Model-assisted estimation in high-dimensional settings for survey data

Abstract

Model-assisted estimators have attracted a lot of attention in the last three decades. These estimators attempt to make an efficient use of auxiliary information available at the estimation stage. A working model linking the survey variable to the auxiliary variables is specified and fitted on the sample data to obtain a set of predictions, which are then incorporated in the estimation procedures. A nice feature of model-assisted procedures is that they maintain important design properties such as consistency and asymptotic unbiasedness irrespective of whether or not the working model is correctly specified. In this article, we examine several model-assisted estimators from a design-based point of view and in a high-dimensional setting, including penalized estimators and tree-based estimators. We conduct an extensive simulation study using data from the Irish Commission for Energy Regulation Smart Metering Project, in order to assess the performance of several model-assisted estimators in terms of bias and efficiency in this high-dimensional data set.

Key words: Design consistency; Elastic net; Lasso; Random forest; Regression tree; Ridge regression.

1 Introduction

Surveys conducted by national Statistical Offices (NSO) aim at estimating finite population parameters, which are those describing some aspect of the finite population under study. In this article, the interest lies in estimating the population total of a survey variable . Population totals can be estimated unbiasedly using the well-known Horvitz-Thompson estimator (Horvitz and Thompson,, 1952). In the absence of nonsampling errors, the Horvitz-Thompson estimator is unbiased with respect to the customary design-based inferential approach, whereby the properties of estimators are evaluated with respect to the sampling design; e.g., see Särndal et al., (1992). However, Horvitz-Thompson type estimators may exhibit a large variance in some situations. The efficiency of the Horvitz-Thompson estimator can be improved by incorporating some auxiliary information, capitalizing on the relationship between the survey variable and a set of auxiliary variables . The resulting estimation procedures, referred to as model-assisted estimation procedures, use a working model as a vehicle for constructing point estimators. Model-assisted estimators remain design-consistent even if the working model is misspecified, which is a desirable feature. When the working model provides an adequate description of the relationship between and , model-assisted estimators are expected to be more efficient than the Horvitz-Thompson estimator.

The class of model-assisted estimators include a wide variety of procedures, some of which have been extensively studied in the literature both theoretically and empirically. When the working model is the customary linear regression model, the resulting estimator is the well-known generalized regression estimator (GREG); e.g., Särndal, (1980), Särndal and Wright, (1984) and Särndal et al., (1992). Other works include model-assisted procedures based on generalized linear models (Lehtonen and Veijanen,, 1998; Firth and Bennett,, 1998), local polynomial regression (Breidt and Opsomer,, 2000), splines (Breidt et al.,, 2005; Goga,, 2005; McConville and Breidt,, 2013; Goga and Ruiz-Gazen,, 2014), neural nets (Montanari and Ranalli,, 2005), generalized additive models (Opsomer et al.,, 2007), nonparametric additive models (Wang and Wang,, 2011), regression trees (Toth and Eltinge,, 2011; McConville and Toth,, 2019) and random forests (Dagdoug et al.,, 2020).

Due to the recent advances of information technology, NSOs have now access to a variety of data sources, some of which may exhibit a large number of observations on a large number of variables. So far, the properties of model-assisted estimator have been established under the customary asymptotic framework in finite population sampling (Isaki and Fuller,, 1982) for which both the population size and the sample size increase to infinity, while assuming that the number of auxiliary variables is fixed. In other words, existing results require to be large relative to . This framework is generally not adequate in the context of high-dimensional data sets as may be of the same order as , or even larger, i.e., . Therefore, a more appropriate asymptotic framework would let increase to infinity in addition to and . Cardot et al., (2017) studied dimension reduction through principal component analysis and established the design consistency of the resulting calibration estimator. More recently, Ta et al., (2020) investigated the properties of the GREG estimator from a model point of view and when is allowed to diverge.

The aim of this paper is to investigate the design properties of a number of model-assisted estimation procedures when is allowed to grow to infinity. We start by showing that, under mild assumptions on the sampling design and the auxiliary information, the GREG estimator is deign-consistent provided that goes to zero. In a high-dimensional setting, one can recourse to penalization methods such as ridge, lasso and elastic net. We investigate the theoretical properties of model-assisted estimators based on these penalized methods and show that, under very mild regularity conditions, these estimators are design-consistent provided that goes to zero. As we argue in Section 3, this rate can be improved if one is willing to make additional assumptions about the rate of convergence of the estimated regression coefficient. In particular, we lay out a set of additional conditions under which the model-assisted ridge estimator is consistent if goes to zero and moreover, is -consistent if with Also, provided that the predictors orthogonal, we show that both the model-assisted lasso and elastic net estimators are consistent provided that goes to zero.

When the relationship between the study and the auxiliary information does not appear to be linear in the auxiliary variables, the problem of model-assisted estimation becomes more challenging, especially in a high-dimensional setting, a phenomenon known as the curse of dimensionality. Tree based methods that include regression trees and random forests tend to be efficient in these conditions. We establish the -design consistency of some tree-based methods in a high-dimensional setting without any condition on the number of auxiliary variables. Hence, these methods remain consistent even when is much larger than , which is an attractive feature. To assess the performance of several model-assisted estimators in a high-dimensional setting, we conduct a simulation study using data from the Irish Commission for Energy Regulation Smart Metering Project. The data set consists of electricity consumption recorded every half an hour for a two-year period and for more than households and businesses, leading to highly correlated data. Due to the high-dimensional feature, linear relationships are difficult to detect and even if we succeed, estimators based on linear models tend to breakdown. In this case, penalized and tree-based model-assisted estimators may provide good alternatives. However, an empirical comparison of these model-assisted estimators in terms of bias and efficiency in a high-dimensional setting is currently lacking. We aim to fill this gap in the article.

The paper is organized as follows. In Section 2, we introduce the theoretical setup. In Section 3, we investigate the asymptotic design properties of several model-assisted estimators: the GREG estimator as well as estimators based on ridge regression, lasso and elastic net. Tree-based methods in a high-dimensional setting are considered in Section 4. Section 5 contains an empirical comparison to assess the performance of several model-assisted estimators in terms of bias and efficiency. We make some final remarks in Section 6. The technical details, including the proofs of some results, are relegated to the Appendix.

2 The setup

Consider a finite population of size . We are interested in estimating , the population total of the survey variable . We select a sample from according to a sampling design with first-order and second-order inclusion probabilities and , respectively. In the absence of nonsampling errors, the Horvitz-Thompson estimator

| (1) |

is design-unbiased for provided that for all ; that is, where denotes the expectation operator with respect to the sampling design . In the sequel, unless stated otherwise, the properties of estimators are evaluated with respect to the design-based approach. Under mild conditions (Robinson and Särndal,, 1983; Breidt and Opsomer,, 2000), it can be shown that the Horvitz-Thompson estimator is design-consistent for .

At the estimation stage, we assume that a collection of auxiliary variables, , is recorded for all . Moreover, we assume that the corresponding population totals are available from an external source (e.g., a census or an administrative file). Let be the -vector associated with unit . Also, we denote by the design matrix and its sample counterpart.

Model-assisted estimation starts with postulating the following working model:

| (2) |

where and the errors are independent random variables such that and for all . Although we assume an homoscedastic variance structure, our results can be easily extended to the case of unequal variances of the form for some known function .

The unknown function is estimated by from the sample data . The fitted model is then used to construct the model-assisted estimator

| (3) |

where denotes the prediction at under the working model (2). Whenever the predictor is sample dependent, the estimator is design-biased, but can be shown to be asymptotically design-unbiased and design-consistent for a wide class of working models, as the population size and the sample size increase.

3 Least squares and penalized model-assisted estimators

3.1 The GREG estimator

Suppose that the regression function is approximated by a linear combination of . The working model (2) reduces to

| (4) |

where is a vector of unknown coefficients. Under a hypothetical census, where we observe and for all the vector would be estimated by through the ordinary least square criterion at the population level:

| (5) |

where Provided that the matrix is of full rank, the solution to (5) is unique and given by

| (6) |

In practice, the vector in (6) cannot be computed as the -values are recorded for the sample units only. An estimator of denoted by is obtained from (6) by estimating each total separately using the corresponding Horvitz-Thompson estimator. Alternatively, the estimator can be obtained using the following weighted least square criterion at the sample level:

| (7) |

where and . Again, the solution to (7) is unique provided that is of full rank and it is given by

| (8) |

The prediction of at under the working model (4) is . Plugging in (3) leads to the well-known GREG estimator (Särndal et al.,, 1992):

| (9) | |||||

If the intercept is included in the working model, the GREG estimator reduces to the population total of the fitted values that is, Also, the GREG estimator can be written as a weighted sum of the sample -values:

| (10) |

where

These weights can be also obtained as the solution of a calibration problem (Deville and Särndal,, 1992). More specifically, the weights are such that the generalized chi-square distance is minimized subject to the calibration constraints This attractive feature may not be shared by model-assisted estimators derived under more general working models.

3.2 Penalized least square estimators

While model-assisted estimators based on linear regression working models are easy to implement, they tend to breakdown when the number of auxiliary variables is growing large. Also, when some of the predictors are highly related to each other, a problem known as multicolinearity, the ordinary least square estimator given by (6) may be highly unstable. As noted by Hoerl and Kennard, (2000), “the worse the conditioning of the more can be expected to be too long and the distance from to will tend to be large”. In survey sampling, the effect of multicolinearity on the stability of point estimators has first been studied by Bardsley and Chambers, (1984) under the model-based approach. Chambers, (1996) and Rao and Singh, (1997) examined this problem in the context of calibration. These authors noted that, using a large number of calibration constraints, may lead to highly dispersed calibration weights, potentially resulting in unstable estimators.

In a classical iid linear regression setting, penalization procedures such as ridge, lasso or elastic-net can be used to help circumvent some of the difficulties associated with the usual least squares estimator . Let be an estimator of obtained through the penalized least square criterion at the population level:

| (11) |

where , and are positive real numbers, is a given norm and is a fixed positive integer representing the number of different norm constraints. The values of and are typically predetermined. The tuning parameters control the strength of the penalty that one wants to impose on the norm of and, most often, is chosen by cross-validation. The coefficients and are specific to the penalization method. Hence, they have an impact on the properties of the resulting estimator Three special cases are considered below.

When and , the estimator is known as the ridge regression estimator (Hoerl and Kennard,, 1970):

where is the usual Euclidian norm of The solution is given explicitly by

| (12) |

where denotes the identity matrix.

When and the estimator is known as the lasso estimator (Tibshirani,, 1996):

| (13) |

where is the -norm of As for the ridge, the lasso has the effect of shrinking the coefficients but, unlike the ridge, it can set some coefficients to zero. Except when the auxiliary variables are orthogonal, there is no closed-form formula for the lasso estimator In survey sampling, McConville et al., (2017) investigated the design-based properties of the lasso model-assisted estimator for fixed .

