Revenue Maximization and Learning in Product Ranking

We consider the revenue maximization problem for an online retailer who plans to display in order a set of products differing in their prices and qualities. Consumers have attention spans, i.e., the maximum number of products they are willing to view, and inspect the products sequentially before purchasing a product or leaving the platform empty-handed when the attention span gets exhausted. Our framework extends the well-known cascade model in two directions: the consumers have random attention spans instead of fixed ones and the firm maximizes revenues instead of clicking probabilities. We show a nested structure of the optimal product ranking as a function of the attention span when the attention span is fixed. Using this fact, we develop an approximation algorithm when only the distribution of the attention spans is given. Under mild conditions, it achieves of the revenue of the clairvoyant case when the realized attention span is known. We also show that no algorithms can achieve more than 0.5 of the revenue of the same benchmark. The model and the algorithm can be generalized to the ranking problem when consumers make multiple purchases. When the conditional purchase probabilities are not known and may depend on consumer and product features, we devise an online learning algorithm that achieves regret relative to the approximation algorithm, despite the censoring of information: the attention span of a customer who purchases an item is not observable. Numerical experiments demonstrate the outstanding performance of the approximation and online learning algorithms.

Ningyuan Chen

Rotman School of Management, University of Toronto, ningyuan.chen@utoronto.ca

Anran Li

Department of Management, London School of Economics and Political Science,

a.li26@lse.ac.uk

Shuoguang Yang

Department of Industrial Engineering and Decision Analytics, HKUST, yangsg@ust.hk,

1 Introduction

Online retailing has seen steady growth over the last decade. According to the Digital Commerce analysis of the US Commerce Department’s year-end retail data, online sales constituted 16% of all retail sales in 2019 and reached higher levels due to the impact of COVID-19. For an e-commerce platform, one of the most important decisions is the products’ display positioning as it plays a crucial role in shaping customers’ shopping behavior. Empirical evidence abounds. Baye et al. (2009) find that a consumer’s likelihood of purchasing from a firm is strongly related to the order in which the firm is listed on a webpage by a search engine. In the online advertising industry, it has been widely observed that ads placed higher on a webpage attract more clicks from consumers (Agarwal et al. 2011, Ghose and Yang 2009). So the products displayed at the top positions can naturally enjoy higher exposure and therefore higher revenue. Given the importance of product ranking positions, the key question for online platform is how to rank the products to maximize the total revenue.

To answer the question, it is crucial to characterize and quantify how exactly customers react to products ranked in different positions. As one of the most popular behavioral models for product ranking, the cascade model has proved its salience and robustness in extensive experimental studies. In the cascade model, a customer with a reserved utility threshold sequentially views the displayed products from top to bottom. Had the customer viewed an item ranked in a certain position, if the product provides a net utility higher than her threshold, then the customer purchases the product and leaves right away. Otherwise, the customer moves on to view the product ranked in the next position. The model succinctly captures the one-way substitutability top-ranked products impose on bottom-ranked products. \Copyrev:no-satisficingIn a large experimental study, Craswell et al. (2008) find that the cascade model best explains the consumer behavior among a number of competing hypotheses. In particular, the customer views products sequentially and directly proceeds to purchase a product once the utility of the product exceeds an acceptable threshold, skipping the remaining products. The empirical success and theoretical tractability have made the cascade model the most widely used model in the literature (see, e.g., Kempe and Mahdian 2008).

However, the cascade model doesn’t provide a sufficient explanation to why a large fraction of customers may leave without purchasing a product. Indeed, the cascade model is originally motivated by clicks on search results, in which leaving without clicking on anything is rare. As a result, when using the cascade model for product ranking, “leaving” only occurs when a satisfactory product has been found or all products have been exhausted. In contrast, eye-tracking experiments show that consumers are more likely to examine the items near the top of the list and may leave without purchasing any product before reaching the bottom of the page (Feng et al. 2007). This phenomenon can be explained by the limited attention span of customers: if a customer arrives with an intrinsic attention span , then she may leave after viewing at most products regardless of whether a purchase has been made. According to Feng et al. (2007), consumers’ attention to an item decreases exponentially with its distance to the top, indicating that the distribution of attention span decays rapidly.

In this paper, we introduce random attention spans to the cascade model. In our model, the attention span of a customer determines the maximum number of items she is willing to view. We capture the limited attention by assigning each customer an attention span sampled from a distribution. When a customer arrives, she sequentially views the displayed products decided by the e-commerce platform (also referred to as the “firm” or the “retailer”) according to the cascade model. Once the attention span is reached or a satisfactory product is found, the customer leaves the firm. Thus, in our model, customers leave for two reasons. First, she may purchase a product in the display whose utility exceeds the threshold for the first time and leave, even though there could be another product with a higher utility within the rest of her attention span. Second, a customer may have exhausted her attention before finding anything satisfactory, in which case she leaves without buying anything or viewing more products.

Within the model, we study the firm’s optimal display order of products in order to maximize the potential revenue. When some of the information is unknown, such as the distribution of the attention span and the attractiveness of the products, we propose a learning algorithm that extracts the information from past observations and maximizes revenues simultaneously. Our contribution is threefold.

-

•

We incorporate attention spans and revenue maximization into the well-known cascade model. \Copyrev:cascadeIn the literature on cascade models, the objective of the firm is typically to maximize the purchase rate of customers, which renders the optimal ranking decision trivial. Indeed, the firm only needs to rank the products in the descending order of their attractiveness. To maximize the revenue, however, the prices of the products also have to be considered. When the attention span is fixed, we develop a dynamic programming algorithm to find the optimal ranking leveraging the fact that the products displayed at the bottom would not cannibalize the demand from the top. We show a surprising nested structure of the optimal ranking and the marginal revenue decreases as the attention span increases. That is, for customers of attention span , the optimal ranking of products is a subset of that for customers with attention span , although the additional product could be inserted in any position under optimality. We also provide sufficient and necessary conditions when the optimal ranking is a prefix as the attention span increases, which is a stronger structure than the nested.

-

•

Despite the structure of the optimal ranking under fixed attention spans, the computational cost can still be prohibitively high when the attention span is random. We develop a novel approximation algorithm for ranking optimization. It leverages the concavity of the optimal revenue as the attention span increases, thanks to the nested structure of the optimal ranking. When the random attention spans have an increasing failure rate (IFR), an assumption satisfied by many distributions, the resulting revenue ratio is relative to a clairvoyant who can access the realized attention span of each customer. We show that no ranking can achieve a revenue higher than 1/2 of the same clairvoyant. So the optimality gap of our algorithm is at most We also look at special cases, for example, when the optimal ranking is a prefix as the attention span increases or when the attention span is geometrically distributed, under which we can provide polynomial-time optimal algorithms. More interestingly, we show that the model and the algorithm can be generalized to the ranking optimization problem when consumers make multiple purchases in a single visit.

-

•

When the customers’ behavior is not known a priori, including the distribution of the attention spans and the attractiveness of the products, the firm may have to learn the unknown information and maximize the revenue simultaneously. What makes the problem challenging is the presence of consumer features and product features, two defining characteristics of online retailing. We consider the interaction (outer product) between both features that determines the product attractiveness. In addition, when customers leave the firm after making a purchase, the attention span information is censored. We propose an online learning algorithm by constructing unbiased estimators for the distribution of the attention span and combining them with the UCB approach to learn the product attractiveness. It achieves good performance ( regret) relative to the offline algorithm.

2 Literature Review

There are two streams of literature that are closely related to this study: (1) choice models (especially those taking the positions of products into account) and the corresponding optimal assortment planning, (2) the online learning of product ranking models. We review the two streams separately below.

