-norm quantile regression screening rule via the dual circumscribed sphere

Abstract

-norm quantile regression is a common choice if there exists outlier or heavy-tailed error in high-dimensional data sets. However, it is computationally expensive to solve this problem when the feature size of data is ultra high. As far as we know, existing screening rules can not speed up the computation of the -norm quantile regression, which dues to the non-differentiability of the quantile function/pinball loss. In this paper, we introduce the dual circumscribed sphere technique and propose a novel -norm quantile regression screening rule. Our rule is expressed as the closed-form function of given data and eliminates inactive features with a low computational cost. Numerical experiments on some simulation and real data sets show that this screening rule can be used to eliminate almost all inactive features. Moreover, this rule can help to reduce up to 23 times of computational time, compared with the computation without our screening rule.

Index Terms:

-norm quantile regression, Screening rule, Dual circumscribed sphere, Computational efficiency.1 Introduction

The availability of high-dimensional data sets has been achieved with the help of advanced technologies. In order to capture different characteristics in these data sets, there are plenty of works about the regularized linear regression, composing of loss function and regularizer. The traditional least square method is sensitive to outliers and heavy-tailed errors in data, so there are many researches about the robust regression. One common choice is the -norm quantile regression, which is given as

where is the quantile function/pinball loss and has been studied in many literatures. See, e.g., Li and Zhu [24], Bellon and Chernozhukoy [4], Fan et al. [7], Koenker [20], Steinwart and Christmann [34][35], Jumutc et al. [17], Huang et al. [16], Mkhadri et al. [26], Yi and Huang [41], Gu et al. [12].

For the -norm quantile regression, there are many algorithms to solve it. For example, Koenker and Ng [20] introduced a modified version of the Frisch-Newton algorithm. Wu and Lange [39] propose the greedy coordinate descent algorithm for the LAD Lasso, a special case of the -norm quantile regression. Yi and Huang [41] use the semismooth Newton coordinate descent algorithm to solve the elastic-net penalized quantile regression, involving the -norm quantile regression. Encouraged by the success of the alternating direction multiplier method (ADMM), Gu et al. [12] build the proximal ADMM and a sparse coordinate descent ADMM to solve the quantile regression with different type regularizer, such as norm, adaptive norm and the folded concave regularizer. Koenker [21] set up an R package (quantreg) for solving the quantile regression. There are no doubt that the standard matlab software for disciplined convex programming CVX (Micheal and Stephen [25]) can be used to solve the -norm quantile regression. Nevertheless, it is a challenging work to efficiently solve the -norm quantile regression in ultra high-dimensional settings.

To speed up the computation of the regularized linear regression in ultra high-dimensional data sets, screening rules are proposed to eliminate inactive features. See, e.g., Fan et al. [9], Ghaoui et al. [11], Tibshirani et al. [36], Wang et al. [37], Wang et al. [38], Ndiaye et al. [27], Kuang et al. [22], Xiang et al. [40], Lee et al. [23], Ren et al. [31], Pan and Xu [28]. Roughly speaking, there are two types of screening rules: safe rule and heuristic rule. Safe rules mean all screened features are guaranteed to be inactive. For example, Ghaoui et al. [11] constructed SAFE rules to eliminate predictors for sparse supervised models, which includes Lasso, -norm regularized logistic regression and -norm regularized support vector machine. Wang et al. [37] built the dual polytope projection (DPP) and the enhanced version EDPP to discard inactive predictors for Lasso. Wang et al. [38] analyzed the dual problem of the Fused Lasso and set up its screening rule via the monotonicity of the subdifferentials. Ndiaye et al. [27] built up statics and dynamic gap safe screening rules for Group Lasso, which are based on the gap between feasible points of Group Lasso and its dual problem. Ren et al. [31] proposed a novel bound propagation algorithm to screen out inactive features for general Lasso problems, including different differentiable loss functions. Instead, heuristic screening rules do not possess this advantage, but they can be more efficient by checking the Karush-Kuhn-Tucker (KKT) condition. For example, Tibshirani et al. [36] proposed strong rules for discarding inactive predictors under the assumption of the unit slope bound. For robust loss functions, there are a few screening rules. For instance, Chen et al. [6] proposed the safe screening rules for the regularized Huber regression. To the best of our knowledge, existing screening rules mainly focus on regularized models with differentiable loss functions, such as the quadratic function, logistic function and Huber function. However, the quantile function/pinball loss is not differentiable, which means that the existing screening rules can not be directly applied to the -norm quantile regression.

