Transaction Fee Mechanism Design for the Ethereum Blockchain: An Economic Analysis of EIP-1559††thanks: This work was funded by the Decentralization Foundation (https://d24n.org/). This report has benefited from comments by and discussions with a number of people: Maryam Bahrani, Abdelhamid Bakhta, Tim Beiko, Vitalik Buterin, Matheus Ferreira, Danno Ferrin, James Fickel, Hasu, Georgios Konstantopoulos, Andrew Lewis-Pye, Barnabé Monnot, Daniel Moroz, Mitchell Stern, Alex Tabarrok, and Peter Zeitz. Thanks to James also for introducing me to the problem.

Abstract

EIP-1559 is a proposal to make several tightly coupled additions to Ethereum’s transaction fee mechanism, including variable-size blocks and a burned base fee that rises and falls with demand. This report assesses the game-theoretic strengths and weaknesses of the proposal and explores some alternative designs.

1 TL;DR

1.1 A Brief Description of EIP-1559

In the Ethereum protocol, the transaction fee mechanism is the component that determines, for every transaction added to the Ethereum blockchain, the price paid by its creator. Since its inception, Ethereum’s transaction fee mechanism has been a first-price auction: Each transaction comes equipped with a bid, corresponding to the gas limit times the gas price, which is transferred from its creator to the miner of the block that includes it.

EIP-1559 proposes a major change to Ethereum’s transaction fee mechanism. Central to the design is a base fee, which plays the role of a reserve price and is meant to match supply and demand. Every transaction included in a block must pay that block’s base fee (per unit of gas), and this payment is burnt rather than transferred to the block’s miner. Blocks are allowed to grow as large as double a target block size; for example, with a target of 12.5M gas, the maximum block size would be 25M gas. The base fee is adjusted after every block, with larger-than-target blocks increasing it and smaller-than-target blocks decreasing it. Users seeking special treatment, such as immediate inclusion in a period of rapidly increasing demand or a specific position within a block, can supplement the base fee with a transaction tip that is transferred directly to the miner of the block that it includes it.

1.2 Ten Key Takeaways

The following list serves as an executive summary for busy readers as well as a road map for those wanting to dig deeper.

-

1.

No transaction fee mechanism, EIP-1559 or otherwise, is likely to substantially decrease average transaction fees; persistently high transaction fees is a scalability problem, not a mechanism design problem. (See Section 3.2.1 for details.)

-

2.

EIP-1559 should decrease the variance in transaction fees and the delays experienced by some users through the flexibility of variable-size blocks. (Section 3.2.2)

-

3.

EIP-1559 should improve the user experience through easy fee estimation, in the form of an “obvious optimal bid,” outside of periods of rapidly increasing demand. (Section 6.3)

- 4.

-

5.

The game-theoretic impediments to double-spend attacks, censorship attacks, denial-of-service attacks, and long-term revenue-maximizing strategies such as base fee manipulation appear as strong under EIP-1559 as with first-price auctions. (Section 7.5)

-

6.

EIP-1559 should at least modestly decrease the rate of ETH inflation through the burning of transaction fees. (Section 9.1)

- 7.

- 8.

-

9.

EIP-1559’s base fee update rule is somewhat arbitrary and should be adjusted over time. (Section 8.6)

- 10.

1.3 Organization of Report

Section 2 reviews Ethereum’s current transaction fee mechanism and provides a detailed description of the changes proposed in EIP-1559. Section 3 considers the market for computation on the Ethereum blockchain and the basic forces of supply and demand at work. Section 4 formalizes the concepts of a “good user experience” and “easy fee estimation” via posted-price mechanisms. Section 5 defines several desirable game-theoretic guarantees at the time scale of a single block, and Section 6 delineates the extent to which the transaction fee mechanism proposed in EIP-1559 satisfies them. Section 7 investigates the possibility of collusion by miners over long time scales. Section 8 spells out the fatal flaws with some natural alternative designs and identifies worthy directions for further design experimentation. Section 9 covers additional benefits of the mechanism proposed in EIP-1559, along with a short discussion of EIP-2593 (the “escalator”). Section 10 concludes.

Sections 2–4, 7, and 9–10 are relatively non-technical and meant for a general audience. Sections 5–6 and 8 are more mathematically intense and aimed at readers who have at least a passing familiarity with mechanism design theory (see e.g. [54] for the relevant background).111Other economic analyses of EIP-1559 include [8, 30, 50, 51, 59].

2 Transaction Fee Mechanisms in Ethereum: Present and Future

This section reviews the economically salient properties of Ethereum transactions (Section 2.1), the status quo of a first-price transaction fee mechanism (Section 2.2), the nuts and bolts of the new transaction fee mechanism proposed in EIP-1559 (Section 2.3), and the intuition behind the proposal (Section 2.4).

2.1 Transactions in Ethereum

The Ethereum blockchain, through its Ethereum virtual machine (EVM), maintains state (such as account balances) and carries out instructions that change this state (such as transfers of the native currency, called ether (ETH)). A transaction specifies a sequence of instructions to be executed by the EVM. The creator of a transaction is responsible for specifying, among other fields, a gas limit and a gas price for the transaction. The gas limit is a measure of the cost (in computation, storage, and so on) imposed on the Ethereum blockchain by the transaction. The gas price specifies how much the transaction creator is willing to pay (in ETH) per unit of gas. For example, the most basic type of transaction (a simple transfer) requires 21,000 units of gas; more complex transactions require more gas. Typical gas prices reflect the current demand for EVM computation and have varied over time by orders of magnitude; readers wishing to keep a concrete gas price in mind could use, for example, 100 gwei (where one gwei is ETH). The total amount that the creator of a transaction offers to pay for its execution is then the gas limit times the gas price:

| (1) |

For example, for a 21,000-gas transaction with a gas price of 100 gwei, the corresponding payment would be ETH (or 1.26 USD at an exchange rate of 600 USD/ETH).

A block is an ordered sequence of transactions and associated metadata (such as a reference to the predecessor block). There is a cap on the total gas consumed by the transactions of a block, which we call the maximum block size. The maximum block size has increased over time and is currently 12.5M gas, enough for roughly 600 of the simplest transactions. Blocks are created and added to the blockchain by miners. Each miner maintains a mempool of outstanding transactions and collects a subset of them into a block. To add a block to the blockchain, a miner provides a proof-of-work in the form of a solution to a computationally difficult cryptopuzzle; the puzzle difficulty is adjusted over time to maintain a target rate of block creation (roughly one block per 13 seconds). Importantly, the miner of a block has dictatorial control over which outstanding transactions are included and their ordering within the block. Transactions are considered confirmed once they are included in a block that is added to the blockchain. The current state of the EVM is then the result of executing all the confirmed transactions, in the order they appear in the blockchain.222Technically, a longest-chain rule is used to resolve forks (that is, two or more blocks claiming a common predecessor). The confirmed transactions are then defined as those in the blocks that are well ensconced in the longest chain (that is, already extended by sufficiently many subsequent blocks).

The transaction fee mechanism is the part of the protocol that determines the amount that a creator of a confirmed transaction pays, and to whom that payment is directed.

2.2 First-Price Auctions

Ethereum’s transaction fee mechanism is and always has been a first-price auction [15].333First-price auctions are also used in Bitcoin [47]. 1. Who pays what? The creator of a confirmed transaction pays the specified gas limit times the specified gas price (as in (1)). 2. Who gets the payment? The entire payment is transferred to the miner of the block that includes the transaction.444We will ignore details concerning transactions that run out of gas or complete with unused gas. \tfn@tablefootnoteprintout

A user submitting a transaction is sure to pay either the amount in (1) (if the transaction is confirmed) or 0 (otherwise). A miner who mines a block is sure to receive as revenue the amount in (1) from each of the transactions it chooses to include. Accordingly, many miners pack blocks up to the maximum block size, greedily prioritizing the outstanding transactions with the highest gas prices.555Technically, because different transactions have different gas limits, selecting the revenue-maximizing set of transactions is a knapsack problem (see e.g. [55]). The minor distinction between optimal and greedy knapsack solutions is not important for this report.,666We use the word “greedy” without judgment—“greedy algorithm” is a standard term for a heuristic that is based on a sequence of myopic decisions.