2.1 Consumer Choice Models and Assortment Optimization

Most classic discrete choice models do not take the positions of products into account. The assortment optimization problem determines the optimal subset of products to include in the assortment to maximize the revenue. For example, Mahajan and van Ryzin (2001), Talluri and Van Ryzin (2004) show that under the well-known multinomial logit (MNL) model, the optimal assortment includes the products with the highest prices. Since this paper studies product ranking, the optimization involves the display order of products. It is significantly different from this line of literature in terms of models and algorithms.

rev:literature-rankingRecently, there have been a number of studies focusing on the business case when consumers may inspect products sequentially or based on their display positions, which is more relevant in online retailing. Next we compare our paper with these studies from the angles of model setups and results. Abeliuk et al. (2016) incorporate the position bias into the deterministic utilities of the MNL model. Their model describes the choice behavior in the population but does not provide a sequential choice model for individual customers. In Gallego et al. (2020), a customer arrives with a random attention span (similar to our model). She then chooses the preferred product among all the products in the span according to a choice model. This is in contrast to our model in which customers choose products sequentially and do not recall past products. Therefore, the optimal assortment in Gallego et al. (2020) does not exhibit the nested property (Theorem 4.3). The model in Aouad and Segev (2020) is similar to Gallego et al. (2020), but focuses on the MNL choice model. In Derakhshan et al. (2022), the customers search products sequentially. They first form their consideration set using an optimal stopping problem to maximize the expected surplus (due to the existence of search cost) and then choose the product inside the consideration set using the MNL model. This model doesn’t consider attention spans and focuses on the maximization of market share instead of revenues. In Chen et al. (2020), the authors model this problem using mechanism design when the sellers of the products have private information. A few recent papers extend discrete choice models to multiple stages. Flores et al. (2019), Feldman and Segev (2019), Liu et al. (2020), Gao et al. (2021) extend the MNL model to multiple stages. In each stage, the customer chooses a product based on the MNL model and leaves the market if a product is chosen; otherwise, the customer moves on to the next stage. The optimization problem is usually NP-hard and the authors give approximation methods. Although the model in this study can be treated as a special case of the models studied in these papers when each stage only has one product, there are two important differences. First, random attention spans are not considered in these papers. Second, we are able to derive richer structures and constant-bound approximation algorithms specific to our setting. Recently, Brubach et al. (2022) study a similar problem in the online matching framework. They design an approximate algorithm using linear programming that obtains -approximation relative to the LP upper bound. They also show that any algorithm can be arbitrarily bad relative to the clairvoyant that foresees the realized attention span. Our focus is on the nested structure of the optimal ranking for fixed attention spans, which allows us to drive a different approximation algorithm that achieves -approximation relative to the clairvoyant instead of the LP upper bound under the mild IFR assumption of attention span distribution. Moreover, our algorithm can be generalized to the purchase of multiple products (Section C in the Appendix), which has not been studied in the display optimization literature. In fact, our model can be viewed as a generalization of the well-known cascade model in Kempe and Mahdian (2008), which provides a quasi-polynomial-time approximation scheme (QPTAS) with a -approximation guarantee. We study the revenue maximization of the cascade model with random attention spans and derive structural properties of the optimal ranking. This setup and derived results are novel in the literature on cascade models. From the perspective of algorithmic design, the approximation algorithm proposed in this study is primarily inspired by the nested structure (Theorem 4.3). This structure and algorithm are not known in the papers mentioned above.

The random attention span considered in this study is analogous to similar behavioral setups in the literature. The primary motivation is the cognitive cost for customers to view and evaluate a large number of products in online retailing. Wang and Sahin (2018) build a model where the customers first form a consideration set by weighing between their expected utility and the search effort. The products in the consideration set are then thoroughly evaluated. Gallego and Li (2017) study the operational decisions of a model with random consideration sets where customers have a fixed preference order and each product enters the consideration set with an exogenous probability. Aouad et al. (2019) relax the fixed preference order assumption of the random consideration set model and focus on an assortment setting.

2.2 Online Learning

The multi-armed bandit framework has seen great success in modeling the exploration/exploitation trade-off for many applications. See Bubeck and Cesa-Bianchi (2012) for a comprehensive survey. In particular, in the field of revenue management, there have been many studies on demand learning and price experimentation using this framework, since the early seminal works by Araman and Caldentey (2009), Besbes and Zeevi (2009), Broder and Rusmevichientong (2012). Many extensions and new features have been studied, such as network revenue management (Besbes and Zeevi 2012, Ferreira et al. 2018, Chen et al. 2019), personalized dynamic pricing (Chen and Gallego 2020, 2018, Miao et al. 2019, Ban and Keskin 2020), limited price experimentations (Cheung et al. 2017), and non-stationarity (Besbes et al. 2015). Readers may refer to den Boer (2015) for a review of papers in this area.

There are several papers applying the multi-armed bandit framework to assortment planning, such as Rusmevichientong et al. (2010), Sauré and Zeevi (2013). Agrawal et al. (2019) consider the learning problem in the well-known MNL choice model under general assumptions compared to the literature. Their algorithm simultaneously explores the optimal assortment and attempts to maximize the revenue. Kallus and Udell (2020) investigate a similar problem under the contextual setting, when customers of different types have various preferences. They exploit the low-rank nature of the parameters to design efficient algorithms. In a related paper, Chen et al. (2018) assume that the contextual information can be non-stationary over time. Oh and Iyengar (2019) leverage Thompson sampling to learn the optimal assortment in the MNL model. The methods used in the literature cannot be directly applied to our model, because customers have dramatically different behavior in a product ranking model from the MNL model. Therefore, our algorithm differs in what to learn and how to actively experiment.

Our work is closely related to the papers studying the learning of the cascade model and product ranking models. The first such algorithm, called “cascading bandits”, is proposed in Kveton et al. (2015). It learns the optimal set of items to display in order to maximize the click rate, when the firm can observe the clicking behavior of past customers. Due to the wide range of applications in online advertising and recommendation systems of the cascade model, the online learning algorithm for such models under generic settings and contextual information has been extensively studied by Katariya et al. (2016), Zoghi et al. (2017), Lagrée et al. (2016), Kveton et al. (2015) and Zong et al. (2016), Cheung et al. (2019).

Compared to cascading bandits, our work has three major differences in problem formulations, which require novel treatments when designing algorithms. First, the items in the cascade model are only differentiated by their clicking probabilities. In our setting, the items generate different revenues. Second, the customers in the cascade model never abandon the system early, while in our model, they have a random attention span whose distribution needs to be learned. These two changes make our problem much more challenging. In the cascade model, the offline optimal solution is rather straightforward: finding the set of items with the highest clicking rates. In our model, it is not clear how to solve the offline problem exactly. Indeed, Kempe and Mahdian (2008) study a similar problem, and are only able to provide a -approximation algorithm. Third, when a customer purchases an item and leaves the system before reaching the limit of the attention span, this information is censored to the firm. We develop novel unbiased estimators to handle the censored observations.

Recently, the learning of product ranking models that generalize the cascade model has drawn attention in the Operations Research community. Ferreira et al. (2022) study a model in which the attention span and the clicking probabilities can be correlated. In this dimension, their model is more general than ours. They focus on maximizing the probability that a customer clicks at least one item. As a result, a greedy policy that ranks products sequentially is -optimal. The greedy policy is their learning target, whose structure can be exploited. In contrast, because we focus on revenue maximization, the target policy doesn’t have a structure to facilitate learning. Golrezaei et al. (2021) propose an algorithm that learns the optimal ranking in the presence of fake users. Gao et al. (2022) investigate the optimal pricing of the cascade model, in which the clicking and purchasing probabilities are parametrized and need to be learned. Their model is more structured and the nested structure doesn’t seem to hold in their model. Their major focus is on pricing and the design of the algorithm deviates significantly from ours. Niazadeh et al. (2020) consider the online learning problem of Asadpour et al. (2020) and focus on the maximization of the sum of a sequence of submodular functions, subject to a permutation of the inputs. It is closely connected to product ranking. However, because we focus on revenue maximization instead of clicking rates, the objective function is no longer submodular. A recent paper (Zhang, Ahn, and Baardman 2022) consider the joint problem of inventory and ranking under a click-then-convert model. The online learning portion of our model is similar to Cao and Sun (2019), Cao et al. (2019). The major distinction is our focus on maximizing the revenue instead of clicks. As mentioned above, the difference in the objective leads to completely different offline optimal solutions. Therefore, the resulting learning algorithm and the analysis differ.

3 The Model

Let denote the universal set of products. There is an online retailer (he) who chooses an assortment to display and rank them in order within slots. We use to refer to a permutation of , where is the set of all permutations of items in . More precisely, for , we use to denote the product displayed in the -th position.11endnote: 1We use () to represent the number of products in the assortment (ranking). Equivalently, for a product , the firm displays it in the -th position.