The core of an efficient screening rule is the easily expressed estimation of the dual solution, but the non-differentiability of the quantile function cause a difficulty to estimate the dual solution of the -norm quantile regression. In this paper, we introduce the dual circumscribed sphere technique to estimate the dual solution and build up a safe feature screening rule. In order to do so, we first present the dual problem of the -norm quantile regression, which maximizes a linear function under some linear constraints. With the help of duality theory, we obtain a screening test for the -norm quantile regression based on its dual solution. This is the basic screening result that can be used to identity the inactive features, but it may be complex to get the dual solution if the data is high-dimensional. To make this screening test implementable, we estimate the dual solution via a region composing with two half spaces and some box constraints. In order to obtain the analytical form of the screening test, we introduce the dual circumscribed sphere technique. With the help of this technique, we develop an easily implementable screening rule for the -norm quantile regression, which has a closed-form formula of given data. As far as we know, this is the first time to use this technique in screening rules. According to this screening rule, we can eliminate the inactive features in data sets and reduce the computational cost of algorithms. For the purpose of illustrating the efficiency of our screening rule, we do some numerical experiments on simulation data and real data. The experiments present that the screening rule can not only help to eliminate inactive features efficiently, but also save the computational time up to 23 times. Note that we adopt the proximal ADMM (Gu et al. [12]) to solve the -norm quantile regression. Nevertheless, our screening rule can be embedded into any algorithm or solver for solving this model.

The rest of this paper is organized as follows. We review basic concepts and results of the -norm quantile regression in Section 2. In Section 3, we build up the -norm quantile regression screening rule via the dual circumscribed sphere technique. In Section 4, we present the numerical results of some simulation data and real data. Some conclusions are given in Section 5.

2 Preliminaries

Some basic concepts and results of the -norm quantile regression are reviewed in this section. See Rockafellar [32] and Beck [3] for more details. First, we present the quantile function/pinball loss as follows. For any ,

| (1) |

Here indicates the quantile of interest. Obviously, the quantile function is not differentiable at 0, so we introduce the concept of subdifferential.

Definition 2.1.

Let be a proper closed convex function and let . A vector is called a subgradient of at x if

, .

The set of all subgradients of at x is called the subdifferential of at x and is denoted by , that is

.

According to this definition, we get the subdifferential of the quantile function.

Lemma 2.1.

Let be the quantile function with . For any , the subdifferential of at is

For any , the norm of x is defined as . By simply calculation, the subdifferential of is , where

Now, we review the definition of the conjugate function.

Definition 2.2.

Let be a proper closed convex function. The conjugate function of is denoted as and is defined as

,

Based on this definition, we can get the conjugate of the quantile function.

Lemma 2.2.

Let be the quantile function with . For any , the conjugate of at is

In addition, the conjugate of norm is the indictor function of norm. That is, for any ,

where is defined as Another norm that we use in this paper is norm. For any , .

Definition 2.3.

Let be a proper closed convex function. The proximal mapping of is the operator given by

prox for any .

Based on this definition, we review the proximal mapping of norm (Beck [3]) in the following lemma.

Lemma 2.3.

Denote . For any , the proximal mapping of is

prox

where denotes the Hadamard product and with

By simple calculation, we get the proximal mapping of quantile function.

Lemma 2.4.

Let be the quantile function with . For any , the proximal mapping of at is

3 -norm quantile regression screening rule

In this section, we build up the -norm quantile regression screening rule. At first, we introduce the dual circumscribed sphere technique, which is used to estimate the dual solution. With the help of this technique, we obtain the safe feature screening rule in this paper.

