Multi-market Oligopoly of Equal Capacity

Abstract

We consider a variant of Cournot competition, where multiple firms allocate the same amount of resource across multiple markets. We prove that the game has a unique pure-strategy Nash equilibrium (NE), which is symmetric and is characterized by the maximal point of a “potential function”. The NE is globally asymptotically stable under the gradient adjustment process, and is not socially optimal in general. An application is in transportation, where drivers allocate time over a street network.

keywords:

Cournot oligopoly; multi-market; multi-product; capacity constraint; learning; Lyapunov function[usc] organization=Department of Civil and Environmental Engineering, University of Southern California, city=Los Angeles, state=CA, postcode=90089, country=USA

[samsi] organization=The Statistical and Applied Mathematical Sciences Institute, city=Durham, state=NC, postcode=27703, country=USA

1 Introduction

Cournot oligopoly is a classic model of economic competition, see [32] for a modern game-theoretic review of oligopoly theory. Selten [30] introduced multiproduct oligopoly models, see also [3, 13]. A similar term is multimarket oligopoly, which often involves transportation cost among spatially separated markets. Besides studying the existence and uniqueness of Nash equilibrium, it is also important to understand the stability of the equilibrium under different dynamic adjustment processes. For a multiproduct oligopoly model, [33] gave sufficient and necessary conditions for the locally stability of equilibrium under best-response dynamics.

The discussion is more difficult in the presence of capacity constraints. Okuguchi and Szidarovszky [25] studied the equilibrium and dynamics of multiproduct oligopoly with capacity constraints. In particular, for asymmetric firms with compact, convex capacities such that their payoffs are concave, they showed that Nash equilibrium exists. If the equilibrium is unique, they provided sufficient conditions for its global asymptotic stability under a dynamic process, where players adjust strategies proportionally to their expected marginal profit, given their expectations of the total output of opponents (also known as expectations a la Cournot) [25, Thm 6.4.2, 6.4.3]. Their used Lyapunov functions to prove dynamic stability. Laye and Laye [20] proved the uniqueness of equilibrium if the demand functions are linear and the cost functions are convex, because the game is equivalent to a convex optimization problem. Other forms of capacity constraints have been discussed, such as transmission capacity constraints [11] or capacity constraints across multiple time period [5, 16]. More papers deal with two-period duopoly using mixed strategy equilibrium [4, 6].

In this paper we consider multimarket oligopoly with capacity constraints and symmetric firms. Unlike [20], we allow for concave production functions, which gives non-increasing demand functions. A situation where symmetry arises is when the players allocate time across different markets. Consider a fishery that gives out license for fishing. All fishermen receive standard device so that, all things being equal, they have no difference in productivity. Fish abundance differs spatially at the fishery, so the fishermen can strategize on their allocation of time at different locations. Another example is the taxi industry, where drivers search on a street network for passengers [34, 35]. For such a multimarket oligopoly, we study its Nash equilibrium of the static game, its stability under dynamic processes, and its economic efficiency.

The rest of this paper is organized as follows. In Section 2, we define multi-market oligopoly of equal capacity. In Section 3, we prove that the game has a unique, symmetric Nash equilibrium. In Section 4, we prove that the NE is globally asymptotically stable under the gradient adjustment process, and discuss other learning rules. In Section 5, we discuss when the NE is socially optimal or not, and conclude with a takeaway.

2 Game Setup

In this section we formalize the game of multi-market competition among firms of equal capacity, denoted as . For the convention of notations, we use subscript for an individual firm (or player), subscript for the opponents of firm , and subscript to denote a market (or product). Boldface denotes a vector. Single subscript indicates summation.

Player strategy. Let be a set of firms and be a set of markets. Each firm has a unit of resource, and allocates amount of resource in a market so that . The strategy of a firm is the vector of resource distribution , which is in its strategy space . Here, is the -dimensional simplex. Denote strategy profile , considered as a vector of length . Denote strategy space .

Production functions. The total revenue in a market depends on the total resource allocated in the market. Without loss of generality, for each , let and .

Player payoff. Assume that revenue in each market is distributed proportionally to resource allocation, and all players have the same cost function , where . Because player payoff is the total revenue a player gets from all the markets minus the cost, it can be written as:

| (1) |

Here, is the revenue per investment in a market, defined by ; and is the aggregate strategy of the opponents. Note that . Denote the aggregate strategy space of the opponents as , then .

