Parametric measures of variability induced by risk measures

Abstract

We present a general framework for a comparative theory of variability measures, with a particular focus on the recently introduced one-parameter families of inter-Expected Shortfall differences and inter-expectile differences, that are explored in detail and compared with the widely known and applied inter-quantile differences.

From the mathematical point of view, our main result is a characterization of symmetric and comonotonic variability measures as mixtures of inter-Expected Shortfall differences, under a few additional technical conditions. Further, we study the stochastic orders induced by the pointwise comparison of inter-Expected Shortfall and inter-expectile differences, and discuss their relationship with the dilation order. From the statistical point of view, we establish asymptotic consistency and normality of the natural estimators and provide a rule of the thumb for cross-comparisons.

Finally, we study the empirical behaviour of the considered classes of variability measures on the S&P Index under various economic regimes, and explore the comparability of different time series according to the introduced stochastic orders.

Keywords: Risk management, variability measures, Expected Shortfall, expectiles, stochastic orders.

1 Introduction

Several measures of distributional variability are widely used in statistics, probability, economics, finance, physical sciences, and other disciplines. In this paper, we study a general theory of variability measures with an emphasis on three symmetric one-parameter families generated by popular parametric risk measures: Value-at-Risk (VaR), Expected Shortfall (ES), and expectiles. The corresponding induced variability measures are the inter-quantile difference, the inter-ES difference, and the inter-expectile difference. While the first one is a classical measure of statistical dispersion widely used e.g. in box plots, the other two are, to the best of our knowledge, relatively new: the inter-ES difference appears in Example 4 of Wang et al. (2020b) as a signed Choquet integral, and the inter-expectile difference has been studied in Bellini et al. (2020) via a connection to option prices. The present paper is a first unifying study, focused on their comparative qualitative and quantitative properties.

The mathematical theory of risk measures is extensive, and a standard reference is Föllmer and Schied (2016). As it is well-known, VaR is simply a quantile and ES is a coherent risk measure in the sense of Artzner et al. (1999). Both VaR and ES are implemented in current banking and insurance regulation frameworks; we refer to McNeil et al. (2015) for a comprehensive background and Wang and Zitikis (2021) for a more recent account. Expectiles, originally introduced in the statistical literature by Newey and Powell (1987), have received an increasing attention in risk management, as it has been shown that they are the only elicitable coherent risk measures (Ziegel (2016)). We refer e.g. to Bellini et al. (2014) and Bellini and Di Bernardino (2015) for more on the theory and financial applications of expectiles. For a comparison of the above risk measures in the context of regulatory capital calculation, see Embrechts et al. (2014) and Emmer et al. (2015).

The theory of variability measures has been studied from different angles; see David (1998) for a review in the context of the measurement of statistical dispersion. A mathematical formulation closer to our setting is the notion of deviation measure introduced in Rockafellar et al. (2006), and further developed by Grechuk et al. (2009, 2010). A similar notion of variability measure was proposed by Furman et al. (2017) with an emphasis on the Gini deviation. We will explain in Section 2 the differences between our general definition and the ones given in the literature; in particular, the inter-quantile difference does not satisfy the definition of deviation measure of Rockafellar et al. (2006) due to its lack of convexity.

Our main contribution is a collection of results towards a general theory of variability measures, with particular emphasis on the three parametric classes mentioned above. Various novel properties are studied to underline the special role these measures play among other variability measures. Since statistical inference for VaR, ES, and expectiles is well developed (see e.g. Shorack and Wellner (2009) for VaR and Krätschmer and Zähle (2017) for the expectiles), the estimation of the corresponding variability measures is quite straightforward.

The rest of the paper is organized as follows. In the remainder of this section, we introduce some notation. The definitions of the three classes of variability measures induced by VaR, ES, and the expectiles is presented in Section 2, with some basic properties. In Section 3, we summarize many properties of some common variability measures which are arguably desirable in practice. A characterization result of these measures is established. The stochastic ordering of the three classes of variability measures based on pointwise comparison is discussed in 4. In Section 5, we discuss non-parametric estimation of the three classes of variability measures. We obtain the asymptotic normality and the asymptotic variances explicitly for the empirical estimators. It may be undesirable and financial unjustifiable to choose the same probability level for the three classes of variability measures induced by VaR, ES, and the expectiles; see Li and Wang (2019) for a detailed analysis on plausible equivalent probability levels when ES is to replace VaR. A simple analysis of a cross-comparison of an equivalent probability level for the variability measures using different distributions is carried out in Section 6. A small empirical analysis using the variability measures on the S&P index is conducted in Section 7, where we observe the differences between these variability measures during different economic regimes. Further, we explore the symmetric variability orders between log-returns of Facebook and Berkshire Hathaway in 2020. In Section 8, we conclude the paper with some discussions on the suitability of the three classes in different situations. Appendix A contains a list of classic variability measures, and proofs of all results are put in Appendix B.

Notation. Throughout the paper, is the set of all random variables in an atomless probability space with finite -th moment, , and is the set of essentially bounded random variables. is the set of all random variables, and is the set of all distributions on . For any , represents the distribution function of , its left-quantile function, and is a uniform random variable such that almost surely. The existence of such a for any is given, for example, in Lemma A.32 of Föllmer and Schied (2016). Two random variables and are said to be comonotonic if there exist two increasing functions such that and . We write if and have the same distribution. In this paper, the terms “increasing” and “decreasing” are meant in the non-strict sense.

2 Definitions

2.1 Basic requirements for variability measures

Generally speaking, a variability measure is a functional that quantifies the magnitude of variability of random variables. In order for our definition to be as general as possible, we only require three natural properties.

Definition 1.

A variability measure is a functional satisfying the following properties.

-

(A1)

Law invariance: if and , then .

-

(A2)

Standardization: for all .

-

(A3)

Positive homogeneity: there exists such that for any and . The number is called the homogeneity index of .

The three properties in Definition 1 are the most basic, and they are satisfied by virtually all examples in the literature; a useful variability measure typically satisfies other desirable properties (see Section 3).

Some examples of classic variability measures are given in Appendix A. Notice that in the literature there are some relative measures of variability that are only defined for positive random variables, such as the Gini coefficient or the relative deviation (see Appendix A). In this paper, we do not deal with these cases, although our definition can be easily amended to include them by replacing with a positive convex cone. We call the set the effective domain of .

Remark 1.

