Cap the Gap: Solving the Egoistic Dilemma under the Transaction Fee-Incentive Bitcoin

Abstract

Bitcoin has witnessed a prevailing transition that employing transaction fees paid by users rather than subsidy assigned by the system as the main incentive for mining. The adjustability of reward in the transaction fee-incentive regime makes room for the mining gap, a period of time in which miners turn mining rigs off until transaction fees are sufficient. Obviously, the mining gap aggressively decreases the transaction throughput, weakens the security of Bitcoin, and is further extended by the selfishness of rational users who prone to provide low transaction fees, acting as free-riders. The phenomena of mining gap and free-riding trap Bitcoin system into the egoistic dilemma which is a challenging problem since it involves games not only between users and miners bilaterally, but also among miners and users internally. Hence, in this paper, we first derive the mathematical characteristics of the interplay among users (miners), where the property of strategic complementarity of their actions are analyzed. This enables us to reasonably untangle the antagonism among the homogenous players, making all the users (miners) act as a whole to game with their adversary. Based on this, an incentive mechanism leveraging the zero-determinant (ZD) theory is designed to arm the user-side for inducing the miner-side to power on its rigs early. Our incentive mechanism is featured by sustained ability, since the user-side can drive the miner-side to be an “early bird” without any additional payment in the long run, and fairness, because even the dominant user-side cannot squeeze miner-side financially. To the best of our knowledge, this paper is the first work to cap the mining gap and solve the egoistic dilemma under the transaction fee-incentive Bitcoin. Both theoretical analyses and numerical simulations demonstrate the effectiveness of our proposed mechanism.

Index Terms:

Transaction fee-incentive Bitcoin, multi-miner and multi-user game, supermodular game, zero-determinant theory.I Introduction

Bitcoin is immune to distrustful entities and can expedite confidence by a mining-based consensus mechanism without a third party, heralding a new era in digital cryptocurrency since introduced in 2008 [1, 2, 3]. As incentives for mining, each consensus participant, called miner, may receive two types of rewards, comprising subsidy, the systematically assigned currency, and transaction fees, attached to the transactions from users. Conventional wisdom has long asserted that subsidy dominates the incentive for mining. However, current Bitcoin has witnessed a prevailing transition from the subsidy-incentive regime to the transaction fee-incentive regime as subsidy of Bitcoin is dwindling ($50 in 2008 and $6.25 for now). Since transaction fee is on its way to becoming the material part of the mining reward, a miner’s strategy of when to start up its rig(s) and a user’s strategy of how to bid transaction fee will deviate from the previous belief dramatically. This triggers unprecedented issues that simply do not appear in the subsidy-incentive regime.

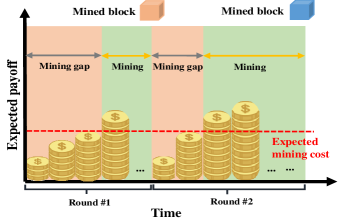

The subsidy-incentive regime can be viewed as a fixed monetary stimulation mechanism since transaction fee is negligible compared to subsidy. Such a fixed incentive regime makes it profitable for miners to power on their rigs from the very beginning of each round, since the earlier the miners start up rigs, the more likely they may get the accounting right due to more trials. Nonetheless, being an “early bird” may be an unfavorable strategy for a miner in the transaction fee-incentive regime. This is because the main source of reward can be adjusted by users in this regime, a rational miner will stop mining until transaction fees are sufficient to assure a larger expected mining payoff than the cost. Such a “no rabbits, no eagles” strategy incurs the mining gap [4, 5], a period of time in which miners turn the mining rigs off to reduce running cost as shown in Fig. 1, rendering no incentives for miners to start up rigs early. Obviously, the “mining gap” phenomenon 1) aggressively decreases the transaction throughput of Bitcoin, daunting its application in high-concurrency fields and 2) makes the blockchain more vulnerable to attacks, such as double spending attack, forking attack, etc., since the computing power required to execute these attacks is significantly decreased when the honest computing power drops, threatening the security of the blockchain.

However, any user is powerless to shrink the mining gap because the starting up strategy of a miner is not driven by any transaction fee unilaterally, but the rewards obtained from all transactions in a block. Aware of this, a rational user might provide low transaction fee, being a free-rider. What’s worse, in this paper we prove mathematically that once there are users who choose to submit low transaction fees as the optimal strategy, the free-riding phenomenon will be overwhelming in Bitcoin quickly, further expanding the mining gap consequently. We name the troubling case where users are prone to offer low transaction fees and miners are reluctant to start up rigs early as the “egoistic dilemma”. Undoubtedly, such a predicament ends up weakening the performance and security of blockchain.

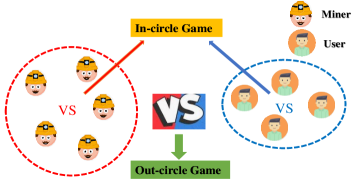

Until now, we are not aware of any previous recognition to present the egoistic dilemma, which motivates our work to address it in this paper. However, it is challenging to get out of the egoistic dilemma in that it is the result of a sophisticated multidimensional game. That is to say, confrontational games exist not only between users and miners bilaterally, but also among miners and users internally. As Fig. 2 shows, we define the interplay among homogenous players (i.e., miner-to-miner or user-to-user) as the in-circle game and the bilateral antagonism between heterogeneous players (i.e., miner-to-user) as the out-circle game. The nature of multidimensionality (i.e., in-circle and out-circle) makes it hard to coordinate the conflicting interests due to the entangled impacts of each player.

