A geometric investigation into the tail dependence of vine copulas

Emma S. Simpson, Jennifer L. Wadsworth and Jonathan A. Tawn

Lancaster University

Abstract

Vine copulas are a type of multivariate dependence model, composed of a collection of bivariate copulas that are combined according to a specific underlying graphical structure. Their flexibility and practicality in moderate and high dimensions have contributed to the popularity of vine copulas, but relatively little attention has been paid to their extremal properties. To address this issue, we present results on the tail dependence properties of some of the most widely studied vine copula classes. We focus our study on the coefficient of tail dependence and the asymptotic shape of the sample cloud, which we calculate using the geometric approach of Nolde, (2014). We offer new insights by presenting results for trivariate vine copulas constructed from asymptotically dependent and asymptotically independent bivariate copulas, focusing on bivariate extreme value and inverted extreme value copulas, with additional detail provided for logistic and inverted logistic examples. We also present new theory for a class of higher dimensional vine copulas, constructed from bivariate inverted extreme value copulas.

Keywords: coefficient of tail dependence; gauge function; multivariate extremes; vine copula.

1 Introduction

In multivariate extreme value analysis, the tail dependence properties of variables are an important consideration for model selection. In particular, one may be interested in whether or not they exhibit so-called asymptotic dependence, where the largest values can occur simultaneously across all variables; see Coles et al., (1999). Suppose we are interested in a model for the random variables , which we assume have standard exponential margins to focus only on dependence, i.e., , , for . For any subset of these variables, , with and , and any , one can consider the measure

| (1) |

which corresponds to the limiting probability that all variables are above some high threshold , given that any one of the variables exceeds . If , all variables in exhibit asymptotic dependence, while means that not all variables in can be simultaneously large. In the latter case, if , the two variables cannot be simultaneously extreme, and are said to exhibit asymptotic independence; if , it is still possible to have for any . That is, variables indexed by could take their largest values simultaneously while at least one of those indexed by are of smaller order. The collection of all sets of variables which can or cannot be simultaneously extreme corresponds to a more complicated extremal dependence structure; see Goix et al., (2017) or Simpson et al., (2020).

Moreover, if , there could be some sub-asymptotic dependence between , despite the lack of asymptotic dependence in the limit, and the measure does not tell the full story. To investigate this behaviour further, it is common to consider the coefficient of tail dependence, introduced by Ledford and Tawn, (1996). Again for a subset of exponential variables , with , this is defined via the relation

| (2) |

as , where denotes a function that is slowly varying at infinity, and . If and , as , the variables in are asymptotically dependent. For , these variables cannot be simultaneously large, and the value of the coefficient quantifies the strength of sub-asymptotic dependence between the variables. The set of measures therefore provide a summary of the key extremal dependence features of .

Often, the value of can be calculated directly from (2) for a given model, but in some cases, only the joint density of can be specified in closed form, and not the required joint survivor function. Nolde, (2014) presents a strategy to overcome this issue, based on the geometry of scaled random samples from the joint distribution of . A simplified version of the approach of Nolde, (2014), which we discuss further in Section 2.1, assumes standard exponential margins, and joint density , with the idea being to study the gauge function such that

| (3) |

as , with being homogeneous of order 1. The limiting shape of suitably scaled samples from is described by the set of points where the gauge function is at most one, i.e., , and studying this set can reveal the value of and provide insight into other aspects of the extremal dependence structure; see Nolde and Wadsworth, (2020). We present some example gauge function calculations in Section 2.3 for the case where , for both asymptotically dependent and asymptotically independent models, and demonstrate how they can be used to obtain .

One drawback of this method is that it is only applicable when the joint density of can be obtained analytically. It may be the case that we have a closed form joint density for variables , but not for all with . Nolde and Wadsworth, (2020) show how to derive lower-dimensional gauge functions from higher-dimensional ones, and in Section 2, we review this technique for the calculation of and in such cases. In our study of vine copulas, which have dimension , this approach can be necessary to obtain even some bivariate results.

In this paper, we focus on investigating the tail behaviour of vine copulas. These models exploit the wide range of existing parametric bivariate copula models to create parametric copula models for higher dimensions, where there are fewer options available. This allows for the construction of flexible models with the possibility of capturing a wide range of dependence features. The idea of combining bivariate copulas in this way was first proposed by Joe, (1996); developed further by Bedford and Cooke, (2001, 2002), who proposed the use of a type of graphical model called vines to aid the modelling procedure; and further studied in an inferential context by Aas et al., (2009). A textbook treatment of these models is provided by Kurowicka and Joe, (2010). We give an introduction to vine copula modelling in Section 3. Vine copulas are widely used in financial applications; a summary of these applications is provided by Aas, (2016), with examples including Brechmann et al., (2012) and Dißmann et al., (2013).

Vine copulas reduce model formulation to a series of pairwise copula selections, and therefore appear to be ideal for modelling extremal dependence since, as noted earlier, such dependence is known to have complex structure. For vine copulas over variables indexed by , Joe et al., (2010) have made major progress in deriving general results about , defined in (1), for any vine copula. In particular, they have determined some relationships of with the values of (for ) associated with the bivariate copulas used in the vine construction. Primarily, they consider the case where all pairwise are non-zero, and therefore focus only on asymptotically dependent copulas. They also study the result of imposing asymptotic independence or asymptotic dependence in certain pair copulas, and how this leads to constraints on .

Some pairwise copulas have , with a range of examples given by Heffernan, (2000). Particularly noteworthy cases include the pairwise Gaussian copula and the Morgernstern copula (see Example 2.1 of Joe et al., (2010)), with parameters and , respectively. For vine copulas, when some of the pairwise , the results of Joe et al., (2010) only give that , and they fail to give any information about the dependence in the joint tail of variables, e.g., the probability that all of the variables are simultaneously large. In that case we are interested in the numerator of (1) (prior to it being taken to its limit for ). When , all we know is that this joint probability is smaller order than the marginal probability of one of the variables being large (as in the denominator of (1)). Such joint tail probabilities are important in characterising the tail, and for assessing risk in applications (Coles and Tawn, , 1994; Heffernan and Tawn, , 2004).

The tail parameter for all in (2) is important, as it captures the level of asymptotic independence, with corresponding to asymptotic dependence (for all cases where ) and corresponding to levels of asymptotic independence. For example, for the bivariate Gaussian copula, (with denoting the usual “correlation coefficient”), and for the Morgenstern copula, for all . So, although these two copulas have identical values, they have different values of unless .

Our paper therefore differs from Joe et al., (2010) in that we aim to find in cases where their results simply give , for all . With this, we seek to better understand how the bivariate copulas and underlying graphical structure used in the construction of a vine copula affect these additional extremal dependence features of the variables, and to be the first to study the gauge function for vine copulas.

Throughout this paper, we consider exponential marginal distributions, but allow a variety of different bivariate copulas to be used in the vine copula construction. If only bivariate Gaussian copulas are used in this construction, the overall joint distribution of the variables will also be Gaussian (Joe, , 1996; Joe et al., , 2010). Since the tail dependence features of the Gaussian model are well-studied in the literature, we focus on cases where the pair copulas are from extreme value or inverted extreme value classes of distributions (Ledford and Tawn, , 1997; Papastathopoulos and Tawn, , 2016). These classes are widely studied in the extreme value literature; while they are not in themselves parametric distributions, they do include a range of well-known parametric examples (Coles and Tawn, , 1991; Cooley et al., , 2010; Ballani and Schlather, , 2011). Bivariate extreme value distributions exhibit asymptotic dependence, while their inverted counterparts exhibit asymptotic independence. Studying these two classes is therefore sufficient to reveal a rich variety of structures within the vine copula framework.

Vine copula models provide an example of when the joint distribution function of the variables generally cannot be calculated analytically. Moreover, the joint densities corresponding to certain subsets of the variables often do not have closed forms. To study the tail behaviour of these models, we calculate for several examples, through the application of the geometric approach of Nolde, (2014). Our investigation reveals interesting features of the shape of the gauge function in (3) for vine copula models.

Having introduced the geometric methodology for studying extremal dependence in Section 2, and provided an overview of vine copula modelling in Section 3, the remainder of the paper is structured as follows. In Section 4, we present calculations and results for cases where each pair copula is from the inverted extreme value family of distributions. In higher than three dimensions, the underlying graphical structure of the copula is a further consideration, and we also present results for inverted extreme value pair copulas here, with two different types of underlying vine structure. In the trivariate and higher-dimensional examples, we present results for inverted logistic examples as a special case. In Section 5, we return to the trivariate case, presenting results for vine copulas constructed from combinations of extreme value and inverted extreme value pair copulas.

2 Geometric approaches for calculating

2.1 The geometric approach of Nolde, (2014)

Nolde, (2014) proposes a method to calculate the coefficient of tail dependence based on the shape of scaled random samples from the vector . This follows earlier work by Balkema and Nolde, (2010), who showed that the limiting shape of the sample cloud could be used to determine the presence of asymptotic independence. Theorem 2.1 of Nolde, (2014) provides the result for marginal distributions with Weibull-type tails. We take a simplified approach by focusing on the special case where all margins have standard exponential distributions, which is possible without losing information about the extremal dependence properties of the variables.

Interest lies with the gauge function , satisfying equation (3). In this case, we consider the scaled random sample , as , with the scaling function chosen due to the exponential margins. The sample cloud converges onto the compact set , which also has the property of being star-shaped, i.e., if , then for all . We denote the part of the boundary of this set where the gauge function equals one by .

Nolde, (2014) shows that the coefficient of tail dependence can be calculated as

| (4) |

which Nolde and Wadsworth, (2020) show is equivalent to

| (5) |

The case where occurs if and only if , corresponding to the intersection in (4) occurring when all variables are equal, i.e., when for all . We also note that the quantity will always provide a lower bound for , and if , then it must be the case that . When analytical minimisation of is difficult or impossible, numerical investigation can be used to determine where the minimum occurs.

This numerical minimisation may be undertaken using optimisation software such as optim in R. Implementation is simpler using the second form in (5), i.e., with , and one can check that the numerical optimisation gives . It is advisable to compare results across a range of starting values of to ensure convergence. If convergence is not reached, an alternative is to carry out the investigation across the range of subspaces of interest, i.e., where different subsets of are equal to one, and to compare these results. While it is clearly preferable to use theoretical results, where this is not possible, this numerical approach can be useful. Moreover, where theoretical results are difficult to obtain, numerical studies may provide additional insight that can facilitate analytical calculations.

We subsequently drop the subscript from the set , density and gauge function when discussing the overall vector of variables , i.e., when .

