Testing the effectiveness of unconventional monetary policy in Japan and the United States††thanks: We appreciate comments from three anonymous referees, Jesús Fernández-Villaverde, Jordi Galí, Simon Gilchrist, Fumio Hayashi, Hibiki Ichiue, Junko Koeda, Davide Porcellacchia, Mototsugu Shintani, and Nao Sudo, seminar and conference participants at CIGS End of the Year Conference 2019, ECB-BoJ-BoE Joint Research Workshop, Econometric Society World Congress 2020, SED 2021, Bank of Japan, University of Pavia, Kobe University, University of Pompeu Fabra, Osaka University, and University of Oxford. Mavroeidis acknowledges the financial support of the European Research Council via Consolidator grant number 647152. Views expressed in the paper are those of the authors and do not necessarily reflect the official views of the Bank of Japan.

Abstract

Unconventional monetary policy (UMP) may make the effective lower bound (ELB) on the short-term interest rate irrelevant. We develop a theoretical model that underpins our empirical test of this ‘irrelevance hypothesis,’ based on the simple idea that under the hypothesis, the short rate can be excluded in any empirical model that accounts for alternative measures of monetary policy. We test the hypothesis for Japan and the United States using a structural vector autoregressive model with the ELB. We firmly reject the hypothesis but find that UMP has had strong delayed effects.

JEL Classification: E52, E58.

Keywords: Effective lower bound, unconventional monetary policy, structural VAR.

1 Introduction

Adjustments in the overnight nominal interest rate have been the primary tool for the implementation of monetary policy since the early 1980s. In recent years, however, the short-term nominal interest rate reached an effective lower bound (ELB) in several countries, making the standard policy tool de facto ineffective. Two prominent examples are Japan whose policy rate has been at the ELB for most of the past quarter century, and the United States that reached the ELB in the aftermath of the global financial crisis of 2007–2008. The central banks in these countries countervailed the inapplicability of the standard policy tool by embarking on unconventional monetary policy (UMP) that involves the purchases of long-term government bonds and the use of forward guidance to signal future policy action.111See Christensen and Rudebusch (2012), Liu et al. (2019), Campbell et al. (2020), and Carlson et al. (2020) for the U.S., and Ugai (2007), and Bank of Japan (2016b) for Japan. Ueda (2012) provides a comparison of monetary policy between the U.S. and Japan.

The effectiveness of UMP is a central issue for policymakers. One view is that the ELB restricts the effectiveness of monetary policy, thus representing an important constraint on what monetary policy can achieve, as argued by Eggertsson and Woodford (2003), Gust et al. (2017) and Eberly, Stock and Wright (2020). An alternative view is that UMP can affect long-term interest rates so significantly that UMP has been fully effective in circumventing the ELB constraint, as argued by Swanson and Williams (2014) and Debortoli, Galí and Gambetti (2019). This latter view has been termed as the ELB ‘irrelevance hypothesis.’ The issue of the effectiveness of UMP has gained relevance since the ELB is likely to bind more often in the future with historically low levels of the longer-run natural rate of interest (Duarte et al., 2020).

This paper studies the irrelevance hypothesis of the ELB both theoretically and empirically. It develops a dynamic stochastic general equilibrium (DSGE) model with UMP. To the best of our knowledge, this is the first study that analytically characterizes the irrelevance hypothesis in a DSGE model. The model provides the theoretical underpinning to our novel empirical tests, and it shows that censored and kinked vector autoregressive models (VARs) are a suitable empirical framework to test the irrelevance hypothesis. Our empirical results show that the hypothesis is strongly rejected for both Japan and the U.S. Despite the rejection, the estimated impulse responses to a monetary policy shock indicate strong delayed effects of UMP in each country.

The idea of the irrelevance hypothesis is that observable properties of macroeconomic variables such as their dynamics and volatilities remain unchanged when the economy moves in and out of an ELB regime, for otherwise the ELB is empirically relevant. This idea can be applied to any theoretical model with the ELB. This insight allows us to test the irrelevance hypothesis using reduced-form VAR models and therefore, our empirical results about this hypothesis hold for any theoretical model with the ELB as long as it has a VAR representation. The purpose of our DSGE model is to formalize this idea by showing that such a theoretical model actually exists, and to guide our empirical approach to identifying the effectiveness of UMP when the irrelevance hypothesis does not hold.

In our model, UMP consists of (i) quantitative easing (QE) implemented by long-term government bond purchases that directly affect long-term government bond yields, and (ii) forward guidance (FG) under which the central bank commits to keeping short-term interest rates low in the future. A key variable in the model is the ‘shadow rate,’ which we label and it is defined as the short-term interest rate that the central bank would set if there were no ELB. The short rate is given by , where is the ELB. The shadow rate is equal to the short rate in a non-ELB regime, but it is unobservable in an ELB regime where the policy rate is constrained at the ELB. The shadow rate can be negative and interpreted as the indicator of the desired stance of monetary policy in terms of the short rate.

In the model the central bank resorts to UMP in an ELB regime by using the shadow rate for the guidance of its policy stance, as in the case of a non-ELB regime where the short rate is equal to the shadow rate. The model shows that UMP entails wide degrees of effectiveness, including the irrelevance of the ELB in which UMP retains the same effectiveness as the conventional policy that adjusts the short rate as if there were no ELB. We show that under the irrelevance of the ELB, the log-linearized DSGE model can be written in terms of inflation, the output-gap, the long-term interest rate or the shadow rate, and it retains the same VAR representation for both ELB and non-ELB regimes, thus providing the theoretical foundation to our empirical tests.

Motivated by our theoretical results, we use the censored and kinked structural VAR model developed by Mavroeidis (2021) to test the irrelevance hypothesis. Our DSGE model shows that a direct appraisal of the irrelevance hypothesis is to test whether a short-term interest rate, which is subject to the ELB, can be excluded from the VARs that include alternative measures of monetary policy that are not subject to the ELB, such as a long-term interest rate and the shadow rate. The exclusion of the short rate in VARs that include the long rate is a novel empirical test developed in this paper. The exclusion of the short rate in VARs that include the shadow rate, which is proposed by Mavroeidis (2021), is our second test for robustness.

Our theoretical model implies that under the irrelevance hypothesis there is no attenuation in the response of the long rate to shocks when short rates are at the ELB, a focal point for the assessment of the irrelevance hypothesis in Swanson and Williams (2014) and Gilchrist, López-Salido and Zakrajšek (2015). We study the attenuation effect by focusing on the different impact of the monetary policy shock on the long rate in the non-ELB and ELB regimes. Our monetary policy shock is a traditional monetary policy shock – a shock to the short rate – in a non-ELB regime while in an ELB regime it is a UMP shock – a shock to the shadow rate. Motivated by our theory, we use the VAR model to characterize analytically a formal test for the attenuation effect in the response of the long rate to a shock to monetary policy at the ELB.

We conduct the tests of the irrelevance hypothesis of the ELB on postwar data for Japan and the U.S. We consider several different VAR specifications, varying the lag order and the estimation sample (to account for structural change), and using alternative measures of monetary policy such as government bond yields with different maturities. In all cases, the tests overwhelmingly and consistently reject the hypothesis that the ELB has been empirically irrelevant for both economies. Our conclusion is therefore fairly robust: the ELB does represent a constraint on what monetary policy can achieve in those economies.222This evidence corroborates Bernanke (2020) who claims that “it also seems unlikely that the new tools deployed during the Great Recession entirely compensated for the limits imposed by the lower bound,”and is consistent with the findings in Gust et al. (2017) and Del Negro et al. (2017), who attribute an important role to the ELB for the decline in output during the financial crisis. We also firmly reject the hypothesis of no attenuation in the response of the yield curve to monetary policy shocks during ELB regimes in both economies.

The rejection of the irrelevance hypothesis leaves open the question of the degree of effectiveness of UMP in an ELB regime compared to the conventional policy in a non-ELB regime. To address this question, we identify the dynamic effects of conventional and unconventional policies by combining the identifying power of the ELB with additional sign restrictions on impulse responses to a monetary policy shock à la Uhlig (2005). The ELB enables partial identification of impulse responses to a monetary policy shock, as shown in Mavroeidis (2021), because a change in the behaviour of the economy across ELB and non-ELB regimes is informative about the relative impact of conventional and unconventional policy. The identified set based only on the ELB turns out to be fairly wide, so we use the insights from our DSGE model to impose the theoretically-congruous sign restrictions that were used in Debortoli, Galí and Gambetti (2019). The sign restrictions markedly sharpen the identified set of impulse responses.

We find that the effects of monetary policy on inflation and output on impact (i.e., within one quarter) declined when the economy entered an ELB regime: they dropped by more than percent in the U.S., and more than percent in Japan, relative to conventional policy. However, the cumulative effects of monetary policy exhibited the opposite pattern one and two years ahead: they appear to have been stronger during an ELB regime relative to a non-ELB regime, except for the response of output gap in the U.S., which remained weaker. Therefore, UMP seems to have had a delayed but stronger effect than conventional policy on inflation in the U.S., and on both inflation and output in Japan. Thus, we conclusively reject the hypothesis that the ELB has been empirically irrelevant in both countries, and find that responses of inflation and output to UMP have been different across time and across countries.

Related literature

Our analysis is closely related to two strands of research. The first pertains to theoretical studies that investigate the transmission mechanism of unconventional monetary policy. Among those, regarding QE, our theoretical model is close in spirit to Andrés, López-Salido and Nelson (2004), Chen, Cúrdia and Ferrero (2012), Harrison (2012), Gertler and Karadi (2013), Liu et al. (2019), and Sudo and Tanaka (2021). These studies introduce assets with different maturities and limit arbitrage across assets to break the irrelevance of QE that is shown by Eggertsson and Woodford (2003).333For other possible channels of QE, see Krishnamurthy and Vissing-Jorgensen (2011). See also Sims and Wu (2021) for a recent discussion on the theoretical frameworks to study UMP. Regarding FG, our model follows Reifschneider and Williams (2000), and it considers this mechanism in a general equilibrium model that directly accounts for QE. Our main contribution to this first strand of literature is to develop a simple model of UMP, which incorporates the shadow rate and provides the theoretical underpinnings to our empirical analyses.