The -norm quantile regression (Li and Zhu [24]) is

| (2) |

where is the unknown coefficient vector and is the tuning parameter. For ease of expression, we denote the response variable and the prediction matrix , where denotes the sample and the feature. In order to emphasize that the solution of (2) relies on the choice of , we denote as it. If , the feature is uncorrelated to the quantile of y and we call it the inactive feature. Since that the quantile function is not differentiable, existing screening rules can not be directly applied to the -norm quantile regression (2). To overcome the challenge of the non-differentiability of the quantile function, we propose the dual circumscribed technique, which is used to estimate the dual solution. In order to do so, we introduce a variable and transform the model (2) to a constraint problem as below.

| (3) |

Similarly, the solution of (3) is denoted as , where is the solution of (2). By introducing the Lagrangian multiplier we obtain the Lagrangian function of the model (3), which is

By direct computation, we obtain that

where the last equality is based on the result of Lemma 2.2 and the argument after it. Therefore, the Lagrangian dual form of the model (2) is

That is,

| (4) |

Denote the solution of the dual problem (4) as . The Karush-Kuhn-Tucker (KKT) system of (3) and (4) is

| (5) |

If a pair satisfies the KKT system, it is called the KKT point of (3) and (4). Note that is a feasible point of the problem (3). Slater constraint qualification (Rockafellar [32]) holds on this problem. Hence, we easily show the following duality theorem.

Theorem 3.1.

According to Theorem 3.1, for any , the solutions of problems (3) and (4) satisfies that

.

This, together with the subdifferential of norm, leads to the basic idea of our screening test.

Theorem 3.2.

Let . For any tuning parameter , if the solution of (4) satisfies that

then , which means that is uncorrelated to the quantile of y.

In this paper, we call as the screening test. For any tuning parameter , according to this theorem, some inactive features can be eliminated. Therefore, this screening test reduces the computational cost of solving the model (2) when the dual solution is known. However, the dual solution is unknown in most cases and it may need high computational cost to solve the dual problem in high-dimensional settings. So, we estimate the dual solution in the following part.

Before estimating the dual solution, we present the lower bound of the tuning parameter such that the solution of (2) is zero.

Let with

| (6) |

Denote

| (7) |

and with

| (8) |

where and . We then obtain the next lemma.

Lemma 3.1.

Denote . The following statements hold.

(i) If , then .

(ii) If , then .

Proof.

(i) Let . By Theorem 3.1 and the KKT system (5), we know that , and with any defined in (6). Because is a set, needs to satisfy that . By the definition of the , we know that

Based on (6) and (7), we know that

Therefore,

(ii) Let . Denote as the optimal value of the problem (2), as the objective function of the problem (4) and

It is clear that , because there are more constraints of when calculating the value of . Based on , we know that any is a feasible point of the problem (4) and . Therefore, for any , and any is a solution of the problem (4). Replacing into the KKT system (5), we obtain the results (a), (b) and (c).

(a) If , we have , which leads to and . Therefore,

(b) If , we have , which leads to and . Therefore,

(c) If , we have , which leads to and . Therefore,

According to these three results, we have

Based on the strong duality theorem, we know that

which means

Clearly, is a solution of (2) when . Moreover, based on and , is the unique solution. ∎

Remark 3.1.

In Lemma 3.1, the expression of seems complex, while it can be determined by the given data and y. The complex expression of is due to that is a set. In the special case that all elements of y are not zero, is a singleton and .

According to this result, we consider about in the rest of this paper. Next, we estimate the dual solution when , via relaxing the dual box constraints.

Lemma 3.2.

Proof.

For any tuning parameter , the dual solution satisfies that

and .

It is sure that the satisfies these constraints for any , so the dual solution must satisfy that

In addition,

where and are defined in (7). This means

| (10) |

To simplify the computation of in the screen test, let

| (11) |

The dual solution must be in this set.

Introducing with , then can be expressed as

| (12) |

where and . To get an easily calculated result of , we relax as

where and is a circumscribed sphere of . ∎

Remark 3.2.

In Lemma 3.2, we estimate the dual solution by employing the circumscribed sphere relaxation of the dual box constraints. Therefore, we name it as the dual circumscribed sphere technique.

From the proof of Lemma 3.2, we get that

and

Combining these results, we obtain that

Next, we present the detailed results of . Before that, we introduce some new notations.

