4 a partial information model apart from the Kalman-Bucy filter.

Definition 2.3.2 (Kalman-Bucy filter).

The optimal filter process defined by , is the two-dimensional MPR process under conditional expectation, for , . The conditional covariance matrix process is given by

| (10) |

for , . ∎

The Kalman-Bucy filter transforms the partial into a full information scenario by replacing the constant parameters by stochastic processes and changing the filtration of the probability space from to the observation filtration . The upcoming result of the partial information model under come from Monoyios [98].

Proposition 2.3.3 (Model under partial information).

The Kalman-Bucy filter from Definition 2.3.2 converts the model from the partial to the full information scenario with asset price SDEs

| (11) |

on the filtered probability space , where are -Brownian motions with correlation according to and are -adapted processes. For , with , the drift processes are

where for and for . They satisfy the SDEs

| (12) | ||||

with the entries of the covariance matrix in (10), given by

Proof.

A proof can be found in Monoyios [98, Proposition 1]. ∎

Thus, under partial information, the investor’s portfolio wealth dynamics from (3) is transformed into

| (13) |

If the prior variances are identical, then and hence holds for all . This case of filtering is similar to the two one-dimensional Kalman-Bucy filters on each asset as developed in [97]. According to Proposition 2.3.3, the MPR of the asset prices have the dependencies

| (14) |

solving the SDEs

In the remainder of this thesis, except where otherwise stated, we are working with the partial information model of Proposition 2.3.3.

Remark 2.3.4 (Ornstein-Uhlenbeck model for MPRs).

A more complicated method of modelling the MPRs would implicate an unknown stochastic process for each unknown MPR. For instance, the MPR dynamics could be expressed as processes of Ornstein-Uhlenbeck type,

| (15) |

with Brownian motions and constant mean reversion rates , mean reversion levels and volatilities . The mean reversion level represents the equilibrium or long-term mean of the MPR variable and the mean reversion rate the velocity by which the MPR variable reverts to its equilibrium. The volatility defines the impact of stochastic shocks on the MPR change. The resulting issue would contain the estimations of these unknown parameters. Brendle [21] modelled the drifts by a multidimensional Ornstein-Uhlenbeck model in the context of a power-utility based optimal portfolio problem under partial information. However, it is not clear how the model parameters from above can be estimated using real market data, because they are assumed as known constants. This model is not pursued here to seek maximally explicit formulas for the valuation and optimal hedge. More applications of stochastic differential equations of Ornstein-Uhlenbeck type in financial economics were treated by, for instance, Barndorff-Nielsen and Shephard [9]. ∎

2.4 Forward utility and local risk tolerance

In the classical utility framework, the expected utility criteria is typically formulated through a deterministic, concave and increasing function of terminal wealth, where both the investment time horizon and the associated risk preferences are chosen a priori. The value function as the optimal solution in the relevant market model has the fundamental property of supermartingality for arbitrary investment strategies and martingality at an optimum, which is a consequence of the dynamic programming principle (see, for example, Merton [90, p. 249]). Since the classical utility is fixed at a time and its value function generated at previous times with the wealth argument , it is also called the backward utility by Musiela and Zariphopoulou [105, pp. 304, 315]. As depicted therein, backward utilities does not accurately capture future changes in the risk preference as the market environment evolves. Therefore, they introduce a new class of dynamic utilities that are constructed forward in time, which offers flexibility with regards to the a priori choices mentioned above while the natural optimality properties of the value function process is preserved. Contrary to the classical utility framework, the forward utility is normalised at present time but not for a fixed investment horizon , and generated for all future times via a self-financing criterion. The forward measurement criterion is defined by Musiela and Zariphopoulou [106] in terms of a family of stochastic processes on indexed by a wealth argument.

In this section, only proofs are outlined in cases that they are instructive, otherwise the reference to the original source is given.

Definition 2.4.1 (Forward performance process).

Let be the subset of strategies starting at . An -adapted stochastic process , where

-

(i)

for each the function is concave and increasing in ,

-

(ii)

for each and each self-financing strategy ,

-

(iii)

there exists a self-financing (optimal) strategy , for which

-

(iv)

it satisfies the initial datum at for all , with a concave and increasing function of wealth,

is called a forward performance process. ∎

The function in (i) is the (forward) performance function. The conditions (ii) and (iii) represent the supermartingality and martingality properties, respectively.

Among others, forward formulations of optimal control problems were proposed and studied in the past by Seinfeld and Lapidus [122] and Vit [133] for the deterministic case and Kurtz [81] for the stochastic case. As in [106], we will consider a special class of time-decreasing and time-monotone forward performance processes expressed by a deterministic function of wealth and time, where the time argument is replaced by an increasing process depending on the market coefficients and not the investor’s preferences. On the contrary, the function is independent of market changes and only depends on the initial datum satisfying a market independent differential constraint for .

Definition 2.4.2 (Mean-variance trade-off process).

For the stock’s market price of risk process , define by

| (16) |

the (mean-variance) trade-off process . ∎

The naming originates from Pham et al. [110, pp. 173–174] in the context of mean-variance hedging of continuous processes. By Definition 2.3.1 and Definition 2.3.2, the process and likewise the trade-off process are, in general, dependent of the asset prices . In the full information scenario, when , the trade-off process simplifies to as the MPR becomes constant.

Proposition 2.4.3 (Forward performance process and general optimal strategy).

Let be a concave and increasing function of the wealth argument with , satisfying the non-linear partial differential equation

| (17) |

and the initial condition , where . Then, the time-decreasing process defined by

| (18) |

is a forward performance process with the time argument replaced by the mean-variance process (16) of Definition 2.4.2. Moreover, the optimal trading strategy is given by

| (19) |

where is the associated wealth process following (3) with .

