A Strict Complementarity Approach to Error Bound and Sensitivity of Solution of Conic Programs

Abstract

In this paper, we provide an elementary, geometric, and unified framework to analyze conic programs that we call the strict complementarity approach. This framework allows us to establish error bounds and quantify the sensitivity of the solution. The framework uses three classical ideas from convex geometry and linear algebra: linear regularity of convex sets, facial reduction, and orthogonal decomposition. We show how to use this framework to derive error bounds for linear programming (LP), second order cone programming (SOCP), and semidefinite programming (SDP).

1 Introduction

Given two finite dimensional Euclidean spaces and , each equipped with an inner product denoted as , we consider a conic program in standard form with decision variable :

| minimize | () | |||||

| subject to | ||||||

Here the problem data comprises a linear map , a right hand side vector , and a cost vector . The cone is proper 333A cone is proper if it is closed, convex, and pointed.. The solution set and optimal value of (LABEL:opt:_primalcone) are denoted as and respectively. When is the nonnegative orthant , the second order cone , or the set of positive semidefinite matrices , we call the corresponding problem (LABEL:opt:_primalcone) an LP, SOCP, or SDP, respectively.

In this paper, we provide an elementary framework based on strict complementarity (see Section 2.1) to establish error bounds and quantify the sensitivity of the solution of Problem (LABEL:opt:_primalcone). In the following, denotes the Euclidean norm induced by the inner product, while is a generic norm that will be specified when we instantiate these bounds later in the paper.

-

•

Error bound: Given , define three error metrics: suboptimality , linear infeasibility , and conic infeasibility as , where the conic part .444 The orthogonal projector is defined as . These errors are easy to measure, while the distance of a given point to the solution is not. This paper shows how to establish an error bound for (LABEL:opt:_primalcone) that bounds the distance to the solution in terms of these measurable error metrics, for some constants and exponent independent of :

(ERB) where is the distance to .

-

•

Sensitivity of the solution: We often wish to understand how the solution of the problem changes with perturbations of the problem data. Given new problem data for Problem (LABEL:opt:_primalcone), where is the set of linear maps from to , Problem (LABEL:opt:_primalcone) admits a new optimal solution set . This paper shows how to quantify the sensitivity of the solution, for some constants and exponent , via the inequality

(SSB) where is the distance between solution sets. In fact, once an error bound of the form (ERB) is available, we can prove an inequality of this form by bounding the error metrics of the new solution with respect to the original problem data in terms of the perturbation .

Importance of the error bound and sensitivity of solution.

The error bound and sensitivity of the solution can be regarded as condition numbers for Problem (LABEL:opt:_primalcone). They guarantee that the output of iterative algorithms to solve (LABEL:opt:_primalcone) is still useful despite optimization error (of the algorithm) and measurement error (of the problem data) [Lew14, DU20]. The error bound is also vital in proving faster convergence for first order algorithms [DL18, ZS17, NNG19, JM17]. Hence a huge body of work has devoted to establish error bounds and sensitivity of solutions [Hof52, DL18, ZS17, Lew14, Stu00, NO99].

Our Contribution.

In this paper, we use the notion of strict complementarity (defined in Section 2.1) to provide an elementary, geometric, and unified framework, described in detail in Section 2, to establish bounds of the form (ERB) and (SSB) for the conic program (LABEL:opt:_primalcone). Specifically, in Section 3 and 4, we show how to construct a bound with exponents for LP and for SOCP and SDP, under strict complementarity, and provide a way to obtain explicit estimates of in terms of the primal and dual solutions and problem data when the primal solution is unique. Table 1 summarizes our results.

The main contribution of this paper is a new and simple framework for proving bounds of this form. As discussed in Section 5, many particular bounds that we present here have been discovered before. On the other hand, we believe that some of the bounds are new: in particular, bounds on the sensitivity of the solution that pertain when the primal or dual solution are not unique.

Paper organization.

The rest of the paper is organized as follows. In Section 2.1, we discuss two important analytical conditions assumed throughout this paper: strong duality and dual strict complementarity. In Section 2.2, we describe the basic framework of the strict complementarity approach: linear regularity of convex sets, facial reduction, and extension via orthogonal decomposition. In Section 3, we apply the framework to specific examples, LP, SOCP, and SDP, to establish error bounds. We next demonstrate how to use the error bound established to characterize the sensitivity of solutions in Section 4 by bounding the error measures of the new solution in terms of the perturbation . Finally, we discuss previous results regarding (ERB) and (SSB), how this work relates to them, and potential new directions.

Notation.

We use to represent generic finite dimensional Euclidean spaces. For a set in , we denote its interior, boundary, affine hull, and relative interior as , , , and respectively. We equip with the dot inner product, and and with the trace inner product. The distance to a set is defined as . We write for an arbitrary norm, and for the norm induced by the underlying inner product. For matrices, the operator norm (maximum singular value), Frobenius norm, and nuclear norm (sum of singular values) are denoted as , , and respectively. For a linear map and a linear space , we write the restriction of to as . We define the largest and smallest singular value of as and respectively.

