mydate\monthname[\THEMONTH] \THEYEAR

Estimation of Large Financial Covariances:

A Cross-Validation Approach111

The authors would like to thank Daniel Bartz, Zdzisław Burda, Mihai Cucuringu, Lisa Goldberg, and Andrzej Jarosz as well as seminar participants at the University of Oxford and Man AHL for the helpful comments. The authors are also grateful to Christian Bongiorno for providing research assistance and valuable feedback. This work was supported by the Oxford-Man Institute of Quantitative Finance.

This version: January 2023)

We introduce a novel covariance estimator for portfolio selection that adapts to the non-stationary or persistent heteroskedastic environments of financial time series by employing exponentially weighted averages and nonlinearly shrinking the sample eigenvalues through cross-validation. Our estimator is structure agnostic, transparent, and computationally feasible in large dimensions. By correcting the biases in the sample eigenvalues and aligning our estimator to more recent risk, we demonstrate that our estimator performs well in large dimensions against existing state-of-the-art static and dynamic covariance shrinkage estimators through simulations and with an empirical application in active portfolio management.

JEL Classification: C13, C58, G11.

Keywords: Cross-validation, exponentially weighted averages, large-dimensional statistics, nonlinear shrinkage, portfolio selection, rotation equivariance.

1 Introduction

The covariance matrix of asset returns is a central object in the portfolio selection problem of Markowitz, (1952). In practical applications, the covariance matrix is not known a priori and we have to resort to estimators. When estimating a large covariance matrix, one confronts the ‘curse of dimensionality’, where the problem size grows quadratically as the number of assets increases. This means that we need to have a long enough historical data set to produce reliable estimates of the covariances. For example, to reliably estimate a covariance matrix of assets, at least years of daily data is needed. The estimation of large numbers of risk parameters relative to the number of observations introduces the possibility of aggregating many estimation errors into a global significant error. When such a matrix is used in the context of portfolio optimization, Jobson and Korkie, (1980) and Chopra and Ziemba, (1993), among others, showed that such optimizers exhibit poor out-of-sample properties, and inevitably become what Michaud, (1989) regards as “error maximization” procedures.

To improve the estimation of a covariance matrix, it is thus imperative to reduce the effective number of risk parameters that require estimation. In finance, factor models are often employed for this purpose with early developments stemming from the single factor model of Sharpe, (1963) and its multi-factor extension in the context of the Arbitrage Pricing Theory (APT) introduced by Ross, (1976), and later generalized by Chamberlain and Rothschild, (1983). Some examples that reify the APT include the fundamental risk factor model of Fama and French, (1992) and commercial risk models that have been built and maintained by companies such as BARRA, Northfield, Axioma, and so on. What is common in these approaches is that the underlying structure of the covariance is being modeled. As a result, the estimation error is typically reduced but at the expense of increased model bias.

Another line of attack is the shrinkage principle introduced by Stein, (1956) and James and Stein, (1961) in the context of the estimation of the means. Shrinkage can be understood as a form of regularization – to use machine learning parlance – to control the effects of sampling variation, which results in overfitting. This idea was extended to covariance matrices by Haff, (1980) and Ledoit and Wolf, 2004b by taking a linear combination of a sample covariance matrix and a (scaled) identity matrix in order to produce a composite matrix that has a favorable model bias-variance trade-off. Besides the identity matrix, other types of structured target matrices considered in the literature include the constant correlation model (Ledoit and Wolf, 2004a, ), or the single factor model (Ledoit and Wolf,, 2003). However, a limitation of the linear shrinkage estimator is that it is constrained by a single common shrinkage intensity, and hence lacks the capacity to suppress further variations in the data.

A more recent and powerful approach that extends upon the linear shrinkage technology attempts to reduce the estimation error without assuming any a priori structure on the covariance. This is achieved by shrinking the eigenvalues at distinct intensities. The inception of this idea goes back to Stein, (1975, 1986) and there are two modern approaches on this front. The first is an analytical approach taken by Ledoit and Péché, (2011) and subsequently, Bun et al., (2017), where the authors utilized the tools from Random Matrix Theory in order to provide a theoretical formula for shrinking the eigenvalues. There are two possible approaches to implementing their formula: discretization (Ledoit and Wolf,, 2015) or kernel estimation (Ledoit and Wolf,, 2020, 2022). In parallel to this development, there is also a numerical scheme from Abadir et al., (2014), Lam, (2016) and Bartz, (2016), where the authors demonstrate that we can accomplish a similar shrinkage effect by means of sample splitting and cross-validation.

Most of the aforementioned developments, however, revolve around a uniformly weighted covariance matrix that weighs every observation equally. However, in finance, it is known since Mandelbrot, (1963) that financial returns exhibit certain empirical regularities such as volatility clustering. This volatility clustering effect can overwhelm our observations, which leaves us with effectively fewer observations than what we originally had because the stock returns are dominated by days with large fluctuations. Thus, the use of exponentially weighted average schemes such as RiskMetrics developed by J.P. Morgan/Reuters, (1996) and Zumbach, (2007) is arguably more relevant for non-stationary or heteroskedastic environments since it restricts the effective sample size so that more local observations are used. However, these models are also susceptible to estimation errors in large dimensions since the effective time scale used to measure the observations is smaller than the sample size.

In this paper, we introduce a simple yet effective covariance estimator that is tailored specifically to address the curse of dimensionality present in exponentially weighted average covariances. In particular, we extend the cross-validation shrinkage procedure of Abadir et al., (2014), Lam, (2016) and Bartz, (2016), towards exponentially weighted average covariances in order to robustify them against large dimensions. The broad appeal of cross-validation is that it is a well-known method that many researchers and practitioners are familiar with, and it is an effective procedure to combat overfitting. The key idea behind our method is to split the original observations into two independent sets; the observations from the ‘test’ set are used to correct the biases that are embedded in the estimated eigenvectors from the ‘training’ set due to in-sample overfitting. As a result, extreme eigenvalues are pulled towards more central values to compensate for those biases. Our method is computationally scalable to large dimensions and it demonstrates superior results in this regime through an empirical application of active portfolio management.

The paper is structured as follows. Section 2 introduces the exponentially weighted average covariance matrix and its decomposition. Section 3 describes our proposed cross-validation-based nonlinear shrinkage covariance estimator. Section 4 contains the simulation study. Section 5 provides the empirical experiments. Section 6 concludes. Appendices A–C contain all the figures, tables, and experimental results for the Markowitz portfolio with signal problem.

2 Setting the Stage

2.1 The Weighted Sample Covariance Matrix

Let be a matrix of observations of a vector of assets, , each of dimensionality . Here, the symbol denotes the transpose operator of a vector or matrix, the symbol is a definition sign, and the symbol is the equal sign. The vector of assets is assumed to have zero means and a population covariance matrix , which is unobserved to the investor. The population covariance in our study may potentially be time-varying over the sample period, in which case, we shall assign a time-index subscript to it, for example, for .

The classical estimator for is the sample covariance matrix is defined as

| (1) |

The standard sample covariance is an estimator of the population covariance since it is unbiased (that is, its expectation coincides with the population covariance matrix). In general, a standard sample covariance can be generalized to include some arbitrary weight profile assigned along the time dimension. In particular, it is expressed in the following form

| (2) |

where is a fixed symmetric and positive-definite matrix. This weighting scheme generalizes the standard sample covariance and it provides us a way to incorporate prior knowledge about the non-independence and non-identicality nature of the observations in the covariance matrix. Indeed, if , where is an -dimensional identity matrix, then we recover the expression for the standard sample covariance in (1).

Without loss of generality, we assume that where denotes the trace of a square matrix or the sum of its diagonal entries. This ensures that these weighted covariance matrices are also unbiased estimators, that is . In other words, the weighting of observations in time should not affect the recovery of the ground truth on average.

2.2 Exponentially Weighted Average Covariance Matrix

To address the problem of non-stationarity in the time-series setting, we look at a (sample) covariance matrix that is measured using an exponentially weighted average scheme, henceforth, EWA-SC, which is given by

| (3) |

Here, is the exponential decay rate. The timescale for which the observations are “effectively” measured with this scheme can be determined using a characteristic time-scale defined as . For example, if , then the timescale would be days (or roughly 4 years). In the limit where tends to one from below the EWA-SC converges towards the standard sample covariance; conversely, if moves away from one, it places more weight on the recent cross-products observations.

The EWA-SC in Equation (3) has a weight matrix profile whose diagonal entries are

| (4) |

for and zero in the off-diagonal entries. Further, let us define the following auxiliary observation matrix:

| (5) |

Since the matrix is diagonal, its matrix factor is simply the square root of its diagonal entries taken with a non-negative sign. Based on our redefinition of the observation matrix, we can see that the EWA-SC can be expressed in a similar form as the standard uniformly weighted sample covariance. The advantage of recasting the EWA-SC in this way is that many of the refinements for the standard sample covariance that have been developed over the years are at our disposal; this includes shrinkage.

