Real-time Inflation Forecasting Using Non-linear Dimension Reduction Techniques

In this paper, we assess whether using non-linear dimension reduction techniques pays off for forecasting inflation in real-time. Several recent methods from the machine learning literature are adopted to map a large dimensional dataset into a lower dimensional set of latent factors. We model the relationship between inflation and the latent factors using constant and time-varying parameter (TVP) regressions with shrinkage priors. Our models are then used to forecast monthly US inflation in real-time. The results suggest that sophisticated dimension reduction methods yield inflation forecasts that are highly competitive to linear approaches based on principal components. Among the techniques considered, the Autoencoder and squared principal components yield factors that have high predictive power for one-month- and one-quarter-ahead inflation. Zooming into model performance over time reveals that controlling for non-linear relations in the data is of particular importance during recessionary episodes of the business cycle or the current COVID-19 pandemic.

JEL: C11, C32, C40, C53, E31

Keywords: Non-linear principal components, machine learning, time-varying parameter regression, density forecasting, real-time data

1 Introduction

Inflation expectations are used as crucial inputs for economic decision making in central banks such as the European Central Bank (ECB) and the US Federal Reserve (Fed). Given current and expected inflation, economic agents decide on how much to consume, save and invest. In addition, measures of inflation expectations are often employed to estimate the slope of the Phillips curve, infer the output gap or the natural rate of interest. Hence, being able to accurately predict inflation is key for designing and implementing appropriate monetary policies in a forward looking manner.

Although the literature on modeling inflation is voluminous and the efforts invested considerable, predicting inflation remains a difficult task and simple univariate models are still difficult to beat (Stock and Watson, 2007). The recent literature, however, has shown that using large datasets (Stock and Watson, 2002a) and/or sophisticated models (see Koop and Potter, 2007; Koop and Korobilis, 2012; D’Agostino et al., 2013; Koop and Korobilis, 2013; Clark and Ravazzolo, 2015; Chan et al., 2018; Jarocinski and Lenza, 2018) has the potential to improve upon simpler benchmarks.

These studies often exploit information from huge datasets. This is commonly achieved by extracting a relatively small number of principal components (PCs) and including them in a second stage regression model (see, e.g., Stock and Watson, 2002a). While this approach performs well empirically and yields consistent estimators for the latent factors, it fails to capture non-linear relations in the dataset. In the presence of non-linearities, using simple PCs potentially reduces predictive accuracy by ignoring important features of the data. Some studies deal with this issue by using flexible factor models which allow for non-linearities in the data. Bai and Ng (2008) use targeted predictors coupled with quadratic principal components and show that allowing for non-linearities yields non-trivial improvements in predictive accuracy for inflation. This suggests that non-linearities (of a known form) are present in US macroeconomic datasets which are commonly employed for inflation forecasting. More recently, Pelger and Xiong (2021) propose a flexible state-dependent factor model and apply this method to US bond yields and stock returns. Using this non-linear and non-parametric technique yields results which differ from linear, PC-based models by extracting significantly more information from the data.

One additional assumption commonly made is that the relationship between inflation and the latent factors is constant. For longer time series which feature multiple structural breaks this assumption is a strong one and may be deleterious for predictive accuracy. Several recent papers deal with this issue by using time-varying parameter (TVP) regressions which, in addition, allow for heteroscedasticity through stochastic volatility (SV) models (Koop and Potter, 2007; Koop and Korobilis, 2012; D’Agostino et al., 2013; Belmonte et al., 2014b; Clark and Ravazzolo, 2015; Jarocinski and Lenza, 2018; Korobilis, 2021).

Investigating whether allowing for non-linearities in the compression stage pays off for inflation forecasting is the key objective of the present paper. Building on recent advances in machine learning (see Gallant and White, 1992; McAdam and McNelis, 2005; Exterkate et al., 2016; Chakraborty and Joseph, 2017; Heaton et al., 2017; Mullainathan and Spiess, 2017; Feng et al., 2018; Coulombe et al., 2019; Kelly et al., 2019; Medeiros et al., 2021), we adopt several non-linear dimension reduction techniques. The resulting latent factors are then linked to inflation in a second stage regression. To investigate whether there exists a relationship between non-linear factor estimation and flexible modeling of the predictive inflation equation, we introduce dynamic regression models that allow for TVPs and SV. Since the inclusion of a relatively large number of latent factors can still imply a considerable number of parameters (and this problem is even more severe in the TVP regression case), we rely on state-of-the-art shrinkage techniques.

From an empirical standpoint it is necessary to investigate how these dimension reduction techniques perform over time and during different business cycle phases. We show this by carrying out a thorough real-time forecasting experiment for the US. Our forecasting application uses monthly real-time datasets (i.e., the FRED-MD database proposed in McCracken and Ng, 2016) and includes a battery of well established models commonly used in central banks and other policy institutions to forecast inflation. These include simple benchmarks as well as more elaborate models such as the specification proposed in Stock and Watson (2002a).

Our results show that non-linear dimension reduction techniques yield forecasts that are highly competitive to (and in fact often better than) the ones obtained from using linear methods based on PCs. In terms of one-month-ahead forecasts we find that models based on the Autoencoder yield point and density forecasts which are more precise than the ones obtained from other sophisticated non-linear dimension reduction techniques as well as traditional methods based on PCs. When the focus is on one-quarter-ahead forecasts we find that non-linear variants of PCs perform best. This performance, however, is not homogeneous over time and some of the models do better than others during different stages of the business cycle. In a brief discussion, we also analyze how our set of models performs during the COVID-19 pandemic.

These findings give rise to the second contribution of our paper. Since we observe that more sophisticated non-linear dimension reduction methods outperform simpler techniques during recessions, we combine the different models using dynamic model averaging (see Raftery et al., 2010; Koop and Korobilis, 2013). We show that combining our proposed set of models with a variety of standard forecasting models yields predictive densities which are very close to the single best performing model in overall terms. Since the set of models we consider is huge, this indicates that using model and forecast averaging successfully controls for model uncertainty.

The remainder of this paper is structured as follows. Section 2 discusses our proposed set of dimension reduction techniques. Section 3 introduces the econometric modeling environment that we use to forecast inflation. Section 4 first provides some in-sample features, then discusses the results of the forecasting horse race and finally presents our findings based on forecast averaging. The last section summarizes and concludes the paper. The Online Appendix provides further details on the econometric techniques as well as the data and additional empirical results.

2 Linear and non-linear dimension reduction techniques

Suppose that we are interested in predicting inflation using a large number of regressors that we store in a matrix , where denotes a -dimensional vector of observations at time . If is large relative to , estimation of an unrestricted model that uses all columns in quickly becomes cumbersome and overfitting issues arise. As a solution, dimension reduction techniques are commonly employed (see, e.g., Stock and Watson, 2002a; Bernanke et al., 2005). These methods strike a balance between model fit and parsimony. At a very general level, the key idea is to introduce a function that takes the matrix as input and yields a lower dimensional representation , which is of dimension , as output. The critical assumption to achieve parsimony is that . The latent factors in are then linked to inflation through a dynamic regression model (see Section 3).

The function is typically assumed to be linear with the most prominent example being PCs. In this paper, we will consider several choices of that range from linear to highly non-linear (such as manifold learning as well as deep learning) specifications. We subsequently analyze how these different specifications impact inflation forecasting accuracy. In the following sub-sections, we briefly discuss the different techniques and refer to the original papers for additional information.

2.1 Principal component analysis

We start our discussion by considering principal component analysis (PCA). Minor alterations of the standard PCA approach allow for introducing non-linearities in two ways. First, we can introduce a non-linear function that maps the covariates onto a matrix . Second, we could alter the sample covariance matrix (the kernel) with a function : . Both and form the two main ingredients of a general PCA reducing the dimension to , as outlined below (for details, see Schölkopf et al., 1998).

Independent of the functional form of and , we obtain PCs by performing a truncated singular value decomposition (SVD) of the transformed sample covariance matrix . Conditional on the first eigenvalues, the resulting factor matrix is of dimension . These PCs, for appropriate , explain the vast majority of variation in . In the following, the relationship between the PCs and is:

| (1) |

with being the truncated eigenvector matrix of (Stock and Watson, 2002a). Notice that this is always conditional on deciding on a suitable number of PCs. The number of factors is a crucial parameter that strongly influences predictive accuracy and inference (Bai and Ng, 2002). In our empirical work, we consider a small (), moderate (), and large () number of PCs.

By varying the functional form of and we are now able to discuss the first set of linear and non-linear dimension reduction techniques belonging to the class of PCA:

-

1.

Linear PCs

The simplest way is to define both and as the unity function, resulting in and . Due to the linear link between the PCs and the data, PCA is very easy to implement and yields consistent estimators for the latent factors if and go to infinity (Stock and Watson, 2002a; Bai and Ng, 2008). Even if there is some time-variation in the factor loadings (and is large), Stock and Watson (2002b) show that principal components asymptotically (i.e., remain a consistent estimator for the factors and also that the resulting forecast is efficient.111Note that this result holds only asymptotically. With relatively small and large , however, forecast efficiency may be improved by better capturing important non-linear features of the dataset.

-

2.

Quadratic and squared PCs

The literature suggests several ways to overcome the linearity restriction of PCs. Bai and Ng (2008), for example, apply a quadratic link function between the latent factors and the regressors, yielding a more flexible factor structure. While squared PC considers just squaring the elements of resulting in

with and denoting element-wise multiplication, quadratic PC is defined as

Both variants also focus on the second moments of the covariate matrix and allow for a non-linear relationship between the principal components and the predictors. Bai and Ng (2008) show that quadratic variables can have substantial predictive power as they provide additional information on the underlying time series. Intuitively speaking, given that we transform our data to stationarity in the empirical work, this transformation strongly overweights situations characterized by sharp movements in the columns of (such as during a recession). By contrast, periods characterized by little variation in our macroeconomic panel are transformed to mildly fluctuate around zero (and thus carry little predictive content for inflation). In our empirical model, our regressions always feature lagged inflation and this transformation thus effectively implies that in tranquil periods, the model is close to an autoregressive model whereas in crisis periods, more information is introduced.

