Detecting and Adapting to Irregular Distribution Shifts in Bayesian Online Learning

Abstract

We consider the problem of online learning in the presence of distribution shifts that occur at an unknown rate and of unknown intensity. We derive a new Bayesian online inference approach to simultaneously infer these distribution shifts and adapt the model to the detected changes by integrating ideas from change point detection, switching dynamical systems, and Bayesian online learning. Using a binary ‘change variable,’ we construct an informative prior such that–if a change is detected–the model partially erases the information of past model updates by tempering to facilitate adaptation to the new data distribution. Furthermore, the approach uses beam search to track multiple change-point hypotheses and selects the most probable one in hindsight. Our proposed method is model-agnostic, applicable in both supervised and unsupervised learning settings, suitable for an environment of concept drifts or covariate drifts, and yields improvements over state-of-the-art Bayesian online learning approaches.

1 Introduction

Deployed machine learning systems are often faced with the problem of distribution shift, where the new data that the model processes is systematically different from the data the system was trained on [Zech et al., 2018, Ovadia et al., 2019]. Furthermore, a shift can happen anytime after deployment, unbeknownst to the users, with dramatic consequences for systems such as self-driving cars, robots, and financial trading algorithms, among many other examples.

Updating a deployed model on new, representative data can help mitigate these issues and improve general performance in most cases. This task is commonly referred to as online or incremental learning. Such online learning algorithms face a tradeoff between remembering and adapting. If they adapt too fast, their performance will suffer since adaptation usually implies that the model loses memory of previously encountered training data (which may still be relevant to future predictions). On the other hand, if a model remembers too much, it typically has problems adapting to new data distributions due to its finite capacity.

The tradeoff between adapting and remembering can be elegantly formalized in a Bayesian online learning framework, where a prior distribution is used to keep track of previously learned parameter estimates and their confidences. For instance, variational continual learning (VCL) [Nguyen et al., 2018] is a popular framework that uses a model’s previous posterior distribution as the prior for new data. However, the assumption of such continual learning setups is usually that the data distribution is stationary and not subject to change, in which case adaptation is not an issue.

This paper proposes a new Bayesian online learning framework suitable for non-stationary data distributions. It is based on two assumptions: (i) distribution shifts occur irregularly and must be inferred from the data, and (ii) the model requires not only a good mechanism to aggregate data but also the ability to partially forget information that has become obsolete. To solve both problems, we still use a Bayesian framework for online learning (i.e., letting a previous posterior distribution inform the next prior); however, before combining the previously learned posterior with new data evidence, we introduce an intermediate step. This step allows the model to either broaden the previous posterior’s variance to reduce the model’s confidence, thus providing more “room” for new information, or remain in the same state (i.e., retain the unchanged, last posterior as the new prior).

We propose a mechanism for enabling this decision by introducing a discrete “change variable” that indicates the model’s best estimate of whether the data in the new batch is compatible with the previous data distribution or not; the outcome then informs the Bayesian prior at the next time step. We further augment the scheme by performing beam search on the change variable. This way, we are integrating change detection and Bayesian online learning into a common framework.

We test our framework on a variety of real-world datasets that show concept drift, including basketball player trajectories, malware characteristics, sensor data, and electricity prices. We also study sequential versions of SVHN and CIFAR-10 with covariate drift, where we simulate the shifts in terms of image rotations. Finally, we study word embedding dynamics in an unsupervised learning approach. Our approach leads to a more compact and interpretable latent structure and significantly improved performance in the supervised experiments. Furthermore, it is highly scalable; we demonstrate it on models with hundreds of thousands of parameters and tens of thousands of feature dimensions.

2 Related Work

Our paper connects to Bayesian online learning, change detection, and switching dynamical systems.

Bayesian Online and Continual Learning

There is a rich existing literature on Bayesian and continual learning. The main challenge in streaming setups is to reduce the impact of old data on the model which can be done by exponentially decaying old samples [Honkela and Valpola, 2003, Sato, 2001, Graepel et al., 2010] or re-weighting them [McInerney et al., 2015, Theis and Hoffman, 2015]. An alternative approach is to adapt the model posterior between time steps, such as tempering it at a constant rate to accommodate new information [Kulhavỳ and Zarrop, 1993, Kurle et al., 2020]. In contrast, continual learning typically assumes a stationary data distribution and simply uses the old posterior as the new prior. A scalable such scheme based on variational inference was proposed by [Nguyen et al., 2018] which was extended by several authors [Farquhar and Gal, 2018, Schwarz et al., 2018]. A related concept is elastic weight consolidation [Kirkpatrick et al., 2017], where new model parameters are regularized towards old parameter values.

All of these approaches need to make assumptions on the expected frequency and strengh of change which are hard-coded in the model parameters (e.g., exponential decay rates, re-weighting terms, prior strengths, or temperature choices). Our approach, in contrast, detects change based on a discrete variable and makes no assumption about its frequency. Other approaches assume situations where data arrive in irregular time intervals, but are still concerned with static data distributions [Titsias et al., 2019, Lee et al., 2020, Rao et al., 2019].

Change Point Models

There is also a rich history of models for change detection. A popular class of change point models includes “product partition models” [Barry and Hartigan, 1992] which assume independence of the data distribution across segments. In this regime, Fearnhead [2005] proposed change detection in the context of regression and generalized it to online inference [Fearnhead and Liu, 2007]; Adams and MacKay [2007] described a Bayesian online change point detection scheme (BOCD) based on conditional conjugacy assumptions for one-dimensional sequences. Other work generalized change detection algorithms to multivariate time series [Xuan and Murphy, 2007, Xie et al., 2012] and non-conjugate Bayesian inference [Saatçi et al., 2010, Knoblauch and Damoulas, 2018, Turner et al., 2013, Knoblauch et al., 2018].

Our approach relies on jointly inferring changes in the data distribution while carrying out Bayesian parameter updates for adaptation. To this end, we detect change in the high-dimensional space of model (e.g., neural network) parameters, as opposed to directly in the data space. Furthermore, a detected change only partially resets the model parameters, as opposed to triggering a complete reset.

Titsias et al. [2020] proposed change detection to detect distribution shifts in sequences based on low-dimensional summary statistics such as a loss function; however, the proposed framework does not use an informative prior but requires complete retraining.

Switching Linear Dynamical Systems

Since our approach integrates a discrete change variable, it is also loosely connected to the topic of switching linear dynamical systems. Linderman et al. [2017] considered recurrent switching linear dynamical systems, relying on Bayesian conjugacy and closed-form message passing updates. Becker-Ehmck et al. [2019] proposed a variational Bayes filtering framework for switching linear dynamical systems. Murphy [2012] and Barber [2012] developed an inference method using a Gaussian sum filter. Instead, we focus on inferring the full history of discrete latent variable values instead of just the most recent one.

Bracegirdle and Barber [2011] introduce a reset variable that sets the continuous latent variable to an unconditional prior. It is similar to our work, but relies on using low-dimensional, tractable models. Our tempering prior can be seen as a partial reset, augmented with beam search. We also extend the scope of switching dynamical systems by integrating them into a supervised learning framework.

3 Methods

Overview

3.1 Problem Assumptions and Structure

We consider a stream of data that arrives in batches at discrete times .111In an extreme case, it is possible for a batch to include only a single data point. For supervised setups, we consider pairs of features and targets , where the task is to model . An example model could be a Bayesian neural network, and the parameters could be the network weights. For notational simplicity we focus on the unsupervised case, where the task is to model using a model with parameters that we would like to tune to each new batch.222 In supervised setups, we consider a conditional model with features and targets . We then measure the prediction error either on one-step-ahead samples or using a held-out test set.

Furthermore, we assume that while the are i.i.d. within batches, they are not necessarily i.i.d. across batches as they come from a time-varying distribution (or in the supervised cases) which is subject to distribution shifts. We do not assume whether these distribution shifts occur instantaneously or gradually. The challenge is to optimally adapt the parameters to each new batch while borrowing statistical strength from previous batches.

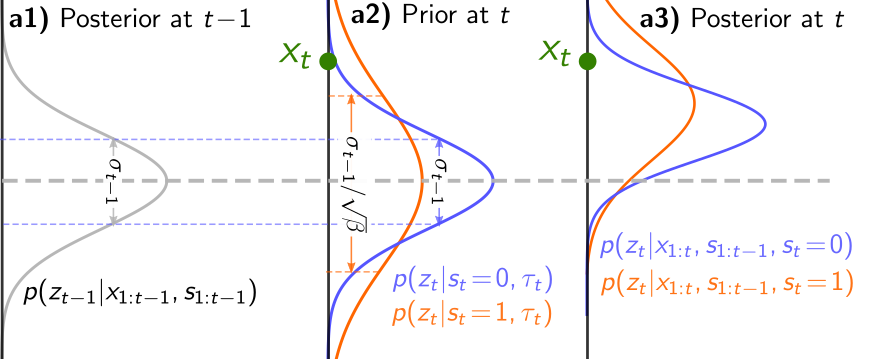

As follows, we will construct a Bayesian online learning scheme that accounts for changes in the data distribution. For every new batch of data, our scheme tests whether the new batch is compatible with the old data distribution, or more plausible under the assumption of a change. To this end, we employ a binary “change variable” , with for no detected change and for a detected change. Our model’s joint distribution factorizes as follows:

| (1) |

We assumed a factorized Bernoulli prior over the change variable: an assumption that will simplify the inference, but which can be relaxed. As a result, our model is fully-factorized over time, however, the model can still capture temporal dependencies through the informative prior . Temporal information enters this prior through certain sufficient statistics that depend on properties of the previous time-step’s approximate posterior.