When a consumer (she) arrives, she views the products sequentially. However, the retailer cannot perfectly predict how many products she is willing to view. Therefore, we capture it by a random attention span , with distribution and tail probability denoted by for . For a consumer with attention span drawn from , she views product first and purchases it if it is satisfactory, i.e., the utility exceeds the no-purchase option. If she purchases the first product, then she leaves and the firm garners revenue . Otherwise, she moves on to the second product and repeats the process until she finds a product satisfactory or has viewed products, after which she leaves permanently. We assume that the probability of product being satisfactory is independent of everything else and denote it by , i.e., conditional on viewing product , the probability that she would purchase it. For the rest of the paper, we refer to it as conditional purchase probability. The consumer keeps viewing the products till she finds one satisfactory or exhausts her attention span , at which point she leaves without purchasing anything.

Therefore, each product is associated with a conditional purchase probability and price .22endnote: 2We assume and for all because removing products with zero conditional purchase probability or zero price from the list does not affect the results. Both quantities are assumed to be fixed and known in the offline setting. (In Section 5, we consider the case when is unknown and to be learned, which may depend on customer/product features.) We index the products such that

| (1) |

In other words, the products are indexed in the descending order of their prices and then in the descending order of their conditional purchase probabilities if the prices are equal. We assume no products have identical characteristics (the combination of price and conditional purchase probability).

Given that position is within a consumer’s attention span, her purchase probability of product is

In other words, the consumer purchases product if it is satisfactory while all products displayed earlier are not. is the cannibalization effect that a product at position exerts on the products displayed later.

3.1 Revenue Maximization for the Retailer

The firm’s goal is to choose an assortment of at most products, as well as its ranking , in order to maximize the expected revenue garnered from a potential consumer. From the earlier introduction we see that the expected revenue from a consumer with an attention span can be expressed as

| (2) |

When a customer arrives, as the retailer does not know her attention span, he takes the expected value of in (2) and obtains the total expected revenue

| (3) |

Therefore, the optimization problem for the firm is the joint assortment, i.e., choosing an such that , and ranking, i.e., deciding to maximize the total expected revenue from a random customer:

| (4) |

From (2) we can see that a product displayed at a later slot does not cannibalize the demand and therefore the revenue for the earlier. As a result, the optimal ranking would occupy all the slots and we only focus on assortments such that .

Note that one customer purchasing at most one product is a defining feature of discrete choice models. And for the cascade model, it is also primarily motivated by clicking one relevant item from online searches. Although the single item clicking/purchasing is widely adopted in the literature, the assumption may be limiting in online retailing: for example, a customer may add several products to the cart on Amazon before checking out. In Section C in the Appendix, by relaxing the cannibalization factor to a broader range, we extend the model to capture multiple purchases. That is, a customer may continue viewing and selecting the products after making some purchases. We show that most results derived in the next section still hold in that setting. In this sense, our work is more general than any of the current discrete choice model based display optimization literature.

Note that if for all , then our model encompasses the well-known classic cascade model (Craswell et al. 2008) as a special case. In this case, the online retailer tries to maximize the click rate, or equivalently, the purchasing probability of at least one product. For the cascade model, the optimal solution follows an intuitive structure: ranking the products in the descending order of their conditional purchase probabilities . In the general case when ’s are not identical, the products are differentiated along two dimensions, and it is unclear how to trade off between their conditional purchase probabilities and prices. For example, it is natural to rank a product with high conditional purchase probability and high price in the top position. However, in most practical scenarios, a product with higher conditional purchase probability is often associated with a lower price. Should the firm first display products that are more attractive or more profitable? How does the decision depend on the display capacity and the distribution of attention spans? We present the following example to shed some light on the complexity of these questions.

Example 3.1

Suppose the online retailer is selling three products, with revenues and conditional purchase probability as: , and . The capacity is . When the customer only views one product (), the optimal ranking is to display product one, which has the highest conditional purchase probability, in the first position. So an optimal ranking is and .

Now suppose the customer always views two products (). As the customer is willing to view more positions, the retailer would prefer to place a product with higher profit first, though it may have a lower conditional purchase probability. So an optimal ranking is and .

Next consider the case when the attention span is random. When and , it can be shown that the optimal ranking is neither nor . In fact, we have and . On the other hand, one can show that generates . Surprisingly, product three never appears in the optimal rankings for fixed attention spans, but should be placed on the top when the attention span is random.

Example 3.1 demonstrates the intricacy of the optimal ranking for random attention spans. A natural question, then, is whether the optimal ranking can be efficiently solved. It turns out that this is a notoriously difficult problem: It shares a similar formulation to the Slate Cascade Model in Kempe and Mahdian (2008), which claims that it is an open question to show the NP-hardness and provides a quasi-polynomial-time approximation scheme (QPTAS) with -approximation guarantee. We devote the next section to a new approximation algorithm that improves the approximation ratio to under a wide class of distributions of .

4 Best-x Algorithm for Optimal Ranking

With the complexity of the problem, we focus on developing a fast and easy-to-implement approximation algorithm for (4) and show there is a performance bound of the garnered revenue. Before presenting our approximation algorithm, we first investigate the revenue maximization problem when the attention span is fixed. It turns out that the problem has rich structures, based on which we then develop an approximation algorithm for random spans.

4.1 Revenue Maximization for Fixed Attention Spans

Suppose the retailer is expecting a customer with fixed attention span . Recall that is the number of available slots so for we can truncate it to . To maximize the revenue, the retailer would choose an assortment of size . We first provide a lemma characterizing the optimal ranking when the assortment is given.

Lemma 4.1

Fix attention span at . Suppose the assortment with size is given and maximizes among . We have that the products in are displayed in increasing order of their product indices, i.e., for .

Combined with condition (1), Lemma 4.1 implies that the products in the optimal ranking are displayed in the descending order of their prices and then in the descending order of their conditional purchase probabilities if there are ties in prices. Lemma 4.1 looks counter-intuitive at the first sight as it prioritizes the price over the conditional purchase probability. \Copyrev:expensive-firstTo understand the intuition, note that we focus on a customer with a fixed attention span , i.e., she would always view products or purchase the first satisfactory product. Given an assortment and ranking, by swapping expensive products to the top, the customer would view expensive products first, which increases the expected revenue.

Although Lemma 4.1 reduces the problem of finding the optimal ranking under a fixed attention span to finding the optimal assortment, it is still a daunting task. Namely, the number of assortments with given size is exponential in . It is computationally intractable to compare the expected revenues of all possible assortments/rankings and pick the optimal one. However, in light of Lemma 4.1, we can develop a dynamic program to quickly solve the joint assortment/ranking problem. The dynamic program employs both the optimal ranking result from Lemma 4.1 and the fact that the revenue can be computed recursively, i.e.,

| (5) | ||||

where we use to denote the sub-ranking of from to . Note that is the revenue from the display when the consumer has attention span . Intuitively, had we known the top position displays product , then the optimal sub-ranking should be chosen from the set to maximize by (5). This is because according to Lemma 4.1, the indices of the rest of the products should not be smaller than . This structure inspires Algorithm 1. In the algorithm, and stand for the optimal revenue and ranking for customers with attention span , when the products are chosen from .

| (6) |

With a slight abuse of notations, when is optimized to be , Lemma 4.1 uniquely determines its ranking order.

Although there might be multiple optimal rankings, Algorithm 1 always outputs one with a specific property. In particular, for two rankings , we say is lexicographically less than if for all , . The next result shows that Algorithm 1 always finds the optimal ranking with the least lexicographic value (referred to as the -optimal ranking) for attention span , denoted as .

Proposition 4.2

For a customer with fixed attention span , Algorithm 1 returns the -optimal ranking.

The property of -optimal rankings plays an important role in the analysis. Two rankings and are said to have a nested structure, or, , if for all there exists an such that and for all , if , then . In other words, if the assortment of is a subset of that of and the products are ranked in the same order.

The next proposition demonstrates a nested structure for the -optimal rankings as the customer’s fixed attention span increases.

Proposition 4.3

The -optimal rankings have a nested structure:

| (7) |

Proposition 4.3 states that the optimal ranking for customers of attention span can be obtained by inserting or appending one product to the optimal ranking for attention span . For example, suppose there are 5 products and the -optimal ranking for is . Then the -optimal ranking for might be or .