2.3 EIP-1559: The Nuts and Bolts

2.3.1 Burning a History-Dependent Base Fee

EIP-1559, following Buterin [16, 17, 18], proposes a mechanism that makes several tightly coupled changes to the status quo. 1. Each block has a protocol-computed reserve price (per unit of gas) called the base fee. Paying the base fee is a prerequisite for inclusion in a block.777Technically, a miner can also include a transaction unwilling to pay the full base fee, but it must then dip into its block reward to make up the difference. We ignore this detail in this report. 2. The base fee is a function of the preceding blocks only, and does not depend on the transactions included in the current block. 3. All revenues from the base fee are burned—that is, permanently removed from the circulating supply of ETH. \tfn@tablefootnoteprintout Removing ETH from the supply increases the value of every ether still in circulation. Fee-burning can therefore be viewed as a lump-sum refund to ETH holders (à la stock buybacks).

The second point is underspecified; how, exactly, is the base fee derived from the preceding blocks? Intuitively, increases and decreases in demand should put upward and downward pressure on the base fee, respectively.888In the economics literature, such demand-dependent price adjustment is called “tâtonnement” (French for “groping”). But the blockchain records only the confirmed transactions, not the transactions that were priced out. If miners publish a sequence of full (12.5M gas) blocks, how can the protocol distinguish whether the current base fee is too low or exactly right?

2.3.2 Variable-Size Blocks

The next key idea is to relax the constraint that every block has size at most 12.5M gas and instead require only that the average block size is at most 12.5M gas.999More generally, EIP-1559 is parameterized by a target block size, which is adjusted by miners over time (like the maximum block size is now). For concreteness, throughout this report we assume a target block size of 12.5M gas, the current maximum block size. The mechanism in EIP-1559 then uses past block sizes as an on-chain measure of demand, with big blocks (more than 12.5M gas) and small blocks (less than 12.5M gas) signaling increasing and decreasing demand, respectively.101010The flexibility provided by variable block sizes can also reduce the variance in equilibrium transaction fees and the delays experienced by some users; see Section 3.2. Some finite maximum block size is still needed to control network congestion; the current EIP-1559 spec [20] proposes using twice the average block size. 4. Double the maximum block size (e.g., from 12.5M gas to 25M gas), with the old maximum (e.g., 12.5M gas) serving as the target block size. 5. Adjust the base fee upward or downward whenever the size of the latest block is bigger or smaller than the target block size, respectively. \tfn@tablefootnoteprintout The specific adjustment rule proposed in the EIP-1559 spec [20] computes the base fee for the current block from the base fee and size of the predecessor block using the following formula, where denotes the target block size:111111For simplicity, we ignore numerical details such as rounding the base fee to an integer.

| (2) |

For example, the base fee increases by 12.5% after a maximum-size block (i.e., double the target size) and decreases by 12.5% after an empty block. A maximum-size block followed by an empty block (or vice versa) leaves the base fee at of its prior value.121212See also Table 1 in Section 3.2.2 for a more complex example of this update rule in action, Monnot [43] for detailed simulations, and Filecoin [4] for a recent deployment.

If the base fee is burned rather than given to miners, why should miners bother to include any transactions in their blocks at all? Also, what happens when there are lots of transactions (more than 25M gas worth) willing to pay the current base fee?

2.3.3 Tips

The transaction fee mechanism proposed in EIP-1559 addresses the preceding two questions by allowing the creator of a transaction to specify a tip, to be paid above and beyond the base fee, which is transferred to the miner of the block that includes the transaction (as in a first-price auction). Small tips should be sufficient to incentivize a miner to include a transaction during a period of stable demand, when there is room in the current block for all the outstanding transactions that are willing to pay the base fee. Large tips can be used to encourage special treatment of a transaction, such as a specific positioning within a block, or the immediate inclusion in a block in the midst of a sudden demand spike. 6. Rather than a single gas price, a transaction now includes a tip and a fee cap. A transaction will be included in a block only if its fee cap is at least the block’s base fee. 7. Who pays what? If a transaction with tip , fee cap , and gas limit is included in a block with base fee , the transaction creator pays ETH. 8. Who gets the payment? Revenue from the base fee (that is, ) is burned and the remainder () is transferred to the miner of the block. \tfn@tablefootnoteprintout For example, consider a block with base fee 100 (in gwei per unit of gas). If the block’s miner includes a transaction with tip 4 and fee cap 200, the creator of that transaction will pay 104 gwei per unit of gas (100 of which is burned, 4 of which goes to the miner). An included transaction with tip 10 and fee cap 105 would pay 105 gwei per unit of gas (100 of which is burned, 5 of which goes to the miner).

A user submitting a transaction with tip and fee cap is sure to pay at most gwei per unit of gas, and will pay less whenever the current base fee is small (i.e., less than ). A miner who mines a block is sure to receive all the revenue from the tips of the transactions it chooses to include. Accordingly, one might expect a typical miner to include all the transactions with fee cap greater than the base fee. If the total gas consumed by such transactions exceeds the maximum block size of 25M gas, one might expect the miner to pack its block full, greedily prioritizing the outstanding transactions with the highest tips.

2.4 An Informal Argument for EIP-1559

The number of new ideas in EIP-1559 can be overwhelming. Why so many changes at once? Does one of the changes necessitate the rest? We next outline one narrative of why EIP-1559 might have to look more or less the way that it does, taking as given the goal of making fee estimation far easier for users than in the status quo. The remainder of this report will interrogate this narrative mathematically and explore some alternative designs. 1. First-price auctions are challenging for users to reason about because a user’s optimal gas price depends on the gas prices offered by other users at the same time. 2. Other common auction designs in which the prices charged depend on the set of included transactions, such as second-price (a.k.a. Vickrey) auctions, can be easily manipulated by miners through fake transactions. 3. Simple fee estimation, in which users are not forced to reason about other users’ behavior, therefore seems to require a base fee—a price that is set independently of the transactions included in the current block. 4. The ideal base fee would result in blocks filled with the highest-value transactions. Demand changes over time, so the base fee must respond in kind. 5. The base fee revenues of a block must be burned or otherwise withheld from the block’s miner, as otherwise the miner could collude with users off-chain to costlessly simulate a first-price auction. 6. Because demand is not recorded on-chain, an on-chain proxy such as variable block sizes must be used to adjust the base fee. 7. Tips are required to disincentivize miners from publishing empty blocks. 8. Tips should be specified by users rather than hard-coded into the protocol so that high-value transactions can be identified and accommodated during a sudden demand spike. 9. Burning any portion of the tips would drive the tip market off-chain, and thus tips may as well be transferred entirely to a block’s miner. \tfn@tablefootnoteprintout

3 The Market for Ethereum Transactions

This section steps away from the discussion of specific mechanisms and focuses instead the basic forces of supply and demand at work in the Ethereum blockchain. Section 3.1 defines a “market-clearing outcome” and posits it as the ideal outcome of a transaction fee mechanism. Section 3.2 emphasizes that no mechanism can guarantee low transaction fees during periods in which the demand for EVM computation significantly outstrips its supply, and clarifies EIP-1559’s likely effect on high transaction fees.

3.1 Market-Clearing Prices and Outcomes

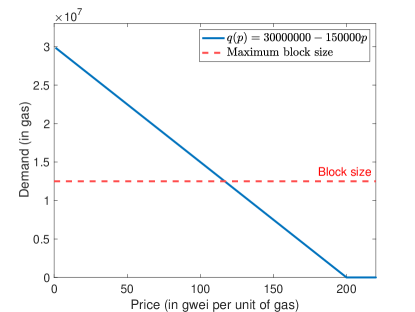

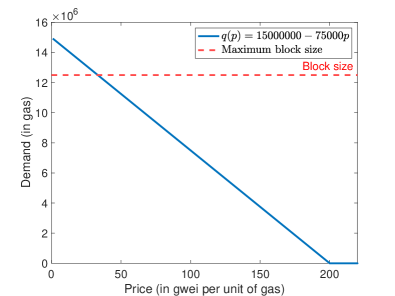

The 12.5M gas available in an Ethereum block is a scarce resource, and in a perfect world it should be allocated to the transactions that derive the most value from it. We can make this idea precise using a demand curve, which is a decreasing function that specifies the total amount of gas demanded by users at a given gas price.131313For simplicity of analysis, throughout this report we assume that demand is exogenous and independent of the choice of or actions by a transaction fee mechanism. Houy [34] and Rizun [52] use a similar formalism to reason about blockchain transaction fee markets. Richer models of demand, with pending transactions excluded from one block persisting to the next, are studied by Monnot [43, 45] in the context of EIP-1559 simulations and by Easley et al. [25] and Huberman et al. [35] to carry out an economic analysis of Bitcoin’s transaction fee mechanism. For example, a linear demand curve has the form , where denotes the gas price and are nonnegative constants (Figure 1).