Proof.

We refer to Musiela and Zariphopoulou [106, Proposition 3]. ∎

The monotonicity of follows from the related assumptions on and the time-monotonicity is obtained from the definition of and from the fact that the time-derivative of is negative, . The process will be simply also referred to as forward utility or dynamic utility. The mean-variance trade-off process behaves as a stochastic time change of the deterministic utility function . Optimal portfolio choice problems under space-time monotonicity was studied in detail by Musiela and Zariphopoulou [107]. As the representation (19) shows, the optimal strategy does not directly depend on but on the differential quantity , which was separately analysed by Zariphopoulou and Zhou [137].

Definition 2.4.4 (Local risk tolerance).

The local risk tolerance function is

| (20) |

with initial function and satisfying (17). The local risk tolerance process is defined by . ∎

Using Definition 2.4.4 in (19), the dynamics (13) of the optimal wealth can be expressed as

| (21) |

with as the local risk tolerance process benchmarked at optimal wealth. This brings up the question whether can be indirectly derived from .

Corollary 2.4.5 (Transport equation).

The utility function satisfies the transport equation

| (22) |

With the knowledge of the first-order partial differential equation (22) can be solved to yield .

Proof.

The transport equation (22) follows from (17) and (20). It can be solved using the method of characteristics. Consider with the characteristic curves . The solution are the curves whose slope is equal to half of the risk tolerance, i. e. with initial value . Then, the function can be successively constructed through the initial condition computed from Definition 2.4.4 and its evaluation along the characteristic curves. ∎

This means that for an infinitesimal time interval , the performance level at time is identical to at , when the wealth is moved from to a higher level . The infinitesimal amount can be interpreted as the compensation required by the investor in order to satisfy his impatience in the time interval . More about the theory of investor’s impatience can be found in Fisher [41, Chapter IV], Koopmans [75, p. 296] and Diamond et al. [34].

Apart from the transport equation (22), the local risk tolerance function solves an autonomous non-linear heat equation, which gives an alternative approach to construct from .

Corollary 2.4.6 (Fast diffusion equation).

Let satisfy the conditions from Proposition 2.4.3. Then, the associated local risk tolerance is the solution of an equation of fast diffusion type, namely

| (23) |

Proof.

We will quote the proof from Musiela and Zariphopoulou [106, Proposition 6]. Differentiating the non-linear partial differential equation from (17) with respect to yields

| (24) |

and a second derivation with respect to gives

| (25) |

The spatial derivatives of the local risk tolerance (20) are

| (26) |

The preceding identities (26), (25) and (24) imply

which proves the assertion. ∎

After choosing an initial condition , the initial datum and furthermore, with (23) and , the values of for can be retrieved. The function , can be computed through successive integration from (20) if certain quantities are correctly specified.

Corollary 2.4.7 (Autonomous SDE system for ).

Proof.

The first equation of the optimal wealth dynamics is taken from (21). Its quadratic variation is

| (27) |

Using Itô’s lemma, the dynamics of the risk tolerance process at optimum wealth can be deduced by

because solves the fast diffusion equation. ∎

The reciprocal of the local risk tolerance is called local risk aversion, which solves a similar partial differential equation of second order. The risk aversion is a well-known parameter in utility theory to express the investor’s risk preference.

Corollary 2.4.8 (Local risk aversion).

The local risk aversion function, defined as

| (28) |

satisfies the partial differential equation

| (29) |

where is the local risk tolerance function from Definition 2.4.4.

Proof.

The partial differential equation (29) is of porous medium type; see for example Vasquez [131]. This and the fast diffusion equation (23) may not have well-defined global solutions for arbitrary initial conditions. Zariphopoulou and Zhou [137] introduced a two-parameter family of so-called asymptotically linear local risk tolerance functions solving (23), which includes the most common cases that lead to exponential, power, and logarithmic utilities.

Proposition 2.4.9 (Asymptotically linear local risk tolerance).

Let be constant parameters, then the function

| (30) |

solves (23) with initial datum . The limiting cases lead to local risk tolerance functions with corresponding utilities for as follows:

| (31) | ||||||

| (32) | ||||||

| (33) |

where .

Proof.

The first partial derivatives of are and . The second derivative with respect to is . As a result, (30) solves the fast diffusion equation

To construct the utilities in the limiting cases, Definition 2.4.4 and the transport equation from Corollary 2.4.5 can be applied. For the exponential case (31), consider from (20) and make the exponential ansatz for as the left side is independent of time. By (22), it is , which yields the product solution .

In the power case (32), the risk tolerance is expressed by . Similar to the exponential case, make a multiplicative ansatz , but with a monomial initial function to solve the problem, because of

Further, the transport equation gives the homogeneous ordinary differential equation of first order . Excluding the trivial solution for simplifies the equation to . After a rearrangement, we get the logarithmic derivative , which is solved by simple integration and taking the inverse function, i. e. . The restriction is needed to ensure only real solutions.

The logarithmic case (33) is easier after the power case. The logarithm function solves and the transport equation becomes . Since an attempt to solve the problem through a multiplicative separation fails, we try an additive approach to get an appropriate solution . With this, the transport equation is apparently solved by . Obviously, the domain of the utility is defined only for . ∎

The family (30) is called asymptotically linear due to its limiting behaviour

The local risk tolerances in (31), (32) and (33) are referred to as exponential, power and logarithmic risk tolerance, respectively. The form of only depends on the range of the parameter , specifically, one the cases and .

Proposition 2.4.10 (Class of forward utility functions).

Let be an asymptotically linear local risk tolerance function as defined in (30) with . The corresponding utility function is given by

for , where are constants derived from integration.

Proof.