To get rid of the egoistic dilemma in the multi-miner and multi-user game, we first derive the mathematical characteristics of the in-circle game via adopting the supermodular game [6], where the optimal strategies of the profit-driven players are analyzed. This enables us to reasonably untangle the antagonism among homogenous players in the in-circle games, making all the users (miners) act as a whole, i.e., the user-side (miner-side), to game with their adversary. Then, we prove that the user-side can utilize the zero-determinant (ZD) strategy [7] to independently set the expected payoff of the miner-side no matter how it acts. Leveraging this powerful ZD strategy, we devise an incentive mechanism to arm the user-side to induce the miner-side to be an “early bird”, narrowing down the mining gap and extricating the players from the egoistic dilemma consequently. To the best of our knowledge, we are the first to present a theoretic study of the mining gap phenomenon and propose an incentive mechanism to solve the egoistic dilemma under the transaction fee-incentive Bitcoin. Conclusively, the contributions of our work can be summarized as follows:

-

•

Reasonable dimension reduction analysis. We prove the interplay among homogenous players can be described as a supermodular game, based on which the actions of players in the in-circle game is derived to be strategic complementary. Such a property reveals that rational homogenous players prefer to behave in unity for maximizing their profits. Aware of this, we can reasonably carry out dimension reduction analysis, transforming the complicated multi-miner and multi-user game into a miner-side and user-side game, highly reducing the analysis complexity.

-

•

Effective ZD-based incentive mechanism. After simplifying the multidimensional game into a miner-side to user-side one, we propose a ZD-based incentive mechanism which can be laid out to hit the egoistic dilemma hurts. Specifically, the proposed mechanism enables the user-side to lure the miner-side to behave as an “early bird”, disengaging both parties from the egoistic dilemma successfully. Both theoretical analyses and numerical simulations demonstrate the effectiveness of our mechanism.

-

•

Sustained ability of motivation. Our ZD-based incentive mechanism empowers the user-side to drive the miner-side to start up rigs early by increasing the short-term payoffs without any additional payment in the long run. This guarantees the user-side to have sustained ability of monetary motivating the miner-side to behave cooperatively.

-

•

Fairness. Even can employ the ZD strategy to dominate the game, the user-side has to pay the highest transaction fee for monetary incentivizing the miner-side to be an “early bird”, implying that the users in the lead cannot squeeze miners financially. The fairness can make the miner-side placed at a disadvantage trust the proposed mechanism, ensuring its sustainability over the long term.

The remainder of the paper is organized as follows. Section II lists the related work and Section III formulates the multi-miner and multi-user game. Based on this, the analysis of the in-circle game and that of the out-circle game are respectively conducted in Sections IV and V. In Section VI, we propose the novel incentive mechanism in light of the ZD theory and testify its effectiveness theoretically. The experimental simulations are carried out in Section VII and Section VIII concludes our paper finally.

II Related Work

To date, transaction fee-incentive Bitcoin has been a largely under-explored domain and research in this field is still in its infancy. In 2016, Carlsten et al. [4] first postulated that when transaction fee dominates the mining reward, immediately after a block has been mined, there is zero expected income but nonzero operation cost for the miner [8]. Thus, rational miners would stop mining in this case, resulting in the so-called “mining gap”. Such a phenomenon presents new strategy pattern of the miners, that is, strategically adjust their starting up times of mining for obtaining profitable payoffs, and pioneers new research direction for the transaction fee-incentive Bitcoin.

Inspired by this, Tsabary et al. [5] studied miners’ strategies in choosing different starting up times by establishing a “gap game”, in which the miner’s utility is comprehensively modeled by considering the expected income and cost. Based on this, they concluded that such a gap forms well before fees are the only incentive. Considering that [5] was carried out under the quasi-static state assumption, Di et al. [8] analyzed a dynamic game with more realistic hypotheses. Consequently, they mentioned that the decentralization of blockchain is heavily threatened in this case. In addition, [9] and [10] illustrated the above game differently via adopting “consensus game” and stochastic game, respectively. This provides us another view of investigating the miners’ strategic actions as well as the stability of blockchain. Moreover, Arenas et al. [10] put forward that the undercutting strategy is a better option for the miners than the honest strategy, i.e., mining on the longest chain, under the transaction fee-incentive regime, which is consistent with the statement in [4]. While Gong et al. in [11] pointed out that contrary to the primary belief, the undercutting behavior is not always beneficial to miners, especially when other miners are aware of these kinds of actions.

In summary, the above studies give the first attempt to analyze the strategy pattern on the transaction fee-incentive regime. However, none of them considers the impact of the users’ strategy on miners but only studies the miners’ behaviors independently, not to mention the in-depth analysis of our proposed egoistic dilemma. Hence, our work fills the gap in addressing the dilemma of the miners and users, providing the first incentive mechanism to cap the mining gap in the transaction fee-incentive Bitcoin.

III Problem Formulation

In this paper, we consider a Bitcoin system that consists of a set of miners (denoted as ) competing for mining blocks and a set of users (denoted as ) bidding transaction packaging. That is, a multi-miner and multi-user game is employed to depict the real Bitcoin system. Following the assumption made in [4, 5], we suppose each miner has one rig, and all rigs are assumed to be identical which means they share the same operation cost and computing power for simplicity111Notably, our scheme is also applicable to the case where each miner has multiple or heterogeneous rigs. One can easily extend our model by appropriately adjusting and defined in the following context.. Primary parameters used in this section are listed in Table 1.

