Credit Freezes, Equilibrium Multiplicity, and Optimal Bailouts in Financial Networks.

Abstract

We analyze how interdependencies in financial networks can lead to self-fulfilling insolvencies and multiple possible equilibrium outcomes. We show that multiplicity arises if and only if there exists a certain type of dependency cycle in the network, and characterize banks’ defaults in any equilibrium. We use this analysis to show that finding the cheapest bailout policy that prevents self-fulfilling insolvencies is computationally hard (and hard to approximate), but that the problem has intuitive solutions in specific network structures. Bailouts have an indirect value as making a bank solvent improves its creditors’ balance sheets and reduces their bailout costs. We show that an algorithm that leverages these indirect benefits ensures systemic solvency at a cost that never exceeds half of the overall shortfall. In core-periphery networks, it is often optimal to bail out peripheral banks first as opposed to targeting core banks directly.

JEL Classification Codes: D85, F15, F34, F36, F65, G15, G32, G33, G38

Keywords: Financial Networks, Systemic Risk, Financial Crisis, Credit Freeze, Default Risk, Financial Interdependencies, Bailouts, Equilibrium Multiplicity

1 Introduction

Today’s financial sector is characterized by strong interdependencies, with large amounts of capital circulating among financial firms. For instance, Duarte and Jones (2017) estimate that 23% of the assets of bank holding companies come from other financial intermediaries, as well as 48% of their liabilities - almost half.111See their Tables 1 and 2. The difference reflects the fact that many other types of financial institutions that are not BHCs (e.g., Real Estate Investment Trusts, insurance companies, etc.) have accounts of cash, money markets, and other deposits held at BHCs that count on the liability side. The value of any financial firm then depends on the payments it gets from its claims on other firms, which might themselves depend on the values of yet other firms, creating rich interdependencies between firms’ balance-sheets.

The literature on financial contagion has studied how interbank obligations enable a shock in one part of the system to spread widely, and how this contagion is magnified if banks incur costs upon default.222See, for instance, Kiyotaki and Moore (1998), Eisenberg and Noe (2001), Gai and Kapadia (2010), Elliott, Golub, and Jackson (2014), Acemoglu, Ozdaglar, and Tahbaz-Salehi (2015), and Jackson and Pernoud (2021b). For a recent survey, see Jackson and Pernoud (2021). What has received less attention is how these interdependencies can lead to multiple equilibria,333We use the term “equilibrium” to keep with the literature, but here this term only reflects the mutual consistency of banks’ values – so a fixed point in accounting balance sheets – and not any strategic behavior. with the defaults of some banks becoming self-fulfilling. For instance, a Bank A defaulting on its obligation to another Bank B, might lead B to default as well. This can lead to further missed payments that feed back to Bank A, making its initial default self-fulfilling.

Such self-fulfilling defaults on payments are not uncommon in practice, especially in times of distress. For instance, Fleming and Keane (2021) find that almost 74% of the settlement failures that occurred in the U.S. Treasury market in March 2020 were effectively “daisy-chain” failures, which could have been avoided had all trades been centrally netted.444Settlement failures were much lower for trades that were centrally cleared (Duffie (2020)). These defaults, even if only temporary, are costly: delayed in payments can lead counterparty risk to build up, dry up liquidity in the market, restrict or stall investments, and even push some banks towards insolvency. The existence of multiple equilibria therefore contributes to the fragility of the financial system: pessimistic beliefs or uncertainty about the state of others’ balance-sheets can become self-fulfilling and lead banks to stop payments to each other—a type of credit freeze—even when another equilibrium exists in which payments are all made.

In this paper, we characterize the network structures and portfolio returns that lead to self-fulfilling defaults and how to prevent them at minimal cost to the regulator. We consider financial networks in which banks are linked via unsecured debt contracts.555The analysis extends to other sorts of contracts as we discuss in the Online Appendix. The value of a bank depends on the value of its assets outside of the network, as well as of its claims on other banks. If a bank’s assets are not enough to cover its liabilities, the bank defaults on part of its debts. Importantly, we allow for failure costs that discontinuously depress a bank’s balance-sheet upon default, and reduce the amount repaid to counterparties. We take as given banks’ exposures to each other throughout the paper. Our analysis is then most relevant for crises scenarios when banks have little leeway to adjust their positions.

There are two main applications/interpretations of our model. One is when a bank’s default involves bankruptcy, and the failure costs are the losses associated with filing for bankruptcy and liquidating assets.666Defaults involve substantial deadweight costs, including fire sales, early termination of contracts, administrative costs of government bailouts, and legal costs, among others. Estimates of bankruptcy recovery rates can be below 60%, and even worse in a crisis. See, for example, Branch (2002), Acharya, Bharath, and Srinivasan (2007), and Davydenko, Strebualaev, and Zhao (2012). The other major application of the model is to situations in which a bank’s default may only be temporary, due to an episode of illiquidity, but can still lead to a sequence of defaults or delayed payments. Failure costs then capture costs associated with delayed payments, as outlined above.777Eisenberg and Noe (2001) and most of the ensuing literature assume that all payments are cleared simultaneously, circumventing this problem. A notable exception is Csoka and Herings (2018) who show that most decentralized clearing processes yield the lowest equilibrium for bank values, providing additional motivation for our analysis. Although not explicit in our model, timing on payments can lead to self-fulfilling defaults: e.g., if Bank A must pay Bank B first, and then Bank B can pay Bank C, and then Bank C can pay Bank A, but Bank A cannot make the payments until it receives the payment from Bank C. We abstract from timing details in the model given the complexity of our analysis, but they offer another interpretation. Such defaults are often avoided in practice by short-term borrowing. However, in situations such as what occurred in 2008, lenders often lose confidence in the market, which leads to a lack of liquidity for short terms borrowing, and then makes a freeze self-fulfilling.

We make the following contributions.

First, we provide a comprehensive analysis of the multiplicity of equilibrium bank values. We show that there exist multiple solutions for bank values if and only if there exists a certain type of cycle in the network. Cycles allow costly defaults to feedback through the financial network, generating the possibility of self-fulfilling defaults. There are well-defined ‘best’ and ‘worst’ equilibria, ordered by banks’ values. In the best equilibrium none of the self-fulfilling cycles of defaults occur,888There can still be some defaults in the best equilibrium, but they are not self-fulfilling. We characterize these in the results below. while in the worst equilibrium they all do. There are also intermediate equilibria that involve some, but not all, of the self-fulfilling cycles defaulting. We then give necessary and sufficient conditions for banks’ solvency under both the best and worst equilibria, assuming that a bank cannot make any payments until it is fully solvent. This applies in practice whenever insolvencies lead to delays in payments, which can cascade and generate a credit freeze.999The insights and main results extend when there are partial payments (a fortiori), but this case provides the most direct intuition. All banks are solvent in the best equilibrium if and only if their portfolio satisfy an appropriate balance condition. Solvency in other equilibria is more demanding, and we show how it is precisely characterized by cycles in the network.

Second, we analyze the most cost-efficient way to inject capital into banks so as to avoid defaults and associated deadweight losses. Injecting capital into a bank has consequences beyond the bank itself: by paying back its obligations to others, it can bring some of its counterparties closer to solvency and lower the cost of bailing them out, or even bring them back to solvency and trigger a repayment cascade. We show that these indirect-bailout values are critical to understanding the minimal injections of capital needed to ensuring systemic solvency. Building on our analysis of equilibrium multiplicity, we identify the minimum bailout payments needed to ensure that all banks are solvent in any given equilibrium.