The market-clearing price is then the price at which the total amount of gas demanded equals the available supply (i.e., 12.5M gas). For example, in Figure 1, the market clearing price is gwei. If the demand at price 0 is less than the supply, we define the market-clearing price as 0.

The market-clearing price is the ideal gas price for a block. For suppose such a price fell magically from the sky and became common knowledge to all users, with the understanding that all confirmed transactions in the current block will pay per unit of gas. In the resulting outcome—the market-clearing outcome—users with maximum willingness to pay at least per unit of gas will opt to have their transactions included, while those with a lower willingness to pay opt out. The end result? The supply of 12.5M gas will be fully utilized (because is a market-clearing price), and moreover will be allocated precisely to the highest-value transactions (those willing to pay a gas price of at least ).141414Or if the supply constraint is not binding (and hence ), all transactions are included. Put differently, the market-clearing outcome maximizes the value of the current block, subject to the supply constraint of 12.5M gas. For this reason, we adopt the market-clearing outcome as the most desirable one for a transaction fee mechanism. Every block is fully utilized by the highest-value transactions, with all transactions paying a gas price equal to the market-clearing price. \tfn@tablefootnoteprintout Both the status quo and EIP-1559 transaction fee mechanisms can be viewed as striving for this ideal, market-clearing outcome. In first-price auctions, users are expected to estimate what the current market-clearing price might be and bid accordingly. In the EIP-1559 mechanism, the protocol continually adjusts the base fee in search of the market-clearing price.

Remark 3.1 (Revenue as a Necessary Evil)

The purpose of the market-clearing price is to differentiate high-value and low-value transactions, so that the scarce resource that is an Ethereum block can be allocated in the most valuable way. Revenue is generated in the market-clearing outcome (provided the supply constraint is binding), but only as a side effect in the service of economic efficiency. The revenue-maximizing price is generally higher than the market-clearing price, and it plays an important role in the discussion in Section 7 of possible attacks by colluding miners.

Remark 3.2 (Non-Zero Marginal Costs)

The preceding definition of a market-clearing outcome assumes that the marginal cost to a miner of including an additional transaction in its block is 0 (or , if including the transaction would violate the cap of 12.5M gas). In reality, every transaction imposes a small marginal cost on the miner; for example, one factor is that the probability that a block is orphaned from the main chain (i.e., the “uncle rate”) increases with the block size [24].

If the overall marginal cost to a miner is gwei per unit of gas, then plays the role of 0 in the more general definitions of market-clearing prices and outcomes.151515Alternatively, is the minimum compensation per unit of gas that a miner is willing to accept for including a transaction. That is, if the demand at price is at most the supply of 12.5M gas, the market-clearing price is ; in the corresponding outcome, all transactions willing to pay a gas price of at least are included in the block.

3.2 Will EIP-1559 Lower Transaction Fees?

The Ethereum community is justifiably concerned about overly high transaction fees crowding out all but the most lucrative uses of the Ethereum blockchain (e.g., DeFi arbitrage opportunities). No transaction fee mechanism can be a panacea to this problem. This section clarifies what effects on transaction fees should and should not be expected from the adoption of the transaction fee mechanism proposed in EIP-1559.

3.2.1 The Problem of High Market-Clearing Prices

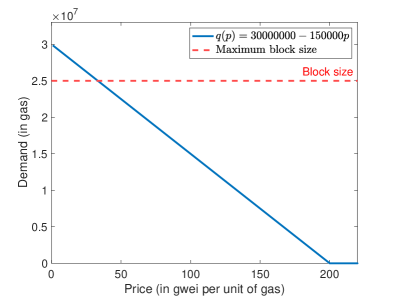

First, whatever the mechanism, real transaction fees cannot be expected to drop significantly below the market-clearing price during a period of relatively stable demand. With fees below that price, demand for gas would exceed supply, resulting in some lower-value transactions replacing higher-value transactions. For example, with the demand curve in Figure 1, if typical fees dropped to 100 gwei per unit of gas, the demand would be 15M gas. The 2.5M gas worth of excluded transactions will inevitably include some for which the creator’s willingness to pay is at least the market-clearing price of gwei. Such users should be expected to push up transaction fees and guarantee inclusion of their transactions, either on-chain through the transaction fee mechanism (e.g., by increasing a transaction’s gas price in a first-price auction), or off-chain through a side agreement with a miner.

But what if the market-clearing price is already unacceptably high? The only ways to decrease the market-clearing price are to increase supply or decrease demand (Figure 2)—actions that are generally outside the purview of mechanism design. Lowering the market-clearing price by increasing supply or decreasing demand is fundamentally a scalability problem, not a mechanism design problem. \tfn@tablefootnoteprintout For example, typical layer-1 scaling solutions like sharding, in which different parts of the blockchain operate in parallel, increase transaction throughput and therefore decrease the market-clearing price. Typical layer-2 scaling solutions like payment channels and rollups, which effectively move some transactions off-chain, decrease demand for EVM computation and likewise decrease the market-clearing price. Looking toward the near future, good scaling solutions will be crucial for keeping transaction fees in check and more generally for encouraging the growth of the Ethereum network.

3.2.2 Two Potential Benefits of EIP-1559

The transaction fee mechanism proposed in EIP-1559 has the potential to partially mitigate high transaction fees in two different ways. First, in a period of relatively stable demand, users can adopt the base fee as a good known-in-advance proxy for the market-clearing price; this should lead to less guesswork and consequent overpayment than in today’s first-price auctions. See also the discussion in Section 4.1.

Second, in a period of volatile demand, the mechanism proposed in EIP-1559 can reduce the variance in transaction fees experienced by users by exploiting variable block sizes—in effect, borrowing capacity from the near future to use in a time of need. This flexibility in block sizes can reduce the maximum transaction fee paid during the period (as well as the delay experienced by some users).

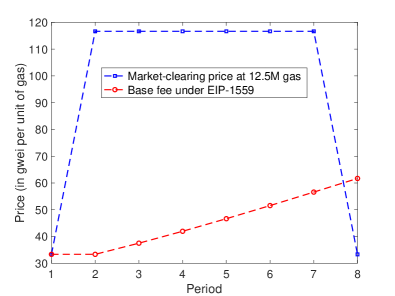

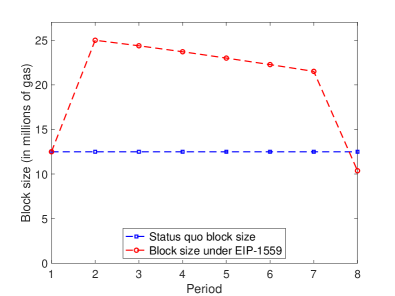

Example 3.3 (Trajectory of EIP-1559)

Consider the trajectory of the EIP-1559 mechanism that is detailed in Table 1 and depicted in Figure 3. For this example, we assume that tips are negligible and that a transaction is included in a block if and only if its fee cap is at least the current base fee. Period 1 represents the end of a long era of stable demand, during which the base fee converged to the market-clearing price for the target block size (12.5M gas). Demand doubles for the next six periods. With a fixed supply of 12.5M gas, the market-clearing price jumps suddenly from to after period 1, and back to after period 7. In the EIP-1559 mechanism, the base fee—the mechanism’s guess at the current market-clearing price for the target block size—increases slowly but surely, with larger-than-target blocks absorbing the excess demand along the way. Once demand returns to its original level, blocks will have size smaller than the target as the mechanism’s base fee slowly but surely decreases to the new market-clearing price. In this example, the maximum base fee of 61.69 (in period 8) is only about 53% of the maximum market-clearing price with a fixed block size of 12.5M gas (, in periods 2–7).

| Period 1 | Period 2 | Period 3 | Period 4 | Period 5 | Period 6 | Period 7 | Period 8 | |

| Demand | Low | High | High | High | High | High | High | Low |

| M-C Price (12.5M) | ||||||||

| EIP-1559 Base Fee | ||||||||

| EIP-1559 Block Size | 12.5M | 25M | 24.38M | 23.71M | 23M | 22.27M | 21.51M | 10.37M |

4 The Purpose of EIP-1559: Easy Fee Estimation

4.1 The Problem of Fee Estimation

With or without EIP-1559, transaction fees will be high whenever the demand for EVM computation far exceeds its supply (Section 3.2). So what’s the point of the proposal? To make transaction fees more predictable and thereby make the fee estimation problem—the problem of choosing the optimal gas price for a transaction—as straightforward as possible.