Denote and as the distance between the origin of the coordinates and the hyperplane . Then

Denote as the angle between and y, it is easy to see that and

.

Denote as the distance between the origin of the coordinates and . Then . Denote as the distance between the origin of the coordinates and . Then .

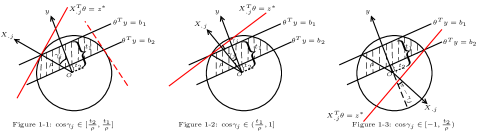

Lemma 3.3.

For any ,

with defined as follows.

| (13) |

Proof.

There are three cases of the relationship between the hyperplane and the sphere :

(i) is tangent to ;

(ii) meets the intersection between and ;

(iii) meets the intersection between and .

From Lemma 3.2, we know that . According to the different values of and , the value of is presented as follows.

Cases 1: and . See Fig. 1 for easy understanding.

Subcases 1-1: is tangent to the sphere . In this case, the distance between the origin of the coordinates and the hyperplane is . The Figure 1-1 in Fig. 1 shows that we use this case if .

Subcases 1-2: meets the intersection between and . Here,

.

The result of Figure 1-2 in Fig. 1 shows that .

Subcases 1-3: meets the intersection between and . Similarly,

.

From Figure 1-3 in Fig. 1, we know that in this case.

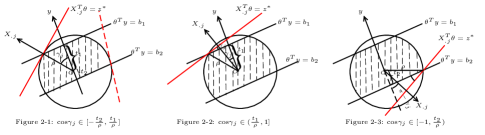

With the similar analysis, we can obtain the other cases as follows.

Cases 2: and . See Fig. 2 for easy understanding.

Subcases 2-1: when .

Subcases 2-2: If ,

.

Subcases 2-3: If

.

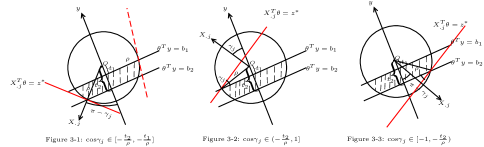

Cases 3: and . See Fig. 3 for easy understanding.

Subcases 3-1: when .

Subcases 3-2: If ,

.

Subcases 3-3: If ,

.

The detailed result of can be gotten in the similar way by defining as the angle between and y.

Lemma 3.4.

In Lemma 3.3 and Lemma 3.4, and show the closed-form expressions of given data, which can be easily computed. Combing these lemma and Theorem 3.2, we obtain the implementable safe feature screening rule for the -norm quantile regression in the next theorem.

Theorem 3.3.

For given and . If

then , which means that is uncorrelated to the quantile of y and can be eliminated.

Remark 3.3.

Theorem 3.1 can be extended to the weighted -norm quantile regression, which is given as

| (14) |

where and holds for all . When the weight in (14), it degrades to the -norm quantile regression. For the model (14),

where is defined in (8). With Lemma 3.3 and Lemma 3.4, we can obtain the next screening rule for the weighted -norm quantile regression.

For given and . If

then , which means that is uncorrelated to the quantile of y and can be eliminated.

4 Numerical results

In order to evaluate the performance of the -norm quantile regression screening rule in Section 3, we do some numerical experiments in this section. All experiments are performed on the MATLAB R2018b with Intel(R) Core(TM) i5-8250U 1.60 CPU and 8G RAM.

For each data set, we run the proximal ADMM (Gu et al. [12]) along a sequence of 100 tuning parameters equally spaced on the from 0.01 to 1. Same as the most papers (Tibshirani et al. [36], Wang et al. [37], Wang et al. [38], Ndiaye et al. [27], Xiang et al. [40] and so on), we use two quantities to measure the screening rule, that are rejection ratio and speedup. The rejection ratio is defined as Under different tuning parameter , denotes the number of discarded features by the screening rule and denotes the actual number of features with zero coefficient. This ratio measures the efficiency of the screening rule. The speedup is defined as where and indicate the calculation time of solver with and without screening rule respectively. This quantity, as the name illustrated, indicates the reduced computational time because of the screening rule. The larger the rejection ratio and speedup are, the more efficient the screening rule is.