2.2 Lower dimensional subsets

The method of Nolde, (2014) can only be used to calculate the coefficient in cases where the density can be obtained analytically. In some cases, including many vine copula examples, we may have the form of , but no closed form of for certain subsets , so the method cannot be directly applied to obtain . Nolde and Wadsworth, (2020) use results on projections of sample clouds to show that the gauge function can be obtained from the gauge function for any set with , by

| (6) |

Once this gauge function has been obtained, the remainder of the procedure to calculate continues as in Section 2.1. In particular, this implies that

| (7) |

If the gauge function still cannot be obtained analytically via the minimisation in (6), numerical methods can again be exploited. Numerical calculation of will require optimising equation (6) within equation (5), as in (7), and the result of this optimisation procedure may again be used to motivate the theoretical calculation of . In Sections 4 and 5 we will study cases where we have the form of and wish to deduce , where the analytical form of is not known. If theoretical arguments or numerical investigations suggest that the minimum in (5) occurs when , i.e., , one can focus solely on this case in (7). That is, only calculation of is needed, which may be possible even when the minimisation in (6) over the full range of values is not. In addition, if we can find any with and , such that , then this must correspond to the required minimum, and .

2.3 Bivariate examples

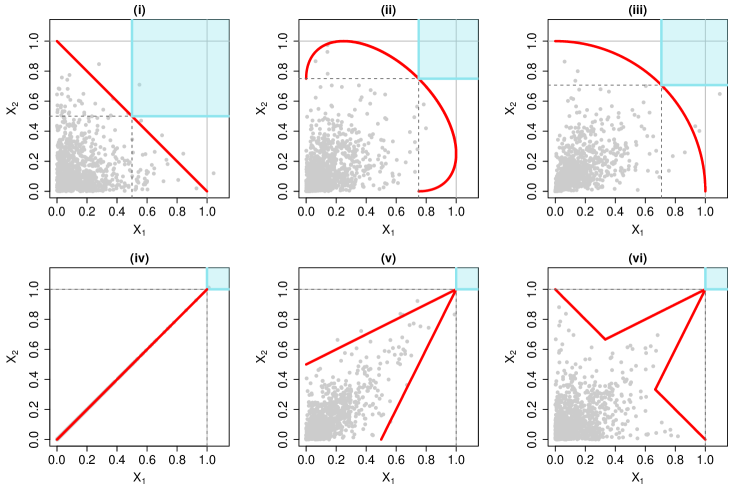

To demonstrate the geometric approach discussed in Section 2.1, we consider six bivariate examples, corresponding to three distributions belonging to each of the asymptotic independence and asymptotic dependence classes. We also comment on interesting features relating to the shape of the set in each case. In this section, we generally use plots to determine where the intersection in (4) occurs, but we note that equation (5) also holds in all cases.

We begin with the example of independent exponential variables, where it is straightforward to obtain the gauge function as , i.e., the set corresponds to the straight line for . This is demonstrated in case (i) of Fig. 1, and it is clear that the smallest value of such that and do not intersect yields . In Fig. 1 we plot scaled samples of size 1000 from the various models; note that since the gauge function calculations are based on asymptotic results, some of this finite sample may lie outside the set .

As a second asymptotically independent model, we consider a bivariate Gaussian copula model having exponential margins and covariance matrix with and . Nolde, (2014) shows that this model has gauge function

with . This is demonstrated in case (ii) of Fig. 1 for . Minimisation as in (5) reveals that , corresponding to the known coefficient for a Gaussian model (Ledford and Tawn, , 1996).

Examples (iii), (v) and (vi) are based on the class of bivariate extreme value distributions, which in exponential margins, have a joint distribution function written as

| (8) |

for and some exponent measure that is homogeneous of order and takes the form

| (9) |

for , and spectral distribution satisfying the moment constraint . We let , and denote the derivatives of the exponent measure with respect to the first, second and both components, respectively, where these are assumed to exist. One example of a method belonging to this class is the logistic distribution, with exponent measure

| (10) |

see Tawn, (1988). We return to the extreme value distribution in case (v), but first use these results to consider a final asymptotically independent model: the inverted bivariate extreme distribution. Models of this class are obtained by exchanging the upper and lower tail features in extreme value distribution (8). In exponential margins, the model has distribution function

for . Differentiating with respect to both components to obtain the density , we have

| (11) |

as , by exploiting the homogeneity of the exponent measure. That is, the gauge function is given by , for . For the bivariate inverted logistic example, this corresponds to the gauge function . This is demonstrated in case (iii) of Fig. 1 for . The smallest value of such that and do not intersect is , occurring when . This corresponds to the known value of for this copula (Ledford and Tawn, , 1996).

We now turn our attention to asymptotically dependent models, the most simple example of which corresponds to perfect dependence, demonstrated by case (iv) of Fig. 1. In this case, the density does not exist, but since the set describes the boundary of the scaled sample cloud, it is clear that this corresponds to the line , and that considering the intersection of and in the usual way gives .

Returning to the bivariate extreme value copula, with exponent measure (9), general results cannot easily be derived, as illustrated in Section G.2 of the Supplementary Material. However, progress is possible if we assume that the corresponding spectral density places no mass on or and has regularly varying tails, as in Heffernan and Tawn, (2004) and Simpson et al., (2020). Specifically, let

| (12) |

for and . In this case the gauge function, as shown in Section G.2 of the Supplementary Material, is

| (13) |

. For the logistic model with dependence parameter , we have . Hence the gauge function is

for . In this case, the point satisfies , and since both variables are at most 1 in the set , we must have , which is the only possible value under the known asymptotic dependence of this model. This is demonstrated in case (v) of Fig. 1 for , with being piecewise linear. In the case where in (13), the set will no longer be symmetric about the line , but will still correspond to two straight lines with intercepts with the axes at and , and intersection at the point . This still corresponds to .

We finally consider the asymmetric logistic model (Tawn, , 1988) with exponent measure

with , and . This model does not satisfy the condition used when calculating the gauge function for bivariate extreme value copulas, that the spectral density places no mass on or , since and . However, calculating the gauge function for this model directly, we obtain

for and all . We note that this gauge function does not depend on the values of and , i.e., the mass on the boundaries of . This is demonstrated by case (vi) of Fig. 1 for , and we again find that since , the coefficient of tail dependence has value . The bivariate asymmetric logistic copula is essentially a mixture of independence and logistic models of cases (i) and (v); this is reflected in the gauge function, which is a combination of the gauge functions corresponding to the two mixture components.

The geometric approach for deriving extremal properties from the gauge function does extend to cases where a joint distribution has singular components, i.e., mass on lower dimensional subspaces. While the density representation is convenient when it exists, more general theory for deriving the limit set is available; see e.g., Balkema et al., (2010). Examples with singular components include perfect dependence (case (iv) of Fig. 1), and the copula of the Marshall-Olkin distribution (Marshall and Olkin, , 1967), which arises as the limit of the asymmetric logistic distribution as . For this copula, and a bivariate extreme value copula with underlying measure placing all of its mass at a finite set of atoms, the set is identical to that of the independence case, but with a line from to , inclusive. As the set contains , i.e., , we have . For a copula based on the inverted bivariate extreme value distribution with underlying measure placing all its mass at a finite number of atoms, the value follows from Ledford and Tawn, (1996), with (unless ), and the asymptotic shape of the sample cloud following from results in Kereszturi and Tawn, (2017). However, in such cases, extremal properties are much easier to derive directly from the joint distribution function, without studying the gauge function.

In the bivariate examples we have studied here, the intersection of interest between the sets and occurred when and were equal, but we note that this is not the case in general. For sets corresponding to cases (i)-(v) are all convex, but this is not true of the asymmetric logistic model in case (vi). This links to another interesting feature of the sets , which is that they can be used to consider the possible values of one variable when the other variable is large. To study the case where takes its largest values, we can consider the intersection of the set with the line . For the independence and inverted logistic examples, cases (i) and (iii), we see that the intersection occurs at , so the largest values of occur only with the smallest values of , while for the Gaussian case (ii), the intersection occurs at , meaning that larger (although not the most extreme) values of occur when takes its largest values. For all three asymptotically dependent cases, the two variables take their largest values simultaneously, with intersection at , but for the asymmetric logistic example of case (vi), the line intersects the set twice, indicating that can take either its smallest or largest values with the largest values of . Nolde and Wadsworth, (2020) elaborate further on how the shape of links to a broader description of extremal dependence than the coefficients .

3 Vine copula modelling

3.1 Preliminaries

As discussed in Section 1, our aim is to apply the methods of Section 2 to investigate some of the extremal dependence properties of vine copulas. These are models for variables, created using bivariate copulas according to an underlying graphical structure. We provide a summary of the key ideas here, where our focus is on models for continuous variables.

By Sklar’s theorem (Sklar, , 1959), the joint distribution function of variables with , for , can be written in terms of a unique copula function as

Differentiating this with respect to each variable gives the joint density function as

| (14) |

for , , representing the marginal densities, and copula density

As outlined by Aas et al., (2009), the joint density can be decomposed as

| (15) |

and by repeatedly applying decomposition (14) to each term in the right-hand side of (15), it is possible to write the joint density of the variables in terms of only marginal and bivariate copula densities. For instance, in the bivariate case, from (15) and from (14), so that

Similarly, in the trivariate case,

Again following Aas et al., (2009),

so that a full decomposition of is given by

| (16) |

For modelling purposes, different bivariate copula densities can be chosen for each of , and , and different marginal distributions can be selected for each variable, i.e., , , and , showing the flexibility in this class of model. A similar process can be applied to obtain models in higher than three dimensions in terms of bivariate copulas.

The decomposition of density is not unique, as we have a choice about the conditioning variable used in each step of the decomposition. Bedford and Cooke, (2001, 2002) proposed an approach to address this issue through the use of regular vines, a class of graphical model, to represent the underlying structure of certain decompositions and help to systematize the different possibilities. Construction (16) gives an example of a vine copula form in the trivariate case. An introduction to the graphical representation of vine copulas is given in Cooke et al., (2010), with formal definitions provided in Kurowicka and Cooke, (2006). We discuss this further in Section 3.2.