A deviation measure in the sense of Rockafellar et al. (2006) satisfies, in addition to (A2) and (A3) with homogeneity index , also subadditivity and strict positivity for non-constant random variables. As we will see in Section 3, the latter two properties are not satisfied by the inter-quantile difference. For this reason, our more general definition is more suitable here than the one of Rockafellar et al. (2006). Alternatively, Furman et al. (2017) required location-invariance instead of positive homogeneity, but this property is not satisfied by relative variability measures. Thus, we identify (A1), (A2), (A3) as the defining properties of a variability measure, and all other properties, such as location invariance and subadditivity, will be additional properties that may or may not be satisfied, as we will discuss in see Section 3.

Remark 2.

In applications, we may choose the domain of a variability measure as a convex cone contained in . For risk measures, the domain plays an essential role, which is often chosen as a general convex cone containing , because many risk measures cannot be naturally extended to ; see e.g., Filipović and Svindland (2012). For variability measures defined on a convex cone , since it takes non-negative values (thus, no issues with which occur for some risk measures), we could always extend the domain by mapping to without affecting the properties studied in this paper.

2.2 Three one-parameter families of risk measures

Value at Risk (VaR), Expected Shortfall (ES) and expectiles are very popular financial risk measures (see e.g. Embrechts et al. (2014) and Emmer et al. (2015)). We recall the basic definitions below.

-

(i)

The right-VaR (right-quantile): for ,

The left-VaR (left-quantile): for ,

-

(ii)

The ES: for ,

The left-ES: for ,

-

(iii)

The expectile: for ,

In the above, and are finite on , while , and are finite on . We only define expectiles on since generalizing them beyond is not natural; on the other hand, can be naturally defined on a set larger than by taking possibly infinite values.

2.3 Three one-parameter families of variability measures

We now introduce the variability measures induced by the aforementioned risk measures, that are the main object of the paper.

-

(i)

The inter-quantile difference: for ,

It is obvious that is finite on .

-

(ii)

The inter-ES difference: for ,

Here, takes values in , and takes values in , and hence the above is well defined on .

-

(iii)

The inter-expectile difference: for ,

and we set by definition for .

We consider also the limiting cases

which is the range functional, and it is simply denoted by . Both and belong to the class of distortion riskmetrics (Wang et al. (2020a, b)), with many convenient theoretical properties. On the other hand, does not belong to this class, but it also has several nice properties, inherited from those of expectiles.

Theorem 1.

For each , the following statements hold.

-

(i)

, , and are variability measures.

-

(ii)

The effective domains of , , and are , , , and , respectively.

-

(iii)

Each of , and is increasing in .

-

(iv)

For each , the following alternative formulations hold:

It is straightforward to check that for , is equal to two times the mean median deviation (see Appendix A, item (v)). The next proposition shows that it suffices to consider , as we will tacitly assume in most results of the next sections.

Proposition 1.

For each , , and

3 Comparative properties and characterization

In this section, we study comparative advantages of , and , among with several other measures of variability, namely the standard deviation (STD), the variance, the mean absolute deviation (MAD), the Gini deviation (Gini-D), and the range; see Appendix A for the definition of these classic variability measures.

We consider the following additional properties of a variability measure , which are all arguably desirable in some situations. In what follows, is the convex order, defined by if for all convex such that the above two expectations exist.

-

(B1)

Relevance: if is not a constant, and there exists such that for all with .

-

(B2)

Continuity: as for all .

-

(B3)

Symmetry: for all .

-

(B4)

Comonotonic additivity (C-additivity): for all comonotonic .

-

(B5)

Convex order consistency (Cx-consistency): if .

-

(B6)

Convexity: for all and .

-

(B7)

Mixture concavity (M-concavity): is concave, where is defined by for .

-

(B8)

Location invariance (L-invariance): for all and .

Relevance (B1) requires to report a positive value for all non degenerate distributions, and the value of should not explode if . Continuity (B2) is very weak and unspecific to the effective domain of . If is finite on for some , then (B2) is implied by continuity. Symmetry (B3) means that is indifferent to the positive and the negative sides of the distribution, and this property is in sharp contrast to classic risk measures for which positive and negative values are interpreted very differently (deficit/surplus or loss/profit). The symmetry property of the measures of variability motivates and simplifies the application of the measures. C-additivity (B4) is a convenient functional property which allows for a characterization result below. The properties (B5)-(B7) describe natural requirements for to increase when the underlying distribution is more spread out in some sense; see Wang et al. (2020a) for further motivation and explanations of these properties. Finally, (B8) requires that variability is measured independently of the location of the distribution and is indeed imposed as an axiom for measures of variability by Furman et al. (2017).

In Table 1 below, represents the homogeneity index. Table 1 shows properties of different variability measures including the inter-quantile, inter-ES, and inter-expectile differences, as well as the aforementioned classic variability measures.

| variance | STD | MAD | Gini-D | range | ||||

| relevance | NO | YES | YES | YES | YES | YES | YES | YES |

| continuity | YES | YES | YES | YES | YES | YES | YES | YES |

| symmetry | YES | YES | YES | YES | YES | YES | YES | YES |

| C-additivity | YES | YES | NO | NO | NO | NO | YES | YES |

| Cx-consistency | NO | YES | YES | YES | YES | YES | YES | YES |

| convexity | NO | YES | YES | YES | YES | YES | YES | YES |

| M-concavity | NO | YES | NO | YES | YES | NO | YES | YES |

| L-invariance | YES | YES | YES | YES | YES | YES | YES | YES |

| homogeneity () | 1 | 1 | 1 | 2 | 1 | 1 | 1 | 1 |

| effective domain |

Theorem 2.

The statements in Table 1 hold true.

The proof of Theorem 2, thus checking the properties in Table 1, relies on several existing results on properties of risk measures and distortion riskmetrics from Newey and Powell (1987), Bellini et al. (2014, 2018), Liu et al. (2020) and Wang et al. (2020a).

Notably, the inter-ES difference satisfies all properties (B1)-(B8), along with the Gini deviation and the range. Next, we establish that any variability measure satisfying (B1)-(B8) admits a representation as a mixture of for .

Theorem 3.

The following statements are equivalent for a variability measure :

-

(i)

satisfies (B1)-(B8).

-

(ii)

satisfies (B1)-(B4) and one of (B5)-(B6).

-

(iii)

is a mixture of , that is, there exists a finite Borel measure on such that

(1)

The measure in (1) for a given is generally not unique. Using Proposition 1, we can require in (1) to be supported on instead of .

Example 1.

As we have seen from Theorem 2, all of , , are invariant under location shifts. In the next result, we show that each of the one-parameter families , , characterize a symmetric distribution up to location shifts.

Proposition 2.