The second strand of literature pertains to empirical studies that assess the effectiveness of unconventional policy. In addition to Swanson and Williams (2014) who estimate the time-varying sensitivity of longer-maturity yields to macroeconomic news using high-frequency data, it includes Debortoli, Galí and Gambetti (2019) who use a SVAR to investigate the (ir)relevance of the ELB constraint by comparing impulse responses to shocks between normal times and ELB episodes. Differing from our SVAR, their SVAR does not include short-term interest rates. Another related study by Inoue and Rossi (2019) uses an SVAR with shocks to the entire yield curve and finds evidence that UMP has been effective in the U.S. Our empirical methodology is closely related to Hayashi and Koeda’s (2019), who propose an SVAR model for Japan that includes short rates and takes into account the ELB, and our empirical model for Japan relies heavily on the insights from their empirical analysis. The main difference of our methodology from Hayashi and Koeda’s (2019) is that we use a shadow rate to model UMP, which nests QE as long-term government bond purchases and FG as a policy rule as in Reifschneider and Williams (2000), while Hayashi and Koeda (2019) use excess reserves to model QE and an inflation exit condition to model FG. Our methodology provides a simpler framework to test the irrelevance hypothesis of the ELB and to compare the effectiveness of UMP relative to conventional policy.

Finally, our empirical analysis uses the estimation methodology in Mavroeidis (2021), who also reports evidence against the irrelevance hypothesis for the U.S. using a three-equation VAR model. We have several differences from that study: we develop a novel theoretical DSGE model of UMP that provides the underpinnings for a new test of the irrelevance hypothesis based on the exclusion of short rates; we characterize analytically and obtain a new formal test of no attenuation of the effect of monetary policy on long rates at the ELB; we use sign restrictions motivated from our theoretical model to sharpen the identification of impulse responses; we estimate the dynamic effects of UMP and the shadow rates in each country; we study Japanese data and conduct several robustness checks.

The structure of the paper is as follows. Section 2 develops a simple New Keynesian DSGE model with UMP that provides theoretical underpinnings to our empirical model and the tests of the irrelevance hypothesis of the ELB. Section 3 introduces the econometric methodology and presents the tests of the irrelevance hypothesis from the reduced-form solution of the SVAR. Section 4 describes the data and reports our empirical results. Section 5 studies the effectiveness of UMP and its differences relative to conventional monetary policy. Section 6 concludes. The Appendix provides supporting material on the derivation of the DSGE model, additional empirical results, and the estimates of the shadow rates for Japan and the U.S.

2 A theoretical model of UMP

In this section, we develop a simple theoretical model of UMP and provide theoretical underpinnings to our empirical specifications and testing approaches to the irrelevance hypothesis. Section 2.1 presents the model with a focus on UMP. Section 2.2 studies the linear and non-linear VAR representations of the model that underpin our empirical analysis. Section 2.3 simulates the model and illustrates how UMP can make the ELB irrelevant. The details of the model, equation derivations, parameterization, and model simulations are reported in Appendix A.

2.1 Central equations

Overview

The model is a New Keynesian model in which QE and FG are active under the ELB. The economy consists of households, firms, and a central bank. The firm sector is standard as in a typical New Keynesian model. The household sector comprises two types of households. Constrained households purchase long-term government bonds only, but unconstrained households can trade both short- and long-term government bonds subject to a trading cost. The trading cost captures bond market segmentation, as in the preferred habitat theory originally proposed by Modigliani and Sutch (1966), and it introduces imperfect substitutability between long- and short-term government bonds that generates a spread between the yields of these bonds.444The preferred habitat model is the predominant modelling framework to study UMP. See among others Chen, Cúrdia and Ferrero (2012), Liu et al. (2019), and Sims and Wu (2021). The trading cost depends on the amount of long-term government bonds circulated in the market. By purchasing long-term government bonds, the central bank can affect the spread and thereby the long-term yield.

Conventional monetary policy

The central bank sets the short-term nominal interest rate using a standard Taylor rule subject to the ELB. Let , , and denote the deviation of output, inflation, and the short-term interest rate from the steady state in period . Following conventional notation, the caret on a variable denotes the deviation of the variable from steady state. The short-term interest rate is set according to

| (1) | |||

| (2) | |||

| (3) |

where , , , , , and is a monetary policy shock. Equation (1) encapsulates the ELB constraint, where is the ELB and is the shadow rate.555For the interest rate, the deviation from steady state is expressed in terms of the gross interest rate. That is, , where is the short-term net interest rate in steady state. Hence, since the ELB is equal to and , the deviation of from the steady-state interest rate can be written as: .

We use the term ‘shadow rate’ since is unobserved under the ELB and therefore censored at the ELB, while it is observed and equal to outside the ELB constraint. Our shadow rate represents the desired stance of monetary policy for the short-term interest rate, as opposed to the effective policy stance, e.g., in Wu and Xia (2016).

A monetary policy shock in our model is a shock to the shadow rate, which is identical to a shock to the short-term interest rate in the non-ELB regime. Equations (2) and (3) allow for FG to influence the system in the ELB regime, as we discuss below. In the non-ELB regime when , equations (1)-(3) reduce to with the Taylor-rule rate being equal to

| (4) |

This equation is a standard Taylor rule that sets the current interest rate in response to the interest rate in period , and current inflation and output.

Forward guidance

Equations (2) and (3) allow FG to maintain the short-term interest rate at a lower level than the rate implied by the standard Taylor rule (4). The intensity of FG is governed by the two parameters and . To see the isolated effect of , we first consider the case of that implies in equation (2). In the non-ELB regime equation (3) collapses to the standard Taylor rule (4). In the ELB regime of , if , the lagged term of equation (3) is ; if , however, the lagged term becomes , exerting additional downward pressures on in equation (3) and on in equation (2) since . The decrease in today keeps the interest rate low from equation (1), and moreover it keeps the future interest rate low by reducing the shadow rate tomorrow, leading to the same effect of FG in Debortoli, Galí and Gambetti (2019).

Next consider the case of . Equation (2) implies that FG is additionally strengthened since the shadow rate is kept lower than the Taylor-rule rate, under the ELB. Our implementation of FG is similar to Reifschneider and Williams (2000). For a given degree of interest rate smoothing (), the parameter generates downward pressure on the shadow rate in the ELB regime, and further magnifies the downward reduction of the shadow rate. Thus, primarily influences the persistence of the shadow rate, while influences its level. Note that we also use below to measure the effectiveness of QE, i.e., it is not a free parameter in equation (3) but will be determined later by equation (13). This helps us simplify the theoretical model, and results in a parameter that jointly influences FG and QE policy, see Lemma 1 below.

Quantitative easing

In the ELB regime, the short-term interest rate is fixed at the ELB, and the central bank starts QE by purchasing long-term government bonds (consol bonds). The long-term bond issued in period pays dollars at time . Let denote the price of the long-term bond, and let denote the return of holding it from period to . The price and the return conditional on period- information are linked as

| (5) |

where is the expectation operator conditional on period- information. The gross yield to maturity (or the long-term interest rate) at time , , can be defined as

or

| (6) |

Log-linearizing equations (5) and (6) around steady state and combining them yields

| (7) |

where is the long-term interest rate in steady state.

Unrestricted households that trade both long- and short-term government bonds pay a unitary cost for trading long-term bonds. An arbitrage between holding short- and long-term bonds yields

| (8) |

where and are the trading cost in deviation from steady state and in steady state, respectively. The trading cost introduces a spread between the returns of holding long- and short-term bonds. The trading cost is assumed to be increasing in the real amount of long-term bonds circulated in the market, , and is given by

| (9) |

where represents the elasticity of the trading cost with respect to the amount of long-term bonds in the market.

The central bank conducts QE according to the rule:

| (10) |

Parameter governs how aggressively the central bank purchases long-term bonds under the ELB, with corresponding to no purchase. In the ELB regime, where holds, the central bank purchases and absorbs long-term bonds from the market, so that . The central bank conducts QE by using the shadow rate as policy guidance similar to the conventional monetary policy. For instance, assume in equation (2), such that . In the ELB regime, the more the shadow rate drops as a result of a decrease in inflation or output, the more the central bank purchases long-term government bonds. Thus, the central bank consistently aims at stabilizing inflation and output in both the non-ELB and ELB regimes.

Since constrained households hold long-term government bonds only while unconstrained households also hold short-term government bonds, the ‘effective’ interest rate relevant to output and inflation is the weighted sum of the returns of holding short- and long-term government bonds, , where is the population share of unconstrained households.666The underlying assumption in deriving the effective interest rate is that the consumption of the two types of households is identical in steady state. The Euler equation is then given by

| (11) |

where is a demand (preference) shock, and . Note that the expected return of holding the long-term bonds depends on the trading cost (equation 8), which depends on the real value of long-term bonds in the market (equation 9), which in turn is controlled by QE that uses the shadow rate as policy guidance (equation 10). Hence, can be written as a function of . Substituting equations (8)–(10) into the Euler equation (11) yields

| (12) |

where is given by

| (13) |

The parameter determines the effectiveness of QE. If , for instance as a result of or , equation (12) reduces to the standard Euler equation that omits the shadow rate. If , QE is ‘fully effective’ and the interest rate becomes irrelevant to the Euler equation and the dynamics of the system, and consequently the ELB will be irrelevant for the dynamics of the economy. From equation (13), the effectiveness of QE increases in the share of restricted households, , the trading cost in steady state, , the elasticity of the trading cost with respect to the amount of long-term government bonds circulated in the market, , and strength in the purchasing of long-term bonds by the central bank in response to a change in the shadow rate, .

Comparing equations (11) and (12) shows that the effective interest rate relevant to output and inflation is equal to the weighted interest rate, . Thus the weighted interest rate can also be interpreted as the effective interest rate, and this appears as a lagged variable in the Taylor rule (3) that implements FG. The parameter depends on structural parameters pertaining to QE, as shown in equation (13). In this sense, the parameter encapsulates the effectiveness of UMP that reflects both QE and FG.

Long-term interest rates

Combining equations (7)–(10) yields the long-term interest rate, given by

| (14) |

where is set by equation (1). Equation (14) shows that the effects of the shadow rate and the degree of the effectiveness of UMP on the long-term interest rate are different between the two regimes. In the non-ELB regime, and the expectation hypothesis holds: the long rate is given by the weighted sum of the expected short rates today and in the future. In the ELB regime, the short rate is bounded at and the long rate is affected by QE as the shadow rate appears in the lower equation in (14).

