longtable

mlOSP: Towards a Unified Implementation of Regression Monte Carlo Algorithms

Abstract

We introduce mlOSP, a computational template for Machine Learning for Optimal Stopping Problems. The template is implemented in the R statistical environment and publicly available via a GitHub repository. mlOSP presents a unified numerical implementation of Regression Monte Carlo (RMC) approaches to optimal stopping, providing a state-of-the-art, open-source, reproducible and transparent platform. Highlighting its modular nature, we present multiple novel variants of RMC algorithms, especially in terms of constructing simulation designs for training the regressors, as well as in terms of machine learning regression modules. Furthermore, mlOSP nests most of the existing RMC schemes, allowing for a consistent and verifiable benchmarking of extant algorithms. The article contains extensive R code snippets and figures, and serves as a vignette to the underlying software package.

1 Introduction

Numerical resolution of optimal stopping problems has been an active area of research for more than two decades. Originally investigated in the context of American option pricing, it has since metamorphosed into a field unto itself, with wide-ranging applications and dozens of proposed approaches. A major strand that is increasingly dominating the subject is simulation-based methods rooted in the Monte Carlo paradigm. Developed in the late 1990s by Longstaff & Schwartz [25] and Tsitsiklis & van Roy [35] this framework remains without an agreed-upon name; I shall refer to it as Regression Monte Carlo (RMC). The main feature of RMC is its marriage of a probabilistic approach, namely simulation of the underlying stochastic state dynamics, and statistical tools for approximating the quantities of interest: the value and/or continuation functions, and the stopping region. This combination of simulation and statistics brings scalability, flexibility in terms of underlying model assumptions, and a vast arsenal of potential implementations. These benefits have translated into excellent performance which has made RMC popular both in the academic and practitioner quantitative finance communities. Indeed, in the opinion of the author, these developments can claim to be the most successful numerical strategy that emerged from Financial Mathematics. RMC has by now percolated down into standard Masters-level curriculum, and is increasingly utilized in cognate engineering and mathematical sciences domains.

Despite hundreds of journal publications presenting and analyzing variants of RMC (see e.g. the surveys [21, 30] and the monograph by Belomestny and Schoenmakers [7]), there remains a dearth of user-friendly benchmarks or unified overviews of the algorithms. In particular, to my knowledge, there is no R (or other common programming environments, such as Python) package for RMC. Small stand-alone versions exist in [5, 36] but are essentially unknown by the research community; see also [14] that has a broader scope and is primarily written in C++. One reason for this gap is that many research articles tend to explore one narrow aspect of RMC and then illustrate their contributions on a few idiosyncratic examples. As a result, it is difficult to independently evaluate the relative pros and cons or to explore the merit of new ideas.

In the present article, I offer an algorithmic template for RMC, dubbed mlOSP (Machine Learning for Optimal Stopping Problems), coupled with its implementation within the R programming language. This endeavor is meant to be a “living” project, offering a platform to centralize and standardize new RMC approaches as they are proposed. The associated {mlOSP} library [27] was first released in late 2020; by September 2022 it is in its Version 1.2 incarnation, and is expected to have further (hopefully regular) updates.

1.1 Contributions

The mlOSP template detailed below offers a unified description of RMC via the underlying statistical concepts. The aim of mlOSP is a generic RMC template that emphasizes the building blocks, rather than specific approaches. This perspective therefore tries to nest as many of the numerous existing approaches as possible, shedding light on the differences and the similarities between them. To specify mlOSP, I utilize statistical terminology (in contrast to financial or probabilistic lingo). In particular, I place RMC in the context of modern statistical machine learning, highlighting links to Design of Experiments, Stochastic Simulation, and Sequential Learning literatures.

By providing a templated perspective and tying disparate extant concepts, mlOSP allows for numerous new twists, extensions, and variants to “classical” RMC. To this end, in this article and in the respective R code I discuss and showcase the following new RMC flavors:

-

i)

Space-filling training designs (multiple variants in Section 4.1);

-

ii)

Variable simulation design size across time-steps (Section 4.1);

-

iii)

Adaptive simulation designs with varying batch sizes generated sequentially (Section 4.3);

-

iv)

Cross-validated kernel regression emulators (Section 5.1);

-

v)

Relevance Vector Machine emulators (Section 5.1);

-

vi)

Heteroskedastic and local Gaussian Process emulators (Section 5.2).

As a further contribution, I extend mlOSP to the context of multiple-stopping problems, designing its analogue for valuing Swing options (Section 7.1). To my knowledge, this is the first paper that applies concepts of simulation design and advanced statistical emulators to swing option pricing. This generalization hints at further possibilities of building upon mlOSP to develop an interlocking collection of computational tools for decision-making under uncertainty.

This article moreover contributes to the literature by providing a comprehensive benchmarking of different RMC schemes across solver types and problem instances. By providing fully reproducible results, I aim to initiate a common collection of testbeds (in the spirit of say the UCI ML repository http://archive.ics.uci.edu/ml) that allow for a transparent, apples-to-apples comparison and can be easily augmented by other researchers.

1.2 Organization of the article

The eponymous R package {mlOSP} [27] is a central companion to this article. Accordingly, I added many R code snippets throughout, providing a “User Guide” to {mlOSP}. Conversely, the code is used to illustrate and interpret the discussion. Appendices provide further information about the R implementation.

Section 2 presents the mlOSP template, emphasizing the three blocks of the RMC framework: stochastic simulation, training design, and statistical approximation. These pieces are modularized and can be fully mixed-and-matched within the core backward dynamic programming loop. Section 3 provides an illustration of this fundamental concepts in {mlOSP} serving as a short vignette. Sections 4 and 5 explore the two key parts of the template: simulation designs and regression emulators. Section 6 benchmarks some of the implemented schemes, running 10 {mlOSP} solvers on 9 instances of Bermudan options in 1-5 dimensions. The solvers range from piecewise linear regression, to RVM kernel regression, to Gaussian process emulators. It also includes additional experimental results related to scheme stability and fine-tuning various algorithm ingredients. Section 7 discusses extensions: Section 7.1 showcases a generalization to handle multiple-stopping problems and Section 7.2 goes through the steps to define a new OSP instance within the package. Section 8 concludes.

2 The mlOSP template

2.1 Regression Monte Carlo methodology

An optimal stopping problem (OSP) is described through two main ingredients: the state process and the reward function. I shall use to denote the state process, assumed to be a stochastic process indexed by the time and taking values in . The reward function represents the net present value (in dollars) of stopping at time in state , where the notation emphasizes the common possibility of the reward depending on time, e.g. due to discounting. I assume the standard probabilistic structure of , where is adapted to the filtration , and .

We seek the decision rule , a stopping time to maximize expected reward until the horizon :

| (1) |

To this end, we wish to evaluate the value function ,

| (2) |

where is the collection of all -stopping times bigger than and less than or equal to .

The state is typically assumed to satisfy a Stochastic Differential Equation of Îto type,

| (3) |

where is a (multi-dimensional) Brownian motion and the drift and volatility are smooth enough to yield a unique strong solution to (3). While utilized in all presented case studies, the structure of (3) is not essential beyond its Markov property, and other stochastic processes , for example jump-diffusions, can be treated interchangeably. Note that while I use to denote the probability and expectation operators, financially we are working under the risk-neutral “”-measure that is the relevant one for contingent claim valuation.

For the remainder of the section I adopt the discrete-time paradigm, where decisions are made at pre-specified instances , where typically for a given discretization step . Henceforth, I index time steps by and work with .

It is most intuitive to think of optimal stopping as dynamic decision making. At each exercise step , the controller must decide whether to stop (0) or continue (1), which within a Markovian structure is encoded via the action strategy with each . The action map gives rise to the stopping region

where the decision is to stop, and in parallel defines the corresponding first hitting time which is an optimal exercise time after . Hence, solving an OSP is equivalent to classifying each pair into or its complement the continuation set. Recursively, the action set is characterized as

| (4) |

i.e. one should continue if the expected reward-to-go on the left of (4) dominates the immediate payoff on the right. Denoting the step-ahead conditional expectation of the value function by

| (5) |

and using the Dynamic Programming principle, we can equivalently write because we have . The -value is also known as the continuation value.

The above logic yields a recursive algorithm to construct approximate action maps ’s through iterating on either (5) or (4). Thus, the RMC framework generates functional approximations of the continuation values in order to build . This is initialized with and proceeds with the following loop:

For repeat:

-

i)

Learn the -value ;

-

ii)

Set and .

The loop makes it clear that RMC hinges on a sequence of probabilistic function approximation tasks that are recursively defined. Note that the principal step i) of learning the continuation function can be represented in multiple ways:

– of approximating ;

– of approximating ;

– by picking some and approximating

Above, the look-ahead horizon allows to combine both pathwise rewards based on and the approximate value function -steps into the future [13]. These choices are not numerically identical, because due to the approximation error.

As a final step, once all the action sets are computed they induce the expected reward

| (6) |

The gap between and (which is the maximal possible expected reward) is the performance metric for evaluating .

