Sequential Deep Learning for Credit Risk Monitoring with Tabular Financial Data

Abstract.

Machine learning plays an essential role in preventing financial losses in the banking industry. Perhaps the most pertinent prediction task that can result in billions of dollars in losses each year is the assessment of credit risk (i.e., the risk of default on debt). Today, much of the gains from machine learning to predict credit risk are driven by gradient boosted decision tree models. However, these gains begin to plateau without the addition of expensive new data sources or highly engineered features. In this paper, we present our attempts to create a novel approach to assessing credit risk using deep learning that does not rely on new model inputs. We propose a new credit card transaction sampling technique to use with deep recurrent and causal convolution-based neural networks that exploits long historical sequences of financial data without costly resource requirements. We show that our sequential deep learning approach using a temporal convolutional network outperformed the benchmark non-sequential tree-based model, achieving significant financial savings and earlier detection of credit risk. We also demonstrate the potential for our approach to be used in a production environment, where our sampling technique allows for sequences to be stored efficiently in memory and used for fast online learning and inference.

1. Introduction

When bank borrowers get into trouble, the early detection of small changes in their financial situation can substantially reduce a bank’s losses when precautionary steps are taken (e.g., lowering the borrower’s credit limit). In fact, the ongoing monitoring of credit risk is an integral part of most loss mitigation strategies within the banking industry (Thomas et al., 2002).

Current credit scoring models to assess risk typically rely on gradient boosted decision trees (GBDTs), which provide several benefits over more traditional techniques such as logistic regression (Friedman, 2001). For instance, interactions between variables are automatically created during the boosting process and provide multiple combinations to improve prediction accuracy. Additionally, preprocessing steps such as missing value imputation and data transformation are generally not required. However, these models also have certain limitations. First, performance improvements are usually derived from feature engineering to create new variables based on extensive domain knowledge and expertise. Second, tree-based models do not take full advantage of the available historical data. Finally, they cannot be used in an online learning setting (where data becomes available in a sequential order) due to their limited capacity for updates, such as altering splits, without seeing the whole dataset from the start (e.g., (Chen and Guestrin, 2016)).

To overcome the limitations of a traditional tree-based approach, we explored several deep learning techniques for assessing credit risk and created a unique method for generating sequences of credit card transactions that looks back one year into borrowers’ financial history. Applying the same input features as the benchmark GBDT model, we show that our final sequential deep learning approach using a temporal convolution network (TCN) provides distinct advantages over the tree-based technique. The main improvement is that performance increases substantially, resulting in significant financial savings and earlier detection of credit risk. We also demonstrate the potential for our approach to be used in an online learning setting for credit risk monitoring without making significant changes to the training process.

Previous research on the application of deep learning to tabular data from credit card transactions has focused on fraud detection (Roy et al., 2018; Efimov et al., 2019), loan applications (Wang et al., 2018; Babaev et al., 2019), and credit risk monitoring (Nanni and Lumini, 2009; Addo et al., 2018). Our work differs from previous deep learning work on credit risk monitoring by extending beyond simple multilayer perceptron networks and into sequential techniques, such as recurrent neural networks (RNNs) and TCNs, that explicitly utilize the available historical data. Additionally, we introduce a novel sampling method for generating sequences of transactions that addresses the drastic differences in sequence length between card members over a full year. The benefits of using sampled transactions from a long time window, as opposed to the total number of transactions, are that it reduces noise, memory requirements, and training/inference time so that the model is able to learn generalizable early warning signs of risky financial behavior while still being able to run in near real time during online credit monitoring.

The main contributions presented in this paper are as follows. We first show the potential of sequential deep learning to improve our current credit scoring system through offline analysis, which revealed significant reductions in financial losses (tens of millions of US dollars annually) and increased early risk detection rates. We also developed a sampling method for generating sequences of transactions over the course of a full year, which allows the model to learn long-term behavioral trends and removes the need to load and process the hundreds of billions of credit card transactions that occur in a given year across card members. Finally, we demonstrate that online learning can be applied to our approach and achieves higher performance over randomly re-initializing the model weights.

2. Methods

2.1. Transactional Data

Credit risk scores are predicted using tabular data from credit card transactions, where each transaction is associated with a set of numerical and categorical variables. We define credit risk prediction as a binary classification task, where the goal is to detect default (non-payment) on credit card debt within 1.5 years following the timestamp of each transaction.

2.1.1. Features

For our modeling experiments, we used transactional data for card members with consumer credit cards. Data sources included both internal and external sources, such as consumer credit reporting agencies, from which 127 raw and engineered features were created. Our features can be divided into two subcategories: transaction-related (credit exposure, ATM indicator, etc.) and account-related (days past due, account tenure, etc.). To ensure fairness, personal demographic information was not included in any of the features. However, due to privacy concerns and strict adherence to data protection laws, we are unable to describe our features in further detail.

2.1.2. Training and Validation

The training dataset consisted of a sample of 15 million card members, with transactions spanning the course of twelve months from March 2016 to February 2017. We shifted the one year window forward by one month twice to create 45 million transactional sequences for training. This simply means that each card member appeared three times in the training dataset with slightly different (time-shifted) sequence data.

The validation dataset consisted of a sample of 6 million non-overlapping (out-of-sample) card members, with transactions spanning twelve months from May 2017 to April 2018 in order to also create an out-of-time validation set. This simulates our production environment, where models are trained on past data.

Within these sample datasets, roughly 2% of card members defaulted on their balance. We addressed this class imbalance in the context of deep learning by creating balanced mini-batches for training models with mini-batch gradient descent, where each mini-batch had the same percentage of defaulting card members as the whole dataset.

2.1.3. Preprocessing

Neural networks are sensitive to feature distributions and performance can drop significantly for non-normal distributions, such as skewed distributions or those with outliers. Our tabular datasets contain many features with similar behavior and thus, standard feature preprocessing approaches would not lead to superior results. Therefore, our preprocessing steps were as follows.

-

•

Missing values for each feature were imputed based on the target label (default/non-default) rates within 10 bins defined by the feature’s percentiles.