The minimum bailouts to ensure systemic solvency in the best equilibrium do not depend on the specific network structure, and only require bringing each bank’s portfolio into balance. In contrast, the minimum bailouts ensuring systemic solvency in any other equilibrium depend on the details of the network structure, as they require injecting enough capital so as to clear whichever self-fulfilling cycles are defaulting in that equilibrium. Characterizing the minimum bailouts needed to ensure solvency in a non-best equilibrium is thus much more complex. In fact, we prove that it is a strongly NP-hard problem - which implies that there are no known practical algorithms for finding approximate solutions, even with relatively small numbers of banks. Part of the complexity comes from the fact that the amount of capital the regulator has to inject in a bank to make it solvent depends on who else is already solvent in the network – in short, the order of bailouts matters, and every bank’s balance sheet can change with each sequence of bailouts. Hence the number of bailout policies to consider is of the order of , where is the number of banks, and so it is already in the trillions with just fifteen banks and beyond with twenty banks, and so an exhaustive search for the optimal policy gets infeasible very quickly.

Despite this complexity, our analysis provides intuitive insights about optimal bailouts. In particular, indirect bailouts are part of an optimal policy: when considering the bailout of a particular bank, instead of injecting capital directly into it, it is often cheaper to inject smaller amounts into banks that owe that bank money, leveraging those banks’ capital. This can be seen as an explanation of the AIG bailout in 2008, which some argue was an indirect bailout of Goldman Sachs and others (Bernard, Capponi and Stiglitz (2022)).101010Roughly, one could view AIG as a peripheral node as it was mainly selling insurance and so was a major debtor rather than creditor, whereas Goldman Sachs is a core dealer and was a major creditor of AIG. Building on this intuition, we propose a simple algorithm that bails out banks in decreasing order of their indirect bailout value to bailout cost ratio. Even though this algorithm is not always optimal, we show that it guarantees systemic solvency at a total cost that never exceeds half of the total overall shortfall.

We then consider some prominent network structures under which there are simpler and intuitive optimal bailout policies that prevent self-fulfilling defaults and freezes. A key example is a star network in which a core bank is linked to peripheral banks. Since only the core bank lies on several cycles, finding the optimal bailout policy is a more tractable problem – specifically, it is only weakly NP-hard and collapses to what is known as a Knapsack problem. We show that it is always cheaper to start by bailing out peripheral banks as opposed to targeting the core bank directly, as it allows the regulator to leverage peripheral banks’ capital buffers.111111Note how considering the network structure yields different insights from the literature on optimal bailout policies when banks are heterogenous. In the latter, it can make sense to bail out stronger banks first as they are closer to solvency (e.g., see Choi (2014)), but this overlooks the indirect value of bailouts. This again highlights the value of indirect bailouts, and we show how some simple bailout algorithms work well in this setting.

We then discuss more general core-periphery networks, in which a similar intuition also holds: if peripheral banks are “small” relative to core banks, then it is always optimal to start by bailing out the periphery. However, finding the overall optimal bailout policy remains strongly NP-hard, as core banks are densely connected and lie on many overlapping cycles. Thus, although we show that finding optimal bailouts is computationally challenging, we also show that there are many settings in which parts of the problem can be solved efficiently, while other parts cannot. Regardless, the indirect bailout values are important to understand and can improve over more naive bailout policies.

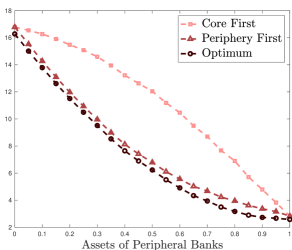

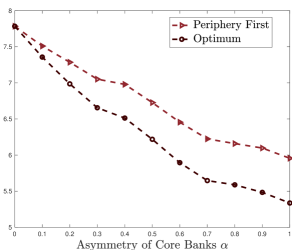

Finally, we use numerical simulations to compare the performance of various bailout policies in a broader class of core-periphery networks. In line with our analytical results, we show that policies that target peripheral banks first often outperform those that target core banks directly. This is particularly true when peripheral banks have assets of intermediate size. Furthermore, we show that “naive” bailout policies perform particularly poorly compared to more sophisticated ones when there are large asymmetries among core banks.

Overall, our results also identify the precise benefit of canceling out cycles of claims—what has become known as ‘payment netting’ (Kahn and Roberds (1998), Martin and McAndrews (2008)) and ‘portfolio compression’ (D’Errico and Roukny (2019) and Schuldenzucker and Seuken (2019))—and we end the paper with a discussion of such netting techniques.

Our model builds on the literature that followed the interbank lending network model of Eisenberg and Noe (2001). They introduce the notion of a clearing vector, which specifies mutually consistent repayments on interbank loans for all banks in the network, and show that it is generically unique. Others have pointed out that the non-negligible failure costs that banks incur whenever they are insolvent facilitate the existence of multiple clearing vectors, and hence of multiple equilibrium for banks’ values (Rogers and Veraart (2013); Elliott, Golub, and Jackson (2014))). This multiplicity comes from the discontinuous drop in a bank’s value at default, which can create self-fulfilling combinations of defaults.121212This source of equilibrium multiplicity differs from bank runs à la Diamond and Dybvig (1983). Here, it stems from reduced payments due to failure costs that become self-fulfilling, and not from the optimizing behavior of agents who, anticipating a bank’s failure, claim their assets and bring it to insolvency. This multiplicity has not been examined in any detail, and instead previous studies restrict attention to equilibrium repayments that lead to the least number of defaults.

One of the only papers that emphasizes the multiplicity of clearing vectors, and hence of equilibrium values for banks, is Roukny, Battiston and Stiglitz (2018). However, the main focus of their paper differs from ours: they show how equilibrium multiplicity makes assessing systemic risk harder, as it means some defaults are indeterminate, and propose a method to measure this source of uncertainty. We give a new and full characterization of equilibrium multiplicity, which we then use to analyze and develop optimal bailout policies.

Our analysis of optimal bailouts relates to Demange (2016), who characterizes the optimal cash injection policy in a network of interbank lending. She defines an institution’s threat index as the marginal impact of an increase in its direct asset holdings on total debt repayments in the system, assuming the policy does not change the set of defaulting banks. Hence a bank’s threat index captures its marginal social value of liquidity. In this paper, we instead examine how much of an injection is needed to change and avoid defaults in any equilibrium, show how complex that problem is, and offer insights into solving it.131313Since the first writing of this paper, others have also analyzed complexity of bailouts (Egressy and Wattenhofer (2021), Klages-Mundt and Minca (2022)). They focus on the best equilibrium and consider other objective functions, more in line with our discussion in Section 7.2 than with our main analysis.

Several papers highlight various distortions induced by bailouts in financial networks. Erol (2019) shows that public bailouts affect banks’ choice of counterparty, and hence the equilibrium structure of the financial network. Leitner (2005) and Kanik (2019) study how linkages between banks can incentivize private sector bailouts, whereby solvent banks bail out insolvent ones, and how this depends on the network structure. Bernard, Capponi and Stiglitz (2022) analyze the interplay between public bailouts and private bail-ins. Capponi, Corell, and Stiglitz (2020) investigate how debt-financed bailouts increase the risk premia on sovereign debt, and hence depress the balance sheets of the very banks the regulator was trying to save, generating a doom loop. Our paper is orthogonal to this literature, as we examine the structure and complexity of bailouts ex-post rather than their external effects on decisions that are made by banks ex-ante.

Finally, the literature on unique implementation in games with strategic complementarities (e.g., Segal (2003) and Winter (2004)) is worth noting. Following Eisenberg and Noe (2001), we do not model interbank repayments as a game but simply presume that banks repay as much of their debts as they can. An equivalent formulation would allow banks to choose how much to repay each other, with payoffs such that banks prefer paying debts when they can. The induced game would feature strategic complementarities and be prone to multiple equilibria.141414Bank can pay back (weakly) more of its liabilities if others do so as well. The optimal bailouts preventing defaults in the worst equilibrium are then the minimal transfers ensuring banks coordinate on the best equilibrium. This is in the spirit of that strand of the literature on unique implementation, which looks for mechanisms that coordinate agents on the best equilibrium in the eyes of the designer.