Suppose that has a symmetric distribution, i.e., . Each of the curves , and for , if it is finite, uniquely determines the distribution of .

Remark 3.

If the distribution of is not symmetric, none of , and for determines its distribution up to location shifts. This is because the inter-quantile difference curve does not determine the quantile curve . For instance, given a quantile curve , we can define another quantile curve by

where is any continuous function satisfying for , such that is increasing in . The inter-quantile difference curves of and are the same, but the distributions of and are not the same up to a location shift unless is a constant.

Remark 4.

From Kusuoka (2001) it is well known that any coherent risk measure admits a representation as a supremum of mixtures of ES; see Bellini et al. (2014) for the case of expectiles. One naturally wonders whether an inter-expectile difference can be represented as the supremum of mixtures of inter-ES differences, i.e., the supremum over functions of form (1). Rather surprisingly, it turns out that such a relationship does not hold in general, as illustrated by Example 3 in Section 4.

4 Symmetric variability orders

Since the variability measures can be easily estimated from real data (see Section 5 below), one may conclude some ordering relations between two data sets with ordered measures of variability. For this purpose, we consider stochastic orders induced by pointwise comparison of inter-quantile, inter-ES, and inter-expectile differences. The first case has been studied in Townsend and Colonius (2005) under the name of quantile spread order, defined as follows:

Note that the order is weaker than the well-known dispersive order, defined by

for which we refer e.g. to Müller and Stoyan (2002) and Shaked and Shantikumar (2007). We define two stochastic orders based on inter-ES and inter-expectile differences as follows:

It turns out that for symmetric random variables, these orders are equivalent to the dilation order , defined by

as shown in (v) and (vi) below; the other properties are summarized in the following.

Proposition 3.

Let . The following statements hold:

-

(i)

For any , ; .

-

(ii)

If , then and ;

-

(iii)

; .

-

(iv)

.

-

(v)

and .

-

(vi)

If and are symmetric with respect to their means, then .

In case or is not symmetric, then the equivalence relations in (vi) may fail, as the following simple example shows. Therefore, the two new orders and are generally weaker than the dilation order. This provides more flexibility for these new orders in real-data applications, as we will illustrate in Section 7.

Example 2.

Let

Then , and

Hence, for each . Also, by a straightforward computation,

It follows that for each . However, because and have the same mean, and the support of is not contained in that of . This shows that and do not imply .

Finally, in the asymmetric case the and orders are not related. In the next example we have that but , and a (real-data) example in which the opposite situation occurs can be found in Section 7.

Example 3.

Let

Then

Hence for each and . Also,

Since , it follows that .

5 Non-parametric estimators

The properties of non-parametric estimators of , and can be derived from those of VaR, ES and expectiles, as we will explain in this section.

Suppose is an iid sample from a random variable . Recall that the empirical distribution of is given by

Let be the empirical estimator of , obtained by applying to the empirical distribution of . Similarly, let and be the empirical estimators of and . We will establish consistency and asymptotic normality of the empirical estimators, based on corresponding results on empirical estimators of VaR, ES and expectiles in the literature, e.g., Chen and Tang (2005), Chen (2008), and Krätschmer and Zähle (2017). We make the following standard regularity assumption on the distribution of the random variable .

-

(R)

The distribution of is supported on a convex set and has a positive density function on the support.

Denote by and let . We will show in the next theorem that the asymptotic variances of the empirical estimators for and are given by, respectively,

| (2) | ||||

| (3) |

and that for is given by

| (4) |

where for ,

Theorem 4.

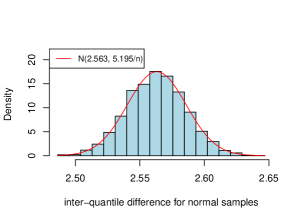

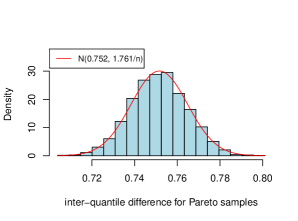

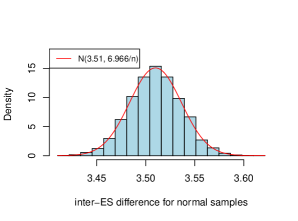

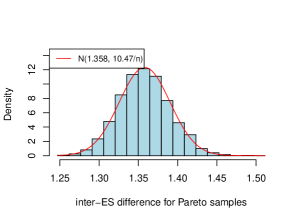

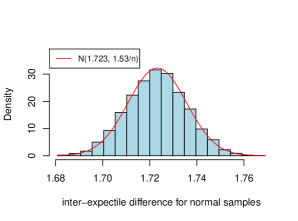

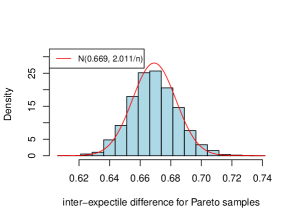

Simulation results are presented in Figure 1 for in the case of standard normal and Pareto risks with tail index , that confirm the asymptotic normality of the empirical estimators in Theorem 4. More general asymptotic results for -mixing processes could be similarly established using results in Chen (2008) and Krätschmer and Zähle (2017). For the sake of space we do not discuss here the case of dependent observations.

Remark 5.

For part (i) of Theorem 4, the assumption (R) is used to guarantee that the empirical quantiles converge to the true quantile (more precisely, we only need the quantile function to be continuous at and ); this is not needed for the consistency statements on and in part (i).

Remark 6.

For a convex risk measure on an Orlicz heart , Krätschmer et al. (2014, Theorem 2.6) showed that the empirical estimator is strongly consistent for a stationary and ergodic data sequence ; that is, almost surely. For a general variability measure , a similar result holds if we further assume that is norm-continuous on , following the same arguments as in the proof of Theorem 2.6 of Krätschmer et al. (2014), where the only used property of is norm-continuity. This statement includes consistency of and on in part (i) of Theorem 4 as special cases. For real-valued convex risk measures, norm-continuity is implied by monotonicity and convexity. To establish such continuity, monotonicity is essential and it plays the role of positivity in the Namioka-Klee theorem for linear functions; see Biagini and Frittelli (2009). For convex variability measures, since monotonicity is not satisfied, we have to assume norm-continuity for the analog of Theorem 2.6 of Krätschmer et al. (2014).