-

•

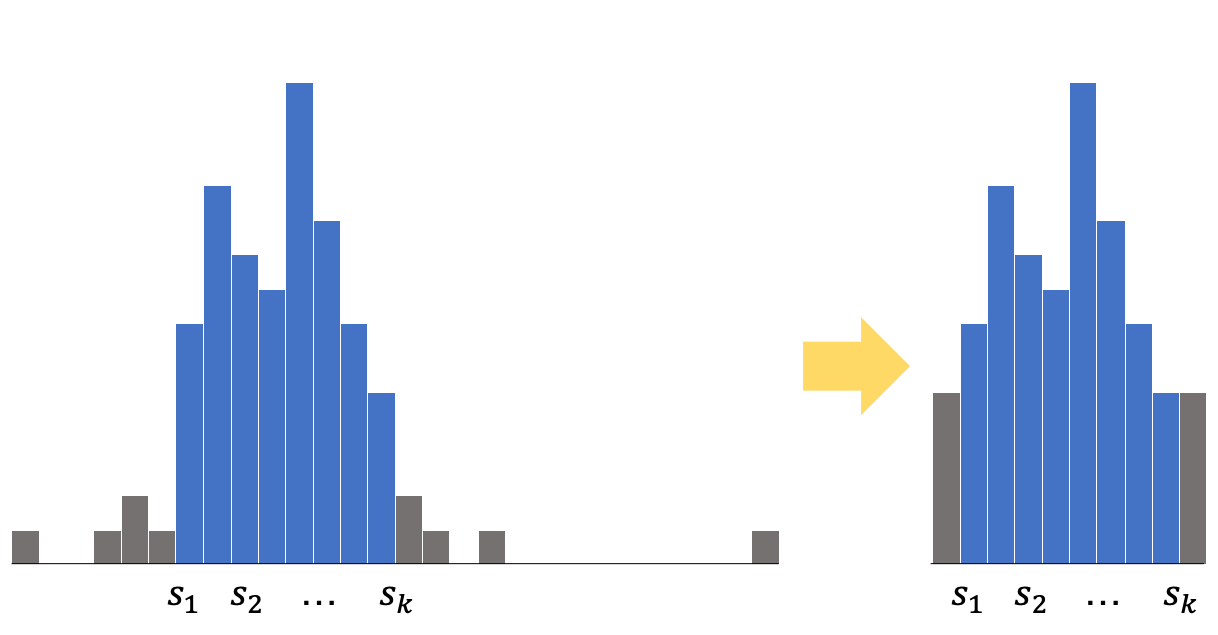

For dealing with numerical outliers, we developed a novel capping procedure to extract the most significant part of the feature distribution by leveraging splits obtained from training a decision tree model (in our case, the GBDT framework was used). For each feature and all trees produced by the model, we sorted all splits in ascending order:

and applied the following capping rules:

where is the original feature and is the transformed feature (see Figure 1 for an illustrative example).

-

•

After imputation and outlier capping, the Box-Cox transformation was applied to reduce feature skewness (Box and Cox, 1964).

-

•

Categorical data were transformed to numerical features using a procedure known as Laplace smoothing (Manning et al., 2008), which contains two main steps:

-

(1)

Calculate the average of the target variable within each category.

-

(2)

Modify the average from step 1 to address categories with a small number of observations:

where is a set of indices for the given category, is the size of the category, is a metaparameter defined empirically ( in our case), and is the average of the target variable for all training observations.

Figure 1. Capping with GBDT splits. -

(1)

-

•

Finally, standard scaling was applied to all features.

2.2. Sampling Transactions for Sequence Generation

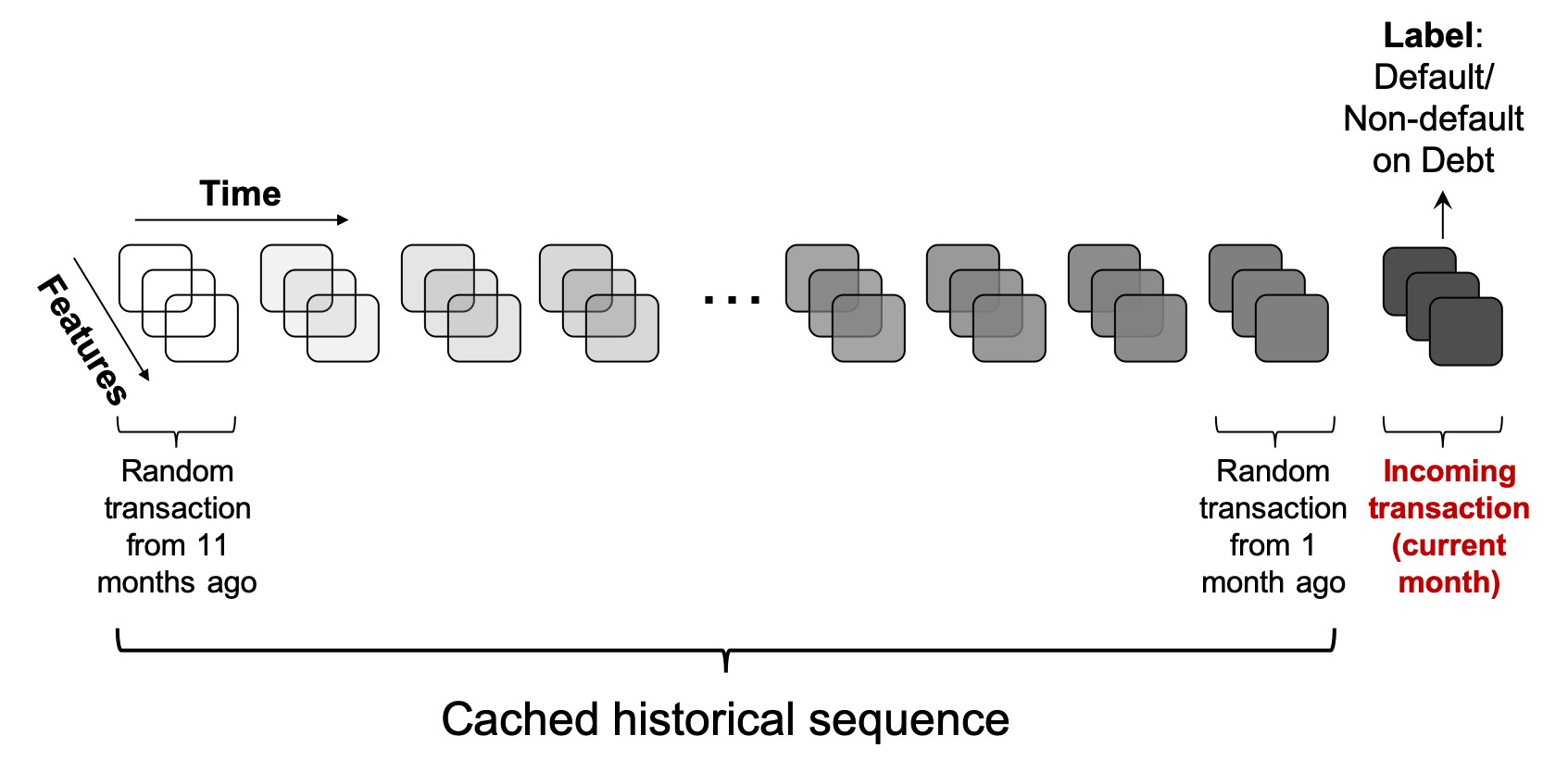

Generating sequences of credit card transactions over a fixed period of time presents a unique challenge for risk assessment. Within a given time frame, card members can have drastically different amounts of transactions. For example, in a single year, one card member might have only a few transactions while another has thousands. Therefore, rather than modeling full sequences of transactions over the course of year, we created a sampling scheme that selects one random historical transaction per card member per month.

The benefit of this sampling technique is twofold. First, it reduces noise in order to expose more general trends in risky card member behavior over a long period of time. Second, it allows us to create and process sequences in near real time because the previous 11 months of transactions can be stored efficiently in memory and loaded quickly. We simply append each incoming transaction in the current month to the end of the sequence before submitting it to a sequential model (see Figure 2 for an illustration). This is important for the implementation of sequential models in our production environment, where a near real-time processing speed is needed to calculate a credit risk score for each incoming transaction before the transaction is approved (usually ¡10 milliseconds).