-

3.

Kernel PCs

Another approach for non-linear PCs is the kernel principal component analysis (KPCA). KPCA dates back to Schölkopf et al. (1998), who proposed using integral operator kernel functions to compute PCs in a non-linear manner. In essence, this amounts to implicitly applying a non-linear transformation of the data through a kernel function and then applying PCA on this transformed dataset. Such an approach has been used for forecasting in Giovannelli (2012) and Exterkate et al. (2016).

We allow for non-linearities in the kernel function between the data and the factors by defining to be a Gaussian or a polynomial kernel (which is of dimension ) with the th element given by

for a Gaussian kernel and

for a polynomial kernel.

Here, (i.e., is the unity function), and denote two columns of while and are scaling parameters. As suggested by Exterkate et al. (2016) we set and with being the th percentile of the distribution with degrees of freedom.

2.2 Diffusion maps

Diffusion maps, originally proposed in Coifman et al. (2005) and Coifman and Lafon (2006), are another set of non-linear dimension reduction techniques that retain local interactions between data points in the presence of substantial non-linearities in the data.222For an application to astronomical spectra, see Richards et al. (2009). The local interactions are preserved by introducing a random walk process.

The random walk captures the notion that moving between similar data points is more likely than moving to points which are less similar. We assume that the weight function which determines the strength of the relationship between to is given by

where denotes the Euclidean distance between and and is a tuning parameter set such that is close to zero except for . Here, is determined by the median distance of the -nearest neighbors of as suggested by Zelnik-Manor and Perona (2004). The number of is approximated using the algorithm suggested by Angerer et al. (2016).

The probability of moving from to is then simply obtained by normalizing:

This probability tends to be small except for the situation where and are similar to each other. As a result, the probability that the random walk moves from to will be large if they are equal but rather small if both covariates differ strongly.

Let denote a transition matrix of dimension with th element given by . The probability of moving from to in steps is then simply the matrix power of , with typical element denoted by . Using a biorthogonal spectral decomposition of yields:

with and denoting left and right eigenvectors of , respectively. The corresponding eigenvalues are given by .

We then proceed by computing the so-called diffusion distance as follows:

with being a normalizing factor that measures the proportion the random walk spends at . This measure turns out to be robust with respect to noise and outliers. Coifman and Lafon (2006) show that

This allows us to introduce the family of diffusion maps from given by:

The distance matrix can then be approximated as:

Intuitively, this equation states that we now approximate diffusion distances in through the Euclidian distance between and . This discussion implies that we have to choose and and we do this by setting according to our approach with either a small, moderate or large number of factors and , the number of time periods. The algorithm in our application is implemented using the R packages diffusionMap and destiny (Richards and Cannoodt, 2019; Angerer et al., 2016).

2.3 Local linear embeddings

Locally linear embeddings (LLE) have been introduced by Roweis and Saul (2000). Intuitively, the LLE algorithm maps a high dimensional input dataset into a lower dimensional space while preserving the neighborhood structure. This implies that points which are close to each other in the original space are also close to each other in the transformed space.

The LLE algorithm is based on the assumption that each is sampled from some underlying manifold. If this manifold is well defined, each and its neighbors are located close to a locally linear patch of this manifold. One consequence is that each can be reconstructed from its neighbors with , conditional on suitably chosen linear coefficients. This reconstruction, however, will be corrupted by measurement errors. Roweis and Saul (2000) introduce a cost function to quantify these errors:

with denoting the th element of a weight matrix . This cost function is then minimized subject to the constraint that each is reconstructed only from its neighbors. This implies that if is not a neighbor of . The second constraint is that the matrix is row-stochastic, i.e., the rows sum to one. Conditional on these two restrictions, the cost function can be minimized by solving a least squares problem.

To make this algorithm operational we need to define our notion of neighbors. In the following, we will use the -nearest neighbors in terms of the Euclidean distance. We choose the number of neighbors by applying the algorithm proposed by Kayo (2006), which automatically determines the optimal number for . The latent factors in , with typical th column , are then obtained by minimizing:

which implies a quadratic form in . Subject to suitable constraints, this problem can be easily solved by computing:

and finding the eigenvectors of associated with the smallest eigenvalues. The bottom eigenvector is then discarded to arrive at factors. For our application, we use the R package lle (Diedrich and Abel, 2012).

2.4 Isometric feature mapping

Isometric Feature Mapping (ISOMAP) is one of the earliest methods developed in the category of manifold learning algorithms. Introduced by Tenenbaum et al. (2000), the ISOMAP algorithm determines the geodesic distance on the manifold and uses multidimensional scaling to come up with a low number of factors describing the underlying dataset. Originally, ISOMAP was constructed for applications in visual perception and image recognition. In economics and finance, some recent papers highlight its usefulness (see, e.g., Ribeiro et al., 2008; Lin et al., 2011; Orsenigo and Vercellis, 2013; Zime, 2014).

The algorithm consists of three steps. In the first step, a dissimilarity index that measures the distance between data points is computed. These distances are then used to identify neighboring points on the manifold. In the second step, the algorithm estimates the geodesic distance between the data points as shortest path distances. In the third step, metric scaling is performed by applying classical multidimensional scaling (MDS) to the matrix of distances. For the dissimilarity transformation, we determine the distance between point and by the Manhattan index and collect those points where is one of the -nearest neighbors of in a dissimilarity matrix. For our empirical application, we again choose the number of neighbors by applying the algorithm proposed by Kayo (2006) and use the implementation in the R package vegan (Oksanen et al., 2019).

The described non-linear transformation of the dataset enables the identification of a non-linear structure hidden in a high-dimensional dataset and maps it to a lower dimension. Instead of pairwise Euclidean distances, ISOMAP uses the geodesic distances on the manifold and compresses information under consideration of the global structure.

2.5 Non-linear compression with deep learning

Deep learning algorithms are characterized by not only non-linearly converting input to output but also representing the input itself in a transformed way. This is called representation learning in the sense that representations of the data are expressed in terms of other, simpler representations before mapping the data input to output values.

One tool which performs representation of itself as well as representation to output is the Autoencoder (AE). The first step is accomplished by the encoder function, which maps an input to an internal representation. The second part, which maps the encoded (transformed) data to the output, is called the decoder function. Their ability to extract factors, which explain a large fraction of the variability in the observed data, in a non-linear manner makes deep learners a powerful tool complementing the range of commonly used dimension reduction techniques (Goodfellow et al., 2016). Andreini et al. (2020), for example, embed a dynamic Autoencoder structure in a dynamic factor model and show that it yields a good now- and forecasting performance for US GDP. In their paper, they allow for additional flexibility by simultaneously estimating the non-linear latent factors and the parameters. In empirical finance, Heaton et al. (2017), Feng et al. (2018) and Kelly et al. (2019) find that the application of these methods is beneficial to predict asset returns.

Based on deep learning techniques, we propose obtaining hierarchical predictors by applying a number of non-linear transformations to . These transformations are called hidden layers with giving the depth of our architecture and denoting an univariate activation function.333In principle, can vary over the different layers. More specifically, in each layer, activation functions (non-linearly) transform the inputs (which are the outputs of the previous layer). A common choice, which we adopt, is the hyperbolic tangent (tanh) given by

We apply this function element-wise to the entries of . Using tanh activation functions is justified by its strong empirical properties identified in recent studies such as Saxe et al. (2019) and Andreini et al. (2020).

The structure of our deep learning algorithm can be represented in form of a composition of univariate semi-affine functions given by

and for . Here, denotes a weighting matrix of dimension (with being the number of neurons in layer ), is a bias vector and is a vector of ones.

The output of the network is then obtained by setting:

Notice that if we set , we achieve dimension reduction and the output of the network is a (non-linearily) compressed version of the input dataset. In principle, what we have just described constitutes the encoding part of the Autoencoder. If we are interested in recovering the original dataset we simply have to add additional layers characterized by increasing numbers of neurons until we reach for .

The optimal sets of and are obtained by computing a loss function, most commonly the mean squared error of the in-sample fit. The complexity of the neural network is determined by choosing the number of hidden layers and the number of neurons in each layer . We perform our forecasting exercise with different sets of tuning parameters and choose one, three, five, and eight hidden layers with the number of neurons evenly being downsized to the desired number of factors.

For the loss function and the optimization algorithm we stick to common choices in the literature and use the mean squared error loss function and the Adaptive Moment Estimation (ADAM). We repeat the optimization procedure in epochs on at least batches which corresponds to the average duration of a business cycle in the US.444The average duration of a business cycle was determined using data provided by The National Bureau of Economic Research on business cycle expansions and recessions. This implies that we train the algorithm in each epoch with a partition of the original data set of at least the length of one business cycle. To capture the dynamics of the different cycles present in the data the optimization procedure needs to be repeated in a reasonably high number of epochs. We find that the algorithm converges quickly and setting the number of epochs to is sufficient.

We employ the R interface to keras (Allaire and Chollet, 2019), a high-level neural networks API and widely used package for implementing deep learning models.

3 A TVP regression for forecasting inflation

In the following, we introduce the predictive regression that links our target variable, inflation in consumer prices, to and other observed factors. Following Stock and Watson (1999), inflation is specified such that:

| (2) |

with denoting the consumer price index in period .

In the empirical application we set . is then modeled using a dynamic regression model:

| (3) |

where is a vector of TVPs associated with covariates denoted by and is a time-varying error variance. might include the latent factors extracted from the various methods discussed in the previous sub-section, lags of inflation, an intercept term or other covariates which are not compressed.

Following much of the literature (Taylor, 1982; Belmonte et al., 2014a; Kalli and Griffin, 2014; Kastner and Frühwirth-Schnatter, 2014; Stock and Watson, 2016; Chan, 2017; Huber et al., 2021) we assume that the TVPs and the error variances evolve according to independent stochastic processes:

| (4) |

with denoting the conditional mean of the log-volatility, its persistence parameter and the error variance of . The matrix is an -dimensional variance-covariance matrix with and being the process innovation variance that determines the amount of time-variation in . This setup implies that the TVPs are assumed to follow a random walk process while the log-volatilities evolve according to an AR(1) process.