2.2 Workflow

The key step requiring numerical approximation in the above loop is learning the continuation functions . In the RMC paradigm it is handled by re-interpreting conditional expectation as the mean response within a stochastic model. Thus, given an input and fixing , there is a generative model which is not directly known but accessible through a pathwise reward simulator , where is a random variable with mean and finite variance. The aim is then to predict the mean output of this simulator for an arbitrary . This learning task is resolved by running the simulator many times and then utilizing a statistical model to capture the observed input-output relationship. It can be broken further down into three sub-problems:

-

1.

Defining the stochastic simulator;

-

2.

Defining the simulation design;

-

3.

Defining the regression model.

Recasting in the machine learning terminology, for sub-step 1 we need to define a Simulation Device that accepts an input (the state at time ) and returns a random sample , which is a random realization of the pathwise reward starting at such that . We have already discussed multiple versions of such simulators, cf. (4)-(5). In sub-step 2, we then need to decide which collection of ’s should be applied as a training set. After selecting such Simulation Design of some size , , we collect the simulation outputs and reconstruct the model

| (7) |

where the inferred Emulator is the approximate continuation value.

The above 3 sub-steps constitute one iteration of the overall loop; the aggregate RMC is a sequence of tasks, indexed by . With that in mind, the following remarks are helpful to guide the implementation:

-

•

The RMC tasks are recursive, the sub-problem at step is linked to the previous simulators/emulators at steps . Therefore, approximation errors will back-propagate.

-

•

While the tasks are inter-related, since they are solved one-by-one, there is a large scope for modularization, adaptation, etc., to be utilized—the solvers need not be identical across .

-

•

When deciding how to train , there is no “data” per se and the controller is fully in charge of selecting what simulations to run. Judicious choice of how to do so is an important criterion of numerical efficiency.

-

•

In classical machine learning tasks, there is a well-defined loss function that quantifies the quality of the constructed approximation . In OSP, this loss function is highly implicit; ultimately we judge algorithm performance in terms of the quality of the overall in (6).

-

•

The stochasticity in RMC is deeply embedded in all the pathwise simulators and the dependence across time-steps. Understanding the sources of this stochasticity is critical for maximizing performance.

-

•

The “error term” in (7) is simulation noise coming from the -simulator. As a result, its statistical properties tend to be quite complex and non-Gaussian. For example, in the common scenario where the reward has a lower bound of zero , has a mixed distribution with a point mass.

-

•

Like in any statistical model, we may distinguish between a training set used to construct the emulators—the functional approximations ’s, and a subsequent test set used to evaluate the quality of the resulting exercise rule .

2.3 Illustration with a Toy Example

To illustrate the recursive construction of ’s, we proceed with a toy example. We take the point of view of a buyer of a Bermudan Put. The contract has an expiration date , a strike , and exercise frequency (such as daily). The state is interpreted as the share price of the underlying asset at date , with state space and is assumed to follow Geometric Brownian motion with constant coefficients . Taking into account the time-value of money, the reward function at time is

where is the constant risk-free interest rate. With this setup, the stopping set is known as the exercise region. For the Black-Scholes Bermudan Put it is known that , i.e. one should stop as soon as the asset price drops below the exercise thresholds .

We assume that , and there are periods, , and illustrate how the RMC steps i)-ii)-iii) might be implemented at . Because we are at the penultimate step, the simulation device is simply a one-step-ahead sampling of the terminal payoff , i.e.

| (8) |

where is the Brownian shock. Note that : since , the -value at is , which is indeed the expectation of . For the Simulation Design I draw

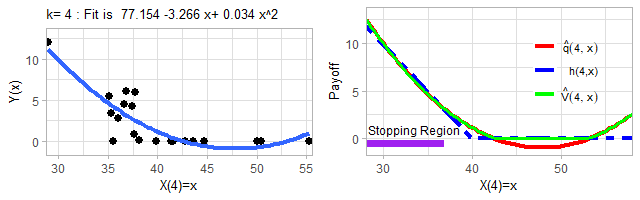

i.i.d., interpreted as the realized values at obtained by simulating paths of starting with the fixed initial share price . Specifically, I take inputs at step (note that the randomness in is superfluous to the algorithm and in particular independent of the ’s in ). The corresponding , are then interpreted as realized future payoffs at if one waits one more period. Because the ’s inside are sampled in an i.i.d. manner, the ’s are independent draws from the conditional payoff distribution given . With a path-based perspective, these payoffs are simply across independent paths of . The left panel of Figure 1 visualizes the resulting scatter plot of these input-output pairs for .

lsModel <- list(dim=1,r=0.05,sigma=0.2,div=0,dt=0.1,T=0.5)

rmc <- list(); paths <- list(); payoff <- list()

x0 <- 40; Np <- 20; Nt <- 5; set.seed(262)

paths[[1]] <- sim.gbm( matrix(rep(x0, Np), nrow=Np,byrow=T), lsModel, lsModel$dt)

for (j in 2:(Nt+1)) # Save paths of X: paths[[j]] = X( j \Delta t)

paths[[j]] <- sim.gbm( paths[[j-1]], lsModel, lsModel$dt)

To infer the continuation value function we apply regression, specifically let me fit a quadratic function of the input to predict the expected value of . In other words I postulate that or

| (9) |

where the regression coefficients parametrize the unknown continuation function we are after, and is assumed to be Gaussian. As is standard, we fit ’s via Ordinary Least Squares, i.e. by minimizing a quadratic penalty function which is the residual sum of squares between observed and predicted values. In R this is achieved by the lm command as follows:

payoff[[4]] <- exp(-0.05*0.5)*pmax(40-paths[[5]],0) # outputs Y(x). Input is paths[[4]]

rmc[[4]] <- lm(y ~ poly(x,2,raw=TRUE), data.frame(y= payoff[[4]], x = paths[[4]]))

Remark: It is instructive to compare the assumed (9) with the exact simulation device in (8). One of the core concepts of RMC is to abstract away from the “innards” of (8) and substitute with a statistical treatment as in (9).

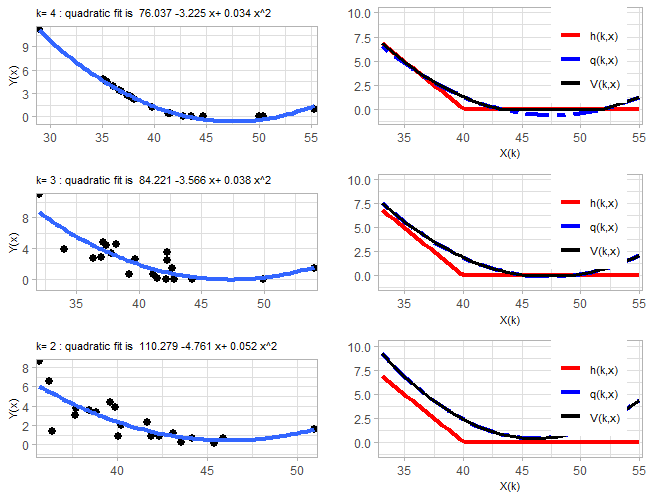

The blue line in the right panel of Figure 1 is our resulting estimate of expected payoff at the terminal time step given . Arithmetically, we have

So for example and = 4.674. Proceeding with step ii) of the RMC loop, we may conclude that (continue at ) and (stop at , since ). Clearly is an approximation: the conditional expectation is not actually quadratic, but since we do not know what it is, we simply model it via that fitted quadratic function.

Note that the output of the regression is not any particular prediction, but the object , so that the corresponding decision rule is implicit. In fact, RMC never requires explicitly characterizing ; all we need is to be able to evaluate at any inputted . In Figure 1 I solve for the stopping boundary by searching at which threshold stopping becomes more profitable than continuing and shading the resulting stopping region . Obtaining the exercise threshold is purely “cosmetic” and plays no role in the solver.

The above completes one step of the RMC recursion, defining and (implicitly) . We can then continue by repeating the above logic over and using (5), i.e. simulating the one-step-ahead value function to obtain ’s. Figure 7 in Appendix B illustrates this sequential estimation of ’s, utilizing training inputs sampled from a log-normal distribution at each , and then constructing quadratic fits.

The above choices of the simulation design (and its size) and regression model are arbitrary and for motivation only. In the next section, they are generalized and scaled up into a generic template that is the main object of study for the remainder of the paper.

2.4 Dynamic Emulation Template

Before presenting the template in Algorithm 1 below, several conceptual adjustments are necessary. First, in order to abstract from the payoff function specifics, mlOSP operates with the timing value,

Exercising is optimal when the timing value is negative ; the stopping boundary is the zero contour of . So instead of learning , mlOSP learns , solely a numerical rather than conceptual change. Given one can recover the value function (and hence the option price) via .

Second, the abstract specification of the timing value emulator is as the empirical minimizer in some function space of the mean squared error from the observations,

| (10) |

For instance, in the linear model as above, are the linear combinations of the basis functions and (10) is a finite-dimensional optimization problem in terms of the respective coefficients , with . Note that is a statistical model; it is viewed as an object (rather than say a vector of numbers) and passed as a “function pointer” to the pathwise reward simulator in subsequent steps. The latter simulator in turn applies a predict method, asking to furnish a predicted timing value at arbitrary .