Ethereum users appear to overpay regularly for EVM computation, offering gas prices that are significantly larger than the market-clearing price [3]. Part of the problem may be attributable to poor fee estimation algorithms in wallets, which could conceivably improve over time (see e.g. [39, 48], in the similar context of Bitcoin). But part of the problem is fundamental to first-price auctions, and addressing it necessitates a major change in the transaction fee mechanism.161616Bidding in a first-price auction has long been known to be a hard problem; see e.g. [22].

EIP-1559 also offers a number of other benefits (see Section 9.1), which are treated in this report as happy accidents—byproducts of the proposed UX improvements.171717This viewpoint appears consistent with the original motivation for EIP-1559. Buterin [19] writes: “Our goal is to discourage the development of complex miner strategies and complex transaction sender strategies in general, including both complex client-side calculations and economic modeling as well as various forms of collusion.”

4.2 Auctions vs. Posted-Price Mechanisms

To what extent does EIP-1559 achieve its goal of a “better UX”? “User experience” is a vague term, and it must be defined mathematically before this question can be answered.

Definition 5.21 presents our formalization of “good UX,” and the intuition for it is simple: Shopping on Amazon is a lot easier than buying a house in a competitive real estate market. On Amazon, there’s no need to be strategic or second-guess yourself; you’re either willing to pay the listed price for the listed product, or you’re not. The outcome is economically efficient in that every user who buys a product has a higher willingness to pay for it than every user who doesn’t buy the product.

When pursuing a house and competing with other potential buyers, you must think carefully about what price to offer to the seller. And no matter how smart you are, you might regret your offer in hindsight—either because you underbid and were outbid at a price you would have been willing to pay, or because you overbid and paid more than you needed to. The house need not be sold to the potential buyer willing to pay the most (if that buyer shades their bid too aggressively), which is a loss in economic efficiency.

Bidding in Ethereum’s first-price auctions is like buying a house. Estimating the optimal gas price for a transaction requires making educated guesses about the gas prices chosen for the competing transactions. From a user’s perspective, any bid may end up looking too high or too low in hindsight. From a societal perspective, lower-value transactions that bid aggressively may displace higher-value transactions that do not.

Could we redesign Ethereum’s transaction fee mechanism so that setting a transaction’s gas price is more like shopping on Amazon? Ideal would be a posted-price mechanism, meaning a mechanism that offers each user a take-it-or-leave-it gas price for inclusion in the next block. We’ll see in Section 6.3 that the transaction fee mechanism proposed in EIP-1559 acts like a posted-price mechanism except when there is a large and sudden increase in demand (Theorem 6.8).

5 Incentive-Compatible Transaction Fee Mechanisms

This section formalizes three desirable game-theoretic guarantees for a transaction fee mechanism. First, miners should be incentivized to carry out the mechanism as intended, and strongly disincentivized from including fake transactions (Section 5.3). Second, the optimal gas price to specify should be obvious to the creator of a transaction (Section 5.4). Finally, there should be no way for miners and users to collude and strictly increase their utility by moving payments off-chain (Section 5.5). Sections 5.1 and 5.2 set up the notation and language necessary to formally state these three definitions.

This and the next section focus on incentives for miners and users at the time scale of a single block, and on two important types of attacks that can be carried out at this time scale (the insertion of fake transactions, and off-chain agreements between miners and users). Section 7 treats incentive issues and attacks that manifest over longer time scales.

5.1 The Basic Model

On the supply side, let denote the maximum size of a block in gas (e.g., 12.5M gas in the status quo or 25M gas under EIP-1559), and the marginal cost of gas to a miner (as in Remark 3.2).181818Equivalently, is the minimum gas price that a profit-maximizing miner is willing to accept in exchange for transaction inclusion when the maximum block size is not a binding constraint. The formal definition of a “profit-maximizing miner” is given in Definition 5.13. For simplicity, we assume that is the same for all miners and common knowledge among users.191919Calculations by Buterin [1] suggest that is, at this time of writing, on the order of 0.4–3.3 gwei. In a proof-of-stake blockchain such as ETH 2.0, the parameter is likely to be even smaller. On the demand side, let denote the set of transactions in the mempool at the time of the current block’s creation.

We associate three parameters with each transaction :

-

•

a gas limit in gas;

-

•

a value in gwei per unit of gas;

-

•

a bid in gwei per unit of gas.

The gas limit is the amount of gas required to carry out the transaction. The value is the maximum gas price the transaction’s creator would be willing to pay for its execution in the current block.202020We assume that the value is independent of the position in the block, ignoring e.g. front-running bots aiming to secure the first position in a block (see [23, 53]). The bid corresponds to the gas price that the creator actually offers to pay, which in general can be less (or more) than the value. With a first-price auction, the bid corresponds to the gas price specified for a transaction. In the transaction fee mechanism proposed in EIP-1559, the bid corresponds to the minimum of the fee cap and the sum of the base fee and the tip ( in the notation of Section 2.3). We view the gas limit and value as immutable properties of a transaction; the bid, by contrast, is under control of the transaction’s creator. The gas limit and bid of a confirmed transaction are recorded on-chain; the value of a transaction is known solely to its creator.

5.2 Allocation, Payment, and Burning Rules

A transaction fee mechanism decides which transactions should be included in the current block, how much the creators of those transaction have to pay, and to whom their payment is directed. These decisions are formalized by three functions: an allocation rule, a payment rule, and a burning rule.

5.2.1 Allocation Rules

We use to denote the sequence of blocks in the current longest chain (with the genesis block and the most recent block) and the pending transactions in the mempool. Generally, bold type (like ) will indicate a vector and regular type (like ) one of its components.

Definition 5.1 (Allocation Rule)

An allocation rule is a vector-valued function from the on-chain history and mempool to a 0-1 value for each pending transaction .

A value of 1 for indicates transaction ’s inclusion in the current block ; a value of 0 indicates its exclusion. We sometimes write , with the understanding that is the set of transactions for which .

We consider only feasible allocation rules, meaning allocation rules that respect the maximum block size .

Definition 5.2 (Feasible Allocation Rule)

An allocation rule is feasible if, for every possible history and mempool ,

| (3) |

We call a set of transactions feasible if they can all be packed in a single block: .

Remark 5.3 (Miners Control Allocations)

While a transaction fee mechanism is generally designed with a specific allocation rule in mind, it is important to remember that a miner ultimately has dictatorial control over the block it creates.

Example 5.4 (First-Price Auction Allocation Rule)

The (intended) allocation rule in a first-price auction is to include a feasible subset of outstanding transactions that maximizes the sum of the gas-weighted bids, less the gas costs. That is, the ’s are assigned 0-1 values to maximize

| (4) |

subject to (3).

5.2.2 Payment and Burning Rules

The payment rule specifies the revenue earned by the miner from included transactions.

Definition 5.5 (Payment Rule)

A payment rule is a function from the current on-chain history and transactions included in the current block to a nonnegative number for each included transaction .

The value of indicates the payment from the creator of an included transaction to the miner of the block (in ETH, per unit of gas).

For example, in a first-price auction, a winner always pays its bid (per unit of gas), no matter what the blockchain history and other included transactions.

Example 5.6 (First-Price Auction Payment Rule)

In a first-price auction,

for all and .

Finally, the burning rule specifies the amount of ETH burned—or equivalently, refunded to ETH holders—for each of the included transactions.

Definition 5.7 (Burning Rule)

A burning rule is a function from the current on-chain history and transactions included in the current block to a nonnegative number for each included transaction .

The value of indicates the amount of ETH burned (per unit of gas) by the creator of an included transaction .

Example 5.8 (First-Price Auction Burning Rule)

Status quo first-price auctions burn no fees, so

for all and .

Remark 5.9 (The Protocol Controls Payments and Burns)

A miner does not control the payment or burning rule, except inasmuch as it controls the allocation, meaning the transactions included in . Given a choice of allocation, the on-chain payments and fee burns are completely specified by the protocol. (Miners might seek out off-chain payments, however; see Section 5.5.)

Remark 5.10 (Mempool-Dependence)

The allocation rule depends on the mempool because a miner can base its allocation decision on the entire set of outstanding transactions. Payment and burning rules must be computable from the on-chain information , and in particular cannot depend on outstanding transactions of excluded from the current block .

5.2.3 Transaction Fee Mechanisms

Formally, a transaction fee mechanism is specified by its allocation, payment, and burning rules.