In the limiting case where the number of unconstrained households becomes infinitesimally small asymptotically, , the difference between the two regimes in equation (14) vanishes and the long-term interest rate can be written in the form

| (15) |

In this case, the expectation hypothesis holds with respect to the effective interest rate, . In addition, equation (15) makes clear the presence of the attenuation bias of the long rate in the ELB regime and that it is related to the UMP effectiveness parameter . In the case of full effectiveness of UMP, i.e., , the long rate is always given by the expected sum of the shadow rates and there will be no attenuation of the long rate in the ELB regime. However, in the case of less effective UMP, i.e., , the long rate responds less to the shadow rate, giving rise to its attenuated response in the ELB regime.

System of equations

We close the model by reporting the standard New Keynesian Phillips curve that relates the current inflation to expected inflation and output, given by

| (16) |

where , , and is a supply (productivity) shock. The supply and demand shocks follow an AR(1) process. To summarize, our model of UMP comprises the six equations (1), (2), (3), (12), (14), and (16), the six endogenous variables , and the three shocks .

2.2 DSGE model and VAR representations

We use our DSGE model developed in Section 2.1 to derive the VAR representations that underpin our empirical models and tests to be introduced in Section 3.

The joint effect of QE and FG

Before deriving VAR representations, it is useful to note that we cannot separate out the effects of the two parameters and in the system, but the model allows us to identify their joint effect on the system, encapsulated by . The next lemma states the result formally.

Lemma 1

For any and that satisfy , the model with and is observationally equivalent to the model with and .

The proof is straightforward. By using equation (2) to substitute out , the effective interest rate, , can be replaced with . The parameter does not appear anywhere in the model except in . The parameter appears only in equation (1) as . But this equation is observationally equivalent to because only is observable, and thus the joint effect of QE and FG is summarized by the parameter that encompasses and .777QE and FG are not separately identifiable here because they both operate only in the ELB regime during which the shadow rate is unobserved and only identified up to scale, see Mavroeidis (2021) for further discussion. It might be possible to disentangle the two policies if, for example, one of them operated also outside the ELB, as in Swanson (2021). This would require some additional assumptions to carefully model more than two endogenously-switching regimes.

As an illustrative example, consider a case in which QE is half as effective as the conventional monetary policy (i.e., ) but FG is active with . In this scenario, the monetary policy shock is twice as large in the ELB regime as the same shock in the non-ELB regime (or, equivalently, at the ELB regime with and ). The impact of such a monetary policy shock at the ELB regime is of the same magnitude as the equivalent shock in the non-ELB regime. Thus, the effectiveness of UMP in the theoretical model depends on that encapsulates the joint effect of and , and encompasses the combination of QE and FG.

Irrelevance of the ELB and VAR representations

Now we establish the VAR representations of the DSGE model under the irrelevance hypothesis of the ELB, where UMP is as effective as the conventional policy: . There will be different VAR representations, depending on what assumptions we impose on the model. Specifically, we begin by considering the following assumption.

Assumption 1

The number of unrestricted households becomes infinitesimally small asymptotically: .

Under the irrelevance of the ELB, the solution to the model entails two VAR(1) representations, as formalized in the following proposition.

Proposition 1

Proof. Appendix A.4.

Proposition 1(i) shows that under the irrelevance of the ELB, the short-term interest rate is redundant for the dynamics of output and inflation once the shadow rate is included in the VAR. Whether the short rate is constrained by the ELB or not does not influence the dynamics of output and inflation, so that the ELB is irrelevant. What distinguishes our VAR from a standard linear VAR is that the shadow rate is censored at the ELB. In other words, for an econometrician, the shadow rate is observable, and equal to the nominal interest rate, only when it is above the ELB (equation 1).

Proposition 1(ii) shows that the long rate can be a sufficient indicator of monetary policy. Under Assumption 1, the shadow rate has no direct effect on the economy while having an indirect effect by affecting the long rate, and under the irrelevance of the ELB, the shadow rate and the long rate become interchangeable as implied by equation (15) with and without loss of generality from Lemma 1. Intuitively, in such a special case, the expectation hypothesis holds and the long rate is given by the expected sum of the shadow rates today and in the future, giving rise to a one-to-one relation between the long rate and the shadow rate. The corollary of Proposition 1(ii) is that under the irrelevance hypothesis there is no attenuation of the response of the long rate, i.e., the dynamics of the long rate are identical between the non-ELB and ELB regimes. We will use Proposition 1 to underpin our approach to testing the irrelevance hypothesis of the ELB and no attenuation effect in Section 3.

Assumption 1 plays a critical role in deriving the VAR representation with the long rate under the irrelevance of the ELB, i.e., the specific irrelevance hypothesis used in the literature (e.g., Debortoli, Galí and Gambetti, 2019). Without the assumption, equation (14) shows that even under the irrelevance of the ELB (), the long rate is kinked at the ELB: the first-term in equation (14) is smaller by in the ELB regime than in the non-ELB regime. Why does the long rate have to decrease more in the ELB regime to make the ELB irrelevant? The reason is straightforward. Unrestricted households hold short-term government bonds whose relevant interest rate is the short rate. To stimulate the aggregate consumption as if the economy were not at the ELB, consumption by the restricted households must be stimulated more, which requires a stronger decrease in the long rate under the ELB. Put differently, the decrease in the long rate needed to satisfy the irrelevance of monetary policy at the ELB regime becomes less pronounced with the reduction of unrestricted agents. Thus, Assumption 1 is important to validate the VAR representation with the long rate.

Relevance of the ELB and VAR representations

Now consider the case of a less effective UMP than conventional policy (i.e., ). In this general case, the model does not have a tractable solution under rational expectations and thus it would not have a VAR representation. However, the model admits a tractable solution if the formation of expectations slightly deviates from rational expectations by the following assumption.

Assumption 2

In each period , agents know the true today and form expectations under the presumption of from period onward.

This assumption implies that agents entail behavioral expectations and believe that UMP will be as effective as the conventional policy from the next period onwards. Under this assumption, the VAR model has a piecewise linear representation, as stated in the following proposition.

Proposition 2

Proof. Appendix A.5

Proposition 2 implies that in the case of the dynamics of the economy differ between the non-ELB and ELB regimes as the dynamics in each regime is represented by a distinct VAR where a change in regimes occurs when the short-term interest rate crosses the ELB. This result echos with Aruoba et al. (2021), who argue that a piecewise linear solution to a DSGE model with an occasionally binding ELB constraint can be interpreted as describing the behavior of boundedly rational agents. Our specific assumption on the expectation formation in Proposition 2 represents a form of bounded rationality.

In our VAR representation in Proposition 2, equation (1) continues to hold, and the shadow rate is unobserved and censored in the ELB regime. By allowing for a kink in the dynamics, Proposition 2 shows that a censored and kinked VAR model provides a suitable empirical specification for testing the irrelevance hypothesis.

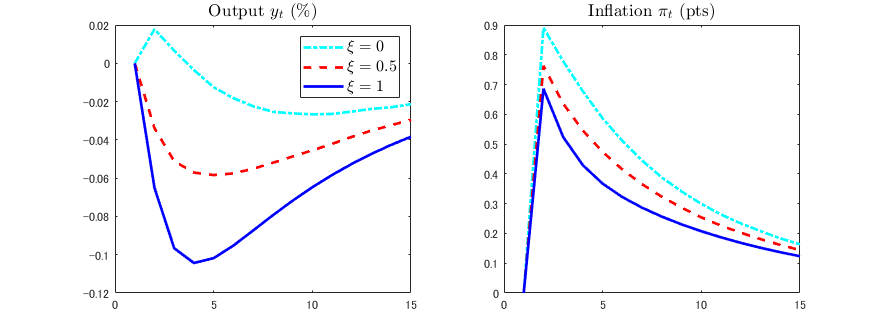

2.3 Simulations

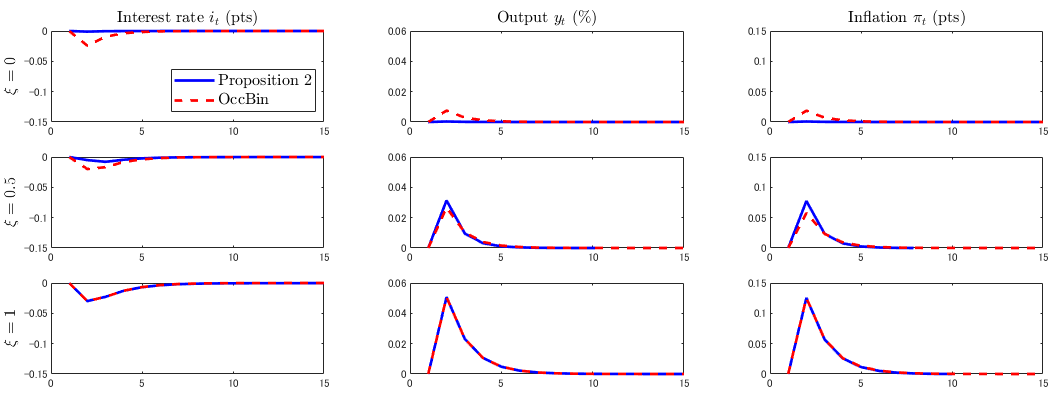

Before developing our empirical framework in the next section, we illustrate the effects of UMP and study impulse responses to a monetary policy shock in the ELB regime by solving the model under Proposition 2.888While our analysis focuses on monetary policy, Appendix A.6 reports the responses of output and inflation to demand and supply shocks under the ELB to illustrate the role of the effectiveness of UMP for these shocks. The analysis aims at illustrating the effects of UMP and it is not designed to draw quantitative implications. Appendix A.3 reports the parameterization of the model.