The elastic-net estimator, that was suggested by Zou and Hastie, (2005), combines two norms: the euclidean norm and the norm, . If, in (11), we set , , and , the resulting estimator is the elastic-net estimator, which can be viewed as a trade-off between the ridge estimator and the lasso estimator, realizing variable selection and regularization simultaneously:

for and a parameter that is usually chosen using a grid of multiple values of . The penalized regression estimator in (11) is unknown as the -values are not observed for the non-sample units. To overcome this issue, we use the following weighted penalized least square criterion at the sample level:

| (14) |

A model-assisted estimator based on a penalized regression procedure is obtained from (3) by replacing with leading to

| (15) | |||||

where is a generic notation used to denote the estimated regression coefficient obtained through either lasso, ridge or elastic net. Unlike the GREG estimator, the penalized model-assisted estimator is sensitive to unit change of the -variables because is sensitive to unit change. This is why, as in the classical regression setting, standardization of the -variables is recommended before computing If the intercept is included in the model, then it is usually left un-penalized.

Remark 3.1.

In the case of ridge regression, the estimator is given by

| (16) |

Using (16) in (15) leads to the ridge model-assisted estimator that can be expressed as a weighted sum of sampled -values, with weights given by

These weights can also be obtained through a penalized calibration problem. It can be shown that they minimize the penalized generalized chi-square distance, (Chambers,, 1996; Beaumont and Bocci,, 2008). If some -variables are left un-penalized in (11), the resulting weights ensure consistency between the survey estimates and their corresponding population totals associated with these variables.

3.3 Consistency of the GREG and penalized GREG estimators in a high-dimensional setting

We adopt the asymptotic framework of Isaki and Fuller, (1982) and consider an increasing sequence of embedded finite populations of size . In each finite population , a sample, of size is selected according to a sampling design with first-order inclusion probabilities and second-order inclusion probabilities . While the finite populations are considered to be embedded, we do not require this property to hold for the samples . This asymptotic framework assumes that goes to infinity, so that both the finite population sizes , the samples sizes and the number of auxiliary variables go to infinity. To improve readability, we shall use the subscript only in the quantities , and ; for instance, quantities such as shall be simply denoted by .

The following assumptions are required to establish the consistency of the GREG and penalized GREG estimators in a high-dimensional setting.

(H1) We assume that there exists a positive constant such that

(H2) We assume that .

(H3) There exist a positive constant such that also, we assume that . (H4) We assume that there exists a positive constant such that, for all , , where denotes the usual Euclidian norm.

(H5) We assume that where is the least square estimator given in (8) and denotes the norm.

The assumptions (H3.3), (H3.3) and (H3.3) were used by Breidt and Opsomer, (2000) in a nonparametric setting and similar assumptions were used by Robinson and Särndal, (1983) to establish the consistency of the GREG estimator in a fixed dimensional setting. These assumptions hold for many usual sampling designs such as simple random sampling without replacement, stratified designs (Breidt and Opsomer,, 2000), or high-entropy sampling designs. Assumptions (H3.3) and (H3.3) can be viewed, respectively, as extensions of Assumption A.1 and Assumption A.3 in Robinson and Särndal, (1983) to -dimensional vectors with growing to infinity. Assumption (H3.3) is not very restrictive in this high-dimensional setting, it requires that components of are all bounded. When is fixed, then our assumptions essentially reduce to those of Robinson and Särndal, (1983).

Result 3.1.

The -consistency obtained by Robinson and Särndal, (1983) is a special case of Result 3.1 with . Result 3.1 highlights the fact that the rate of convergence decreases as the number of auxiliary variables increases. Yet, this result guarantees the existence of a consistent GREG estimator, even when the number of auxiliary variables is allowed to diverge. An improved consistency rate for may be obtained if the usual euclidean norm is used instead of -norm. Establishing the rate of convergence of the sampling error may also be utilized to obtain a lower consistency rate for . This is beyond of the scope of this article.

The next result establishes the design-consistency of model-assisted penalized regression estimators. The proof is similar to that of result 3.1 and is given in the Appendix.

Result 3.2.

The above result makes no use of the asymptotic convergence rate of which depends on the penalization method. For example, if one can establish that , then Alternatively, improved consistency rates of may be obtained if one can establish the extent of the sampling error in a high-dimension setting. However, obtaining these improved rates requires additional assumptions, while Result 3.2 is obtained under relatively mild assumptions.

Next, we show that, under additional assumptions on the auxiliary variables, the model-assisted ridge estimator is design-consistent for if goes to zero and that it has the usual -consistency rate if with which constitutes a significant improvement over Result 3.2.

Result 3.3.

Assume (H3.3)-(H3.3). Also, assume that there exists a positive constant such that where is the largest eigenvalue of Assume also that

-

1.

Then, there exists a positive constant such that and

If the numbers of auxiliary variables and the sample sizes satisfy , then

-

2.

If then

-

3.

We have the following asymptotic equivalence:

where

and

If with then

The case of model-assisted estimators based on lasso and elastic-net is more intricate. This is due to the fact that both estimators involve the -norm. As a result, a closed-form of these estimators cannot be obtained. However, if the predictors are orthogonal, a closed-form expression exists for the lasso and elastic-net estimators and improved consistency rates can be obtained; see Proposition 3.1 below. The case of non-orthogonal predictors is more challenging and is beyond the scope of this article.

4 Tree-based methods

The penalization procedures considered in Section 3 required the -vector of auxiliary variables to be available for and the corresponding vector of population totals . In other words, the individual values of were not needed. Also, the GREG estimator and the model-assisted estimators based on ridge regression, lasso and elastic net, were all based on a linear working model. In practice, the relationship between the survey variable and may be nonlinear and one may have access to complete auxiliary information, which arises when the -vector is recorded for all . In this case, we may consider additional model-assisted estimators based on nonparametric procedures; e.g., kernel or spline regression (Breidt and Opsomer,, 2000; Breidt et al.,, 2005; Goga,, 2005; McConville and Breidt,, 2013). However, these methods are vulnerable to the so-called curse of dimensionality, which arises when is large. The reader is referred to (Hastie et al.,, 2011, chapter 1) and (Györfi et al.,, 2006, chapter 2) for a discussion. In contrast, tree-based methods, that include regression trees and random forests as special cases, may prove useful when the number of auxiliary variables, is large. McConville and Toth, (2019) and Dagdoug et al., (2020) studied model-assisted estimators based on regression trees and random forests under the customary framework that treats the dimension of the -vector, as fixed.

4.1 Model-assisted estimators based on regression trees

Regression trees is one of the most popular statistical learning methods which assumes that the regression function has the form

| (17) |

where are non-overlapping regions of built recursively from the sample data and by using some optimization criterion for better prediction of A regression tree can be viewed as a linear regression model based on the set of predictors for The regions are highly dependent on the sample data in terms of shape and number. Given the unknown parameters from (17) are estimated by determined using the following weighted least-square criterion at the sample level:

| (18) |

where The criterion (18) is different from the one used in the customary iid setup as it incorporates the sampling weights . The solution to (18) is given by

| (19) |

where and . Each unit belongs to one and only one region. As a result, the matrix is diagonal with elements equal to for Usually, most algorithms leading to the regions use a stopping criterion. The most common consists of specifying a minimum number, of observations in each region. To avoid unduly large nodes, the algorithm also ensures that the number of observations in each node does not exceed Therefore, for all and the matrix is non-singular for all samples The vector is always well-defined and, using (19), we obtain

The estimator is simply the weighted mean of the -values associated with sample units falling in region

The prediction of at is then given by

| (20) |

and a model-assisted estimator based on regression trees is given by

| (21) | |||||

where is defined in (20). As noted by McConville and Toth, (2019), the form of the estimator (21) is similar to that of a post-stratified estimator with sample-based post-strata . However, unlike the customary post-stratified estimator which requires the population counts only, the estimator requires complete auxiliary information.

It can be shown that (21) can be expressed as a projection-type estimator. Let be the -dimensional vector of ones. We have for all since the vector contains only one coordinates equal to one and the rest are zero as belongs to only one region . It follows that the second term on the right hand-side of (21) is equal to zero since

As a result, the estimator reduces to

| (22) |

Several regression tree algorithms may be used to obtain the set of non-overlapping regions of . One popular algorithm is the CART algorithm suggested by Breiman, (1984). The CART algorithm recursively searches for the splitting variable and the splitting position (i.e., the coordinates on the predictor space where to split) leading to the greatest possible reduction of the residual mean of squares before and after the splitting. More specifically, let be a region or node and let be the number of units falling in A split in consists in finding a pair where is the variable coordinate, whose value lies between and and denotes the position of the split along the th coordinate, within the limits of Let be set of all possible pairs in . The splitting process is performed by searching for the best split in the following sense:

where is the measure of -th variable for the th individual, , with the th coordinate of is the mean of for those units such that . The splitting algorithm stops when an additional split in a cell would cause the subsequent terminal nodes to have less than observations. Also, the algorithm ensures that the maximum number of units is less that in each terminal node. The tree model-assisted estimator suggested by McConville and Toth, (2019) is based on a different regression tree algorithm, but both share many properties since the splitting criterion has a limited impact on the theoretical properties of the resulting model-assisted estimators.

To establish the consistency of given by (21), we need the following additional assumption:

(H6) We assume that , with .

Assumption (H4.1) (Toth and Eltinge,, 2011) requires the sample data to be regular (i.e. without extreme observations). This means that the partition has a decreasing influence on the probability that two elements belong to the sample. The reader is referred to Toth and Eltinge, (2011), McConville and Toth, (2019) and Dagdoug et al., (2020) for more details about this assumption.

We show below that the tree-based model-assisted is design-consistent by using the analogy between linear regression and regression trees and adapting the proof of Robinson and Särndal to a high-dimensional setting, which is different from the method used by McConville and Toth, (2019).

Result 4.1.

It is worth pointing out that Result 4.1 holds for a broader class of algorithms, namely any regression tree where the splitting criterion requires a minimal number of elements in each terminal node. When there is no minimal number of element in each terminal node, the estimator may be unstable and additional assumptions would be needed.

4.2 Model-assisted estimators based on random forests

While regression trees are simple to interpret, their predictive performances are often criticized. If the number of elements in each terminal node is too small, the predictions may suffer from a high-model variance. When the number of observations in each terminal node is large, the model variance decreases but the model bias increases. Random forests (Breiman,, 2001) have been suggested to improve on the efficiency of regression trees. Random forests are widely recognized for their predictive performances in a wide variety of scenarios. In a survey sampling framework, Dagdoug et al., (2020) studied the properties of model-assisted estimators based on random forests.