3.2 Graphical representations of vine copulas

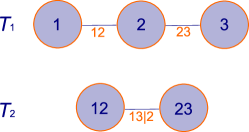

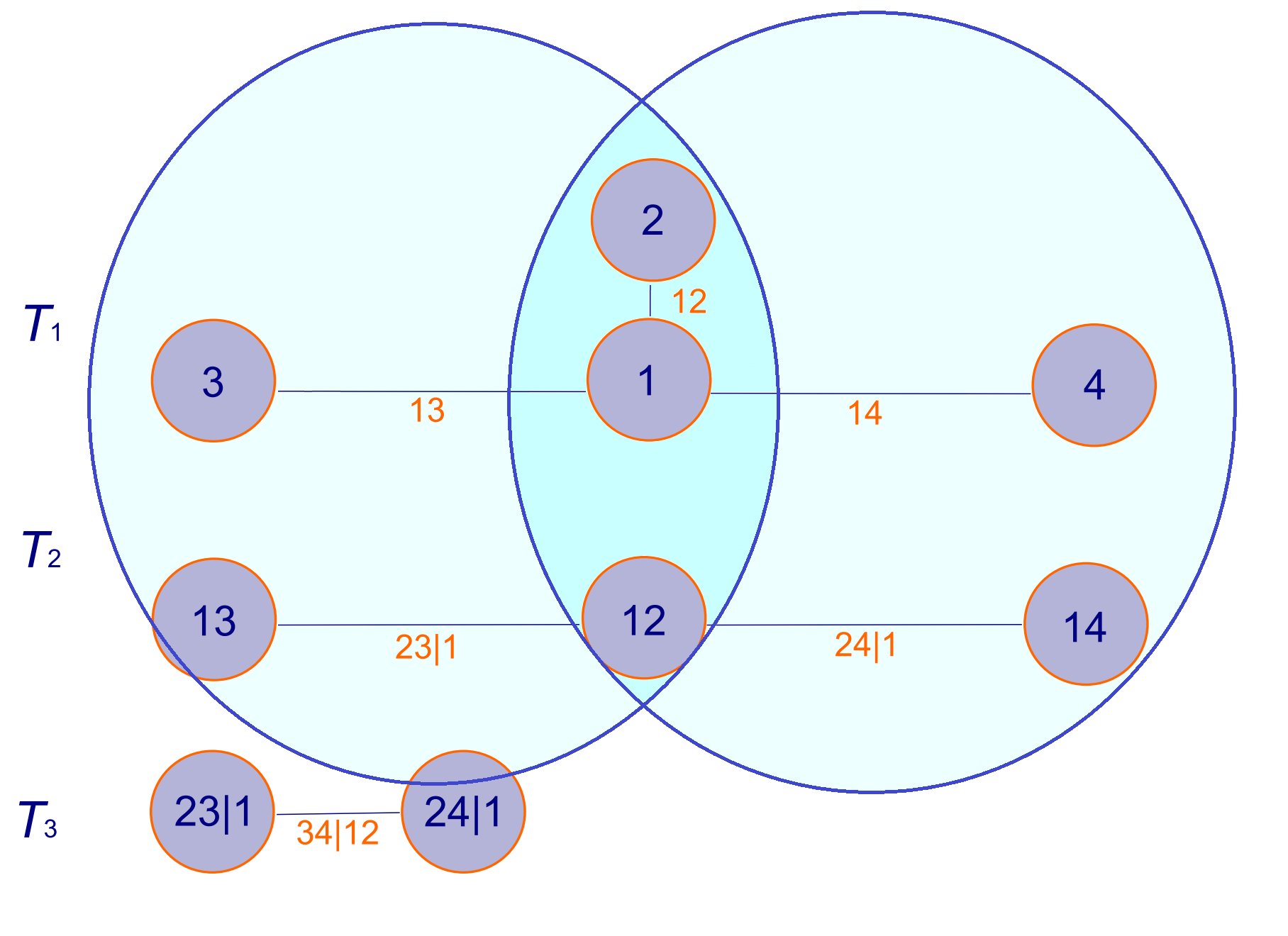

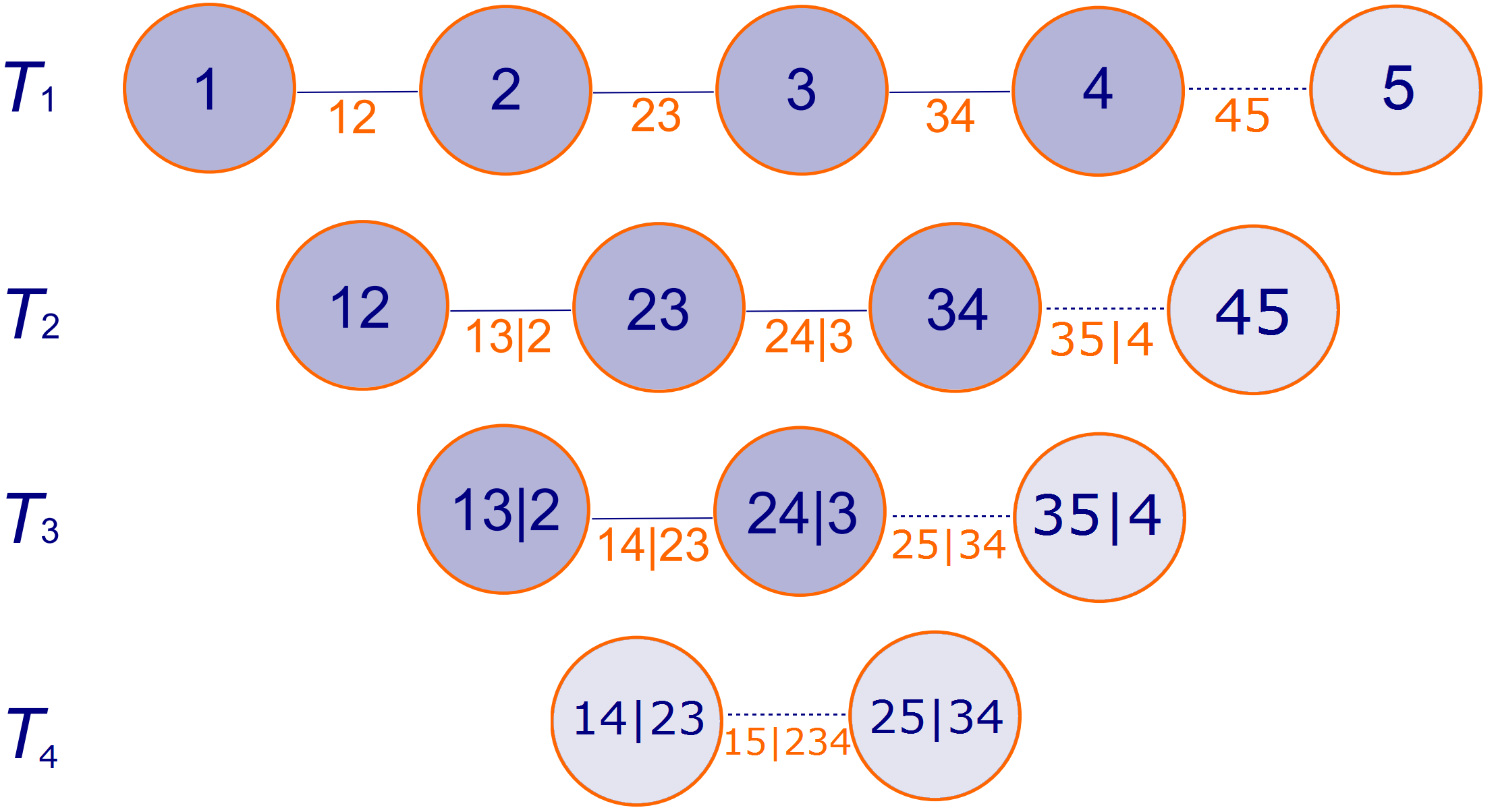

Suppose we are interested in modelling variables . A regular vine, first introduced by Bedford and Cooke, (2002), corresponding to these variables consists of connected trees labelled , with tree having nodes and edges. The nodes in tree each have a different label in the set , and the edges are labelled according to the pair of nodes they connect. The labels of the nodes in tree correspond to the labels of the edges in tree , for , creating a nested structure among the set of all trees. In tree , , the pair of nodes connected by each edge will have variable labels in common; these become the conditioning variables in the corresponding edge label of . The underlying vine structure for copula (16) is shown in Fig. 2.

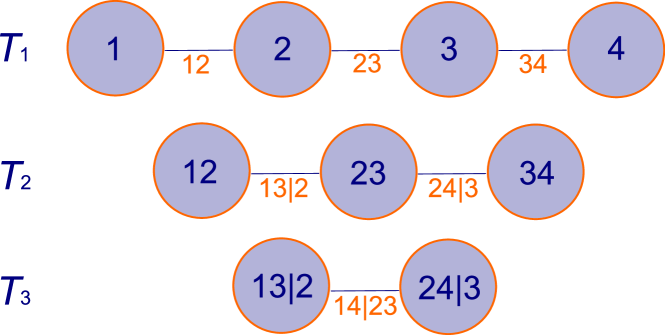

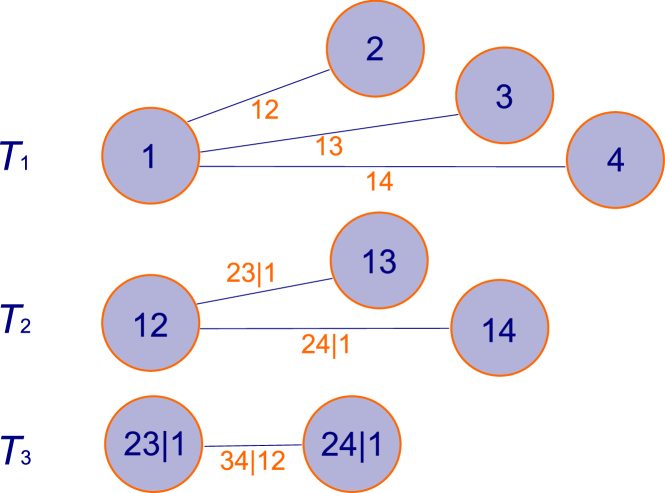

Each edge in a regular vine can be used to represent one of the copula densities used in the decomposition of the joint density. There are certain subclasses of vine copula that are often of interest. These include -vines, where each tree is a path, and -vines, where each tree has exactly one node that is connected to all other nodes. Fig. 3 gives an example of these vine structures for . For the -vine example, the corresponding decomposition of the density is

with the result for the -vine found in a similar way. More detail on regular vines and the subclasses of -vines and -vines can be found in Cooke et al., (2010).

For modelling variables, there are possible -vines, and the same number of possible -vines (Aas et al., , 2009). For , all vine structures are equivalent, with different decompositions only occurring with different labelling of the nodes. For , all possible structures fall into either the -vine or -vine category. For , the more general regular vines provide a greater range of possible structures, with structure selection considered by Dißmann et al., (2013); Zhu et al., (2020), for example, but we only study -vines and -vines here.

4 Vine copulas with inverted extreme value copula components

4.1 Trivariate gauge calculation

We now turn our attention to applying the methods discussed in Section 2 to calculate the coefficient of tail dependence for various vine copulas, initially focusing on cases where all bivariate copulas used in the construction belong to the family of inverted extreme value models. Our first vine copula gauge function calculation is for a trivariate vine, with graphical structure as in Fig. 2 and density (16), constructed from three inverted extreme value pair copulas.

A bivariate inverted extreme value copula with exponent measure has the form

Let , and denote the derivative of the exponent measure with respect to the first, second, and both components, respectively. Differentiating with respect to the second component gives the conditional distribution function

| (17) |

for , and subsequently differentiating with respect to the first component gives the copula density

| (18) |

In calculating values of for a trivariate vine with density (16), we are interested in the behaviour of

| (19) |

for , as . In Section B of the Supplementary Material, we show that the gauge function of a trivariate vine copula with three inverted extreme value components is

| (20) |

where the superscripts of the exponent measures and correspond to the pair copulas used to construct the vine.

