Random Planted Forest: A Directly Interpretable Tree Ensemble

Abstract

We introduce a novel interpretable tree based algorithm for prediction in a regression setting. Our motivation is to estimate the unknown regression function from a functional decomposition perspective in which the functional components correspond to lower order interaction terms. The idea is to modify the random forest algorithm by keeping certain leaves after they are split instead of deleting them. This leads to non-binary trees which we refer to as planted trees. An extension to a forest leads to our random planted forest algorithm. Additionally, the maximum number of covariates which can interact within a leaf can be bounded. If we set this interaction bound to one, the resulting estimator is a sum of one-dimensional functions. In the other extreme case, if we do not set a limit, the resulting estimator and corresponding model place no restrictions on the form of the regression function. In a simulation study we find encouraging prediction and visualisation properties of our random planted forest method. We also develop theory for an idealized version of random planted forests in cases where the interaction bound is low. We show that if it is smaller than three, the idealized version achieves asymptotically optimal convergence rates up to a logarithmic factor. Code is available on GitHub https://github.com/PlantedML/randomPlantedForest.

Keywords: Random Forest; Interpretable Machine Learning; Functional Decomposition; Backfitting.

1 Introduction

In many ways machine learning has been very disruptive in the last two decades. The class of neural networks has shown unprecedented and previously unthinkable predictive accuracy in fields such as image recognition (Rawat and Wang, 2017; LeCun et al., 2015), speech recognition (Hinton et al., 2012), and natural language processing (Collobert et al., 2011). Deep neural networks are strong in applications where huge amounts of data can be assembled and many variables interact with each other. A second disruptive class of machine learning algorithms are decision tree ensembles. The gradient boosting machine (Friedman, 2001) in particular excels in many applications. It often is the best performing algorithm for tabular data (Grinsztajn et al., 2022) and as such it is praised by many practitioners. Among the 29 challenge-winning solutions posted on Kaggle during 2015, 17 used xgboost – a variant of a gradient boosting machine (Chen and Guestrin, 2016). The second most popular method, deep neural networks, was used in 11 solutions. A downside of such algorithms is that they are black box methods in the sense that they are hard to visualize and interpret on the one hand, and lack theoretical backing on the other.

These black box methods are in contrast to classical statistical models that assume an explicit structure such as a linear (Nelder and Wedderburn, 1972) or additive model (Friedman and Stuetzle, 1981; Buja et al., 1989). Estimators received from classical statistical models are highly accurate if the model is correctly specified. However, they perform poorly if the data deviates strongly from the structure assumed by the model. Our aim is to combine the best of the two worlds. In a regression set-up we consider a regression problem and assume that the regression function can be approximated well by a function satisfying the bounded interaction BI() condition for a predefined small .

Condition 1 (BI())

A function satisfies BI() if it can be written as

| (1) |

for functions , where and .

Equivalently, we write for functions , where only depends on the values of , . We will use both versions interchangeably throughout this work. For a function that satisfies BI(), the components are not identified without additional constraints. For our work, the constraints used are of secondary importance. Possible constraints are deferred to the supplementary material. Note that is a constant. Thus if we assume that the regression function can be well approximated by a functional decomposition including only low dimensional structures (Stone, 1994; Hooker, 2007; Chastaing et al., 2012). Observe that if , we impose no additional restraint to the function . We propose a new tree based algorithm we call random planted forests (rpf) which given any satisfies BI().