The model described by Eq. (3) and Eq. (4) is a flexible state space model that encompasses a wide range of models commonly used for forecasting inflation. For instance, if we set and , we obtain a constant parameter model with homoscedastic errors. If is instead a full matrix but of reduced-rank, we obtain the model proposed in Chan et al. (2020). If includes the lags of inflation and (lagged) PCs, we obtain a model closely related to the one used in Stock and Watson (2002a). If we set and allow for TVPs, we obtain a specification similar to the unobserved components stochastic volatility model successfully adopted in Stock and Watson (1999). A plethora of other models can be identified by appropriately choosing , and . This flexibility, however, calls for model selection. We select appropriate submodels by using Bayesian methods for estimation and forecasting. These techniques are further discussed in Section B of the Online Appendix and allow for data-based shrinkage towards simpler nested alternatives.

4 Forecasting US inflation

4.1 Data overview, design of the forecasting exercise and competitors

In our empirical application we consider the popular FRED-MD database. This dataset is publicly accessible and available in real-time. The monthly data vintages ensure that we only use information that would have been available at the time a given forecast is being produced. A detailed description of the databases can be found in McCracken and Ng (2016). To achieve approximate stationarity we transform the dataset as outlined in Section C of the Online Appendix. Furthermore, each time series is standardized to have sample mean zero and unit sample variance prior to using the non-linear dimension reduction techniques.

Our US dataset includes 105 monthly variables that span the period from 1963:01 to 2021:01. The forecasting design relies on a rolling window, as justified in Clark (2011), that initially ranges from 1980:01 to 1999:12. For each month of the hold-out sample, which starts in 2000:01 and ends in 2019:12, we compute the -month-ahead predictive distribution for each model (for ), keeping the length of the estimation sample fixed at observations (i.e., a rolling window of years).555In addition to our baseline sample ending in 2019:12, we present the results of our forecasting exercise including observations covering the COVID-19 pandemic (2020:01 to 2020:08) in Sub-section 4.5. Since the pandemic caused severe outliers in our dataset, including those periods helps to test the forecasting performance of our models during turbulent times. For these periods we contrast each forecast with the realization of inflation in the vintage one-quarter-ahead, following the evaluation approach of Chan (2017). As most data revisions take place in the first quarter while afterwards the vintages remain relatively unchanged (see, e.g., Croushore, 2011; Pfarrhofer, 2020), we make sure that realized inflation is not subject to revisions anymore.

One key limitation is that all methods are specified conditionally on and thus implicitly on the specific function used to move from to . Another key objective of this paper is to control for uncertainty with respect to by using dynamic model averaging techniques. For obtaining predictive combinations, we use the first observations of our hold-out sample. The remaining periods (i.e., ranging from 2002:01 to 2019:12) then constitute our evaluation sample and the respective predictions are again contrasted to the one-quarter-ahead vintage of inflation.

In terms of competing models we can classify the specifications along two dimensions:

-

1.

How is constructed. First, let denote a -dimensional vector of covariates except for . is then composed of lags of with . In our empirical work we set and include all variables in the dataset (except for the transformed CPI series, i.e., ). We then use the different dimension reduction techniques outlined in Section 2 to estimate . Moreover, we include lags of as additional observed factors to . This serves to investigate how different dimension reduction techniques perform when interest centers on predicting inflation. We also consider simple AR() models as well as a small- and a large-scale AR specification augmented with (observed) exogenous covariates (henceforth labeled ARX) as additional competitors. For the small-scale variants we include five exogenous regressors, while for the large-scale ARX model we use additional covariates. Since the macroeconomic forecasting literature is quite inconclusive about variable inclusion in such predictive ARX models for inflation (see, e.g., De Mol et al., 2008; Stock and Watson, 2008; Koop and Korobilis, 2012; Hauzenberger et al., 2019), we use a semi-automatic approach which handles this issue rather agnostically. We discuss this in more detail in Sub-section 4.2.

-

2.

The relationship between and . The second dimension along which our models differ is the specific relationship described by Eq. (3). To investigate whether non-linear dimension reduction techniques are sufficient to control for unknown forms of non-linearities, we benchmark all our models that feature TVPs with their respective constant parameter counterparts. To perform model selection we consider two priors. The first one is the horseshoe (HS, Carvalho et al., 2010) prior and the second one is an adaptive Minnesota (MIN, see Carriero et al., 2015; Giannone et al., 2015) prior (for further details see Section B of the Online Appendix).

4.2 Properties of the factors

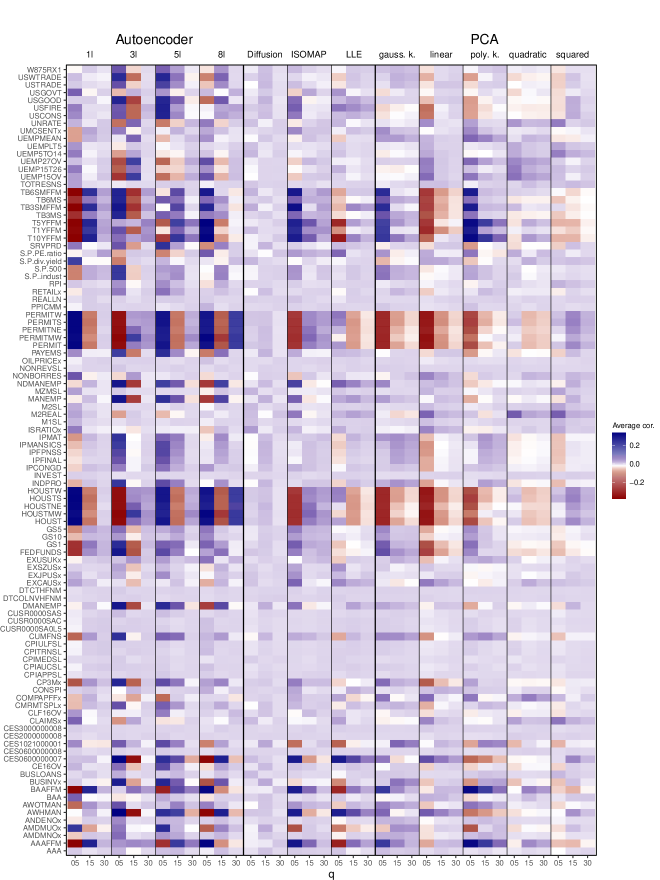

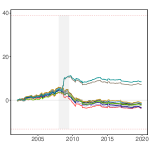

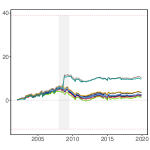

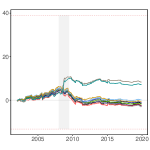

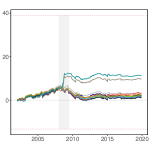

In this sub-section we analyze bivariate correlations between the factors, obtained from using different dimension reduction techniques, and the variables in our dataset as well as inflation. These correlations provide some information on the specific factor dynamics and (with caution) on how to interpret the factors in from a structural perspective.666The estimates of the factor are considerably more difficult to interpret. Nevertheless, to provide some intuition on how the factors for the best performing specifications evolve over time, see Figure A.1 in the Online Appendix. The recent literature (Crawford et al., 2018, 2019; Joseph, 2019) advocates using linear approximations or Shapley values to improve interpretability of these highly non-linear models. In this paper, we opt for a simple correlation-based approach given the large amount of competing dimension reduction techniques and the fact that for some of these the different techniques work better than for other methods.

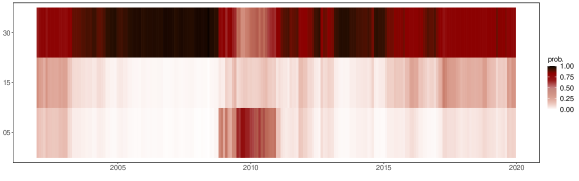

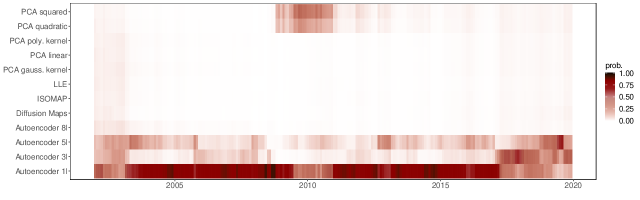

Figure 1 is a heatmap of the correlations with rows denoting the different covariates in and columns representing the different dimension reduction techniques. These correlations are averages across the factors (in case that ) and, since we include several lags of the input dataset, are also averaged across the lags.

The figure suggests for most dimension reduction techniques that the factors are correlated with housing quantities (PERMIT and HOUST alongside their sub-components) as well as interest rate spreads. Some variables which measure real activity (such as industrial production and several of its components) also display comparatively large correlations with the factors. In some cases, these correlations are positive whereas in other cases, correlations are negative. In both instances, however, the absolute magnitudes are similar. The three exceptions from this rather general pattern are diffusion maps as well as PCA quadratic and squared. In this case, the corresponding columns indicate lower correlations.

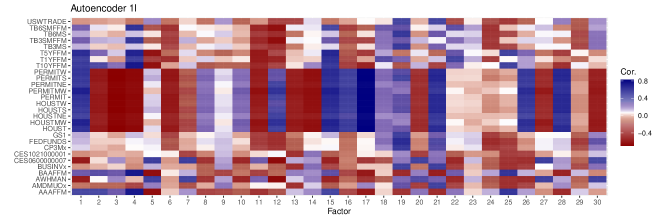

Averaging over the factors, as done in Figure 1, potentially masks important features of individual factors. Next we ask whether there are relevant differences by analyzing the correlations between each and each column of . For brevity, we focus on a specific model that performs extraordinarily well in terms of density forecasts: the Autoencoder with a single hidden layer and factors. Figure 2 shows, for each factor, the five variables which display the largest absolute correlation. The variables in the rows are a union over the sets of top-five variables for each factor. This figure shows that several factors display quite similar correlation patterns. For all of them, housing quantities are either positively or negatively correlated (with similar magnitudes). Apart from that, and in consistence with the findings discussed above, we observe that financial market variables (such as interest rate spreads) show up frequently for several factors. Only very few factors depart from this overall pattern. In the case of factors 9, 22, 23 and 24 we find low correlations with housing and much stronger correlations with financial markets. In fact, factor 9 is closely tracking the credit (BAAFFM) and term spreads (e.g., T10YFFM).