2 The strict complementary slackness approach

In Section 2.1, we introduce two important structural conditions, strong duality and dual strict complementarity, that are essential to our approach. Next in Section 2.2, we describe the main ingredients of the strict complementary slackness approach: linear regularity (Section 2.2.1), facial reduction (Section 2.2.2), and orthogonal decomposition (Section 2.2.3). Our main result, Theorem 1, is in Section 2.2.3.

2.1 Analytical conditions

Here we define two conditions that are essential to our framework: strong duality and dual strict complementarity. To start, let us recall the dual problem of (LABEL:opt:_primalcone) is

| () |

The vector is the decision variable, the linear map is the adjoint of the linear map , and the cone is the dual cone of , i.e., . Let us introduce strong duality first.

Definition 1 (Strong duality).

The primal and dual problems (LABEL:opt:_primalcone) and satisfy strong duality (SD) if the primal and dual solution sets are nonempty, is compact, and there exists a primal and dual solution pair such that

| (SD) |

Equivalently, define the slack vector to rewrite the equality SD as

Note that we require the existence of primal and dual optimal solutions instead of just equality of optimal values. Strong duality in the stated form is ensured by primal and dual Slater’s condition: there is a primal and dual feasible pair with .

Next we state the second condition: dual strict complementarity. This condition is the key to established error bounds for a variety of optimization problems [DL18, ZS17].

Definition 2 (Dual strict complementarity (DSC)).

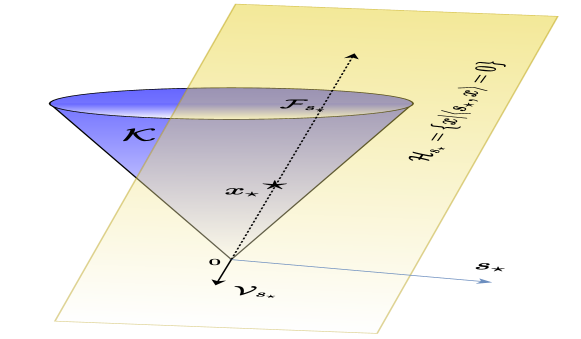

Let us now unpack the definition of and dual strict complementarity. Also see Figure 1 for a graphical illustration of the condition.

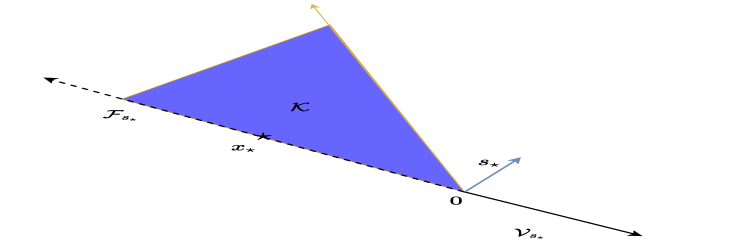

Understanding the complementary face .

To understand the name complementary face, let us introduce the complementary hyperplane, the hyperplane orthogonal to the slack vector . The complementary face is simply the intersection of and the cone . The intersection is nonempty due to strong duality. We can see that is indeed a face because its intersection with is nonempty (it contains ), and every lies on the same side of the hyperplane , , as . In particular, we see the face is exposed.

Dual strict complementarity (DSC) and Slater’s condition.

To better understand dual strict complementarity, define the complementary space as the affine hull of , . The complementary face is a cone, so the complementary space is a linear subspace. Imagine modifying problem (LABEL:opt:_primalcone) by replacing the cone by in problem (LABEL:opt:_primalcone) and restricting the decision variable to the subspace . Note that is still a solution to this problem, so this procedure is related to facial reduction: the modified problem restricts to a face of the original cone . DSC means that there is a primal in the interior of the cone , where the interior is taken w.r.t. the subspace . Hence DSC is equivalent to the usual Slater’s condition for the modified problem.

Primal strict complementarity and strict complementarity.

Given dual strict complementarity (DSC), a natural way to define primal strict complementarity (PSC) is to reverse the role of and in the definition of DSC. Precisely, PSC means that there exists with . Primal and dual strict complementarity are not always equivalent unless the cone is exposed.555 For a discussion on primal and dual strict complementarity, see [DJS17, Remark 4.10] Happily, all the symmetric cones are exposed, including , , and . [DJS17] shows that DSC and PSC actually hold “generically” 666Roughly speaking, this condition holds except on a measure set of problems parameterized by , conditioning on the existence of a primal dual solution pair. We refer the reader to the references for more details. for general conic programs. It is worth noting that the standard notion of strict complementarity (SC) for SDP [AHO97, Definition 4] and LP, both defined algebraically, are equivalent to the geometric notion of DSC here.777The definition of SC for LP and SDP, and the proof of the equivalence can be found in Section B. SC always holds for LP [GT56], holds “generically” for SDP as shown in [AHO97], and even holds for some structured instances of SDP [DU20]. Due to the equivalence, DSC also holds under the same conditions for LP and SDP.