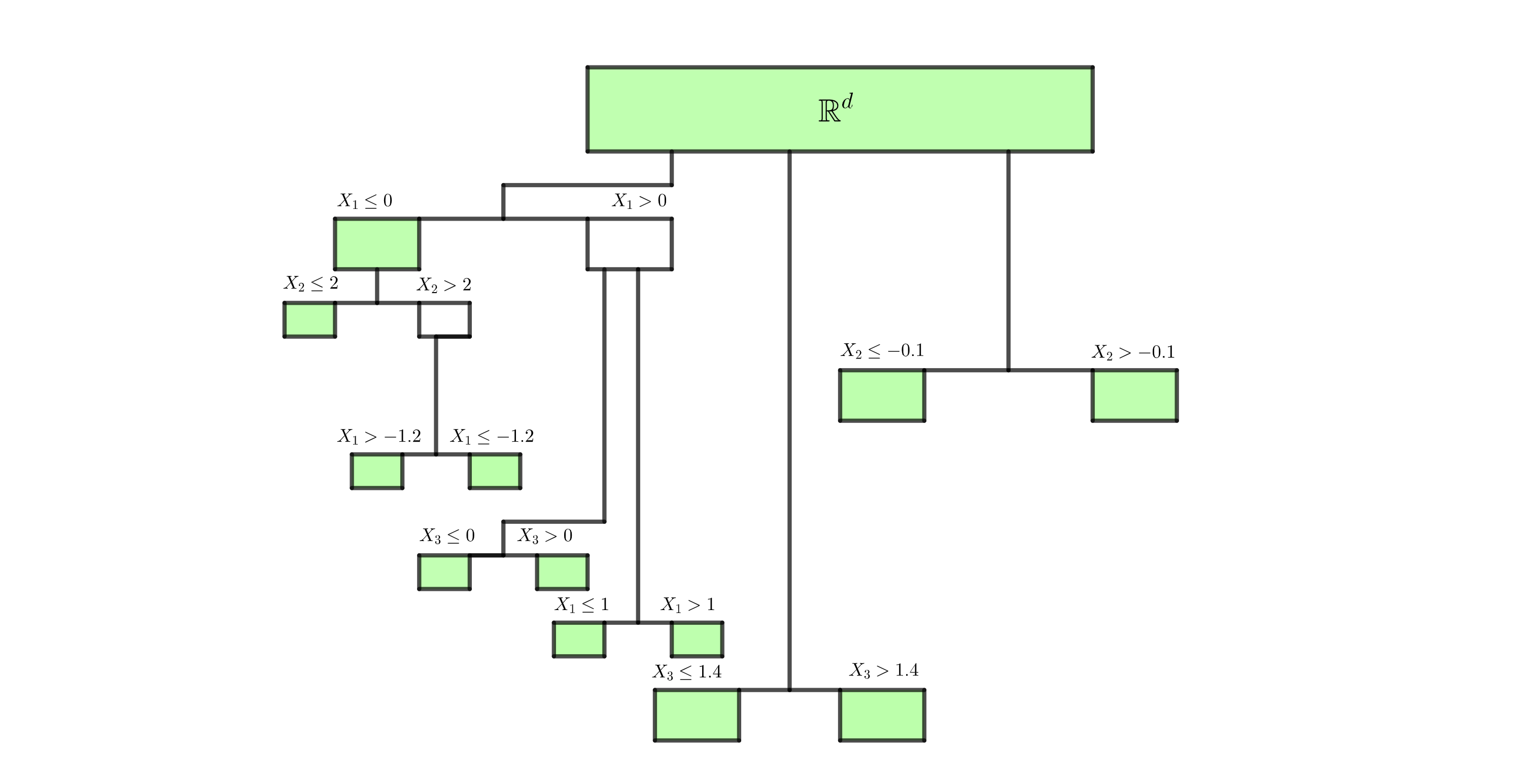

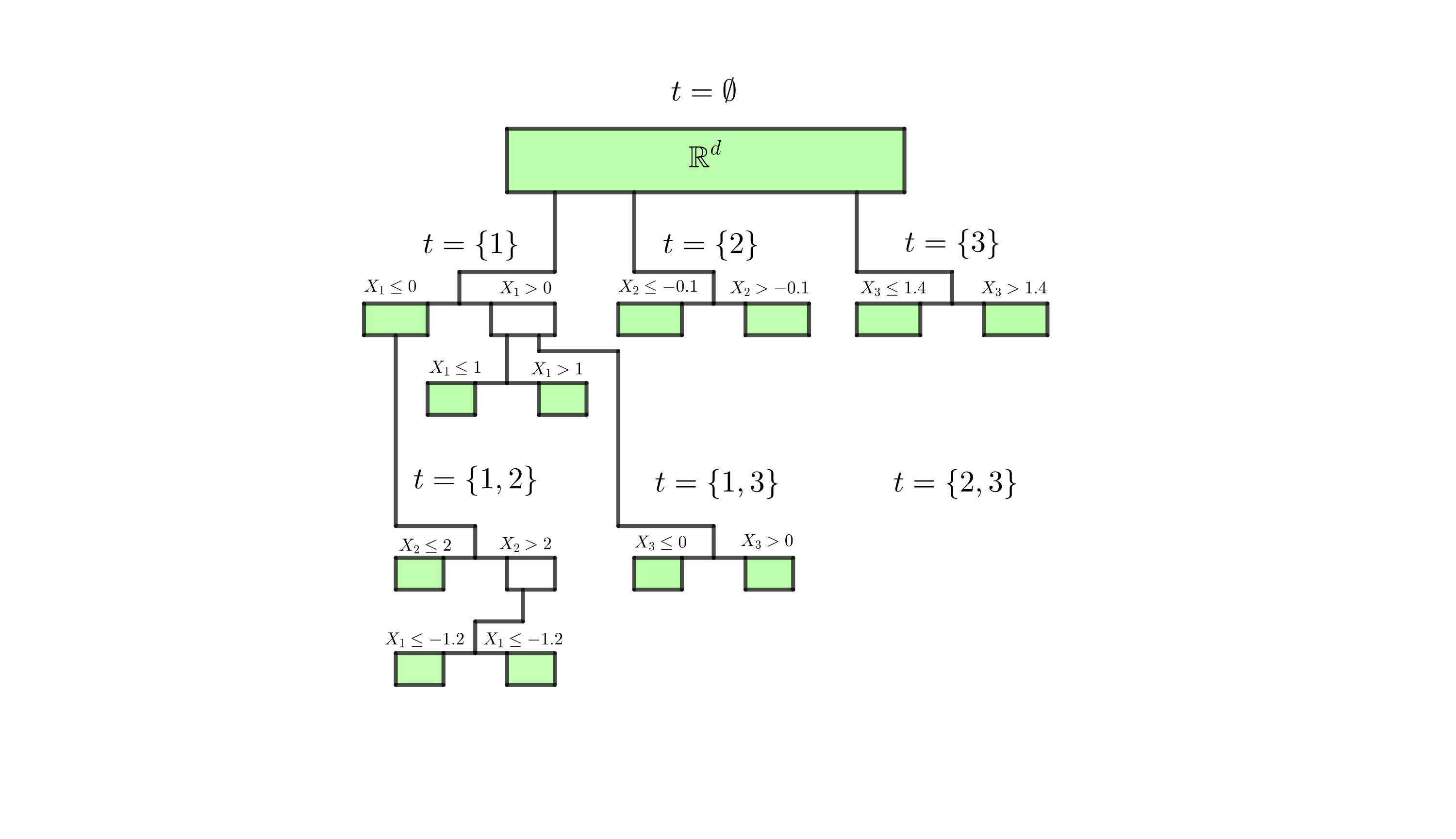

A tree in rpf can be thought of as a single traditional decision tree in which a leaf is not removed from the algorithm when split in some cases, see Rule (a) in Subsection 2.2. Furthermore, if a leaf was created using max_interaction coordinates, we only allow for splits with respect to coordinates which were already used, see Rule (b) in Section 2.2. Here is a tuning parameter. These rules are the main ingredients of rpf and they lead to a non-binary tree structure. We also made use of further rules that have been proposed in other implementations of random forests, see Rules (a)—(f) in Section 2.2 for a full description of rpf. The resulting estimator satisfies BI(max_interaction). Figure 1a provides a short illustration. A simple heuristic why it may be beneficial not to remove a leaf from a tree when splitting is the following. Consider the regression problem with and for large . If we never remove the original leaf, one can approximate by splitting the original leaf once with respect to each covariate . Thus for each covariate data points are considered for finding the optimal split value. Additionally we end up with on average data points in each leaf. In the original random forests algorithm, in order to find a similar function one would have to grow a tree where each leaf is constructed by splitting once with respect to each covariate. This implies that we end up with leaves, which on average contain data points. Thus the estimation should be much worse both because of less precise split points and less accurate fit values.

This example shows that rpf behaves quite differently than classical random forests independent of the interaction bound max_interaction imposed on the algorithm. In the simulation study presented in Section 3, we find that even in the case where no interaction bound is set () the results are promising.

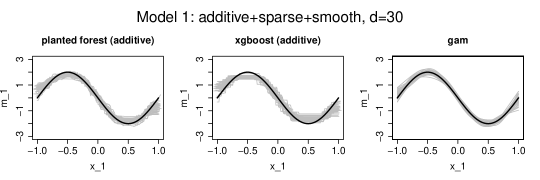

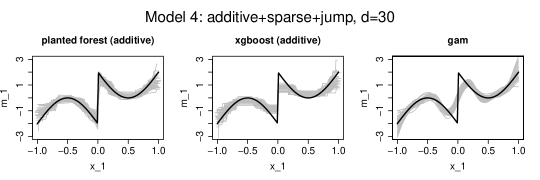

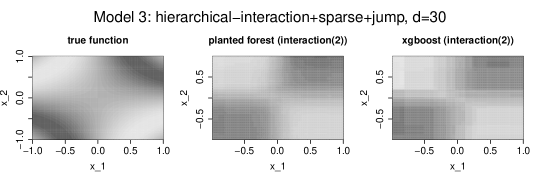

In practice, the value of the underlying regression function is unknown. Bounding the order of interaction does increase the performance of rpf if the true model satisfies BI, . An additional advantage of choosing or is that predictions can be visualized easily. Figures 2 – 4 show plots that visualize one and two dimensional components of a high dimensional model respectively. The models we use for comparison were chosen since they are the strongest competitors in the simulation results in Section 3 which satisfy BI() or BI().

In the past, other algorithms satisfying BI() for certain have been developed. Rpf differs from the tree based explainable boosting machine (Lou et al., 2012, 2013; Caruana et al., 2015; Lengerich et al., 2020) and the neural network based neural additive model (Agarwal et al., 2020) recently introduced in several ways. Similar to rpf, these methods aim to approximate the regression function via the functional decomposition (1) for or . However, they rather resemble classical statistical methods described earlier. After specifying a fixed structure, the explainable boosting machine assumes that every component is relevant and all components are fit via a backfitting algorithm (Breiman and Friedman, 1985). A similar principle using backpropagation instead of backfitting is applied in the neural additive model. In contrast, the rpf algorithm may ignore certain components completely. Additionally, when considering interaction terms do not need to be specified beforehand. Hence explainable boosting machine and the neural additive model do not share two key strengths of rpf: a) automatic interaction detection up to the selected order, b) strong performance in sparse settings, see Section 3. Some model-based boosting algorithms (Hofner et al., 2014) have similar properties to the ones given above. In particular, they also suffer from the fact that they do not have automatic interaction detection, which is especially troublesome if a large number of covariates are present. An algorithm not suffering from this problem is multivariate adaptive regression splines (Friedman, 1991). However, it has a continuous output. Thus it does not adapt well when single jumps are present. Furthermore, as seen in our simulation study in Section 3, multivariate adaptive regression splines are less accurate when many covariates are active. Considering the random forests algorithm, Tan et al. (2022) find that it performs poorly in models which satisfy BI(1). They propose a modification of random forests where each tree is replaced by a finite fixed number of trees that grow in parallel. For a discussion of the performance of rpf in such models, see also the theory developed in an earlier version of this paper Hiabu, Mammen and Meyer (2020).

From a theoretical point of view, the most comparable algorithm is random forests. A theoretical study of Breiman’s original version of random forests (Breiman, 2001) is rather complex due to the double use of data, once in a CART splitting criterion and once in the final fits. Scornet et al. (2015) provide a consistency proof for Breiman’s algorithm while assuming an BI(1). They also show that the forest adapts to sparsity patterns. In more recent papers, theory has been developed for subsampled random forests. By linking to theory of infinite order U-statistics, asymptotic unbiasedness and asymptotic normality has been established for these modifications of random forests, see Mentch and Hooker (2016, 2017), Wager and Athey (2018), Peng et al. (2019). In our mathematical analysis of rpf we assume that the splitting values do not strongly depend on the response variables which excludes using the CART splitting criterion. In this respect we follow a strand of literature on random forests, see e.g. Biau et al. (2008) and Biau (2012). Thus we circumvent theoretical problems caused by the double use of data as in Breiman’s random forest. We leave it to future research to study the extent to which theory introduced here carries over to random planted forests with data-dependent splitting rules, in particular for the case of random planted forests based on subsampling or sample-splitting.

In summary, rpf is useful for the following reasons: Rpf is a tree based algorithm that given an satisfies BI(). In contrast to most tree based algorithms, this enables interpretability of the regression fucntion by choosing a small . Another tree based algorithm that can be set to satsify BI() for any is gradient boosting machine by setting the tree depth to . However, our simulation study shows that small in xgboost does not always lead to satisfactory results. In general, intuitively, the difference between gradient boosting and rpf is that gradient boosting iteratively updates an estimator globally, while rpf approximates the components locally. Thus we conjecture that rpf performs better in the presense of highly irregular functional components, while gradient boosting may have an edge in highly regular settings. In this sense, we believe rpf to be complementary to existing algorithms. Our simulation study shows a good overall performance of rpf. The theoretical analysis suggests almost optimal convergence rates for rpf in low interaction settings. The theory developed is interesting in itself since it shows optimal convergence rates for tree based algorithms satisfying the conditions given in Section 4.

2 Random Planted Forests

2.1 Notation on Trees

A tree produces an estimator of the form for some sets which we refer to as leaves. The set is referred to as root. We split leaves by setting and for some , . These new leaves are either included in the estimator or replace . A set which was replaced is no longer referred to as leaf but as inner node.

2.2 Setup

We are handed data consisting of i.i.d. observations with and consider the regression problem

with the goal of estimating . Growing a planted tree in rpf is similar to the construction of a tree in random forests. It depends on a parameter , which corresponds to the parameter in BI(). In order to obtain a decomposition of the form (1), we sort leaves into leaf types, depending on which variables were used to construct the respective leaf. Rpf differs from random forests in the following way.

-

(a)

When splitting a leaf into two new leaves with respect to a coordinate which was not used in the construction of , the leaf is not deleted and may be used for splitting again in the future.

-

(b)

Leaves with leaf type may only be split with respect to dimensions .

-

(c)

If a leaf is updated, the corresponding estimator is updated by adding the average residual within the leaf.

For example, the root will never be deleted during a planted tree construction. An illustration of the algorithm unfolding is given in Figure 1a. Since a leaf may be split multiple times, the resulting final leaves of a planted tree are typically not disjoint. Thus simply defining the estimator as the sample average within a leaf does not yield useful results. Instead we keep track of the estimator during the algorithm and update it by averaging residuals in each iteration step similar to gradient boosting or backfitting. Since the order in which the splits occur makes a difference, we indicate the order by vertical position in Figure 1a. Note that (a) is important for obtaining a useful estimator satisfying BI(). For an intuition, assume (b) for and leaves are deleted after splitting as is the case for random forests. Then each tree will only depend on 1 variable, which does not result in a useful estimator. As discussed above, leaves are sorted into leaf types . An alternative illustration of rpf highlighting this sorting is given in Figure 1b.