In more detail, is a functional on the previous time step’s approximate posterior, .333 Subscripts indicates the integers from to inclusively. Throughout this paper, we will use a specific form of , namely capturing the previous posterior’s mean and variance.444 In later sections, we will use a Gaussian approximation to the posterior, but here it is enough to assume that these quantities are computable. More formally,

| (2) |

Based on this choice, we define the conditional prior as follows:

| (3) |

Above, is a hyperparameter referred to as inverse temperature555 In general it only requires to be inverse temperature. We further assume in this paper as this value interval broadens and weakens the previous posterior. See the following paragraphs. . If no change is detected (i.e., ), our prior becomes a Gaussian distribution centered around the previous posterior’s mean and variance. In particular, if the previous posterior was already Gaussian, it becomes the new prior. In contrast, if a change was detected, the broadened posterior becomes the new prior.

For as long as no changes are detected (), the procedure results in a simple Bayesian online learning procedure, where the posterior uncertainty shrinks with every new observation. In contrast, if a change is detected (), an overconfident prior would be harmful for learning as the model needs to adapt to the new data distribution. We therefore weaken the prior through tempering. Given a temperature , we raise the previous posterior’s Gaussian approximation to the power , renormalize it, and then use it as a prior for the current time step.

The process of tempering the Gaussian posterior approximation can be understood as removing equal amounts of information in any direction in the latent space. To see this, let be a multivariate Gaussian with covariance and be a unit direction vector. Then tempering removes an equal amount of information regardless of , , erasing learned information to free-up model capacity to adjust to the new data distribution. See Supplement B for more details.

Connection to Sequence Modeling

Our model assumptions have a resemblance to time series modeling: if we replaced with , we would condition on previous latent states rather than posterior summary statistics. In contrast, our model still factorizes over time and therefore makes weaker assumptions on temporal continuity. Rather than imposing temporal continuity on a data instance level, we instead assume temporal continuity at a distribution level.

Connection to Changepoint Modeling.

We also share similar assumptions with the changepoint literature [Barry and Hartigan, 1992]. However, in most cases, these models don’t assume an informative prior, effectively not taking into account any sufficient statistics . This forces these models to re-learn model parameters from scratch after a detected change, whereas our approach allows for some transfer of information before and after the distribution shift.

3.2 Exact Inference

Before presenting a scalable variational inference scheme in our model, we describe an exact inference scheme when everything is tractable, i.e., the special case of linear Gaussian models.

According to our assumptions, the distribution shifts occur at discrete times and are unobserved. Therefore, we have to infer them from the observed data and adapt the model accordingly. Recall the distribution shift is represented by the binary latent variable at time step . Inferring the posterior over at will thus notify us how likely the change happens under the model assumption. As follows, we show the posterior of is simple in a tractable model and bears similarity with a likelihood ratio test. Suppose we moved from time step to step and observed new data . Denote the history decisions and observations by , which enters through . Then by Bayes rule, the exact posterior over is again a Bernoulli, , with parameter

| (4) |

Above, is the sigmoid function, and are the log-odds of the prior and serves as a bias term. is the model evidence. Overall, specifies the probability of given and .

Eq. 4 has a simple interpretation as a likelihood ratio test: a change is more or less likely depending on whether or not the observations are better explained under the assumption of a detected change.

We have described the detection procedure thus far, now we turn to the adaptation procedure. To adjust the model parameters to the new data given a change or not, we combine the likelihood of with the conditional prior (Eq. 3). This corresponds to the posterior of , , obtained by Bayes rule. The adaptation procedure is illustrated in Fig. 1 (a), where we show how a new observation modifies the conditional prior of model parameters.

As a result of Eq. 4, we obtain the marginal distribution of at time as a binary mixture with mixture weights and : .

Exponential Branching

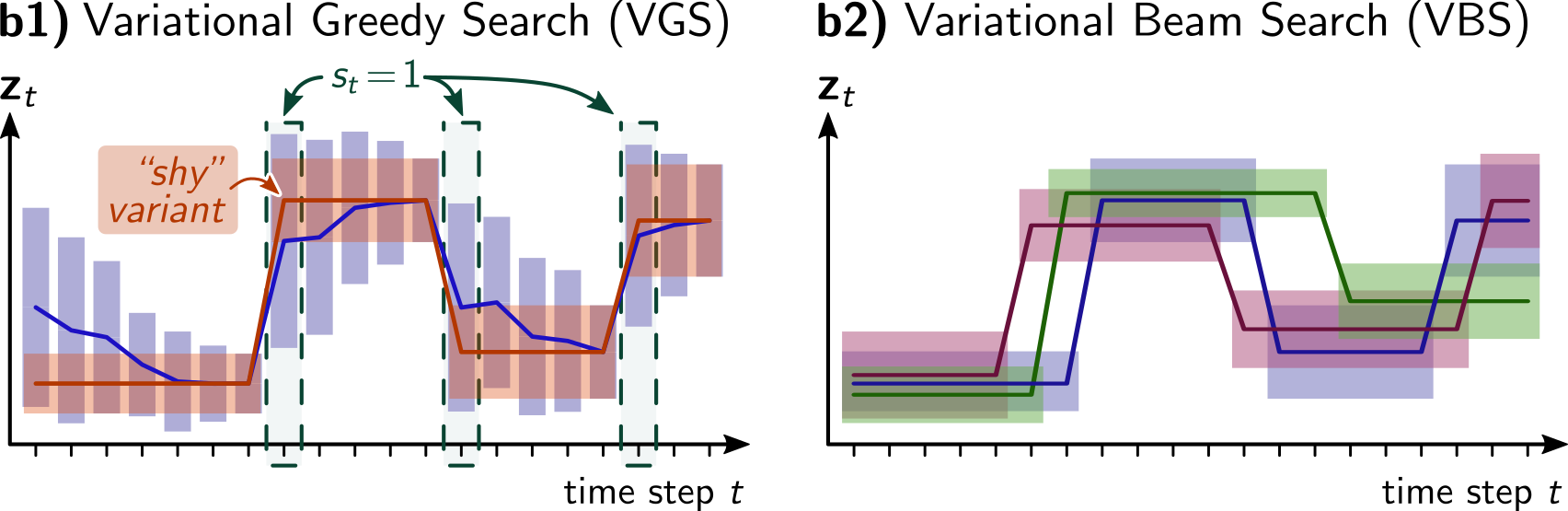

We note that while we had originally started with a posterior at the previous time, our inference scheme resulted in being a mixture of two components as it branches over two possible states.666 See also Fig. 4 in Supplement C. When we iterate, we encounter an exponential branching of possibilities, or hypotheses over possible sequences of regime shifts . To still carry out the filtering scheme efficiently, we need a truncation scheme, e.g., approximate the bimodal marginal distribution by a unimodal one. As follows, we will discuss two methods—greedy search and beam search—to achieve this goal.

Greedy Search

In the simplest “greedy” setup, we train the model in an online fashion by iterating over time steps . For each , we update a truncated distribution via the following three steps:

-

1.

Compute the conditional prior (Eq. 3) based on and evaluate the likelihood upon observing data .

-

2.

Infer whether a change happens or not using the posterior over (Eq. 4) and adapt the model parameters for each case.

-

3.

Select that has larger posterior probability and its corresponding model hypothesis (i.e., make a “hard” decision over with a threshold of ).

The above filtering algorithm iteratively updates the posterior distribution over each time it observes new data . In the version of greedy search discussed above, the approach decides immediately, i.e., before observing subsequent data points, whether a change in has occurred or not in step 3. (Please note the decision is irrelevant to history, as opposed to the beam search described below.) We illustrate greedy search is illustrated in Fig. 1 (b1) where VGS is the variational inference counterpart.

Beam Search

A greedy search is prone to missing change points in data sets with a low signal/noise ratio per time step because it cannot accumulate evidence for a change point over a series of time steps. The most obvious improvement over greedy search that has the ability to accumulate evidence for a change point is beam search. Rather than deciding greedily whether a change occurred or not at each time step, beam search considers both cases in parallel as it delays the decision of which one is more likely (see Fig. 1 (b2) and Fig. 2 (left) for illustration). The algorithm keeps track of a fixed number of possible hypotheses of change points. For each hypothesis, it iteratively updates the posterior distribution as a greedy search. At time step , every potential continuation of the sequences is considered with , thus doubling the number of histories of which the algorithm has to track. To keep the computational requirements bounded, beam search thus discards half of the sequences based on an exploration-exploitation trade-off.

Beam search simultaneously tracks multiple hypotheses necessitating the differentiation between them. In greedy search, we can distinguish hypotheses based on the most recent ’s value since only two hypotheses are considered at each step. However, beam search considers at most hypotheses each step, which exceeds the capacity of a single . We thus resort to the decision history to further tell hypotheses apart. The weight of each hypothesis can be computed recursively:

| (5) |

where the added information at step is the posterior of (Eq. 4). This suggests the “correction in hindsight” nature of beam search: re-ranking the sequence as a whole at time indicates the ability to correct decisions before time .

Another ingredient is a set , which contains the most probable “histories” at time . From time to , we evaluate the continuation of each hypothesis as the first two steps of greedy search, leading to hypotheses. We then compute the weight of each hypothesis using Eq. 5. Finally, select top hypotheses into and re-normalize the weights of hypotheses in .

This concludes the recursion from time to . With and , we can achieve any marginal distribution of , such as .

Beam Search Diversification

Empirically, we find that the naive beam search procedure does not realize its full potential. As commonly encountered in beam search, histories over change points are largely shared among all members of the beam. To encourage diverse beams, we constructed the following simple scheme. While transitioning from time to , every hypothesis splits into two scenarios, one with and one with , resulting in temporary hypotheses. If two resulting hypotheses only differ in their most recent -value, we say that they come from the same “family.” Each member among the hypotheses is ranked according to its posterior probability in Eq. 5. In a first step, we discard the bottom of the hypotheses, leaving hypotheses (we always take integer multiples of for ). To truncate the beam size from down to , we rank the remaining hypotheses according to their posterior probability and pick the top ones while also ensuring that we pick a member from every remaining family. The diversification scheme ensures that underperforming families can survive, leading to a more diverse set of hypotheses. We found this beam diversification scheme to work robustly across a variety of experiments.