2.2 Defining the strict complementary slackness approach

In this section, we explain how to use the two assumptions in Section 2.1 to establish a framework to prove error bounds of the form (ERB) and sensitivity bounds of the form (SSB). As we explained in the introduction, an error bound (ERB) can be used to derive a sensitivity bound (SSB). Hence, we focus on proving an error bound first. Our main theorem, Theorem 1 in Section 2.2.3, reduces the task to bounding the quantity .888Here is orthogonal complementary space of , and is the corresponding projection. Recall the conic part is . We explain how to further bound this quantity in Section 3.

2.2.1 From optimality to feasibility: linear regularity of convex sets

Our first step is to identify problem (LABEL:opt:_primalcone) with the feasibility problem of finding such that

| (1) |

This transformation activates the following geometric result, called linear regulairty regularity of convex sets [BBL99, Theorem 4.6], [Zha00, Theorem 2.1], a classical result on error bounds for feasibility systems. This result states that the distance to the intersection of two sets is bounded by the sum of distances to the two sets.

Lemma 1 (Linear regularity).

Suppose the is an affine space with , where is a linear map, and is a closed convex cone. If and is compact, then there are some such that for all ,

| (2) |

Now it is tempting to set and , and conclude (ERB) holds with exponent , since . The catch is that for most problems of interest, the optimal solution lies on the boundary of the cone , and the condition does not hold! Indeed, unless , which makes (LABEL:opt:_primalcone) a feasibility problem, we always have .

2.2.2 Facial reduction

We may still use Lemma 1 to establish an error bound. The key is to use the facial reduction idea mentioned earlier. Recall the condition required is , which does not hold for (LABEL:opt:_primalcone) with nonzero . The problem is that the cone lies in the large space , so its interior (with respect to ) does not contain . Instead, consider restricting the variable to the complementary space and replacing the cone by the complementary face . The interior of the cone with respect to the space does contain under strict complementarity, so we may activate Lemma 1.

This modification enables an error bound for as stated in Lemma 2 below. We also provide a more concrete estimate of the constants when is a singleton.

Lemma 2.

Suppose strong duality and dual strict complementarity hold. Then there are constants such that for any :

| (3) |

Moreover, if is a singleton, then we may take and . Here, the linear map is restricted to and is the smallest singular value of .

Proof.

The inequality 3 is immediate by using Lemma 1 with , , and . Indeed, this choice gives . The condition , where the interior is taken with respect to the space , is exactly (DSC): such that .

Now we show that and when is a singleton. First assume has a trivial nullspace, so is the only solution in to . Hence and so for any , . Finally, we show by contradiction that the nullspace of is trivial whenever is a singleton. If the nullspace is not trivial, then there is some such that . Hence for some small enough is still optimal, as , which contradicts our hypothesis that the solution set is a singleton.

∎

This choice of the face and the corresponding linear space correspond to the idea of facial reduction [DW17, BW81]. Facial reduction is a conceptual and numerical technique designed to handle conic feasibility problems for which constraint qualifications (such as Slater’s condition) fail. Note that such failure is the interesting case for a feasibility system (1) when the optimal solution . Indeed, our choice of face can be considered as one step of the facial reduction procedure.

2.2.3 Extension to the whole space: orthogonal decomposition

In this section, we derive our main result, Theorem 1, by extending the previous result to the whole space using the orthogonal decomposition with .

Theorem 1.

Suppose strong duality and dual strict complementarity hold. Then for some constants described in Lemma 2 and for all , we have

| (4) | ||||

where and are orthogonal projections to and respectively. The terms and can themselves be bounded by .

Proof.

Recall Lemma 2 establishes an error bound for only those . Using the orthogonal decomposition proposed, for any ,

This decomposition immediately gives

| (5) |

The second term can be bounded using Lemma 2:

| (6) |

To translate the above bound to linear infeasibility and conic infeasibility , we note that and 999Recall and . With these two decompositions, and tad more algebra, we arrive at the theorem. ∎

To go further, we need to bound the following two terms in terms of , , and :

-

1.

The distance to the space : .

-

2.

The term .

In Section 3, we show how to bound both terms for the special cases of LP, SOCP, SDP, and more general conic programs (LABEL:opt:_primalcone) where is a finite product of LP, SOCP, or SDP cones. A quick summary of results can be found in Table 1.

As we shall see in Section 3, the term is usually zero. Thus the major challenge is bounding 101010Bounding this term is in some sense necessary in establishing an error bound. See more discussion in Section C in the appendix.. Note that under this condition, for feasible of (LABEL:opt:_primalcone), the bound (4) reduces to

| (7) |

If the solution set is a singleton, then from Lemma 2, we know , and we encounter a condition number like quantity in (7). Depending on applications, the condition number may scale with the problem dimension but the bound is still tight as the following example shows.

Example 1.

Consider an SDP with , where is the all one vector, , and . This is a simplification of the SDP for synchronization [Ban18, DU20]. For this SDP, it is easily verified that the unique optimal solution is and dual strict complementarity holds with dual optimal slack . The condition number like quantity in this case is which does scale with the dimension . However, if in (7) we let , the identity matrix which is feasible, then the LHS and RHS of (7) are and respectively. Thus the bound is actually tight for large .