Remark: In {mlOSP} implementation, the emulator is employed only when the decision is non-trivial, i.e. in the in-the-money region . This insight dates back to Longstaff and Schwartz [25] who noted that learning is only necessary when ; otherwise it is clear that and hence we may set . Thus, the simulation design is restricted to be in .

Finally, I index everything by the time steps , with corresponding by default, and the following notation:

-

•

: number of training inputs at step (can again vary across );

-

•

: simulation design, i.e. the collection of training inputs at step ;

-

•

: functional approximation space where is searched within;

-

•

pathwise samples of timing value used as the responses in the regression model.

Equipped with above, Algorithm 1 presents the mlOSP template, emphasizing the “moving parts” of the simulation designs and fitting . These two building blocks are explored in Sections 3 and 4 below.

The last piece of Algorithm 1 that remains to be clarified concerns the simulation device and the respective lookahead parameter that determines how long are the forward trajectories. The two most common approaches are TvR (for Tsitsiklis-van Roy [35]) and LS (for Longstaff-Schwartz [25]). In the TvR variant and the simulator generates one-step-ahead paths, resulting in the regression of against . In the LS variant, , and one regresses the pathwise timing values against .

2.4.1 Expected Payoff

The output of Algorithm 1 is the approximate decision rules . These are functions, taking as input the system state and returning the action to take (stop or continue). Additional computation is needed to evaluate the corresponding expected payoff of the stopping rule in (6). To do so, one again employs Monte Carlo simulation, approximating with a sample average on a set of fresh forward test scenarios , ,

| (11) |

where is the pathwise stopping time. Eqn. (11) also yields a confidence interval for the expected payoff by using the empirical standard deviation of ’s. Because is based on out-of-sample test scenarios, it is an unbiased estimator of and hence for large enough test sets it will yield a lower bound on the true optimal expected reward, . The interpretation is that the simulation design defines a training set, while forms the test set. The latter is not only important to obtain unbiased estimates of expected reward from the rule , but also to enable an apples-to-apples comparison between multiple solvers which should be run on a fixed test set of -paths.

2.4.2 Longstaff-Schwartz Scheme

In the LS variant of [25], the training sets are constructed from a single global simulation of the -process, so that and the forward paths that yield ’s are re-used across time-steps. This requires storing all those paths in memory, but reduces the need to keep generating new shocks ’s underlying . Moreover, it provides access to an in-sample estimator which is the average payoff on the training paths. As is well known, suffers from look-ahead bias and therefore cannot be reliably compared to the true option price. Heuristically, it has been observed that the in-sample estimator that is available in the global-path design approach tends to give upper bounds, and hence can be used to roughly “sandwich” the final estimate of the option price between the lower bound of the test set and the upper bound of the training set, “”.

Remark: our RMC formulation returns the action map globally, or at least anywhere within the neighborhood of the training sets . As such, during forward simulation one may evaluate the expected payoff with arbitrary initial condition . Since the LS scheme is based on starting all training paths from a fixed (i.e. a degenerate ) it is sensitive to testing with a different initial condition.

2.4.3 What is Random?

The core of RMC is its probabilistic (hence Monte Carlo) nature. Indeed, Algorithm 1 is random and re-running it would yield a different set of functional approximations at each , and ultimately a different . Why does this happen exactly?

In the mlOSP template, the immediate place where random samples are generated is during the forward simulation of trajectories (step 3 of Algorithm 1) . In other words, the “y”s in the regression indeed have a random component to them. Secondly, in the LS variant the simulation design is random, i.e. the “x”s in (step 2) are random. Namely, the training set is based on simulated trajectories which vary across algorithm runs. Third, many machine learning emulators involve nonlinear optimization during the fitting step 6, and the low-level optimizers frequently invoke randomization. For example, neural network and Gaussian process emulators rely on stochastic gradient descent and/or genetic optimization and thus return not the true global minimizer but a randomly found local minimum in . Fourth, the test collection of paths is random.

To sum up, is a random variable, and so are all the intermediate solution outputs, such as or . Indeed, due to the coupling between and , as soon as has some probabilistic aspect to it, so will all preceding-in-time emulators. Similarly, the budget of the solver in terms of its running time and number of uniform variates generated is also non-constant across runs. With so many random pieces, scheme stability is important. The standard way to measure stability is through sampling variance, i.e. the variance of across independent algorithm runs, holding the test set fixed. More efficient RMC versions would be expected to yield lower sampling variance, exhibiting less dependence on the particular training set. Statistically, this dependence is primarily driven by the sensitivity of the regression emulator to the realizations in , and thus it is preferable to “regularize” the regression architecture to avoid sensitivity to outliers, or other statistical mis-specifications, cf. Section 5.

3 Getting Started with {mlOSP}

The {mlOSP} package [27] implements multiple versions of Algorithm 1. The following user guide highlights its key aspects. I have strived to make it fully reproducible, with the full underlying R code available on GitHub. Since the schemes are intrinsically based on generating random outputs from the underlying stochastic simulator, I fix the random number generator (RNG) seeds. Depending on the particular machine and R version, these seeds might nevertheless lead to different results.

The workflow pipeline in {mlOSP} consists of:

-

(i)

Defining the model, which is a list of (a) parameters that determine the dynamics of in (3); (b) the payoff function ; and (c) the tuning parameters determining the regression emulator specification.

-

(ii)

Calling the appropriate top-level solver. The solvers are indexed by the underlying type of simulation design. They also use a top-level method argument that selects from a collection of implemented regression modules. Otherwise, all other parameters are passed through the above model argument. The solver returns a collection of fitted emulators—an R list containing the respective regression object of for each time step , plus a few diagnostics;

-

(iii)

Evaluating the obtained fitted emulators through an out-of-sample forward simulator via forward.sim.policy that evaluates (6). The latter is a top-level function that can work with any of the implemented regression objects. Alternatively, one may also visualize the emulators through a few provided plotting functions.

The aim of the above architecture is to maximize modularity and to simplify construction of user-defined OSP instances, such as additional system dynamics or bespoke payoffs. The latter piece is illustrated in Section 7.2.

The following example illustrates this workflow. We consider a 1-D Bermudan Put with payoff where the underlying dynamics are given by Geometric Brownian Motion (GBM)

with scalar parameters . Thus, can be simulated exactly by sampling from the respective log-normal distribution. In the model specification below we have and the Put strike is . Exercising the option is possible times before expiration, i.e., . To implement the above OSP instance just requires defining a named list with the respective parameters (plus a few more for the regression model specified below):

put1d.model <- c(K=40, payoff.func=put.payoff, # payoff function

x0=40,sigma=0.2,r=0.06,div=0,T=1,dt=0.04,dim=1, sim.func=sim.gbm,

km.cov=4,km.var=1,kernel.family="matern5_2", # GP emulator params

pilot.nsims=0,batch.nrep=200,N=25)

As a representative solver, I utilize osp.fixed.design that asks the user to specify the simulation design directly. To select a particular regression approach, osp.fixed.design has a method field which can take a large range of regression methods. Specifics of each regression are controlled through additional model fields. As example, the code snippet below employs the {DiceKriging} Gaussian Process (GP) emulator with fixed hyperparameters and a constant prior mean, selected through method="km". The kernel family is Matérn-5/2, with hyperparameters specified via km.cov, km.var above. For the simulation design (input.domain field) I take with 200 replications (batch.nrep) per site, yielding , see Section 4.1. The replications are treated using the SK method [2], pre-averaging the replicated outputs before training the GP.

train.grid.1d <- seq(16, 40, len=25) # simulation design

km.fit <- osp.fixed.design(put1d.model,input.domain=train.grid.1d, method="km")

Note that no output is printed: the produced object km.fit contains an array of 24 (one for each time step, except at maturity) fitted GP models, but does not yet contain the estimate of the option price . Indeed, we have not defined any test set, and consequently are momentarily postponing the computation of .

3.1 Comparing solvers

{mlOSP} has several solvers and allows straightforward swapping of the different pieces of the template. Below, for example, I consider the LS scheme, implemented in the osp.prob.design solver, where the simulation design is based on forward -paths. I moreover replace the regression module with a smoothing cubic spline (smooth.spline; see [20] for a discussion of using splines for RMC). The latter requires specifying the number of knots model$nk. Only 2 lines of code are necessary to make all these modifications and obtain an alternative solution of the same OSP:

put1d.model$nk=20 # number of knots for the smoothing spline

spl.fit <- osp.prob.design(N=30000,put1d.model,method="spline") # 30000 training paths

Again, there is no visible output; spl.fit now contains a list of 24 fitted spline objects that are each parametrized by 20 (number of chosen knots) cubic spline coefficients.