For inactive card members with zero transactions in a given month, data were collected at the timestamp of their monthly billing statement date. The reason we use random historical transactions instead of the billing statement date for active card members is because we want to predict credit risk for each incoming transaction, which does not occur at a fixed time interval. Therefore, we introduce noise to the time interval in order to reduce the model’s dependence on it.

For low tenure card members with less than 12 months of transactions available, we zero-padded the sequences and applied a binary mask to the loss calculations during training. This technique excludes the padded timestamps from being used to update the model weights.

2.3. Model Evolution

We compared four different types of deep learning classification models, from simple neural networks to more complex ones, and compared their performance to a benchmark GBDT model for predicting credit risk. Since the GBDT algorithm was not designed to accommodate sequential data, we only used the last (i.e., most recent) month’s transaction to train the model. Similarly, two of the deep learning models (multilayer perceptron and TabNet) are also non-sequential and only used the most recent month’s transaction.

2.3.1. Multilayer Perceptron

We started our deep learning experiments with a straightforward implementation of the standard vanilla multilayer perceptron (MLP) neural network with dropout regularization. The MLP connects multiple layers of nodes/neurons in a forward-directed graph. Dropout regularization stochastically ”drops” some of these neurons during training in order to simulate an ensemble of different MLPs (Hinton et al., 2012). To train the connection weights of the model, a generalization of the least mean squares algorithm known as backpropagation was used to calculate the gradient of the loss function with respect to each weight by the chain rule, iterating backward from the last layer.

2.3.2. TabNet

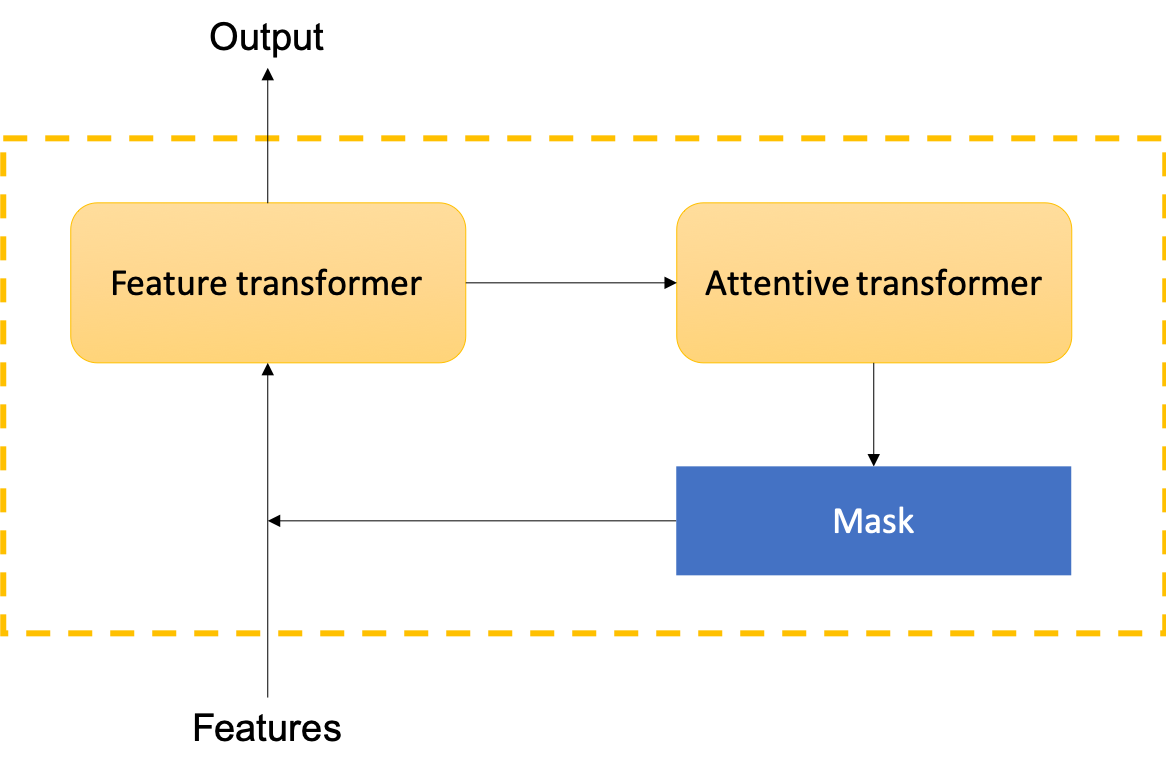

TabNet is a more recently developed neural network designed specifically for tabular, non-sequential data (Arik and Pfister, 2019). It utilizes an iterative attention mechanism for feature selection, where the final prediction score is an aggregate of all of the processed information from the previous iterations. A single iteration of the TabNet architecture contains two parts: a feature transformer and an attentive transformer. The output of the feature transformer is combined with the outputs from the previous iterations in order to obtain a final output decision. The attentive transformer creates a sparse feature mask vector, which is applied back to the initial feature set to generate a smaller subset of features that is fed into the next decision step (see Figure 3). The benefit of this technique is that it allows the network to fully utilize the most relevant features in a tabular dataset at each decision step, which enables more efficient learning.

2.3.3. Recurrent Neural Network

The aforementioned deep learning models suffer from a similar limitation as the baseline GBDT model: they don’t explicitly utilize card members’ historical data. RNNs address this issue by iteratively processing and saving information from previous transactions in its hidden nodes, which is then added to the current transaction in order to produce a more informed credit risk prediction.