We refer to Zariphopoulou and Zhou [137, Proposition 3.2]. ∎

To preserve the monotonicity of , the constraint is necessary. As the utility is well-defined for all with exception of the situation , the non-negativity limitation on the investor’s wealth is omitted. This property is useful for indifference valuation.

3 Exponential forward valuation and hedging of European options under partial information

The previous section prepared for the option’s indifference pricing and optimal hedging of basis risk in an incomplete market model with partial information using a forward exponential utility approach. In this section, we derive the optimal hedging strategy, the dual representation of the forward indifference price with a PDE, the residual risk, pay-off decompositions and asymptotic expansions of the indifference price as results.

3.1 Perfect hedging in a complete market

Suppose the market is complete, this means that the Brownian motions of the assets are perfectly negatively or positively correlated with correlation coefficient . In this case, effectively becomes a traded asset and perfect hedging of the stock by an European contingent claim (European option) on is possible due to the no-arbitrage requirement of the market. More about the arbitrage theory of capital asset pricing can be found in Delbaen and Schachermayer [32, p. 473] and Ross [117]. The complete market case under full information was treated by Monoyios [97, p. 334]. An important result is that the perfect hedge does not require the knowledge of the MPR processes , making the hedging strategy in the full and the partial information scenario identical.

Proposition 3.1.1 (Pricing in a complete market).

In a complete market, that means a correlation of , the claim price process is given by the Black-Scholes pricing formula.

Proof.

We will give a proof based on Davis [30] and Monoyios [95]. Apply the scenario under partial information with its notation from Subsection 2.2, because the calculations and results under full information are exactly the same. Without loss of generality let the correlation coefficient be , implying the identity . The no-arbitrage theory requires an unique market price of risk, since the random process is the only existing risk factor in the basis risk model. Therefore, the MPRs are related by with according to Subsection 2.1. Like (9), the solutions of the asset price dynamics (11) are

| (34) | ||||

Thus, the asset is a function of the stock , given by

Apply the Itô lemma on the (contingent) claim price process (value process of the European option on ) , so that

| (35) |

The replication conditions are for the investor’s optimal wealth . A comparison of the random terms between the wealth dynamics (13) and (3.1) provides the perfect hedging strategy

| (36) |

which is independent of the MPRs and so is conform with both the full and partial information scenarios. The claim price process solves the Black-Scholes SDE

with a bounded continuous process and the non-negative random variable as the pay-off at expiry T of the European contingent claim. ∎

3.2 Forward performance problem in an incomplete market

Now, suppose the market is incomplete, meaning that the correlation of is not perfect, . Then the claim is not perfectly replicable in general. The ensuing indifference valuation and hedging problem of the claim is embedded in a exponential forward performance maximisation framework. Firstly, we define essential terms of the valuation and hedging theory regardless of the specific forward utility and the information scenario.

Definition 3.2.1 (Value process, indifference price and optimal hedging strategy).

Presume, the investor holds a long position in the stock and a short position in the claim on the non-traded asset to hedge the stock. The maximal -conditional expected forward performance of terminal portfolio wealth from trading,

| (37) |

is called (primal forward) value process. When no claim is sold, the value process is

| (38) |

The terminal values (maximal expected performances) are

| (39) |

The (forward performance) indifference price process is defined by (Hodges and Neuberger [56, p. 226])

| (40) |

Evaluating the value and indifference price processes given the deterministic point delivers the value and indifference price functions and , respectively. We abbreviate with the conditional expectation . As in Becherer [11, p. 7] defined, the optimal hedging strategy

| (41) |

is the difference between the optimal strategy for the problem with the claim (37) and the optimal strategy without the claim (38). ∎

The notion of essential supremum (likewise essential infimum ) is taken from Karatzas and Shreve [72, p. 323]. For a real-valued function , it is with the Lebesgue measure .

By Definition 2.4.1, it is with the associated optimal wealth in absence of the claim. In terms of the stock-weighted trading strategy , the optimal hedging strategy is . The portfolio strategies are denoted as () to express them as functions of the asset prices. The indifference price implicitly defined in (40) is also called the writer’s indifference price, since the option in the portfolio is sold. The solution to the optimisation problem (37) in classical utility theory is well-studied in Zariphopoulou [136] and Monoyios [95, p. 248] using the so-called distortion transformation to linearise the Hamilton-Jacobi-Bellman (HJB) equation for the value function. References for the HJB equation are, for example, Pham [109, pp. 42–46] and [72, p. 130].

Theorem 3.2.2 (Optimal strategy in terms of the value process).

Proof.

The value function solves the non-linear HJB equation

| (43) |

where the supremum is derived through differentiation with respect to ,

which gives the optimal strategy function . Evaluating the optimal strategy function at the random point provides the optimal strategy process (42). ∎

In terms of the cash value, the optimal strategy is

| (44) |

The first term of (44) is called the Merton strategy, because it made its first appearance in [90, p. 250] as Merton’s optimal solution in the setting of a simplified market with only one asset. Since in the full information scenario the value process does not directly depend on regarding the known MPR , the mixed partial derivative is zero and thus the partial information component of the strategy vanishes. The last term is induced by the claim on the non-traded asset and reflects the hedging component of the strategy. The sensitivity of the marginal utility of wealth with respect to changes of the option’s price is measured by . For the uncorrelated case , the hedging component becomes zero and the stock cannot be hedged by the option. Therefore, the optimal strategy in the uncorrelated full information scenario is identical to the one of Merton.

By Proposition 2.4.9, the limiting case (31) of the exponential linear local risk tolerance corresponds to the exponential utility function . By Corollary 2.4.8, the utility has the more familiar form with the local risk aversion . Applying Proposition 2.4.3, the exponential forward performance process is

| (45) |

In comparison to the classical exponential utility function the dynamic utility decreases in time, valuing less future utility. The primal value process (37) is the maximal expected forward performance

| (46) |

Remark 3.2.3 (Wealth independence of indifference price).