2 A Model of Financial Interdependencies

2.1 Financial Institutions and their Portfolios

Consider a set of organizations involved in the network. We treat as the financial organizations, or “banks” for simplicity in terminology. These should be interpreted as a broad variety of financial organizations, including banks, venture capital funds, broker-dealers, central counterparties (CCPs), insurance companies, and many other sorts of shadow banks that have substantial financial exposures on both sides of their balance sheets. These are organizations that can issue as well as hold debt.

We lump all other actors into node as these are entities that either hold debt in the financial organizations (for instance private investors and depositors), or borrow from the financial organizations (for instance, most private and public companies), but not both. Their balance sheets may be of interest as well, as the defaults on mortgages or other loans could be important triggers of a financial crisis. The important part about the actors in node is that, although they may be the initial trigger and/or the ultimate bearers of the costs of a financial crisis, they are not the dominoes, becoming insolvent and defaulting on payments as a result of defaults on their assets. In aggregate, it may appear that there is debt going both in and out of node 0, but none of the individual private investors that comprise node 0 have debt coming both in and out.151515Of course, this is an approximation and there is a spectrum that involves a lot of gray area. For instance, Harvard University invests tens of billions of dollars, including making large loans. At the same time it borrows money and has issued debt of more than five billion dollars. It is far from being a bank, but still has incoming and outgoing debt and other obligations. This is true of many large businesses, and all those that could become dominoes should be included in . It is not so important for us to draw an arbitrary line through this grey area to make our points. Nonetheless, this is something a regulator does have to take a stand on when trying to address systemic risk, and in practice may even be dictated by jurisdictional rules.

Bank portfolios are composed of investments in assets outside the system as well as financial contracts within the system. Investments in primitive assets involve some initial investment of capital and then pay off some cash flows over time, often randomly; e.g., government securities, asset backed securities, corporate and private loans, mortgages, etc. This is part of a bank’s capital. We let denote the current total market value of ’s investments in those assets and denote the associated vector. (Analogous bold notation is used for all vectors and matrices.)

The book values of banks in the network are based not only on the capital in these outside investments, but also on assets from and liabilities to others in the financial system. In this paper, we restrict attention to interbank debt contracts, but the model extends to allow for other types of financial contracts between banks.161616See Appendix B.7 of the online material for an extension of the model and results when banks also hold equity claims on each other. A debt contract between a creditor and a debtor is characterized by its face value . As a bank cannot have a debt on itself, we set for all . Let the matrix whose -th entry is equal to , and denote a bank’s total nominal debt assets and liabilities by, respectively, and .

2.1.1 The Weighted Directed Network

The financial network generated by interbank lending contracts is thus represented by a weighted directed graph on , where a directed edge pointing from bank to bank means has a debt liability toward with a weight of , so edges point from the debtor to the creditor.

A directed path in the network from to is a sequence of banks , for some such that: and and for each . Thus a directed path is such that owes a debt to some bank, which owes a debt to another bank, and so forth, until is reached.

A dependency cycle, or cycle for short, is a directed cycle in the network which is a sequence of banks , for some such that: and for each . A directed cycle is simple if is the only bank repeated in the sequence.

Given that node 0 is comprised of entities that cannot be involved in cycles, to avoid confusion with the network of debts, we set for all , and any debts owed from outside of the network of banks are instead recorded in . Outsiders can still default on a payment to a bank, but that is captured in a lower value of .

2.2 Defaults and Equilibrium Values of Banks

A main object of interest in this paper is a bank’s book value . Following Eisenberg and Noe (2001), we focus on bank values ex post, taking as given their exposures to each other and realized portfolios. We first need to introduce defaults and their associated costs, before characterizing bank values.

If the value of bank ’s assets falls below the value of its liabilities, the bank is said to fail and incurs failure costs . These costs capture the fact that the value of a bank’s balance sheet can be discontinuously depressed upon insolvency, for instance due to direct costs of bankruptcy: legal and auditors’ fees, fire sales, premature withdrawals, or other losses associated with halted or decreased operations.

In our setting, can also capture some indirect costs: it is not necessary that the bank declares bankruptcy, but simply that its insolvency causes it to renegotiate its contracts or delay payments, leading to a freeze and imposing costs on it and its creditors. Such failure costs can depend on the degree to which and others are insolvent as well as the value of their portfolios. Hence we allow these costs to depend on the vector of bank values and returns on outside investments .171717We have reduced the portfolios to only track their total value, but in practice the failure costs incurred could depend on detailed information about the composition of the bank’s portfolio as well as the portfolios of others.

With the possibility of default, the realized debt payment from a bank to one of its creditors depends on the value of , and thus its solution depends ultimately on the full vector . To make these interdependencies explicit, let denote the amount of debt that bank actually pays back to .

There are two regimes. If bank remains solvent, it can repay its creditors in full, and then for all

If instead defaults, then debt holders become the residual claimants, and are rationed proportionally to their claim on :

| (1) |

with .

It is useful to introduce notation for a bank’s realized failure costs, , which are 0 if the bank remains solvent and equal to if it defaults:181818This allows us to use the same notation for solvent and insolvent banks, and makes equilibrium bank values easier to write down.

| (2) |

We add conditions on failure costs to avoid the possibility that these costs per se, and not the reduced payments they imply, induce multiple equilibria for bank values. The key assumption is that failure costs cannot increase faster than the value of a bank’s assets. In particular, we assume that is nondecreasing in .

Note also that we have carefully written failure costs as a function of how a bank’s assets compare to its liabilities , instead of as a function of directly. This avoids having defaults or freezes driven solely by the anticipation of failure costs, even when a bank has more than enough assets, even cash on hand, to cover its liabilities. Such a self-fulfilling default would go beyond a bank run, since it would not be due to the bank not having enough cash on hand to pay its debts. It would instead be due to self-fulfilling failure costs with no interaction with the financial network or portfolio values. We rule this out as it seems of no practical interest. However, as noted above, we do allow realized failure costs to depend on the value of other banks; e.g., a bank can incur higher costs upon default if others are defaulting as well, because of fire sales. Such a dependency is important as it can worsen contagion, and we include it in our analysis.

A canonical example of admissible failure costs corresponds to the case where

| (3) |

with and .191919If , these failure costs are similar to the ones considered in Rogers and Veraart (2013), who also observe that costs of default can generate equilibrium multiplicity. They, however, do not study which network structures generate multiple equilibria nor how to prevent such multiplicity, and instead restrict attention to the best equilibrium to study rescue consortia (see the discussion in Kanik (2019)). In that case, failure costs are composed of some fixed amount (e.g., legal costs), as well as some share of the value of the bank’s assets. This is a reasonable assumption if, for instance, the bank only recovers some fraction of its assets upon sale (e.g., due to a markdown on a fire sale of its assets) or has a portion of its legal costs that scales with the size of the enterprise.202020Several papers estimate marginal bankruptcy costs being around 20% or 30% of the value of a bank’s assets (see for instance Davydenko et al. (2012)), suggesting should be in that range. As mentioned above, these can be even larger, Branch (2002), Acharya, Bharath, and Srinivasan (2007), particularly in times of a financial crisis. Fixed costs associated with bankruptcies are harder to estimate, but are presumably strictly positive given the structure of legal and accounting costs, as well as the fact that marginal cost estimates are much lower than overall costs.

It can be that failure costs exceed the value of the defaulting bank’s assets; e.g., if is large enough in the above example. These excess costs should be interpreted as real costs, for instance, debts or legal costs that are never paid, capital or labor that are idled, etc., which can be incurred by the bank itself if it does not act under limited liability, or by the government or agents outside of the network (so node in our framework). What matters for our analysis is not whether failure costs can exceed the bank’s assets, but that they crowd out some of the debt repayments to creditors.