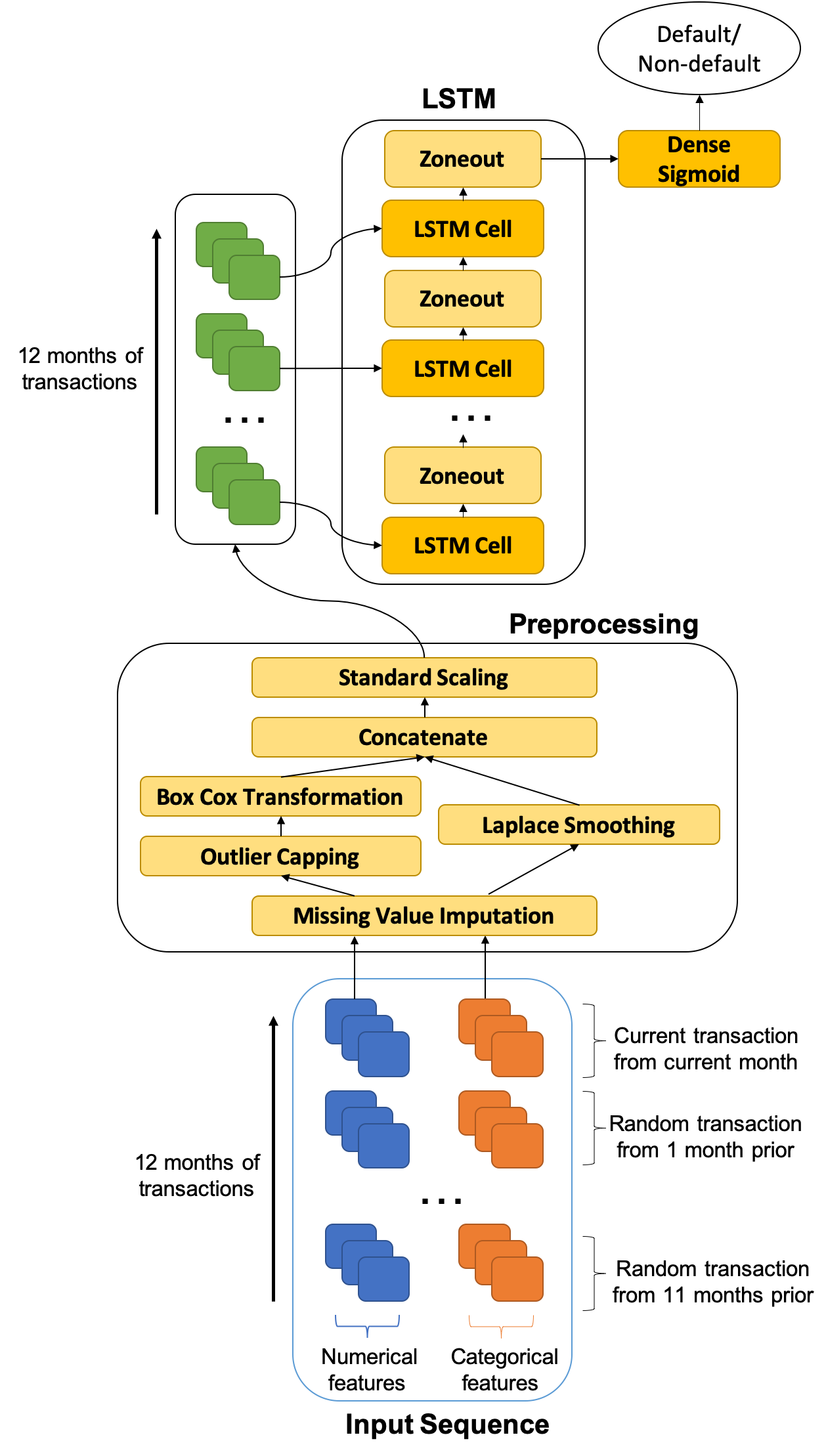

For this paper, we used a long short-term memory (LSTM) RNN (Hochreiter and Schmidhuber, 1997), which is a popular variant of the vanilla RNN that has been shown to more effectively learn long-term dependencies in sequential data. We also utilized a newer method for RNN regularization known as zoneout regularization (Krueger et al., 2017). Like dropout regularization, zoneout uses random noise to approximate training an ensemble of different RNNs. However, instead of dropping random recurrent connection weights, zoneout stochastically forces some of the hidden nodes to maintain their previous values from the previous transaction. The benefit of using zoneout over recurrent dropout is that it allows the RNN to remember more information from past transactions. An example of a single-layer LSTM model with zoneout regularization for predicting credit risk scores using our preprocessing approach is shown in Figure 4.

2.3.4. Temporal Convolutional Network

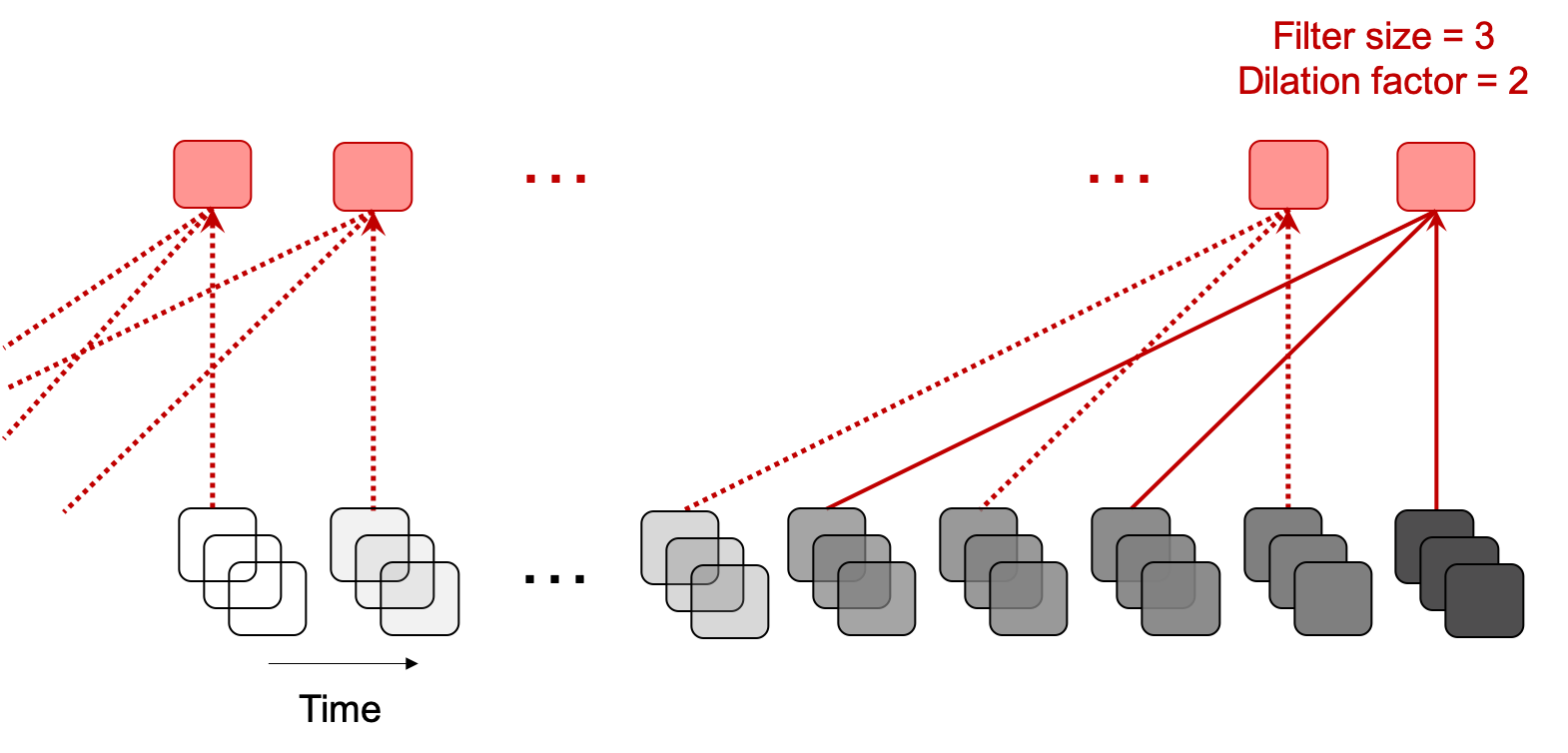

An important limitation of the RNN framework is that training the model can be time-consuming because sequences of data are processed iteratively. Additionally, the ability of RNNs to capture long-term dependencies in sequences remains a fundamental challenge (Pascanu et al., 2013). Therefore, more recent techniques have focused on more efficient convolution-based approaches for sequential data (Oord et al., 2016; Kalchbrenner et al., 2016; Dauphin et al., 2017; Gehring et al., 2017; Bai et al., 2018). Since convolutions can be done in parallel, sequences are processed as a whole instead of iteratively as in RNNs. Convolutional neurons can also utilize their receptive field to retain even more information from the distant past. Causal convolutions prevent leakage from the future by only convolving the output at time t with elements from time t and earlier (see Figure 7) (Waibel et al., 1989).