These two heatmaps provide a rough overview on what variables drive the factors. Next, we ask whether we can construct models based on including variables which display the strongest correlations with the factors. This approach can be interpreted as a simple selection device which takes non-linearities in the input dataset implicitly into account. Since the heatmap is based on full-sample results and we are interested in using these small-scale models for out-of-sample forecasting we compute the correlation for each point in our hold-out period. In summary, the variables which frequently show up across hold-out periods and dimension reduction techniques are:

-

•

Real activity and housing: Variables on industrial production (INDPRO, IPMANSICS), capacity utilization (CUMFNS) and private housing starts (HOUST) and permits (PERMIT),

-

•

Labor market: Variables on (un-)employment (MANEMP, USGOOD) and average hours worked (CES0600000007, AWHMAN),

-

•

Prices: Sub-indicators of consumer prices (CUSR0000SA0L5),

-

•

Interest rates and other stock market variables: Spreads (to the Fed funds rate) of treasuries (TB3SMFFM, TB6SMFFM, T1YFFM, T10YFFM) and of corporate bonds (AAAFFM, BAAFFM, COMPAPFFx),

-

•

Money stocks and reserves: Non-borrowed reserves (NONBORRES) and adjusted monetary base (AMBSL).

These variables are also the ones which display high correlations to the factors in Figure 1 and are included in the large-scale ARX model. Here, it is worth stressing that there seems to be appreciable heterogeneity with respect to dimension reduction methods. Most of them generate factors that are highly correlated with real activity and housing measures as well as interest rates and other stock market variables. Interestingly, when we focus on the second group we observe that the factors arising from using PCA squared (and to a somewhat lesser extent PCA quadratic) are heavily related to labor market measures. Average correlations with prices (i.e., CUSR0000SA0L5) are small for most techniques (with PCA quadratic yielding the largest correlations of around ). Some methods also yield factors that are strongly correlated to money stocks and reserves (e.g., diffusion maps). Table C.3 of the Online Appendix provides a much more detailed picture on the precise variables used to build the small-scale models.

| Business Cycle | No. of factors | PCA linear | PCA quadratic | PCA squared | PCA gauss. kernel | PCA poly. kernel | ISOMAP | Diffusion Maps | LLE | Autoen- coder 1l | ||

| Full Sample | q = 05 | 0.017 | 0.114 | 0.113 | 0.013 | 0.016 | 0.007 | 0.061 | 0.009 | 0.008 | ||

| q = 05 | (0.003,0.043) | (0.006,0.251) | (0.006,0.250) | (0.004,0.024) | (0.003,0.035) | (0.002,0.010) | (0.002,0.163) | (0.003,0.017) | (0.002,0.018) | |||

| q = 15 | 0.086 | 0.069 | 0.068 | 0.030 | 0.069 | 0.034 | 0.052 | 0.013 | 0.035 | |||

| q = 15 | (0.003,0.198) | (0.003,0.251) | (0.005,0.250) | (0.004,0.133) | (0.003,0.206) | (0.003,0.095) | (0.001,0.163) | (0.001,0.035) | (0.004,0.090) | |||

| q = 30 | 0.108 | 0.049 | 0.050 | 0.052 | 0.106 | 0.043 | 0.063 | 0.036 | 0.036 | |||

| q = 30 | (0.002,0.259) | (0.003,0.251) | (0.005,0.250) | (0.004,0.274) | (0.003,0.292) | (0.001,0.143) | (0.001,0.185) | (0.001,0.168) | (0.001,0.163) | |||

| Expansion | q = 05 | 0.027 | 0.069 | 0.055 | 0.033 | 0.030 | 0.021 | 0.045 | 0.010 | 0.023 | ||

| q = 05 | (0.016,0.049) | (0.003,0.151) | (0.003,0.110) | (0.013,0.059) | (0.019,0.050) | (0.009,0.050) | (0.022,0.098) | (0.003,0.02) | (0.006,0.043) | |||

| q = 15 | 0.073 | 0.057 | 0.055 | 0.030 | 0.061 | 0.035 | 0.049 | 0.020 | 0.039 | |||

| q = 15 | (0.001,0.192) | (0.003,0.151) | (0.003,0.110) | (0.003,0.087) | (0.009,0.194) | (0.003,0.118) | (0.005,0.098) | (0.003,0.068) | (0.003,0.115) | |||

| q = 30 | 0.103 | 0.047 | 0.045 | 0.049 | 0.098 | 0.040 | 0.053 | 0.043 | 0.041 | |||

| q = 30 | (0.001,0.290) | (0.001,0.151) | (0.001,0.110) | (0.001,0.276) | (0.009,0.285) | (0.001,0.134) | (0.005,0.116) | (0.003,0.209) | (0.001,0.196) | |||

| Recession | q = 05 | 0.098 | 0.250 | 0.248 | 0.121 | 0.116 | 0.042 | 0.180 | 0.065 | 0.071 | ||

| q = 05 | (0.040,0.156) | (0.123,0.442) | (0.123,0.442) | (0.049,0.149) | (0.051,0.163) | (0.014,0.091) | (0.122,0.269) | (0.007,0.114) | (0.012,0.190) | |||

| q = 15 | 0.152 | 0.137 | 0.136 | 0.097 | 0.143 | 0.090 | 0.133 | 0.067 | 0.068 | |||

| q = 15 | (0.004,0.286) | (0.012,0.442) | (0.016,0.442) | (0.003,0.321) | (0.022,0.326) | (0.015,0.205) | (0.019,0.269) | (0.003,0.172) | (0.010,0.188) | |||

| q = 30 | 0.152 | 0.110 | 0.114 | 0.118 | 0.158 | 0.104 | 0.132 | 0.081 | 0.077 | |||

| q = 30 | (0.004,0.297) | (0.009,0.442) | (0.011,0.442) | (0.003,0.321) | (0.022,0.424) | (0.005,0.366) | (0.003,0.306) | (0.003,0.180) | (0.003,0.297) | |||

| Pandemic | q = 05 | 0.320 | 0.285 | 0.287 | 0.124 | 0.231 | 0.199 | 0.367 | 0.303 | 0.087 | ||

| q = 05 | (0.059,0.631) | (0.188,0.424) | (0.216,0.423) | (0.020,0.210) | (0.017,0.642) | (0.101,0.303) | (0.127,0.610) | (0.087,0.506) | (0.046,0.131) | |||

| q = 15 | 0.292 | 0.322 | 0.314 | 0.292 | 0.260 | 0.173 | 0.308 | 0.228 | 0.126 | |||

| q = 15 | (0.059,0.631) | (0.015,0.641) | (0.012,0.642) | (0.020,0.734) | (0.008,0.642) | (0.022,0.559) | (0.053,0.610) | (0.088,0.402) | (0.017,0.365) | |||

| q = 30 | 0.269 | 0.348 | 0.320 | 0.260 | 0.262 | 0.261 | 0.313 | 0.358 | 0.160 | |||

| q = 30 | (0.029,0.631) | (0.015,0.641) | (0.010,0.642) | (0.020,0.796) | (0.008,0.646) | (0.001,0.764) | (0.001,0.886) | (0.057,0.821) | (0.007,0.475) |

Note: The values are averaged across the number of factors stated in the second column with minimum and maximum values in parentheses. All correlation values are absolute values. The periods are divided into business cycle phases according to the NBER (https://www.nber.org/research/business-cycle-dating).

Next, we ask whether the factors are correlated to inflation. Table 1 shows the correlation with inflation averaged across the number of factors for each dimension reduction techniques as well as the minimum and maximum value (across these factors) in parentheses. To assess whether these correlations differ over time, we divide our sample into expansionary and recessionary periods.777Recessions are defined by using the the business cycle classification of the National Bureau of Economic Research (NBER). Since the COVID-19 pandemic marks an extraordinary period in our sample, we also compute the correlations for 2020 only and include it at the bottom of Table 1.

For the full sample as well as during expansions, we find that the factors obtained from using the linear variants of PCA display comparatively higher correlations relative to the other dimension reduction techniques (with some of the factors featuring a correlation of close to ). In recessions and the pandemic, these correlations increase substantially to reach average correlations close to (with the factor displaying the maximum correlation being strongly related to inflation, with values of around ). The non-linear dimension reduction techniques yield strong correlations during turbulent times (i.e., recessions and the pandemic). This is not surprising since these methods tend to work well if there are strong deviations from linearity (which mostly occurs in recessions). Such a feature can be easily demonstrated by considering PCA squared. In normal times, the factors will be centered around zero and typically display little variation. But in recessions the link function implies that larger changes will dominate the shape of the factors and imply pronounced movements which could be helpful for predicting turning points in inflation.