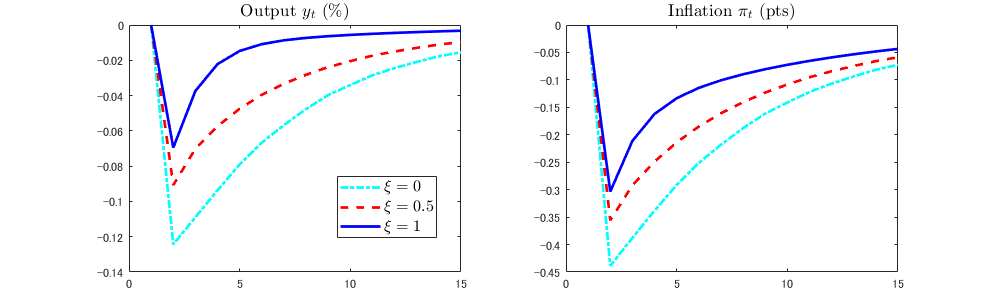

No UMP

The dash-dotted line in Figure 1 shows simulated paths for the theoretical model under Proposition 2 in the case of no UMP (). The economy starts from the steady state and large negative demand shocks hit in periods and . The consecutive negative demand shocks bring the economy to the ELB and generate a severe recession by decreasing output and inflation sharply. At the ELB (dash-dotted line), the interest rate cannot be lowered in response to the fall in inflation. This raises the real interest rate, decreases consumption and output, and puts further downward pressure on inflation through the Phillips curve (16). This negative feedback loop magnifies the falls in output and inflation compared to the hypothetical economy without the ELB (the star-marked line).

UMP

UMP can offset the negative impact of the ELB. When UMP is partially effective (; the dashed line), the magnitude of the falls in output and inflation are mitigated relative to the case without UMP (; the dash-dotted line). When UMP is fully effective (; the solid line), although the interest rate remains at the ELB, output and inflation follow the same paths as in the case of no ELB (the star-marked line), as shown in Figure 1. In response to a decrease in the shadow rate , the central bank increases the purchase of long-term government bonds and, by doing so, it lowers the long-term government bond yield by compressing its premium, which boosts consumption and output. When , UMP perfectly offsets the contractionary effect of the ELB. The interest rate becomes irrelevant to the dynamics of the economy, which evolves as if there were no ELB.

Impulse responses to a monetary policy shock

Figure 2 plots impulse responses to a 0.25 percentage points cut in the shadow rate under the ELB starting from period for the theoretical model solved under Proposition 2 (the solid line) and the model solved by the OccBin algorithm (the dashed line), developed by Guerrieri and Iacoviello (2015), which has been a popular approach to solving DSGE models at the ELB (see Atkinson, Richter and Throckmorton, 2020).999The impulse responses are computed by using the same method employed in reporting our empirical results. For the details, see Section 5.1. The OccBin solution assumes that agents in the model form expectations by treating the non-ELB regime as an absorbing state, i.e., by assuming that interest rates will remain positive once the economy exits the ELB regime. Thus, OccBin uses an alternative behavioural assumption on the formation of expectations than the one used in Proposition 2.

Overall the responses of the interest rate, output, and inflation are similar between the model solution under Proposition 2 and the OccBin solution, as shown in Figure 2. The responses of the interest rate are muted because the economy starts from the ELB triggered by a severe demand shock in period . Without the ELB, the interest rate (left panels) would fall by about 0.15 percentage points (pts), reported in the figure as the lowest value on the y-axis.101010The responses of the interest rate are slightly negative because they are calculated relative to the expected interest rate conditional on no monetary policy shock in the initial period, which is slightly positive due to the realizations of shocks that bring the economy above the ELB. In the case of no UMP (; top panels), the responses of output (central panels) and inflation (right panels) are muted for both the model solution under Proposition 2 and the OccBin solution. Because the economy is at the ELB, the monetary policy shock in period does not have significant effects on the economy without UMP. In the case of partial UMP (; middle panels), QE is activated in response to a decrease in the shadow rate triggered by the monetary policy shock, and output and inflation increase. In the case of fully effective UMP (; bottom panels), the ‘irrelevance hypothesis’ holds and the responses of output and inflation coincide with those under the hypothetical economy with no ELB under both solution methods.

3 Empirical model

Our theoretical model in Section 2 highlights three important features to study the irrelevance hypothesis: i) the censoring of the shadow rate at the ELB, ii) a potential kink of the dynamics of the economy at the ELB, and iii) a parameter that encapsulates the effectiveness of UMP. We embed these features in our empirical model designed to test the irrelevance hypothesis using the flexible VAR approach of the literature on monetary policy. In this section, we present our empirical model, derive the tests of the irrelevance of the ELB and no attenuation hypotheses, and describe our approach to the identification of the effects of conventional and unconventional monetary policy.

3.1 Censored and kinked SVAR

The econometric model that we use is the censored and kinked SVAR (CKSVAR) developed by Mavroeidis (2021). Its structural form is given by:

| (17a) | ||||

| (17b) | ||||

| (17c) | ||||

where is the short-term interest rate that is subject to the observable lower bound of , is the shadow rate, is a vector of unconstrained endogenous variables such as inflation and output, comprises exogenous and predetermined variables, including lags of and , consists of lags of and are i.i.d. structural shocks with identity covariance matrix.

Equation (17a) represents the ELB constraint, and it corresponds to equation (1) in the theoretical model, except for the lower bound that is allowed to vary over time in equation (17a). Thus, the shadow rate is censored and unobservable under the ELB, as in the theoretical model.

Equation (17b) represents the short-term interest rate rule that nests the FG rule of Reifschneider and Williams (2000), and it corresponds to equations (2) and (3) in the theoretical model. The parameter has the same interpretation as in the theoretical model.

Equation (17c) describes the dynamics of variables of interest such as inflation and output and the relationship between these variables and interest rates. The parameter is the equivalent of in the theoretical model and characterizes the effectiveness of UMP relative to conventional policy on impact. Specifically, from equation (17c) we see that above the ELB (i.e., when ), the contemporaneous effect of a change in the short-term interest rate by one unit on is but the corresponding effect at the ELB, driven by a change in the shadow rate is When the two effects are equal, while corresponds to the case in which UMP has no contemporaneous effect on

Similar to the theoretical model, the parameter partially characterizes the impulse responses to a monetary policy shock at the ELB, since the response of the interest rate also depends on the degree of FG, and thus the joint effect of and determines the response of endogenous variables to UMP. To see this in the context of the SVAR model, consider the impulse response to the monetary policy shock of ignoring nonlinearities.111111We will discuss the specification of the impulse response functions in Section 5, see equation (26). The effect on is above the ELB, and at the ELB, where:

| (18) |

So, it is, in fact, , not , that measures the effectiveness of an UMP shock – a shock to the shadow rate below the ELB, see Mavroeidis (2021) for further discussion. The parameter is the equivalent in Lemma 1 of the theoretical model. In the proof of Proposition 2 (see Appendix A.5), we show that the UMP parameter in the theoretical model under Proposition 2 can be mapped in the system of equations (17a)-(17c), and the in the theoretical model coincides with the corresponding parameter in the empirical model.

Our discussion about the parameter concerned the relative effectiveness of UMP on impact. The dynamic effects of UMP on are governed by the coefficients on the lags of the shadow rate in equation (17c). For example, the case of completely ineffective UMP on at all horizons can be represented by the joint restrictions and . A more restrictive case is that UMP is also ineffective on the short-term interest rate , in addition to having no effect on , which can be implemented by , , and This implies that the shadow rate has no contemporaneous and cumulative impact on the endogenous variables and completely drops out of the right-hand side of equations (17a)-(17c). We refer to this case as the kinked SVAR (KSVAR), using the same terminology in Mavroeidis (2021).

3.2 Reduced-form solution of the SVAR and identification

To implement our empirical tests and gain intuition on the identification and estimation of the CKSVAR model, we derive the reduced-form solution for and using equations (17a)-(17c). Mavroeidis (2021) develops the methodology for the identification and estimation of the CKSVAR, showing that the model is generally under-identified, but the parameter , defined in equation (18), and the impulse responses to the monetary policy shock , are partially identified in general. The reduced-form solution for and is:

| (19a) | ||||

| (19b) | ||||

where is the indicator of the ELB regime, , consists of the lags of , the matrices , , and are reduced-form coefficients, are reduced-form errors, and

The reduced-form equations in (19) represent a censored and kinked VAR. Equation (19a) entails the censoring of the shadow rate, represented by the operator. Equation (19b) allows for a kink at the ELB and the coefficients and variance can change across regimes. Therefore, our empirical model nests the theoretical model under Proposition 2, while imposing minimal structure and allowing for flexible coefficients in the VAR.

The coefficient of the kink in equation (19b) is identified, together with the remaining reduced-form parameters. In other words, we can infer from the data whether the slope coefficients and the variance of change across regimes by testing whether However, the parameter does not have a structural interpretation and relates to the underlying structural parameters through the following equations:

| (20) | ||||

| (21) |

As shown in Mavroeidis (2021), the structural parameters and are partially identified, in the sense that there is a set of different combinations for values of the structural parameters that satisfy equations (20) and (21) and generate any given value of the reduced-form parameters and . Therefore, the impulse responses to a monetary policy shock are set-identified. In our empirical analysis below, we will sharpen the identified set by using sign restrictions on the impulse responses.

3.3 Hypothesis tests of the irrelevance of the ELB

We now develop our tests for the irrelevance hypothesis (IH) of the ELB from the reduced-form solution of the SVAR. A central implication of our theoretical framework was that the dynamics of the economy are independent from whether policy rates are at the ELB or not. We use this fundamental implication to formulate two testable hypotheses.

Irrelevance hypothesis 1 (IH1)

Our first approach to test the IH is motivated by Swanson (2018) and Debortoli, Galí and Gambetti (2019), who argue that monetary policy remains similarly effective across ELB and non-ELB regimes and that long-term interest rates are a plausible indicator of the stance of monetary policy. Debortoli, Galí and Gambetti (2019) use SVARs that include long-term, rather than short-term interest rates as indicators of monetary policy. They use such VARs to identify the impulse responses of the macroeconomic variables to monetary policy as well as the response of policy to economic conditions, and find that those responses are similar across ELB and non-ELB regimes in the U.S. The implicit and testable assumption that underlies their analysis is that the short-term interest rate can be excluded from the dynamics of all the other variables in the system, and the dynamics of the system do not change when the economy enters the ELB regime. In other words, under the IH, the dynamics of the economy can be represented by VARs with the long rate but without the short rate, which we formally showed in Proposition 1(ii).