Since under full information, the stock’s MPR is observable and therefore a known constant with respect to the background filtration , the trade-off process becomes a deterministic linear function of time. Hence, the investor’s risk preference simplifies to the exponential performance process

Factoring out the MPR term, one gets the classical primal problem

3.3 Dual representation of the stochastic control problem

In the 1970s and 80s, Bismut [17], Karatzas et al. [70], [71] and Cox & Huang [27] realised that the use dual methods from convex analysis provided valuable comprehension of solutions to optimal stochastic control problems, which are more general than the original problem from Merton [90]. Kramkov and Schachermayer [77] studied the dual approach for solving maximisation problems under classical utility. Rogers [115] delved deeper into the theory by applying methods from functional analysis and presenting various examples solved with duality methods. We follow Žitković [138] and Berrier et al. [16] to briefly introduce the dual approach for solving forward performance maximisation problems. Firstly, recall the notion of relative entropy for equivalent local martingale measures from Definition 2.1.1. For the subset of these measures with finite relative entropy, we introduce the Radon-Nikodym derivative (see Shreve [126, pp. 65–79] or Platen and Heath [111, pp. 338–339]), allowing us to perform measure changes.

Definition 3.3.1 (Radon-Nikodym derivative process).

For measures , the positive likelihood ratio -martingale process defined by

| (47) |

is called the Radon-Nikodym derivative process. It is the density process of with respect to . ∎

For admissible portfolio strategies (5), is a non-negative -local martingale, hence a supermartingale satisfying

The map induced by (47) creates an one-to-one correspondence between the class of equivalent locale martingale measures with finite relative entropy and the set of density processes . If , then the Radon-Nikodym derivative is and the relative entropy (4) can be expressed by

where denotes the expectation with respect to , whereas is the -expectation. The relative entropy can be interpreted as a measure of distance, even though it is not a metric. The density process and relative entropy will be generalised to conditional versions in order to formulate the dual problem to Definition 3.2.1.

Definition 3.3.2 (Conditional density and conditional relative entropy).

The ratio

| (48) |

is called conditional density process and motivates the conditional relative entropy

| (49) |

of with respect to over the interval . ∎

At , the conditionality becomes trivial with density and relative entropy . Frittelli [46, p. 42] showed the existence and uniqueness of a minimal entropy martingale measure (MEMM) , that minimises over all . According to Kabanov and Stricker [64, pp. 131–132], also minimises the for an arbitrary , so that we can write

| (50) |

We say, the minimal conditional density process minimises the conditional relative entropy process .

Our aim is to give the optimal strategy from Theorem 3.2.2 in terms of derivatives of the indifference price from Definition 3.2.1, which we will approach through framing the dual problem.

Definition 3.3.3 (Convex conjugate (dual) performance and its inverse marginal).

The (convex) conjugate (or dual) of the performance is

| (51) |

where denotes its inverse of the marginal satisfying

| (52) |

The conjugate function solves the bidual relation

as well as with equality if and only if . The marginal dual performance satisfies the identity . ∎

Both and are continuous, strictly decreasing and map onto itself satisfying the Inada conditions (see Färe and Primont [40], Inada [59])

where we have abbreviated for the limit (analogous the other limits). The conjugate function is convex, decreasing, continuously differentiable with the limits

The dual function is the Legendre-transform of (cf. Rockafellar [113, p. 251]). Pliska [112] showed some useful applicatios for computing value functions and optimal strategies. The methods and the exposition of the results given there are similar to the corresponding methods used by [113].

Lemma 3.3.4 (Dual value process and dual problem).

For the primal value function from Definition 3.2.1 the dual value process is

| (53) |

The primal and dual value functions are conjugate with respect to the wealth space,

| (54) | ||||

The partial derivatives of he primal and dual value functions at the optimum are related by

| (55) |

Proof.

As noticed in Mania and Schweizer [87, p. 2116], the terminology “primal” corresponds for any problem optimising over the portfolio strategy and “dual” when the optimiser is the density resp. measure .

Since the main results of duality theory for solving stochastic control problems are worked out, they will be applied to the primal performance maximisation problem (46) of exponential forward type to obtain the corresponding dual problem. The next theorem covers the valuation of the dual performance process and the dual entropic representation of the problem.

Theorem 3.3.5 (Dual forward performance problem).

The dual representation of the primal optimisation problem (46) is given by

| (56) |

Proof.

Definition 3.3.3 is considered to calculate the dual performance process. Inserting the derivative into (52), leads to its inverse

Putting the inverse into (51), provides the dual performance

| (57) |

Before moving to the dual value function, consider the conditional relative entropy

| (58) |

where in the second equation we have applied Lemma 5.2.2 from Shreve [125, p. 212], concerning the expression of conditional expectations of random variables under measure change. Obviously, the conditional density has the expectation

| (59) |

Then, by Lemma 3.3.4, the dual value function is given by

| (60) |

Thus, the dual forward performance problem amounts to the minimisation of

| (61) |

which will be referred to as the minimal entropy process. Given (55), the derivative of the dual value function at the optimum satisfies

As the latter equation defines the functional expression of by , rearrange it to get the inverse expression

Using this in the bidual relation (54) delivers

which proves (56). ∎

When writing the primal forward performance problem (46) as

and comparing both this and its dual representation (56) to the classical utility case from [98], the claim pay-off term in the forward model is instead of in the classical model. Thus, the forward case adds value to the terminal value of the option.

Corollary 3.3.6 (Dual representation of the indifference price).

The indifference price process has the entropic representation

| (62) |

Proof.