Proposition 4.3 naturally leads to a simple algorithm to compute for all . In particular, Algorithm 2 provides an iterative approach to compute the -optimal assortment. Note that we only need to find the optimal assortment, and the ranking is automatically determined by Lemma 4.1.

Based on Proposition 4.3, we are able to show the following structural property, which serves as a building block for the approximation algorithm. In particular, we can show that the marginal revenue from increasing the attention span is diminishing:

Theorem 4.4

The optimal revenues for fixed attention spans satisfy

4.2 Random Attention Spans: The Best-x Algorithm and Approximation Ratio

rev:exp-approxWhen the attention spans are random, the optimal ranking doesn’t necessary have the nested property in Proposition 4.3 (see Example 3.1) and dynamic programming cannot be applied. However, the optimal rankings for fixed attention spans lend us the following intuition: if we choose a proper and use the optimal ranking for customers with fixed attention span , then how does it perform when the attention span is actually random? To analyze the performance of such an algorithm, note that for a given ranking, the expected revenue is non-decreasing for consumers with longer attention spans. Therefore, if we use the optimal ranking developed for customers with fixed attention span , then for customers with attention span , the expected revenue is at least . Moreover, the fraction of customers with attention spans no less than is given by . Therefore, a lower bound for the expected revenue when applying the ranking for customers with random attention spans is . Because of this observation, we proceed to designing an approximation algorithm to maximize this lower bound:

| (8) |

The algorithm, referred to as the Best-x Algorithm, is summarized in Algorithm 3.

To analyze the performance of the Best-x Algorithm, we impose the following assumption on the distribution of consumers’ attention spans: {assumption} The distribution of the attention span has increasing failure rate (IFR). That is,

Note that many common distributions used in practice have IFR, including exponential distribution, geometric distribution, normal distribution, uniform distribution and negative binomial distributions (Rinne 2014). Therefore, Assumption 4.2 does not significantly limit the generality of our results. Moreover, empirical evidences (Feng et al. 2007) show that consumers’ attention to an item decreases exponentially with its distance to the top, which is consistent with the IFR assumption.

We aim to show the ranking returned from the Best-x algorithm can guarantee an approximation ratio of the optimal revenue. That is, if

for some under all possible inputs — conditional purchase probability , product revenue and attention span distribution — then we may claim that the Best-x Algorithm achieves approximation ratio .

However, directly comparing with the optimal expected revenue is difficult as we do not know the value of . Therefore, we first provide an intuitive upper bound for the optimal revenue based on a clairvoyant. We then provide an approximation ratio relative to the upper bound.

Clairvoyant upper bound for the expected revenue.

Recall the definition of in Section 4.1: the optimal ranking for the customer with fixed attention span . Note that for , the revenue of any ranking is dominated by , i.e., . Therefore, we have for any :

Taking the maximum over on the left-hand side, it leads to the following upper bound:

Proposition 4.5

The optimal expected revenue (4) is upper bounded by the expected clairvoyant revenue, where we can personalize the recommendation for each customer with realized attention span, i.e.,

| (9) |

rev:clairvoyantNote that the upper bound can be interpreted as follows: if the retailer is a clairvoyant, i.e., it can access the realized attention span and provide a customized ranking for customers with attention span , then the optimal revenue is given in (9). Apparently, the expected revenue obtained from any ranking is upper bounded by that obtained by the clairvoyant.

Next we show that our Best-x algorithm can guarantee a approximation ratio relative to the upper bound (9) under the mild IFR Assumption 4.2. For any fixed , because , we have

Note that the output of the Best-x Algorithm maximizes . Therefore, in order to find the approximation ratio of the Best-x Algorithm, it suffices to provide a lower bound for

| (10) |

where the numerator is the lower bound of the expected revenue from Best-x and the denominator is an upper bound for the optimal expected revenue.

We prove the performance guarantee of Best-x by examining the worst-case structure of over all distributions of that satisfy Assumption 4.2 and all functions of that satisfy Theorem 4.4. For convenience, we normalize the upper bound (9) to one and consider the following min-max problem:

| (11) |

The first three constraints capture the fact that is the tail probability of a random variable with IFR. The fourth and fifth constraints follow from Theorem 4.4. The sixth constraint normalizes the upper bound to one.

Next, we prove that the optimal value of the min-max problem (11) is at least .

Theorem 4.6

The optimal value of (11) is at least . As a result,

and the approximation ratio of the Best-x Algorithm is at least .

The intuition for the theorem is briefly discussed below. We keep track of , the minimum integer that exceeds the expected value of . Clearly we have and let us consider the ranking . In order to show the revenue obtained by is at least of the upper bound, we resort to the decreasing margin property in Theorem 4.4, which is analogous to concavity in the discrete sense. In particular, we can construct a continuous piecewise-linear concave increasing function such that . Utilizing the concavity of , we have

where the second inequality is due to Jensen’s Inequality. Meanwhile, for any random variable following IFR, we can show that . Combining the two results, we have

which implies an approximation ratio.

rev:clairvoyant-1/2Theorem 4.6 is in sharp contrast to Brubach et al. (2022), where they show that any algorithm can be arbitrarily bad relative to the clairvoyant upper bound. By adding the arguably mild IFR assumption, we can guarantee a performance ratio relative to the clairvoyant revenue. Next, we show that the ratio is close to the best one can get relative to the upper bound.

Proposition 4.7

There exist , , and a distribution of satisfying Assumption 4.2 such that no algorithm can achieve more than of the clairvoyant upper bound:

In the proof, we construct a special instance in which we prove that no algorithms can achieve an expected revenue higher than of the clairvoyant upper bound. Therefore, for random attention spans with IFR, the approximation algorithm we develop is rather efficient: the optimality gap is at most .

Remark 4.8 (Rank the remaining products.)

rev:fillingAfter finding the best x in Algorithm 3, the algorithm doesn’t fill in the remaining positions automatically. In fact, the theoretical results in Theorem 4.6 hold even with the remaining positions unfilled. Empirically, however, filling the remaining positions with products always increases the expected revenue. In practice, after ranking products for the Best-x algorithm, we can fill the positions up to greedily, i.e., iteratively inserting one of the remaining products into the current ranking that yields the highest marginal increase of the expected revenue. In Section 6.1, we show that empirically, Best-x algorithm with greedy filling always achieves more than 86% of the clairvoyant upper bound, significantly outperforming a number of heuristic benchmarks.

Remark 4.9 (Comparison with Kempe and Mahdian (2008))

rev:comparison_kempeCompared to the model in Kempe and Mahdian (2008), we have made three technical contributions. (1) Under Assumption 4.2, we improve the -approximation ratio of Kempe and Mahdian (2008) to . Our algorithm is easy to interpret and implement while Kempe and Mahdian (2008) consider a dynamic program with continuous state space and the error margin appears in discretization. We also show that no algorithm can achieve better than of the clairvoyant revenue; (2) The computational cost for our Best-x algorithm is while Kempe and Mahdian (2008) only provide a quasi-polynomial-time approximation scheme (QPTAS); and (3) we provide a nested structural for the optimal rankings under the fixed attention span, which provides insights to the design of approximation algorithms and heuristics for future work.

4.3 Special Cases with Solvable Optimal Ranking

Although we have established the performance bound of the Best-x algorithm, it is developed for the worst-case scenario. For some special cases, the optimal ranking under the random attention spans can be found in polynomial time. We provide two such cases in this section.

Case one: prefixing rankings. Inspired by the nested structure in Proposition 4.3, we next identify the conditions under which the optimal ranking for customers with attention span is a prefix to that for customers with attention span . That is, can be attained by appending one product to the bottom of , which is even stronger than Proposition 4.3. Note that this condition automatically leads to the optimal ranking for random attention spans. The retailer can simply use , the optimal ranking for customers with attention span , which can be solved using Algorithm 2. For customers with attention span , they are essentially offered the first products in , which is exactly displayed in the same order as . Therefore, is the optimal ranking for attention spans with any distribution.

We next provide the sufficient and necessary condition for prefixing rankings. Suppose is the product that has the th highest among all products for . That is, for .

Proposition 4.10

The optimal ranking is a prefix of for all if and only if .