4.3 Density and point forecast performance

We now consider point and density forecasting performance of the different models and dimension reduction techniques. The forecast performance is evaluated through log predictive likelihoods (LPLs) for density forecasts and root mean squared errors (RMSEs) for point forecasts. Superior models are those with high scores in terms of LPL and low values in terms of RMSE. We benchmark all models relative to the autoregressive (AR) model with constant parameters and the Minnesota prior. The first entry in the tables gives the actual value of the LPL (cumulated over the hold-out sample) with actual RMSEs in parentheses (averaged over the hold-out sample) for our benchmark model. The remaining entries are differences in LPLs with relative RMSEs in parentheses. We mark statistically significant results according to the Diebold and Mariano (1995) test at the one, five and ten percent significance levels with one, two and three asterisks, respectively.

| Specification | const. (MIN) | const. (HS) | TVP (MIN) | TVP (HS) | |

| AR | -329.28 | 0.23 | -0.99 | -1.04 | |

| (1.24) | (0.98) | (0.98) | (0.98) | ||

| Large ARX | 2.46 | -9.80*** | -8.95*** | ||

| (0.97) | (1.06***) | (1.04***) | |||

| Autoencoder 1l (q = 05) | 2.19 | -2.06 | 1.12 | -1.43 | |

| (0.98) | (0.99) | (0.97) | (0.99) | ||

| Autoencoder 1l (q = 15) | 16.26*** | 12.71*** | 21.41*** | 13.69*** | |

| (0.90***) | (0.91***) | (0.87***) | (0.90***) | ||

| Autoencoder 1l (q = 30) | 38.19*** | 29.92*** | 35.48*** | 31.39*** | |

| (0.81***) | (0.84***) | (0.80***) | (0.83***) | ||

| Autoencoder 3l (q = 05) | 3.55 | -1.59 | 1.90 | -2.35 | |

| (0.97) | (0.99) | (0.97) | (0.99) | ||

| Autoencoder 3l (q = 15) | 11.52*** | 8.90** | 13.19** | 8.35** | |

| (0.94**) | (0.95*) | (0.92**) | (0.95**) | ||

| Autoencoder 3l (q = 30) | 23.63*** | 16.44*** | 18.62* | 12.81* | |

| (0.86***) | (0.88***) | (0.83***) | (0.87***) | ||

| Autoencoder 5l (q = 05) | 2.50 | -2.07 | 1.55 | -2.74 | |

| (0.97) | (0.99) | (0.97) | (0.99) | ||

| Autoencoder 5l (q = 15) | 10.05* | 4.45 | 11.65* | 5.62 | |

| (0.94**) | (0.95) | (0.93**) | (0.94*) | ||

| Autoencoder 5l (q = 30) | 26.91*** | 22.80*** | 26.72*** | 23.12*** | |

| (0.85***) | (0.86***) | (0.84***) | (0.86***) | ||

| Autoencoder 8l (q = 05) | 1.79 | -2.58 | 3.27 | -3.05 | |

| (0.97) | (0.99) | (0.97) | (0.99) | ||

| Autoencoder 8l (q = 15) | 2.86 | -4.34 | 1.49 | -2.52 | |

| (0.98) | (1.00) | (0.97) | (1.00) | ||

| Autoencoder 8l (q = 30) | 5.64 | -0.97 | 7.21* | 0.13 | |

| (0.97) | (0.99) | (0.95) | (0.98) | ||

| Diffusion Maps (q = 05) | 2.12 | -3.64 | 2.97 | -2.40 | |

| (0.98) | (1.00) | (0.98) | (1.00) | ||

| Diffusion Maps (q = 15) | 2.10 | -8.17** | 2.13 | -7.54** | |

| (0.98) | (1.03**) | (0.99) | (1.03**) | ||

| Diffusion Maps (q = 30) | 2.55 | -9.13** | 3.81 | -6.79* | |

| (0.98) | (1.03**) | (0.97) | (1.02**) | ||

| ISOMAP (q = 05) | 2.55 | -3.36 | 2.28 | -1.24 | |

| (0.98) | (0.99) | (0.97) | (0.99) | ||

| ISOMAP (q = 15) | 3.01 | -5.33* | 1.31 | -5.46* | |

| (0.97) | (1.01) | (0.98) | (1.01*) | ||

| ISOMAP (q = 30) | 1.50 | -6.04** | 2.36 | -4.53 | |

| (0.97) | (1.01**) | (0.97) | (1.01) | ||

| LLE (q = 05) | 1.39 | -2.23 | 1.93 | -1.84 | |

| (0.98) | (0.99) | (0.98) | (1.00) | ||

| LLE (q = 15) | 2.68 | -5.87** | 0.83 | -5.18* | |

| (0.97) | (1.02*) | (0.97) | (1.01) | ||

| LLE (q = 30) | 1.86 | -11.38** | 0.45 | -11.49** | |

| (0.98) | (1.02*) | (0.98) | (1.01*) | ||

| PCA gauss. kernel (q = 05) | 2.44 | -1.37 | 1.50 | 0.07 | |

| (0.98) | (0.99) | (0.97) | (0.98) | ||

| PCA gauss. kernel (q = 15) | 2.97 | -1.30 | 1.85 | -3.88 | |

| (0.98) | (0.99) | (0.98) | (0.99) | ||

| PCA gauss. kernel (q = 30) | 2.68 | -2.94 | 3.10 | -1.36 | |

| (0.97) | (1.00) | (0.97) | (0.99) | ||

| PCA linear (q = 05) | 1.96 | -3.74 | 1.27 | -2.46 | |

| (0.98) | (1.00) | (0.98) | (0.99) | ||

| PCA linear (q = 15) | 3.78 | -4.89 | 3.35 | -3.76 | |

| (0.97) | (1.01) | (0.97) | (1.00) | ||

| PCA linear (q = 30) | 3.25 | -7.51** | 2.10 | -5.38 | |

| (0.97) | (1.02**) | (0.98) | (1.02**) | ||

| PCA poly. kernel (q = 05) | 3.74 | -1.06 | 2.50 | -0.76 | |

| (0.98) | (0.99) | (0.98) | (0.99) | ||

| PCA poly. kernel (q = 15) | 1.01 | -1.90 | 2.37 | -2.17 | |

| (0.98) | (0.99) | (0.98) | (0.99) | ||

| PCA poly. kernel (q = 30) | 4.28 | -1.78 | 2.51 | -2.43 | |

| (0.97) | (0.99) | (0.97) | (0.99) | ||

| PCA quadratic (q = 05) | 10.56** | 7.15 | 9.72* | 8.32 | |

| (0.91*) | (0.93) | (0.90*) | (0.93) | ||

| PCA quadratic (q = 15) | 4.63 | 0.01 | 6.79 | 1.34 | |

| (1.00) | (0.99) | (0.97) | (0.98) | ||

| PCA quadratic (q = 30) | 3.15 | -7.23 | 5.11 | -4.72 | |

| (0.97) | (1.04**) | (0.96) | (1.03*) | ||

| PCA squared (q = 05) | 9.78* | 8.44 | 11.30* | 7.10 | |

| (0.90*) | (0.92) | (0.89*) | (0.92) | ||

| PCA squared (q = 15) | 5.77 | 0.70 | 7.36 | 2.47 | |

| (0.97) | (0.98) | (0.93) | (0.98) | ||

| PCA squared (q = 30) | 4.33 | -1.49 | 6.79* | -3.58 | |

| (0.97) | (1.01) | (0.95) | (1.02) |

-

•

Note: The table shows LPLs with RMSEs in parentheses below. The first (red shaded) entry gives the actual LPL and RMSE scores of our benchmark (an autoregressive (AR) model with constant parameters and a Minnesota prior). Asterisks indicate statistical significance for each model relative to the benchmark at the 1% (***), 5% (**) and 10% (*) significance levels. Since the large ARX model with time-varying parameters would features period-specific coefficients and is computationally intractable, we assume that the TVPs feature a factor structure (with three factors) to reduce the dimension of the state space (see Section B of the Online Appendix and Chan et al., 2020).

Starting with the one-month-ahead horizon, Table 2 depicts the inflation forecasting results. This table suggests that, in terms of density forecasts, using dimension reduction techniques (both linear and non-linear) improves predictions substantially. These improvements arise not only relative to the AR benchmark but also related to the large AR models with additional exogenous regressors. For some models, these improvements are sizable, irrespective of the regression specification (i.e., whether we use a constant parameter or a TVP model). Especially the Autoencoder with one and five layers sharply improves upon the benchmark (and all the remaining competitors) by large margins. Moreover, it yields statistically significant improvements at the one percent level. A similar story emerges when we focus on point forecasts. Non-linear dimension reductions help slightly. Relative RMSEs are smaller but close to one for most models. Again, the Autoencoder works well and yields RMSEs which are, across regression specifications, almost 20 percent lower than the ones from the benchmark. It is worth emphasizing that PCA squared also yields highly competitive point forecasts which are statistically significant according to the Diebold and Mariano (1995) test.

When we compare model performance across regression specifications and focus on the Minnesota-type priors, we find that constant parameter models work quite well if non-linear dimension reduction techniques such as the Autoencoder are adopted. With a single exception (diffusion maps), introducing TVPs does not pay off and yields density forecasts which are slightly more imprecise than the ones obtained from their time-invariant counterparts. If we use a horseshoe prior, this result somewhat reverses (with the caveat that the models coupled with the horseshoe sometimes yield weaker inflation forecasts than the benchmark). Here, we observe that introducing TVPs often improves log predictive likelihoods relative to the constant parameter model with the same prior.