Auxiliary functions. With aggregate strategy , define marginal player payoff in a market at equilibrium and potential function :

| (2) | ||||

| (3) |

Here, is the partial derivative operator with respect to the -th variable. Note that .

We impose the following assumption on function forms.

Assumption 1.

For all , is concave and differentiable; is convex and differentiable; at least either all but one are strictly concave or is strictly convex.

Note that this assumption is quite generic. Because of the law of diminishing returns, production functions are usually concave, and cost functions are usually convex. We require differentiability so that is well-defined. The strict concavity or convexity requirement is easy to satisfy as well. For example, [35] shows that the expected revenue as a function of vehicle supply on a street segment is increasing, strictly concave, and smooth. Given this assumption, it is easy to see that is (decreasing) non-increasing. Notice that we use parentheses for optional conditions that strengthen a statement. We adopt this convention throughout this paper for a tighter presentation.

Multi-market oligopoly of equal capacity is defined as the game , where payoffs , such that Assumption 1 hold. Later we will see that, unlike the Cournot game, it is not an aggregative game [30] or even a generalized aggregative game [17, 10]. It is also not a strictly convex game [27] or a potential game [23], although it could be considered as a Lyapunov game [8]. In the following sections we derive equilibrium and stability results without referencing these classes of games.

3 Equilibrium

In this section we prove that the game has a unique pure-strategy Nash equilibrium (NE), which is symmetric and is characterized by the unique maximal point of the potential function. We follow a list of propositions and then give the main result. Before getting into the details, we point out the keys to the proofs: convex game guarantees that NE exists; equal capacity leads to symmetry; and strictly concave potential function gives a unique solution.

Proposition 1.

is strictly concave, .

Proof.

Because simplex is a convex subset of the non-negative cone , if is strictly concave on , , then is also strictly concave on , . It suffices to prove the former statement without constraints on opponent strategies, that is, is strictly concave on , . By Equation 1 and Assumption 1, it suffices to show that is (strictly) concave on , . To simplify notations, it is equivalent to show that is (strictly) concave on , . Proof by definition is straightforward but tedious, so we do not include the steps here. The key to this proof is that is (strictly) concave and is (decreasing) non-increasing. Strict concavity is guaranteed if any or is strictly concave/convex. This proves Proposition 1. ∎

Proposition 2.

has NE, all strict.

Proof.

By Proposition 1, is a convex game, which is a game where each player has a convex strategy space and a concave payoff function for all opponent strategies. A convex game has NE if it has a compact strategy space and continuous payoff functions [24]. Because a finite product of simplices is compact, the strategy space is compact. Because and are differentiable by Assumption 1, player payoff is differentiable and thus continuous. Therefore, has NE. Since is strictly concave, all NEs are strict. This proves Proposition 2. ∎

Proposition 3.

can only have symmetric NE.

Proof.

Given a NE , for all player , the equilibrium strategy solves the following optimization problem, which is convex by Proposition 1:

| maximize | (4) | |||||

| subject to | ||||||

Since this convex optimization problem is strictly feasible, by Slater’s theorem, it has strong duality. Since the objective function is differentiable, the Karush-Kuhn-Tucker (KKT) theorem states that optimal points of the optimization problem is the same with the solutions of the KKT conditions:

| (saddle point) | (5) | |||||

| (primal constraint 1) | ||||||

| (dual constraint) | ||||||

| (complementary slackness) | ||||||

| (primal constraint 2) |

Here, operator denotes the Hadamard product: . Given the saddle point conditions , the dual constraint implies that the marginal payoff for player in market is bounded above: . If player invests in market , , by complementary slackness the upper bound is tight, , which means the marginal payoffs for player are uniform in all markets where invests. From Equation 1, marginal player payoffs have the form:

| (6) |

Since , we have , with equality if . If player invests more in market than player does, , this implies

| (7) |

But because the players have the same capacity, player must have invested less in some market than player does: , which implies

| (8) |

Denote , , and . For all , multiply to Equation 7. For all , multiply to Equation 8. Sum these inequalities together and note that , we have:

| (9) |

If all but one are strictly concave, then all but one are nonzero. Since at least two entries of are nonzero, this means that the first term in Equation 9 is positive. Note that the second term can be written as . If is strictly convex, then equivalently , , which means and therefore the second term is positive. By Assumption 1, the left-hand side of Equation 9 is positive, which is a contradiction. Therefore all players must have the same strategy in equilibrium. This proves Proposition 3. ∎

Proposition 4.

is strictly concave.