Recall that we index products in the order of decreasing prices according to (1). Therefore, the condition in Proposition 4.10 states that the order of the product prices is consistent with the expected revenues that take into account their attractiveness. In other words, the products need to display clear ordering for the retailer: more expensive products also generate higher expected revenues. If there are products sold at high prices, but their purchase probabilities are low and drag down the expected revenues, then prefixing rankings are not optimal.

Case two: geometric span distribution. When the attention span is random, we do not have an iterative formula like (5). As a result, we cannot gradually add products to existing rankings to construct longer rankings and resort to dynamic programming. This motivates us to investigate special attention distributions that preserve the iterative structure in (5). We show that when the attention spans have a geometric distribution, i.e., the tail probability can be written as for , we can develop dynamic programming to solve the optimal ranking.

Under the (truncated) geometric distribution, the optimal expected revenue (3) can be expressed as

where denotes the sub-ranking of from position two to . Note that is expected revenue conditional on the event that the customer doesn’t purchase the first product. By the structure of the geometric distribution, it is the same as the expected revenue from displaying from position one to position for customers whose attention spans are geometrically distributed and truncated at . The above formula gives us the basis for dynamic programming.

However, we still need a similar result to Lemma 4.1 that dictates the ordering of the products in the optimal ranking. Otherwise, the state space of dynamic programming, which is the set of products in the sub-rankings, is combinatorial and growing exponentially. This is given in the next proposition:

Proposition 4.11

Suppose for with some . The optimal ranking satisfies

By Proposition 4.11, we can relabel the products according to the descending order of , i.e., product one has the largest value . In the optimal ranking, the products must obey this order, which greatly limits the search space for dynamic programming and enables us to apply the same philosophy of Algorithm 1.

| (12) |

5 Personalized Ranking via Online Learning

In Section 4, we develop the Best-x Algorithm to compute a ranking that preserves a guaranteed revenue of the optimal. However, the efficiency of the algorithm does not obscure its obstacles when applied in practice:

-

•

The algorithm requires the prior knowledge of the conditional purchase probabilities ’s and the distribution of the attention span, which are typically unknown to the retailer in most real world scenarios, especially for new entrants to the industry.

-

•

Customers may have vastly distinct tastes and preferences toward the products. That is to say, the conditional purchase probability of the same product may vary for different customers. Fortunately, customers usually arrive with a characterizing feature that can reveal her preference, and it is desirable to design personalized product rankings accordingly. However, the relationship between the feature and the preference is usually unknown.

-

•

In online retailing, the firm is usually able to display a huge catalog of products even for the same search keyword or category. Some products can be very similar and only differ in a few dimensions such as color and size. In this case, one would expect the conditional purchase probabilities of the products may also be correlated with the product features.

In this section, we develop a framework based on online learning to address these practical considerations. We assume the customers have the same attention span distribution, but distinct conditional purchase probabilities based on their own features. The products may also be differentiated by product-related features. We develop a learning algorithm that actively learns the span distribution and the conditional purchase probabilities, and simultaneously approximates the personalized -optimal ranking for each customer.

5.1 Preliminaries

The online-retailer is expecting the arrival of future customers. Customer has a random attention span with distribution . Note that we use the superscript to denote the actual value, to differentiate with the estimation. Moreover, her probability of purchasing item depends on both the customer feature and the product feature . Moreover, we assume there exists an unknown matrix encoding the interaction between the product and customer that yields a conditional purchase probability . In particular, we have

| (13) |

Feature vectorization: For customer with feature , let and be the vectorization of and . The term can be expressed as . Throughout the rest of the paper, we use to represent the vectorized feature and to represent their compounded dimension for ease of notation. We assume that the -norm of the features and the parameter are bounded: {assumption} For all customer and product , the vectorized feature is bounded by . The parameter satisfies for some constant . This assumption is mild and can always be satisfied by proper rescaling of the features.

Online learning: We denote as the maximal revenue among all products. To maximize the revenue, after observing the feature of a consumer , and thus for all , the firm would calculate the conditional purchase probabilities according to (13) and optimize the personalized ranking using the algorithm in Section 4. However, the firm usually does not know or for initially. Therefore, we set up an online learning framework to address the problem.

Suppose the firm is expecting customers arriving in sequence. For customer , the firm may display a ranking . The feature determines the purchase probability , and the expected revenue conditional on is denoted as . The goal of the firm is to maximize the total expected revenue gained from the customers.

The key component of online learning is that the decision of depends on the information extracted from the interactions with customers prior to , but not on the unknown or . This is referred to as the information structure. For a past customer facing ranking , there are two possible outcomes observed by the firm. She may purchase a product in , say, the product in the third position. She may also leave without purchasing anything. In the latter case, we assume that the firm observes the product position after which the consumer leaves. For example, she leaves after viewing four products. This is a typical setting in online retailing as the product view in a mobile phone can be precisely tracked.

To encode the information structure, we use to represent the observed behavior of customer . More precisely, and if and only if customer purchases a product. In this case, is the position of the product that is purchased. Otherwise, if , then is the number of products customer views before leaving. With this set of notations, the ranking determined by the firm may depend on , i.e., all the past observations, and , or equivalently, for .

Performance metric: We use the cumulative regret to evaluate the performance of the proposed algorithm, which is one of the most common metrics in online learning. For a given customer and its feature , an oracle who knows the model parameters would calculate the conditional purchase probabilities according to (13) and choose the optimal ranking for the customer. For the ease of presentation, we denote

throughout this section as the expected revenue from displaying to a customer with conditional purchase probability and attention span distribution . For customer , the oracle would optimize the expected revenue

| (14) |

On the other hand, the expected revenue for the firm using is .

Usually, the cumulative regret is defined to be the performance gap between the oracle and the firm that uses an online learning algorithm. In our case, because of the computation cost in finding the optimal ranking for the oracle, we consider the Best-x Algorithm to be the target to learn. More precisely, for a sequence of customers , we can define

The target of the firm is not to learn the optimal ranking under the true parameters, but the Best-x algorithm which is guaranteed to have approximation ratio by Theorem 4.6. In other words, if the firm can effectively implement Best-x after learning the values of and as increases, then the regret per period is diminishing, i.e., . \Copyrev:other-learning-targetWe point out that the proposed learning algorithm can be slightly modified to achieve the same rate of regret when the target is another offline algorithm or even the optimal ranking (if the computational cost is not a concern) other than the Best-x algorithm. In the latter case, we don’t have the scaling factor in the regret calculation.

Challenges in the algorithmic design and analysis: Although online learning has been studied extensively and various standard frameworks have been proposed, the personalized ranking problem has several unique challenges. First, in contrast to the classic multi-armed bandit problem, the observations in each round are censored and highly non-regular. In particular, the customer may leave after viewing the first product and provides no information for the attractiveness of products displayed below the first one. Or the customer may purchase the second product, providing a right-truncated censored sample for her attention span. It is unclear how to rank the products to explore effectively and learn the distribution of the attention span as well as in the presence of censoring. For example, for large , there are hardly any consumers viewing products ranked below, say, the th position. The scarcity of samples makes it impossible to accurately estimate for . We show that our algorithm is not sensitive to the parameters associated with a high degree of censoring. Intuitively, this is because for large has little impact on the expected revenue of any rankings.

The second difficulty due to censoring lies in the estimation of . An ideal unbiased estimator would be the fraction of customers whose attention span is greater than or equal to . However, because of the censoring mentioned above, the fraction is not observed, unless the firm only utilizes the uncensored observations from consumers who leave empty-handed. Such inefficient use of data may lead to inefficient learning. We show that even the censored observations can be used effectively to estimate the failure rate , instead of . We construct unbiased estimators for the failure rate, which serve as a building block for the learning algorithm.

The third difficulty lies in the simultaneous learning of attention spans and feature-based conditional purchase probabilities. Unlike existing works in cascade bandits that assume customers leave the platform after viewing exactly products, the random attention span in our model introduces another source of randomness, which drastically complicates the structure of the observed information and the analysis. We develop efficient learning algorithm that incorporates both conditional purchase probabilities and attention spans into a unified framework, and achieve good performance in both theoretical and practical perspectives.

Remark 5.1 (Vectorized features)

In practice, the vectorized outer product may be high-dimensional, which leads to unstable estimation for or . A popular remedy is to use the concatenated features, , instead of the outer product. It tremendously reduces the dimension while ignoring the potential interaction effects of consumers and products. Based on the data availability, either formulation can be preferable. In this study, we focus on the outer product, which is more technically challenging because of the singularity of the outer product (not having full rank). Moreover, the algorithm can be easily adapted to the concatenated formulation.