The hypothesis can be tested as an exclusion restriction in an SVAR that includes both the short and long rates. Since the short rate is subject to the ELB constraint, the relevant framework is the CKSVAR (that allows for the shadow rate to affect the economy in the ELB regime) and the special case of KSVAR (that precludes the shadow rate to affect the economy in the ELB regime) introduced in Section 3.1. Specifically, looking at the reduced-form specification in equation (19b), the IH can be formulated as:

| (22) |

In words, means that lags of the short rate () and the shadow rate () can be excluded from the equation (19b) that governs the unconstrained variables () in the VAR, and means that the slope coefficients and the variance of the errors of those equations (for ) remain the same when the economy moves across regimes.

Irrelevance hypothesis 2 (IH2)

The second test of the IH is motivated by Proposition 1(i), which shows that when UMP is fully effective, the dynamics of the economy can be adequately represented by a VAR that entails the pure censoring of and no kink. Such a VAR is a special case of the reduced-form VAR (19) that arises when the following testable restrictions are imposed:

| (23) |

In words, and means that the lags of the short rate () can be excluded from equation (19), and means that the slope coefficients and the variance of the errors of those equations (for ) remain the same when the economy moves across regimes. We call the structural form of the VAR under IH2 as a purely censored SVAR (CSVAR) as the shadow rate is censored but affects the dynamics equally across regimes.

It is worth noting that both IH1 and IH2 do not rely on a specific model of UMP, such as the one in Section 2, as long as the long rate or the shadow rate represents the monetary policy stance, because any VAR that includes short rates must admit a CSVAR representation with constant parameters across regimes when the irrelevance hypothesis holds. Otherwise, the ELB would result in observable changes across regimes, violating the hypothesis that the ELB is empirically irrelevant.

3.4 Attenuation effect

Swanson and Williams (2014) and Gilchrist, López-Salido and Zakrajšek (2015) argue that an implication of a binding ELB constraint is that the effect of shocks on long-term interest rates may be attenuated when the policy rate lies at the ELB. They investigate this phenomenon empirically using time-varying-parameter regressions of different maturity yields on news shocks at daily frequency.

We shall use the CKSVAR model to characterize analytically and obtain formal tests of the aforementioned attenuation effect. Specifically, we will show analytically how the model-implied impulse response of the long yields to a monetary policy shock on impact is attenuated during ELB-regimes relative to non-ELB regimes, and that this attenuation effect is state-dependent and thus time-varying.

Let denote the impact response of variable to an infinitesimal monetary policy shock derived from the CKSVAR model in Equation (17). Also, let denote the same response under the assumption that there is no attenuation. Then, it can be shown that (see Appendix B):

| (24) |

where and are the th elements of the coefficient vectors that appear in structural and reduced-form equations, (17) and (19), respectively, is the predicted value of the shadow rate in period , is the standard deviation of when the monetary policy shock is zero, and is the Standard Normal cumulative distribution function. The factor attenuates the impact of the monetary policy shock on as the economy approaches the ELB, provided . This attenuation is notably time-varying and depends on the distance of the shadow rate from the ELB . When the shadow rate is far above the ELB, is approximately zero and there is no attenuation. The attenuation increases in , provided .

Equation (24) allows us to derive a formal test of the hypothesis that there is no attenuation based only on the reduced-form VAR specification (19). In other words, this test does not rely on any additional assumptions (such as sign restrictions) that one might use to identify the structural parameters and the structural impulse responses. Specifically, suppose that the vector of unconstrained variables in the empirical model (19) includes a long-term yield of a particular maturity, , and let denote the coefficient of the kink in the reduced-form equation associated with in equation (19b). Then, the hypothesis that there is no attenuation of the response of to monetary policy shocks arising from the ELB is given by:

| (25) |

In the theoretical model studied in Section 2, no attenuation effect is equivalent to the irrelevance of the ELB as implied by Proposition 1(ii). But the empirical model is less restrictive than the theoretical model, and HNA is clearly a weaker hypothesis than the irrelevance hypotheses IH1 (22) and IH2 (23) defined above. Therefore, in our empirical framework, failing to reject HNA does not necessarily imply that the ELB is empirically irrelevant.

We will test HNA using long yields at various maturities in Section 4.3.

4 Empirical results

This section discusses the data for the U.S. and Japan, and tests the hypothesis that the ELB has been empirically irrelevant in each country using the hypothesis testing approach that is underpinned by Proposition 1 and established in Section 3.3. In addition, it tests the hypothesis of no attenuation effect in the response of long-term interest rates at the ELB, as formulated in Section 3.4, and it examines whether the short-term interest rate, including the shadow rate at the ELB, is a sufficient indicator of monetary policy including UMP, as implied by Proposition 2.

4.1 Data

Our empirical analysis focuses on the U.S. and Japan. We choose data series for the baseline specification of the SVAR model to maintain the closest specification possible to related studies and thereby include representative series for inflation, output, and measures for short- and long-term yields.

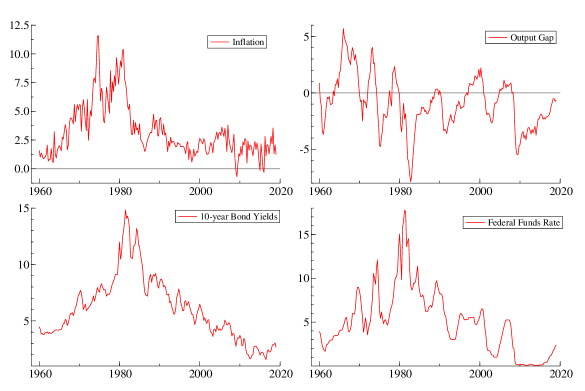

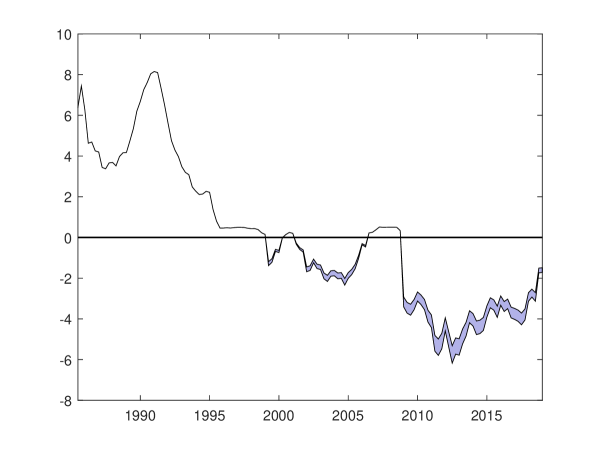

For the U.S., we use quarterly data for inflation based on the GDP deflator (U.S. Bureau of Economic Analysis, 2019a), a measure of the output gap (U.S. Bureau of Economic Analysis, 2019b; U.S. Congressional Budget Office, 2019), the short-term interest rate from the Federal Funds Rate (Board of Governors of the Federal Reserve System (2019b)Board of Governors of the Federal Reserve System (US), US), and the 10-year government bond yield from the 10-year Treasury constant maturity rate (Board of Governors of the Federal Reserve System (2019g)Board of Governors of the Federal Reserve System (US), US). Figure 3 plots these series. We also consider the different measures of monetary aggregates listed in Appendix C. The data are from the FRED database at the Federal Reserve Bank of St. Louis (Board of Governors of the Federal Reserve System (2019m)Board of Governors of the Federal Reserve System (US), US) and The Center for Financial Stability (2019) databases. The estimation sample for the baseline specification is from 1960q1 to 2019q1.121212See Appendix C for further details about the data. Alternative specifications with money are estimated over different time periods due to constraints on data availability. We set the value of the effective lower bound on the Federal Funds Rate equal to 0.2, such that the short-term interest rate is at the ELB regime for 11 percent of the time, which is consistent with Bernanke and Reinhart (2004) who suggest that the effective lower bound on nominal interest rates may be above zero for institutional reasons.

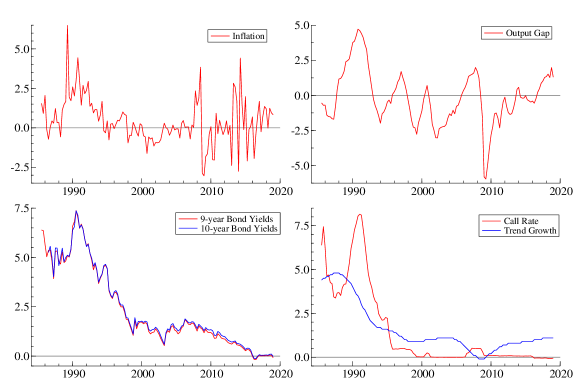

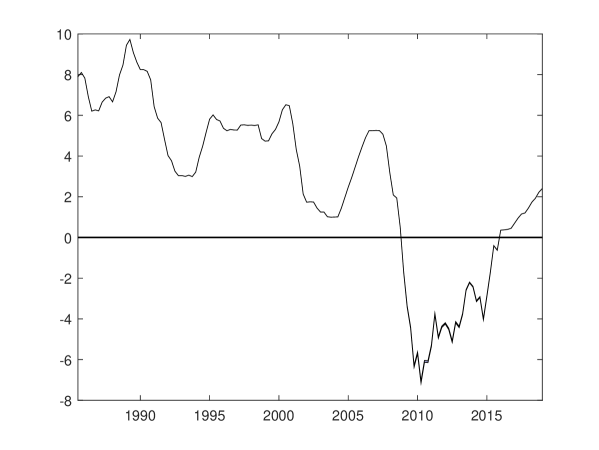

For Japan, we use quarterly data for core CPI inflation, a measure of the output gap provided by the Bank of Japan, and the call rate. In addition, we use two alternative measures for long yields: the 9-year and the 10-year government bond yields, which are available for different sample periods. The data sources are the Bank of Japan for the output gap (Bank of Japan, 2019b) and the call rate Bank of Japan (2019a), the Ministry of Finance for the 9-year and the 10-year government bond yields Ministry of Finance of Japan (2019), and Statistics Bureau of Japan for core CPI inflation (Statistics Bureau of Japan, 2019). The available sample is from 1985q3 to 2019q1 if we include the 9-year government bond yield in the VAR, which is our baseline case, and from 1987q4 to 2019q1 if we use the 10-year yield. Following Hayashi and Koeda (2019), we set the ELB to track the interest on reserves (IOR) (Bank of Japan, 2008, 2016a).131313Specifically, ELB = IOR + 7bp, which is slightly higher than Hayashi and Koeda (2019) who use IOR+5bp, in order to treat 2016q1 as being at the ELB. For the sample period 1985q3-2019q1, the call rate is at the ELB for 49 percent of the observations. Following Hayashi and Koeda (2019), we use a trend growth series (Cabinet Office of Japan, 2019) to account for the declining equilibrium real interest rate in Japan during the 1990s.141414Specifically, we use the annual average growth rate of potential GDP as an additional control in our model. See Hayashi and Koeda (2019, pp. 1081–1083) for an extended discussion of this issue and its implications. Figure 4 plots these series.