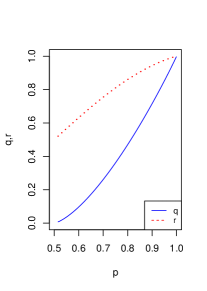

6 A rule of thumb for cross comparison

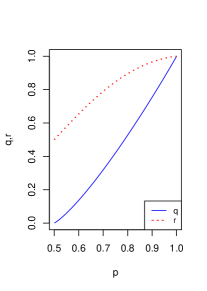

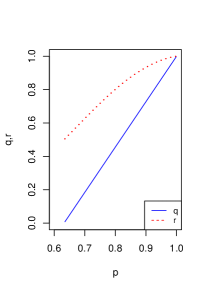

As mentioned in the introduction, we are interested in comparing the inter-quantile, the inter-ES and the inter-expectile differences. Due to the different meanings of the parameter in , and , there is no reason to directly compare , and using the same probability level . For a fair cross comparison, we may calibrate such that the variability measures have the same value, that is,

for some common choices of distributions. In particular, we will consider normal (N), - and exponential distributions as benchmarks, and the curves of and in terms of for these distributions are plotted in Figure 2. We observe that the values of is typically much closer to than the corresponding or . The matching value of is smaller than the corresponding but the relationship between and is close to linear; a corresponding observation on comparing VaR and ES is noted by Li and Wang (2019), where they obtained the ratios for normal risks and for exponential risks (this corresponds to the straight line in Figure 2(b)).

In empirical studies, it has been costumary in the literature to use the matching values for normal distribution as a rule of thumb for general comparisons; note that the location and scale parameters are irrelevant for such a comparison due to location-invariance and positive homogeneity. Roughly, we obtain

for . For the particular choice of , it means that for normal risks. We will compare these variability measures on real data in the next section, confirming the well-known departure from normality of financial returns.

7 Empirical analysis

In this section, we illustrate the three classes of variability measures studied in this paper by means of a few empirical studies on financial data.

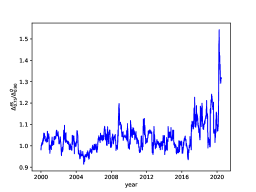

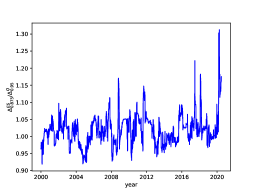

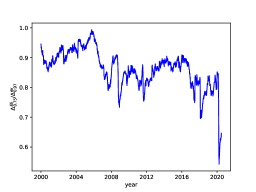

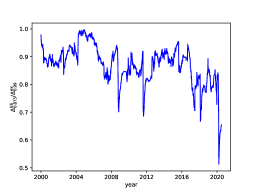

We first analyze the difference between the performances of these variability measures during different periods of time (different economic regimes). Our data are the historical price movements spanned from to of the S&P index.111The source of the price data is Yahoo Finance. We use its daily log-loss data222We use the log-loss (negative log-return) to be consistent with most studies on financial asset return data. Note that since our variability measures are symmetric, using log-losses is equivalent to using log-returns. over the observation period with moving window of days for daily estimation of the variability measures. To compare the relative performance of the three measures, we report the ratios and for the S&P daily log-losses in Figures 3 and 4 using the rule of thumb for obtained in Section 6 induced by the normal distribution. In Figure 3, spikes in the ratio of are located around the subprime crisis and the COVID- period. On the other hand, the ratio in Figure 4 experiences a down-slide around the subprime crisis and the COVID- period. These results suggest that is more sensitive to extremely large losses than , but is even more sensitive than . Recall that these ratios should be if the underlying losses are normally distributed, whereas we observe and for most dates during the period of 2000 - 2020 ( is almost always smaller than 1). Hence, Figures 3 and 4 confirm that the log-losses of S&P are not normally distributed, and in fact, they typically show paretian tails, as is well studied in the literature (see, e.g., McNeil et al. (2015)).

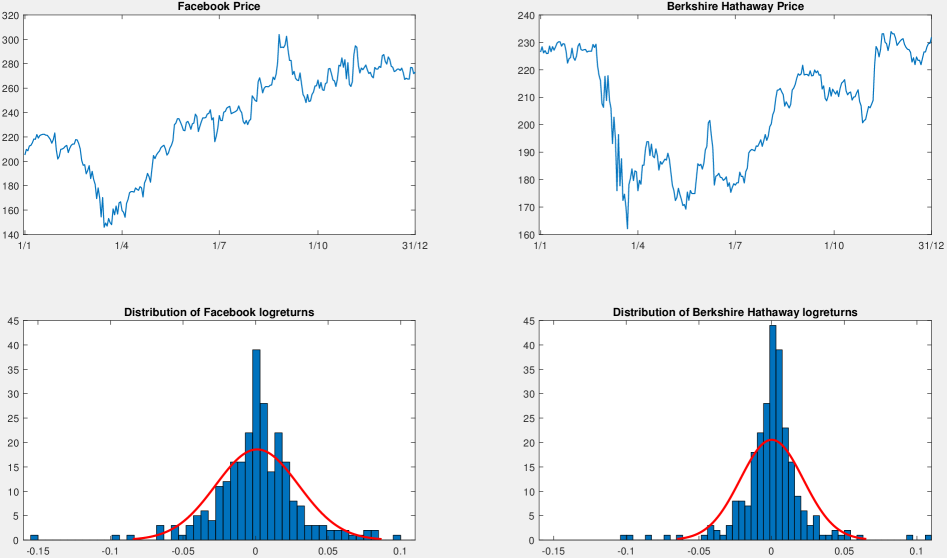

As a second empirical illustration, we compare the distributions of the log-returns of Facebook and Berkshire Hathaway Inc. during the year 2020, displayed in Fig. 5. In this very peculiar year Facebook made with annualized volatility , and Berkshire Hathaway’s made only with annualized volatility . In order to check if the two distributions are comparable in one of the symmetric variability orders considered in Section 4, we recall that an equivalent condition for the dilation order is given by