Proof.

Let . Since is a differentiable real function with a convex domain, it is (strictly) concave if and only if it is globally (strictly) dominated by its linear expansions: , . This is true because is (decreasing) non-increasing. Because is also (strictly) concave, is (strictly) concave. Therefore, the first term of in Equation 3 is (strictly) concave on the non-negative cone . Because the simplex is a convex subset of , the first term of is also (strictly) concave on . By Assumption 1, is strictly concave. This proves Proposition 4. ∎

Theorem 1.

has a unique NE, which is symmetric and the aggregate strategy maximizes .

Proof.

From Propositions 2 and 3, has NE, which are symmetric. For a symmetric NE with aggregate strategy , we have player strategy , and marginal player payoffs in invested markets are the same for all players: . Note that . Summing up Equation 5 for all , and let , we see that satisfies:

| (saddle point) | (10) | |||||

| (primal constraint 1) | ||||||

| (dual constraint) | ||||||

| (complementary slackness) | ||||||

| (primal constraint 2) |

Since the potential function has a compact domain , by Proposition 4, it has a unique maximal point . By the KKT theorem, is the solution set of the KKT conditions, which is exactly Equation 10. Therefore, . This proves Theorem 1. ∎

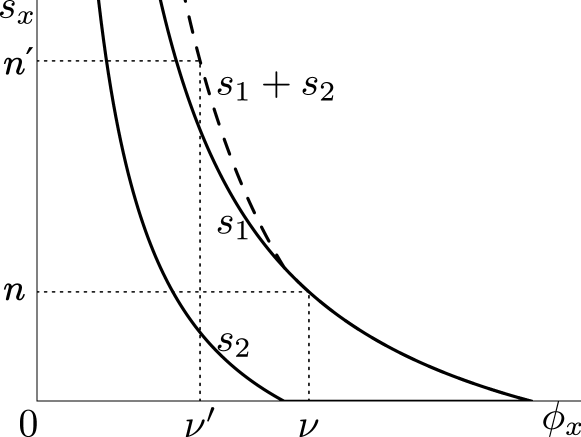

Embedded in the proof is a procedure to find the NE, which is to optimize . Here we give better insight into this procedure, for the case where the cost function is separable: . Since is a uni-variate differentiable (strictly) concave function, is (decreasing) non-increasing. Because and is also (decreasing) non-increasing, is (decreasing) non-increasing. Define inverse function , so that for . The function is non-increasing, and decreasing for . Then the equilibrium satisfies:

| (11) |

Since total investment equals the number of players, , marginal player payoff in invested markets is determined by:

| (12) |

Because the left-hand side of Equation 12 is decreasing for where the left-hand side is positive, the equation gives a unique solution . Thus, Equation 11 gives a unique . Figure 1 shows this process graphically.

4 Stability and Learning

In this section we prove the global asymptotic stability of the NE under a myopic learning rule called the gradient adjustment process, and discuss player learning of the NE under other dynamics. The gradient adjustment process [1] is a heuristic learning rule where players adjust their strategies according to the local gradient of their payoff functions, projected onto the tangent cone of player strategy space. Formally, gradient adjustment process is a dynamical system:

| (13) |

Here denotes the gradient with respect to player strategy , is the tangent cone of player strategy space at point , and is the projection operator. For all interior points of , is simply the centering matrix: .

Assumption 2.

For all , is continuously differentiable; is quadratic.

Theorem 2.

With Assumption 2, the NE of is globally asymptotically stable under the gradient adjustment process.

Proof.

To prove that Equation 13 is globally asymptotically stable, we show that the following function is a global Lyapunov function of the dynamical system, i.e. a function that is positive-definite, continuously differentiable, and has negative-definite time derivative:

| (14) |

Here, is the symmetrized strategy profile.

Since is the unique maximal point of , this means with equality only at , so is positive-definite. We add a regularization term , which equals zero when and is positive otherwise. Because , we have , with equality only at . Therefore, is positive-definite.