Random forests is an ensemble method based on randomized regression trees. A predictor is said to be randomized if there exists a random variable such that . In other words, a randomized predictor is a predictor which may use a random variable to yield its prediction; the reader is referred to Dagdoug et al., (2020) and Biau et al., (2008) for more details. There exist several random forests algorithms which either differ in the way the regression trees are built or in the type of randomization they use. We now describe the random forest algorithm suggested by Breiman, (2001).

Let be random variables used to randomize the regression trees. The main steps of the algorithm can be summarized as follows:

-

Step 1:

Consider B bootstrap data sets by selecting pairs from with replacement.

-

Step 2:

On each bootstrap data set for fit a regression tree and determine the prediction of the unknown regression function from model (2). For each regression tree, only variables randomly chosen among the variables are considered to search for the best split in (4.1). Typical values of include and A stopping criterion is also used for obtaining the terminal nodes of each of the trees. For example, the splitting algorithm stops when a minimum number of units is reached in each terminal node.

-

Step 3:

The predicted value at is obtained by averaging the predictions at the point from each of the regression trees:

(23)

The random forest model-assisted estimator of is obtained by plugging in (3), which leads to

| (24) |

where is given by (23).

Result 4.2.

Proof.

Dagdoug et al., (2020) noted that the model-assisted estimator given by (24) can also be viewed as a bagged estimator

where

is a model-assisted estimator of based on the -th stochastic regression tree. Since

the results follows from noting that the model-assisted estimator is design-consistent for the total see Result 4.1. ∎

5 Simulation study

In this section, we provide an empirical comparison of several model-assisted estimators. In addition to the estimators discussed in Sections 3 and 4, we have included model-assisted estimators based on least angle regression (Efron et al.,, 2004), principal component regression, -nearest neighbors, XGBoost (Chen and Guestrin,, 2016) and Cubist (Quinlan et al.,, 1992). For a description of these methods, see Hastie et al., (2011) and Dagdoug et al., (2021) and the references therein.

We used data from the Irish Commission for Energy Regulation (CER) Smart Metering Project that was conducted in 2009-2010 (CER, 2011)111The data are available on request at: https://www.ucd.ie/issda/data/commissionforenergyregulationcer/. (Cardot et al.,, 2017). This project focused on energy consumption and energy regulation. About 6000 smart meters were installed to collect the electricity consumption of Irish residential and business customers every half an hour over a period of about two years.

We considered a period of consecutive days and a population of smart meters (households and companies). Each day consisted of 48 measurements, leading to 672 measurements for each household. We denote by the electricity consumption (in kW) at instant and by the value of recorded by the th smart meter for It should be noted that the matrix was ill-conditioned with a condition number equal to . This suggests that some of the -variables were highly correlated with each other.

We generated four survey variables based on these auxiliary variables according to the following models:

where denotes the empirical variance and the errors in the model for were generated from an and these errors were centered so as to obtain a mean equal to zero.

Our goal was to estimate the population totals From the population, we selected samples, of size which corresponds to a sampling fraction of about 10%. We considered two sampling schemes: simple random sampling without replacement and stratified sampling with both optimal allocation and proportional allocation.

In each sample, we computed twelve model-assisted estimators of the form

where the predictors , were obtained using the following procedures:

-

Procedure 1:

"LR" : Deterministic linear regression, leading to the GREG estimator.

- Procedure 2:

-

Procedure 3:

"RF": Random forests with the algorithm of Breiman, (2001) with trees, a minimal number of elements in each terminal node and , where denotes the customary floor function. The algorithm leads to the estimator described in Dagdoug et al., (2020). Simulations were implemented with the -package ranger.

-

Procedure 4:

"Ridge": Ridge regression with a regularization parameter determined by cross-validation and implemented with the -package glmnet. The estimator was studied by Goga and Shehzad, (2010).

-

Procedure 5:

"Lasso": Lasso regression with a regularization parameter determined by cross-validation and implemented with the -package glmnet (McConville et al.,, 2017).

-

Procedure 6:

"EN": Elastic net regression with penalization coefficients determined by cross-validation with the -package glmnet.

-

Procedure 7:

"XGB": XGBoost algorithm (Hastie et al.,, 2011) with trees in the additive model, each tree being with a depth of at most and a learning rate . Simulations were implemented with the -package XGBoost.

-

Procedure 8:

"5NN": -nearest neighbors predictor with the euclidean distance and implemented with the -package caret.

- Procedure 9:

-

Procedure 10:

"PCR1": Principal component regression based on the first components kept and implemented with the -package pls (Cardot et al.,, 2017).

-

Procedure 11:

"PCR2": Principal component regression based on the first components kept.

-

Procedure 12:

"PCR3": Principal component regression based on the first components kept.

As a measure of bias of the model-assisted estimators , , we computed the Monte Carlo percent relative bias defined as

where denotes the estimator at the th iteration, . As a measure of efficiency, we computed the relative of efficiency, using the Horvitz-Thompson estimator given by (1), as the reference. That is,

where and is defined similarly.

We were also interested in investigating to which extent the model-assisted estimators were affected by the inclusion of a large number of predictors in the working models. To that end, in addition to the variables - we included predictors in the working models. These predictors were available in the Irish data set. We used the following values for : 5, 10, 20, 50, 100, 200, 300 and 400.

5.1 Simple random sampling without replacement

In this section, we present the results obtained under simple random sampling without replacement (SRSWOR) of size . All the point estimators exhibited a negligible or small percent RB with a maximum value of about (obtained in the case of the GREG estimator). For this reason, results pertaining to relative bias are not reported here.