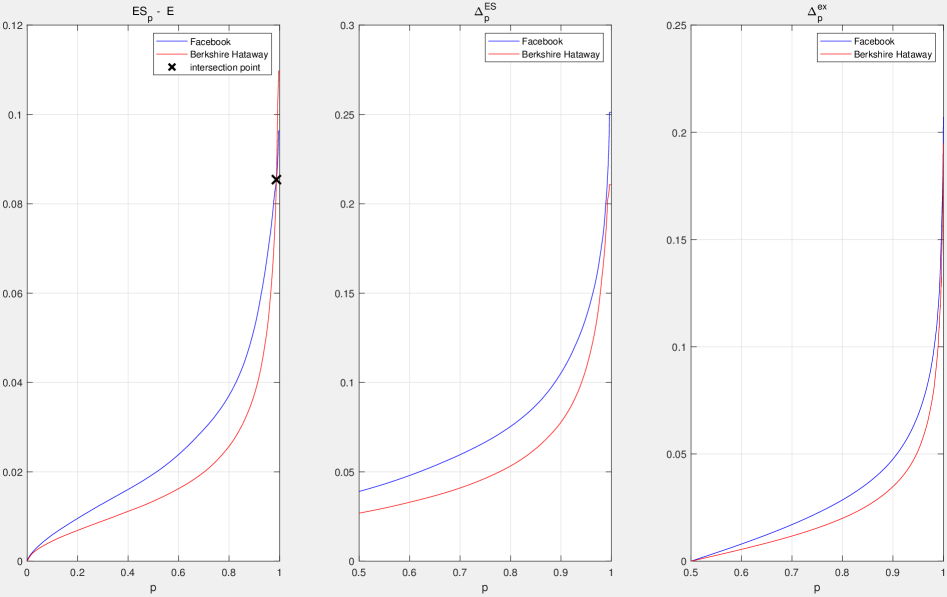

We see in the left panel of Fig. 6 that there is an intersection point in the curves, so Facebook’s log-returns do not dominate Berkshire Hathaway’s according to the dilation order (and vice versa). In this specific example, this is due to the presence of two large values in the distribution of Berkshire Hathaway’s daily log-returns. On the contrary, looking at the center and left panels of Fig. 6 we see that there are no intersection points, so Facebook’s log-returns dominate Berkshire Hathaway’s according to both the and orders. Hence, both and are able to model an ordering relation in the variability between two distributions, when the classic dilation order fails to hold, and this shows the additional flexibility of the new orders over the classic notion.

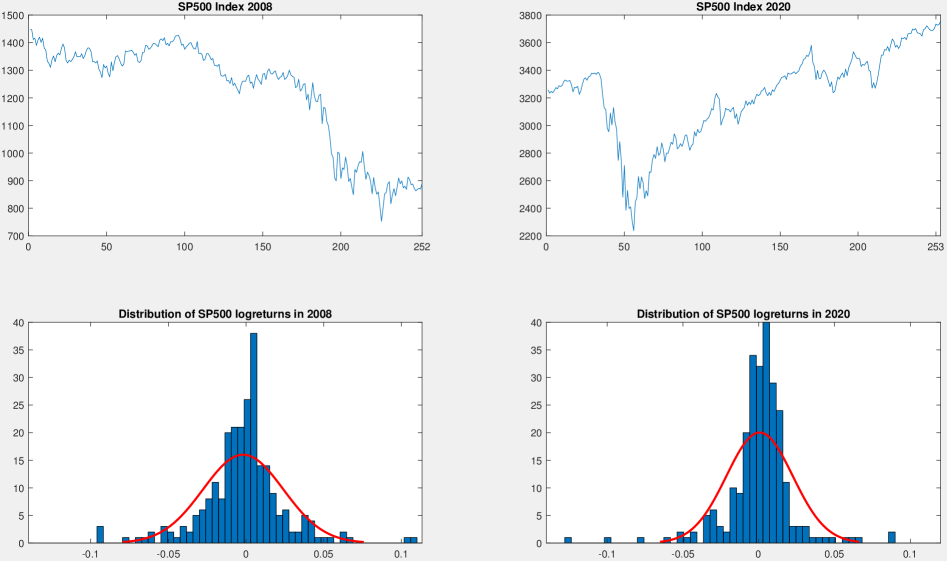

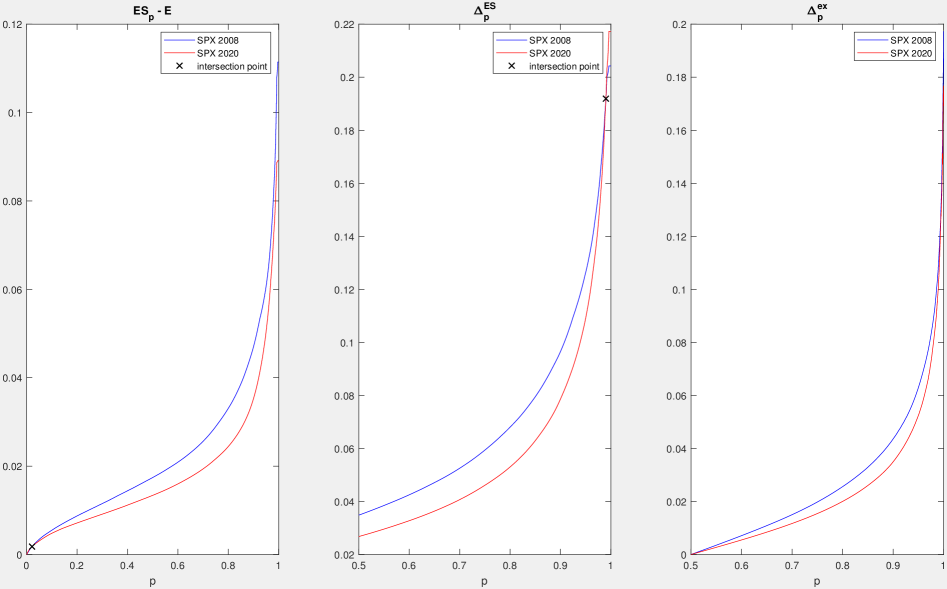

As a third example, we compare the distributions of log-returns of the S&P500 Index in 2008 and in 2020, displayed in Fig. 7. As in the previous example, we plot the relevant curves in Fig. 8. Here there is an intersection point both in the left and in the center panel, and no intersections in the right panel, so only the order applies.