Additionally, the following methods are implemented which are typical for forest type algorithms.

-

(d)

A forest is obtained by averaging the estimators from trees grown from bootstrap samples.

-

(e)

Dimensions and leaves used for splitting are selected from a random subset of possible dimension-leaf combinations. The parameter controlling the size of the subset is .

-

(f)

Split values are chosen from a set of random points.

Thus, the algorithm depends on five tuning parameters: The number of splits , the number of trees , the order of interaction and the parameters , . The importance of the parameters is discussed in the supplement.

We proceed by explaining the algorithm rigorously. A planted tree consists of a finite set of leaves and corresponding values . Observe that we sort the leaves with respect to their leaf type . Here denotes the number of leaves with type . For and we have

| (2) |

where for and for . Define the estimator for by with

Note that for any , due to (2), only depends on the values of . Thus satisfies BI(). Next, we introduce the calculation of a split in Subsection 2.3 followed by the iteration procedure in Subsection 2.4. We conclude with the extension to a forest and a discussion on the driving parameters.

2.3 Calculating a Split

We are handed a leaf of the form (2), a value , a splitting coordinate , a splitting value , and residuals . Define a partition by and Let , and

Observe that is constant on each of the sets , , and . We update the values values , and residuals . Pseudo-code of this procedure is given in Algorithm 1.

2.4 Random Planted Tree

In addition to , the algorithm depends on which determines the number of iterations before the algorithm stops. We start off by setting the residuals for . We define the root with value and thus the number of leaves with type is . Since we start off with no other leaves, for we have .

Each iteration step is carried out as follows. In step we are handed leaves with values and residuals . The leaves are of the form (2). Assume for now that we have selected a leaf , a coordinate , a split point and use Algorithm 1. The chosen combination must be viable in the sense that if . Now, there are two cases with different updating procedures.

-

•

If , we use as an input for Algorithm 1. Then the resulting leaves and are of type . We replace by and in the set of leaves of type .

-

•

If , we use as an input for Algorithm 1. The leaves and obtained are of type . We keep in the set of leaves of type and add leaves to the set of leaves of type .

The values and are set to be the corresponding values of and respectively. The residuals are updated accordingly. All other leaves and values are taken over from step . In order to select , , and we use the CART methodology. Thus we set

| (3) |

where for we denote by the residual one obtains by using Algorithm 1 with inputs , , , and if , otherwise. The algorithm stops after nsplits iterations. Pseudo-code of this procedure is given in Algorithm 2.

2.5 Random Planted Forests

The random planted forests algorithm depends on additional tuning parameters ntrees which denotes the number of trees in the forest, t_try which corresponds to the m_try parameter from random forests, and split_try which imposes a mechanism similar to extremely random forests (Geurts et al., 2006).

More precisely, in order to reduce variance, we extend Algorithm 2 to a forest estimator similar to the random forest procedure. We draw ntrees independent bootstrap samples from our original data. On each of these bootstrap samples, we apply Algorithm 2 with two minor adjustments. In each iteration step, given a coordinate and a leaf , we uniformly at random select split_try values (with replacement) from

Secondly, define a set representing the viable combinations

In each iteration step we select a subset uniformly at random, where for some given value . In step 4, when calculating in Equation (3), we minimize under the additional conditions that and or . The resulting estimators are denoted by for . The forest estimator is given by with

Further remarks on the algorithm including discussions on the tuning parameters can be found in Section A in the supplement.

3 Simulations

In this section we conduct an extensive simulation study in order to arrive at an understanding of how rpf copes with different settings and how it compares to other methods. For each of 100 Monte-Carlo simulations we consider the regression setup

where . We consider twelve different models outlined in Table 1. Following Nielsen and Sperlich (2005), the predictors are distributed as follows. We first generate from a -dimensional standard multi-normal distribution with mean equal to 0 and for . Then we set

This procedure is repeated independently 500 times.

| Description | Meaning |

|---|---|

| additive+sparse | |

| hierarchical interaction | |

| +sparse | |

| pure interaction+sparse | |

| additive+dense | |

| hierarchical interaction+dense | |

| pure interaction+dense | |

| smooth | |

| jump | |

The methods we compare are given in Table 2. With sbf, gam and MARS we included the most popular methods used for models satisfying BI(1). We also included xgboost and random forest which are the most popular tree based methods used in practice. Furthermore, we included BART as a benchmark for methods not satisfying BI() for small . Note that BART has a high complexity and computation time due to the fact that trees are not only grown but also trimmed again in some iterations.

| Description | short | Code-Reference |

| A gradient boosting variant | xgboost | Chen et al. (2020) |

| rpf | rpf | Supplement |

| Random forest | rf | Wright and Ziegler (2015) |

| Smooth backfitting111Smooth backfitting for additive models with a local linear kernel smoother | sbf | Supplement |

| Generalized additive models222A generalized additive model implementation via smoothing splines | gam | Wood (2011) |

| Bayesian additive regression trees | BART | Sparapani et al. (2021) |

| multivariate additive regression splines | MARS | Hastie and Tibshirani (2022) |

| 1 nearest neighbours | 1-NN | |

| Sample average | mean |

Performance is evaluated by the empirical mean squared error (MSE) from 100 simulations. The MSE is evaluated on test points which are generated independently from the data

where represents the estimator depending on the data . For xgboost and rpf we record results for the case when the estimators satisfy BI(). For the rpf algorithm, we further distinguish between an estimator satisfying BI(). We chose parameters via an independent simulation for each method from the parameter options outlined in Table 6 beforehand. For xgboost and rpf we also considered data-driven parameter choices (indicated by CV). We ran a 10-fold cross validation considering all parameters outlined in Table 6 including all sub-methods and options.

We only show selected parts of the overall study in the main part of this paper. Additional tables can be found in Section C in the supplement.

| Method | dim=4 | dim=10 | dim=30 | BI() |

|---|---|---|---|---|

| xgboost (depth=1) | 0.119 (0.021) | 0.142 (0.021) | 0.176 (0.027) | 1 |

| xgboost | 0.141 (0.024) | 0.166 (0.028) | 0.193 (0.033) | |

| xgboost-CV | 0.139 (0.028) | 0.152 (0.029) | 0.194 (0.035) | |

| rpf (max_interaction=1) | 0.087 (0.018) | 0.086 (0.017) | 0.097 (0.019) | 1 |

| rpf (max_interaction=2) | 0.107 (0.015) | 0.121 (0.025) | 0.142 (0.026) | 2 |

| rpf | 0.112 (0.017) | 0.134 (0.026) | 0.162 (0.028) | |

| rpf-CV | 0.103 (0.02) | 0.102 (0.035) | 0.105 (0.022) | |

| rf | 0.209 (0.021) | 0.252 (0.027) | 0.3 (0.029) | |

| sbf | 0.071 (0.026) | 0.134 (0.013) | 0.388 (0.073) | 1 |

| gam | 0.033 (0.012) | 0.035 (0.013) | 0.058 (0.021) | 1 |

| BART | 0.085 (0.019) | 0.076 (0.017) | 0.091 (0.023) | |

| BART-CV | 0.09 (0.019) | 0.081 (0.014) | 0.09 (0.02) | |

| MARS | 0.054 (0.014) | 0.061 (0.025) | 0.076 (0.031) | |

| 1-NN | 1.509 (0.1) | 3.228 (0.182) | 5.534 (0.313) | |

| average | 3.811 (0.217) | 3.689 (0.183) | 3.748 (0.202) | 0 |

Table 3 contains the additive sparse smooth setting. Considering algorithms satisfying BI(), we observe that algorithms relying on continuous estimators (sbf, gam) outperform the others with gam being the clear winner, irrespective of the number of predictors . Rpf (max_interaction=1) outperforms xgboost (depth=1). From the other algorithms, MARS does best with BART as runner up. Interestingly, rpf (max_interaction=2) and rpf perform very well and even outperform xgboost (depth=1). In the hierarchical interaction sparse smooth setting which is visualized in Table 4, we only show results from methods which can deal with interactions. Other cases are deferred to the supplement. Note that among the considered algorithms, rpf is the only algorithm satisfying BI(2). Performance wise, we find that BART as well as MARS outperform rpf. The latter slightly outperforms xgboost. In Table 8 in the supplement, a similar picture can be observed in the pure interaction case. In particular, BART proves to be much stronger than all competing algorithms. This comes at the cost of increased computational time.