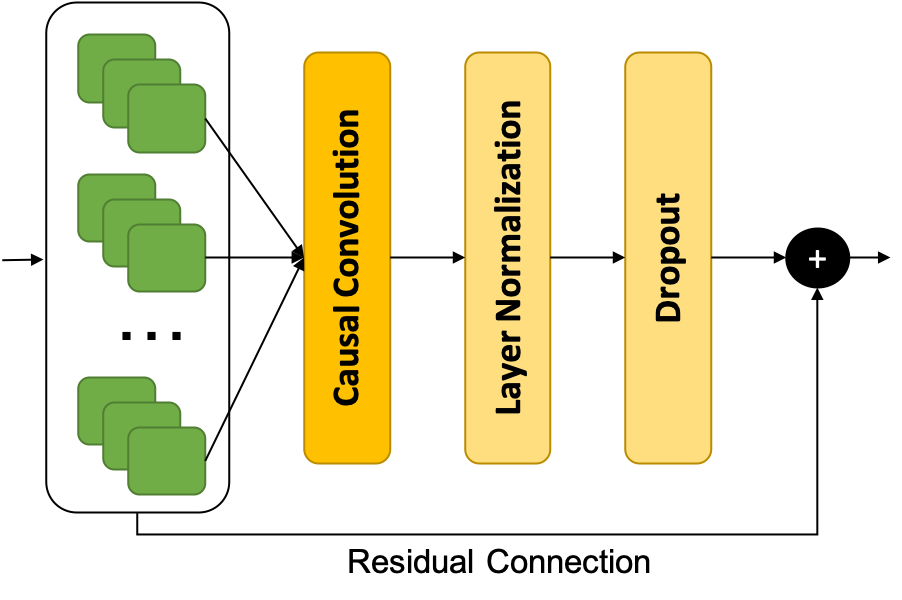

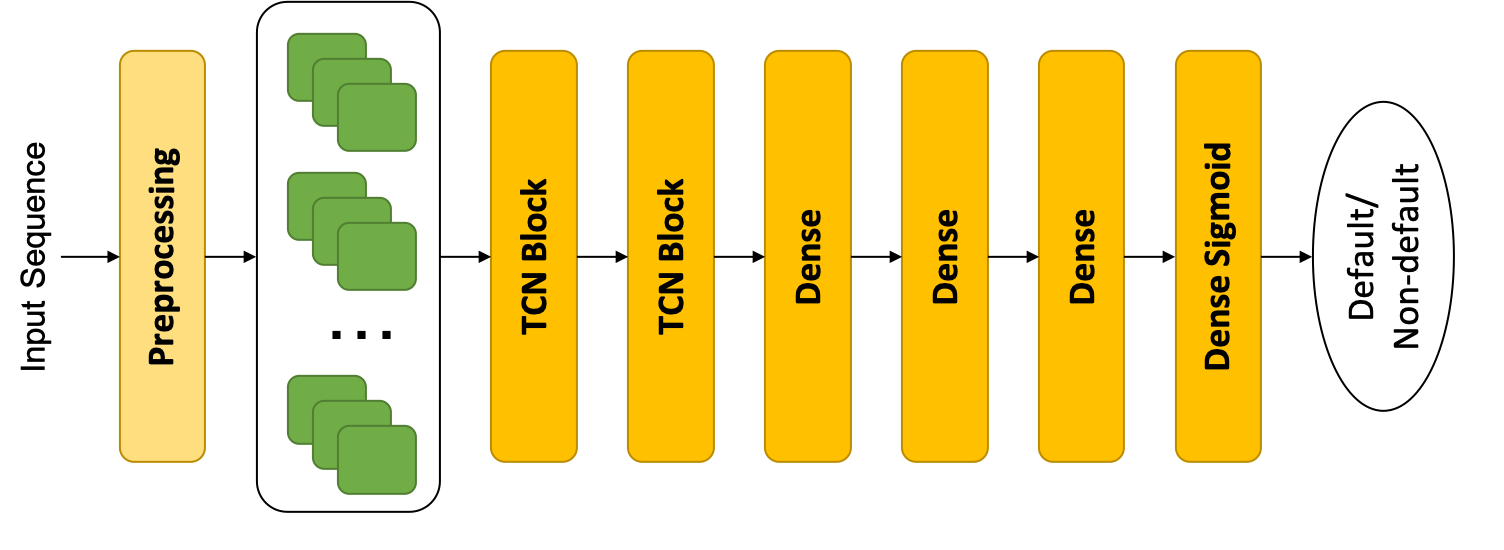

Perhaps the most popular recent causal convolution-based approach is the temporal convolutional network (TCN) (Bai et al., 2018). In addition to convolution and dropout, TCNs utilize dilation to enable larger receptive field sizes that look back at longer history lengths by introducing a fixed step size between every two adjacent convolutional filter taps (Yu and Koltun, 2016). TCNs also employ residual connections so that each convolutional layer learns an identity mapping rather than the entire transformation (see Figure 7), which helps stabilize deeper and wider models (He et al., 2016). Within each residual TCN block, layer normalization is applied to the output of the convolutional layer and dropout is added for regularization. An illustration of our final deep TCN architecture for the credit risk prediction task is shown in Figure 7.

2.4. Model Optimization and Tuning

2.4.1. Architecture Search

The final number of layers, neurons per layer, and dropout/zoneout rates used in each deep learning model were determined using an iterative Bayesian optimization approach with SigOpt (Dewancker et al., 2015). However, several of the top models performed similarly. We found that the best performance occurred for the 5-layer MLP, 3-layer LSTM (with 2 LSTM layers and one dense output layer), and 6-layer TCN (with 2 TCN blocks and 4 dense layers). Dropout and zoneout rates were kept fairly low in each model (averaging ~0.2).

2.4.2. Optimization

Each deep learning model was trained using the Adam optimization algorithm (Kingma and Ba, 2014) and early stopping (Prechelt, 1998). We used the default beta parameters for the Adam algorithm (betas = 0.9, 0.999) that control the decay rate for the first and second moment estimates of the gradient, although other values were explored and showed no obvious improvement. The classic binary cross entropy function for classification tasks was used as the loss function to be optimized.

2.4.3. Batch Size and Learning Rate

We also experimented with several batch sizes, learning rates, and learning rate schedules for the different architectures. We found that a universal batch size of 512 credit card members and a decay rate of 0.8, starting from an initial learning rate of 1e-4, was generally the most effective for all models.