4.2 Testing the irrelevance hypothesis of the ELB

We now test the irrelevance hypothesis of the ELB for the U.S. and Japan using the two null hypotheses, IH1 and IH2, formalized by (22) and (23), respectively.

| Panel A: KSVAR | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| United States | Japan | |||||||||||

| p | loglik | pv-p | AIC | LR | df | -val | loglik | pv-p | AIC | LR | df | -val |

| 5 | -213.4 | - | 2.62 | 53.12 | 18 | 0.000 | 248.1 | - | -2.18 | 27.82 | 18 | 0.065 |

| 4 | -221.5 | 0.446 | 2.55 | 49.57 | 15 | 0.000 | 239.9 | 0.425 | -2.30 | 28.10 | 15 | 0.021 |

| 3 | -234.4 | 0.112 | 2.53 | 42.13 | 12 | 0.000 | 232.2 | 0.471 | -2.42 | 28.58 | 12 | 0.004 |

| 2 | -266.0 | 0.000 | 2.66 | 41.93 | 9 | 0.000 | 223.8 | 0.445 | -2.53 | 25.71 | 9 | 0.002 |

| 1 | -296.7 | 0.000 | 2.78 | 32.87 | 6 | 0.000 | 184.8 | 0.000 | -2.19 | 32.32 | 6 | 0.000 |

| Panel B: CKSVAR | ||||||||||||

| p | loglik | pv-p | AIC | LR | df | -val | loglik | pv-p | AIC | LR | df | -val |

| 5 | -191.3 | - | 2.60 | 82.43 | 33 | 0.000 | 284.7 | - | -2.42 | 90.39 | 33 | 0.000 |

| 4 | -202.7 | 0.290 | 2.53 | 72.15 | 27 | 0.000 | 277.1 | 0.766 | -2.61 | 91.55 | 27 | 0.000 |

| 3 | -223.0 | 0.011 | 2.53 | 51.93 | 21 | 0.000 | 258.1 | 0.081 | -2.62 | 73.52 | 21 | 0.000 |

| 2 | -256.3 | 0.000 | 2.64 | 49.44 | 15 | 0.000 | 242.1 | 0.018 | -2.68 | 56.16 | 15 | 0.000 |

| 1 | -290.3 | 0.000 | 2.76 | 37.12 | 9 | 0.000 | 204.8 | 0.000 | -2.43 | 63.03 | 9 | 0.000 |

Testing IH1

The basic idea of IH1 is that a long-term interest rate is a sufficient indicator of monetary policy stance, and thereby a short-term interest rate becomes redundant and can be excluded from the VAR under the irrelevance of the ELB. The results of the likelihood ratio test of the null hypothesis IH1 in (22) are reported in Table 1. Panel A reports results based on a KSVAR model, in which lags of the shadow rate do not appear on the right-hand-side of equation (19). In this case, we test IH1 against an alternative hypothesis that imposes , and this test only has power against the violation of . We do so because the KSVAR model is simpler to estimate, and a rejection of would suffice to reject IH1. Panel B reports the results using the general CKSVAR. The table reports results for specifications with different lag lengths of the VAR(), where . Column pv-p reports the -value of a test for selecting the number of lags in the model,which is an alternative approach to the Akaike Information Criterion (AIC), also reported in the Table. Both measures consistently select four lags for the U.S. and two lags for Japan. Column p-val reports the asymptotic -value of our test of (22).

| Panel A: KSVAR | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| United States | Japan | |||||||||

| YTM | sample | p | LR | df | -val | sample | p | LR | df | -val |

| 7 | 1970q4–2019q1 | 3 | 38.69 | 12 | 0.000 | 1985q3–2019q1 | 2 | 23.20 | 9 | 0.006 |

| 5 | 1963q2–2019q1 | 3 | 41.93 | 12 | 0.000 | 1985q3–2019q1 | 2 | 25.15 | 9 | 0.003 |

| 3 | 1963q2–2019q1 | 3 | 46.32 | 12 | 0.000 | 1985q3–2019q1 | 2 | 30.97 | 9 | 0.000 |

| 2 | 1977q4–2019q1 | 4 | 38.82 | 15 | 0.001 | 1985q3–2019q1 | 2 | 33.05 | 9 | 0.000 |

| 1 | 1963q2–2019q1 | 3 | 59.65 | 12 | 0.000 | 1985q3–2019q1 | 2 | 49.90 | 9 | 0.000 |

| Panel B: CKSVAR | ||||||||||

| YTM | sample | p | LR | df | -val | sample | p | LR | df | -val |

| 7 | 1970q4–2019q1 | 3 | 51.03 | 21 | 0.000 | 1985q3–2019q1 | 2 | 58.32 | 15 | 0.000 |

| 5 | 1963q2–2019q1 | 3 | 56.33 | 21 | 0.000 | 1985q3–2019q1 | 2 | 58.50 | 15 | 0.000 |

| 3 | 1963q2–2019q1 | 3 | 58.54 | 21 | 0.000 | 1985q3–2019q1 | 2 | 62.04 | 15 | 0.000 |

| 2 | 1977q4–2019q1 | 4 | 66.84 | 27 | 0.000 | 1985q3–2019q1 | 2 | 63.77 | 15 | 0.000 |

| 1 | 1963q2–2019q1 | 3 | 73.06 | 21 | 0.000 | 1985q3–2019q1 | 2 | 72.41 | 15 | 0.000 |

Table 1 shows that the data strongly reject the exclusion restrictions implied by IH1 for both countries and in both the KSVAR and CKSVAR specifications. Hence, the short-term interest rate cannot be excluded from the VAR, and thus it makes the dynamics of the system differ between the non-ELB and ELB regimes even if the long-term interest rate – 10-year yields for the U.S. and 9-year yields for Japan – is added to the VAR. The result continues to hold for Japan with 10-year yields, which are available from 1987q3, and is reported in Table 14 in Appendix D.

The result of the rejection of IH1 continues to hold even if we use yields with shorter maturities. Table 2 shows the results for the null hypothesis IH1 when we include yields with maturities in the range from 1 to 7 years in the VAR for the U.S. (Board of Governors of the Federal Reserve System (2019o)Board of Governors of the Federal Reserve System (US), US) and Japan (Ministry of Finance of Japan, 2019). The entries show results for the VAR specification with the preferred number of lags according to the AIC. The results show that the exclusion restrictions from IH1 are strongly and consistently rejected across the whole range of maturities for both countries. Our results imply that a government bond yield with maturity within the 1- to 10-year range cannot replace the shadow rate as the indicator of monetary policy stance, and the dynamics of the economy differ between the non-ELB and ELB regimes.

Testing IH2

The idea of the hypothesis IH2 in (23) is that once the shadow rate is included in the VAR, the short-term interest rate can be excluded from the VAR under the irrelevance hypothesis. We test IH2 with the three core observables, inflation and output gap in , and the short-term interest rate, and we also include the long-term interest rate in for robustness. Under IH2 the shadow rate is censored in the ELB regime but affects equally in both regimes according to the reduced form equation (19). We test IH2 using a likelihood ratio test as we tested IH1.

Table 3 reports the results of the likelihood ratio test of IH2 for the U.S. and Japan. The results for our baseline specifications are reported in the row starting with ‘10 or 9’ in the first column. We include lags for the U.S. and lags for Japan, according to the AIC. The results show that the IH2 is rejected for both economies at the 5 percent level of significance. The result continues to hold for Japan with 10-year yields and is reported in Table 15 in Appendix D. Table 3 also shows that the result of the rejection of IH2 continues to hold even if we include an alternative yield within the range of 1 to 7 years in .

| United States | Japan | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| YTM | sample | p | LR | df | -val | sample | p | LR | df | -val |

| 10 or 9 | 1960q1–2019q1 | 4 | 34.42 | 19 | 0.016 | 1985q3-2019q1 | 2 | 51.02 | 11 | 0.000 |

| 7 | 1970q4–2019q1 | 3 | 26.80 | 15 | 0.030 | 1985q3–2019q1 | 2 | 50.86 | 11 | 0.000 |

| 5 | 1963q2–2019q1 | 3 | 29.26 | 15 | 0.015 | 1985q3–2019q1 | 2 | 49.27 | 11 | 0.000 |

| 3 | 1963q2–2019q1 | 3 | 31.83 | 15 | 0.007 | 1985q3–2019q1 | 2 | 53.09 | 11 | 0.000 |

| 2 | 1977q4–2019q1 | 4 | 45.49 | 19 | 0.001 | 1985q3–2019q1 | 2 | 56.03 | 11 | 0.000 |

| 1 | 1963q2–2019q1 | 3 | 51.04 | 15 | 0.000 | 1985q3–2019q1 | 2 | 70.62 | 11 | 0.000 |

Robustness checks

It is possible that the short rate is necessary to explain long rates even if the short rate is not necessary to characterize inflation and output dynamics. This could occur if real rates trend over time, so having both in the VAR picks up low-frequency movements. We address this concern by testing IH and for the inflation and output equations only while allowing the short and shadow rates to affect the long rate. We find that this weaker version of IH1 is also robustly rejected (Table 7 in Appendix D).

Next we check the robustness of our results to possible omission of alternative channels of unconventional monetary policy, by adding money growth to the variables of the VAR that we use to test the null hypothesis IH1 in (22). Using several different monetary aggregates for the U.S., we consistently reach the same conclusion: the IH1 is firmly rejected (Table 8 in Appendix D).