3 Application: error bounds

In this section, we show how to use the framework established in Section 2 to analyze conic programs (LABEL:opt:_primalcone) over the nonnegative orthant, the second order cone, the set of positive semidefinite matrices, or a finite product of these cones. Our analysis has two main steps:

-

1.

Identify and write out the complementary face and .

-

2.

Bound the term via a function , called the violation of complementarity, using the explicit structure of .

We summarize the findings of this section as the following lemma and corollary. Refer to Table 1 for a quick summary of the results.

Lemma 3.

Define the complementarity error . Suppose strong duality holds. The quantity can be bounded by several different functions , which we call the violation of complementarity, depending on the slack vector and the cone . The first two trivial cases are the following.

-

1.

If , then .

-

2.

If , then , where .

Moreover, for the nontrivial case , we have the following bounds:

-

3.

: where is the smallest nonzero element of .

-

4.

: .

-

5.

: . Here is the smallest nonzero eigenvalue of .

Proof.

Let us first consider the two trivial cases (1) and (2) . These cases are excluded whenever and are both nonzero. In the first case, , and we simply have . In the second case, we have , and , where . We defer the proof for the other cases to Section 3.1, 3.2, and Section 3.3 for LP, SOCP, and SDP respectively. ∎

Combining Lemma 3, and Theorem 1, we reach the following corollary. The quantity can be verified to be zero for the two trivial cases by noting (i) the complementary space and for the case , and (ii) the complementary space and is a closed cone for the case . It is also zero for other three cases as shown in Sections 3.1–3.3.

Corollary 1.

Suppose strong duality and dual strict complementarity hold, and one of the five cases in Lemma 3 pertains. Then there exists constants so that for all ,

| (8) | ||||

where the condition number . In particular, when is a singleton, then and . Here the formula for can be found in Lemma 3 for each of the different cases, and we can further decompose the complementarity error using .

A few remarks regarding the lemma and the corollary are in order.

Remark 1 (Global and local error bound).

Note the formula for the violation of complementarity uses for SOCP and for SDP. Hence the bound (8) for these two cases does not quite align with the form of the error bound (ERB) we seek. To eliminate the dependence on this norm (by bounding the norm), either of the following conditions suffices:

-

•

for some constant ,

-

•

for some constant .

The second requirement combined with (8) for SOCP (SDP) implies () is bounded by some depending on but independent of (). We may then replace the term () by or in . Requiring either of these two conditions produces a local error bound. Interestingly, no such condition on the norm is not necessary for the LP case and the other two trivial cases; hence the bounds (8) in these cases are global error bounds.

Remark 2 (Value of and estimate of in (ERB)).

Ignoring the term , the bound (8) in Lemma 3 is linear in . For LP and the two trivial cases, is linear in , hence the error bound (ERB) holds with exponent . For SOCP and SDP, the square root of appears in , hence (8) gives an error bound of the form (ERB) with exponent , under the assumption .

Now let’s consider the constants , , and in the error bound (ERB). It is cumbersome to estimate these for general ; here, suppose is feasible. For the SOCP and SDP cases, also suppose . Then the bound (8) reduces to

| (9) |

The resulting constant for in the error bound (ERB) for each of the five cases appears in Table 1.

| Conic | LP | SOCP | SDP | ||

|---|---|---|---|---|---|

| program | |||||

| violation of | 0 | ||||

| complementarity | |||||

| exponents in | 1 | 1 | 1 | 2 | 2 |

| (ERB) and (SSB) | |||||

| constant for | 0 |

Remark 3 (Conditions for LP).

Recall that for linear programming, dual strict complementarity is the same as strict complementarity, which always holds under strong duality [GT56]. Hence we need not explicitly require the dual strict complementarity condition. Also the compactness condition for strong duality in Section 2.1 can be dropped if we establish Theorem 1 using Hoffman’s lemma [Hof52] instead of Lemma 1.

Remark 4 (Finite product of cones).

Error bounds for a conic program whose cone is a finite product of , and can be established by bounding the term by a sum of te correponding s in Lemma 3. We omit the details.

Next, we prove the bound , violation of complementarity, in Lemma 3 for the LP, SOCP, and SDP comes by following the aforementioned procedure: (i) identify and write out and , and (ii) bound the term .

3.1 Linear programming (LP)

In linear programming, the cone .

Identify and .

For a particular dual optimal solution , satisfying dual strict complementarity, the complementary face , and the complementary space . Hence, the term is simply zero as .

Bound the term .

3.2 Second order programming (SOCP)

In second order cone programming, the cone is .

Identify and .

Given a dual solution satisfying dual strict complementarity, the complementary face is defined as . We can further simplify this expression as

The complementary space for the nontrivial case is simply

For the dual optimal solution , denote . Note that the term is again simply zero as .

Bound the term .

We now turn to analyze , which can be written explicitly as

| (11) |

Now introduce the shorthand . The norm square of can be written as

| (12) | ||||

where in step , we use the fact that and the definition of . In step , we use the fact . Lemma 3 for the SOCP case is established by noting .