III-A Strategy Model

For any miner , it can choose a starting up time to launch mining, where represents the duration from the time when the previous block is generated to that when the current block is created. We denote the strategy of miner as , in which . It is obvious that the earlier miner starts up its rigs, the smaller is and the larger is. Let be the strategy of any arbitrary user , which represents the bidding fee it offers, with as the maximum value. In order to analyze the strategies of miners and users, we introduce the following definition.

Definition 1 (Lattice [6]).

Set is a lattice if the following three conditions are satisfied:

-

•

S is a partially ordered set.

-

•

S has the least upper bound or the greatest lower bound.

-

•

, if we define and , then the join and meet of each pair should be contained in .

Theorem 1.

The strategy space of miner and that of user , i.e., , are lattices.

Proof:

We can prove is a lattice from two steps considering that the second condition is met because of . Firstly, should be reflexive, antisymmetric, and transitive in order to be a partially ordered set; secondly, the join and meet of each pair in belong to .

According to the definition of , all elements are ordered in real line. Hence, , we have (reflexive); if , then (antisymmetric); if , then (transitive). Thus, is a partially ordered set. Besides, the join and meet of satisfy and [6]. Hence, is a lattice. We omit the proof of for reducing repetition since they are very similar.

| , | Set of miners and users |

| Miner ’s starting up time of its rig | |

| The time duration of each round | |

| The time when a block is mined | |

| Rate parameter of | |

| Maximum fee the user may offer | |

| , | Miner and user ’s strategy |

| Vector of strategies of all miners and users | |

| Vector of strategies of all users expect | |

| , | Miner and user ’s strategy space |

| , | Expected payoff of miner and user |

| , | Number of active rigs of the system and of miner at time |

| The mining duration of active rigs in the system | |

| Profit of mining/being packaged for the miner/user | |

| Cost of mining/bidding for the miner/user | |

| The first order partial derivatives of | |

| Positive scaling parameters |

III-B Payoff Model

According to the above analyses, the expected payoff of miner can be defined as

| (1) |

In (1), and express the probability and profit of miner when a block is successfully mined at time . According to [5], can be formulated as a shift-exponentially distribution. That is,

| (2) |

where and present the number of active rigs in the system at time and the mining duration of them until time . Besides, is a rate parameter which is related to the mining difficulty of the system and we denote as the vector of all the rigs’ starting up strategies. Obviously, both and are monotonically increasing with the starting up strategy, thus we set and .

As for miner ’s profit, can be devised as the difference between the income and expense, namely,

| (3) |

where is the number of active mining rig of miner at time , thus ; the ratio between and indicates the success mining rate of miner . Additionally, and show the respective profit and cost of a successful block, in which denotes all the users’ bidding strategies. It is evident that has a monotonically increasing relationship with regard to , thus we set . And , are scaling parameters.

With a comparable structure, the expected payoff of user can be defined as

| (4) |

in which represents the probability that transaction of user is packaged at time by submitting transaction fee as while others offering , and denotes the profit of user . To be specific, can be calculated by , which satisfies a simple rule that the probability of being packed rises with the increase of , but decreases as other users’ fees lift. As for user ’s profit when its transaction is selected into a mined block, is designed as

| (5) |

where means the income of user and is an endogenous variable showing packaging delay or other impact factors that may influence the user’s utility. Besides, presents the cost of the user which is monotonically increasing with , hence we set . And , are scaling parameters.

IV Analysis of the In-Circle Game

As mentioned above, the multi-miner and multi-user interaction in Bitcoin can be further divided into two kinds of games, i.e., the in-circle and out-circle games. In this section, we focus on the in-circle game to investigate the interplay of homogenous players. To that aim, we establish a supermodular game-based model to elaborately describe the actions of in-circle players. After that, the mathematical characteristics of players’ strategies are figured out, which can be well captured by the term strategic complementarity [12]. This allows us to reasonably simplify the multi-miner and multi-user game to a bilateral confrontation game, based on which, an in-depth inspection stressing the interaction between heterogeneous players will be conducted in the next section. In the following, we first introduce the definition of supermodular game.

Definition 2 (Supermodular Game [6]).

A game with a set of players , strategy space and payoff function (denoted as ) is a supermodular game if for each player :

-

•

the strategy space is a lattice.

-

•

the payoff function is continuous in for fixed , where and respectively denote the strategy of player and the strategy vector of other players except .

-

•

has increasing differences in (), i.e., .

Theorem 2.

The in-circle game among any miner and its peers, denoted as , is a supermodular game if and hold.

Proof:

We prove this theorem according to Definition 2. 1) Initially, the strategy space of miner , i.e., , is a lattice in light of Theorem 1; 2) it is clear that , when is fixed, the left and right limits of are equal, implying that the payoff function of miner is continuous in ; 3) we proceed to prove that , in the following.

Let . To prove , we need to testify in light of the differentiability property in [13, 14]. Further, if holds, the above inequation can be proved by utilizing the integral property in [14]. Hence, we are going to find the conditions to meet . In detail, the explicit mathematical form of can be written as:

| (6) | ||||

Next, we divide (6) into two parts for convenience of expression, recognized as . Then, the second order partial derivatives of and are respectively

| (7) | ||||

| (8) | ||||

Thus, if and , we have . Therefore, Theorem 2 is proved.

Theorem 3.