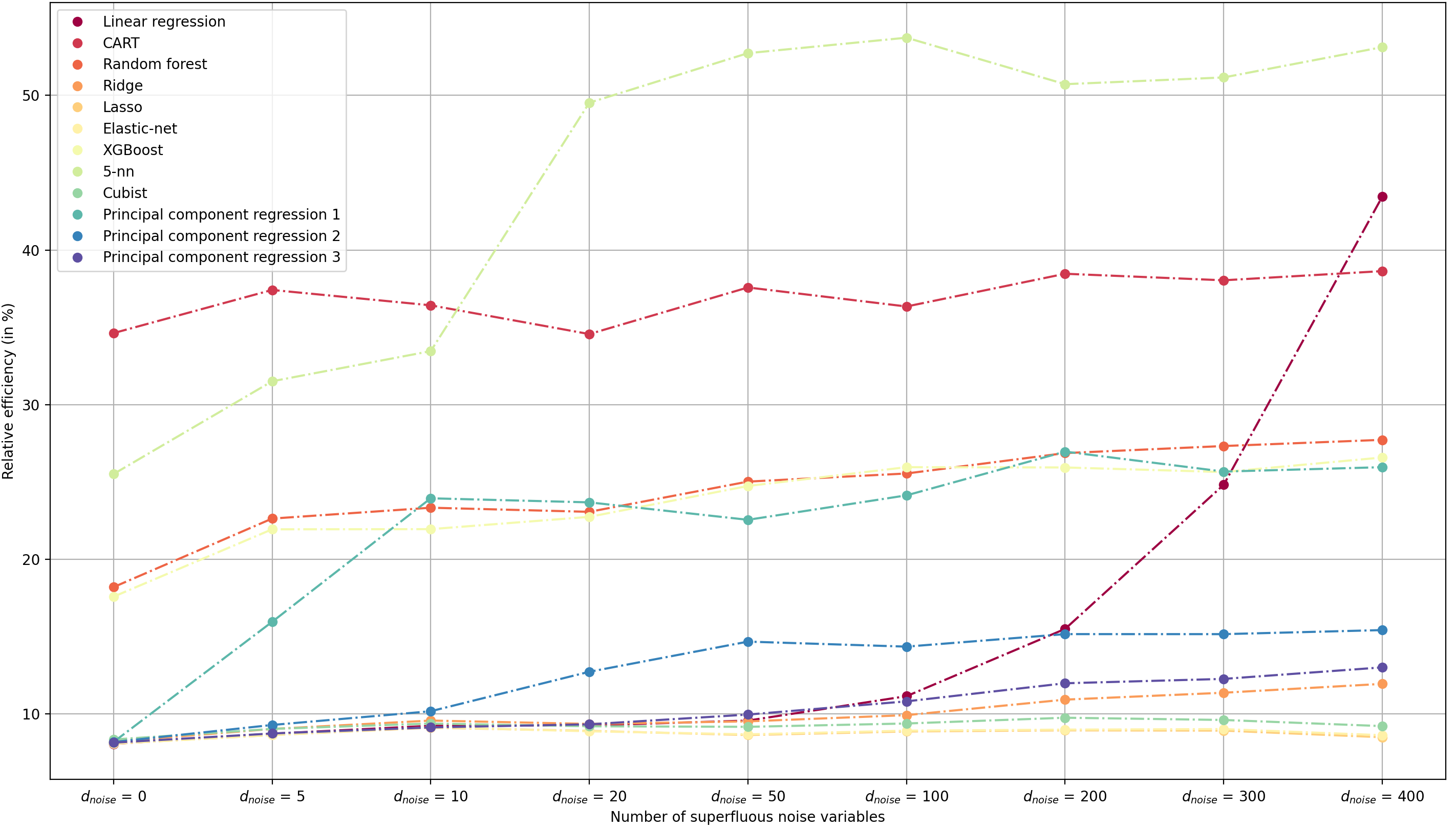

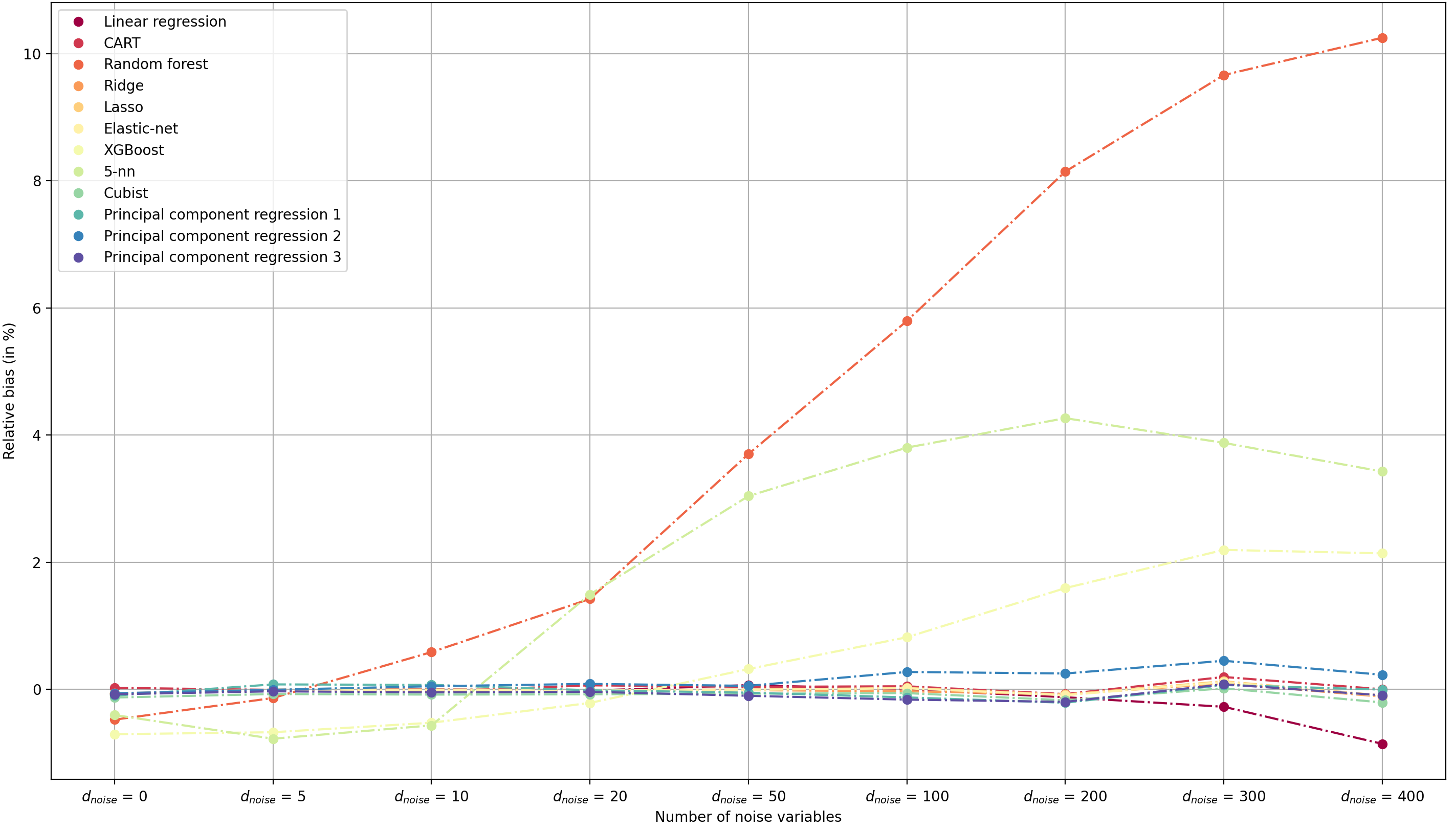

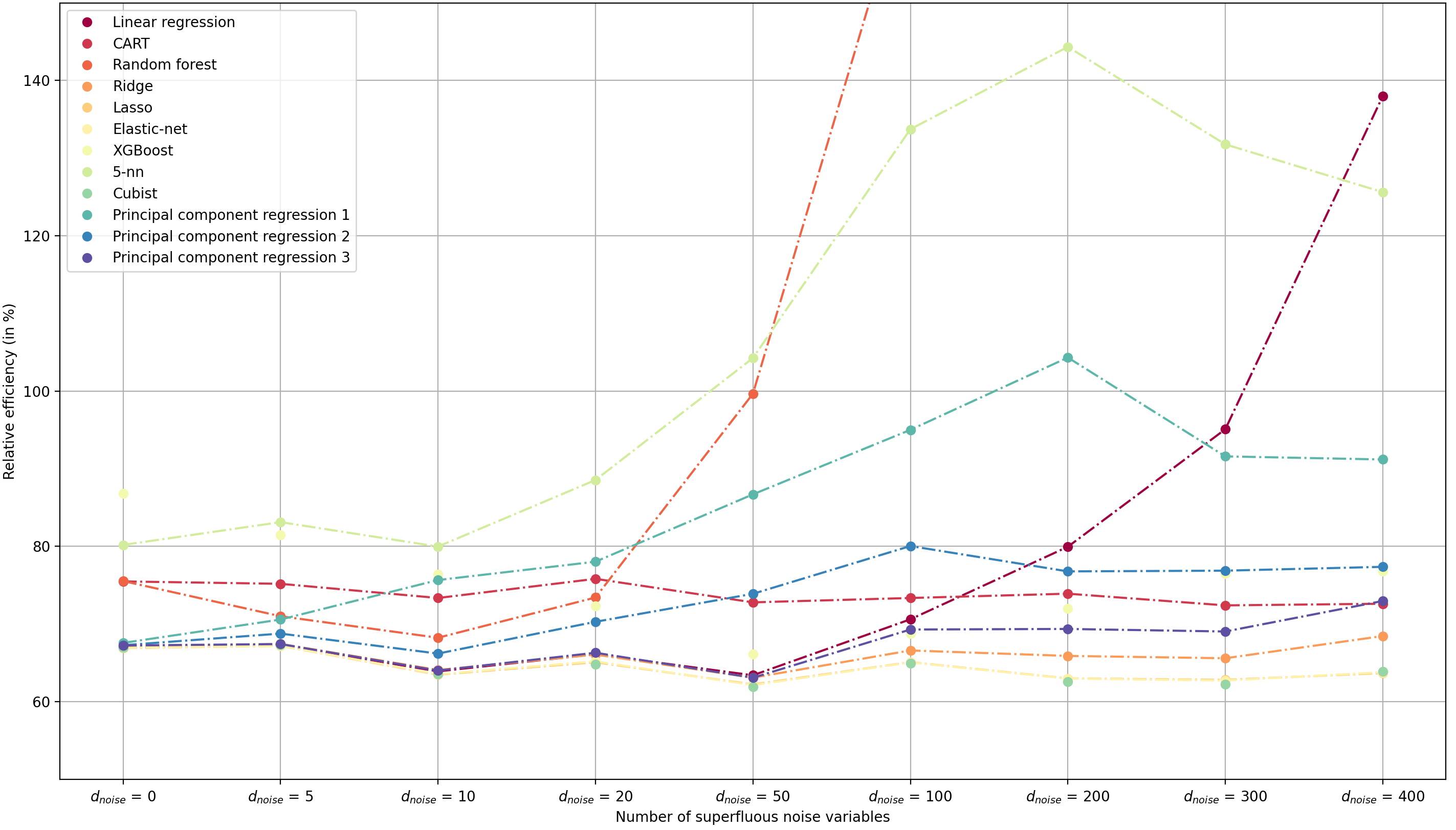

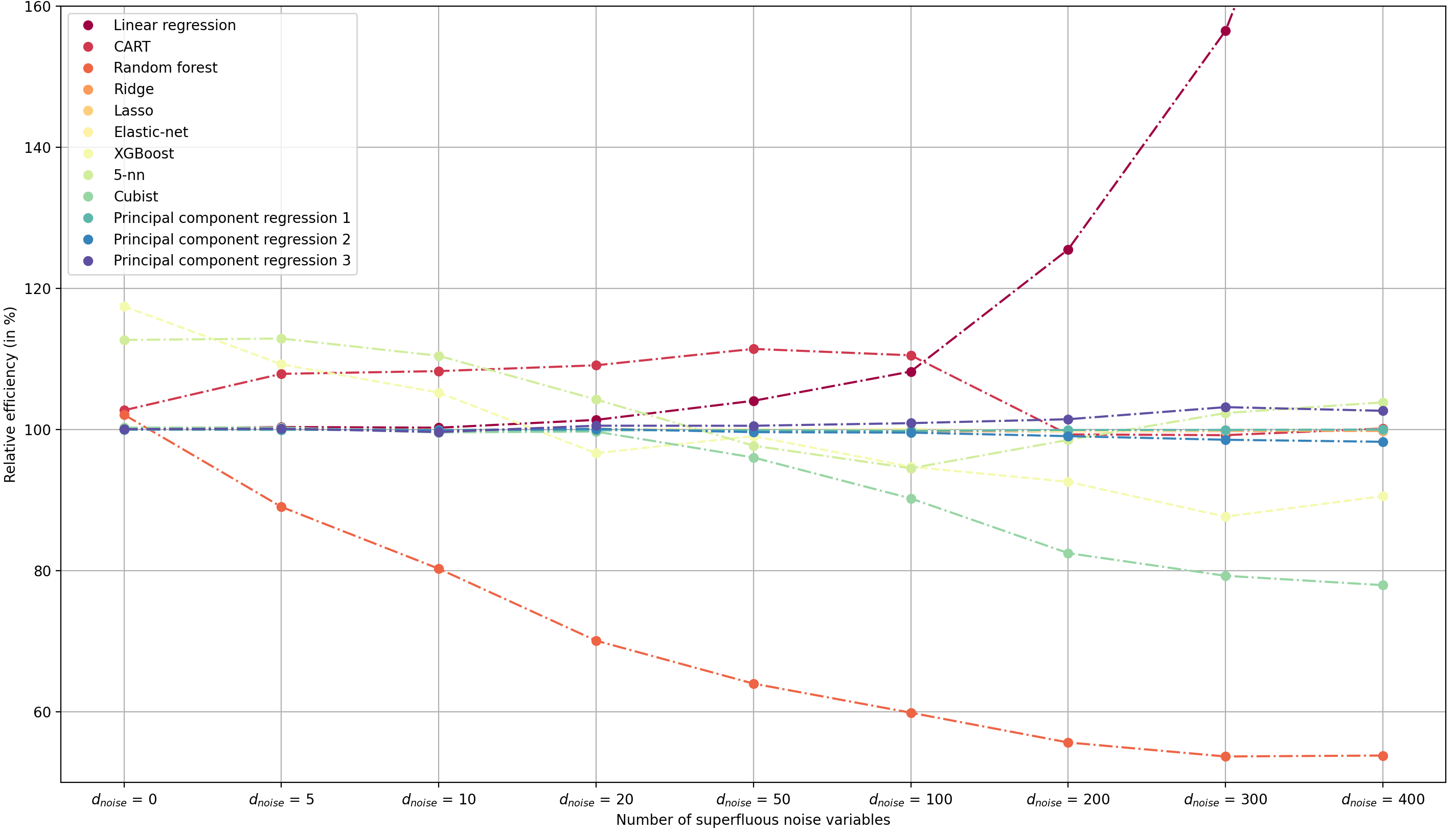

Figures 1-4 display the relative efficiency of the model-assisted estimators as a function of the number of auxiliary variables incorporated in the working models. To improve readability, we have truncated some large values of RE, when applicable.