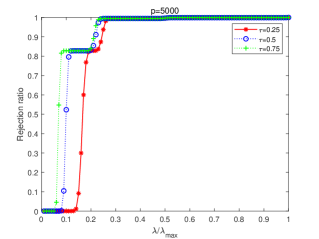

4.1 Simulation

We evaluate the screening rule on some simulation data, which are generated from the true linear regression

with and . In the true model, is generated from the multivariate normal distribution with mean vector and covariance matrix . Here, we consider two cases, that are and as in Belloni[4], Li and Zhu[24] and so on. To show the difference between features (every column of presents a feature), we set as , and . The true coefficient vector is set as follows.

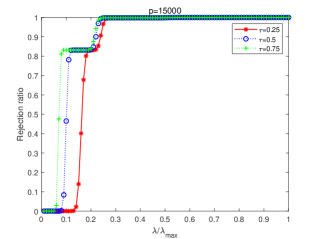

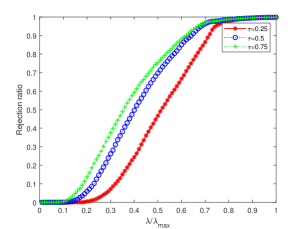

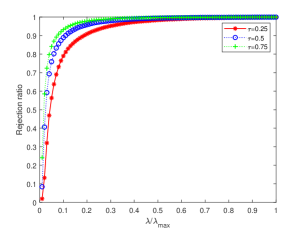

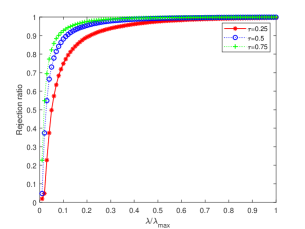

From Fig. 4, for the simulated data, we conclude that performs best in rejection ratio. In this case, our screening rule identifies over 80 percent inactive features. In addition, the gap of rejection ratios of and is very small. In order to clearly present the different performance of our screening rule under different , and , we report the speedup in the TABLE 1.

| speedup | sd | ||||

|---|---|---|---|---|---|

| 5000, | 0.25 | 30.0053 | 9.3310 | 3.2157 | 0.0299 |

| 0.50 | 29.8827 | 6.7459 | 4.4298 | 0.0589 | |

| 0.75 | 22.2410 | 5.0821 | 4.3763 | 0.0652 | |

| 10000, | 0.25 | 112.2569 | 29.9057 | 3.7537 | 0.0340 |

| 0.50 | 112.5967 | 20.5164 | 5.4881 | 0.0526 | |

| 0.75 | 84.6651 | 14.0857 | 6.0107 | 0.0574 | |

| 15000, | 0.25 | 318.0094 | 78.7775 | 4.0368 | 0.1530 |

| 0.50 | 250.6742 | 41.8572 | 5.9888 | 0.0495 | |

| 0.75 | 186.1347 | 27.2497 | 6.8307 | 0.0428 | |

| 5000, | 0.25 | 29.2768 | 9.2876 | 3.1522 | 0.0420 |

| 0.50 | 29.3762 | 6.7878 | 4.3278 | 0.0749 | |

| 0.75 | 21.8868 | 5.1286 | 4.2676 | 0.0723 | |

| 10000, | 0.25 | 111.4912 | 30.4614 | 3.6601 | 0.0479 |

| 0.50 | 110.9368 | 20.7868 | 5.3369 | 0.0341 | |

| 0.75 | 82.8418 | 14.4750 | 5.7231 | 0.0374 | |

| 15000, | 0.25 | 302.2332 | 77.3164 | 3.9090 | 0.0472 |

| 0.50 | 312.9282 | 53.6676 | 5.8309 | 0.1181 | |

| 0.75 | 232.9686 | 35.3582 | 6.5888 | 0.2220 |

According to the results in TABLE 1, we have some conclusions. Firstly, our screening rule shrinks the computational time in different degrees. The smallest speedup is 3.1522 and the largest is 6.8307. Secondly, with the same sample size, the speedup value increases with increasing. From TABLE 1, we know that rapidly increase when increases, while increases slightly. Thirdly, the standard variances of the speedup values are relatively small. These standard variances show that our screening rule has a stable performance on speedup. Finally, there are slightly differences between and , which means our screening rule is stable on data sets with uncorrelated features or correlated features.