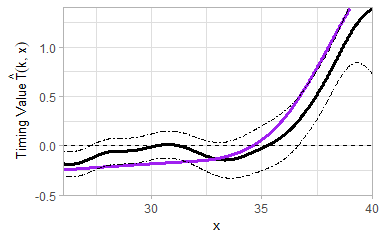

Figure 2 visualizes the fitted timing value from one time step. To do so, I predict based on a fitted emulator (at ) over a collection of test locations. In the Figure, this is done for both of the above solvers (GP-km and Spline), moreover we also display the 95% credible intervals of the GP emulator for . Keep in mind that the exact shape of is irrelevant in mlOSP, all that matters is the implied which is the zero level set of the timing value, i.e. determined by the sign of . Therefore, the two regression methods yield quite similar exercise rules, although they do differ (e.g. at the spline-based rule is to continue, while the GP-based one is to stop and exercise the Put). Since asymptotically both solvers should recover the optimal rule, their difference can be attributed to training errors. As such, uncertainty quantification of is a useful diagnostic to assess the perceived accuracy of . In Figure 2 the displayed uncertainty band shows that the GP emulator has low confidence about the right action to take for nearly all , since zero is inside the 95% credible band and therefore the positivity of in that region is not statistically significant.

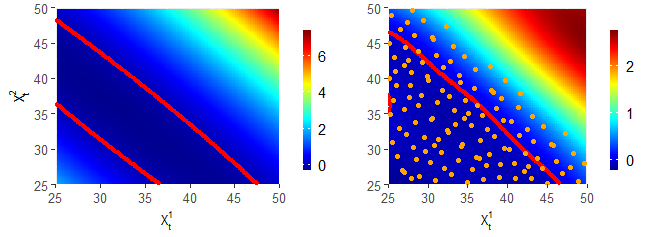

{mlOSP} is designed to be dimension-agnostic, so that building a multi-dimensional model follows the exact same steps. For example, the two-line snippet below defines a 2D model with Geometric Brownian motion dynamics for the two assets and a basket average Put payoff The two assets are assumed to be uncorrelated with identical dynamics. I continue to use a strike of and at-the-money (ATM) initial condition .

model2d <- list(K=40,x0=rep(40,2),sigma=rep(0.2,2),r=0.06,div=0,

T=1,dt=0.04,dim=2,sim.func=sim.gbm, payoff.func=put.payoff)

With the model defined, we can use the same solvers as above, with exactly the same syntax. To illustrate a different regression module, let us employ a linear model, method="lm". To do so, we need to first define the basis functions that are passed to the model$bases parameter. Below I select polynomial bases of degree , ; by default the R lm model also includes the constant term, so there are a total of 6 regression coefficients .

bas22 <- function(x) return(cbind(x[,1],x[,1]^2,x[,2],x[,2]^2,x[,1]*x[,2]))

model2d$bases <- bas22

prob.lm <- osp.prob.design(15000,model2d, method="lm") # Train with 15,000 paths

For comparison, I re-solve with a GP emulator that has a space-filling training design of sites replicated with batches of each for a total of simulations again.

model2d$N <- 150 # N_unique

model2d$kernel.family <- "gauss" # squared-exponential kernel

model2d$batch.nrep <- 100

model2d$pilot.nsims <- 0

sob150 <- sobol(276, d=2) # Sobol space-filling sequence

# triangular approximation domain for the simulation design

sob150 <- sob150[ which( sob150[,1] + sob150[,2] <= 1) ,]

sob150 <- 25+30*sob150 # Lower-left triangle in [25,55]x[25,55], see Fig

sob.km <- osp.fixed.design(model2d,input.domain=sob150, method="trainkm")

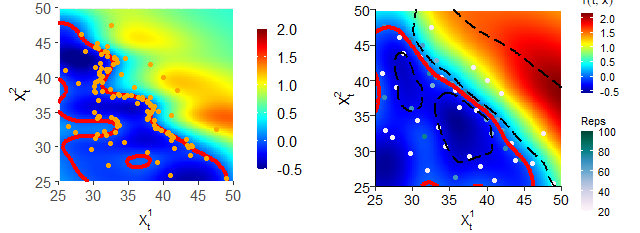

Figure 3 visualizes the estimated stopping boundary from the above 2 solvers using the plt.2d.surf function from the package. It shows an image plot of the emulator at a single time-step . Recall that the stopping region is the level set where the timing value is negative, indicated with the red contours that delineate the exercise boundary. In the left panel, the exercise boundary is a parabola because is modeled as a quadratic. On the right panel, the exercise boundary has a much more complex shape since that has many more degrees of freedom. For the latter case, Figure 3 also displays the underlying training design of sites.

Appendix C lists all the simulation, payoff and solver functions available in {mlOSP}.

3.2 Out-of-sample Tests

By default, the solvers only create the functional representations of the timing/value function and do not return any explicit estimates of the option price or stopping rule. This reflects the strict separation between training and testing, as well as the fact that RMC builds a global estimate of and hence can be used to obtain a range of option prices (e.g. by changing ).

The following code snippet builds an out-of-sample database of -paths. This is done iteratively by employing the underlying simulator, already saved under the model2d$sim.func field. The latter is interpreted as the function to generate a vector of ’s conditional on . By applying payoff.func to the final vector (which stores values of ) we can get an estimate of the respective European option price . By calling forward.sim.policy with a previously saved {mlOSP} object we then obtain a collection of that can be averaged to obtain a as in (11).

nSims.2d <- 40000 # use N'=40,000 fresh trajectories

nSteps.2d <- 25

set.seed(102)

test.2d <- list() # store a database of forward trajectories

test.2d[[1]] <- model2d$sim.func( matrix(rep(model2d$x0, nSims.2d),nrow=nSims.2d,byrow=T),

model2d, model2d$dt)

for (i in 2:(nSteps.2d+1)) # generate forward trajectories

test.2d [[i]] <- model2d$sim.func( test.2d [[i-1]], model2d, model2d$dt)

oos.lm <- forward.sim.policy( test.2d, nSteps.2d, prob.lm$fit, model2d) # prob.lm payoff

oos.km <- forward.sim.policy( test.2d, nSteps.2d, sob.km$fit, model2d) # sob.km payoff

cat( paste('Price estimates', round(mean(oos.lm$payoff),3), round(mean(oos.km$payoff),3)))

## Price estimates 1.446 1.44

# check: estimated European option value

cat(mean( exp(-model2d$r*model2d$T)*model2d$payoff.func(test.2d[[nSteps.2d]], model2d)))

## 1.214149

Since we evaluated both estimators on the same set of test paths, we can conclude that the LM-Poly emulator leads to a better approximation 1.446 1.44 than the GP-km one. The reported European Put estimate of 1.214 can be used as a control variate to adjust since it is based on the same test paths and so we expect that .

The osp.prob.design LS solver can evaluate in parallel the in-sample estimator and the out-of-sample by splitting the total simulation budget between training and testing paths. This is controlled by the subset parameter. For example, I re-run the linear model from above but now using 15,000 training inputs and 15,000 test paths:

ls.lm <- osp.prob.design(30000,model2d,method="lm",subset=1:15000)

## [1] "In-sample price estimate 1.462; and out-of-sample: 1.446"

The returned price estimates are consistent with the previous discussion that (in-sample) is biased high and (out-of-sample) is biased low compared to the true .

4 Training Designs

The simulation designs determine the training domains of the regression emulators. While the size of the training set obviously plays a major role in how accurate the approximation will end up, the geometry of also has a significant impact. To represent the design geometry I consider the respective training density , with ’s viewed as samples from that target density

| (12) |

In a randomized simulation design, this is precisely how samples are generated. For instance, the LS scheme [25] constructs ’s by sampling from the conditional density of ; thus in the case where the dynamics are GBM, is log-normal and concentrates on regions reachable by starting from . Uniform target densities, for a given bounded input domain , are common because they correspond to space-filling simulation designs. The latter capture the intuition of learning through exploration, i.e. sampling a diverse set of ’s in order to observe the corresponding ’s. However, note that a Uniform requires the user to specify the supporting bounding region , something not needed when is log-normal.

Alternatively, one can generate deterministic representations of . For example, one can replace sampling from a uniform with placing ’s on a lattice (i.e. a grid which is a discrete-uniform target density). Yet another way is to mimic a Uniform by using a Quasi Monte Carlo (QMC) sequence.

Replication. Conventionally, a training design of size consists of unique sites . In contrast, in a replicated design, all (some) sites appear multiple times. In a most common batched design, we have distinct sites, the so-called macro-design, and each unique is then repeated times, so that

| (13) |

where the superscripts now index unique inputs and the total simulation budget is . The corresponding simulator outputs are denoted as .

A replicated design allows to pre-average the corresponding -values, , and then to call the regression module on the reduced dataset . This is especially relevant for non-parametric regressions, where such pre-averaging greatly cuts down on the regression overhead. For example, kernel-type regressions have cubic runtime complexity and orders-of-magnitude savings are achieved by training them on only samples rather than . Thus, replication is a must to be able to tractably implement kernel regression in a moderately-high dimensional problem where thousands of samples are needed . Since pre-averaging involves loss of information, an additional approximation error would be incurred.