Summing up this discussion, we observe that the Autoencoder yields favorable point and density forecasts, irrespective of the prior and regression specification chosen. This strong performance of the Autoencoder, however, depends on the number of layers as well as the number of factors. The literature (see, e.g., Huang, 2003; Heaton, 2008) suggests that the number of hidden layers should increase with the complexity of the dataset. Our results, however, suggest the opposite. For a typical US macroeconomic dataset the forecast performance of the Autoencoder seems to be strongest when a single hidden layer coupled with a large number of factors is used.

| Specification | const. (MIN) | const. (HS) | TVP (MIN) | TVP (HS) | |

| AR | -322.66 | 9.79 | 20.02 | 18.53 | |

| (1.27) | (0.94*) | (0.89*) | (0.89**) | ||

| Large ARX | 19.68 | 14.44 | 11.03 | ||

| (0.89*) | (0.94) | (0.94) | |||

| Autoencoder 1l (q = 05) | 18.26 | 15.86 | 14.72 | 17.25 | |

| (0.89*) | (0.89*) | (0.89*) | (0.89*) | ||

| Autoencoder 1l (q = 15) | 24.56 | 27.39 | 22.94 | 26.17 | |

| (0.86**) | (0.85**) | (0.86**) | (0.85**) | ||

| Autoencoder 1l (q = 30) | 22.17 | 27.55 | 24.62 | 26.65 | |

| (0.85**) | (0.84**) | (0.85**) | (0.83**) | ||

| Autoencoder 3l (q = 05) | 19.24 | 22.33 | 21.18 | 19.49 | |

| (0.87**) | (0.85**) | (0.87**) | (0.86**) | ||

| Autoencoder 3l (q = 15) | 20.24 | 21.49 | 20.54 | 20.60 | |

| (0.86**) | (0.86**) | (0.86**) | (0.85**) | ||

| Autoencoder 3l (q = 30) | 23.97 | 20.29 | 21.60 | 20.45 | |

| (0.86**) | (0.85**) | (0.86**) | (0.85**) | ||

| Autoencoder 5l (q = 05) | 20.87 | 16.60 | 18.60 | 19.66 | |

| (0.86**) | (0.86**) | (0.87**) | (0.86**) | ||

| Autoencoder 5l (q = 15) | 15.15 | 14.34 | 15.71 | 14.00 | |

| (0.86**) | (0.86**) | (0.87**) | (0.86**) | ||

| Autoencoder 5l (q = 30) | 21.13 | 22.40 | 19.67 | 21.44 | |

| (0.86**) | (0.85**) | (0.86**) | (0.85**) | ||

| Autoencoder 8l (q = 05) | 20.82 | 18.27 | 16.17 | 17.18 | |

| (0.88*) | (0.88*) | (0.89*) | (0.88*) | ||

| Autoencoder 8l (q = 15) | 12.21 | 6.51 | 8.01 | 7.27 | |

| (0.88*) | (0.92) | (0.90) | (0.91) | ||

| Autoencoder 8l (q = 30) | -3.75 | -16.20 | -11.91 | -14.54 | |

| (0.89) | (0.90) | (0.89) | (0.90) | ||

| Diffusion Maps (q = 05) | 16.27 | 20.18 | 12.09 | 18.18 | |

| (0.86**) | (0.86**) | (0.86**) | (0.86**) | ||

| Diffusion Maps (q = 15) | 19.69 | 16.58 | 17.53 | 14.27 | |

| (0.86**) | (0.86**) | (0.86**) | (0.86**) | ||

| Diffusion Maps (q = 30) | 17.02 | 13.20 | 20.08 | 12.27 | |

| (0.87**) | (0.89*) | (0.86**) | (0.88**) | ||

| ISOMAP (q = 05) | 18.01 | 16.89 | 15.62 | 18.45 | |

| (0.86**) | (0.86**) | (0.87**) | (0.86**) | ||

| ISOMAP (q = 15) | 19.75 | 11.58 | 13.79 | 11.19 | |

| (0.86**) | (0.86**) | (0.87**) | (0.86**) | ||

| ISOMAP (q = 30) | 12.01 | 3.63 | 5.41 | 2.66 | |

| (0.86**) | (0.85**) | (0.87**) | (0.86**) | ||

| LLE (q = 05) | 14.10 | 5.25 | 9.71 | 5.27 | |

| (0.87**) | (0.87**) | (0.87**) | (0.87**) | ||

| LLE (q = 15) | -11.38 | -13.20 | -18.14 | -10.97 | |

| (0.88*) | (0.88) | (0.89) | (0.88) | ||

| LLE (q = 30) | -1.39 | -38.94 | -11.37 | -40.18 | |

| (0.87**) | (0.87*) | (0.88*) | (0.87*) | ||

| PCA gauss. kernel (q = 05) | 17.21 | 17.81 | 20.04 | 15.67 | |

| (0.88*) | (0.88**) | (0.88*) | (0.88*) | ||

| PCA gauss. kernel (q = 15) | 15.63 | 14.29 | 16.88 | 17.30 | |

| (0.88*) | (0.88*) | (0.88*) | (0.88*) | ||

| PCA gauss. kernel (q = 30) | 19.03 | 19.01 | 18.04 | 18.17 | |

| (0.88**) | (0.88**) | (0.88**) | (0.88**) | ||

| PCA linear (q = 05) | 17.05 | 15.66 | 15.05 | 14.73 | |

| (0.90*) | (0.90*) | (0.90) | (0.90*) | ||

| PCA linear (q = 15) | 18.79 | 19.39 | 16.35 | 14.59 | |

| (0.88*) | (0.88*) | (0.89*) | (0.88*) | ||

| PCA linear (q = 30) | 21.39 | 18.10 | 19.18 | 18.21 | |

| (0.87**) | (0.87*) | (0.88*) | (0.87*) | ||

| PCA poly. kernel (q = 05) | 18.98 | 16.48 | 15.09 | 14.71 | |

| (0.89*) | (0.90*) | (0.89*) | (0.89*) | ||

| PCA poly. kernel (q = 15) | 18.73 | 19.44 | 18.52 | 20.78 | |

| (0.88*) | (0.88**) | (0.88*) | (0.88**) | ||

| PCA poly. kernel (q = 30) | 22.11 | 20.63 | 19.63 | 21.22 | |

| (0.87**) | (0.87**) | (0.88**) | (0.87**) | ||

| PCA quadratic (q = 05) | 40.33*** | 46.67** | 41.31*** | 48.50*** | |

| (0.84**) | (0.79***) | (0.84**) | (0.79***) | ||

| PCA quadratic (q = 15) | 20.37 | 33.39 | 17.63 | 34.40 | |

| (0.91) | (0.86*) | (0.91) | (0.86*) | ||

| PCA quadratic (q = 30) | 24.90 | 26.61 | 28.50* | 26.91 | |

| (0.87**) | (0.89**) | (0.87**) | (0.90**) | ||

| PCA squared (q = 05) | 46.84*** | 46.30** | 45.90*** | 47.62** | |

| (0.80**) | (0.76***) | (0.81**) | (0.76***) | ||

| PCA squared (q = 15) | 24.28 | 33.35* | 23.02 | 32.54* | |

| (0.87*) | (0.87*) | (0.87*) | (0.88*) | ||

| PCA squared (q = 30) | 28.25* | 27.59 | 26.46* | 27.35 | |

| (0.86**) | (0.88**) | (0.86**) | (0.88**) |

-

•

Note: The table shows LPLs with RMSEs in parentheses below. The first (red shaded) entry gives the actual LPL and RMSE scores of our benchmark (an autoregressive (AR) model with constant parameters and a Minnesota prior). Asterisks indicate statistical significance for each model relative to the benchmark at the 1% (***), 5% (**) and 10% (*) significance levels. Since the large ARX model with time-varying parameters would features period-specific coefficients and is computationally intractable, we assume that the TVPs feature a factor structure (with three factors) to reduce the dimension of the state space (see Section B of the Online Appendix and Chan et al., 2020).

Next, we inspect the longer forecast horizon in greater detail. Table 3 depicts the forecast performance of all competitors for the one-quarter-ahead horizon. The table indicates that several non-linear dimension reduction techniques (most notably the Autoencoder, PCA quadratic and PCA squared) clearly outperform the autoregressive benchmark as well as models based on linear PCs. The improvements relative to linear PCs are sizable and statistically significant (especially for squared and quadratic PCs). For this horizon, the large ARX models also exhibit excellent forecasting properties.

Zooming into the different approaches to dimension reduction reveals that PCA quadratic with TVPs yields highest LPLs. Among the different dimension reduction techniques, both PCA quadratic and squared stand out and improve appreciably against all other dimension reduction techniques. The Autoencoder also provides density forecasts which are highly competitive.

When we consider point forecasts a similar picture arises. Here we find that models which do well in terms of LPLs also yield precise point forecasts. The single best performing specification, however, is PCA squared with five factors, constant parameters and a horseshoe prior. This model improves upon the AR benchmark by around 24 percent. Notice, however, that the same model but with TVPs also yields forecasts which are 24 percent more precise than the ones of the benchmark. This suggests that the horseshoe shrinks the TVPs close to zero and the corresponding point estimators are almost identical. Since the LPLs differ, the remaining time-variation in the coefficients mainly impacts the LPLs through the predictive variance.

Table 4 provides a summary of the best performing models for the one-month and the one-quarter-ahead forecasts, respectively. Moreover, we also assess how a model which includes the five variables displaying the highest average correlations to the factors performs (see discussion in Sub-section 4.2). These models are labeled small ARX in the table. The results suggest that for one-month-ahead forecasts, replacing the latent factors arising from the Autoencoder with observed variables that display a high correlation to the factors does not pay off in terms of point and density forecasts. Across all regression specifications, the RMSEs are higher and the LPLs lower. When we consider one-quarter-ahead forecasts, however, this strategy seems to work much better. In this case, smaller models with covariates selected based on their correlations to the factors obtained by using PCA squared and PCA quadratic yield density predictions which are close to the ones obtained from exploiting all available data. Notice, however, that for point forecasts, the performance of the small models is inferior.

| Specification | const. (MIN) | const. (HS) | TVP (MIN) | TVP (HS) | ||

| One-month-ahead | ||||||

| AR | -329.28 | |||||

| (1.24) | ||||||

| Autoencoder 1l (q = 30) | 38.19*** | 29.92*** | 35.48*** | 31.39*** | ||

| (0.81***) | (0.84***) | (0.80***) | (0.83***) | |||

| Small ARX based on | 1.39 | -2.02 | 1.97 | -2.27 | ||

| Autoencoder 1l (q = 30) | (0.98) | (0.99) | (0.98) | (0.99) | ||

| One-quarter-ahead | ||||||

| AR | -322.66 | |||||

| (1.27) | ||||||

| PCA quadratic (q = 05) | 40.33*** | 46.67** | 41.31*** | 48.50*** | ||

| (0.84**) | (0.79***) | (0.84**) | (0.79***) | |||

| PCA squared (q = 05) | 46.84*** | 46.30** | 45.90*** | 47.62** | ||

| (0.80**) | (0.76***) | (0.81**) | (0.76***) | |||

| Small ARX based on | 38.20** | 43.73** | 39.41** | 43.28** | ||

| PCA quadratic (q = 5) | (1.05) | (0.93) | (1.04) | (0.93) | ||

| Small ARX based on | 36.25** | 42.90** | 38.87** | 44.25** | ||

| PCA squared (q = 5) | (1.09) | (0.95) | (1.09) | (0.95) | ||

-

•

Note: The table shows LPLs with RMSEs in parentheses below. While the first entry denotes the benchmark (shaded in red), other entries contrast the best performing model(s) as presented in the Tables 2 and 3 with ARX models. For these ARX specifications the best performing model solely serves as an unsupervised variable selection device. Conditional on the latent factors of this best performing dimension reduction technique, we always include the top-five correlated variables as covariates alongside the lags of inflation (see Figure C.1 of the Online Appendix). Asterisks indicate statistical significance for each model relative to the benchmark at the 1% (***), 5% (**) and 10% (*) significance levels.