2.3 Decomposing the Covariance Matrix

The analysis of a covariance matrix would be easier if the entries are uncorrelated. While this is not generally true for asset returns, it is nonetheless useful if we can summarize the contents of a matrix in terms of key low-dimensional objects with mutually uncorrelated components. Fortunately, the EWA-SC is symmetric and so for a fixed decay rate , they admit the following spectral decomposition:

| (6) |

where denotes a system of sample eigenvalues and eigenvectors of , and denotes a system of eigenvalues and eigenvectors of the population covariance .222Both the sample eigenvalues and sample eigenvectors are implicitly parameterized by the decay rate since the underlying EWA-SC depends on it. We suppress their dependence on the decay rate for brevity. The eigenvalues are assumed to be sorted in ascending order.

The main advantage of the sample eigenvalues and sample eigenvectors is that they are consistent estimators; that is, they recover the population eigenvalues and eigenvectors when the number of observations becomes large while the number of assets is held fixed. However, this desirable statistical property breaks down in financial applications where the number of assets is of the same order of magnitude in comparison to the number of observations. In particular, the sample eigenvalues and sample eigenvectors end up being biased estimates of their population counterparts. We defer to Burda et al., (2011) for an in-depth explanation of this phenomenon for the EWA-SC matrix.

3 Shrinkage Estimation

3.1 Covariance for Portfolio Selection

In light of the previous discussion, we consider the framework of Stein, (1975, 1986) as a guide to correct the biases of the EWA-SC. It suggests that the sample eigenvalues should be corrected while retaining the sample eigenvectors of the original matrix. This can be formulated mathematically as:

| (7) |

where is an -dimensional vector that we have to obtain. This framework serves as a reasonable starting point to address the systematic biases in the sample covariance. Indeed, absent any a priori knowledge about the structure of the covariance matrix, the most natural guess that we have about the population eigenvectors is the sample eigenvectors that we observe. Hence, the sample eigenvectors are the only ones that we get to keep and we have to try to make the best out of this situation by coming up with a set of bias-corrected eigenvalues so that the covariance matrix as a whole is ‘closer’ to the truth.

The question is how we should choose the vector of bias-corrected eigenvalues . We answer this question by choosing the one that minimizes a loss function between estimators of the form (7) and the population covariance matrix. To determine the optimal estimator within the postulated form of (7), we consider a loss function between the population and the estimated covariance matrix based on the minimum variance loss function proposed by Engle et al., (2019, Definition 1), which is tailored specifically for the purpose of portfolio selection:

| (8) |

The loss function can be interpreted as the excess out-of-sample portfolio variance that would be materialized from using an estimator instead of the population covariance matrix, and it should be reduced as much as possible.

If we insert the postulated estimator (7) into Equation (8), then from the cyclic property of the trace operator and orthogonality of the eigenvectors, we get

| (9) |

By minimizing this loss function with respect to , we have

| (10) |

where the scalar value is independent of the asset index . The scalar can be chosen such that the trace of the population covariance matrix is preserved. This can be achieved by setting the scalar to the value 1; see for example Ledoit and Wolf, (2017, Proposition 4.1).

We see that is neither the sample eigenvalue nor the population eigenvalue. Rather, it is an ‘eigenvalue’ that internalizes both the sample and population information in order to differentiate itself from its sample and population counterparts. From the economic perspective, one can interpret each as an out-of-sample variance of a portfolio whose weights are the th sample eigenvector . This is an enhancement over the sample eigenvalues , which is an in-sample variance computed from a portfolio that uses the same observations as the weights . Further, Ledoit and Wolf, 2004b (, Section 2.3) showed that is less dispersed cross-sectionally than the sample eigenvalue . Hence, it constitutes a form of shrinkage itself that corrects the biases in the sample eigenvalues.

If we plug into Equation (7), we arrive at the following covariance estimator:

| (11) |

An advantage of is that it is positive for as long as is positive definite. In this case, the covariance estimator (11) is positive definite and invertible when . Unfortunately, is not attainable in practice since it depends on the population covariance , which is the very object that we wanted to estimate in the first place. While this seems paradoxical at first sight, it is possible to substantiate the estimator with real data and this is what we aim to achieve with our proposed method in the next subsection.

3.2 Out-of-Sample Variance Estimation by Cross-Validation

Another perspective on the biased nature of the sample eigenvalues and sample eigenvectors is that they are objects that have been obtained through numerical optimization routines. Hence, they are likely to overfit a given data. To address this problem, cross-validation is a powerful scheme to mitigate overfitting and estimate the out-of-sample performance for independent and identically distributed (i.i.d.) observations. In our setting, the out-of-sample performance that we are interested in is , which is the out-of-sample variance of the th sample eigenvector portfolio for a pre-specified decay rate.

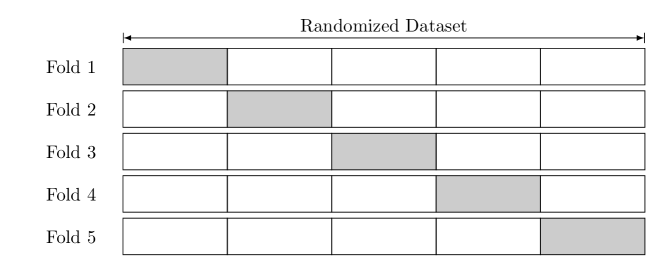

To perform cross-validation, we start by splitting the (randomized) observations into non-overlapping index sets (or folds) given by . Each set indexed by is called a ‘test’ fold, whereas the set of indices of the remaining observations forms a ‘training’ fold. From this construction, we can estimate the out-of-sample variance ; we introduce our -fold cross-validation estimator, which is defined as

| (12) |

where denotes the cardinality of the th test set such that each of them is approximately equal in size, that is, . Here, is the th sample eigenvector of a sample covariance matrix that is obtained from the training fold, and is a sample vector of the auxiliary observation matrix in Equation (5) from the test fold. This is a more general estimator of Abadir et al., (2014), Lam, (2016) and Bartz, (2016) since if tends to one, we recover the cross-validation estimator of the standard sample covariance as the auxiliary observation vectors become the original ones.

Figure 1 provides a schematic representation of the construction of the training and test sets for folds. We start by randomizing the auxiliary observation matrix from Equation (5) along the time axis.333The randomization step in the algorithm is needed to break the temporal correlations of the auxiliary observation vector induced by the exponential weights so that the observations in each fold can be approximately independent. This allows the cross-validated eigenvalue reproduces the out-of-sample variance along the th eigenvector through conditional averaging. Hence, they can be seen as an approximation to the optimal unattainable out-of-sample variance of the th sample eigenvector portfolio . We then split the (randomized) auxiliary observations into non-overlapping folds of equal size. Each of the folds is used as a test set, whereas all other folds are merged into a training set. For each fold configuration, we estimate the sample eigenvectors from the training set and then estimate an -dimensional vector of out-of-sample variances using the test set and the sample eigenvectors. Finally, we average the out-of-sample variance estimates over to give us the bias-corrected eigenvalue of the th sample eigenvector portfolio denoted as for all .

Finally, we plug into the estimator (7) to yield our operational covariance estimator, which we term EWA-CV:

| (13) |

By invoking a result in Lam, (2016, Corollary 4), EWA-CV readily yields a positive-definite covariance matrix as long as the population covariance is also positive-definite. An estimate for the inverse covariance can be obtained by taking the inverse of the covariance estimator.

Note that our covariance estimator (13) is not entirely restricted to weight profiles that are exponentially declining in time. In principle, our auxiliary variable definition (5) can accommodate any weight matrix design , provided it can be factorized into a matrix and a conjugate transpose. Thus, our estimator is general enough to incorporate other forms of weighting schemes to model the time dependence of asset returns or to be employed in other financial applications. We leave this investigation for future research.

Remark 1 (Unbiasedness).

The cross-validated eigenvalue in Equation (12) is an unbiased estimator of the variance along the eigenvector directions conditional on the EWA-SC. Indeed, since the weighted covariances (2) are unbiased estimators of the population covariance, then provided and are independent we have

| (14) |

In other words, the cross-validated eigenvalue reproduces the out-of-sample variance along the th eigenvector through conditional averaging. Thus, they can be seen as an approximation to the unattainable out-of-sample variance of the th sample eigenvector portfolio from Equation (11).

Remark 2 (Monotonicity of Eigenvalues).

The ordering of cross-validated eigenvalues is often violated in practice. This may be unsettling for some researchers since it can be argued that the eigenvalues should satisfy a ranking where there they are ordered from the smallest to the largest; for example, see Sheena and Takemura, (1992). To address this concern, we adopt the approach from Stein, (1975) and apply an isotonic regression of the set cross-validated eigenvalues on the sample eigenvalues of in order to enforce a monotonic structure on the estimated out-of-sample variances.

3.3 Related Literature

Our proposed estimator corresponds to a single choice of a split location (that is, the size of the training fold), which we denote as . The approach of Abadir et al., (2014) considers averaging the estimated eigenvalues over different fold as well as the split location where is the range of split locations. Their estimator is then given by the following grand average

| (15) |

where is the estimator (13) with for a given split location . This estimator is asymptotically optimal if the split location satisfies , with ; see Abadir et al., (2014, Proposition 3).