The in-circle game among any user and its peers, denoted as , is a supermodular game when is satisfied.

Proof:

The proof is similar to that of Theorem 2. It can be easily obtained that satisfies the first two conditions of Definition 2 to be a supermodular game. Thus, we focus on the third one i.e., . Set , we have

| (9) | ||||

Hence, when , the theorem holds.

According to [6, 15, 12], supermodular game () indicates that the marginal payoff of any miner (user ) can be increased if all players in the in-circle game behave in unity. That is to say, when other miners select late starting up strategies, it becomes more profitable for miner to power on its rigs lately and vice versa; similarly, if other users bid low transaction fees, offering a low transaction fee as well will benefit user and vice versa. Such a complementary strategy occurs in homogenous players is termed as strategic complementarity [12] and we can use another metaphor, i.e., theatre effect, to illustrate it more intuitively: when most of the audience stand up to watch a movie, the best response of the other is to stand up as well, keeping the same pace with others.

V Analysis of the Out-Circle Game

The strategic complementarity of the in-circle game presents that a rational player should act synchronously with others for maximizing its payoff. As a result, once there are users who choose to provide low transaction fees and become free-riders, all other users will select the same strategy, enlarging the mining gap consequently, as mentioned in Section I. However, the strategic complementarity is a double-edged sword since it can serve to reshape the out-circle game from the multi-miner and multi-user game to the miner-side and user-side one, in which all miners share one strategy and all users own one strategy due to the synchronous actions among homogenous players. In such a game, the payoff functions of the miner-side and user-side can be devised as:

| (10) |

| (11) |

Specifically, and are profit functions for the miner-side and user-side, which are monotonically increasing with the user-side’s bidding devotion and the miner-side’s starting up strategy . Besides, and are the cost functions, sharing the increasing relationship with variables and , respectively. And are positive scaling parameters. Additionally, compared with (1) and (4), we omit the probabilities of mining blocks successfully of the miner-side and being packaged of the user-side, i.e., and in (10) and (11). This is because no matter which miner mines a block and which user’s transaction is selected, it means that the miner-side mines successfully and the transactions of the user-side are packaged. That is to say, and in this case. The parameters used in this section is summarized in Table II.

| Strategy of the miner-side and user-side | |

| Strategy space of the two sides | |

| , | Payoff function of the two sides |

| Profit function of the two sides | |

| Cost function of the two sides | |

| Positive scaling parameters | |

| Mixed strategy of the user-side in round | |

| Mixed strategy of the miner-side in round | |

| Markov transition matrix in round | |

| Joint transition probability in round | |

| Expected payoff of the two sides in round | |

| The number of partitions of and | |

| The partition interval of and | |

| Payoff vector of the two sides in the discrete form | |

| Mixed strategy of the user-side and miner-side in discrete form |

In the out-circle game, the user-side sets its transaction fee as the bidding strategy first. After observing current transaction fee, the miner-side chooses a profitable starting up strategy subsequently. Note that the game is led by the user-side and then followed by the miner-side, it is therefore called a sequential game.

Theorem 4.

An egoistic dilemma exists in the sequential game between the user-side and miner-side.

Proof:

To begin with, holds because both and are positive. This means the payoff of the user-side is inversely proportional to its strategy , thus offering the minimum fee no matter what strategy the miner-side selects is the best strategy of the user-side. Comparatively, we also obtain because of and . Such a reverse relationship between the miner-side’s payoff and its strategy results in the best response of the miner-side being . Hence, the equilibrium of the game is , which is an unexpected outcome for the players compared with the state . Accordingly, an egoistic dilemma exists in the sequential game between the user-side and miner-side.

Aware of the above theorem, we can state that the user-side and miner-side may be trapped in the egoistic dilemma, where the user-side is not willing to submit high transaction fee and the miner-side is reluctant to start up rigs early. In the short run, such egoistic strategies decrease social welfare for both parties, and meanwhile, it may lead to low efficiency or even break down the Bitcoin system in the long run. To address this problem, we equip the user-side with a novel incentive mechanism to lure the miner-side’s early starting up strategy. The reason why we facilitate the user-side instead of the miner-side is that in the sequential game, it is the user-side that acts first, showing its advantages in influencing the miner-side’s action. Hence, by teaching the miner-side to get the cognition that starting up earlier may bring about higher payoffs, the user-side is capable of incentivizing the interest-driven miner-side to wake up rigs early. Such an aim can be greatly achieved by leveraging the revolutionary sequential ZD strategy presented in [16, 7, 17].

The classical ZD strategy [7] offers valuable insights to understand the Markov games, which enables the ZD adopter can unilaterally set the expected payoff of its adversary no matter how the adversary acts. Such a capability in controlling the expected payoff of others allows us to enact an incentive mechanism to induce the miner-side to be an “early bird”. To that aim, we need to answer two fundamental questions:

-

•

can the user-side be a ZD adopter?

-

•

what should the user-side do to incentivize the miner-side to start up rigs at the earliest time?