We note that a general exponent measure is non-increasing in and , so it follows that is non-decreasing in and . From this, we can deduce that (20) is non-decreasing in and , so the minimum required to solve equation (5) must occur when . For , the problem is more subtle. In the following section, we consider an example where all components are taken to be inverted logistic copulas, with the form of their exponent measures given by (10). In this case, we demonstrate that the minimum also occurs at , and suggest that a similar approach could be taken for other cases.

4.1.1 Inverted logistic example

Let , and have dependence parameters , respectively. Then the corresponding gauge function is

| (21) |

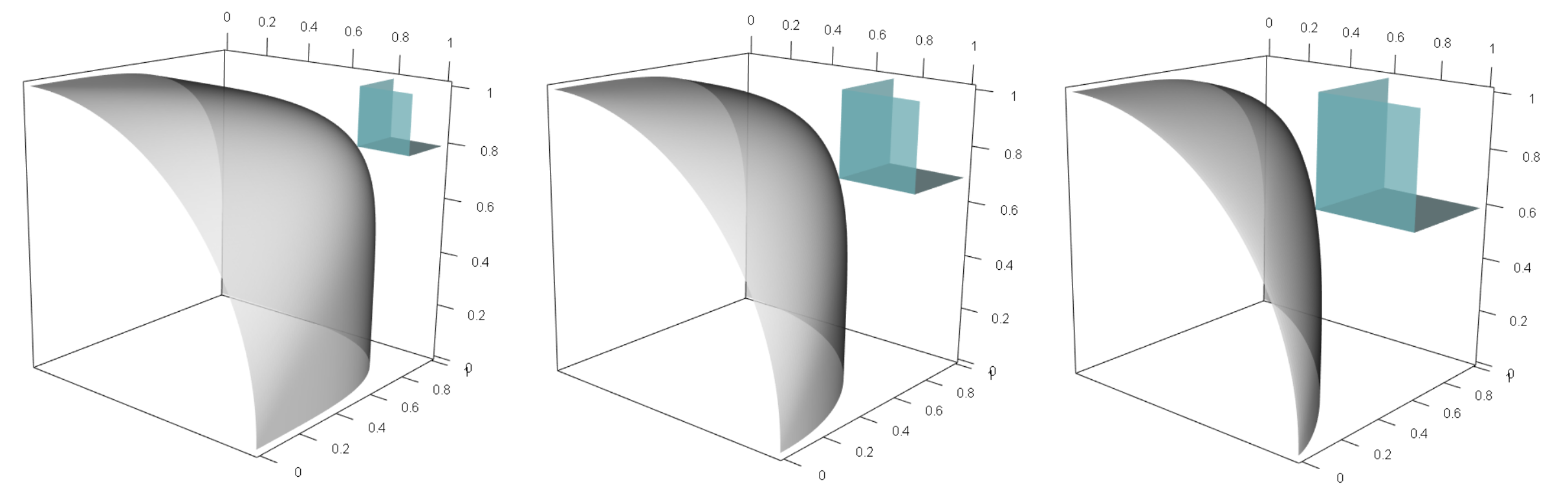

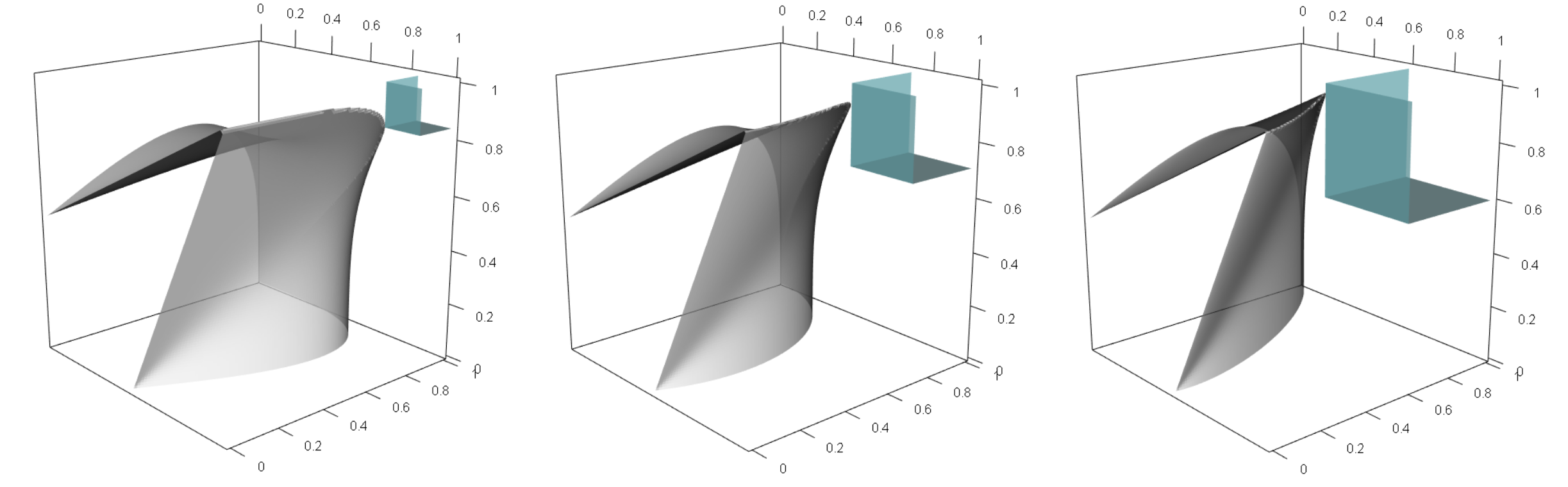

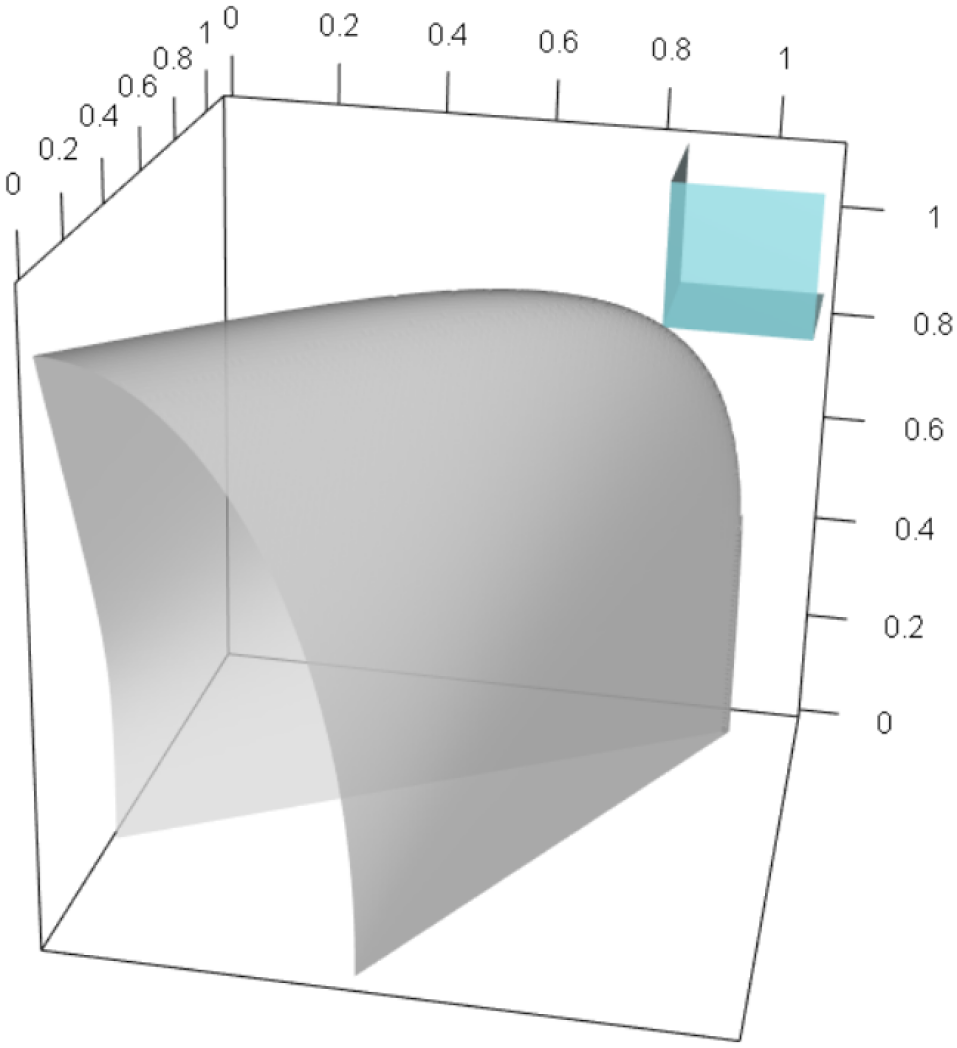

Fig. 4 demonstrates the sets for this gauge function, with , and . As was the case with the bivariate inverted logistic copula, the surface corresponding to the set is smooth and convex, and considering the intersection of with the lines , , shows that each variable takes its largest values while the other two take their smallest.

From Section 4.1, we already know that the minimum in (5) occurs when , since is increasing with respect to both these variables. In Section C of the Supplementary Material, we show that the gauge function is also increasing with respect to . Hence, we know that the minimum occurs at , i.e., that the intersection of and occurs on the diagonal . This is supported by the plots in Fig. 4, and yields

| (22) |

As , , corresponding to complete independence, and as , .