In contrast, Lam, (2016) considers a similar setup but studies the large-dimensional setting where as such that . Instead of averaging over a range of splits, Lam, (2016, Theorem 5) proposed a split , with some constant , that is asymptotically efficient. However, this asymptotic property may be challenged in finite samples or as approaches a constant smaller than 1, and there is no practical guide for setting the constant . Lam, (2016, Section 4.2) proposes to search over seven candidate split locations in order to minimize a criterion similar to that of Bickel and Levina, (2008).

In our paper, we avoid the non-trivial task of choosing the split locations entirely following Bartz, (2016) to reduce the number of required computations to build the estimator.

3.4 Comparison to DCC-NL

Another estimator that is often compared to a covariance matrix measured through an exponentially weighted scheme is the Dynamic Conditional Correlation (DCC) model proposed by Engle, (2002) to model the time-varying dynamics of multivariate financial returns due to conditional heteroskedasticity. As is well known, the DCC model also suffers from the ‘curse of dimensionality’. There have been efforts from Engle et al., (2019) to successfully enable the estimation of the DCC to be both (i) computationally feasible in the large dimensions through the use of composite likelihood functions from Pakel et al., (2021), and (ii) with reduced estimation error through the nonlinear shrinkage (NL) of Ledoit and Wolf, (2015). This estimator is referred to as the DCC-NL.

Both EWA-CV and DCC-NL are intimately related by the concept of shrinkage but they also differ in a few other ways.444Lam, (2016) proved the data splitting scheme of Abadir et al., (2014) is a nonparametric approach of achieving a similar nonlinear shrinkage effect in Ledoit and Wolf, (2012). First, the latter explicitly applies devolatization to the returns. Therefore, in order to allow for a more fair comparison between both estimators, EWA-CV should also be applied to a panel of returns series that have been devolatized through a univariate GARCH model of Bollerslev, (1986). Second, the dynamic nature of DCC requires that the covariance be determined recursively, while the EWA-SC requires only matrix multiplications. Third, the DCC-NL is governed by two parameters, while EWA-CV has just one. Our view is that maintaining a single parameter can offer a more parsimonious representation of asset returns, which provides insights into the sensitivity of the estimator’s performance to only changes in the decay rate. Moreover, since the decay rate is typically specified by the user in practice, it possesses less implementation overhead over the DCC, whose dynamic parameters are typically estimated via maximum likelihood. Admittedly, EWA-CV is a numerical scheme compared to NL, an analytical method, but it only employs a few spectral decompositions and vectorized operations to estimate an -dimensional vector, which are fast to execute. Finally, EWA-CV is conceptually simpler since it relies on the principle of cross-validation, which many practitioners are familiar with, whereas the DCC-NL requires recourse to the theory of random matrices. Notwithstanding the similarities and differences between both approaches, we formally compare their performances in Section 5.

4 Simulation Study

4.1 Return Generating Process

We now study the effectiveness of our proposed estimator against different competing estimators through a challenging simulation environment, where the risk dynamics are driven by the RiskMetrics model of J.P. Morgan/Reuters, (1996).555 The RiskMetrics 1996 methodology is a covariance matrix that evolves recursively according to an exponentially weighted moving average. It has a similar form to our EWA-SC (3) up to timing in the measurement. This allows us to assess if our proposed estimator is accurate enough to be useful in an ideal environment where it is supposed to thrive. In particular, we consider a return-generating process (RGP) that is drawn from a multivariate standard normal distribution given by

| (16) |

where is a population covariance matrix that evolves according to

| (17) |

The parameter is the ‘intrinsic’ decay rate of the population covariance matrix, which we set to in this simulation study. We use this RGP to generate a data set of asset returns with daily return observations, which corresponds to roughly 5 years of daily data.

4.2 Candidate Estimators

From the generated data set of asset returns, we can estimate a covariance matrix. Given the plethora of covariance estimators in the literature, we shall limit our analysis to the following candidate estimators for , which are either uniformly weighted or exponentially weighted:

-

•

LS: the linear shrinkage estimator of Ledoit and Wolf, 2004b , with the shrinkage target being (a scaled multiple of) the identity matrix.

-

•

NL: the quadratic inverse shrinkage estimator of Ledoit and Wolf, (2022).

-

•

CV: the cross-validation shrinkage estimator of Bartz, (2016) with folds.

-

•

EWA-SC: the estimator from Equation (3).

-

•

EWA-CV: based on our proposed cross-validation shrinkage estimator from Equation (13) with folds.

For EWA-based estimators, we shall consider various specifications of decay rates ranging from to . This would allow us to see how they behave under model misspecification.

4.3 Performance Assessment

To compare the performance of various covariance estimators against the population covariance, we need a loss function and an evaluation metric. The loss between an estimator and the population covariance matrix is based on Equation (8).

A simple metric to quantify an improvement of an estimator over a benchmark model is the so-called, PRIAL (percentage of relative improvement in average loss). If we let the standard sample covariance be the benchmark model, then the PRIAL is defined as

| (18) |

where is a population covariance obtained at the end of the sample period, and is a loss function. The PRIAL is when our estimator coincides with the population covariance at time , and with the uniformly-weighted sample covariance . A negative value for PRIAL is possible, which indicates that the estimator did not improve over the reference matrix . The notation denotes an expected value of the losses, which is taken to be the average over the 100 simulation trials.

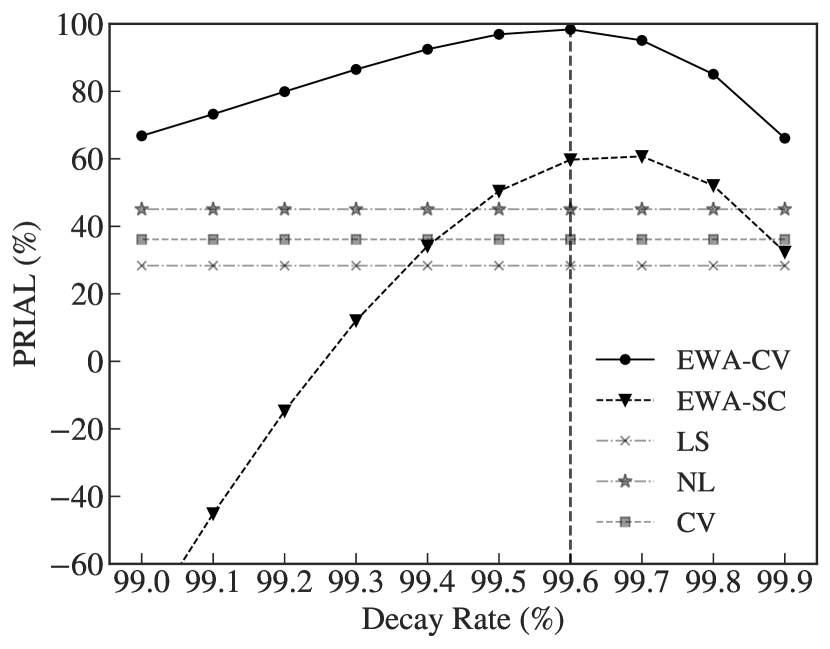

4.4 Simulation Results

We now present the results of the Monte Carlo simulations. Figure 2 shows the PRIAL for different covariance estimators against the different decay rate specifications. Starting with the uniformly weighted-based estimators, we see that LS, NL, and CV perform better than the standard sample covariance as seen by their positive PRIAL values. This improvement owes to the benefits of shrinkage. However, their performances remain flat for all decay rate specifications since, by their uniformly weighted construction, they are not parameterized by them. This lack of flexibility of the uniformly-weighted estimators fundamentally limits their ability to align themselves toward more recent risk, which gives rise to higher estimation errors.

In contrast, EWA-based estimators beat uniformly weighted estimators when their decay rate is in the vicinity around the intrinsic decay rate at with EWA-CV performing the best having PRIAL values of greater than 90%. This is reassuring for us because the EWA-based estimators (3) have the same form as the RGP in (17) (up to timing in measurement). Moreover, this also speaks to the importance of capturing time series variation of risk since the EWA-based estimators differ from their uniformly weighted counterparts by how the observations are measured across time.

A further inspection into the performance of EWA-SC shows that there is very little margin for error in specifying . In particular, EWA-SC starts to rapidly underperform all other estimators as decreases and even takes on negative values for less than . Fortunately, our proposed EWA-CV does not share that fragile behavior. The shrinkage technology that we have introduced in Section 3.2 has allowed it to be robust against a large ensemble of noisy observations causing it to yield stellar outperformance even with a misspecified decay rate. This is a desirable feature because, in practice, the actual decay rate of an ensemble of non-stationary return series is not known and we want to be protected from placing bets on risky sample eigenvectors by mistake.

Finally, we ran this experiment on a single server with an (256GB RAM 48 cores) Intel Xeon Gold 6252N 2.3GHz CPU. To estimate a 500-dimensional covariance of this setup, EWA-CV takes about 0.5 seconds wall-clock time and, by way of comparison, NL takes about 0.1 seconds. Thus, our method is fast to execute and incurs negligible runtime overhead.