Next, we give the optimal hedging strategy in terms indifference price derivatives, which is derived analogously to the classical case from Monoyios [98, Theorem 1].

Theorem 3.3.7 (Optimal hedging strategy in terms of the indifference price).

Suppose the forward indifference price function is of class . Then the optimal hedging strategy for a short position in the claim is given by

| (63) |

Proof.

By differentiating the entropic representation of the value function given in Theorem 3.3.5, we obtain the partial derivatives

| (64) |

for the case with the claim and the case without the claim. Apply them to Theorem 3.2.2 to obtain the optimal strategy in terms of derivatives of the minimal entropy process,

for . Finally, consider the optimal hedging strategy formula from (41) and use Corollary 3.3.6 to eliminate the Merton strategy term and obtain the optimal hedging strategy expressed by the indifference price (63). The required regularity of the indifference price is shown in [98, Subsection 3.3]. ∎

3.4 Forward indifference price valuation

After we have defined the dual stochastic control problem, we are going to give a more explicit representation formula for the forward indifference price from Corollary3.3.6 following Monoyios [98, Subsection 3.2] and Leung et al. [84, Subsection 3.2]. For this, we will characterise the martingale measure by giving the corresponding density process and then perform a measure change to the basis risk model. The measures characterised by their densities , are parametrised via -adapted processes satisfying -a.s. and , according to the stochastic exponential

| (65) | ||||

Since is a strictly positive square-integrable continuous process, Novikov’s condition

| (66) |

is fulfilled. Denote with the set of integrands such that (66) is satisfied. Hence, the density process is indeed a -martingale. Applying Girsanov’s theorem from [125, pp. 224–225] for a measure change to , provides the two-dimensional Brownian motion defined by

| (67) |

The integrand process is commonly referred to as the volatility risk premium for the second Brownian motion . The so-called minimal martingale measure (MMM) corresponds to the case . It was originally introduced by Föllmer and Schweizer [42] for the risk-minimised (optimal) quadratic hedging strategy in an incomplete market. It alters the MPR of the stock’s Brownian motion, but does not change the MPR of Brownian motions orthogonal to those driving the stock. By (65), it has the Radon-Nikodym derivative process

The second equation of (67) implies that is also a -Brownian motion.

Proposition 3.4.1 (Representation of conditional relative entropy).

The conditional relative entropy between and satisfies

| (68) |

In the full information scenario, the conditional relative entropy simplifies to

| (69) |

which is minimised by . Hence, in the full information scenario, the MEMM coincides with the MMM . Using as the reference measure, the conditional relative entropy above can be additively decomposed to

with

| (70) |

Proof.

The conditional relative entropy from Definition (3.3.2) is

where the integrability on the right hand side implied by Novikov’s condition (66) is associated with the finite conditional relative entropy condition. The second assertion (69) directly follows from (68) for . To show (70), consider the Radon-Nikodym derivative under ,

| (71) |

Then again, apply Lemma 5.2.2 from [125, p. 212], giving the conditional expectation under measure change to compute the density process of with respect to ,

| (72) |

As in Definition 3.3.2, for any measure , the conditional density is given by

| (73) |

Then, directly compute the conditional relative entropy over the interval ,

by using the -martingale property of . The conditional relative entropy is analogously determined given . ∎

Proposition 3.4.1 implies the generalised additivity formula

| (74) |

for any martingale measure (see also Monoyios [99, p. 902]).

Theorem 3.4.2 (Forward indifference price valuation).

The forward indifference price is the solution of the stochastic control problem

| (75) |

with optimal control

| (76) |

and solves the semi-linear partial differential equation of second order

| (77) |

The marginal performance-based price (marginal forward indifference price) is

| (78) |

Proof.

Denote with the set of volatility risk premia such that (68) is satisfied. Then parametrises all the through the well-defined map induced by (65). Therefore in control theory is called the control set and a control. Using Proposition 3.4.1, the minimal entropy process (61) can be represented as

| (79) |

Hence, the dual value process (56) becomes

| (80) |

Denote by the optimal control in (3.4) with the claim. Analogous, let be the optimal control in absence of the claim. In the latter case, the relative entropy is minimised by the control and gives the minimal entropy process

| (81) |

so that the value function has the optimal wealth and simplifies to

| (82) |

With (3.4), (81), the forward indifference price from Corollary 3.3.6 has the expression

| (83) |

By (11), (67), the asset prices have the -dynamics

| (84) | ||||

with the -Brownian motion

| (85) |

Then, with as the generator of under (cf. (3.2)), the HJB equation for , by (83), is given by

| (86) |

with terminal value and . Consider the function and determine its maximum by solving the equation , which gives the optimal control (76), because of . Substituting this into the HJB equation (86) yields the PDE (77) for the forward indifference price. The marginal performance-based indifference price (78) follows from the Feynman-Kac theorem (cf. Theorem 6.4.1 from [125, p. 268]), when the non-linear term in the PDE (77) vanishes for . ∎

Le us compare the forward indifference price valuation results of Theorem 3.4.2 with the classical theory from [98]. The classical minimal entropy process with the claim admits the representation

| (87) |

with as in (68). Without the claim, the formula turns into

| (88) |

where is the MEMM, the minimal conditional relative entropy and the minimal entropy control process. The value processes with and without the claim are

| (89) | ||||

Because of the relative entropy additivity from (74), the classical indifference price is the solution of the dual control problem

| (90) |

which was shown by Monoyios [99, p. 903]. The HJB equation for (87) is

Solving yields the optimal control and further the PDE

| (91) |

Without the claim, the same approach returns and an analogous PDE for with . Hence, the optimal (hedging) control is

| (92) |

Subtract the PDEs (91) for and according to (62) and apply the identities and to obtain the PDE for ,

Expressed by the differential operator , the indifference price PDE has the form

| (93) |

and the marginal utility-based price process is .