In order to give a first exploratory assessment of how often the various symmetric variability orders do apply, we checked the comparability of daily log-returns of the S&P500 Index for each pair of years ranging from 2008 to 2020, for a total of pairs. The results are reported in Table 2. It turns out that in cases the order applies, and so as a consequence also the other two weaker orders apply. In the remaining cases, one or both of the and orders apply in cases, so when the order does not apply, we have a fraction of of cases in which the data can still be compared. Notice also that the order without the order never occurred for this dataset; however, Example 3 in Section 4 shows that also this situation is theoretically possible.

| N | pairs of years (XX) | |||

|---|---|---|---|---|

| 66 | all the others | |||

| 6 | ||||

| 0 | - | |||

| 2 | ||||

| 4 |

8 Conclusion

In this paper, we introduce variability measures induced by three very popular parametric families of risk measures, that is, the inter-quantile, the inter-ES, and the inter-expectile differences. The three classes of variability measures enjoy many nice theoretical properties (Theorem 1); in particular, each of them characterizes symmetric distributions up to a location shift (Proposition 2). We study several desirable functional properties of general variability measures including the above three classes and many other classic ones; a grand summary is obtained in Theorem 2 and Table 1. The family of variability measures that satisfy a set of desirable properties is characterized as mixtures of inter-ES differences (Theorem 3). It is important to note that the three classes of variability measures introduced in this paper are well defined on and that each depends on a single parameter which allows for flexible applications. This distinguishes them from other deviation measures (e.g., Rockafellar et al. (2006)) where no parametric family is given. The empirical estimators of the inter-quantile, the inter-ES, and the inter-expectile differences can be formulated based on those of , and the expectile, and the asymptotic normality of the estimators is established (Theorem 4). In the financial application, we observe that the behaviour of these variability measures is similar to the corresponding parametric families of risk measures. However, a comparison of different ratio of the variability measures reveals that is the most sensitive to extreme losses, and is the least sensitive.

For the end-user, if tail risk is of particular concern, then may be a better variability measure to use, as it captures tail-heaviness quite effectively. However, is usually cumbersome in computation and optimization because of the lack of explicit formulas in terms of quantile or distribution functions; another technical disadvantage is that is not concave with respect to mixtures. On the other hand, if robustness is more important and tail risk is not relevant, then is a good choice, because quantiles are easy to compute and they are generally more robust than coherent risk measures including ES and expectiles (see Cont et al. (2010)). Moreover, is well defined on risks without a finite mean; nevertheless we should keep in mind that ignores tail risk just like a quantile. Finally, lies somewhere in between and regarding the above considerations, which giving rise to a good compromise; further, it is the only one among the three classes that is concave with respect to mixtures (see Table 1), and it is the building block for many other measures of variability (see Theorem 3).

In the literature, risk measures are commonly defined on a space of both positive and negative random variables. For this reason, our variability measures are also defined on such spaces, and we omit a detailed study of relative variability measures which are defined only for positive random variables. Relative variability measures include important examples such as the relative deviation and the Gini coefficient; see Appendix A. By replacing classic risk measures with relative risk measures (e.g., Peng et al. (2012)), one could define new classes of relative risk measures. On the other hand, other parametric families of risk measures, such as entropic risk measures (e.g., Föllmer and Schied (2016)) and RVaR (e.g., Embrechts et al. (2018)), can also be used to design flexible variability measures.

Appendix A Classic variability measures

Below we list some classic variability measures, which are formulated on their respective effective domains.

-

(i)

The variance ()

-

(ii)

The standard deviation (STD):

-

(iii)

The range ():

-

(iv)

The mean absolute deviation (MAD):

-

(v)

The mean median deviation (MMD):

-

(vi)

The Gini deviation (Gini-D):

-

(vii)

The relative deviation:

-

(viii)

The Gini coefficient:

Here, , is the set of all non-negative random variables in with .

Appendix B Proofs of main results

Proof of Theorem 1.

-

(i)

Law invariance (A1) is obvious. For standardization (A2), note that the risk measures are all monetary (Föllmer and Schied (2016)) and satisfies for any constant . Hence, for a constant , . Positive homogeneity follows from that of , , , and .

-

(ii)

The effective domains of these variability measures can be easily checked from the effective domain of the corresponding risk measures.

-

(iii)

Since is increasing in and is decreasing in , is increasing in . The same applies to and .

-

(iv)

It is well known that, for , ; see e.g., Föllmer and Schied (2016, (4.44)). Hence,

The formula for , follows directly from definition.

Proof of Theorem 2.

We first explain some general observations on all variability measures in Table 1. The effective domains and the homogeneity indices follow directly from definition. Continuity (B2) is implied by continuity since all variability measures are finite and thus continuous on their effective domains. Symmetry (B3) and location invariance (B8) are straightforward to check, and they hold for all variability measures in Table 1.

The conditions (B5)-(B7) are connected. In particular, Theorem 3 of Wang et al. (2020a) states that (B5)-(B7) are equivalent for distortion riskmetrics, which are functionals satisfying (A1), (B4) and some continuity assumptions. It is well known that the inter-quantile differences and the inter-ES differences are distortion riskmetrics.

Next, we explain that convexity (B6) implies Cx-consistency (B5) for all variability measures we consider. By Theorem 2.2 of Liu et al. (2020), all law-invariant convex risk functionals, i.e., functionals satisfying (A1), (B6) and (B8), can be written as the supremum of a family of convex distortion riskmetrics. Each distortion riskmetric is Cx-consistent as stated in Theorem 3 of Wang et al. (2020a), and hence (B5) is implied by (B6). The only negative statement for (B5) is made for the inter-quantile difference, which is a non-convex distortion riskmetric; this is shown in Table 1 of Wang et al. (2020a), which contains also a list of other examples of distortion riskmetrics with their corresponding properties. Hence, the inter-quantile difference does not satisfy any of (B5)-(B7).

It remains to verify (B1), (B4), (B6), (B7) for each variability measure.

-

(i)

The following example shows that does not satisfy (B1). Take such that and . Notice that is not a constant but . C-additivity (B4) is satisfied since is a distortion riskmetric. (B6)-(B7) are explained above.

-

(ii)

, Gini-D and range are all convex distortion riskmetrics; see Table 1 of Wang et al. (2020a). Hence, they all satisfy (B4)-(B7). Relevance (B1) can be easily verified.

-

(iii)

If is not a constant, by Newey and Powell (1987, Theorem 1), is strictly increasing in , which means that for . By Proposition 7 of Bellini et al. (2014), is increasing in , so for , for . Thus and Relevance (B1) is satisfied. Convexity (B6) is satisfied by Theorem 1 (iv) and convexity of expectiles.

We show that M-concavity (B7) is not satisfied by via the following example from Bellini et al. (2018). Take . Define by , and ; by , . Then and .

Let and . Then

and hence is not mixture concave.

C-additivity (B4) is not satisfied since by Theorem 3, a variability measure satisfying (B1)-(B5) must satisfy (B7).

-

(iv)

For the variance, Relevance (B1) can be easily verified. Variance does not satisfy (B4) since (B4) requires the homogeneity index to be . For (B6), the variance is well known to be convex (Deprez and Gerber (1985)); see also Example 2.2 of Liu et al. (2020). The variance satisfies M-concavity (B7) because of the well known equality

Since is the minimum of mixture-linear functionals, we know that it is mixture concave.