To answer the first question, we employ the Markov game to model the interaction between the user-side and miner-side. We first assume that the user-side makes decisions based on the outcomes of previous rounds, while the miner-side sets its strategy after knowing the user-side’s strategy in this round. In light of this, we define the mixed strategy of the user-side in round as , which denotes the probability density222The reason why we use probability density rather than probability is that the strategy spaces of our scenario are continuous. of offering as the bidding fee when the previous outcome is and holds. Comparably, the mixed strategy of the miner-side is thereby described as , expressing the probability density of starting up rigs with strategy after realizing the user-side’s fee is provided as in round and also, we have . Hence, the Markov matrix representing the state transition probability density from round to can be deduced as . Accordingly, the joint probability density that the user-side adopting strategy while the miner-side choosing strategy in round can be denoted as . Therefore, the expected payoffs of the user-side and miner-side in round can be presented as:

| (12) |

| (13) |

Subsequently, we divide the strategy spaces of the miner-side and user-side as and with sufficiently small and large enough , satisfying and . Thus, the strategy spaces can be approximated to continuous ones if and . Accordingly, the payoffs of the two players can be partitioned as and . Based on this, we can rewrite the mixed strategy of the user-side in the discrete form as for round , in which , representing the probability of submitting as the bidding fee in round when the user-side provides the payment as while the miner-side choosing strategy in the previous round. Similarly, the mixed strategy of the miner-side can be thereby depicted as in round , where , denoting the probability of choosing strategy currently with knowing as the user-side’s strategy.

Based on the partitioned strategy spaces and payoffs above, we can conclude that the user-side can control the expected payoff of the miner-side through being a ZD adopter, which is demonstrated in the following theorem.

Theorem 5.

When the user-side sets its strategy as , the expected payoffs of the user-side and miner-side meet a linear relationship, i.e., , in which are coefficients and satisfies

| (14) |

Proof:

Firstly, the Markov matrix can be explicitly expressed as , where represents the vector consisting of the transition possibilities from all the previous states to current state , i.e., . According to the ZD strategy [7], if the stationary vector of is , then we can obtain and where with as the unitary matrix. In light of Cramer’s law, we get , where is the adjugate matrix of . Hence, we can define an arbitrary -vector, i.e., , and conduct dot product of the stable vector with to obtain a new Markov matrix after elementary column transformation [7, 16], which is

| (15) |

From (15), one can easily get that the penultimate column is solely determined by the user-side, which can be denoted as . Thus, when the user-side sets its strategy, i.e., , equal to the last column, we can obtain since there are two identical columns in a determinant. Further, when , holds [7]. Thus, the user-side is capable of setting strategy equal to and resulting in a linear relationship between the expected payoffs of the user-side and miner-side, that is, . Therefore, we obtain Theorem 5.

Now, we can answer the first question by stating that the user-side is capable of being a ZD adopter by appropriately setting its strategy according to Theorem 5, so as to unilaterally determine the expected payoff of the miner-side as when is set as 0. It is also worth to note that in sequential games, only the leader can employ the powerful ZD strategy to control the outcome of the game while the follower is not adequate to do so [16].

VI ZD-based Incentive Mechanism

In this section, we are going to answer the second question by equipping the user-side with a ZD-based incentive mechanism. To begin with, we consider the miner-side to be brainy whose strategy is adaptive and iterative rather than fixed and permanent. That is to say, the rational miner-side may learn the utilities of different strategies and adjust its actions towards the best strategy which leads to favorable payoffs while keeping away from the ones that trigger disadvantageous payoffs. Such a property in strategy selection is rooted in the players since they are born with the nature of “seeking profit and avoiding harm”, which is similar to the principle of “survival of the fittest” in biological evolution. Hence, we consider an evolutionary miner-side in this paper, who can reasonably adjust its strategy to maximize its payoff by evaluating the corresponding payoffs under different strategies.

We give an example of the evolutionary strategy inspired by [18, 19] and claim that other evolutionary strategies shown in [20] and so on share the same mathematical core. Let the probability that the miner-side starts up rigs at the earliest time in round be , then such a probability in round iterates as follows:

| (16) |

In (16), indicates the expected payoff of the miner-side in round when its strategy is , which can be deduced by , and represents the frequency of the user-side choosing as its strategy in round . Besides, presents the total expected payoff of the miner-side in round , calculated by , and is estimated by the frequency of the miner-side setting as its strategy in round . In addition, is the expected payoff when the miner-side chooses as its strategy, and is defined as .

In the following, we devise a ZD-based incentive mechanism for the user-side to drive the miner-side to be an “early bird”, which is illustrated in Algorithm 1. Conclusively, the essence of our mechanism is to reward the miner-side with a higher payoff when it starts up rigs at the earliest time, yet penalizing it by setting its payoff as a lower one if it begins to mine lately. Leveraging such a market regulation mechanism, the user-side can make the miner-side perceive the positive relationship between the earlier starting up strategy and the more profitable utility, encouraging the miner-side to be the earliest strategy adopter eventually.

We elaborate the pseudo-code in Algorithm 1 detailedly as follows. Considering that the user-side acts first to set the miner-side’s payoff without seeing its strategy, it is necessary for the user-side to predict the possible strategy of its opponent in each round. Hence, we set a preliminary phase containing rounds to estimate the state transition probability matrix as the basis of predicting the miner-side’s action, in which denotes the probability that the miner-side transits from previous strategy to current strategy . To be specific, in round can be calculated by , where and respectively refer to the probability of choosing strategy and in round .