Before proceeding to the next sub-section we briefly discuss two important issues. First, it is worth stressing that the factors used in this forecasting exercise are extracted from the full set of variables in . In Table A.1 and Table A.2 of the Online Appendix we divide the dataset into slow- and fast-moving variables (Bernanke et al., 2005) and extract the latent factors from these partitioned datasets exclusively. The main results based on extracting the factors from the full dataset remain in place: for one-month-ahead forecasts we find the Autoencoder to perform particularly well whereas for one-quarter-ahead predictions PCA squared and quadratic yield accurate forecast densities.

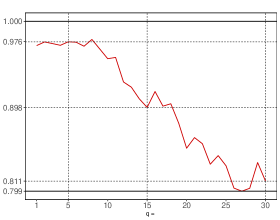

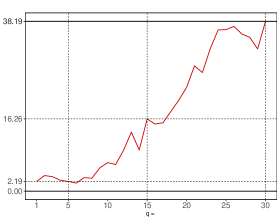

Second, for one of our best performing models (the Autoencoder with one hidden layer) forecasting performance changes sharply when the number of factors is changed. This raises the question on how the relationship between the number of factors and forecast performance is. In Figure 3 in the Online Appendix we show two graphs that discuss how point and density forecasting performance change with the number of factors. In this exercise we find that the largest jumps in predictive accuracy is found when increasing the number of factors from 17 to 24 and again from 29 to 30 in terms of LPLs and from 18 to 26 and 29 to 30 in terms of RMSE.

4.4 Assessing model calibration using probability integral transforms

The results based on RMSEs and LPLs provide information on relative forecasting performance. In the next step, we ask whether the different methods and models we propose yield predictive distribution which are better calibrated. To this end, we consider the normalized forecast errors obtained through the probability integral transform (PIT). If a model is correctly specified the PITs are iid uniformly distributed and the respective standardized forecast errors should be iid normally distributed. Departures from the standard Gaussian distribution allow us to inspect along what dimensions the model is poorly calibrated. For instance, if the variance of the normalized forecast error is too small (i.e., below one) this is evidence that the predictive distribution is too wide (i.e., too many predictions are in the tails) while values greater than one indicate that the variance is too tight (i.e., the tails are not adequately represented).

| Specification | const. (MIN) | const. (HS) | TVP (MIN) | TVP (HS) | ||||||||||||

| Mean | Variance | AR(1) coef. | Mean | Variance | AR(1) coef. | Mean | Variance | AR(1) coef. | Mean | Variance | AR(1) coef. | |||||

| AR | 0.018 | 1.171 | 0.063 | 0.035 | 1.182 | 0.067 | 0.024 | 1.165 | 0.032 | 0.038 | 1.189 | 0.063 | ||||

| Large ARX | 0.036 | 1.166 | 0.086 | 0.029 | 1.198 | 0.061 | 0.026 | 1.195 | 0.069 | |||||||

| Autoencoder 1l (q = 05) | 0.028 | 1.182 | 0.082 | 0.031 | 1.194 | 0.068 | 0.024 | 1.188 | 0.081 | 0.034 | 1.191 | 0.063 | ||||

| Autoencoder 1l (q = 15) | 0.020 | 1.176 | 0.067 | 0.029 | 1.203 | 0.054 | 0.007 | 1.155 | 0.066 | 0.030 | 1.199 | 0.054 | ||||

| Autoencoder 1l (q = 30) | 0.010 | 1.293** | 0.010 | 0.028 | 1.336** | 0.002 | 0.005 | 1.307** | -0.013 | 0.023 | 1.317** | -0.004 | ||||

| Autoencoder 3l (q = 05) | 0.030 | 1.175 | 0.083 | 0.038 | 1.191 | 0.063 | 0.030 | 1.183 | 0.067 | 0.035 | 1.196 | 0.067 | ||||

| Autoencoder 3l (q = 15) | 0.045 | 1.187 | 0.084 | 0.044 | 1.200 | 0.059 | 0.029 | 1.193 | 0.062 | 0.045 | 1.203 | 0.057 | ||||

| Autoencoder 3l (q = 30) | -0.005 | 1.277* | 0.050 | 0.009 | 1.315** | 0.018 | -0.041 | 1.343* | 0.061 | 0.005 | 1.357** | 0.027 | ||||

| Autoencoder 5l (q = 05) | 0.034 | 1.181 | 0.084 | 0.036 | 1.189 | 0.065 | 0.031 | 1.183 | 0.077 | 0.039 | 1.192 | 0.062 | ||||

| Autoencoder 5l (q = 15) | 0.040 | 1.191 | 0.068 | 0.057 | 1.220 | 0.041 | 0.032 | 1.196 | 0.056 | 0.058 | 1.218 | 0.035 | ||||

| Autoencoder 5l (q = 30) | 0.062 | 1.225 | 0.074 | 0.067 | 1.230 | 0.058 | 0.039 | 1.244 | 0.059 | 0.066 | 1.233 | 0.046 | ||||

| Autoencoder 8l (q = 05) | 0.034 | 1.190 | 0.088 | 0.039 | 1.193 | 0.068 | 0.034 | 1.167 | 0.081 | 0.036 | 1.201 | 0.064 | ||||

| Autoencoder 8l (q = 15) | 0.038 | 1.174 | 0.079 | 0.033 | 1.201 | 0.075 | 0.030 | 1.193 | 0.090 | 0.039 | 1.189 | 0.071 | ||||

| Autoencoder 8l (q = 30) | 0.032 | 1.164 | 0.070 | 0.027 | 1.187 | 0.048 | 0.025 | 1.152 | 0.072 | 0.026 | 1.180 | 0.045 | ||||

| Diffusion Maps (q = 05) | 0.025 | 1.193 | 0.079 | 0.023 | 1.212 | 0.070 | 0.012 | 1.166 | 0.070 | 0.026 | 1.198 | 0.067 | ||||

| Diffusion Maps (q = 15) | 0.037 | 1.192 | 0.079 | 0.031 | 1.211 | 0.068 | 0.027 | 1.188 | 0.075 | 0.031 | 1.210 | 0.064 | ||||

| Diffusion Maps (q = 30) | 0.032 | 1.194 | 0.083 | 0.034 | 1.212 | 0.059 | 0.029 | 1.187 | 0.070 | 0.033 | 1.190 | 0.054 | ||||

| ISOMAP (q = 05) | 0.024 | 1.170 | 0.085 | 0.026 | 1.197 | 0.057 | 0.020 | 1.175 | 0.082 | 0.031 | 1.178 | 0.060 | ||||

| ISOMAP (q = 15) | 0.027 | 1.180 | 0.086 | 0.027 | 1.189 | 0.058 | 0.024 | 1.181 | 0.080 | 0.021 | 1.194 | 0.059 | ||||

| ISOMAP (q = 30) | 0.031 | 1.195 | 0.079 | 0.026 | 1.194 | 0.068 | 0.026 | 1.193 | 0.085 | 0.031 | 1.188 | 0.065 | ||||

| LLE (q = 05) | 0.029 | 1.196 | 0.083 | 0.025 | 1.191 | 0.071 | 0.019 | 1.177 | 0.085 | 0.026 | 1.181 | 0.071 | ||||

| LLE (q = 15) | 0.027 | 1.189 | 0.083 | 0.025 | 1.206 | 0.067 | 0.020 | 1.185 | 0.084 | 0.022 | 1.196 | 0.066 | ||||

| LLE (q = 30) | 0.031 | 1.194 | 0.080 | 0.034 | 1.261* | 0.045 | 0.013 | 1.194 | 0.086 | 0.033 | 1.247* | 0.040 | ||||

| PCA gauss. kernel (q = 05) | 0.027 | 1.174 | 0.081 | 0.035 | 1.190 | 0.066 | 0.025 | 1.194 | 0.084 | 0.035 | 1.175 | 0.072 | ||||

| PCA gauss. kernel (q = 15) | 0.032 | 1.178 | 0.087 | 0.041 | 1.189 | 0.067 | 0.030 | 1.192 | 0.080 | 0.036 | 1.205 | 0.066 | ||||

| PCA gauss. kernel (q = 30) | 0.032 | 1.178 | 0.078 | 0.034 | 1.203 | 0.069 | 0.023 | 1.170 | 0.083 | 0.038 | 1.182 | 0.065 | ||||

| PCA linear (q = 05) | 0.033 | 1.190 | 0.083 | 0.042 | 1.208 | 0.075 | 0.023 | 1.192 | 0.091 | 0.041 | 1.183 | 0.063 | ||||

| PCA linear (q = 15) | 0.034 | 1.177 | 0.083 | 0.037 | 1.192 | 0.070 | 0.026 | 1.172 | 0.083 | 0.038 | 1.187 | 0.064 | ||||

| PCA linear (q = 30) | 0.031 | 1.185 | 0.081 | 0.035 | 1.210 | 0.067 | 0.025 | 1.176 | 0.087 | 0.030 | 1.187 | 0.063 | ||||