Failure costs are imposed on banks’ balance sheets directly, and so the book value of a bank is

| (4) |

where is defined by (2) and by (1) whenever there are some defaults. In matrix notation:

| (5) |

A vector of bank values is an equilibrium if it is a solution to equation (5). Note that these are banks’ equilibrium values (ex post), at the time of settlement, once returns and defaults are realized. Any shock to outside investments is already realized, observed, and encoded into . Equilibrium values can be negative if a bank’s liabilities exceed the value of its assets. These can then be interpreted as “hypothetical” values and not equity values. If a bank is solvent, then its equity value coincides with . However, if its “hypothetical” value is negative then defaults, and its equity value is zero. The extra negative value means that a bank’s assets are not enough to cover its liabilities, and hence that some debt payments are not made in full. Coupled with failure costs, there are deadweight losses in the economy.

3 Multiplicity of Bank Values and Self-Fulfilling Defaults

Although the possibility of multiple equilibria for bank values in financial networks is well-known, the conditions under which they exist and their implications are not. In this section we characterize when there exists a multiplicity. We also derive necessary and sufficient conditions on portfolio values for all banks to be solvent, which depend on the equilibrium being considered.

All of the definitions that follow are relative to some specification of , and we omit its mention.

3.1 The Multiplicity of Equilibrium Values

Because the value of a bank is weakly increasing in others’ values, there always exists a solution to equation (5). Furthermore, there can exist multiple solutions given the interdependence in values, and in fact, the set of equilibrium values forms a complete lattice.212121This can be seen by an application of Tarski’s fixed point theorem, since banks’ values depend monotonically on each other. They are bounded above by the maximum values of banks’ assets . Thus, there exists a “best” as well as a “worst” equilibrium, in which bank values hit an overall maximum and minimum, respectively. The set of defaulting banks is hence the largest in the worst equilibrium, and the smallest in the best.

The following algorithm finds the best equilibrium. Start from bank values that are at least as high as the best equilibrium values (e.g., ) and then compute

If any values are negative, the associated banks default and the values are computed again accordingly. Iterating this process yields the best equilibrium. The worst equilibrium can be found using a similar algorithm, but starting from values that must lie below the worst equilibrium values (e.g., , where is a cap on how large failure costs can be).

Figure 1 provides a simple example, for which we compute bank values using these two algorithms.222222See Section B.1 of the Appendix for an example with three different equilibria for bank values.

Suppose , , and for . So a bank loses half of the value of its assets upon default.

Let us first derive the best equilibrium for bank values using the above algorithm. We initiate at

. Since , no

failure costs are incurred and all

debts are repaid . Then .

Since the algorithm stops, and bank values in the best equilibrium are

.

We now derive the worst equilibrium for bank values.

Note that failure costs cannot be greater than . We hence initiate the algorithm at . Since , it has to be that bank 1 does not default: and . Debt repayments for bank 2 and 3 solve

Hence, , and . Since no new solvencies are induced – indeed for – the algorithm stops, and bank values in the worst equilibrium are .

When there are multiple equilibria, any equilibrium other than the best equilibrium must involve cycles of defaults that could have been avoided: these are defaults that are triggered either by pessimistic beliefs about the balance-sheets of others—valuing their debt at a low value—which become self-fulfilling, or by a liquidity freeze in which debts are not paid in and thus not paid out. These avoidable defaults are essentially coordination failures: cycles of banks could have written-off (some) of their counterparties’ debt so as to avoid at least some of the defaults and associated costs. Given that financial markets are prone to runs and freezes, understanding when such self-fulfilling cascades exist is of practical importance.

The following proposition highlights how equilibrium multiplicity depends on the presence of cycles of liabilities, combined with failure costs.

Proposition 1.

For each , let the failure costs depend only on ’s value and the values of banks on which has a (potentially indirect) debt claim, and be a contraction as a function of (e.g., the canonical failure costs in (3)).

-

(i)

If there is no dependency cycle, then the worst and best (and thus all) equilibria coincide.

-

(ii)

Conversely, if there is a dependency cycle, then there exist failure costs (satisfying the above conditions) and values of bank investment portfolios such that the best and worst equilibria differ.

-

(iii)

Any equilibrium that differs from the best equilibrium consists of the defaults in the best equilibrium plus the defaults of all banks that lie on some set of dependency cycles. Any other banks defaulting in this equilibrium but not in the best equilibrium lie on outpointing paths from the original defaulting banks and the newly defaulting dependency cycles.232323It is possible that the new defaults on an additional dependency cycle leads banks that defaulted in the best equilibrium to payout even less than in the best equilibrium, which can lead to additional defaults on rays outwards from the original banks, not just the newly defaulting banks.

We are not the first to notice that cycles are necessary to generate multiple equilibria, as they are required for self-fulfilling feedbacks (e.g., see Elliott et al. (2014), Roukny et al. (2018)), and a similar intuition is at play here and underlies part (i). Proposition 1 however goes beyond that as it proves that cycles are also sufficient (part (ii)),242424They are sufficient in the sense that they always enable equilibrium multiplicity for some realization of portfolios and failure costs. and it highlights the general structure of the set of equilibria (part iii). This last observation is particularly useful, as even though there is a lattice of equilibria, figuring out what those equilibria are could be quite complex. This result ensures that one can find all equilibria by examining combinations of cycles, which can greatly simplify the calculations.

Although proving part (i) is straightforward, proving part (ii) requires finding returns and failure costs that generate multiple equilibria. The specific failure costs we use in the proof are for above some threshold; that is, a bank loses a fraction of its assets when defaulting. Hence, we do not need to construct costs that depend on other banks’ values to generate multiplicity: it is enough for them to only depend on the value of the defaulting bank’s assets. It is also not necessary for banks to lose the entirety of their assets () for the multiplicity to arise, though we assume they do in our analysis of minimum bailouts for the sake of transparency.

Part (iii) is intuitive, but is important to state as it is very helpful in calculating equilibria.252525Even in problems with complementarities and a complete lattice of equilibria, finding all equilibria can be very challenging (see Echenique (2007) for an algorithm). Essentially, beyond the best equilibrium, all other equilibria involve self-fulfilling cycles of defaults; and this can focus the search for equilibria. Those cycles can also lead to additional casualties that are on outward paths from an originally defaulting bank or an additional cycle, but the equilibria must be based on some dependency cycles. Not just any combination of dependency cycles will work (some banks might be strong enough to never default), but each equilibrium must differ from other equilibria by the inclusion/exclusion of at least one cycle.

With the restriction that failure costs can only depend on a bank’s direct and indirect neighbors, the feedback that leads to multiple equilibria can only occur through a dependency cycle (Proposition 1 (i)). If instead, the costs incurred by bank upon default are larger if defaults as well, even though has no network path to , then failure costs themselves can generate “indirect” cycles. For example, if fire sales change bank values, then ’s value could depend on whether becomes insolvent even if is not path-connected to in the network of debts. It is then possible to have multiple equilibria for bank values even in the absence of any cycle in the network of debt. The following example illustrates this.

Suppose Bank 2 and Bank 1’s outside investments yield and , respectively. Since Bank 2 has no other assets, it must default in any equilibrium. Bank 1’s outside investments are not quite enough to pay back its liabilities, but a small repayment from Bank 2 would be enough to ensure its solvency. Suppose Bank 2’s failure costs are small if Bank 1 is solvent, , but large if it is not, . There exist two equilibria despite the absence of cycles in the network. In the first equilibrium, Bank 1 remains solvent and Bank 2 incurs a small cost, and thus repays to Bank 1 (which then indeed has enough assets to be solvent). In the second equilibrium, Bank 1 defaults and Bank 2 incurs a large cost and repays nothing to Bank 1.