-

(v)

For STD, Relevance (B1) can be easily verified. C-additivity (B4) is not satisfied by STD since STD is not additive for comonotonic random variables and with correlation less than . STD is convex (B6); see Example 2.1 of Liu et al. (2020). To show that STD satisfies M-concavity (B7), take and let for . By definition,

which is equivalent to .

-

(vi)

For the mean absolute deviation (MAD), Relevance (B1) can be easily verified. MAD satisfies convexity (B6), since, for and ,

We give an example showing that MAD does not satisfy M-concavity (B7). Take , and . Let and . It is easy to calculate that , , , and . On the other hand,

Therefore,

and hence MAD is not mixture concave.

C-additivity (B4) is not satisfied by MAD since by Theorem 3, a variability measure satisfies (B1)-(B5) must satisfy (B7). ∎

Proof of Theorem 3.

Write the functional , which is the right-hand side of (1). First, obviously (i) implies (ii). It is also straightforward to check that (iii) implies (i), since for satisfies (B1)-(B8) by Theorem 2, and so is ; the only non-trivial statement is (B2) of which is guaranteed by Theorem 5 of Wang et al. (2020a), which shows that the representation belongs to a class of convex distortion riskmetrics with continuity (B2). Below, we show (ii)(iii).

Let be the effective domain of . Take such that . By (B4), . Hence, the homogeneity index of is .

Suppose that Cx-consistency (B5) holds. Take any and let and such that and are comonotonic. It is well known that ; see e.g., Theorem 3.5 of Rüschendorf (2013). Using (B4) and (B5), we have

Therefore, is subadditive, that is,

| (6) |

Note that convexity (B6) and homogeneity (A3) with together also imply subadditivity. Hence, either assuming (B5) or (B6), we get (6). It follows from (6) and (B1) that there exists such that where is the essential supremum of . Hence, is uniformly continuous with respect to the supremum norm. Moreover, as a consequence of (B1), (A3) and (6), is a convex cone that contains .

Theorem 1 of Wang et al. (2020a) states that a real functional on a convex cone that is uniformly continuous with respect to the supremum norm, law-invariant, and satisfying (B2) and (B4) is a distortion riskmetric in the sense of that paper; see (7) below. Further, Theorem 3 of Wang et al. (2020a) says that each of (B5)-(B7) is equivalent to the convexity of a distortion riskmetric. Hence, is a convex distortion riskmetric on . Theorem 5 of Wang et al. (2020a) gives a representation of convex distortion riskmetrics; that is, has a representation, for some finite measures and ,

| (7) |

By symmetry (B3), we know

Hence, we can take , and get

Relevance (B1) implies , which in turn implies , as the effective domain of is for . Hence, the two functionals and coincide on which contains . Also note that both and satisfy continuity (B2), and hence one can approximate any random variable outside with truncated random variables, and obtain that and also coincide on . ∎

Proof of Proposition 2.

-

(i)

If has a symmetric distribution, then by Theorem 1 (iv), we have

Assume and are symmetric distributions with finite for . It follows that for . By the left-continuity of the left-quantile, . By symmetry of the distribution of , we have almost every , and thus and have the same distribution.

-

(ii)

If has a symmetric distribution, then similarly to (i), we have Assume that and have symmetric distributions with finite for . It follows that for , holds, which means

(8) By taking a derivative of both sides of (8) with respect to , we get

at all common continuity points of and . Since both functions are right-continuous, we know that the two functions are identical. This argument can be applied to any . Similarly to part (i), we conclude that and have the same distribution.

-

(iii)

If has a symmetric distribution, then similarly to (i), we have

Suppose and have symmetric distributions with finite for . Then for By symmetry, we observe that , which means , so for .

The expectile has alternative definitions from Newey and Powell (1987),

which leads to

Since is continuous in and takes all values in the range of , we know

for all , implying that the distributions of and are identical. ∎

Proof of Proposition 3.

(i), (ii), (iii) follow immediately, respectively from location invariance, positive homogeneity of order and symmetry of and , while (iv) follows immediately from the second part of the thesis of Proposition 1.

-

(v)

By passing if necessary to the random variables and , from (i) we can assume without loss of generality that . Then , and the thesis follows from Cx-consistency of and , for each .

-

(vi)

As in (v), we can assume without loss of generality that . Then , so , for each . From symmetry and the assumption it follows that the same inequality holds also for each , that implies by Theorem 3.A.5 in Shaked and Shantikumar (2007). Similarly, under symmetry , so for each , and since , the opposite inequality holds for . By reasoning as in the proof of Theorem 12 of Bellini et al. (2018), it follows that for each , where and are the usual stop-loss transforms of and ; the thesis then follows from Theorem 3.A.1 of Shaked and Shantikumar (2007). ∎

Proof of Theorem 4.

-

(i)

Let , , and be the empirical estimators of , , and based on sample data points. It is well known (e.g., Bahadur (1966)) that at each of continuous point of , which implies under assumption (R). Since and are law-invariant convex risk measures, by Theorem 2.6 of Krätschmer et al. (2014), and for each . Hence we have and .

-

(ii)

By Proposition 1 of Shorack and Wellner (2009, p.640), if assumption (R) is satisfied, then we have

(9) where is a standard Brownian bridge. With assumption (R), . Hence,

which has a Gaussian distribution. Using the covariance property of the Brownian bridge, that is, for , we have

Therefore, where is in (2), namely,

This completes the proof. ∎

Acknowledgements

We thank an Editor, an Associate Editor, and two anonymous referees for helpful comments. T. Fadina and R. Wang are supported by the Natural Sciences and Engineering Research Council of Canada (RGPIN-2018-03823, RGPAS-2018-522590).

References

- Artzner et al. (1999) Artzner, P., Delbaen, F., Eber, J.-M. and Heath, D. (1999). Coherent measures of risk. Mathematical Finance, 9(3), 203–228.

- Bahadur (1966) Bahadur, R. R. (1966). A note on quantiles in large samples. The Annals of Mathematical Statistics, 37(3), 577–580.

- Bellini et al. (2018) Bellini, F., Bignozzi, V. and Puccetti, G. (2018). Conditional expectiles, time consistency and mixture convexity properties. Insurance: Mathematics and Economics, 82, 117–123.

- Bellini and Di Bernardino (2015) Bellini, F. and Di Berhardino, E. (2015). Risk management with expectiles. The European Journal of Finance, 23(6), 487–506.

- Bellini et al. (2014) Bellini, F., Klar, B., Müller, A. and Rosazza Gianin, E. (2014). Generalized quantiles as risk measures. Insurance: Mathematics and Economics, 54(1), 41–48.