In comparison to the well known classical case (90), (93), the relative entropy term in the forward indifference problem of Theorem 3.4.2 is computed with respect to instead of . The reason is that through the suitable choice of the mean-variance trade-off process , the conditional relative entropy under the physical measure in the minimal entropy function is transformed into the relative entropy under the MMM by eliminating the entropy term . These representations for American versions of the indifference prices were derived by Leung and Sircar [83] for classical utility and by Leung, Sircar and Zariphopoulou [84] for forward utility. The optimal hedging control in (76) and (92) have the same representation formula. The classical value processes (89) have, in comparison to the value processes (80), (82) of the forward model, no trade-off term, which only shows up in the forward performance process. In the forward problem, the optimal control without the claim vanishes, i. e. , but in the classical model is not in general zero. This difference only occurs in the partial information scenario when from (14). In the case , the stock’s MPR loses the dependence on the non-traded asset price , so that, after (84), is directly affected by and therefore becomes independent of . Thus, the drift term is excluded from the minimal entropy process (88). If the full information scenario is applied, then the classical problem takes the MMM because of and the trade-off term with the drift under the background filtration is again excluded from (88). In conclusion, an appropriate selection of the initial variance estimations with in the Kalman-Bucy filter under partial information from Proposition 2.3.3, ensures the same pricing in the forward and classical model.

Remark 3.4.3 (Distortion solution of the indifference price).

Monoyios [96] proved, that if the asset prices follow SDEs with stochastic volatilities of the form

then the distortion transformation from Musiela and Zariphopoulou [104, pp. 222–223] leads to the solution of the classical indifference price PDE (93),

| (94) |

given by Oberman and Zariphopoulou [108]. Leung et al. [84, pp. 16–17] gave the solution in the forward performance model using the appropriate measure . The indifference price solution under full information looks like (94) with and can be found in Henderson and Hobson [53, p. 344], Musiela and Zariphopoulou [104, p. 233] and Monoyios [95, p. 248]. ∎

3.5 Residual risk

In Subsection 3.1 we have discussed the complete market case, where perfect hedging of the stock by the derivative is possible, when the underlying non-traded asset price perfectly correlates with the stock price. One says, that the stock is replicated by the derivative on the non-tradeable underlying. If the asset prices are not perfectly correlated, as in Subsection 3.2, then the hedge becomes imperfect and a non-hedgeable basis risk (hedging error) remains. The basis is the difference between the price of the asset to be hedged and the price of the hedging instrument, which is why residual risk is commonly also referred to as basis risk. Hedging a financial instrument by another correlated instrument is called cross hedging.

The reasons why an instrument is practically non-tradeable are diverse. For instance, its liquidity (trading volume) in the market could be very low or the spreads and commission fees very high, so that trading is not economical. Or it is simply not tradeable, because the instrument is an abstract synthetic product, like an index. There are many examples in the commodities and OTC (over-the-counter) and derivatives markets with exotic products like weather and insurance indices or credit default derivatives. Ankirchner and Imkeller [6] introduced a typical example for a cross hedge, where an airline company wants to manage kerosene price risk. Since there is no liquid kerosene futures market, the airline company may fall back on futures on less refined oil, such as crude oil futures, for hedging its kerosene risk. This is a reasonable approach, if the price evolutions of kerosene and crude oil are highly correlated. Ankirchner, Imkeller and Popier [8] dealt with optimal cross hedging strategies for insurance related derivatives. Other papers dealing with cross hedging including practical examples are Ankirchner et al. [5], [7].

Definition 3.5.1 (Residual risk process).

Suppose, the investor shorts the claim at time for the price . To hedge this position over , the optimal hedging strategy is used. His overall portfolio value is given by the residual risk process , defined by

| (95) |

with initial and terminal values and the forward indifference price . The terminal residual risk is the terminal portfolio value that appeared in the forward performance problem (37). The stock’s position value process is given by

| (96) |

and the riskless interest rate . ∎

Proposition 3.5.2 (Residual risk process).

The residual risk process of the forward performance-based model under the partial information scenario solves the SDE

| (97) |

Proof.

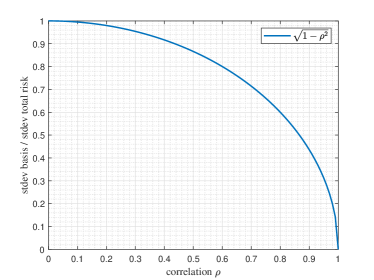

The version of the residual risk SDE (97) under full information and classical utility is in [104] and [97]. The residual risk evolution is expressed by a forward indifference price-based drift term containing the coefficient together with a stochastic term including the orthogonal Brownian motion and the scale parameter . In the complete market scenario , the residual risk vanishes and no hedging error remains. But even if the absolute correlation is very high, meaning close to , then a considerably high residual risk remains. If the correlation was high as , the scale parameter of the drift term would be and of the stochastic term even . This means, that the standard deviation of the basis would still represent about of the total risk induced by the stochastic term. If the correlation is almost perfect, a small change leads to significant change in the percentage of the basis risk relative to total risk. Conversely, in the virtually uncorrelated case, a small change in the correlation leads to essentially no change in the percentage of basis risk relative to total risk (see Figure 1). This fact complicates effective hedging, since asset correlations in real markets do not tend to perfectly correlate. Boucrelle et al. [19] analysed the U.S. stock and bond markets and figured out that correlations fluctuate widely over time. In addition, correlations increase in periods of high market volatility. Sandoval Junior and De Paula Franca [120] have come to a similar conclusion with more recent data. Using eigenvalues and eigenvectors of correlation matrices of main financial market indices, they have shown on the basis of price data from the largest crises of the last decades, that high volatility of markets is directly linked with strong correlations between them. When instruments like Exchange Traded Funds (ETF) or derivatives try to replicate another (untradeable) instrument like an index, then the measured correlation is not always perfect as desired and a so-called tracking-error arises. This was shown by Jorion [62], Aber, Can and Li [1] and Lobe, Röder and Schmidhammer [86] in various settings. Models for dynamic conditional correlation were studied by Engle [39] and Franses and Hafner [44].