Next, we re-visit the case where BI(1) is satisfied. However, this time the regression function is not continuous. The results are tabulated in Table 5. Considering algorithms satisfying BI(), rpf (max_interaction=1) performs best with xgboost (depth=1) following up. A visual picture of the excellent fit of rpf was provided in Figure 3. From the other algorithms, BART is the first competitor. Unsurprisingly, models based on continuous estimators can not deal with jumps in the regression function. Cases including interaction terms and jumps are deferred to the supplement.

| Method | dim=4 | dim=10 | dim=30 | BI() |

|---|---|---|---|---|

| xgboost | 0.374 (0.035) | 0.481 (0.064) | 0.557 (0.089) | |

| xgboost-CV | 0.393 (0.051) | 0.499 (0.058) | 0.563 (0.089) | |

| rpf (max_interaction=2) | 0.248 (0.038) | 0.327 (0.045) | 0.408 (0.07) | 2 |

| rpf | 0.263 (0.034) | 0.357 (0.044) | 0.452 (0.076) | |

| rpf-CV | 0.277 (0.039) | 0.366 (0.051) | 0.463 (0.083) | |

| rf | 0.432 (0.039) | 0.575 (0.061) | 0.671 (0.08) | |

| BART | 0.214 (0.03) | 0.223 (0.04) | 0.252 (0.037) | |

| BART-CV | 0.242 (0.043) | 0.276 (0.053) | 0.315 (0.047) | |

| MARS | 0.355 (0.089) | 0.282 (0.038) | 0.414 (0.126) | |

| 1-NN | 2.068 (0.156) | 5.988 (0.624) | 11.059 (0.676) | |

| average | 8.366 (0.43) | 8.086 (0.246) | 8.207 (0.496) | 0 |

| Method | dim=4 | dim=10 | dim=30 | BI() |

|---|---|---|---|---|

| xgboost (depth=1) | 0.19 (0.029) | 0.282 (0.044) | 0.401 (0.045) | 1 |

| xgboost | 0.198 (0.031) | 0.265 (0.053) | 0.286 (0.034) | |

| xgboost-CV | 0.209 (0.028) | 0.281 (0.052) | 0.313 (0.058) | |

| rpf (max_interaction=1) | 0.159 (0.033) | 0.198 (0.075) | 0.179 (0.041) | 1 |

| rpf (max_interaction=2) | 0.185 (0.028) | 0.24 (0.066) | 0.259 (0.043) | 2 |

| rpf | 0.192 (0.026) | 0.251 (0.065) | 0.282 (0.043) | |

| rpf-CV | 0.169 (0.033) | 0.207 (0.072) | 0.183 (0.042) | |

| rf | 0.274 (0.035) | 0.322 (0.05) | 0.375 (0.037) | |

| sbf | 0.342 (0.049) | 0.603 (0.053) | 1.112 (0.138) | 1 |

| gam | 0.41 (0.047) | 0.406 (0.027) | 0.431 (0.06) | 1 |

| BART | 0.177 (0.047) | 0.162 (0.038) | 0.157 (0.034) | |

| BART-CV | 0.179 (0.051) | 0.163 (0.041) | 0.159 (0.036) | |

| MARS | 0.751 (0.136) | 0.74 (0.104) | 0.687 (0.123) | |

| 1-NN | 2.393 (0.229) | 3.029 (0.308) | 3.512 (0.333) | |

| average | 1.276 (0.075) | 1.25 (0.063) | 1.213 (0.054) | 0 |

We now consider dense models. In the additive dense smooth model, see Table 11 in the supplement, the clear winners are sbf and gam, with gam having the best performance. This is not surprising, since these methods have more restrictive model assumptions than the others. Additionally, gam typically has an advantage over sbf in our setting. This is because splines usually fit trigonometric curves well, while kernel smoothers would be better off with a variable bandwidth in this case, which we did not implement. Observe that MARS does not deal well with this situation. Our rpf method is in third place, tied with BART and slightly outperforming xgboost. This suggests that the rpf is especially strong in sparse settings. In dense settings, the advantage towards xgboost and BART shrinks. This observation is underpinned in the hierarchical interaction dense smooth model, tabulated in Table 12 in the supplement. While rpf and BART perform best with only four predictors, in dimension 10 xgboost outperforms rpf.

We close this section by making some concluding remarks on the simulation results. Considering algorithms satisfying BI(), we observe that rpf (max_interaction=1) adapts well to various models, in particular in sparse settings. While other algorithms such as gam outperform rpf in specific settings, rpf shows a good overall performance and higher flexibility. Additionally, rpf has the advantage of providing estimators which can approximate interactions and satisfy BI() for predefined . The simulations also show that non-restricted versions (rpf and rpf-CV) are competitive, while BART outperforms rpf in most cases. Note that BART is computationally quite intensive and we indeed struggled to get BART running in higher dimensional cases without error. Computational problems may increase if one goes to larger data sets, . Xgboost showed very strong results in terms of accuracy while being very fast and resources effective. However, accuracy turns out to be slightly worse than that of rpf in low-interaction settings.A short comparison of rpf-CV, xgboosting-CV, BART-CV and random forest can also be found in the supplement.

4 Theoretical properties

In this section we derive asymptotic properties for a slightly modified rpf algorithm. The main difference is that in the tree construction of the modified forest estimator, splitting does not depend on the responses directly, at least not strongly, see Condition 2. With this modification we follow other studies of forest based algorithms to circumvent mathematical difficulties which arise if settings are analyzed where the same data is used to choose the split points as well as to calculate the fits in the leaves. Clearly, one can apply the results in this section to a similar modification of rpf making use of data splitting to separate splitting and fitting. An alternative route would be to use subsampling approaches as has been done in Mentch and Hooker (2016, 2017), Wager and Athey (2018), Peng et al. (2019). However, it is not clear if this would allow a detailed analysis of the rate of convergence of a subsampling version of rpf. Our results imply two findings. First for the estimator can achieve optimal rates up to logarithmic terms in the nonparametric model where the interaction terms (for ) allow for continuous second order derivatives. Secondly, for all choices of one achieves faster rates of convergence for the forest estimator than for tree estimators that are based on calculating only one single tree. We will comment below why the situation changes for compared to . A major challenge in studying rpf lies in the fact that the estimator is only defined as the result of an iterative algorithm and not as the solution of an equation or of a minimizing problem. In particular, our setting differs from other studies of random forests where tree estimates are given by leaf averages of terminal nodes. In such settings the tree estimator only depends on the terminal leaves, but not on other structural elements of the tree, and in particular not on the way the tree was grown. Secondly, the definition of the estimator as a leaf average allows for simplifications in the mathematical analysis. The main point of our mathematical approach is to show that approximately the tree estimators and the forest estimators are given by a least squares problem defined by the leaves at the end of the algorithm.

We assume that the regression function fulfills BI() with parameter . We write , where the components are smooth functions which only depend on the values of . The data is generated as

In the model equation, the ’s are mean zero error variables and, for simplicity, the covariables are assumed to lie in ; . We introduce a class of theoretical random planted forests. The class depends on an updating procedure of leaves which must satisfy the conditions below. An example and explanation of the conditions is given in Section B in the supplement. As initialisation we set , and for . In iteration steps , a leaf type is selected and sets of a partition of with are updated with some (random) procedure satisfying the conditions below. Here and in the following, we sometimes write instead of for functions that depend only on via . Similarly, we sometimes write . For a subset of we write for the Lebesgue measure of . Note that for finite sets , we also use for the number of Elements in . Additionally, we write for the empirical measure of . In order to update , we define the density estimator for and the -dimensional estimator for . With this notation an update for leave type can be written as

| (4) |

Here for with the function is a marginal estimator defined by . For we set . Note that (4) is a mathematically convenient rewriting of an update in the rpf algorithm. For residuals for with are averaged and the average is added to the old fit of in . After () steps we get the estimators for . Now, the tree estimator of the function is given by . For the forest estimator tree estimators are repeatedly constructed. They are denoted by for and for (). We define the forest estimator as for and . If necessary, we will also write , , ,, … instead of , , ,, … to indicate that we discuss the tree estimator with index .

4.1 Main results

For our results we make use of the following assumptions.

Condition 2

The tuples are i.i.d. The functions are twice continuously differentiable and for all . The covariable has a density that is bounded from above and below (away from ). For the joint density of the tuple allows continuous derivatives of order 2. Conditionally on and the iterative construction of the leaves, the error variables have mean zero, variance bounded by a constant, and the products are mean zero for . Conditionally on the iterative construction of the leaves in the trees are i.i.d. for .

Note that the number of iterations in the tree construction and the number of constructed trees may depend on . The parameter is of the same order as the number of leaves in the final partition. is assumed to converge to infinity, see Condition 3. When considering the forest estimator one usually requires to converge to infinity as well in order to obtain useful convergence rates, see also Conditions 7,8. In the next condition we assume that each leave type is chosen often enough.

Condition 3

For large enough we assume that there exists a constant such that, with probability tending to one, for and there exists a partition such that for the set contains all elements of . Here and are the smallest integers larger or equal to and respectively.

We now assume that the tree partitions become fine enough.

Condition 4

For , , we define such that . We assume that with probability tending to one uniformly over , ,

for a sequence with and for large enough.

The next two conditions assume that there are not too large changes in the tree partitions in the last logarithmic iterations and that the histogram estimators in the updating equations converge to the underlying design densities.

Condition 5

It holds for , and that

with probability tending to one.

Condition 6

It holds uniformly for , , that

with probability tending to one for sequences , with and .

Theorem 4.1

Under Conditions , for the tree estimators satisfy

with probability tending to one, where denotes the norm.

The proof of Theorem 4.1 can be found in Section 4.2. We shortly discuss this result. Suppose that the leaves have side lengths of order for some sequence . Then is of order , is of order and up to logarithmic terms we obtain a rate of order for the estimation error of .

We now discuss the performance of the forest estimator. For the result we need the following additional assumptions for discussing the complete forest estimator.

Condition 7

It holds uniformly for , that

with probability tending to one for some sequences .

Condition 8

For we write and . It holds uniformly for that

with probability tending to one for a sequence . Here denotes the norm.

Below we will argue that the averaged estimators and in Condition 8 can achieve rates of convergence compared to their summands which have a bias of order . If the density is twice continuously differentiable, qualitatively, behaves like a kernel density estimator with bandwidth of order . We switch from the norm to the norm in Condition 8 and the next theorem. The reason is that at the boundary of size with large enough we have a bias of order where the bias is of order in the interior. Thus measured by the norm we get a bias of order whereas the norm has a slower rate caused by the boundary effects.

Theorem 4.2

Under Conditions , for the forest estimator we have

with probability tending to one.