3.3 Variational Inference

In most practical applications, the evidence term is not available in closed-form, leaving Eq. 4 intractable to evaluate. However, we can follow a structured variational inference approach [Wainwright and Jordan, 2008, Hoffman and Blei, 2015, Zhang et al., 2018], defining a joint variational distribution , to approximate . This procedure completes the detection and adaptation altogether.

One may wonder how the exact inference schemes for and are modified in the structured variational inference scenario. In Supplement A, we derive the solution for . Surprisingly we have the following closed-form update equation for that bears strong similarities to Eq. 4. The new scheme simply replaces the intractable evidence term with a lower bound proxy – optimized conditional evidence lower bound (CELBO, defined later), giving the update

| (6) |

Above, we introduced a parameter (not to be confused with ) to optionally downweigh the data evidence relative to the prior (see Experiments Section 4).

Now we define the CELBO. To approximate by variational distribution , we minimize the KL divergence between and , leading to

| (7) | ||||

denotes the variational family (i.e., factorized normal distributions), and we term CELBO.

The greedy search and beam search schemes also apply to variational inference. We name them variational greedy search (VGS, VBS (K=1)) and variational beam search (VBS) (Fig. 1 (b)).

Algorithm Complexity

VBS’s computational time and space complexity scale linearly with the beam size . As such, its computational cost is only about times larger than greedy search777This also applies to the baselines “Bayesian Forgetting” (BF) and Variational Continual Learning” (VCL) introduced in Section 4.2.. Furthermore, our algorithm’s complexity is in the sequence length . It is not necessary to store sequences as they are just symbols to distinguish hypotheses. The only exception to this scaling would be an application asking for the most likely changepoint sequence in hindsight. In this case, the changepoint sequence (but not the associated model parameters) would need to be stored, incurring a cost of storing exactly binary variables. This storage is, however, not necessary when the focus is only on adapting to distribution shifts.

4 Experiments

Overview

The objective of our experiments is to show that, compared to other methods, variational beam search (1) better reacts to different distribution shifts, e.g., concept drifts and covariate drifts, while (2) revealing interpretable and temporally sparse latent structure. We experiment on artificial data to demonstrate the “correct in hindsight” nature of VBS (Section 4.1), evaluate online linear regression on three datasets with concept shifts (Section 4.3), visualize the detected change points on basketball player movements, demonstrate the robustness of the hyperparameter (Section 4.3), study Bayesian deep learning approaches on sequences of transformed images with covariate shifts (Section 4.4), and study the dynamics of word embeddings on historical text corpora (Section 4.5). Unstated experimental details are in Supplement G.

4.1 An Illustrative Example

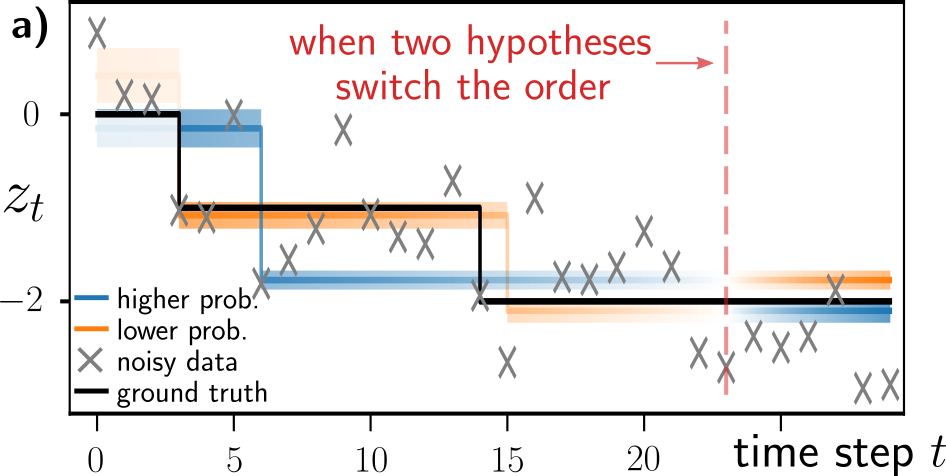

We first aim to dynamically demonstrate the “correction in hindsight” nature of VBS based on a simple setup involving artificial data. To this end, we formulated a problem of tracking the shifting mean of data samples. This shifting mean is a piecewise-constant step function involving two steps (seen as in black in Fig. 2 (a)), and we simulated noisy data points centered around the mean. We then used VBS with beam size to fit the same latent mean model that generated the data. The color indicates the ranking among both hypotheses at each moment in time (blue as “more likely” vs. orange as “less likely”). While hypothesis 1 assumes a single distribution shift (initially blue), hypothesis 2 (initially orange) assumes two shifts. We see that hypothesis 1 is initially more likely, but gets over-ruled by the better hypothesis 2 later (note the color swap at step 23).

4.2 Baselines

In our supervised experiments (Section 4.3 and Section 4.4), we compared VBS against adaptive methods, Bayesian online learning baselines, and independent batch learning baselines.888 As a reminder, a “batch” at discrete time is the dataset available for learning; on the other hand, a “mini-batch” is a small set of data used for computing gradients for stochastic gradient-based optimization. Among the adaptive methods, we formulated a supervised learning version of Bayesian online changepoint detection (BOCD) [Adams and MacKay, 2007].999 1) Although BOCD is mostly applied for unsupervised learning, its application in supervised learning and its underlying model’s adaptation to change points are seldom investigated. 2) When the model is non-conjugate, such as Bayesian neural networks, we approximate the log evidence by the evidence lower bound. We also implemented Bayesian forgetting (BF) [Kurle et al., 2020] with convolutional neural networks for proper comparisons. Bayesian online learning baselines include variational continual learning (VCL) [Nguyen et al., 2018] and Laplace propagation (LP) [Smola et al., 2003, Nguyen et al., 2018]. Finally, we also adopt a trivial baseline of learning independent regressors/classifiers on each batch in both a Bayesian and non-Bayesian fashion. For VBS and BOCD we always report the most dominant hypothesis. In unsupervised learning experiments, we compared against the online version of word2vec [Mikolov et al., 2013] with a diffusion prior, dynamic word embeddings [Bamler and Mandt, 2017].

4.3 Bayesian Linear Regression Experiments

As a simple first version of VBS, we tested an online linear regression setup for which the posterior can be computed analytically. The analytical solution removes the approximation error of the variational inference procedure as well as optimization-related artifacts since closed-form updates are available. Detailed derivations are in Supplement D.

Real Datasets with Concept Shifts.

We investigated three real-world datasets with concept shifts:

-

•

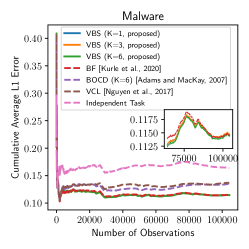

Malware This dataset is a collection of 100K malignous and benign computer programs, collected over 44 months [Huynh et al., 2017]. Each program has 482 counting features and a real-valued probability of being malware. We linearly predicted the log-odds.

-

•

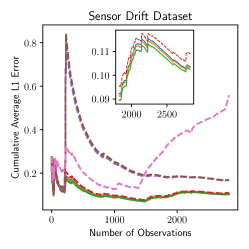

SensorDrift A collection of chemical sensor readings [Vergara et al., 2012]. We predicted the concentration level of gas acetaldehyde, whose 2,926 samples and 128 features span 36 months.

-

•

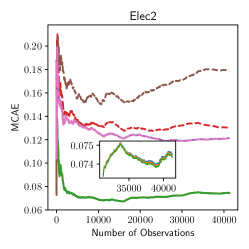

Elec2 The dataset contains the electricity price over three years of two Australian states [Harries and Wales, 1999]. While the original problem formulation used a majority vote to generate 0-1 binary labels on whether the price increases or not, we averaged the votes out into real-valued probabilities and predicted the log-odds instead. We had 45,263 samples and 14 features.

At each step, only one data sample is revealed to the regressor. We evaluated all methods with one-step-ahead absolute error101010We measured the error in the probability space for classification problems (Malware and Elec2) and the error in the data space for regression problems (SensorDrift). and computed the mean cumulative absolute error (MCAE) at every step. In Table 1, we didn’t report the variance of MCAEs since there is no stochastic optimization noise. Table 1 shows that VBS has the best average of MCAEs among all methods. We also reported the running performance in Supplement G.2, where other experimental details are available as well.

| Models | CIFAR-10 | SVHN | Malware | SensorDrift | Elec2 | NBAPlayer |

|---|---|---|---|---|---|---|

| (Accuracy) | (MCAE ) | (LogLike ) | ||||

| VBS (K=6)∗ | 69.20.9 | 89.60.5 | 11.61 | 10.53 | 7.28 | 29.493.12 |

| VBS (K=3)∗ | 68.90.9 | 89.10.5 | 11.65 | 10.71 | 7.28 | 29.222.63 |

| VBS (K=1)∗ | 68.20.8 | 88.90.5 | 11.65 | 10.86 | 7.27 | 29.252.59 |

| BOCD (K=6)♯ | 65.60.8 | 88.20.5 | 12.93 | 24.34 | 12.49 | 22.967.42 |

| BOCD (K=3)♯ | 67.30.8 | 88.80.5 | 12.74 | 24.31 | 12.49 | 20.937.83 |

| BF¶ | 69.80.8 | 89.90.5 | 11.71 | 11.40 | 13.37 | 24.172.29 |

| VCL† | 66.70.8 | 88.70.5 | 13.27 | 24.90 | 16.59 | 3.4825.53 |

| LP‡ | 62.61.0 | 82.80.9 | 13.27 | 24.90 | 16.59 | 3.4825.53 |

| IB§ | 63.70.5 | 85.50.7 | 16.6 | 27.71 | 12.48 | -44.8716.88 |

| IB§ (Bayes) | 64.50.3 | 87.80.1 | 16.6 | 27.71 | 12.48 | -44.8716.88 |

| ∗ proposed, ♯ [Adams and MacKay, 2007], ¶ [Kurle et al., 2020] | ||||||

| † [Nguyen et al., 2018], ‡ [Smola et al., 2003], § Independent Batch | ||||||

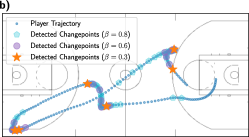

Basketball Player Tracking.