Remark 3.5.3 (Effect of correlation on diversification).

As the instability of the residual risk for absolute correlations close to makes hedging more difficult, a similar effect can be found in classical portfolio theory from Markowitz [88]. For diversification purpose, consider a portfolio containing two assets with relative weights . The standard deviation of is then

The inequation follows from the evaluation of the binomial and delivers an equation when the assets are perfectly correlated. Since has a low slope when is close to , a decrease of and therefore a diversification effect only occurs, when rapidly falls towards . In the case of negative correlation this effect reverses. A small negative correlation may significantly lower the portfolio volatility. Sharpe [123], [124] and Lintner [85] deal also with classical portfolio theory. ∎

3.6 Pay-off decompositions and asymptotic expansions

In this subsection, we shall obtain pay-off decompositions of the claim followed by an asymptotic representation for the forward indifference price valid for small values of risk aversion. We pursue an approach as for classical utility from Monoyios [98].

Definition 3.6.1 (Preference-adjusted exponential of the residual risk).

The process

| (98) |

is called preference-adjusted exponential of the residual risk (PAERR). ∎

Corollary 3.6.2 (Preference-adjusted exponential of the residual risk).

The PAERR process from Definition 3.6.1 is a -martingale with dynamics

| (99) |

Proof.

By Proposition 3.5.2 and Itô’s lemma it is

The martingale property follows, because the orthogonal Brownian motion is a martingale under both measures and . ∎

Corollary 3.6.2 is similar to Proposition 6 of [104, p. 237] under full information and classical utility, but with the forward indifference price depending on rather than the single variable due to the partial information scenario. Under classical utility and partial information as in [98, Subsection 4.1], the dynamics (99) is in general a -martingale. Remark, that therein the process starts with rather than . Since is a martingale, the classical exponential utility of the residual risk is and therefore remains constant, whereas the exponential forward utility of the residual risk,

decreases over time.

Corollary 3.6.3 (Pay-off decomposition).

The claim pay-off decomposes into

| (100) |

where is the optimal hedging strategy for the claim, given in Theorem 3.3.7.

Proof.

The classical version under the full information scenario of Corollary 3.6.3 is Theorem 7 of [104, p. 238]. Under the partial information classical model of [98, Lemma 1], the pay-off decomposition (100) is measured under , whereas the forward version always takes . Pay-off decomposition is the suitable term, because is a -martingale with respect to , which is strongly orthogonal to the -martingale , that in turn, is defined as a stochastic integral with respect to the -Brownian motion induced by . Mania and Schweizer [87, pp. 2129–2130] obtained an analogous pay-off decomposition in a more general backward SDE model under the classical framework.

Definition 3.6.4 (Marginal preference-adjusted exponential of the residual risk).

Define the marginal preference-adjusted exponential of the residual risk (MPAERR) by the process . With the marginal performance-based price from (78) the evolution is . The MPAERR is also a -martingale. ∎

Corollary 3.6.5 (Föllmer-Schweizer-Sondermann pay-off decomposition).

Proof.

Corollary 3.6.6 (Forward indifference price representation).

The forward indifference price admits the representation

| (102) |

Proof.

The classical version of Corollary 3.6.6 under is dealt in [98, Corollary 2]. Again, in the forward performance framework, the measure is used.

Proposition 3.6.7 (Asymptotic expansion of the forward indifference price).

The forward indifference price has the asymptotic representation

| (103) |

where denotes the profit and loss of the wealth from to under the marginal hedging strategy and its covariation.

Proof.

We make the same ansatz as in the classical version from [98, Theorem 2] and write the asymptotic expansion

| (104) |

with an appropriate process . By Corollary 3.6.6 and Corollary 3.6.2 it follows

and further leads to the solution

| (105) |

Inserting (105) into (104) gives the asymptotic expansion of the indifference price

| (106) |

Notice, that by switching from the PAERR in (102) to the MPAERR in (106), an expansion term of order is added to the indifference price representation. The Föllmer-Schweizer-Sondermann decomposition (101) implies the pay-off variance

| (107) |

because and are orthogonal -martingales. Inserting (107) after a rearrangement into (106) gives the asymptotic expansion (103). ∎

4 Exponential forward valuation and hedging of American options under partial information

Early exercise claims arise often in situations in which a certain project is undertaken or abandoned (Smith and Nau [130], Smith and McCardle [129]), executives exercise their employee stock options (Aboody [2], Huddart [58]), household owners prepay their mortgages or sell their property (Hall [48], Kau and Keenan [74], Schwartz and Torous [121]). Allowing early exercise gives rise to stochastic control problems with stopping times. Early exercise options were priced for the first time by Davis and Zariphopoulou [31] in the setting, where the option’s underlying asset is traded but with proportional transaction costs. Karatzas and Wang [73] studied utility maximisation problems of mixed optimal stopping and control type in complete markets, which can be solved by reduction to a family of related pure optimal stopping problems. Oberman and Zariphopoulou [108] introduced a utility-based methodology for the valuation of early exercise contracts in incomplete markets. Henderson and Hobson [54] considered the case of infinite time horizon, where the problem is expressed with respect to horizon-unbiased utility functions, a class of utility functions satisfying certainconsistency conditions over time, which are nothing less than forward utilitie. Leung and Sircar [83] studied problems of hedging American options with exponential utility within a general incomplete market model. In Leung, Sircar and Zariphopoulou [84] this theory was expanded to the forward performance framework.