We also check the robustness of the U.S. results to the well-documented fall in macroeconomic volatility in the mid-1980s, known as the Great Moderation, as well as a possible change in monetary policy regime occurring at that time by performing the same tests over the subsample 1984q1–2019q1 (see Tables 9 and 10 in Appendix D). In addition, Caldara and Herbst (2019) show that accounting for the endogenous reaction of financial conditions is critical to avoiding an attenuation bias in the responses of variables to monetary policy shocks. Gilchrist and Zakrajsek (2012) use credit spreads to internalize the central contribution of financial frictions during ELB episodes. Thus, we check the robustness of our results by including credit spreads (Favara et al., 2019; Federal Reserve Bank of St. Louis, 2019) in the VAR (see Tables 11-13 in Appendix D). Our conclusion remains the same: the IH1 and IH2 are firmly rejected.

Finally, we check the power of our irrelevance tests IH1 and IH2 by generating simulated series from our theoretical model for values of in the range . Since the theoretical model is solved under Proposition 2, in the theoretical model coincides with in the empirical model and the simulated series are equivalent between the two models. We find that the rejection rate of the tests declines as approaches the value of one (i.e., the irrelevance hypothesis holds true), showing that our tests are powerful. The result is reported in Tables 16 and 17 in Appendix D.

4.3 Testing the attenuation effect

We use our CKSVAR model to test the null hypothesis of no attenuation in the response of long-term interest rates to monetary policy shocks at the ELB, formalised as HNA in (25) in Section 3.4. Table 4 reports the results of the test for the VAR model that includes long rates of different maturities ranging from 1 year to 10 years. The null is firmly and consistently rejected across different yields to maturity for both countries. The result implies that long rates of different maturities have responded differently to monetary policy shocks between the ELB and non-ELB regimes in both the U.S. and Japan.

Our approach to testing no attenuation effect differs from the one employed by Swanson and Williams (2014) who find that responses of 1- and 2-year U.S. bond yields to various macroeconomic news shocks, identified using high frequency data over the period 1990–2012, were not attenuated throughout 2008 to 2010 but became attenuated in late 2011. We instead focus on responses to a monetary policy shock – a shock to the shadow rate using quarterly data over a longer sample. We discuss the implications of different sample periods at the end of Appendix D.

| United States | Japan | |||||

|---|---|---|---|---|---|---|

| YTM | p | LR | -val | p | LR | -val |

| 10 or 9 | 4 | 15.84 | 0.000 | 2 | 16.63 | 0.000 |

| 7 | 3 | 10.33 | 0.001 | 2 | 14.95 | 0.000 |

| 5 | 3 | 13.19 | 0.000 | 2 | 15.13 | 0.000 |

| 3 | 3 | 17.15 | 0.000 | 2 | 27.70 | 0.000 |

| 2 | 4 | 16.81 | 0.000 | 2 | 33.17 | 0.000 |

| 1 | 3 | 35.90 | 0.000 | 2 | 46.06 | 0.000 |

4.4 Testing the (ir)relevance of long rates

Our statistical tests rejected the irrelevance hypothesis of the ELB and the possibility of excluding the short rate by controlling for the long rate. We now assess whether movements in the short rate, including the shadow rate during ELB regimes, are sufficient to encapsulate the effects of both conventional and unconventional monetary policies for inflation and output by testing the exclusion restriction on the long rate. Proposition 2 implies that the exclusion restriction on the long rate holds in the theoretical model.

| United States | Japan | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| YTM | sample | p | LR | df | -val | sample | p | LR | df | -val |

| 10 or 9 | 1960q1–2019q1 | 3 | 2.43 | 6 | 0.876 | 1985q3–2019q1 | 2 | 6.32 | 4 | 0.177 |

| 7 | 1970q4–2019q1 | 3 | 5.15 | 6 | 0.524 | 1985q3–2019q1 | 2 | 10.38 | 4 | 0.035 |

| 5 | 1963q2–2019q1 | 3 | 4.99 | 6 | 0.545 | 1985q3–2019q1 | 2 | 7.00 | 4 | 0.136 |

| 3 | 1963q2–2019q1 | 3 | 7.05 | 6 | 0.316 | 1985q3–2019q1 | 2 | 4.99 | 4 | 0.288 |

| 2 | 1977q4–2019q1 | 4 | 11.53 | 8 | 0.174 | 1985q3–2019q1 | 2 | 3.40 | 4 | 0.493 |

| 1 | 1963q2–2019q1 | 3 | 11.70 | 6 | 0.069 | 1985q3-2019q1 | 2 | 5.19 | 4 | 0.268 |

We perform this test using the CKSVAR model that includes inflation, output gap, the long rate, and the short rate. The null hypothesis is that lags of the long rate can be excluded from the equations for inflation and output gap. In performing this test, we impose the assumption that the short rate does not react to the long rate by imposing zero restrictions on the lags of long rates in the interest rate equation (19a). This is consistent with the standard Taylor rule (3) in the theoretical model, and our modelling of QE in equation (10). Table 5 reports the results using long rates of various maturities. It shows that the null hypothesis cannot be rejected and that the long rate can be excluded from the model at the 5 percent level of significance in both countries and at most maturities. The result implies that the short rate and the shadow rate may be sufficient indicators of monetary policy during the non-ELB and ELB regimes in both countries.

5 The effectiveness of UMP

Our testing results established that the dynamics of the economy are different across the ELB and non-ELB regimes for both the U.S. and Japan, leading us to conclude that the ELB has been empirically relevant. But the results are silent on the magnitude of the differences in the effects of monetary policy between the two regimes. Here we address this issue by estimating the (partially identified) impulse responses to a monetary policy shock from the CKSVAR models over time to gauge the effectiveness of UMP relative to conventional monetary policy. In doing so, we use inflation, output gap, the short rate, and the shadow rate for the CKSVAR models, as this specification is broadly in line with the test results obtained in Section 4.

5.1 State-dependent impulse responses

Since the empirical model is nonlinear, the impulse response functions (IRFs) are state-dependent. We will follow the approach in Koop, Pesaran and Potter (1996), already used in Section 2.3, according to which the IRF to a monetary policy shock of magnitude is given by the difference in the expected path of the endogenous variables when the policy shock takes the value , versus the path when the shock is zero, conditional on the state of the economy prior to the shock. This approach is the most commonly used in the literature, see, e.g., Hayashi and Koeda (2019). In our model, there is an additional complication that lagged shadow rates are unobserved, so we evaluate the IRFs at the smoothed estimates of those latent variables. In the same notation of the empirical model in Section 3, let denote the vector of endogenous variables, and denote a state vector whose -th component is given by for , where is the order of the VAR. Then, our IRFs starting from period up to the horizon are given by:

| (26) |

where consists of the lagged values of for , and is the smoothed estimate of the state vector when it is unobserved.

5.2 The impact effects of UMP

As explained in Section 3, the IRFs are generally set-identified unless we assume there is no contemporaneous effect of UMP on , which corresponds to setting in the CKSVAR model. We will not be imposing such an assumption in our analysis. We proceed by first obtaining the identified set for , and by solving equations (20) and (21) at the estimated values of and as explained in Section 3 (see the discussion following equations (20) and (21)), and then we simulate the paths of the empirical model at each of the values of the structural parameters in the identified set.

The estimation results for the parameter are as follows. Recall that the parameter determines the impact effect of UMP, where the two limiting cases of and correspond to UMP being completely ineffective on impact and as effective as conventional policy in non-ELB regimes on impact, respectively. When we restrict the range of to and impose no further identifying restrictions, the identified set for is for the U.S. and for Japan.

We sharpen the identified sets by using sign restrictions. We follow Debortoli, Galí and Gambetti (2019) and impose the restrictions that a negative monetary policy shock should have a nonnegative effect on inflation and output, and a nonpositive effect on interest rates at a one-year horizon.151515Note that because IRFs are state-dependent, these sign restrictions need to be imposed for all values of the initial states. In principle, this means working out the worst cases over the support of the distribution of the variables. However, a very similar conservative estimate of the identified set can be obtained if we simply impose the sign restrictions in every period. These sign restrictions are consistent with the theoretical model studied in Section 2 (see Figure 2). With these sign restrictions, the identified set for the parameter narrows down substantially for the U.S., from to . For Japan the impact of the sign restrictions is more modest, from to .

Appendix E compares our identification based on sign restrictions against the standard Choleski identification that imposes restrictions on the impact response of the variables to the monetary policy shock. Consistent with the results in Gertler and Karadi (2015) and Kubota and Shintani (2022), we find that the Choleski identification presents several puzzling responses.