| PCA poly. kernel (q = 05) | 0.029 | 1.170 | 0.081 | 0.036 | 1.193 | 0.067 | 0.029 | 1.178 | 0.081 | 0.037 | 1.189 | 0.061 | ||||

| PCA poly. kernel (q = 15) | 0.028 | 1.201 | 0.078 | 0.034 | 1.193 | 0.061 | 0.034 | 1.187 | 0.077 | 0.031 | 1.192 | 0.068 | ||||

| PCA poly. kernel (q = 30) | 0.031 | 1.166 | 0.090 | 0.043 | 1.185 | 0.066 | 0.029 | 1.182 | 0.080 | 0.042 | 1.199 | 0.059 | ||||

| PCA quadratic (q = 05) | 0.029 | 1.071 | 0.044 | 0.031 | 1.070 | 0.023 | 0.034 | 1.055 | 0.026 | 0.032 | 1.052 | 0.016 | ||||

| PCA quadratic (q = 15) | 0.032 | 1.178 | 0.069 | 0.008 | 1.190 | 0.063 | 0.021 | 1.158 | 0.056 | 0.003 | 1.181 | 0.052 | ||||

| PCA quadratic (q = 30) | 0.028 | 1.177 | 0.086 | -0.003 | 1.251* | 0.085 | 0.032 | 1.163 | 0.061 | -0.004 | 1.232 | 0.090 | ||||

| PCA squared (q = 05) | 0.042 | 1.071 | 0.035 | 0.035 | 1.056 | 0.021 | 0.040 | 1.030 | 0.027 | 0.031 | 1.061 | 0.013 | ||||

| PCA squared (q = 15) | 0.031 | 1.174 | 0.070 | 0.006 | 1.173 | 0.049 | 0.033 | 1.145 | 0.041 | 0.007 | 1.157 | 0.043 | ||||

| PCA squared (q = 30) | 0.037 | 1.172 | 0.079 | -0.002 | 1.203 | 0.069 | 0.043 | 1.148 | 0.062 | -0.008 | 1.224 | 0.080 | ||||

-

•

Note: This table summarizes the normalized forecast errors, which are obtained with probability integral transformations (PIT). Similar to Clark (2011) we show the mean, the variance and the AR() coefficient of the normalized forecast errors. Given a well-calibrated model (i.e. the null-hypothesis), normalized forecast errors should have zero mean, a variance of one and experience no autocorrelation. These conditions are tested separately: 1) To test for a zero mean we compute the p-values with a Newey–West variance (with five lags). 2) To test for a unit variance we regress the squared normalized forecast errors on an intercept and allow for a Newey–West variance (with three lags). 3) To test for no autocorrelation we obtain the p-values with an AR(1) model that features an unconditional mean and heteroskedasticity-robust standard errors. Asterisks indicate statistical significance for each model at the 1% (***), 5% (**) and 10% (*) significance levels.

Table 5 shows the results for the one-month-ahead normalized forecast errors.888The results for one-quarter-ahead forecasts are provided in Section A of the Online Appendix. In principle, we observe that the mean across methods is close to zero (with some few exceptions such as PCA quadratic for ). Nevertheless, these differences are never statistically significantly different from zero. Considering the variances shows that most models yield forecast distributions which seem to be slightly too narrow (with variances exceeding one). The asterisks indicate whether the variances are significantly different from one. For some few models, this is the case (especially if we assume constancy of the parameters) but if we allow for TVPs there are only a handful of cases left. This, however, strongly depends on the shrinkage prior adopted. Turning to the autocorrelation of the normalized shocks reveals that these are mostly close to zero and never statistically significantly different from zero.

Comparing sophisticated to simple dimension reduction methods suggests no discernible differences in model calibration. In principle, approaches based on linear PCs yield normalized forecast errors with similar statistical properties than the ones obtained from using more sophisticated dimension reduction techniques.

(a) Autoencoder 1l (q = 30), const. (MIN)

(b) PCA squared (q = 05), const. (MIN)

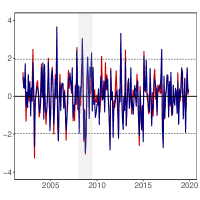

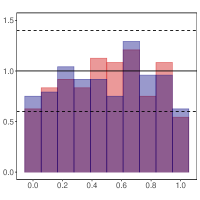

Note: This figure shows the evolution of normalized forecast errors for the one-month-ahead horizon in the left panel, the histogram of the PITs in the middle panel and the empirical cumulative density function of the PITs in the right panel. If a model is correctly specified the PITs are standard uniformly distributed and the normalized forecast errors standard normally distributed. This theoretically correct specification is indicated by the black lines, with the dashed lines referring to the respective confidence interval. In red we present the results of the benchmark, whereas in blue we indicate the respective model. The light gray shaded areas refer to the global financial crisis.

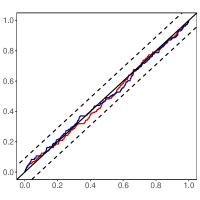

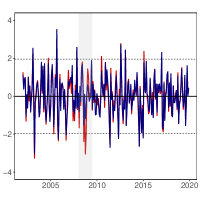

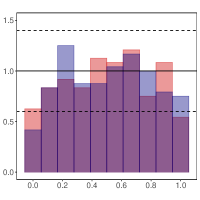

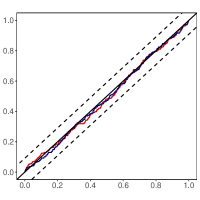

The discussion above might mask important differences in calibration of different parts of the predictive distribution. We now turn to a deeper analysis of the one-month-ahead predictive distribution of the two best performing models vis-á-vis the benchmark: the Autoencoder 1l and PCA squared . This analysis is based on visual inspection of the normalized forecast errors (left panel of Figure 3), a histogram of the PITs (middle panel of Figure 3) and the visual diagnostic of the empirical cumulative density function proposed in Rossi and Sekhposyan (2019) (right panel of Figure 3). Recall that, under correct specification, the PITs should be iid uniformly and the normalized forecast errors should be iid standard normally distributed, respectively.

The left panel of the figure indicates that for both models under consideration, normalized forecast errors are centered on zero, display little serial correlation and a variance close to one (with the Autoencoder generating slightly more spread out normalized forecast errors). In some periods, normalized forecast errors depart significantly from the standard normal distribution (i.e., the corresponding observations lie outside the 95% confidence intervals). But in general, and for both models (and the benchmark), model calibration seems to be adequate. Next, we focus on the histogram in the middle panel of Figure 3 (which includes 95% confidence intervals). From this figure, we learn that both models are well calibrated with some tendency to overestimate the upper tail risk. Finally, considering the right panel shows that all models appear to be well calibrated, with most observations being clustered around the 45 degree lines and not a single observation being outside the 95% confidence intervals.

4.5 A note on the pandemic

To the detriment of linear modeling techniques, the COVID-19 pandemic caused severe outliers for several of the time series we include in our dataset. Following the recent literature (e.g., Huber et al., 2020; Clark et al., 2021; Coulombe et al., 2021) which advocates using non-linear and non-parametric modeling techniques in turbulent times, we briefly investigate whether the non-linear dimension reduction techniques proposed in this paper yield more precise inflation forecasts during the pandemic.

Figure 4 depicts the differences in LPLs for the period 2020:01 to 2020:08. For illustrative purposes, we only consider the models with 30 factors.999The findings for the other factors are very similar and available from the corresponding author upon request.

The figure provides a few interesting insights. First, we observe that in March 2020, models based on the Autoencoder improve upon the benchmark, irrespective of the prior and regression specification adopted. This finding is less pronounced for the other techniques in the constant parameter case. Comparing the performance of the constant parameter and the TVP regression models reveals that, irrespective of the prior, allowing for time variation in the parameters improves density forecasts during the pandemic. This finding is consistent with findings in, e.g., Huber et al. (2020), who show that flexible models improve upon linear models during the pandemic due to increases in the predictive variance.

q = 30

const. (HS)

const. (MIN)

TVP (HS)

TVP (MIN)

Note: The initial value in 2020:01 also takes into account the density forecast performance in the previous hold-out periods (ranging from 2002:01 to 2019:12). The red dashed lines refer to the maximum/minimum Bayes factor over the full hold-out sample. The light gray shaded areas indicate the periods of the COVID-19 pandemic.

4.6 Dynamic model learning based on density forecast performance

In the previous sub-section and Section A of the Online Appendix we provide some evidence that model performance varies considerably over time (see Figure A.3). The key implication is that non-linear compression techniques (and time-varying parameters) might be useful during turbulent times whereas forecast evidence is less pronounced in normal times. In this sub-section, we ask whether combining models in a dynamic manner further improves predictive accuracy.

After having obtained the predictive densities of for the different dimension reduction techniques and model specifications, the goal is to exploit the advantages of both linear and non-linear approaches. This is achieved by combining models in a model pool such that better performing models over certain periods receive larger weights while inferior models are subsequently down-weighted. The literature on forecast combinations suggests several different weighting schemes, ranging from simply averaging over all models (see, e.g., Hendry and Clements, 2004; Hall and Mitchell, 2007; Clark and McCracken, 2010; Berg and Henzel, 2015) to estimating weights based on the models’ performances according to the minimization of an objective or loss function (see, e.g., Timmermann, 2006; Hall and Mitchell, 2007; Geweke and Amisano, 2011; Conflitti et al., 2015; Pettenuzzo and Ravazzolo, 2016) or according to the posterior probabilities of the predictive densities (see, e.g., Raftery et al., 2010; Koop and Korobilis, 2012; Beckmann et al., 2020). More recent approaches set up separate state space models which assume sophisticated law of motions for the weights associated with each predictive distribution (Billio et al., 2013; Pettenuzzo and Ravazzolo, 2016; McAlinn and West, 2019). These approaches, while being elegant and having the advantage of incorporating all available sources of uncertainty (i.e., also control for estimation uncertainty in the weights), are computationally cumbersome if the number of models to be combined is large.