4.5 Sensitivity Analysis to the Number of Folds

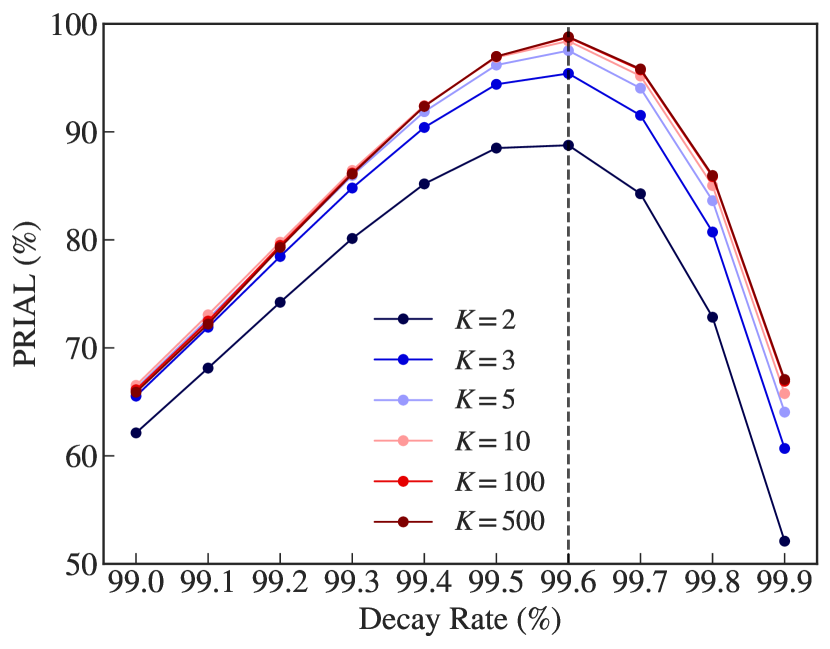

We also conduct a sensitivity analysis of EWA-CV to the different number of folds . Figure 2 shows that overall, the performance of EWA-CV is not highly sensitive to the number of folds. While its performance can be sub-optimal for , it is consistently optimal for . The intuition is that for , there is not enough averaging across the folds to further suppress the noise from the projections of the test observation onto the sample eigenvectors. However, for , we find that the performances remain similar. In light of these findings, we will use folds for all of our experiments, which is sufficient for us to reap the most benefits from averaging and to strike an appropriate balance between computational tractability and precision.

5 Empirical Analysis

5.1 Data and Portfolio Construction Rules

We now analyze the out-of-sample performance of our proposed estimator using real financial data. We first obtain daily stock returns data from the Center for Research in Security Prices (CRSP), starting at and ending at . Our analysis is limited to stocks traded on the NYSE, AMEX, and NASDAQ stock exchanges. The size of the investment universe that we consider is .

We define one ‘month’ and ‘year’ as and consecutive trading days, respectively. The portfolios are rebalanced on a monthly basis using a rolling window scheme where only past information is used to avoid a look-ahead bias. During the month, the number of shares is kept fixed in order to avoid incurring unnecessary transaction costs. The covariance matrices are estimated using an in-sample period of size , which is approximately 5 years. The out-of-sample period starts from and ends at . This provides us with a total of months (or trading days) of consecutive nonoverlapping observations of length days for which the portfolios are rebalanced.

To construct a well-defined investment universe on which we can estimate the covariances on, we use a similar procedure described in Engle et al., (2019). For each rebalancing month (using zero-based indexing), we first select the stocks that have complete data over the days in the in-sample period as well as over the days in the out-of-sample period. The backward and forward restrictions ensure that we have data to estimate our models and to evaluate out-of-sample. Then, we search for pairs of highly correlated stocks (that is, those with a sample correlation exceeding ) and remove the stock with the lower volume in each pair. From this remaining set of stocks, we select the largest stocks as measured by their market capitalization on the rebalancing month to include in our investment universe.

5.2 Base Candidate Portfolios

To test the performance of different covariance matrix estimators in the context of portfolio selection, we consider two investment problems: (1) the global minimum variance (GMV) portfolio and (2) the Markowitz portfolio with a given signal. Both problems are described in Section 5.4 and Appendix C, respectively. In either setting, we employ the following candidate estimators as their inputs:

-

•

SC: the sample covariance matrix (1).

-

•

LS: the linear shrinkage estimator of Ledoit and Wolf, 2004a , with the shrinkage target being (a scaled multiple of) the identity matrix.

-

•

NL: the quadratic inverse shrinkage (QIS) estimator of Ledoit and Wolf, (2022).

-

•

EWA-SC: the exponentially-weighted average sample covariance (3).

-

•

EWA-CV: our proposed method based on estimator (13) with .

-

•

AFM1-NL: an approximate single factor model of De Nard et al., (2021) with NL applied to the residuals.

-

•

AFM1-EWA-CV: our second proposed method based on an approximate single factor model with EWA-CV applied to the residuals.

Note that for the EWA-based estimators, we choose a fixed decay rate that is relatively high at , which makes them slightly closer to the uniformly weighted setting. While this choice might seem ad-hoc, nonetheless, our robustness checks show that it is a suitable choice for our financial application.

Remark 3 (Factor models).

While many active portfolio managers tend to hold relatively concentrated portfolios of less than 100 stocks, there are quantitative portfolio managers that invest in a broad investment universe spanning thousands of single stock equities in order to benefit from efficiency gains in large dimensions. In such a case, they tend to exploit some form of factor structure in order to make the investment problem more manageable. To accommodate for this practice, we can also extend our proposed estimator towards data that have been generated by a factor model in a similar spirit to De Nard et al., (2021) but with EWA–CV applied to the residual terms. In particular, we will utilize the market factor, which is easily accessible to researchers, and term our second proposed covariance estimator in this paper AFM1-EWA-CV.

5.3 Evaluation Methodology

To evaluate the performance of the different portfolios, we report four main out-of-sample performance measures: the average out-of-sample returns (AV), the standard deviation of portfolio returns (SD), the information ratio (IR), and the Sharpe ratio (SR). For ease of interpretability, all performance measures are annualized with 252 trading ‘days’. The information ratio is computed with respect to the actual returns (as opposed to returns in excess of the risk-free rate) since we believe it is more relevant in our context where the portfolios are formed solely on the basis of risky assets. On the other hand, the Sharpe ratio is the information ratio with the risk-free rate as the benchmark. In addition, we also include the maximum drawdown (MDD), which measures the largest cumulative loss from peak to trough over the entire out-of-sample period.

We also report the information ratio and Sharpe ratio net transaction costs denoted as and , respectively. In particular, we assume a constant transaction cost of 5 bps for all stocks, which is a reasonable approximation today. Even though the investment problem that we consider below does not explicitly account for transaction costs at the portfolio pre-formation stage, it is nevertheless worthwhile to investigate if our methods survive transaction costs in an unconstrained setup.

Additionally, we report the following portfolio weight statistics averaged over the 400 trading months: turnover (TO), gross exposure (GE; computed as the sum of the absolute value of long and short positions), proportional leverage (PL; computed as the fraction of negative weights), minimum weight (MIN), maximum weight (MAX), the standard deviation of weights (SD), and mean absolute deviation from an equally-weighted portfolio (MAD). Note that these statistics are not our primary focus since our proposed method is not optimized to account for these measures. Nevertheless, they are provided to give a better overview of the different methods.

5.4 Global Minimum Variance Portfolio

The global minimum variance (GMV) portfolio is expressed as

| (19) | ||||

| such that |

where is a vector of portfolio weights. The GMV portfolio allocation framework is useful for isolating the estimation error stemming from the expected returns and allows us to focus solely on evaluating the quality of a covariance matrix estimator. This application is similar to Engle et al., (2019) for reproducibility. Empirical studies of Haugen and Baker, (1991) and Jagannathan and Ma, (2003), among others, have found that the GMV portfolios enjoy favorable out-of-sample performance both in terms of risk and Sharpe ratio when compared with other benchmark portfolios. Moreover, it is also adopted in practice, as is the case, for example, with the iShares Edge MSCI Min Vol USA ETF, which has seen high asset inflows since early 2013; see for example, Goldberg et al., (2014).

In this setting, the solution for optimal weights has an explicit form given by

| (20) |

where is an -dimensional conformable vector of ones. To yield a feasible portfolio denoted as that can be computed from the returns data, we replace with the covariance matrix estimator . We also include the equal-weighted portfolio promoted by DeMiguel et al., (2009) as another benchmark, which is denoted by , since it is argued to be difficult to beat.

The primary metric for which we evaluate the performance of the GMV portfolio will be the out-of-sample standard deviation. We also report the statistical significance of the differences between the SD values of EWA-SC and EWA-CV derived by using the two-sided p-value of the prewhitened test described by Ledoit and Wolf, (2011, Section 3.1). Since the purpose of this paper is to demonstrate that EWA-CV is an improvement over EWA-SC, we confine our attention to the comparison of EWA-SC with EWA-CV to avoid multiple testing problems.

The out-of-sample performances are reported in Table 1 and the results from the SD column are summarized as follows:

-

•

EWA-CV outperforms EWA-SC for all and is statistically significant at the 0.01 level for .