Remark 5.2 (The benefit of using features)

The benefit of collecting and leveraging the consumer feature to the retailer is clear: it allows the firm to design personalized product display, which better matches consumers to their preferred products and thus extracts more revenue. The benefit of using product features, as opposed to treating products independently, is less straightforward. In fact, if there are not many products, then it may be more efficient to learn independently for each product, where the coefficient encodes how product attracts consumers of certain features. The use of product features is most helpful when there are a large number of similar products which differ in a few dimensions. For example, in online retailing, the number of products usually exceeds 1,000, and they can usually be compactly represented by product features whose dimension is typically less than 20. Nevertheless, our algorithm works for both settings.

5.2 The RankUCB Algorithm

Next we introduce the algorithm, which is referred to as RankUCB. To introduce the algorithm, we first note that the observations from customer cannot be readily used. In order to present the algorithm more compactly, we re-encode them as below. We define a set of random variables , , and for , contingent on . More precisely, if , then for all

if , then

To interpret, consider to be a Bernoulli random variable with mean , i.e., the failure rate at , to indicate whether customer leaves after inspecting position ; and to be a Bernoulli random variable with mean , to indicate whether customer finds the product at position satisfying. For example, if customer purchases the product ranked at the -th position, then ’s are zero for and . More importantly, and indicate whether and are observed (not censored), respectively. For example, if customer purchases the product ranked at position , then we only observe that her attention span is no less than , and thus if and only if . Note that the censoring has a nested structure: if , then for . The censoring mechanism is illustrated in Figure 1.

Estimating : After observing the behavior of customers, we use

| (15) |

to estimate , where , is the identity matrix and . This is a typical -regularized least square estimator.

Estimating the failure rate : Recall that the failure rate is defined as , for , and . We estimate the failure rate by

| (16) |

where is the number of observed ’s up to round . In other words, we use the frequency that a customer moves on to inspect the product ranked at from that at .

The theoretical guarantees of the estimators are provided below in the form of a confidence region. We denote for a positive definite matrix .

Lemma 5.3

For any , with probability at least , the following event occurs:

where .

Optimistic estimator: The design of our algorithm follows the principle of “optimism in the face of uncertainty,” which is shared by all UCB-type algorithms. In particular, when customer arrives, based on the confidence region provided in Lemma 5.3, the firm calculates the optimistic estimators in the confidence region:

In other words, we estimate the hazard rate to be the minimum in the confidence region; such choice guarantees that customers would view as many products as possible and thus generates the most optimistic revenue. Moreover, gives an optimistic estimator for , denoted as . The quantity provides an optimistic estimator for the conditional purchase probability of product , given the confidence region of and the feature of customer .

We present the details in Algorithm 5. When customer arrives, the firm first calculates the optimistic estimators and , as shown in Steps 5 and 6. Then, the optimistic estimators are plugged into Best-x to calculate the optimal ranking for customer (Step 7). After the observation of customer is collected, the firm updates the confidence region, which in turn is used for the next customer.

Next we analyze the regret of Algorithm 5, which is formally presented in the next theorem.

Theorem 5.4

We first remark on the dependence on various model parameters. The regret grows at , which is the typical optimal rate in online learning problems. The linear dependence on is also necessary, which is the maximum of the single-period reward. The regret is linear in , the number of positions to display. This is similar to the cascade bandit literature (Zong et al. 2016). In terms of the dimension of the contextual information , the dependence is , which is the same as the contextual bandit literature (Zong et al. 2016). The linear dependence on , the bound on , is also understandable, as the reward in each period scales linearly in . Therefore, the regret matches the best-achievable rate in the literature.

We briefly remark on how we address the challenges raised in Section 5.1. To utilize censored observations, we construct novel estimators and that can fully capture the information contained in the observation and are yet easy to manipulate to obtain unbiased estimators for the target quantities in spite of the censoring. For the difficulty in estimating , we transform it to the failure rate which can be efficiently estimated, whose estimation error is also easy to control. To simultaneously learn the conditional purchase probabilities and span distribution, we explicitly interpret the observing mechanism of choice and continuation action of customers (see Figure 1), and express the induced regret in terms of estimation errors of feature-based conditional purchase probabilities and failure rates. These techniques allow us to show the regret bound which is of the same order as other similar problems with simpler settings.

6 Numerical Experiments

In this section, we conduct numerical experiments to examine the performance of the algorithms in practice. In particular, we first demonstrate the performance of Best-x when the conditional purchase probabilities and the distribution of the attention span are known. Then we show the performance of Algorithm 5 when the parameters are unknown and need to be learned.

6.1 The Best-x Algorithm

In our experiment, we consider 1000 products, products to display and two possible distributions of the attention span (geometric and uniform), both satisfying Assumption 4.2:

-

•

Setting one: .

-

•

Setting two: .

For each setting, we randomly generate the conditional purchase probabilities and the prices independently for 1000 instances. More specifically, for each instance we generate independent prices from and conditional purchase probability from , 1000 samples each, where stands for a uniform random sample between and . We then sort prices and conditional purchase probabilities in the opposite order and assign the values to products such that and for . This is to create a realistic (popular products are more expensive) and “hard” scenario for algorithmic solutions, which highlights the price and conditional purchase probability trade-off.