4.2 Real data

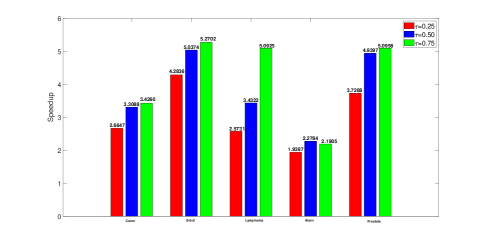

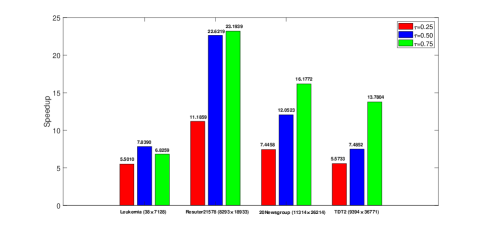

We analyze some real data sets, named Colon[2], Srbct[18], Lymphoma[1], Brain[30], Prostate[5], Leukemia , Reuters21578, 20Newsgroups and TDT2. Obviously, not all feature have connections with the quantile of the response variable. Therefore, we do not need to input all these features when calculating their relationships, which means the screening rule is needed before dealing with this issue. We apply the screening rule to , and as Scheetz et al. [33], Peng and Wang [29], Gu et al. [12] and so on.

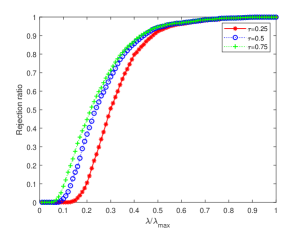

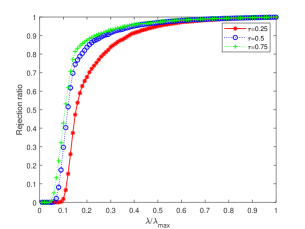

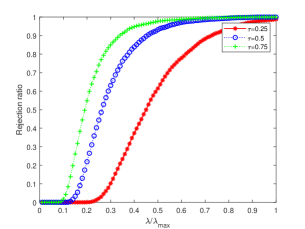

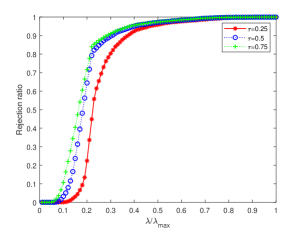

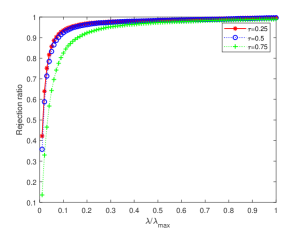

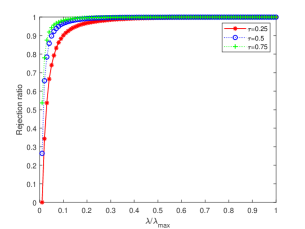

From results in Fig. 5, Fig. 6 and Fig. 7, we have the following conclusions. (i) Our screening rule eliminates sufficient number of inactive features in all these data sets. The rejection ratio of these data sets are almost near 1. (ii) The speedup value differs with the data scale. In these data sets, the speedup of these data sets varies between 2 to 23. (iii) Except the Leukemia and Brain, the speedup value increases with the parameter increasing. According to these results, we conclude that our screening rule is efficient on these high-dimensional data sets.

5 Conclusion

In this paper, we introduce the dual circumscribed sphere technique to estimate the dual solution. Based on this technique, we build up a safe feature screening rule for the -norm quantile regression, which has a closed-form formula of given data and can be computed with low cost. In the numerical experiments, we adopt the proximal ADMM to solve the -norm quantile regression and illustrate the efficiency of our screening rule, which shows that the screening rule performs well in eliminating inactive features and saving up to 23 times of computational time in some cases. Actually, our screening rule can be embedded into any algorithm or solver for solving this model.

Acknowledgments

This work was supported by the National Science Foundation of China (11671029).