One can extend Proposition 1 to take into account such fire-sale cycles that arise under more general failure costs. To do so, the network must be augmented to account for all the ways a bank’s value can influence another’s. That is, it must feature an edge from bank to whenever ’s failure costs vary with ’s value , even if has no obligation to . If that augmented network has no cycles, then there exists a unique equilibrium for bank values. Otherwise, fire sales can generate equilibrium multiplicity even in the absence of cycles of liabilities, as illustrated above.

For the remainder of the paper, we analyze the extreme but illuminating case in which even if a bank has some money coming in it cannot use that money to pay some of its debt until it is fully solvent. In particular, we assume “Full Bankruptcy Costs:”

Under this specification for failure costs, the worst equilibrium for bank values arises whenever we take the timing of payments seriously. Indeed, the algorithm that finds the worst equilibrium starts by assuming everyone defaults, which here means that no one makes any debt payments. The only solvent banks are then those that are able to make their payments out even without receiving any payments in. This first wave of payments might enable other banks to meet their obligations, etc, and iterating on this yields the worst equilibrium for bank values. Hence this assumption applies in practice when insolvency leads to delays in payments, which can lead to cascading delays and cycles, and thus at least to a temporary freeze.

These failure costs make solvency more demanding: the set of defaulting banks can be strictly larger under this rule than when partial repayments are allowed. Nonetheless, this case provides the basic intuitions and insights without cluttering the calculations with partial payments. Some of our results do not rely on this assumption, and in particular results from Section 4 on the complexity of bailouts, which only require failure costs to be strictly positive. Our characterizations of systemic solvency and of the optimal bailout policy in some specific networks do leverage this assumption, and are more complicated to state without it, even though the underlying intuitions remain.

3.2 A Characterization of Systemic Solvency

Proposition 1 shows that cycles of debts are vital to the existence of multiple equilibria, and that such multiplicity means the defaults of some banks can be self-fulfilling. In this section, we investigate in more details which banks default, and how it depends on the equilibrium being considered. We give necessary and sufficient conditions on portfolio values for all banks to be solvent, which we call systemic solvency.

3.2.1 Balance Conditions

To characterize solvency, and minimal bailouts, it is useful to define the following balance conditions.

We say that a bank is weakly balanced if

and that the network is weakly balanced if this holds for all .

Weak balance requires that a bank’s assets are enough to cover its debt liabilities, presuming its incoming debt assets are all fully valued. A network being weakly balanced is sufficient for all banks to be solvent in the best equilibrium. This follows since, if all banks but honor their debt contracts, then can also pay back its debt fully in a weakly balanced network. Essentially, all debts can be canceled out, irrespective of the network structure. Things are different in the worst equilibrium, as we know from Proposition 1.

We say that a bank is exactly balanced if

and that the network is exactly balanced if this holds for all . An exactly balanced bank has no capital buffer: its assets, if fully valued, are exactly enough to cover its liabilities. Exact balance is a much stronger condition than weak balance, but is very useful as a benchmark condition in characterizing optimal bailouts, as we shall see.

We say that a bank is critically balanced if it is weakly balanced and for each for which ,

The network is critically balanced if this holds for all .

Critical balance is a special case of weak balance which includes exact balance as a special case, but is not as restrictive and is useful as a benchmark condition in characterizing optimal bailouts. It implies that not receiving any one of its incoming debt payments is enough to make a bank insolvent.

3.2.2 Characterizing Systemic Solvency

When there exist cycles of debt, by Proposition 1, the best and worst equilibria can differ. We now fully characterize when these cycles fail to clear.

Determining whether cycles clear at a given vector of portfolio values involves an iterative definition of solvency, since a bank being solvent can affect the solvency of other banks.

We say that a bank is unilaterally solvent if . This means that regardless of whether any of the other banks pay the debts that they owe to , is still able to cover its liabilities.

A set of banks is iteratively strongly solvent if it is the union of sets , such that banks in are unilaterally solvent; and then banks in any for are solvent whenever they receive the debts from all banks in sets :

Note that if is iteratively strongly solvent, then all banks are solvent in the worst equilibrium. Proposition 2 provides weaker conditions that are necessary and sufficient for systemic solvency. This then provides a base to understand optimal bailout policies.

Proposition 2.

All banks are solvent in the best equilibrium if and only if the network is weakly balanced.

All banks are solvent in the worst equilibrium if and only if the network is weakly balanced and there exists an iteratively strongly solvent set that intersects each directed (simple) cycle.262626A simple cycle is such that the only repeated bank is the starting/ending bank. Note that something intersects each cycle if and only if it intersects each simple cycle, and so the statement is correct whether or not it is restricted to simple cycles.

An implication of Proposition 2 is that in a weakly balanced network, if there is an iteratively strongly solvent set that intersects each cycle, then that implies that the whole set of banks is iteratively strongly solvent. This is the crux of the proof.

The proposition is less obvious than it appears since an insolvent bank can lie on several cycles at once, and could need all of its incoming debts to be paid before it can pay any out. Solvent banks on different cycles could lie at different distances from an insolvent bank, and showing that each bank eventually gets all of its incoming debts paid before paying any of its outgoing debts is subtle. The proof is based on how directed simple cycles must work in a weakly balanced network and appears in the appendix.

Proposition 2 is useful for at least two reasons. First, it highlights the structure of the set of equilibria, which is very useful in our analysis of optimal bailouts. Second, it gives necessary and sufficient conditions to find the worst (and other) equilibria that are easier to check than preexisting algorithms. Example 3 illustrates this.

As all banks have as much debt in as out, they are weakly balanced and hence all solvent in the best equilibrium. Identifying which banks default in the worst equilibrium requires checking the iterative condition. Bank 5 is the only unilaterally solvent bank. Its solvency ensures the solvency of Bank 4, and so there is at least an iteratively strongly solvent set intersecting the left and middle cycles. However, Bank 4 paying back its debt is not enough to make Bank 6 solvent, and so we can stop the iteration there: no iteratively strongly solvent set intersects the right cycle, and all banks on that cycle must default in the worst equilibrium. Interestingly, this is faster than checking that the entire set of banks forms an iteratively strongly solvent set, as we can stop checking banks’ solvencies once we have reached key banks that lie at the intersection of multiple cycles (here Banks 4 and 6). It is also faster than algorithms that have been developed to find Nash equilibria of games with strategic complements.272727Equilibrium values for banks correspond to Nash equilibrium outcomes of an auxiliary game in which banks choose whether to be solvent () or not, and best responses are . The worst equilibrium is usually found by iterating on best-responses starting from the lowest strategies for all agents (see Echenique (2007), and references therein), which in our setting boils down to checking whether the whole set of banks is iteratively strongly solvent.

Proposition 2 also implies that if both conditions are satisfied, then there is a unique equilibrium. Conversely, if the network is weakly balanced but there is no iteratively strongly solvent set intersecting every cycle, then there are necessarily multiple equilibria. Thus, in a weakly balanced network, there is a unique equilibrium if and only if there exists an iteratively strongly solvent set that intersects each directed (simple) cycle.

Clearly, without some unilaterally solvent banks, having an iteratively solvent set is precluded, and all banks must default in the worst equilibrium. This is not directly implied by Proposition 2, but still follows from the reasoning behind it. To see why this is true, recall the algorithm introduced in Section 3.1 to find the worst equilibrium. The algorithm initiates at values that lie below the worst equilibrium values; e.g., . Since we here consider full failure costs, and . That is, if we start from the pessimistic assumption that all banks are insolvent, then they get no repayments from their debtors. Thus a bank is solvent in the following step of the algorithm if and only if , that is if and only if it is unilaterally solvent. If no bank is unilaterally solvent, the algorithm stops: assuming that all banks are insolvent is self-fulfilling.

A Sufficient Condition for Iterative Solvency.