Note that . With Assumption 2, every is continuous, so is continuously differentiable with respect to . With some derivation, we have , which is apparently continuous. Therefore, is continuously differentiable.

To simplify discussion, let be an interior point of , and we study the dynamics of and separately. With Equation 13, the time derivative of is:

With Equation 6, we have . With Assumption 2, the cost function can be written as , where is a positive semi-definite matrix. Note that any linear term can be normalized into the production functions , which becomes . Since is linear, we have , and therefore . Now we have:

Here, and . Thus, , with equality if and only if all are equal. If this is the case, let , where is a constant. Then Equation 10 is satisfied where and . Therefore . So , with equality only at .

Similarly, the time derivative of is:

Note that does not depend on , and , so the last term in the above equation can be dropped. With Equation 6, we have:

Note that does not depend on , and , so in the above equation can be dropped. The term with expands to , which is non-positive because , and it equals zero when for all . The term with simplifies to . Note that , this is equal to , which is non-positive because , and it equals zero when for all . With Assumption 1, is non-positive and equals zero only when for all , that is, . Together with the result on , we have , with equality only at , so is negative-definite in the interior of .

If is a boundary point of , we can drop those where . With the same argument, we have , with equality only at . Therefore, the time derivative is negative-definite. We have thus shown that is a global Lyapunov function of the dynamical system, which immediately implies Theorem 2. ∎

From the proof we see that, during the gradient adjustment process, the potential function is increasing as long as the aggregate strategy differs from that of the NE, and the regularization term is decreasing as long as the strategy profile is not symmetric. In other words, this myopic dynamics simultaneously pushes the player strategies to be more similar to each other and pushes the aggregate strategy towards the equilibrium.

The stability result in Theorem 2 is only intended to show that under a simple and plausible learning rule, global asymptotic stability of Nash equilibrium is possible in , so that the equilibrium can be empirically observed given real-world perturbations to the competition. The gradient adjustment process adopted in this paper is not meant to be the exact learning rule used in real life, which is hard to determine. But compared with Bayesian or best-response learning rules, it is less demanding on the players as it only requires instantaneous local information instead of complete information of the game or long-term memory of the players. And even if some players adopt alternative, non-economic learning rules, the stability of the equilibrium may well be preserved. For example, some players may simply choose imitative learning [28, 14]; in other words, new players copy the more experienced players, and less successful players copy the more successful ones. In this case the Nash equilibrium is still the stable focus as all players adopt the same strategy and the rational payoff-improving players adjust to the equilibrium. By imitative learning, newcomers save the possibly long process of strategy adjustment and quickly converge to the equilibrium strategy. This allows the equilibrium remain stable under an evolving set of players.

We note that the payoff in is not diagonally strictly concave, which is much stronger than Proposition 1, so the uniqueness and stability results cannot follow [27]. But the eigenvalues of the Jacobian are always negative, so local asymptotic stability at the equilibrium is guaranteed under gradient dynamics with individual-specific adjustment speeds. We also note that unlike the Cournot game, is not an aggregative game defined in [30] or later generalizations [17, 10], because player strategies are multi-dimensional. Thus it does not inherit the stability under discrete-time best-response dynamics. It is also not a potential game and thus does not inherit the general dynamic stability properties in [23]. Instead, we provided a “potential function” that is a global Lyapunov function for the gradient dynamics.

5 The Problem of Social Cost

In this section we show that the Nash equilibrium of is not socially optimal in general, and conclude with a takeaway message and hint at a possible fix. A socially optimal strategy profile maximizes the total income , while per Theorem 1 the equilibrium maximizes the potential function . Since , total income is generally not maximized at the NE, thus not socially optimal. In fact, if total income is maximized, marginal income should be the same for all invested markets of all players. Instead, at NE, is the same for all invested markets. By Equation 2, includes the marginal cost at equilibrium and a weighted average of marginal and average revenue, with more weight on average revenue as the number of players increases. This difference implies an inefficiency of the NE in general.

However, the NE can be socially optimal given special forms of . For example, if market revenues are power functions of the same order: , then total payoff and player payoff . At social optimum, is a constant for all markets . Since , social optimal strategy is . Let . At Nash equilibrium, is a constant for all markets and all players. This means is a constant for all markets, which gives an aggregate strategy where . Note that , so the NE is socially optimal in this case.