After obtaining the prediction of , the user-side will set the miner-side’s payoff for each round accordingly. To be concrete, the user-side will initially reward the miner-side proportionally to its estimated average probability of being an “early bird”, i.e., and set the parameter (Line 1). After that, when the previous strategy of the miner-side is regarded as (Line 3), then whether the miner-side is an “early bird” or not can be deduced from the following two cases: if the transition probability from the previous strategy to the earliest strategy is no less than that of any other possible transitions, i.e., (Line 4), then the miner-side can be deemed as an “early bird”, who will be rewarded with a higher payoff by setting , where and is a scaling parameter (Line 5-6). Note that the higher is, the more increment of will have, and the higher reward the miner-side could possess, until the maximum value of the miner-side could obtain. On the other hand, if , such that (Line 7), the user-side in this case may utilize the ZD strategy to penalize the miner-side for giving a lower payoff by making , in which and is a scaling parameter (Line 8-9). It is worth to note that the lower is, the higher is and the lower payoff the miner-side is rewarded, until the minimum value it could possess. When each round ends, the user-side will collect the game results and recalculate for a more precise estimation of the miner-side’s next action (Line 12-14). The above procedures repeat until rounds are carried out.

Theorem 6 (Effectiveness).

For any evolutionary miner-side who is encouraged by the ZD-based incentive mechanism, its probability of choosing the earliest starting up strategy becomes to 1 at last, i.e., .

Proof:

According to (16), increases only when . Thus, we proceed to prove from two cases, where the miner-side is recognized as an “early bird” or not.

Case 1): if the miner-side is regarded as an “early bird” in round with strategy , then the user-side will set . Under this case, the miner-side’s probability of choosing the earliest strategy and the corresponding expected payoff come to

and

Since the probability of a miner-side’s strategy is not higher than the sum of possibilities of all the non-earliest actions , holds. Therefore, we have

When , because of and , turns to

| (17) |

Case 2): when the miner-side’s strategy in round is predicted as , the miner-side’s expected payoff is thereby controlled as . Accordingly, the miner-side’s probability of selecting to be an “early bird” or not are respectively

and

with

Hence, we can get

when , on account of , we obtain

Since , remains unchanged and rises. Besides, we have

| (18) | ||||

Hence, we have and . Consequently, we have .

To sum up, Case 1) indicates raises while holds unchanged as the round goes up; Case 2) suggests that decreases with keeping stable. Hence, , such that . Based on which, turns to

Hence, when is satisfied, equals to , resulting in the inevitability of the miner-side being an “early bird”. Therefore, we obtain Theorem 6.

In light of Theorem 6, one may raise a question that if the user-side is so powerful to guide the miner-side to be an “early bird”, will it be possible to squeeze the miner-side financially by offering low transaction fee to achieve greedy purpose? We address the above issue by presenting the following theorem.

Theorem 7 (Fairness).

When the miner-side is driven to choose the earliest starting up strategy, the only rational strategy of the user-side who employs the ZD strategy is to provide the highest transaction fee.

Proof:

| (19) |

We can use and to describe and as

| (20) |

Hence, the range of can be derived as [7, 16]. Accordingly, when and , gets the maximum, i.e., = . The upper bound demonstrates that when the miner-side is lured to select the earliest starting up strategy, the user-side will set its strategy as to reward the miner-side with the maximum expected payoff. Thus, the proposed ZD-based incentive mechanism makes no room for the user-side to behave greedily through financially squeezing the miner-side, showing its fairness to both sides.

Theorem 8 (Sustained ability of motivation).

In the long run, the actual payoff of the miner-side is equivalent to .

Proof:

Based on Theorem 6 and Theorem 7, we can conclude that such that , the probability that the miner-side starts up rigs at the earliest time is 1, i.e., . In this case, the expected payoff of the miner-side is . Accordingly, the actual payoff of the miner-side can be derived as the average of the expected payoffs in which and where . Hence, can be calculated as

| (21) |

Notably, Theorem 7 and Theorem 8 conclusively indicate that the maximum payoff of the miner-side in each round which is controlled by the user-side, i.e, equals to the actual payoff of the miner-side over the long run, i.e., . This reveals that only through offering transaction fee generously as in each round, is the user-side capable of incentivizing the miner-side to be an “early bird” in the long run without any additional payment. Moreover, does not exceed the maximum payment the user-side can afford, which ensures the user-side to have sustained ability to monetarily incentivize the miner-side to behave collaboratively.

VII Experimental Evaluations

In this section, we testify the effectiveness of the proposed ZD-based incentive mechanism experimentally. To begin with, suppose the profit functions and cost functions of the miner-side and user-side are defined to satisfy the linear relationship for simplicity with because current Bitcoin subsidy is set as , , , and . And the scaling parameters are , and . Notably, other parameter settings and multiple monotonically increasing functions have been tested and derive very similar results, thus we omit to present them to avoid redundancy. Further, we partition the continuous strategy spaces and into 10 sub-spaces in order to present a precise statistical calculation of the miner-side’s state transition probability matrix with . Note that the number of the preliminary phase is set as and we carry out rounds for the simulation process. However, we only depict the game results of the first several rounds to get a clearer observation of the experimental trends. Each simulation is repeated 50 times so as to gain the average value for statistical confidence.