One way to ensure having an iteratively strongly solvent set intersecting each directed cycle is to have at least one unilaterally solvent bank on each cycle, but this is not always necessary, and so the iterative solvency condition is important. Nonetheless, an extended version of unilateral solvency is both necessary and sufficient whenever the banks that lie on multiple (simple) cycles are critically balanced.

Let us say that a cycle is maximal if there is no larger cycle containing all the banks in the original cycle.

Corollary 1.

If all banks that lie on multiple (simple) cycles are critically balanced, then all banks are solvent in the worst equilibrium if and only if the network is weakly balanced and every (simple) cycle has at least one unilaterally solvent bank presuming that all debts owed into each maximal cycle are paid.

An implication of Corollary 1 is that the iterative portion of the iterative solvency condition only matters when some of the banks that lie at the intersection of several cycles have capital buffers, so that they only need some of their incoming debts to be paid before they become solvent and can make their debt payments. In that case, those banks can be part of a repayment cascade in which payments in one cycle spread to another. As an illustration, recall the network depicted in Figure 1. Bank 2 is the only bank at the intersection of several (simple) cycles and is exactly balanced. In the worst equilibrium only Bank 1 is solvent, as there is no unilaterally solvent bank on the right cycle. Suppose instead that . Bank 2 now has enough of a capital buffer so that, even if it gets payments from only one cycle, it can make all of its payments. All banks are then solvent in the worst equilibrium: though Bank 2 is not unilaterally solvent itself, it has enough buffer so that the debt payment initiated by Bank 1 cascades and spreads to the right cycle.

4 Minimum Bailouts Ensuring Solvency in any Given Equilibrium

The results above characterize systemic solvency in the best and worst equilibria. Next, we leverage these results to deduce the minimum bailouts needed to return the whole network to solvency whenever there are some insolvencies. These bailouts are the smallest transfers that avoid all failure costs and other inefficiencies associated with a dysfunctional financial system, and are optimal in this sense.282828If anticipated, these bailouts could distort banks’ incentives and lead them to take on more risks ex ante. Such moral hazard problems are well-studied, and so we do not argue that the regulator should always ensure solvency ex post. We simply acknowledge the fact that regulators often have to intervene to restore solvency when faced with a crisis that has a potential for large cascades. This is thus an important problem, and we analyze what is the most efficient way of doing so. Minimum bailouts depend on the network structure: just as losses can cascade and cycle through the network, the same operates in reverse and well-placed bailouts can have far-reaching consequences.

4.1 The Minimum Bailout Problem

Consider a regulator who can inject capital into each bank in the network, increasing the value of bank ’s balance sheet by . The timeline is as follows:

First, returns on outside investments p are realized. Then, anticipating that some banks will be insolvent absent intervention at p, the regulator can inject capital into the network. Importantly, the capital is injected before banks officially start bankruptcy proceedings, and hence before the associated failure costs are incurred.

To ensure systemic solvency at minimum cost, the regulator solves

| (OPT) | ||||

Since there can be multiple equilibria for bank values, we need to be precise about which equilibrium is selected in the constraint of (OPT). For simplicity, we suppose that the transfers do not impact the equilibrium selection, although they conceivably could. Thus, to examine the minimum bailouts preventing defaults in the best equilibrium, we always select the best equilibrium for bank values in (OPT). Similarly, if the goal is to prevent defaults in the worst equilibrium, then optimal bailouts are the minimum transfers such that all banks are solvent if we select the worst equilibrium for .292929More generally, fix any equilibrium of . Let the set of solvent banks in that equilibrium absent intervention, and the set of defaulting banks. To keep the equilibrium selection fixed, is computed by assuming that banks in are all solvent, and then finding the maximum set of defaults among the originally defaulting banks. Optimal bailouts are specific to an equilibrium. For instance, it can be that all banks are solvent in the best equilibrium but some default in the worst. Optimal bailouts for the best equilibrium are then null since all banks are already solvent, but are strictly positive for the worst equilibrium.

We start by noting that Proposition 2 yields a first characterization of such minimum bailouts for both the best and the worst equilibria, as well as other equilibria.

The best equilibrium is relatively easy to understand. If the network is not weakly balanced then some banks must be defaulting, and each bank that is not weakly balanced needs bailouts to be brought back to solvency. It is thus necessary and sufficient for each bank to receive its net imbalance (by Proposition 2).

Since the minimum injections of capital that ensure systemic solvency in the best equilibrium are fully characterized and relatively easy to calculate, for the remainder of the paper we focus on the additional capital needed to ensure solvency in other equilibria.

Note that it is weakly optimal for the regulator to start by providing each bank with its net imbalance , as these payments are necessary for solvency in all equilibria and may trigger some repayment cascades. To analyze minimum bailouts for an equilibrium other than the best, it is then without loss of generality to restrict attention to the banks that remain insolvent in that equilibrium once net imbalances have been injected, redefining their portfolio values to account for these transfers and any debt payments they received from solvent banks.

Proposition 2 then tells us that the additional payments needed are the smallest ones that generate an iteratively solvent set of banks that hits each defaulting cycle.

We first point out that even though (OPT) is written as a simultaneous choice of payments, , it is equivalent to specify an ordered list of banks to bailout. Indeed, any set of (simultaneous) payments leads banks to become solvent in a particular order: first some banks are made unilaterally solvent by the payments; then given their induced debt payments and the bailout payments, some other banks become solvent, and so forth. Reciprocally, any ordered list of bailouts can be implemented via simultaneous payments by setting precisely equal to ’s shortfall given the payments it gets from already solvent banks. Hence, just knowing which banks get payments under the optimal bailout policy is not enough to characterize minimum bailouts as the order in which banks are brought back to solvency matters.

To illustrate this, consider the network depicted in Figure 4, in which all banks default in the worst equilibrium. Since Bank 2 lies on all cycles, bailing it out ensures systemic solvency and costs . This is however not the optimal policy, as the regulator can significantly reduce the cost of bailing out Bank 2 if it first bails out Bank 3. Indeed, bailing out Bank 3 costs , and allows for the repayment of its debt to Bank 2. Bailing out the latter then only costs . The optimal bailout policy is then , which can be equivalently expressed as a sequence of banks that are bailed out .

As mentioned above, the order of bailouts matters, because the bailout cost of remaining banks depends on which banks have already been bailed out. Bailing out 3 and then 2 costs less than the reverse, and both lead to systemic solvency.

4.2 The Computational Complexity of Finding Minimum Bailouts

Proposition 2 implies that ensuring systemic solvency in equilibria other than the best requires that, beyond establishing weak balance, one also needs to inject enough capital so as to ensure the existence of an iteratively strongly solvent set intersecting all directed cycles on which banks are insolvent. We examine this in what follows.

We begin by showing that this problem is computationally complex, using concepts from the computer science literature. Precisely, we prove that it is strongly NP-hard. We provide formal definitions of such notions of complexity in Appendix B.2, but what matters is that every strongly NP-hard problem has instances for which finding exact or even approximate solutions involves impractically many calculations (more than polynomially many in the size of the problem, based on known techniques).

Proposition 3.

Finding whether there exists a bailout policy that ensures systemic solvency and costs no more than some budgeted amount is strongly NP-hard. Thus, finding a minimum cost bailout policy (OPT) is also strongly NP-hard.303030Checking whether there exists a bailout policy that ensures systemic solvency and costs no more than some budgeted amount is an “easier” problem than finding a minimum cost policy since knowing an optimal policy enables one to answer the question of whether it can be done within some budget. Thus, showing that the decision problem is strongly NP-hard establishes that (OPT) is as well, and working with decision problems is a standard technique.