Aspects of the simulation design that can be varied include randomized or deterministic; replicated or not; sequential or one-shot. For example, the classical LS scheme has a randomized, adaptive, non-replicated design. In the subsections below I describe the various design options that can be specified within the mlOSP template. In {mlOSP} these choices are controlled through the selection of the top-level solvers, as well as model parameters. Most of these ideas are new for RMC training and to my knowledge have not appeared elsewhere except for a tangential mention in Ludkovski [26]. In aggregate they offer a lot of latitude for finetuning RMC.

4.1 Space Filling Designs

A space-filling design aims to “uniformly” cover the domain of approximation . Space-filling simulation designs are implemented within the osp.fixed.design solver and primarily controlled through the input.domain parameter which determines the domain of approximation . Below I illustrate how these are used on the 2D Basket Put case study.

-

(i)

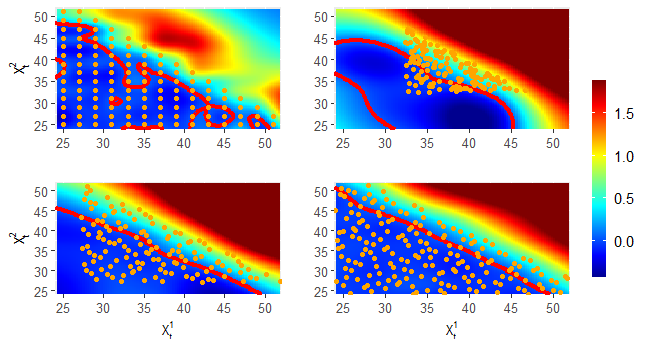

One may directly specify a simulation design to be used as-is. For example, can be chosen to be a space-filling lattice. The next code snippet generates a fixed training lattice over a triangular (namely the lower-left triangle since we only train in-the-money). Based on model parameters a good domain of approximation is , cf. Figure 4 top-left. I batch each of the resulting inputs with replications/site for a total simulation budget of . For the regression module I utilize a GP-km Matérn-5/2 emulator.

lattice136 <- as.matrix(expand.grid( seq(25,55,len=16), seq(25,55,len=16)))

lattice136 <- lattice136[ which( lattice136[,1] + lattice136[,2] <= 80) ,]

model2d$batch.nrep <- 100

put2d.lattice <- osp.fixed.design(model2d,input.dom=lattice136, method="km")

-

(ii)

A bit more generally, one can specify a hyper-rectangular and then space-fill by employing QMC sequences to place . The {randtoolbox} package provides several space-filling methods, such as Sobol sequences, Halton sequences, etc. In {mlOSP} this is achieved by providing the ranges for each coordinate (activated if length(input.domain)==2*model$dim) and specifying model$qmc.method. The implementation then automatically clips to the in-the-money region.

The first two approaches above select the same across the time-steps. We next consider time-varying domains of interest. Since the variance of grows in , the training region should also be larger for later steps.

-

(iii)

To adaptively construct an expanding , {mlOSP} offers an automated space-filling procedure based on pilot simulations. The pilot simulations are forward trajectories from the given initial condition ( set via pilot.nsims). An adaptive hyper-rectangular is then obtained in terms of the coordinate-wise quantiles of , with the latter acting as “scaffolding” to determine an appropriate size of the bounding box. Given , it can be space-filled as before. The motivation for the pilot trajectories is to absolve the end-user from having to directly specify the range of .

To illustrate, I use Latin Hypercube Sampling (LHS, a randomized space filling method, as implemented in the {tgp} package, selected by qmc.method=NULL) to space-fill a rectangle between the 4th and 96th percentiles (selected via input.domain=0.04) of the pilot.nsim=1000 pilot trajectories at each time step. The resulting organically expands in , cf. Figure 4 top-right.

model2d$pilot.nsims <- 1000

model2d$qmc.method <- NULL # Use LHS to space-fill

model2d$N <- 400 # number of inputs to propose. Only in-the-money ones are kept

put2d.lhsAdaptive<- osp.fixed.design(model2d,input.dom=0.04, method="trainkm")

In this setting, is randomized and since we only keep in-the-money inputs, the resulting is non-constant. For example, in the above run I obtain 142 at , 139 and 146.

Remark: A non-uniform space-filling approach is proposed in [15] and consists in using QMC sampling to draw the ’s in the log-normal representation of . This keeps a log-normal target training density but simultaneously space-fills the (unbounded) region of interest.

In option (iii) above, is generated separately for each . As such, one can straightforwardly also vary the design size . One reason why variable is useful is to reflect the growing volume of based on the pilot trajectories. Indeed, learning over a larger domain necessarily requires more simulation effort. Moreover, backpropagation of approximation errors implies that the algorithm is more sensitive to errors in the middle/end time-steps than in the early ones. While conventional RMC schemes use a constant , this restriction is superfluous for constructing a training set .

In {mlOSP} this feature is achieved by making the model$N parameter a vector. Further note that all the space-filling methods can handle arbitrary $N_k$ in contrast to naive lattice designs that force to be a product of marginal lattice lengths.

In the code snippet below I use the full range of the pilot scenarios to select (achieved by setting input.domain=-1) together with space-filling based on the Halton QMC sequence and a varying model$N. Note that the latter is not equal to since the algorithm internally drops all out-of-the-money inputs.

model2d$qmc.method <- randtoolbox::halton

model2d$N <- c(rep(300,8), rep(500,8), rep(800,8)) # design size across time-steps

put2d.haltonRange <- osp.fixed.design(model2d,input.dom=-1, method="km")

-

(iv)

For completeness, I mention briefly one further option supported by {mlOSP}. If input.domain is omitted entirely, osp.fixed.design creates a path-based directly from the pilot paths. This choice still embeds the replication aspect via batch.nrep, but otherwise is equivalent to osp.prob.design. Thus, input.domain=NULL generates a probabilistic, replicated design.

Figure 4 compares training designs at from option (i) with Lattice space-filling ( 120); option (iii) with LHS space-filling ( 146), and time-varying using Halton-sequence space-filling. For the latter, I visualize both at with 132 and (), where 206, but the training region is much larger too.

I end this section by comparing the above three solvers head-to-head in order to assess how the training domain affects the ultimate option price :

oos.1 <- forward.sim.policy(test.2d, nSteps.2d, put2d.lattice$fit, model2d)

oos.2 <- forward.sim.policy(test.2d, nSteps.2d, put2d.lhsAdaptive$fit, model2d)

oos.3 <- forward.sim.policy(test.2d, nSteps.2d, put2d.haltonRange$fit, model2d)

print( round(c(mean(oos.1$payoff), mean(oos.2$payoff), mean(oos.3$payoff)), 3) )

## [1] 1.432 1.448 1.445

The main take-away is that there is not much impact from the specifics of the space-filling, but the range and density of plays a significant role. Above, the hard-coded lattice design does noticeably worse, because its fixed domain of approximation and number of inputs are not adjusting to the time-dependent region of interest of the optimal stopping problem. Thus, I strongly advocate adaptive construction of .

4.2 Sequential Designs

The quality of the training design is linked to how well it supports the learning of . As discussed in [26], it is most efficient to select inputs around the exercise boundary, i.e. the region where the correct decision rule is most unclear. Of course, the exercise boundary is unknown a priori, motivating a sequential construction of , gradually adding training samples indexed by . The goal of such adaptive is to improve simulation efficiency through targeted placement of ’s to maximize the learning of the timing value. Such active learning methods are common in machine learning applications.

The osp.seq.design solver implements active learning of the exercise region through greedily optimizing an acquisition function that is a proxy for the information gain for the respective input location . The selection of is done one-by-one by maximizing . Currently, five different acquisition functions are implemented, specified via the ei.func parameter: “smcu”, “tmse”, “sur”, “csur”, “amcu”, cf. [8] and [26]. Because all these acquisition function rely on the posterior uncertainty of , they require working with a GP-type emulator, namely method being one of “km”, “trainkm”, “hetgp” or “homtp”.

The left panel of Figure 5 illustrates a sequential design constructed using the straddle Maximum Contour Uncertainty sMCU acquisition heuristic. The resulting design at time step (i.e. ) has a total of unique training sites. Compared to the space-filling designs in Figure 4, osp.seq.design yields a highly non-uniform placement of ’s, placing them around the stopping boundary. The different heuristics above vary in how aggressively they do this, known as the exploitation-exploration trade-off. This adaptive behavior improves upon the space-filling designs that will often have many simulation sites far from the stopping boundary (e.g. deep in-the-money) and which are therefore not informative about the optimal stopping rule. See Ludkovski [26] for a detailed analysis of sequential designs in RMC, including the trade-off between number of unique inputs and replication count (keeping fixed).