In this section, we apply the forward performance model under the partial information scenario from Proposition 2.3.3 to American options to derive hedging and valuation results comparable to the European counterparts of Section 3.

4.1 Optimal control and stopping problem

Suppose is now an early exercise claim (American option) written on the non-traded asset . The investor sets up a hedging portfolio consisting of a long position in the stock and a short position in the option as in the European scenario of Section 3.

Definition 4.1.1 (Admissible exercise times).

The collection of admissible exercise times is the set of stopping times with respect to the observation filtration that take values in . For , define the subset of stopping times taking values in . ∎

In addition to the dynamic trading strategy , the investor chooses an exercise time , in order to maximise his expected forward performance of his hedging portfolio . Therefore, let denote the subset of strategies starting at and terminating at . The claim pay-off becomes with the exercise time as the terminal date instead of the fixed date .

Definition 4.1.2 (Optimal control and stopping problem).

The value process of the investor’s portfolio is the combined stochastic control and optimal stopping problem

| (108) |

The double essential supremum notation will be shortened to . ∎

In comparison to the European case (37), the optimisation is additionally performed under the stopping time. The forward indifference price is defined as in Definition 3.2.1 and is useful to characterise the optimal exercise time .

Corollary 4.1.3 (Optimal stopping time).

Corollary 4.1.3 implies, that the investor exercises the American option as soon as the forward indifference price reaches from above the option pay-off and allows analysing the optimal exercise time through the forward indifference price.

Corollary 4.1.4 (Primal forward performance problem with American claim).

To obtain the dual optimal control and stopping problem, some preparation is required. Firstly, a reconsideration and extension of the conditional relative entropy from Definition 3.3.2 is needed, to include the case of stopping times. Secondly, a relation between the conditional relative entropies up to time and is derived. Lastly, a particular dynamic programming property of the classical Merton problem is recalled and applied to the American option case.

Definition 4.1.5 (Stopped conditional relative entropy).

Define by

| (109) |

the right stopped (conditional) relative entropy over the stochastic interval and by

| (110) |

the left stopped (conditional) relative entropy over the stochastic interval . ∎

By Proposition 3.4.1, the right stopped relative entropy (109) is given by

The only difference to the European case is, that is replaced by . From here, the new notation is used for . Remark, that the left stopped relative entropy (110) is -conditional. According to Definition 4.1.5, the conditional relative entropy over splits into .

Lemma 4.1.6 (Decomposition of the relative entropy under stopping times).

The conditional relative entropy decomposes into the right and left entropies

under the stopping time .

Proof.

A proof is given by Leung and Sircar [83, Lemma 2.7]. ∎

Proposition 4.1.7 (Primal and dual classical Merton problem with stopping time).

For an investor with starting wealth at , the classical Merton value process

has the dual separable representation

With starting wealth at , the classical value process can be written as

| (111) |

Proof.

We refer to [83, Propositions 2.5 and 2.6]. ∎

The dynamic programming property (111) is called the self-generating condition by Musiela and Zariphopoulou [105], and horizon-unbiased condition by Henderson and Hobson [54].

Proposition 4.1.8 (Dual classical problem with American option).

The dual classical value process in the American option case is given by

The classical exponential indifference price is given by

Proof.

A detailed proof is given in [83, Propositions 2.4 and 2.8]. Therein, the claim is additionally dependent on the stock , i. e. . ∎

Theorem 4.1.9 (Forward indifference price valuation with American option).

The dual forward performance problem with the American option has the representation

| (112) |

with the entropic representation of the forward indifference price

| (113) |

Proof.

Follow the approach from [84, Proposition 2.7] by transforming the pay-off into

| (114) |

Then recall the primal forward performance problem from Corollary 4.1.4,

through a substitution of the claim pay-off by the transform . Now, the application of Proposition 4.1.8 yields

which proves (4.1.9). The forward indifference price representation (113) is then implied by (40). ∎

5 Conclusions and future research directions

In this thesis we applied the forward performance framework, defined by Musiela and Zariphopoulou [106] to the basis risk model with partial information from Monoyios [98] to solve the forward utility maximisation problem of exponential type of an investor with a hedging portfolio consisting of a long position in the traded stock and a short position of a claim written on the non-traded asset . We obtained the optimal hedging strategy, value function and indifference price representation using methods from duality theory. In the case of an European option, we discussed the main result containing the change of the MEMM to the MMM after Theorem 3.4.2. We derived the residual risk, pay-off decompositions and an asymptotic expansion of the indifference price. Then we changed to the market model with an American option having a random exercise time inspired by Leung, Sircar and Zariphopoulou [84]. We formulated the optimal control problem with stopping time and obtained the representations for the value function and forward indifference price. Hereinafter, we take up some points of the thesis to discuss future research topics. We carry out a comprehensive review of the parameter uncertainty in the Kalman-Bucy filter used in our partial information model and discuss alternatives from recent publications. Furthermore, we present the semi-martingale framework for utlity maximisation problems allowing to use weaker assumptions on the model. Moreover, we outline the approach of solving the forward indifference price PDE in the European option’s case with numerical methods, by applying the asymptotic expansion of the indifference price as an approximation. For the case with an American option, we describe the variational inequality for the forward indifference price to be expected and a suggestion for solving it numerically. In addition, we propose a larger market model by making more claims available for the market agent, and discuss other large markets in utility maximisation theory. Lastly, we present a generalisation of stochastic utilities used in forward utility-based optimisation theory.

5.1 Parameter uncertainty in the Kalman-Bucy filter