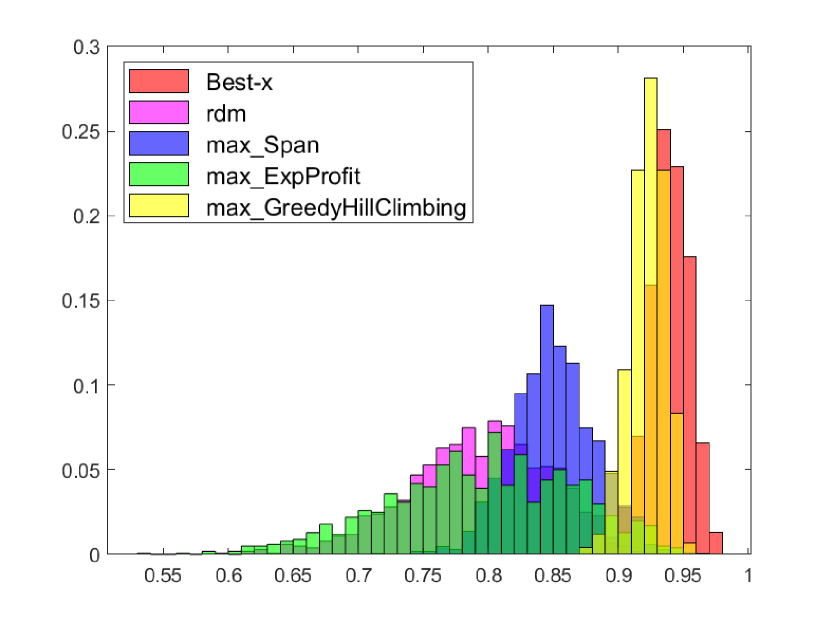

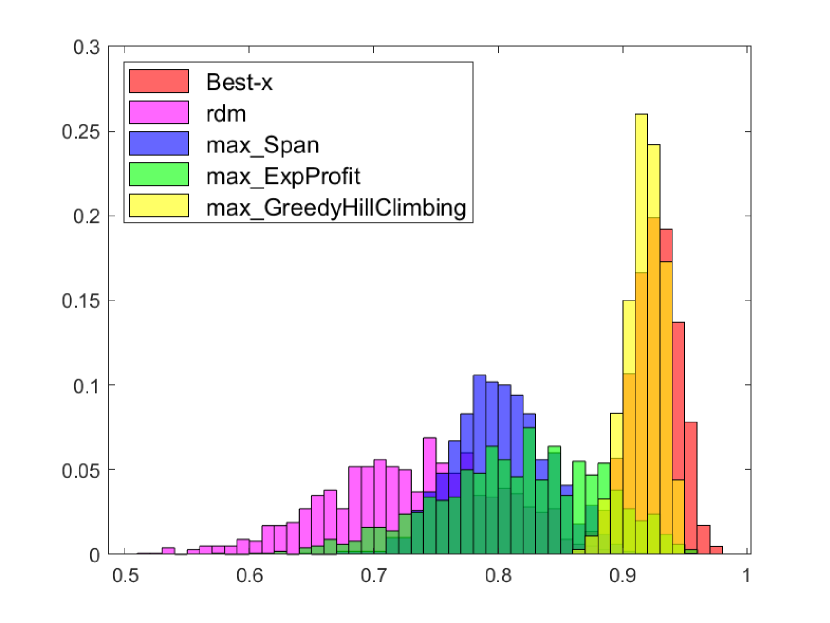

The benchmark is the expected revenue relative to the upper bound provided in Proposition 4.5, as the optimal ranking is computationally difficult to solve. We compare the performance of Best-x with four heuristic algorithms: (1) rdm, randomly selecting 20 products, (2) max_Span, using the optimal ranking when the attention span is fixed at , \Copyrev:new_heuristics(3) max_ExpProfit, displaying the 20 products with the highest expected profits (price times the purchase probability), and (4) max_GreedyHillClimbing, adding 20 products greedily that maximize the marginal increase of the expected revenue. More precisely, for any ranking containing products, max_GreedyHillClimbing constructs by inserting a product from the remaining pool at any position of that yields the largest marginal increase of the expected revenue, without changing the relative order of products within . The performance is measured as the ratio to the upper bound derived in Proposition 4.5.33endnote: 3We have also tested two simple heuristics: max_Profit, displaying the 20 most profitable products (with the highest prices) and max_Choice, displaying the 20 products with the highest purchase probabilities. Both heuristics perform badly compared to others and we thus do not include them in the results. The histogram of 1000 instances is illustrated in Figure 2. We can see that ranking 20 products randomly performs worst among all strategies. Meanwhile, ranking the products based on their expected profits (max_ExpProfit), using the optimal ranking for customers with attention span 20 (max_Span), or the greedy heuristic are reasonable strategies: they usually generate more than 80% of the clairvoyant revenue. The Best-x algorithm consistently outperforms all other heuristics. It exceeds 86% of the clairvoyant revenue in all the instances in both settings.

(a)

(b)

6.2 RankUCB

Next, we investigate the performance of Algorithm 5 RankUCB. In this experiment, we adopt a similar setting to that in Section 6.1. In particular, we consider 1000 products and . We implement the RankUCB for 10 independent simulations, each with 10000 customers arriving sequentially. For each customer, her attention span has a geometric distribution from setting one in the last section, unknown to the firm. We conduct 10 simulation instances. At the beginning of each simulation instance, we randomly generate the prices of the products uniformly from and their features with . The product features are then normalized to . In each round, we randomly generate the customer feature with and also normalize it to . We generate and then normalized such that . The same remains the same for the 10 independent simulations. In this setup, for any product , it is guaranteed that the conditional purchase probability .

Because of the dimension of the problem, the instances tend to have high variances due to the random draw of the feature vectors. To show the performance, we use a different measure than the regret. In particular, in each round we calculate the expected revenue of the ranking suggested by RankUCB conditional on the feature and thus the conditional purchase probabilities. Then we calculate the ratio over the conditionally expected revenue of the Best-x Algorithm (Algorithm 3) when all the information is known. The expected revenue instead of the realized revenue helps smooth the performance. Figure 3 illustrates the ratio over 10000 rounds as well as the standard error of 10 simulations. As we can observe, the expected reward of RankUCB increases to around 90% in 10000 rounds. This demonstrates its practical efficiency even under high dimensions .

We also investigate the learning of the failure rate in the experiment. In particular, we show the point estimator and the optimistic estimator for the failure rate at . We plot the absolute errors relative to the actual value . The results are illustrated in Figure 4.

From Figure 4, we observe that the estimators for smaller converge faster, because there is less censoring for products ranked at the front. The optimistic estimators converge much slower than the point estimators, because of the slow decay of the confidence region. In particular, , and are very accurate over after 5000 rounds, while , and are still too optimistic after 10000 rounds. Nevertheless, as increases, the convergence of the estimates is reflected in the experiment.

7 Conclusion

In this paper, we study the revenue maximization problem of an online retailer, when customers browse the ranked products in order. The model extends the well-known cascade model in two directions: customers may have random attention spans, and the products have different prices. Based on the structure of the optimal ranking under fixed attention span, we develop an approximation algorithm with -approximation ratio. When the conditional purchase probabilities of the products (which may be based on customer and product features) and the distribution of customers’ attention spans are unknown , we provide a learning algorithm that can effectively learn the parameters and achieve near-optimal regret. Our study addresses the two major challenges of the product ranking model when the firm is interested in revenue instead of click maximization.

References

- Abbasi-Yadkori et al. (2011) Abbasi-Yadkori, Y., D. Pál, and C. Szepesvári (2011). Improved algorithms for linear stochastic bandits. In Advances in Neural Information Processing Systems, pp. 2312–2320.

- Abeliuk et al. (2016) Abeliuk, A., G. Berbeglia, M. Cebrian, and P. Van Hentenryck (2016). Assortment optimization under a multinomial logit model with position bias and social influence. 4OR 14(1), 57–75.

- Agarwal et al. (2011) Agarwal, A., K. Hosanagar, and M. D. Smith (2011). Location, location, location: An analysis of profitability of position in online advertising markets. Journal of Marketing Research 48(6), 1057–1073.

- Agrawal et al. (2019) Agrawal, S., V. Avadhanula, V. Goyal, and A. Zeevi (2019). Mnl-bandit: A dynamic learning approach to assortment selection. Operations Research 67(5), 1453–1485.

- Aouad et al. (2019) Aouad, A., J. Feldman, D. Segev, and D. Zhang (2019). Click-based mnl: Algorithmic frameworks for modeling click data in assortment optimization. Working Paper.

- Aouad and Segev (2020) Aouad, A. and D. Segev (2020, 01). Display optimization for vertically differentiated locations under multinomial logit choice preferences. SSRN Electronic Journal.

- Araman and Caldentey (2009) Araman, V. F. and R. Caldentey (2009). Dynamic pricing for nonperishable products with demand learning. Operations research 57(5), 1169–1188.

- Asadpour et al. (2020) Asadpour, A., R. Niazadeh, A. Saberi, and A. Shameli (2020). Ranking an assortment of products via sequential submodular optimization. arXiv preprint arXiv:2002.09458.

- Ban and Keskin (2020) Ban, G.-Y. and N. B. Keskin (2020). Personalized dynamic pricing with machine learning: High dimensional features and heterogeneous elasticity. Working Paper.

- Baye et al. (2009) Baye, M. R., J. R. J. Gatti, P. Kattuman, and J. Morgan (2009). Clicks, discontinuities, and firm demand online. Journal of Economics & Management Strategy 18(4), 935–975.

- Besbes et al. (2015) Besbes, O., Y. Gur, and A. Zeevi (2015). Non-stationary stochastic optimization. Operations research 63(5), 1227–1244.

- Besbes and Zeevi (2009) Besbes, O. and A. Zeevi (2009). Dynamic pricing without knowing the demand function: Risk bounds and near-optimal algorithms. Operations Research 57(6), 1407–1420.

- Besbes and Zeevi (2012) Besbes, O. and A. Zeevi (2012). Blind network revenue management. Operations Research 60(6), 1537–1550.

- Broder and Rusmevichientong (2012) Broder, J. and P. Rusmevichientong (2012). Dynamic pricing under a general parametric choice model. Operations Research 60(4), 965–980.

- Brubach et al. (2022) Brubach, B., N. Grammel, W. Ma, and A. Srinivasan (2022). Online matching frameworks under stochastic rewards, product ranking, and unknown patience. Working Paper.

- Bubeck and Cesa-Bianchi (2012) Bubeck, S. and N. Cesa-Bianchi (2012). Regret analysis of stochastic and nonstochastic multi-armed bandit problems. Foundations and Trends in Machine Learning 5(1), 1–122.

- Cao and Sun (2019) Cao, J. and W. Sun (2019). Dynamic learning of sequential choice bandit problem under marketing fatigue. In Proceedings of the AAAI Conference on Artificial Intelligence, Volume 33, pp. 3264–3271.

- Cao et al. (2019) Cao, J., W. Sun, and Z.-J. M. Shen (2019). Sequential choice bandits: Learning with marketing fatigue. Working Paper.