5.3 The dynamic effects of UMP

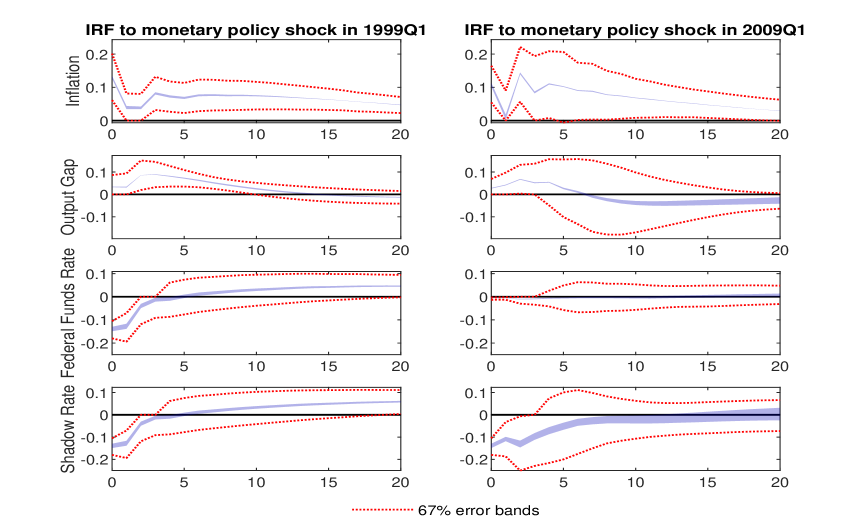

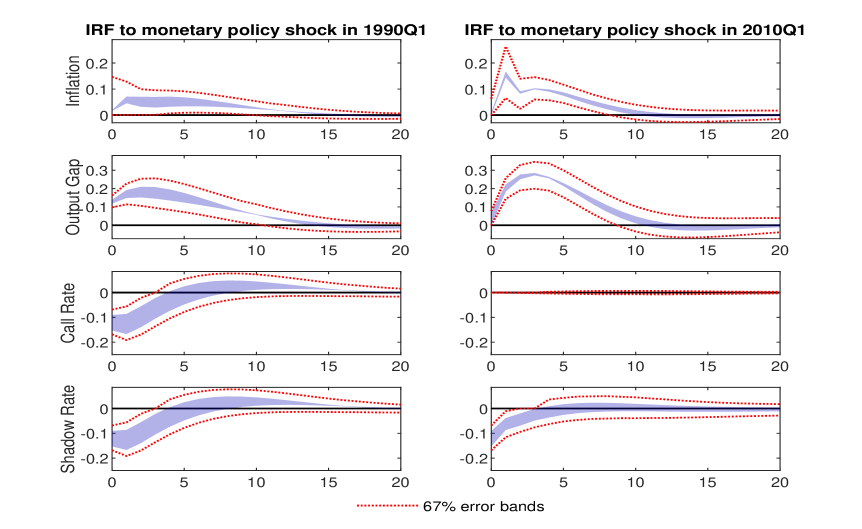

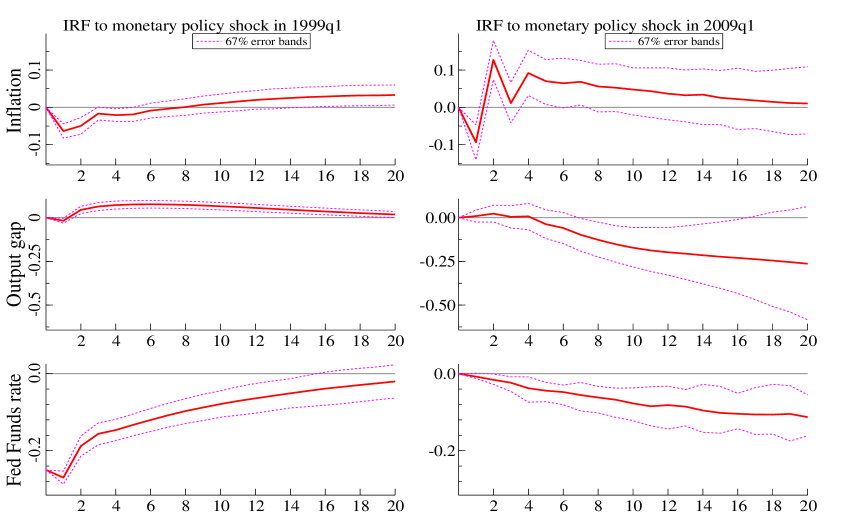

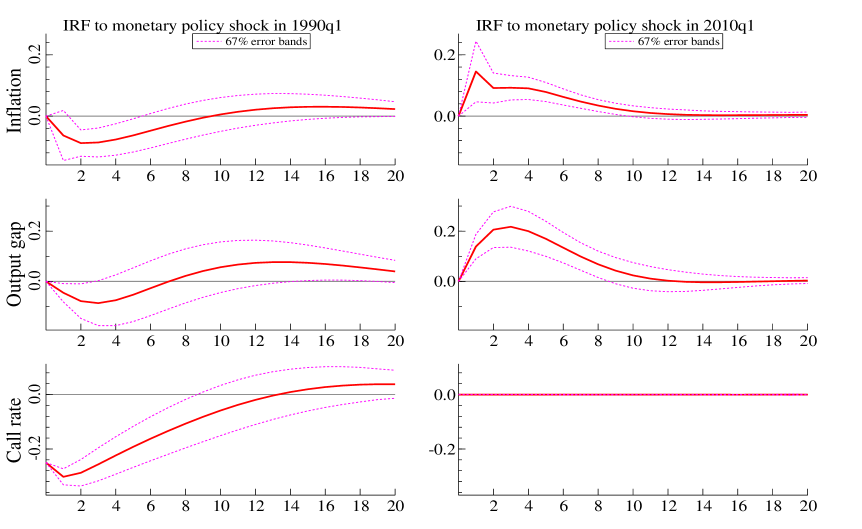

Now we study the dynamic effects of UMP by examining the IRFs for the identified sets of for the U.S. and Japan. Figures 5 and 6 report the identified IRFs of inflation, the output gap, the policy rate, and the shadow rate to a -25 basis points monetary policy shock. The figure also reports asymptotic confidence intervals obtained using the method of Imbens and Manski (2004), where we also impose the sign restrictions on the confidence bands, as in Granziera, Moon and Schorfheide (2018). The IRFs are computed at two different dates: the left panels report IRFs at dates when interest rates are well above the ELB (1999q1 for the U.S. and 1990q1 for Japan) so that monetary policy is conventional; the right panels report IRFs at dates when interest rates are at the ELB (2009q1 for the U.S. and 2010q1 for Japan) so that monetary policy is unconventional.

The policy effects differ across the two periods. For both countries, the conventional monetary policy shock – the reduction in the short-term interest rate – has a larger contemporaneous effect on all variables in the pre-ELB dates than the corresponding unconventional policy shock – the reduction in the shadow rate – during the ELB dates, and the difference is larger in Japan than in the U.S. This is because is estimated lower in Japan than in the U.S. However, in Japan the impulse responses to the unconventional policy shock appear to be stronger a few quarters out.161616The reason why the delayed effects of UMP can be stronger than conventional policy even though is because in the empirical model the coefficients on the lags of the shadow rate are completely unrestricted. This is more general than the theoretical model of Section 2 with the monetary policy rule (3), where the coefficient on the lagged shadow rate was restricted to be a constant fraction of the coefficient on the lagged policy rate above the ELB. The result of that restriction was that restricted UMP to have a uniformly weaker effect than conventional policy over all horizons. We did not need to impose this overidentifying restriction in the empirical analysis. In addition, the responses of short rates and shadow rates are identical when both rates are far above the ELB. By contrast, the shadow rates decrease whilst the responses of short rates are muted during the ELB dates. The reductions in shadow rates affect inflation and output through unconventional policy during the ELB regime.

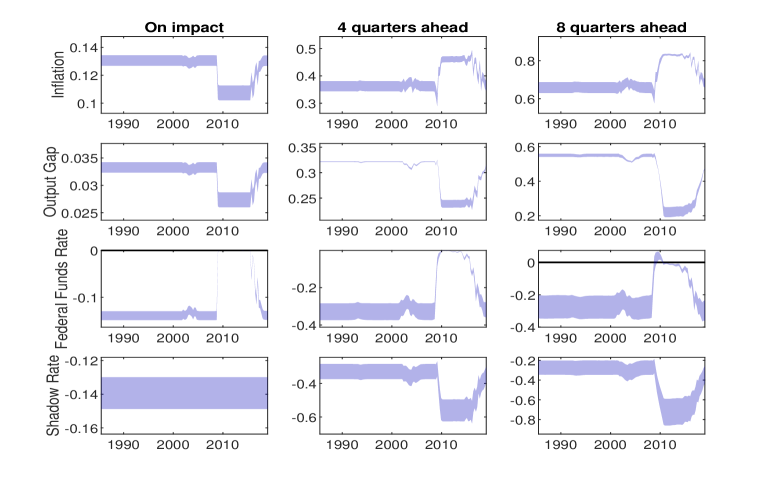

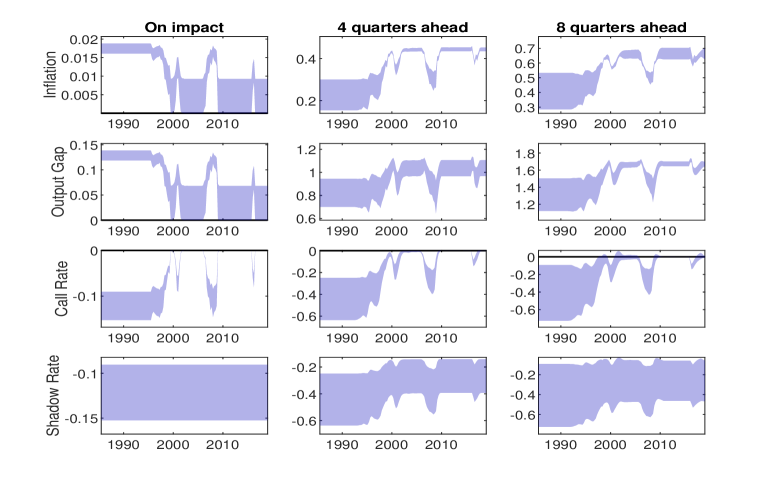

To shed further light on the differences in the responses over time, and in light of the fact that the IRFs are time-varying, we look at the evolution of the impulse responses at given horizons, 0, 4 and 8 quarters, over time. The results are reported in Figures 7 and 8 for the U.S. and Japan, respectively. In each figure, the panels on the left column report the impact effects of a -25 basis point monetary policy shock at each quarter from 1985q3 to the end of our sample. The panels in the middle column show the cumulative impulse responses after a year, while the panels on the right column give the corresponding cumulative responses after two years.

Before discussing each country, it is worth noting that the impact effect of the shock on shadow rates is invariant and non-zero over time in both countries. This is because the shadow rates are unrestricted across both ELB and non-ELB regimes. By contrast, the responses of short rates vary according to the probability of entering the ELB regime over time. When the economy is far above the ELB, the effects on short rates are identical to those on shadow rates. As the short rates approach the ELB, the probability that the ELB constraint binds increases, and the average response of short rates diminishes.

Now we discuss each country in turn. In the U.S. (Figure 7), we see a drop in the impact effect of policy during the ELB period relative to the pre-ELB period. The relative difference in the effectiveness of policy on both inflation and output on impact is over 15 percent. For the output gap, this difference remains, and increases one and two years ahead. However, the effect on inflation is the reverse: the cumulative effect of UMP on inflation is much stronger one and two years ahead. Therefore, UMP in the U.S. seems to have had a delayed but strong effect on inflation, but has been persistently less effective on output than conventional policy.