To set up the osp.seq.design solver, several additional ingredients must be specified. First, I initialize the experimental design of a given size and provide the respective locations (taken from a space-filling QMC sequence). Second, the number of sequential rounds is specified via seq.design.size parameter which determines the final number of unique inputs. Thus, a total of seq.design.size-init.size rounds are run, during each of which is maximized to pick the next unique input. To collect more samples, osp.seq.design relies on replication, i.e. a simulation design of the form (13). Third, I specify the details of the acquisition heuristic. In the example below I start with space-filling design sites (init.size=30), and add an additional 90 with replications each, for a total . The sMCU acquisition function has another parameter ucb.gamma which is on the order of 1. Larger ucb.gamma emphasizes expoitation over exploration.

model2d$init.size <- 30 # initial design size

sob30 <- randtoolbox::sobol(55, d=2) # build a Sobol space-filling design to initialize

sob30 <- sob30[ which( sob30[,1] + sob30[,2] <= 1) ,]

sob30 <- 25+30*sob30

model2d$init.grid <- sob30

model2d$batch.nrep <- 25 # N_rep

model2d$seq.design.size <- 120 # final design size -- a total of 3000 simulations

model2d$ei.func <- "smcu" # straddle maximum contour uncertainty

model2d$ucb.gamma <- 1 # sMCU parameter

model2d$kernel.family <- "Matern5_2"

model2d$update.freq <- 5 # frequency of re-fitting GP hyperparameters

put2d.mcu.gp <- osp.seq.design(model2d, method="hetgp")

oos.mcu.gp <- forward.sim.policy( test.2d, nSteps.2d, put2d.mcu.gp$fit, model2d)

The primary take-away is that osp.seq.design is highly efficient in terms of keeping low, but is rather slow due to shifting the work from running simulations to updating the emulator. Indeed, since each round has nontrivial overhead in optimizing oer , I do not recommend that users run it with more than 150 or so sequential rounds. The gains from sequential design would be higher in models where simulation is expensive (e.g. where very small simulation steps are needed to generate ).

4.3 Deep Dive: Adaptive Batching

Conceptually, active learning is intended to favor locations close to the exercise boundary where the correct decision rule is hardest to resolve. As a result, sequential designs will increasingly concentrate, i.e. the added ’s cluster as grows, see Figure 5 left. Adaptive batching takes advantage of this by gradually increasing the replication level, in effect replacing clusters of ’s with a single replicated input. This allows to reduce the number of unique inputs and speeds up the construction of the sequential design. In an adaptively batched design, the constant in (13) is replaced with input-dependent replication counts :

| (14) |

where the algorithm now specifies both the unique inputs and the respective . This idea was explored in detail in Lyu and Ludkovski [29] that proposed several strategies to construct sequentially and is implemented in the osp.seq.batch.design function. The latter works with a GP-based emulator and includes a choice of several batching heuristics that control how is obtained: fb (Fixed Batching); mlb: Multi-Level Batching; rb: Ratchet Batching; absur: Adaptively Batched SUR; adsa: Adaptive Batching Design with Stepwise Allocation; ddsa: Deterministic Batching Design with Stepwise Allocation.

To implement adaptive batching one needs to specify the batch heuristic via batch.heuristic and the sequential design acquisition function as in Section 4.2 via ei.func. Below I apply the Adaptive Design with Sequential Allocation (ADSA) scheme. ADSA relies on the AMCU acquisition function and at each batching round either adds a new training input or allocates additional simulations to existing . Below I employ ADSA with a heteroskedastic GP emulator (method set to hetgp). The other settings match the osp.seq.design solver from the previous section to allow for the best comparison.

model2d$total.budget <- 3000 # total simulation budget N

set.seed(110)

model2d$batch.heuristic <- 'adsa' # ADSA with AMCU acquisition function

model2d$ei.func <- 'amcu'

model2d$cand.len <- 1000

put2d.adsa <- osp.seq.batch.design(model2d, method="hetgp")

At ADSA yields with 65 unique inputs and with replication counts ranging up to , see right panel of Figure 5. Note that the geometry of is very similar to that in Figure 5 left, but is noticeably lower. Thus, adaptive batching allows to reduce the number of sequential design rounds and the associated computational overhead, running multiple times faster than a comparable osp.seq.design solver. The respective contract prices are 1.4453 for sMCU and 1.4478 for ADSA which are both excellent, however the running times of 7.46 and 1.7 minutes respectively, show that the ADSA-based solver is more than 4 times faster. osp.seq.batch.design yields the most (so far) time-efficient GP-based solver in dimensions higher than .

5 Regression Emulators

The selection of the regression module is the most well known aspect of RMC. Over the past two decades, numerous proposals have been put forth beyond the original idea of ordinary least squares regression with user-specified basis functions. Indeed, there are literally hundreds of potential tools to fit a or equivalently , coming from the worlds of statistical and/or machine learning. With {mlOSP} I take advantage of the standardized R regression API to implement more than a dozen such emulators. At its core, a regression module is based on the generic fit and predict methods and is otherwise fully interchangeable in terms of learning . This means that it is possible to, say, substitute a neural network emulator with a random forest one, keeping all other aspects of the scheme exactly the same, and only changing a couple lines of code. In {mlOSP} this is enabled through the method field of the respective solver. The implementation allows for a straightforward swapping of regression methods, facilitating comparison and experimentation.

Before presenting new ideas for emulating , below is a summary of the best-known extant proposals and their corresponding {mlOSP} implementation if available:

-

•

Piecewise regression with adaptive sub-grids by Bouchard and Warin [9, osp.probDesign.piecewisebw solver, see below];

-

•

Regularized regression, such as LASSO, by Kohler and Krzyżak [22];

-

•

Kernel regression by Belomestny [6]. method=rvm implements relevance vector machine regression, with the radial basis function kernel as one option.

- •

-

•

Neural nets by Kohler et al. [23]. method=nnet implements a single-layer neural network with a linear activation function.

-

•

Dynamic trees by Gramacy and Ludkovski [18]. method=dynatree implements dynamic trees using {dynaTree} package, representing via a piecewise regression with adaptively generated spatial partitions. The hierarchical partitioning is similar to random forest, but utilizes a different Bayesian-inspired mechanism.

Appendix C.2 lists all the available choices, including further tools like Multivariate Adaptive Regression Splines, Local Linear Regression (LOESS), and smoothing splines.

5.1 A potpourri of {mlOSP} regressions

As a way to showcase new variants of RMC emulators, I illustrate them on a fixed multidimensional OSP, ending with an apples-to-apples horse race of their performance. To this end, consider a 3D OSP instance of a max-Call option

where the underlying assets follow i.i.d. GBMs. Following [1, (MS’04), Table 2 p. 1230] I take with , i.e. exercise dates. I further take an OTM initial condition with strike . The true price of this max-Call is about under continuous exercise optionality.

modelBrGl3d <- list(K=100, r=0.05, div=0.1, sigma=rep(0.2,3),T=3, dt=1/3,

x0=rep(90,3),dim=3, sim.func=sim.gbm,payoff.func=maxi.call.payoff)

To allow comparisons between solvers, I generate a shared test set of 20,000 out-of-sample trajectories and report the resulting mean payoff on that same, fixed test.3d.

I start with the random forest (RF) regression emulator. Tompaidis and Yang [34] investigated the use of regression trees for RMC, but I could not find a prior reference for RF’s. RF regression generates a piecewise constant fit obtained as an ensemble estimator from a collection of hierarchical partition trees. Even though the fit is discontinuous, RF’s are known to be among the most robust (in terms of scalability, resistance to non-Gaussianity, etc.) emulators and perform excellently in many statistical learning contexts. To specify a RF emulator requires inputting the number of trees (rf.ntree) and the maximum size of each tree terminal node (rf.maxnode) that are passed to the {randomForest} package. The rest is all taken care of by {mlOSP} and the previously defined model. RF is not very fast, but can be scaled to inputs and is agnostic (in terms of coding effort) to problem dimension . Below I use training paths.

modelBrGl3d$rf.ntree = 200 # random forest parameters

modelBrGl3d$rf.maxnode=200

call3d.rf <- osp.prob.design(100000,modelBrGl3d,method="randomforest")

Another general-purpose emulator is neural networks (NN). The {nnet} package builds a neural network for with a single hidden layer specified via the number of neurons nn.nodes (40 below) and the linear activation function. It provides a streamlined interface that is agnostic to . More advanced versions, such as those in {keras} tend to require much more fine-tuning.

modelBrGl3d$nn.nodes <- 40

call3d.nnet <- osp.prob.design(N=100000,modelBrGl3d, method="nnet")

Both RF and NN provide non-parametric fits which are attractive in the sense of universal approximation—zero asymptotic regression error as data and model complexity go to infinity. The oldest and best-understood non-parametric emulators are furnished by kernel regression. {mlOSP} provides a couple of different variants. First, I propose to use Relevance Vector Machine (RVM) emulators from the package {kernlab}. The underlying rvm.kernel kernel defaults to the Gaussian radial basis functions (rbfdot). RVM is computationally intensive in the number of kernel functions to use and directly using thousands of is too slow. To this end, I propose to combine RVM with a replicated design. The example below uses 800 unique inputs and total simulation budget of , i.e. replicates per site. This time, for variety’s sake, I pick a space-filling design:

modelBrGl3d$N <- 800 # N_unique

modelBrGl3d$batch.nrep <- 25 # N_rep

modelBrGl3d$pilot.nsims <- 1000

lhs.rect <- matrix(0, nrow=3, ncol=2) # domain of approximation

lhs.rect[1,] <- lhs.rect[2,] <- lhs.rect[3,] <- c(50,150)

modelBrGl3d$qmc.method <- randtoolbox::sobol # space-filling using QMC sequence

call3d.lhsFixed.rvm <- osp.fixed.design(modelBrGl3d,input.domain=lhs.rect, method="rvm")