- Chen and Gallego (2018) Chen, N. and G. Gallego (2018). A primal-dual learning algorithm for personalized dynamic pricing with an inventory constraint. Working Paper.

- Chen and Gallego (2020) Chen, N. and G. Gallego (2020). Nonparametric pricing analytics with customer covariates. Operations Research Forthcoming.

- Chen et al. (2019) Chen, Q., S. Jasin, and I. Duenyas (2019). Nonparametric self-adjusting control for joint learning and optimization of multiproduct pricing with finite resource capacity. Mathematics of Operations Research 44(2), 601–631.

- Chen et al. (2018) Chen, X., Y. Wang, and Y. Zhou (2018). Dynamic assortment optimization with changing contextual information. Working Paper.

- Chen et al. (2020) Chen, Y.-J., G. Gallego, P. Gao, and Y. Li (2020). Position auctions with endogenous product information: Why live-streaming advertising is thriving. Working Paper.

- Cheung et al. (2017) Cheung, W. C., D. Simchi-Levi, and H. Wang (2017). Dynamic pricing and demand learning with limited price experimentation. Operations Research 65(6), 1722–1731.

- Cheung et al. (2019) Cheung, W. C., V. Tan, and Z. Zhong (2019). A thompson sampling algorithm for cascading bandits. In The 22nd International Conference on Artificial Intelligence and Statistics, pp. 438–447.

- Craswell et al. (2008) Craswell, N., O. Zoeter, M. Taylor, and B. Ramsey (2008). An experimental comparison of click position-bias models. In Proceedings of the 2008 international conference on web search and data mining, pp. 87–94.

- den Boer (2015) den Boer, A. V. (2015). Dynamic pricing and learning: historical origins, current research, and new directions. Surveys in operations research and management science 20(1), 1–18.

- Derakhshan et al. (2022) Derakhshan, M., N. Golrezaei, V. Manshadi, and V. Mirrokni (2022). Product ranking on online platforms. Management Science 68(6), 3975–4753.

- Feldman and Segev (2019) Feldman, J. and D. Segev (2019, 01). Improved approximation schemes for mnl-driven sequential assortment optimization. Working Paper.

- Feng et al. (2007) Feng, J., H. K. Bhargava, and D. M. Pennock (2007). Implementing sponsored search in web search engines: Computational evaluation of alternative mechanisms. INFORMS Journal on Computing 19(1), 137–148.

- Ferreira et al. (2022) Ferreira, K. J., S. Parthasarathy, and S. Sekar (2022). Learning to rank an assortment of products. Management Science 68(3), 1828–1848.

- Ferreira et al. (2018) Ferreira, K. J., D. Simchi-Levi, and H. Wang (2018). Online network revenue management using Thompson sampling. Operations Research 66(6), 1586–1602.

- Flores et al. (2019) Flores, A., G. Berbeglia, and P. Van Hentenryck (2019). Assortment optimization under the sequential multinomial logit model. European Journal of Operational Research 273(3), 1052 – 1064.

- Fotakis et al. (2011) Fotakis, D., P. Krysta, and O. Telelis (2011). Externalities among advertisers in sponsored search. In G. Persiano (Ed.), Algorithmic Game Theory, Berlin, Heidelberg, pp. 105–116. Springer Berlin Heidelberg.

- Gallego and Li (2017) Gallego, G. and A. Li (2017, 01). Attention, consideration then selection choice model. SSRN Electronic Journal.

- Gallego et al. (2020) Gallego, G., A. Li, V.-A. Truong, and X. Wang (2020). Approximation algorithms for product framing and pricing. Operations Research 68(1), 134–160.

- Gao et al. (2021) Gao, P., Y. Ma, N. Chen, G. Gallego, A. Li, P. Rusmevichientong, and H. Topaloglu (2021). Assortment optimization and pricing under the multinomial logit model with impatient customers: Sequential recommendation and selection. Operations Research 69(5), 1509–1532.

- Gao et al. (2022) Gao, X., S. Jasin, S. Najafi, and H. Zhang (2022). Joint learning and optimization for multi-product pricing (and ranking) under a general cascade click model. Management Science Forthcoming.

- Ghose and Yang (2009) Ghose, A. and S. Yang (2009). An empirical analysis of search engine advertising: Sponsored search in electronic markets. Management Science 55(10), 1605–1622.

- Golrezaei et al. (2021) Golrezaei, N., V. Manshadi, J. Schneider, and S. Sekar (2021). Learning product rankings robust to fake users. In Proceedings of the 22nd ACM Conference on Economics and Computation, pp. 560–561.

- Kallus and Udell (2020) Kallus, N. and M. Udell (2020). Dynamic assortment personalization in high dimensions. Operations Research.

- Katariya et al. (2016) Katariya, S., B. Kveton, C. Szepesvari, and Z. Wen (2016). Dcm bandits: Learning to rank with multiple clicks. In International Conference on Machine Learning, pp. 1215–1224.

- Kempe and Mahdian (2008) Kempe, D. and M. Mahdian (2008). A cascade model for externalities in sponsored search. In International Workshop on Internet and Network Economics, pp. 585–596. Springer.

- Kveton et al. (2015) Kveton, B., C. Szepesvari, Z. Wen, and A. Ashkan (2015). Cascading bandits: Learning to rank in the cascade model. In International Conference on Machine Learning, pp. 767–776.

- Kveton et al. (2015) Kveton, B., Z. Wen, A. Ashkan, and C. Szepesvari (2015). Combinatorial cascading bandits. In Advances in Neural Information Processing Systems, pp. 1450–1458.

- Lagrée et al. (2016) Lagrée, P., C. Vernade, and O. Cappe (2016). Multiple-play bandits in the position-based model. In Advances in Neural Information Processing Systems, pp. 1597–1605.

- Liu et al. (2020) Liu, N., Y. Ma, and H. Topaloglu (2020). Assortment optimization under the multinomial logit model with sequential offerings. INFORMS Journal on Computing 32(3), 835–853.

- Mahajan and van Ryzin (2001) Mahajan, S. and G. van Ryzin (2001). Stocking retail assortments under dynamic consumer substitution. Operations Research 49(3), 334–351.

- Miao et al. (2019) Miao, S., X. Chen, X. Chao, J. Liu, and Y. Zhang (2019). Context-based dynamic pricing with online clustering. Working Paper.

- Niazadeh et al. (2020) Niazadeh, R., N. Golrezaei, J. Wang, F. Susan, and A. Badanidiyuru (2020). Online learning via offline greedy: Applications in market design and optimization. Working Paper.

- Oh and Iyengar (2019) Oh, M.-h. and G. Iyengar (2019). Thompson sampling for multinomial logit contextual bandits. In Advances in Neural Information Processing Systems, pp. 3151–3161.

- Rinne (2014) Rinne, H. (2014). The Hazard Rate: Theory and Inference (with Supplementary MATLAB-Programs).

- Rusmevichientong et al. (2010) Rusmevichientong, P., Z.-J. M. Shen, and D. B. Shmoys (2010). Dynamic assortment optimization with a multinomial logit choice model and capacity constraint. Operations research 58(6), 1666–1680.

- Sauré and Zeevi (2013) Sauré, D. and A. Zeevi (2013). Optimal dynamic assortment planning with demand learning. Manufacturing & Service Operations Management 15(3), 387–404.

- Talluri and Van Ryzin (2004) Talluri, K. and G. Van Ryzin (2004). Revenue management under a general discrete choice model of consumer behavior. Management Science 50(1), 15–33.

- Wang and Sahin (2018) Wang, R. and O. Sahin (2018). The impact of consumer search cost on assortment planning and pricing. Management Science 64(8), 3649–3666.

- Wang and Tulabandhula (2019) Wang, Y. and T. Tulabandhula (2019). Thompson sampling for a fatigue-aware online recommendation system.

- Wen et al. (2017) Wen, Z., B. Kveton, M. Valko, and S. Vaswani (2017). Online influence maximization under independent cascade model with semi-bandit feedback. In Advances in neural information processing systems, pp. 3022–3032.

- Zhang et al. (2022) Zhang, Z., H.-S. Ahn, and L. Baardman (2022). Ordering and ranking products for an online retailer. Working Paper.