-

•

Overall, the EWA-CV portfolio delivers the best results, owing in part to its ability to adapt to the non-stationary nature of the financial returns. Its performance can be seen to improve with increasing universe size .

-

•

The EWA-SC portfolio is competitive for and even outperforms portfolios that are regularized with shrinkage. This is probably due to the fact that at relatively small dimensions, a covariance estimator may benefit more from picking up more recent time series variations. However, as increases, the EWA-SC portfolio starts to underperform. This also corroborates the empirical findings of Engle et al., (2019, Table 7) in their application of the RiskMetrics 2006 methodology of Zumbach, (2007), which is a more elaborate version to the EWA-SC but also inherits the same cross-sectional estimation errors.

-

•

Even though AFM1-EWA-CV has slightly better performance than the NL estimators, it does not lead to any material improvement above EWA-CV.

-

•

The reduction in the standard deviation of EWA-CV over NL in amounts to 5%, 4%, and 2%, respectively. While the outperformance for may not be statistically significant at the 0.01 level, it is still an improvement and our method offers a viable alternative to the analytical nonlinear shrinkage method. A similar conclusion holds for EWA-CV and AFM1-NL since both AFM1-NL and NL share similar performance, which is consistent with the findings of De Nard et al., (2021, Table A.1).

Additionally, we find that EWA-CV outperforms in terms of information ratio and Sharpe ratio for although the performance between the portfolios is similar for . Once we have taken into account the transaction costs at the post-formation stage of the portfolio, we see a decline in the information and Sharpe ratios across all portfolios but the relative performance remain similar. In terms of the maximum drawdown incurred by the portfolio, we see that both EWA-CV and AFM1-EWA-CV suffer the least. For instance, if , the maximum drawdown for is 55.04%, while for EWA-CV, it is 25.63%, which is a 50% reduction.

Table 2 describes the distribution of the portfolio weights of the estimated portfolios. We see that EWA-CV has the least dispersed weight while both SC and EWA-SC have the most dispersed weight. Furthermore, EWA-CV and AFM1-EWA-CV have the lowest turnover, which is interesting given that we make no effort to control the trajectory of the weights. Moreover, EWA-CV also has the lowest amount of gross exposure and proportion of leverage.

5.5 Robustness Checks

In this section, we inspect whether the outperformance of our proposed estimator is robust to different revisions in the current empirical set-up. In particular, we will be interested in parameters dictating the (1) subsample period, (2) exponential decay rate, (3) no short-sale constraint, and (4) devolatization.

5.5.1 Subsample Analysis

Here, we check if there are any peculiar subsample effects that may drive the performances of our proposed scheme. We divide the out-of-sample period into four equally-sized subsamples of 100 months (that is, roughly 8 trading years) each: (1) 09/04/1986 to 12/21/1994, (2) 12/22/1994 to 04/25/2003, (3) 04/28/2003 to 08/25/2011, and (4) 08/26/2011 to 12/31/2019. Then we perform the same procedure in each subsample. The results are provided in Table 3.

We see that the ranking of performance across different portfolios is relatively consistent over time. Generally, EWA-CV is the best performer although there are brief episodes where it is not. For example, for , EWA-SC outperforms in Sample 1, while for , NL (and AFM1-NL) outperforms in Sample 4. Nevertheless, the performance of EWA-CV is close to the leading ones in these scenarios.

5.5.2 Sensitivity Analysis

In our base experiments, we parameterized the EWA-based estimators with a decay rate of . We now repeat the same backtest exercise as in the previous section but focus only on EWA-based estimators for different exponential decay rate specifications and . This allows us to examine if the performance of our estimator is sensitive to changes in the decay rate specification or if there are other choices that may lead to better results.

Table 4 shows that the outperformance of EWA-CV over EWA-SC is robust across different decay rates for while for , it only marginally outperforms EWA-CV in Sample 1 for . Moreover, EWA-CV tends to deliver a lower standard deviation with decay rates greater than . Unreported simulation results also indicate that decay rates lower than 0.985 consistently give a higher standard deviation. This observation holds over the full sample period as well as across different subsamples. These empirical findings are certainly at odds with the recommended value of 0.94 suggested by J.P. Morgan/Reuters, (1996) for modeling exponentially weighted moving average covariances.

5.5.3 No Short-Sale Constraint

In our original investment problem (19), we allow for the possibility of short-selling. However, shorting in the equity markets is difficult and a 50% margin must be posted. Since some portfolio managers may encounter a no-short-sale constraint in practice, we now impose a non-negative constraint on the portfolio weights in the optimization objective.

Table 5 presents the results. As can be seen, SC and EWA-SC are now competitive in terms of standard deviation, even though it differs only slightly from other estimators. By comparing these results to Table 1, it is evident that prohibiting short sales benefits SC and EWA-SC but harms other shrinkage estimators, including EWA-CV. Based on Jagannathan and Ma, (2003), these results concur with them that enforcing a no-short-sales constraint has an implicit shrinkage effect on the sample covariances when estimating the global minimum variance portfolio.

5.5.4 Devolatization

The base case experiments focus exclusively on the performance improvement that exponential weighting adds over a uniformly weighted shrinkage estimator. We now consider applying EWA-based estimators to a panel of returns series that have been devolatized through a univariate GARCH model. For this effort, we use Kevin Sheppard’s Python arch package to implement the GARCH(1,1) model.

We are now in a position to compare against the DCC-NL model of Engle et al., (2019) as well as the AFM1-DCC-NL model of De Nard et al., (2021). To this end, we use the Matlab implementation of DCC-NL found on Michael Wolf’s website but replaced the correlation targeting matrix with the QIS estimator.666The code can be downloaded at http://www.econ.uzh.ch/en/people/faculty/wolf/publications.html. Note that if at any rebalancing date, the estimation of the GARCH model (via the Matlab routine) produces a convergence issue, we add to the returns a noise term that is normally distributed with an expected value of 0 and a level of standard deviation, which increases from to in step size of 20 according to a geometric progression until convergence is achieved.

Finally, given that we exclude one of the two assets whose correlations are in excess of 0.95, our investment universe includes only stocks with ‘moderate’ correlations. In such an environment, it may be the case that having an accurate correlation matrix estimate is of second-order importance relative to estimating the variances of each asset accurately. Thus, as another benchmark, we consider a GMV portfolio, which assumes a diagonal correlation matrix with the variances estimated with a GARCH(1,1) model, denoted as VOL.

Table 6 summarizes the performances of the five portfolios: VOL, DCC-NL, EWA-CV, AFM1-DCC-NL, and AFM1-EWA-CV. Compared to Table 1, the standard deviation of EWA-CV estimators has reduced with devolatization for . For example, for , the standard deviation for EWA-CV and AFM1-EWA-CV decreased by 9.7% and 16.4%, respectively. Moreover, AFM1-EWA-CV appears to benefit the most from devolatization and is now the best performer for .

We also see that the performance of EWA-CV estimators is better than VOL for all by a wide margin. Hence, the performance improvements we observe in our estimator are not just due to better estimates of individual stocks’ volatility; they also stem from better estimates of correlations.

Interestingly, the performances of EWA-CV and DCC-NL estimators are quite similar for all investment sizes . For instance, for , the standard deviation reduction of EWA-CV over DCC-NL is 3%, whereas for AFM1-EWA-CV over AFM1-DCC-NL it is 1%. This observation is not unexpected given that both estimators employ a similar dynamic capture and shrinkage technology. The EWA-CV estimators also tend to be accompanied by a marginal improvement in average returns compared to their DCC-NL analogs, and also slightly better gross and net information and Sharpe ratios.

6 Conclusion

This paper introduces a novel covariance estimator that performs in large dimensions and adapts to the non-stationarities or persistent heteroskedastic environments of financial stock returns. Such scenarios are often found in practical applications of portfolio optimization for which our estimator is highly relevant. We accomplish this goal by (1) weighting the sample covariance matrix towards more recent data with exponentially weighted averages (EWA), and (2) through a novel application of the cross-validation (CV) shrinkage technology of Abadir et al., (2014), Lam, (2016) and Bartz, (2016). The former allows us to capture the non-stationary dynamics of financial time series with more flexible sample eigenvectors, while the latter attenuates the adverse noise effects that are embedded in the sample eigenvalues. We call our estimator, EWA-CV. Beyond these statistical benefits, our proposed estimator possesses several appealing features such as the simplicity of implementation, low runtime overhead for research prototyping, and transparency for independent verification.

We have provided simulation experiments to help us to gain insights into the channels that drive the outperformance of our estimator over the sample exponentially weighted average covariance and other uniformly weighted estimators. Our empirical experiments on real financial data reinforce its superiority over the exponentially weighted sample covariance and uniformly weighted shrinkage estimators with improved realized measures in large investment universe sizes. We also demonstrated that our proposed shrinkage estimator(s) rivals the performance of the state-of-the-art dynamic conditional correlation non-linear shrinkage (DCC-NL) estimator of Engle et al., (2019) and its factor model extension by De Nard et al., (2021) while incurring less implementation and computational overhead as well as simpler routines. Hence, our proposal offers practitioners of risk and asset management an attractive reduced-form alternative to the existing large-dimensional multivariate dynamic volatility models for financial returns.