4.1.2 Calculation of

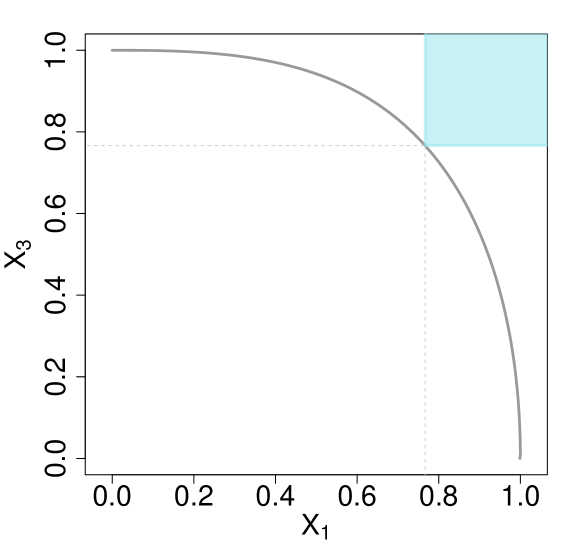

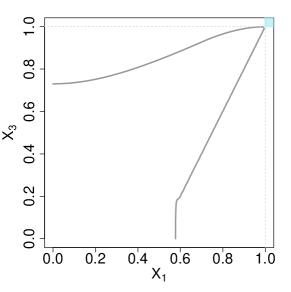

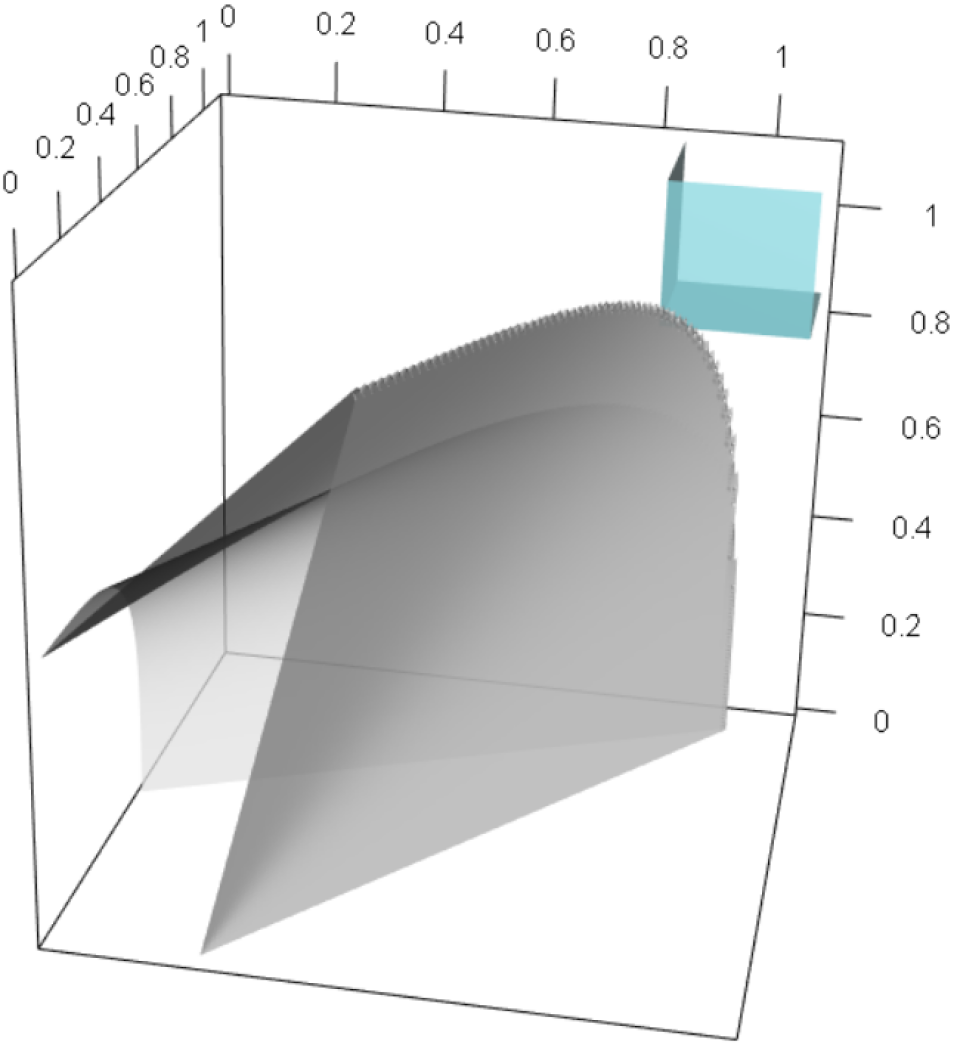

We now consider the coefficient of tail dependence for the variables and , i.e., the pair that is not directly linked in tree of the underlying vine. The joint density of and cannot be found analytically for a trivariate vine with inverted logistic pair copula components; we therefore use the method discussed in Section 2.2, with the gauge function for this pair of variables being , for in (21). To demonstrate the boundary of the scaled sample cloud, we carry out this minimisation numerically. In the left panel of Fig. 5, we plot the set for , chosen to match the parameter values for the central panel of Fig. 4.

To calculate , we follow the steps in Section 2.2, where we have . We have already seen that is increasing with respect to and , so we focus on , and have . That is,

with satisfying , i.e.,

| (23) |

In Section C of the Supplementary Material, we show that (23) has a unique solution that lies in the range . In general, equation (23) has no closed form solution, except in the case where , which leads to

but it can be solved numerically when . In the right panel of Fig. 5, we demonstrate the resulting value of for a variety of and values. We note that , revealing flexibility in the asymptotic independence features this model can capture. In particular, for the case, , as .

4.2 Higher dimensional results

We now extend the results of Section 4.1 by considering vine copulas with dimension constructed from inverted extreme value pair copulas, with the aim being to find the gauge function and value of in each case. We focus on copulas with two types of underlying structure: the class of vine copulas known as -vines, where all trees in the vine are paths; and -vines, which have exactly one node that is connected to all other nodes in each tree. These correspond to the two classes demonstrated in Fig. 3 for the case . In the final part of this section, we demonstrate the values of calculated using these gauge functions for both classes of model.

4.2.1 Gauge functions for -vines

A -dimensional -vine is made up of trees, labelled , and a total of edges. We suppose that the pair copula represented by each edge is an inverted extreme value copula, with the superscript on the exponent measure corresponding to the edge-label, as in the trivariate case. For the four-dimensional example in Fig. 3, we have

| (24) |

We note that several of these terms can be thought of in terms of lower-dimensional vine copulas that are subsets of the four-dimensional vine. In particular, all terms in the trivariate formula (19) for the set of variables appear in (24). Let denote the joint density corresponding to this trivariate case. The density corresponding to variables also comes from a trivariate vine copula equivalent to up to a labelling of the variables. The sections of the four-dimensional vine corresponding to these two trivariate subsets are highlighted in Fig. 6, and can be thought of as sub-vines of the overall vine copula. We note that these two sub-vines overlap in the centre, as they share the variables . This suggests that if we try to represent for the overall model in terms of and , we will count the section corresponding to twice, with denoting the joint density of . Taking this inclusion-exclusion into account, equation (24) can be simplified to

| (25) |

In Section D of the Supplementary Material, we show that the gauge function can be written in terms of the gauge functions of the three sub-vines highlighted in Fig. 6 and the exponent measure corresponding to the pair copula in tree . In particular,

| (26) |

for . For -vine copulas, this same structure can be extended to higher dimensions, creating an iterative formula for calculating the gauge function; this is stated in Theorem 1.

Theorem 1.

The gauge function for a -dimensional -vine with inverted extreme value pair copula components is given by

for , .

4.2.2 Gauge functions for -vines

Using similar arguments as for the -vines in Section 4.2.1, we can construct an iterative formula for the gauge functions of -dimensional -vines. We now consider the sub-vines as corresponding to the sets of variables and , which overlap at . This is demonstrated in Fig. 7 for the four-dimensional case. Following the same steps as in the previous section, we obtain the gauge function

with , .

4.2.3 Calculating for -dimensional -vines and -vines with inverted logistic components

As for the trivariate vine copula examples with inverted logistic pair copula components, numerical results suggest that the intersection of the set and for these -vines and -vines occurs when . As before, this suggests that in this case.

Due to the nested structure of the gauge functions, the value of can be written in terms of the values of for various sub-vines of the copula, and the exponent measure corresponding to tree of the vine. In particular, for -vines, we have

| (27) |

and for -vines,

Setting for , we now have an iterative method for calculating the values of for these classes of model for dimensions.

As an example, we consider the case where all the pair copulas of the vine are inverted logistic with the same dependence parameter . In this case, the known value of for the bivariate copula is . We can therefore use our iterative formulas to calculate for higher dimensional vine copulas. Since the exponent is homogeneous of order , the expression for in (27) in this case simplifies to

| (28) |

and we can use the iterative method to derive the exact value of for any -dimensional -vine copula. For this example, we can extend the results to higher -dimensional vine copulas, yielding, for ,

| (29) |

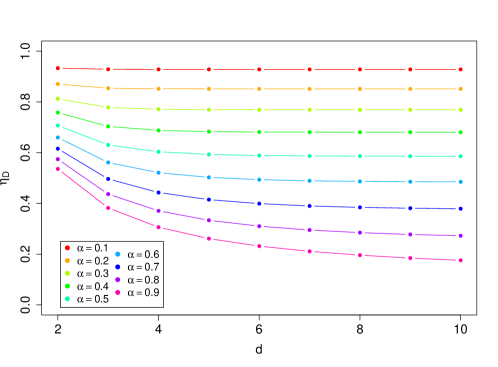

which can be shown to be decreasing in . We prove result (29) by induction in Section F of the Supplementary Material. We note that when the pair copulas, and therefore the corresponding exponent measures, are all taken to be identical, the value of is the same for the -vines and -vines of the same dimension. These values are demonstrated in Fig. 8 for and , where we have in all cases, corresponding to asymptotic independence. Complete independence in the -dimensional vine copula corresponds to . We see from Fig. 8 that for , we approach this case, while for , the values of are close to 1, corresponding to strong residual dependence. These models are therefore able to capture a range of sub-asymptotic dependence strengths in the asymptotic independence case.

5 Trivariate vine copulas with inverted extreme value and extreme value copula components

5.1 Overview

We have so far focused on the tail dependence properties of vine copulas with inverted extreme value pair copula components. Now, we investigate these same properties for trivariate vine copulas where the components are either extreme value or inverted extreme value copulas. We consider five such cases, which along with the results in Section 4.1 cover the range of possible scenarios. In Section 5.2.1, the two copulas in tree of Fig. 2 belong to the inverted extreme value class, and there is an extreme value copula in tree ; tree has one extreme value and one inverted extreme value copula in Sections 5.2.2 and 5.2.3, with the copula in tree being either inverted extreme value or extreme value, respectively; and in Sections 5.2.4 and 5.2.5, both copulas in tree are from the extreme value family with the copula in tree being inverted extreme value and extreme value in the respective sections. This section will therefore consist of a series of examples, and the gauge functions resulting from these vine structures generally have a complicated form, with the corresponding sets exhibiting interesting shapes including non-convexity and non-smoothness. This differs from other well-known examples such as the multivariate Gaussian distribution. The gauge function calculations are provided in Sections G to I of the Supplementary Material for each of these cases, with the extreme value components satisfying conditions analogous to (12). Specifically, let , , denote the spectral density for each pair copula component. We assume that each of these densities has as and as , for some and .

Our results are summarised in Section 5.2, where we also investigate the corresponding values of and for logistic and inverted logistic examples, with exponent measure (10). In some subsections, this is achieved by obtaining results for more general gauge functions. In other cases this is not possible, and we focus only on the (inverted) logistic examples, but suggest that similar strategies could be used for other cases. Whether the copula is logistic or inverted logistic, we denote the parameters associated with exponent measures of copulas , and by , respectively. We note that in the logistic case, we have ; and .