Definition 5.11 (Transaction Fee Mechanism (TFM))

A transaction fee mechanism (TFM) is a triple in which is a feasible allocation rule, is a payment rule, and is a burning rule.

For example, a first-price auction is mathematically encoded by the triple in which is the revenue-maximizing allocation rule (Example 5.4), is the pay-as-bid payment rule (Example 5.6), and is the all-zero burning rule (Example 5.8).

Finally, we consider only individually rational mechanisms, meaning TFMs that cannot force users to pay more than their declared willingness to pay.

Definition 5.12 (Individual Rationality)

A TFM is individually rational if, for every history ,

for every transaction .

5.3 Incentive Compatibility (Myopic Miners)

This section formalizes what it means for a TFM to be game-theoretically sound from the perspective of miners—intuitively, that a miner is incentivized to implement the intended allocation rule and disincentivized from including fake transactions. As a reminder, our current focus is on incentives at the time scale of a single block, with longer time scales discussed in Section 7.

5.3.1 Myopic Miner Utility Function

In addition to choosing an allocation (Remark 5.3), we assume that miners can costlessly add any number of fake transactions to the mempool (with arbitrary gas limits and bids). We call a miner myopic if its utility—meaning the quantity that it acts to maximize—equals its net revenue from the current block.212121We ignore the block reward (currently 2 ETH), as it is independent of the miner’s actions and therefore irrelevant for the single-block game-theoretic analysis in this and the next section. The block reward does, of course, affect the security of the Ethereum blockchain (e.g. [10, 14]).

Definition 5.13 (Myopic Miner Utility Function)

For a TFM , on-chain history , mempool , fake transactions , and choice of included transactions (real and fake), the utility of a myopic miner is

| (5) |

The first term sums over only the real included transactions, as for fake transactions the payment goes from the miner to itself. The second term sums over only the fake transactions, as for real transactions the burn is paid by their creators (not the miner). In (5), we highlight the dependence of the utility function on the two arguments that are under a miner’s direct control, the choices of the fake transactions and included (real and fake) transactions .222222We can assume that , as there’s no point to creating and then excluding a fake transaction.

5.3.2 Incentive-Compatibility for Myopic Miners

A transaction fee mechanism is generally designed with a specific allocation rule in mind (Remark 5.3), but will miners actually implement it?

Definition 5.14 (Incentive-Compatibility for Myopic Miners (MMIC))

A TFM is incentive-compatible for myopic miners (MMIC) if, for every on-chain history and mempool , a myopic miner maximizes its utility (5) by creating no fake transactions (i.e., setting ) and following the suggestion of the allocation rule (i.e., setting ).

Example 5.15 (First-Price Auctions Are MMIC)

A status quo first-price auction is MMIC. Because is the all-zero function (Example 5.8), the second term in (5) is zero. Because payments equal bids (Example 5.6), miner utility equals the exact same quantity (4) maximized by the allocation rule (Example 5.4). Thus, myopic miner utility is maximized by following the allocation rule and setting .

Example 5.16 (Vickrey (Second-Price) Auctions Are Not MMIC)

Vickrey (a.k.a. second-price) auctions play as central a role in traditional auction theory as first-price auctions. Their claim to fame is that, assuming the auction is implemented by a trusted third party, truthful bidding (i.e., setting one’s bid equal to one’s value ) is a dominant strategy, meaning it maximizes a bidder’s utility no matter what the other bidders do. This property sure sounds like “easy fee estimation,” so why not use it as a TFM?

Unfortunately, Vickrey auctions can be manipulated via fake transactions and thus fail to be MMIC. For example, consider a set of transactions that all have the same gas limit and a block that has room for three of them. In this setting, a Vickrey auction would prescribe including the three transactions with the highest bids and charging each of them (per unit of gas) the lowest of these three bids.232323Actually, a Vickrey auction would prescribe charging the highest losing bid rather than the lowest winning bid. The former is off-chain and thus unimplementable in a blockchain context, while the latter is on-chain and typically close enough. Now imagine that the top three bids are 10, 8, and 3. If a miner honestly executes a Vickrey auction, its revenue will be . If the miner instead submits a fake transaction with bid 8 and executes a Vickrey auction (with the top two real transactions included along with the fake transaction), its net revenue jumps to .

Remark 5.17 (Credible Mechanisms)

The definition of MMIC (Definition 5.14) is closely related to Akbarpour and Li’s notion of a credible mechanism [9]. Intuitively, a mechanism is credible if the agent tasked with carrying it out has no plausibly deniable utility-improving deviation. For instance, Example 5.16 is a proof that the Vickrey auction is not credible in this sense. Akbarpour and Li [9] study both single-shot (a.k.a. “static”) mechanisms and mechanisms that require many rounds (such as ascending auctions); the former type are much more practical for blockchain transaction fee mechanisms. Interestingly, one of the main results in [9, Theorem 3.7] is that first-price auctions with an exogenously restricted bid space are the only static credible mechanisms.242424The results in [9] assume a computationally unbounded auctioneer. Ferreira and Weinberg [26] explore what other credible mechanisms are possible assuming a computationally bounded auctioneer and the existence of cryptographically secure hash functions. All of the MMIC mechanisms appearing in this report—first-price auctions (Example 5.15), the 1559 mechanism (Theorem 6.4), and the tipless mechanism of Section 8.5 (Theorem 8.8)—can be viewed as first-price auctions with different restricted bid spaces.252525First-price auctions correspond to the bid space ; the 1559 mechanism to the bid space , where is the block’s base fee; and the tipless mechanism to the bid space , where is the block’s base fee and is a protocol-defined hard-coded tip.

Returning to status quo first-price auctions, the argument in Example 5.15 highlights two of their properties:

-

(i)

excluding real transactions suggested by the allocation rule strictly decreases myopic miner utility;

-

(ii)

including fake transactions does not increase myopic miner utility.

We next pursue a stronger version of property (ii).

5.3.3 -Costly Transaction Fee Mechanisms

A stronger version of property (ii) would state that, as with excluding real transactions, fake transactions significantly decrease myopic miner utility. First-price auctions possess this stronger property when the maximum block size constraint is binding (as fake transactions then displace real ones) or when the marginal cost is large. Otherwise, a miner can devote any extra room in a block to fake transactions without suffering a significant cost.

The next definition formalizes this stronger version of property (ii).

Definition 5.18 (-Costly Transaction Fee Mechanism)

A TFM is -costly if, for every on-chain history , mempool , fake transactions , and block chosen by a miner, the fake transactions of decrease myopic miner utility (5) by at least per unit of gas:

For example, first-price auctions are -costly, where is the marginal cost of gas to a miner, and are not -costly for any . We’ll see later (Corollary 6.5) that the transaction fee mechanism proposed in EIP-1559 is generally -costly for larger values of , and in this sense more aggressively punishes fake transactions.

5.4 Incentive Compatibility (Users)

Next we formalize what it means for a TFM to be game-theoretically sound from the perspective of users—intuitively, that there is an “obvious’ optimal bid” when creating a new transaction. This is also our definition of a “good user experience” is the sense of easy fee estimation (see Section 4).

5.4.1 User Utility Function

Recall from Section 5.1 that the value of a transaction is the maximum gas price the transaction’s creator would be willing to pay for its inclusion in the current block. We assume that a user bids in order to maximize its net gain (i.e., the value for inclusion minus the cost for inclusion). To reason about the different possible bids for a transaction submitted to a mempool , we use to denote the result of adding the transaction with bid to . For simplicity, we assume that each transaction in the current mempool has a distinct creator.

Definition 5.19 (User Utility Function)

For a TFM , on-chain history , and mempool , the utility of the originator of a transaction with value and bid is

| (6) |

if is included in and 0 otherwise.

In (6), we highlight the dependence of the utility function on the argument that is directly under a user’s control, the bid submitted with the transaction. We assume that a transaction creator bids to maximize the utility function in (6).262626While the creator of a transaction has no direct control over , , or , its bid is embedded in and therefore can affect . This, in turn, can affect and . For example, whether or not generally depends on whether or not is large relative to the bids of competing transactions in .

5.4.2 Bidding Strategies and Ex Post Nash Equilibrium

Intuitively, “easy fee estimation” should mean that the “obvious” bidding strategy is optimal. Formally, a bidding strategy is a function that specifies a bid for a transaction as a function of the value of that transaction. A bidding strategy is a function of the value only (which is known to the transaction creator) and not, for example, bids submitted by competing transactions (which are not).272727A bidding strategy can depend also on the blockchain history (e.g., with EIP-1559, on the current base fee). For the purposes of a single-block game-theoretic analysis, we can take the history as fixed and suppress this dependence in the notation. For example, a plausible bidding strategy in a first-price auction is to shade one’s bid, but not by too much, perhaps by setting for all .