In general, the adverse noise effects from a large-dimensional regime can be further reduced by incorporating additional prior knowledge about the orientation of the eigenvectors. For example, this can include overlaying the covariance matrix with economically driven models that possess a small number of risk parameters or with an appropriately structured block matrix reflecting the sector relationships of the stock returns. A cross-pollination of a postulated covariance matrix with the technology of nonlinear shrinkage provides an interesting avenue for further research.

We hope that EWA-CV will serve as a valuable addition to a portfolio manager’s armory and a new benchmark in large cross-sectional financial applications.

References

- Abadir et al., (2014) Abadir, K. M., Distaso, W., and Žikeš, F. (2014). Design-free estimation of variance matrices. Journal of Econometrics, 181(2):165–180.

- Bartz, (2016) Bartz, D. (2016). Cross-validation based nonlinear shrinkage. arXiv preprint arXiv:1611.00798.

- Bickel and Levina, (2008) Bickel, P. J. and Levina, E. (2008). Regularized estimation of large covariance matrices. The Annals of Statistics, 36(1):199–227.

- Bollerslev, (1986) Bollerslev, T. (1986). Generalized autoregressive conditional heteroskedasticity. Journal of Econometrics, 31(3):307–327.

- Bun et al., (2017) Bun, J., Bouchaud, J.-P., and Potters, M. (2017). Cleaning large correlation matrices: Tools from random matrix theory. Physics Reports, 666:1–109.

- Burda et al., (2011) Burda, Z., Jarosz, A., Nowak, M. A., Jurkiewicz, J., Papp, G., and Zahed, I. (2011). Applying free random variables to random matrix analysis of financial data. Part I: The Gaussian case. Quantitative Finance, 11(7):1103–1124.

- Chamberlain and Rothschild, (1983) Chamberlain, G. and Rothschild, M. (1983). Arbitrage, factor structure, and mean-variance analysis on large asset markets. Econometrica, 51(5):1281–304.

- Chopra and Ziemba, (1993) Chopra, V. K. and Ziemba, W. T. (1993). The effect of errors in means, variances, and covariances on optimal portfolio choice. The Journal of Portfolio Management, 19(2):6–11.

- De Nard et al., (2021) De Nard, G., Ledoit, O., and Wolf, M. (2021). Factor models for portfolio selection in large dimensions: The good, the better and the ugly. Journal of Financial Econometrics, 19(2):236–257.

- DeMiguel et al., (2009) DeMiguel, V., Garlappi, L., and Uppal, R. (2009). Optimal versus naive diversification: How inefficient is the portfolio strategy? The Review of Financial Studies, 22(5):1915–1953.

- Engle, (2002) Engle, R. (2002). Dynamic conditional correlation: A simple class of multivariate generalized autoregressive conditional heteroskedasticity models. Journal of Business & Economic Statistics, 20(3):339–350.

- Engle and Colacito, (2006) Engle, R. and Colacito, R. (2006). Testing and valuing dynamic correlations for asset allocation. Journal of Business & Economic Statistics, 24(2):238–253.

- Engle et al., (2019) Engle, R. F., Ledoit, O., and Wolf, M. (2019). Large dynamic covariance matrices. Journal of Business & Economic Statistics, 37(2):363–375.

- Fama and French, (1992) Fama, E. F. and French, K. R. (1992). The cross-section of expected stock returns. The Journal of Finance, 47(2):427–465.

- Goldberg et al., (2014) Goldberg, L. R., Leshem, R., and Geddes, P. (2014). Restoring value to minimum variance. Journal Of Investment Management, 12(2):32–39.

- Haff, (1980) Haff, L. (1980). Empirical bayes estimation of the multivariate normal covariance matrix. The Annals of Statistics, 8(3):586–597.

- Haugen and Baker, (1991) Haugen, R. A. and Baker, N. L. (1991). The efficient market inefficiency of capitalization–weighted stock portfolios. The Journal of Portfolio Management, 17(3):35–40.

- Jagannathan and Ma, (2003) Jagannathan, R. and Ma, T. (2003). Risk reduction in large portfolios: Why imposing the wrong constraints helps. The Journal of Finance, 58(4):1651–1683.

- James and Stein, (1961) James, W. and Stein, C. (1961). Estimation with quadratic loss. In Proceedings of the Fourth Berkeley Symposium on Mathematical Statistics and Probability, volume 1, pages 361–379.

- Jegadeesh, (1990) Jegadeesh, N. (1990). Evidence of predictable behavior of security returns. The Journal of Finance, 45(3):881–898.

- Jegadeesh and Titman, (1993) Jegadeesh, N. and Titman, S. (1993). Returns to buying winners and selling losers: Implications for stock market efficiency. The Journal of Finance, 48(1):65–91.

- Jobson and Korkie, (1980) Jobson, J. D. and Korkie, B. (1980). Estimation for Markowitz efficient portfolios. Journal of the American Statistical Association, 75(371):544–554.

- J.P. Morgan/Reuters, (1996) J.P. Morgan/Reuters (1996). RiskMetrics - technical document. New York: J.P. Morgan/Reuters.

- Lam, (2016) Lam, C. (2016). Nonparametric eigenvalue-regularized precision or covariance matrix estimator. The Annals of Statistics, 44(3):928–953.

- Ledoit and Péché, (2011) Ledoit, O. and Péché, S. (2011). Eigenvectors of some large sample covariance matrix ensembles. Probability Theory and Related Fields, 151(1):233–264.

- Ledoit and Wolf, (2003) Ledoit, O. and Wolf, M. (2003). Improved estimation of the covariance matrix of stock returns with an application to portfolio selection. Journal of Empirical Finance, 10(5):603–621.

- (27) Ledoit, O. and Wolf, M. (2004a). Honey, I shrunk the sample covariance matrix. The Journal of Portfolio Management, 30(4):110–119.

- (28) Ledoit, O. and Wolf, M. (2004b). A well-conditioned estimator for large-dimensional covariance matrices. Journal of Multivariate Analysis, 88(2):365–411.

- Ledoit and Wolf, (2008) Ledoit, O. and Wolf, M. (2008). Robust performance hypothesis testing with the Sharpe ratio. Journal of Empirical Finance, 15(5):850–859.

- Ledoit and Wolf, (2011) Ledoit, O. and Wolf, M. (2011). Robust performances hypothesis testing with the variance. Wilmott, 2011(55):86–89.

- Ledoit and Wolf, (2012) Ledoit, O. and Wolf, M. (2012). Nonlinear shrinkage estimation of large-dimensional covariance matrices. The Annals of Statistics, 40(2):1024–1060.

- Ledoit and Wolf, (2015) Ledoit, O. and Wolf, M. (2015). Spectrum estimation: A unified framework for covariance matrix estimation and PCA in large dimensions. Journal of Multivariate Analysis, 139:360–384.

- Ledoit and Wolf, (2017) Ledoit, O. and Wolf, M. (2017). Nonlinear shrinkage of the covariance matrix for portfolio selection: Markowitz meets Goldilocks. The Review of Financial Studies, 30(12):4349–4388.

- Ledoit and Wolf, (2020) Ledoit, O. and Wolf, M. (2020). Analytical nonlinear shrinkage of large-dimensional covariance matrices. The Annals of Statistics, 48(5):3043–3065.

- Ledoit and Wolf, (2022) Ledoit, O. and Wolf, M. (2022). Quadratic shrinkage for large covariance matrices. Bernoulli, 28(3):1519–1547.

- Mandelbrot, (1963) Mandelbrot, B. B. (1963). The variation of certain speculative prices. The Journal of Business, 36:394–394.

- Markowitz, (1952) Markowitz, H. (1952). Portfolio selection. The Journal of Finance, 7:77–91.

- Michaud, (1989) Michaud, R. (1989). The Markowitz optimization enigma: Is optimized optimal? Financial Analysts Journal, 45:31–42.

- Pakel et al., (2021) Pakel, C., Shephard, N., Sheppard, K., and Engle, R. F. (2021). Fitting vast dimensional time-varying covariance models. Journal of Business & Economic Statistics, 39(3):652–668.

- Ross, (1976) Ross, S. A. (1976). The arbitrage theory of capital asset pricing. Journal of Economic Theory, 13(3):341–60.

- Sharpe, (1963) Sharpe, W. F. (1963). A simplified model for portfolio analysis. Management Science, 9(2):277–293.

- Sheena and Takemura, (1992) Sheena, Y. and Takemura, A. (1992). Inadmissibility of non-order-preserving orthogonally invariant estimators of the covariance matrix in the case of Stein’s loss. Journal of Multivariate Analysis, 41(1):117–131.

- Stein, (1956) Stein, C. (1956). Inadmissibility of the usual estimator for the mean of a multivariate normal distribution. In Proceeding of the Fourth Berkeley Symposium on Mathematical Statistics and Probability, volume 1, pages 197–206. University of California Press.