We begin by discussing the results on relative efficiency pertaining to the estimation of the total of the survey variable . For low-dimensional settings, the GREG estimator was very efficient with values of RE below . These results can be explained by the fact that was linearly related to the -variables. However, as the number of variables increased, the efficiency of the GREG estimator rapidly deteriorated, suggesting that the performance of the GREG estimator is sensitive to the dimension of the -vector. As expected, model-assisted estimators based on regularization methods such as ridge, lasso, elastic-net or dimension reduction methods such as principal components regression, performed generally very well. Unlike the GREG, these estimators were not much affected by the number of auxiliary variables incorporated in the model. Turning to the model-assisted estimator based on a -nn, we note that it was less efficient than most competitors and that its efficiency got worse as increased, a phenomenon referred to as the curse of dimensionality. The model-estimators based on XGBoost, Cubist and random forests performed quite well and did not seem to be affected by the number of auxiliary variables incorporated in the model. Finally, the estimators based on CART were less efficient than those obtained through the other machine learning methods.

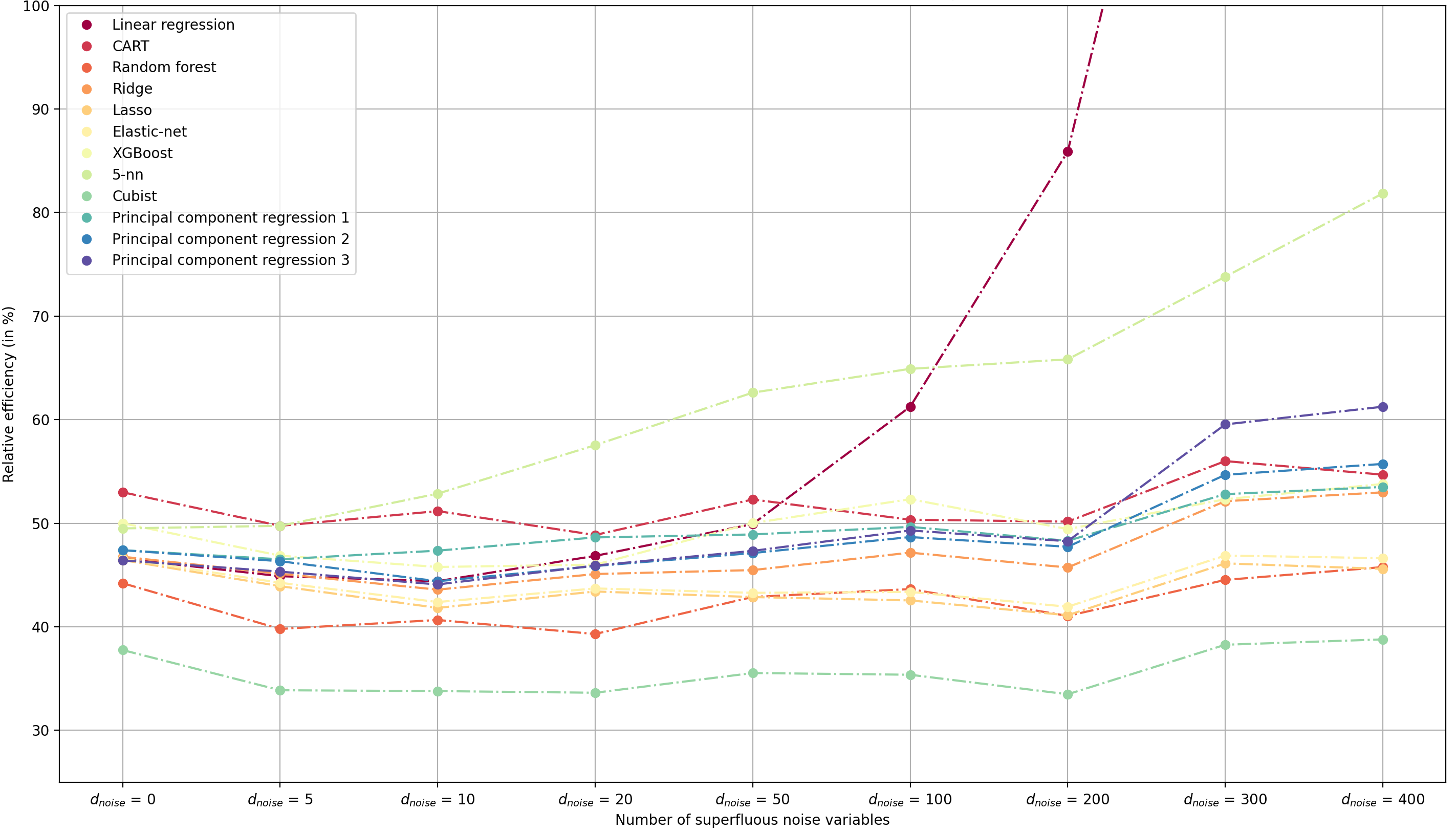

The results pertaining to the survey variable and displayed in Figure 2 were fairly consistent with those obtained for the survey variable with one exception: the Cubist algorithm was significantly more efficient than the other procedures in all the scenarios.

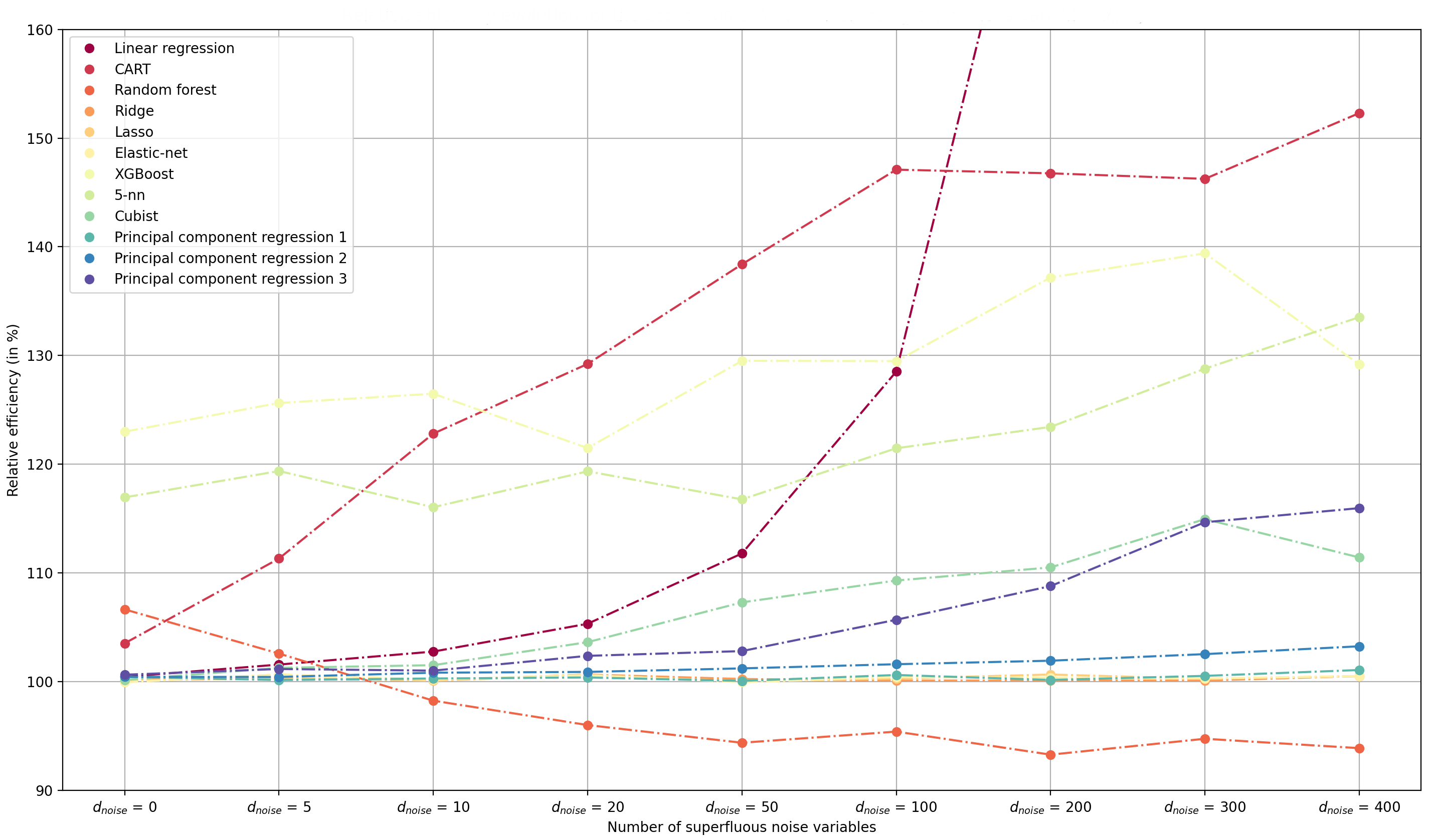

Turning to the survey variable (see Figure 3), the model-assisted estimator based on random forests was significantly more efficient than the Horvitz–Thompson estimator, especially for large values of . The other procedures led to estimators less efficient than the Horvitz-Thompson estimator with values of RE above . In particular, the GREG estimator broke down as the number of auxiliary variable increased. The performance of model-assisted estimators based on CART and XGBoost algorithms deteriorated as the dimension increased. In a high-dimension setting with highly correlated predictors, random forests improved over CART due to the random subsampling of variables among the variables, generating then decorrelated trees (Hastie et al.,, 2011).