5.2 Gauge functions for trivariate vines with extreme value and inverted extreme value components

5.2.1 Inverted extreme value copulas in ; extreme value copula in

The calculations in the Supplementary Material demonstrate that the gauge function is

with , and

To calculate , we must here consider two separate cases. First, we assume that , so the gauge function simplifies to

Since , is non-decreasing in and we can set to find the solution of (5). We therefore need to minimise

such that . Now, the function is non-increasing in , which should therefore be taken to be as large as possible. Since is non-decreasing in , this function should also be as large as possible, i.e., the largest value of occurs when , and the gauge function becomes

Again, this is non-decreasing in , so the minimum occurs when , i.e., . For the case where , by a similar argument, . In summary, we have

For the value of , we observe that

As discussed in Section 2.2, this is the smallest possible value of , and therefore must be our required minimum. We therefore have .

For an example with logistic and inverted logistic components, the gauge function is

with and .

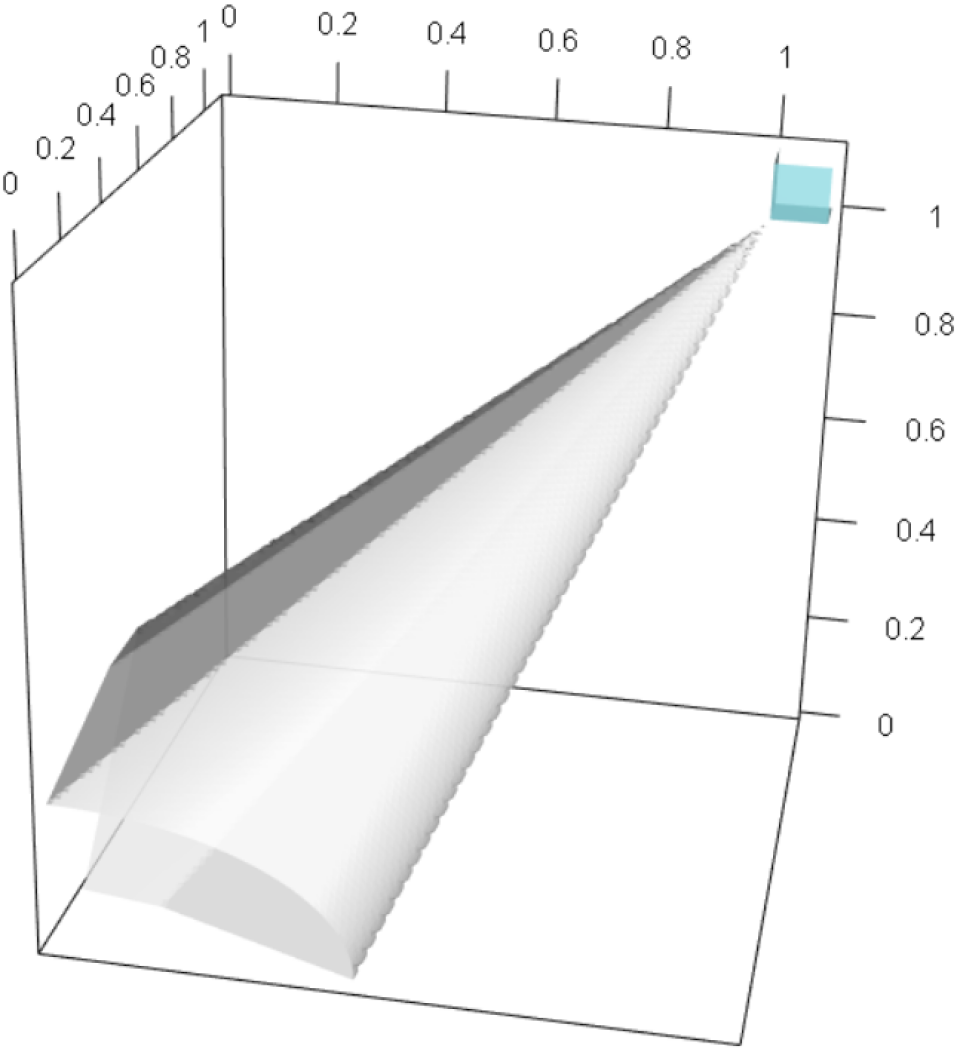

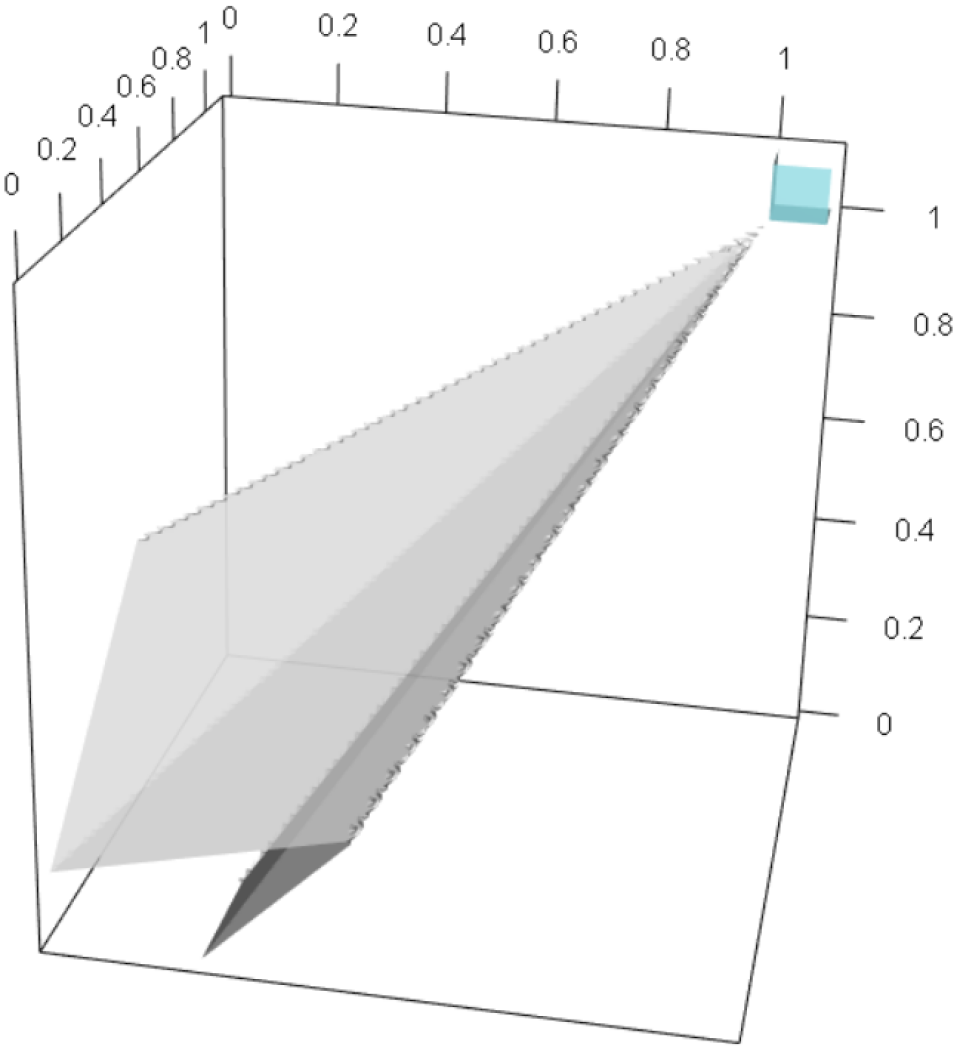

In Fig. 9, we demonstrate the set for this example, with , and , where the surface corresponding to the set turns out to be non-convex. The plots in Fig. 9 support our analytical calculations. The intersection of and occurs at in the first panel with , and in the remaining two panels, where . The gauge function for the pair of variables is demonstrated in Fig. 10. This plot supports that , and we note the non-convex shape of .

5.2.2 Extreme value and inverted extreme value copulas in ; inverted extreme value copula in

From the calculations in the Supplementary Material, the gauge function for this model is

To find , there are two cases to consider. If , it is clear that the function is decreasing in , which should therefore be taken to be as large as possible by fixing . The gauge function then simplifies to

which is non-decreasing in both and , so we find the minimum by setting , yielding . Similarly, for , the gauge function is non-decreasing in , and we can again fix with the resulting gauge function being

Again, this is non-decreasing in and , so the minimum is given by . Hence,

For the case with logistic and inverted logistic components, the gauge function is

An example of this gauge function is shown in Fig. 11(a), and we have .

We now consider the bivariate coefficient of tail dependence between and . Since we have already shown that , we must have , and can focus only on the case where . Here, the gauge function is increasing in and , so we fix , and should minimise the function

for . We therefore find that , with such that

Following an argument almost identical to the one presented for the calculation of in Section 4.1.2, this equation has a unique solution, with .

5.2.3 Extreme value and inverted extreme value copulas in ; extreme value copula in

The gauge function for this copula is

with

so that for the case with logistic and inverted logistic components, we have

As in the previous example, we consider the two cases and separately. In the former, the gauge function increases with , so that the minimum required to obtain occurs when . On the other hand, the function is decreasing with respect to , which must therefore take its largest possible value, i.e., we can fix . This implies we should focus on minimising

under the constraint that . We have

If we solve the equation , we obtain the root , and note that if and only if . In this case, the minimum value of is given by

On the other hand, if , for , so is an increasing function of , and the minimum occurs at , i.e., . In summary, if , we have

| (30) |

For , the problem spilts into a further two cases. If , the gauge function becomes

This is an increasing function of , but a decreasing function of . These two variables should therefore take their smallest and largest possible values, respectively. This occurs with equality at , and an equivalent argument holds for the case. To obtain the required minimum, we can therefore focus on a simplified version of the gauge function, i.e.,

with . The function is increasing with respect to both and , so we have

We now have two candidates for the required minimum of the full gauge function; either , or the form given in (30). For , it is straightforward to see that . For , we have , , and , so

Hence, we find that the minimum in (5) occurs when , and . This is supported by the plot in Fig. 11(b), and suggests that the inverted logistic copula in tree particularly controls the level of asymptotic independence in the overall model.

We now consider . Following the example in Section 5.2.2, we can focus on the case where . Moreover, by a similar argument to the one used in the calculation of , we only need to consider the case where , yielding

Since these functions are increasing in and , respectively, we set . Hence, the minimum of the gauge function corresponds to , with such that . We therefore have

We note that if , we have for . Moreover, and . Hence, is an increasing function for , and the equation has a unique root in the range . This also implies that .

5.2.4 Extreme value copulas in ; inverted extreme value copula in

The gauge function in this case is

with and

For this gauge function, we observe that , which implies that . Moreover, if , then for any set with . As such, we also find that in this case. This result agrees with the findings of Joe et al., (2010), who show that a vine copula will have overall upper tail dependence if each of the copulas in tree also have this property and the copula in tree has support on , as is the case here.

For the case with logistic and inverted logistic components,

with . This is demonstrated in Fig. 11(c).

5.2.5 Extreme value copulas in ; extreme value copula in

The gauge function here has the form

with and

As for the previous case, we note that , which implies that . For a trivariate vine consisting of three logistic pair copulas, this gives the gauge function

with ; see Fig. 11(d) for an example.