An alternative kernel regression package is {npreg}. Below I use it with a Epanechnikov order-4 kernel and local-constant regression np.regtype=lc. The bandwidth is estimated using least squares cross-validation (default npreg option).

modelBrGl3d$np.kertype <- "epanechnikov"

modelBrGl3d$np.kerorder <- 4; modelBrGl3d$np.regtype <- "lc"

call3d.sobFixed.np <- osp.fixed.design(modelBrGl3d,input.domain=lhs.rect, method="npreg")

As a final emulation idea, consider multivariate adaptive regression splines (MARS) as implemented in the {earth} package. MARS provides adaptive feature selection using a forward-backward selection algorithm. I set the degree to be earth.deg=2, so that bases consist of linear/quadratic hinge functions, and allow up to earth.nk=200 hinges. Finally I also set the backward fit threshold earth.thresh. I take this opportunity to also illustrate the TvR scheme which relies on the one-step-ahead value function instead of during the regression. This is available via the top-level solver osp.tvr that otherwise follows the exact same syntax as osp.prob.design and so can be mixed and matched with any of the above regression methods.

earthParams <- c(earth.deg=2,earth.nk=200,earth.thresh=1E-8) # passed to {earth}

call3d.tvr.mars <- osp.tvr(N=100000, c(modelBrGl3d,earthParams), method="earth")

To my knowledge, most of the above choices are new, or at least partially new. Many more can be added. After having built all these models one can do horse racing on a fixed out-of-sample set of scenarios. A typical call to do so is

oos.tvr.mars <- forward.sim.policy( test.3d,nSteps.3d,call3d.tvr.mars$fit, modelBrGl3d)

I repeat this for 25 times each in order to record also the sampling standard error of each estimator, which is a measure of the scheme’s stability. The above sampling error reflects sensitivity to the training data, keeping all model tuning parameters and the test set fixed.

| () Emulator | Mean Price | Std. Error | Time (secs) |

|---|---|---|---|

| () | |||

| RF | 11.138 | 0.0058 | 34.5 |

| NNet | 11.152 | 0.0071 | 349.0 |

| npreg | 10.738 | 0.0095 | 62.9 |

| RVM | 11.151 | 0.0078 | 35.2 |

| MARS | 10.932 | 0.0041 | 51.6 |

| () |

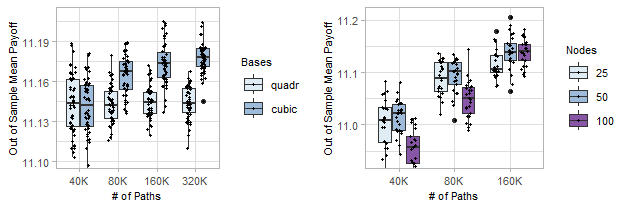

According to Table LABEL:tbl:2dput, RVM and NNet emulators perform best, yielding the highest out-of-sample payoffs. At the other end, npreg and MARS perform quite poorly. However, looking at running times, NNet is in fact seen to be the slowest of the bunch, taking more than 10x extra time compared to RVM, which is the fastest. In terms of standard errors, all emulators are quite close to another, with npreg (which performs worst) being the most stable. We note that direct comparisons are not straightforward since the different solvers utilized different training sets, i.e. is method-specific. In Section 6.3 below, I carry out additional fine-tuning of the LM and NNet solvers.

5.2 Deep Dive: Specifying bases for a linear model

The most extensively studied RMC approach follows the classical regression paradigm of a linear model with explicitly specified bases . This means that the approximation space has degrees of freedom and . From a statistical perspective, any set of linearly independent bases will do, although for theoretical analysis one often picks special (orthogonal) basis families, such as Hermite polynomials. In {mlOSP} selecting method=lm allows the user to specify any collection of bases, giving complete transparency on constructing .

It is well known that linear models are prone to overfitting, in part due to their sensitivity to the Gaussian homoskedastic noise assumption that is strongly violated in RMC. The skewed distribution of and state-dependent simulation variance make the resulting fit biased and less stable compared to regularized regression approaches, such as MARS or RF. To avoid overfitting, large training sets are needed, illustrating one of the trade-offs that must be considered for RMC implementations: namely the trade-off between speed (lm is effectively the fastest possible regression emulator) and memory (very large N required in order not to overfit). The memory constraint precludes scalability of method=lm to high dimensions whereby the needed number of bases grows quickly.

As an illustration, below I provide definitions of polynomial bases of degree up to 2 (bas2) and up to degree 3 (bas3) for the above 3D max-Call example, using (300 thousand) paths. In the latter case, I also append the payoff to the set of bases. The first expression below takes and similarly for degree-3 polynomials.

# polynomials of degree <= 2

bas2 <- function(x) return(cbind(x[,1],x[,1]^2,x[,2],x[,2]^2,x[,1]*x[,2],x[,3],x[,3]^2,

x[,3]*x[,2],x[,1]*x[,3]))

# polynomials up to degree 3 + the payoff

bas3 <- function(x) return(cbind(x[,1],x[,1]^2,x[,2],x[,2]^2,x[,1]*x[,2],x[,3],x[,3]^2,

x[,3]*x[,2],x[,1]*x[,3], x[,1]^3,x[,2]^3,x[,3]^3,

x[,1]^2*x[,2],x[,1]^2*x[,3],x[,2]^2*x[,1],x[,2]^2*x[,3],

x[,3]^2*x[,1],x[,3]^2*x[,2],x[,1]*x[,2]*x[,3],

maxi.call.payoff(x,modelBrGl3d)) ) # include the payoff

modelBrGl3d$bases <- bas2 # 10 coefficients to fit

lm.run2 <- osp.prob.design(300000,modelBrGl3d,method="lm")

oos.lm2 <- forward.sim.policy(test.3d, nSteps.3d, lm.run2$fit, modelBrGl3d)

modelBrGl3d$bases <- bas3 # 21 coefficients to fit

lm.run3 <- osp.prob.design(300000,modelBrGl3d,method="lm")

oos.lm3 <- forward.sim.policy(test.3d, nSteps.3d, lm.run3$fit, modelBrGl3d)

The second estimator is found to be significantly better, yielding 11.2239 compared to 10.7213 for the first one. In other words, having 21 bases is better than having only 10. At the same time it is also 2.5 times slower (11.21 vs 3.999 seconds).

One may straightforwardly apply more sophisticated bases, for example based on order statistics of which is a common trick in the context of a max-Call payoff [10]. Below I first sort as and then work with the 10-dimensional .

modelBrGl3d$bases <-function(x) {

sortx <- t(apply(x, 1, sort, decreasing = TRUE)) # sort coordinates in decreasing order

return(cbind(sortx[,1],sortx[,1]^2, sortx[,1]^3,sortx[,1]^4, sortx[,2],

sortx[,2]^2, sortx[,3], sortx[,1]*sortx[,2], sortx[,1]*sortx[,3] ))

}

lm.run4 <- osp.prob.design(300000,modelBrGl3d,method="lm")

oos.lm.sorted <- forward.sim.policy(test.3d, nSteps.3d, lm.run4$fit, modelBrGl3d)

print(mean(oos.lm.sorted$payoff))

## [1] 11.27393

The sorted coordinates better convey information about than the unsorted ones, yielding the highest option price among all solvers presented. The above examples allude to the limitless scope for customizing that is possible with mlOSP.

Another approach within the linear model regression framework is to build a piecewise-linear fit for that is defined in terms of partitions of the state space. The Bouchard-Warin algorithm [9] adaptively picks the regression sub-domains based on an equi-probable partition of . Thus, the sub-domains are empirically selected, typically with a fixed number of partitions in each coordinate of . The osp.probDesign.piecewisebw solver implements the above, generating from forward trajectories like in the LS scheme (cf. osp.prob.design). In the example below, I take nBins=5 bins per coordinate. With and training samples, this implies having sub-domains with 2400 trajectories in each. The overall then has 500 coefficients to be fitted, based on running 125 degree-1 lm models across the partitions.

modelBrGl3d$nBins <- 5

bw.run <- osp.probDesign.piecewisebw(300000,modelBrGl3d,tst.paths=test.3d)

## In-sample estimated price: 11.245 and out-of-sample 11.107

5.3 Variants of GP Emulators

Gaussian Process emulators for RMC were originally proposed in Ludkovski [26] and also investigated in Goudenege et al. [15]. One of their benefits is uncertainty quantification of the resulting fit, enabling the use of sequential design via osp.seq.design and osp.seq.batch.design. Another advantage is their expressivity, i.e. ability to fit complex input-output relations based on just a few training inputs. Thanks to these properties, GP emulators can provide highly accurate fits even with juts a few dozen (well-placed) training . At the same time, GPs have a cubic computational complexity in design size, and hence cannot directly handle more than a couple thousand unique inputs. Replicated designs offer one way out of this challenge; other solutions could be local GPs or sparse GPs.