3.3 Semidefinite programming (SDP)

In semidefinite programming, the cone is . Note that we use capital letter and for matrices.

Identify and .

For a dual optimal solution with satisfying dual strict complementarity, the complementary face , where , and is a matrix with orthonormal columns that span . In this case, the complementary space . We note that the term is again zero as .

Bound the term .

We now turn to bound the term . We utilize Lemma 4 [DYC+19, Lemma 4.3] to bound the term with , and use the observation that .

Lemma 4.

Suppose are both positive semidefinite. Let be the matrix formed by the eigenvectors with the smallest eigenvalues of and define . Let . If , then

4 Application: sensitivity of solution

As discussed in the introduction, to study the sensitivity of the solution, we consider a solution of the perturbed problem

| () | ||||||

| subject to | ||||||

where the problem data for some small perturbation , and ask how the distance changes according to .

Note that once the error bound (ERB) is established, we can understand the sensitivity of the solution by estimating the suboptimality, linear and conic infeasibility of the new solution with respect to the original problem (LABEL:opt:_primalcone) via the perturbation . Following this strategy, we prove the following theorem:

Theorem 2.

To facilitate the proof, we define the smallest nonzero singular value of as , and the pseudoinverse of as .

Proof.

Consider any solution to the problem (LABEL:opt:_primalconeperturbed). Suppose the following assumptions are satisfied (proved in Appendix A):

-

1.

Primal and dual Slater’s condition for (LABEL:opt:_primalconeperturbed): there exist a primal and dual solution feasible for problem (LABEL:opt:_primalconeperturbed) and its dual that satisfy for some independent of , and for some independent of .

-

2.

Boundedness of primal solutions of (LABEL:opt:_primalconeperturbed): There is some independent of such that any solution to (LABEL:opt:_primalconeperturbed) satisfies .

Let us start with the linear infeasibility . Using the linear feasibility of , , w.r.t. (LABEL:opt:_primalconeperturbed), we have

| (13) | ||||

This shows for any .

Next, consider . We would like to use the optimality of to (LABEL:opt:_primalconeperturbed) and compare it against . However, since is not necessarily feasible for (LABEL:opt:_primalconeperturbed), we need more subtle reasoning. Consider with . Here exists and has largest singular value at most as long as . We have for some independent as . Note that since

if . The case of is trivial. We also know is feasible with respect to the linear constraints of (LABEL:opt:_primalconeperturbed):

| (14) | ||||

Note by construction with . Hence for some constant . Now using the optimality of , we have

| (15) |

Hence for large enough using . ∎

5 Discussion

Using the framework established in Section 2, we have shown an error bound of the form (ERB) and a bound on the sensitivity of the solution with respect to problem data (SSB) for a broad class of problems: LP, SOCP, and SDP, and conic programs for which the cone is a finite product of the LP, SOCP, and SDP cones. Let us now compare the results we have obtained with the literature on error bounds and sensitivity of solution.

Error bound

The celebrated results of [Hof52] show that the error bound is linear for linear programming: in (ERB), the exponent . The work of Sturm [Stu00, Section 4] shows that under strict complementarity and compactness of the solution set, SDPs satisfy a quadratic error bound: in (ERB). Sturm also discusses the exponent of without strict complementarity: it can be bounded by where is the singularity degree, which is at most [Stu00, Lemma 3.6]. A recent result shows that under dual strict complementarity type conditions when the cone is an amenable cone, which includes all symmetric cones [Lou19]. When the cone is defined as a semialgebraic set (LP, SOCP, SDP are special cases), Drusvyatskiy, Ioffe, and Lewis [DIL16, Corrollary 4.8] showed that for generic cost vector , the exponent is always when the inequality is restricted to feasible . We note that the proofs for these bounds do not provide estimates for . In our framework, estimates of (expressed in terms of the primal and dual solution) can be obtained supposing the primal solution is unique.

Sensitivity of solution

When , the bound describing the sensitivity of the solution (SSB) is also called stability or metric regularity [Rus11, Definition A.6], discussed in detail in [Rus11, Appendix A], and [KK06, BS13]. In the context of semidefinite programming, when the primal and dual solutions are unique and strict complementarity holds, Nayakkankuppam and Overton [NO99] shows that (SSB) holds with . When the cone is a semialgebraic set, Drusvyatskiy, Ioffe, and Lewis [DIL16, section 5] showed that for generic perturbations in the cost vector and the right hand side vector , the sensitivity bound (SSB) holds with .

Other Cones?

An interesting future direction is the extension to other cones, e.g., the copositive cone, the completely positive cone, and the doubly positive cone (the intersection of nonnegative matrices and positive semidefinite matrices). Can we still bound the term ? For the cones , , and , our technique relies on the explicit structure of , , and to bound . Characterizing the facial structure seems to be challenging for other cones.

Extension to quadratic programming (QP)

A potential future direction is to use the approach of the paper to establish error bounds for QP. The strategy consists of three steps: (1) reducing the QP to an SOCP, (2) utilizing the error bound for the SOCP, and (3) translating the error bound to the QP setting. We leave the detail to future work.