We explored a collection of basketball player movement trajectories.111111 https://github.com/linouk23/NBA-Player-Movements Each trajectory has wide variations in player velocities. We treated the trajectories as time series and used a Bayesian transition matrix to predict the next position based on the current position . This matrix is learned and adapted on the fly for each trajectory.

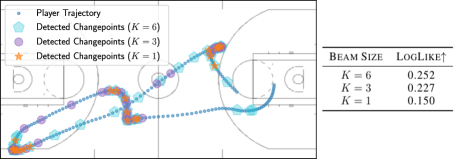

We first investigated the effect of the temperature parameter in our approach. To this end, we visualized the detected change points on an example trajectory. We used VBS (K=1, greedy search) and compared different values of in Fig. 2 (b). The figure shows that the larger , the more change points are detected; the smaller , the detected change points get sparser, i.e., determines the model’s sensitivity to changes. This observation confirms the assumption that controls the assumed strength of distribution shifts.

In addition, the result also implies the robustness of poorly selected s. When facing an abrupt change in the trajectory, the regressor has two adapt options based on different s – make a single strong adaptation or make a sequence of weak adaptations – in either case, the model ends up adapting itself to the new trajectory. In other words, people can choose different for a specific environment, with a trade-off between adaptation speed and the erased amount of information.

4.4 Bayesian Deep Learning Experiments

Our larger-scale experiments involve Bayesian convolutional neural networks trained on sequential batches for image classification using CIFAR-10 [Krizhevsky et al., 2009] and SVHN [Netzer et al., 2011]. Every few batches, we manually introduce covariate shifts through transforming all images globally by combining rotations, shifts, and scalings. Each transformation is generated from a fixed, predefined distribution (see Supplement G.3). The experiment involved 100 batches in sequence, where each batch contained a third of the transformed datasets. We set the temperature and set the CELBO temperature (in Eq. 6) for all supervised experiments.

Table 1 shows the performances of all considered methods and both data sets, averaged across all of the 100 batches. Within their confidence bounds, VBS and BF have comparable performances and outperform the other baselines. We conjecture that the strong performance of BF can be attributed to the fact that our imposed changes are still relatively evenly spaced and regular. The benefit of beam search in VBS is evident, with larger beam sizes consistently performing better.

4.5 Unsupervised Experiments

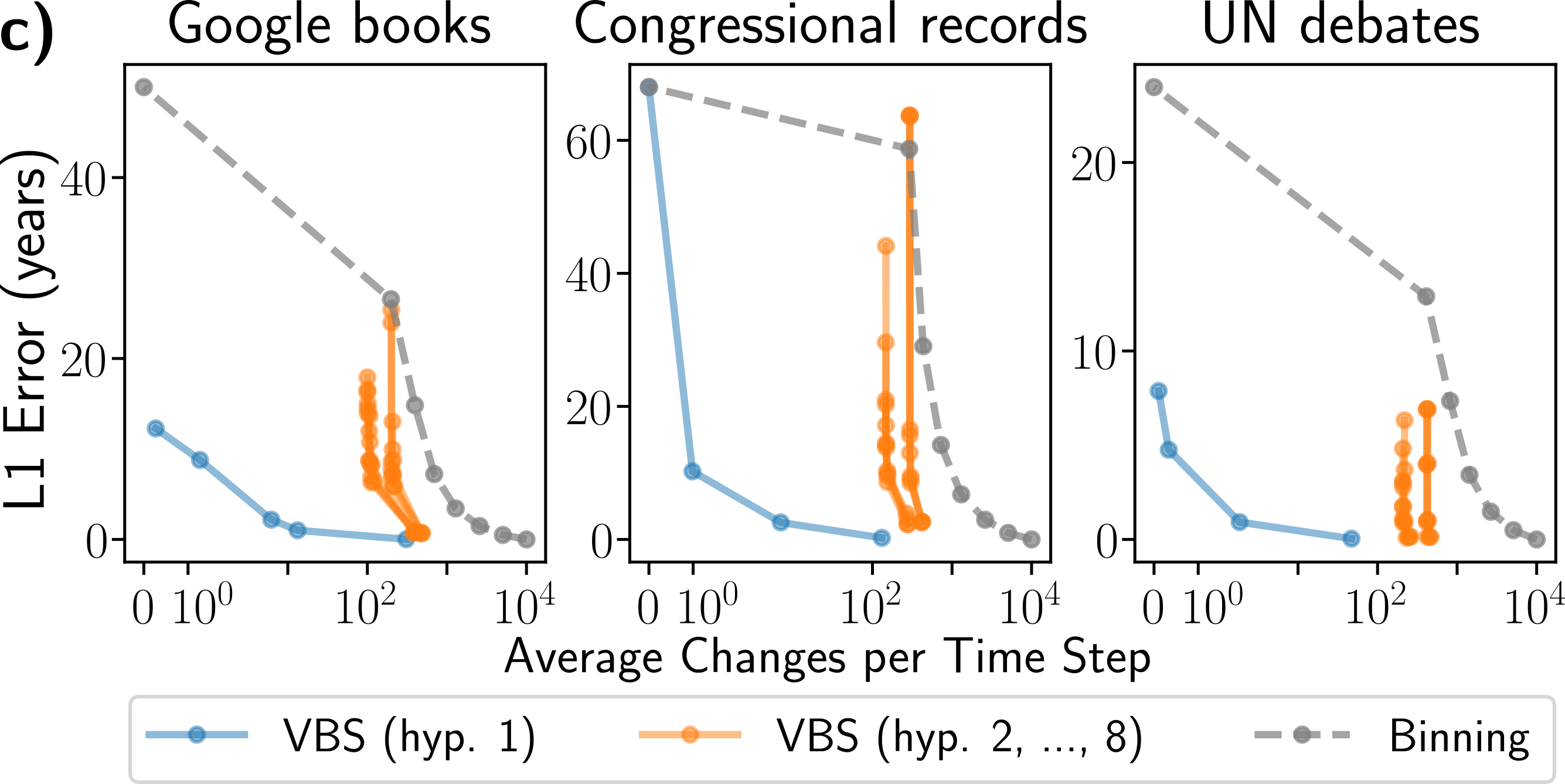

Our final experiment focused on unsupervised learning. We intended to demonstrate that VBS helps uncover interpretable latent structure in high-dimensional time series by detecting change points. We also showed that the detected change points help reduce the storage size and maintain salient features.

Towards this end, we analyzed the semantic changes of individual words over time in an unsupervised setup. We used Dynamic Word Embeddings (DWE) [Bamler and Mandt, 2017] as our base model. The model is an online version of Word2Vec [Mikolov et al., 2013]. Word2Vec projects a vocabulary into an embedding space and measures word similarities by cosine distance in that space. DWE further imposes a time-series prior on the embeddings and tracks them over time. For our proposed approach, we augmented DWE with VBS, allowing us to detect the changes of words meaning.

We analyzed three large time-stamped text corpora, all of which are available online. Our first dataset is the Google Books corpus [Michel et al., 2011] in -grams form. We focused on 1900 to 2000 with sub-sampled 250M to 300M tokens per year. Second, we used the Congressional Records dataset [Gentzkow et al., 2018], which has 13M to 52M tokens per two-year period from 1875 to 2011. Third, we used the UN General Debates corpus [Jankin Mikhaylov et al., 2017], which has about 250k to 450k tokens per year from 1970 to 2018.

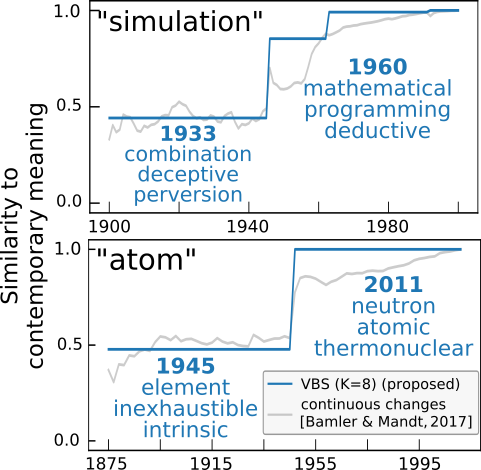

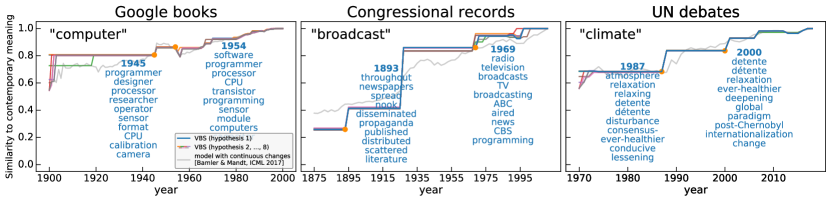

Our first experiments demonstrate VBS provides more interpretable step-wise word meaning shifts than the continuous shifts (DWE). Due to page limits, in Fig. 3 we selected two example words and their three nearest neighbors in the embedding space at different years. The evolving nearest neighbors reflect a semantic change of the words. We plotted the most likely hypothesis of VBS in blue and the continuous-path baseline (DWE) in grey. While people can roughly tell the change points from the continuous path, the changes are surrounded by noisy perturbations and sometimes submerged within the noise. VBS, on the other hand, makes clear decisions and outputs explicit change points. As a result, VBS discovers that the word “atom” changes its meaning from “element” to “nuclear” in 1945–the year when two nuclear bombs were detonated; word “simulation” changes its dominant context from “deception” to “programming” with the advent of computers in the 1950s. Besides interpretable changes points, VBS provides multiple plausible hypotheses (Supplement G.4).