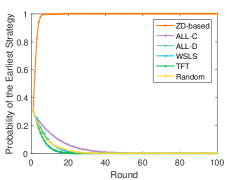

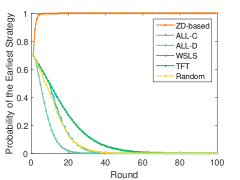

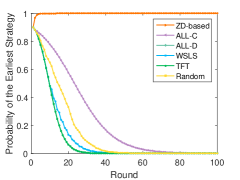

Fig. 3 shows the evolutions of the earliest starting up probabilities of the miner-side when the user-side respectively adopts the proposed ZD-based incentive mechanism and five classical strategies, i.e., all cooperation (ALL-C), all defection (ALL-D), win-stay-lose-shift (WSLS), tit-for-tat (TFT) and random strategy. In ALL-C (ALL-D) strategy, no matter what strategy employed last round, the user-side chooses the highest (lowest) bidding strategy for each round; in WSLS strategy, the user-side keeps the same action as the previous one if it creates a beneficial payoff, otherwise, it chooses the opposite strategy; in TFT strategy, the user-side selects the opposite action to that of the miner-side previously; in random strategy, the user-side sets its strategy arbitrarily for each round. We set the initial probabilities that the miner-side chooses the earliest starting up strategy and the user-side offering the maximal transaction fee as and , respectively. Here, denotes an 11-dimensional vector with all components 0.3, so does for . One can conclude that the probability of choosing the earliest strategy of the miner-side can always reach when the user-side employs the ZD-based incentive mechanism no matter what initial probabilities are set. However, other classical strategies fail. Such a superiority undoubtedly demonstrates the effectiveness of our ZD-based incentive mechanism in driving the miner-side to be an “early bird”.

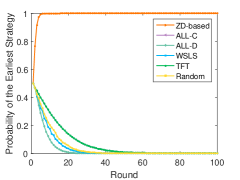

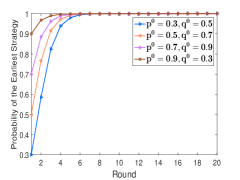

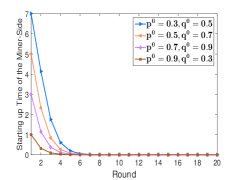

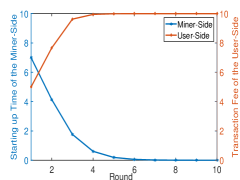

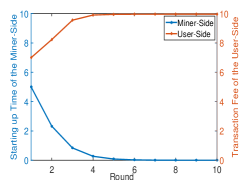

Fig. 4 displays the change in the probability of powering on rigs at the earliest time (Fig. 4 (a)) and the starting up time (Fig. 4 (b)) of the miner-side under different initial probability settings when fighting with the user-side who adopts the ZD strategy. From this, we can state that 1) the probability of choosing the earliest starting up strategy will eventually tend to 1; and 2) the starting up time of the miner-side decreases continuously until , both implying that the miner-side is motivated to mine at the very beginning of each round finally. This result more directly validates the efficacy of our mechanism.

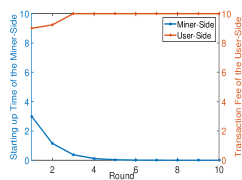

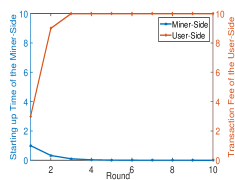

Fig. 5 demonstrates that when the starting up time of the miner-side decreases with the help of the ZD strategy, the user-side is also confined to offer the highest transaction fee. This is an indication of the fairness of our ZD-based incentive mechanism, in which the ZD adopter has no way to squeeze the miner-side financially even can dominate the game.

VIII Conclusion

In this work, we design a ZD-based incentive mechanism to cap the mining gap and address the egoistic dilemma presented in the transaction fee-incentive Bitcoin. We start by modeling the in-circle games among homogenous players as supermodular games and derive the strategic complementarity consequently. Based on this, the multi-miner and multi-user game can be simplified as a miner-side and user-side game. In such a game, we devise a powerful ZD-based incentive mechanism for the user-side to coerce the miner-side to be an “early bird”, making both players get rid of the egoistic dilemma successfully. Our mechanism has the sustained ability of motivation and is featured by fairness, showing its vitality over the long run.

Acknowledgment

This work has been supported by National Key R&D Program of China (No. 2019YFB2102600), National Natural Science Foundation of China (No. 61772080, 61672321, 61771289, 61832012, and 62072044), the Blockchain Core Technology Strategic Research Program of Ministry of Education of China (No. 2020KJ010301), BNU Interdisciplinary Research Foundation for the First-Year Doctoral Candidates (No. BNUXKJC2022), the International Joint Research Project of Faculty of Education, Beijing Normal University, and Engineering Research Center of Intelligent Technology and Educational Application, Ministry of Education.

References

- [1] S. Nakamoto et al., “Bitcoin: A peer-to-peer electronic cash system.(2008),” 2008.

- [2] H. Shi, S. Wang, and Y. Xiao, “Queuing without patience: A novel transaction selection mechanism in blockchain for iot enhancement,” IEEE Internet of Things Journal, 2020.

- [3] H. Shi, S. Wang, Q. Hu, X. Cheng, J. Zhang, and J. Yu, “Fee-free pooled mining for countering pool-hopping attack in blockchain,” IEEE Transactions on Dependable and Secure Computing, 2020.

- [4] M. Carlsten, H. Kalodner, S. M. Weinberg, and A. Narayanan, “On the instability of bitcoin without the block reward,” in Proceedings of the 2016 ACM SIGSAC Conference on Computer and Communications Security, 2016, pp. 154–167.

- [5] I. Tsabary and I. Eyal, “The gap game,” in Proceedings of the 2018 ACM SIGSAC conference on Computer and Communications Security, 2018, pp. 713–728.

- [6] D. M. Topkis, Supermodularity and complementarity. Princeton university press, 1998.