- Bellini et al. (2018) Bellini, F., Klar, B. and Müller, A. (2018). Expectiles, Omega Ratios and Stochastic orderings. Methodology and Computing in Applied Probability, 20, 855–873.

- Bellini et al. (2020) Bellini, F., Mercuri, L. and Rroji, E. (2020). On the dependence structure between S&P500, VIX and implicit Interexpectile Differences. Quantitative Finance, 20(11), 1839–1848.

- Biagini and Frittelli (2009) Biagini, S. and Frittelli, M. (2009). On the extension of the Namioka-Klee theorem and on the Fatou property for risk measures. In Optimality and Risk: Modern Trends in Mathematical Finance (F. Delbaen et al., Eds), 1–28. Springer, Berlin, Heidelberg.

- Chen (2008) Chen, S. X. (2008). Nonparametric estimation of Expected Shortfall. Journal of Financial Econometrics, 6, 87–107.

- Chen and Tang (2005) Chen, S. X. and Tang, C. Y. (2005). Nonparametric inference of Value-at-Risk for dependent financial returns. Journal of Financial Econometrics, 3, 227–255.

- Cont et al. (2010) Cont, R., Deguest, R. and Scandolo, G. (2010). Robustness and sensitivity analysis of risk measurement procedures. Quantitative Finance, 10(6), 593–606.

- David (1998) David, H. A. (1998). Early sample measures of variability. Statistical Science, 13(4), 368–377.

- Deprez and Gerber (1985) Deprez, O. and Gerber, H. U. (1985). On convex principles of premium calculation. Insurance: Mathematics and Economics, 4(3), 179–189.

- Embrechts et al. (2014) Embrechts, P., Puccetti, G., Rüschendorf, L., Wang, R. and Beleraj, A. (2014). An academic response to Basel 3.5. Risks, 2(1), 25-48.

- Embrechts et al. (2018) Embrechts, P., Liu, H. and Wang, R. (2018). Quantile-based risk sharing. Operations Research, 66(4), 936–949.

- Emmer et al. (2015) Emmer, S., Kratz, M. and Tasche, D. (2015). What is the best risk measure in practice? A comparison of standard measures. Journal of Risk, 18(2), 31–60.

- Filipović and Svindland (2012) Filipović, D. and Svindland, G. (2012). The canonical model space for law-invariant convex risk measures is . Mathematical Finance, 22(3), 585–589.

- Föllmer and Schied (2016) Föllmer, H. and Schied, A. (2016). Stochastic Finance. An Introduction in Discrete Time. Walter de Gruyter, Berlin, Fourth Edition.

- Furman et al. (2017) Furman, E., Wang, R. and Zitikis, R. (2017). Gini-type measures of risk and variability: Gini shortfall, capital allocation and heavy-tailed risks. Journal of Banking and Finance, 83, 70–84.

- Grechuk et al. (2009) Grechuk, B., Molyboha, A. and Zabarankin, M. (2009). Maximum entropy principle with general deviation measures. Mathematics of Operations Research, 34(2), 445–467.

- Grechuk et al. (2010) Grechuk, B., Molyboha, A. and Zabarankin, M. (2010). Chebyshev inequalities with law invariant deviation measures, Probability in the Engineering and Informational Sciences, 24(1), 145–170.

- Krätschmer et al. (2014) Krätschmer, V., Schied, A. and Zähle, H. (2014). Comparative and quantitiative robustness for law-invariant risk measures. Finance and Stochastics, 18(2), 271–295.

- Krätschmer and Zähle (2017) Krätschmer, V. and Zähle, H. (2017). Statistical inference for expectile-based risk measures. Scandinavian Journal of Statistics, 44(2), 425–454.

- Kusuoka (2001) Kusuoka, S. (2001). On law-invariant coherent risk measures. Advances in Mathematical Economics, 3, 83–95.

- Li and Wang (2019) Li, H. and Wang, R. (2019). PELVE: Probability equivalent level of VaR and ES. SSRN: 3489566.

- Liu et al. (2020) Liu, F., Cai, J., Lemieux, C. and Wang R. (2020). Convex risk functionals: representation and applications. Insurance: Mathematics and Economics, 90, 66–79.

- McNeil et al. (2015) McNeil, A. J., Frey, R. and Embrechts, P. (2015). Quantitative Risk Management: Concepts, Techniques and Tools. Revised Edition. Princeton, NJ: Princeton University Press.

- Müller and Stoyan (2002) Müller, A. and Stoyan, D. (2009). Comparison Methods for Stochastic Models and Risks. John Wiley & Sons, Ltd., West Sussex..

- Newey and Powell (1987) Newey, W. and Powell, J. (1987). Asymmetric least squares estimation and testing. Econometrica, 55(4), 819–847.

- Peng et al. (2012) Peng, L., Qi, Y., Wang, R. and Yang, J. (2012). Jackknife empirical likelihood method for some risk measures and related quantities. Insurance: Mathematics and Economics, 51(1), 142–150.

- Rockafellar et al. (2006) Rockafellar, R. T., Uryasev, S. and Zabarankin, M. (2006). Generalized deviation in risk analysis. Finance and Stochastics, 10, 51–74.

- Rüschendorf (2013) Rüschendorf, L. (2013). Mathematical Risk Analysis. Dependence, Risk Bounds, Optimal Allocations and Portfolios. Springer, Heidelberg.

- Shaked and Shantikumar (2007) Shaked, M. and Shantikumar, J.G. (2009). Stochastic Orders. Springer, New York.

- Shorack and Wellner (2009) Shorack, G. and Wellner, J. (2009). Empirical Processes with Applications to Statistics. Society for Industrial and Applied Mathematics.

- Townsend and Colonius (2005) Townsend, J.T. and Colonius, H. (2005). Variability of the max and min statistic: A theory of the quantile spread as a function of the sample size. Psychometrika, 70(4), 759–772.

- Wang et al. (2020a) Wang, Q., Wang, R. and Wei, Y. (2020a). Distortion riskmetrics on general spaces. ASTIN Bulletin, 50(4), 827–851.

- Wang et al. (2020b) Wang, R., Wei, Y. and Willmot, G. E. (2020b). Characterization, robustness and aggregation of signed Choquet integrals. Mathematics of Operations Research, 45(3), 993–1015.

- Wang and Zitikis (2021) Wang, R. and Zitikis, R. (2021). An axiomatic foundation for the Expected Shortfall. Management Science, 67, 1413–1429.

- Ziegel (2016) Ziegel, F. (2016). Coherence and elicitability. Mathematical Finance, 26(4), 901–918.