Our second experiments exemplify the usefulness of the detected sparse change points, which lead to sparse segments of embeddings. The usefulness comes in two folds: 1) while alleviating the burden of the disk storage by storing one value for each segment, 2) the sparsity preserves the salient features of the original model. To illustrate these two aspects, we design a document dating task that exploits the probabilistic interpretation of word embeddings. The idea is to assign a test document to the year whose embeddings provide the highest likelihood. In Figure 2 (c), we measure the model sparsity on the x-axis with the average updated embeddings per step (The maximum is 10000, which is the vocabulary size). The feature preservation ability is measured by document dating accuracy on the y-axis. We adjust the prior log-odds (Eq. 6) to have successive models with different change point sparsity and then measure the dating accuracy. We also designed an oracle baseline named “binning” (grey, Supplement G.4). For VBS, we show the dominant hypothesis (blue) as well as the subleading hypotheses (orange). The most likely hypothesis of VBS outperforms the baseline, leading to higher document dating precision at much smaller disk storage.

5 Discussion

Beyond Gaussian Posterior Approximations.

While the Gaussian approximation is simple and is widely used (and broadly effective) in practice in Bayesian inference [e.g., Murphy [2012], pp.649-662], our formulation does not rule out the extensions to exponential families. in Eq. 2 could be generalized by reading off sufficient statistics of the previous approximate posterior. To this end, we need a sufficient statistic that is associated with some measure of entropy or variance that we broaden after each detected change. For example, the Gamma distribution can broaden its scale, and for the categorical distribution, we can increase its entropy/temperature. More intricate (e.g. multimodal) possible alternatives for posterior approximation are also possible, for example, Gaussian mixtures.

6 Conclusions

We introduced variational beam search: an approximate inference algorithm for Bayesian online learning on non-stationary data with irregular changes. Our approach mediates the tradeoff between a model’s ability to memorize past data while still being able to adapt to change. It is based on a Bayesian treatment of a given model’s parameters and aimed at tuning them towards the most recent data batch while exploiting prior knowledge from previous batches. To this end, we introduced a sequence of a discrete change variables whose value controlled the way we regularized the model. For no detected change, we regularized the new learning task towards the previously learned solution; for a detected change, we broadened the prior to give room for new data evidence. This procedure is combined with beam search over the discrete change variables. In different experiments, we showed that our proposed model (1) achieved lower error in supervised setups, and (2) revealed a more interpretable and compressible latent structure in unsupervised experiments.

Broader Impacts.

As with many machine learning algorithms, there is a danger that more automation could potentially result in unemployment. Yet, more autonomous adaptation to changes will enhance the safety and robustness of deployed machine learning systems, such as self-driving cars.

Acknowledgements

We gratefully acknowledge extensive contributions from Robert Bamler (previously UCI, now at the University of Tübingen), which were indispensable to this work.

This material is based upon work supported by the National Science Foundation under the CAREER award 2047418 and grant numbers 1633631, 1928718, 2003237, and 2007719; by the National Science Foundation Graduate Research Fellowship under grant number DGE-1839285; by the Defense Advanced Research Projects Agency (DARPA) under Contract No. HR001120C0021; by an Intel grant; and by grants from Qualcomm. Any opinion, findings, and conclusions or recommendations expressed in this material are those of the authors and do not necessarily reflect the views of the National Science Foundation, nor do they reflect the views of DARPA. Additional revenues potentially related to this work include: research funding from NSF, NIH, NIST, PCORI, and SAP; fellowship funding from HPI; consulting income from Amazon.com.

References

- Zech et al. [2018] John R Zech, Marcus A Badgeley, Manway Liu, Anthony B Costa, Joseph J Titano, and Eric Karl Oermann. Variable generalization performance of a deep learning model to detect pneumonia in chest radiographs: A cross-sectional study. PLoS medicine, 15(11):e1002683, 2018.

- Ovadia et al. [2019] Yaniv Ovadia, Emily Fertig, Jie Ren, Zachary Nado, David Sculley, Sebastian Nowozin, Joshua V Dillon, Balaji Lakshminarayanan, and Jasper Snoek. Can you trust your model’s uncertainty? evaluating predictive uncertainty under dataset shift. In Advances in Neural Information Processing Systems, 2019.

- Nguyen et al. [2018] Cuong V Nguyen, Yingzhen Li, Thang D Bui, and Richard E Turner. Variational continual learning. In International Conference on Learning Representations, 2018.

- Honkela and Valpola [2003] Antti Honkela and Harri Valpola. On-line variational bayesian learning. In 4th International Symposium on Independent Component Analysis and Blind Signal Separation, 2003.

- Sato [2001] Masa-Aki Sato. Online model selection based on the variational bayes. Neural computation, 13(7):1649–1681, 2001.

- Graepel et al. [2010] Thore Graepel, Joaquin Quinonero Candela, Thomas Borchert, and Ralf Herbrich. Web-scale bayesian click-through rate prediction for sponsored search advertising in microsoft’s bing search engine. In ICML, 2010.

- McInerney et al. [2015] James McInerney, Rajesh Ranganath, and David Blei. The population posterior and bayesian modeling on streams. Advances in neural information processing systems, 28:1153–1161, 2015.

- Theis and Hoffman [2015] Lucas Theis and Matt Hoffman. A trust-region method for stochastic variational inference with applications to streaming data. In International Conference on Machine Learning, pages 2503–2511. PMLR, 2015.

- Kulhavỳ and Zarrop [1993] R Kulhavỳ and Martin B Zarrop. On a general concept of forgetting. International Journal of Control, 58(4):905–924, 1993.

- Kurle et al. [2020] Richard Kurle, Botond Cseke, Alexej Klushyn, Patrick van der Smagt, and Stephan Günnemann. Continual learning with bayesian neural networks for non-stationary data. In International Conference on Learning Representations, 2020.

- Farquhar and Gal [2018] Sebastian Farquhar and Yarin Gal. A unifying bayesian view of continual learning. Third workshop on Bayesian Deep Learning (NeurIPS 2018), 2018.

- Schwarz et al. [2018] Jonathan Schwarz, Daniel Altman, Andrew Dudzik, Oriol Vinyals, Yee Whye Teh, and Razvan Pascanu. Towards a natural benchmark for continual learning. In NeurIPS Workshop on Continual Learning, 2018.

- Kirkpatrick et al. [2017] James Kirkpatrick, Razvan Pascanu, Neil Rabinowitz, Joel Veness, Guillaume Desjardins, Andrei A Rusu, Kieran Milan, John Quan, Tiago Ramalho, Agnieszka Grabska-Barwinska, et al. Overcoming catastrophic forgetting in neural networks. Proceedings of the national academy of sciences, 114(13):3521–3526, 2017.

- Titsias et al. [2019] Michalis K Titsias, Jonathan Schwarz, Alexander G de G Matthews, Razvan Pascanu, and Yee Whye Teh. Functional regularisation for continual learning with gaussian processes. In International Conference on Learning Representations, 2019.

- Lee et al. [2020] Soochan Lee, Junsoo Ha, Dongsu Zhang, and Gunhee Kim. A neural dirichlet process mixture model for task-free continual learning. In International Conference on Learning Representations, 2020.

- Rao et al. [2019] Dushyant Rao, Francesco Visin, Andrei Rusu, Razvan Pascanu, Yee Whye Teh, and Raia Hadsell. Continual unsupervised representation learning. In Advances in Neural Information Processing Systems, pages 7647–7657, 2019.

- Barry and Hartigan [1992] Daniel Barry and John A Hartigan. Product partition models for change point problems. The Annals of Statistics, pages 260–279, 1992.

- Fearnhead [2005] Paul Fearnhead. Exact bayesian curve fitting and signal segmentation. IEEE Transactions on Signal Processing, 53(6):2160–2166, 2005.

- Fearnhead and Liu [2007] Paul Fearnhead and Zhen Liu. Online inference for multiple changepoint problems. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 69(4):589–605, 2007.

- Adams and MacKay [2007] Ryan Prescott Adams and David JC MacKay. Bayesian online changepoint detection. arXiv preprint arXiv:0710.3742, 2007.

- Xuan and Murphy [2007] Xiang Xuan and Kevin Murphy. Modeling changing dependency structure in multivariate time series. In Proceedings of the 24th international conference on Machine learning, pages 1055–1062, 2007.

- Xie et al. [2012] Yao Xie, Jiaji Huang, and Rebecca Willett. Change-point detection for high-dimensional time series with missing data. IEEE Journal of Selected Topics in Signal Processing, 7(1):12–27, 2012.

- Saatçi et al. [2010] Yunus Saatçi, Ryan D Turner, and Carl Edward Rasmussen. Gaussian process change point models. In ICML, 2010.

- Knoblauch and Damoulas [2018] Jeremias Knoblauch and Theodoros Damoulas. Spatio-temporal bayesian on-line changepoint detection with model selection. In International Conference on Machine Learning, pages 2718–2727. PMLR, 2018.

- Turner et al. [2013] Ryan Turner, Steven Bottone, and Clay Stanek. Online variational approximations to non-exponential family change point models: With application to radar tracking. In Proceedings of the 26th International Conference on Neural Information Processing Systems-Volume 1, pages 306–314, 2013.

- Knoblauch et al. [2018] Jeremias Knoblauch, Jack Jewson, and Theodoros Damoulas. Doubly robust bayesian inference for non-stationary streaming data with -divergences. volume 31, 2018.