References

- [1] A. A. Alizadeh, M. B. Eisen, E. Davis, C. Ma, et. al., Distinct types of diffuse large b-cell lymphoma identified by gene expression profiling, Nature, vol. 403, pp. 503-511, 2000.

- [2] U. Alon, N. Barkai, D. A. Notterman, K. Gish, et. al., Broad patterns of gene expression revealed by clustering analysis of tumor and normal colon 590 tissues probed by oligonucleotide arrays, Cell Biology, vol. 96, pp. 6745-6750, 1999.

- [3] A. Beck, First-order methods in optimization, Society for industrial and applied marhematics: Philadelphia, 2017.

- [4] A. Bellon, and V. Chernozhukov, “ penalized quantile regression in high-dimensional sparse models,” Ann. Statist., vol. 39(1), pp. 82-130, 2011.

- [5] E. Bradley, Large-scale inference: empirical Bayes methods for estimation, testing and prediction, Cambridge University Press, 2010.

- [6] H. Chen, L. Kong, P. Shang and S. Pan, “Safe feature screening rules for the regularized Huber regression,” Appl. Math. Comput., vol. 386, pp. 125500, 2020.

- [7] J. Fan, Y. Fan and E. Barut, “Adaptive robust variable selection,” Ann. Statist., vol. 42(1), pp. 324-351, 2014.

- [8] J. Fan, Q. Li and Y. Wang, “Estimation of high dimensional mean regression in the absence of symmetry and light tail assumptions”, J. R. Statist. Soc. B, vol. 79, pp. 247-265, 2017.

- [9] J. Fan and J. Lv, “Sure independence screening for ultrahigh dimensional feasure space (with discussion)”, J. R. Statist. Soc. B, vol, 70, pp. 849-911, 2008.

- [10] M. Fazek, T. K. Pong, D. Sun and P. Tseng, “Hankel matrix rank minization with applications to system identification and realization”, SIAM J. Matrix Anal. Appl., vol, 34(3), pp. 946-977, 2013.

- [11] E. L. Ghaoui, V. Viallon and T. Rabbani, “Safe feature elimination in sparse supervised learning”, Pac J. Optim., vol. 8(4), pp. 667-698, 2012.

- [12] Y. W. Gu, J. Fan, L. Kong, S. Q. Ma and H. Zou, “ADMM for high-dimensional sparse penalized quantile regression”, Technometrics, vol. 60(3), pp. 319-331, 2018.

- [13] J. B. Hiriart-Urruty and C. Lemarchal, Convex analysis and minization algorithms, Berlin: Springer-Verlag, 1993.

- [14] P. J. Huber, “Robust regression: asymptotics, conjectures and monte carlo”, Ann. Statist., vol. 1, pp. 799-821, 1973.

- [15] J. Huang, S. Ma and C. H. Zhang, “Adaptive Lasso for sparse high-dimensional regression models”, Stat. Sinica., pp. 1603-1618, 2008.

- [16] X. Huang, L. Shi and J. A. K. Suykens, “Support vector machine classifier with pinball loss”, IEEE. T. Pattern. Anal., vol. 36(5), pp. 984-997, 2014.

- [17] V. Jumutc, X. L. Huang and J. A. K. Suykens, “Fixed-size pegasos for hinge and pinball loss SVM”. in Proc. Int. Joint Conf. Neural Networks, pp. 1-7, 2013.

- [18] J. Khan, J. S. Wei, M. Ringner, L. H. Saal, et. al., Classification and 595 diagnostic prediction of cancers using gene expression profiling and artificial neural networks, Nature Medicine, vol. 7, pp. 673-679, 2001.

- [19] R. Koenker and G. Bassett, “Regression Quantiles”, Econometrica, vol. 46, pp. 33-50, 1978.

- [20] R. Koenker and P. Ng, “A Frisch-Newton algorithm for sparse quantile regression”, Acta Mathematicae Applicatae Sinica, vol. 21, pp. 225-236, 2005.

- [21] R. Koenker, “quantreg: Quantile Regression, R package version 5.19”, 2015.

- [22] Z. B. Kuang, S. N. Geng and D. Page, “A screening rule for -regularized ising model estimation”, in Adv. Neural. Inf. Process Syst., vol. 30, pp. 720-731, 2017.