The complexity comes from the fact that some of the capital that a bank needs to become solvent can come from the debts paid by others, and so it can be cheaper to first bail out a bank’s debtors rather than bailing it out directly. The number of possible combinations that could be optimal explodes factorially in the number of banks. Moreover, given that there are many cycles in interbank networks there are no obvious starting points and so there are many situations where it is not obvious how to focus on just a small number of those combinations.

We prove Proposition 3 by showing that for some network structures, finding whether one can make all banks solvent at no more than a certain cost enables one to solve the “Largest Minimal Vertex Cover Problem,” which is known to be strongly NP-hard and hard to even approximate.313131 Boria et al. (2015) show that, unless , this problem cannot be approximated by a polynomial time algorithm within ratio , for any . Given some undirected graph, a vertex cover is a set of vertices that contains at least one endpoint of all edges in the graph. A vertex cover is minimal if it is not the superset of another vertex cover. It turns out that, for some networks, the optimal bailout policy consists in bailing out banks belonging to a minimal vertex cover of maximum size.

To be more specific, consider any undirected graph, and interpret an edge between and in that network as bilateral claims of 1 that and have on each other (i.e., ). So any edge generates a cycle between banks and in the financial network. Let for all banks, such that the network is critically balanced: Banks’ outside assets are not enough to absorb the default of any one of their counterparties. We know that, to ensure solvency of all, the regulator must bailout at least one bank per cycle, and so the set of bailed out banks forms a vertex cover. We furthermore show that this vertex cover has to be minimal (as otherwise the regulator is bailing out banks that need not be bailed out) and that overall bailout costs sum up to the number of edges net of the value of outside assets of all bailed out banks. Hence an optimal bailout policy consists in bailing out banks in a minimal vertex cover of maximal size, as this allows the regulator to leverage the outside assets of more banks. This means any Largest Minimal Vertex Cover Problem can be translated into a Bailout Problem on an appropriately constructed network, and so Bailout problems are at least as hard as Largest Minimal Vertex Cover Problems.

We emphasize, however, that finding the optimal bailout policy is, in more general networks, even more complicated than the Largest Minimal Vertex Cover Problem. As banks are bailed out, they repay their debts and change the balance sheets of each other, thus altering the remaining network of insolvent banks. This adds another layer of complexity, and means that the number of bailout policies that the regulator would have to compare absent a better algorithm is of the order of , which very quickly gets too large for any computer to handle. With just 15 banks the problem already involves trillions of possible bailout strategies, and with 20 banks more than . Furthermore, as the order of bailouts matters, (OPT) is not easily expressed as a linear program, and standard dynamic programming algorithms that have proved effective for NP-hard problems do not directly extend.323232This makes the bailout problem an interesting class of problems for further study in complexity. This problem is strongly NP-complete as it is easy to check whether a given bailout policy costs no more than a certain amount. Yet it provides an interesting twist on well-studied problems given that combinations of bailouts changes the cost and value of other bailouts. One can expand the problem to have different values for every ordering, but then the linear problem has factorially many inputs as a function of .

As discussed above, finding the minimum bailouts ensuring solvency in the best equilibrium is easy, so the added complexity for non-best equilibria comes from the fact that bailouts need to clear all the cycles. Hence the complexity of the problem does not scale with the number of banks in the network per se, but with the number of cycles, which can be huge. However, if the network happens to contain few cycles (e.g., it has a core-periphery structure with a small core), then the minimum bailout problem remains tractable. We formalize this intuition in Appendix B.5 and provide an upper bound on the number of calculations needed to find the optimal policy that is exponential in the number of cycles only, but not in the number of banks.

4.3 An Upper Bound on Bailout Costs

Even though finding the optimal bailout policy can be complex, we can provide an upper bound on the total injection of capital that is necessary to bring the network to solvency. As discussed above, we assume that net imbalances have already been injected, so this is a bound on the additional injections needed to prevent self-fulfilling defaults. We also provide a simple algorithm that ensures systemic solvency, and leads to total bailout costs that never exceed this bound. This is helpful since we know from Proposition 3 that the minimum bailout problem is hard to approximate, and that no known algorithm performs well.

The algorithm that we propose leverages the idea that bailing out a bank has an indirect value: it brings ’s counterparties closer to solvency, or makes them solvent altogether.333333The indirect bailout value differs from the concept of threat index of Demange (2016), which captures the impact of marginally increasing a bank’s repayments on total debt repayments, assuming the set of defaulting banks remains the same. A key difference is that our notion of indirect bailout value is not calculated on the margin, and the value of bailing out a bank propagates further if we account for induced changes in the solvency status of other banks.

Define the first-step indirect bailout value of a bank as : it captures by how much ’s solvency reduces the bailout cost of other banks in the network. Note that this is a near-sighted measure of indirect bailout value as it only accounts for a bank’s direct payments, but not for the fact that ’s solvency can induce the solvency of one of its creditors , which then repays its debts, and so forth. We can thus define a th-step indirect bailout value of bank by all the cascades of payments that are induced by the bailout of up to iterations of induced solvencies. We provide formal definitions in the appendix, together with the proof of Proposition 4.

When deciding whether to bailout , the regulator must trade-off a bank’s indirect bailout value with the cost of its bailout, . Consider the greedy algorithm that bails out the defaulting bank with highest ratio of its th-step indirect bailout value to its bailout cost (for any ) until all are solvent, recomputing these values after each step to account for all new solvencies.343434If there are any ties – i.e., more than one bank with the highest indirect bailout value to bailout cost ratio – then break the ties arbitrarily. We show that this algorithm leads to total bailout costs that never exceed the following bound.

Proposition 4.

For any , bailing out banks in decreasing order of the ratio of their th-step indirect bailout value over bailout cost until all are solvent leads to a cost of at most

Thus, the optimal bailout cost is no more than this, and this bound is reached in some networks.

When following this algorithm, the regulator is guaranteed to inject at most half of banks’ total shortfall in order to ensure solvency of all banks. This bound holds for all equilibria, and can be made tighter by only summing over the banks that default in the equilibrium of interest, instead of summing over all banks. The bound is reached whenever the network is composed of disjoint cycles, no bank is unilaterally solvent, and banks are all equally costly to bailout – so for all .

This upper bound is not straightforward. Consider, for instance, a clique of critically balanced banks, such that all banks have claims on each other and none of them has enough capital buffer to sustain the default of some of its counterparties. Then, to ensure systemic solvency in the worst equilibrium, the regulator has to bailout all banks but one. What Proposition 4 shows is that, even in such a network, total bailout costs do not add up to more than half of banks’ total shortfall: the optimal policy leverages the fact that payments from banks that have already been bailed out reduce the cost of future bailouts.

Nonetheless, Proposition 4 does not imply that following the above algorithm always finds an optimal bailout policy. For instance, in the example from Figure 4 it would begin by bailing out Bank 2 rather than Bank 3 and would overpay. In other instances it could overpay by arbitrarily large amounts and so does not approximate the optimal bailout policy well, as we show in Section 5.2 below. The same is true of an algorithm that chooses banks in the order of the indirect values that their bailouts generate.353535Maximizing the indirect value divided by the cost, or just the indirect value, can lead the regulator to bail out the center bank in a star network if it has the highest debt liability/cost ratio, while bailing out some peripheral banks can lead to (arbitrarily) lower total bailout costs.

Similarly, algorithms that bail out banks in increasing order of their bailout cost can also lead to total injections of capital arbitrarily larger than necessary. For example, the network in Figure 5 illustrates how badly a greedy algorithm based on minimizing costs can perform. The example consists of a chain of cycles of length . Note that banks have enough capital buffer to absorb the default of their smallest debtor, that is . Hence if a bank is solvent, then this is enough to make its follower solvent as well, which is then enough to make solvent, and this unravels until Bank . The reverse is, however, not true: Bank repaying its debts is not enough to make its predecessor solvent. Given this asymmetry, the optimal policy is to bailout Bank 1: this guarantees solvency of all for a total cost of . Now suppose the regulator uses a simple greedy algorithm, which consists in bailing out banks in increasing order of their bailout cost. The algorithm bails out Bank first, as this only requires injecting for all . The algorithm then bails out Bank at a cost of , and then Bank , etc. This leads the regulator to inject a total of . Hence, the performance of the greedy algorithm relative to the optimal policy can be arbitrarily bad for long enough chains.