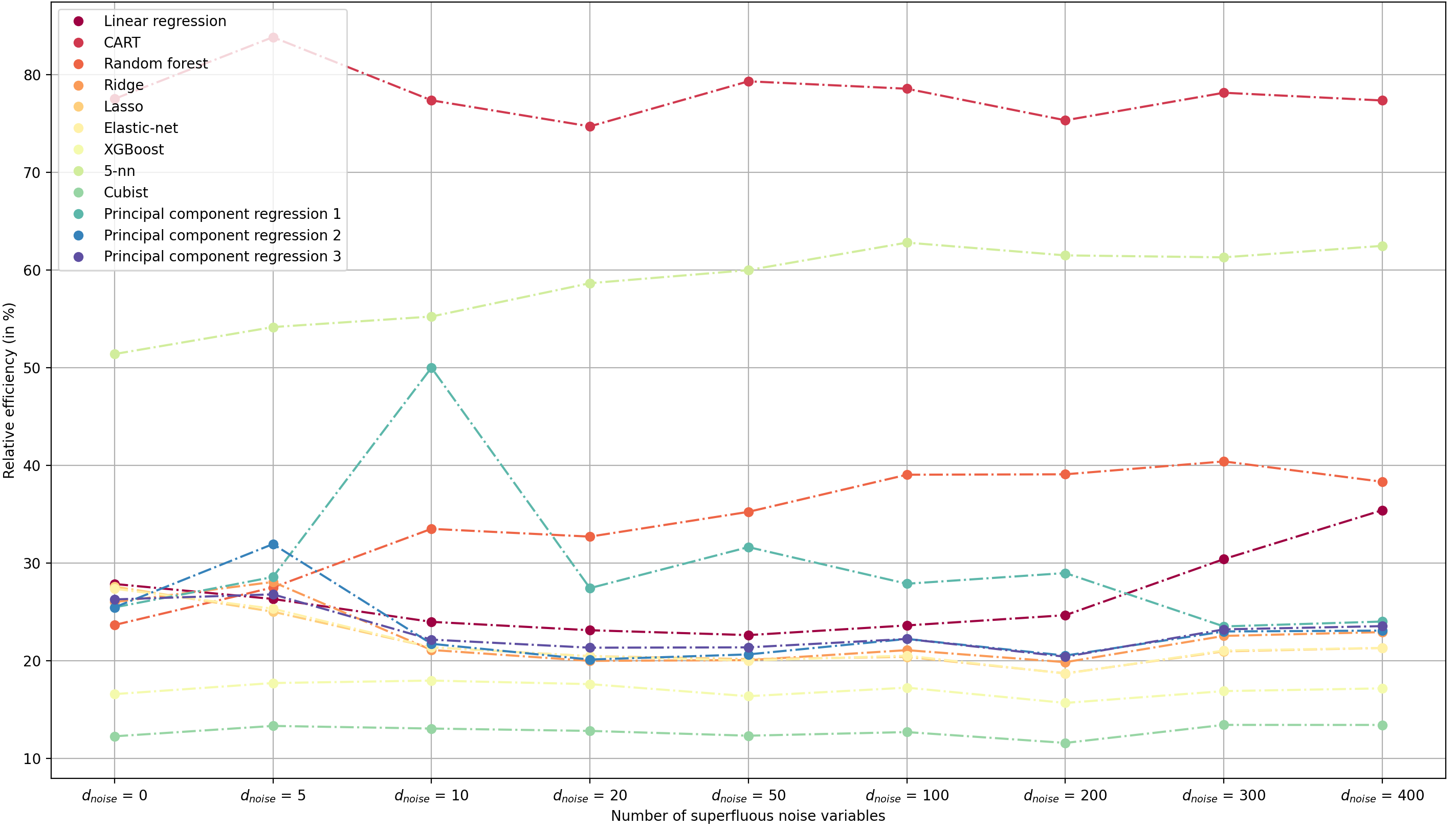

The results in Figure 4 about the survey variable were similar to the ones in previous figures. Most estimators remained mostly unaffected by the number of auxiliary variables . Again, the model-assisted estimator based on the Cubist algorithm was the best in all the scenarios.

5.2 Stratified simple random sampling with optimal allocation

In the second simulation study, we partitioned the Irish residential and business customer population into four strata using an equal quantile method with respect to the variable, the electricity consumption at instant From the population, we selected stratified simple random samples, of size The stratum sample sizes were determined using an -optimal allocation, where denotes the electricity consumption recorded at instant This led to and The first-order inclusion probabilities, and the sampling weights are shown in Table 1.

| Stratum | 1 | 2 | 3 | 4 |

|---|---|---|---|---|

| 0.012 | 0.022 | 0.028 | 0.316 | |

| 77.85 | 43.83 | 35.11 | 3.16 |

We confined to the survey variables and only and we aimed at estimating and . It is worth pointing out that the resulting sampling design was informative as the variables used at the design stage ( and ) were also related to the survey variables and . In fact, the Monte Carlo coefficient of correlation between the sampling weights and was approximately equal to We do not report the coefficient of correlation between between the sampling weights and as the relationship between and the set of predictors is not linear.

Again, in each sample we computed twelve model-assisted estimators for each of and Since most machine learning software packages do not take the sampling weights into account, we have included the design variables and in the set of predictors.

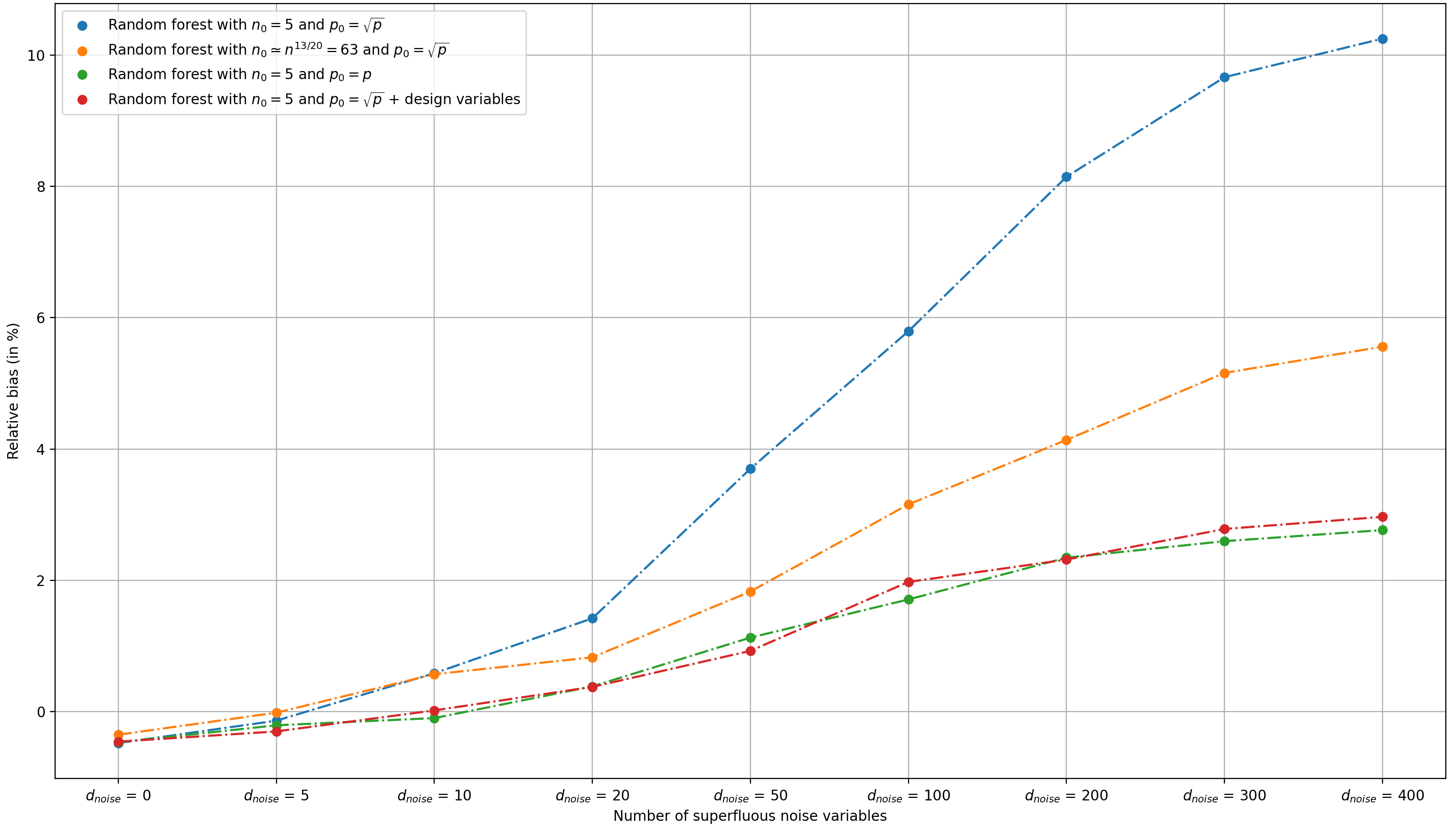

We begin by discussing the results pertaining to the estimation of the total of the survey variable Figure 5 and Figure 6 display the Monte Carlo percent relative bias and the Monte Carlo relative efficiency as a function of the number of variables . Except for the model-assisted estimators based on -nn and random forest, the other estimators exhibit a small value of RB for all values of . Again, the -nn model-assisted estimator suffered from the curse of dimensionality. Turning to the estimator based on random forests, we note from Figure 5 that the bias increased as the number of predictors increased. For instance, for the value of RB was just above 10%. This significant bias may be explained by the fact that random forests is the only procedure among the ones considered in our simulation that randomly selects variables among the initial predictors at each split. For instance, for , only 20 variables are randomly selected at each split. As a result, most predictions obtained trough a random forests algorithm were based on misspecified working models, leading to potentially bad fits and large residuals. Also, each prediction corresponds to a weighted mean computed within each node with observations only. Therefore, each predictions corresponds to a ratio-type estimate based on 5 observations only. This, together with the fact that the sampling weights are highly variable, constitutes a conducive ground for the occurrence of small sample bias. In terms of efficiency, except for the GREG, the -nn and the random forest estimators, the other procedures performed well with values of RE ranging from 60% to 80%. The best procedures were Cubist and Lasso.

We now turn to the survey variable First, the Monte Carlo relative bias was negligible for all the estimation procedures and are not reported here. Results about relative efficiency are plotted in Figure 7. Random forests performed extremely well and their performance improved as increased. This suggests that the method was able to extract the information contained in the predictors. This was also true for Cubist and XGBoost, although to a lesser extent.

To get a better understanding of the performance of random forests for the survey variable we conducted additional scenarios based on different values of the hyper parameters the number of observations within each terminal nodes, and the number of variables randomly selected at each split among the initial model variables. We used the following values for and :

-

•

observations and variables which are the default choices in the -package rangers;

-

•

observations and variables;

-

•

observations and variables and the stratification variable was selected with probability 1, at each split, besides the variables;

-

•

observations and variables.

The Monte Carlo percent relative bias is displayed in Figure 8. We note that relative bias was much smaller when all the predictors were considered at each split or if the stratification variables were considered besides variables at each split. Moreover, the bias decreased when more observations were allowed in each terminal node. These results suggest, that, in order to avoid significant small sample bias, we recommend to use more observations in each terminal nodes and/or to avoid the randomization in the process of growing trees and/or to force the design variables to be selected at each split. The latter option is available in the package ranger.