- Titsias et al. [2020] Michalis K Titsias, Jakub Sygnowski, and Yutian Chen. Sequential changepoint detection in neural networks with checkpoints. arXiv preprint arXiv:2010.03053, 2020.

- Linderman et al. [2017] Scott Linderman, Matthew Johnson, Andrew Miller, Ryan Adams, David Blei, and Liam Paninski. Bayesian learning and inference in recurrent switching linear dynamical systems. In Artificial Intelligence and Statistics, pages 914–922, 2017.

- Becker-Ehmck et al. [2019] Philip Becker-Ehmck, Jan Peters, and Patrick Van Der Smagt. Switching linear dynamics for variational bayes filtering. In International Conference on Machine Learning, pages 553–562, 2019.

- Murphy [2012] Kevin P Murphy. Machine learning: A probabilistic perspective. MIT press, 2012.

- Barber [2012] David Barber. Bayesian reasoning and machine learning. Cambridge University Press, 2012.

- Bracegirdle and Barber [2011] Chris Bracegirdle and David Barber. Switch-reset models: Exact and approximate inference. In Proceedings of The Fourteenth International Conference on Artificial Intelligence and Statistics, pages 190–198, 2011.

- Wainwright and Jordan [2008] Martin J Wainwright and Michael I Jordan. Graphical models, exponential families, and variational inference. Foundations and Trends® in Machine Learning, 1(1-2):1–305, 2008.

- Hoffman and Blei [2015] Matthew D Hoffman and David M Blei. Structured stochastic variational inference. In Artificial Intelligence and Statistics, 2015.

- Zhang et al. [2018] Cheng Zhang, Judith Bütepage, Hedvig Kjellström, and Stephan Mandt. Advances in variational inference. IEEE transactions on pattern analysis and machine intelligence, 41(8):2008–2026, 2018.

- Smola et al. [2003] Alexander J Smola, Vishy Vishwanathan, and Eleazar Eskin. Laplace propagation. In NIPS, pages 441–448, 2003.

- Mikolov et al. [2013] Tomas Mikolov, Ilya Sutskever, Kai Chen, Greg S Corrado, and Jeff Dean. Distributed representations of words and phrases and their compositionality. In Advances in neural information processing systems, pages 3111–3119, 2013.

- Bamler and Mandt [2017] Robert Bamler and Stephan Mandt. Dynamic word embeddings. In Proceedings of the 34th International Conference on Machine Learning-Volume 70, pages 380–389. JMLR. org, 2017.

- Huynh et al. [2017] Ngoc Anh Huynh, Wee Keong Ng, and Kanishka Ariyapala. A new adaptive learning algorithm and its application to online malware detection. In International Conference on Discovery Science, pages 18–32. Springer, 2017.

- Vergara et al. [2012] Alexander Vergara, Shankar Vembu, Tuba Ayhan, Margaret A Ryan, Margie L Homer, and Ramón Huerta. Chemical gas sensor drift compensation using classifier ensembles. Sensors and Actuators B: Chemical, 166:320–329, 2012.

- Harries and Wales [1999] Michael Harries and New South Wales. Splice-2 comparative evaluation: Electricity pricing. 1999.

- Krizhevsky et al. [2009] Alex Krizhevsky, Geoffrey Hinton, et al. Learning multiple layers of features from tiny images. 2009.

- Netzer et al. [2011] Yuval Netzer, Tao Wang, Adam Coates, Alessandro Bissacco, Bo Wu, and Andrew Y Ng. Reading digits in natural images with unsupervised feature learning. 2011.

- Michel et al. [2011] Jean-Baptiste Michel, Yuan Kui Shen, Aviva Presser Aiden, Adrian Veres, Matthew K Gray, Joseph P Pickett, Dale Hoiberg, Dan Clancy, Peter Norvig, Jon Orwant, et al. Quantitative analysis of culture using millions of digitized books. science, 331(6014):176–182, 2011.

- Gentzkow et al. [2018] Matthew Gentzkow, JM Shapiro, and Matt Taddy. Congressional record for the 43rd-114th congresses: Parsed speeches and phrase counts. In URL: https://data. stanford. edu/congress text, 2018.

- Jankin Mikhaylov et al. [2017] Slava Jankin Mikhaylov, Alexander Baturo, and Niheer Dasandi. United Nations General Debate Corpus, 2017. URL https://doi.org/10.7910/DVN/0TJX8Y.

- Ranganath et al. [2014] Rajesh Ranganath, Sean Gerrish, and David Blei. Black box variational inference. In Artificial Intelligence and Statistics, pages 814–822, 2014.

- Kingma and Welling [2014] Diederik P Kingma and Max Welling. Auto-encoding variational bayes. 2014.

- Kalman [1960] Rudolph Emil Kalman. A new approach to linear filtering and prediction problems. Journal of Basic Engineering, page 82(1):35–45, 1960.

- Rusmassen and Williams [2005] C Rusmassen and C Williams. Gaussian process for machine learning, 2005.

- Bishop et al. [1995] Christopher M Bishop et al. Neural networks for pattern recognition. Oxford university press, 1995.

- Friedman et al. [2001] Jerome Friedman, Trevor Hastie, and Robert Tibshirani. The elements of statistical learning, volume 1. Springer series in statistics New York, 2001.

- Harrison et al. [2020] James Harrison, Apoorva Sharma, Chelsea Finn, and Marco Pavone. Continuous meta-learning without tasks. Advances in Neural Information Processing Systems, 33, 2020.

- Buslaev et al. [2020] Alexander Buslaev, Vladimir I. Iglovikov, Eugene Khvedchenya, Alex Parinov, Mikhail Druzhinin, and Alexandr A. Kalinin. Albumentations: Fast and flexible image augmentations. Information, 11(2), 2020. ISSN 2078-2489. doi: 10.3390/info11020125. URL https://www.mdpi.com/2078-2489/11/2/125.

- Zenke et al. [2017] Friedemann Zenke, Ben Poole, and Surya Ganguli. Continual learning through synaptic intelligence. Proceedings of machine learning research, 70:3987, 2017.

- Lopez-Paz and Ranzato [2017] David Lopez-Paz and Marc’Aurelio Ranzato. Gradient episodic memory for continual learning. In Advances in neural information processing systems, pages 6467–6476, 2017.

- Glorot and Bengio [2010] Xavier Glorot and Yoshua Bengio. Understanding the difficulty of training deep feedforward neural networks. In Proceedings of the thirteenth international conference on artificial intelligence and statistics, pages 249–256, 2010.

- Kingma and Ba [2015] Diederik P Kingma and Jimmy Ba. Adam: A method for stochastic optimization. 2015.

- Wen et al. [2018] Yeming Wen, Paul Vicol, Jimmy Ba, Dustin Tran, and Roger Grosse. Flipout: Efficient pseudo-independent weight perturbations on mini-batches. In International Conference on Learning Representations, 2018.

Appendix A Structured Variational Inference

According to the main paper, we consider the generative model at time step , where the dependence on is contained in . Upon observing the data , both and are inferred. However, exact inference is not available due to the intractability of the marginal likelihood . To tackle this, we utilize structured variational inference for both the latent variables and the Bernoulli change variable . To this end, we define the joint variational distribution as in the main paper. For notational simplicity, we omit the dependence on . Then the updating procedure for and is obtained by maximizing the ELBO :

Given the generative models, we can further expand to simplify the optimization:

| (8) |

where the second step pushes inside the expectation with respect to , the third step re-orders the terms, and the final step utilizes the definition of CELBO (Eq. 7 in the main paper).

Maximizing Eq. A therefore implies a two-step optimization: first maximize the CELBO to find the optimal and , then compute the Bernoulli distribution by maximizing while the CELBOs are fixed.

While typically needs to be inferred by black box variational inference [Ranganath et al., 2014, Kingma and Welling, 2014, Zhang et al., 2018], the optimal has a closed-form solution and bears resemblance to the exact inference counterpart (Eq. 4 in the main paper). To see this, we assume are given and is parameterized by (for the Bernoulli distribution). Rewriting Eq. A gives

which is concave since the second derivative is negative. Thus taking the derivative and setting it to zero leads to the optimal solution of

which attains the closed-form solution as stated in Eq. 6 in the main paper without temperature .

Appendix B Additive vs. Multiplicative Broadening

There are several possible choices for defining an informative prior corresponding to . In latent time series models, such as Kalman filters [Kalman, 1960, Bamler and Mandt, 2017], it is common to define a linear transition model where and . Propagating the posterior at time to the prior at time results in . To simplify the discussion, we set and ; the same argument also applies for the more general case. Adding a constant noise results in adding the variance of all variables with a constant . We thus call this convolution scheme additive broadening. The problem with such a choice, however, is that the associated information loss is not homogeneously distributed: ignores the uncertainty in , and dimensions of with low posterior uncertainty lose more information relative to dimensions of that are already uncertain. We found that this scheme deteriorates the learning signal.

We therefore consider multiplicative broadening (or relative broadening since the associated information loss depends on the original variance) as tempering described in the main paper, resulting in for . For a Gaussian distribution, the resulting variance scales the original variance with . In practice, we found relative or multiplicative broadening to perform much better and robustly than additive posterior broadening. Since tempering broadens the posterior non-locally, this scheme does not possess a continuous latent time series interpretation 121212This means that it is impossible to specify a conditional distribution that corresponds to relative broadening..

Appendix C Details on “Shy” Variational Greedy Search and Variational Beam Search

diverse_truncation;

“Shy” Variational Greedy Search.

As illustrated in Fig. 1 in the main text, one obtains better interpretation if one outputs the variational parameters and at the end of a segment of constant . More precisely, when the algorithm detects a change point , it outputs the variational parameters and from just before the detected change point . These parameters define a variational distribution that has been fitted, in an iterative way, to all data points since the preceding detected change point. We call this the “shy” variant of the variational greedy search algorithm, because this variant quietly iterates over the data and only outputs a new fit when it is as certain about it as it will ever be. The red lines and regions in Fig. 1 (a) in the main paper illustrate means and standard deviations outputted by the “shy” variant of variational greedy search.