Suppose we have in mind an “obvious” bidding strategy for users to employ. What does it mean that bidding in this obvious way is “always optimal”? The answer is formalized by the concept of a symmetric ex post Nash equilibrium (symmetric EPNE). Intuitively, obvious bidding should maximize a user’s utility as long as all the other users are also bidding in the obvious way.282828“Symmetric” refers to the fact that the obvious bidding strategy is the same for every transaction .

Definition 5.20 (Symmetric Ex Post Nash Equilibrium (Symmetric EPNE))

Fix a TFM and the on-chain history . A bidding strategy is a symmetric ex post Nash equilibrium (symmetric EPNE) if, for every mempool in which all transactions’ bids were set according to this strategy, and for every transaction with value , bidding maximizes the utility (6) of ’s creator.

Crucially, following the bid recommendation of a symmetric EPNE does not require reasoning about competing transactions in , other than keeping the faith that their bids were set according to the bid recommendations of the symmetric EPNE.292929An even stronger notion is a dominant-strategy equilibrium, in which is optimal for ’s creator no matter what the other users do. “Obvious bidding” is not a dominant-strategy equilibrium in the transaction fee mechanism proposed in EIP-1559 (see Remark 6.10), but it is in a variant with hard-coded tips (see Theorem 8.9 and footnote 56).

We can now define a TFM to be incentive-compatible from the user perspective if there’s always an obvious bidding strategy in the form of a symmetric EPNE.

Definition 5.21 (Incentive-Compatibility for Users (UIC))

A TFM is incentive-compatible for users (UIC) if, for every on-chain history , there is a symmetric EPNE.

In this report, we identify “mechanisms with easy fee estimation” and “mechanisms with good UX” with the UIC condition of Definition 5.21.

Example 5.22 (First-Price Auctions Are Not UIC)

First-price auctions are not easy to reason about, in the sense that they are not UIC. Intuitively, the utility-maximizing bid depends on the precise numerical values of others’ bids, and not merely on the qualitative knowledge that they are following a particular bidding strategy.

For example, consider a block with room for one transaction, a transaction with value , and suppose that all transactions other than use the same bidding strategy . If the highest value of of any transaction is 10, then the highest bid by any such transaction will be 7.5, and the utility-maximizing bid for ’s creator will be 7.51. If the highest other value is 8, the optimal bid is 6.01; and so on. The key point is that the optimal bid to include with the transaction is a function not only of that transaction’s value, but also of the values of the competing transactions (even after assuming that all their bids are set using a known bidding strategy ).

Thus, in a precise sense, first-price auctions do not offer “good UX” in the form of an easy-to-follow optimal bid recommendation. We’ll see later (Theorem 6.8) that the transaction fee mechanism proposed in EIP-1559 is UIC except during periods of rapidly increasing demand.

5.5 Off-Chain Agreements

The game-theoretic guarantees in Section 5.3 concern attacks that manipulate the contents of a block (by including fake transactions, or more generally deviating from the allocation intended by the transaction fee mechanism). This section treats a different type of attack that is also implementable at the time scale of a single block, namely collusive agreements between miners and users. Recall that a set of transactions is feasible if the total gas is at most the maximum block size .

Definition 5.23 (Off-Chain Agreement (OCA))

For a feasible set of transactions and a miner , an off-chain agreement (OCA) between ’s creators and specifies:

-

(i)

a bid vector , with indicating the bid to be submitted with the transaction ;

-

(ii)

a per-gas-unit ETH transfer from the creator of each transaction to the miner .

In an OCA, each creator of a transaction agrees to submit on-chain with a bid of while transferring per unit of gas to the miner off-chain; the miner, in turn, agrees to mine a block comprising the transactions in (with on-chain bids ).

Example 5.24 (Moving Payments Off-Chain)

To get a feel for OCAs, imagine a first-price auction in which 50% of the revenue is burned and the other 50% is transferred to the miner. (See also Section 8.2.) Miners and users could then collude as follows:

-

1.

Users bid zero on-chain and communicate off-chain what they would have bid in a standard first-price auction.

-

2.

Miners keep 75% of the (off-chain) bids of the transactions they include, with the other 25% refunded to those transactions’ creators.

In the notation of Definition 5.23, this is the OCA in which and , where denotes what ’s creator would have bid in a first-price auction without fee-burning. Compared to the “honest” on-chain outcome with bids , miners earn 50% more revenue and users enjoy a 25% discount, both at the expense of the network.

Given a TFM and on-chain history , the utility of ’s creator from such an OCA is given by the right-hand side of (6), less its transfer to the miner:

| (7) |

(Users not part of receive zero utility.) The miner’s utility is given by the sum of on-chain and off-chain payments received, less the costs incurred:

| (8) |

Adding up these utility functions—one per transaction , plus one for the miner—results in the joint utility enjoyed by all parties in an OCA :

From the coalition’s perspective, on-chain and off-chain payments from the users to the miner (the ’s and ’s) remain within the coalition and thus cancel out; the fee burn (the ’s) is transferred outside the coalition (to the network) and is therefore a loss. Thus, the point of an OCA is to maximize the joint utility—the amount of transaction value that is not lost to the protocol or to the miner’s costs.

Definition 5.25 (Joint Utility)

For an on-chain history , the joint utility of the miner and users for the block is

| (9) |

We assume that miners and users act to maximize their joint utility. Using transfers, a miner and users can then split this joint utility among themselves in an arbitrary way.303030For example, suppose an OCA increases the joint utility of a coalition by increasing the utility of six users by 1 ETH each while decreasing the miner’s utility by 5 ETH. The OCA transfers can then be adjusted so that all parties enjoy strictly higher individual utility, for example by sending an extra ETH from each of these users to the miner. Additional transfers can be used to also strictly increase the utility of the creators of the transactions excluded from the block . For this reason, when analyzing OCAs, we can focus on the joint utility (9) of the miner and the creators of the included transactions, without concern about how it might be split among them and the creators of the excluded transactions.

A TFM is then OCA-proof if, for every OCA, there is an equally good on-chain outcome. For a set of transactions and bids for those transactions, we denote by the corresponding mempool.

Definition 5.26 (OCA-Proof)

A TFM is OCA-proof if, for every on-chain history and set of outstanding transactions, there exists bids for the transactions of such that, for the resulting on-chain outcome ,

| (10) |

for every feasible subset of transactions and OCA between their creators and the miner .

In other words, if a TFM is not OCA-proof, there are scenarios in which a miner and users can collude to achieve higher joint utility—and, after defining appropriate transfers, higher individual utilities—than in any on-chain outcome.

Intuitively, first-price auctions are OCA-proof because off-chain payments can be costlessly replaced by on-chain bids. The next example formally verifies Definition 5.26.

Example 5.27 (First-Price Auctions Are OCA-Proof)

Remark 5.28 (OCA-Proofness and Fee Burning)

OCAs are the biggest game-theoretic driver for the why and the how of the fee burn in the transaction fee mechanism proposed in EIP-1559. For example, adding a fee burn to a first-price auction destroys its OCA-proofness (Section 8.2). Meanwhile, because of OCAs, a history-dependent base fee has no teeth unless revenue from it is burned or otherwise withheld from the miner (Section 8.1).

6 Formal Analysis of the 1559 Mechanism with Myopic Miners

This section investigates to what extent the transaction fee mechanism proposed in EIP-1559—henceforth, the 1559 mechanism—satisfies the three game-theoretic guarantees identified in Section 5 (MMIC, UIC, and OCA-proofness). Section 6.1 translates the description of the mechanism in Section 2.3 into the formalism introduced in Section 5. Sections 6.2–6.4 prove that the mechanism is always MMIC and OCA-proof, and is UIC except during periods of rapidly increasing demand.

6.1 The 1559 Mechanism

Recall from Section 2.3 that, in the 1559 mechanism, each block is associated with a base fee that is fixed by the history of past blocks and independent of the contents of the current block; we denote by the base fee for the next block that is determined by a particular history . The specific function proposed in EIP-1559 is the iteration of the base fee update rule in (2), although these details will not be important for the single-block game-theoretic analysis carried out in this section.