- [7] W. H. Press and F. J. Dyson, “Iterated prisoners dilemma contains strategies that dominate any evolutionary opponent,” Proceedings of the National Academy of Sciences, vol. 109, no. 26, pp. 10 409–10 413, 2012.

- [8] Y. Liu, J. Ke, Q. Xu, H. Jiang, and H. Wang, “Decentralization is vulnerable under the gap game,” IEEE Access, vol. 7, pp. 90 999–91 008, 2019.

- [9] L. Di, G. X. Yuan, and T. Zeng, “The consensus equilibria of mining gap games related to the stability of blockchain ecosystems,” The European Journal of Finance, pp. 1–22, 2020.

- [10] M. Arenas, J. Reutter, E. Toussaint, M. Ugarte, F. Vial, and D. Vrgoč, “Cryptocurrency mining games with economic discount and decreasing rewards,” in 37th International Symposium on Theoretical Aspects of Computer Science (STACS 2020). Schloss Dagstuhl-Leibniz-Zentrum für Informatik, 2020.

- [11] T. Gong, M. Minaei, W. Sun, and A. Kate, “Undercutting bitcoin is not profitable,” arXiv preprint arXiv:2007.11480, 2020.

- [12] J. I. Bulow, J. D. Geanakoplos, and P. D. Klemperer, “Multimarket oligopoly: Strategic substitutes and complements,” Journal of Political economy, vol. 93, no. 3, pp. 488–511, 1985.

- [13] Z. Wang, “Generalization of integral derivatives of functions with variables,” College Mathematics, vol. 21, no. 3, pp. 104–105, 2005.

- [14] C. Y. Jixiu Chen, Mathematical Analysis. Higher Education Press, 2010.

- [15] P. Milgrom and J. Roberts, “Rationalizability, learning, and equilibrium in games with strategic complementarities,” Econometrica: Journal of the Econometric Society, pp. 1255–1277, 1990.

- [16] Q. Hu, S. Wang, P. Ma, X. Cheng, W. Lv, and R. Bie, “Quality control in crowdsourcing using sequential zero-determinant strategies,” IEEE Transactions on Knowledge and Data Engineering, vol. 32, no. 5, pp. 998–1009, 2019.

- [17] S. Wang, H. Shi, Q. Hu, B. Lin, and X. Cheng, “Moving target defense for internet of things based on the zero-determinant theory,” IEEE Internet of Things Journal, vol. 7, no. 1, pp. 661–668, 2019.

- [18] X. Liu, W. Wang, D. Niyato, N. Zhao, and P. Wang, “Evolutionary game for mining pool selection in blockchain networks,” IEEE Wireless Communications Letters, vol. 7, no. 5, pp. 760–763, 2018.

- [19] J. M. Smith, Evolution and the Theory of Games. Cambridge university press, 1982.

- [20] R. M. Dawes, A. J. Van De Kragt, and J. M. Orbell, “Not me or thee but we: The importance of group identity in eliciting cooperation in dilemma situations: Experimental manipulations,” Acta Psychologica, vol. 68, no. 1-3, pp. 83–97, 1988.

![[Uncaptioned image]](/html/2012.14561/assets/x13.png) |

Hongwei Shi received her B.S. degree in Computer Science from Beijing Normal University in 2018. Now she is pursuing her Ph.D. degree in Computer Science from Beijing Normal University. Her research interests include blockchain, game theory and combinatorial optimization. |

![[Uncaptioned image]](/html/2012.14561/assets/x14.png) |

Shengling Wang is a full professor in the School of Artificial Intelligence, Beijing Normal University. She received her Ph.D. in 2008 from Xi an Jiaotong University. After that, she did her postdoctoral research in the Department of Computer Science and Technology, Tsinghua University. Then she worked as an assistant and associate professor from 2010 to 2013 in the Institute of Computing Technology of the Chinese Academy of Sciences. Her research interests include mobile/wireless networks, game theory, crowdsourcing. |

![[Uncaptioned image]](/html/2012.14561/assets/x15.png) |

Qin Hu received her Ph.D. degree in Computer Science from the George Washington University in 2019. She is currently an Assistant Professor in the department of Computer and Information Science, Indiana University - Purdue University Indianapolis. Her research interests include wireless and mobile security, crowdsourcing/crowdsensing and blockchain. |

![[Uncaptioned image]](/html/2012.14561/assets/x16.png) |

Xiuzhen Cheng [F] received her M.S. and Ph.D. degrees in computer science from the University of Minnesota Twin Cities in 2000 and 2002. She is a professor in the Department of Computer Science, George Washington University, Washington, DC. Her current research interests focus on privacy-aware computing, wireless and mobile security, dynamic spectrum access, mobile handset networking systems (mobile health and safety), cognitive radio networks, and algorithm design and analysis. She has served on the Editorial Boards of several technical publications and the Technical Program Committees of various professional conferences/workshops. She has also chaired several international conferences. She worked as a program director for the U.S. National Science Foundation (NSF) from April to October 2006 (full time), and from April 2008 to May 2010 (part time). She published more than 170 peer-reviewed papers. |

![[Uncaptioned image]](/html/2012.14561/assets/jianhuihuang.jpg) |

Jianhui Huang received the Ph.D. degree in computer science from Xi an Jiaotong University, Xi an, China, in 2009. He is currently an Associate Professor with the Institute of Computing Technology, Chinese Academy of Sciences, Beijing, China. His current research interests include the mobile applications, opportunistic network, and cloud computing. |