Acknowledgment

L. Ding and M. Udell were supported from NSF Awards IIS1943131 and CCF-1740822, the ONR Young Investigator Program, DARPA Award FA8750-17-2-0101, the Simons Institute, Canadian Institutes of Health Research, and Capital One. L. Ding would like to thank James Renegar for helpful discussions.

References

- [AHO97] Farid Alizadeh, Jean-Pierre A Haeberly, and Michael L Overton. Complementarity and nondegeneracy in semidefinite programming. Mathematical programming, 77(1):111–128, 1997.

- [Ban18] Afonso S Bandeira. Random laplacian matrices and convex relaxations. Foundations of Computational Mathematics, 18(2):345–379, 2018.

- [BBL99] Heinz H Bauschke, Jonathan M Borwein, and Wu Li. Strong conical hull intersection property, bounded linear regularity, jameson’s property (g), and error bounds in convex optimization. Mathematical Programming, 86(1):135–160, 1999.

- [BS13] J Frédéric Bonnans and Alexander Shapiro. Perturbation analysis of optimization problems. Springer Science & Business Media, 2013.

- [BW81] Jon M Borwein and Henry Wolkowicz. Facial reduction for a cone-convex programming problem. Journal of the Australian Mathematical Society, 30(3):369–380, 1981.

- [DIL16] Dmitriy Drusvyatskiy, Alexander D Ioffe, and Adrian S Lewis. Generic minimizing behavior in semialgebraic optimization. SIAM Journal on Optimization, 26(1):513–534, 2016.

- [DJS17] Mirjam Dür, Bolor Jargalsaikhan, and Georg Still. Genericity results in linear conic programming—a tour d’horizon. Mathematics of operations research, 42(1):77–94, 2017.

- [DL18] Dmitriy Drusvyatskiy and Adrian S Lewis. Error bounds, quadratic growth, and linear convergence of proximal methods. Mathematics of Operations Research, 43(3):919–948, 2018.

- [DU20] Lijun Ding and Madeleine Udell. On the regularity and conditioning of low rank semidefinite programs. arXiv preprint arXiv:2002.10673, 2020.

- [DW17] Dmitriy Drusvyatskiy and Henry Wolkowicz. The many faces of degeneracy in conic optimization. arXiv preprint arXiv:1706.03705, 2017.

- [DYC+19] Lijun Ding, Alp Yurtsever, Volkan Cevher, Joel A Tropp, and Madeleine Udell. An optimal-storage approach to semidefinite programming using approximate complementarity. arXiv preprint arXiv:1902.03373, 2019.

- [GT56] Alan J Goldman and Albert W Tucker. Theory of linear programming. Linear inequalities and related systems, 38:53–97, 1956.

- [Hof52] Alan J Hoffman. On approximate solutions of systems of linear inequalities. Journal of Research of the National Bureau of Standards, 49(4), 1952.

- [JM17] Patrick R Johnstone and Pierre Moulin. Faster subgradient methods for functions with holderian growth. arXiv preprint arXiv:1704.00196, 2017.

- [KK06] Diethard Klatte and Bernd Kummer. Nonsmooth equations in optimization: regularity, calculus, methods and applications, volume 60. Springer Science & Business Media, 2006.

- [Lew14] AS Lewis. Nonsmooth optimization: conditioning, convergence and semi-algebraic models. In Proceedings of the International Congress of Mathematicians, Seoul, volume 4, pages 872–895, 2014.

- [Lou19] Bruno F Lourenço. Amenable cones: error bounds without constraint qualifications. Mathematical Programming, pages 1–48, 2019.

- [NNG19] Ion Necoara, Yu Nesterov, and Francois Glineur. Linear convergence of first order methods for non-strongly convex optimization. Mathematical Programming, 175(1-2):69–107, 2019.

- [NO99] Madhu V Nayakkankuppam and Michael L Overton. Conditioning of semidefinite programs. Mathematical programming, 85(3):525–540, 1999.

- [Rus11] Andrzej Ruszczynski. Nonlinear optimization. Princeton university press, 2011.

- [Stu00] Jos F Sturm. Error bounds for linear matrix inequalities. SIAM Journal on Optimization, 10(4):1228–1248, 2000.

- [Zha00] Shuzhong Zhang. Global error bounds for convex conic problems. SIAM Journal on Optimization, 10(3):836–851, 2000.

- [ZS17] Zirui Zhou and Anthony Man-Cho So. A unified approach to error bounds for structured convex optimization problems. Mathematical Programming, 165(2):689–728, 2017.

Appendix A Proof for Section 4

We first show the Slater’s condition for (LABEL:opt:_primalconeperturbed) and its dual. Recall the Slater’s condition for the original (LABEL:opt:_primalcone) means that the two points satisfying . This implies that for some constant . We now construct and from and . It can be easily verified if , , and , then the choice

| (16) |

satisfy , , and are feasible for(LABEL:opt:_primalconeperturbed) and its dual.

Now for the boundedness condition of any solution to (LABEL:opt:_primalconeperturbed). Using the previous constructed and , we know

| (17) | ||||

The rest is a simple consequence of the following lemma.