Variational Beam Search.

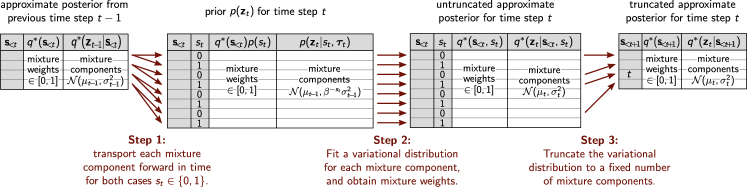

As follows, we present a more detailed explanation of the variational beam search procedure mentioned in Section 3.3 of the main paper. Our beam search procedure defines an effective way to search for potential hypotheses with regards to sequences of inferred change points. The procedure is completely defined by detailing three sequential steps, that when executed, take a set of hypotheses found at time step and transform them into the resulting set of likely hypotheses for time step that have appropriately accounted for the new data seen at . The red arrows in Figure 4 illustrate these three steps for beam search with a beam size of .

In Figure 4, each of the three steps maps a table of considered histories to a new table. Each table defines a mixture of Gaussian distributions where each mixture component corresponds to a different history and is represented by a different row in the table. We start on the left with the (truncated) variational distribution from the previous time step, which is a mixture over Gaussian distributions. Each mixture component (row in the table) is labeled by a 0-1 vector of the change variable values according to that history. Each mixture component further has a mixture weight , a mean, and a standard deviation.

We then obtain a prior for time step by transporting each mixture component of forward in time via the broadening functional (“Step 1” in the above figure). The prior (second table in the figure) is a mixture of Gaussian distributions because each previous history splits into two new ones for the two potential cases . The label for each mixture component (table row) is a new vector or , appending to the tail of .

“Step 2” in the above figure takes the data and fits a variational distribution that is also a mixture of Gaussian distributions. To learn the variational distribution, we (i) numerically fit each mixture component individually, using the corresponding mixture component of as the prior; (ii) evaluate (or estimate) the CELBO of each fitted mixture component, conditioned on ; (iii) compute the approximate posterior probability of each mixture component, in the presence of the CELBOs; and (iv) obtain the mixture weight equal to the posterior probability over , i.e., , best approximated by .

“Step 3” in the above figure truncates the variational distribution by discarding of the mixture components. The truncation scheme can be either the “vanilla” beam search or diversified beam search outlined in the main paper. The truncated variational distribution is again a mixture of only Gaussian distributions, and it can thus be used for subsequent update steps, i.e., from to .

The pseudocode is listed in Algo 1.

Appendix D Online Bayesian Linear Regression with Variational Beam Search

This section will derive the analytical solution of online updates for both Bayesian linear regression and the probability of change points. We consider Gaussian prior distributions for weights. The online update of the posterior distribution is straightforward in the natural parameter space, where the update is analytic given the sufficient statistics of the observations. If we further allow to temper the weights’ distributions with a fixed temperature , then this corresponds to multiplying each element in the precision matrix by . We applied this algorithm to the linear regression experiments in Section 4.3. For unified names, we still use the word “variational” even though the solutions are analytical.

D.1 Variational Continual Learning for Online Linear Regression

Let’s start with assuming a generative model at time :

| (9) |

and the noise is constant over time.

The posterior distribution of is of interest, which is Gaussian distributed since both the likelihood and prior are Gaussian. To get an online recursion for ’s posterior distribution over time, we consider the natural parameterization. The prior distribution under this parameterization is

where are the natural parameters and the terms unrelated to are absorbed into the normalizer .

Following the same parameterization, the posterior distribution can be written

Thus we get the recursion over the natural parameters

from which the posterior mean and covariance can be solved.

D.2 Prediction and Marginal Likelihood

We can get the posterior predictive distribution for a new input through inspecting Eq. 9 and utilizing the linear properties of Gaussian. Assuming the generative model as specified above, we replace with in Eq. 9. Since is Gaussian distributed, by its linear property, conforms to . Then the addition of two independent Gaussian results in .

The marginal likelihood shares this same form with the posterior predictive distribution, with a potentially different pair of sample . To see this, given a prior distribution , then the marginal likelihood of is

| (10) |

with being the noise variance. Note that in variational inference with an intractable marginal likelihood (not like the linear regression here), this is the approximated objective (Evidence Lower Bound (ELBO), indeed) we aim to maximize.

Computation of the Covariance Matrix

Since we parameterize the precision matrix instead of the covariance matrix, the variance of the new test sample requires to take the inverse of the precision matrix. In order to do this, we employ the eigendecomposition of the precision matrix and re-assemble to the covariance matrix through inverting the eigenvalues. A better approach is to apply the Sherman-Morrison formula for the rank one update131313https://en.wikipedia.org/wiki/Sherman%E2%80%93Morrison_formula, which can reduce the computation from to .

Logistic Normal Model

If we are modeling the log-odds by a Bayesian linear regression, then we need to map the log-odds to the interval by the sigmoid function, to make it a valid probability. Specifically, suppose and (note we abuse by variances and functions, but it is clear from the context and the subscripts) where is a logistic sigmoid function. Then has a logistic normal distribution. Given , we can make decisions for the value of . There are three details that worth noting. First is from the non-linear mapping of . One special property of is that can be bimodal if the base variance or is large. A consequence is that the mode of does not necessarily correspond to ’s mode and . Second is for the binary classification: the decision boundary of , i.e., 0.5, is consistent with the one of , i.e., 0, for decisions either by or by . See Rusmassen and Williams [2005] (Section 3.4) and Bishop et al. [1995] (Section 10.3). Third, if our loss function for decision making is the absolute error, then the best prediction is the median of [Friedman et al., 2001] where is the median of . This follows from the monotonicity of that does not change the order statistics.

D.3 Inference over the Change Variable

To infer the posterior distribution of given observations , we apply Bayes’ theorem to infer the posterior log-odds as in the main paper

where is exactly Eq. 10 but has different parameter values dictated by and .

In the next part, we show the resulting distribution of the broadening operation.

D.3.1 Tempering a Multivariate Gaussian

We will show the tempering operation of a multivariate Gaussian corresponds to multiplying each element in the precision matrix by the fixed temperature, a simple form in the natural space.

Suppose we allow to temper / broaden the ’s multivariate Gaussian distribution before the next time step, accommodating more evidence. Let the broadening constant or temperature be . We derive how affects the multivariate Gaussian precision.

Write the tempering explicitly,

among which we are interested in the relationship between and and . To this end, re-write the quadratic form in the summation

where we can identify an element-wise relation: for all possible

D.3.2 Prediction

As above, we are interested in the posterior predictive distribution for a new test sample after absorbing evidence. Let’s denote the parameters of ’s posterior distributions by and , where the dependence over is made explicit. We then make posterior predictions with each component

Appendix E Visualization of Catastrophic Remembering Effects

In order to demonstrate the effect of catastrophic remembering, we consider a simple linear regression model. We will see that, when the data distribution changes, a Bayesian online learning framework becomes quickly overconfident and unable to adjust to the changing data distribution. On the other hand, with tempering, variational greedy search (VGS) can partially forget the previous knowledge and then adapt to the shifted distribution.

Data Generating Process

We generated the samples by the following generative model:

where equals or . In this experiments, we sampled the first 20 points from and the remaining 20 points from .

Model Parameters

We applied the Bayes updates mentioned in Section D to do inference over the slope and intercept. We set the initial priors of the weights to be standard Gaussian and the observation noise to be the true scale, 0.1. This setting is enough for VCL.

For VGS, we set the same noise variance . For the method-specific parameters, we set and .

We plotted the noise-free posterior predictive distribution for both VCL and VGS. That is, let be the fitted function, we plotted where is the observed samples so far.

Results

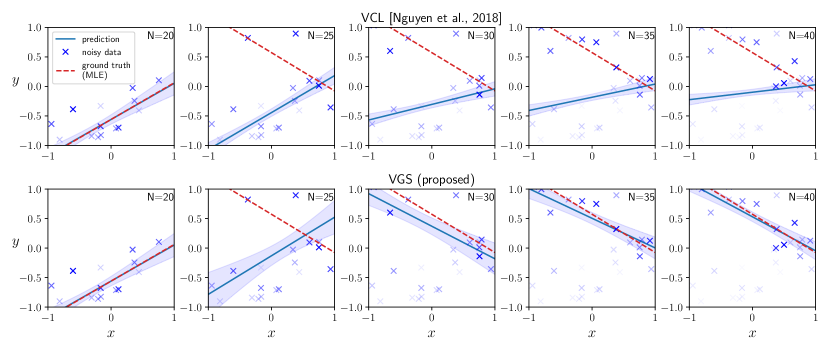

We first visualized the catastrophic remembering effect through a 1D online Bayesian linear regression task where a distribution shift occurred unknown to the regressor (Fig. 5). In this setup, noisy data were sampled from two ground truth functions and , where, with constant additive noise, the first 20 samples came from and the remaining 20 samples were from . The observed sample is presented one by one to the regressor. Before the regression starts, the weights (slope and intercept) were initialized to be standard Gaussian distributions. We experimented two different online regression methods, original online Bayesian linear regression (VCL [Nguyen et al., 2018]) and the proposed variational greedy search (VGS). In Fig. 5, to show a practical surrogate for the ground truth, we plotted the maximum likelihood estimation (MLE) for each function given the observations. The blue line and the shaded area correspond to the mean and standard deviation of the posterior predictive distribution after observing samples. As shown in Fig. 5, both VCL (top) and VGS (bottom) faithfully fit to after observing the first 20 samples. However, when another 20 new observations are sampled from , VCL shows catastrophic remembering of and cannot adapt to . VGS, on the other hand, tempers the prior distribution automatically and succeeds in adaptation.