Recall also that, in EIP-1559, each transaction specifies a tip and a fee cap . These two parameters induce a bid for the transaction with respect to any given base fee , namely

| (11) |

Definition 6.1 (1559 Allocation Rule)

For each history and corresponding base fee , the (intended) allocation rule of the 1559 mechanism is to include a feasible subset of outstanding transactions that maximizes the sum of the gas-weighted bids, less the gas costs and total base fee paid. That is, the ’s are assigned 0-1 values to maximize

| (12) |

subject to the block size constraint (3).

The payment rule transfers the difference between the bid and the base fee to the miner.

Definition 6.2 (1559 Payment Rule)

In the 1559 mechanism, letting ,

for all and .

The burning rule burns the base fee.

Definition 6.3 (1559 Burning Rule)

In the 1559 mechanism, letting ,

for all and .

6.2 The 1559 Mechanism Is Incentive Compatible for Myopic Miners

This section evaluates the 1559 mechanism from the perspective of myopic miners, and specifically the MMIC property (Definition 5.14) and -costliness (Definition 5.18).

Theorem 6.4 (The 1559 Mechanism is MMIC)

The 1559 mechanism is MMIC.

Proof.

Fix an on-chain history , a mempool , and a marginal cost of gas (as in Remark 3.2). Let denote the corresponding base fee for the current block. Substituting in Definitions 6.2 and 6.3, myopic miner utility (5) equals

| (13) |

where denotes the transactions included by the miner and the fake transactions that it creates. Included fake transactions strictly increase the second term (by per unit of gas) while leaving the first unaffected, so a myopic miner will only include real transactions in . In this case, myopic miner utility equals

which is identical to the quantity (12) maximized by the allocation rule (Definition 6.1). Thus, myopic miner utility is maximized by following the allocation rule and setting equal to . ∎

From the expression (13) for myopic miner utility in the 1559 mechanism, we can see immediately that it is -costly (Definition 5.18) for .

Corollary 6.5 (The 1559 Mechanism is -Costly)

Fix an on-chain history and corresponding base fee for the current block, a mempool , and a marginal cost of gas . The 1559 mechanism is -costly.

Remark 6.6 (Role of the Fee Burn)

If the base fee was paid to miners rather than burned, the 1559 mechanism would only be -costly and fake transactions would be only mildly disincentivized. The primary motivation for the fee burn, however, is to rule out its evasion by off-chain agreements (see Section 8.1).

6.3 The 1559 Mechanism Is Typically Incentive Compatible for Users

The 1559 mechanism is always incentive compatible for myopic miners, no matter what the current base fee and demand for block space (Theorem 6.4). We next show that the mechanism is also incentive compatible for users, except in periods of rapidly increasing demand.

6.3.1 Excessively Low Base Fees

The next definition is a proxy for a period of rapidly increasing demand.

Definition 6.7 (Excessively Low Base Fee)

Let denote the marginal cost per unit of gas. A base fee is excessively low for a mempool of transactions if the demand at price exceeds the maximum block size :

| (14) |

Excessively low base fees arise from large and sudden demand spikes. In Example 3.3 in Section 3.2, for instance, none of the eight periods suffer from an excessively low base fee, despite the sudden doubling of demand. Modifying that example so that demand more than doubles in period 2, there is a sequence of periods with excessively low base fees, ending once the base fee has increased enough to bring demand back down below 25M gas (Table 2).

| Period 1 | Period 2 | Period 3 | Period 4 | Period 5 | Period 6 | Period 7 | Period 8 | |

| Demand | Low | High | High | High | High | High | High | Low |

| EIP-1559 Base Fee | ||||||||

| EIP-1559 Block Size | 12.5M | 25M | 25M | 25M | 25M | 25M | 24.49M | 10.04M |

| Excessively low? | No | Yes | Yes | Yes | Yes | Yes | No | No |

6.3.2 The 1559 Mechanism Is UIC Except with Excessively Low Base Fees

When the base fee is excessively low, users must compete for scarce block space through their tips, and the 1559 mechanism effectively reverts back to a first-price auction. As first-price auctions are essentially never UIC (see Example 5.22), the 1559 mechanism is not UIC when the base fee is excessively low. The good news is that an excessively low base fee is the only reason why the 1559 mechanism might fail to be UIC. That is, whenever the base fee is not excessively low, there is an “obvious optimal bid” in the form of a symmetric EPNE (Definition 5.20). This optimal bid corresponds to setting a transaction’s fee cap equal to its creator’s value (i.e., ), and a transaction’s tip equal to the marginal cost of gas to a miner (i.e., ).

Theorem 6.8 (The 1559 Mechanism Is Typically UIC)

Fix an on-chain history and corresponding base fee , a marginal cost of gas to miners, and a mempool of transactions for which is not excessively low. The bidding strategy

| (15) |

constitutes a symmetric EPNE under the 1559 mechanism.

Proof.

Suppose each creator of a transaction sets its bid according to the strategy in (15); we need to show that no creator could increase its expected utility (6) by changing its bid (holding the bids of other transactions fixed).

The objective (12) of the 1559 allocation rule prescribes including precisely the transactions with . Because for all , these are precisely the transactions with . In particular, because is not excessively low for , this allocation is feasible:

| (16) |

There are two types of transactions to consider, high-value () and low-value (); see also Table 3. When all bids are set according the strategy in (15), the former transactions are included (and pay per unit of gas) while the latter are excluded (and pay nothing). The utility (6) of ’s creator is if is a high-value transaction and 0 otherwise. Every alternative bid for a high-value transaction either has no effect on its creator’s utility (if ) or leads to ’s exclusion from the block (if ) and reduces this utility from to 0. Every alternative bid for a low-value transaction either has no effect on its creator’s utility or leads to ’s inclusion in the block; the latter can only occur when , in which case the creator’s utility drops from 0 to . We conclude that there is no alternative bid for any transaction of that increases its creator’s utility. ∎

Theorem 6.8 and its proof show that, at its symmetric EPNE, the 1559 mechanism acts a posted-price mechanism (Section 4.2) except when the base fee is excessively low. The 1559 mechanism acts as a posted-price mechanism at the price , where is the base fee and is the marginal cost of gas, except during periods of rapidly increasing demand. \tfn@tablefootnoteprintout

| Low-Value () | High-Value () | |

|---|---|---|

| Bid at EPNE | ||

| Utility at EPNE | 0 | |

| Utility of Alternative | 0 |

Remark 6.9 (Welfare Properties of the 1559 Mechanism)

An attractive property of the symmetric EPNE in (15) is that the outcome perfectly differentiates between high-value () and low-value () transactions, including the former while excluding the latter. This outcome can be viewed as a market-clearing outcome (Section 3.1) with respect to a supply of gas, where denotes the demand at price .

Remark 6.10 (The Obvious Bid Is Not a Dominant Strategy)

The symmetric EPNE (15) in the proof of Theorem 6.8 is not a dominant-strategy equilibrium in the sense of footnote 29. The issue arises when the creators of other transactions overstate their fee caps, in which case the base fee could become excessively low with respect to the stated demand (even though it is not with respect to the true demand). In particular, the equality in (16) need not hold if other transactions’ bids are set arbitrarily.

Remark 6.11 (Expected Frequency of Excessively Low Base Fees)

Demand for EVM computation has generally been volatile, at both short and long time scales. For this reason, one would expect at least occasional excessively low base fees. It would be interesting to predict, perhaps based on experiments using historical demand data, the likely frequency of excessively low base fees in a post-EIP-1559 world.

6.4 The 1559 Mechanism Is OCA-Proof

Finally, we show that, under the 1559 mechanism, miners and users cannot improve their joint utility through off-chain agreements. A key driver of this result is that the fee burn (per unit of gas) does not depend on the current actions of the miner or users (cf., Section 8.2).

Theorem 6.12 (The 1559 Mechanism is OCA-Proof)

The 1559 mechanism is OCA-proof.

Proof.

Fix an on-chain history and corresponding base fee . Consider a set of transactions and set for every . Then, because is the constant function always equal to (Definition 6.3), the objective (12) maximized by the allocation rule is identical to the joint utility (9). Thus, the joint utility of the on-chain outcome with bids cannot be improved upon by any OCA. ∎

7 Miner Collusion at Longer Time Scales

Section 6 demonstrates that the 1559 mechanism enjoys several game-theoretic guarantees at the time scale of a single block. But what about longer time scales? For example, to achieve the typically-UIC guarantee in Theorem 6.8, the mechanism introduces a history-dependent base fee that is burned; a natural worry is that miners may be incentivized to manipulate and artificially decrease this base fee over time.