Lemma 5.

Suppose is closed and convex. Given and with , there is a such that for any satisfying , and for some with , its norm satisfies .

Proof.

Suppose such does not exist, then there is a sequence with , , and .

Now consider . Since and are bounded, we can choose a appropriate subsequence of which converges to certain as . Call the subsequence still. Using and , we see

This is not possible as . Hence such must exist. ∎

Appendix B Equivalence between DSC and SC for LP and SDP

We define the strict complementarity of LP and SDP, and show it is equivalent to DSC defined in Section 2.1. For a vector , denote as its number of nonzeros.

Definition 3.

For LP, if there exists optimal primal dual pair with such that

we say (LABEL:opt:_primalcone) satisfies strict complementarity. Similary, for SDP, if there exists optimal primal dual pair with such that

we say (LABEL:opt:_primalcone) satisfies strict complementarity.

Lemma 6.

For both LP and SDP, under strong duality, the strict complementarity defined is equivalent to dual strict complementarity.

Proof.

For LP, under strong duality (see (SD)), we have for any optimal , . The relative interior of is

The equivalence between DSC and SC is then immediate.

For SDP, under strong duality (see (SD)), we know that for any optimal , . The relative interior of is

The equivalence is immediate by using Rank-nullity theorem for . ∎

Appendix C A lower bound on distance to optimality:

We have shown how to establish upper bounds on with an upper bound on . In this section, we show that the same quantity also yields a lower bound. Hence, it is important to understand the behavior of . For simplicity, we suppose in this section that is feasible for the problem (LABEL:opt:_primalcone) : in this case, . The argument for infeasible is essentially the same.

First recall for feasible , the only nonzero error metric is the suboptimality . Also note that using complementary slackness. Hence, there is some nonnegative function such that . Now note that for any feasible , we always have the lower bound on distance given by as ,

| (18) |

The lower bound (18) hence shows that provides a lower bound on the distance , and provides hope that this bound might scale with the suboptimality . We summarize our findings in the following theorem.

Theorem 3.

Suppose there exists a increasing continuous with so that for any feasible for Problem (LABEL:opt:_primalcone)111111 The assumption being feasible is just for convenience of presentation. The equivalence still holds for all with suboptimality, infeasibility, and conic infeasibility bounded above by some constant . with ,

| (19) |

Then the following inequality holds:

| (20) |

Remark 5.

Appendix D Conic Decomposition

In the main paper, we decompose a general according to the subspace . A different decomposition uses the cone : every admits the conic decomposition where is the polar cone of , i.e., the negative dual cone .

Theorem 4.

Suppose strong duality and dual strict complementarity hold. Then for some constants described in Lemma 2 and for all , we have

| (22) |

Let us compare the above bound (22) and (4) in Theorem 1. To make the comparison easier, first note that from the proof of Theorem 1, we can bound the distance from to using the decomposition :

| (23) |

The bound (4) in Theorem 1 is further obtained via the decomposition .

Comparing (23) and (22), we find that there is an extra term in (23) and the term in (23) is replaced by . Since , it is not immediately clear which bound is tighter.

A more subtle difference between (22) and (4) in Theorem 1 is that we are not able to further bound using the decomposition with respect to . We reach this impasse because the projection operator is not linear and so we cannot rely on the triangle inequality . Hence we cannot bound using conic infeasibility.

Thus, to use (23), we must use (which may be infeasible with respect to the cone ) directly to bound . We now consider how to bound this term for the cases considered in the main text.

Case .

For , we have . Thus and . For , we have . Thus and . We can bound as in Lemma 3.

Case .

For , the projection of where is the vector zeroing all entries in the support of and is the vector zeroing out all entries not in the support of . Hence, and we can further bound as in Lemma 3.

Case .

For , considering the nontrivial case , the projection of is

Thus we have

| (24) | ||||

In the step , we use and . Hence, one can bound by combining the above bound and the bound on established in the main text.

Case .

For , is

Since , we know

| (25) | ||||

In step , we use the fact that has orthonormal columns, and in step , we use the fact that is still positive semidefinite and projection to the convex set is nonexpansive. Thus, we can bound using the result for in the main text.

Case is feasible.