6 Discussion

The aim of this paper was to investigate some of the tail dependence properties of vine copulas, via the coefficient of tail dependence of Ledford and Tawn, (1996). We demonstrated how to apply the geometric approach of Nolde, (2014) to calculate these values from a density, and applied further theory from Nolde and Wadsworth, (2020) for cases where the joint density of cannot be obtained analytically, but the joint density of with is known. While values of allow us to deduce that there is asymptotic independence between the variables , these geometric approaches do not enable distinction between asymptotic independence and asymptotic dependence when .

We focused on trivariate vine copulas constructed from extreme value and inverted extreme value pair copulas, and higher dimensional -vine and -vine copulas constructed only from inverted extreme value pair copulas. In the latter case, there is overall asymptotic independence between the variables. In the former case, the copulas in tree particularly influence the overall tail dependence properties of the vine. If there are two asymptotically dependent extreme value copulas in tree , there is overall asymptotic dependence in the vine, as found by Joe et al., (2010), otherwise, all three variables cannot be large together, although other subsets of the variables could be simultaneously extreme.

In Section 1, we discussed the idea of extremal dependence structures, i.e., that different subsets of variables can take their largest values simultaneously while others are of smaller order (Simpson et al., , 2020). Let the extremal dependence structure of the variables be denoted by a set , such that if the variables indexed by can be simultaneously large while the others are small. For the trivariate case, our examples comprise all possible combinations of asymptotically independent and asymptotically dependent pair copulas for the three components of the vine. Throughout the paper, the spectral density of the asymptotically dependent components was restricted to placing mass on as in (12), while asymptotic independence corresponds to mass on and . Our results suggest that the only extremal dependence structures possible in this setting are , , , and . While it is unclear whether the structure is possible for the specific form of the vine we consider (Fig. 2), it is possible with relabelling of the variables, hence its inclusion here. This suggests that each variable is only represented in one of the simultaneously-extreme subsets, and it is likely that this issue would also occur in higher dimensions. Obtaining more complicated structures would require pair copulas that place extremal mass on different combinations of the sets and , such as the asymmetric logistic model of Tawn, (1990) discussed in case (vi) of Section 2.3. However, we conjecture that certain extremal dependence structures will never be possible due to restrictions imposed by the vine.

As an example, suppose we are interested in the structure , so that only pairs of variables can be large simultaneously while the third is of smaller order. If both pair copulas in tree place mass on , the set will be included in the extremal dependence structure (Joe et al., , 2010). This implies that at least one component of must exhibit asymptotic independence to obtain our required structure. However, any pair of variables for which asymptotic independence is imposed in can never be simultaneously extreme, i.e., it would not possible for both and to be included in the dependence structure in this case. The structure can therefore not be achieved, and actually the pairs and cannot both be included in the extremal dependence structure unless also is.

Although the full set of extremal dependence structures may not be captured using vine copulas, it appears that they do allow for a wide range of possibilities, and investigating this topic further presents a possible avenue for future work.

Acknowledgments

This paper is based on work completed while E. Simpson was part of the EPSRC funded STOR-i centre for doctoral training (EP/L015692/1). J. Wadsworth gratefully acknowledges the support of EPSRC fellowship EP/P002838/1. We thank Ingrid Hobæk Haff and Arnoldo Frigessi for helpful discussions, and the Editor, Associate Editor and referees for their comments. In particular, we appreciate feedback from the referees that allowed us obtain some results in closed form that we previously thought could only be found numerically.

Appendix

Appendix A Proof of Theorem 1

A.1 Identifying sub-vines of -vines to construct the gauge function

A -vine is represented graphically by a series of trees, labelled . Each of these trees is a path, and we suppose that the nodes are labelled in ascending order, as in the left plot of Fig. 3 for the case where . Moving from a -vine of dimension to one of dimension involves first adding an extra node and edge onto each tree in the graph. In tree , the extra node has label , and the extra edge label is . In tree the extra node is labelled and the edge is labelled , and this continues until we reach tree , where the extra node is labelled and the corresponding edge is labelled . We finally must also add the tree , with nodes labelled and , and corresponding edge label . This is demonstrated in Fig. 12, for an example where we move from a -vine of dimension four to one of dimension five.

Due to this iterative construction, we can consider a -dimensional -vine in terms of three lower dimensional ‘sub-vines’ in a similar way to in Fig. 6 for the case. In particular, in trees , we have two sub-vines of dimension ; the first corresponds to variables with labels in , and the second to variables with labels in . In the graph, these two sub-vines will overlap in the region corresponding to a further sub-vine, this time of dimension and corresponding to variables with labels in .

In order to calculate the gauge function, we consider the behaviour of , as . By considering these three sub-vines, we see that this can be written as

. Note that this is the form given for the case in equation (25). We can therefore infer that the -dimensional gauge function , defined as as , satisfies

| (31) |

, where, as ,

| (32) |

In Section E of the Supplementary Material, we present two lemmas concerning properties of inverted extreme value copulas that will be used in A.2 to find , and hence the form of the gauge function for a -dimensional -vine with inverted extreme value components.

A.2 Calculation of the gauge function

We claim that the -dimensional -vine has a gauge function of the form stated in Theorem 1. From equation (26), we have already shown this to be the case for . To prove this more generally, we assume that the result holds for the two -dimensional sub-vines of the -dimensional -vine, i.e.,

| (33) |

and

where we have dropped the arguments to simplify notation. Further, we claim that the conditional distribution functions used in the calculation of (32) have the form

| (34) |

and

| (35) |

as , for some not depending on . From result (44), we see that this claim holds for . To prove this more generally, we assume that (34) and (35) hold in the -dimension case, so that as ,

and

for some . Results from Joe, (1996) show that

with result (17) giving the form of the required derivative of an inverted extreme value copula. Applying Lemma 2, with and , we see that for some , as ,

Result (35) can be proved by a similar argument. From results (34) and (35), we see that and can be written in the form required to apply Lemma 1, with and . Applying Lemma 1, we have

and combining this with the gauge function result in (31), we have

hence proving Theorem 1 by induction.

References

- Aas, (2016) Aas, K. (2016). Pair-copula constructions for financial applications: A review. Econometrics, 4(4).

- Aas et al., (2009) Aas, K., Czado, C., Frigessi, A., and Bakken, H. (2009). Pair-copula constructions of multiple dependence. Insurance: Mathematics and Economics, 44(2):182–198.

- Balkema et al., (2010) Balkema, A. A., Embrechts, P., and Nolde, N. (2010). Meta densities and the shape of their sample clouds. Journal of Multivariate Analysis, 101(7):1738–1754.

- Balkema and Nolde, (2010) Balkema, A. A. and Nolde, N. (2010). Asymptotic independence for unimodal densities. Advances in Applied Probability, 42(2):411–432.

- Ballani and Schlather, (2011) Ballani, F. and Schlather, M. (2011). A construction principle for multivariate extreme value distributions. Biometrika, 98(3):633–645.

- Bedford and Cooke, (2001) Bedford, T. and Cooke, R. M. (2001). Probability density decomposition for conditionally dependent random variables modeled by vines. Annals of Mathematics and Artificial Intelligence, 32(1-4):245–268.

- Bedford and Cooke, (2002) Bedford, T. and Cooke, R. M. (2002). Vines–a new graphical model for dependent random variables. The Annals of Statistics, 30(4):1031–1068.

- Brechmann et al., (2012) Brechmann, E. C., Czado, C., and Aas, K. (2012). Truncated regular vines in high dimensions with application to financial data. The Canadian Journal of Statistics, 40(1):68–85.

- Coles et al., (1999) Coles, S. G., Heffernan, J. E., and Tawn, J. A. (1999). Dependence measures for extreme value analyses. Extremes, 2(4):339–365.

- Coles and Tawn, (1991) Coles, S. G. and Tawn, J. A. (1991). Modelling extreme multivariate events. Journal of the Royal Statistical Society. Series B (Methodological), 53(2):377–392.

- Coles and Tawn, (1994) Coles, S. G. and Tawn, J. A. (1994). Statistical methods for multivariate extremes: an application to structural design (with discussion). Journal of the Royal Statistical Society. Series C (Applied Statistics), 43(1):1–48.

- Cooke et al., (2010) Cooke, R. M., Joe, H., and Aas, K. (2010). Vines arise. In Kurowicka, D. and Joe, H., editors, Dependence Modeling: Vine Copula Handbook, chapter 3, pages 37–71. World Scientific.

- Cooley et al., (2010) Cooley, D., Davis, R. A., and Naveau, P. (2010). The pairwise beta distribution: A flexible parametric multivariate model for extremes. Journal of Multivariate Analysis, 101(9):2103–2117.

- Dißmann et al., (2013) Dißmann, J., Brechmann, E. C., Czado, C., and Kurowicka, D. (2013). Selecting and estimating regular vine copulae and application to financial returns. Computational Statistics & Data Analysis, 59:52–69.

- Goix et al., (2017) Goix, N., Sabourin, A., and Clémençon, S. (2017). Sparse representation of multivariate extremes with applications to anomaly detection. Journal of Multivariate Analysis, 161:12–31.

- Heffernan, (2000) Heffernan, J. E. (2000). A directory of coefficients of tail dependence. Extremes, 3:279–290.

- Heffernan and Tawn, (2004) Heffernan, J. E. and Tawn, J. A. (2004). A conditional approach for multivariate extreme values (with discussion). Journal of the Royal Statistical Society: Series B (Statistical Methodology), 66(3):497–546.

- Joe, (1996) Joe, H. (1996). Families of -variate distributions with given margins and bivariate dependence parameters. Lecture Notes-Monograph Series, 28:120–141.

- Joe et al., (2010) Joe, H., Li, H., and Nikoloulopoulos, A. K. (2010). Tail dependence functions and vine copulas. Journal of Multivariate Analysis, 101(1):252–270.

- Kereszturi and Tawn, (2017) Kereszturi, M. and Tawn, J. (2017). Properties of extremal dependence models built on bivariate max-linearity. Journal of Multivariate Analysis, 155:52–71.

- Kurowicka and Cooke, (2006) Kurowicka, D. and Cooke, R. M. (2006). Uncertainty Analysis with High Dimensional Dependence Modelling. Wiley.

- Kurowicka and Joe, (2010) Kurowicka, D. and Joe, H., editors (2010). Dependence Modeling: Vine Copula Handbook. World Scientific.

- Ledford and Tawn, (1996) Ledford, A. W. and Tawn, J. A. (1996). Statistics for near independence in multivariate extreme values. Biometrika, 83(1):169–187.

- Ledford and Tawn, (1997) Ledford, A. W. and Tawn, J. A. (1997). Modelling dependence within joint tail regions. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 59(2):475–499.

- Marshall and Olkin, (1967) Marshall, A. W. and Olkin, I. (1967). A multivariate exponential distribution. Journal of the American Statistical Association, 62:30–44.

- Nolde, (2014) Nolde, N. (2014). Geometric interpretation of the residual dependence coefficient. Journal of Multivariate Analysis, 123:85–95.