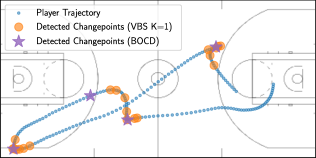

Appendix F NBAPlayer: Change Point Detection Comparisons

VBS vs. BOCD

We investigated the changepoint detection characteristics of our proposed methods and compared against the BOCD baseline in Fig. 6 (left). On the shown example trajectory, BOCD detects abrupt change points, corresponding to different plays, a similar phenomenon observed by [Harrison et al., 2020]. However, we argue that it is insufficient and late to identify a player’s strategy purpose – it only triggers an alarm after a new play starts. VBS, on the other hand, characterizes the transition phases between plays, triggers an early alarm before the next play starts. It also shows the difference between BOCD and VBS in changepoint detection: while BOCD only detects abrupt changes, VBS detects gradual changes as well.

Practical Considerations of VBS and BOCD

Using our variational inference extensions of BOCD, we can overcome the inference difficulty of non-conjugate models. But, considering practical issues, VBS is better in that the detected change points are easy to read from the binary change variable values and free from post-processing – a procedure that BOCD has to exercise. BOCD often outputs a sequence of run lengths either online or offline, among which the change points do not always correspond to the time when the most probable run length becomes one. Instead, the run length oftentimes is larger than one when change point happens. Then people have to inspect the run lengths and set a subjective threshold to determine when a change point occurs, which is not data-driven and may incur undesirable detection. For example, in our basketball player tracking experiments, we set the threshold of change points to be 50; VBS, on the other hand, is free from this post-process thresholding and provides multiple plausible, completely data-driven hypotheses of change points.

Ablation Study of Beam Size

The right plot and the table in Fig 6 shows, on the example trajectory, the detected change points and the average log-likelihood as the beam size changes. When , VBS characterizes the trajectory where the velocity direction changes; when or , it seems that some parts where the velocity value changes are detected. We also observed that the average predictive log-likelihood improves as increases.

Appendix G Experiment Details and Results

In this section, we provide the unstated details of the experiments mentioned in the main paper. These details include but are not limited to hardware infrastructure used to experiment, physical running time, hyperparameter searching, data generating process, evaluation metric, additional results, empirical limitations, and so on. The subsection order corresponds to the experiments order in the main paper. We first provide some limitations of our methods during experiments.

Limitations

Our algorithm is theoretically sound. The generality and flexibility renders a great performance in experiments, however, at the expense of taking more time to search the hyperparameters in a relatively large space. Specifically, there are two hyperparameters to tune: and . The grid search over these two hyperparameters could be slow. When we further take into account the beam size , it adds more burden in parameter searching. But we give a reference scope to the tuning region where the search should perform. Oftentimes, we use the same parameters across beam sizes.

G.1 An Illustrative Example

Data Generating Process

To generate Figure 2 in the main paper, we used a step-wise function as ground truth, where the step size was 1 and two step positions were chosen randomly. We sampled 30 equally-spaced points with time spacing 1. To get noisy observations, Gaussian noise with standard deviation 0.5 was added to the points.

Model Parameters

In this simple one-dimensional model, we used absolute broadening with a Gaussian transition kernel where and . The inference is thus tractable because is conditional conjugate to (and both are Gaussian distributed). We set the prior log-odds to , where . We used beam size 2 to do the inference.

G.2 Bayesian Linear Regression Experiments

We performed all linear regression experiments on a laptop with 2.6 GHz Intel Core i5 CPU. All models on SensorDrift, Elec2, and NBAPlayer dataset finished running within 5 minutes. Running time on Malware dataset varied: VCL, BF, and Independent task are within 10 minutes; VGS takes about two and half hours; VBS (K=3) takes about six hours; VBS (K=6) takes about 12 hours. BOCD takes similar time with VBS. The main difference between VCL’s computation cost and VBS’s computation cost lies in the necessarity of inverting the precision matrix into covariance matrix. However, the matrix inverse computation in VBS and BOCD can be substantially reduced from to by the recursion of Sherman–Morrison formula; we will implement this in the future.

Problem Definitions

We considered both classification experiments (Malware, Elec2) and regression experiments (SensorDrift, NBAPlayer). The classification datasets have real-value probabilities as targets, permitting to perform regression in log-odds space.

Setup and Evaluation

We defined each task to consist of a single observation. Models made predictions on the next observation immediately after finishing learning current task. Models were then evaluated with one-step-ahead absolute error141414in probability space for classification tasks; in data space for regression tasks. With the exception of NBAPlayer dataset, we evaluated models with predictive log probability ., which is then used to compute the mean cumulative absolute error (MCAE) at time : where is the predicted value and is the ground truth. We further approximated the Gaussian posterior distribution by a point mass centered around the mode. It should be noticed that for linear regression, the Laplace Propagation has the same mode as Variational Continual Learning, and the independent task has the same mode as its Bayesian counterpart.

Results

We reported the result of the dominant hypothesis of VBS with large beam size. Fig. 7 shows MCAE over time for the first three datasets. Our methods remain lower prediction error of all time while baselines are subject to strong fluctuations or inability to adapt to distribution shifts. Another observation is that VBS with different beam sizes performed similarly in this case.

G.2.1 Baseline Hyperparameters

BOCD

We only keep the top three or six most probable run length after each time step.

We tuned the hyperparameter in the hazard function, or the transition probability. is searched in .

Malware selects ; Elec2 selects ; SensorDrift selects ; NBAPlayer selects .

BF

We implemented Bayesian Forgetting according to [Kurle et al., 2020].

We tuned the hyperparameter as the forgetting rate such that where . is searched in .

Malware selects ; Elec2 selects ; SensorDrift selects ; NBAPlayer selects .

G.2.2 Malware151515https://archive.ics.uci.edu/ml/datasets/Dynamic+Features+of+VirusShare+Executables

Dataset

There are 107856 programs collected from 2010.11 to 2014.7 in the monthly order. Each program has 482 counting features and a real-valued probability of being malware. This ground truth probability is the proportion of 52 antivirus solutions that label malware. We used the first-month data (2010.11) as the validation dataset and the remaining data as the test dataset. To enable analytic online update, we cast the binary classification problem in the log-odds space and performed Bayesian linear regression. We filled log-odds boundary values to be and , corresponding to probability and , respectively. Our methods achieved comparable results reported in [Huynh et al., 2017] on this dataset.

Hyperparameters

We searched the hyperparameters , and using the validation set. Specifically, we extensively searched , , . On most values the optimization landscape is monotonic and thus the search quickly converges around a local optimizer. Within the local optimizer, we performed the grid search, which focused on .

We found all methods favored . And for VGS and VBS, the uninformative prior of the change variable was already a suitable one. VGS selected , VBS (K=3) selected , and VBS (K=6) selected . Although searched varies for different beam size, the performance of different beam size in this case, based on our experience, is insensitive to the varying .

G.2.3 SensorDrift161616http://archive.ics.uci.edu/ml/datasets/Gas+Sensor+Array+Drift+Dataset+at+Different+Concentrations

Dataset

We focused on one kind of gas, Acetaldehyde, retrieved from the original gas sensor drift dataset [Vergara et al., 2012], which spans 36 months. We formulated an regression problem of predicting the gas concentration level given all the other features. The dataset contains 128 features and 2926 samples in total. We used the first batch data (in the original dataset) as the validation set and the others as the test set. Since the scales of the features vary greatly, we scaled each feature with the sample statistics computed from the validation set, leading to zero mean and unit standard deviation for each feature.

Hyperparameters

We found that using a Bayesian forgetting module (instead of tempered posterior module mentioned in the main paper), which corresponds to , works better for this dataset. Since we scaled the dataset, we therefore set the hyperparameter for all methods. We searched and using the validation set. Specifically, we did the grid search for the prior probability of change point and the temperature . The search procedure selects and for all beam size .

G.2.4 Elec2171717https://www.openml.org/d/151

Dataset

The dataset contains the electricity price over three years of two Australian states, New South Wales and Victoria [Harries and Wales, 1999]. While the original problem was 0-1 binary classification, we re-produced the targets with real-value probabilities since all necessary information forming the original target is contained in the dataset. Specifically, we re-defined the target to be the probability of the price in New South Wales increasing relative to the price of the last 24 hours. Then we performed linear regression in the log-odds space. We filled log-odds boundary values to be and , corresponding to probability and , respectively. After removing the first 48 samples (for which we cannot re-produce the targets), we had 45263 samples, and each sample comprised 14 features. The first 4000 samples were used for validation while the others were used for test.

Hyperparameters

We searched the hyperparameters , and using the validation set. Specifically, we extensively searched , , .

VCL favored , and we set this value for all other methods. VGS selected . VBS (K=3) and VBS (K=6) inherited the same value from VGS.

G.2.5 NBAPlayer181818https://github.com/linouk23/NBA-Player-Movements

Dataset

The original dataset contains part of the game logs of 2015-2016 NBA season in json files. The log records each on-court player’s position (in a 2D space) at a rate of 25 Hz. We pre-processed the logs and randomly extracted ten movement trajectories for training set and another ten trajectories for test set. For an instance of the trajectory, we selected Wesley Matthews’s trajectory at the 292th event in the game of Los Angeles Clippers vs. Dallas Mavericks on Nov 11, 2015. The trajectories vary in length and correspond to players’ strategic movement. After extracting the trajectories, we fix the data set and then evaluate all methods with it. Specifically, we regress the current position on the immediately previous position–modeling the player’s velocity.

Hyperparameters

We searched the hyperparameters , and using the training set. Specifically, we searched and and .

VCL favored , and we set this value for all other methods. VBS (K=1, VGS) selected and . VBS (K=3) selected and . VBS (K=6) selected and . In generating the plots on the example trajectory, we used with varying and varying beam size .

G.3 Bayesian Deep Learning Experiments