The proof of the theorem will be given in Section 4.3. Again, we shortly discuss this result. As above, suppose that the leaves have side lengths of order for some sequence . Then is of order and is of order . The sequence is the rate of a histogram estimator of dimension which up to logarithmic terms is of order for dimensional estimators. For sufficiently far away from the boundary of assume that the random variables and approximately follow the same distribution, where are the lower and upper bounds of the leaf which contains with respect to dimension . Then the bias terms of order cancel and we get that the bias terms measured by are of order . Thus, up to logarithmic terms, we get a bound on the accuracy of the forest estimator of order . This rate is faster than the tree rate if , i.e. we need consistency of dimensional histogram estimators. Let us discuss this for a bandwidth that is rate optimal for the estimation of twice differentiable functions with dimensional argument. Then is of order and the -dimensional estimators are consistent for . Thus, we get from our theory that for optimal tuning parameters forest estimators outperform tree estimators. For we obtain optimal rates by the forest estimator, i.e. for and for .

We now explain where the consistency of the density histogram estimators is essential. The estimators show up as kernels in integral equations which define the tree and forest estimators. This means that, approximately, the tree estimators are given as solutions of integral equations of the form with random integral operators , where the operators are defined by up to dimensional density estimators. If these density estimators are consistent, the operators are approximately equal to an operator not depending of . Then approximately solves and the forest estimator approximately solves . In order to get faster convergence rates for the forest estimator one shows that the average has faster rates as the summands .

For the whole argument it is crucial that up to dimensional density estimators are consistent. In case these estimators are inconsistent invertibility of the operator does not carry over to the operator . Thus, the equation may not have a unique solution which suggests that the solution to which the algorithm converges depends on how the tree was grown. In particular, this excludes a mathematical study along our lines.

4.2 Proof of Theorem 4.1

In the proof we denote different constants by . The meaning of may change, also in the same formula. In this proof we omit the index in the notation.

We rewrite (4) as

| (5) |

where , and where

for a function . Iterative application of (5) gives for

| (6) | |||||

We will use this equality in the proofs of the following lemmas for the choices and with .

Lemma 4.3

It holds that

Proof:

It can be easily shown that for

| (7) |

Furthermore, for any function we have

| (8) |

For a proof of (8) consider the space of functions endowed with the pseudo metric

Then is the orthogonal projection onto the space of piecewise constant functions that are constant on the leaves . Furthermore, is the orthogonal projection onto the orthogonal complement of this space. This shows (8). The statement of the lemma now follows from (7) and (8) by application of (6) with and .

The previous lemma can be used to show a bound for the norm of which we denote by

Lemma 4.4

It holds that with probability tending to one

Proof:

For we get by application of Condition 6 that

The statement of the lemma now follows by application of Lemma 4.3.

Lemma 4.5

It holds for some and that with probability tending to one

Here for an operator mapping into we denote the operator norm by . Before we come to the proof of this lemma let us discuss its implications. Using the representation (5) we get from Lemmas 4.4, 4.5 that for all we can choose a constant such that if is large enough with probability tending to one

| (9) |

where

Note that only depends on the growth history of the tree in the last steps. Thus we have shown that approximately the same holds for the tree estimators . Below we will go a step further and show that the tree estimator approximately only depends on the data averages in the terminal leaves and in particular not on the growth of the tree in the past. Before we come to this refinement we first give a proof of Lemma 4.5. For this purpose we will introduce population analogues of the operators and we will discuss some theory on backfitting estimators in interaction models. We consider the following subspaces of functions with for

In particular, is the subspace of that contains only constant functions. In abuse of notation for a function we also write with instead of . Thus can be interpreted as a function with domain or with domain . The projection of onto is denoted by . For and with one gets

with

We now consider operators of the form with . We call these operators complete. We argue that there exists a constant such that for all complete operators of this form we have

| (10) |

Note that in particular does not depend on the order of . Our notation is a little bit sloppy because in the representation of the summands are not uniquely defined because may be nonempty for some , . A more appropriate notation would be to define as an operator mapping into and to endow this space with the pseudo norm . For a proof of (10) we will show that are closed subspaces of for all choices of . In particular, by a result of Deutsch (1985), see also Appendix A.4 in Bickel, Klaassen, Ritov and Wellner (1993), this implies that for , where for two linear subspaces and of the quantity is the cosine of the minimal angle between and , i.e.

According to a result of Smith, Solomon and Wagner (1977) this implies that for an operator of the above form we have that

where is chosen such that . We remark that this bound is also valid if the space is identical to the same space for several choices of . In this case we have for all such values of the index with the exception of the last appearance of . Because there are only finitely many ways to order elements we get by the last remark that (10) holds with some for all operators . For a proof of (10) it remains to show that are closed subspaces of for all choices of . For this claim we will argue that are closed subspaces of for all choices of , where for . According to Proposition 2 in the supplement material A.4 of Bickel, Klaassen, Ritov and Wellner (1993) this follows if there exists some such that implies that for some . This can be easily verified with by noting that for it holds that

In particular, one can use (10) to show that with

we have for with some , and some

where

with . Note that

Proof:

[Proof of Lemma 4.5] By Condition 6 we have by application of Cauchy-Schwarz inequality that

| (11) |

with probability tending to one. This implies that, with probability tending to one,

and we get by a telescope argument that, with probability tending to one, for

Because by Condition 3 is a complete operator with high probability, we get from (10) that, with probability tending to one, for

This inequality can be used to show the bound on , claimed in Lemma 4.5.

As discussed above, Lemma 4.5 implies (9). We now approximate by where

Note that differs from by having always the superindex for the operators and the functions . In the following lemma we compare and . The bound can be shown by similar arguments as in the proof of (9). In this proof one uses Condition 5 instead of (11). One gets that for all we can choose a constant such that if in Condition 3 is large enough with probability tending to one . If is chosen large enough we get the following lemma, see Assumption Condition 4.

Lemma 4.6

If in Condition 3 is large enough it holds that with probability tending to one

We now define as a minimizer of

over all function that are piecewise constant on the leaves . Then we have for all which implies that

| (12) |

This shows that

This equation can be used to prove the following result:

Lemma 4.7

If in Condition 3 is large enough it holds that with probability tending to one

We now decompose into a stochastic and a bias term

where minimizes

over all function that are piecewise constant on the leaves and minimizes

over the same class of piecewise constant functions. We see that is the projection of onto an -dimensional linear subspace of . We conclude that

| (13) |

For the study of the bias term define with

for . Now, by definition of , we have that

Furthermore, we have by an application of Condition 4 that

Using the same arguments as in the proof of Lemma 4.4 one gets the same bound with empirical norm replaced by the norm . This concludes the proof of the theorem.

4.3 Proof of Theorem 4.2

We now introduce the super index again which denotes the number of the respective tree . Note that the bound of Lemma 4.7 holds uniformly over . We can decompose into a stochastic and a bias term

and we get from (13) that

For the treatment of the averaged bias term note that for

where for . Now by subtracting we get

where . This can be rewritten as

where

By averaging the integral equations over we get

| (14) | |||

where , , and .

We now argue that with probability tending to one

| (15) | |||

| (16) | |||

| (17) |

Note that with we can rewrite (14) as

| (18) |

Order the elements of as . Iterative application of (18) gives that

| (19) |

where and . Because is a complete operator we get from (10) that for with . Furthermore, one can easily verify for with some constant . With the help of (15)–(17) this shows and with probability tending to one where . From (19) we get with . With probability tending to one, it holds which implies . We conclude with probability tending to one. This shows the statement of Theorem 4.2. It remains to verify (15)–(17). The first claim follows directly from Condition 7. For the proof of (16) one makes use of the bounds for , and which we have shown during the proof of Theorem 4.1 and which carry over to the averaged values. For the proof of (17) note that

holds with

Using similar arguments as above, one can easily verify and with probability tending to one. This concludes the proof of the theorem.

References

- Agarwal et al. (2020) Agarwal, R., N. Frosst, X. Zhang, R. Caruana, and G. E. Hinton (2020). Neural additive models: Interpretable machine learning with neural nets. arXiv preprint arXiv:2004.13912, 1–17.

- Apley and Zhu (2020) Apley, D. W. and J. Zhu (2020). Visualizing the effects of predictor variables in black box supervised learning models. Journal of the Royal Statistical Society: Series B (Statistical Methodology) 82(4), 1059–1086.

- Biau (2012) Biau, G. (2012). Analysis of a random forests model. Journal of Machine Learning Research 13(1), 1063–1095.

- Biau et al. (2008) Biau, G., L. Devroye, and G. Lugosi (2008). Consistency of random forests and other averaging classifiers. Journal of Machine Learning Research 9, 2015–2033.

- Breiman (2001) Breiman, L. (2001). Random forests. Machine Learning 45(1), 5–32.

- Breiman and Friedman (1985) Breiman, L. and J. H. Friedman (1985). Estimating optimal transformations for multiple regression and correlation. Journal of the American Statistical Association 80(391), 580–598.

- Buja et al. (1989) Buja, A., T. Hastie, and R. Tibshirani (1989). Linear smoothers and additive models. Annals of Statistics 17(2), 453–510.

- Caruana et al. (2015) Caruana, R., Y. Lou, J. Gehrke, P. Koch, M. Sturm, and N. Elhadad (2015). Intelligible models for healthcare: Predicting pneumonia risk and hospital 30-day readmission. In Proceedings of the 21th ACM SIGKDD international conference on knowledge discovery and data mining, pp. 1721–1730.

- Chastaing et al. (2012) Chastaing, G., F. Gamboa, C. Prieur, et al. (2012). Generalized Hoeffding-Sobol decomposition for dependent variables-application to sensitivity analysis. Electronic Journal of Statistics 6, 2420–2448.

- Chen and Guestrin (2016) Chen, T. and C. Guestrin (2016). Xgboost: A scalable tree boosting system. In Proceedings of the 22nd ACM SIGKDD international conference on knowledge discovery and data mining, pp. 785–794.