This phenomenon of difference between cooperative and competitive decisions has been studied for a long time under different names. Economic inefficiency [22, 31] refers to a situation where total income, or social wealth, is not maximized. The problem of social cost [26, 18] is the divergence between private and social costs or value. Later developments include external effect [21], rent dissipation [15], market failure [2], transaction cost [9], and price of anarchy [19, 29]. [9] dismissed the discussion of social cost, calling the reduced social income as transaction cost. Externality evolved out of external effect, whose proponents typically call for government regulation, see [12]. Institution cost is a generalization of transaction cost, see [7]. Algorithmic game theory uses price of anarchy [19, 29] and price of stability for this inefficiency of equilibria.

Despite the various terminology, the essence of the problem is the same: when individuals do not have incentive to maximize the total income, equilibrium naturally will differ from the optimum set, which by definition results in less total revenue. Here we propose the main takeaway in the case of multi-market oligopoly of equal capacity: if a property is heterogeneous in productivity, the owner cannot obtain the optimal rent by leasing to multiple tenants without contracting on their allocation of effort.

Acknowledgments

The authors thank Ketan Savla, Sami F. Masri, Juan Carrillo, Matthew Kahn, Hashem Pesaran, and Geert Ridder of USC for helpful comments. Research is funded by the National Science Foundation (NSF) Grant 14-524 and, in part, by NSF Grant DMS-1638521.

References

- Arrow and Hurwicz [1960] Arrow, K.J., Hurwicz, L., 1960. Stability of the gradient process in n-person games. Journal of the Society for Industrial and Applied Mathematics 8, 280–294. URL: http://www.jstor.org/stable/2098966.

- Bator [1958] Bator, F.M., 1958. The anatomy of market failure. Quarterly Journal of Economics 72, 351. doi:10.2307/1882231.

- Baumol et al. [1982] Baumol, W.J., Panzar, J.C., Willig, R.D., 1982. Contestable Markets and the Theory of Industry Structure. Harcourt College Pub.

- van den Berg et al. [2012] van den Berg, A., Bos, I., Herings, P.J.J., Peters, H., 2012. Dynamic cournot duopoly with intertemporal capacity constraints. International Journal of Industrial Organization 30, 174–192. doi:10.1016/j.ijindorg.2011.08.002.

- Besanko and Doraszelski [2004] Besanko, D., Doraszelski, U., 2004. Capacity dynamics and endogenous asymmetries in firm size. The RAND Journal of Economics 35, 23–49. doi:10.2307/1593728.

- Chen et al. [2015] Chen, Y.H., Nie, P.Y., Wang, X.H., 2015. Asymmetric doupoly competition with innovation spillover and input constraints. Journal of Business Economics and Management 16, 1124–1139. doi:10.3846/16111699.2013.823104.

- Cheung [1998] Cheung, S.N., 1998. The transaction costs paradigm: 1998 presidential address western economic association. Economic Inquiry 36, 514–521. doi:10.1111/j.1465-7295.1998.tb01733.x.

- Clempner [2018] Clempner, J.B., 2018. On lyapunov game theory equilibrium: Static and dynamic approaches. International Game Theory Review 20, 1750033. doi:10.1142/s0219198917500335.

- Coase [1960] Coase, R.H., 1960. The problem of social cost. Journal of Law and Economics 3, 1–44. doi:10.1086/466560.

- Cornes and Hartley [2012] Cornes, R., Hartley, R., 2012. Fully aggregative games. Economics Letters 116, 631–633. doi:10.1016/j.econlet.2012.06.024.

- Cunningham et al. [2002] Cunningham, L.B., Baldick, R., Baughman, M.L., 2002. An empirical study of applied game theory: transmission constrained cournot behavior. IEEE Transactions on Power Systems 17, 166–172.

- Davis and Whinston [1962] Davis, O.A., Whinston, A., 1962. Externalities, welfare, and the theory of games. Journal of Political Economy 70, 241–262. doi:10.1086/258637.

- De Fraja [1996] De Fraja, G., 1996. Product line competition in vertically differentiated markets. International Journal of Industrial Organization 14, 389–414. doi:10.1016/0167-7187(95)00483-1.