This section investigates the incentives for miner collusion, both under the status quo and under EIP-1559. Section 7.1 formalizes “extreme miner collusion” through a thought experiment in which a single miner controls 100% of Ethereum’s hashrate. Section 7.2 identifies the revenue-maximizing strategy for such a miner in a first-price auction; in some cases, the miner is incentivized to artificially restrict the supply of EVM computation in order to boost the bids submitted by creators of high-value transactions. Section 7.3 repeats the exercise for the 1559 mechanism and determines that the outcome of extreme collusion would be similar to that with today’s first-price auctions. Section 7.4 classifies different types of miner collusion and reviews to what extent each type appears to occur in Ethereum at present. Section 7.5 argues that the game-theoretic impediments to double-spend, censorship, denial-of-service, and revenue-maximizing 100% miner strategies (including base fee manipulation) appear as strong under EIP-1559 as under the status quo. Finally, Section 7.6 brainstorms possible reasons for why miner collusion might nevertheless be more likely under EIP-1559 than it is today.

7.1 Extreme Collusion: The 100% Miner Thought Experiment

The fidelity of the myopic miner model of Sections 5–6 depends on the degree of decentralization in Ethereum mining. For example, with extreme decentralization, such as the hashrate being spread equally across millions of non-colluding miners, any given miner mines a block so rarely that there is no point to non-myopic strategies (i.e., strategies that forego immediate rewards in favor of future rewards). In particular, in the 1559 mechanism, because the base fee is set by past history and independent of the current block, no such miner will be interested in manipulating it.

To meaningfully study miner deviations such as base fee manipulation, we must therefore consider miners (or tightly coordinated mining pools) that possess a significant fraction of the total hashrate and strategize at time scales longer than a single block.313131We continue to assume that users are myopic, and bid to maximize their utility in the current block (Definition 5.19). Simulations by Monnot [45] suggest that more complex user strategies do not significantly change the behavior of the mechanism proposed in EIP-1559. To get the lay of the land, we next investigate both first-price auctions and the 1559 mechanism in the opposite extreme scenario in which all of the hashrate is controlled by a single miner or, equivalently, a perfectly coordinated cartel comprising all of the miners.323232A similar approach is taken by Hasu et al. [32] in the context of Bitcoin and Zoltu [59] in the context of EIP-1559. 1. A single miner controls 100% of the hashrate. 2. The miner acts to maximize its net revenue received from transaction fees over a significant period of time (e.g., thousands of blocks). 3. The demand curve (see Section 3) is the same for every block, independent of the miner’s actions, and known to the miner. \tfn@tablefootnoteprintout The second assumption clarifies that the thought experiments in Sections 7.2 and 7.3 will not consider off-chain rewards, for example from a double-spend attack, in order to isolate incentive issues specific to the transaction fee mechanism. The point of the third assumption is to stack the deck against a protocol by making it as easy as possible for a miner or cartel of miners to identify and carry out optimal deviations from the protocol’s prescriptions.

7.2 First-Price Auctions with a 100% Miner

What would a 100% miner do under the status quo of first-price auctions? Let denote the demand curve—the total gas demanded at a gas price of gwei. We assume that is a continuous and strictly decreasing function, and that once is sufficiently large. We continue to assume that the demand curve is exogenous, the same for every block, and known to the miner.

We consider strategies of the following form: 1. Price-setting: for a gas price with , include a transaction in the block if and only if its gas price is at least . (As usual, denotes the maximum block size.)333333For an analogy, think of a consultant with a unique skill set committing to an hourly rate. 2. Quantity-setting: for a quantity , include the transactions with the highest gas prices, up to a limit of on the total gas.343434For an analogy, think of a restriction on oil production set by the Organization of the Petroleum Exporting Countries (OPEC). \tfn@tablefootnoteprintout In our model, these two types of strategies are equivalent—a price-setting strategy at the price has the same effect as a quantity-setting strategy at the quantity . In either case, a creator of a transaction with should be expected to respond by bidding the fixed price (enough for inclusion in the block), and one with to bid something between 0 and (in any case, being excluded from the block).

Because there are no dependencies between first-price auctions in different blocks and no fee burn, a 100% miner maximizes its net revenue by maximizing its revenue from each block separately. For a single block, the revenue earned by a miner using a price-setting strategy with price (or the equivalent quantity-setting strategy) is the price times the quantity willing to pay it:353535For simplicity, we assume in this section that the marginal cost of gas to a miner—the parameter in Sections 5–6—is zero. The conclusions of this section remain the same for a positive marginal cost.

| (17) |

For ease of exposition, in this section we focus on demand curves for which the revenue (17) is a strictly concave function (as is the case with, for example, a linear demand curve).

Because a 100% miner can be thought of as a monopoly on EVM computation, there is an obvious price and quantity to focus on:

Definition 7.1 (Monopoly Price and Quantity)

Consider a maximum block size and a demand curve for which the revenue (17) is a strictly concave function of price. If attains the maximum in (17), then:

-

(a)

the monopoly price is the revenue-maximizing price or the market-clearing price, whichever is larger:363636See Section 3.1 for the definition of a market-clearing price.

(18) -

(b)

the monopoly quantity is the revenue-maximizing quantity or the maximum block size, whichever is smaller:

(19)

Example 7.2 (Monopoly Prices and Quantites)

Suppose the maximum block size is 12.5M gas and the demand curve is (as in Figure 1). The revenue (17) as a function of price is . This function is differentiable and strictly concave, so its unique maximum is the point at which the derivative equals 0. Thus, gwei and gas. This exceeds the maximum block size of 12.5M gas, and hence the monopoly price is the market-clearing price gwei.

If instead the demand curve was , would be gwei and would be 10M gas. In this case, the monopoly price is strictly higher than the market-clearing price (of 50 gwei) and the monopoly quantity is strictly smaller than the maximum block size.

Price-setting at the monopoly price or quantity-setting at the monopoly quantity both have the effect of maximizing revenue (17) subject to the maximum block size. That is, these are precisely the optimal strategies for a 100% miner: • A 100% miner would price-set at the monopoly price or quantity-set at the monopoly quantity. • If the monopoly quantity is the maximum gas size (equivalently, the monopoly price is the market-clearing price), a 100% miner would not deviate from the intended allocation rule of a first-price auction (Example 5.4). \tfn@tablefootnoteprintout We conclude that, with a first-price auction, extreme miner collusion can increase transaction fee revenue if and only if the monopoly quantity is less than the maximum block size; in this case, miners can boost revenues by artificially restricting the supply of EVM computation, thereby forcing the creators of high-value transactions to submit higher bids for their inclusion.

Remark 7.3 (Detecting a Price- or Quantity-Setting Strategy)

Suppose a cartel of miners implemented a quantity-setting strategy (with quantity less than 12.5M gas), or the corresponding price-setting strategy. Would anyone notice? Naively executed, persistent underfull blocks would be a dead giveaway. But if miners include fake transactions to keep all the blocks full, such a strategy could be difficult to conclusively detect.

7.3 EIP-1559 with a 100% Miner

EIP-1559, described in Section 2.3, would have two immediate consequences for the 100% miner thought experiment. First, a miner would strive to simultaneously maximize the transaction fee revenue (as in a first-price auction) and minimize the amount of these fees lost to the fee burn. Second, a miner’s allocation decision in one block would affect the base fee (and hence net revenue earned) in future blocks. Now what’s the miner’s optimal strategy?

First suppose that the monopoly quantity (Definition 7.1) is at most the target block size of 12.5M gas. (Recall that the maximum block size is double this amount under EIP-1559.) In this case, the maximum block size may as well be 12.5M gas—a 100% miner will never use more than this, as doing so would decrease its net revenue both in the current block (for including more gas than the monopoly quantity) and in future blocks (because of the increased base fee, as per (2)). Thus, the best-case scenario for a 100% miner is to match the revenue of a 100% miner under the status quo (Section 7.2) while simultaneously paying no fee burn. A 100% miner can closely approximate this best-case scenario: 1. Drive the base fee to zero (or its minimum amount) from its initial value, for example by publishing a sequence of empty blocks. 2. For all future blocks, proceed as a 100% miner would with first-price auctions, by using the monopoly quantity-setting strategy. \tfn@tablefootnoteprintout Because the monopoly quantity is at most the target block size, the base fee will remain at its minimum value forevermore. Notably, in this case, the outcome of extreme miner collusion is essentially the same under EIP-1559 as under the status quo!