- Stein, (1975) Stein, C. (1975). Estimation of a covariance matrix. Rietz lecture, 39th Annual Meeting IMS. Atlanta, Georgia.

- Stein, (1986) Stein, C. (1986). Lectures on the theory of estimation of many parameters. Journal of Mathematical Sciences, 34(1):1373–1403.

- Zumbach, (2007) Zumbach, G. (2007). The RiskMetrics 2006 methodology. Technical Report, RiskMetrics Group.

Appendix A Figures

Appendix B Tables

| AV | SD | IR | SR | MDD | |||

| Panel A: Universe Size, | |||||||

| SC | |||||||

| EWA-SC | |||||||

| LS | |||||||

| NL | |||||||

| EWA-CV | |||||||

| AFM1-NL | |||||||

| AFM1-EWA-CV | |||||||

| Panel B: Universe Size, | |||||||

| SC | |||||||

| EWA-SC | |||||||

| LS | |||||||

| NL | |||||||

| EWA-CV | |||||||

| AFM1-NL | |||||||

| AFM1-EWA-CV | |||||||

| Panel C: Universe Size, | |||||||

| SC | |||||||

| EWA-SC | |||||||

| LS | |||||||

| NL | |||||||

| EWA-CV | |||||||

| AFM1-NL | |||||||

| AFM1-EWA-CV | |||||||

| TO | GE | PL | MIN | MAX | SD | MAD | |

| Panel A: Universe Size, | |||||||

| SC | |||||||

| EWA-SC | |||||||

| LS | |||||||

| NL | |||||||

| EWA-CV | |||||||

| AFM1-NL | |||||||

| AFM1-EWA-CV | |||||||

| Panel B: Universe Size, | |||||||

| SC | |||||||

| EWA-SC | |||||||

| LS | |||||||

| NL | |||||||

| EWA-CV | |||||||

| AFM1-NL | |||||||

| AFM1-EWA-CV | |||||||

| Panel C: Universe Size, | |||||||

| SC | |||||||

| EWA-SC | |||||||

| LS | |||||||

| NL | |||||||

| EWA-CV | |||||||

| AFM1-NL | |||||||

| AFM1-EWA-CV | |||||||

| Sample 1 | Sample 2 | Sample 3 | Sample 4 | ||||||||

| SD | IR | SD | IR | SD | IR | SD | IR | ||||

| Panel A: Universe Size, | |||||||||||

| SC | |||||||||||

| EWA-SC | 10.91 | ||||||||||

| LS | |||||||||||

| NL | |||||||||||

| EWA-CV | 13.07 | 11.00 | 9.19 | ||||||||

| AFM1-NL | |||||||||||

| AFM1-EWA-CV | |||||||||||

| Panel B: Universe Size, | |||||||||||

| SC | |||||||||||

| EWA-SC | |||||||||||

| LS | |||||||||||

| NL | |||||||||||

| EWA-CV | 7.41 | 8.73 | 8.83 | 4.54 | |||||||

| AFM1-NL | |||||||||||

| AFM1-EWA-CV | |||||||||||

| Panel C: Universe Size, | |||||||||||

| SC | |||||||||||

| EWA-SC | |||||||||||

| LS | |||||||||||

| NL | 4.61 | ||||||||||

| EWA-CV | 5.84 | 6.69 | 7.90 | ||||||||

| AFM1-NL | |||||||||||

| AFM1-EWA-CV | |||||||||||

| Full Sample | Sample 1 | Sample 2 | Sample 3 | Sample 4 | ||||||||||

| SD | IR | SD | IR | SD | IR | SD | IR | SD | IR | |||||

| Panel A: EWA-SC, Universe Size: | ||||||||||||||

| Panel B: EWA-CV, Universe Size: | ||||||||||||||

| Panel C: EWA-SC, Universe Size: | ||||||||||||||

| Panel D: EWA-CV, Universe Size: | ||||||||||||||

| AV | SD | IR | SR | MDD | |||

| Panel A: Universe Size, | |||||||

| SC | |||||||

| EWA-SC | |||||||

| LS | |||||||

| NL | |||||||

| EWA-CV | 12.10 | ||||||

| AFM1-NL | |||||||

| AFM1-EWA-CV | |||||||

| Panel B: Universe Size, | |||||||

| SC | |||||||

| EWA-SC | 9.23 | ||||||

| LS | |||||||

| NL | |||||||

| EWA-CV | |||||||

| AFM1-NL | |||||||

| AFM1-EWA-CV | |||||||

| Panel C: Universe Size, | |||||||

| SC | |||||||

| EWA-SC | 7.32 | ||||||

| LS | |||||||

| NL | |||||||

| EWA-CV | |||||||

| AFM1-NL | |||||||

| AFM1-EWA-CV | |||||||

| AV | SD | IR | SR | MDD | |||

| Panel A: Universe Size, | |||||||

| VOL | |||||||

| DCC-NL | |||||||

| EWA-CV | |||||||

| AFM1-DCC-NL | 11.52 | ||||||

| AFM1-EWA-CV | |||||||

| Panel B: Universe Size, | |||||||

| VOL | |||||||

| DCC-NL | |||||||

| EWA-CV | |||||||

| AFM1-DCC-NL | |||||||

| AFM1-EWA-CV | 7.13 | ||||||

| Panel C: Universe Size, | |||||||

| VOL | |||||||

| DCC-NL | |||||||

| EWA-CV | |||||||

| AFM1-DCC-NL | |||||||

| AFM1-EWA-CV | 5.44 | ||||||

Appendix C Markowitz Portfolio with Signal

The Markowitz problem with a fully-invested constraint is expressed as

| (21) |

where is a predictive signal and is an investor’s minimum target expected return. We consider the momentum signal as there is substantial empirical evidence that documents this anomaly in the returns of individual stocks (Jegadeesh,, 1990; Jegadeesh and Titman,, 1993). A momentum signal is calculated by taking the geometric average of the past year’s stock returns, excluding the most recent month’s returns. Taking the current momentum values for all stocks in the universe produces a cross-sectional predictive signal . This application is similar to Engle et al., (2019) for reproducibility.

The well-known solution to this optimization problem is given by

| (22) | ||||

where is a vector of ones. A feasible portfolio can be obtained by replacing the unknown covariance with an estimator in Equation (22). We also include an equally-weighted portfolio of the top quintile stocks sorted according to their momentum value, which is labeled as EW-TQ. Further, we set the target expected return to be the average of the momentum values of the stocks from in this portfolio.

The primary metric for which we evaluate the performance of Markowitz portfolios will be the out-of-sample information ratio. We also report the statistical significance of the differences between the IR values of EWA-SC and EWA-CV derived by using the two-sided p-value of the prewhitened test described by Ledoit and Wolf, (2008, Section 3.1). Since the purpose of this paper is to demonstrate that EWA-CV is an improvement over EWA-SC, we confine our attention to the comparison of EWA-SC with EWA-CV to avoid a multiple testing problem.

The out-of-sample performances are reported in Table 7 and the results from the IR column are summarized as follows:

-

•

EWA-CV outperforms EWA-SC for all and is statistically and economically significant at the 0.01 level for .

-

•

Overall, the EWA-CV portfolio delivers the best results, owing in part to its ability to adapt to the non-stationary nature of the financial returns. Its performance can be seen to improve with increasing universe size .

-

•

Even though AFM1-EWA-CV has slightly better performance than the NL estimators, it does not lead to any material improvement above EWA-CV.

-

•

The increase in information ratio of EWA-CV over NL in amounts to 1%, 6%, and 9%, respectively. While this outperformance may not be statistically significant at the 0.01 level or economically meaningful, it is still an improvement and our method offers a viable alternative to the analytical nonlinear shrinkage method. A similar conclusion holds for the comparison between EWA-CV and AFM1-NL since both AFM1-NL and NL share similar performance, which is consistent with the findings of De Nard et al., (2021, Table A.3).

In addition, we find that EWA-CV produces the highest out-of-sample information ratio and Sharpe ratio after incorporating transaction costs at the post-formation stage of the portfolio for . Further, Engle and Colacito, (2006) suggests assessing the performance of a Markowitz portfolio in terms of the out-of-sample standard deviation. Based on this metric, we find that EWA-CV has the lowest value across different . In terms of the maximum drawdown incurred by the portfolio, we see that both EWA-CV and AFM1-EWA-CV suffer the least for . For instance, if , the maximum drawdown for EW-TQ is 58.56%, while for EWA-CV, it is 23.19%, which is a 60% reduction.

Table 8 describes the distribution of the portfolio weights of the estimated portfolios. We see that EWA-CV has the least dispersed weight while both SC and EWA-SC have the most dispersed weight. Furthermore, EWA-CV and AFM1-EWA-CV have the lowest turnover, which is interesting given that we make no effort to control the trajectory of the weights. Moreover, EWA-CV also has the lowest amount of gross exposure and proportion of leverage.

C.1 Robustness Checks

In this section, we inspect whether the outperformance of our proposed estimator is robust to different revisions in the current empirical set-up. In particular, we will be interested in parameters dictating the (1) subsample period, (2) exponential decay rate, (3) no short-sale constraint, and (4) devolatization.