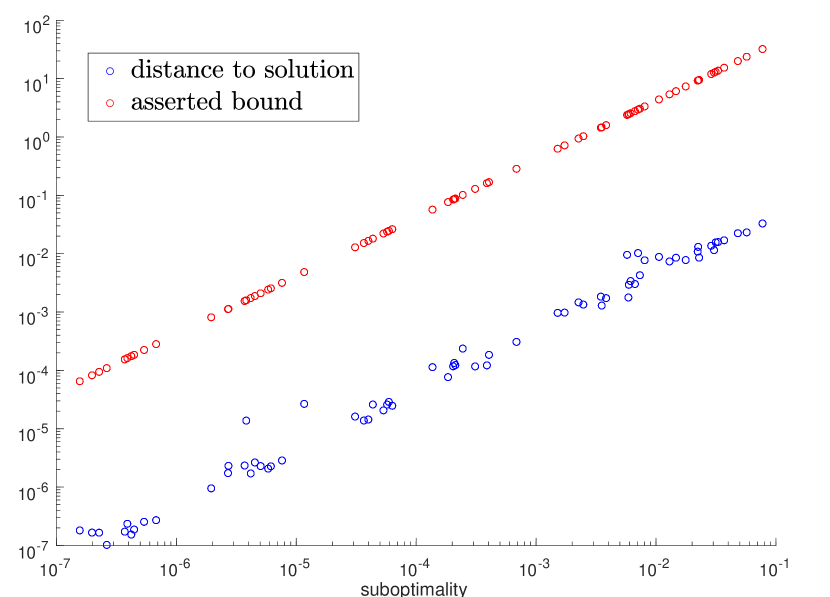

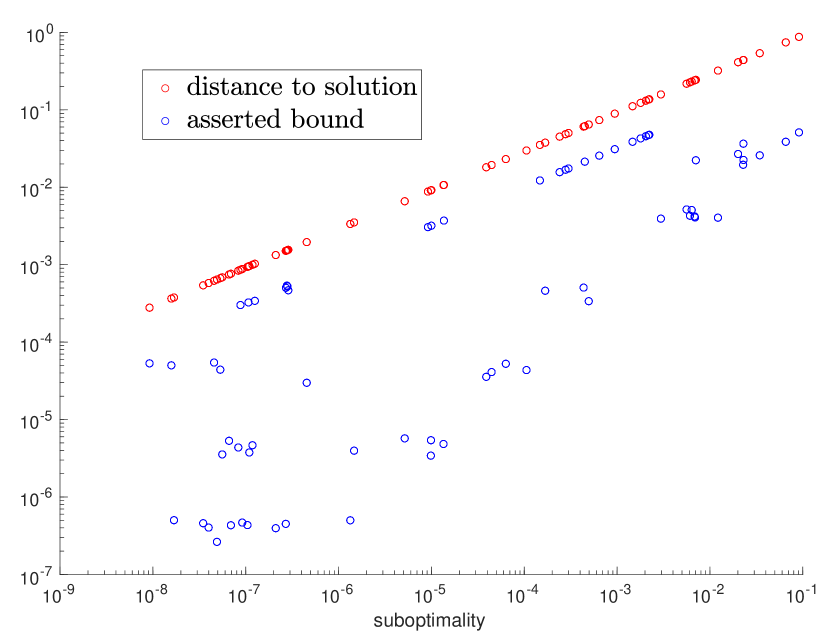

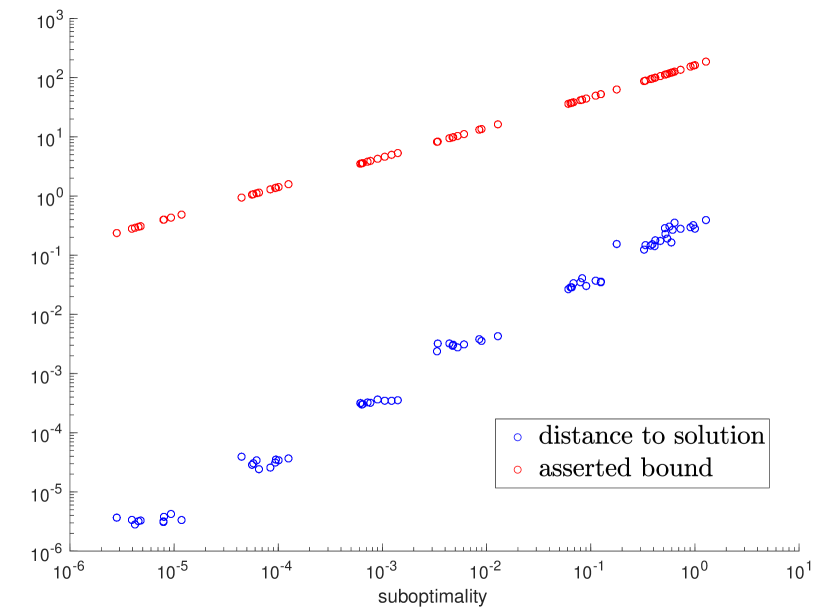

Appendix E Numerical simulation for the bound (8)

Here we numerically verify the correctness of the inequality (8) for feasible :

| (28) |

The function can be found in Table 1.

Experiment setup

We generated a random instance for each of LP, SOCP, and SDP. We solved the corresponding conic problem and obtain the optimal solution and a dual optimal . We numerically verified that the strict complementarity (by checking Definition 3 for LP and SDP and (DSC) for SOCP) and the uniqueness of the primal (by checking whether ) both hold for the three cases. We compute according to Lemma 2. Next, we randomly perturbed the solution many times and obtained possibly infeasible . We then projected to the feasible set to obtain . Finally, we plotted the suboptimality of versus the distance to (in blue), and the the suboptimality of versus the bound (in red) in Figure 2.

From Figure 2, we observe that the bounds are above the actual distance which assures (28). However, for SDP, the bounds appear to be looser compared to the cases of LP and SOCP.