2.4.4. Performance Metrics

Performance was measured in terms of the Gini coefficient and recall. The Gini coefficient is a common measurement of the discriminatory power of rating systems such as credit scoring models and is directly proportional to the area under the receiver operator characteristic curve (Gini = (2*AUROC) - 1). Recall, or sensitivity, is a measurement for the correct predictions of credit card default within a fixed fraction of the model’s top prediction scores. This fraction was determined by existing business principles and fixed across models.

3. Results

The performance results for each individual deep learning model and its ensemble with the benchmark GBDT are shown in Table 1. Performance results for the high debt exposure subpopulation (card members with a balance exceeding $15,000) are also included in this table to demonstrate the potential for substantial financial savings using our proposed approach.

The sequential models, LSTM and TCN, both outperformed the benchmark GBDT in isolation. The non-sequential neural networks, MLP and TabNet, performed worse than the benchmark. Additionally, a much larger boost in prediction performance was observed when the LSTM and TCN were used in an ensemble with GBDT, suggesting that historical information provides orthogonal information that is predictive of risky financial behavior. While these performance improvements may seem modest, it is important to keep in mind the large volume of card members that exists in the dataset, implying that small improvements lead to significant savings (in our case, an annual savings of tens of millions of US dollars).

| Overall | High Debt | |||

| Model | Gini (%) | Recall (%) | Gini (%) | Recall (%) |

| GBDT | 92.19 | 63.85 | 84.12 | 60.68 |

| MLP | 92.06 | 63.42 | 83.98 | 60.82 |

| TabNet | 92.03 | 63.5 | 83.92 | 61.02 |

| LSTM | 92.28 | 64.04 | 84.27 | 61.00 |

| TCN | 92.33 | 64.13 | 84.47 | 61.33 |

| GBDT + MLP | 92.26 | 64.10 | 84.44 | 61.64 |

| GBDT + TabNet | 92.26 | 64.11 | 84.46 | 61.57 |

| GBDT + LSTM | 92.49 | 64.75 | 84.83 | 62.13 |

| GBDT + TCN | 92.48 | 64.81 | 84.83 | 62.01 |

3.1. Early Risk Detection

In addition to capturing more risky behavior types, another important task for the model was to catch risky behavior as early as possible before the credit default occurred. This is essential when precautionary measures need to be implemented months in advance in order to reduce future financial losses.

| Gini/Recall (%) by Default Date | |||

| April - | November, 2018 - | May - | |

| Model | October, 2018 | April, 2019 | November, 2019 |

| GBDT | 95.56 / 81.60 | 90.38 / 59.64 | 86.24 / 45.95 |

| MLP | 95.48 / 80.90 | 90.24 / 59.26 | 86.08 / 45.81 |

| TabNet | 95.43 / 81.08 | 90.21 / 59.26 | 86.07 / 45.90 |

| LSTM | 95.53 / 81.27 | 90.50 / 60.11 | 86.43 / 46.43 |

| TCN | 95.49 / 81.09 | 90.58 / 60.32 | 86.57 / 46.75 |

A comparison of LSTM and TCN to GBDT for three different time bins (with the default event occurring in the near term, mid term, and long term) is shown in Table 2. While GBDT seems to outperform the sequential model in predicting defaults in the near term (within 6 months after the most recent transaction), the historical information incorporated in the sequential model helps predict defaults in medium term (between 7-12 months after the most recent transaction) and long term (between 13-18 months after the most recent transaction) more effectively, indicating that our approach improves early risk detection.

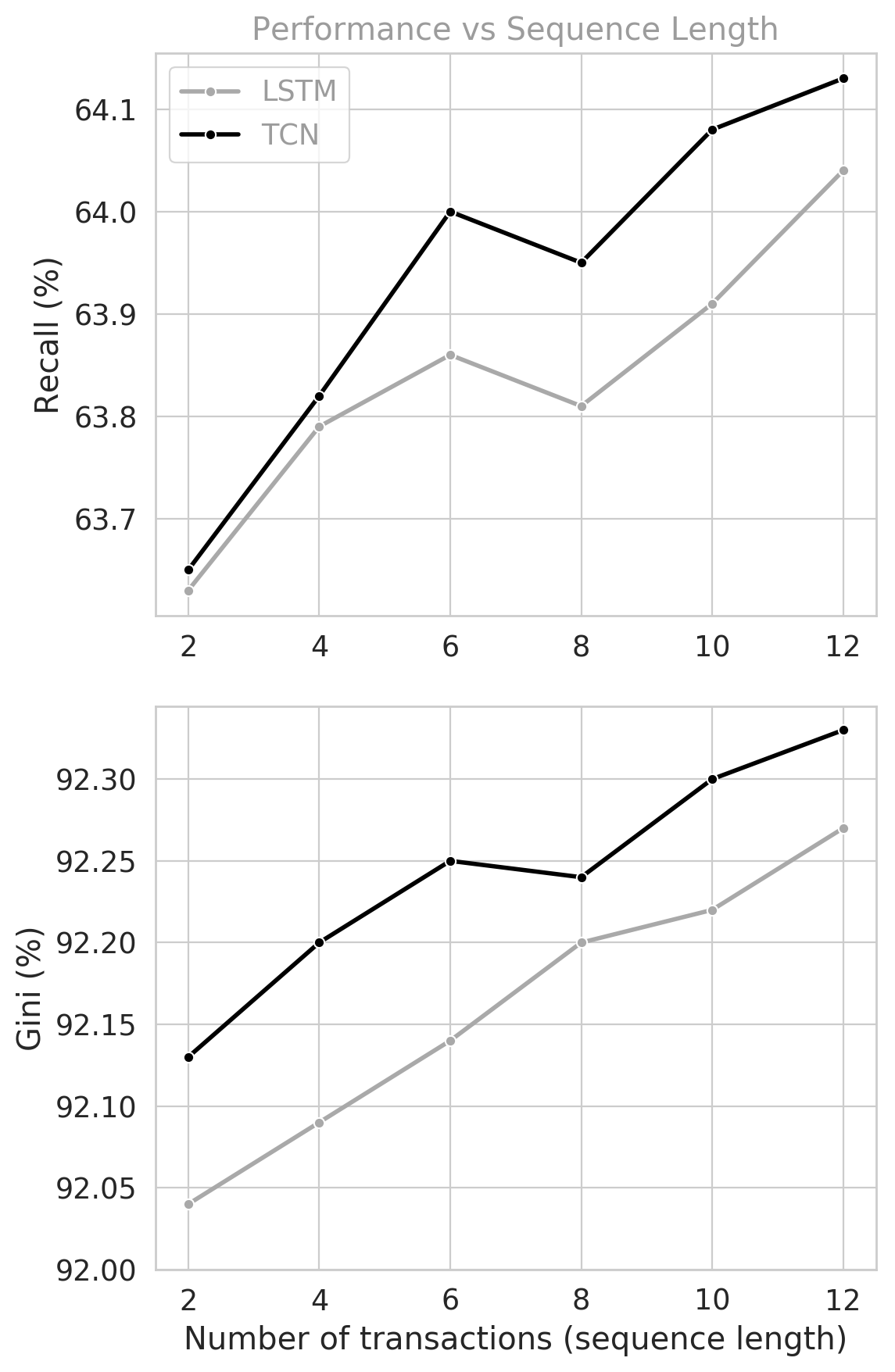

3.2. Sequence Length

Performance of the sequential models was also dependent on the number of input transactions used (i.e., the sequence length). In Figure 9, we show the degradation of performance in terms of Gini and recall as the number of monthly historical transactions included in the sequences decreased, meaning the ”look-back” period was shorter than a full year. Both the LSTM and TCN achieved the best results with 12 months of transactions, with TCN outperforming LSTM at each sequence length. Given the linear increase in performance as the sequence length increased, this suggests that looking back even further into borrowers’ financial history might provide better performance. However, we were limited by the available data that does not predate 2016.