5.3 Stratified sampling with proportional allocation

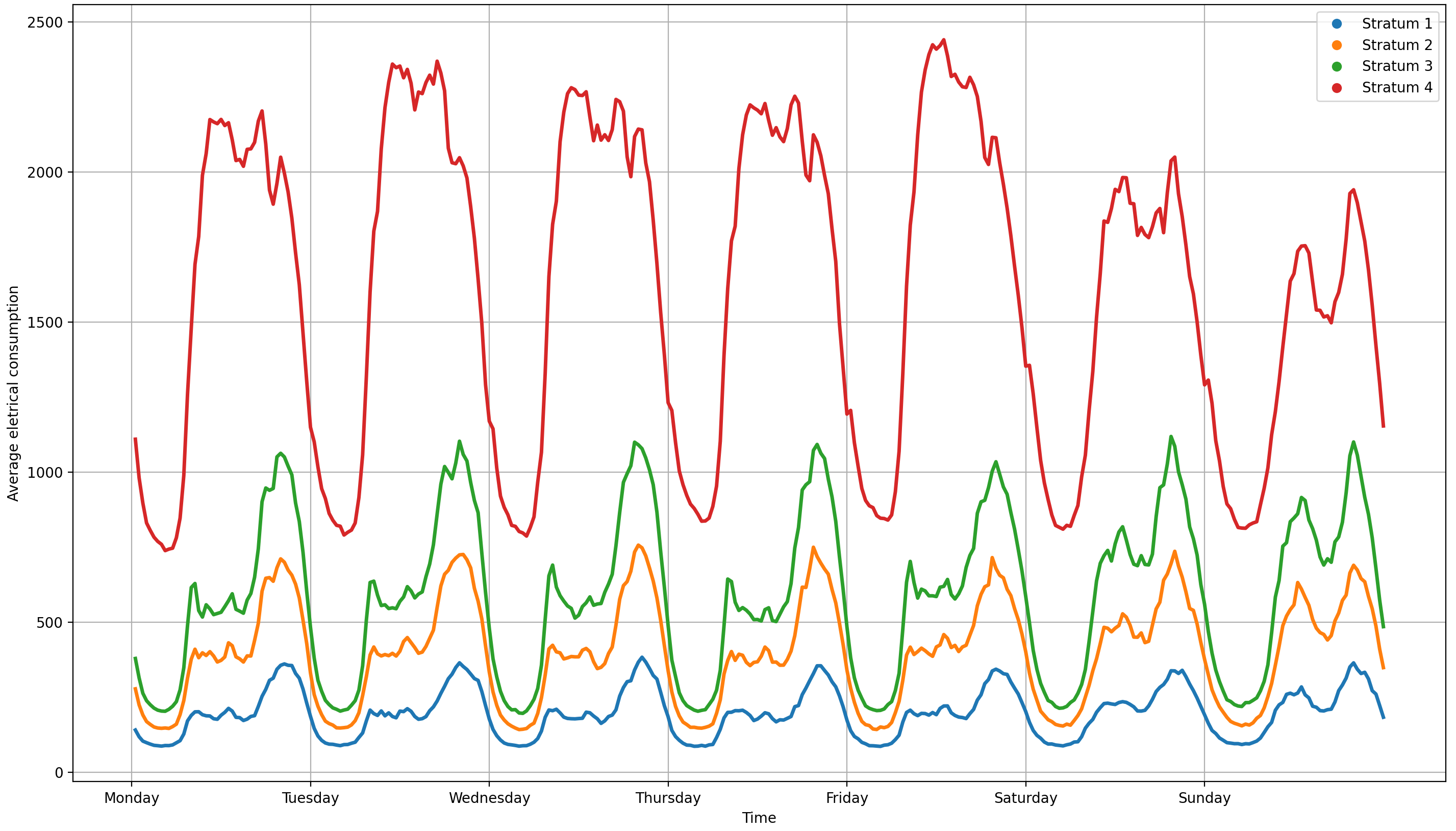

In this section, we consider a more realistic scenario based again on the Irish residential and business customer data. As a stratification variable, we used the mean electricity consumption recorded during the first week. Again, we constructed four strata using an equal-quantile method based, this time, on the mean electricity consumption; see also Cardot et al., (2013) who used a similar design. The mean trajectories during the first week within each stratum are plotted in Figure 9. From Figure 9, we note that Stratum 1 corresponds to consumers with low global levels of electricity consumption, whereas Stratum 4 consists of consumers who have high levels of electricity consumption.

Our aim was to estimate the total electricity consumption recorded on the Monday of the second week and given by where is the electricity consumption recorded for the -th unit at the -th instant. Within each stratum, we selected a sample, of size according to simple random sampling without replacement. The ’s were determined according to proportional allocation; i.e, with . In each of the 2,500 samples, we computed the same 12 model-assisted estimators as in the previous sections. Again, we computed the Monte Carlo percent relative bias and the relative efficiency for each the 12 estimators. The results are presented in Table 2.

| Estimator | Relative bias | Relative efficiency | ||

|---|---|---|---|---|

| LR | 0.2 | 9.3 | ||

| CART | -0.1 | 41.0 | ||

| RF | -1.1 | 17.0 | ||

| Ridge | 0.1 | 4.0 | ||

| Lasso | 0.2 | 4.1 | ||

| EN | 0.2 | 4.1 | ||

| XGB | -1.7 | 24.9 | ||

| NN5 | -4.0 | 65.6 | ||

| Cubist | -0.0 | 4.3 | ||

| PCR1 | 0.1 | 4.9 | ||

| PCR2 | 0.1 | 4.2 | ||

| PCR3 | 0.1 | 4.2 |

From Table 2, we note that the -nn model-assisted estimator was the only estimator to exhibit a non-negligible bias. Although it was less efficient than its competitors, it was more efficient than the Horvitz-Thompson estimator with a value of RE of about . The ridge estimator was the most efficient with a value of RE equal to and was closely followed by lasso, elastic-net, Cubist and principal components model-assisted estimators. The GREG estimator performed very well with a value of RE of about 9.3%. Random forests led to considerable improvement over the CART model-assisted estimator with values of RE of 17% and 41%, respectively. Still, random forests were less efficient than the GREG estimator, which is not surprising as the relationship between the survey variable and the auxiliary variables was linear.

6 Final remarks

In this paper, we have examined a number of model-assisted estimation procedures in a high-dimensional setting both theoretically and empirically. If the relationship between the survey variable and the auxiliary information can be well described by a linear model, our results suggest that penalized estimators such as ridge, lasso and elastic net perform very well in terms of bias and efficiency, even in the case . Model-assisted estimators based on random forests, Cubist and XGBoost methods were mostly unaffected by the number of predictors incorporated in the working model, even in the case of complex relationships between the study and the auxiliary variables. As expected, the GREG estimator suffered from poor performances in the case of a large number of auxiliary variables.

The procedure Cubist stood out from the other machine learning procedure with very good performances in virtually all the scenarios. Further work is needed to establish the theoretical properties of model-assisted estimators based on Cubist in both a low-dimensional and high-dimensional settings.

Variance estimation is an important stage of the estimation process. Further research includes identifying the regularity conditions under which the variance estimators are design-consistent in a high-dimensional setting.

We end this article by mentioning that virtually all the machine learning software packages cannot handle design features such as unequal weights and stratification. For instance, some random forests algorithms may involve a bootstrapping procedure and/or a cross-validation procedure. To fully account for the sampling design, both procedures must be modified so as to account for the design features. Not fully accounting for the sampling design may be viewed as a form of model misspecification. However, model-assisted estimation procedures remain design-consistent even if the model is misspecified. In our experiments, several machine learning procedures (e.g., random forests, Cubist, XGboost) performed very well in most scenarios even though we did not modify the bootstrapping and cross-validation procedures to account for design features. In other words, it seems that, accounting for predictors that are highly predictive of the -variable, seems to be the preponderant factor with respect the to efficiency aspect of model-assisted estimators. We conjecture that, fully accounting for the sampling design, will likely lead to additional efficiency gains but that the predictive power of the model likely constitutes the "determining factor". Developing machine learning procedures that fully account for the sampling design is currently under investigation.

Acknowledgment

We thank the Editor, an Associate Editor, and two referees for their comments and suggestions, which helped improving the paper substantially. We are very grateful to Professor Patrick Tardivel from the Université de Bourgogne for enlightening discussions about the lasso method. The work of Mehdi Dagdoug was supported by grants of the Franche-Comté region and Médiamétrie. The work of David Haziza was supported by a grant of the Natural Sciences and Engineering Research Council of Canada.

References

- Bardsley and Chambers, (1984) Bardsley, P. and Chambers, R. (1984). Multipurpose estimation from unbalanced samples. Applied Statistics, 33:290–299.

- Beaumont and Bocci, (2008) Beaumont, J.-F. and Bocci, C. (2008). Another look at ridge calibration. Metron-International Journal of Statistics, LXVI:260–262.

- Biau et al., (2008) Biau, G., Devroye, L., and Lugosi, G. (2008). Consistency of random forests and other averaging classifiers. Journal of Machine Learning Research, 9:2015–2033.

- Breidt et al., (2005) Breidt, F., Claeskens, G., and Opsomer, J. (2005). Model-assisted estimation for complex surveys using penalized splines. Biometrika, 92:831–846.

- Breidt and Opsomer, (2000) Breidt, F.-J. and Opsomer, J.-D. (2000). Local polynomial regression estimators in survey sampling. The Annals of Statistics, 28:1023–1053.

- Breiman, (1984) Breiman, L. (1984). Classification and regression trees. Routledge.

- Breiman, (2001) Breiman, L. (2001). Random forests. Machine learning, 45:5–32.

- Cardot et al., (2013) Cardot, H., Dessertaine, A., Goga, C., Josserand, E., and Lardin, P. (2013). Comparison of different sample designs and construction of confidence bands to estimate the mean of functional data : an illustration on ellectricity consumption. Survey Methodology, 39(2):283–301.

- Cardot et al., (2017) Cardot, H., Goga, C., and Shehzad, M.-A. (2017). Calibration and partial calibration on principal components when the number of auxiliary variables is large. Statistica Sinica, 27(243-260).

- Chambers, (1996) Chambers, R. (1996). Robust case-weighting for multipurpose establishment surveys. Journal of Official Statistics, 12:3–32.

- Chen and Guestrin, (2016) Chen, T. and Guestrin, C. (2016). XGBoost. In Proceedings of the 22nd ACM SIGKDD International Conference on Knowledge Discovery and Data Mining - KDD 16. ACM Press.

- Dagdoug et al., (2020) Dagdoug, M., Goga, C., and Haziza, D. (2020). Model-assisted estimation through random forests in finite population sampling. arXiv preprint arXiv:2002.09736.

- Dagdoug et al., (2021) Dagdoug, M., Goga, C., and Haziza, D. (2021). Imputation procedures in surveys using nonparametric and machine learning methods: an empirical comparison. Journal of Survey Statistics and Methodology, to appear.

- Deville and Särndal, (1992) Deville, J.-C. and Särndal, C.-E. (1992). Calibration estimators in survey sampling. Journal of the American Statistical Association, 87:376–382.