- Chen et al. (2020) Chen, T., T. He, M. Benesty, V. Khotilovich, Y. Tang, H. Cho, K. Chen, R. Mitchell, I. Cano, T. Zhou, M. Li, J. Xie, M. Lin, Y. Geng, and Y. Li (2020). xgboost: Extreme gradient boosting. R package version 1.2.0.1.

- Collobert et al. (2011) Collobert, R., J. Weston, L. Bottou, M. Karlen, K. Kavukcuoglu, and P. Kuksa (2011). Natural language processing (almost) from scratch. Journal of Machine Learning Research 12, 2493–2537.

- Friedman (1991) Friedman, J. H. (1991). Multivariate adaptive regression splines. Annals of Statistics 19(1), 1–67.

- Friedman (2001) Friedman, J. H. (2001). Greedy function approximation: a gradient boosting machine. Annals of Statistics 29(5), 1189–1232.

- Friedman and Stuetzle (1981) Friedman, J. H. and W. Stuetzle (1981). Projection pursuit regression. Journal of the American Statistical Association 76(376), 817–823.

- Geurts et al. (2006) Geurts, P., D. Ernst, and L. Wehenkel (2006). Extremely randomized trees. Machine Learning 63(1), 3–42.

- Grinsztajn et al. (2022) Grinsztajn, L., E. Oyallon, and G. Varoquaux (2022). Why do tree-based models still outperform deep learning on typical tabular data? In Thirty-sixth Conference on Neural Information Processing Systems Datasets and Benchmarks Track.

- Hastie and Tibshirani (2022) Hastie, T. and R. Tibshirani (2022). mda: Mixture and flexible discriminant analysis. R package version 0.5-3.

- Hiabu et al. (2022) Hiabu, M., J. T. Meyer, and M. N. Wright (2022). Unifying local and global model explanations by functional decomposition of low dimensional structures. arXiv preprint arXiv:2208.06151.

- Hinton et al. (2012) Hinton, G., L. Deng, D. Yu, G. E. Dahl, A.-R. Mohamed, N. Jaitly, A. Senior, V. Vanhoucke, P. Nguyen, T. N. Sainath, et al. (2012). Deep neural networks for acoustic modeling in speech recognition: The shared views of four research groups. IEEE Signal Pprocessing Magazine 29(6), 82–97.

- Hofner et al. (2014) Hofner, B., A. Mayr, N. Robinzonov, and M. Schmid (2014). Model-based boosting in r: a hands-on tutorial using the R package mboost. Computational Statistics 29(1), 3–35.

- Hooker (2007) Hooker, G. (2007). Generalized functional ANOVA diagnostics for high-dimensional functions of dependent variables. Journal of Computational and Graphical Statistics 16(3), 709–732.

- LeCun et al. (2015) LeCun, Y., Y. Bengio, and G. Hinton (2015). Deep learning. Nature 521(7553), 436–444.

- Lengerich et al. (2020) Lengerich, B., S. Tan, C.-H. Chang, G. Hooker, and R. Caruana (2020). Purifying interaction effects with the functional anova: An efficient algorithm for recovering identifiable additive models. In International Conference on Artificial Intelligence and Statistics, pp. 2402–2412. PMLR.

- Lou et al. (2012) Lou, Y., R. Caruana, and J. Gehrke (2012). Intelligible models for classification and regression. In Proceedings of the 18th ACM SIGKDD international conference on knowledge discovery and data mining, pp. 150–158.

- Lou et al. (2013) Lou, Y., R. Caruana, J. Gehrke, and G. Hooker (2013). Accurate intelligible models with pairwise interactions. In Proceedings of the 19th ACM SIGKDD international conference on knowledge discovery and data mining, pp. 623–631.

- Mentch and Hooker (2016) Mentch, L. and G. Hooker (2016). Quantifying uncertainty in random forests via confidence intervals and hypothesis tests. Journal of Machine Learning Research 17(1), 841–881.

- Mentch and Hooker (2017) Mentch, L. and G. Hooker (2017). Formal hypothesis tests for additive structure in random forests. Journal of Computational and Graphical Statistics 26(3), 589–597.

- Nelder and Wedderburn (1972) Nelder, J. A. and R. W. Wedderburn (1972). Generalized linear models. Journal of the Royal Statistical Society: Series A (General) 135(3), 370–384.

- Nielsen and Sperlich (2005) Nielsen, J. P. and S. Sperlich (2005). Smooth backfitting in practice. Journal of the Royal Statistical Society: Series B (Statistical Methodology) 67(1), 43–61.

- Peng et al. (2019) Peng, W., T. Coleman, and L. Mentch (2019). Asymptotic distributions and rates of convergence for random forests via generalized U-statistics. arXiv preprint arXiv:1905.10651 Preprint, 1–62.

- Rawat and Wang (2017) Rawat, W. and Z. Wang (2017). Deep convolutional neural networks for image classification: A comprehensive review. Neural Computation 29(9), 2352–2449.

- Scornet et al. (2015) Scornet, E., G. Biau, J.-P. Vert, et al. (2015). Consistency of random forests. Annals of Statistics 43(4), 1716–1741.

- Sparapani et al. (2021) Sparapani, R., C. Spanbauer, and R. McCulloch (2021). Nonparametric machine learning and efficient computation with Bayesian additive regression trees: the BART R package. Journal of Statistical Software 97(1), 1–66.

- Stone (1994) Stone, C. J. (1994). The use of polynomial splines and their tensor products in multivariate function estimation. Annals of Statistics 22(1), 118–171.

- Tan et al. (2022) Tan, Y. S., A. Agarwal, and B. Yu (2022). A cautionary tale on fitting decision trees to data from additive models: generalization lower bounds. In International Conference on Artificial Intelligence and Statistics, pp. 9663–9685. PMLR.

- Wager and Athey (2018) Wager, S. and S. Athey (2018). Estimation and inference of heterogeneous treatment effects using random forests. Journal of the American Statistical Association 113(523), 1228–1242.

- Wood (2011) Wood, S. N. (2011). Fast stable restricted maximum likelihood and marginal likelihood estimation of semiparametric generalized linear models. Journal of the Royal Statistical Society: Series B (Statistical Methodology) 73(1), 3–36.

- Wright and Ziegler (2015) Wright, M. N. and A. Ziegler (2015). ranger: A fast implementation of random forests for high dimensional data in C++ and R. arXiv preprint arXiv:1508.04409.

Appendix A The Random Planted Forest Algorithm

In this section we add some technical details which improve the understanding of the rpf algorithm. We shortly discuss the parameters introduced and explain why choices were made when designing the algorithm. We then give a short overview over the algorithm in the additive case, i.e. if . The simplification is easier to understand and of particular interest in our simulation study in Section 3. Next, we include the discussion of an identification constraint for the functional decomposition, which is important for plotting the components.

A.1 max_interaction

The rpf estimator satisfies BI(max_interaction). This is one of the main benefits of rpf. Additionally, max_interaction can be seen as a tuning parameter of the algorithm. Our simulations show that its value does not have much impact if it is high enough, while there are benefits if one specifies the model precisely. Note that by setting max_interaction to a high value, one looses the benefit of interpretability.

A.2 Leaves

It is important that some leaves may be split multiple times. Consider a naive random forest estimator with the additional condition that leaves with type are only splittable with respect to dimensions . If we set , the naive estimator would only ever depend on 1 coordinate. Thus the root leaf must be kept in the algorithm. Similar but slightly more involved examples show that one should not delete leaves when they are split with respect to a new dimension. An other idea may be to never delete any leaf when splitting. We found that this considerably increases computational cost while not decreasing the performance of the algorithm.

Furthermore, in the random forest algorithm, the order in which one splits leaves does not make a difference. However, as discussed above, it makes a difference for rpf. It seems most natural to decide on which leaf to split by optimizing via (3). We note that this procedure increases the computational cost.

A.3 nsplits

The parameter nsplits determines the number of iterations in a planted tree. In random forests other termination criteria are used such as bounding the tree depth from above or the number of data points in a leaf from below. These criteria do not terminate rpf since for example the root is always splittable in both cases.

A.4 t_try

In random forests one limits the number of coordinates considered in each iteration step using a parameter m_try. The idea is to reduce the variance by forcing the trees to differ more substantially. Similarly, we limit the number of combinations of leaf types and coordinates considered in each iteration step. The number of combinations is defined as a proportion t_try of the number of viable combinations . Thus the number of combinations considered increases as the algorithm unfolds. We assessed many different similar mechanisms in order to restrict the number of combinations used in an iteration step. First of all, we found that using a random subset of the viable combinations instead of simply restricting the coordinates for splitting is far superior. Roughly speaking, the reason is that the algorithm may lock itself in a tree if all leaves are splitable in each step. The question remains how to quantify the amount of combinations used. Selecting a constant number of viable combinations has the disadvantage of either allowing all combinations in the beginning or having essentially random splits towards the end of the algorithm. Thus the number of combinations considered must depend on the number of viable combinations. While other functional connections between the number of viable and the number of considered combinations are possible, choosing a proportional connection seems natural.

A.5 split_try

In contrast to t_try, the parameter split_try implies an almost constant number of considered split points in each iteration. The split_try split options are selected uniformly at random with replacement. In Section 3, we find that the optimal value for split_try is usually small compared to the data size. In our experience, using a proportion of the split points available either leads to totally random splits for small leaves or essentially allows all splits for large leaves. The reason is that for large leaves, if a small number of data points are added or removed from the leaf, the estimation is basically the same. The version we use here yielded the best results. The choice as well as only using split_try split points is done in order to reduce the variance of the estimator by reducing correlation between trees. It also reduces computational cost. While it is not obvious which of the two parameters, split_try or t_try, should be lowered in order to reduce variance, our results significantly improved as soon as we introduced the mechanisms regarding the parameters.