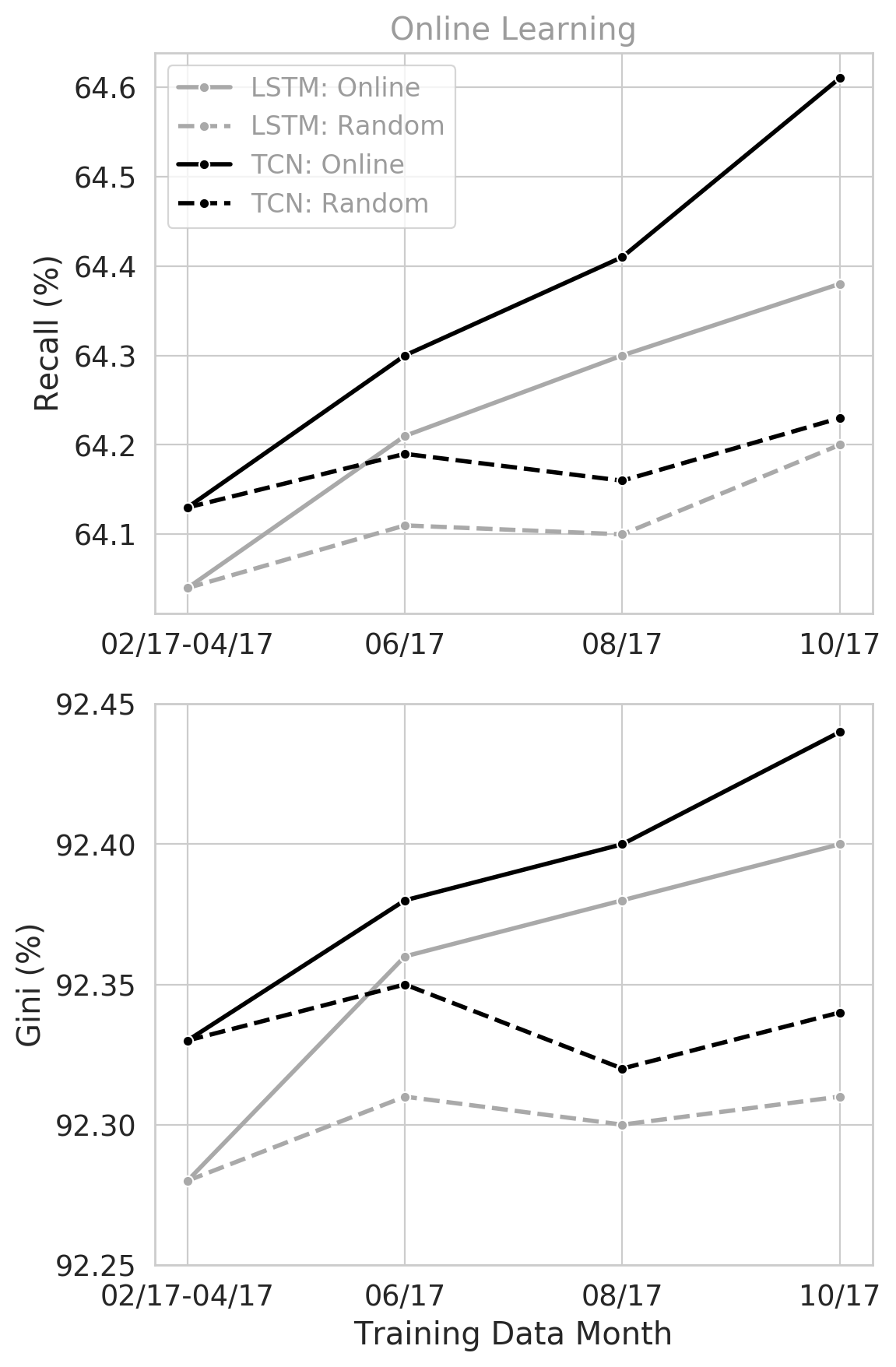

3.3. Online Learning

Since model performance is known to deteriorate with changes in consumer behavior and economic conditions, we also tested the LSTM’s and TCN’s ability to adapt to incoming data via online learning. To do this, we progressively tuned the weights of each model using sequences collected from three future months in 2017. We compared this method to the standard random weight initialization method in Figure 9, where the weights of the model are set to small random numbers before training.

As expected, performance gradually improved as more recent data were used to create the predictions. Additionally, progressively tuning the weights with incoming data outperformed the standard random weight initialization approach.

3.4. Training and Inference Time

Although the TCN outperformed the LSTM in terms of prediction performance, it is also important to consider their performance in terms of training and inference time for use in a production environment. Using an NVDIA Tesla V100 GPU, it took an average of ~30ms to train the TCN on a single mini-batch of 512 card members, compared to ~50ms for the LSTM. This was expected because the input sequence is processed as a whole by the TCN instead of sequentially as in the LSTM.

Anecdotally, inference time for the LSTM should be faster than the TCN. As suggested by Bai et al. (Bai et al., 2018), the LSTM only needs to save the next-to-last hidden state to memory and take in the current/incoming transactional data in order to generate a prediction. In contrast, the TCN needs to process the entire sequence. However, both methods were able to process a sequence in ¡1ms, which is much less than the time required for inference in our production environment (¡10ms). In future work, we will analyze the full pipeline for inference that includes the time it takes to preprocess the data for the incoming transaction in addition to the time it takes load the historical data (TCN) and the next-to-last hidden state (LSTM).

4. Conclusions

Current models for monitoring credit risk typically utilize boosted decision trees for their superior generalization accuracy when compared to that of other popular techniques, such as the multilayer perceptron. However, this approach is limited by its input features and inability to process sequential data efficiently.

In this paper, we investigated sequential deep learning methods for credit risk scoring and proposed a novel sampling method to generate sequences from one year of transaction-related tabular financial data. We compared the performance of our approach to the current tree-based production model and showed that our TCN, when combined with our sampling technique, achieved superior performance in terms of financial savings and early risk detection. Finally, we provided evidence that this framework would be suitable in our production environment and for online learning.

One major concern with our approach is the lack of interpretability that plagues black-box models such as the proposed LSTM and TCN. However, since GBDT also suffers from a similar interpretability problem, we do not directly use the prediction scores of the model to make account-level decisions. Instead, established and strategic business rules are used on top of (and in parallel with) the prediction score to ensure fairness and customer satisfaction.