- Nolde and Wadsworth, (2020) Nolde, N. and Wadsworth, J. L. (2020). Connections between representations for multivariate extremes. arXiv preprint arXiv:2012.00990.

- Papastathopoulos and Tawn, (2016) Papastathopoulos, I. and Tawn, J. A. (2016). Conditioned limit laws for inverted max-stable processes. Journal of Multivariate Analysis, 150:214–228.

- Simpson et al., (2020) Simpson, E. S., Wadsworth, J. L., and Tawn, J. A. (2020). Determining the dependence structure of multivariate extremes. Biometrika, 107(3):513–532.

- Sklar, (1959) Sklar, A. (1959). Fonctions de répartition à dimensions et leurs marges. Publications de l’Institut de Statistique de l’Université de Paris, 8:229–231.

- Tawn, (1988) Tawn, J. A. (1988). Bivariate extreme value theory: Models and estimation. Biometrika, 75(3):397–415.

- Tawn, (1990) Tawn, J. A. (1990). Modelling multivariate extreme value distributions. Biometrika, 77(2):245–253.

- Zhu et al., (2020) Zhu, K., Kurowicka, D., and Nane, G. F. (2020). Common sampling orders of regular vines with application to model selection. Computational Statistics & Data Analysis, 142:106811.

Supplementary Material for ‘A geometric investigation into the tail dependence of vine copulas’

Emma S. Simpson, Jennifer L. Wadsworth and Jonathan, A. Tawn

Lancaster University

Appendix B Calculation of the gauge function for a trivariate vine copula with inverted extreme value pair copula components

In Section 4.1, we presented the form of the gauge function for a trivariate vine copula constructed from three inverted extreme value components. The exponent measures are denoted , and , corresponding to the links in the vine. Here, we provide a proof of this result.

To investigate the form of the gauge function, we study the asymptotic form of , and for a trivariate vine this can be broken down into the six components in (19). We consider each of these in turn. Working in standard exponential margins, we have , for with . We also have marginal distribution functions , for . Noting that ; the exponent measure is homogeneous of order ; and are homogeneous of order ; and is homogeneous of order , we have

| (36) |

and by similar calculations,

| (37) |

Substituting the marginal distribution functions , , into the corresponding conditional copulas, we have

and similarly,

Setting and defining analogously,

with and not depending on . This implies that

| (38) |

Substituting results (36), (37) and (38) into (19) yields

| (39) |

i.e., the gauge function of this model is

Appendix C Proof that (21) is an increasing function of and that (23) has a unique solution

Our calculations of and in Section 4.1 rely on certain properties of the gauge function in (21), which we prove here. In particular, we are aiming to show that equation (21) is an increasing function of , and that equation (23) has a unique solution.

Let , with the gauge function defined as in equation (21). Then,

Note that for and , , with as and as . Moreover,

so , and by analogy , is a decreasing function of . We also note that the second derivative has the form

Then we have

and

| (40) |

Since , we clearly have . We now consider the two terms within the square brackets in (40) separately. First note that for , and

Secondly, since we have already shown that , it follows that

So all terms in (40) are strictly positive. That is, for all , which implies that is increasing for .

We note that , and we have

Since , for , we have for , so

Without loss of generality, assume that , so and , then

So is increasing in the range , and we have shown that and , so that solution of the equation in equation (23) is unique, and lies in the range .

Moreover, this implies that for , so is increasing for , and therefore , which is required for equation (22) to hold.

Appendix D Proof of (26)

In Section 4.1, we studied gauge functions of trivariate vine copulas with inverted extreme value components. From calculation (39), we know that

| (41) |

, and considering as equivalent to up to labelling of the variables, we have

| (42) |

. Moreover, from the four-dimensional vine, the pair is modelled by an inverted extreme value copula with exponent measure , so by equation (11) we have

| (43) |

As such, is the only term of (24) left for us to study. Joe, (1996) shows that

and

Since we focus on inverted extreme value copulas, the derivatives have the form (17), where the arguments and are replaced by the appropriate bivariate conditional distributions. We find that for some functions not depending on ,

| (44) |

and an analogous result for . These are similar to the results for the trivariate vine, and applying an argument analogous to (38), we see that

| (45) |

We can now substitute the results (41), (42), (43) and (45) into equation (25) to obtain the gauge function for this four-dimensional vine copula as

This gauge function can be written more simply in terms of the gauge functions of the three sub-vines highlighted in Fig. 6 and the exponent measure corresponding to the pair copula in tree . That is,

Appendix E Properties of inverted extreme value copulas

Lemma 1.

For the density of an inverted extreme value copula, of the form (18), if and for some , then as ,

Proof.

∎

Lemma 2.

For the conditional distribution function of an inverted extreme value copula, of the form (17), if and for some , then as ,

for some .

Proof.

for . ∎

Appendix F Proof of result (29)

Proposition 1.

For any even value of ,

Proof.

We first show this is true for . We have

Now we assume the result holds for some with and , and show the result also holds for . We have

Hence the result is proved by induction. ∎

To prove result (29), we first show that it holds for and . In the former case, we have

as obtained by setting in equation (21), and in the latter case we have

as achieved by exploiting equation (28). We now assume the result holds for some and being odd and even, respectively, and show that it also holds for . To make the notation clearer in the proof, we let denote the value of for an -dimensional -vine copula with inverted logistic components with parameter . From equation (28), we have

Under the assumption that (29) holds for , we have

Further, we see that

Hence result (29) is proved by induction.

Result (29) can be simplified further by exploiting sums of geometric series. For the case where is odd, we have

and for even,

Appendix G Properties of extreme value copulas

G.1 Some properties of the exponent measure

Proposition 2.

If the exponent measure has corresponding spectral density placing no mass on , and with as , for some and , then

Proof.

By the definition of the exponent measure,

For and , by Karamata’s theorem, we have

| (46) |

Hence, we have

Moreover, differentiating expression (46) with respect to gives

and we can therefore infer that

∎

Proposition 3.

If the exponent measure has corresponding spectral density placing no mass on , and with as , for some and , then

Proof.

By the definition of the exponent measure,

For and , by Karamata’s theorem, we have

| (47) |

Hence, we have

Moreover, differentiating expression (47) with respect to gives

and we can therefore infer that

∎

G.2 Asymptotic behaviour of

For representing an exponent measure defined as in equation (9), an extreme value copula has the form

Differentiating with respect to the second argument, we have

and differentiating with respect to both arguments yields the copula density

with , and denoting the derivatives of the exponent measure with respect to the first, second, and both components, respectively.

For this class of models, setting exponential margins with , , we have

We impose the assumption that the corresponding spectral density places no mass on or and has regularly varying tails. In particular, that as and as , for some and . By a result from Coles and Tawn, (1991), we have

and can therefore deduce that

| (48) |

To investigate the behaviour of as , we consider three cases; , , and .

Case 1:

Case 2:

Case 3:

These three cases can be combined into a single expression, so that as , we have

G.3 Asymptotic behaviour of

For a bivariate extreme value copula, the conditional distribution function has the form

To investigate the behaviour of as , we again consider three cases.

Case 1:

Case 2:

Case 3:

Appendix H for (inverted) extreme value copulas

In Section 5, we aim to investigate cases where the copula density in tree belongs to either the extreme value or inverted extreme value families of distributions. Here, we denote these by and , respectively. In Section I, we find that we should focus on the conditional distributions and having three different asymptotic forms. In this section, we therefore consider the behaviour of and for and of the form

for , using the results that

and

We also have the assumption that the spectral density corresponding to the copula in tree places no mass on or , and has as , and as , for some and . In the following nine cases, we provide results for the asymptotic behaviour of and , as , for and taking different combinations of the forms stated above.

Case 1: ,

Case 2: ,

Case 3: ,

Case 4: ,

Case 5: ,

Case 6: ,

Case 7: ,

Case 8: ,

Case 9: ,

Appendix I Gauge function calculations for Section 5

In Section 5, we aim to investigate the coefficients and for trivariate vine copulas constructed from inverted extreme value and extreme value pair copulas. We present the necessary calculations here.

For any trivariate vine copula, has the form (19). In our gauge function calculations, we work with variables having exponential margins, so that the first three terms of this expression always satisfy

| (49) |

and we have , for . For inverted extreme value copulas, we have shown in equations (36) and (37) that

| (50) |

and

| (51) |

Recall that in order to investigate the behaviour of the extreme value pair copula components, we impose the condition that the corresponding spectral densities place no mass on or and have regularly varying tails. Let , , denote the spectral density for each pair copula component. We assume that each of these densities has as and as , for some and . In Section G.2 of the Supplementary Material, we show that

| (52) | ||||

| (53) |

and

| (54) | ||||

| (55) |

so that the final term of (19), i.e., , is the only one left for us to consider.

In Section E of the Supplementary Material, we showed that for the components in tree being inverted extreme value copulas, we have

| (56) |

| (57) |

for and . We consider the extreme value case in Section G.3 of the Supplementary Material. Placing the same conditions on the spectral density as for the and calculations, we obtain

| (58) |

and

| (59) |

So, as , the conditional distributions of the extreme value copula in equation (58) tends towards either , or , and expression (59) tends towards , or . We must therefore consider three different cases in our gauge function calculations for any extreme value copula in tree . Based on the asymptotic forms of and for (inverted) extreme value copulas, we focus on investigating for and of the form

for . We provide these results in Section H of the Supplementary Material for all nine combinations of the asymptotic forms of and , and for being either an extreme value or inverted extreme value copula density.

Together, these results provide all the necessary information to calculate the gauge functions. We first demonstrate how to combine all these results to obtain the gauge function of a vine copula with two inverted extreme value copulas in tree , and an extreme value copula in tree , and subsequently find the gauge functions for the remaining cases.

I.1 Inverted extreme value copulas in ; extreme value copula in

For this case, we use results (49), (50) and (51) in equation (19), which gives the form of for a trivariate vine copula. We have

| (60) |

From equations (56) and (57), we see that and , for and . Using results from case 9 of Section H, we deduce that

Combining this with result (60), we find that the required gauge function has the form

i.e.,

with , and

I.2 Extreme value and inverted extreme value copulas in ; inverted extreme value copula in

To calculate the gauge function for this model, we use results (49), (51) and (53) to give the asymptotic form of the first five terms of equation (19). For the final term, equations (57) and (58) give the required form of the conditional distributions, and we apply the inverted extreme value results from cases 3, 6 and 9 of Section H to yield the gauge function

I.3 Extreme value and inverted extreme value copulas in ; extreme value copula in

I.4 Extreme value copulas in ; inverted extreme value copula in

For this model, the first five terms of equation (19) are given by results (49), (53) and (55). Since both of the extreme value copulas in tree can have three different asymptotic behaviours, we require all nine inverted extreme value cases from Section H, and the conditional distributions (58) and (59) to study the final term of (19). The gauge function in this case is

with and