The classical GP emulator assumes homoskedastic Gaussian simulation noise in (7) and learns its magnitude as part of the MLE fitting. However, this is a poor assumption for RMC because the variance in pathwise rewards is highly state-dependent, i.e. heteroskedastic. Indeed, deep out-of-the-money the conditional variance of the payoff is negligible, whereas it is very high deep in-the-money. A partial solution to account for this is to combine a replicated design with Stochastic Kriging (SK) [2]. SK estimates empirically via the classical MC variance estimator based on the batch of the pathwise timing values originating at :

SK does require a large batch size to be reliable; in practice we find that is necessary.

In {mlOSP} I implement the following types of GP emulators:

-

•

km based on user-specified hyperparameters km.var, km.cov. The GP is fit via the {DiceKriging} [33] package that offers several choices for kernel.family and utilizes SK. Thus, the GP-km emulator treats noise variance as known (rather than a parameter to be estimated) and uses as a proxy for the true .

-

•

trainkm based on MLE-optimized GP hyperparameters as implemented in {DiceKriging} and SK;

-

•

homgp which is essentially the same as trainkm but with a different MLE optimizer from the {hetGP} package. Also uses SK;

-

•

homtp: homoskedastic -Process regression also implemented in {hetGP};

-

•

lagp based on local approximate GP regression proposed in Gramacy and Apley [17] and implemented in {laGP};

-

•

hetgp heteroskedastic Gaussian process regression based on the eponymous {hetGP} package from Binois et al. [8];

The latter two choices are new in the RMC literature, and are proposed here for the first time due to their relevance for mlOSP, namely handling heteroskedasticity and spatial non-stationarity. The hetGP framework directly learns via a second spatial model that is jointly inferred with the model for the mean response. This has been recently implemented [8] in the {hetGP} package and available in {mlOSP} via method="hetgp".

modelBrGl3d$N <- 500

modelBrGl3d$batch.nrep <- 60

modelBrGl3d$kernel.family <- "Matern5_2" # different naming compared to km

put3d.hetgp <- osp.fixed.design(modelBrGl3d,input.dom=0.02, method="hetgp")

oos.hetgp <- forward.sim.policy(test.3d, nSteps.3d, put3d.hetgp$fit, modelBrGl3d)

cat(round(mean(oos.hetgp$payoff),3) )

## 11.114

Another way to achieve better scalability is to replace a single GP emulator that assumes a global correlation/noise structure with a local GP fit, analogous to replacing a global linear model with LOESS regression. To this end, I leverage the laGP framework which adopts a prediction-focused approach that builds a new sparse GP every time a is needed. Those GPs are local (akin to nearest neighbors), allowing to capture spatial non-stationarity and heteroskedasticity. To illustrate, I utilize lagp with a non-replicated design of 5000 unique inputs which would be prohibitively expensive with km. The variant below constructs local fits with 40 inputs, selected according to the alcray criterion.

modelBrGl3d$lagp.type="alcray"

modelBrGl3d$lagp.end=40

put3d.lagp <- osp.prob.design(7500,modelBrGl3d,method="lagp",subset=1:2500)

## [1] "In-sample price estimate 12.224; and out-of-sample: 10.584"

6 Benchmarks

A key motivation for building the mlOSP template was to create transparent and verifiable benchmarks for RMC algorithms. While many published works contain detailed comparisons between a particular RMC version and competing approaches, these results are necessarily limited in scope and are often very difficult to reproduce. The numerous nuances that inevitably crop up when implementing RMC make such comparisons fraught, leading to a lack of consensus on what strategies are more efficient. Some of the challenges inherent to benchmarking are:

-

•

RMC algorithms tend to have a slew of tuning parameters that significantly affect performance (from the number of simulations, to the precise choice of the regression specification);

-

•

One must define a complete problem instance, i.e. the payoff function, state dynamics, initial condition, etc. While some test cases have appeared repeatedly in numerous articles, there is no agreed-upon portfolio of test instances. Many algorithms are highly sensitive to the dimensionality of the problem, the geometry of the value function, the initial condition, etc., requiring a diverse set of tests to reveal all their pros and cons.

-

•

There are multiple criteria one could utilize to compare solution quality across algorithms, including accuracy at a fixed simulation budget, accuracy at a fixed computation time, running time at fixed budget.

-

•

The above metrics are heavily affected by the particular environment, including the programming language (e.g. R vs. C++), hardware setup, operating system, etc.

-

•

A key practical goal of benchmarking is to assess scalability of an RMC scheme, i.e. its ability to work well for a wide range of OSP instances. However, scalability is again a multi-faceted concept, related to simulation budget, running time, memory requirements, and of course accuracy, that all change nonlinearly as problems become more complex.

Due to all the above, the only way to create a “level playing field” for the different algorithms is to bring them all under one roof, coded side-by-side within a transparent computing environment. This is precisely what is achieved in {mlOSP}. In the companion software appendix, posted also on GitHub, I provide the RMarkdown code that can be run by any reader or end-user who downloads the {mlOSP} package to fully reproduce our results, figures and tables. To my knowledge, this is the most comprehensive verifiable set of RMC benchmarks (the StochOpt [14] also contains some benchmarks but primarily addresses more general stochastic control problems). The R code also makes completely transparent the chosen set of fully specified problem instances, which would be useful for other researchers in the future.

Remark: the preprint Herrera et al. [19] provides a related set of benchmarks for high-dimensional OSP instances with .

6.1 Benchmarked {mlOSP} instances

Below I present a list of 9 models and 10 solvers. All of them have appeared in previous articles. The OSP instances span a range of case studies (see Table 2 as well as Appendix D for a full specification) in terms of:

-

•

Problem dimension : 1D, 2D, 3D and 5D;

-

•

Number of time-steps from 9 to 50;

-

•

Underlying dynamics, including Geometric Brownian motion and stochastic volatility;

-

•

Option payoffs , including Puts, basket average Puts, max-Calls;

-

•

Problem geometry: both symmetric settings with i.i.d. assets (coordinates of ), as well as asymmetric/correlated asset dynamics.

| Model | Dim | Steps | Payoff | Dynamics | Notes | Ref |

|---|---|---|---|---|---|---|

| M1 | 1 | 25 | Put | GBM | Classic 1D at-the-money Put | [25] |

| M2 | 1 | 25 | Put | GBM | Same as M1 but out-of-the-money | [25] |

| M3 | 2 | 25 | Ave Put | GBM | 2D symmetric in-the-money basket Put | [25] |

| M4 | 2 | 9 | Max Call | GBM | 2D symmetric in-the-money max-Call | [25] |

| M5 | 2 | 50 | SV Put | SV Heston | Put in a Stochastic volatility model, in-the-money | [31] |

| M6 | 3 | 9 | Max Call | GBM | 3D symmetric out-of-the-money max-Call | [10] |

| M7 | 5 | 9 | Max Call | GBM | 5D symmetric at-the-money max-Call | [10] |

| M8 | 5 | 9 | Max Call | GBM | 5D Asymmetric out-of-the-money max-Call | [10] |

| M9 | 5 | 20 | Ave Put | GBM Cor | 5D asymmetric correlated basket Put | [24] |

The resulting benchmarks are reproducible (all random number seeds fixed and provided) and utilize shared out-of-sample test sets which are available upon request from the author, comprising more than 100Mb of data.

6.2 Benchmark Results

| Model | S1-LM | S2-RF | S3-MARS | S4-TvR | S5-NNet | S6-BW | S7-GP | S8-ADSA | S9-Seq | S10-hetGP |

|---|---|---|---|---|---|---|---|---|---|---|

| M1 | 2.07 | 2.24 | 2.30 | 2.20 | 2.31 | 2.30 | 2.31 | 2.31 | 2.31 | 2.29 |

| M2 | 1.01 | 1.04 | 1.09 | 1.07 | 1.09 | 1.10 | 1.10 | 1.10 | 1.10 | 1.09 |

| M3 | 1.23 | 1.33 | 1.45 | 1.37 | 1.45 | 1.44 | 1.46 | 1.43 | 1.44 | 1.44 |

| M4 | 21.48 | 21.21 | 21.39 | 20.21 | 21.44 | 21.36 | 21.41 | 21.30 | 21.32 | 21.31 |

| M5 | 16.43 | 16.44 | 15.99 | 16.40 | 16.35 | 15.97 | 16.41 | 10.00 | 16.39 | 16.17 |

| M6 | 11.15 | 11.04 | 11.13 | 10.85 | 11.05 | 11.01 | 11.06 | 11.15 | 11.12 | 11.10 |

| M7 | 25.84 | 25.34 | 25.32 | 25.10 | 25.31 | 25.00 | 25.44 | 25.12 | 25.31 | 25.37 |

| M8 | 11.81 | 11.51 | 11.65 | 11.74 | 11.69 | 11.53 | 11.39 | 11.60 | 11.60 | 11.65 |

| M9 | 2.71 | 3.90 | 4.10 | 3.50 | 4.15 | 3.95 | 4.11 | 4.12 | 4.10 | 4.13 |