Future work will focus on stress testing our deep sequential models and probing the prediction scores to determine if there exists sub-populations of card members for whom our new approach performs better than the benchmark on. It is also important to note that our data were collected during a relatively stable economic period that did not include any major recessions. As more data are collected going forward, we will be able to test the stability and generalization capability of our approach.

References

- (1)

- Addo et al. (2018) Peter Martey Addo, Dominique Guegan, and Bertrand Hassani. 2018. Credit risk analysis using machine and deep learning models. Risks 6, 2 (2018), 38. https://doi.org/10.3390/risks6020038

- Arik and Pfister (2019) Sercan O. Arik and Tomas Pfister. 2019. TabNet: Attentive Interpretable Tabular Learning. (2019). arXiv:1908.07442

- Babaev et al. (2019) Dmitrii Babaev, Alexander Tuzhilin, Maxim Savchenko, and Dmitrii Umerenkov. 2019. E.T.-Rnn: Applying deep learning to credit loan applications. In Proceedings of the ACM SIGKDD International Conference on Knowledge Discovery and Data Mining. 2183–2190. https://doi.org/10.1145/3292500.3330693

- Bai et al. (2018) Shaojie Bai, J. Zico Kolter, and Vladlen Koltun. 2018. An Empirical Evaluation of Generic Convolutional and Recurrent Networks for Sequence Modeling. (2018). arXiv:1803.01271

- Box and Cox (1964) George EP Box and David R Cox. 1964. An analysis of transformations. Journal of the Royal Statistical Society: Series B (Methodological) 26, 2 (1964), 211–243.

- Chen and Guestrin (2016) Tianqi Chen and Carlos Guestrin. 2016. Xgboost: A scalable tree boosting system. In Proceedings of the 22nd ACM SIGKDD Unternational Conference on Knowledge Discovery and Data Mining. 785–794.

- Dauphin et al. (2017) Yann N Dauphin, Angela Fan, Michael Auli, and David Grangier. 2017. Language modeling with gated convolutional networks. In Proceedings of the 34th International Conference on Machine Learning. 933–941.

- Dewancker et al. (2015) Ian Dewancker, Michael McCourt, and Scott Clark. 2015. Bayesian Optimization Primer.

- Efimov et al. (2019) Dmitry Efimov, Di Xu, Alexey Nefedov, and Archana Anandakrishnan. 2019. Using Generative Adversarial Networks to Synthesize Artificial Financial Datasets. In 33rd Conference on Neural Information Processing Systems, Workshop on Robust AI in Financial Services.

- Friedman (2001) Jerome H. Friedman. 2001. Greedy function approximation: A gradient boosting machine. Annals of Statistics 29, 5 (2001), 1189–1232. https://doi.org/10.2307/2699986

- Gehring et al. (2017) Jonas Gehring, Michael Auli, David Grangier, Denis Yarats, and Yann N Dauphin. 2017. Convolutional sequence to sequence learning. In Proceedings of the 34th International Conference on Machine Learning. 1243–1252.

- He et al. (2016) Kaiming He, Xiangyu Zhang, Shaoqing Ren, and Jian Sun. 2016. Identity mappings in deep residual networks, Vol. 9908 LNCS. Springer Verlag, 630–645. https://doi.org/10.1007/978-3-319-46493-0_38 arXiv:1603.05027

- Hinton et al. (2012) Geoffrey E Hinton, Nitish Srivastava, Alex Krizhevsky, Ilya Sutskever, and Ruslan R Salakhutdinov. 2012. Improving neural networks by preventing co-adaptation of feature detectors. arXiv:1207.0580 (2012).

- Hochreiter and Schmidhuber (1997) Sepp Hochreiter and Jürgen Schmidhuber. 1997. Long Short-Term Memory. Neural Computation 9, 8 (1997), 1735–1780. https://doi.org/10.1162/neco.1997.9.8.1735

- Kalchbrenner et al. (2016) Nal Kalchbrenner, Lasse Espeholt, Karen Simonyan, Aaron van den Oord, Alex Graves, and Koray Kavukcuoglu. 2016. Neural machine translation in linear time. arXiv preprint arXiv:1610.10099 (2016).

- Kingma and Ba (2014) Diederik P Kingma and Jimmy Ba. 2014. Adam: A method for stochastic optimization. arXiv preprint arXiv:1412.6980 (2014).

- Krueger et al. (2017) David Krueger, Tegan Maharaj, János Kramár, Mohammad Pezeshki, Nicolas Ballas, Nan Rosemary Ke, Anirudh Goyal, Yoshua Bengio, Aaron Courville, and Chris Pal. 2017. Zoneout: Regularizing rnns by randomly preserving hidden activations. In Proceedings of the 5th International Conference on Learning Representations. arXiv:1606.01305

- Manning et al. (2008) Christopher D Manning, Prabhakar Raghavan, and Hinrich Schütze. 2008. Introduction to information retrieval. Cambridge University Press. 234–265 pages.

- Nanni and Lumini (2009) Loris Nanni and Alessandra Lumini. 2009. An experimental comparison of ensemble of classifiers for bankruptcy prediction and credit scoring. Expert Systems with Applications 36, 2 (2009), 3028–3033. https://doi.org/10.1016/j.eswa.2008.01.018

- Oord et al. (2016) Aaron van den Oord, Sander Dieleman, Heiga Zen, Karen Simonyan, Oriol Vinyals, Alex Graves, Nal Kalchbrenner, Andrew Senior, and Koray Kavukcuoglu. 2016. Wavenet: A generative model for raw audio. arXiv preprint arXiv:1609.03499 (2016).

- Pascanu et al. (2013) Razvan Pascanu, Tomas Mikolov, and Yoshua Bengio. 2013. On the difficulty of training recurrent neural networks. In Proceedings of the 30th International Conference on Machine Learning. 1310–1318.

- Prechelt (1998) Lutz Prechelt. 1998. Early stopping-but when? In Neural Networks: Tricks of the trade. Springer, 55–69.

- Roy et al. (2018) Abhimanyu Roy, Jingyi Sun, Robert Mahoney, Loreto Alonzi, Stephen Adams, and Peter Beling. 2018. Deep learning detecting fraud in credit card transactions. In Proceedings of the Systems and Information Engineering Design Symposium, 2018. 129–134. https://doi.org/10.1109/SIEDS.2018.8374722

- Thomas et al. (2002) Lyn C Thomas, David B Edelman, and Jonathan N Crook. 2002. Credit scoring and its applications. SIAM.

- Waibel et al. (1989) Alex Waibel, Toshiyuki Hanazawa, Geoffrey Hinton, Kiyohiro Shikano, and Kevin J Lang. 1989. Phoneme recognition using time-delay neural networks. IEEE transactions on acoustics, speech, and signal processing 37, 3 (1989), 328–339.

- Wang et al. (2018) Chongren Wang, Dongmei Han, Qigang Liu, and Suyuan Luo. 2018. A deep learning approach for credit scoring of Peer-to-Peer lending using attention mechanism LSTM. IEEE Access 7 (2018), 2161–2168.

- Yu and Koltun (2016) Fisher Yu and Vladlen Koltun. 2016. Multi-scale context aggregation by dilated convolutions. In Proceedings of the 4th International Conference on Learning Representations. arXiv:1511.07122