- Fudenberg and Levine [2009] Fudenberg, D., Levine, D.K., 2009. Learning and equilibrium. Annual Review of Economics 1, 385–420. doi:10.1146/annurev.economics.050708.142930.

- Gordon [1954] Gordon, H.S., 1954. The economic theory of a common-property resource: the fishery. Journal of Political Economy 62, 124–142.

- Ishibashi [2008] Ishibashi, I., 2008. Collusive price leadership with capacity constraints. International Journal of Industrial Organization 26, 704–715. doi:10.1016/j.ijindorg.2007.01.007.

- Jensen [2010] Jensen, M.K., 2010. Aggregative games and best-reply potentials. Economic Theory 43, 45–66. doi:10.1007/s00199-008-0419-8.

- Knight [1924] Knight, F.H., 1924. Some fallacies in the interpretation of social cost. Quarterly Journal of Economics 38, 582–606. URL: http://qje.oxfordjournals.org/content/38/4/582.full.pdf+html.

- Koutsoupias and Papadimitriou [1999] Koutsoupias, E., Papadimitriou, C., 1999. Worst-case equilibria, in: STACS 99. Springer Berlin Heidelberg, pp. 404–413. doi:10.1007/3-540-49116-3_38.

- Laye and Laye [2008] Laye, J., Laye, M., 2008. Uniqueness and characterization of capacity constrained cournot-nash equilibrium. Operations Research Letters 36, 168–172. doi:10.1016/j.orl.2007.05.008.

- Meade [1952] Meade, J.E., 1952. External economies and diseconomies in a competitive situation. Economic Journal 62, 54. doi:10.2307/2227173.

- Mill [1859] Mill, J.S., 1859. On liberty. J. W. Parker and Son.

- Monderer and Shapley [1996] Monderer, D., Shapley, L.S., 1996. Potential games. Games and Economic Behavior 14, 124–143. doi:10.1006/game.1996.0044.

- Nikaido and Isoda [1955] Nikaido, H., Isoda, K., 1955. Note on non-cooperative convex games. Pacific Journal of Mathematics 5, 807–815. URL: http://projecteuclid.org/euclid.pjm/1171984836.

- Okuguchi and Szidarovszky [1999] Okuguchi, K., Szidarovszky, F., 1999. The Theory of Oligopoly with Multi-Product Firms. 2nd ed., Springer.

- Pigou [1920] Pigou, A.C., 1920. The economics of welfare. 1st ed., Macmillan and Co., London.

- Rosen [1965] Rosen, J.B., 1965. Existence and uniqueness of equilibrium points for concave n-person games. Econometrica 33, 520–534. URL: http://www.jstor.org/stable/1911749.

- Roth and Erev [1995] Roth, A.E., Erev, I., 1995. Learning in extensive-form games: experimental data and simple dynamic models in the intermediate term. Games and Economic Behavior 8, 164–212. doi:10.1016/S0899-8256(05)80020-X.

- Roughgarden [2002] Roughgarden, T., 2002. Selfish routing. Ph.D. thesis. Department of Computer Science, Cornell University. Ithaca, New York.

- Selten [1970] Selten, R., 1970. Preispolitik der Mehrproduktenunternehmung in der statischen Theorie. Number v. 16 in Okonometrie und Unternehmensforschung, Springer-Verlag.

- Sidgwick [1883] Sidgwick, H., 1883. Principles of political economy. Macmillan and co.

- Vives [1999] Vives, X., 1999. Oligopoly Pricing: Old Ideas and New Tools. MIT Press Ltd.

- Zhang and Zhang [1996] Zhang, A., Zhang, Y., 1996. Stability of a cournot-nash equilibrium: The multiproduct case. Journal of Mathematical Economics 26, 441–462. doi:10.1016/0304-4068(95)00760-1.

- Zhang and Ghanem [2020a] Zhang, R., Ghanem, R., 2020a. Demand, supply, and performance of street-hail taxi. IEEE Transactions on Intelligent Transportation Systems 21, 4123–4132. doi:10.1109/TITS.2019.2938762.

- Zhang and Ghanem [2020b] Zhang, R., Ghanem, R., 2020b. Drivers learn city-scale dynamic equilibrium. URL: https://arxiv.org/abs/2008.10775.