- Efron et al., (2004) Efron, B., Hastie, T., Johnstone, I., Tibshirani, R., et al. (2004). Least angle regression. The Annals of statistics, 32:407–499.

- Firth and Bennett, (1998) Firth, D. and Bennett, K. (1998). Robust models in probability sampling. Journal of the Royal Statistical Society: Series B, 60:3–21.

- Goga, (2005) Goga, C. (2005). Réduction de la variance dans les sondages en présence d’information auxiliaire: une approche non paramétrique par splines de régression. The Canadian Journal of Statistics, 33:163–180.

- Goga and Ruiz-Gazen, (2014) Goga, C. and Ruiz-Gazen, A. (2014). Efficient estimation of non-linear finite population parameters by using non-parametrics. Journal of the Royal Statistical Society: Series B, 76:113–140.

- Goga and Shehzad, (2010) Goga, C. and Shehzad, M. A. (2010). Overview of ridge regression estimators in survey sampling. Université de Bourgogne: Dijon, France.

- Györfi et al., (2006) Györfi, L., Kohler, M., Krzyzak, A., and Walk, H. (2006). A distribution-free theory of nonparametric regression. Springer Science & Business Media.

- Hastie et al., (2011) Hastie, T., Tibshirani, R., and Friedman, J. (2011). The Elements of Statistical Learning: Data Mining, Inference and Prediction. Springer, New York.

- Hoerl and Kennard, (1970) Hoerl, A. E. and Kennard, R. W. (1970). Ridge regression: biased estimation for nonorthogonal problems. Technometrics, 12:55–67.

- Hoerl and Kennard, (2000) Hoerl, A. E. and Kennard, R. W. (2000). Ridge regression: Biased estimation for nonorthogonal problems. Journal of the American Statistical Association, 42:80–86.

- Horvitz and Thompson, (1952) Horvitz, D. and Thompson, D. (1952). A generalization of sampling without replacement from a finite universe. Journal of the American Statistical Association, 47:663–685.

- Isaki and Fuller, (1982) Isaki, C.-T. and Fuller, W.-A. (1982). Survey design under the regression superpopulation model. Journal of the American Statistical Association, 77:49–61.

- Kuhn and Johnson, (2013) Kuhn, M. and Johnson, K. (2013). Applied predictive modelling. Springer.

- Lehtonen and Veijanen, (1998) Lehtonen, R. and Veijanen, A. (1998). Logistic generalized regression estimators. Survey Methodology, 24:51–56.

- McConville and Breidt, (2013) McConville, K. and Breidt, F. J. (2013). Survey design asymptotics for the model-assisted penalised spline regression estimator. Journal of Nonparametric Regression, 25:745–763.

- McConville and Toth, (2019) McConville, K. and Toth, D. (2019). Automated selection of post-strata using a model-assisted regression tree estimator. Scandinavian Journal of Statistics, 46:389–413.

- McConville et al., (2017) McConville, K. S., Breidt, F. J., Lee, T. C., and Moisen, G. G. (2017). Model-assisted survey regression estimation with the lasso. Journal of Survey Statistics and Methodology, 5:131–158.

- Montanari and Ranalli, (2005) Montanari, G. E. and Ranalli, M. G. (2005). Nonparametric model calibration in survey sampling. Journal of the American Statistical Association, 100:1429–1442.

- Opsomer et al., (2007) Opsomer, J. D., Breidt, F. J., Moisen, G., and Kauermann, G. (2007). Model-assisted estimation of forest resources with generalized additive models. Journal of the American Statistical Association, (478):400–409.

- Quinlan et al., (1992) Quinlan, J. et al. (1992). Learning with continuous classes. In 5th Australian joint conference on artificial intelligence, volume 92, pages 343–348. World Scientific.

- Rao and Singh, (1997) Rao, J. and Singh, A. C. (1997). A ridge-shrinkage method for range-restricted weight calibration in survey sampling. In Proceedings of the Section on Survey Research Methods, American Statistical Association.

- Robinson and Särndal, (1983) Robinson, P. M. and Särndal, C.-E. (1983). Asymptotic properties of the generalized regression estimator in probability sampling. Sankhyā Series B, 45:240–248.

- Särndal, (1980) Särndal, C.-E. (1980). On the -inverse weighting best linear unbiased weighting in probability sampling. Biometrika, 67:639–650.

- Särndal et al., (1992) Särndal, C.-E., Swensson, B., and Wretman, J. (1992). Model assisted survey sampling. Springer Series in Statistics. Springer-Verlag, New York.

- Särndal and Wright, (1984) Särndal, C.-E. and Wright, R. (1984). Cosmetic form of estimators in survey sampling. Scandinavian Journal of Statistics, 11:146–156.

- Ta et al., (2020) Ta, T., Shao, J., Li, Q., and Wang, L. (2020). Generalized regression estimators with high-dimensional covariates. Statistica Sinica.

- Tibshirani, (1996) Tibshirani, R. (1996). Regression shrinkage and selection via the lasso. Journal of the Royal Statistical Society: Series B, 58(1):267–288.

- Toth and Eltinge, (2011) Toth, D. and Eltinge, J. L. (2011). Building consistent regression trees from complex sample data. Journal of the American Statistical Association, 106:1626–1636.

- Wang and Wang, (2011) Wang, L. and Wang, S. (2011). Nonparametric additive modelassisted estimation for survey data. Journal of Multivariate Analysis, 102:1126–1140.

- Zou and Hastie, (2005) Zou, H. and Hastie, T. (2005). Regularization and variable selection via the elastic net. Journal of the royal statistical society: series B, 67:301–320.

Appendix

Proof of Result 3.1

We adapt the proof of Robinson and Särndal, (1983) to a high-dimensional setting. Let be the sample membership indicator for unit such that if and otherwise. Let for all . We consider the following decomposition:

| (25) |

where for Now, the first term does not depend on the auxiliary information and we have (Robinson and Särndal,, 1983; Breidt and Opsomer,, 2000):

| (26) |

We have and for by Assumption (H3.3). It follows from (H3.3), (H3.3) and (H3.3) that

| (27) |

and so,

| (28) |

Now, consider the second term from the right-side of (25):

| (29) |

By Assumption (H3.3), we have that Furthermore,

and

| (30) |

by Assumptions (H3.3)-(H3.3). It follows that

| (31) |

The result follows by using (25), (28), (29), (31) and Assumption (H3.3):

Proof of Result 3.2

From the proof of result (3.1), we only need to show that or where is one of the penalized regression coefficient: ridge, lasso and elastic-net.

Consider first the ridge regression coefficient, The ridge regression estimator has the advantage of having an explicit expression. We will show that for Let denote sample counterpart of Moreover, let be the eigenvalues of in decreasing order and the orthonormal corresponding eigenvectors, Then, the eigenvalues of the matrix are with the same eigenvectors Using the same arguments as those used in Hoerl and Kennard, (1970), we obtain and Let denote by then

It follows that and we get

We now consider the lasso regression estimator, which minimizes the design-based version of the optimization problem given in (13):

The lasso-estimator may be also obtained as the solution of a constrained optimization problem:

under the constraint

for some small enough constant If the ordinary least-square estimator satisfies the constraint, namely if then the solution of the constrained optimization problem is otherwise, if then the solution will be different from the least-square estimator and So, in both cases, we have

Finally, consider the elastic-net regression estimator, Consider the following objective functions:

where and with and The cases and lead, respectively, to the ridge and lasso regression estimators which have been discussed above. The ordinary least squares estimator verifies and the elastic-net estimator verifies . Since minimizes , we have . Similarly, we have . Therefore, the following inequalities hold:

which implies

| (32) |

Furthermore, since , we can write

| (33) |

Using (32), (33) and the fact that we obtain

which implies

and so,

Proof of Result 3.3

-

1.

As in the proof of result (3.2), we consider the eigenvalues of the matrix in decreasing order: . The matrix is always invertible and the eigenvalues of are We then obtain

(34) where is the spectral norm matrix defined for a squared matrix as For a symmetric and positive definite matrix , we have that where is the largest eigenvalue of Now, we can write

where The symmetric and positive semi-definite matrix has the same non-null eigenvalues as those of the positive definite matrix . Therefore,

Using Assumptions (H3.3) and (H3.3), we have

Finally, using also the fact that we have

It follows that

(35) -

2.

We can write

(36) where with Using the same arguments as those used in the proof of Result 3.1, we get

(37) Furthermore,

(38) by Assumptions (H3.3) and (H3.3) and the fact that

(39) To obtain the above inequality, we have also used the fact that which can be proved by using the same arguments as the ones used for showing that in point (1). Expressions (37) and (38) lead to

(40) The result follows from (36), (40) and the fact that

(41) - 3.

Proof of Proposition 3.1

From the proof of Result 3.1 (more specifically, Equations 29 and 30), we need to show that and that . The same result holds for and We have under the assumption of uniformly bounded forth moment of

We first show that, under the assumed orthogonality condition, , and also

Consider again the objective function as in the proof of Result 3.2. We can write

| (42) |

where and for all Let The columns of denoted by are assumed to be orthogonal. This means that for The ordinary least-square estimator is given by

Under the orthogonality condition, is a diagonal matrix with diagonal elements given by which corresponds to the Horvitz-Thompson estimator of Therefore, and the -th coordinate is given by

The lasso estimator as well as the elastic-net estimator are obtained by using the cyclic soft-thresholding algorithm (Hastie et al.,, 2011):

and

where and is the soft-thresholding function with if and zero otherwise. If the columns of are orthogonal, then and is the soft-threshold estimator of the least-square estimator :

The elastic-net estimator is given by

It follows that

and Similarly,

Proof of Result 4.1

Again, we use the decomposition (25) as in the proof of Result 3.1:

where with for We have

| (44) |

We obtain from the proof of Result 3.1, (see Equation (27)) that

| (45) |

Now, consider the second term on the right-side of (44). We have

| (46) |

We show first that

| (47) |

We have

and since the matrix is diagonal with diagonal elements equal to for all by the stopping criterion and not depending on the sampling design. Moreover, we get following the same lines as in the proofs of result (3.3) or proposition (3.1):

using Assumption (H3.3) and the fact that the matrix is diagonal with diagonal elements equal to for all by the stopping criterion. therefore, Finally, we obtain

Now,

| (48) |

The first term on the right hand-side of (48) can be bounded as follows:

| (49) |

where the -dimensional vector with contains only one non-null value, so for all Turning to the second on from the right-side of (48), we have where . By Assumption (H3.3), there exists a positive quantity such that Then,

by Assumptions (H3.3)-(H4.1) and the fact that for all From (48), (49) and (LABEL:Bv_tree_mixte), it follows that

which, combined with (47) in (46), leads to

| (51) |

Finally, from (44), (45) and (51) we get that