A.6 Driving Parameters

Although the presence of the mechanisms involving split_try and t_try improve the results of rpf, the exact value they take on is not as relevant. Rather, we consider them to be fine-tuning parameters. Similarly, the number of trees ntrees in a forest does not have much impact as long as ntrees is large enough; in our simulation study, seemed satisfactory. The main driving parameter for the estimation quality of rpf is the number of iteration steps nsplits. While the estimation is quite stable under small changes of nsplits, strongly lowering nsplits results in a bias, while vastly increasing the parameter leads to overfitting.

A.7 Random Planted Forests for BI()

In this section we explain the rpf algorithm in the additive case, i.e. if we set . Recall that the resulting estimator satisfies BI(). The algorithm then simplifies in the following way. All non-root leaves grown during the algorithm have leaf type for some . The set introduced in Subsection 2.5 reduces to

In particular, it does not depend on the current state of the of planted tree. Noting that , the value is constant throughout the algorithm. Thus the parameter t_try or equivalently m_try act exactly the same as the parameter m_try in Breimans implementation of random forests. In this case, rpf differs from extremely random forest mainly due to the fact that the root is never deleted during the algorithm and all leaves are constructed using only one coordinate.

A.8 Identification Constraint

If , the components can be visualized easily. In order to reasonably compare plots, we need a condition that ensures uniqueness of the functional decomposition. Note that in contrast to the problem considered by Apley and Zhu (2020), the constraint itself is of secondary importance. The reason is that we do not aim to approximate a multivariate estimator by (1). The rpf estimator is already in the form of (1). Hence, the constraint does not have an effect on the quality of the estimator. One possible constraint family is that for every and ,

| (20) |

for some weight function . Another option is assuming that for every ,

| (21) |

where is some estimator of the density of , see Hiabu et al. (2022). Observe that the constraints are not an additional assumption on the overall function . The constraint ensures that the functional decomposition is unique for non-degenerated cases. One possibility for the weight in (20) is . With the burden of extra computational cost, one can choose as an estimate of the full design density, see also Lengerich et al. (2020). Compared to the previous example, a computationally more efficient constraint has recently been proposed in Apley and Zhu (2020). Depending on the viewpoint, different choices for may be advantageous. Since the precise constraint is not the focus of this paper, we settled for (20) with the simple constraint which suffices in the sense that it allows us to compare plots of different estimators.

Note that while we obtain an estimator for every component in (1), in general, these estimators do not satisfy the constraint (20). Thus in order to obtain suitable estimators for the components, we must normalize the estimated components without changing the overall estimator. This can be achieved by using an algorithm similar to the purification algorithm given in Lengerich et al. (2020).

Appendix B Example for a Theoretical Random Planted Forest Algorithm

We now describe in more detail the iteration steps of a tree algorithm that motivates the setting in Section 4. As initialisation we set , and for . In iteration steps partitions of with are updated by splitting one of the leaves for one , one along one coordinate . Here in abuse of notation, we write for the set of tuples with coordinates ordered according to the value of and not according to the appearance in the product sign subindices. We now describe step where the leaves are updated. At step one chooses a , an , a and a splitting value . The values are chosen by some random procedure that satisfies the conditions in Section 4. Using these values one splits into and , where , , and . For we set . Then we update the leaf for and by defining with . All other leaves are taken over identically from the last step. Finally, for the chosen tree , the values are updated by averaging residuals over the intervals for . Then for with the estimator can be written as

Because is constant on the set we can rewrite the formula with equal to for as follows

One can easily check that in the notation of Section 4 the estimator is in the form (4).

When one compares the estimator described here and in Section 4 there are three further differences from the rpf algorithm as decribed in the first sections of the main part of the paper. First now we construct trees based on the full sample and not on bootstrap samples. As we have seen in the results of Section 4 bootstrap is not necessary, neither for rate optimality for nor rate improvement by averaging the trees. Our results can be generalized to versions that make use of bootstrap. Second for each ”leaf type” we grow one tree with an own root and do not allow for more trees of the same leaf type that grow in parallel. This modification is made to simplify mathematical theory. Third in each iteration step we update the estimator on all leaves () of ”leaf type” . In our practical implementation of rpf we only did this for the splitted leaf, i.e. for and . From simulations we concluded that the third change is not severe.

Appendix C Further Simulation Results

In this section we provide further results from our simulation study omitted in the main part of this paper. The results are given in Tables 6–16 and further confirm the discussion of Section 5.