- [23] S. Lee, N. Gornitz, E. P. Xing, “Heckerman, D. and Lippert C.: Ensembles of Lasso screening rules”, IEEE. T. Pattern. Anal., vol. 40(12), pp. 2841-2852, 2018.

- [24] Y. Li, and J. Zhu, “-norm quantile regression”, J. Comput. Graph. Stat., vol. 17(1), pp. 163-185, 2008.

- [25] G. Michael and B. Stephen, “CVX: Matlab software for disciplined convex programming, version 2.0 beta.” http://cvxr.com/cvx, 2013.

- [26] A. Mkhadri, M. Ouhourane and K. Oualkacha, “Coordinate descent algorithm for computing penalized smooth quantile regression”, Stat. Comput., vol. 27(4), pp. 865-883, 2017.

- [27] E. Ndiaye, O. Fercoq, A. Gramfort and J. Salmon, “Gap safe screening rules for sparsity enforcing penalties,” J. Mach. Learn. Res., vol. 18, pp. 1-33, 2017.

- [28] X. Pan and Y. Xu, “A novel and safe two-stage screening method for support vector machine”, IEEE T. Neur. Net. Lear., vol. 30(8), pp. 2263-2274, 2018.

- [29] B. Peng and L. Wang, “An iterative coordinate descent algorithm for high-dimensional nonconvex penalized quantile regression”, J. Comput. Graph. Stat., vol. 24(3), pp. 676-694, 2015.

- [30] S. L. Pomeroy, T. Pablo, G. Michelle, L. M. Sturla, et. al., Prediction of central nervous system embryonal tumour outcome based on gene expression, Nature, vol. 415. pp. 436-442, 2002.

- [31] S. Ren, S. Huang, J. Ye and X. Qian, “Safe feature screening for generalized Lasso”, IEEE. T. Pattern. Anal., vol. 40(12), pp. 2992-3006, 2018.

- [32] R. T. Rockafellar, Convex Analysis. New York, NY, Princeton: Princeton Univ., 1970.

- [33] T. E. Scheetz, K. Y. Kim, R. E. Swiderski, A. R. Philp, K. L. Knudtson, A. M. Dorrance, G. F. Dibona, J. Huang, T. L. Casavant, V. C. Sheffield and E. M. Stone, “Regulation of gene expression in the mammalian eye and its relevance to eye disease”, in Proceedings of the National Academy of Sciences of the United States of America, vol. 103, pp. 14429-14434, 2006.

- [34] I. Steinwart and A. Christmann, “How SVMs can estimate quantiles and the median,” in Adv. Neural. Inf. Process Syst., pp. 305-312, 2007.

- [35] I. Steinwart and A. Christmann, “Estimating conditional quantiles with the help of the pinball loss,” Bernoulli, vol. 17(1), pp. 211-225, 2011.

- [36] R. Tibshirani, J. Bien, T. Hastie, N. Simon, J. Taylor and R. J. Tibshirani, “Strong rules for discarding predictors in Lasso-type problems”, J. R. Statist. Soc. B, vol. 74(2), pp. 1-22, 2012.

- [37] J. Wang, P. Wonka and J. Ye, “Lasso screening rules via dual polytope projection”, J. Mach. Learn. Res., vol. 16, pp. 1063-1101, 2015.

- [38] J. Wang, W. Fan and J. Ye, “Fused Lasso screening rules via the monotonicity of subdifferentials”, IEEE. T. Pattern. Anal., vol. 37(9), pp. 1806-1820, 2015.

- [39] T. T. Wu and K. Lange, “Coordinate descent algorithms for Lasso penalized regression”, Ann. Appl. Stat., vol. 2, pp. 224-244, 2008.

- [40] Z. J. Xiang, Y. Wang and J. P. Ramadge, “Screening tests for Lasso problems”, IEEE. T. Pattern. Anal., vol. 5(39), pp. 1008-1027, 2017.

- [41] C. Yi and J. Huang, “Semismooth Newton coordinate descent algorithm for elastic-net penalized Huber loss regression and quantile regression”, J. Comput. Graph. Stat., vol. 26(3), pp. 547-557, 2017.