C.1.1 Subsample Analysis

Here, we check if there are any peculiar subsample effects that may drive the performances of our proposed scheme. We divide the out-of-sample period into four equally-sized subsamples of 100 months (that is, roughly 8 trading years) each: (1) 09/04/1986 to 12/21/1994, (2) 12/22/1994 to 04/25/2003, (3) 04/28/2003 to 08/25/2011, and (4) 08/26/2011 to 12/31/2019. Then we perform the same procedure in each subsample. The results are provided in Table 9.

We see that the ranking of performance across different portfolios is relatively consistent over time for with EWA-CV estimators being the best performers. For , however, there are brief episodes where it is not; EWA-SC outperforms in Sample 1, EW-TQ in Sample 2, and NL (and AFM1-NL) in Sample 4. Nevertheless, the performance of EWA-CV is close to the leading ones in these scenarios. In terms of standard deviation, EWA-CV consistently has the lowest value across all subsamples and universes.

C.1.2 Sensitivity Analysis

In our base experiments, we parameterized the EWA-based estimators with a decay rate of . We now repeat the same backtest exercise as in the previous section but focus only on EWA-based estimators for different exponential decay rate specifications and . This allows us to examine if the performance of our estimator is sensitive to changes in the decay rate specification or if there are other choices that may lead to better results.

According to Table 10, EWA-CV outperforms EWA-SC across different decay rates for , whereas for , EWA-SC outperforms EWA-CV only marginally in Sample 1. Moreover, for , EWA-CV tends to deliver a higher information ratio with decay rates greater than . Unreported simulation results also indicate that decay rates lower than 0.985 consistently give a lower information ratio. This observation holds over the full sample period as well as across different subsamples. For , there appears to be some performance benefit from tilting the EWA-CV towards more recent observations in some periods. For example, in Sample 2 and Sample 4, gives the highest information ratio, which is a 23% and 15% improvement over using .

C.1.3 No Short-Sale Constraint

In our original investment problem (21), we allow for the possibility of short-selling. Since some portfolio managers may encounter a no-short-sale constraint in practice, we now impose a non-negative constraint on the portfolio weights in the optimization objective.

Table 11 presents the results. As can be seen, SC and EWA-SC are now competitive in terms of information ratio, even though it differs only slightly from other estimators. By comparing these results to Table 7, it is evident that prohibiting short sales benefits SC and EWA-SC but harms other shrinkage estimators, including EWA-CV.

C.1.4 Devolatization

The base case experiments focus exclusively on the performance improvement exponential weighting adds over a uniform weighted shrinkage estimator. We now consider applying EWA-based estimators to a panel of returns series that have been devolatized through a univariate GARCH model. This will allow us to facilitate comparison with the DCC-NL model of Engle et al., (2019). As another benchmark, we consider a Markowitz portfolio, which assumes a diagonal correlation matrix with the variances estimated with a GARCH(1,1) model, denoted as VOL.

Table 12 summarizes the performances of the five portfolios: VOL, DCC-NL, EWA-CV, AFM1- DCC-NL, and AFM1-EWA-CV. Compared to Table 7, it can be seen that the information ratio of EWA-CV has increased with devolatization for but reduced for . AFM1-EWA-CV appears to benefit the most from devolatization and is now the best performer for .

We also see that the information ratios of EWA-CV estimators are higher than VOL for all by a wide margin. Hence, the performance improvements we observe in our estimator are not just due to better estimates of individual stocks’ volatility; they also stem from better estimates of correlations.

Interestingly, the performances of EWA-CV and DCC-NL estimators are quite similar for all investment sizes . For instance, the information ratio improvement of EWA-CV over DCC-NL for is 4%, whereas for AFM1-EWA-CV over AFM1-DCC-NL it is 1%. EWA-CV estimators also have slightly better net information and Sharpe ratios.

| AV | SD | IR | SR | MDD | |||

| Panel A: Universe Size, | |||||||

| EW-TQ | |||||||

| SC | |||||||

| EWA-SC | |||||||

| LS | |||||||

| NL | |||||||

| EWA-CV | |||||||

| AFM1-NL | |||||||

| AFM1-EWA-CV | |||||||

| Panel B: Universe Size, | |||||||

| EW-TQ | |||||||

| SC | |||||||

| EWA-SC | |||||||

| LS | |||||||

| NL | |||||||

| EWA-CV | |||||||

| AFM1-NL | |||||||

| AFM1-EWA-CV | |||||||

| Panel C: Universe Size, | |||||||

| EW-TQ | |||||||

| SC | |||||||

| EWA-SC | |||||||

| LS | |||||||

| NL | |||||||

| EWA-CV | |||||||

| AFM1-NL | |||||||

| AFM1-EWA-CV | |||||||

| TO | GE | PL | MIN | MAX | SD | MAD | |

| Panel A: Universe Size, | |||||||

| EW-TQ | |||||||

| SC | |||||||

| EWA-SC | |||||||

| LS | |||||||

| NL | |||||||

| EWA-CV | |||||||

| AFM1-NL | |||||||

| AFM1-EWA-CV | |||||||

| Panel B: Universe Size, | |||||||

| EW-TQ | |||||||

| SC | |||||||

| EWA-SC | |||||||

| LS | |||||||

| NL | |||||||

| EWA-CV | |||||||

| AFM1-NL | |||||||

| AFM1-EWA-CV | |||||||

| Panel C: Universe Size, | |||||||

| EW-TQ | |||||||

| SC | |||||||

| EWA-SC | |||||||

| LS | |||||||

| NL | |||||||

| EWA-CV | |||||||

| AFM1-NL | |||||||

| AFM1-EWA-CV | |||||||

| Sample 1 | Sample 2 | Sample 3 | Sample 4 | ||||||||

| SD | IR | SD | IR | SD | IR | SD | IR | ||||

| Panel A: Universe Size, | |||||||||||

| EW-TQ | 0.90 | ||||||||||

| SC | |||||||||||

| EWA-SC | 0.91 | ||||||||||

| LS | |||||||||||

| NL | 1.19 | ||||||||||

| EWA-CV | |||||||||||

| AFM1-NL | |||||||||||

| AFM1-EWA-CV | 1.09 | ||||||||||

| Panel B: Universe Size, | |||||||||||

| EW-TQ | |||||||||||

| SC | |||||||||||

| EWA-SC | |||||||||||

| LS | 1.46 | ||||||||||

| NL | |||||||||||

| EWA-CV | 1.44 | 1.21 | |||||||||

| AFM1-NL | |||||||||||

| AFM1-EWA-CV | 1.36 | ||||||||||

| Panel C: Universe Size, | |||||||||||

| EW-TQ | |||||||||||

| SC | |||||||||||

| EWA-SC | |||||||||||

| LS | |||||||||||

| NL | |||||||||||

| EWA-CV | 1.69 | 1.71 | 1.83 | ||||||||

| AFM1-NL | |||||||||||

| AFM1-EWA-CV | 1.42 | ||||||||||

| Full Sample | Sample 1 | Sample 2 | Sample 3 | Sample 4 | ||||||||||

| SD | IR | SD | IR | SD | IR | SD | IR | SD | IR | |||||

| Panel A: EWA-SC, Universe Size: | ||||||||||||||

| Panel B: EWA-CV, Universe Size: | ||||||||||||||

| Panel C: EWA-SC, Universe Size: | ||||||||||||||

| Panel D: EWA-CV, Universe Size: | ||||||||||||||

| AV | SD | IR | SR | MDD | |||

| Panel A: Universe Size, | |||||||

| EW-TQ | |||||||

| SC | |||||||

| EWA-SC | |||||||

| LS | |||||||

| NL | |||||||

| EWA-CV | |||||||

| AFM1-NL | |||||||

| AFM1-EWA-CV | 0.74 | ||||||

| Panel B: Universe Size, | |||||||

| EW-TQ | |||||||

| SC | |||||||

| EWA-SC | |||||||

| LS | |||||||

| NL | |||||||

| EWA-CV | 1.01 | ||||||

| AFM1-NL | |||||||

| AFM1-EWA-CV | |||||||

| Panel C: Universe Size, | |||||||

| EW-TQ | |||||||

| SC | |||||||

| EWA-SC | |||||||

| LS | |||||||

| NL | |||||||

| EWA-CV | 1.01 | ||||||

| AFM1-NL | |||||||

| AFM1-EWA-CV | |||||||

| AV | SD | IR | SR | MDD | |||

| Panel A: Universe Size, | |||||||

| VOL | |||||||

| DCC-NL | |||||||

| EWA-CV | 0.94 | ||||||

| AFM1-DCC-NL | |||||||

| AFM1-EWA-CV | |||||||

| Panel B: Universe Size, | |||||||

| VOL | |||||||

| DCC-NL | |||||||

| EWA-CV | |||||||

| AFM1-DCC-NL | |||||||

| AFM1-EWA-CV | 1.42 | ||||||

| Panel C: Universe Size, | |||||||

| VOL | |||||||

| DCC-NL | |||||||

| EWA-CV | |||||||

| AFM1-DCC-NL | |||||||

| AFM1-EWA-CV | 1.63 | ||||||