As the example helps illustrate, the complexity arises from the fact that cycles overlap, and that a repayment cascade in one cycle can spread to another. More generally, as banks are bailed out, they can either increase or decrease each other’s indirect bailout values. On the one hand, their bailouts and debt payments bring others closer to solvency and thus reduce how much they still need, but then also make it easier to cause them to return to solvency and induce subsequent payments. So, a bank’s bailout can affect others’ indirect bailout values in either direction. This becomes especially complex when cycles overlap.

The optimal bailout problem is easier in networks in which interferences between cycles are limited. This is for instance the case if cycles do not overlap, and we fully characterize the optimal bailout policy in such networks in Section 5.1. This is also the case if all banks that lie on multiple cycles are critically balanced – i.e., have no capital buffer – as then a repayment cascade cannot spread from one cycle to another (Corollary 1).363636See Online Appendix B.4 for an analysis of critically balanced networks.

5 Some Prominent Network Structures

We showed that finding an optimal bailout policy can be both computationally hard, and hard to approximate. In some financially relevant cases, however, the analysis simplifies and provides insights regarding the structure of optimal bailouts. In this section, we first consider networks in which cycles of banks do not overlap, and then examine networks that have a core-periphery structure. A main takeaway of our analysis is the importance of indirect bailouts: to ensure the solvency of a large core bank, it is generally cheaper to bailout small peripheral banks that owe money to it rather than to bailout the core bank directly, so as to leverage the outside assets of more banks.

As in the previous section, we presume weak balance is satisfied and restrict attention to the subnetwork of insolvent banks, accounting for all the debt payments that they receive from solvent banks.

5.1 Disjoint Cycles

The first set of networks that we examine are those in which the cycles are disjoint, so that no bank lies on more than one cycle.

There can still be banks that lie on no cycles, but for instance lie on directed paths coming out from some bank on a cycle. There can also exist a directed path that goes from one cycle to another, as long as there is no directed path that goes back (which would violate each bank lying on at most one cycle).373737Note that there cannot exist banks with no incoming debts but with outgoing debts, since those are already solvent under weak balance.

Let be the simple cycles in the network, where denotes the set of banks in the -th cycle. Order the cycles so that if and for , then there is no directed path from to .383838Given that and lie on different cycles, there cannot be both a directed path from to and one from to , as that would imply that these banks lie on multiple cycles. Thus, there must exist such an order, and in fact there can be multiple such orders. Pick any one satisfying this condition, as all such orders will lead to the same bailout costs.

The optimal bailout policy is described as follows. Pick the bank on that is the cheapest to bailout:

This then ensures that all banks on that cycle are solvent, and can also lead to further solvencies as the banks on that cycle may owe debts to banks outside of that cycle. Let denote the set of banks that are made solvent if all banks on are solvent (which is the same regardless of which bank on is bailed out). If this includes banks on any other cycles, then that cycle will be fully solvent as well. Consider the smallest such that . Accounting for all the payments that have come in from , find the cheapest bank to bailout on :

As before, let denote the set of banks made solvent by this bailout and its cascade. Iteratively, after such steps, one finds the lowest indexed insolvent cycle and finds the cheapest bank on that cycle to bailout:

After at most steps the full network will be solvent.

Proposition 5.

Suppose that each bank lies on at most one cycle. Then, the optimal bailout policy consists of bailing out the bank closest to solvency on each simple cycle, accounting for bailouts of previous cycles, as described above.

5.2 Star Networks

A star network is composed of one center bank, Bank , that is exposed to all banks in the periphery: . Each bank in the periphery is exposed only to the center bank. A star network is then a simple example of a core-periphery network, in which there is only one core bank. We first consider star networks as they provide part of the intuition needed for the analysis of more general core-periphery networks.

The optimal bailout policy is more tractable in star networks than in some other networks as only one bank, the center bank, lies on multiple (simple) cycles. This reduces the complexity of the problem: finding the optimal bailout policy is no longer strongly NP-hard and becomes equivalent to the Knapsack Problem.393939A Knapsack Problem consists of items that each have a weight and a value, and a knapsack that has some limit on the total weight it can hold. The goal is to select which items to pack so as to maximize the total value, while not exceeding the weight limit. Our problem is similar as, intuitively, each peripheral bank has a value – the amount of liquidity flow into the core induced by its solvency,– and a cost – how much capital the regulator needs to inject to make it solvent. The goal is then to minimize the total cost of bailed out peripheral banks while inducing sufficient liquidity flow into the core to ensure its solvency. The Knapsack Problem is still an NP-hard problem, but there exist several algorithms that approximate it arbitrarily well. Hence our analysis suggests that these types of algorithms should be considered when deciding which peripheral banks to bailout in core-periphery networks.

If the star network also satisfies some symmetry conditions, then the optimal bailout policy can be fully characterized and needs not be approximated. Let all peripheral banks be symmetrically exposed to the center bank: they all have a debt claim of on the center bank, and a liability to it. So the total debt assets and liabilities of the center bank equal and , respectively. As before, let the network be weakly balanced, and suppose none of the banks are unilaterally solvent. If the center bank were unilaterally solvent, the whole network would always clear, and regulatory intervention would be unnecessary. Similarly, if some peripheral banks were unilaterally solvent, then they could pay back their debt to the center bank for sure, and we could redefine the network to account for these payments. See Figure 6 for an example of a star network.

Bailing out the center bank costs and clears the whole system, as the center bank lies on all cycles. However, unless all peripheral banks have , this is not optimal and can be much costlier than optimal.

To understand the optimal bailout policy, let

Without loss of generality, let the peripheral banks be indexed in decreasing order of .

The optimal policy always involves first bailing out the peripheral banks with the highest portfolio values. This leverages their ’s and gets an amount of liquidity into the center bank at a potentially much lower cost than paying it directly to the center. This then just leaves a comparison between the marginal shortfall of the center bank

and the cost of bailing out the -st peripheral bank

It is optimal to do the remaining bailout via the center bank instead of the -st peripheral bank if and only if404040Note that if happens to be an integer, then the center bank is already solvent.

Proposition 6.

The optimal bailout policy is: to bailout the first peripheral banks if

and otherwise to bail out the first peripheral banks, and then inject into the center bank.

The proposition implies that it is always best to start by bailing out peripheral banks, so as to leverage their outside assets and reduce the overall cost of bailouts. Then, once only one more peripheral bank’s payment is needed to return the center bank to solvency, the regulator either injects the center bank’s marginal shortfall or bails out one last peripheral bank, depending on which is cheaper.

An implication of Proposition 6 is that mistakenly bailing out the center bank when the optimal policy is to target peripheral banks can be much costlier to the regulator than the reverse. Indeed, this can lead the regulator to waste the value of the outside assets owned by peripheral banks. In contrast, the only reason why bailing out peripheral banks may not be optimal is if this leads the regulator to bailout “one too many” of them due to the integer constraint, which implies a waste of capital of at most .

Corollary 2.

Bailing out all peripheral banks leads the regulator to inject at most an extra compared to the total amount required by the optimal bailout policy.

Bailing out the center bank leads the regulator to inject at most an extra compared to the total amount required by the optimal bailout policy.

Thus, in situations where the portfolio values among the needed peripheral banks () is much larger than the amount any one of them owes to the center bank (), bailing out the periphery is a much safer policy in terms of wasted capital.

5.3 Core-Periphery Networks and Cliques