| Method | Parameter range |

|---|---|

| xgboost | (if depth = 1), |

| = 2,3,4, | |

| eta = | |

| rpf | (if max_interaction = 1), |

| = 2 (if max_interaction=2), | |

| = , | |

| t_try = | |

| nsplits = , | |

| split_try = | |

| rf | m_try = |

| , | |

| . | |

| sbf | |

| gam | select =TRUE, method = ’REM’ (in sparse models), |

| default settings (in dense models). | |

| BART | , |

| ntree = 50,100,150,200,250,300, | |

| sparsity parameter = 0.6,0.75,0.9. | |

| MARS | , |

| . |

| Method | dim=4 | dim=10 | dim=30 | BI() |

|---|---|---|---|---|

| xgboost (depth=1) | 2.435 (0.157) | 2.542 (0.15) | 2.587 (0.152) | 1 |

| xgboost | 0.374 (0.035) | 0.481 (0.064) | 0.557 (0.089) | |

| xgboost-CV | 0.393 (0.051) | 0.499 (0.058) | 0.563 (0.089) | |

| rpf (max_interaction=1) | 2.36 (0.165) | 2.43 (0.17) | 2.404 (0.145) | 1 |

| rpf (max_interaction=2) | 0.248 (0.038) | 0.327 (0.045) | 0.408 (0.07) | 2 |

| rpf | 0.263 (0.034) | 0.357 (0.044) | 0.452 (0.076) | |

| rpf-CV | 0.277 (0.039) | 0.366 (0.051) | 0.463 (0.083) | |

| rf | 0.432 (0.039) | 0.575 (0.061) | 0.671 (0.08) | |

| sbf | 2.298 (0.168) | 2.507 (0.181) | 3.163 (0.207) | 1 |

| gam | 2.242 (0.172) | 2.311 (0.159) | 2.277 (0.185) | 1 |

| BART | 0.214 (0.03) | 0.223 (0.04) | 0.252 (0.037) | |

| BART-CV | 0.242 (0.043) | 0.276 (0.053) | 0.315 (0.047) | |

| MARS | 0.355 (0.089) | 0.282 (0.038) | 0.414 (0.126) | |

| 1-NN | 2.068 (0.156) | 5.988 (0.624) | 11.059 (0.676) | |

| average | 8.366 (0.43) | 8.086 (0.246) | 8.207 (0.496) | 0 |

| Method | dim=4 | dim=10 | dim=30 | BI() |

|---|---|---|---|---|

| xgboost (depth=1) | 2.176 (0.14) | 2.236 (0.176) | 2.183 (0.136) | 1 |

| xgboost | 0.417 (0.082) | 0.797 (0.16) | 1.381 (0.234) | |

| xgboost-CV | 0.443 (0.078) | 0.872 (0.136) | 1.497 (0.326) | |

| rpf (max_interaction=1) | 2.172 (0.133) | 2.236 (0.164) | 2.199 (0.145) | |

| rpf(max_interaction=2) | 0.416 (0.082) | 1.289 (0.224) | 1.822 (0.208) | |

| rpf | 0.219 (0.035) | 0.556 (0.143) | 1.186 (0.236) | |

| rpf-CV | 0.233 (0.033) | 0.603 (0.163) | 1.313 (0.253) | |

| rf | 0.304 (0.047) | 0.744 (0.305) | 1.295 (0.317) | |

| sbf | 2.249 (0.159) | 2.473 (0.181) | 3.133 (0.22) | 1 |

| gam | 2.161 (0.13) | 2.222 (0.172) | 2.209 (0.168) | 1 |

| BART | 0.168 (0.022) | 0.172 (0.032) | 0.202 (0.021) | |

| BART-CV | 0.192 (0.03) | 0.199 (0.039) | 0.223 (0.025) | |

| MARS | 0.245 (0.088) | 0.831 (0.728) | 0.429 (0.403) | |

| 1-NN | 1.323 (0.117) | 2.642 (0.317) | 4.173 (0.413) | |

| average | 2.187 (0.125) | 2.226 (0.174) | 2.177 (0.146) | 0 |

| Method | dim=4 | dim=10 | dim=30 | BI() |

|---|---|---|---|---|

| xgboost(depth=1) | 2.974 (0.112) | 3.046 (0.12) | 3.098 (0.223) | 1 |

| xgboost | 1.02 (0.152) | 1.28 (0.16) | 1.418 (0.156) | |

| xgboost-CV | 1.049 (0.125) | 1.279 (0.157) | 1.475 (0.185) | |

| rpf (max_interaction=1) | 2.941 (0.117) | 2.942 (0.123) | 2.913 (0.197) | 1 |

| rpf (max_interaction=2) | 0.767 (0.096) | 1.082 (0.139) | 1.34 (0.132) | 2 |

| rpf | 0.745 (0.089) | 1.093 (0.142) | 1.307 (0.113) | |

| rpf-CV | 0.769 (0.101) | 1.167 (0.152) | 1.404 (0.14) | |

| rf | 0.914 (0.091) | 1.237 (0.121) | 1.415 (0.152) | |

| sbf | 2.791 (0.098) | 2.926 (0.12) | 3.756 (0.284) | 1 |

| gam | 2.782 (0.085) | 2.728 (0.105) | 2.793 (0.208) | 1 |

| BART | 0.611 (0.078) | 0.644 (0.106) | 0.67 (0.094) | |

| BART-CV | 0.661 (0.111) | 0.772 (0.173) | 0.791 (0.133) | |

| MARS | 2.306 (0.17) | 2.325 (0.145) | 3.374 (2.716) | |

| 1-NN | 4.559 (0.409) | 8.883 (0.692) | 13.434 (0.674) | |

| average | 8.721 (0.334) | 8.449 (0.229) | 8.638 (0.412) | 0 |

| Method | dim=4 | dim=10 | dim=30 | BI() |

|---|---|---|---|---|

| xgboost (depth=1) | 2.662 (0.078) | 2.616 (0.105) | 2.565 (0.153) | 1 |

| xgboost | 1.034 (0.177) | 1.723 (0.178) | 2.337 (0.378) | |

| xgboost-CV | 1.196 (0.371) | 2.056 (0.3) | 2.481 (0.385) | |

| rpf (max_interaction=1) | 2.682 (0.076) | 2.653 (0.103) | 2.601 (0.155) | 1 |

| rpf (max_interaction=2) | 1.252 (0.164) | 2.268 (0.13) | 2.534 (0.175) | 2 |

| rpf | 0.834 (0.121) | 1.729 (0.156) | 2.337 (0.284) | |

| rpf-CV | 0.886 (0.142) | 1.939 (0.2) | 2.438 (0.246) | |

| rf | 0.805 (0.172) | 1.696 (0.168) | 2.276 (0.306) | |

| sbf | 2.757 (0.094) | 2.893 (0.128) | 3.705 (0.282) | 1 |

| gam | 2.645 (0.096) | 2.617 (0.095) | 2.674 (0.165) | 1 |

| BART | 0.583 (0.074) | 0.632 (0.124) | 0.798 (0.29) | |

| BART-CV | 0.608 (0.106) | 0.73 (0.184) | 1.16 (0.655) | |

| MARS | 2.324 (0.14) | 2.549 (0.296) | 2.522 (0.291) | |

| 1-NN | 3.769 (0.323) | 5.459 (0.419) | 6.247 (0.434) | |

| average | 2.637 (0.092) | 2.59 (0.106) | 2.55 (0.14) | 0 |

| Method | dim=4 | dim=10 | BI() |

|---|---|---|---|

| xgboost (depth=1) | 0.2 (0.035) | 0.662 (0.059) | 1 |

| xgboost | 0.273 (0.028) | 1.233 (0.127) | |

| xgboost-CV | 0.209 (0.043) | 0.673 (0.06) | |

| rpf (max_interaction=1) | 0.162 (0.025) | 0.578 (0.068) | 1 |

| rpf (max_interaction=2) | 0.191 (0.017) | 0.798 (0.097) | 2 |

| rpf | 0.222 (0.019) | 1.052 (0.115) | |

| rpf-CV | 0.178 (0.03) | 0.6 (0.072) | |

| rf | 0.567 (0.044) | 10.527 (0.772) | |

| sbf | 0.071 (0.021) | 0.183 (0.026) | 1 |

| gam | 0.055 (0.012) | 0.171 (0.045) | 1 |

| BART | 0.155 (0.023) | 0.438 (0.053) | |

| BART-CV | 0.165 (0.032) | 0.465 (0.094) | |

| MARS | 0.166 (0.035) | 4.4 (0.36) | |

| 1-NN | 2.05 (0.108) | 11.634 (0.702) | |

| average | 7.71 (0.381) | 18.986 (1.391) | 0 |

| Method | dim=4 | dim=10 | BI() |

|---|---|---|---|

| xgboost (depth=1) | 3.509 (0.266) | 10.108 (0.425) | 1 |

| xgboost | 0.645 (0.053) | 2.895 (0.271) | |

| xgboost-CV | 0.678 (0.042) | 3.013 (0.338) | |

| rpf (max_interaction=1) | 3.408 (0.237) | 9.717 (0.378) | 1 |

| rpf (max_interaction=2) | 0.414 (0.047) | 3.643 (0.349) | 2 |

| rpf | 0.385 (0.034) | 3.357 (0.372) | |

| rpf-CV | 0.413 (0.033) | 3.665 (0.467) | |

| rf | 0.77 (0.034) | 12.265 (1.447) | |

| sbf | 3.42 (0.208) | 9.215 (0.419) | 1 |

| gam | 3.258 (0.227) | 9.212 (0.483) | 1 |

| BART | 0.34 (0.04) | 1.889 (0.324) | |

| BART-CV | 0.354 (0.059) | 2.133 (0.363) | |

| MARS | 0.624 (0.114) | 10.885 (0.635) | |

| 1-NN | 2.516 (0.141) | 17.728 (1.215) | |

| average | 10.696 (0.621) | 26.502 (1.892) | 0 |

| Method | dim=4 | dim=10 | BI() |

|---|---|---|---|

| xgboost (depth=1) | 3.108 (0.197) | 8.091 (0.359) | 1 |

| xgboost | 0.596 (0.063) | 3.888 (0.411) | |

| xgboost-CV | 0.684 (0.069) | 3.974 (0.508) | |

| rpf (max_interaction=1) | 3.119 (0.209) | 8.156 (0.366) | 1 |

| rpf (max_interaction=2) | 0.712 (0.101) | 5.944 (0.324) | 2 |

| rpf | 0.38 (0.049) | 4.747 (0.329) | |

| rpf-CV | 0.395 (0.055) | 4.789 (0.335) | |

| rf | 0.657 (0.074) | 5.784 (0.409) | |

| sbf | 3.385 (0.183) | 9.177 (0.479) | 1 |

| gam | 3.109 (0.216) | 8.183 (0.389) | 1 |

| BART | 0.266 (0.034) | 1.425 (0.183) | |

| BART-CV | 0.299 (0.054) | 1.738 (0.254) | |

| MARS | 0.618 (0.552) | 6.257 (0.824) | |

| 1-NN | 1.482 (0.126) | 7.358 (0.514) | |

| average | 3.156 (0.221) | 8.109 (0.363) | 0 |

| Method | dim=4 | dim=10 | BI() |

|---|---|---|---|

| xgboost (depth=1) | 0.325 (0.068) | 1.095 (0.106) | 1 |

| xgboost | 0.376 (0.085) | 1.437 (0.153) | |

| xgboost-CV | 0.36 (0.073) | 1.187 (0.145) | |

| rpf (max_interaction=1) | 0.321 (0.047) | 1.273 (0.161) | 1 |

| rpf (max_interaction=2) | 0.402 (0.059) | 2.18 (0.139) | 2 |

| rpf | 0.429 (0.067) | 2.804 (0.192) | |

| rpf-CV | 0.326 (0.051) | 1.303 (0.166) | |

| rf | 0.807 (0.104) | 4.051 (0.186) | |

| sbf | 0.588 (0.078) | 1.685 (0.185) | 1 |

| gam | 0.923 (0.15) | 4.405 (0.379) | 1 |

| BART | 0.369 (0.079) | 1.164 (0.093) | |

| BART-CV | 0.39 (0.076) | 1.436 (0.253) | |

| MARS | 1.749 (0.151) | 5.424 (0.304) | |

| 1-NN | 3.822 (0.296) | 11.278 (1.097) | |

| average | 2.5 (0.116) | 6.332 (0.41) | 0 |

| Method | dim=4 | dim=10 | BI() |

|---|---|---|---|

| xgboost(depth=1) | 4.19 (0.238) | 13.112 (0.83) | 1 |

| xgboost | 1.666 (0.159) | 9.327 (0.594) | |

| xgboost-CV | 1.87 (0.312) | 9.407 (0.653) | |

| rpf(max_interaction=1) | 4.19 (0.253) | 12.997 (0.831) | 1 |

| rpf (max_interaction=2) | 1.43 (0.205) | 9.238 (0.648) | 2 |

| rpf | 1.26 (0.165) | 9 (0.64) | |

| rpf-CV | 1.303 (0.171) | 9.441 (0.604) | |

| rf | 1.681 (0.14) | 13.6 (1.247) | |

| sbf | 3.972 (0.254) | 12.234 (0.688) | 1 |

| gam | 3.997 (0.251) | 12.524 (0.858) | 1 |

| BART | 1.01 (0.121) | 7.116 (0.653) | |

| BART-CV | 1.165 (0.224) | 7.897 (0.917) | |

| MARS | 3.595 (0.15) | 16.307 (1.266) | |

| 1-NN | 5.839 (0.649) | 30.736 (1.933) | |

| average | 11.471 (0.498) | 29.623 (2.046) | 0 |

| Method | dim=4 | dim=10 | BI() |

|---|---|---|---|

| xgboost (depth=1) | 3.787 (0.297) | 11.106 (0.546) | 1 |

| xgboost | 1.606 (0.164) | 10.005 (0.531) | |

| xgboost-CV | 1.768 (0.456) | 10.868 (0.648) | |

| rpf (max_interaction=1) | 3.816 (0.259) | 11.246 (0.596) | 1 |

| rpf (max_interaction=2) | 2.005 (0.237) | 10.846 (0.488) | 2 |

| rpf | 1.441 (0.187) | 10.264 (0.433) | |

| rpf-CV | 1.564 (0.214) | 10.582 (0.536) | |

| rf | 1.36 (0.175) | 10.235 (0.424) | |

| sbf | 3.928 (0.262) | 12.129 (0.639) | 1 |

| gam | 3.794 (0.271) | 11.154 (0.573) | 1 |

| BART | 0.972 (0.129) | 6.835 (0.579) | |

| BART-CV | 1.04 (0.158) | 7.208 (0.775) | |

| MARS | 3.541 (0.289) | 11.03 (0.574) | |

| 1-NN | 4.819 (0.475) | 19.802 (1.51) | |

| average | 3.768 (0.283) | 11.03 (0.574) | 0 |